blair final ppt

TRANSCRIPT

Miami University Oxford, OH

Matt Murtha | Kasey Marenco | Alex Puthumana | Jack Bennett

Skipper’s Sporting GoodsValuation and Suggestion

Executive Summary

Company & Industry Overview

Potential Buyers

Valuation

Recommendation

3

5

10

14

22

Appendix 24

2

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation 3

Executive Summary

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation

Project Overview Football Field Valuation

IRR Analysis

4

Executive Summary

Asked to value Skipper’s Sporting Goods within the sports manufacturing and wholesale industry

Identify prospective investor opportunities and provide distinguishable factors that set them apart

Analysis

Skipper’s is a trusted, top-ranked firm that has positioned itself at the forefront of a growing industry

Its proven innovation and consistent growth would add value to both strategic and financial buyers

Talented management team with an expressed desire to grow with the company provides stability and experience

Devotion to superior quality solidifies strong brand reputation amongst retail partners and customers, making Skipper’s a “must-have brand”

Dependency on upstream suppliers could possibly cut into future operations margins

Costs increased 5% in Asia and 1% in the US during the last few years

Sponsor

Equity

2015 265% (416) 1,521

2016 109% (416) 0 1,815

2017 70% (416) 0 0 2,040

2018 54% (416) 0 0 0 2,316

2019 45% (416) 0 0 0 0 2,667

IRRExit Year

Sources: Case Materials, Team

Models

Executive SummaryCompany &

Industry OverviewPotential Buyers Valuation Recommendation 5

Company & Industry Overview

Executive SummaryCompany &

Industry OverviewPotential Buyers Valuation Recommendation

Key Selling Points Competitive Advantages

Growth ProfileYOY LTM % Growth

6

Skipper’s Sporting Goods Profile

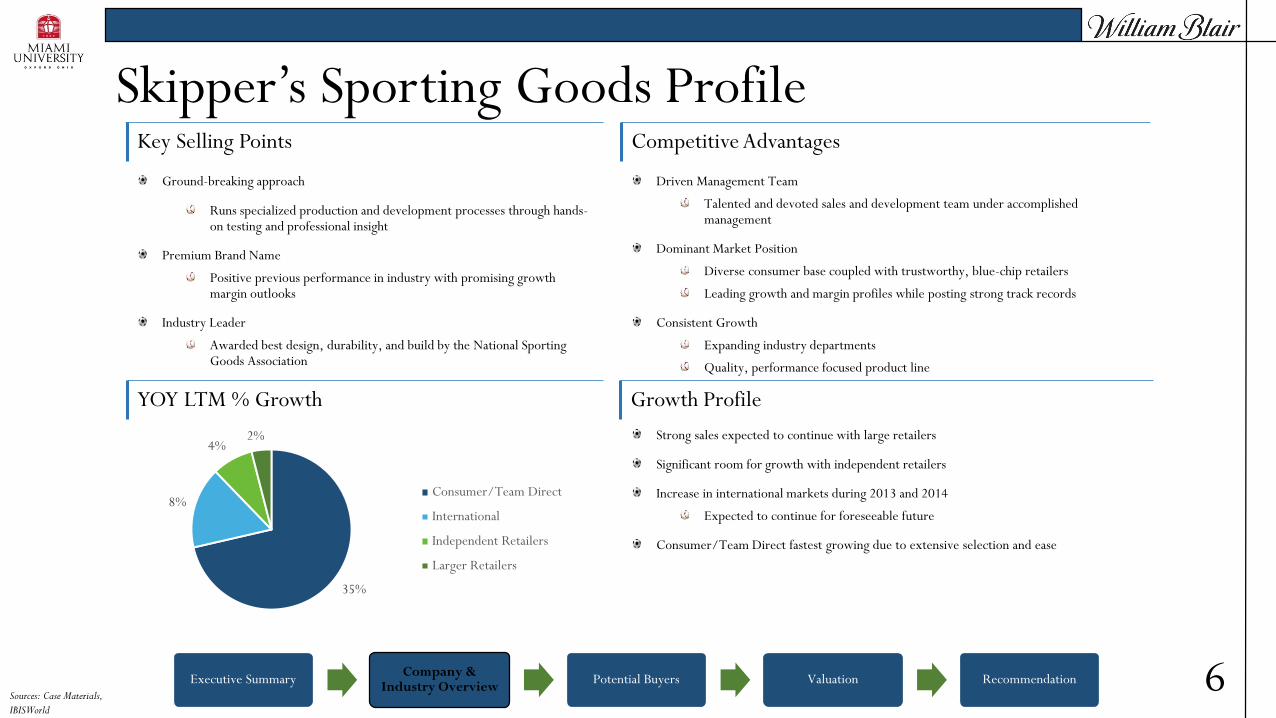

Ground-breaking approach

Runs specialized production and development processes through hands-on testing and professional insight

Premium Brand Name

Positive previous performance in industry with promising growth margin outlooks

Industry Leader

Awarded best design, durability, and build by the National Sporting Goods Association

Sources: Case Materials,

IBISWorld

Driven Management Team

Talented and devoted sales and development team under accomplished management

Dominant Market Position

Diverse consumer base coupled with trustworthy, blue-chip retailers

Leading growth and margin profiles while posting strong track records

Consistent Growth

Expanding industry departments

Quality, performance focused product line

Strong sales expected to continue with large retailers

Significant room for growth with independent retailers

Increase in international markets during 2013 and 2014

Expected to continue for foreseeable future

Consumer/Team Direct fastest growing due to extensive selection and ease

35%

8%

4%2%

Consumer/Team Direct

International

Independent Retailers

Larger Retailers

Executive SummaryCompany &

Industry OverviewPotential Buyers Valuation Recommendation

Segment Offerings and Operational Overview Revenue by Segment

Segment Growth

7

Segments Analysis

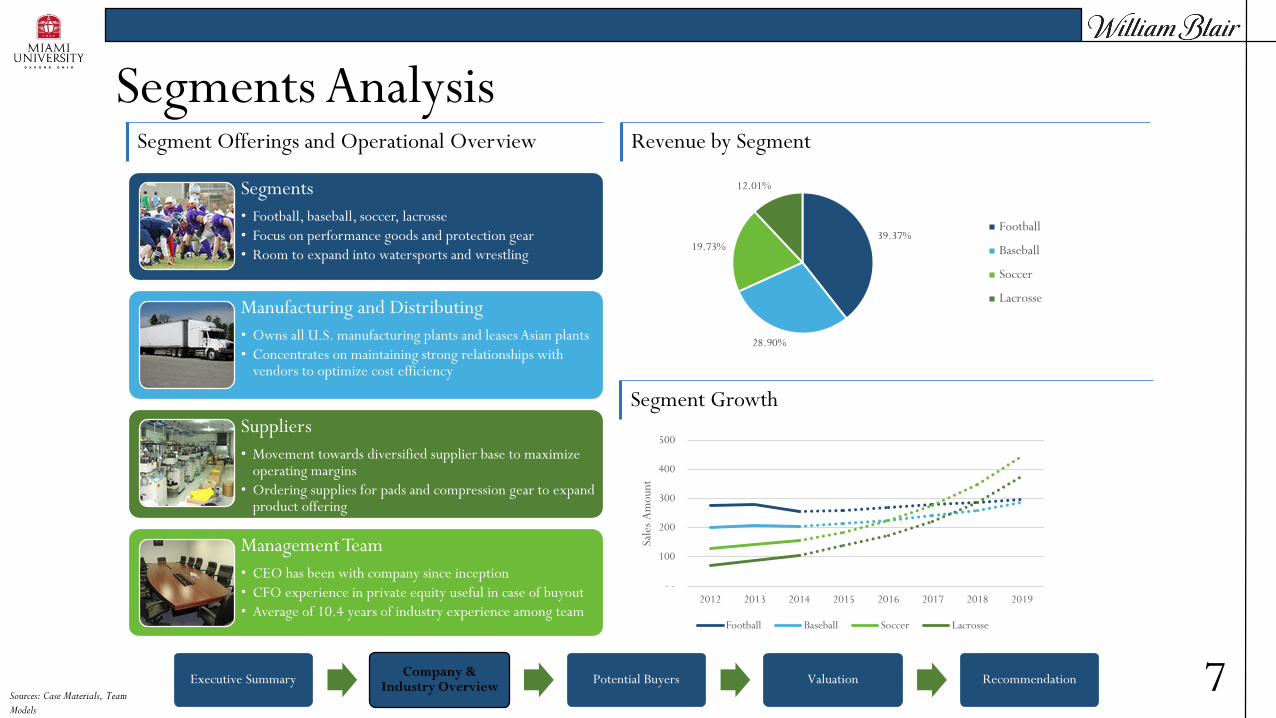

Segments

• Football, baseball, soccer, lacrosse

• Focus on performance goods and protection gear

• Room to expand into watersports and wrestling

Manufacturing and Distributing

• Owns all U.S. manufacturing plants and leases Asian plants

• Concentrates on maintaining strong relationships with vendors to optimize cost efficiency

