big debates 2011 – europe

DESCRIPTION

TRANSCRIPT

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.

For analyst certification and other important disclosures, refer to the Disclosures Section. += Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to NASD/NYSE restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

December 8, 2010

We are well into the third year of macro. Debates around the outlook of different economies and asset classes continue to dominate investors’ agendas and the movements of individual securities across regions and sectors.

Our global team of economists and strategists is focused on these key debates, expectations and risk-reward scenarios (for their latest risk-reward views, please consult the Global Debates Playbook monthly and their special year-end publications).

In this series, Big Debates: 2011, our industry analysts around the globe look at the industry- and company-specific investor debates that are likely to drive stocks in the upcoming year. We looked for debates that are likely to matter, that are likely to be settled (or significantly advanced) in the coming year, and for which we have a view that differs sharply from the current market view.

Our job as securities analysts starts with conversations with leading investors. We look to identify which debates matter today, and more important, which will matter tomorrow. Through these conversations, along with an increasing array of analytics, we also get a read for “what’s in the price” – what are the types of expectations that may warrant the current price.

As always, we look forward to your feedback.

Linda Riefler Global Head of Research

Juan-Luis Perez Global Director of Research

Rupert Jones Director of EU Research

Big Debates: 2011 – North America December 6, 2010

Big Debates: 2011 – Asia Pacific December 7, 2010

Global Debates Playbook November 16, 2010

M O R G A N S T A N L E Y R E S E A R C H

E U R O P E

Big Debates: 2011 Key Investor Debates Likely to Drive Stocks in the Upcoming Year

