bond covenants and investment policy - nyu la covenants...finally, this paper contributes to the...

TRANSCRIPT

Electronic copy available at: https://ssrn.com/abstract=3241645

Bond Covenants and Investment Policy

Sandrine Docgne Penlap∗

August 30, 2018

Abstract

I provide evidence that covenants in bond indentures affect the firm’s investment policy outside of

covenant violations. Using a large dataset of public bonds, and controlling for the self-selectivity of

covenant inclusion, I find that bonds with investment (financing) restrictions are associated with

a decrease (increase) in investment in the two years following the issue. The effect of investment

restrictions is entirely driven by firms that are more financially constrained. Both financially

constrained and unconstrained firms have significantly higher investment spending after issuing a

bond with financing restrictions, although the magnitude of the effect is higher in the latter group.

These findings suggest that while bond covenants can help mitigate agency problems and reduce

the cost of debt, they may also have externalities that lead to more investment distortions in firms

that are closer to financial distress. This paper is the first to document a positive relationship

between a covenant restriction and ex-post investment.

Keywords: Agency conflicts, Bond covenants, Investment, capital expenditures

JEL classification: G31 G32 D82 E22

∗C.T. Bauer College of Business, University of Houston, 334 Melcher Hall. Email:[email protected].

Electronic copy available at: https://ssrn.com/abstract=3241645

1 Introduction

How do restrictive covenants in bonds affect investment policy ex-post? Although covenants

are ubiquitous in debt contract, we still have limited empirical evidence on how different types

of covenants affect firms policies. Most empirical studies have looked either at the likelihood

of including covenants given a firms growth opportunities or at what happens to investment

once a covenant is violated. By contrast, this paper investigates firms’ investment behavior

in the years following the issuance of bonds that include covenant with restrictions on in-

vestment or financing activities. Because covenant violations are less frequent with public

bonds due to the very high cost of renegotiation, this paper focuses on public bonds to flush

out the ex-post effect of covenant inclusion before any violation occurs.

The costly contracting hypothesis, stemming from the work of Jensen and Meckling

(1976), Myers (1977), and Smith and Warner (1979) provide the main theoretical framework

for the inclusion of covenants in debt contracts. Managers of a levered firm, acting on behalf

of shareholders, have an incentive to adopt investment, financing and dividend policies that

maximize the value of equity rather than the value of the firm. Rationale bondholders

anticipate these agency conflicts and impose the entire expected cost to the firm in the

pricing of debt. Because stockholders bear the full costs of agency conflicts, they have an

incentive to minimize these costs. The theory argues that restrictive covenants are effective

instruments in mitigating these agency conflicts by aligning the interests of managers with

those of bondholders. By agreeing to these restrictive covenants, shareholders can reduce

agency costs and thus the cost of debt. However, these restrictions impose limitations on

managerial actions and thus can have a negative effect on profitability as managers might

be unable to undertake optimal decisions in certain states of the world because of limited

flexibility (Jensen and Meckling, 1976). Shareholders agree to restrictive covenants when the

expected cost (loss of flexibility) is less than the expected profit (lower cost of debt).

The costly contracting hypothesis implies therefore that firms policies depend on whether

1

Electronic copy available at: https://ssrn.com/abstract=3241645

or not the bond contains a covenant. However, most studies on the role and purpose of

covenants have focused on ex-ante firms characteristics to try and understand which firms

are more likely to include a specific type of covenants. The question of how firms behavior

change depending on the type of restriction in their debt contract is still largely unexplored.

Studies by Chava and Roberts (2008) and Nini et al. (2009) show that after a violation

or a deterioration of credit quality, covenants restriction lead to lower capital expenditure.

However, these studies highlight the monitoring role of private lenders who use the threat

of recalling the loan to intervene with management. In this paper, I look at capital expen-

diture spending in the years following a bond issue with or without a covenant restriction.

Bond creditors are more dispersed and have little influence on management. However, the

cost of violating a covenant is higher for bonds since renegotiation rarely occurs outside

of bankruptcy. These characteristics make bond contract ideal to studying the effect of

covenant outside of technical default.

The primary challenge when attempting to determine the causal effect of covenant re-

strictions on investment policy is that covenant choice is not exogenous. Managers anticipate

these effects when making their financing decisions. To address the endogeneity of covenant

inclusion, I use a two-stage estimation method. Ziliak and Kniesner (1998) and Wooldridge

(2002) show that under the assumption of normality, adding the inverse Mills ratio from the

first stage selection model to the differenced equation in the second stage results in a consis-

tent estimation. Following several studies that estimate the likelihood of covenant inclusion

(Malitz, 1986; Begley, 1994; Nash et al., 2003; Billett et al., 2007; Reisel, 2014), I estimate

a first stage probit regression using firms and loan characteristics. From this regression, I

obtain the inverse Mills ratio, with which I augment a traditional q model of investment.

The analysis focuses on two groups of covenants: restrictions on investment and financing

activities. I find that following a bond issuance, firms with a covenant restricting investment

have lower capital expenditures relative to those firms that do not have the covenants in

their bond contracts. However, this effect is entirely driven by firms that are more financially

2

Electronic copy available at: https://ssrn.com/abstract=3241645

constrained. Since these firms are also more likely to overinvest in risky assets, these results

may suggest that covenant restricting risky investment are effective a mitigating the agency

problems of overinvestment and asset substitution. I also find that covenant restricting

financing activities have an externality on investment policy. Following the issuance of

bonds, firms with financing restrictions have higher capital expenditures than firms without

those covenants. Both financially constrained and unconstrained firms have significantly

higher investment spending after issuing a bond with financing restrictions, although the

magnitude of the effect is higher in the latter group. These results may suggest that issuing

bonds with only financing restrictions may help lower the cost of debt, which allows firm

to undertake more investment, but it might also exacerbate the overinvestment problem in

firms that are closer to financial distress.

This paper contributes to the literature on the role of covenant in public bonds. Some

researchers argue that covenants in bond indentures are boilerplate contracts and have no

effect on the firms. Kahan and Yermack (1998) argue that the absence of covenants in pub-

licly traded convertible bonds is a proof that convertibility is a more effective mechanism to

mitigate agency problems linked to investment policies in public debt. Verde (1999) contends

that bond covenants are written loosely and offer very little protection to bondholders when

compared to covenants in private loan agreements. Within this view, covenants in bonds

should have no impact on the firm’s behavior, and creditors should rely on other mechanisms

to resolve the agency conflicts. This paper shows that covenants in bond affect investment

behavior. It shows that while covenants in public bonds can mitigate agency problems, they

can also exacerbate investment distortions.

This paper is also related to studies that investigate the agency costs of debt and their

consequence for investment policies. Because the primary purpose of covenants in bond is

to alleviate agency problems, several studies have looked at the role of covenant in miti-

gating investment distortions. Secured debt, leasing, dividend restrictions can alleviate the

underinvestment problem (Smith and Warner, 1979; Kalay, 1982; Stulz and Johnson, 1985;

3

Electronic copy available at: https://ssrn.com/abstract=3241645

Smith and Wakeman, 1985) but can also increase overinvestment (Berkovitch and Kim,

1990). This paper document a positive relationship between covenants restricting financing

activities, which includes restrictions on the issuance of additional debt and negative pledge

covenants, and investment. However, I cannot conclude if the observed behavior is reducing

underinvestment or increasing overinvestment.

Finally, this paper contributes to the literature on financial frictions in the debt market

and their impact on investment. Whited (1992) and Hennessy (2004) use structural econo-

metric models to show that financially unhealthy firms have difficulty obtaining external

finance, which results in lower investment. Lang et al. (1996) show that high leverage neg-

atively impacts investment. Whited (2006) show that external financing constraints affect

the timing of large investment projects. These results are consistent with the findings in

this paper. Investment restrictions are more likely to be imposed on firms that are already

financially constrained, and lead to lower levels of investment. These firms may have lower

capital expenditure because they are delaying investment. One reason that firms with fi-

nancing restrictions have higher levels of investment could be that they are able to have a

lower cost of debt which enables them to undertake more investment sooner. My analysis

suggests that the terms of the bond contract could affect the timing of investment.

2 Motivation and Literature

2.1 Motivation

The main theoretical framework that we have for understanding the purpose and impli-

cation of covenants stems from the work of Jensen and Meckling (1976), Myers (1977), and

Smith and Warner (1979). Jensen and Meckling define the concept of agency costs of debt

and its effect on firm’s value. Myers extend the model to show that levered corporation

with growth options have an incentive to underinvest. Finally, Smith and Warner show how

4

Electronic copy available at: https://ssrn.com/abstract=3241645

covenants are included in bond contract in order to reduce the agency cost. The Costly

Contracting Hypothesis posits that bond covenants can increase the value of the firm by re-

ducing the opportunity loss that results from the fact that stockholder’s in a levered firm have

an incentive to adopt equity value maximizing rather than firm value maximizing policies.

Smith and Warner (1979) argue that covenants reduce the agency costs of debt and that the

benefits accrue to the firm’s owners. However, covenants also impose direct and opportunity

costs that are substantial and explain the observed heterogeneity in debt contracts. Only

firms that expect the cost-reducing benefits of covenants to exceed the costs associated with

their restrictions will agree to have covenants included in their debt contracts.