Suppliers

• Movement towards diversified supplier base to maximize operating margins

• Ordering supplies for pads and compression gear to expand product offering

Management Team

• CEO has been with company since inception

• CFO experience in private equity useful in case of buyout

• Average of 10.4 years of industry experience among team

Sources: Case Materials, Team

Models

39.37%

28.90%

19.73%

12.01%

Football

Baseball

Soccer

Lacrosse

- -

100

200

300

400

500

2012 2013 2014 2015 2016 2017 2018 2019

Sale

s A

mou

nt

Football Baseball Soccer Lacrosse

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation

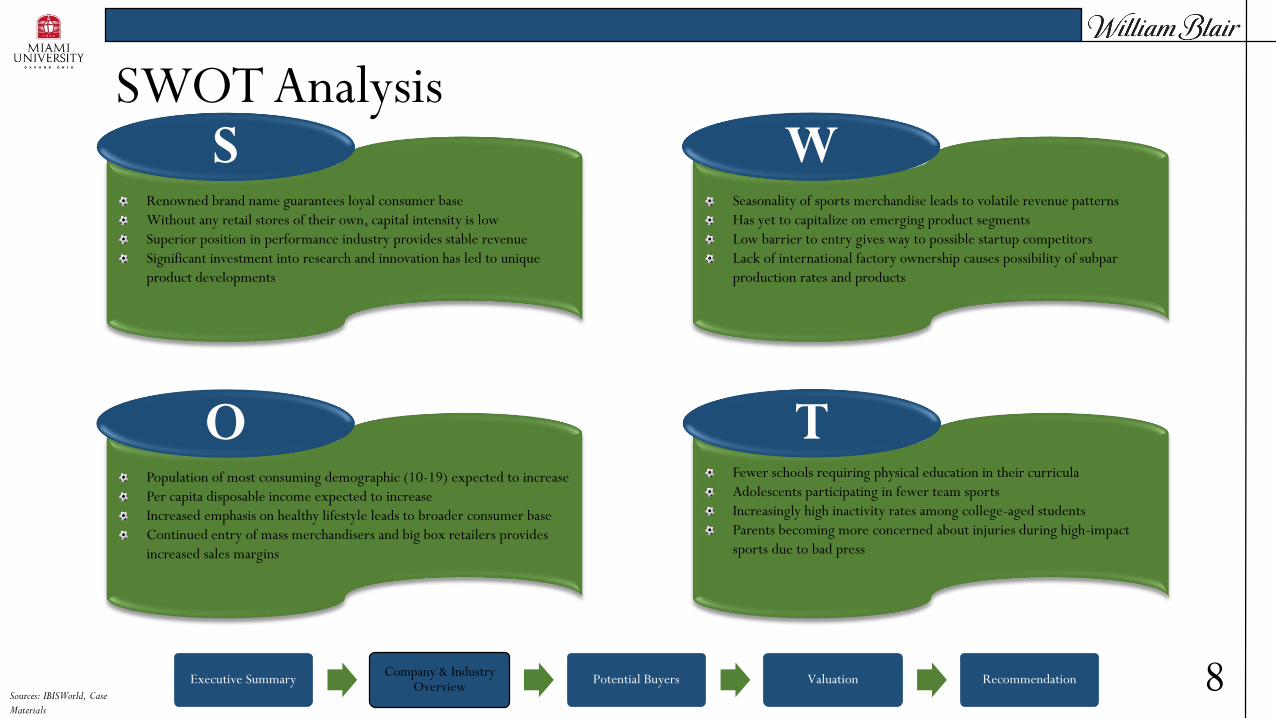

Seasonality of sports merchandise leads to volatile revenue patterns

Has yet to capitalize on emerging product segments

Low barrier to entry gives way to possible startup competitors

Lack of international factory ownership causes possibility of subpar

production rates and products

Fewer schools requiring physical education in their curricula

Adolescents participating in fewer team sports

Increasingly high inactivity rates among college-aged students

Parents becoming more concerned about injuries during high-impact

sports due to bad press

Population of most consuming demographic (10-19) expected to increase

Per capita disposable income expected to increase

Increased emphasis on healthy lifestyle leads to broader consumer base

Continued entry of mass merchandisers and big box retailers provides

increased sales margins

Renowned brand name guarantees loyal consumer base

Without any retail stores of their own, capital intensity is low

Superior position in performance industry provides stable revenue

Significant investment into research and innovation has led to unique

product developments

S W

TO

SWOT Analysis

8Sources: IBISWorld, Case

Materials

Executive SummaryCompany &

Industry OverviewPotential Buyers Valuation Recommendation

Industry Trends Sales by Channel

Industry Performance

9

Sports Manufacturing and Wholesale

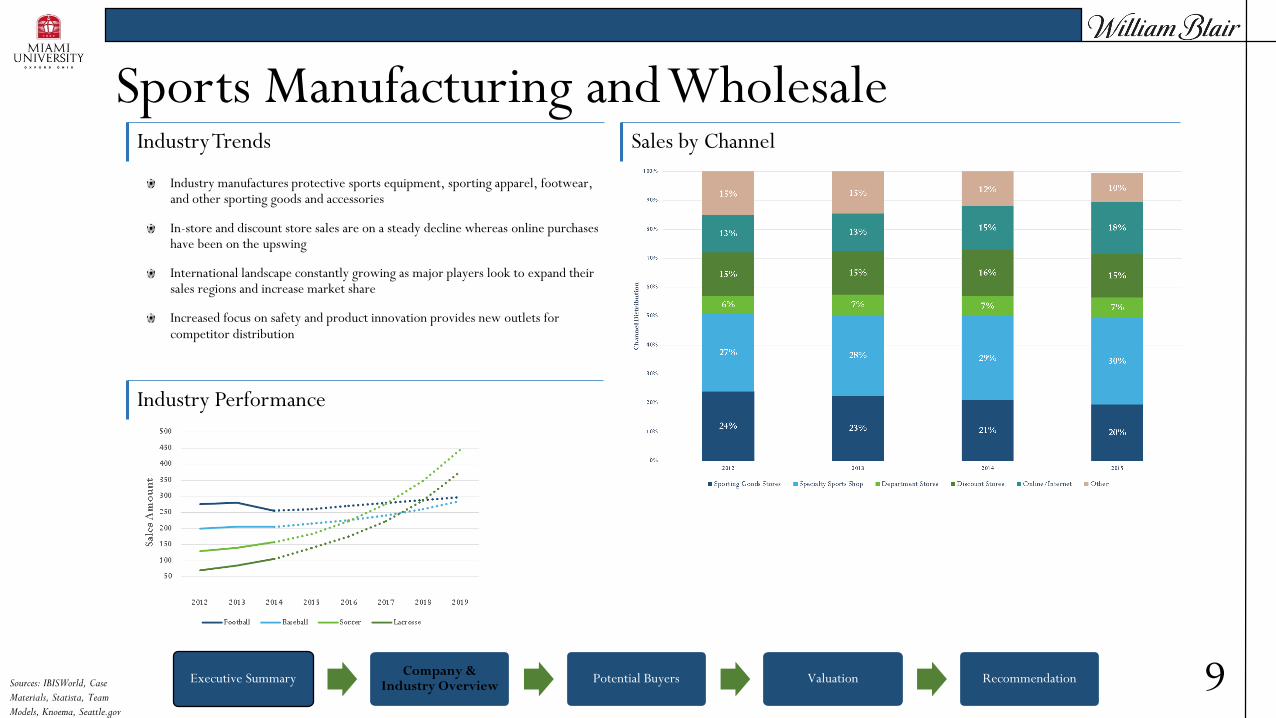

Industry manufactures protective sports equipment, sporting apparel, footwear, and other sporting goods and accessories

In-store and discount store sales are on a steady decline whereas online purchases have been on the upswing

International landscape constantly growing as major players look to expand their sales regions and increase market share

Increased focus on safety and product innovation provides new outlets for competitor distribution

Sources: IBISWorld, Case

Materials, Statista, Team

Models, Knoema, Seattle.gov

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation 10

Potential Buyers

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation

PE Overview PE Fundraising & Financing

0

0.2

0.4

0.6

0.8

1

1.2

0

0.2

0.4

0.6

0.8

1

1.2

Capital Raised (Bil.) Avg. Equity Financing

PE Dry Powder

$0

$200

$400

$600

$800

$1,000

$1,200

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Dry Powder (Bil.)

