bogumil brzezinski tomasz kardach tax competition in poland - national ... · 1 bogumil brzezinski...

TRANSCRIPT

1

Bogumil Brzezinski

Tomasz Kardach

Zbigniew Wojcik

Centre of Tax Documentation and Studies

University of Lodz

e-mail: [email protected]

Tax Competition in Poland - National Report

I. General aspects of the domestic tax situation

Insufficient attention has been put so far to the aspects of tax competition in the Polish tax

literature. Neither lawyers nor economists have so far covered the issue in depth so that one

could draw a clear picture of a scientific approach towards the notion of the “tax

competition”. It is however widely recognized that the tax competition is one of the fields

that demands deep research especially in the light of globalization of production and trade and

the growing mobility of capital. Another reason for the more extensive research of this issue

results from the lack of proper awareness of the Polish governments and legislators as to what

the competitiveness of a tax system means.

The tax law is one of the youngest areas of the Polish law and as a result contains deficiencies

and errors which the following governments attempt to fix. The fixing of the mistakes is

usually an ad hoc action which lacks a comprehensive view of the whole tax system including

among other things its competitiveness. The competitiveness has both the positive and the

negative dimensions - the negative dimension being called the “unfair tax competition”.

Structuring of the tax system should assume the positive competitiveness of the domestic tax

system and inclusion of measures aimed at combating the negative effects of the unfair tax

competition applied by other countries.

A general look at the Polish tax system seem to indicate that it lacks the positive aspects of

the competitiveness of the tax system while missing measures against the negative effects of

the unfair tax practices of certain other countries. As a result Poland is not perceived as the

country with friendly tax legislation and what is important to note rather unfriendly attitude of

2

the tax administration. The economic effects of the current situation are negative for Poland

for two major reasons (a) the foreign (and domestic) “capital” is discouraged from investing

into Poland due to the unfriendly tax environment i.e. the number of investment is lower than

expected and (b) due to the lack of certain domestic provisions and necessary awareness of

the tax administration certain income arising in Poland escape the taxation in Poland.

It is expected that since the Polish tax system becomes more mature the current deficiencies

shall progressively disappear.

II. Elements of tax competition in the domestic tax system

The assessment whether the domestic tax regulations contain provisions which may be

considered as unfair from a tax competitiveness perspective requires the analysis of the

following major elements:

1. Tax rates

1.1.Business profits

The Polish CIT law provides for a flat 28% CIT rate,1 which is applicable to all business

income except for so-called exempt income or where different tax rates apply see below. The

same tax rate is applicable to residents as well as to non-residents.

1.2 Capital gains

There is no special capital gains tax rate in Poland. Capital gains are taxed with a standard

CIT rate.

1.3 Interest

The interest paid between residents is subject to a standard CIT rate. There is no withholding

tax on interest paid between resident taxpayers.

1 The current CIT Law provides that for the tax year starting on 1 January 2003 the CIT rate will be reduced to24 %. Beginning of 1 January 2004 the CIT tax rate shall be 22%.

3

The interest paid to non-residents is subject to 20% withholding tax unless relevant provisions

of a double tax treaty provide otherwise.

1.4 Royalties

Royalties paid between residents are subject to a standard CIT rate. There is no withholding

tax on royalties paid between resident taxpayers.

Royalties paid to non-residents are subject to 20% withholding tax unless relevant provisions

of a double tax treaty provide otherwise.

1.5 Dividends

Dividends paid by resident taxpayers are subject to 15 % withholding tax no matter the

percentage of interest held in the paying company. If the recipient of the interest is a non-

resident entity the withholding tax rate may be reduced by relevant provisions of a tax treaty.

1.6 Special tax rates applicable to particular activities performed by non-residents

a) Non-resident shipping and air transportation companies

Non resident shipping and air transportation companies are subject to 10% lump sum CIT rate

on their gross income derived from the passenger and cargo transportation services performed

at the territory of Poland unless relevant provisions of a tax treaty provide otherwise.

b) Special rules/rates for non-residents who do not keep proper accounting books

In general all taxpayers (both resident and non-resident) are obliged to keep proper accounting

records in accordance with the accounting rules. The accounting books should be kept in a

manner that ensures proper calculation of an income (loss) and the amount of CIT due in a

given tax year including proper record of fixed and intangible assets allowing for the

calculation of the amount of depreciation write-offs. In case where the calculation of income

4

is not possible due to the lack of proper accounting records the tax authorities shall estimate

the amount of income by way of assessment.

There are special rules with respect to non-resident taxpayers failing to keep proper

accounting books. In case such taxpayers do not posses proper accounting records their

income is established based on a special ratio of income (net income) to revenue (gross

income). The following percentage ratios are applicable:

i) 5 % in respect of wholesaling and retailing2;

ii) 10 % in respect of construction and installation services or transport service;

iii) 60 % in respect of services of intermediary, where remuneration for those services is

in a form of commission;

iv) 80 % in respect of legal counsel services or expert services;

v) 20 % in respect of other sources of revenue.

The above rules apply unless the provisions of a relevant tax treaty provide otherwise.

1.7 Final remarks

The standard corporate income tax rate in Poland does not seem to be either excessive or

lower than the tax rates applicable in other OECD countries. With the exception of those non-

resident taxpayers who do not keep proper accounting books the Polish tax regulations do not

provide for special corporate income tax rates for non-residents. Accordingly, the same tax

rate applies to resident and non-resident taxpayers.

The special rules of estimating income of non-residents derived from certain activities

performed at the territory of Poland might be seen as giving those taxpayers a flexibility of

choosing the method under which they would be taxed in case they do not want to comply

with the strict rules of keeping proper accounting books. It should be however noted that as a

matter of principle all taxpayers should keep proper accounting books i.e. it is not an option

2 The "wholesaling or retailing" carried on in the territory of the Republic of Poland shall be understood to coverthe sale of goods to Polish customers against payment, regardless of the place of execution of contract-where the

5

for the taxpayers to keep the records. The ratios have been established on the basis of the

expected profitability of those businesses and seem to be rather aggressive that conservative.

Accordingly, although in particular circumstances it might be more beneficial to use this form

of estimating tax base in general the provisions are not perceived to be particularly attractive

for the non-residents and in practice are rather rarely applied. In addition, it should be noted

that the lack of proper accounting records means that the taxpayer is in breach of its

obligations following from the tax and accounting rules. This in turn is likely to result in

fiscal and penal consequences for the individuals responsible for keeping accounting records

or in case of a lack of such allocated person the negative consequences may reach the

members of the management board of such taxpayer.

2. Tax accounting

2.1 Tax income v. accounting profit

As mentioned in the section above all taxpayers earning income in Poland are obliged to keep

proper accounting books. Proper accounting books mean that the records should be kept in

accordance with the Polish accounting law.

Although the taxpayers are obliged to keep proper accounting books the taxable base is

calculated based on the tax regulations. In other words the tax income is not calculated as the

accounting profit plus adjustments made for tax purposes (although in practice this may be

seen such). The Polish tax law keeps its own terminology and methods, which are different

from those contained in the accounting rules.

Depending on the particular situation of a given taxpayer the difference between the

accounting profit achieved by him and his actual income subject to corporate income tax (or

in case of individual entrepreneurs the personal income tax) may be significant. The major

differences between the accounting profit and the tax income result from a different

classification for tax purposes of specific revenue and costs items. In case of revenue those

differences include among other things the accrued interest (due but not yet received) which is

added to the accounting profit. For tax purposes such an interest is not taxable since based on

said taxpayers maintain in the territory of the Republic of Poland a representative office operating under a permit

6

the tax regulations only the so called “realized” interest (mostly paid up interest) is treated as

income in the hands of the recipient. This is the so-called temporary difference between the

accounting profit and the taxable income. There are also permanent differences like the value

of debt forgiveness or debt reduction certified by the court based on the special regulations.

Such a value (amount) increases the accounting profit while it will never be treated as the

revenue for tax purposes. On the costs side the major discrepancies include the differences in

depreciation (both in terms and methods), the treatment of doubtful debts (the debts which

from an accounting perspective should be provisioned or written off do not have to be treated

as deductible costs), and a significant number of other non-deductible costs listed in the

corporate income tax law. An exemplary list of such costs is provided in the Appendix 1 to

the Report.

With regard to the tax accounting issue two things should be noted:

a) The Polish regulations concerning the tax accounting do not appear to be more

advantageous then the respective rules of the other OECD countries. If differences

exist they do not seem to be favorable for the taxpayers settling their tax liability in

Poland and,

b) As far as the calculation of the taxable income is concerned the Polish tax law does

not treat differently the resident and the non-resident taxpayers with the limited

exceptions mentioned elsewhere in the Report.

2.2. Double taxation relief and other advantages for cross-border business

a) Interest and royalties

There is no withholding tax due on interest or royalties paid between resident taxpayers. The

income from interest and royalties is cumulated with the trading and other income in the

hands of the recipient and taxed with a standard corporate income tax.

Interest and royalties paid by residents to non-resident recipients are subject to 20%

withholding tax unless the relevant tax treaty provides for a lower tax rate. The Appendix 2

lists the withholding tax rates applicable in the tax treaties concluded by Poland.

issued by the minister proper for the economy or by another minister of competent jurisdiction.