Most studies on the role of covenants focus on ex-ante firms’ characteristics to explain

the observed heterogeneity in covenant choice. Malitz (1986) finds that the presence of

covenants in public debt is negatively related to the size of the firm and positively related to

the firm’s leverage. Begley (1994) finds that firms with a higher probability of bankruptcy,

less assets in place, and generating less cash flow from operations are more likely to include

covenants restricting dividends and additional debt in bonds contracts. Growth opportunity

is negatively (Kahan and Yermack, 1998; Nash et al., 2003; Reisel, 2014), positively (Billett

et al., 2007; Bradley and Roberts, 2015) correlated with covenant inclusion. Chava et al.

(2010) show that managerial entrenchment and the risk of managerial fraud significantly

impact the choice of bond covenants. These studies show that ex-ante firms characteristics

affect the choice of covenants in public and private debt, providing support for the costly

contracting hypothesis.

However, the question of how firms characteristics are affected ex-post by covenant choice

remains largely unexplored. More specifically, there is insufficient empirical evidence on the

direct and indirect consequences of covenants on firm’s investment policy despite theoretical

predictions on the externality of covenants on investment policy. Brennan and Schwartz

(1984) build a theoretical model of firm’s financing and show that in the presence of fi-

nancial frictions, firms with low levels of profitability and leverage that issue bonds with

5

Electronic copy available at: https://ssrn.com/abstract=3241645

covenants restricting debt issuance have a higher level of investment than if they issued the

bond without covenants. This shows that while the purpose of financing restrictions is to

prevent wealth expropriation through claim dilution, the covenants can have an externality

on investment policy. Brennan and Schwartz (1984) analysis does not suggest whether the

externality is good or bad for firm’s value, several studies suggest that covenants can have

negative indirect consequences on investment policy. Stulz and Johnson (1985) and Smith

and Wakeman (1985) show that secured debt and leasing can alleviate the underinvest-

ment problem. Smith and Warner (1979) and Kalay (1982) show that dividend restrictions

might help alleviate the underinvestment problem. Berkovitch and Kim (1990) show that

senior debt and debt with dividend covenants may decrease underinvestment while increas-

ing overinvestment. Hennessy (2004) show that the issuance of additional secured debt can

mitigate underinvestment stemming from debt overhang. These results suggest that includ-

ing covenants in bonds that restrict financing activities can have an impact on investment

policy.

2.2 Related Literature

Few studies look at the ex-post effect of covenants on investment, and those studies

usually look at the effect after a technical default or a deterioration of credit quality. Looking

at a sample of private loans, (Chava and Roberts, 2008) examine the effect of violation of

financial covenants such as minimum net worth and current ratio on investment. Exploiting

a discontinuity around the covenant threshold, they are able to show that capital expenditure

declines sharply following a covenant violation. This decline is higher for firms with relatively

larger agency and information problems. Also using a sample of private loans, (Nini et al.,

2009) find that capital expenditure restrictions reduce firms’ investment and that these

restrictions are more likely to be put in place after credit quality deteriorates, which may

suggest that these firms have already violated a covenant. Both of these studies provide

6

Electronic copy available at: https://ssrn.com/abstract=3241645

support for the role that financial covenants play in the contingent allocation of control rights;

after violation, creditors use the right to recall the loan to intervene in firm’s management. In

contrast to these studies, I focus on the ex-post effect of restrictive covenants in public bonds

on investment expenditure, outside of violation. Restrictive covenants differ from financial

covenants in that they impose a limitation of managerial action, while financial covenants

impose threshold on accounting ratios that are volatile and not under the full control of

managers. Financial covenants are less prevalent in public bonds because the high number

of dispersed investor reduces the incentive to monitor and renegotiation rarely occurs outside

of bankruptcy.

Other studies look at the ex-post effect of covenants on various firms performance.

Demiroglu and James (2010) find that following the issuance of loans with tight covenants,

the accounting ratios associated with the covenant improve while investment expenditure and

net debt issuance decreases. They also focus their analysis on the ex-post effect of covenants

outside of default and show that tight financial covenants are correlated with lower level

of investment. In this paper, I extend a similar analysis to bond covenants to further our

understanding in the difference of covenants in private and public debt. Cook and Easter-

wood (1994) examine the effect of poison put covenants in bonds and find a negative effect of

stockholders wealth but a positive effect on the wealth of bondholders. Spyridopoulos (2018)

show that stricter loan covenants lead to higher profitability and lower operating costs, but

the effect is driven only by firms with poor governance, providing support for the disciplin-

ing role of debt. Asquith and Wizman (1990) show that public bonds with strong covenant

protection gain value in leveraged buyouts while those with no protection lose value. These

studies show issuing debt with covenants affect firm’s value in the long run. This paper

extend this literature by showing that restrictive covenants in public bonds can also results

in unanticipated impact, from the agency theory perspective, on investment behavior.

7

Electronic copy available at: https://ssrn.com/abstract=3241645

3 Data and Sample Characteristics

3.1 Data Sources

The data comes from 2016 Fixed Investment Securities Database (FISD) for bond data,

Compustat annual files for firm’s financial statement data, CRSP monthly stock data for

market value, and the Federal Reserve bank of St Louis (FRED) for secondary yields on

the Treasury and corporate bonds required to compute term and credit spreads respectively.

FISD contains various information on the covenants associated with a bond at the time of

issuance for a large set of firms.

Following Billett et al. (2007) and Reisel (2014), I only consider public bonds issued by

U.S. domiciled non-financial companies that are in U.S. dollars. I exclude Yankee, Canadian,

foreign currency, and government and utilities companies bonds. In addition, I exclude all

bonds for which covenant information, subsequent data from prospectuses or other detailed

sources, offering yield, offering date, maturity date, or security level are not available. Finally,

I exclude medium term notes (MTN), private placements, and bonds with rule 144a. The

final sample is in the intersection of FISD, CRSP and Compustat during 1989-2015 and

includes 4221 bonds issued by 1005 firms. I winsorize firm and bond data at the 1% and

99% levels to alleviate the effect of outliers.

3.2 Key variables

The investment variable is CAPEX, which is the ratio of capital expenditure to the

start of period assets. In all the regression, the dependent variable is the change in capital

expenditure, δCAPEX, after the bond is issued relative to the year prior to the bond

issuance. I investigate the change in investment expenditure in the first and second fiscal

years after the fiscal year in which the bond is issued. The two specifications attempt to

shade a light on what happens to investment over time after a firm issue a bond with a

8

Electronic copy available at: https://ssrn.com/abstract=3241645

covenant relative to if the it had issued the bond without the covenant.

Bond covenants are provisions in the bond contract that impose restrictions on the issuer

once the bond is issued. I use the framework provided by Smith and Warner (1979) to

group covenants into primary categories based on the nature of the restriction, with a focus

on covenants that restrict investment and financing activities. Appendix A provides more

details on the specific covenants in each category. Investment restrictions are covenants that

either directly restricts risky investments or do so indirectly by imposing restrictions on the

firms dealings with it subsidiaries, and on the acquisition and sale of assets. There are 12.4%

of bonds that are issued with a restriction on investments.

Financing restrictions include covenants on the issuance of additional debt, sale-leaseback

transactions, and negative pledge. 19.4% of the bonds include restrictions on the issuance

of additional debt which restricts the seniority and the amount of debt that the firm can

incurred as well as impose leverage and net earnings test that must be met before the firm

can issue any new debt. Restrictions on sale-leaseback activities are present in 61.7% of the

sample and restrict the firm to the type and amount of property used in a sale-leaseback

transaction. 70% of the bonds include a negative pledge covenant that requires the firm to

issue secured debt only if it secures the current issue on a pari passu basis. In total, 81.2%

of bonds include restrictions on financing activities.

3.3 Firms characteristics and covenant inclusion

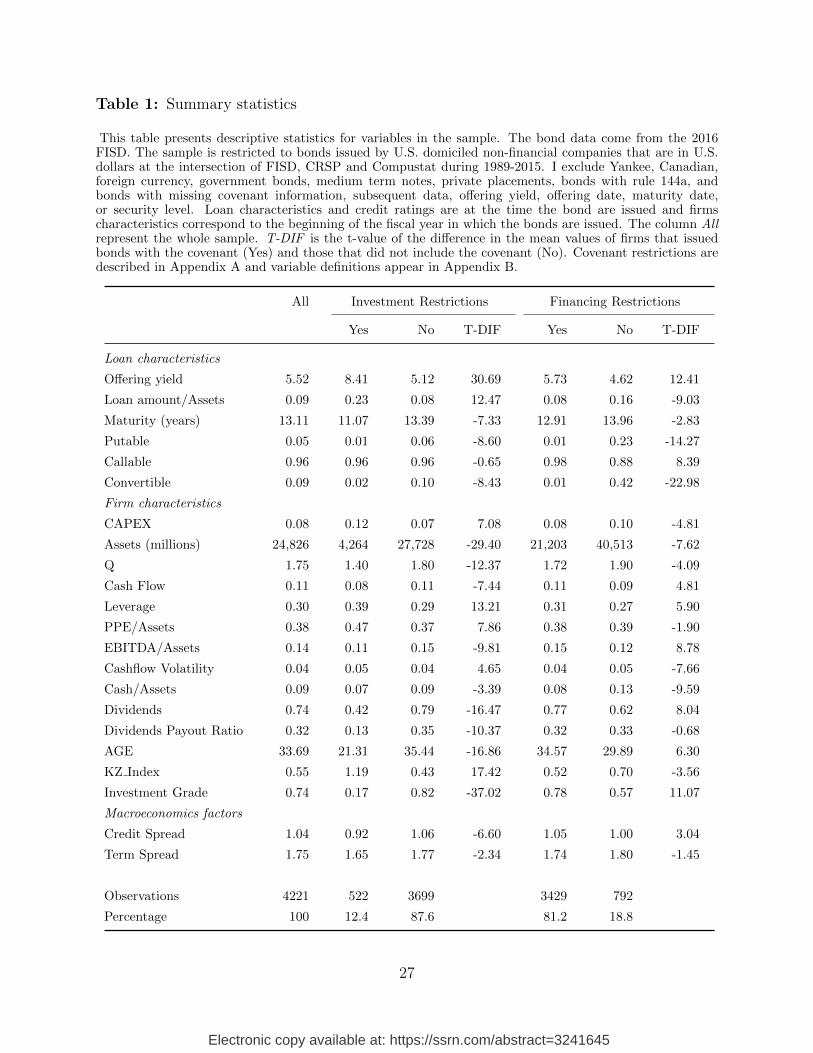

Table 1 presents some summary statistics for the whole sample (All) as well for the