PE Exits

$0

$10

$20

$30

$40

$50

$60

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Exit Amount (Bil.)

11

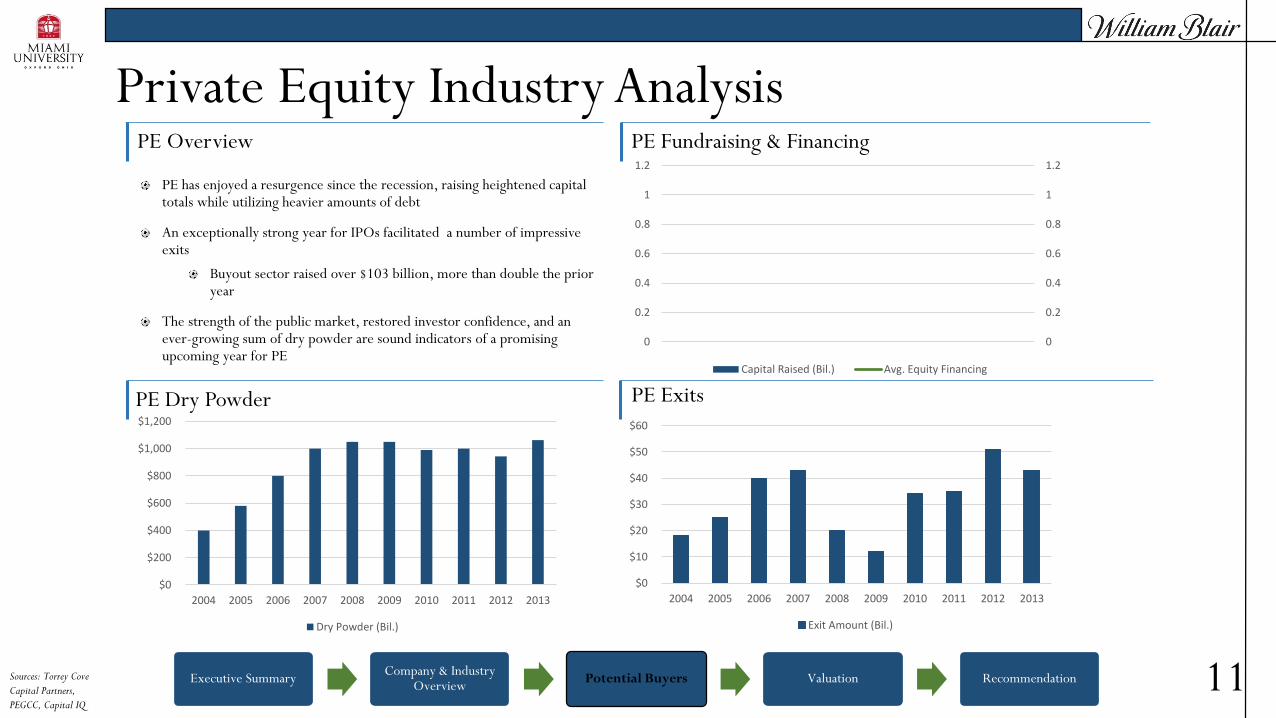

Private Equity Industry Analysis

PE has enjoyed a resurgence since the recession, raising heightened capital totals while utilizing heavier amounts of debt

An exceptionally strong year for IPOs facilitated a number of impressive exits

Buyout sector raised over $103 billion, more than double the prior year

The strength of the public market, restored investor confidence, and an ever-growing sum of dry powder are sound indicators of a promising upcoming year for PE

Sources: Torrey Cove

Capital Partners,

PEGCC, Capital IQ

Industry Overview Company Profile Potential Buyers Valuation Recommendation 12

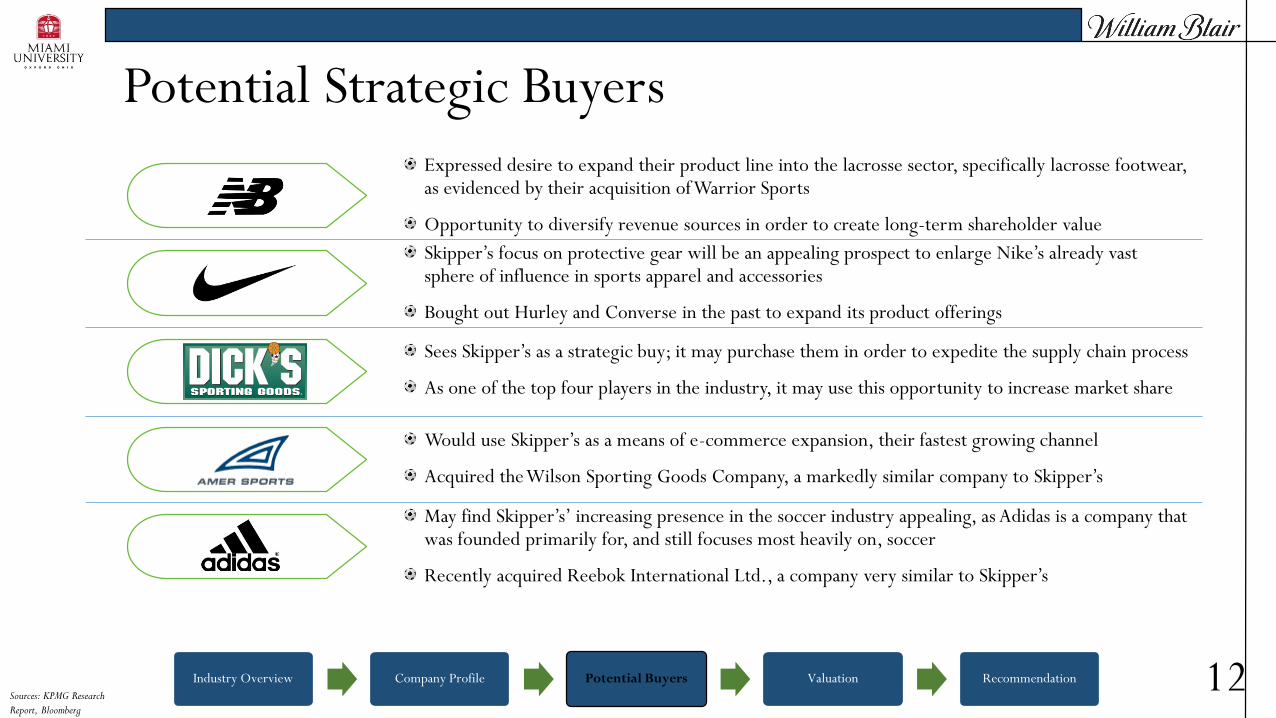

Potential Strategic Buyers

Expressed desire to expand their product line into the lacrosse sector, specifically lacrosse footwear, as evidenced by their acquisition of Warrior Sports

Opportunity to diversify revenue sources in order to create long-term shareholder value

Skipper’s focus on protective gear will be an appealing prospect to enlarge Nike’s already vast sphere of influence in sports apparel and accessories

Bought out Hurley and Converse in the past to expand its product offerings

Sees Skipper’s as a strategic buy; it may purchase them in order to expedite the supply chain process

As one of the top four players in the industry, it may use this opportunity to increase market share

Would use Skipper’s as a means of e-commerce expansion, their fastest growing channel

Acquired the Wilson Sporting Goods Company, a markedly similar company to Skipper’s

May find Skipper’s’ increasing presence in the soccer industry appealing, as Adidas is a company that was founded primarily for, and still focuses most heavily on, soccer