7

b) Dividends

As far as the flow of dividends between resident taxpayers is concerned the Polish CIT law

provides for a credit method as the method of avoiding double taxation. Based on the relevant

regulations the amount of the paid withholding tax from dividends and “other income from

the participation in profits of legal persons” resident in Poland is deducted from the total tax

liability calculated under the CIT law. In case the deduction is not possible (a company is in a

loss making position) then the tax paid may be deducted in the following tax years (without

time limit).

In case of dividends received from non-residents the double taxation is avoided based on the

provisions of the relevant tax treaty (See Appendix 2).

In case of dividends received from non-residents based in countries with which Poland does

not a have a tax treaty these are subject to a standard corporate income tax and no tax relief is

available.

Since the 1st January 2001 CIT law grants credit for underlying tax, subject to certain

requirements. If a Polish parent company has at least 75 per cent of the voting rights in the

subsidiary resident in a country with that Poland concluded a tax treaty, the parent may credit

not only the foreign withholding tax paid on dividends but also the amount of the underlying

foreign corporate income tax paid by that subsidiary on the income out of that the dividends

have been paid. The credit may not however be higher than the amount of tax calculated

before the deduction that would in proportion concern income from the given source.

4. Procedural advantages

4.1 Secrecy provisions and the exchange of information

As any other OECD country Poland adopted the regulations governing the issue of the tax

secrecy.3 In general, those provisions are aimed at ensuring that the fiscal information

concerning a particular taxpayer remains known only to the tax authorities and is properly

3 Section VII of the Polish tax code (arts 293-305).

8

used by the tax authorities in the process of any tax investigations. The Polish regulations

define the types of information covered by the secrecy provisions, the persons to whom the

obligation of confidentiality specifically applies as well as the rules of exchanging

confidential information.

The Polish regulations on the tax secrecy do not appear to create any procedural advantages in

comparison to other OECD countries. The law provides that the tax authorities reveal the tax

information to the extend and according to the rules contained in the domestic laws and the

ratified international agreements to which Poland is a party.

A specific provision of the Polish tax code states that the tax information may be exchanged

with the tax authorities of other countries to the extend and according to the rules of the tax

treaties and other ratified international agreements to which Poland is a party and under the

condition that the domestic provisions of the other countries guarantee that the confidential

information will be used in accordance with the rules provided for in such agreements.

The tax treaties concluded by Poland are based on the OECD Model Convention and

accordingly contain specific provisions dealing with the exchange of information. It is usually

the Art. 27 of the tax treaties which provides for the rules of exchanging information between

the tax administrations of the parties to the treaty.

The issue of the exchange of information is particularly relevant with respect to cross border

transactions with affiliated entities (also called the “related parties”). The establishment of an

arms’ length price by the tax authorities may not always be in line with what the authorities of

the other country consider being the price at arm’s length. In case of such a conflict proper

and timely exchange of information is crucial. As indicated separately in this report the Polish

provisions on transfer pricing are in line with the OECD guidelines and the Polish tax

authorities put special emphasis on identifying suspicious transactions.

In general the Polish tax authorities seem open to any co-operation with the tax authorities of

other countries (especially the tax authorities of the OECD countries). It must be however

noted that besides the positive attitude the proper exchange of information requires certain

technical abilities including, but not limited to proper databases, appropriate training of the

tax administration, including teaching of foreign languages (English in particular), and as

9

always realistic budgets available to the tax administration for these purposes. Unfortunately,

the Polish tax authorities lack most of the necessary technical abilities and as a result there is

a significant area for improvement as far as the exchange of information is concerned. It

should be noted however that there is no winner of the current situation. Both the tax

authorities (Polish and the foreign) and the taxpayers suffer from the insufficient information

exchange. Maybe except for those taxpayers who use the current situation for the tax evasion

purposes.

4.2 Rulings

The concept of the tax rulings quite popular in some of the OECD countries has been

introduced into the Polish tax regulations only in 1997. The relevant regulations provide that

the Ministry responsible for the financial matters generally supervises the tax matters. The

Ministry is also responsible for securing the uniform application of the tax laws by the tax

authorities. Such uniform application shall, among other things be achieved through the

official formal interpretation of the tax laws taking into account the case law of the courts and

the Constitutional Tribunal. Such official interpretation is then published in an official

gazette. It is not directed to a particular taxpayer and as a consequence it is not intended to

solve a particular issue of an individual taxpayer. By its nature however the official

interpretation should concern issues having more general application to all or a significant

number of taxpayers. The law clearly states that the taxpayers cannot suffer from following

the official interpretation.

In case where a taxpayer has doubts as to the application of a particular provision of the tax

law to his case and provided no formal tax investigation has been initiated by the tax

authorities with regard to the application of such provision for the taxpayer such a taxpayer

may apply to the tax office for a written ruling. The introduction of the tax rulings was aimed

at facilitating the co-operation between the taxpayers and the tax administration and ensuring

that prior to executing certain actions which may lead to negative tax effects the taxpayers

may obtain assurance as to the tax consequences of such actions. It is important to note

however that the actual construction of the relevant provision as well as the practice of its

application raises doubts as to the effectiveness of the Polish rulings’ provisions. There are

two major reasons for these doubts (a) there is no legal assurance in the tax laws that the

addressee of the ruling may not suffer from the following of the ruling issued to him i.e. if the

10

tax authorities change their mind the one who suffers will be the taxpayer and (b) the actual

approach of the tax authorities is extremely fiscal i.e. the rulings are usually negative

especially where the issue at stake is not straightforward but more sophisticated and requires

more complex interpretation of law.

The above short description of the Polish rulings system implies that both the construction

and the actual application of the rulings do not appear competitive versus the other OECD

countries and do not seem encouraging the non-Polish taxpayers to use it as a way of

obtaining a favorable tax treatment in Poland.

5. Other

5.1 Tax groups

In 1996 Poland introduced provisions allowing certain taxpayers to file consolidated tax

return. The Polish provisions are construed in such a way that they provide for the possibility

of forming a new taxpayer which consists of previously separate taxpayers. As a result of

forming the new taxpayer - the so-called “tax group”, the individual taxpayers cease to exist

or more precisely their existence is suspended for the period of filing the consolidated tax

return as the tax group.

Normally such provisions should be seen as advantageous and encouraging e.g. additional

investment in Poland by allowing the initial start up losses of one entity within a group of

companies to be fully and immediately set off against the profits of another profit making

entity (entities). Even if limited to resident taxpayers the provisions of the tax consolidation

could be seen as an important element of the tax competition.

The content of the relevant provisions and the actual practice of their application in Poland

indicate however that the possibility of the tax consolidation in Poland should be seen as a

theoretical rather than the actual option. The conditions of forming and operating of the tax

group are so strict that in vast majority of cases they exclude making of a reasonable decision

to create the tax group. In practice therefore a very limited number of tax groups have been

registered in Poland (the number does probably not exceed 3-5 tax groups in Poland).

11

Accordingly, the provisions of the tax consolidation in Poland should not be seen in practice

as an element of the tax competition.

5.2 Special economic zones

In 1994 Poland adopted rules allowing for the creation of the so-called Special Economic

Zones (“SEZ”). The SEZ is an area where the investors may benefit from specific incentives.

The most important being the tax advantages.

The available tax relieves have been determined by a decree for each zone (there are currently

[14] SEZ in Poland). Persons qualifying for relieves are legal entities and individuals

performing business activities exclusively within a zone's territory. The provisions of special

economic zones are applicable to entities incorporated under the Polish law. In other words

the foreign investors can only benefit from the special tax treatment if they invest in Poland

by establishing a legal entity with its registered address within the territory of the zone.

The most important relieves include:

(a) an exemption from the corporate income tax of income derived in a particular zone up

to an amount equal to the investment expenditure incurred in the zone by a taxpayer. If

the expenditure exceeds a certain threshold, the income is fully exempt. The

thresholds range from ECU 350,000 to ECU 2 million depending on the zone.

(b) in general a 10% deduction from income may be claimed for every 10 employees, up

to a maximum of 100%.

Relief is granted generally for a period of 10 years (in some cases 6 years). After the expiry of

the 10-year period the tax exemption amounts up to 50% of a taxpayer’s income. No tax

relieves are available after the expiry of the period for which a zone was established.

The provisions of the special economic zones have been heavily criticized especially by the

members of the European Union for creating an unfair tax competition. It should be noted that

the creation of special economic zones have been aimed at encouraging foreign investors to

locate their investments in areas significantly suffering from high structural unemployment.

No doubts the possibility of saving on taxes is always an important factor in deciding where

to locate possible investment. As a matter of principle therefore the provisions of special

12

economic zones may be considered as creating an unfair tax competition. It should however

be noted that in practice the special economic zones do not appear to be successful. The actual

number of investors comparing to the original expectations is very low. In addition, the

investment in the zones is perceived by certain taxpayers as a trap from which they cannot

escape for the next couple of years. It is common that the taxpayers in the zones are subject to

a permanent tax audits and spend significant amount of time on dealing with the tax

authorities and what should not be forgotten a significant amount of money for the tax

advisors while the actual tax savings, taking into account the start up losses and the general

recession may be in some instances minimal or null.

III. Measures against “unfair” competition in the domestic tax system

1. General anti-avoidance measures

The tax law does not provide for any general measures with regard to counteracting the tax

avoidance although attempts to introduce such instruments have been made in the past.

