biotechnology: industry report ,march 2013

DESCRIPTION

The Indian biotechnology sector is one of the fastest growing knowledge-based sectors in India and is expected to play a key role in shaping India's rapidly developing economy. With numerous comparative advantages in terms of research and development (R&D) facilities, knowledge, skills, and cost effectiveness, the biotechnology industry in India has immense potential to emerge as a global key player.The Indian biotech industry registered 18.5 per cent growth in FY12; total industry size stood at US$ 4.3 billion by the end of the financial year. The industry is expected to increase in size to US$ 11.6 billion by 2017, driven by a range of factors including growing demand, intensive R&D activities and strong Government initiatives.This exceptional growth has been facilitated by the robust performance of all the sub-sectors of the Indian biotechnology industry, namely, bio-pharmaceuticals, bio-services, agri-biotech, bio-industrial, and bio-informatics. Bio-pharmaceuticals is the largest sub-sector of the industry, whereas agri-biotech is the fastest growing. Out of the top 10 biotech companies in India (by revenue), six specialise in bio-pharmaceuticals and four specialise in agri-biotech.TRANSCRIPT

11

Biotechnology

For updated information, please visit www.ibef.org

MARCH2013

22

Contents Advantage India Market overview and trends Growth drivers Success stories: Biocon Opportunities Useful information

For updated information, please visit www.ibef.org

Biotechnology

MARCH2013

33

Biotechnology

For updated information, please visit www.ibef.org ADVANTAGE INDIA

Advantage India

MARCH2013

Advantage

India

• India’s billion-plus population base offers a huge market for biotech products and services

• Increasing economic prosperity and health consciousness will continue to fuel demand for healthcare services

• Public funding for product innovation and research in the biotech sector

• The private sector has been aggressive in pursuing focused R&D

• FDI investment up to 100 per cent is permitted via the automatic route

• A low cost and skilled labour force is attracting outsourced research activity

• The sector has experienced significant growth in government spending since 1985

• Increasing budgetary allocations to the biotech sector

• Setting up of Biotechnology Industry Research Assistance Council

Market size:

USD11.6 billion

FY17F

Market size:

USD4.3 billion

FY12

Source: Association of Biotechnology Led Enterprises (ABLE) June 2012, Global Industry Analysts report (GIA), Aranca Research

Notes: 2017F - Forecast for 2017

Demand potential

Innovation opportunities

Increasing investments Policy support

44

Contents Advantage India Market overview and trends Growth drivers Success stories: Biocon Opportunities Useful information

For updated information, please visit www.ibef.org

Biotechnology

MARCH2013

55For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

Major milestones in Indian biotechnology industry

Biotechnology

• 1978: India’s first biotech firm, Biocon, was setup

• 1981: Centre for Cellular and Molecular Biology was setup in Hyderabad

• 1984: Institute for Microbial Technology, Chandigarh was setup

• 1986: Department of Biotechnology (DBT) was formed

• 1987: National Institute of Immunology was setup by DBT

• 1989: Bangalore Genei commenced operations

• 1991: National Centre for Biological Sciences pursues R&D in molecular biology

• 1994: Syngene, India’s first Contract Research Organisation(CRO), starts its R&D services

• 1997: Centre for Biological Technology (CBT) was established to focus on bioinformatics and genomics

• 1998: Monsanto Research established an R&D centre for plant genomics

• 1998: DBT approves Mahyco-Monsanto to grow Bt cotton

• 2001: The drug authority implements Good Clinical Practice (GCP) guidelines for clinical trials

• 2002: Genetic Engineering Approval Committee (GEAC) approves Bt cotton for commercial planting

• 2007: National Biotechnology Development Strategy launched

• 2009: National Biotechnology Regulatory Authority Bill 2008 to be introduced in parliament

• 2011: Government approved setting up of Biotechnology Industry Research Assistance Council (BIRAC)

1978-1990 1990-1999 Post 2000

Source: EXIM bank of India research, Aranca ResearchNotes: R&D - Research and Development

MARCH2013

66For updated information, please visit www.ibef.org

Key segments in the Indian biotechnology industry

Source: ABLE - Biospectrum industry survey, June 2012; Aranca Research

MARKET OVERVIEW AND TRENDS

Biotechnology

Bio-pharmaceutical products are therapeutic or preventativemedicines that are derived frommaterials naturally present in livingorganisms, using recombinant DNA(rDNA) technology

Bio-services mainly include clinicalresearch and CRO along with custom manufacturing

Bio-agriculture is segmented into hybrid seeds, transgenic crops, bio-pesticides and bio-fertilizers

Bio-industrial predominantly comprises enzymemanufacturing and marketing companies

Bio-informatics deals with the creation and maintenance ofextensive electronic databases on various biological systems; it is the smallest part of the current domestic biotechnology industry