subsamples of loan with and without the indicated category of covenants; restrictions on

investment or on financing activities. The values under columns “Yes” and “No” represent

the sample mean of the corresponding variable, and the value under column “T-DIF” is

the t-value of the difference in the means of the two subsamples. Covenant restrictions are

described in Appendix A and variable definitions appear in Appendix B. The table shows

9

Electronic copy available at: https://ssrn.com/abstract=3241645

significant heterogeneity between firms that issue bonds with covenant restrictions and those

that issue without. The data shows that the yield is higher for bonds with covenants. Bradley

and Roberts (2015) and Reisel (2014) show that covenant inclusion leads to a reduction of

the price of debt. Put together, the results from the table suggests that the yield would

have been even higher if those bonds did not include a covenant. The data also shows

a negative relation with covenant and bond maturity. This may suggests that in bonds,

restrictive covenants and maturity are complement and not substitute. However a more

formal analysis is required before drawing conclusions.

The data in Table 1 shows that firms that issue bonds with restrictive covenants are on

average smaller, where size is measured by the log of book assets. Firms without an invest-

ment restriction are approximate 6.5 times larger than firms with the restriction. The data

also shows a negative relation between covenants and firm’s growth option (Q), as measured

by market-to-book, and with cash on hands, but a positive relation with leverage. These are

consistent with the agency theory of debt. The theory predicts that firms that are closer to

financial distress are more likely to include restrictive covenants in their debt contract. Cash

flow, profitability, dividend payments, and age are negatively related to investment restric-

tions, but positively correlated with restrictions on financing activities. Asset tangibility,

cash flow volatility, KZ index which indicates a firm’s relative level of financial constraint

are positively (negatively) correlated with investment (financing) restrictions. Finally, credit

spread has a negative (positive) relation with investment (financing) covenants, suggesting

that firms are more likely to agree to covenants that restrict their investment decisions, but

not future financing when the risk premium is low.

10

Electronic copy available at: https://ssrn.com/abstract=3241645

4 Ex-Post Effect of Restrictive Covenants

4.1 Empirical strategy

The non randomness of covenant inclusion introduces a significant identification prob-

lem when trying to measure the impact of the restriction on firm investment. The costly

contracting hypothesis predicts that borrowers weight the costs and benefits of restrictive

covenants when making decisions. Thus there exist some unobservable firm characteristics

that affect both investment policy and covenant selection. To control for the endogeneity

of covenant inclusion dummy, I follow the two-step estimation methodology similar to the

one used by Goyal (2005) and Reisel (2014). In the first stage, I estimate the probability of

covenant inclusion using a reduced form probit.

Covt = ΓZt−1 + ηt (1)

where Cov is a dummy variable that equals 1 if the bond contains the restrictive covenant,

Z is a set of variables that affect the decision to include the covenant in the bond contract,

and η is a random error with mean zero and a normalized variance of 1. Under assumption

of normality, I obtain from the equation (1)the estimates of the inverse Mills ratios that

equal φ(ΓZ)/Φ(ΓZ) for bonds with covenants and −φ(ΓZ)/[1 − Φ(ΓZ)] for bonds with-

out covenants. φ is the standard normal density function and Φ is the standard normal

cumulative distribution function.

In the second stage, I estimate a traditional investment equation with the covenant

dummy and the inverse Mills ratio as explanatory variables

∆CAPEXt+1 = β0Covt + α0 IMRi + β1 ∆Xt−1 + εt+1. (2)

∆CAPEX is the change in capital expenditure relative to its value before the bond was

11

Electronic copy available at: https://ssrn.com/abstract=3241645

issued, X is a vector of control variables. Ziliak and Kniesner (1998) and Wooldridge (2002)

show that under assumption of normality, adding the inverse Mills ratio from the probit

regression to the differenced equation results in consistent estimation.

The motivation for the specification in equation (2) comes from the theory and empirical

work. Classical q theory implies that investment is only a function of marginal q, which is

unobservable. However several works such Hennessy (2004) and Bakke and Whited (2010)

show that empirical proxies of marginal q along with additional control variables such as

cash flow, size, and leverage are effective in addressing a potential omitted variable issue in

the investment regression. The difference-in-difference approach accounts for time-invariant

unobservable differences between firms that issue bonds with covenants and those that do

not. The parameter of interest is β0, which represents the impact of a covenant inclusion on

investment (i.e. the treatment effect). The coefficient of the inverse Mills ratio, α0 captures

the correlation between the error terms ε and η

4.2 Primary Results

4.2.1 Covenant selection

The covenant selection model is based on the theory and empirical evidence on the factors

that affect covenant inclusion in a debt agreement. I use firms and bond characteristics, and

macroeconomic factors to determine the likelihood of covenant inclusion. According to the

Costly Contracting Hypothesis, firms that are associated with higher agency costs are more

likely to have covenants included in their debt contracts. In line with this theory, size and

leverage (Malitz, 1986), growth option (Nash et al., 2003; Billett et al., 2007), the proportion

of tangible assets and cash flow (Begley, 1994) are firms characteristics associated with the

likelihood of covenant inclusion. Following Reisel (2014) I also include company credit ratings

since they may provide additional information about firm performance. Because other loan

characteristics can be used to mitigate agency costs (see Nash et al., 2003, for a discussion), I

12

Electronic copy available at: https://ssrn.com/abstract=3241645

include the bond’s maturity and amount, and dummies for putable, callable, and convertible

features. Following Bradley and Roberts (2015) I control for macroeconomic factors using the

difference between the 10-year and 1-year treasury bonds (Term Spread) and the difference

in the yields on BAA and AAA corporate bonds (Credit Spread). Since agency costs may

vary across industries, I include dummies for one-digit sic codes in all the regressions.

Table 2 reports the results of the probit model for the probability of including a covenant

in the bond contract. The results of this estimation are used to estimate the inverse mill ratios

use in the investment regression. Consistent with previous findings, firm size is negatively

correlated with covenant inclusion. The coefficient on market-to-book has a negative sign,

but is only statistically significant for investment restrictions. This suggests that firms with

high growth options may find covenant restricting investment very costly, but not those

restricting financing activities. Firms with more tangible assets are more likely to have

investment restrictions but less likely to have financing restrictions in their bond indenture.

One of the strongest determinant of covenant inclusion is convertibility, as indicated by

the t-statistics on the coefficient. The negative sign suggest that restrictive covenants and

convertibility might be substitute in addressing agency conflicts.