In the light of the lack of any specific tax law provision the Polish courts attempted, on

several occasions, to invoke a general anti-avoidance rule contained in the Polish civil code.

The relevant provision reads as follows: “Legal activity performed contrary to the law in force

or aiming at circumvention of the law is void unless a special regulation exists that provides

for another effect of such performance, particularly the one that provides for replacement of

void activities by relevant provisions of a statute”. The opinion whether provisions of the civil

code, which governs the private law relationships, could be effectively applied with regard to

the public law relationship (the liabilities arising from the public law provisions) differs

among the scholars. However as mentioned above the Polish courts invoked this provision on

several occasions.

In one of its judgements the Supreme Court stated:

“Provisions of tax law include adequate instruments for fulfilling tasks inscribed into them

and the tax authorities are not obliged to respect legal activities aiming at circumvention of a

tax statute…”(Judgement of the High Court of 08. February 1978, sygn. II CR 1-78).

13

In another case the Supreme Administrative Court took a similar position:

“In tax cases the authorities deciding on merits are allowed to evaluate civil law contracts not

only from the narrowly understood fiscal interest but also are allowed to evaluate essential

parts of contracts with a view to legal effects derived from general provisions of the civil code

on legal activities and provisions on contractual obligations not excluding examination in

light of regulation included in art. 58 § 1 in conjunction with art. 353 § 1 of the civil code.” (

Supreme Administrative Court judgement of 07 April 1999, sygn. III S.A. 1610/98).

Application and especially the scope of application of the provision of Art. 58 of the civil

code in tax cases may be questionable. If it is established that the mentioned above provision

is to be applied in tax cases one has to accept all the consequences of such a position. The

most important is the one that application of the provision in tax law case is directly

dependant upon meeting the prerequisites provided for in civil law. The legal action

performed in fraudem legis may be defined as act that is not illegal as such but resulting in an

effect that is contrary to the law. If the definition is considered for purposes of tax law one

may get to the conclusion that a civil law act resulting in lowering of the final tax burden

should be regarded as performed in fraudem legis so a general legal rule should be inscribed

into tax law either providing for requirement of payment the highest possible tax or on the

other hand providing for prohibition of lowering tax burden. A conclusion might be that if a

taxpayer has a choice of the way (a sequence of legal acts) of getting to a given result by

shaping his activities in certain manner he would be obliged to perform such legal acts that

would result in highest final tax burden.

The legal sanction provided for in Art. 58 §1 of the civil code is not applicable in tax law

cases. The Supreme Administrative Court took several times the position that legal acts

aiming at circumvention of the tax law is not void but the tax authorities are allowed not to

respect their provisions (Supreme Administrative Court judgements of 22 May 1997 sygn. I

SA\Po 1052\96, and of 19 March 1997, sygn. SA\Ka 30\95).4

2. Controlled Foreign Corporations Legislation

There is no CFC legislation in Poland

4 M. Kalinowski “Granice legalnoœci unikania opodatkowania w polskim systemie podatkowym” p. 103 Toruñ2001

14

3. Residence rules

3.1. General principles

a) Corporate income tax

Taxpayers with their seats or management in the territory of Poland are liable to tax on the

whole of their income regardless of the location of its sources i.e. worldwide taxation or the

“unlimited tax liability”.

Taxpayers with no seat or management in the territory of Poland are liable to tax on income

obtained (earned) only in the territory of Poland; the “limited tax liability”.

b) Personal income tax

Individuals who have their place of abode in the territory of Poland or stay within the territory

of Poland for a period longer than 183 days in a given tax year are subject to tax on the whole

of their income regardless of the location of its sources i.e. worldwide taxation or unlimited

tax liability.

Individuals who do not have their place of abode in the territory of Poland are subject to tax

only on income from “work” performed in the territory of Poland on the basis of professional

or a labour relationship irrespective of the place of payment of the remuneration and on other

income earned in the territory of Poland (limited tax liability).

The limited tax liability applies also to individuals who stay in Poland temporarily, even if for

more than 183 days in a tax year, but who are employed by corporations with foreign

participation (including branches and representation offices of foreign enterprises and banks).

Members of foreign diplomatic missions or consulates are treated as non-residents

irrespective of their domicile or length of stay in Poland.

a) Territory of Poland

15

For the purposes of both the corporate income tax and the personal income tax the territory of

the Republic of Poland shall include any exclusive economic zones situated outside the

territorial sea limit in which the Republic of Poland exercises, pursuant to domestic laws and

international laws, rights relating to the exploration and exploitation of the sea bed and sub-

soil and of the natural resources therein.

3.2 Selected issues connected with the determination of the residence status

a) Seat and management

As mentioned in the section above the two factors determining the residence status are the

seat and the management of the company.

The term “seat” of the company has not been defined in the tax laws. The seat of the company

is determined by the constitutive documents of the company. Based on separate provisions of

commercial companies code a company incorporated in the territory of Poland must have its

place of seat in the territory of Poland. Accordingly, each legal entity established under the

Polish commercial law by definition becomes the Polish tax resident.

The term “management” of the company has not been defined in the tax laws. It is however

clear that the management of a Polish entity does not have to be exercised from the territory

of Poland i.e. the management can be placed outside of Poland.

An important issue concerns the situation of non-residents having the actual place of

management in the territory of Poland. The Polish law does not provide for any test to be

passed for the purposes of determining if an entity has a place of management in the territory

of Poland. The situation is less problematic if the case involves a company resident in the

country, which concluded the tax treaty with Poland. The relevant provisions of the tax treaty

use the term “place of effective management” which has been extensively defined in the

OECD guidelines, i.e. in case of doubt the place of effective management is decisive..

Less clear is however the situation when the entity involved has been incorporated under the

legislation of a country which did not conclude the tax treaty with Poland, especially if the

company is based in a tax haven. The lack of proper tax residency test may result in either

16

“too extensive” or “to narrow” interpretation of the term “management in Poland”. Since

there are no clear guidelines in the domestic law the tax authorities may attempt to apply very

broad interpretation of the term “management” and as a result the might try to tax “more”

than they normally should. As far as the issue concerns entities based in a tax haven country

one should not have generally a problem with “unfair tax competition towards a tax haven”.

The problem may however equally concern entities based in non-tax haven country which has

not (yet) signed a tax treaty with Poland i.e. in such case the current Polish tax legislation plus

the fiscal approach of the Polish tax authorities might theoretically result in practices of unfair

tax competition. It should be noted that no cases of such an approach have been observed so

far.

Moreover the lack of proper test regarding the “place of management” appear to involve more

potential exposure for Poland been insufficiently prepared to combat possible unfair tax

competition of other countries and/or the tax evasion of non-resident taxpayers. There are two

major reasons behind it (a) although no survey to this extend has been made there seem to be

many companies incorporated in a tax haven which are effectively managed from the territory

of Poland; (b) there seem to be insufficient awareness of the above factor among both the tax

authorities and the legislator.

As a result of the above factors Poland may actually be suffering from the lack of proper,

more detailed definition of the term “management” in the corporate income tax law and

taxpayers, which should have been treated as residents in Poland escape any (even limited)

taxation in Poland.

b) Permanent establishment

The considerations in the section above indicate that the Polish tax law does not provide for

proper rules on the taxation of permanent establishments.

The provisions of the corporate income tax and the personal income tax laws, which refer to

the taxation of non-residents, provide that such taxpayers are subject to tax on income

obtained in the territory of Poland. There are no provisions stating which factors should be

taken into consideration to establish if a company is subject to taxation in Poland i.e. if it has

17

a permanent establishment in Poland. In other words the domestic provisions do not provide

for any rules similar to those contained in Article 5 of the OECD Model Convention.

Similarly there are no provisions in the Polish tax law that would provide for the methods of

allocation of profits between the permanent establishment and the head office like the rules

contained in the Article 7 of the OECD Model Convention.

Depending on the actual approach of the tax authorities in Poland the lack of proper rules

might lead to either to excessive or to narrow application of the Polish provisions of the

limited tax liability. It should be noted that so far the tax authorities did not put enough

attention to the taxation of permanent establishments and as a result the current situation

results in rather negative fiscal effects for Poland Although no research on this issue have

been made it is probable that the is a significant number of foreign taxpayers operating in

Poland through permanent establishments which have not been identified (and consequently

not taxed) by the Polish tax authorities.

4. Restrictions of deductions of payments to tax haven entities

There are no provisions that would specifically restrict the deduction payments made to

entities based in tax havens.

However, since 1 January 2001 Poland introduced regulations that are literally aimed at

controlling transactions with entities based in tax havens. These provisions however in

practice restrict the deductibility of payments if the rules provided for in the regulations are

not met.

Based on the relevant regulations taxpayers entering into transactions, in which a payment is

effected directly or indirectly to an entity having its seat or place of management in the

territory or in the state “applying harmful tax competition” are obliged to report such

transactions disclosing the following data:

1. role of parties to the transaction (including capitals engaged and undertaken risk),

2. costs incurred with regard to the transaction as well as form and terms of payment,

3. methods of profit calculation and method of establishing the price of the object of the

transaction,

18

4. description of corporate strategy in case if the value of the transaction was influenced by

the strategy applied by the taxpayer,

5. indication of other features in case they influenced value of the transaction,

6. indication of gains expected by the party obliged to produce the report if it is receiver of

services of intangible character.