Bio-pharma Bio-services Bio-agri Bio-industrial Bio-informatics

Biotechnology

MARCH2013

77For updated information, please visit www.ibef.org

Major products/services of the Indian biotechnology industry

MARKET OVERVIEW AND TRENDS

Sources: ABLE - Biospectrum Industry Survey, June 2012; Aranca Research

Biotechnology

Biotechnology

Bio-pharma Bio-services Bio-agri Bio-industrial Bio-informatics

Vaccines

Diagnostic

Therapeutic

Custom Manufacturin

g

CRO Hybrid seeds

Bio-fertilizers

Bio-pesticides

Industrial enzymes

Database services

Integrated research app

softwareBiotech software services

MARCH2013

88For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

→ Keeping on with the growth momentum of the previous years, the Indian biotech industry registered 18.5 per cent growth in FY12; total industry size stood at USD4.3 billion by the end of the financial year

→ Fast-paced growth is likely to continue; the industry is expected to increased in size to USD11.6 billion by 2017, driven by a range of factors including growing demand, intensive R&D activities and strong government initiatives

Market size over the past few years in USD billion

Source: ABLE - Biospectrum industry survey, June 2012, Aranca Research

Notes: CAGR - Compound Annual Growth Rate

Biotechnology

Source: Global Industry Analysts report (GIA)

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY120.0

1.0

2.0

3.0

4.0

5.0

1.01.4

1.82.1

2.53.0

3.6

4.3

CAGR23.2 %

MARCH2013

Robust growth in the biotech industry

99For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

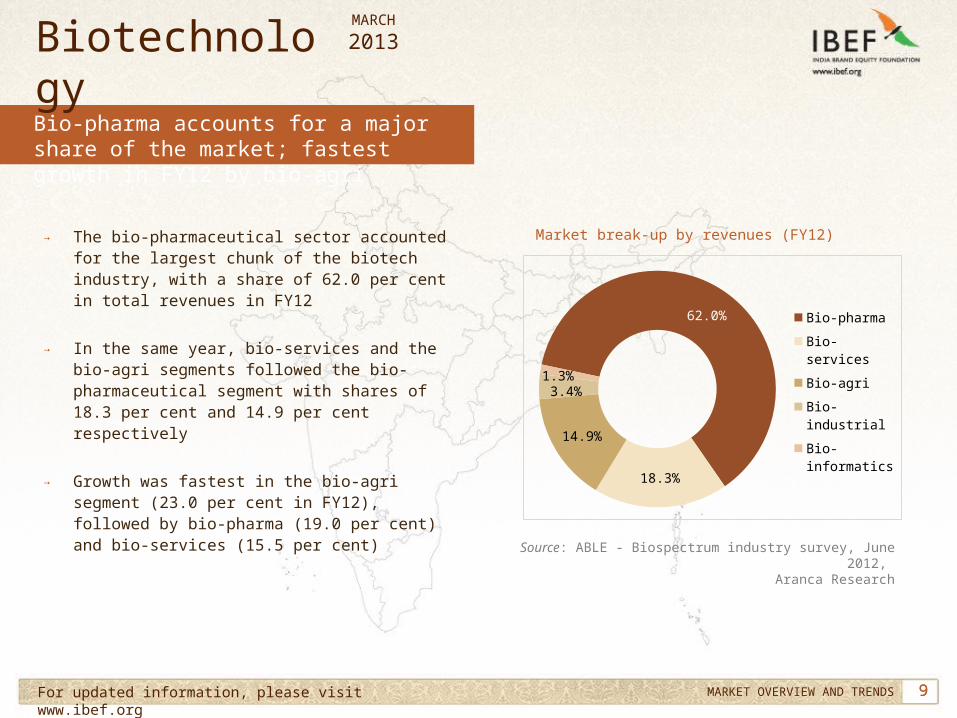

→ The bio-pharmaceutical sector accounted for the largest chunk of the biotech industry, with a share of 62.0 per cent in total revenues in FY12

→ In the same year, bio-services and the bio-agri segments followed the bio-pharmaceutical segment with shares of 18.3 per cent and 14.9 per cent respectively

→ Growth was fastest in the bio-agri segment (23.0 per cent in FY12), followed by bio-pharma (19.0 per cent) and bio-services (15.5 per cent)

Market break-up by revenues (FY12)

Source: ABLE - Biospectrum industry survey, June 2012, Aranca Research

Bio-pharma accounts for a major share of the market; fastest growth in FY12 by bio-agri

Biotechnology

62.0%

18.3%

14.9%

3.4%1.3%

Bio-pharma

Bio-services

Bio-agri

Bio-industrial

Bio-informatics

MARCH2013

1010For updated information, please visit www.ibef.org

Growth was driven by both domestic and export markets … (1/2)

MARKET OVERVIEW AND TRENDS

→ Domestic bio-services sector grew an astounding 102 per cent in FY12 to USD109.3 million

→ The domestic bio-pharma sector, which accounts for more than 61 per cent of the domestic biotech industry, registered a 26.6 per cent growth in FY12; in comparison growth in domestic bio-informatics sector was 24 per cent

Domestic business growth of biotech industry (FY12)

