biogen, inc. biotechnology - credit suisse

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

19 January 2016Americas/United States

Equity ResearchBiotechnology

Biogen, Inc. (BIIB)

INITIATION Rating NEUTRALPrice (15-Jan-16,US$) 273.33Target price (US$) 322.0052-week price range 475.98 - 256.04Market cap (US$ m) 60,926.11Enterprise value (US$ m) 60,770.06*Stock ratings are relative to the coverage universe in each analyst's or each team's respective sector.¹Target price is for 12 months.

Research AnalystsAlethia Young

212 538 [email protected]

Eliana Merle212 538 0678

Grant Hesser212 325 2587

Cautious Pipeline Optimism Is Not Enough■ We are initiating coverage of Biogen with a Neutral rating and a $322 target

price target. We think their base businesses continue to have headwinds and that its pipeline is the big upside driver. We think the level of credit we give to anti-LINGO1 and Alzheimer's is appropriate based on what we will learn this year, but we find it hard to get enough conviction to see upside at this point.

■ Cautious on Base Business: We expect competition from new regimens to affect base business growth in the long term. Our 2016 rev and EPS estimates are $11.13B and $17.75 vs. the Street of $11.24B and $18.55. We are ~$400M and $600M under 2017 and 2018 estimates due to MS and haemophilia competitive headwinds.

■ Some Pipeline Is Baked into Shares: Even with significant pipeline credit baked in based on what we know about Alzheimer's, Lingo, and SMA, our DCF valuation is $284/share. We assume 40%, 25%, and 65%, respectively.

■ Catalysts; Pipeline Focused: Catalysts include (1) synergy MS study anti-LINGO1 data in mid-2016 (2) BAN2401 top-line data in AD, (3) E2609 BACE safety look, (4) Solanezumab (Lilly) Ph3 data in the October 2016 read-through, and (5) adacanumab titration updates on the PRIME AD study.

■ Valuation: Our TP is a 50/50 split of DCF and P/E multiple. Our DCF is $284/sh based on an 8% discount rate and 2% terminal growth, which is in-line with peers. Our P/E valuation is $360/sh. We assign a 20.3x multiple to 2016 EPS of $17.75, which is a 5% premium to the large-cap sector ex-GILD and a 23% premium to the S&P 500. We believe that this multiple is justified based on Biogen's base business and pipeline profile. Upside risks include robust pipeline data and stronger base business results. Downside risks include pipeline failure and weaker base business results.

Share price performance

BIIB.O Q S& P 5 0 0 IN D EX

A p r - 1 5 Ju l - 1 5 O ct - 1 5 Jan - 1 52 0 0

3 0 0

4 0 0

5 0 0

On 15-Jan-2016 the S&P 500 INDEX closed at 1880.33Daily Jan16, 2015 - Jan15, 2016, 01/16/15 = US$352.75

Quarterly EPS Q1 Q2 Q3 Q42014A 2.02 3.05 3.61 3.742015E 3.48 3.92 4.38 3.602016E 4.14 4.00 4.13 4.22

Financial and valuation metricsYear 12/14A 12/15E 12/16E 12/17EEPS (CS adj.) (US$) 13.83 16.76 17.75 19.43Prev. EPS (US$) - - - -P/E (x) 19.8 16.3 15.4 14.1P/E rel. (%) 110.8 92.0 92.9 95.7Revenue (US$ m) 9,703.3 10,682.8 11,136.7 11,686.7EBITDA (US$ m) 4,660.6 5,408.9 5,622.7 5,945.7OCFPS (US$) 12.40 16.64 18.69 19.81P/OCF (x) 27.4 16.4 14.6 13.8EV/EBITDA (current) 12.9 11.2 10.7 9.9Net debt (US$ m) -620 -156 -537 -1,925ROIC (%) 29.19 33.28 31.21 30.47

Number of shares (m) 222.90 IC (current, US$ m) 10,194.31Net debt (Next Qtr., US$ m) - EV/IC (x) -Net debt/tot eq (Next Qtr.,%) - Dividend (current, US$) -Source: Company data, Thomson Reuters, Credit Suisse estimates

19 January 2016

Biogen, Inc. (BIIB) 2

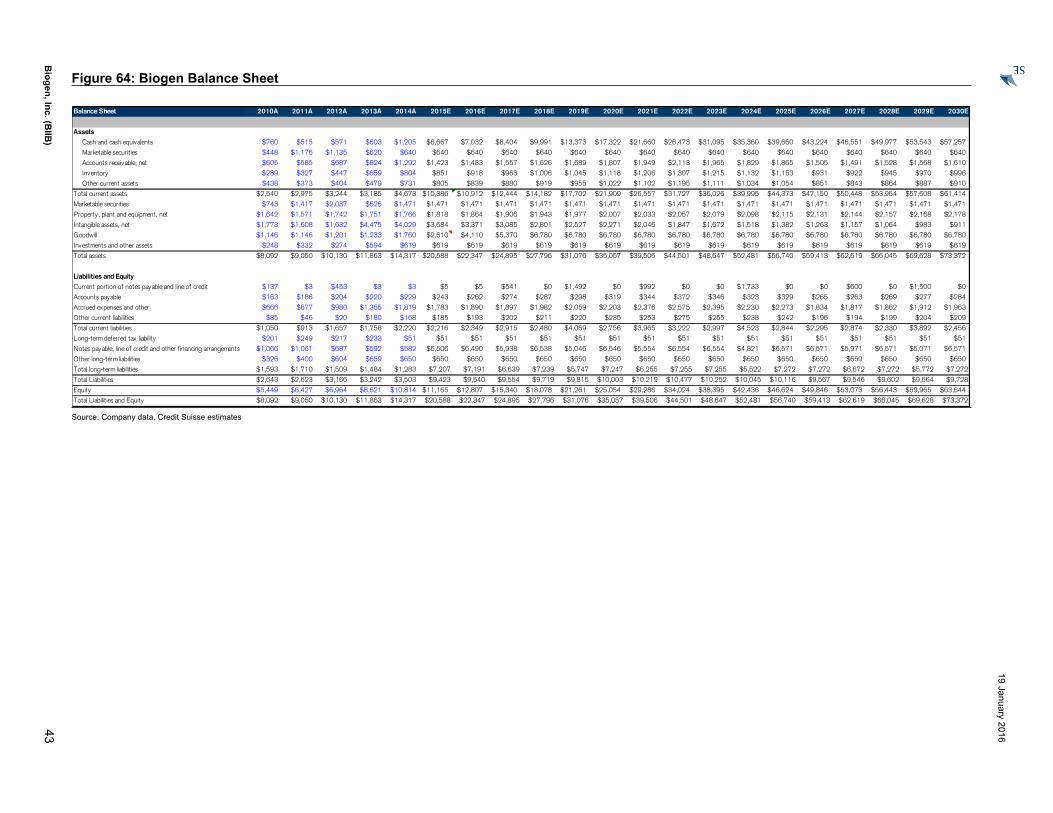

Biogen, Inc. (BIIB)Price (15 Jan 2016): US$273.3; Rating: NEUTRAL; Target Price: US$322Income Statement 12/14A 12/15E 12/16E 12/17ERevenue (US$ m) 9,703.3 10,682.8 11,136.7 11,686.7EBITDA 4,661 5,409 5,623 5,946Depr. & amort. (688) (542) (517) (495)EBIT (US$) 3,972 4,867 5,106 5,451Net interest exp (17) (62) (191) (151)Associates 0 0 0 0Other adj. (8) (31) 0 0PBT (US$) 3,947 4,773 4,915 5,300Income taxes (990) (1,180) (1,229) (1,325)Profit after tax 2,957 3,593 3,687 3,975Minorities - - - -Preferred dividends - - - -Associates & other (22) (62) 0 0Net profit (US$) 2,935 3,531 3,687 3,975Other NPAT adjustments 7 49 0 0Reported net income 2,942 3,580 3,687 3,975Cash Flow 12/14A 12/15E 12/16E 12/17EEBIT 3,972 4,867 5,106 5,451Net interest (17) (62) (191) (151)Cash taxes paid - - - -Change in working capital (484) (257) (28) (130)Other cash & non-cash items (529) (682) (712) (830)Cash flow from operations 2,942 3,866 4,175 4,340CAPEX (288) (250) (250) (250)Free cashflow to the firm 2,654 3,616 3,925 4,090Aquisitions 0 0 0 0Divestments - - - -Other investment/(outflows) (1,255) (850) (1,500) (1,260)Cash flow from investments (1,543) (1,100) (1,750) (1,510)Net share issue(/repurchase) (832) (3,230) (2,044) (1,442)Dividends paid 0 0 0 0Issuance (retirement) of debt (3) 5,926 (16) (16)Other 89 (5,926) 16 16Cashflow from financing activities (745) (3,230) (2,044) (1,442)Effect of exchange rates (41) 0 0 0Changes in Net Cash/Debt 613 (464) 381 1,388Net debt at start (7) (620) (156) (537)Change in net debt (613) 464 (381) (1,388)Net debt at end (620) (156) (537) (1,925)Balance Sheet (US$) 12/14A 12/15E 12/16E 12/17EAssetsCash & cash equivalents 1,205 6,667 7,032 8,404Account receivables 1,292 1,423 1,483 1,557Inventory 804 851 918 963Other current assets 1,371 1,445 1,479 1,521Total current assets 4,673 10,386 10,912 12,444Total fixed assets 1,766 1,818 1,864 1,906Intangible assets and goodwill 5,789 6,294 7,481 8,455Investment securities - - - -Other assets 2,089 2,089 2,089 2,089Total assets 14,317 20,588 22,347 24,895LiabilitiesAccounts payables 229 243 262 274Short-term debt 0 0 0 0Other short term liabilities 1,991 1,974 2,088 2,641Total current liabilities 2,220 2,216 2,349 2,915Long-term debt 582 6,506 6,490 5,938Other liabilities 701 701 701 701Total liabilities 3,503 9,423 9,540 9,554Shareholder equity 10,814 11,165 12,807 15,340Minority interests - - - -Total liabilities and equity 14,317 20,588 22,347 24,895Net debt (620) (156) (537) (1,925)

Per share 12/14A 12/15E 12/16E 12/17ENo. of shares (wtd avg) 237 232 223 219CS adj. EPS 13.83 16.76 17.75 19.43Prev. EPS (US$)Dividend (US$) 0.00 0.00 0.00 0.00Dividend payout ratio 0.00 0.00 0.00 0.00Free cash flow per share 11.19 15.57 17.57 18.67Earnings 12/14A 12/15E 12/16E 12/17ESales growth (%) 40.0 10.1 4.2 4.9EBIT growth (%) 57.9 22.5 4.9 6.8Net profit growth (%) 57.6 20.3 4.4 7.8EPS growth (%) 54.3 21.1 6.0 9.4EBITDA margin (%) 48.0 50.6 50.5 50.9EBIT margin (%) 40.9 45.6 45.8 46.6Pretax margin (%) 40.7 44.7 44.1 45.4Net margin (%) 30.2 33.1 33.1 34.0Valuation 12/14A 12/15E 12/16E 12/17EEV/Sales (x) 6.22 5.69 5.42 5.05EV/EBITDA (x) 12.9 11.2 10.7 9.9EV/EBIT (x) 15.2 12.5 11.8 10.8P/E (x) 19.8 16.3 15.4 14.1Price to book (x) 6.0 5.6 4.8 3.9Asset turnover 0.7 0.5 0.5 0.5Returns 12/14A 12/15E 12/16E 12/17EROE stated-return on (%) 30.3 32.6 30.8 28.2ROIC (%) 0.3 0.3 0.3 0.3Interest burden (%) 0.99 0.98 0.96 0.97Tax rate (%) 25.1 24.7 25.0 25.0Financial leverage (%) 0.05 0.58 0.51 0.42Gearing 12/14A 12/15E 12/16E 12/17ENet debt/equity (%) (5.7) (1.4) (4.2) (12.5)Net Debt to EBITDA (x) Net

CashNet

CashNet

CashNet

CashInterest coverage ratio (X) 229.6 78.1 26.8 36.2Quarterly EPS Q1 Q2 Q3 Q42014A 2.02 3.05 3.61 3.742015E 3.48 3.92 4.38 3.602016E 4.14 4.00 4.13 4.22

Share price performance

BIIB.O Q S& P 5 0 0 IN D EX

A p r - 1 5 Ju l - 1 5 O ct - 1 5 Jan - 1 62 0 0

3 0 0

4 0 0

5 0 0

On 15-Jan-2016 the S&P 500 INDEX closed at 1880.33Daily Jan16, 2015 - Jan15, 2016, 01/16/15 = US$352.75