Obligation derived from article 9a covers transactions in that a payment is effected directly or

indirectly to an entity having its seat or place of management in a territory or in a state

applying harmful tax competition if a total value of the transaction in a tax year amounts to

more than EUR 20.000.

The tax authorities may at any time require from a taxpayer the data mentioned above and the

taxpayer is obliged to provide the tax authorities with necessary information within a period

of 7 days from placing the request by the tax authorities.

The above obligation of keeping relevant tax documentation concerns the transactions in

which a payment is effected directly or indirectly to an entity having its seat or place of

management in the territory or in the state applying harmful tax competition irrelevant

whether the transaction is entered into between the affiliated entities or not. The provision

relates to any transaction where the payment is made to an entity based in a tax haven.

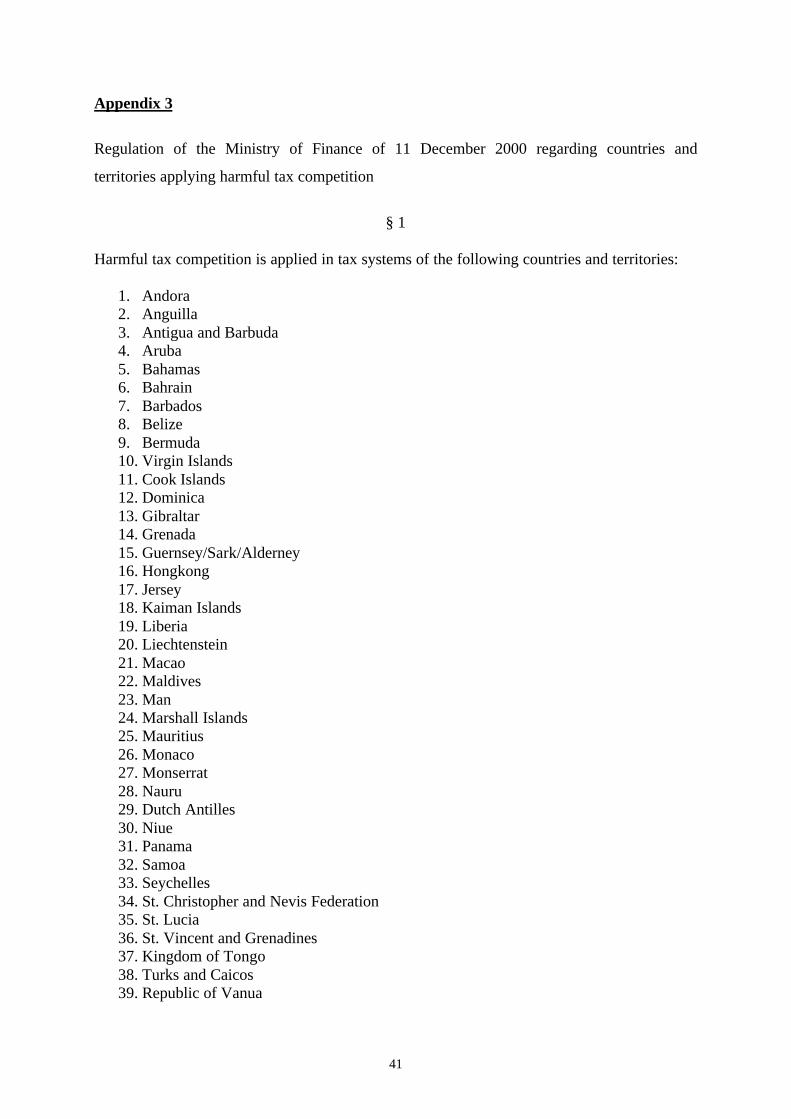

The ministry responsible for public finance (the Ministry of Finance) settled a list of states

and territories applying harmful tax competition and published it in the form of a regulation.

The list is included in Appendix 3. It is noticeable that the regulation covers quite a large

number of countries and territories. That indicates the strict policy of the Polish government

aiming at combating phenomena of tax avoidance and tax evasion.

In case of doubt whether the transaction effected with tax haven entity is made on market

conditions the tax authorities may estimate the market value of the transaction as well as the

income and tax arising out of such transaction. If the tax authorities estimate the taxable

income higher than declared by a taxpayer or a loss is estimated lower than declared with

regard to transactions where the payment is effected directly or indirectly to an entity having

its seat or place of management in the tax haven territory and the taxpayer does not provide

the tax authorities with data (mentioned above) proving that tax authorities’ calculation is

19

wrong the tax rate of 50% is applicable to the difference between the income declared by the

taxpayer and the income estimated by the authorities.

5. Other

5.1. Transfer pricing regulations

It is generally known that from a consolidated perspective of the MNC’s the transactions

performed between their individual parts do not have to be concluded on market conditions.

On the other hand deviations from the market prices in their internal - but cross border

transactions - may have significant damaging effects for the countries in which certain entities

of the MNC’s are based.

The Polish tax regulations do not seem to be particularly attractive in comparison to many

other countries, even those which are not regarded as the tax havens. Accordingly, one of the

major problems of the Polish tax administration concerns the actions of those taxpayers who

are members of multinational corporations having their parts based in different geographical

locations including those of a very preferential tax treatment.

Prior to 1997 Poland did not have proper transfer pricing regulations. Before 1996 the law

provided for only one method that could be used for estimation of prices in transactions

entered into between related parties, namely the comparable uncontrolled price method

(CUP). The law was amended to incorporate other OECD methods such as cost plus and

resale price methods as well as profit based methods.

The relevant provisions in the shape envisaged by the OECD guidelines were introduced on

01 January 1997.5

The Polish the transfer pricing provisions are applicable to both the cross border and the

internal transactions between the related parties.6 This is one of the peculiarities of the Polish

regulations since they are not only aimed at cross border situations.

5 Regulations concerning transfer pricing are included both in the Corporate income tax law of 15 February19925 (art. 11) and Individual income tax law of 26 July 1991 (art.25)6 The notion of related parties when one is the Polish and the other is a foreign enterprise encompasses thefollowing situations:

20

In cases where prices in transactions between the related parties are not arm’s length the tax

authorities may assess the arm’s length price based on the transfer pricing methods provided

for in the regulations. Following the OECD guidelines the Polish regulations list the following

transactional methods that may be used to estimate the arm’s length prices

(a) the comparable uncontrolled price method,

(b) the resale price method

(c) the reasonable margin ("cost plus") method.

Where the application of the methods referred to above should be impracticable, the profit

based methods may be adopted. The allowable methods include: profit split method and

transactional net margin method.

Since the introduction of the transfer pricing regulations the tax authorities significantly

increased the number of tax audits performed on “affiliated” taxpayers. Both the tax

authorities as well as the taxpayers put a significant attention into respectively controlling and

properly structuring the inter-company transactions to ensure that they are made in

compliance with the regulations.

5.2 Reporting requirements

- a taxpayer of income tax having its seat (headquarters) or place of abode in the territory of the Republic ofPoland, hereinafter called "domestic subject", involves directly or indirectly in the management or supervision ofa business situated abroad or is a shareholder of that business, or- an individual or a corporation whose place of abode or seat (headquarters) is outside the territory of theRepublic of Poland, hereinafter called "foreign subject", involves directlyor indirectly in the management or supervision of a domestic subject or is a shareholder of that domestic subject,or- the same individuals or corporations involve contemporaneously, whether directly or indirectly, in themanagement or supervision of a domestic subject and a foreign subject, or are shareholders of the said subjects.

The domestic relationship is defined as follows: taxpayer remains associated with a domestic subject.where the subjects or persons discharging management, supervision or control functions in respect of thesubjects are connected by family, capital or property ties or by a relationship of employment. The associationshall likewise be understood to exist where any of the aforesaid persons holds contemporaneously positions ofmanagement, supervision or control in the subjects. The provisions will as well be applicable in case of businessaffiliations with another domestic subject. Such situation may take place in particular where the said subjects arelinked by an agreement of partnership organised under the civil law, general partnership, limited partnership,joint venture, joint usufruct of things or rights, or co-operation agreement.

21

The new provisions of art.9a have recently been introduced into the corporate income tax law7

(they have been in force since the 1st of January 2001).

Taxpayers entering into transactions with associated enterprises are obliged to report such

transactions disclosing the following data:

1. role of parties to the transaction (including capitals engaged and undertaken risk),

2. costs incurred with regard to the transaction as well as form and terms of payment,

3. methods of profit calculation and method of establishing the price of object of the

transaction,

4. description of corporate strategy in case if the value of the transaction was influenced by

the strategy applied by the taxpayer,

5. indication of other features in case if they influenced value of the transaction,

6. indication of gains expected by the party obliged to produce the report if it is receiver of

services of intangible character.

Obligation envisaged in new provision of art. 9a indent 1 covers transactions entered into by

associated enterprises in that a total value of the transaction in a tax year amounts to more

than:

a) EUR 100.000 if the value of transaction amounts to less than 20% of share capital,

b) EUR 30.000 in case of providing for services, sale of intangibles,

c) EUR 50.000 in all other cases.

Tax authorities may in any time require from a taxpayer data indicated in article 9a and a

taxpayer is obliged to provide tax authorities with necessary information within the period of

7 days from the date on which tax authorities turned to a taxpayer.