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Table of Contents

2

4 Aerospace & Defence EADS: Could the A350XWB be on time? Rupinder Vig

6 Autos & Auto Parts Sharp Recovery in US Consumption – Buy FIAT Stuart Pearson

8 Banks & Diversified Financials Which Banks Could Refocus Portfolios and Create Value in 2011? Huw van Steenis

10 Beverages Can Carlsberg Close the Valuation Discount to Peers in 2011? Michael Steib

12 Biotech & Medical Technology EU Austerity Measures: Does Past Data Predict Future Performance? Michael Jungling

14 Brands Is Big Becoming the New Beautiful? Louise Singlehurst

16 Building & Construction Is EM Exposure an Earnings Driver or an Earnings Risk in 2011? Alejandra Pereda

18 Business & Employment Services Can HomeServe Roll Out Its UK Business Model Successfully in the US? Jessica Alsford

20 Capital Goods Will Grid Investment Recover in 2011? Ben Uglow

22 Chemicals Petrochemical Margins – Imminent Decline or Supercycle? Paul Walsh

24 Clean Energy EDP Renovaveis: Further Capex Cuts Could Crystallize Value Allen Wells

26 Food Producers Will Danone Return to Historical Growth Rates? Michael Steib

28 Insurance Does Aegon Need to Raise Equity to Repay Dutch State Aid? Farooq Hanif

30 Leisure & Hotels Could Hotel RevPAR Increase 10%+ in 2011? Jamie Rollo

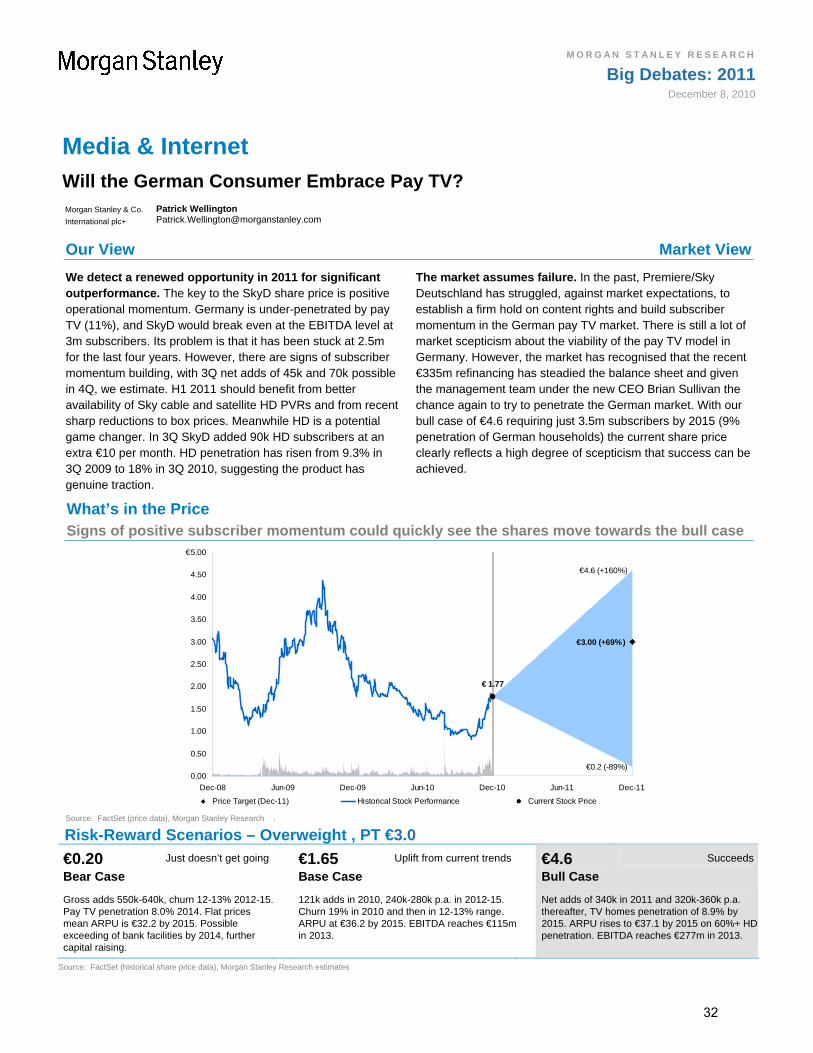

32 Media & Internet Will the German Consumer Embrace Pay TV? Patrick Wellington

34 Metals & Mining Will Kazakhmys Dispose of Its Stake in ENRC? Ephrem Ravi

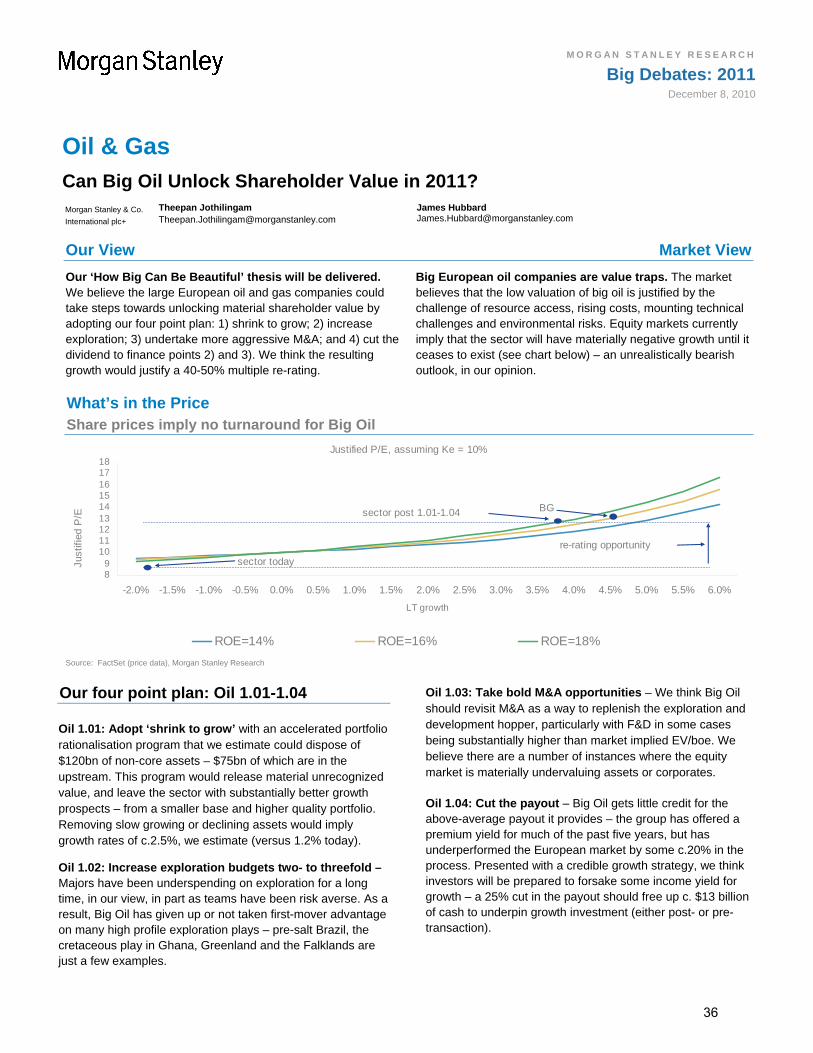

36 Oil & Gas Can Big Oil Unlock Shareholder Value in 2011? Theepan Jothilingam

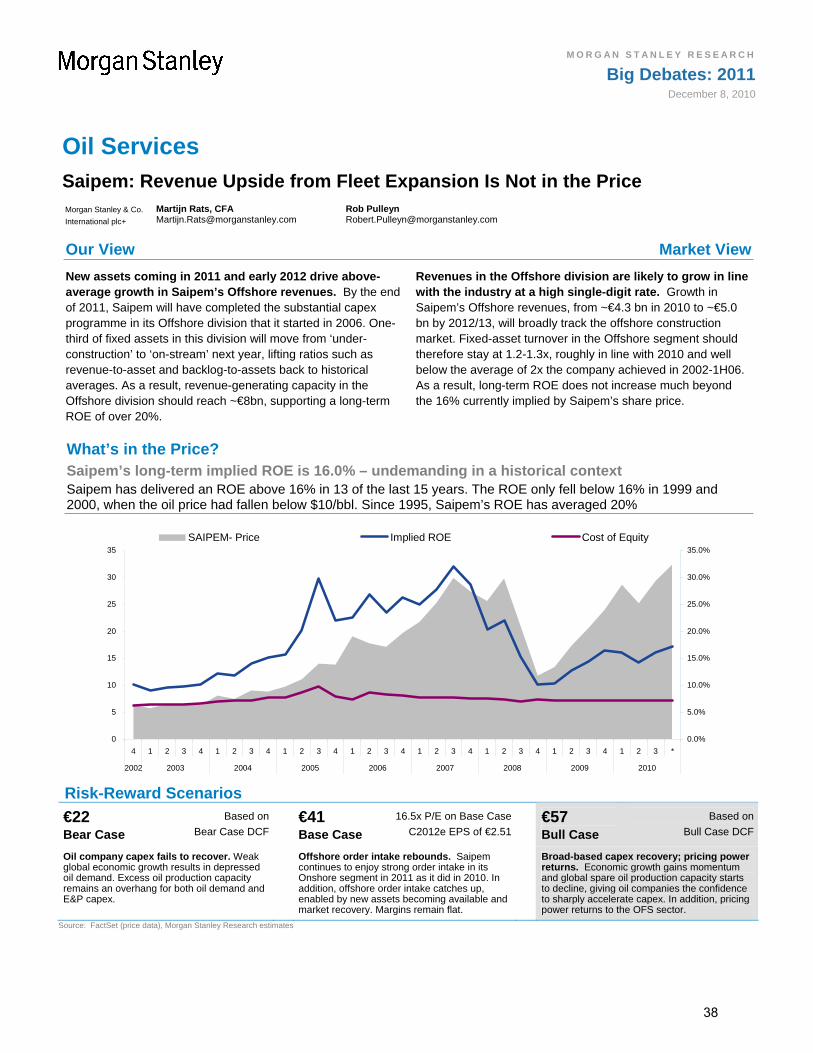

38 Oil Services Saipem: Revenue Upside from Fleet Expansion Is Not in the Price Martijn Rats

40 Paper & Packaging Will Consolidation Finally Begin in 2011? Markus Almerud

42 Pharmaceuticals Cheap Sector or Value Trap? Andrew Baum

44 Property Macro Tailwinds versus Debt-Related Headwinds Bart Gysens

46 Retail Unprecedented Apparel Inflation: What Is the Price Elasticity of Clothing? Charlie Muir-Sands

48 Technology Can Nokia Turn Around the Smartphone Business? Patrick Standaert

50 Telecommunications Services KPN: Can Fibre Drive a Wireline Inflection and Stable FCF? Luis Prota

52 Tobacco Can Imperial Tobacco Deliver Organic Growth? Toby McCullagh

54 Transport Container Shipping: Could Better Rate Discipline Drive Upside for Maersk? Menno Sanderse

56 Utilities Could 2011 Bring an Inflection Point in Earnings? We Think Not Emmanuel Turpin

58 EEMEA Banks Can Credit Normalization Continue to Drive Outperformance? Magdalena Stoklosa

60 EEMEA Oil & Gas Is Russian Oil Tax Reform Actually Happening … And Does It Matter? Matthew Thomas

62 Turkey Tekfen Holding AS: Contract Awards to Pick Up Materially Sayra Can Altuntas

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

3

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Aerospace & Defence EADS: Could the A350XWB Be on Time?

Morgan Stanley & Co.

International plc+

Rupinder Vig [email protected]

Ovunc Okyay [email protected]

Our View Market View

We see a possibility that development of the A350XWB (new wide-bodied Airbus aircraft) meets current management guidance of a 2H13 EIS. Management could be in a position to dedicate sufficient engineering time and resource to complete final assembly in 3Q11 followed by on-time first flight in mid-2012. This would leave ~12 months for flight testing before entry-into-service in 2H13. In this scenario, EADS shares could move towards our bull case of €32.

The market expects a 12-18 month delay in the A350XWB (particularly given past experience on the A380 and B787). Concerns over program execution on A350XWB have weighed on EADS shares over the past 18 months. Although management remains confident it can deliver the A350XWB on time in 2H13, the market remains very sceptical. Any indication that the project is on track during 2011 could therefore have a material impact on the share price.

What’s in the Price Successful execution on A350XWB would be a key positive surprise for EADS shares Morgan Stanley Risk-Reward View (Left.) vs. Probabilities Implied by Option Prices (Right)

Price Target : € 24 Stock Rating : OverweightMS Industry view : In-Line

The probabilities of our Bull, Base, and Bear case scenarios playing out were estimated with implied volatility data from the options market as of Dec 2,2010. All figures are approximaterisk-neutral probabilities of the stock reaching beyond the scenario price in one-year’s time.

EADS NV

€ 17.58

Prob(> € 32 ) < 5%€ 32

€ 13 Prob(< € 13 ) ~ 20%

€ 24 Prob(> € 24 ) ~ 15%

€

-

5

10

15

20

25

30

35

40

45

Dec-08

Feb-09

May-09

Aug-09

Nov-09

Feb-10

May-10

Aug-10

Oct-10

Jan-11

Mar-11

May-11

Jul-11

Sep-11

Nov-11

~ 15% probability the stock will reach above € 24 price target in 12 months

Risk-Reward Scenarios

€12.50 Bear Case

12.3x P/E on Bear Case

2012e EPS of €1.02

€24.00 Base Case

11.6x P/E on Base Case

2012e EPS of €2.07

€32.00 Bull Case

10.0x P/E on Bull Case

2012e EPS of €3.19

Airbus deliveries fall, euro strengthens. EUR/USD trends to 1.50, market accords zero value for Airbus, customer financing concerns are realized and margins trend to 4.0-4.5% long term.

Airbus remains robust; cycle remains elevated, euro remains stable. Deliveries remain stable in 2011 and then increase in 2012 on the back of rising production rates. Airbus margins trend to 6.0-6.5% long term.

Airbus restructures further, deliveries rise, euro weakens further. New aircraft order flow picks up, EUR/USD rate trends to 1.25 and additional cost savings push group margins up to 9.0-9.5% long term.

Source: FactSet (price data), Morgan Stanley Research estimates

4

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Potential Catalysts

FY10 results – March 2011 Management will provide an update on whether A350XWB remains on track (and on cost)

Final assembly of first aircraft – 3Q11 Completion of final assembly of MSN001 (first A350-900) is scheduled for 3Q11

First flight – Mid 2012 First flight is scheduled for mid-2012, followed by a 12-month flight test program (on 5 aircraft)

Entry into service – 2013 Management expects the A350 to enter service in 2H13

Delays to new aircraft programs have been a major overhang on EADS shares. The past few years have seen program execution become something of an Achilles heel for EADS, with a number of problems on major programs, including A380 and A400M. Exhibit 1 below shows how the EADS share price has fallen following delay announcements, with a total aggregate relative underperformance from the four A380 delay announcements of 37% versus MSCI Europe and 39% versus Boeing.

The market is very sceptical that the A350XWB will be able to launch in 2H13. Given the past experience of A380, A400M and also B787, the market clearly expects A350XWB

to be delayed beyond 2013. This view was given further fuel when EADS announced a two-month delay on November 12 (the shares have since fallen by 7%, despite the strengthening dollar).

The consensus view appears to be that a delay of 12-18 months is likely. Many investors now expect the November 12 delay announcement to be the first of a series that will ultimately see A350XWB delayed by 12-18 months (a similar length of delay experienced by other recent development programs undertaken by Boeing and Airbus).

We therefore think the shares would react very positively to signs that A350XWB could launch on time. In our view, the next 12 months will be crucial in giving the market confidence that management can deliver on its guidance for a 2H13 entry into service. Final assembly is scheduled for 3Q11, and first flight is expected within six months of this date. If both occur on time, the market is likely to gain more confience that A350XWB can deliver in 2013.

We remain Overweight on EADS with A350XWB a key catalyst (and potential positive surprise). Although 2011 is likely to be a tough year for EADS, given the numerous challenges that remain, we continue to believe that valuation is very attractive, pricing is picking up and that program execution is showing signs of improvement. This, coupled with the cyclical upturn, makes EADS a compelling buy for longer-term investors, in our view. Successful execution on A350XWB could trigger a material re-rating in the stock.

Exhibit 1

Program delays have historically hit EADS hard, so on-time A350XWB development would be a key catalyst

5

10

15

20

25

30

35

40

45

Jan-05

Apr-05

Jul-05

Oct-05

Jan-06

Apr-06

Jul-06

Oct-06

Jan-07

Apr-07

Jul-07

Oct-07

Jan-08

Apr-08

Jul-08

Oct-08

Jan-09

Apr-09

Jul-09

Oct-09

Jan-10

Apr-10

Jul-10

Oct-10

EA

DS

sh

are

pric

e (

€)

First delay (June 1, 2005): Delivery will slip by 6-months. 2009 planned deliveries down to 90–100 (from 120). EADS down 3% vs. MSCI in the following 2 weeks.