Source: ABLE - Biospectrum industry survey, June 2012, Aranca Research

Biotechnology

Bio-services Bio-Pharma Bio-Informat -ics

Bio-agri Bio-industrial0%

20%

40%

60%

80%

100%

120%

101.9%

26.6% 24.0% 20.4%

11.1%

MARCH2013

1111For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

→ Bio-pharma export revenues contribute more than 63 per cent to total export revenues of the biotech sector; the segment registered a growth of 12.2 per cent in FY12 to touch USD1.3 billion

→ Most impressive was the growth in bio-agri sector export revenues which more than doubled in FY12 to USD31.9 million; this yet again points to the export potential in the segment and one that the industry looks set to exploit in the coming years

Export business growth of biotech industry (FY12)

Source: ABLE - Biospectrum industry survey, June 2012, Aranca Research

Biotechnology

Bio-agri Bio-pharma Bio-industrial Bio-services Bio-informat -ics

-30%

0%

30%

60%

90%

120%106.8%

12.2% 11.3% 8.0%

-19.8%

MARCH2013

Growth was driven by both domestic and export markets … (2/2)

1212For updated information, please visit www.ibef.org

Bio-pharma leads the export earning business

MARKET OVERVIEW AND TRENDS

→ Biotech export revenue reached USD2.1 billion in FY12, nearly half (48 per cent)of total industry revenue

→ Over the years export revenue has growth considerably from USD0.4 billion in FY05 to USD2.1 billion in FY12 (a CAGR of 25.6 per cent)

Exports of biotechnology products (FY12) (USD billion)

Source: ABLE - Biospectrum industry survey, June 2012, Aranca Research

Biotechnology

Export share among major sub sectors (FY12)

Source: ABLE - Biospectrum industry survey, June 2012, Aranca Research

63.1%

32.8%

1.6% 1.7%0.9%

Bio-pharma

Bio-services

Bio-agri

Bio-industrial

Bio-informatics

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY120.0

0.5

1.0

1.5

2.0

2.5

0.4

0.7

1.01.2

1.5 1.6

1.82.1CAGR

25.6 %

MARCH2013

1313For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

Source: ABLE - Biospectrum industry survey, June 2012,Aranca Research

Notes: * - Estimates

The Indian biotech industry is fairly competitive

Biotechnology

Top 10 players in the Indian biotech industry

CompanyRevenue (USD million) FY12

CompanyRevenue (USD million)

FY12

Serum Institute of India 355.8 Rasi seeds 81.7

Biocon 349.3 Panacea Biotec* 80.0

Nuziveedu Seeds 155.2 Bharat Biotech 67.9

Reliance Life sciences* 144.4 Ankur Seeds 67.7

NovoNordisk * 134.9 Mahyco 65.4

Top 20 companies accounted for 76.1 per cent of industry revenues in FY12

MARCH2013

1414For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

Source: Aranca Research, Indian Law Offices

Notable trends in the Indian biotech sector

Biotechnology

Remarkable global positioning

Pharma companies are

focusing on biotech

• Ranbaxy, Cadila Healthcare, Lupin, Wockhardt and Dr Reddy’s are among the major Indian pharmaceutical companies that operate in the bio-pharma segment

Global companies setting up base

• Lonza, the global leader in the production and support of pharmaceutical and biotech products, is planning to set up a manufacturing base in India at an investment of USD150 million in Hyderabad. The investment outlay has been planned over two phases:

• Phase I (from 2011 to 2013) would include the development of R&D labs for more than 100 resources

• Phase II (from 2014 to 2015) would include the expansion of manufacturing capabilities and the provision for increasing R&D lab capacity for biologics with 200 additional resources

• India is amongst the top 12 biotech destinations in the world• India ranks second in Asia, after China• India is the largest producer of recombinant Hepatitis B vaccine in the

world

MARCH2013

1515

Contents Advantage India Market overview and trends Growth drivers Success stories: Biocon Opportunities Useful information