If tax authorities estimate taxable income higher than declared by a taxpayer or a loss is

estimated lower than declared with regard to transactions with associated enterprises or

transactions in that a payment is effected directly or indirectly to an entity having its seat or

place of management in the territory or in the state applying harmful tax competition and the

taxpayer does not provide tax authorities with required evidence – the tax rate of 50% is

7 Dz.U. of 2000 No 60 pos.700

22

applicable to deference between income declared by the taxpayer and income estimated by the

authorities.

5.3 Thin capitalisation

“Thin capitalisation” takes place if a company in its activity uses mainly loan or credit capital

restricting its equity to a necessary minimum. In other words a company is said to be “thin

capitalised” when its equity capital is small in comparison to its debt capital.

From the tax law point of view the difference is significant. Interests paid by a company with

regard to loans (credits) are usually treated as costs of earning revenue on the other hand a

dividend paid by a company may never be a cost from the tax law point of view (for the

provisions of CIT law see Appendix 4).

5.3.1 Loans and credits that come under restrictions

Article 16 item 1 point 60 covers interests from loans and credits granted to company by its

shareholders and article 16 item 1 point 61 covers interests from loans and credits granted by

one company to another where in the both companies the same shareholder holds no less than

25 percent capital (shares).

The thin capitalisation rules do no apply to interest on loans granted by resident companies

provided that these companies do not benefit from income tax incentives or exemptions.

5.3.2 Assessment of allowed level of debt-to-equity ratio

Interest due on loans (credits) made to a company by a shareholder whose equity stake

(shares) in the company represent no less than 25 percent of the company's capital (shares) or

by those shareholders whose cumulative holdings in the company represent no less than 25

percent of the company's capital (shares), where the company's aggregate debt to the said

shareholders accounting cumulatively for 25 percent or more of the capital (shares) and to

those other entities which own no less than 25 percent stakes in the capital of the said

23

shareholder should exceed an amount equal to three times the capital (share capital) of the

company.

The debt-to-equity ratio is established at the level of threefold amount of the share capital of

the company. In other words debt-to-equity ratio amounts to 3:1. The attention should be

paid to the procedure of assessment of the said ratio. The legislator envisaged that also loans

and credits granted by the indirect shareholders should be included into the amount

established for the debt-to-equity ratio assessment. Debt to the following entities is considered

when assessment of the ratio is made:

1. direct shareholders whose holdings amount to at least 25 % of shares (voting rights)

2. indirect shareholders whose holdings in companies granting loan or credit amount to at

least 25 % of shares.

While establishing the aggregate level of debt the provisions of the corporate income tax

statute envisage cumulative treatment of debt to “significant” shareholders of the company,

that is ones whose holding amounts at least to 25 % of voting rights as well as cumulative

treatment of debt to “significant” shareholders of the direct shareholders.

5.3.3 Assessment of the share capital of a company

Not all elements of the share capital should be taken under consideration while assessing the

debt-to-equity ratio. The share capital is understood in accordance with relevant provisions of

the code of commercial companies but for the purposes of assessing of the ratio the corporate

income tax statute envisages a few modifications.

The value of the cooperative members' fund or of the company's capital (share capital) shall

be determined to the exclusion of:

- that proportion of the said fund or capital which has not been effectively contributed or

paid up or

- parts of capital which has been contributed in the form of receivables held by cooperative

members or company shareholders against, respectively, the cooperative or the company

for reasons of loans (credits) made to the cooperative or company and interest thereon, or

- parts of capital in the form of those intangible and legal assets on which no depreciation

write-offs included into costs of earning revenue may be made.

24

The legislator aimed at introducing provisions that would encourage companies to finance

their activity by equity and restrict financing with use of debt capital.

The ratio should be established as for the day of payment of interest.

5.3.4 Final remarks

Transfer pricing and thin capitalisation are treated as different phenomena but of similar

character and roots. This is the reason why within performed controls (usually these are

general controls concerning assessment of income tax burden for a particular tax year) tax

authorities and tax control authorities while analysing shaping of a taxable base pay attention

to issues of transfer pricing, possibility of shifting of income and qualifying expenses as costs

of earning revenue.

Although Polish internal regulations in the field of transfer pricing are compatible with the

OECD Guidelines, not all concepts included in the OECD Guidelines may be applied. For

example Polish regulations do not provide a basis for taxpayers to conclude APA’s.

The new documentation requirements create for the tax authorities possibility of evaluation of

transactions entered into by taxpayers with foreign related parties. On the other hand such

documentation may also serve taxpayers in supporting their transfer pricing positions.

One may observe the growing focus of the tax authorities in Poland on limiting transfer of

profit from Poland that will probably result in the near future in increased number of

inspections and at the end growing number of court cases concerning transfer pricing issues.

25

VI. Measures against “unfair” competition at the international level

1. Double taxation agreement

1.1 General aspects

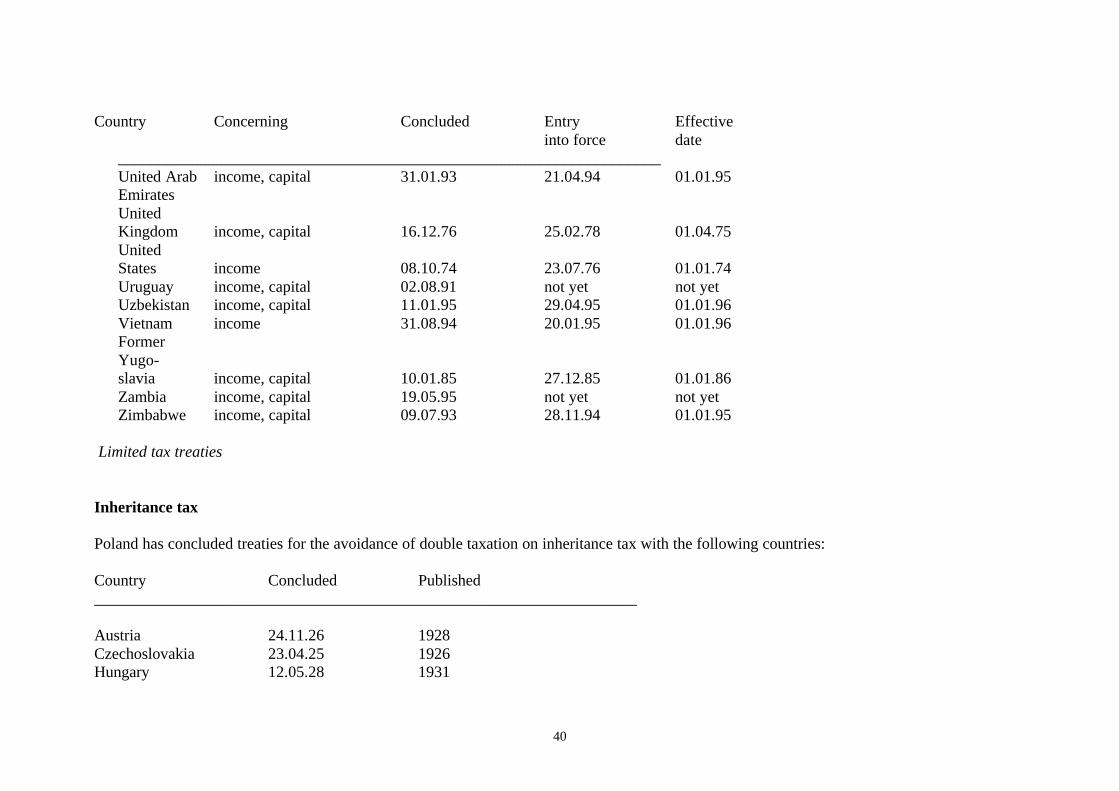

Poland has a comprehensive bilateral tax treaty network for the avoidance of double taxation

on income and capital. Poland has also concluded a number of limited tax treaties, i.e. on

inheritance tax and on income from shipping and air transport (see Tax treaties chart in

Appendix 2).

To date Poland concluded 78 bilateral double taxation agreements. Tax treaties with Algeria,

Armenia, Chile, Egypt, Georgia, Iran, Kirgistan, Lebanon, Macedonia, Mexico, Mongolia,

Nigeria, Uruguay have been signed but await ratification. 57 tax treaties were entered into by

Poland from the beginning of 1990’s.

The provisions of the bilateral tax treaties are based on the OECD Model Convention for the

avoidance of double taxation with respect to taxes on income and capital. There are however

some variations from the Model Convention. It is also interesting to mention that also tax

treaties concluded by Poland before the country became member of the OECD were based on

the wording of the OECD Model Tax Convention on Income and Capital (list of tax treaties

concluded by Poland is included in Appendix 2).

1.2 Avoidance of double taxation

Taking the criterion of applicable method for avoidance of double taxation the tax treaties

concluded by Poland may be divided into two groups. The first group includes treaties

providing for credit method as the only one for example tax treaties with USA, United

Kingdom, Sweden, Russia, Armenia, Denmark, Macedonia, Kazakhstan, Moldova. The

second group consists of treaties providing for exemption method as the main one and credit

method applicable to certain categories of income for example treaties with Germany, France,

the Netherlands, Spain).