Source: Company data, Thomson Reuters, Credit Suisse estimates

19 January 2016

Biogen, Inc. (BIIB) 3

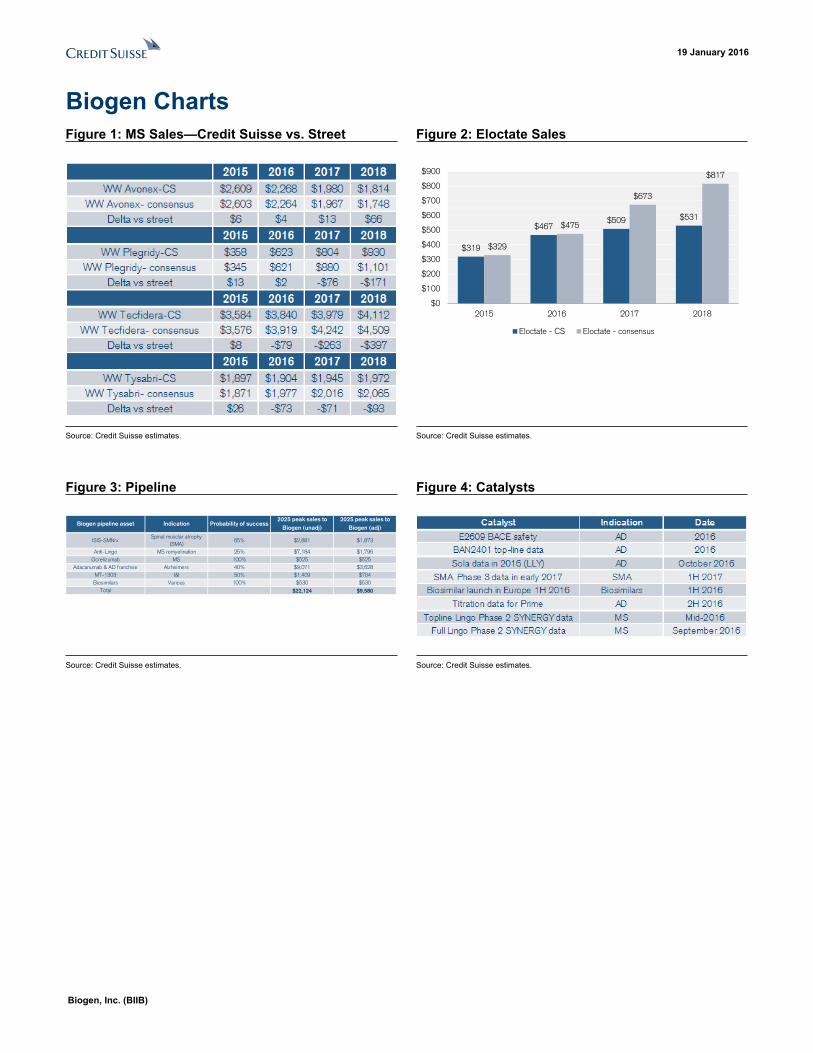

Biogen ChartsFigure 1: MS Sales—Credit Suisse vs. Street Figure 2: Eloctate Sales

$319

$467$509 $531

$329

$475

$673

$817

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2015 2016 2017 2018

Eloctate - CS Eloctate - consensus

Source: Credit Suisse estimates. Source: Credit Suisse estimates.

Figure 3: Pipeline Figure 4: Catalysts

Biogen pipeline asset Indication Probability of success2025 peak sales to

Biogen (unadj)2025 peak sales to

Biogen (adj)

ISIS-SMNrxSpinal musclar atrophy

(SMA)65% $2,881 $1,873

Anti-Lingo MS remyelination 25% $7,184 $1,796 Ocrelizumab MS 100% $525 $525

Adacanumab & AD franchise Alzheimers 40% $9,071 $3,628 MT-1303 I&I 50% $1,409 $704 Biosimilars Various 100% $530 $530

Total $22,124 $9,580

Source: Credit Suisse estimates. Source: Credit Suisse estimates.

19 January 2016

Biogen, Inc. (BIIB) 4

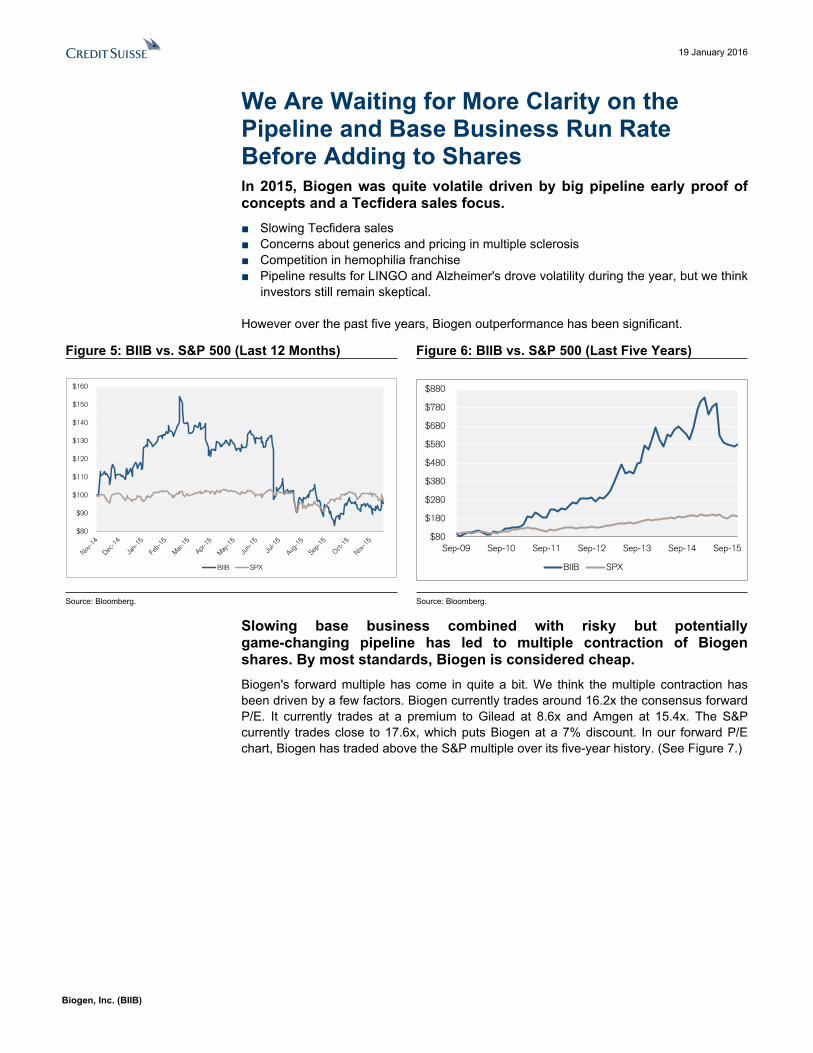

We Are Waiting for More Clarity on the Pipeline and Base Business Run Rate Before Adding to SharesIn 2015, Biogen was quite volatile driven by big pipeline early proof of concepts and a Tecfidera sales focus. ■ Slowing Tecfidera sales■ Concerns about generics and pricing in multiple sclerosis■ Competition in hemophilia franchise■ Pipeline results for LINGO and Alzheimer's drove volatility during the year, but we think

investors still remain skeptical.

However over the past five years, Biogen outperformance has been significant.

Figure 5: BIIB vs. S&P 500 (Last 12 Months) Figure 6: BIIB vs. S&P 500 (Last Five Years)

$80

$90

$100

$110

$120

$130

$140

$150

$160

BIIB SPX

$80

$180

$280

$380

$480

$580

$680

$780

$880

Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15

BIIB SPX

Source: Bloomberg. Source: Bloomberg.

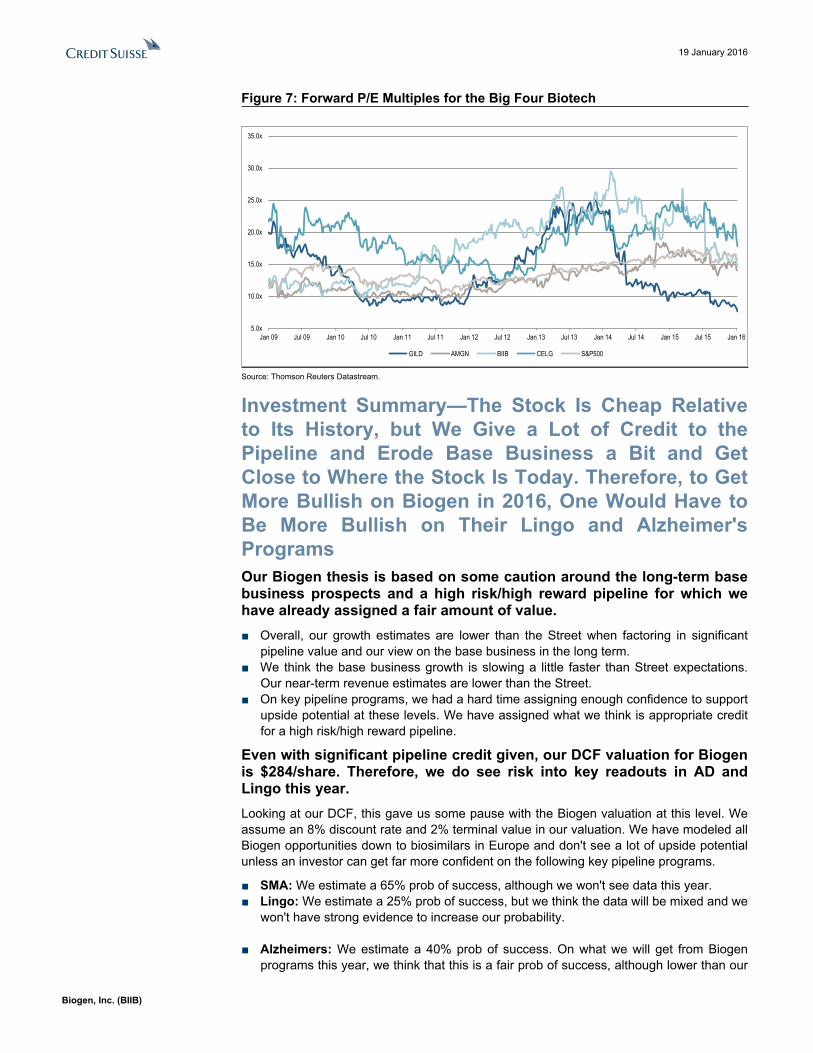

Slowing base business combined with risky but potentially game-changing pipeline has led to multiple contraction of Biogen shares. By most standards, Biogen is considered cheap.Biogen's forward multiple has come in quite a bit. We think the multiple contraction has been driven by a few factors. Biogen currently trades around 16.2x the consensus forward P/E. It currently trades at a premium to Gilead at 8.6x and Amgen at 15.4x. The S&P currently trades close to 17.6x, which puts Biogen at a 7% discount. In our forward P/E chart, Biogen has traded above the S&P multiple over its five-year history. (See Figure 7.)

19 January 2016

Biogen, Inc. (BIIB) 5

Figure 7: Forward P/E Multiples for the Big Four Biotech

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

35.0x

Jan 09 Jul 09 Jan 10 Jul 10 Jan 11 Jul 11 Jan 12 Jul 12 Jan 13 Jul 13 Jan 14 Jul 14 Jan 15 Jul 15 Jan 16

GILD AMGN BIIB CELG S&P500

Source: Thomson Reuters Datastream.

Investment Summary—The Stock Is Cheap Relative to Its History, but We Give a Lot of Credit to the Pipeline and Erode Base Business a Bit and Get Close to Where the Stock Is Today. Therefore, to Get More Bullish on Biogen in 2016, One Would Have to Be More Bullish on Their Lingo and Alzheimer's Programs Our Biogen thesis is based on some caution around the long-term base business prospects and a high risk/high reward pipeline for which we have already assigned a fair amount of value.■ Overall, our growth estimates are lower than the Street when factoring in significant

pipeline value and our view on the base business in the long term.■ We think the base business growth is slowing a little faster than Street expectations.

Our near-term revenue estimates are lower than the Street. ■ On key pipeline programs, we had a hard time assigning enough confidence to support

upside potential at these levels. We have assigned what we think is appropriate credit for a high risk/high reward pipeline.

Even with significant pipeline credit given, our DCF valuation for Biogen is $284/share. Therefore, we do see risk into key readouts in AD and Lingo this year.Looking at our DCF, this gave us some pause with the Biogen valuation at this level. We assume an 8% discount rate and 2% terminal value in our valuation. We have modeled all Biogen opportunities down to biosimilars in Europe and don't see a lot of upside potential unless an investor can get far more confident on the following key pipeline programs.

■ SMA: We estimate a 65% prob of success, although we won't see data this year.■ Lingo: We estimate a 25% prob of success, but we think the data will be mixed and we

won't have strong evidence to increase our probability.

■ Alzheimers: We estimate a 40% prob of success. On what we will get from Biogen programs this year, we think that this is a fair prob of success, although lower than our

19 January 2016

Biogen, Inc. (BIIB) 6

typical 65-75% for a Phase 3 program. However, Lilly Solanezumab data is a big catalyst in October since there is a likely read-through to be made.

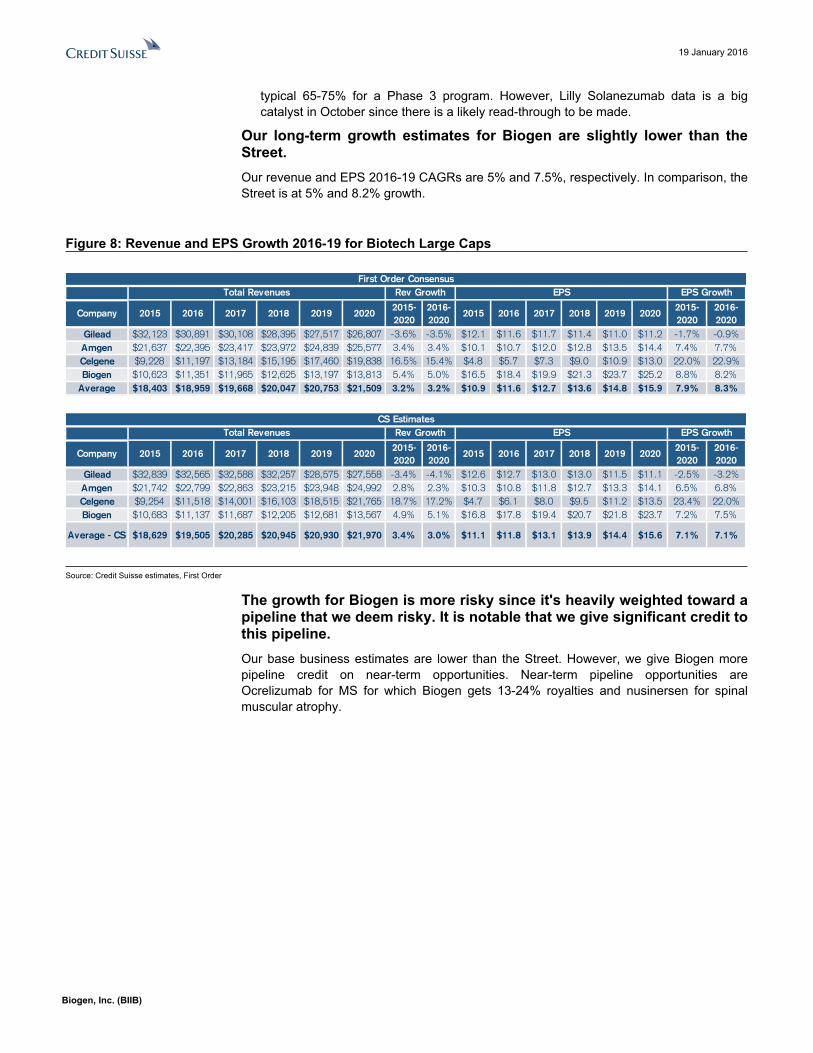

Our long-term growth estimates for Biogen are slightly lower than the Street.Our revenue and EPS 2016-19 CAGRs are 5% and 7.5%, respectively. In comparison, the Street is at 5% and 8.2% growth.