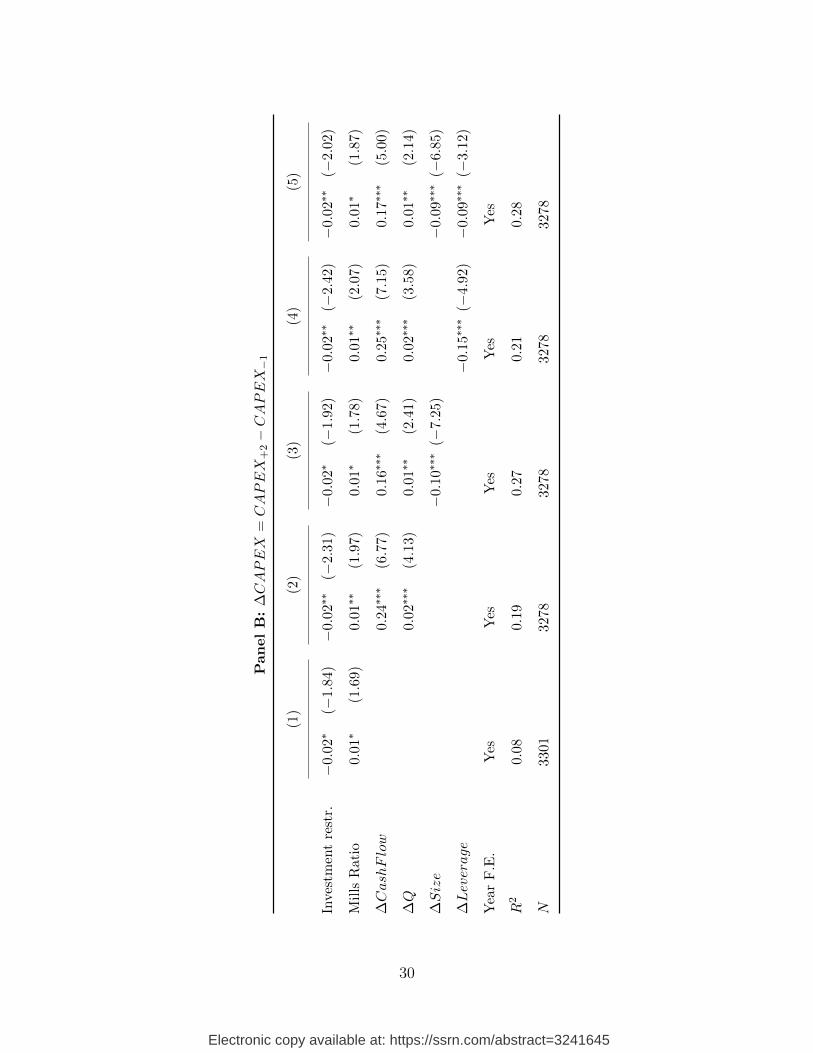

4.2.2 Investment restrictions

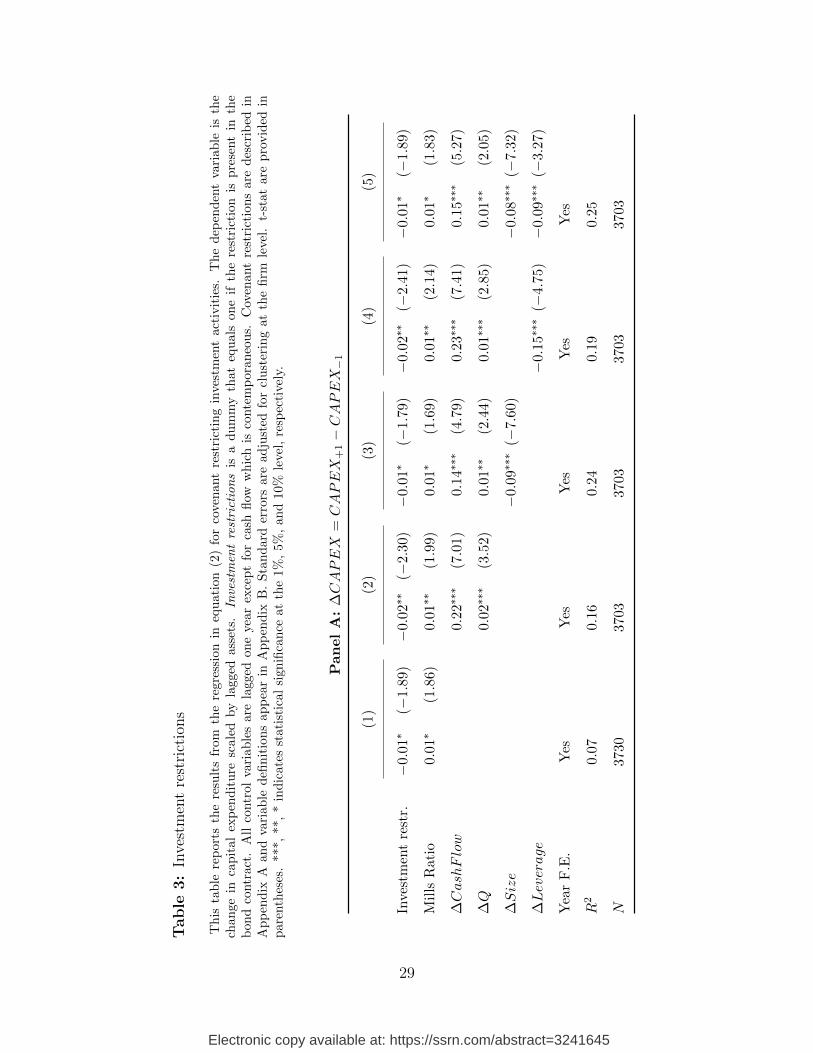

Table 3 presents the estimation results of the investment regression for covenants re-

stricting investments. All specifications include year fixed effects. In Panel A the dependent

variable is the change in capital expenditure one year after the bond is issued relative to the

year before the issuance. In Panel B the dependent variable is the change two years after.

In all specifications, the coefficient on the inverse mills ratio is positive and significant. This

implies that I can reject the null hypothesis that there is no self selection bias. The positive

sign on the inverse Mills ratio suggest that unobservable firm characteristics that increase

the likelihood of the inclusion of covenant restricting investments are positively correlated

with an increase in investment spending. According to the costly contracting hypothesis, the

13

Electronic copy available at: https://ssrn.com/abstract=3241645

purpose of investment restrictions in bond indenture is to mitigate the agency risk of over-

investment in risky assets (Smith and Warner, 1979). The positive and significant sign on

the inverse Mills ratio suggest that covenant restricting risky investment in bond indentures

might be effective at mitigating the agency cost of asset substitution and overinvestment.

It also implies that it is important to control for the endogeneity of the covenant decision

when investigating the effect on firm’s policies.

Consistent with previous findings that restrictions on investment lead to lower investment

expenditure, I find the coefficient on the covenant dummy is always negative and significant

after controlling for the self selection bias. Using the specification in column (4) that includes

all control variables, I find that in the first year following the year of the bond issuance, the

change in the proportion of capital expenditure to assets is 1.17 percentage points lower for

firms with investment restrictions relative to those firms without the restriction. Given the

average capital expenditure of 8% of assets prior to the security issuance, this correspond

to a difference of almost 15%. In the second year following the issuance, the difference is

even more substantial. Firms with investment restriction have a capital expenditure 1.58

percentage points lower than firms without the covenant, which correspond to a difference of

20% relative to the average capital expenditure in the year before the bond is issued. This

results show that the effect of investment restrictions on capital expenditure is economically

significant and persistent. The coefficient estimates on cash flow, Tobin’s Q, size, and leverage

are consistent with previous studies examining capital expenditures.

4.2.3 Financing restrictions

Table 4 reports the estimation results of the investment regression for covenants restrict-

ing financing activities. In Panel A (B) the dependent variable is the change in capital

expenditure one (two) year after the bond is issued relative to the year prior to the issuance.

The inverse mills ratio is significant at the 1% level in all the specifications, indicating

the prevalence of self selection in the decision to include financing restrictions in the bond

14

Electronic copy available at: https://ssrn.com/abstract=3241645

contract. The negative sign on the selectivity variable suggests that firms with a higher

probability of issuing bonds with restrictions on financing activities are also more likely to

reduce capital expenditure. The purpose of financing restrictions is to prevent wealth trans-

fer through claim dilution. However, the presence of financial frictions create a link between

financing and investment activities. One possible reason for the negative sign on the inverse

Mills ratio is that these firms have liquidity constrains ex-ante and would not have been able

to undertake additional investment without issuing the bond. Another possible explanation

is that these firms are more likely to underinvest. Mauer and Ott (2000) show that a levered

firm tend to underinvest when shareholders must bear the full cost of new investment while

sharing the profits with bondholders. This analysis does not distinguishes between both

explanation, but simply suggest that these firms are more likely to reduce investment.

In all the specification in table 4, the coefficient estimates on the financing restrictions

dummy is positive and significant at the 1% level after controlling for the selection bias. The

results are also economically significant. Firms that issue bonds with covenant restricting

financing show capital expenditure of 2.32 percentage point higher than firms without the

covenants. This difference correspond to 29% of the average investment spending in year

prior to the bond being issued, using specification in column (4). In the second year following

the year of the bond, the change in investment spending for firms with financing restriction is

3.89 percentage points higher, which correspond to 49% of th capital expenditure spending in

the year prior to the bond issuance. These results suggest that after issuing bonds with only

financing restrictions, firms are able to undertake more investment relative to those firms

that issue bonds without these covenants. These results are consistent with the theoretical

prediction of the model by Brennan and Schwartz (1984). A possible explanation for the

observed behavior is that agreeing to the restrictions allows firm to reduce the cost of debt

and thus undertake more investment. Another possible explanation is that these firms are

financially constrained and are more willing to gamble with the new influx of cash. Since

they don’t have investment restrictions, they overinvest in risky investment. My analysis

15

Electronic copy available at: https://ssrn.com/abstract=3241645

does not differentiate between these possible explanations.

4.3 Robustness

For robustness purpose, I also perform a counterfactual analysis of the effect of covenant

inclusion on ex-post investment in the second stage. I estimate the investment regression,

with the appropriate inverse Mills ratio, separately for firms with and without the covenants.

Using the estimates from these regression excluding the inverse Mills ratio, I obtain two sets

of predicted capital expenditure for the whole sample: one corresponding to loans with a

particular covenant and the other corresponding to loans without the covenant. I am thus

able to estimate a counterfactual for each loan in the sample. Table 5 reports the average

value of the predicted capital expenditure with and without investment restrictions, and

their difference. On average, investment spending decrease in the years following the bond

issuance. However, the decrease is larger if the bond contains restrictions on investment ac-

tivities. The difference is statistically and economically significant. In the first year following

the bond, the difference is 1.2 percentage points and 2.15 percentage point in th second year.