Second delay (June 13, 2006): Additional delay of 7-months. EADS down 20% vs. MSCI in the following 2 weeks. EADS CEO, Airbus CEO and A380 program manager departed.

Third delay (October 3, 2006): Additional delay of one year. EADS down 10%vs. MSCI in the following 2 weeks. Fourth delay (May 13, 2008):

Reduced deliveries for 2008 and 2009. EADS down 4% vs. MSCI in the following 2 weeks.

Source: FactSet, Company data, Morgan Stanley Research

5

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Autos & Auto Parts Sharp Recovery in US Consumption – Buy FIAT Morgan Stanley & Co.

International plc+

Stuart Pearson, CFA [email protected]

Our View Market View

We expect the US car market to surprise materially in 2011, jumping +20% to a 14m SAAR. Rebounding US consumer confidence provides the final ingredient to a set of conditions already ripe for a sharp recovery in demand. These include record high used vehicle prices, the oldest US fleet age on record, strong credit quality, and improving credit availability. The latter should also aid Chrysler’s market share recovery, given the lower average credit score of its customers. With an effective 35% stake in Chrysler (and option to move to 51%), we see Fiat as the best European play on the recovering US market.

Consensus assumes a slow recovery in the US market to a c.13m SAAR next year. The recovery of the US market thus far has been lackluster, constrained by the lack of credit availability and weak consumer confidence. Consensus assumes this continues into 2011e, driving more modest +10% growth. Furthermore, consensus remains highly skeptical on Chrysler’s ability to deliver the necessary product to win back market share. Sceptics doubt the heavy ‘refresh’ work on Chrysler’s 10 new model launches in Q410 will prove sufficient to win back retail share.

What’s in the Price Fiat shares assign a low probability to a sharp US recovery

Morgan Stanley Risk-Reward (left) versus Probabilities Implied by Option Prices (right) Price Target : € 17

Stock Rating : OverweightMS Industry view : In-Line

The probabilities of our Bull, Base, and Bear case scenarios playing out were estimated with implied volatility data from the options market as of Dec 2,2010. All figures are approximaterisk-neutral probabilities of the stock reaching beyond the scenario price in one-year’s time.

FIAT SPA

€ 13.48

Prob(> € 22 ) ~ 5%€ 22

€ 9 Prob(< € 9 ) ~ 20%

€ 17 Prob(> € 17 ) ~ 20%

€

-

5

10

15

20

25

30

Dec-08

Feb-09

May-09

Aug-09

Nov-09

Feb-10

May-10

Aug-10

Oct-10

Jan-11

Mar-11

May-11

Jul-11

Sep-11

Nov-11

~ 20% probability the stock will reach above € 17 price target in 12 months

Risk-Reward Scenarios

€9 Bear Case

€2.5 for Fiat Auto, €1.5 for

Chrysler, €5 for Industrial

€17 Base Case

€6.4 for Fiat Auto, €3.6 for

Chrysler, €7 for Industrial

€22 Bull Case

€8 for Fiat Auto, €5 for

Chrysler, €9 for Industrial

Fiat Auto delivers a trading margin of 2% in 2011e, rising to 3% by 2013e. Fiat Industrial delivers a trading margin of 6% in 2011e, rising to 7% by 2013e. Chrysler delivers a trading margin of 2% in 2011e, rising to 3% by 2013e.

Fiat Auto delivers a trading margin of 3% in 2011e, rising to 5% by 2013e. Fiat Industrial delivers a trading margin of 7% in 2011e, rising to 8% by 2013e. Chrysler delivers a trading margin of 3.7% in 2011e, rising to 6.4% by 2013e.

Fiat Auto delivers a trading margin of 3% in 2011e, rising to 6% by 2013e. Fiat Industrial delivers a trading margin of 7% in 2011e, rising to 10% by 2013e. Chrysler delivers a trading margin of 3.7% in 2011e, rising to 8% by 2013e.

Source: FactSet (price data), Morgan Stanley Research estimates

6

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

We think Chrysler may prove to be one of 2011’s most surprising success stories. With refreshed product meeting a sharp recovery in the US market and a restructured cost base, we believe Chrysler’s US share and profitability could step up in 2011-12. We highlight a number of factors moving in Chrysler’s favour in recent months:

US market recovery. We forecast a 20% jump in the US car market in 2011. With 70% of unit sales to the US, Chrysler carries by far the largest exposure to the market of any global OEM. This is an exposure we want to own heading into 2011.

Market share revival. Within the US market we believe Chrysler can steadily reclaim lost market share. The acid test for Chrysler will be the success of its refreshed product offerings arriving in 2011, and all new models from 2012. We conservatively see share recovering to 10.5%. We believe consensus expectations here are too low, at c.9%.

Debt restructuring. Chrysler’s strong gross cash position ($8.3bn) and potential DoE loan approval (for c.$3-4bn) should allow the firm to repay US treasury loans ($7bn outstanding). This could materially reduce Chrysler’s interest burden, given interest rates on state debt currently range between 7% and 20%. We estimate Chrysler’s interest costs could fall by c.$400m.

Perhaps more significantly for Fiat shareholders, the repayment of Chrysler’s government loans would also clear one hurdle for Fiat to move to a majority share in the company. This could be timed to coincide with a possible Chrysler IPO, one of several options being considered. However, any such move would require the agreement of all the stakeholders in Chrysler (including the US treasury and UAW).

Bull case value of up to €22 per share Chrysler is the key point of differentiation between our base and bull case valuations for Fiat – and especially for the post demerger Fiat Auto business. Under our base case, we value Chrysler at €3.6 of our €9.3 per share Fiat Auto 2011 sum of parts. This assumes Chrysler margins peak at 6% in 2013 on a 10.5% US share.

Under our bull case scenario of a 13% US share and 8% peak margins (closer to Chrysler’s actual business plan), we value Chrysler at up to €6 per Fiat share. This would increase our Fiat Auto valuation to close to €12/share, and help take our group bull case valuation to €22 per share.

Potential catalysts for Fiat equity

First day of each month US sales data release revealing demand, inventory and incentive levels

January 3rd, 2011 Demerger of Fiat into separate Industrial and Automotive units

1H 2011e Chrysler likely to receive DoE loans and repay high cost US Treasury debt

2H 2011e Potential Chrysler IPO (as flagged by management)

Exhibit 1

Chrysler US sales and market share

0

50,000

100,000

150,000

200,000

250,000

300,000

Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10

0%

2%

4%

6%

8%

10%

12%

14%

16%

US Unit Sales (LHS) US Market Share, % Source: Autodata, Morgan Stanley Research

Exhibit 2

Chrysler bull/base share and margin assumptions

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2010e 2011e 2012e 2013e 2014e

0%

2%

4%

6%

8%

10%

12%

14%

Base Case EBIT Margin Bull Case EBIT Margin Base Case US Share Bull Case US Share

Source: Morgan Stanley Research estimates

7

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Banks & Diversified Financials Which Banks Could Refocus Portfolios and Create Value in 2011? Morgan Stanley & Co.

International plc+

Huw van Steenis Francesca Tondi, Maxence Le Gouvello, Henrik Schmidt, Steve Hayne , Hubert Lam, [email protected] Chris Manners, Thibault Nardin, Alice Timperley, Wouter Janssens

Our View Market View

2011 is likely to be a year for difficult portfolio choices, which could drive considerable value if we get clarity on the macro environment and regulation. We would look at the sub-scale fixed income players and those seeking to sell assets to meet Basel 3 norms or to refocus business. Stocks in focus: UBS, Barclays, Soc Gen, UCG

The market thinks the large wholesale/universal banks will be very heavily impacted by Basel III and their current portfolio mix. The banks are therefore trading at 0.7-0.85x 2011e TNAV (or in the case of UBS the investment bank is at this type of valuation). The market doubts that we will get the regulatory or macro clarity for transformation programmes.

What’s in the Price Book value growth at a reasonable price will be key for stock performance

DANSKE

SHB

NDA SWED

CSGN

STAN

BNP

HSBC

BP PMI

MBUCG

MPS

ISP

UBS

SocGenCASA

BAC

BARC

KN

DBKLLOY

RBSC

DNB

SEB

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

0% 10% 20% 30% 40% 50% 60% 70%Accumulated Book value creation 1H10e-2012e

Pri

ce/1

1e

Ta

ng

ible

Bo

ok

Va

lue

Source: FactSet (price data), Morgan Stanley Research estimates

Greater differentiation in European banks stocks is likely, we think, as the market is not reflecting very different book value growth, macro risks, credit recovery stage, funding profiles or deleveraging risks. Given our view of lacklustre book growth for many banks, funding being a drag anchor on lending and provisions, the teething pains of a new paradigm in banking regulation and macro uncertainty, there is no one theme to play such a diverse group of European banks. We wrote extensively about this in our December 1 report, Expect

Greater Differentiation and in our November 16 note, Sovereign Risk and Bank Funding.

Regulatory pragmatism shouldn't be mistaken for no action. We still expect regulators to have tougher standards, but the repricing of risk and a pragmatic approach to enable credit creation are likely to allow banks to generate reasonable returns.

8

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

2011 will be a critical year when banks review and reshape business plans for the new regulatory paradigm and market conditions. The stocks in focus, in our minds, are those where we see a strong possibility that major decisions will be made on portfolios, whether it be UBS rethinking the scale of its ambitions in fixed income, Barclays reshaping its group portfolio, Soc Gen beginning to consider divesting non-core assets more quickly to meet new regulatory standards, or Unicredit rethinking its portfolio and/or geographical footprint. We look at these four examples in turn.