For updated information, please visit www.ibef.org

Biotechnology

MARCH2013

1616For updated information, please visit www.ibef.org GROWTH DRIVERS

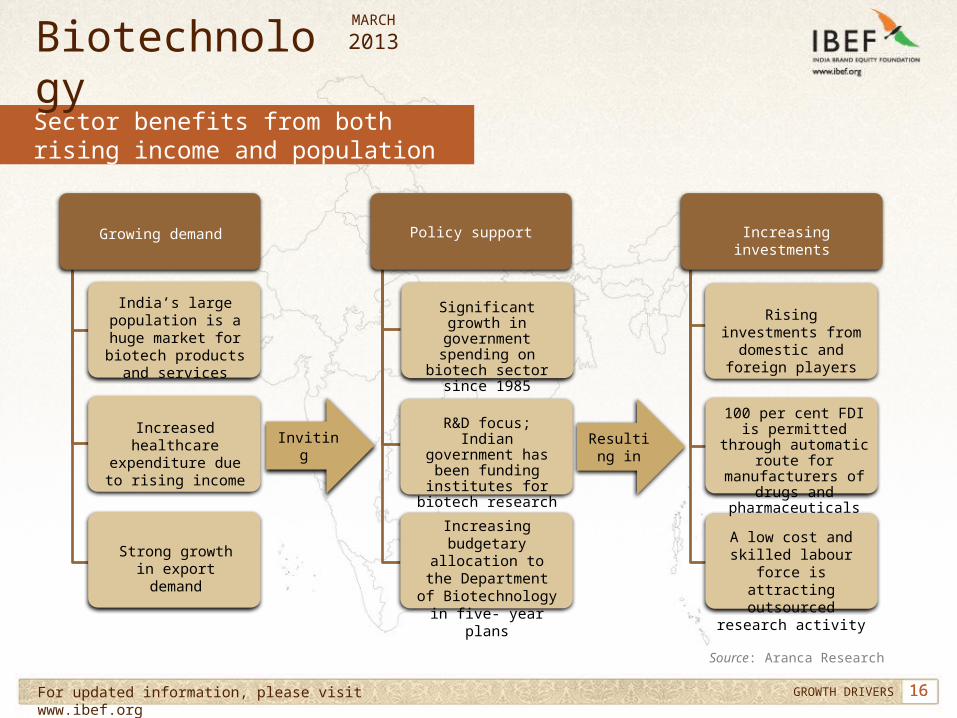

Sector benefits from both rising income and population

Biotechnology

Strong government

support

Large domestic market

Growing demand

Inviting Resulting in

Growing demand Increasing investments Policy support

India’s large population is a

huge market for biotech products

and services

Increased healthcare

expenditure due to rising income

Strong growth in export demand

Significant growth in government spending on

biotech sector since 1985

R&D focus; Indian government has

been funding institutes for

biotech research

Increasing budgetary

allocation to the Department of

Biotechnology in five- year plans

Rising investments from domestic and

foreign players

100 per cent FDI is permitted through automatic route for manufacturers of

drugs and pharmaceuticals

A low cost and skilled labour force

is attracting outsourced research

activity

Source: Aranca Research

MARCH2013

1717For updated information, please visit www.ibef.org

Source: Mid term appraisal," Eleventh Five Year Plan, National Biotechnology development strategy, DBT,

Aranca ResearchNotes: FYP - Five Year Plan

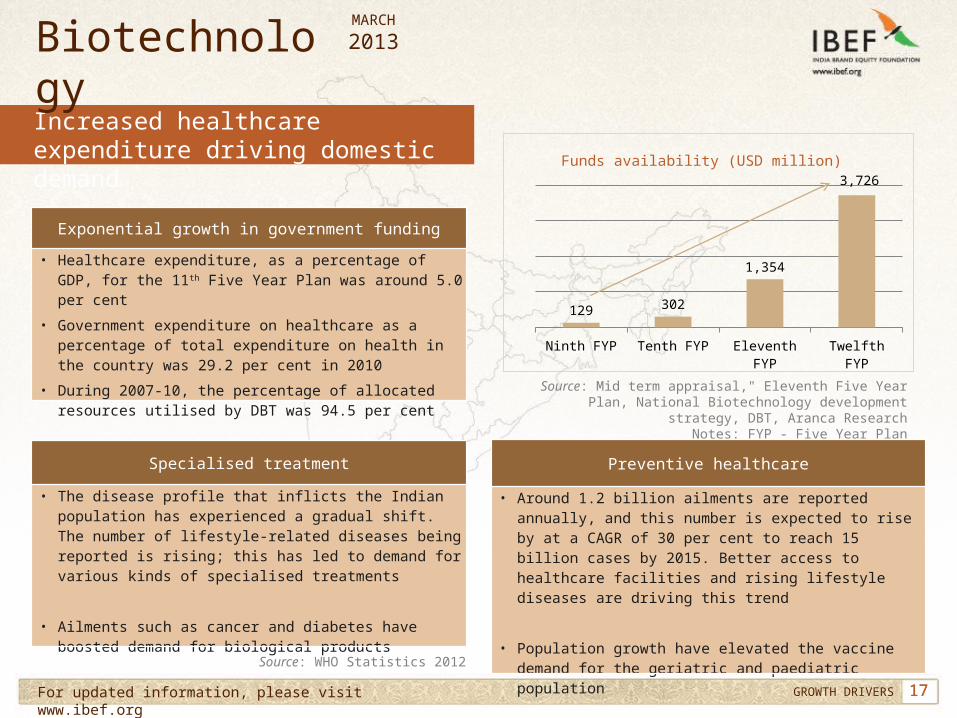

Increased healthcare expenditure driving domestic demand

GROWTH DRIVERS

Biotechnology

Exponential growth in government funding• Healthcare expenditure, as a percentage of GDP, for

the 11th Five Year Plan was around 5.0 per cent• Government expenditure on healthcare as a

percentage of total expenditure on health in the country was 29.2 per cent in 2010

• During 2007-10, the percentage of allocated resources utilised by DBT was 94.5 per cent

Preventive healthcare

• Around 1.2 billion ailments are reported annually, and this number is expected to rise by at a CAGR of 30 per cent to reach 15 billion cases by 2015. Better access to healthcare facilities and rising lifestyle diseases are driving this trend

• Population growth have elevated the vaccine demand for the geriatric and paediatric population