These difference correspond to 15% and 27% of the average capital expenditure in the year

prior to the bond, respectively. These results implies that after controlling for the self se-

lection of covenant inclusion, firms that issue bonds with investment restriction will see a

larger decrease in investment spending relative to if they had not agreed to the restriction.

Table 6 show the same results for loans with and without financing restrictions. While

investment spending decrease in the years following the issuance of the bond relative to the

year prior to the issue, the decrease is much larger when the firm issues bond without financ-

ing restrictions. The difference in change in capital expenditure is 2.27 and 3.56 percentage

points in the first and second year respectively. These values correspond to 29% and 45%

of the average capital expenditure in the year preceding the bond issue. Thus similar to

the results in previous section, firms that issue bonds with financing restrictions are able

16

Electronic copy available at: https://ssrn.com/abstract=3241645

to invest more in the following years relative to if they had issue the bond without the

covenants. Again this could be that these firms are able to reduce the cost of debt which

allows them to invest more, or it could be that they are taking on more risky investment in

order to maximize their expected returns. In the next section, I investigate how this effect

differ among firms with different level of financial constraints.

5 Cross-Sectional Variations

In this section I test whether the ex-post effect of covenants on investment covary with

the ex-ante financial health of the firm using several proxies for financing constraints. This

is important to further understand what is driving the investment response to the inclusion

of restrictive covenants.

5.1 Proxies for financial constraints

I examine four different proxies for financial constraints. The first proxy is the age of

the firm as measured by the number of years in Compustat. Since younger firms are more

likely to face more frictions in capital-markets, firm age can be used as a proxy for financial

constraints (Hovakimian and Titman, 2006; Almeida and Campello, 2007). If a firm has

a higher probability of investing in negative net present value project with a high upward

potential, the agency cost will be higher for a younger firm relative to an older firm. In this

case, younger firms that issue bonds with restrictive covenants on investment should see a

larger decrease in capital expenditure. On the other hand, younger firms are less likely to

underinvest and thus should see a smaller impact on investment after issuing bonds with

financing restrictions.

The second proxy is the proportion of assets held in cash. Financial slack has been

associated with financial constraints by many researchers. Some have argued that firms

accumulate more cash when they expect higher cost of external financing (Fazzari et al.,

17

Electronic copy available at: https://ssrn.com/abstract=3241645

2000; Almeida et al., 2011). However, others argue that firms with large cash balance are

not financially constrained since it is an indication that investment is not limited by an

availability of internal funds (Kaplan and Zingales, 1997). Although the evidence supports

the fact that cash holdings are more valuable for constrained firms, Denis and Sibilkov (2010)

also show that some constrained firms exhibit low level of cash holdings due to persistent

low cash flow. In our sample firms that issue bond with investment restrictions are younger

with higher leverage, lower cash flow, lower profitability, higher cash flow volatility, lower

dividend payout ratio, higher KZ index and lower cash flow. This suggest that these firms

are financially constrained. I expect then that firms with lower cash balances that agree

to restrictions on investment are more likely to overinvest and thus should see the larger

decrease in investment. On the other hand, firms with larger cash balances that agree to

financing restrictions should display more sensitivity to covenant inclusion since these firms

are more likely to delay investment.

The third proxy is the dividend payout ratio. I classify firms in three groups following

Fazzari et al. (1988). Several studies have linked a firm’s payout ratio to financial constraints

(Alti, 2003; Almeida and Campello, 2007). Firms that have a higher earnings retention rate

display excess sensitivity of investment to internal funds. The higher retention rate suggests

that these firms face steeper cost of external finance and must rely on internally generated

cash flow to fund investments. The response of investment to covenant for lower and higher

dividend firms is the same as for cash holdings. The final proxy is the KZ index based

on the work of Kaplan and Zingales (1997). The synthetic index is constructed following

several authors who have used it to classify firms as financially constrained or not (Baker

et al., 2003; Bakke and Whited, 2010). Firms with higher values are considered financially

constrained. In so far as the constraints is caused by the agency conflicts, more financially

constrained firms should see the stronger effect after covenant inclusion.

18

Electronic copy available at: https://ssrn.com/abstract=3241645

5.2 Test of cross-sectional variations

To test for the hypotheses of cross sectional variations in investment response, I augment

the model in equation (2) by interacting all the variables with a proxy of financing constraints.

The specification follows Chava and Roberts (2008) and provides a more straightforward test

to compare the two main coefficients of interest. The empirical model is

∆CAPEXi = β0 I(A)Covi + β1 (1 − I(A))Covi + α0 I(A)IMRi

+ α1 (1 − I(A))IMRi + Γ0 I(A)∆Xi + Γ1 (1 − I(A))∆Xi + εi, (3)

where I(A) is an indicator function equal to one if the event A is true, and zero otherwise.

The indicator function correspond to one of the proxy discussed above and is measured at

the end of the fiscal year preceding the bond issuance. The coefficients of interest are β0

and β1 which correspond, respectively, to the interaction of the covenant dummy with I(A)

and (1 − I(A)). The first represent the effect of covenant inclusion on the investment of

firms that are financially constrained and the second the effect for firms that are financially

unconstrained. In all the regressions, Xi is a vector of covariates that include Cash Flow,

Tobin’s Q, Leverage. I also include year fixed effects.

To construct the dummy variable for financially constrained firms, I divided the sample

in three for each proxy. Firms in the lower (upper) third of the distribution for age and

cash holdings are considered financially constrained (unconstrained). Firms that pay less

than 10% of their income are classified as low dividend firms and firms that pay more than

30% are considered high paying firms. Firms that have negative payout rate because of

reported negative earnings are also considered high dividend paying firms since by definition

they are paying more than 100% of their earnings. Low (high) dividend paying firms are

considered financially constrained (unconstrained). Finally, firms in the higher(lower) third

of the distribution for KZ index are considered financially constrained (unconstrained).

19

Electronic copy available at: https://ssrn.com/abstract=3241645

Table 7 display the results of the analysis for covenant restricting investment activities.

I only display the estimated coefficients and t-statistics of β0 and β1 as well as the t-statistic

of the difference between these two estimates. In Panel A, the dependent variable is the

change in capital expenditure one year after the bond is issued relative to the year before

the issue. In Panel B, I look at the change two years after. The results show that capital

spending response to covenants restricting investment activities is driven by firms that are

financially constrained. If the firm is younger, has low cash on hand, or low dividend payout

ratio, then issuing bonds with investment restrictions lead to a significant decrease in capital

expenditure in the following years, relative to a similar firm who issue the bond without

the covenant. These results may suggest that covenant restricting risky investment in bond

indenture might be effective at addressing the overinvestment problem since firms that are

closer to financial distress are also more likely to engage in asset substitution.

Table 8 reports the result of the analysis for covenant restricting financing activities.

While all groups of firms see a significant impact on investment from the inclusion of the

covenant, firm that are classified as less constrained exhibit a higher sensitivity. Across

all measured of financial health, firms that classify as unconstrained see a very significant

increase in investment after issuing bonds with financing restrictions relative to those firms

that issue the bonds without the covenants. This may suggest that financially unconstrained

firms that issue bonds with financing restrictions do so in order to reduce the cost of debt,

which enables them to undertake more investment opportunities. However, firms that are

classified as financially constrained also see a significant increase in investment following the

issuance of a bond with covenant restricting financing activities, relative to similar firms

that issue the bond without the covenants. Because agency cost is higher for these firms,

including the covenant may also reduce the cost of debt relative to similarly constrained

firms and thus enable them to invest more. However, these firms are also more likely to

engage in risky asset substitution and overinvestment. Because they are closer to financial

distress, higher investment volatility is more valuable since it increases the upside without

20

Electronic copy available at: https://ssrn.com/abstract=3241645

changing the downside. This suggests that issuing bonds with only financing restriction may

exacerbate the overinvestment problem in financially constrained firms.

6 Conclusion

This paper investigates the ex-post effect of covenants restricting investment and financ-

ing activities on investment policy. Using a two-stage estimation method to control for the

fact that firms choose to include covenants, I find that the investment response differs be-

tween the two groups of covenants. Firms that issue bonds with investment restrictions

have lower level of capital expenditure in the following years, relative to similar firms that

issue bonds without the restrictions. This effect is concentrated among firms that are more

financially constrained. This results suggest that investment restrictions can be effective at

mitigating overinvestment in risky assets. On the other hand, firms that issue bonds with

financing restrictions have higher level of capital expenditure in the following years, relative

to similar firms that issue the bond without the restrictions. The effect is just as strong

in firms that are financially constrained and those that are not. These results may imply

that issuing bonds only with financing restrictions enables firms to lower the cost of debt

and invest more, but may exacerbate overinvestment behavior in firms that are closer to

financial distress.

21

Electronic copy available at: https://ssrn.com/abstract=3241645

References

Almeida, Heitor, and Murillo Campello, 2007, Financial Constraints, Asset Tangibility, andCorporate Investment, Review of Financial Studies 20, 1429–1460.

Almeida, Heitor, Murillo Campello, and Dirk Hackbarth, 2011, Liquidity Mergers, Journalof Financial Economics 102, 526–558.

Alti, Aydogan, 2003, How Sensitive Is Investment to Cash Flow When Financing Is Fric-tionless?, Journal of Finance 58, 707–722.