Figure 8: Revenue and EPS Growth 2016-19 for Biotech Large Caps

Company 2015 2016 2017 2018 2019 20202015-2020

2016-2020

2015 2016 2017 2018 2019 20202015-2020

2016-2020

Gilead $32,123 $30,891 $30,108 $28,395 $27,517 $26,807 -3.6% -3.5% $12.1 $11.6 $11.7 $11.4 $11.0 $11.2 -1.7% -0.9%Amgen $21,637 $22,395 $23,417 $23,972 $24,839 $25,577 3.4% 3.4% $10.1 $10.7 $12.0 $12.8 $13.5 $14.4 7.4% 7.7%Celgene $9,228 $11,197 $13,184 $15,195 $17,460 $19,838 16.5% 15.4% $4.8 $5.7 $7.3 $9.0 $10.9 $13.0 22.0% 22.9%Biogen $10,623 $11,351 $11,965 $12,625 $13,197 $13,813 5.4% 5.0% $16.5 $18.4 $19.9 $21.3 $23.7 $25.2 8.8% 8.2%

Average $18,403 $18,959 $19,668 $20,047 $20,753 $21,509 3.2% 3.2% $10.9 $11.6 $12.7 $13.6 $14.8 $15.9 7.9% 8.3%

EPSRev Growth EPS GrowthTotal RevenuesFirst Order Consensus

Company 2015 2016 2017 2018 2019 20202015-2020

2016-2020

2015 2016 2017 2018 2019 20202015-2020

2016-2020

Gilead $32,839 $32,565 $32,588 $32,257 $28,575 $27,558 -3.4% -4.1% $12.6 $12.7 $13.0 $13.0 $11.5 $11.1 -2.5% -3.2%Amgen $21,742 $22,799 $22,863 $23,215 $23,948 $24,992 2.8% 2.3% $10.3 $10.8 $11.8 $12.7 $13.3 $14.1 6.5% 6.8%Celgene $9,254 $11,518 $14,001 $16,103 $18,515 $21,765 18.7% 17.2% $4.7 $6.1 $8.0 $9.5 $11.2 $13.5 23.4% 22.0%Biogen $10,683 $11,137 $11,687 $12,205 $12,681 $13,567 4.9% 5.1% $16.8 $17.8 $19.4 $20.7 $21.8 $23.7 7.2% 7.5%

Average - CS $18,629 $19,505 $20,285 $20,945 $20,930 $21,970 3.4% 3.0% $11.1 $11.8 $13.1 $13.9 $14.4 $15.6 7.1% 7.1%

CS EstimatesTotal Revenues EPSRev Growth EPS Growth

Source: Credit Suisse estimates, First Order

The growth for Biogen is more risky since it's heavily weighted toward a pipeline that we deem risky. It is notable that we give significant credit to this pipeline.Our base business estimates are lower than the Street. However, we give Biogen more pipeline credit on near-term opportunities. Near-term pipeline opportunities are Ocrelizumab for MS for which Biogen gets 13-24% royalties and nusinersen for spinal muscular atrophy.

19 January 2016

Biogen, Inc. (BIIB) 7

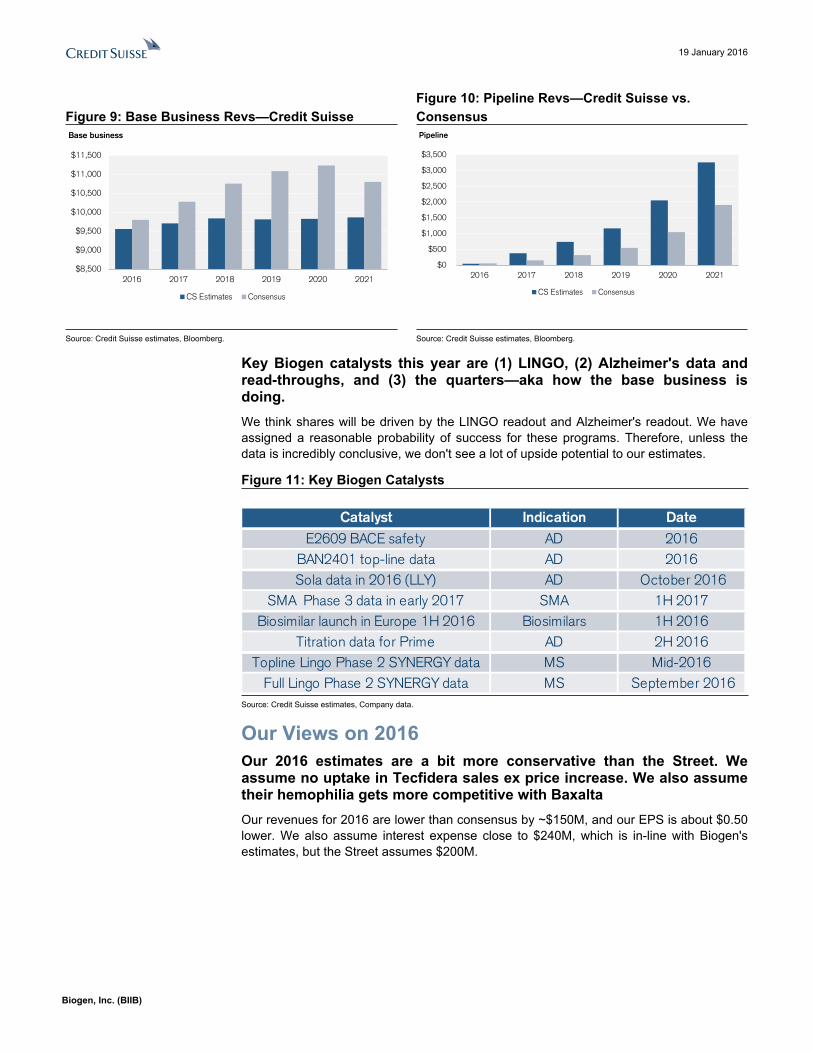

Figure 9: Base Business Revs—Credit Suisse Figure 10: Pipeline Revs—Credit Suisse vs. Consensus

$8,500

$9,000

$9,500

$10,000

$10,500

$11,000

$11,500

2016 2017 2018 2019 2020 2021

Base business

CS Estimates Consensus

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

2016 2017 2018 2019 2020 2021

Pipeline

CS Estimates Consensus

Source: Credit Suisse estimates, Bloomberg. Source: Credit Suisse estimates, Bloomberg.

Key Biogen catalysts this year are (1) LINGO, (2) Alzheimer's data and read-throughs, and (3) the quarters—aka how the base business is doing.We think shares will be driven by the LINGO readout and Alzheimer's readout. We have assigned a reasonable probability of success for these programs. Therefore, unless the data is incredibly conclusive, we don't see a lot of upside potential to our estimates.

Figure 11: Key Biogen Catalysts

Catalyst Indication DateE2609 BACE safety AD 2016

BAN2401 top-line data AD 2016Sola data in 2016 (LLY) AD October 2016

SMA Phase 3 data in early 2017 SMA 1H 2017Biosimilar launch in Europe 1H 2016 Biosimilars 1H 2016

Titration data for Prime AD 2H 2016Topline Lingo Phase 2 SYNERGY data MS Mid-2016

Full Lingo Phase 2 SYNERGY data MS September 2016Source: Credit Suisse estimates, Company data.

Our Views on 2016Our 2016 estimates are a bit more conservative than the Street. We assume no uptake in Tecfidera sales ex price increase. We also assume their hemophilia gets more competitive with BaxaltaOur revenues for 2016 are lower than consensus by ~$150M, and our EPS is about $0.50 lower. We also assume interest expense close to $240M, which is in-line with Biogen's estimates, but the Street assumes $200M.

19 January 2016

Biogen, Inc. (BIIB) 8

Figure 12: Total Revs—Credit Suisse vs. Consensus Figure 13: EPS—Credit Suisse vs. Consensus

$2,777

$2,738

$2,791

$2,831

$2,736

$2,808

$2,852

$2,888

$2,650

$2,700

$2,750

$2,800

$2,850

$2,900

1Q16E 2Q16E 3Q16E 4Q16E

Total revenues- CS Total revenues- consensus

$4.46

$4.32

$4.45

$4.54

$4.34$4.39

$4.58

$4.71

$4.10

$4.20

$4.30

$4.40

$4.50

$4.60

$4.70

$4.80

1Q16E 2Q16E 3Q16E 4Q16E

EPS - CS EPS- Consensus

Source: Credit Suisse estimates, Bloomberg. Source: Credit Suisse estimates, Bloomberg.

We still remain cautious on Biogen's core multiple sclerosis (MS) business over the next 12 months. Biogen's MS franchise still makes up 75% of revenues, so weaker-than-expected MS franchise sales is meaningful for Biogen shares.

We think that Street expectations may be too high for Tecfidera and Tysabri.■ Slower Tecfidera Growth than the Street: Biogen is making a significant investment

into direct-to-consumer campaigns to re-energize patient interest in Tecfidera following the new FDA label that contains a PML warning. We have been looking at IMS scripts, which have historically been a good predictor of Tecfidera oral pill trends. We have not seen an increase so far, although we note the holidays. We are about $260-400M under Street estimates in 2017 and 2018.

■ Slower Tysabri Growth than the Street: We expect Roche will file for Ocrelizumab in early 2016, which would set up for an early 2017 approval at the worst case. From our checks, doctors are very excited (as with many new MS) about Ocrelizumab. It is an IV therapy for MS. We think that Tysabri will experience competition from excitement around this launch starting in 2017. If the approval happens earlier than expected, there could be pressures on Tysabri earlier than expected.

19 January 2016

Biogen, Inc. (BIIB) 9

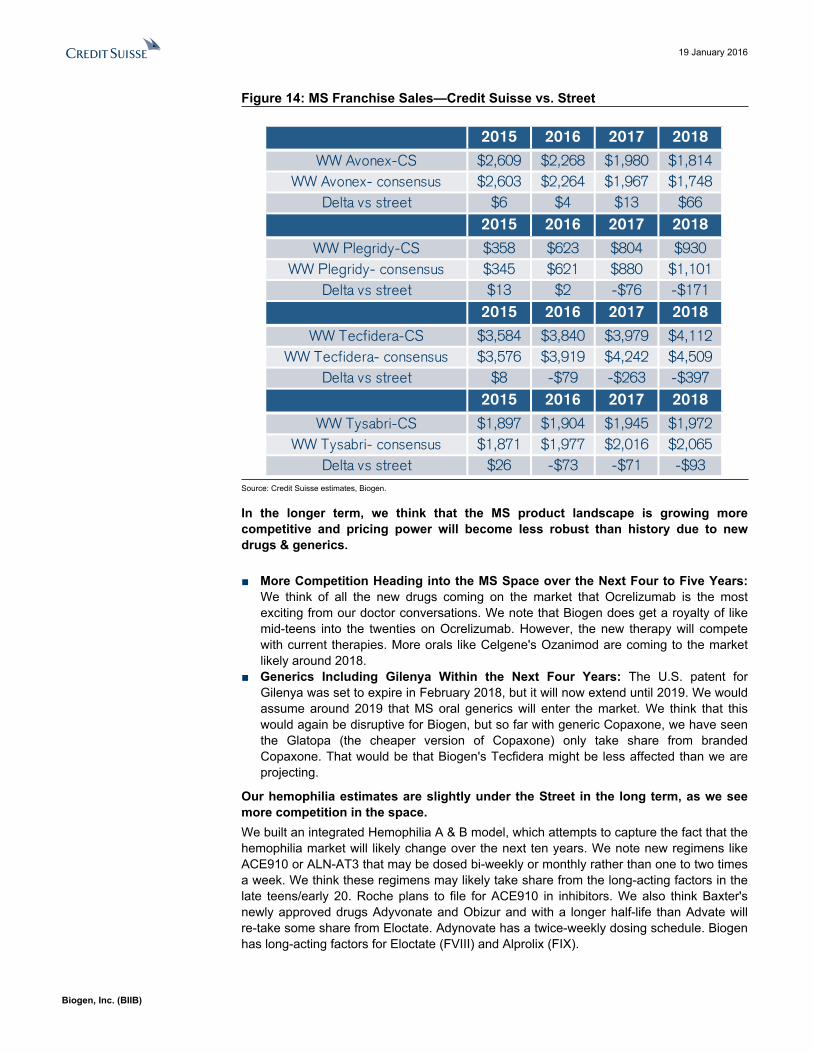

Figure 14: MS Franchise Sales—Credit Suisse vs. Street

2015 2016 2017 2018

WW Avonex-CS $2,609 $2,268 $1,980 $1,814WW Avonex- consensus $2,603 $2,264 $1,967 $1,748

Delta vs street $6 $4 $13 $662015 2016 2017 2018

WW Plegridy-CS $358 $623 $804 $930WW Plegridy- consensus $345 $621 $880 $1,101

Delta vs street $13 $2 -$76 -$1712015 2016 2017 2018

WW Tecfidera-CS $3,584 $3,840 $3,979 $4,112WW Tecfidera- consensus $3,576 $3,919 $4,242 $4,509

Delta vs street $8 -$79 -$263 -$3972015 2016 2017 2018

WW Tysabri-CS $1,897 $1,904 $1,945 $1,972WW Tysabri- consensus $1,871 $1,977 $2,016 $2,065

Delta vs street $26 -$73 -$71 -$93Source: Credit Suisse estimates, Biogen.