1. UBS’s equities franchise has regrouped to be top five YTD on reported revenues, but the bank is still outside the top 10 in FICC trading and has seen far more volatility than the flowmonsters. UBS has had about two-fifths of the FICC revenue share of JPM this year, but with materially higher volatility. The strategic response has been to reinvest and grow scale, but this means the fixed cost base has significantly increased, making UBS even more operationally geared to markets and contributing to the investment bank breaking even in Q3. For instance, if we use our assumptions on Basel 3 (published previously), the investment bank may need allocated equity of SFr 35-40bn (up to ~80% of the total targeted capital of the group). Management targets suggest SFr 6bn of PBT for the investment bank. Assuming a 30% tax rate (although we recognise huge DTAs for the coming years) means the i-bank would only make a ~10.5% post-tax return on capital in 2013, which is below our view of the cost of equity and leaves no room for error. Our 2012 estimate of SFr 4.5bn is clearly well below the cost of equity, which implies UBS has to cut costs, focus on generating higher returns on less capital-intensive businesses, rethink its priorities and be ruthless on capital allocation decisions, and/or execute flawlessly. This will be no mean feat in FICC trading. Hence, we think the market will remain reluctant to attribute a value to the investment bank much above 1x. The opportunity is whether UBS can reshape the allocation (perhaps saving SFr 5-10bn of equity) and so drive stronger returns. Today management is focused on growing its way out of low profits, but we believe a more fundamental rethink could well begin in 2011.

2. Over the next 18-24 months, Soc Gen’s management will focus on executing its industrial plan. In our view, much of the plan’s success will depend on management’s ability to shed more light on group core businesses and to dispose of non-core assets, such as legacy assets or non-leading, non-funded franchises. SG’s solvency is heavily penalised by its €54bn legacy portfolio, which represents more than 42% of RWA inflation under Basel 3. We saw clear

motivation to reduce this portfolio in Q3, when Soc Gen disposed of €2.6bn in assets, giving more flexibility to group solvency. We expect this trend to continue, but it will also depend on market conditions. Last June, Soc Gen announced it would refocus its business on core franchises with the following criteria: significant market share, L/D ratio <130%, and potential upside. As we noted in our March 16 note Roadmap to Crystallize Value, we see the group launching a strategic review on SFS and some CEE countries.

3. UCG's new CEO is also facing difficult choices to increase the group’s return (from the current depressed level of c. 4% RoNAV) and further improve capital to put the group on a more solid footing. This may require some radical decisions, possibly reversing recent expansion strategies, both in terms of business mix (for example, reducing the CIB division, which now absorbs over 50% of group RWA) and geographical footprint (the group is present in nearly 20 countries, not all of them profitable). Indeed, UCG may not be alone in shifting geographical strategy away from ‘putting flags on the map’ towards a focus on a few key ‘home markets’ where it can attain critical mass. It is not yet clear to us whether the new CEO has the mandate to undertake a radical review of the group, and we are concerned that a ‘slow burn’ strategy could see returns staying depressed for longer.

At Barclays, management is now focusing on returns and execution over growth, with the stock trading at a 23% discount to book value. It hopes to achieve this by: i) raising the ROTE in the underperforming businesses (such as Western Europe retail banking, where a review is to be conducted); and ii) growing in higher ROE business lines, such as equities, M&A and wealth management. We think the new CEO Bob Diamond, who was started a review of returns on allocated capital in the 50 business lines, is likely to make some tough decisions to refocus the group. We consider this a reassuring message, as the sub cost of capital ROE expectations are a root cause of the discount (trading at 0.7x 11e TNAV). We forecast a ROTE of 13.1% by 2012, and so expect the discount to narrow should changes in the portfolio come through.

Potential Catalysts

UCG and Barclays – news flow on reshaping strategy / portfolios as new management takes control, presumably starting with the FY results

April / May 2011 – business reviews post Q1 results

4Q 11 results – as banks reflect on 2011 performance and budget for 2012

9

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Carlsberg Can Carlsberg Close the Valuation Discount to Peers in 2011? Morgan Stanley & Co.

International plc+

Michael Steib [email protected]

Eveline Varin [email protected]

Our View Market View

Carlsberg’s valuation gap with ABI and SAB should narrow as Russia helps deliver strong earnings growth. Carlsberg derives some 40% of its profits in Russia, where we think the risks are weighted to the upside. Strong macro-economic factors are supportive of a recovery in consumer demand, consumer trend preferences are moving in favour of beer, and future regulatory moves are likely to be softer than the tax increase put through in January 2010.

The market applies a discount to Carlsberg’s valuation due to the risks associated with its exposure to Russia. We estimate Carlsberg’s current share price is discounting long-term earnings growth of around 3.5%, against 5% on average for ABI and SAB.

What’s in the Price Carlsberg’s shares are discounting lower LT growth than peers – we think this is undeserved

0%

20%

40%

60%

80%

100%

ABInBev SABMiller Carlsberg Heineken

% v

alu

e im

plie

d in

cu

rre

nt

sha

re p

rice

Current earnings Explicit period LT growth

Carlsberg's LT growth implied in current share price remains below that of ABInBev and SABMiller

Source: FactSet (price data and consensus earnings), Morgan Stanley Research

We expect strong macro factors to support the recovery of the beer market in Russia, and forecast volume growth of 5% in FY11. Our economics team expects private consumption in Russia to grow by 4.5% next year, outperforming GDP growth. The Russian beer market was hurt badly by the recession in 2009, but with the oil price recovering, the RUB strengthening against the euro and strong stimulus-fuelled GDP forecast for 2010, we expect beer volume growth to recover over the next three years to at least Carlsberg’s medium-term guidance of 3-5% a year.

Beer should continue to gain share from vodka. Beer accounts for only 38% of alcohol consumption in Russia,

Exhibit 1

Russia’s macro environment is supportive of a recovery in consumer demand 2007 2008 2009 2010E 2011E

Real GDP (% YoY) 8.1 5.6 -7.9 3.8 4.5

Private Consumption 13.9 10.8 -7.7 4.5 5.5

Unemployment Rate (%, ILO, eop) 6.1 7.8 8.2 7.2 6.7

CPI Inflation (Annual Average) 9.0 14.1 11.7 6.7 8.5Source: Morgan Stanley Economics team

compared with an average of ~60% in Western European countries. The beer market has gained 10ppt volume market share (based on equivalent units) since 2003, and we think this trend should continue in the medium to long term.

10

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Exhibit 2

In Russia, beer has consistently gained market share against spirits in the past five years

28% 30% 32% 33% 37% 38%

72% 70% 68% 67% 63% 62%

0%10%20%30%40%50%60%70%80%90%

100%

2003 2004 2005 2006 2007 2008

Ru

ssia

n V

iolu

me

ma

rke

t sh

are

(in

E

qu

iva

len

t un

it)

Beer Spirits Source: Euromonitor

In North and Western Europe, the Business Standardisation program should boost margins by ~50-80bps a year for the next five years. Carlsberg recently reiterated its medium-term group margin target of 20%, including a 15-17% margin target in N&W Europe. We forecast 16% EBIT margin in N&W Europe in FY14 with 50-80bps annual margin improvement from the Business Standardisation program.

We expect Carlsberg to deliver the fastest three-year CAGR in net sales and profits among the global brewers. Over the next three years, we forecast Carlsberg to grow organic net sales by 6-7%, against peers at 3.5-6.5%, thanks to Russian volume growth and strong margin expansion from N&W Europe. On our forecasts, Carlsberg will also deliver the fastest three-year CAGR in profit among the global brewers, at 22%. We expect Carlsberg to grow profits by ~12% versus peers at 6.5-10.5%, driven by higher margins in N&W Europe.

Exhibit 3

We are below consensus EPS for FY10e but above for FY11e

0

10

20

30

40

50

60

FY09 FY10e FY11e FY12e

ModelWare EPS (DKr) Consensus EPS (DKr)§

New MW EPS Consensus

We are 4% below consensus for FY10e but 6% above for FY11e

Source: Company data, FactSet, Morgan Stanley Research estimates (e)

Potential Catalysts

1Q CY11 – Potential government decision on restricting the sale of beer above 5% alcohol via kiosks

21 Feb 2011 – Preliminary FY10 results

11 May 2011 – 1Q11 results

Exhibit 4

We expect Carlsberg to grow sales and profit faster

Three-year CAGR

(CY11e-CY13e)

Organic net sales growth

Carlsberg (%) 6.0

ABInBev (%) 4.5

Heineken (%) 3.4

SABMiller (%) 5.9

Organic profit growth

Carlsberg (%) 12.8

ABInBev (%) 9.5

Heineken (%) 9.4

SABMiller (%) 9.7 Source: Morgan Stanley Research estimates

The shares should rerate towards ABI and SAB in the medium term, in our view. Given the robust earnings outlook, we argue that Carlsberg should trade more in line with ABI and SAB in the medium term, as higher earnings growth offsets the discount for Russia exposure that we believe should apply in the long run. We forecast a 19% three-year EPS CAGR for Carlsberg, against 15-18% for the other global brewers.

Our bull case scenario implies low double-digit organic net sales growth in FY11 versus our base case of ~7%. This could come from higher than expected pricing in N&W Europe and Russia, more than covering raw material cost pressure. Our bull case valuation of DKr 770 implies a target multiple of 16.5x CY11e.