Recently acquired Reebok International Ltd., a company very similar to Skipper’s

Sources: KPMG Research

Report, Bloomberg

Industry Overview Company Profile Potential Buyers Valuation Recommendation 13

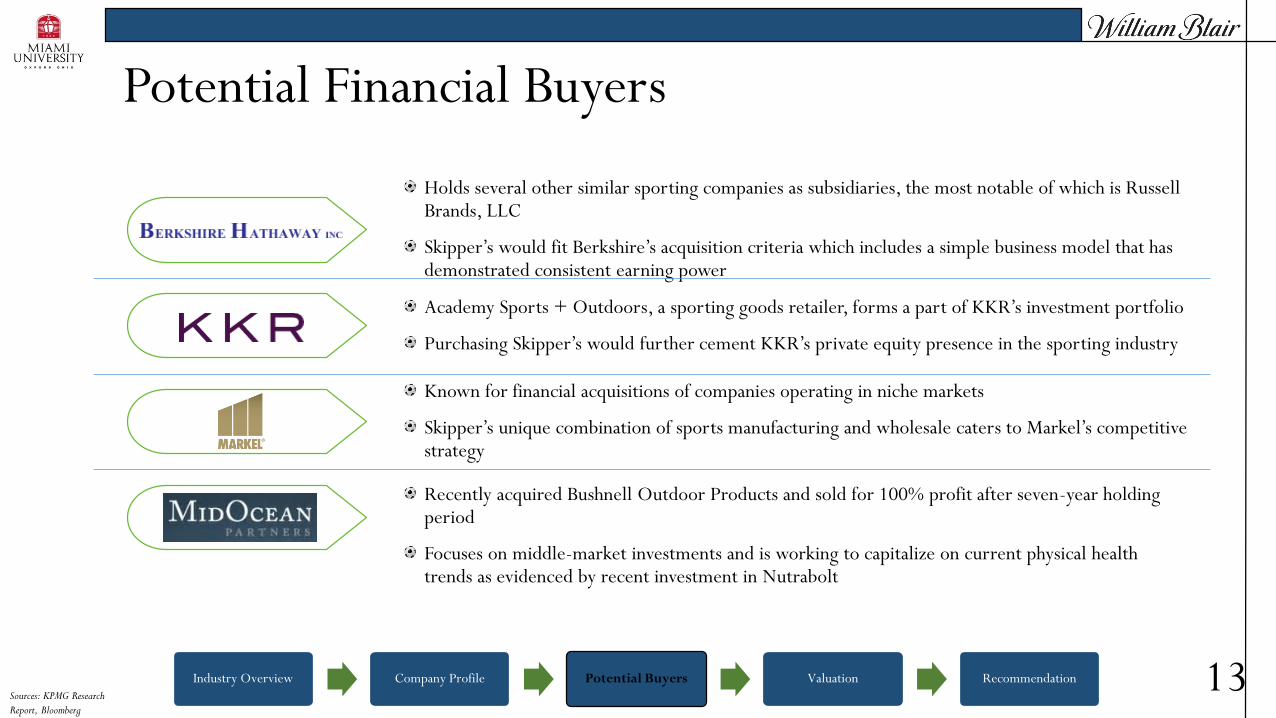

Holds several other similar sporting companies as subsidiaries, the most notable of which is Russell Brands, LLC

Skipper’s would fit Berkshire’s acquisition criteria which includes a simple business model that has demonstrated consistent earning power

Academy Sports + Outdoors, a sporting goods retailer, forms a part of KKR’s investment portfolio

Purchasing Skipper’s would further cement KKR’s private equity presence in the sporting industry

Known for financial acquisitions of companies operating in niche markets

Skipper’s unique combination of sports manufacturing and wholesale caters to Markel’s competitive strategy

Recently acquired Bushnell Outdoor Products and sold for 100% profit after seven-year holding period

Focuses on middle-market investments and is working to capitalize on current physical health trends as evidenced by recent investment in Nutrabolt

Potential Financial Buyers

Sources: KPMG Research

Report, Bloomberg

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation 14

Valuation

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation

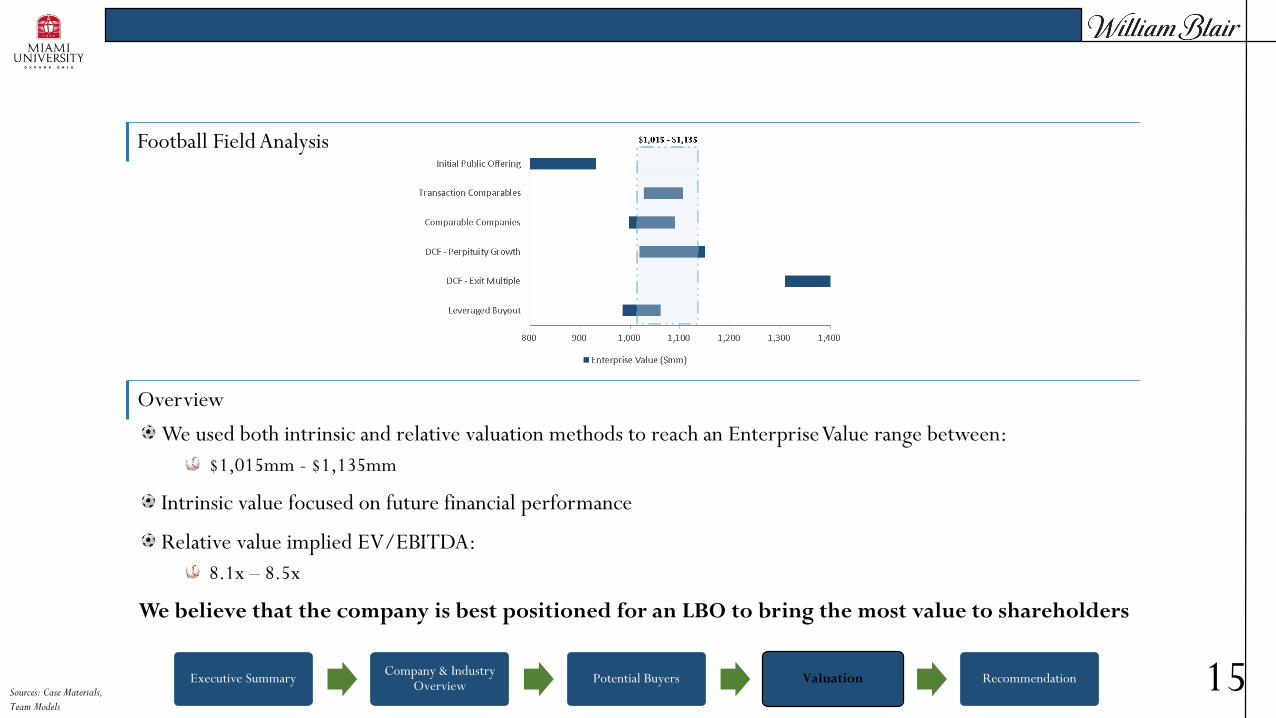

Football Field Analysis

Overview

15

We used both intrinsic and relative valuation methods to reach an Enterprise Value range between:

$1,015mm - $1,135mm

Intrinsic value focused on future financial performance

Relative value implied EV/EBITDA:

8.1x – 8.5x

We believe that the company is best positioned for an LBO to bring the most value to shareholders

Sources: Case Materials,

Team Models

Big Dogs

Consumer Direct

Niche Providers

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation

Industry Analysis Industry Consolidation

Competitive Dispersion

0

0.2

0.4

0.6

0.8

1

1.2

0

0.2

0.4

0.6

0.8

1

1.2

Gro

wth

Re

tail

Lo

cat

ion

s

Year

Stores Jobs

16

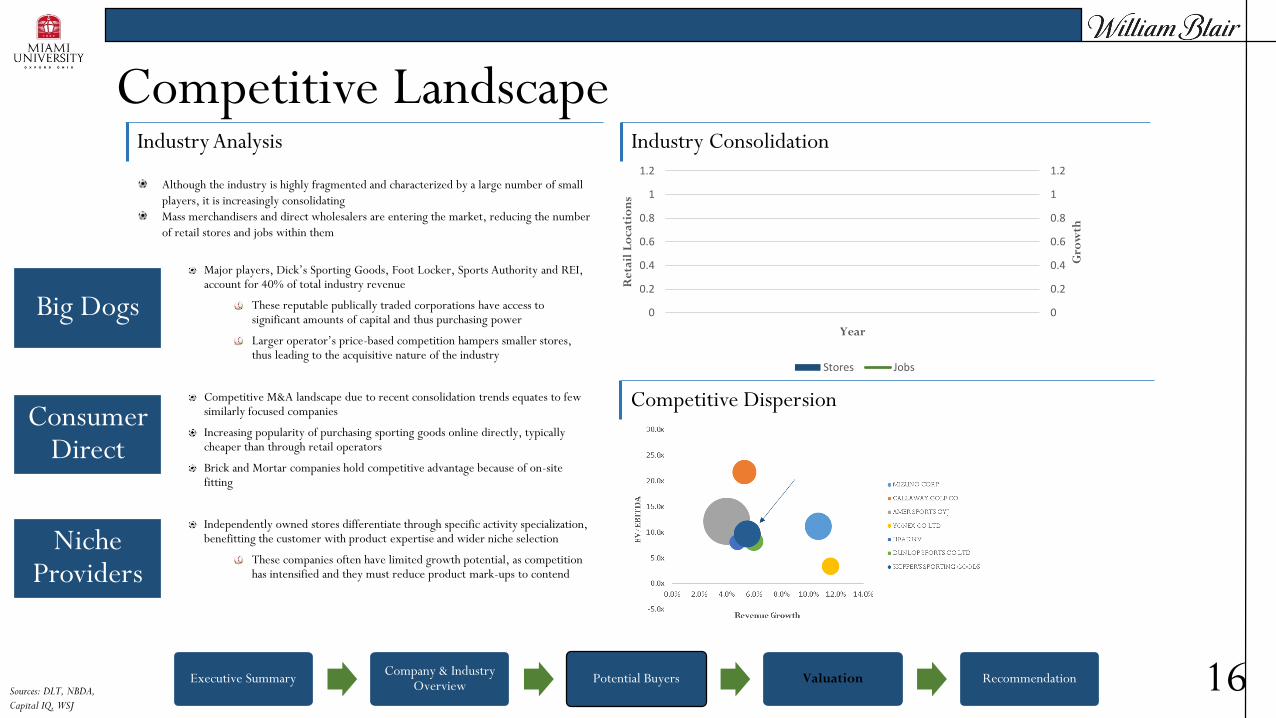

Competitive Landscape

Although the industry is highly fragmented and characterized by a large number of small

players, it is increasingly consolidating

Mass merchandisers and direct wholesalers are entering the market, reducing the number

of retail stores and jobs within them

Major players, Dick’s Sporting Goods, Foot Locker, Sports Authority and REI, account for 40% of total industry revenue