Asquith, Paul, and Thierry A. Wizman, 1990, Event Risk, Covenants, and BondholderReturns in Leveraged Buyouts, Journal of Financial Economics 27, 195–213.

Baker, Malcolm, Jeremy C. Stein, and Jeffrey Wurgler, 2003, When Does the Market Matter?Stock Prices and the Investment of Equity-Dependent Firms, The Quarterly Journal ofEconomics 118, 969–1005.

Bakke, Tor-erik, and Toni M. Whited, 2010, Which Firms Follow the Market? An Analysisof Corporate Investment Decisions, Review of Economic Studies 23, 1941–1980.

Begley, Joy, 1994, Restrictive Covenants Included in Public Debt Agreements: An EmpiricalInvestigation by, Working Paper .

Berkovitch, Elazar, and E. Han Kim, 1990, Financial Contracting and Leverage InducedOver- and Under-Investment Incentives, Journal of Finance 45, 765–794.

Billett, Matthew T., Tao-hsien Dolly King, and David C. Mauer, 2007, Growth Opportunitiesand the Choice of Leverage , Debt Maturity , and Covenants, Journal of Finance 62, 697–730.

Bradley, Michael, and Michael R. Roberts, 2015, The Structure and Pricing of CorporateDebt Covenants, Quarterly Journal of Finance 05, 1550001.

Brennan, Michael J., and Eduardo S. Schwartz, 1984, Optimal Financial Policy and FirmValuation, Journal of Finance 39, 593–607.

Chava, Sudheer, Praveen Kumar, and Arthur Warga, 2010, Managerial Agency and BondCovenants, Review of Financial Studies 23, 1120–1148.

Chava, Sudheer, and Michael R. Roberts, 2008, How Does Financing Impact Investment?The Role of Debt Covenants, Journal of Finance 63, 2085–2121.

Cook, Douglas O., and John C. Easterwood, 1994, Poison Put Bonds: An Analysis of TheirEconomic Role, Journal of Finance 49, 1905–1920.

Demiroglu, Cem, and Christopher M. James, 2010, The Information Content of Bank LoanCovenants, Review of Financial Studies 23, 3700–3737.

22

Electronic copy available at: https://ssrn.com/abstract=3241645

Denis, David J., and Valeriy Sibilkov, 2010, Financial Constraints, Investment, and the Valueof Cash Holdings, Review of Financial Studies 23, 247–269.

Fazzari, Steven M., R. Glenn Hubbard, and Bruce C. Petersen, 1988, Financing CorporateConstraints Investment, Brookings Papers on Economic Activity 1, 141–206.

Fazzari, Steven M., R. Glenn Hubbard, and Bruce C. Petersen, 2000, Investment-CashFlow Sensitivities are Useful: a Comment on Kaplan and Zingales, Quarterly Journal ofEconomics 115, 695–705.

Goyal, Vidhan K., 2005, Market Discipline of Bank Risk: Evidence from Subordinated DebtContracts, Journal of Financial Intermediation 14, 318–350.

Hennessy, Christopher A., 2004, Tobin ’ s Q, Debt Overhang, and Investment, Journal ofFinance 59, 1717–1742.

Hovakimian, Gayane, and Sheridan Titman, 2006, Corporate Investment with FinancialConstraints : Sensitivity of Investment to Funds from Voluntary Asset Sales, Journal ofMoney, Credit and Banking 38, 357–374.

Jensen, Michael C., and William H. Meckling, 1976, Theory of the Firm : ManagerialBehavior, Agency Costs and Ownership Structure, Journal of Financial Economics 3,305–360.

Kahan, Marcel, and David Yermack, 1998, Investment Opportunities and the Design of DebtSecurities, Journal of Law, Economics, and Organization 14, 136–151.

Kalay, Avner, 1982, Stockholder-Bondholder Conflict and Dividend Constraints, Journal ofFinancial Economics 10, 211–233.

Kaplan, Steven N., and Luigi Zingales, 1997, Do Investment-Cash Flow Sensitivities ProvideUseful Measures of Financing Constraints ?, Quarterly Journal of Economics 112, 169–215.

Lang, Larry, Eli Ofek, and Rene M. Stulz, 1996, Leverage, Investment, and Firm Growth,Journal of Financial Economics 40, 3–29.

Malitz, Ileen, 1986, On Financial Contracting: of Bond The Determinants, Financial Man-agement 15, 18–25.

Mauer, David C., and Steven H. Ott, 2000, Agency Costs, Underinvestment, and OptimalCapital Structure, Project flexibility, agency, and competition: New developments in thetheory and application of real options. Oxford 151–179.

Myers, Stewart C., 1977, Determinants of Corporate Borrowing, Journal of Financial Eco-nomics 5, 147–175.

Nash, Robert C., Jeffry M. Netter, and Annette B. Poulsen, 2003, Determinants of Con-tractual Relations between Shareholders and Bondholders: Investment Opportunities andRestrictive Covenants, Journal of Corporate Finance 9, 201–232.

23

Electronic copy available at: https://ssrn.com/abstract=3241645

Nini, Greg, David C. Smith, and Amir Sufi, 2009, Creditor Control Rights and Firm Invest-ment Policy, Journal of Financial Economics 92, 400–420.

Reisel, Natalia, 2014, On the Value of Restrictive Covenants: Empirical Investigation ofPublic Bond Issues, Journal of Corporate Finance 27, 251–268.

Smith, Clifford W., and L. MacDonald Wakeman, 1985, Determinants of Corporate LeasingPolicy, Journal of Finance 40, 895–908.

Smith, Clifford W., and Jerold B. Warner, 1979, On Financial Contracting, Journal ofFinancial Economics 7, 117–161.

Spyridopoulos, Ioannis, 2018, Tough Love: The Causal Effects of Debt Covenants on FirmPerformance, Working Paper .

Stulz, Rene M., and Herb Johnson, 1985, An Analysis of Secured Debt, Journal of FinancialEconomics 14, 501–521.

Verde, Mariarosa, 1999, Loan Preserver: The Value of Covenants, FitchIBCA Loan ProductsSpecial Report .

Whited, Toni M., 1992, Debit, Liquidity Constraints, and Corporate Investment: Evidencefrom Panel Data, Journal of Finance 47, 1425–1460.

Whited, Toni M., 2006, External Finance Constraints and the Intertemporal Pattern ofIntermittent Investment, Journal of Financial Economics 81, 467–502.

Wooldridge, Jeffrey M., 2002, Econometric Analysis of Cross Section and Panel Data, vol-ume 58 (MIT Press).

Ziliak, James P., and Thomas J. Kniesner, 1998, The Importance of Sample Attrition in LifeCycle Labor Supply Estimation, Journal of Human Resources 33, 507–530.

24

Electronic copy available at: https://ssrn.com/abstract=3241645

Appendix A: Classification of bond covenants

Bond Covenant in FISD Description in FISD

Investment Restrictions

AFTER ACQUIRED PROPERTY CLAUSE Property acquired after the sale of current debt issues willbe included in the current issuer’s mortgage.

TRANSACTION AFFILIATES Issuer is restricted in certain business dealings with its sub-sidiaries.

SUBSIDIARY REDESIGNATION Indicates if restricted subsidiaries may be reclassified as anunrestricted subsidiaries.

ASSET SALE CLAUSE Covenant requiring the issuer to use net proceeds from thesale of certain assets to redeem the bonds at par or at apremium.

SALE XFER ASSETS UNRESTRICTED Issuer must use proceeds from sale of subsidiaries’ assets toreduce debt.

SECURITY LEVEL = SS Indicates if the security is a secured issue of the issuer.STOCK TRANSFER SALE DISP Restricts the issuer from transferring, selling, or disposing

of it’s own common stock or the common stock of a sub-sidiary.

INVESTMENTS Restricts issuer’s investment policy to prevent risky invest-ments.

INVESTMENTS UNRESTRICTED SUBS Restricts subsidiaries’ investments.

Financing Restrictions

FUNDED DEBT IS Restricts issuer from issuing additional funded debt.INDEBTEDNESS IS Restricts user from incurring additional debt with limits on

absolute dollar amount of debt outstanding or percentagetotal capital.

FUNDED DEBT SUB Restricts issuer’s subsidiaries from issuing additionalfunded debt.

INDEBTEDNESS SUB Restricts the total indebtedness of the subsidiaries.SENIOR DEBT ISSUANCE Restricts issuer to the amount of senior debt it may issue

in the future.SUBORDINATED DEBT ISSUANCE Restricts issuance of junior or subordinated debt.NET EARNINGS TEST ISSUANCE To issue additional debt the issuer must have achieved or

maintained certain profitability levels.LEVERAGE TEST IS Restricts total-indebtedness of the issuer.LEVERAGE TEST SUB Limits subsidiaries’ leverage.BORROWING RESTRICTED Indicates subsidiaries are restricted from borrowing, except

from parent.NEGATIVE PLEDGE COVENANT The issuer cannot issue secured debt unless it secures the

current issue on a pari passu basis.SALES LEASEBACK IS Restricts issuer to the type or amount of property used in

a sale leaseback transaction and may restrict its use of theproceeds of the sale.

SALES LEASEBACK SUB Restricts subsidiaries from selling then leasing back assetsthat provide security for the debtholder.