In the longer term, we think that the MS product landscape is growing more competitive and pricing power will become less robust than history due to new drugs & generics.

■ More Competition Heading into the MS Space over the Next Four to Five Years: We think of all the new drugs coming on the market that Ocrelizumab is the most exciting from our doctor conversations. We note that Biogen does get a royalty of like mid-teens into the twenties on Ocrelizumab. However, the new therapy will compete with current therapies. More orals like Celgene's Ozanimod are coming to the market likely around 2018.

■ Generics Including Gilenya Within the Next Four Years: The U.S. patent for Gilenya was set to expire in February 2018, but it will now extend until 2019. We would assume around 2019 that MS oral generics will enter the market. We think that this would again be disruptive for Biogen, but so far with generic Copaxone, we have seen the Glatopa (the cheaper version of Copaxone) only take share from branded Copaxone. That would be that Biogen's Tecfidera might be less affected than we are projecting.

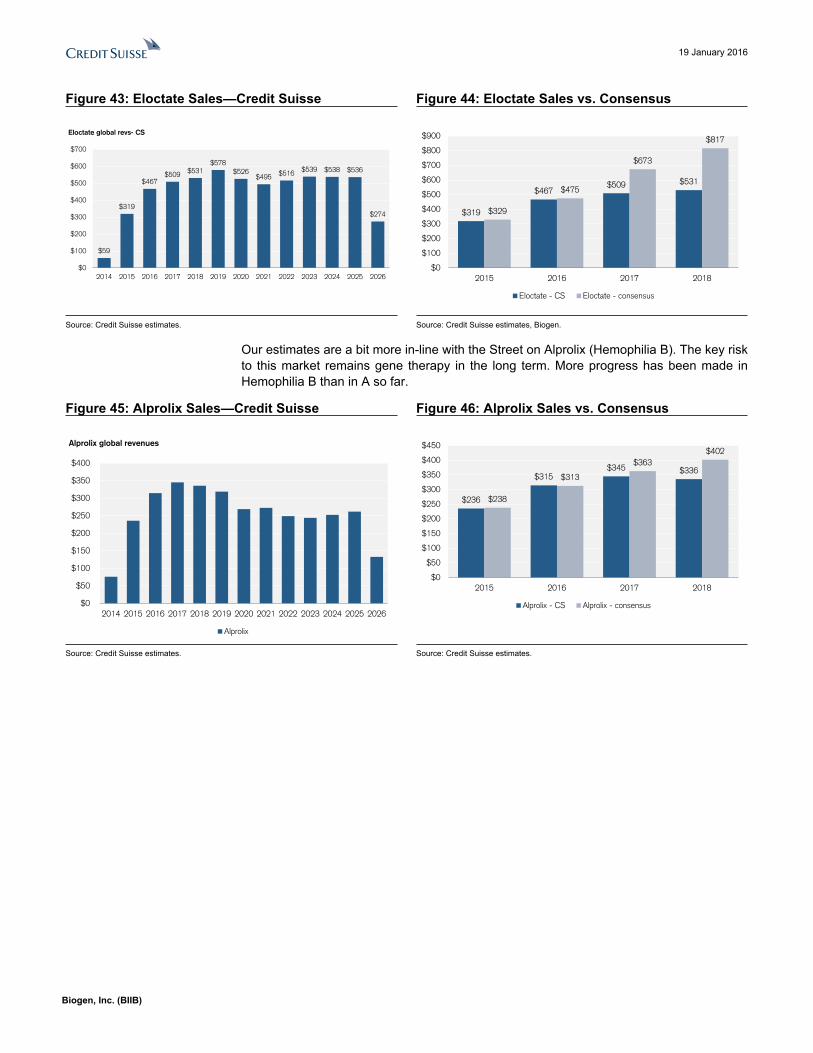

Our hemophilia estimates are slightly under the Street in the long term, as we see more competition in the space.We built an integrated Hemophilia A & B model, which attempts to capture the fact that the hemophilia market will likely change over the next ten years. We note new regimens like ACE910 or ALN-AT3 that may be dosed bi-weekly or monthly rather than one to two times a week. We think these regimens may likely take share from the long-acting factors in the late teens/early 20. Roche plans to file for ACE910 in inhibitors. We also think Baxter's newly approved drugs Adyvonate and Obizur and with a longer half-life than Advate will re-take some share from Eloctate. Adynovate has a twice-weekly dosing schedule. Biogen has long-acting factors for Eloctate (FVIII) and Alprolix (FIX).

19 January 2016

Biogen, Inc. (BIIB) 10

Figure 15: Eloctate Revs—Credit Suisse vs. Consensus Figure 16: Alprolix—Credit Suisse vs. Consensus

$319

$467$509 $531

$329

$475

$673

$817

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2015 2016 2017 2018

Eloctate - CS Eloctate - consensus

$236

$315$345 $336

$238

$313

$363$402

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2015 2016 2017 2018

Alprolix - CS Alprolix - consensus

Source: Credit Suisse estimates, Biogen. Source: Credit Suisse estimates, Biogen.

Biogen's Pipeline—We Are Skeptical, So It's Hard for Us to Be More Bullish Here on Biogen SharesOur pipeline assumptions add $134/share to our Biogen DCF.We think the pipeline is very risky, and ultimately, we think to be bullish on Biogen shares here, we would need to assign more probability of success to many of their big market opportunities in Alzheimer's and Lingo. We currently assign value to their SMA program; Ocrelizumab; MT-1303, their S1P1 drug; and biosimilars in Europe.

Figure 17: Biogen Pipeline Assumptions—Credit Suisse

Biogen pipeline asset Indication Probability of success2025 peak sales to

Biogen (unadj)2025 peak sales to

Biogen (adj)

ISIS-SMNrxSpinal musclar atrophy

(SMA)65% $2,881 $1,873

Anti-Lingo MS remyelination 25% $7,184 $1,796 Ocrelizumab MS 100% $525 $525

Adacanumab & AD franchise Alzheimers 40% $9,071 $3,628 MT-1303 I&I 50% $1,409 $704 Biosimilars Various 100% $530 $530

Total $22,124 $9,580

Source: Credit Suisse estimates.

Biogen's two lead pipeline opportunities are the Alzheimer's franchise and the anti-Lingo franchise. In our DCF valuation, we have $100/share baked in for Lingo and Alzheimers. We would say the pipeline is mostly a free call option.We would slightly disagree with the statement that Biogen's pipeline is a completely free call option. We think investors likely have a ~25% probability assigned to these two programs, which could conceptually be over $5B products. We definitely think there is downside risk to shares if the MS Lingo program does not move forward. Based on us assigning a 25% probability of success, perhaps if the MS Lingo study is wildly successful, investors would assign 40-50%. We think it would be hard to be over 50% confident moving into Phase 3 of this program.

19 January 2016

Biogen, Inc. (BIIB) 11

We assume Lingo and the Alzheimer's franchises are worth ~$8B and ~$9B in 2025. These are the company's two biggest shots on goal, hence all the attention from the Street and investors.We assume a 25% probability of success on $7B peak revenues for Lingo and 40% probability of success on $7B peak revenues for the Alzheimer's (AD) franchise. If we assumed 100% success to Lingo and Alzheimers, our Biogen valuation is $488/share.

Figure 18: Lingo Sales—Credit Suisse Figure 19: AD Franchise Sales—Credit Suisse

$432$1,229

$2,221

$3,737

$5,355

$7,184$7,966$8,242$8,528$8,822$9,126

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

BIIB-33 revenues

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

AD US AD-ex-US

Source: Credit Suisse estimates. Source: Credit Suisse estimates.

For Alzheimer's, it was hard for us to assign a typical Ph3 probability of success like 65-75%. We assign 40%, but read-through on Sola may increase probability if that works. Alzheimer's Program: Biogen's lead asset is aducanumab (an anti-amyloid Beta agent). We think the data that has emerged so far from the Prime study for aducanumab is encouraging that the drug has activity. We think it looks potentially to be the most potent. Our checks agreed with our view. Lilly Phase 3 data on Solanezumab (another anti-Amyloid Beta) could also drive some Biogen upside if that data works.

For Lingo, we assign a 25% probability of success. We are not sure if Synergy is going to show the definitive evidence, but we believe the programs continue forward after Synergy.Biogen has a pivotal moment on the Lingo program in 2016 with the Synergy program in MS patients. They are studying in a Phase 2 program Anti-Lingo1 with Avonex. Our checks have been skeptical about the program working on its primary endpoint, which is disability reduction. We could see some hints when considering the totality of the evidence. We think 25% fairly accounts for what we expect to be some progress this year with the Lingo program but not definitive evidence.

Data for nusinersen likely reads out in early 2017. We don't think that the drug gets approved by the FDA earlier than mid-2H 2017. SMA is worth ~$50/share at 100% success (we assume 65%)We know that IONS and Biogen are working with the regulators to see if nusinersen might be able to get to market faster for such a devastating disease as SMA. We are assuming that the drug comes to market in early 2017, so a faster outcome is upside to our estimates. We think there is clear proof of biology and concept with the Phase 1&2 study. The biggest risk is clinical for this program and showing a benefit in Phase 3. We do wonder (from looking at DMD) if there might be a clinical path if the Phase 3 studies fail. For now, we assume a 65% probability of success on ~$3B sales to Biogen in 2025.

19 January 2016

Biogen, Inc. (BIIB) 12

Biogen Valuation Our target price is $322 for Biogen. Like all four of our large caps, we are valuing Biogen shares using a DCF and a P/E multiple. We assign 50% to the DCF valuation and 50% to the P/E multiple valuation.

DCF: Our DCF valuation for Biogen is $284/share.We model cash flows out to 2029. We assign a 2% terminal growth rate, which is in-line with large-cap biotech companies with sustainable franchises. We assume an 8% discount rate, which is in-line with its large-cap peers (Gilead, Celgene, and Amgen).

P/E Multiple: Our forward P/E multiple valuation is $360/share. We estimate 2016 EPS of $17.75 (vs. consensus of $18.50). We assign a multiple of 20.3x to our 2016 EPS estimate. This multiple represents a 5% premium to the large-cap sector ex-Gilead and a 23% premium to the S&P 500. We believe that this multiple is justified due to Biogen's base business stability and several pipeline opportunities.

Risks to Our Neutral RatingKey Upside Risks■ Success (meaning hitting primary endpoint) on the anti-Lingo program in mid-2016■ Positive data that provides greater confidence around BAN2401 (anti-amyloid Beta

antibody)■ Tecfidera sales reaccelerate■ Hemophilia assets continue to take share in spite of competition■ SMA program gets to market earlier than our expectations through surprise regulatory

approval

Key Downside Risks ■ Anti-Lingo1 program discontinues after failure in Ph2 Synergy study■ Efficacy or safety concern with aducanumab Ph3 program■ Worse-than-expected MS and haemophilia sales during 2016■ SMA program has a surprise efficacy or safety failure in Ph3

19 January 2016

Biogen, Inc. (BIIB) 13

We Think There Are More Headwinds than Tailwinds When We Consider Biogen's MS FranchiseWe Built a Detailed Integrated MS Market Model for the U.S. and ROW That Captures All New and Current PlayersWe are more cautious on multiple sclerosis in the next years than the Street currently projects for the class. Our estimates are $150-600M under Street estimates over the next three years.We will discuss throughout this report many reasons why are cautious on the multiple sclerosis space. Since Biogen is a big player in the MS space, we are under Street estimates for many products. In particular, we are under estimates on Tecfidera and Tysabri. We think Avonex share does not erode as fast and are above consensus.

Figure 20: WW MS Sales—Credit Suisse Figure 21: Total MS Sales vs. Consensus

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

WW Avonex -CS WW Plegridy- CS WW Tecfidera- CS WW Tysabri- CS

$8,635$8,708

$8,828$8,781

$9,105

$9,423

$8,200

$8,400

$8,600

$8,800

$9,000

$9,200

$9,400

$9,600

2016 2017 2018

WW sales Tecfidera, Tysabri, Avonex, and Plegridy

WW Biogen MS franchise- CS WW Biogen MS franchise- Consensus

Source: Credit Suisse estimates. Source: Credit Suisse estimates, Biogen.

By Far, the Most Exciting New Drug Is Ocrelizumab in Speaking to the Doctor CommunityWe do think Ocrelizumab is a blockbuster with peak sales of $4B, but Biogen gets a royalty.Biogen gets a royalty from that program of 13-25% on U.S. sales only. We start off with a 14% royalty, and our peak rate is 22%. We may learn more from Biogen in 2016 about royalty rates in more detail. We would view royalty rates as potentially material to Biogen sales, and it sounds like the company views it the same way.