Our base case target multiple of 15.5x Cal 11 P/E would bring the stock closer to ABI and SABMiller, which are currently trading at 15-17x. This implies more than a two-point rerating from the current valuation of 13x.

11

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Biotech & Medical Technology EU Austerity Measures: Does Past Data Predict Future Performance?Morgan Stanley & Co.

International plc+

Michael Jungling [email protected]

Our View Market View

We see a risk that further EU austerity measures lead to material cuts in government healthcare budgets. Data from the previous two recessions in Europe shows that most countries experience year-on-year reductions in healthcare expenditure within two years of negative GDP growth. The recession that ended in 3Q 2009 therefore suggests headwinds to health spend in 2011 and 2012. We are cautious on the reimbursed portion of our coverage universe that is paid by the government, especially EU Pharma Distribution, Ostomy and Incontinence sub-sectors. As such, we have Underweight ratings on Celesio and Coloplast.

The market is discounting no impact from EU austerity measures across the most exposed EU medtech companies – our bear case implies -5-15% downside. While the potential impact of EU austerity measures is recognized by investors, we feel that consensus is not reflecting the risk in its numbers. Our bear case scenarios for each stock reflect the potential impact from healthcare budget declines and imply between -5% and -15% downside to consensus estimates. We therefore see downside risk should past observations on healthcare spending materialize over the next 12-24 months.

What’s in the Price Government budget cuts put our bear case EPS forecasts well below consensus estimates

0.4% 0.5%

-1.2%-1.0%

-1.4%-1.2%-1.0%-0.8%-0.6%-0.4%-0.2%0.0%0.2%0.4%0.6%

CLSGn.DE COLOb.CO

MS Sales vs. Consensus MS Bear Case Sales vs. Consensus

Source: FactSet (Consensus), Morgan Stanley Research estimates .

-7.1%

4.0%

-12.4%

-4.5%

-14.0%-12.0%-10.0%

-8.0%-6.0%-4.0%-2.0%0.0%2.0%4.0%6.0%

CLSGn.DE COLOb.CO

MS EPS vs. Consensus MS Bear Case EPS vs. Consensus

Source: FactSet (consensus), Morgan Stanley Research estimates

Past experience suggests 2011 could be the toughest year for healthcare spending To understand the risk that the financial crisis poses to European healthcare and the timing of any cuts, we refer to a McKinsey & Company report commissioned by the UK Department of Health in 2009, the results of which were released by the Coalition government in 2010. Historical data shows that in the majority of European countries, healthcare spend declines year on year within two years of negative GDP growth (Exhibit 1).

During the oil crisis of 1980-83, 77% of European countries recorded a decline in healthcare spend within two years, while during the post Soviet destabilization between 1988 and 1993, the figure was 59% of countries. Note that we

have not yet seen any material healthcare spending cuts in 2010 for most European countries, including the largest markets of Germany, the UK, France and Italy. However, Germany has made some adjustments to its pharmaceutical spend, by asking pharma companies to give larger rebates, while the UK has cut the healthcare capital budget.

Most European countries exited the recession in 3Q 2009 (Exhibit 2). In our view, it should not be surprising therefore that governments had little time to adjust cost bases in 2010, and that 2011 could well be a tougher year for European healthcare spending. This would be within the two-year time frame highlighted in the McKinsey report. As a result, we believe it is prudent for investors to take a cautious view on Europe in 2011.

12

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Exhibit 1

% of EU countries with negative YOY healthcare growth within two years of negative GDP growth

77%59%

23%41%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Oil Crisis (1980-83) Post Soviet Destabilization(1988-93)

Negative Healthcare Growth No Healthcare Decline

Source: ‘Achieving World Class Productivity in the NHS 2009/10 – 2013/14: Detailing the Size of the Opportunity’ March 2009, McKinsey & Company, Morgan Stanley Research.

Exhibit 2

European GDP growth – quarterly data

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

Mar-06 Sep-06 Mar-07 Sep-07 Mar-08 Sep-08 Mar-09 Sep-09 Mar-10 Sep-10

France Germany Greece Italy Portugal Spain UK

Source: Morgan Stanley Research

All reimbursed names would be affected, but we see most downside for Celesio and Coloplast. Although budget constraints could affect several of our reimbursed medical device stocks, including Elekta (reduction in capital equipment spend) and Smith & Nephew (reduced procedure volumes), we are particularly cautious on the EU Pharma Distribution and Ostomy and Incontinence sub-sectors. We are therefore Underweight Celesio and Coloplast. Our bear case scenario for each stock assumes healthcare budget declines in 2011, suggesting downside to consensus estimates of at least -15% for Celesio and -5% for Coloplast.

Celesio can no longer offset downside from reimbursement cuts. Celesio has faced very negative and broad reimbursement headwinds over the past two to three years, and one could reasonsably expect that the reimbursement cycle should ease over the next few years. However, given Celesio’s material exposure to a number of

European countries with large 2010 budget deficits, including the UK (-9.2% of nominal GDP), France (-7.7%) and Germany (-4.2%), we feel the risk of further ad-hoc reimbursement changes is high. Although there is little news flow on pending reimbursement cuts – with the exception of the UK – we feel the market is not adequately reflecting the risk of healthcare reform in current valuations. Celesio’s profitability has already been materially reduced in the past two years by ad hoc reimbursement challenges, leaving little room for organic improvements to offset structural downside. We now expect the company’s two-year EPS CAGR of +8% to be below that of the EU market consensus of +10%, and see downside risk to the shares as investors assign a discount to the current market relative P/E of ~1x to closer to 0.8x.

Coloplast derives 60-70% of sales from prices regulated by EU governments. In Europe (73% of group sales) the majority of products that Coloplast sells – ostomy bags, intermittent catheters and wound dressings – are used within the community setting (often dispensed through pharmacies) and are more typically directly price regulated. We estimate that 60-70% of Coloplast’s revenues are exposed to price cuts that could result from further European austerity measures, making it the most exposed medical device company under our coverage. Our bear case assumes additional 2% pricing cuts, which reduce sales growth by c.1-1.5% a year and deliver a FY11-14e EPS CAGR of 9.7% – 220bps lower than our base case. In addition, our residual income model – which calculates the implied long-term growth rate for Coloplast based on consensus estimates – shows that since Q4 FY09 the implied market view on long-term growth has declined by 29%, while the share price has appreciated by 65%. On this basis, the stock looks expensive relative to its recent history.

Exhibit 3

Coloplast – the implied long-term growth rate is declining but the share price is increasing.

0

100

200

300

400

500

600

700

800

900

4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 *

2002 2003 2004 2005 2006 2007 2008 2009 2010

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

COLOPLAST- Price Implied long - term growth rate

Source: Morgan Stanley Research

13

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Brands Is Big Becoming the New Beautiful? Morgan Stanley & Co.

International plc+

Lousie Singlehurst [email protected]

Our View Market View

‘Big’ is becoming more beautiful within brands. We believe that size is going to be a more dominant theme over the next five years as brands with the fastest growth are those with a global footprint, best-in-class product and customer service and strong brand awareness (particularly among emerging market consumers). This requires investment. We like the merits of a multibrand structure – sourcing, distribution, advertising and retail efficiencies – and think these will drive superior EBIT growth. With brands increasing their exposure to non-core categories, we explore a scenario in which Richemont expands the leather goods category within Cartier.

The market has tended to favour monobrands over large multibrands. Historically, investors have favoured monobrands for their superior growth prospects (under penetrated expansion) and potential returns (large groups typically contain sub-scale loss making brands). The market has two main concerns about the multibrand structure, in our view: 1) the inherent risk of M&A activity – strong niche brands within luxury are rare and may command a high price premium; and 2) the ability to maintain brand integrity within a large group. However, we think these preferences will begin to reverse.

Richemont – potential earnings uplift from soft category expansion scenario

1.50

2.00

2.50

3.00

3.50

4.00

2012e 2013e 2014e 2015e 2016e

EP

S €

Base Case Scenario

Source: Morgan Stanley Research estimates

We see scope for new revenue opportunities at Cartier within the soft luxury category, taking advantage of the brand’s global recognition and retail footprint

There has been no intention indicated by management to move more extensively into the soft category at Cartier, but the segment does exist in a minor capacity

The merits of a well-run leather and accessory brand – higher gross margin, higher store footfall – could have a halo effect at Cartier, in our view

The greatest challenge is to introduce a new product category and not dilute the brand image

We expect the bigger brands to outperform over the next five years. Major brands are increasing their exposure to non-core categories; for example, Watches (Gucci and Burberry), Leather goods (Bulgari and Tiffany) and Jewellery (Louis Vuitton, Chanel). Expansion into categories such as perfumes and sunglasses is now commonplace. In this context, we look at a scenario in which Richemont expands the leather goods category within Cartier.

Richement is likely to explore revenue opportunities in the soft category. Richemont has exposure to the soft category through smaller brands (Lancel, Chloe, Dunhill) but we see scope for new revenue opportunities, taking advantage of Cartier’s global brand recognition and retail footprint (c.275 stores globally). At some point, we would expect Richemont to explore the revenue opportunities of the

soft category within the group – particularly following the acquisition of net-a-porter, the leading luxury online portal, announced earlier this year. The website already sells products from brands such as Chloe, and the company has announced the launch of Mr Porter, dedicated to men’s product, which will include Dunhill.