These reputable publically traded corporations have access to significant amounts of capital and thus purchasing power

Larger operator’s price-based competition hampers smaller stores, thus leading to the acquisitive nature of the industry

Competitive M&A landscape due to recent consolidation trends equates to few similarly focused companies

Increasing popularity of purchasing sporting goods online directly, typically cheaper than through retail operators

Brick and Mortar companies hold competitive advantage because of on-site fitting

Independently owned stores differentiate through specific activity specialization, benefitting the customer with product expertise and wider niche selection

These companies often have limited growth potential, as competition has intensified and they must reduce product mark-ups to contend

Sources: DLT, NBDA,

Capital IQ, WSJ

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation

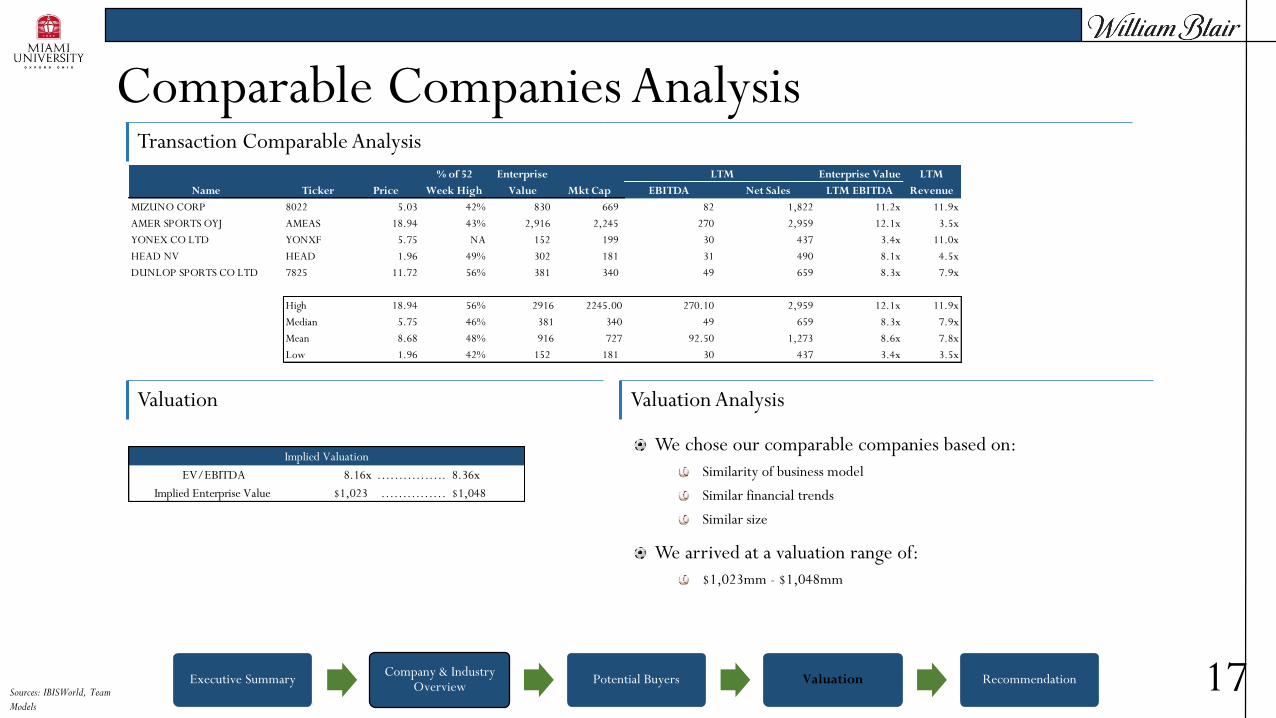

Transaction Comparable Analysis

Valuation AnalysisValuation

17

Comparable Companies Analysis

We chose our comparable companies based on:

Similarity of business model

Similar financial trends

Similar size

We arrived at a valuation range of:

$1,023mm - $1,048mm

Enterprise Value

EBITDA Net Sales LTM EBITDA

MIZUNO CORP 8022 5.03 42% 830 669 82 1,822 11.2x 11.9x

AMER SPORTS OYJ AMEAS 18.94 43% 2,916 2,245 270 2,959 12.1x 3.5x

YONEX CO LTD YONXF 5.75 NA 152 199 30 437 3.4x 11.0x

HEAD NV HEAD 1.96 49% 302 181 31 490 8.1x 4.5x

DUNLOP SPORTS CO LTD 7825 11.72 56% 381 340 49 659 8.3x 7.9x

High 18.94 56% 2916 2245.00 270.10 2,959 12.1x 11.9x

Median 5.75 46% 381 340 49 659 8.3x 7.9x

Mean 8.68 48% 916 727 92.50 1,273 8.6x 7.8x

Low 1.96 42% 152 181 30 437 3.4x 3.5x

LTM LTM

Revenue Name Ticker Price

% of 52

Week High

Enterprise

Value Mkt Cap

EV/EBITDA 8.16x ……………. 8.36x

Implied Enterprise Value $1,023 …………… $1,048

Implied Valuation

Sources: IBISWorld, Team

Models

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation

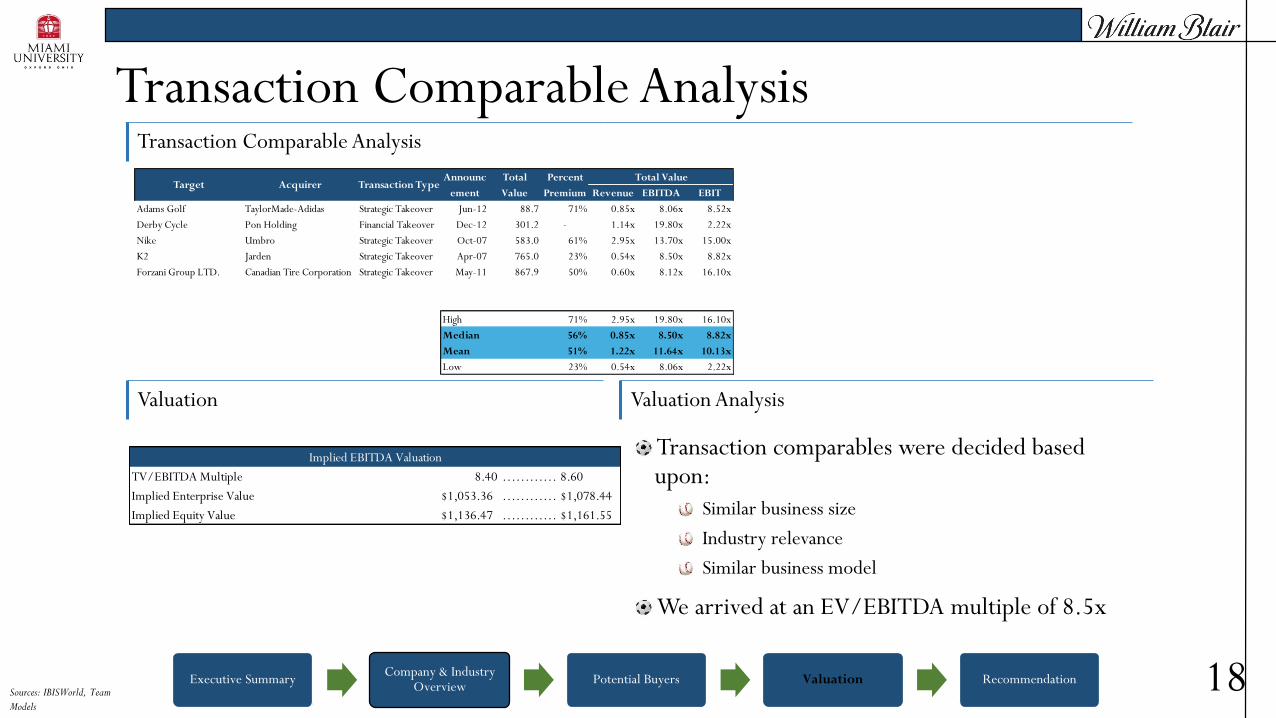

Transaction Comparable Analysis

Valuation AnalysisValuation

18

Transaction Comparable Analysis

Transaction comparables were decided based upon:

Similar business size

Industry relevance

Similar business model

We arrived at an EV/EBITDA multiple of 8.5x

Revenue EBITDA EBIT

Adams Golf TaylorMade-Adidas Strategic Takeover Jun-12 88.7 71% 0.85x 8.06x 8.52x

Derby Cycle Pon Holding Financial Takeover Dec-12 301.2 - 1.14x 19.80x 2.22x

Nike Umbro Strategic Takeover Oct-07 583.0 61% 2.95x 13.70x 15.00x

K2 Jarden Strategic Takeover Apr-07 765.0 23% 0.54x 8.50x 8.82x

Forzani Group LTD. Canadian Tire Corporation Strategic Takeover May-11 867.9 50% 0.60x 8.12x 16.10x

High 71% 2.95x 19.80x 16.10x

Median 56% 0.85x 8.50x 8.82x

Mean 51% 1.22x 11.64x 10.13x

Low 23% 0.54x 8.06x 2.22x

Total ValueTarget Acquirer Transaction Type

Announc

ement

Total

Value

Percent

Premium

TV/EBITDA Multiple 8.40 ………………8.60

Implied Enterprise Value $1,053.36 ………………$1,078.44

Implied Equity Value $1,136.47 ………………$1,161.55

Implied EBITDA Valuation

Sources: IBISWorld, Team

Models

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation

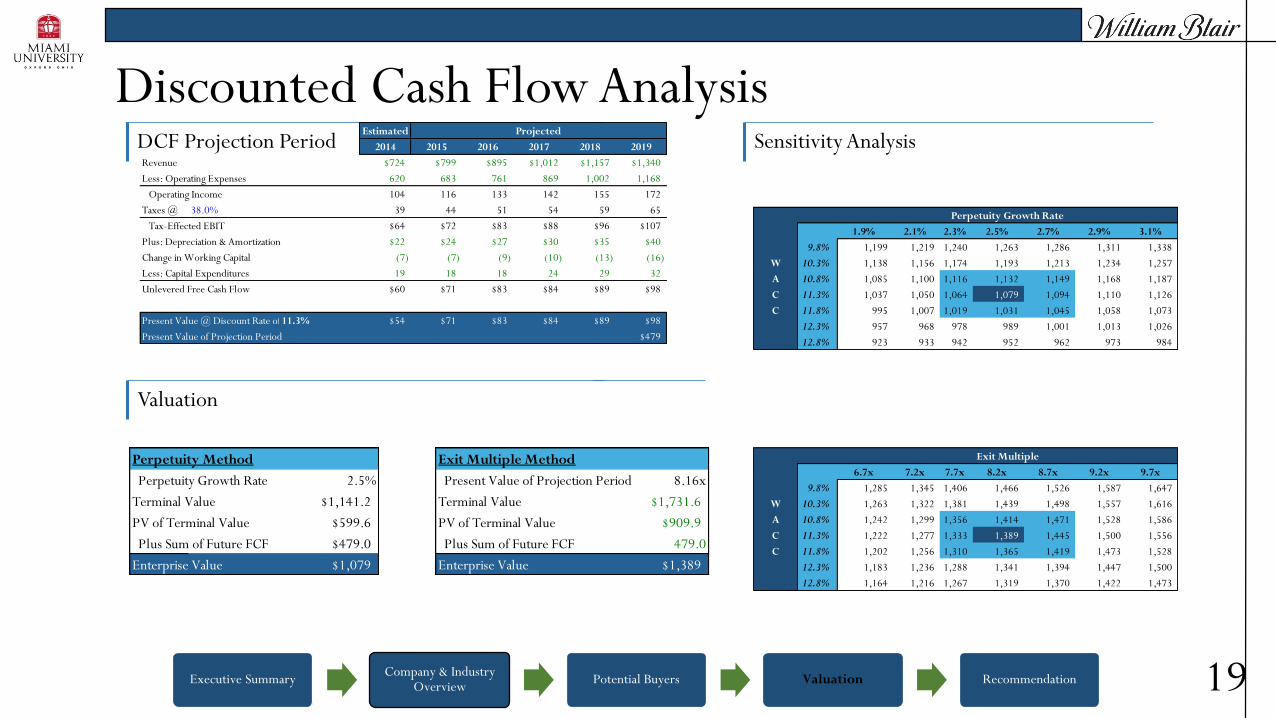

DCF Projection Period

Valuation

Sensitivity Analysis

19

Discounted Cash Flow Analysis

Perpetuity Method

Perpetuity Growth Rate 2.5%

Terminal Value $1,141.2

PV of Terminal Value $599.6

Plus Sum of Future FCF $479.0

Enterprise Value $1,079

Exit Multiple Method

Present Value of Projection Period 8.16x

Terminal Value $1,731.6

PV of Terminal Value $909.9

Plus Sum of Future FCF 479.0

Enterprise Value $1,389

Perpetuity Growth Rate

1.9% 2.1% 2.3% 2.5% 2.7% 2.9% 3.1%

9.8% 1,199 1,219 1,240 1,263 1,286 1,311 1,338

W 10.3% 1,138 1,156 1,174 1,193 1,213 1,234 1,257

A 10.8% 1,085 1,100 1,116 1,132 1,149 1,168 1,187

C 11.3% 1,037 1,050 1,064 1,079 1,094 1,110 1,126

C 11.8% 995 1,007 1,019 1,031 1,045 1,058 1,073

12.3% 957 968 978 989 1,001 1,013 1,026

12.8% 923 933 942 952 962 973 984

Exit Multiple

6.7x 7.2x 7.7x 8.2x 8.7x 9.2x 9.7x

9.8% 1,285 1,345 1,406 1,466 1,526 1,587 1,647

W 10.3% 1,263 1,322 1,381 1,439 1,498 1,557 1,616

A 10.8% 1,242 1,299 1,356 1,414 1,471 1,528 1,586

C 11.3% 1,222 1,277 1,333 1,389 1,445 1,500 1,556

C 11.8% 1,202 1,256 1,310 1,365 1,419 1,473 1,528

12.3% 1,183 1,236 1,288 1,341 1,394 1,447 1,500

12.8% 1,164 1,216 1,267 1,319 1,370 1,422 1,473

Estimated

2014 2015 2016 2017 2018 2019

Revenue $724 $799 $895 $1,012 $1,157 $1,340

Less: Operating Expenses 620 683 761 869 1,002 1,168

Operating Income 104 116 133 142 155 172

Taxes @ 38.0% 39 44 51 54 59 65

Tax-Effected EBIT $64 $72 $83 $88 $96 $107

Plus: Depreciation & Amortization $22 $24 $27 $30 $35 $40

Change in Working Capital (7) (7) (9) (10) (13) (16)