Specialised treatment

• The disease profile that inflicts the Indian population has experienced a gradual shift. The number of lifestyle-related diseases being reported is rising; this has led to demand for various kinds of specialised treatments

• Ailments such as cancer and diabetes have boosted demand for biological products

Source: WHO Statistics 2012

Ninth FYP Tenth FYP Eleventh FYP Twelfth FYP

129 302

1,354

3,726Funds availability (USD million)

MARCH2013

1818For updated information, please visit www.ibef.org

Source: Fortis Healthcare Limited 2008-09 ANR

Rising income and incidence of chronic diseases

GROWTH DRIVERS

Biotechnology

Rising incomes; growing middle class• Growing per-capita incomes; rural incomes also rising

• Expanding middle class population; this segment’s size is estimated to touch 550 million by 2025 from 50 million in 2010

• Rising per capita income leads to increased spending on medical and healthcare services

Higher incidence of chronic diseases• Lifestyle diseases are set to account for a greater part

of the healthcare market

• Lifestyle diseases such as cardiac diseases, cancer and diabetes are treated with the help of biotechnology products, thereby boosting revenues of biotech companies

Notes: Greater distributional efficiencies, increasing demand (especially from rural areas) due to rising disposable

incomes have created new markets for products within the country

22%

78%

2001

Acute in-fections

Lifestyle & Others

14%

86%

2012F

2005 2010 2015 2020 20250

10

20

30

40

50

60

70

Strivers Seekers DeprivedAspirers Globals

Source: McKinsey Quarterly, Aranca Research

Aspirers: annual income

INR90,000 -200,000

million households Seekers: annual income INR200,000 -

500,000

Deprived annual income

<INR90,000

Globals: annual income

>INR1,000,000

Strivers: annual income INR500,000 -

1,000,000

MARCH2013

1919For updated information, please visit www.ibef.org

Strong policy support is crucial to the sector’s development

GROWTH DRIVERS

Biotechnology

Source: “Biotechnology facilities,” Department of Biotechnology, Aranca Research

Note: BIRAC - Biotechnology Industry Research Assistance Council

• As per NBDS, a proposal has been made to set up National Biotechnology Regulatory Authority (NBRA) to provide a single-window clearance mechanism for all bio-safety clearances of products to create efficiencies and streamline the drug approval process

New facilities

National Biotechnology Development

Strategy

• DBT designed National Biotechnology Development Strategy (NBDS) to strengthen the industry’s human resources and infrastructure while promoting growth and trade

• As part of the NBDS, government has decided to spend 30 per cent of DBT’s budget in public private partnerships to promote Research & Development at various stages

Single-window clearance

• DBT set up 35 facilities during 2002-07 to produce and supply biological products, reagents, culture collections and laboratory animals to scientists, industries and students at nominal costs

• The government launched a biotechnology industry partnership programme for developing new technologies

Biotechnology Industry Research Assistance Council

• BIRAC has been established to promote research and innovation capabilities in India’s biotech industry

• Under BIRAC, the government will provide funding to biotech companies for technology and product development

MARCH2013

2020For updated information, please visit www.ibef.org

Government funding is crucial for the biotech industry

GROWTH DRIVERS

Biotechnology

Source: Ernst & Young, Aranca Research

Venture fund

Infrastructure development

• India’s central government and the state governments in collaboration with private players continue to develop new infrastructure facilities, especially through biotechnology parks

• Government is developing three major biotech clusters at Mohali in Punjab, Faridabad in Haryana, Bengaluru in Karnataka.

International collaborations

• International collaborations with different countries are directed at enabling the effective transition of knowledge

• India has partnered with countries such as the UK, Russia, Italy, the US and France to enable knowledge transition

• The government announced a plan to set up a USD2.2 billion venture fund for supporting drug discovery and research infrastructure development projects

• Government funding is crucial for the biotech industry as they have limited access to other sources of funding

Clinical Establishments Bill

• In a move to standardise procedures, the Indian Parliament passed the Clinical Establishments Bill 2010, which would make registration of clinical trials as well as clinical research organisations mandatory in the country

• The bill also includes standard operating procedures for various trial related tasks