In our scenario analysis, leather goods and accessories reach 20% of brand sales by 2016. This assumes that Richemont announces the expansion of the soft category (leather and accessories) at Cartier in 2011. We anticipate it would take time to build scale in this division, but believe the execution risk would be reduced, given Cartier would introduce new product within its own directly operated stores (using wall space not used for watches and jewellery) and would be able to monitor immediate customer feedback

14

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

through the retail channel. We assume initial investment in 2011 and 2012, and leather goods and accessories accounting for 20% of brand sales by 2016 (fiscal year end) with a 30% operating margin (for reference, Bulgari’s accessories division is 10% of brand sales in 2010e). This increases Richemont’s earnings by 15% in FY2016e and enhances group margin by ~250 bp (we assume a ~30% operating margin for the product category).

Over the medium term, we believe the greater demands of the luxury consumer – service, store experience and choice – coupled with rising investment demands, will become a greater challenge to the monobrands. We see Hermes as an exception (with a reported EBIT margin of 24% in 2009), reflecting its leading position within the high-end luxury category.

Exhibit 1

Greater demands of the luxury consumer will mean more pressure for the monobrands, in our view

0

50

100

150

200

250

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

e

EB

IT G

row

th (10

-yr be

nchm

ark)

LVMHHermesSwatch

Richemont

Tiffany

Bulgari

Source: Company data, Morgan Stanley Research estimates (e) *Hermes is not covered, FactSet consensus used for 2010e

Exhibit 2

Brand exposure to non-core categories B rand Core competence Brand extension

Tiffany Jewellery Leather goods

Louis Vuitton Leather goods & accessories High-end jewellery Watches

Bulgari Jewellery Watches Perfume Sunglasses Leather goods

Cartier Jewellery Small leather goods

Mont Blanc Writing instruments Jewellery, leather goods

Dunhill Leather goods & accessories Watches Perfume Source: Morgan Stanley Research

Exhibit 3

Our preferred stocks are within the soft luxury category and the larger groups. We least favour the more cyclical hard luxury brands and those that lack scale (4 top picks, 4 least preferred)

-60%

-40%

-20%

0%

20%

40%

60%

LVMH Adidas PPR Pandora Bulgari Puma Swatch Richemont

Ris

k R

ew

ard

Pa

yoff

Ma

trix

Base Bear Bull

For valuation methodology and risks associated with any price targets above, please email [email protected] with a request for valuation methodology and risks on a particular stock. Source: Morgan Stanley Research estimates

15

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Building & Construction Is EM Exposure an Earnings Driver or an Earnings Risk in 2011? Morgan Stanley & Co.

International plc+

Alejandra Pereda [email protected]

Our View Market View

We expect the earnings contribution from emerging markets to stagnate on a growing cost/price imbalance. Booming growth in emerging markets is pushing up the cost of energy and raw materials, and we expect cement producers to face 5-10% cost inflation in 2011. At the same time, large net capacity additions will lower utilization rates and make it harder for the industry to pass on higher costs. We therefore expect margins to fall in most emerging markets over the next 12 months, denting earnings growth for global cement companies.

Emerging markets will remain the engine of earnings growth until developed markets recover. Consensus estimates do not appear to reflect our concerns over cost and pricing in emerging markets. Thus, for the global cement players, such as Holcim, our 2011 and 2012 EBITDA expectations are 4-10% below consensus. Moreover, Holcim is still trading at a premium to peers, based on its emerging market exposure.

What’s in the Price Little concern over EM earnings delivery – Holcim has the most EM exposure and trades at a material premium to peers, even stripping out India

8

12

16

20

2010e 2011eHolcim EV/EBIT Holcim EV/EBIT ex India Cement EV/EBIT ex Holcim

Holcim (adjusted for India subsidiaries) trades at a substantial premium to other cement stocks, as investors seek EM growth. Holcim is also on a premium to locally traded EM stocks, and we see material downside potential if EM disappoint.

Source: FactSet (price data), Morgan Stanley Research estimates .

We are worried about a cost/price imbalance in emerging markets next year. With energy and distribution accounting for >50% of total cost in most emerging markets, cost inflation per tonne looks likely to remain above 5% throughout 2011. We see a risk that the industry will be unable to fully offset this increase through higher volume or prices. Pricing power in the industry is diminishing, for three key reasons:

1) Market fragmentation. Many emerging markets remain substantially less consolidated than developed markets, with small regional players still playing a material role and often prioritising market share over profitability.

2) New capacity coming on stream. We expect the influx of new plants to significantly reduce utilization rates and lead to further market fragmentation. This – coupled with the lower cash costs of new plants and the need to generate cash to pay down debt incurred in building them – could intensify price competition until utilisation recovers. We believe this could take four to eight quarters, depending on the strength of local demand.

3) Low freight costs support global trade. Average freight cost per ton remains $20 on routes between Asia, Europe and Africa, according to International Cement magazine, which

16

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

compares to >$80 at the 2007/08 peak. Freight capacity is also in good supply, allowing for profitable global trade to and from destinations that were not viable three years go. This adds to overall price competition.

These factors are likely to weigh on margin recovery for the global cement players in 2011. We expect Heidelberg Cement to be less affected (+290bp growth) as it has less emerging market exposure, while Holcim shows the smallest margin increase, on our forecasts, at only 60bp in 2009-2012.

Exhibit 1

Energy (mainly coal & petcoke) and distribution are >50% of cement costs in EM vs <40% in DM

% of total cost

0%

20%

40%

60%

80%

100%

Mature India Brazil/MX MiddleEast

Indonesia

Energy Transportation Raw Materials Others* Source: Company data (2009), Morgan Stanley Research

Potential Catalysts

4Q 2010 and 1H 2011 earnings are likely to show a negative cost/price balance in EM This would be the second or third quarter in a row, and could prompt investors to question near-term EM earnings growth, particularly as energy and raw materials prices trend higher

4Q 2010 and 1Q 2011 should see significant earnings growth in DM The easy comp and mild autumn should help the US and Western Europe deliver robust volume growth, neutral price/cost balance and better margins on improved cost-cutting visibility

Ongoing coal, power and oil prices will see cement companies raise energy cost guidance for 2011 Holcim has already revised guidance, announcing a 2H10 expected impact of >5% and 2011 energy per ton guidance of +4% on a group average

Exhibit 2

St Gobain and HeidelbergCement – large exposure to DM and our top picks in building materials for 2011

PT

BEAR

BASE

BULL

currentprice

7%14%

21%

-12%-9%

-60%

-40%

-20%

20%

40%

60%

80%

100%

St Gobain Lafarge HeidelbergCement CRH Holcim

For valuation methodology and risks associated with any price targets above, please email [email protected] with a request for valuation methodology and risks on a particular stock. Source: FactSet, Morgan Stanley Research estimates

17

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Business & Employment Services Can HomeServe Roll Out Its UK Business Model Successfully in the US? Morgan Stanley & Co.

International plc+

Jessica Alsford [email protected]

Our View Market View

HomeServe successfully replicates its UK home emergency services business model in the US. The growth trajectory is in line with that achieved in the UK at the same point of its business life cycle, with US policies increasing from 756k in FY10 to 13.8m in FY14. HomeServe’s marketing efforts serve to educate the US consumer, improving awareness of home emergency insurance. This scenario is factored into our bull case, which implies c.165% upside potential to the shares. Our price target of 566p (c.24% upside) assumes a 15% probability of the bull case (and 10% probability of the bear case).

HomeServe does not achieve perfect execution in the US. Roll-out of the US operations is steady, but not perfect (consensus forecasts are in line with our base case). Growth is slower than that experienced in the UK, due to the fragemented Utilities market and lack of consumer awareness of home emergency services. According to our ‘What’s In the Price’ analyser, the market is currently pricing in an earnings growth rate of only c.1% post-FY13 (see chart).

What’s in the Price HomeServe’s current share price implies a growth rate of only ~1% post FY13

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 *

2002 2003 2004 2005 2006 2007 2008 2009 2010

-20%

-15%

-10%

-5%

0%

5%

10%HOMESERVE- Price Implied long - term grow th rate

Risk-Reward Scenarios

210p Bear Case

11.5x FY14 (March) Bear

Case EPS of 19p (-3% EPS

CAGR FY10-14e)

485p Base Case

14.0x FY14 (March) Base

Case EPS of 34.5p (12%

EPS CAGR FY10-14e)

1,210p Bull Case

14.9x FY14 (March) Bull

Case EPS of 81p (39%

EPS CAGR FY10-14e)

Earnings pressure in the UK, slower US roll-out. The UK business loses market share to the AA. Customer numbers fall by 3% pa, whilst prices also decline by the same amount. The US strategy works, but it is slower to make progress.

Slowing growth in UK, steady growth in US and CE. UK EBITA growth slows to +6% (FY10-14e) compared to +18% in FY05-10. HomeServe continues to increase its penetration and profitability in the US and CE, with US penetration increasing +140bp to 7.2% and EBITA to £26.1m (from £1.5m in FY10). This results in low double-digit EPS growth over the next four years.

Successful growth strategy in US and UK. US affinity partners treble to 64m by 2014, with the penetration rate reaching 12% (vs 12.3% in the UK). Revenue per customer increases from $101 in the base case to $115 in the bull case, driven by multiple policies and price inflation. In the UK, HomeServe achieves +8% customer growth pa.