19 January 2016

Biogen, Inc. (BIIB) 14

Figure 22: Ocrelizumab Sales Figure 23: Royalties Paid to Biogen

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

Ocrelizumab sales

Ocrelizumab US

$8

$84

$219

$326 $380

$452 $487 $499 $512 $525 $538 $551 $564

$0

$100

$200

$300

$400

$500

$600

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

Ocra royalties to BIIB

Ocrelizumab Royalties to Biogen

Source: Credit Suisse estimates. Source: Credit Suisse estimates.

We think MS overall is becoming more competitive, which creates challenges for Biogen, given it still has a significant portion of revenues coming from multiple sclerosis. Over the next few years, we think the MS landscape will become more competitive with many new agents potentially coming to market

Figure 24: Key MS Drugs on Market or in Development

Injectables Orals Intravenous

Avonex Aubagio TysabriBetaseron/Betaferon Gilenya Lemtrada

Copaxone Tecfidera OcrelizumabRebif Laquinimod Zinbryta (daclizumab)

Extavia OzanimodPlegridy MT-1303

Glatopa (generic Copaxone) siponimod (BAF312)

Source: Credit Suisse, Company data.

Our sense is that decision making for MS patients is very doctor/patient specific.Many of the potent drugs like Tysabri have less safety. Some of the injectables like Avonex are deemed to have less efficacy but more safety. Roche recently showed a diagram of the MS market and where each drug fell on the risk/benefit profile.

19 January 2016

Biogen, Inc. (BIIB) 15

Figure 25: Risk/Benefit of MS Therapies Filed/on Market in 2016

Source: Company data.

We Are a Little More Conservative on Domination by the Orals Post-2020. We Think the Injectables and Ocrelizumab Will DominateInjectables (including Copaxone) still have over 50% of the market share, but we and the industry are expecting oral share to increase significantly over the next few years.One major reason for the increase is that more developers are making pills for the treatment of MS after Tecfidera's success. In the first full year of sales in 2014, Tecfidera was ~$3B globally. Gilenya by Novartis has also expanded the oral market.

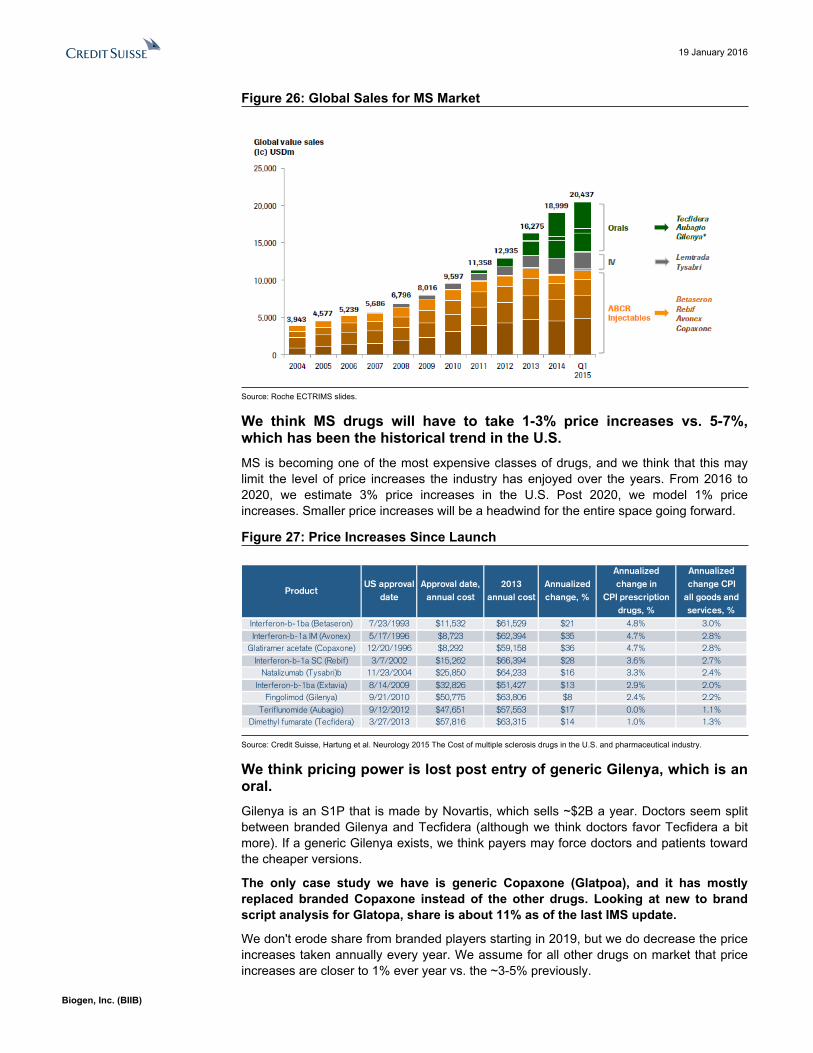

We Think Price Increases Seen in MS Will Decelerate in the Next Few Years. MS Is a Very Expensive Drug Class, and We Think Payers Are Beginning to Act with So Many DrugsMS is a $20B market in which Biogen has significant market share.Roche also projects that by 2020 multiple sclerosis is the third largest market behind type 2 diabetes and rheumatoid arthritis. Number four and five markets are breast cancer and HIV. Growing and big market opportunities attract a lot of competition, and this has been the case in MS.

19 January 2016

Biogen, Inc. (BIIB) 16

Figure 26: Global Sales for MS Market

Source: Roche ECTRIMS slides.

We think MS drugs will have to take 1-3% price increases vs. 5-7%, which has been the historical trend in the U.S.MS is becoming one of the most expensive classes of drugs, and we think that this may limit the level of price increases the industry has enjoyed over the years. From 2016 to 2020, we estimate 3% price increases in the U.S. Post 2020, we model 1% price increases. Smaller price increases will be a headwind for the entire space going forward.

Figure 27: Price Increases Since Launch

ProductUS approval

dateApproval date,

annual cost2013

annual costAnnualized change, %

Annualized change in

CPI prescription drugs, %

Annualized change CPI

all goods and services, %

Interferon-b-1ba (Betaseron) 7/23/1993 $11,532 $61,529 $21 4.8% 3.0%Interferon-b-1a IM (Avonex) 5/17/1996 $8,723 $62,394 $35 4.7% 2.8%

Glatiramer acetate (Copaxone) 12/20/1996 $8,292 $59,158 $36 4.7% 2.8%Interferon-b-1a SC (Rebif) 3/7/2002 $15,262 $66,394 $28 3.6% 2.7%

Natalizumab (Tysabri)b 11/23/2004 $25,850 $64,233 $16 3.3% 2.4%Interferon-b-1ba (Extavia) 8/14/2009 $32,826 $51,427 $13 2.9% 2.0%

Fingolimod (Gilenya) 9/21/2010 $50,775 $63,806 $8 2.4% 2.2%Teriflunomide (Aubagio) 9/12/2012 $47,651 $57,553 $17 0.0% 1.1%

Dimethyl fumarate (Tecfidera) 3/27/2013 $57,816 $63,315 $14 1.0% 1.3%

Source: Credit Suisse, Hartung et al. Neurology 2015 The Cost of multiple sclerosis drugs in the U.S. and pharmaceutical industry.

We think pricing power is lost post entry of generic Gilenya, which is an oral.Gilenya is an S1P that is made by Novartis, which sells ~$2B a year. Doctors seem split between branded Gilenya and Tecfidera (although we think doctors favor Tecfidera a bit more). If a generic Gilenya exists, we think payers may force doctors and patients toward the cheaper versions.

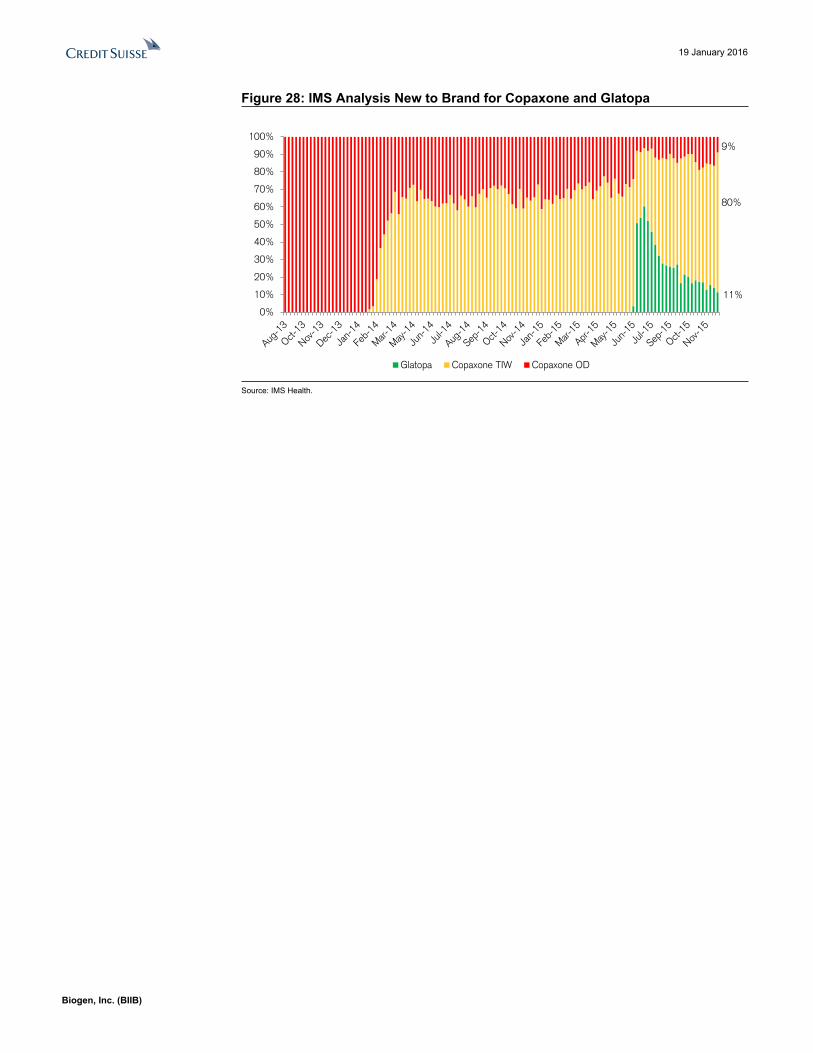

The only case study we have is generic Copaxone (Glatpoa), and it has mostly replaced branded Copaxone instead of the other drugs. Looking at new to brand script analysis for Glatopa, share is about 11% as of the last IMS update.

We don't erode share from branded players starting in 2019, but we do decrease the price increases taken annually every year. We assume for all other drugs on market that price increases are closer to 1% ever year vs. the ~3-5% previously.

19 January 2016

Biogen, Inc. (BIIB) 17

Figure 28: IMS Analysis New to Brand for Copaxone and Glatopa

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Glatopa Copaxone TIW Copaxone OD

9%

80%

11%

Source: IMS Health.

19 January 2016

Biogen, Inc. (BIIB) 18

We Think Tecfidera Is Stable for the Next Couple Years at ~$4B, but We Don't See Meaningful Share UptakeWe think Tecfidera sales grow mostly from price increases in the U.S going forwardWe assume market shares were at their highest in 2015 and start to come down in the coming years. In the U.S., we think there are some pricing pressures that are starting to emerge around MS. We think Street numbers still need to come down a little bit over the near- and long-term

Figure 29: Tecfidera Sales—Credit Suisse Figure 30: Tecfidera Annual Market Share

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

Total Tecfidera revs -CS

$3,840 $3,979 $4,112 $4,098 $4,224$3,919

$4,242$4,509 $4,584 $4,617

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

2016 2017 2018 2019 2020

Global Tecfidera Revs

WW Tecfidera revenues -CS WW Tecfidera - Consensus

Source: Credit Suisse estimates. Source: Credit Suisse estimates.

We assume Tecfidera has a flat market share in 2016 but remains the dominant oral regimen during the branded era.From looking at IMS scripts, we think share is remaining consistent at 19-20% for Tecfidera.

Figure 31: Weekly Trx Market Share Since Tecfidera Launch

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Tecfidera

Aubagio

Gilenya

Tysabri

Lemtrada

Rebif

Plegridy

Extavia

Betaseron

Avonex

Glatopa

Copaxone OD

11%

6%

23%

7%

9%

20%

13%

2%

2%

ABCRs60%

Orals37%

88%

12%

4%

Source: IMS Health.

19 January 2016

Biogen, Inc. (BIIB) 19

We estimate that Biogen pays ~$1B in cash for 2016, 2017, and 2018 to Fumapharm for Tecfidera salesIn speaking to Biogen, roughly every $1B in Tecfidera sales is about $300M in cash paid to Fumapharma. Cash is paid to Fumapharma until Tecfidera sells a cumulative $20B globally. We estimate that happens in 2019. This cash outflow is subtracted from our discounted cash flow analysis.

Why We Are More Conservative on Tecfidera? Doc Checks and ScriptsOur doc checks around Tecfidera suggested similar trends that we are modeling. Two main issues are GI and worries about PML.Our doc checks support our modeling assumption that market share likely peaked in 1H 2015. In the general community prescriber mind, we think that GI issues and PML still worry doctors.

Gastrointestinal (GI):

Tecfidera is an oral dimethyl fumerate, which has been used in psoriasis in Germany for well over ten years. GI side effects are known of the class and were seen in Biogen's Phase 3 clinical trials.