Less: Capital Expenditures 19 18 18 24 29 32

Unlevered Free Cash Flow $60 $71 $83 $84 $89 $98

Present Value @ Discount Rate of:11.3% $54 $71 $83 $84 $89 $98

Present Value of Projection Period $479

Projected

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation

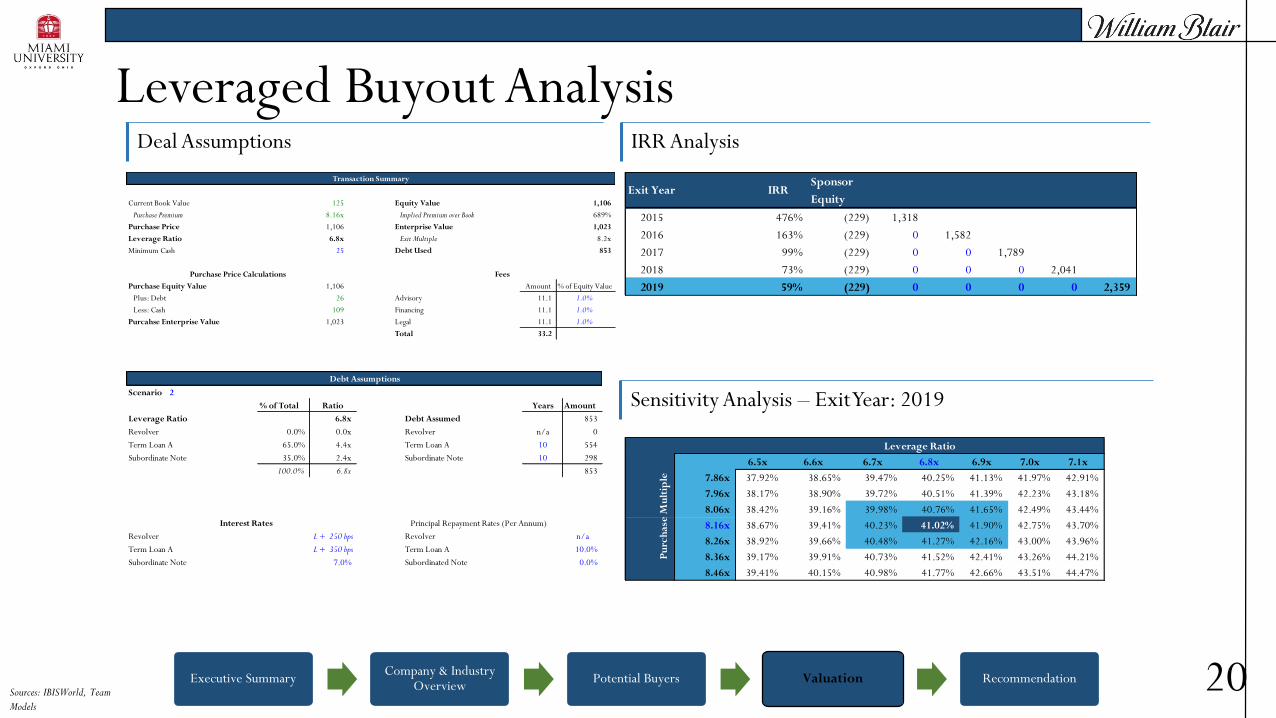

Deal Assumptions IRR Analysis

Sensitivity Analysis – Exit Year: 2019

20

Leveraged Buyout Analysis

Sponsor

Equity

2015 476% (229) 1,318

2016 163% (229) 0 1,582

2017 99% (229) 0 0 1,789

2018 73% (229) 0 0 0 2,041

2019 59% (229) 0 0 0 0 2,359

IRRExit Year

6.5x 6.6x 6.7x 6.8x 6.9x 7.0x 7.1x

7.86x 37.92% 38.65% 39.47% 40.25% 41.13% 41.97% 42.91%

7.96x 38.17% 38.90% 39.72% 40.51% 41.39% 42.23% 43.18%

8.06x 38.42% 39.16% 39.98% 40.76% 41.65% 42.49% 43.44%

8.16x 38.67% 39.41% 40.23% 41.02% 41.90% 42.75% 43.70%

8.26x 38.92% 39.66% 40.48% 41.27% 42.16% 43.00% 43.96%

8.36x 39.17% 39.91% 40.73% 41.52% 42.41% 43.26% 44.21%

8.46x 39.41% 40.15% 40.98% 41.77% 42.66% 43.51% 44.47%

Leverage Ratio

Pu

rch

ase

Mu

ltip

le

Current Book Value 125 Equity Value 1,106

Purchase Premium 8.16x Implied Premium over Book 689%

Purchase Price 1,106 Enterprise Value 1,023

Leverage Ratio 6.8x Exit Multiple 8.2x

Minimum Cash 25 Debt Used 853

Fees

Purchase Equity Value 1,106 Amount % of Equity Value

Plus: Debt 26 Advisory 11.1 1.0%

Less: Cash 109 Financing 11.1 1.0%

Purcahse Enterprise Value 1,023 Legal 11.1 1.0%

Total 33.2

Transaction Summary

Purchase Price Calculations

Scenario 2

% of Total Ratio Years Amount

Leverage Ratio 6.8x Debt Assumed 853

Revolver 0.0% 0.0x Revolver n/a 0

Term Loan A 65.0% 4.4x Term Loan A 10 554

Subordinate Note 35.0% 2.4x Subordinate Note 10 298

100.0% 6.8x 853

Interest Rates Principal Repayment Rates (Per Annum)

Revolver L + 250 bps Revolver n/a

Term Loan A L + 350 bps Term Loan A 10.0%

Subordinate Note 7.0% Subordinated Note 0.0%

Debt Assumptions

Sources: IBISWorld, Team

Models

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation

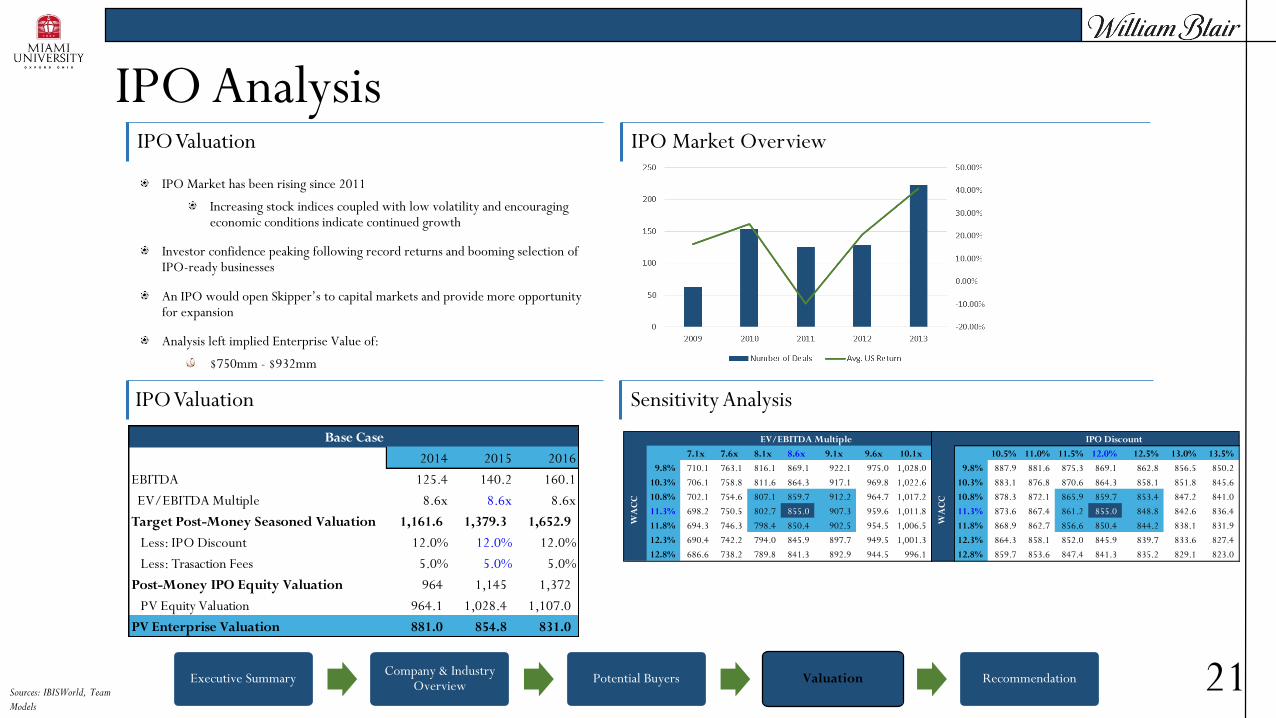

IPO Valuation IPO Market Overview

Sensitivity AnalysisIPO Valuation

21

IPO Analysis

IPO Market has been rising since 2011

Increasing stock indices coupled with low volatility and encouraging economic conditions indicate continued growth

Investor confidence peaking following record returns and booming selection of IPO-ready businesses

An IPO would open Skipper’s to capital markets and provide more opportunity for expansion

Analysis left implied Enterprise Value of:

$750mm - $932mm

EV/EBITDA Multiple

7.1x 7.6x 8.1x 8.6x 9.1x 9.6x 10.1x

9.8% 710.1 763.1 816.1 869.1 922.1 975.0 1,028.0

10.3% 706.1 758.8 811.6 864.3 917.1 969.8 1,022.6

10.8% 702.1 754.6 807.1 859.7 912.2 964.7 1,017.2

11.3% 698.2 750.5 802.7 855.0 907.3 959.6 1,011.8

11.8% 694.3 746.3 798.4 850.4 902.5 954.5 1,006.5

12.3% 690.4 742.2 794.0 845.9 897.7 949.5 1,001.3

12.8% 686.6 738.2 789.8 841.3 892.9 944.5 996.1

WA

CC

IPO Discount

10.5% 11.0% 11.5% 12.0% 12.5% 13.0% 13.5%

9.8% 887.9 881.6 875.3 869.1 862.8 856.5 850.2

10.3% 883.1 876.8 870.6 864.3 858.1 851.8 845.6

10.8% 878.3 872.1 865.9 859.7 853.4 847.2 841.0

11.3% 873.6 867.4 861.2 855.0 848.8 842.6 836.4

11.8% 868.9 862.7 856.6 850.4 844.2 838.1 831.9

12.3% 864.3 858.1 852.0 845.9 839.7 833.6 827.4

12.8% 859.7 853.6 847.4 841.3 835.2 829.1 823.0

WA

CC

2014 2015 2016

EBITDA 125.4 140.2 160.1

EV/EBITDA Multiple 8.6x 8.6x 8.6x

Target Post-Money Seasoned Valuation 1,161.6 1,379.3 1,652.9

Less: IPO Discount 12.0% 12.0% 12.0%

Less: Trasaction Fees 5.0% 5.0% 5.0%

Post-Money IPO Equity Valuation 964 1,145 1,372

PV Equity Valuation 964.1 1,028.4 1,107.0

PV Enterprise Valuation 881.0 854.8 831.0

Base Case

Sources: IBISWorld, Team

Models

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation 22

Recommendation

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation

Valuation Range LBO

Discounted Cash Flows Public Comparable and Precedent Transactions

23

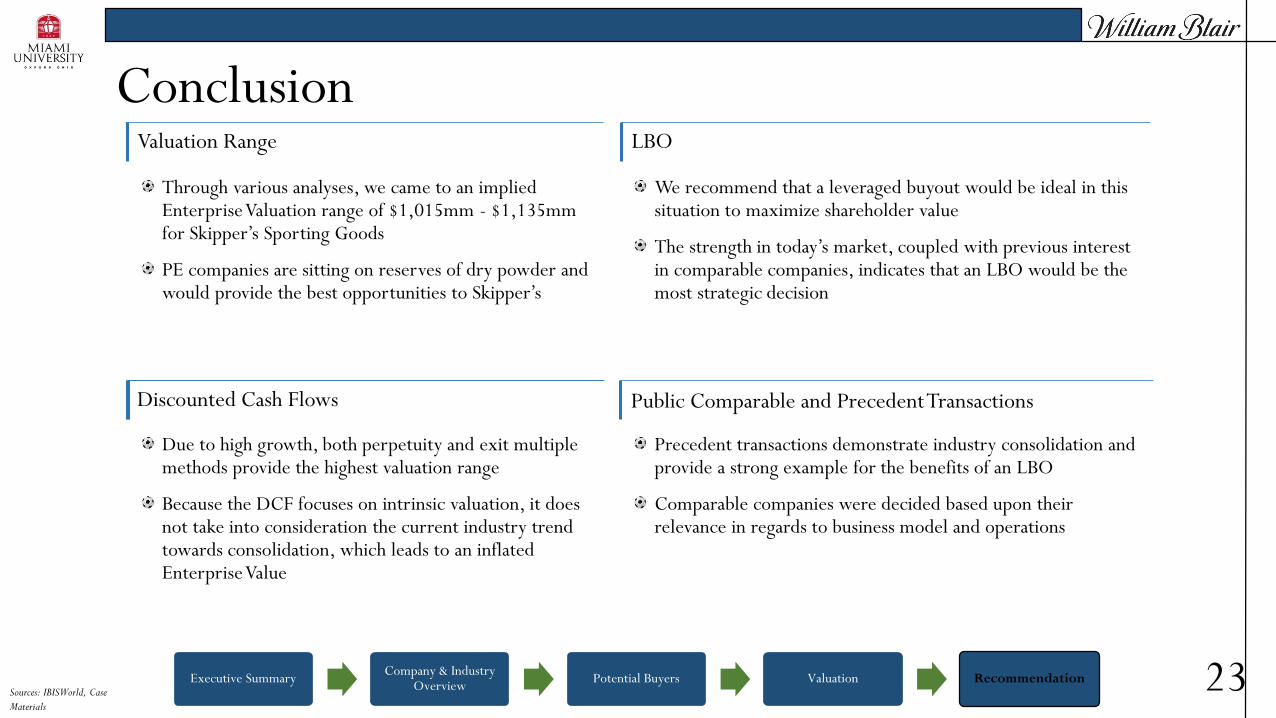

Conclusion

Through various analyses, we came to an implied Enterprise Valuation range of $1,015mm - $1,135mm for Skipper’s Sporting Goods

PE companies are sitting on reserves of dry powder and would provide the best opportunities to Skipper’s

Precedent transactions demonstrate industry consolidation and provide a strong example for the benefits of an LBO

Comparable companies were decided based upon their relevance in regards to business model and operations

Due to high growth, both perpetuity and exit multiple methods provide the highest valuation range

Because the DCF focuses on intrinsic valuation, it does not take into consideration the current industry trend towards consolidation, which leads to an inflated Enterprise Value

We recommend that a leveraged buyout would be ideal in this situation to maximize shareholder value

The strength in today’s market, coupled with previous interest in comparable companies, indicates that an LBO would be the most strategic decision

Sources: IBISWorld, Case

Materials

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation 24

Appendix

Executive SummaryCompany & Industry

OverviewPotential Buyers Valuation Recommendation 25

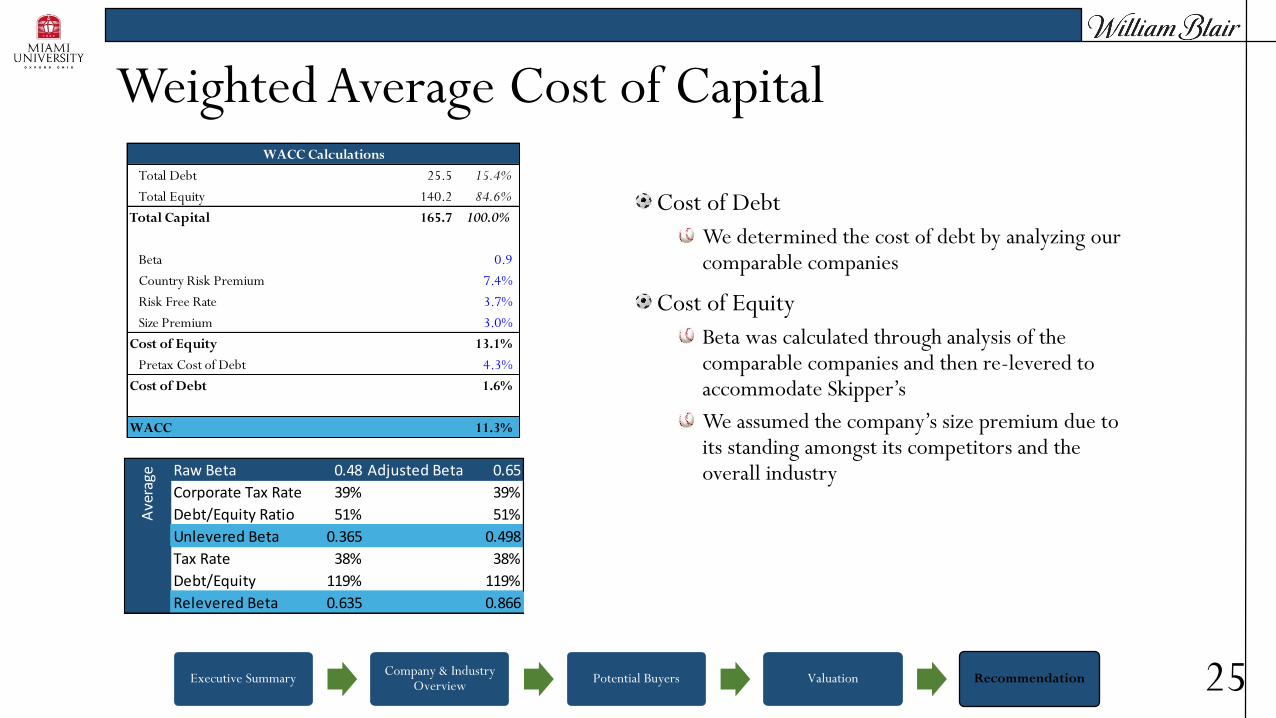

Weighted Average Cost of Capital

Cost of Debt

We determined the cost of debt by analyzing our comparable companies

Cost of Equity

Beta was calculated through analysis of the comparable companies and then re-levered to accommodate Skipper’s

We assumed the company’s size premium due to its standing amongst its competitors and the overall industry

Total Debt 25.5 15.4%

Total Equity 140.2 84.6%

Total Capital 165.7 100.0%

Beta 0.9

Country Risk Premium 7.4%

Risk Free Rate 3.7%

Size Premium 3.0%

Cost of Equity 13.1%

Pretax Cost of Debt 4.3%

Cost of Debt 1.6%

WACC 11.3%

WACC Calculations

Raw Beta 0.48 Adjusted Beta 0.65

Corporate Tax Rate 39% 39%

Debt/Equity Ratio 51% 51%

Unlevered Beta 0.365 0.498

Tax Rate 38% 38%

Debt/Equity 119% 119%

Relevered Beta 0.635 0.866

Ave

rage