25

Electronic copy available at: https://ssrn.com/abstract=3241645

Appendix B: Variable Definitions

CAPEX : Capital expenditure divided by start of period assets (lagged assets).

CashFlow : Sum of Income Before Extraordinary Items and Depreciation and Amortiza-

tion divided by start of period assets.

Q (Market to book): Book value of assets minus book value of equity plus market value

of equity divided by book value of assets. Book value of equity is stockholders equity minus

preferred stock redemption value plus deferred taxes and investment tax credit.

Size: Natural logarithm of total assets.

Leverage: Sum of debt in current liabilities and long-term debt divided by assets.

Cash: Cash and cash equivalents divided by assets.

PPE/Assets : Ratio of net property, plant and equipment to total assets.

EBITDA/Assets :Ratio of earnings before interest to total assets.

Cash Flow Volatility : Standard deviation of the ratio of EBITDA/Assets and is computed

using historical data for up to 10 years as available.

Dividends : A dummy variable that indicates whether the firm declared any dividends to

its common shareholders.

Dividend Payout Ratio: Ratio of Dividends declared to common shareholders to Income

Before Extraordinary Items.

AGE : Number of years in Compustat.

KZ Index : Sum of (-1.002) times CashFlow, (-39.368) times total dividend divided by

assets, (-1.315) times Cash, 3.139 times Leverage, and 0.283 times Q.

Investment Grade: A dummy variable that equals 1 if the company S&P long-term credit

rating is ’BBB-” or better, and equals 0 if the rating is worse than ’BBB-” or the company

is unrated.

Offering yield is the yield-to-maturity at the time of issuance.

Loan amount/Assets is the ratio of the bond offering amount to total assets.

Maturity is the number of years between the offering date and the maturity date.

Putable, Callable, Convertible are dummies equal to one if the feature is present in the

bond.

Credit Spread is the difference in the yields on BAA and AAA corporate bonds.

Term Spread is the difference between the 10-year and 1-year treasury bonds.

26

Electronic copy available at: https://ssrn.com/abstract=3241645

Table 1: Summary statistics

This table presents descriptive statistics for variables in the sample. The bond data come from the 2016FISD. The sample is restricted to bonds issued by U.S. domiciled non-financial companies that are in U.S.dollars at the intersection of FISD, CRSP and Compustat during 1989-2015. I exclude Yankee, Canadian,foreign currency, government bonds, medium term notes, private placements, bonds with rule 144a, andbonds with missing covenant information, subsequent data, offering yield, offering date, maturity date,or security level. Loan characteristics and credit ratings are at the time the bond are issued and firmscharacteristics correspond to the beginning of the fiscal year in which the bonds are issued. The column Allrepresent the whole sample. T-DIF is the t-value of the difference in the mean values of firms that issuedbonds with the covenant (Yes) and those that did not include the covenant (No). Covenant restrictions aredescribed in Appendix A and variable definitions appear in Appendix B.

All Investment Restrictions Financing Restrictions

Yes No T-DIF Yes No T-DIF

Loan characteristics

Offering yield 5.52 8.41 5.12 30.69 5.73 4.62 12.41

Loan amount/Assets 0.09 0.23 0.08 12.47 0.08 0.16 -9.03

Maturity (years) 13.11 11.07 13.39 -7.33 12.91 13.96 -2.83

Putable 0.05 0.01 0.06 -8.60 0.01 0.23 -14.27

Callable 0.96 0.96 0.96 -0.65 0.98 0.88 8.39

Convertible 0.09 0.02 0.10 -8.43 0.01 0.42 -22.98

Firm characteristics

CAPEX 0.08 0.12 0.07 7.08 0.08 0.10 -4.81

Assets (millions) 24,826 4,264 27,728 -29.40 21,203 40,513 -7.62

Q 1.75 1.40 1.80 -12.37 1.72 1.90 -4.09

Cash Flow 0.11 0.08 0.11 -7.44 0.11 0.09 4.81

Leverage 0.30 0.39 0.29 13.21 0.31 0.27 5.90

PPE/Assets 0.38 0.47 0.37 7.86 0.38 0.39 -1.90

EBITDA/Assets 0.14 0.11 0.15 -9.81 0.15 0.12 8.78

Cashflow Volatility 0.04 0.05 0.04 4.65 0.04 0.05 -7.66

Cash/Assets 0.09 0.07 0.09 -3.39 0.08 0.13 -9.59

Dividends 0.74 0.42 0.79 -16.47 0.77 0.62 8.04

Dividends Payout Ratio 0.32 0.13 0.35 -10.37 0.32 0.33 -0.68

AGE 33.69 21.31 35.44 -16.86 34.57 29.89 6.30

KZ Index 0.55 1.19 0.43 17.42 0.52 0.70 -3.56

Investment Grade 0.74 0.17 0.82 -37.02 0.78 0.57 11.07

Macroeconomics factors

Credit Spread 1.04 0.92 1.06 -6.60 1.05 1.00 3.04

Term Spread 1.75 1.65 1.77 -2.34 1.74 1.80 -1.45

Observations 4221 522 3699 3429 792

Percentage 100 12.4 87.6 81.2 18.8

27

Electronic copy available at: https://ssrn.com/abstract=3241645

Table 2: Covenant selection reduced form probit

This table presents the results of the probit regression of covenant inclusion from equation (1). The bonddata come from the 2016 FISD. The sample is restricted to bonds issued by U.S. domiciled non-financialcompanies that are in U.S. dollars at the intersection of FISD, CRSP and Compustat during 1989-2015.I exclude Yankee, Canadian, foreign currency, government bonds, medium term notes, private placements,bonds with rule 144a, and bonds with missing covenant information, subsequent data, offering yield, offeringdate, maturity date, or security level. Loan characteristics and credit ratings are at the time the bond areissued and firms characteristics correspond to the beginning of the fiscal year in which the bonds are issued.Covenant restrictions are described in Appendix A and variable definitions appear in Appendix B. Standarderrors are adjusted for clustering at the firm level. t-stats are provided in parentheses. ***, **, * indicatesstatistical significance at the 1%, 5%, and 10% respectively.

Investment Restrictions Financing Restrictions

Estimate t-stat Estimate t-stat

Log(Assets) −0.41∗∗∗ (−7.06) −0.23∗∗∗ (−3.46)

Log(Market to Book) −0.82∗∗∗ (−5.09) −0.22 (−1.38)

Leverage 0.65∗ (1.84) 1.68∗∗∗ (3.24)

PPE/Assets 0.58∗∗ (2.33) −0.80∗∗ (−2.53)

EBITDA/Assets −0.50 (−0.70) 1.92∗∗ (2.08)

Cashflow Volatility −2.38 (−1.52) −2.27 (−1.41)

Firm Rating

A −0.52∗∗∗ (−2.73) 0.39∗ (1.92)

BBB −1.14∗∗∗ (−6.14) 0.87∗∗∗ (4.37)

BB 0.62∗∗∗ (3.62) 0.55∗∗ (2.53)

B 0.83∗∗∗ (3.57) 0.37 (1.54)

Log(Maturity) 0.08 (0.99) 0.05 (1.00)

Loan amount/Assets 1.12∗∗∗ (3.09) −0.29 (−0.71)

Putable −0.62∗ (−1.69) −0.75∗∗∗ (−3.35)

Callable 0.19 (0.62) 1.04∗∗∗ (4.95)

Convertible −2.02∗∗∗ (−9.53) −2.54∗∗∗ (−12.87)

Credit Spread 0.06 (0.49) 0.04 (0.47)

Term Spread 0.02 (0.57) −0.13∗∗∗ (−3.73)

Intercept 2.34∗∗∗ (3.44) 2.76∗∗∗ (3.59)

One digit sic code Yes Yes

R2 0.51 0.41

N 4221 4221

covenant = yes 522 3429

28

Electronic copy available at: https://ssrn.com/abstract=3241645

Tab

le3:

Inve

stm

ent

rest

rict

ions

Th

ista

ble

rep

orts

the

resu

lts

from

the

regr

essi

on

ineq

uati

on

(2)

for

cove

nant

rest

rict

ing

inves

tmen

tact

ivit

ies.

The

dep

end

ent

vari

ab

leis

the

chan

gein

capit

alex

pen

dit

ure

scal

edby

lagge

dass

ets.

Inve

stm

ent

rest

rict

ion

sis

ad

um

my

that

equ

als

on

eif

the

rest

rict

ion

ispre

sent

inth

eb

ond

contr

act.

All

contr

olva

riab

les

are

lagg

edon

eye

ar

exce

pt

for

cash

flow

wh

ich

isco

nte

mp

ora

neo

us.

Cov

enant

rest

rict

ion

sare

des

crib

edin

Ap

pen

dix

Aan

dva

riab

led

efin

itio

ns

app

ear

inA

pp

endix

B.

Sta

nd

ard

erro

rsare

ad

just

edfo

rcl

ust

erin

gat

the

firm

leve

l.t-

stat

are

pro

vid

edin

par

enth

eses

.**

*,**

,*

ind

icat

esst

atis

tica

lsi

gnifi

can

ceat

the

1%

,5%

,an

d10%

leve

l,re

spec

tive

ly.