Source: FactSet (price data), Morgan Stanley Research estimates

18

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Potential Catalysts

January / February 2011 3Q11 IMS will provide an update on progress in the US, including efforts to increase penetration

Ad hoc HomeServe doubled its US Affinity Partner (AP) households this year by aquiring existing policies and entering into AP marketing agreements. We expect this kind of activity to continue in 2011 and to positively impact the shares

Our bull case scenario assumes a successful US growth strategy. The US market is five times the size of the UK in terms of households, and market penetration is much lower at c.10% (vs. 32% in the UK). Over the next three years, HomeServe achieves perfect execution in this market, capitalizing on the progress it has made so far (total number of US policies has grown by an average 20% p.a. since 2005 to 756k in 2010, while AP households have increased from 0.5m to 20m).

HomeServe grows its US operations through acquisitions and AP marketing agreements. HomeServe has a strong growth track record in the UK under its current CEO and founder. It leverages its expertise in this market to capitalize on the US opportunity through acquisitions of existing policy books, new marketing agreements with APs and increased brand awareness.

The business grows customer numbers by educating US consumers on the benefits of home emergency cover. Consumer education is key to the business’s success. Our AlphaWise survey showed that initially only 4% of non-policy holders surveyed said they were extremely or quite likely to take out a policy. However, once respondents were made aware of HomeServe’s offering, 31% said they would consider taking out a policy.

US EBITA grows rapidly from £1.5m in FY10 to £166m in FY14. This assumes that HomeServe increases its number of US Affinity Partner households from 20m at present to 64m in FY14. The penetration of this marketable consumer base also increases from 5.8% in FY10 to 12.0% in FY14.

Beyond FY14, the US opportunity is even bigger. In our blue sky scenario, we assume that the US business reaches the levels of penetration and income per customer that HomeServe currently achieves in the UK. This alone would mean that the US business generates c. £390m of EBITA – almost four times FY10 group EBITA of £104m.

Exhibit 1

The US market is much less developed than the UK

0 20 40 60 80 100 120 140

UK

US

HomeServe policies relative to total country households (mn)

FY10 FY14e - Base FY14e - Bull Potential

Source: Company data, Morgan Stanley Research e = Morgan Stanley Research estimates

Exhibit 2

Bull case assumes the same household penetration rate in US as in UK after 12 years of operations

UK 2010

UK 2014e

US 2010 US 2014e

US Bull Case

0%

5%

10%

15%

20%

25%

30%

35%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

No. of yrs of operation

No

. of

polic

ies

as

% o

f Ho

use

hol

ds

Source: Morgan Stanley Research estimates

Exhibit 3

Replicating the UK success story increases US bull case EBITA by c.180%

0

100

200

300

400

500

600

FY14 group basecase EBITA

FY14 base case+ US bull case

FY14 base case+ US bull case +

US blue sky

EB

ITA

(£m

n)

+85%

+240%

+85%

Source: Morgan Stanley Research estimates

19

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Capital Goods Will Grid Investment Recover in 2011? Morgan Stanley & Co.

International plc+

Ben Uglow [email protected]

Our View Market View

An upside surprise on grid investment drives expectations higher for ABB and Schneider. Grid investment will be the key upside surprise for 2011, we believe, and will be at least double the growth rates in consensus earnings models. We expect international suppliers to surprise the market in 1H11 by winning large UHV contracts – even in China. Although some pricing pressure will remain next year, it will not be as acute as consensus currently believes.

Grid investment will remain subdued and transformer pricing will fall further. The prevailing view embedded in consensus is that grid investment will remain subdued in 2011, with growth rates in low to mid single digits. The Chinese market will remain dominated by local suppliers. Internationally, the secular shift in transformer production will continue to depress prices, driving transformer margins lower.

What’s in the Price ABB shares are pricing in weakness in grid investment in 2011

Morgan Stanley Risk-Reward (left) versus Probabilities Implied by Option Prices (right)

Source: FactSet (price data), Morgan Stanley Research estimates

Four drivers of higher grid investment

1. We think State Grid spending in China will come back strongly next year, an increase from Rmb330bn in 2010 to Rmb370bn (+12%). Chinese companies alone will not be able to meet additional demand in the UHV segment, and this could lead to large contract awards – which would be a surprise – for ABB, Alstom and Siemens, in particular.

2. Commercial adoption of so-called ‘smart grid’ applications will begin in earnest in 2011. In a recent presentation, Schneider Electric showed that there could be

an incremental opportunity of €40bn+ in smart grid between 2015 and 2020. We see the single biggest market opportunity in distribution automation: Pike Research estimates the global market increases from $2.2bn in 2010 to $8.8bn by 2012.

3. In the US, SPX (the largest domestic transformer manufacturer) recently indicated that demand was bottoming out and that its transformer backlog had increased by ~14%. The Edison Electric Institute, the largest industry association in the US, expects transmission investment to increase from $9.7bn in 2010 to $12.3bn in 2013, an 8.3% CAGR.

20

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

4. Globally, we suspect that the pricing risks are overstated. The only Asian player where there has been clear evidence of new competition is Hyundai Heavy (covered by Sangkyoo Park) which generates some $2.7bn in revenues globally in this market. Yet, its recent quarterly results showed operating margins expanding to 15.8% from 12.4% the previous year. Although we are concerned about Chinese competitors in the medium term, we believe that demand recovery will drive prices higher in 2011.

Long-term drivers of grid investment We think the case for another investment upcycle in transmission and distribution infrastructure is quite compelling. In the US, the average age of substations exceeds 40 years, already more than the designed shelf-life of these products. In China, the 12th five-year plan envisages investment in UHV alone of Rmb270-300bn, in addition to the Rmb370bn of ‘normal’ investment. In Europe, evolution of offshore wind is leading to substantial new contract awards, and on the distribution side there is ongoing impetus from solar PV installation (despite short-term headwinds).