MARCH2013

2121For updated information, please visit www.ibef.org

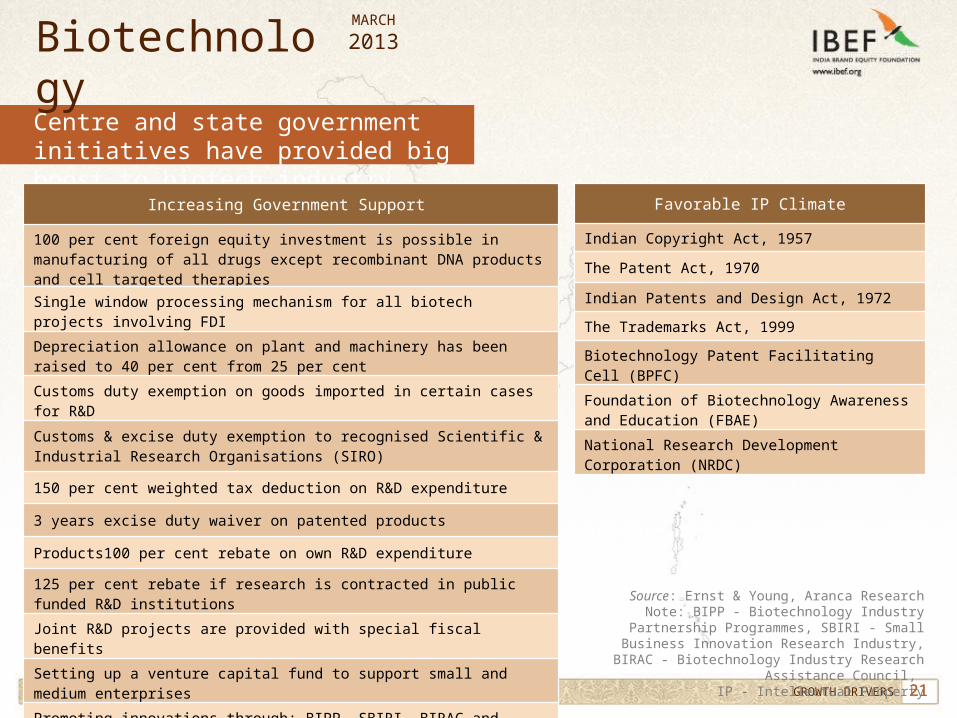

Centre and state government initiatives have provided big boost to biotech industry

GROWTH DRIVERS

Biotechnology

Source: Ernst & Young, Aranca ResearchNote: BIPP - Biotechnology Industry Partnership Programmes, SBIRI - Small Business Innovation

Research Industry, BIRAC - Biotechnology Industry Research Assistance Council,

IP - Intellectual Property

Increasing Government Support

100 per cent foreign equity investment is possible in manufacturing of all drugs except recombinant DNA products and cell targeted therapiesSingle window processing mechanism for all biotech projects involving FDIDepreciation allowance on plant and machinery has been raised to 40 per cent from 25 per centCustoms duty exemption on goods imported in certain cases for R&D

Customs & excise duty exemption to recognised Scientific & Industrial Research Organisations (SIRO)

150 per cent weighted tax deduction on R&D expenditure

3 years excise duty waiver on patented products

Products100 per cent rebate on own R&D expenditure125 per cent rebate if research is contracted in public funded R&D institutionsJoint R&D projects are provided with special fiscal benefitsSetting up a venture capital fund to support small and medium enterprisesPromoting innovations through: BIPP, SBIRI, BIRAC and Biotech parks

Favorable IP ClimateIndian Copyright Act, 1957 The Patent Act, 1970Indian Patents and Design Act, 1972 The Trademarks Act, 1999 Biotechnology Patent Facilitating Cell (BPFC)Foundation of Biotechnology Awareness and Education (FBAE)National Research Development Corporation (NRDC)

MARCH2013

2222For updated information, please visit www.ibef.org

Source: Policy and rules,” Department of Biotechnology website, Aranca Research

Regulatory framework of the Indian Biotech Sector

GROWTH DRIVERS

Biotechnology

Government of India

Ministry of Science & Technology

Ministry of Environment &

Forests

Department of Biotechnology

Department of Environment,

Forests & Wildlife

Recombinant DNA Advisory Committee

(RDAC)

Regulatory Committee on

Genetic Manipulation

(RCGM)

Institutional Biosafety

Committee (IBSC)

Genetic Engineering

Approval Committee

(GEAC)

MARCH2013

2323For updated information, please visit www.ibef.org

→ The 12th Five Year Plan aims to set up 3-5 bio-clusters with technology incubators, technology parks, innovation centers and entrepreneurship development units

→ Biotechnology infrastructure is witnessing a shift from traditional clusters to specialised industrial infrastructure such as biotech or science parks

→ States such as Andhra Pradesh, Maharashtra, Tamil Nadu and Kerala have been early movers in establishing world-class biotech parks and clusters

→ Investors such as TCG Bio-pharma and Alexandria have significantly contributed to the establishment of biotechnology-related infrastructure in India

Source: Planning Commission, Aranca Research, "Mid term appraisal," Eleventh Five Year Plan

Solid industry infrastructure would drive growth

GROWTH DRIVERS

Biotechnology

JogindernagarShimla

Chandigarh

AlwarSohnaJodhpur Jaipur

Gandhinagar AnandJamnagarBaroda

AurangabadPune

Hyderabad

BhubaneshwarKonark

Midnapore

Pantnagar

BengaluruChennai

Puducherry

Visakhapatnam

Kochi

Karwar

Madurai

Operational biotech parks

MARCH2013

2424For updated information, please visit www.ibef.org

Source: MISSOURI, International Trade and Investment Office - India bio 2012, Aranca

Research

Karnataka: The biotech capital of India

GROWTH DRIVERS

Biotechnology

19%

17%

10%26%

8%

8%

13% Bangalore

Hyderabad

Pune

Mumbai

NCR

Ahmedabad

Others

Top biotech clusters in India - 2011→ 60 per cent of biotech companies in India have a base in Bengaluru

→ 50 per cent of total revenues in the national biotechnology sector comes from Bengaluru