PML Cases:

We have seen some cases of PML with Tecfidera, which led to the FDA updating the label in late November 2014. From our doc checks, we think that this issue remains a concern for non-academic treating MS doctors. Even with the academic KOLs, they are certain more PML cases will emerge, which does not bother them unless the PML was seen in patients that did not have severe lymphopenia.

Figure 32: History of PML Tecfidera Cases

Date EventOctober 22, 2014 First case of PML reported

November 25, 2014FDA releases safety announcement

about 1st PML case, and subsequent label change, with Tecfidera

July 16th, 2015Second PML case reported in patient

with severe lymphopenia

September 21st, 2015Third PML case reported in patient with

severe lymphopenia

November 11th, 2015Fourth PML case reported in patient

with moderate lymphopeniaSource: Credit Suisse, Company data.

From looking at scripts for Tecfidera, we don't see much acceleration yet, although November and December are holiday months.Biogen is running a pretty robust direct-to-consumer campaign. We think the best way to see if Biogen is getting results is to just track the weekly scripts.

19 January 2016

Biogen, Inc. (BIIB) 20

Figure 33: Weekly Trx Ramp for Key MS Drugs Post Launch

0

2,000

4,000

6,000

8,000

10,000

12,000

1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 61 65 69 73 77 81 85 89 93 97 101

105

109

113

117

121

125

129

133

137

141

Tecfidera Gilenya Aubagio Plegridy Glatopa Copaxone TIW

8,989

3,404

2,380

965759

10,273

Source: Credit Suisse, IMS Health.

IMS analysis suggests loss of share in new to brand, both from less switches and a lower share of new starts. NBRx (new to brand) measures the scripts of patients that are first-time users of the drug. Since this measures the patients at the margin (those switching drugs or new starts), we view NBRx as an important leading indicator for scripts.

Conclusions of Our Analysis:■ Declining NBRx share, both from declining share of new starts (NTS) and switches ■ TRx volumes flattening out as a result of declining share in new patients

Figure 34: NBRx Weekly Tecfidera Share

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013

/11/

29…

2013

/12/

20…

2014

/01/

10…

2014

/01/

31…

2014

/02/

21…

2014

/03/

14…

2014

/04/

04…

2014

/04/

25…

2014

/05/

16…

2014

/06/

06…

2014

/06/

27…

2014

/07/

18…

2014

/08/

08…

2014

/08/

29…

2014

/09/

19…

2014

/10/

10…

2014

/10/

31…

2014

/11/

21…

2014

/12/

12…

2015

/01/

02…

2015

/01/

23…

2015

/02/

13…

2015

/03/

06…

2015

/03/

27…

2015

/04/

17…

2015

/05/

08…

2015

/05/

29…

2015

/06/

19…

2015

/07/

10…

2015

/07/

31…

2015

/08/

21…

2015

/09/

11…

2015

/10/

02…

2015

/10/

23…

2015

/11/

13…

2015

/12/

04…

NBRx Market Share

Tecfidera Gilenya Aubagio

Source: IMS.

19 January 2016

Biogen, Inc. (BIIB) 21

Figure 35: Switch Market Share Figure 36: NTS Market Share

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013

/11/

29…

2013

/12/

13…

2013

/12/

27…

2014

/01/

10…

2014

/01/

24…

2014

/02/

07…

2014

/02/

21…

2014

/03/

07…

2014

/03/

21…

2014

/04/

04…

2014

/04/

18…

2014

/05/

02…

2014

/05/

16…

2014

/05/

30…

2014

/06/

13…

2014

/06/

27…

2014

/07/

11…

2014

/07/

25…

2014

/08/

08…

2014

/08/

22…

2014

/09/

05…

2014

/09/

19…

2014

/10/

03…

2014

/10/

17…

2014

/10/

31…

2014

/11/

14…

2014

/11/

28…

2014

/12/

12…

2014

/12/

26…

2015

/01/

09…

2015

/01/

23…

2015

/02/

06…

2015

/02/

20…

2015

/03/

06…

2015

/03/

20…

2015

/04/

03…

2015

/04/

17…

2015

/05/

01…

2015

/05/

15…

2015

/05/

29…

2015

/06/

12…

2015

/06/

26…

2015

/07/

10…

2015

/07/

24…

2015

/08/

07…

2015

/08/

21…

2015

/09/

04…

2015

/09/

18…

2015

/10/

02…

2015

/10/

16…

2015

/10/

30…

2015

/11/

13…

2015

/11/

27…

Switch / Add Rx Market Share

Tecfidera Gilenya Aubagio

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013

/11/

29…

2013

/12/

20…

2014

/01/

10…

2014

/01/

31…

2014

/02/

21…

2014

/03/

14…

2014

/04/

04…

2014

/04/

25…

2014

/05/

16…

2014

/06/

06…

2014

/06/

27…

2014

/07/

18…

2014

/08/

08…

2014

/08/

29…

2014

/09/

19…

2014

/10/

10…

2014

/10/

31…

2014

/11/

21…

2014

/12/

12…

2015

/01/

02…

2015

/01/

23…

2015

/02/

13…

2015

/03/

06…

2015

/03/

27…

2015

/04/

17…

2015

/05/

08…

2015

/05/

29…

2015

/06/

19…

2015

/07/

10…

2015

/07/

31…

2015

/08/

21…

2015

/09/

11…

2015

/10/

02…

2015

/10/

23…

2015

/11/

13…

2015

/12/

04…

NTSRx Market Share

Tecfidera Gilenya Aubagio

Source: IMS Health. Source: IMS Health.

Figure 37: Week Tecfidera TRx

2,000

4,000

6,000

8,000

10,000

12,000

2013

/11/

29…

2013

/12/

20…

2014

/01/

10…

2014

/01/

31…

2014

/02/

21…

2014

/03/

14…

2014

/04/

04…

2014

/04/

25…

2014

/05/

16…

2014

/06/

06…

2014

/06/

27…

2014

/07/

18…

2014

/08/

08…

2014

/08/

29…

2014

/09/

19…

2014

/10/

10…

2014

/10/

31…

2014

/11/

21…

2014

/12/

12…

2015

/01/

02…

2015

/01/

23…

2015

/02/

13…

2015

/03/

06…

2015

/03/

27…

2015

/04/

17…

2015

/05/

08…

2015

/05/

29…

2015

/06/

19…

2015

/07/

10…

2015

/07/

31…

2015

/08/

21…

2015

/09/

11…

2015

/10/

02…

2015

/10/

23…

2015

/11/

13…

2015

/12/

04…

Tecfidera TRx Weekly

Source: IMS Health.

We are closely watching scripts but think these data suggest little impact from DTC campaigns so far. We assume Tecfidera goes generic in 2023, although there are patents that have long expiration dates, but we think 2023 is fair.Later patents are formulation patents for Tecfidera. There is currently an interference hearing between Biogen and Forward regarding claims on the 480mg dose of DMF, which is the active ingredient in Tecfidera. Oral hearings are now scheduled in January 2017, so we think that this interference case will not be an overhang in 2016.

19 January 2016

Biogen, Inc. (BIIB) 22

MT-1303—S1P1 Similar to Ozanimod Moving into Phase 3 for UC and Crohn'sWe assign a 50% probability to $1.4B sales in 2025; we think the big year for this program isn't really until 2018.MT-1303 is partnered with Mitsubishi (worldwide rights to Biogen, Asia rights to Mitsubishi). MT-1303 has the same target as Ozanimod (Phase 3) and Gilenya (marketed in MS). Biogen has not yet decided if it will pursue MT-1303 in MS, so for now the focus is the Crohn's and Ulcerative Colitis (UC) Phase 3 programs beginning in the second half of 2016.

Preclinical and clinical comparisons of S1P1 modulators suggest MT-1303 could have higher specificity, but all eyes on Ozanimod and MT-1303 Phase 3.

Figure 38: BIIB's Comparison of S1P1 Assets

Source: Company data.

Phase 2 data in MS suggests early hints of better efficacy than other S1P1 modulators, but we have yet to see efficacy data in UC and Crohn's, which are what Biogen is studying in Phase 3.So far, we have seen data from a placebo-controlled Phase 2 study in MS. Early data suggest we may see greater activity than with other S1P1 inhibitors, Ozanimod (Phase 3), and Gilenya (marketed).

Multiple Sclerosis data takes:

■ Overall: Comparable or better lymphocyte count reduction, reduction in cumulative Gd +T1 lesions and reduction in annual relapse rates with Ozanimod and Gilenya (not head to head)

■ Better ARR reduction in early studies could pan out to show higher efficacy in Phase 3: Higher reduction in annual relapse rates (ARR) in the highest dose cohort (.4mg) of 82% vs. 53% for Ozanimod and 54% for Gilenya suggests early hints of better efficacy.

19 January 2016

Biogen, Inc. (BIIB) 23

Phase 3 programs will begin in 2016 in UC and Crohn's. Biogen plans to run two Phase 3s for each program: a placebo-controlled ten-week induction followed by a 52-week placebo-controlled maintenance study. The first patient is anticipated in 2H16. We think we could potentially get ten-week data in 2017 but won't really learn more from these studies until 2018.

Mitsubishi is running a Phase 2 study in Crohn's that could potentially read out in the second half of 2016 or 2017. We note that on clinicaltrials.gov (NCT02378688), Mitsubishi (Biogen's partner) is running a Phase 2 trial in Crohn's that could potentially read out in the second half of 2016 or early 2017. We do not know the status of this trial, but if Misubishi releases the data, we think it would be a meaningful catalyst for the program.

19 January 2016

Biogen, Inc. (BIIB) 24

We See Increased Competition Coming Back to the Hemophilia Market in 2016 and BeyondWe expect a significant change in the hemophilia market over time due to therapies, which lead to longer dosing frequency to facilitate clotting.When Eloctate was approved for Hemophilia A, it was the only longer-acting factor on the market. However, Baxalta has been approved for a new longer-acting factor that is dosed bi-weekly. Bayer will soon have a longer-acting product on the market as well. In the longer term, we see real threats to the market from bi-weekly to monthly products for hemophilia. Currently, Alnylam and Roche both have therapies in Ph2 moving into Phase 3 that could be real category killers

Figure 39: New Hemophilia Therapies

Agent Developer Prophylaxis Dosing Status

Eloctate Biogen Every 3-5 days On marketAdynovate (BAX 855) Baxter Twice a week On market NovoEight/Zonovate Novo Nordisk 3-4 times a week On market

Advate Biogen 3-4 times a week On marketKogenate Bayer 3-4 times a week On market

Kovaltry (BAY 81-8973) Bayer Twice a week Application FiledACE910 Roche Biweekly-monthly Phase 2ALN-AT3 Alnylam Monthly - quarterly Phase 2

Source: Company data, Credit Suisse estimates.

We Have Built an Integrated Model That Includes Factor Therapies, Newer Targeted Therapies (Like ACE910 & ALN-AT3), and Gene Therapy. Our Takes from the ModelWe estimate that ~50% of the market is long-term factor market by 2023.We estimate that new longer-acting therapies take market starting around 2019-2022.

Figure 40: Estimated Timelines for Longer-Acting Agents

Market Agent Phase III Timeline Estimated Readout Estimated Launch

ACE910 Initiated December 2015 Mid 2017 Late 2018ALN-AT3 Initiate in Mid 2016 Late 2017 Early 2019ACE910 Initiate in 2016 Mid 2018 Late 2019ALN-AT3 Initiate in Mid 2016 Mid 2018 Late 2019

Factor IX ALN-AT3 Initiate in Mid 2016 Mid 2018 Late 2019

Inhibitors

Factor VIII

Source: Credit Suisse estimates, Company data.

Figure 41 shows the output from our integrated model around how the overall shares do change for the hemophilia market in the U.S. starting as early as 2020.

19 January 2016

Biogen, Inc. (BIIB) 25

Figure 41: U.S. Hemophilia A Market by Class of Therapy

0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%90.0%

100.0%

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

Long acting factors ACE910 & ALN-AT3 Gene therapy

Source: Credit Suisse estimates.

By 2020, we do model some share taken by gene therapy products. There is no data so far in Hemophilia A; however, BioMarin may have early proof-of-concept data in 2016.We have attempted to capture all the key programs for treatment of Hemophilia A and B. We decided to build an integrated model to make sure that we were not giving any one hemophilia therapy or class too much market share.

Figure 42: U.S. Integrated Hemophilia Model

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029

Advate/Recombinate - Baxter Refacto - Pfizer Kogenate - Bayer

Helixate - CSL Eloctate - Biogen ACE910- Roche

ALN-AT3 - Alnylam BMN-270- BioMarin Other Gene therapy options

Source: Credit Suisse estimates.

We assume a sustainable long-term share for Eloctate of 15% from our integrated market model. Our peak sales for Eloctate globally is $531M vs. consensus of $817M in 2018.We model more competition from new therapies starting in 2018. Therefore, our Eloctate estimates are well below consensus estimates in 2018.

19 January 2016

Biogen, Inc. (BIIB) 26

Figure 43: Eloctate Sales—Credit Suisse Figure 44: Eloctate Sales vs. Consensus

$59

$319

$467$509 $531

$578$526

$495 $516 $539 $538 $536

$274

$0

$100

$200

$300

$400

$500

$600

$700

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Eloctate global revs- CS

$319

$467$509 $531

$329

$475

$673

$817

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2015 2016 2017 2018

Eloctate - CS Eloctate - consensus

Source: Credit Suisse estimates. Source: Credit Suisse estimates, Biogen.

Our estimates are a bit more in-line with the Street on Alprolix (Hemophilia B). The key risk to this market remains gene therapy in the long term. More progress has been made in Hemophilia B than in A so far.