26

In the second group as a rule the credit method is applicable exclusively to categories of

passive income that may be taxable in the state of source. One has to notice that in some of

the tax treaties in the described group credit method is applicable also to the other categories

of income for example in tax treaties with France and Germany credit method is applicable to

income classified as Director’s fees and income derived by artistes and sportsmen.

Treaties with countries like Albania, Cyprus, China, Croatia, Estonia, Greece, The

Netherlands, Ireland, Canada, Malta, Mongolia, Mexico, Nigeria, Norway, Portugal, Republic

of South Africa, Romania, Slovenia, Ukraine, Turkey, Italy, United Arab Emirates,

Zimbabwe, Singapore, Slovakia, Vietnam, Lithuania, Japan, Kuwait provide for asymmetric

use of methods for avoidance of double taxation:

• in Poland with regard to dividend, royalties and interest ordinary credit method is

applicable and to the other categories of income exemption with progression method is

applicable,

• in the countries mentioned above regarding all categories of income derived from

sources in Poland ordinary credit method is applicable.

Polish tax treaties include some specific provisions directly influencing application of

methods aiming at avoidance of double taxation. Most important are provisions regarding

credit for underlying tax (e.g. treaties with USA, Australia, Lithuania, Singapore, Armenia)

and tax sparing credit (e.g. treaties with Morocco and Philippine).

It is necessary to mention that the construction of provisions in tax treaties concluded by

Poland providing for methods of avoidance of double taxation differs and for that reason the

description given above is only the general one. Each of the treaties may contain specific

provisions worded in a way differing from the one envisaged in the OECD Model Tax

Convention on Income and Capital.8

1.3 Application of tax treaties

To apply the tax treaty rate for withholding taxes a taxpayer is obliged to present a certificate

of residence issued by the tax authorities of the relevant country. This requirement is

provided for by the provisions that entered into force on the 1st of January 2001. Before that

date the reduced treaty rates were applied directly.

8 see J. Bia³obrzeski “Miê dzynarodowe prawo podatkowe. Komentarz.” Warszawa 2001, J. Banach “Polskieumowy o unikaniu podwójnego opodatkowania” Warszawa 2002, „Taxation and Investment in Central and EastEuropean Countries” IBFD Amsterdam 2002

27

2. OECD

Poland became member of the OECD in 1996 and since then actively participates in the

works of different committees of the organisation.

After the accession the tax system has been gradually changed aiming also at incorporation

into Polish legal system of solutions and experiences of countries having more developed and

stable tax systems.

As far as combating harmful tax competition is at issue Poland generally follows

recommendations elaborated by the OECD. The list of countries and territories applying

harmful tax competition issued by the Ministry of Finance in 2000 was based on the

documents of the OECD (Appendix 3).

3. European Union – Code of Conduct on business taxation

Poland is in course of negotiations aiming at joining the European Union in the near future.

All the drafts of legal acts that are to be enacted have to be examined considering obligations

envisaged in the Europe Agreement9. Article 68 of the Europe Agreement provides for that

Poland shall put efforts to assure conformity of the domestic law with the provisions of

European Union law.

Though the Code of Conduct on business taxation is “soft law” and non-binding political

statement it should be considered by the Polish legislator and in this way influence

development of the tax system. The Code embodies legislative drafting strategy targeting

potentially harmful tax measures on business – laws, regulations, administrative practices

which may be found unfairly competitive. Most important factor taken under consideration is

a potential impact of tax law provisions on location of business activity. Other factors include

tax benefits available only to non-residents or ring-fenced from the domestic market and

national tax system, determination of profit levels for transactions within corporate groups

departing from principles agreed upon by the OECD, tax provisions lacking transparency also

covert relaxation of rules at the administrative level.

9 Europe Agreement on Association between the Republic of Poland and the European Communities and theirMember States of 16 December 1991 entered into force on 1 February 1994 (Dz. U. of 1994 No 11 pos. 38)

28

It is difficult to point out how far changes in Polish tax system are the result of a direct

influence of the Code but the discussion on tax system reform is being held within the

government. The arguments concerning law or policy of the European Union are raised quite

often.

29

Appendix 1

Non-tax deductible costs include, but are not limited to the following:

1) expenditures on:

a) the purchase of land or of a perpetual usufruct interest in land, save for perpetual usufructrent charges,

b) the purchase or production by the taxpayer of fixed assets and intangible and legal assets,including the assets of an acquired business or of organised parts thereof,

c) such improvements (conversion, expansion, reconstruction, adjustment or modernisation)as, pursuant to separate provisions, are recognised as adding to the improved assets'depreciation-base value, --which expenditures, re-rated pursuant to separate provisions andreduced by depreciation write-offs, shall be recognised, subject to item 8a, as costs of earningrevenue for purposes of assessing income from the sale, at whatever time, of the said fixedassets and intangible and legal assets,

2) such expenditures incurred by the tenant or lessee or usufructuary for reasons of renting orlease of things or property rights or for reasons of execution of contracts of a similar nature asare made in settlement of the value, as determined in the contract, of the thing [or right]rented, leased or held for use, where under separate provisions the said thing or right isrecognised as part of the tenant's, lessee's or usufructuary's assets; where the contract doesnot specifically identify that share of the tenant's, lessee's or usufructuary's rent or leasepayments which is to be credited to the settlement of the value of the things or rights, the saidshare shall be set in proportion to the life of the contract for rent or lease,

3) such expenditures as the landlord or lessor has incurred in purchasing or producing thethings and property rights rented or leased or turned over to another under a contract of asimilar nature, where the said thing or right is recognised by force of separate provisions aspart of the tenant's, lessee's or usufructuary's assets; where the thing or right is included in thelandlord's or lessor's assets, subject to item 1, those expenditures shall be recognised as costsof earning revenue,

4) depreciation write-offs made pursuant to separate provisions on a passenger in suchproportion as is attributable to an excess of the car's value over and above an equivalent ofECU10,000 converted into zloty at the National Bank of Poland's average published ECUexchange rate of that day on which the car has been released for use,

5) losses on current assets, fixed assets and intangible and legal assets, in such proportion as iscovered by depreciation write-offs; damages received shall not be taken into account forpurposes of determining the loss,

6) losses arising from the liquidation of partly depreciated fixed assets, where those assets areno longer commercially useful due to the taxpayer's having diverted to another type ofbusiness or modified its hitherto business practices,

7) expenditures on such shares or equity stakes in a company or member interests in a co-operative as have been taken up or purchased for an in-kind contribution; where those

30

interests or shares are sold, the cost of acquisition thereof, given as on the date of taking up orpurchase, shall be understood to cover those outlays on the purchase, production orimprovement of the assets brought into [the company or co-operative] as the in-kindcontribution, re-rated pursuant to separate provisions and adjusted for depreciation write-offsmade prior to the making of contribution, which are recognised as costs of earning revenue,

8) expenditures on:

a) the repayment of loans (credits), save for capitalised interest thereon,

b) the repayment of other liabilities, including those arising under [the taxpayer's] guaranteeand surety commitments,

c) the amortisation of capital involved in the creation (acquisition), enlargement orimprovement of a source of revenue,

9) interest, charged but outstanding or forgiven, on liabilities, including on loans (credits),

10) those interest liabilities, commissions, and exchange rate differentials on loans (credits)which add to the costs of an investment project in the project gestation period,

11) gifts and donations of whatever kind, other than those made among member companies ofa taxable capital group,

12) income tax and certain profit disbursements defined in separate provisions,

13) execution costs relating to the satisfaction of outstanding obligations,

14) fines and other pecuniary penalties adjudicated in criminal proceedings, in proceedings oncharges of an offence against the Treasury and in administrative proceedings, likewise intereston the said fines and pecuniary penalties,

15) fines, charges, damages and interest on the same, where the fine, charge or damage hasbeen imposed for:

a) non-compliance with the environmental protection provisions;

b) non-compliance with instructions issued by inspection and supervision authorities ofcompetent jurisdiction regarding the bringing up of unsatisfactory work safety and hygieneconditions to required standards;

16) amounts receivable written off as incapable of being enforced due to limitation,

17) penalty interest on delayed settlement of budget dues and those other dues which fallunder the Tax Law Act,

18) contractual penalties and damages for defects in products supplied and in works andservices provided and for delayed delivery of defect-free products or delayed removal ofdefects in the products supplied or works and services provided,

31

19) publicity and advertising costs in excess of 0.25 percent of the [taxpayer's] revenue, savewhere the advertising campaign is conducted in mass media or in another public manner,

20) member contributions to those organisations the membership of which is not mandatoryupon the taxpayer, except for:

21) expenditures incurred for benefit of members of supervisory boards, audit commissions orcorporate decision-making bodies, save for remunerations paid [to those members] for thefunctions performed,

22) national insurance contributions, Labour Fund contributions and such contributions toother targeted funds created pursuant to separate provisions as are due on awards andbonuses paid in cash or in securities out of after-income-tax income,

23) forgiven loans, where the forgiving of those is not connected with a bank-organisedarrangement with creditors proceeding as defined in the provisions on the restructuring ofenterprise and bank finances or with an arrangement with creditors proceeding as defined inthe arrangement with creditors provisions,

24) goods and services tax, provided that the following shall be recognised as costs of earningrevenue:

a) tax assessed:

-- where the taxpayer is exempt from goods and services tax or where the taxpayer haspurchased [certain taxable] goods and services with the object of producing or re-selling suchgoods or providing such services as are exempt from goods and services tax,