→ Extensive intellectual capital→ 12 biotechnology finishing schools under

Millennium Biotech Policy II→ 103 R&D centers

→ Extensive industrial infrastructure→ Sector focused SEZs: Mysore, Mangalore, Hubli -

Dharwar, Belgaum, Shimoga, Gulbarga, Kolar and Mandya

→ 86 acre biotechnology park - Bangalore Helix with 52 acre Alexandria Knowledge Park in Bengaluru

→ Pro industry policy: State Millennium Biotech Policy II 2010, State Industrial Policy 2009-14

→ K-Bio Venture Capital Fund of USD10.4 million with 26 per cent stake by Government of Karnataka

→ Financial support of 20 per cent of the project cost for PPP-based projects for creation of biotech parks

MARCH2013

2525For updated information, please visit www.ibef.org

→ During the 11th Five Year Plan, the government started six new institutions in different fields of biotechnology across India

→ Fellowships rose from 100 to 250 per year for PhD students in addition to 100 postdoctoral and 50 biotechnology overseas associateships

→ Government provide grant-in-aid to the industry for R&D in certain diseases such as malaria and leishmaniasis or kala-azar

High-end research infrastructure creates scope for innovation

GROWTH DRIVERS

Biotechnology

Details of key biotechnology parks in IndiaParks City Area (in

acres)Shapoorji Pallonji Biotech Park Hyderabad 300

ICICI Knowledge Park Hyderabad 200International Biotech Park Pune 103

Lucknow Biotech Park Lucknow 20Golden Jubilee Biotech Park Chennai 8

Ticel Bio Park Chennai 5

Key research institutes in IndiaCentral Drug Research Institute (CDRI), LucknowNational Institute of Pharmaceutical Education and Research (NIPER), MohaliIndian Institute of Chemical Technology (IICT), HyderabadCentre for Cellular & Molecular Biology (CCMB), HyderabadIndian Institute of Chemical Biology (IICB), KolkataIndian Toxicology Research Institute (ITRI), LucknowInstitute of Genomics and Integrative Biology (IGIB), New DelhiInstitute of Microbial Technology (IMTECH), ChandigarhNational Chemical Laboratory (NCL), PuneNational Centre for Biological Sciences (NCBS), BengaluruJawaharlal Nehru Centre for Advanced Scientific Research (JNCASR), BengaluruIndian Institute of Science (IISc), BengaluruNational Institute of Immunology (NII), New Delhi

Source: Aranca Research, "Mid term appraisal," Eleventh Five Year Plan

MARCH2013

2626For updated information, please visit www.ibef.org

→ From November 2000 to August 2010, the drugs and pharmaceuticals sector attracted foreign direct investment (FDI) worth USD1.8 billion

Strong inflows of foreign investment

GROWTH DRIVERS

Biotechnology

Source: Thomson One Banker, Aranca analysisNote: * - Estimated value

Date Announced Acquirer Name Target Name Value of Deal(USD million)

Nov 2012 Bristol-Myres squibb Biocon’s (IN-105) oral insulin 300-350*

Jul 2012 Serum Institute of India Ltd NVI - Vaccin Production Unit 40.28

Jun 2012 Nandan Cleantec PLC Xtraa Cleancities Infra -

Mar 2012 Investor Group Titan Biotech Ltd -

Jan 2012 Xenetic Biosciences plc Symbiotec Pharmalab Ltd 9.34

Jan 2011 Evolvence India Life Sciences Fermenta Biotech Ltd 8.90

Jul 2010 Marck Biosciences Ltd Ravish Infusions Ltd 1.22

Jun 2010 Piramal Healthcare Ltd BioSyntech Inc 4.20

May 2010 Sequoia Capital India Invest Celon Laboratories Ltd 15.74

Apr 2010 Anu's Laboratories Ltd Stilbene Chemicals Ltd -

MARCH2013

2727

Contents Advantage India Market overview and trends Growth drivers Success stories: Biocon Opportunities Useful information

For updated information, please visit www.ibef.org

Biotechnology

MARCH2013

2828For updated information, please visit www.ibef.org SUCCESS STORIES: BIOCON

Biocon: An early mover to the global biotech market

Biocon’s position in the Indian market during FY12

Ranked 1st among Indian Insulin companies

Ranked 1st in the Glargine vial market

Ranked 3rd in the 40 IU Insulin market

Ranked 4th in overall Insulin market

Biotechnology

• Incorporated in 1978 at Bengaluru, India

• IPO offering in 2004 (BSE, NSE India)

• Among the world’s largest producers of statins and immuno -suppressants

• 2011: Launched INSUPen®, a convenient and affordable reusable insulin delivery device

• Market cap of USD1.2 billion

• Revenue reported in H1FY13 was USD257.3 million (up 23 per cent YoY) while net profit was USD35.08 million

Source: Biocon Fact Sheet

FY08 FY09 FY10 FY11 FY12 H1FY13

227249

311

387448

257

47 49 56 7171

35

Revenue (USD million) Net Profit (USD million)