Figure 45: Alprolix Sales—Credit Suisse Figure 46: Alprolix Sales vs. Consensus

$0

$50

$100

$150

$200

$250

$300

$350

$400

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Alprolix global revenues

Alprolix

$236

$315$345 $336

$238

$313

$363$402

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2015 2016 2017 2018

Alprolix - CS Alprolix - consensus

Source: Credit Suisse estimates. Source: Credit Suisse estimates.

19 January 2016

Biogen, Inc. (BIIB) 27

We Are Still Cautious on LINGO, but We Do Give the Program Some Credit in Our ValuationBiogen Is Going for the Holy Grail of MS Treatment with Anti-LINGO Therapy to Promote Re-Myelination Re-myelination is a concept that is clearly distinct from immune modulation, and we know demyelination is the key pathological feature of MS.Multiple sclerosis (MS) is an immune mediated disease involving the central nervous system in which lymphocytes invade and attack myelin. This leads to de-myelination and the neurons being degraded. MS is currently treated with drugs that dampen an overactive immune response to lower disease activity. Remyelination is an endogenous repair mechanism that restores functions of axons that have lost their coating, and it also delays their deterioration.

Figure 47: Re-Myelination vs. Immune Modulation

Source: Company data, Credit Suisse.

Anti-LINGO would be absolutely revolutionary in the world of MS, and it would be used on top of current MS drugs. Anti-LINGO is Biogen's fully humanized antibody that is currently in Phase 2. The IP is robust with protection out to the late 2020s. LINGO-1 is a protein on the cell surface that controls the axons' (nerve fibers) ability to meyelinate and regenerate.

The company also has an oral pill (BIIB061) for re-meylination that is Phase 2 ready.

There is clear scientific evidence that anti-LINGO is involved with remyelination, but this protein is not the only one involved.Myelination is the coating of fat around axons that allows for more efficient nerve impulse conduction. When anti-LINGO is activated, it is a brake on normal nerve functioning. When the break is lifted with an anti-LINGO antibody, normal nerve functioning should resume.

19 January 2016

Biogen, Inc. (BIIB) 28

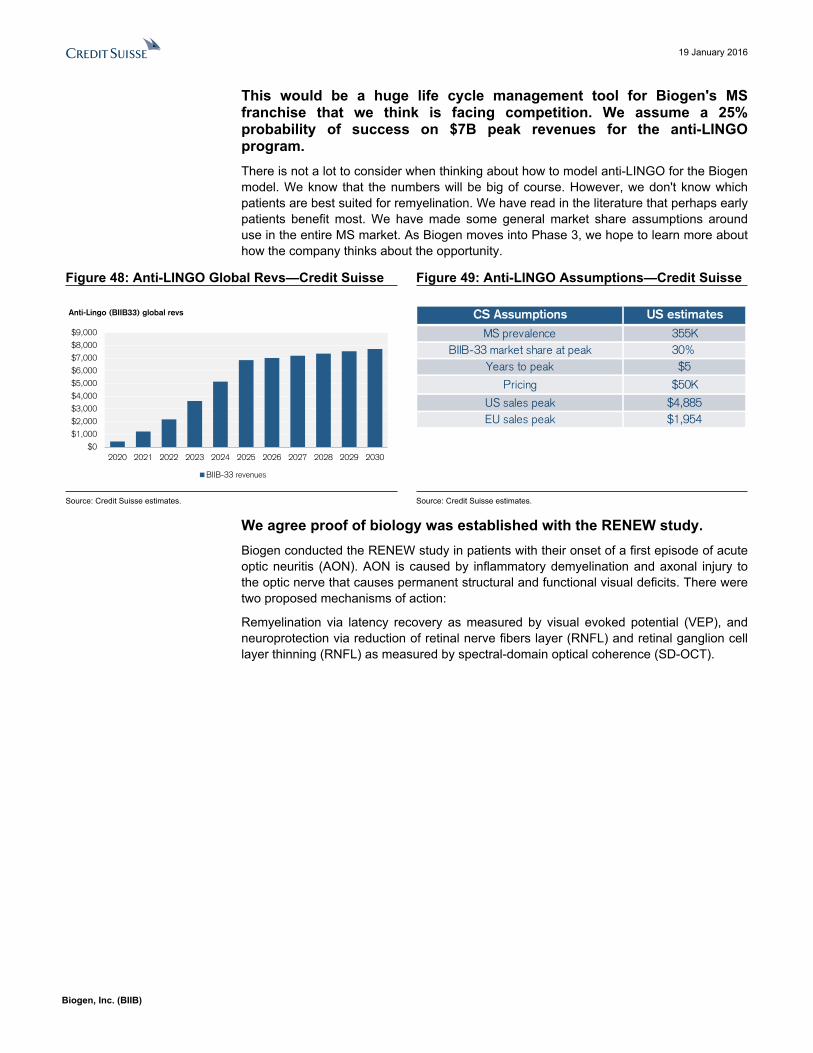

This would be a huge life cycle management tool for Biogen's MS franchise that we think is facing competition. We assume a 25% probability of success on $7B peak revenues for the anti-LINGO program.There is not a lot to consider when thinking about how to model anti-LINGO for the Biogen model. We know that the numbers will be big of course. However, we don't know which patients are best suited for remyelination. We have read in the literature that perhaps early patients benefit most. We have made some general market share assumptions around use in the entire MS market. As Biogen moves into Phase 3, we hope to learn more about how the company thinks about the opportunity.

Figure 48: Anti-LINGO Global Revs—Credit Suisse Figure 49: Anti-LINGO Assumptions—Credit Suisse

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Anti-Lingo (BIIB33) global revs

BIIB-33 revenues

CS Assumptions US estimates

MS prevalence 355KBIIB-33 market share at peak 30%

Years to peak $5

Pricing $50K

US sales peak $4,885EU sales peak $1,954

Source: Credit Suisse estimates. Source: Credit Suisse estimates.

We agree proof of biology was established with the RENEW study.Biogen conducted the RENEW study in patients with their onset of a first episode of acute optic neuritis (AON). AON is caused by inflammatory demyelination and axonal injury to the optic nerve that causes permanent structural and functional visual deficits. There were two proposed mechanisms of action:

Remyelination via latency recovery as measured by visual evoked potential (VEP), and neuroprotection via reduction of retinal nerve fibers layer (RNFL) and retinal ganglion cell layer thinning (RNFL) as measured by spectral-domain optical coherence (SD-OCT).

19 January 2016

Biogen, Inc. (BIIB) 29

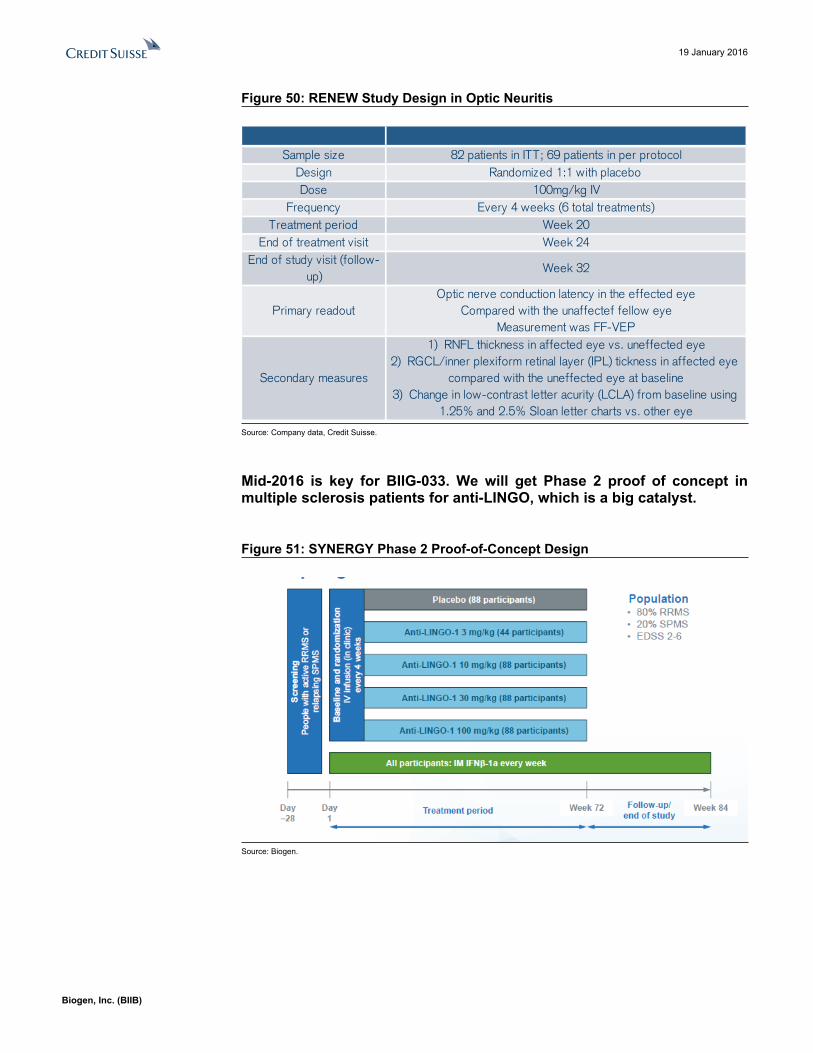

Figure 50: RENEW Study Design in Optic Neuritis

Sample size 82 patients in ITT; 69 patients in per protocolDesign Randomized 1:1 with placeboDose 100mg/kg IV

Frequency Every 4 weeks (6 total treatments)Treatment period Week 20

End of treatment visit Week 24End of study visit (follow-

up)Week 32

Primary readoutOptic nerve conduction latency in the effected eye

Compared with the unaffectef fellow eyeMeasurement was FF-VEP

Secondary measures

1) RNFL thickness in affected eye vs. uneffected eye2) RGCL/inner plexiform retinal layer (IPL) tickness in affected eye

compared with the uneffected eye at baseline3) Change in low-contrast letter acurity (LCLA) from baseline using

1.25% and 2.5% Sloan letter charts vs. other eye

Source: Company data, Credit Suisse.

Mid-2016 is key for BIIG-033. We will get Phase 2 proof of concept in multiple sclerosis patients for anti-LINGO, which is a big catalyst.

Figure 51: SYNERGY Phase 2 Proof-of-Concept Design

Source: Biogen.

19 January 2016

Biogen, Inc. (BIIB) 30

Figure 52: SYNERGY Key Criteria

Locations US and Ex-USPatientPopulation

Includes RRMS or SPMS with ongoing disease activity within 12 months of enrollment Excludes RRMS patients with history of inadequate response to interferon β treatments Excludes patients who experienced a relapse within 90 days prior to Day 1/Baseline or have not been stabilized

from a previous relapse prior to ScreeningPrimary EndP Percentage of patients with confirmed improvement of neuro-physical and/or cognitive function and/or disabilityKey Secondary Endpoint(s)

Percentage of patients with confirmed worsening of neuro-physical and/or cognitive function and/or disability Advanced MRI analyses Safety (up to 84 weeks); Pharmacokinetic assessment (up to 84 weeks)

Readout Topline PII data expected in Mid-2016

Source: Company data, Credit Suisse.

Synergy study is a 400 patient study with RRMS and SPMS patients, with 68% of patients coming from Eastern Europe.Here are the key design points of the synergy study.

■ Four doses are being studied: 3, 10, 30, and 100mg/kg every 4 weeks via IV■ Placebo controlled■ Avonex is given weekly■ Patients are dosed for 72 weeks and then followed for another 12 weeks■ 533 patients were screened, and 418 patients were randomized and received at least

one dose of study medication■ Includes 330 RRMS patients and 88 SPMS patients■ Mean age is 40, and SPMS patients were a bit older■ 69% of patients had two or more relapses in two years■ 72 sites in 12 countries■ 68% of the patients are from Eastern Europe, with about 15% from the U.S.

The design has many different endpoints to fully understand the potential benefit of the anti-LINGO one. In speaking to Biogen, we might expect a top-line readout and then full data perhaps at a medical meeting. (We would guess ECTRIMS.)The primary endpoint in Synergy is a composite one based on disability measured by EDSS, cognitive function, physical function including timed walking, and upper limit function. MRI relevant endpoints in this study are a change in brain volumes, change in magnetization transfer, and change in lesion diffusivity

Exploratory endpoints include:

■ Changes in cognition as measured using the MS-COG, a composite cognitive endpoint of two tests of processing speed (two- and three-second PASAT and Symbol Digit Modality Test [SDMT]) and two tests of memory and learning (Selective Reminding Test [SRT] and Brief Visuospatial Memory Test-Revised [BVMT-R])

■ Severity of clinical relapses measured by Scripps Neurological Rating Scale ■ Worsening from baseline in six-minute walk (6MW) – ■ Analysis of diverse MRI endpoints, including the magnetization transfer ratio (MTR)

and diffusion tensor imaging (DTI)

Our most interesting findings came from the doctors, but they still expressed skepticism in the study achieving its primary endpoint. In our view, the totality of the evidence will be the focus here.■ More encouraged by data seen at ECTRIMS in the fall of 2015 vs. what was seen at

the AAN medical meeting in April

19 January 2016

Biogen, Inc. (BIIB) 31

■ Doctors were generally more encouraged when comparing the data to the fellow eye vs. the full field visual potential seen earlier in the year. They believed that it showed some neuroprotective effects

■ Agreed that the optic neuritis model is the best one to potentially show a benefit■ Expressed skepticism about the Synergy study hitting its primary endpoint■ Concerns focused on the trial being designed to hit the primary endpoint. There were

some questions around the secondary endpoints being able to show effect■ Avonex is used as the disease-modifying drug of choice due to (1) Biogen owning it

and, (2) it being perceived to be the least effective drug, so perhaps easiest to show a benefit

For Lingo, we assign a 25% probability of success. We are not sure if Synergy is going to show the definitive evidence, but we believe the programs continues forward post-SynergyBiogen has a pivotal moment on the Lingo program in 2016 with the Synergy program in MS patients. They are studying in a Phase 2 program Anti-Lingo1 with Avonex. Our checks have been skeptical about the program working on its primary endpoint, which is disability reduction. We could see some hints when considering the totality of the evidence. We think 25% fairly accounts for what we expect to be some progress this year with the Lingo program but not definitive evidence.