-- in that proportion against which, under the goods and services tax provisions and exciseprovisions, the taxpayer may not legitimately claim a reduction of its goods and services taxliability or a goods and services tax differential refund, where the goods and services taxassessed does not add to the value of a fixed asset,

b) tax due on:

-- imported services other than transport services,

-- goods and services given or provided by the taxpayer for publicity and advertisingpurposes,

25) excise tax on above-standard wastage or shortage of goods due to culpable actions oromissions,

26) fixed asset depreciation write-offs made pursuant to separate provisions in respect of thatproportion of the fixed asset value which corresponds to outlays on the purchase or

32

production thereof by the taxpayer, [if] deducted from the income tax base or refunded to thetaxpayer in any other manner,

27) a proportion of interest due on loans (credits) made to a company by a shareholder whoseequity stake (shares) in the company represent no less than 25 percent of the company'scapital (shares) or by those shareholders whose cumulative holdings in the company representno less than 25 percent of the company's capital (shares), where the company's aggregate debtto the said shareholders accounting cumulatively for 25 percent or more of the capital (shares)and to those other entities which own no less than 25 percent stakes in the capital of the saidshareholder should exceed an amount equal to three times the capital (share capital) of thecompany--the said proportion corresponding to an excess of the loan (credit) over the saiddebt as on the interest due date; the aforesaid shall apply equally to the co-operative, membersof the co-operative and the members' fund of the co-operative (thin capitalization),

28) a proportion of interest on loans (credits) made by one company to another, where in theboth companies the same shareholder holds no less than 25 percent capital (shares) and wherethe value of the borrower company's [aggregate] debt to those shareholders who owncumulatively 25 percent or more of the capital (shares), to those other entities which own noless than 25 percent stakes in the said shareholders and to the lender company should exceedan amount equal to three times the capital (share capital) of the [borrower] company--the saidproportion corresponding to an excess of the loan (credit) over the said debt as on the interestdue date; the aforesaid shall apply equally to the co-operative, members of the co-operativeand the members' fund of the co-operative (thin capitalization).

33

Appendix 2

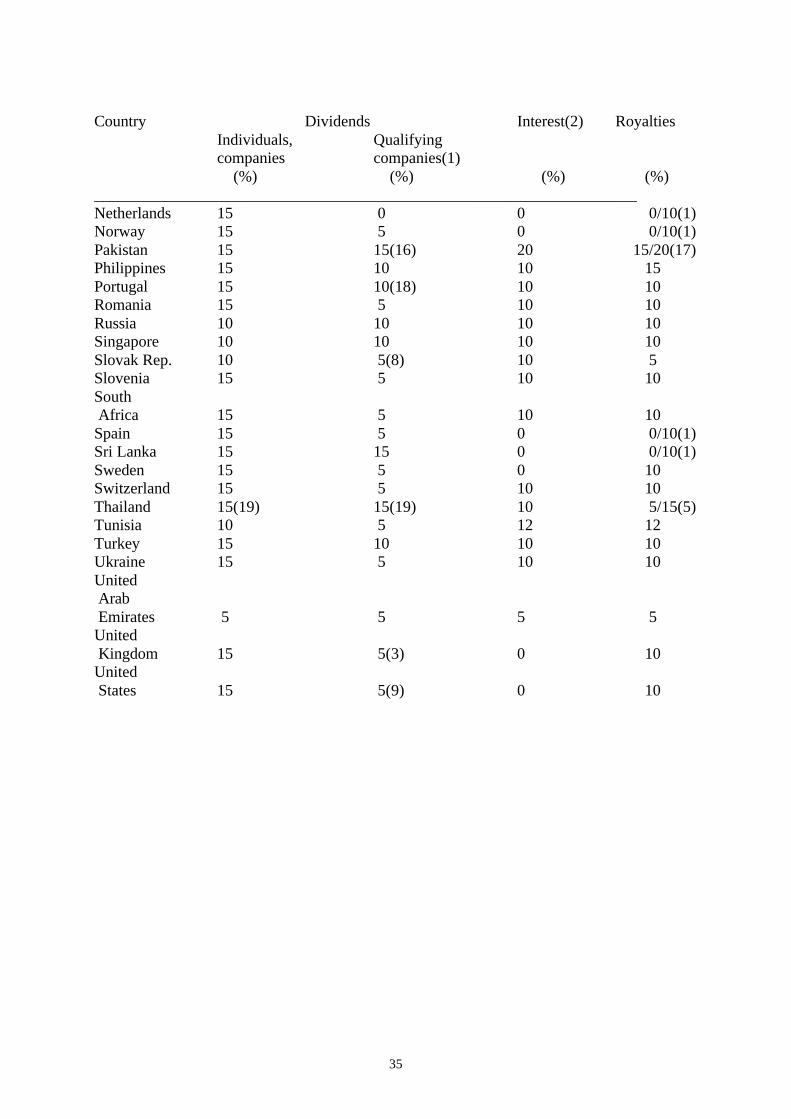

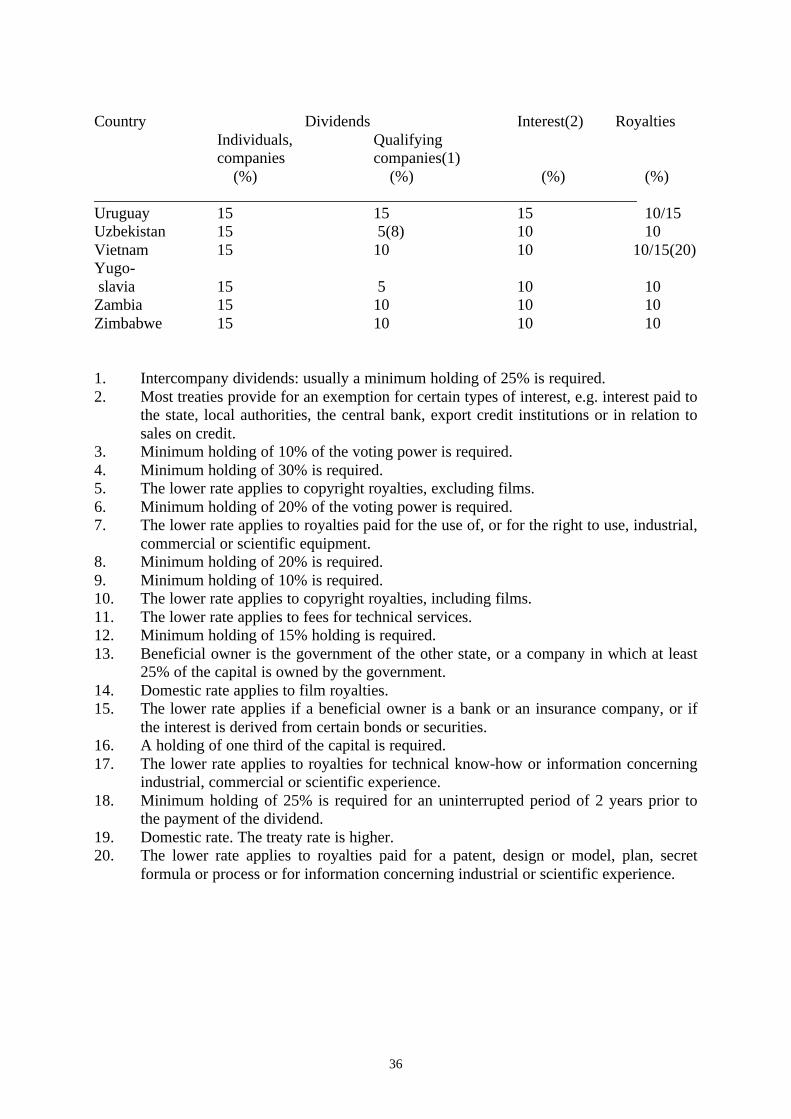

Treaty chart: withholding taxes

The following chart contains the withholding tax rates that are applicable to paymentsmade by Polish companies to non-residents under the ratified tax treaties. The lower of thedomestic and treaty rate is given.