PanelA:

∆CAPEX

=CAPEX

+1−CAPEX

−1

(1)

(2)

(3)

(4)

(5)

Inve

stm

ent

rest

r.−

0.01

∗(−

1.89

)−

0.02

∗∗(−

2.30

)−

0.01

∗(−

1.79

)−

0.02∗

∗(−

2.41

)−

0.01∗

(−1.

89)

Mil

lsR

ati

o0.

01∗

(1.8

6)0.

01∗∗

(1.9

9)0.

01∗

(1.6

9)0.

01∗∗

(2.1

4)

0.01

∗(1.8

3)

∆CashFlow

0.2

2∗∗∗

(7.0

1)0.

14∗∗

∗(4.7

9)0.

23∗

∗∗(7.4

1)0.

15∗

∗∗(5.2

7)

∆Q

0.0

2∗∗∗

(3.5

2)0.

01∗∗

(2.4

4)0.

01∗∗

∗(2.8

5)

0.01

∗∗(2.0

5)

∆Size

−0.0

9∗∗∗

(−7.6

0)−

0.0

8∗∗∗

(−7.3

2)

∆Leverage

−0.1

5∗∗∗

(−4.7

5)−

0.0

9∗∗∗

(−3.2

7)

Yea

rF

.E.

Yes

Yes

Yes

Yes

Yes

R2

0.0

70.1

60.2

40.1

90.2

5

N37

30

3703

3703

3703

3703

29

Electronic copy available at: https://ssrn.com/abstract=3241645

PanelB:

∆CAPEX

=CAPEX

+2−CAPEX

−1

(1)

(2)

(3)

(4)

(5)

Inve

stm

ent

rest

r.−

0.02

∗(−

1.84

)−

0.02

∗∗(−

2.31

)−

0.02

∗(−

1.92

)−

0.02∗

∗(−

2.42

)−

0.02∗

∗(−

2.02

)

Mil

lsR

ati

o0.

01∗

(1.6

9)0.

01∗∗

(1.9

7)0.

01∗

(1.7

8)0.

01∗∗

(2.0

7)

0.01

∗(1.8

7)

∆CashFlow

0.2

4∗∗∗

(6.7

7)0.

16∗∗

∗(4.6

7)0.

25∗

∗∗(7.1

5)0.

17∗

∗∗(5.0

0)

∆Q

0.0

2∗∗∗

(4.1

3)0.

01∗∗

(2.4

1)0.

02∗∗

∗(3.5

8)

0.01

∗∗(2.1

4)

∆Size

−0.1

0∗∗∗

(−7.2

5)−

0.0

9∗∗∗

(−6.8

5)

∆Leverage

−0.1

5∗∗∗

(−4.9

2)−

0.0

9∗∗∗

(−3.1

2)

Yea

rF

.E.

Yes

Yes

Yes

Yes

Yes

R2

0.0

80.1

90.2

70.2

10.2

8

N33

01

3278

3278

3278

3278

30

Electronic copy available at: https://ssrn.com/abstract=3241645

Tab

le4:

Fin

anci

ng

rest

rict

ions

Th

ista

ble

rep

orts

the

resu

lts

from

the

regr

essi

on

ineq

uati

on

(2)

for

cove

nant

rest

rict

ing

fin

an

cin

gact

ivit

ies.

Th

ed

epen

den

tva

riab

leis

the

chan

ge

inca

pit

alex

pen

dit

ure

scal

edby

lagg

edas

sets

.F

inan

cin

gre

stri

ctio

ns

isa

du

mm

yth

at

equ

als

on

eif

the

rest

rict

ion

isp

rese

nt

inth

eb

on

dco

ntr

act

.A

llco

ntr

olva

riab

les

are

lagg

edon

eye

arex

cep

tfo

rca

shflow

wh

ich

isco

nte

mp

ora

neo

us.

Cov

enant

rest

rict

ion

sare

des

crib

edin

Ap

pen

dix

Aan

dva

riab

led

efin

itio

ns

app

ear

inA

pp

end

ixB

.S

tan

dard

erro

rsare

ad

just

edfo

rcl

ust

erin

gat

the

firm

leve

l.t-

stat

are

pro

vid

edin

pare

nth

eses

.***,

**,

*in

dic

ates

stat

isti

cal

sign

ifica

nce

atth

e1%

,5%

,an

d10%

leve

l,re

spec

tive

ly.

PanelA:

∆CAPEX

=CAPEX

+1−CAPEX

−1

(1)

(2)

(3)

(4)

(5)

Fin

anci

ng

rest

r.0.0

4∗∗∗

(4.0

0)0.

03∗∗

∗(4.0

1)0.

02∗∗

∗(3.0

6)0.

03∗

∗∗(3.9

3)0.

02∗

∗∗(3.0

6)

Mil

lsR

atio

−0.0

1∗∗∗

(−4.0

0)−

0.0

1∗∗∗

(−3.9

9)−

0.0

1∗∗∗

(−3.1

3)−

0.0

1∗∗∗

(−3.9

4)−

0.0

1∗∗∗

(−3.1

3)

∆CashFlow

0.2

1∗∗∗

(6.8

5)0.

14∗∗

∗(4.7

1)0.

22∗∗

∗(7.2

5)

0.15

∗∗∗

(5.1

8)

∆Q

0.0

2∗∗∗

(3.7

1)0.

01∗∗

∗(2.5

8)0.

01∗

∗∗(3.0

4)0.

01∗

∗(2.1

9)

∆Size

−0.0

9∗∗∗

(−7.5

8)−

0.0

8∗∗∗

(−7.2

8)

∆Leverage

−0.1

5∗∗∗

(−4.6

6)−

0.0

9∗∗∗

(−3.1

9)

Yea

rF

.E.

Yes

Yes

Yes

Yes

Yes

R2

0.0

80.1

70.2

40.1

90.2

5

N37

30

3703

3703

3703

3703

31

Electronic copy available at: https://ssrn.com/abstract=3241645

PanelB:

∆CAPEX

=CAPEX

+2−CAPEX

−1

(1)

(2)

(3)

(4)

(5)

Fin

anci

ng

rest

r.0.0

5∗∗∗

(4.5

3)0.

05∗∗

∗(4.8

0)0.

04∗∗

∗(4.0

2)0.

05∗

∗∗(4.7

3)0.

04∗

∗∗(4.0

1)

Mil

lsR

atio

−0.0

2∗∗∗

(−4.5

6)−

0.0

2∗∗∗

(−4.6

8)−

0.0

1∗∗∗

(−4.0

4)−

0.0

2∗∗∗

(−4.6

1)−

0.0

1∗∗∗

(−4.0

2)

∆CashFlow

0.2

4∗∗∗

(6.7

6)0.

16∗∗

∗(4.6

5)0.

24∗∗

∗(7.1

3)

0.17

∗∗∗

(4.9

7)

∆Q

0.0

2∗∗∗

(4.4

3)0.

01∗∗

∗(2.6

4)0.

02∗

∗∗(3.8

8)0.

01∗

∗(2.3

7)

∆Size

−0.1

0∗∗∗

(−7.0

8)−

0.0

9∗∗∗

(−6.6

5)

∆Leverage

−0.1

5∗∗∗

(−4.7

5)−

0.0

9∗∗∗

(−2.9

9)

Yea

rF

.E.

Yes

Yes

Yes

Yes

Yes

R2

0.0

80.1

90.2

70.2

10.2

8

N33

01

3278

3278

3278

3278

32

Electronic copy available at: https://ssrn.com/abstract=3241645

Tab

le5:

Cou

nte

rfac

tual

regr

essi

onin

vest

men

tre

stri

ctio

ns

Th

ista

ble

rep

orts

the

mea

nof

pre

dic

ted

chan

gein

cap

ital

exp

end

itu

reu

sin

geq

uati

on

∆CAPEX

=α0IMR

+β1

∆Cashfow

+β2

∆Q

+β3

∆Size

+β4

∆Leverage

+ε i

Th

ed

epen

den

tva

riab

leis

the

chan

gein

cap

ital

exp

end

iture

scale

dby

lagged

ass

ets.

Th

ere

gre

ssio

nis

esti

mate

dse

para

tely

for

firm

sw

ith

an

dw

ith

out

Inve

stm

ent

rest

rict

ion

s.T

wo

sets

ofp

red

icte

dch

an

ge

inca

pit

al

exp

end

itu

reis

then

com

pu

ted

,ex

clu

din

gth

ein

vers

eM

ills

rati

o,

for

the

enti

resa

mp

leu

sin

gth

ees

tim

ates

from

bot

hre

gre

ssio

ns,

on

ese

tw

ith

the

coven

ant

rest

rict

ion

s)an

da

corr

esp

on

din

gse

tw

ith

ou

tit

.A

llco

ntr

ol

vari

able

sar

ela

gged

one

year

exce

pt

for

cash

flow

wh

ich

isco

nte

mp

ora

neo

us.

Cov

enant

rest

rict

ion

sare

des

crib

edin

Ap

pen

dix

Aan

dva

riab

led

efin

itio

ns

app

ear

inA

pp

end

ixB

.S

tan

dar

der

rors

are

ad

just

edfo

rcl

ust

erin

gat

the

firm

leve

l.t-

stat

are

pro

vid

edin

pare

nth

eses

.***,

**,

*in

dic

ates

stat

isti

cal

sign

ifica

nce

atth

e1%

,5%

,an

d10%

leve

l,re