MARCH2013

2929

Contents Advantage India Market overview and trends Growth drivers Success stories: Biocon Opportunities Useful information

For updated information, please visit www.ibef.org

Biotechnology

MARCH2013

3030For updated information, please visit www.ibef.org

Source: India Law Offices, Aranca Research

Huge opportunities for innovation in agriculture/healthcare

Biotechnology

• India has the potential to become a major producer of transgenic rice and several genetically modified (GM) or engineered vegetables

• Hybrid seeds, including GM seeds, represent new business opportunities in India based on yield improvement

Vaccines

Bioactive therapeutic proteins

• Protein and antibody production and the fabrication of diagnostic protein chips is a promising area for investment

• Stem cell research, cell engineering and cell-based therapeutics is another area, wherein India will cash in its expertise

Agriculture sector

• Vaccines and recombinant therapeutics are the leading sectors driving the biotechnology industry’s growth in India

• Newer therapies are anticipated to launch in the next few years, prominent among these are monoclonal antibodies products, stem cell therapies and growth factors

• The country’s huge population places it among the world’s largest markets for vaccines

OPPORTUNITIES

MARCH2013

3131For updated information, please visit www.ibef.orgSource: India Law Offices, Aranca Research

Outsourcing opens up further avenues of growth for biotech

Biotechnology

• Indian bioinformatics companies can play a significant role in critical areas such as data mining, mapping and DNA sequencing

• There is also opportunity in functional genomics, proteonics and molecule design simulation

Contract research

Clinical trials and outsourcing

• India offers a suitable population for clinical trials because of its diverse gene pools, which cover a large number of diseases

• Cost effectiveness, competition, and increased confidence on capabilities and skill sets have propelled many global pharmaceutical companies to expand their own clinical research investment in the nation

Bio informatics

• The R&D sector has huge potential; many opportunities have been created with a number of foreign companies investing in this sector

• Indian pharmaceutical companies possess competitive skills in chemical synthesis and process engineering; the companies can leverage these skills to develop new chemical entities

• Some other potential areas of development include medicinal and aromatic plants, animal biotechnology, aquaculture and marine biotechnology, seri biotechnology, stem cell biology, environmental biotechnology, biofuels, biopesticides, human genetics, genome analysis, and others

Others

OPPORTUNITIES

MARCH2013

3232

Contents Advantage India Market overview and trends Growth drivers Success stories: Biocon Opportunities Useful information

For updated information, please visit www.ibef.org

Biotechnology

MARCH2013

3333For updated information, please visit www.ibef.org USEFUL INFORMATION

Industry Associations

Association of Biotechnology Led Enterprises (ABLE)# 123/C, 16th Main Road, 5th Cross, 4th BlockNear Sony World Showroom/Headstart School Koramangala, Bengaluru - 560034Phone: 91 80 41636853 25633853E-mail: [email protected]: www.ableindia.org

All India Biotech Association (AIBA)"VIPPS Center" 2. Local Shopping Centre Block EFGH, Masjid Moth, Greater Kailash-II, New Delhi - 110048Tel: 91 11 29211487 (Direct), 29220546/547Fax: 91 11 29223089, 29229166Email: [email protected] Website: www.aibaonline.com

Biotechnology

MARCH2013

3434For updated information, please visit www.ibef.org

Glossary→ Bt: Bacillus thuringiensis→ CAGR: Compound Annual Growth Rate→ CRO: Contract Research Organisation→ DNA: Deoxyribonucleic acid→ FYP: Five Year Plan→ GCP: Good Clinical Practice→ INR: Indian Rupee→ NBTB: National Biotechnology Board→ OAD: Oral anti-diabetic drugs→ R&D: Research And Development→ FY: Indian financial year (April to March)

→ So FY10 implies April 2009 to March 2010→ USD: US Dollar

→ Conversion rate used: USD1= INR48→ Wherever applicable, numbers have been rounded off to the nearest whole number

USEFUL INFORMATION

Biotechnology

MARCH2013

35

India Brand Equity Foundation (IBEF) engaged Aranca to prepare this presentation and the same has been prepared by Aranca in consultation with IBEF.

All rights reserved. All copyright in this presentation and related works is solely and exclusively owned by IBEF. The same may not be reproduced, wholly or in part in any material form (including photocopying or storing it in any medium by electronic means and whether or not transiently or incidentally to some other use of this presentation), modified or in any manner communicated to any third party except with the written approval of IBEF.

This presentation is for information purposes only. While due care has been taken during the compilation of this

presentation to ensure that the information is accurate to the best of Aranca and IBEF’s knowledge and belief, the content is not to be construed in any manner whatsoever as a substitute for professional advice.

Aranca and IBEF neither recommend nor endorse any specific products or services that may have been mentioned in this presentation and nor do they assume any liability or responsibility for the outcome of decisions taken as a result of any reliance placed on this presentation.

Neither Aranca nor IBEF shall be liable for any direct or indirect damages that may arise due to any act or omission on the part of the user due to any reliance placed or guidance taken from any portion of this presentation.

For updated information, please visit www.ibef.org DISCLAIMER

Biotechnology

MARCH2013

Disclaimer