Country Dividends Interest(2) RoyaltiesIndividuals, Qualifyingcompanies companies(1) (%) (%) (%) (%)

____________________________________________________________________

Albania 10 5 10 5Armenia 10 10 5 10Australia 15 15 10 10Austria 10 10 0 0Bangladesh 15 10(3) 10 10Belarus 15 10(4) 0 0Belgium 10 10 10 10Bulgaria 10 10 10 5Canada 15 15 15 0/10(5)Chile 15 5(6) 15 5/15(7)China (People's Rep.) 10 10 10 7/10(7)Croatia 15 5 10 10Cyprus 10 10 10 5Czech Rep. 10 5(8) 10 5Denmark 15 5 0 10Egypt 12 12 12 12Estonia 15 5 10 10

34

Country Dividends Interest(2) RoyaltiesIndividuals, Qualifyingcompanies companies(1) (%) (%) (%) (%)

____________________________________________________________________Finland 15 5 0 10France 15 5(9) 0 0/10(1)Germany 15 5 0 0Greece 15 15 10 10Hungary 10 10 10 10Iceland 15 5 0 10India 15 15 15 20Indonesia 15 10(8) 10 15Ireland 15 0 10 0/10(1)Israel 10 5(12) 5 5/10(7)Italy 10 10 10 10Japan 10 10 10 0/10(1)Jordan 10 10 10 10Kazakhstan 15 10(8) 10 10Korea (Rep.) 10 5(9) 10 10Kuwait 5 0(13) 0/5 15Latvia 15 5 10 10Lebanon 5 5 5 5Lithuania 15 5 10 10Luxembourg 15 5 10 10Macedonia 15 5 10 10Malaysia 0 0 15 15/20(14)Malta 15 5(8) 10 10Mexico 15 5 10/15(15) 10Moldova 15 5 10 10Morocco 15 7 10 10

35

Country Dividends Interest(2) RoyaltiesIndividuals, Qualifyingcompanies companies(1) (%) (%) (%) (%)

____________________________________________________________________Netherlands 15 0 0 0/10(1)Norway 15 5 0 0/10(1)Pakistan 15 15(16) 20 15/20(17)Philippines 15 10 10 15Portugal 15 10(18) 10 10Romania 15 5 10 10Russia 10 10 10 10Singapore 10 10 10 10Slovak Rep. 10 5(8) 10 5Slovenia 15 5 10 10South Africa 15 5 10 10Spain 15 5 0 0/10(1)Sri Lanka 15 15 0 0/10(1)Sweden 15 5 0 10Switzerland 15 5 10 10Thailand 15(19) 15(19) 10 5/15(5)Tunisia 10 5 12 12Turkey 15 10 10 10Ukraine 15 5 10 10United Arab Emirates 5 5 5 5United Kingdom 15 5(3) 0 10United States 15 5(9) 0 10

36

Country Dividends Interest(2) RoyaltiesIndividuals, Qualifyingcompanies companies(1) (%) (%) (%) (%)

____________________________________________________________________Uruguay 15 15 15 10/15Uzbekistan 15 5(8) 10 10Vietnam 15 10 10 10/15(20)Yugo- slavia 15 5 10 10Zambia 15 10 10 10Zimbabwe 15 10 10 10

1. Intercompany dividends: usually a minimum holding of 25% is required.2. Most treaties provide for an exemption for certain types of interest, e.g. interest paid to

the state, local authorities, the central bank, export credit institutions or in relation tosales on credit.

3. Minimum holding of 10% of the voting power is required.4. Minimum holding of 30% is required.5. The lower rate applies to copyright royalties, excluding films.6. Minimum holding of 20% of the voting power is required.7. The lower rate applies to royalties paid for the use of, or for the right to use, industrial,

commercial or scientific equipment.8. Minimum holding of 20% is required.9. Minimum holding of 10% is required.10. The lower rate applies to copyright royalties, including films.11. The lower rate applies to fees for technical services.12. Minimum holding of 15% holding is required.13. Beneficial owner is the government of the other state, or a company in which at least

25% of the capital is owned by the government.14. Domestic rate applies to film royalties.15. The lower rate applies if a beneficial owner is a bank or an insurance company, or if

the interest is derived from certain bonds or securities.16. A holding of one third of the capital is required.17. The lower rate applies to royalties for technical know-how or information concerning

industrial, commercial or scientific experience.18. Minimum holding of 25% is required for an uninterrupted period of 2 years prior to

the payment of the dividend.19. Domestic rate. The treaty rate is higher.20. The lower rate applies to royalties paid for a patent, design or model, plan, secret

formula or process or for information concerning industrial or scientific experience.

37

List of tax treaties on income and capital

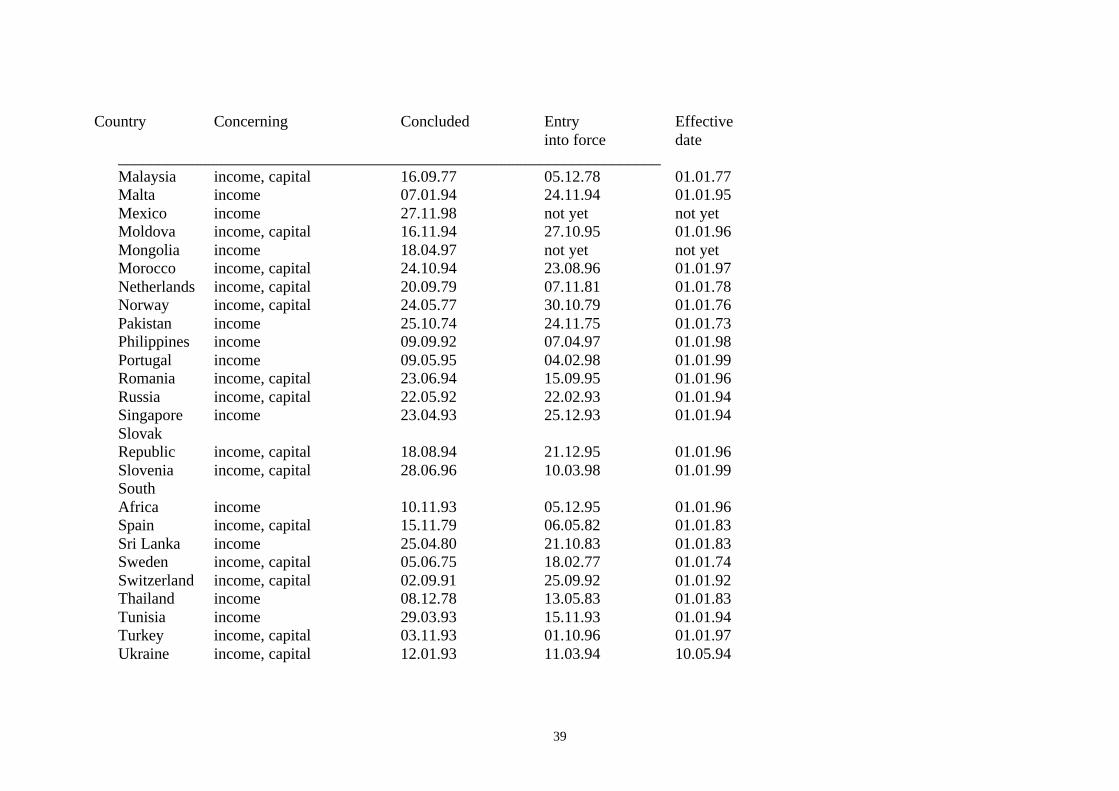

Poland has concluded conventions for the avoidance of double taxation on income and capital with the following countries:

Country Concerning Concluded Entry Effectiveinto force date

____________________________________________________________________

Albania income, capital 05.03.93 27.06.94 01.01.95Armenia income 14.07.99 not yet not yetAustralia income 07.05.91 04.03.92 01.01.93Austria income, capital 02.10.74 22.07.75 01.01.74Azerbaijan income 26.08.97 not yet not yetBangladesh income 08.07.97 28.01.99 01.01.00Belarus income, capital 18.11.92 30.07.93 01.01.94Belgium income, capital 14.09.76 21.09.78 01.01.79Bulgaria income, capital 11.04.94 10.05.95 01.01.96Canada income, capital 04.05.87 30.11.89 01.01.89Chile income 10.03.00 not yet not yetChina(People'sRep.) income 07.06.88 07.01.89 01.01.90Croatia income, capital 19.10.94 11.02.96 01.01.97Cyprus income, capital 04.06.92 07.07.93 01.01.92CzechRepublic income, capital 24.06.93 20.12.93 01.01.94Denmark income, capital 06.04.76 20.11.76 01.01.76Protocol income, capital 17.05.94 13.01.95 01.01.92

(Denmark)01.01.96(Poland)

38

Country Concerning Concluded Entry Effectiveinto force date

____________________________________________________________________Egypt income, capital 24.06.96 not yet not yetEstonia income, capital 09.05.94 09.12.94 01.01.95Finland income, capital 26.10.77 30.03.79 01.01.80Protocol income, capital 28.04.94 21.01.95 01.01.96France income, capital 20.06.75 12.09.76 01.01.74Germany income, capital 18.12.72 14.09.75 01.01.72Protocol income, capital 24.10.79 20.12.81 01.01.77Greece income, capital 20.11.87 28.09.91 01.01.91Hungary income, capital 23.09.92 10.09.95 01.01.96Iceland income, capital 19.06.98 20.06.99 01.01.00India income 21.06.89 26.10.89 01.01.90Indonesia income 06.10.92 25.08.93 01.01.94Iran - 04.10.98 not yet not yetIreland income 13.11.95 22.12.95 01.01.96Israel income 22.05.91 30.12.91 01.01.92Italy income 21.06.85 26.09.89 01.01.84Japan income, capital 20.02.80 23.12.82 01.01.82Jordan income 04.10.97 22.04.99 01.01.00Kazakhstan income, capital 21.09.94 13.05.95 01.01.96Korea(Rep.) income 21.06.91 21.02.92 01.01.91Kuwait income, capital 16.11.96 25.04.00 01.01.96Kyrgyzstan income 19.11.98 not yet not yetLatvia income, capital 17.11.93 30.11.94 01.01.95Lebanon income 26.07.99 not yet not yetLithuania income, capital 20.01.94 19.07.94 01.01.95Luxembourg income, capital 14.06.95 31.07.96 01.01.97Macedonia income, capital 28.11.96 not yet not yet

39

Country Concerning Concluded Entry Effectiveinto force date