19 January 2016

Biogen, Inc. (BIIB) 32

We Think Nusinersen (ISIS-SMNrx) Readout Is a 2017 CatalystSpinal muscular atrophy is a rare disease that leads to progressive muscle atrophy and loss of motor function.SMA is a rare and devastating disease that is the leading cause of deaths in infants. There are currently no approved therapies. Nusinersen is a therapy that targets the genetic flaw of SMA. There are four different types of SMA with type 1 being the most severe, and patients live under six months.

We think the Phase 2 multiple dose study (MAD) has provided evidence that the drug has activity and has shown effectiveness in UN-CONTROLLED Ph2 studies.IONS plans to update their data from the multiple dose study this year. The last update was mid-2015. In April, the median event free age of four patients in the 6mg arm had gone from 16.3 mos to 19.9 mos and from 11.6 mos to 16.7 mos in the 12 mg arm. Of infants in the original group, seven saw their median age increase from 9.6 mos to 21 mos at the April 2015 update. As of the June 2015, there were no new events.

Data for nusinersen likely read out early 2017. We don't think that the drug gets approved by the FDA earlier than mid-2H 2017. SMA is worth ~$50/share at 100% success. (We assume 65%.)We know that IONS and Biogen are working with the regulators to see if nusinersen might be able to get to market faster for such a devastating disease as SMA. We are assuming that the drug comes to market in early 2017, so a faster outcome is upside to our estimates. We think there is clear proof of biology and concept with the Phase 1&2 study. The biggest risk is clinical for this program and showing a benefit in Phase 3. We do wonder (from looking at DMD) if there might be a clinical path if the Phase 3 studies fail. For now, we assume a 65% probability of success on ~$3B sales to Biogen in 2025.

Our peak sales are $3B for nusinersen.We assume a 70% market share in Type 1. We assume 45% share in type 2 and 25% share in type 3. The type 3 patients typically live full lives but have compromised quality of life, whether it be loss of mobility, sclerosis, or respiratory illnesses. The literature says with palliative care that their life span can be similar.

19 January 2016

Biogen, Inc. (BIIB) 33

Figure 53: Nusinersen Sales by Type—Credit Suisse

$0.0

$500.0

$1,000.0

$1,500.0

$2,000.0

$2,500.0

$3,000.0

$3,500.0

$4,000.0

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

SMA Type 1 sales SMA Type 2 sales SMA Type 3 sales

Source: Credit Suisse estimates, Company data.

19 January 2016

Biogen, Inc. (BIIB) 34

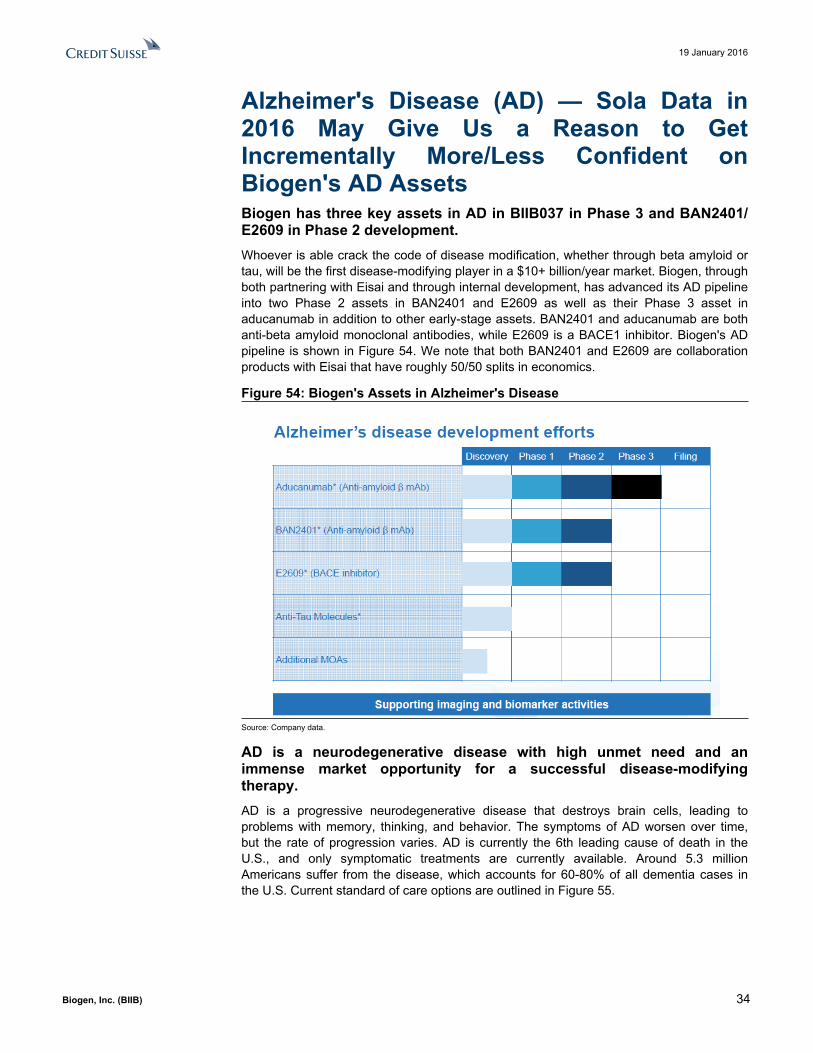

Alzheimer's Disease (AD) — Sola Data in 2016 May Give Us a Reason to Get Incrementally More/Less Confident on Biogen's AD AssetsBiogen has three key assets in AD in BIIB037 in Phase 3 and BAN2401/ E2609 in Phase 2 development.Whoever is able crack the code of disease modification, whether through beta amyloid or tau, will be the first disease-modifying player in a $10+ billion/year market. Biogen, through both partnering with Eisai and through internal development, has advanced its AD pipeline into two Phase 2 assets in BAN2401 and E2609 as well as their Phase 3 asset in aducanumab in addition to other early-stage assets. BAN2401 and aducanumab are both anti-beta amyloid monoclonal antibodies, while E2609 is a BACE1 inhibitor. Biogen's AD pipeline is shown in Figure 54. We note that both BAN2401 and E2609 are collaboration products with Eisai that have roughly 50/50 splits in economics.

Figure 54: Biogen's Assets in Alzheimer's Disease

Source: Company data.

AD is a neurodegenerative disease with high unmet need and an immense market opportunity for a successful disease-modifying therapy.AD is a progressive neurodegenerative disease that destroys brain cells, leading to problems with memory, thinking, and behavior. The symptoms of AD worsen over time, but the rate of progression varies. AD is currently the 6th leading cause of death in the U.S., and only symptomatic treatments are currently available. Around 5.3 million Americans suffer from the disease, which accounts for 60-80% of all dementia cases in the U.S. Current standard of care options are outlined in Figure 55.

19 January 2016

Biogen, Inc. (BIIB) 35

Figure 55: Current AD Standard of Care—Symptomatic NOT Disease-Modifying

Product Company Drug ClassAricept Pfizer/Eisai AChE inhibitorExelon Novartis AChE inhibitor

Razadyne ER JNJ/Shire AChE inhibitorCognex Sciele AChE inhibitor

Namenda Forest/Actavis NMDA antagonistSource: Company data.

Amyloid beta is clearly implicated in the pathogenesis of Alzheimer's, but tau is suspected as well.The brains of AD patients accumulate two types of proteins that are believed to be contributive to the disease: plaques and tangles. Plaques are deposits of a protein fragment called amyloid beta that build up in the spaces between nerve cells, while tangles are twisted fibers of another protein called tau that build up inside the cells. Disease-modifying therapies are currently in development to target both of these. At the forefront of these therapies are treatments that seek to block amyloid beta production and enhance amyloid beta clearance or inhibit the accumulation and spreading of misfolded tau proteins. We show in Figure 56 the development profiles of some of these key assets.

Figure 56: Development Profiles of Disease-Modifying Therapies in AD

Compound Company Stage Patients Primary CompletionAC-1204 Accera Phase 2/3 Mild to moderate July 2016

MEDI1814 Astrazeneca Phase 1 Mild to moderate November 2016AZD-3293 Astrazeneca/Lilly Phase 2/3 Mild August 2019

BIIB037 Biogen Phase 3 Prodromal and Mild February 2020BAN2401 Eisai / Biogen Phase 2 Mild June 2018

E2609 Eisai / Biogen Phase 2 Prodromal or Mild August 2017EVP6124 Forma Phase 3 Mild to moderate August 2017

Solanezumab Lilly Phase 3 Mild October 2016MK8931 Merck Phase 3 Prodromal July 2019MK8931 Merck Phase 3 Mild to moderate July 2017

PF-05212377 Pfizer Phase 2 Mild to moderate December 2016Crenezumab Roche Phase 1 Mild and moderate September 2015

Gantenerumab Roche Phase 3 Mild July 2018

Source: Company data, Credit Suisse estimates.

Solanezumab (Lilly Anti-Amyloid Antibody) Will Be a Focus in 2016 as a Potential Read-Through to Biogen's Program Solanezumab data for Expedition 3 is expected to read out in 2016. We think investors will make a read-through to Biogen's program whatever the outcome.Because Solanezumab and aducanumab share similar mechanisms of action and targets, we believe that data from Expedition 3 will affect investors' perceptions of BIIB037's probability of success. Lilly made some changes to the trial design in Expedition 3, which is similar to Biogen's design of their Phase 3 with aducanumab. We show the respective trial designs for both Lilly and Biogen in Figure 57.

19 January 2016

Biogen, Inc. (BIIB) 36

Figure 57: Expedition 3 Versus EMERGE/ENGAGE Trial Designs

Trials: EXPIDITION 3 EMERGE/ENGAGEAsset Solanezumab AducanumabPhase 3 3

Primary Endpoint

Change from baseline in Alzheimer's Disease Assessment Scale-Cognitive 14 Item

Subscore and Alzheimer's Disease Cooperative Study- Instrumental Activities of

Daily Living

Change from baseline in CDR-SB score

Patients 2,100 1,350 each

Key inclusion criteria

1) Met criteria for probable AD 2) Has a MMSE of 20 through 26 3) Has had a MRI/CT

scan performed within the past 2 years that has not confirmed AD 6) Has a PET/CSF result consistent with amyloid pathology

1) A CDR Global Score of 0.5 2) Evidence of cognitive impairment 3) MMSE score

between 24 and 30 4) Positive amyloid PET scan

Study Start Date July 2013 August 2015Estimated Completion October 2016 February 2020

# of Centers 198 study locations 148 study locations

Source: Company data.

If the outcome is positive, we think Biogen's stock will react to the upside ($9-$13/share up).Even if the Sola trial is positive, we won't exactly know if the Phase 3 Biogen study will be positive as well. We know with these anti-amyloid beta antibodies, each are a little different. With that being said, we think investors would assign another 10-15% probability of success to Biogen's program if Sola hits this year. Increasing the POS by 10-15% would add $9-$13/sh.

If the outcome is negative, we think Biogen's stock will be down, as it would prompt greater concerns that the amyloid beta hypothesis really holds. We think Biogen's stock could be down ~$17/sh.Again to be balanced, we can't assume that the drugs are exactly the same, so we wouldn’t assume Biogen's program is dead if the Sola trial doesn’t work. We would guess that investors lower the Biogen probability at least 20%, which lowers our DCF by $17.

How We Model the Market Opportunity for Alzheimer'sAD is one of the biggest unmet disease categories in biotech left, and the prevalence is huge as is the population.We started modeling Alzheimer's disease in the U.S. by an initial prevalence of ~5.3 million, noting however that this estimate would be much larger if there were better diagnostics, particularly in the early stages of the disease. The prevalence of mild cognitive impairment (MCI) is much higher; not all MCI develops into AD, but if early treatments for AD could penetrate this population as a preventative treatment, this would provide upside potential to our base-case estimate.

Diagnosis and treatment rates remain around 50% probably due to lack of disease-modifying therapies.From here, we broke the market down by the percentage of the population that is diagnosed & treated and found that there are approximately 2.4 million patients currently on drugs for AD per IMS scripts. We see this as a reasonable base-case market size as (1) more treatments come to market, and (2) better diagnostics are likely to expand the market itself over the next several years. After referencing literature focused on segmenting the Alzheimer's population according to severity, we found that ~27% of total

19 January 2016

Biogen, Inc. (BIIB) 37

diagnoses are classified as mild, which totaled ~650k. This was the first component of our addressable patient population.

We model the prodromal population separately and assume ~10% prodromal conversion rate annually to mild. This is a key assumption since it may be the case that these therapies work particularly well in this population.What is the prodromal population?Prodromal AD is a very early stage of the disease in which a person’s memory loss has become worse than what can be expected by the normal aging process alone but other areas of cognition and the daily living activities are not significantly affected.

Before seeing the Biogen slide, which showed the prodromal opportunity, we found many different estimates for the potential prodromal population.

We cited this population at ~3.8 million with approximately 10% of these patients eventually converting to the mild form of the disease. This was our second component of our patient population, which led us to a complete total slightly above 1M. We assumed similar market characteristics in the EU but with a higher initial prevalence of the disease at 8 million.

Figure 58: Biogen's Market Analysis on AD Based on Disease Course

Source: Company data.