Exhibit 1

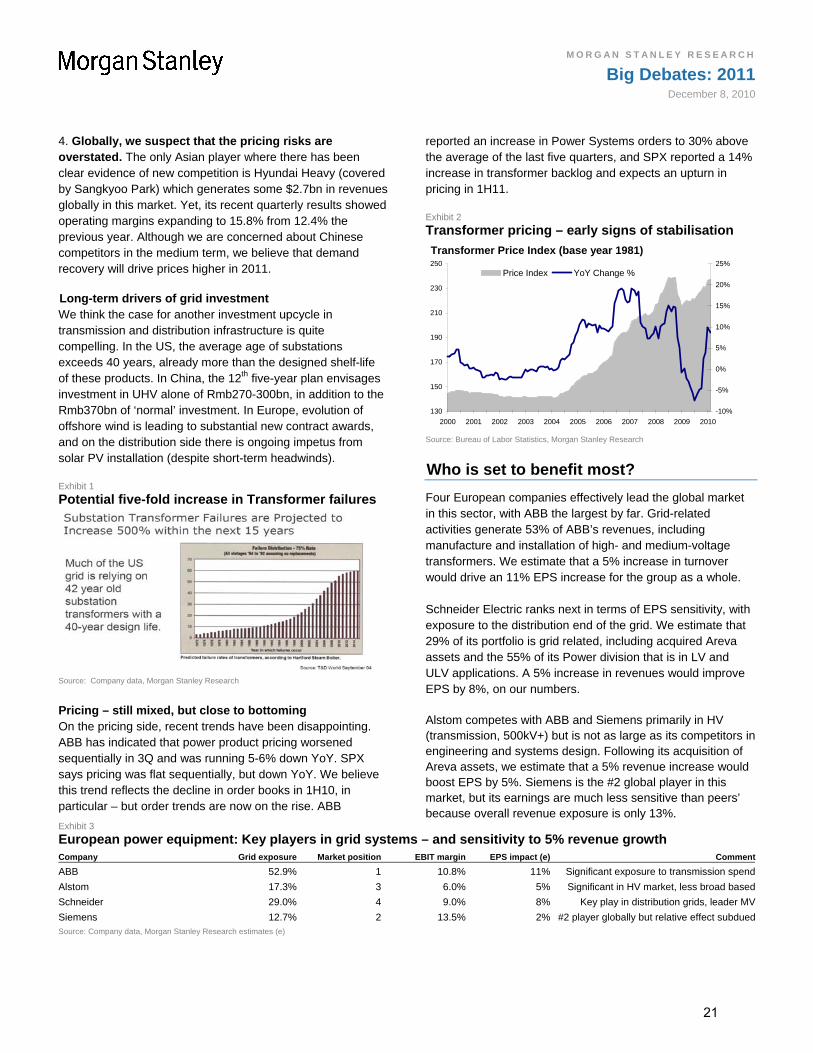

Potential five-fold increase in Transformer failures

Source: Company data, Morgan Stanley Research

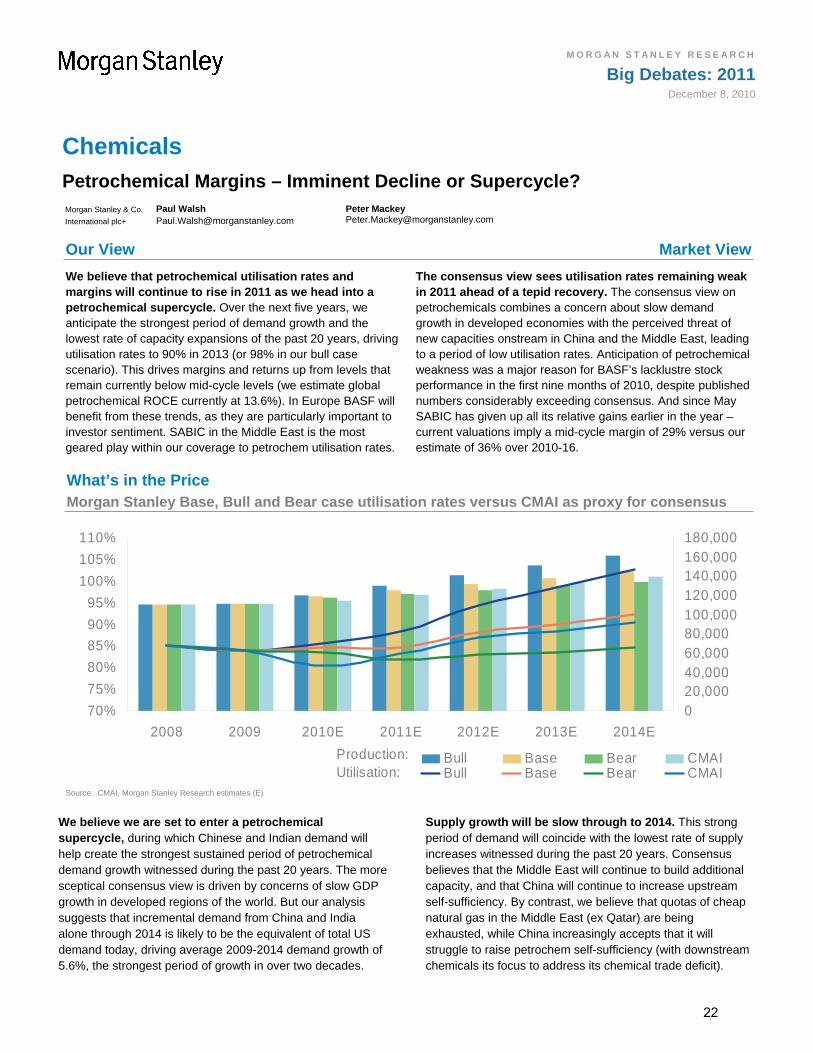

Pricing – still mixed, but close to bottoming On the pricing side, recent trends have been disappointing. ABB has indicated that power product pricing worsened sequentially in 3Q and was running 5-6% down YoY. SPX says pricing was flat sequentially, but down YoY. We believe this trend reflects the decline in order books in 1H10, in particular – but order trends are now on the rise. ABB

reported an increase in Power Systems orders to 30% above the average of the last five quarters, and SPX reported a 1increase in transf

4% ormer backlog and expects an upturn in

pricing in 1H11.

Transformer pricing – early signs of stabilisation Exhibit 2

Transformer Price Index (base year 1981)

130

150

170

190

210

230

250

2009 2010

-10%

-5%

0%

5%

10%

15%

20%

25%Price Index

2000 2001 2002 2003 2004 2005 2006 2007 2008

YoY Change %

Source: Bureau of Labor Statistics, Morgan Stanley Research

Who is set to benefit most?

Four European companies effectively lead the global min this sector, with ABB the largest by far. Grid-relatedactivities generate 53% of ABB’s revenues, including manufacture and installation of high- and medium-voltage transformers. We estimate that a 5% increase in turnover

arket

would drive an 11% EPS increase for the group as a whole.

t

se in revenues would improve EPS by 8%, on our numbers.

uld

han peers’ because overall revenue exposure is only 13%.

Schneider Electric ranks next in terms of EPS sensitivity, with exposure to the distribution end of the grid. We estimate tha29% of its portfolio is grid related, including acquired Arevaassets and the 55% of its Power division that is in LV and ULV applications. A 5% increa

Alstom competes with ABB and Siemens primarily in HV (transmission, 500kV+) but is not as large as its competitors inengineering and systems design. Following its acquisition of Areva assets, we estimate that a 5% revenue increase woboost EPS by 5%. Siemens is the #2 global player in this market, but its earnings are much less sensitive t

Exhibit 3

European power equipment: Key players in grid systems – and sensitivity to 5% revenue growth Company Grid exposure Market position EBIT margin EPS impact (e) Comment

on spendABB 52.9% 1 10.8% 11% Significant exposure to transmissi

Alstom

Schneid

17.3% 3 6.0% 5% Significant in HV market, less broad based

er

Siemens

29.0% 4 9.0% 8% Key play in distribution grids, leader MV

12.7% 2 13.5% 2% #2 player globally but relative effect subduedSource: Company data, Morgan Stanley Research estimates (e)

21

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Chemicals Petrochemical Margins – Imminent Decline or Supercycle? Morgan Stanley & Co.

International plc+

Paul Walsh [email protected]

Peter Mackey [email protected]

Our View Market View

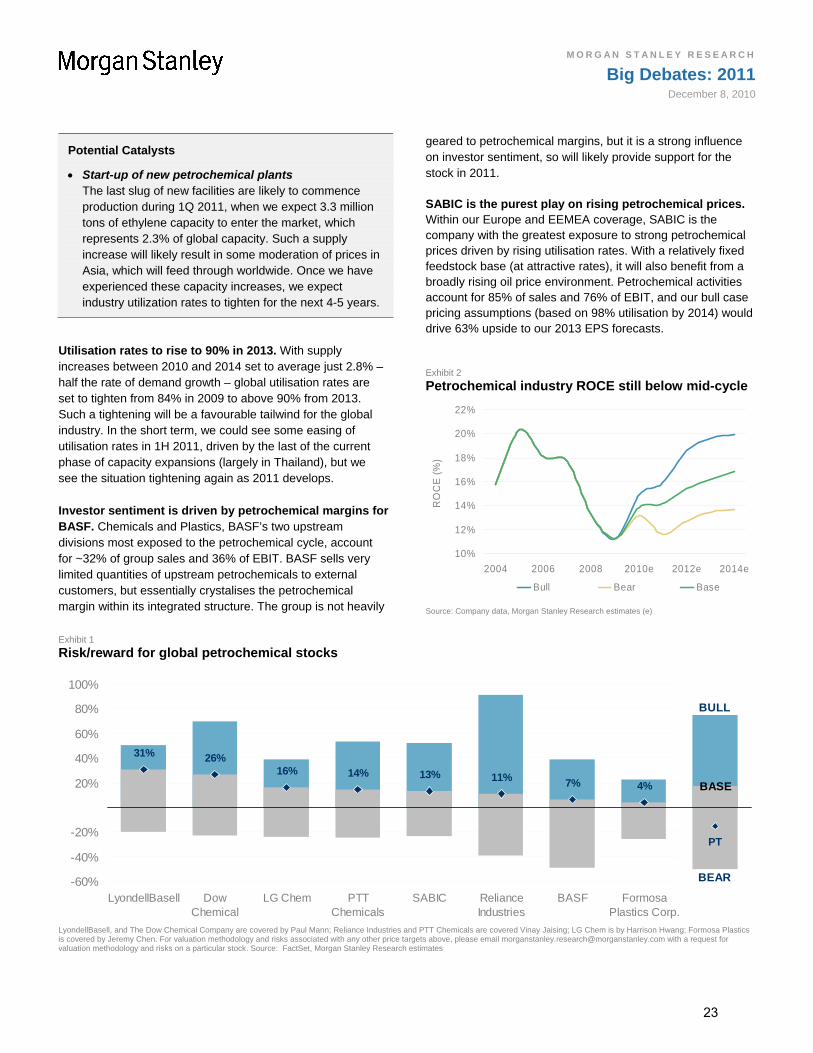

We believe that petrochemical utilisation rates and margins will continue to rise in 2011 as we head into a petrochemical supercycle. Over the next five years, we anticipate the strongest period of demand growth and the lowest rate of capacity expansions of the past 20 years, driving utilisation rates to 90% in 2013 (or 98% in our bull case scenario). This drives margins and returns up from levels that remain currently below mid-cycle levels (we estimate global petrochemical ROCE currently at 13.6%). In Europe BASF will benefit from these trends, as they are particularly important to investor sentiment. SABIC in the Middle East is the most geared play within our coverage to petrochem utilisation rates.

The consensus view sees utilisation rates remaining weak in 2011 ahead of a tepid recovery. The consensus view on petrochemicals combines a concern about slow demand growth in developed economies with the perceived threat of new capacities onstream in China and the Middle East, leading to a period of low utilisation rates. Anticipation of petrochemical weakness was a major reason for BASF’s lacklustre stock performance in the first nine months of 2010, despite published numbers considerably exceeding consensus. And since May SABIC has given up all its relative gains earlier in the year – current valuations imply a mid-cycle margin of 29% versus our estimate of 36% over 2010-16.

What’s in the Price Morgan Stanley Base, Bull and Bear case utilisation rates versus CMAI as proxy for consensus

70%

75%

80%

85%

90%

95%

100%

105%

110%

2008 2009 2010E 2011E 2012E 2013E 2014E

020,00040,00060,00080,000100,000120,000140,000160,000180,000

Bull Base Bear CMAIBull Base Bear CMAIUtilisation:

Production:

Source: CMAI, Morgan Stanley Research estimates (E)

We believe we are set to enter a petrochemical supercycle, during which Chinese and Indian demand will help create the strongest sustained period of petrochemical demand growth witnessed during the past 20 years. The more sceptical consensus view is driven by concerns of slow GDP growth in developed regions of the world. But our analysis suggests that incremental demand from China and India alone through 2014 is likely to be the equivalent of total US demand today, driving average 2009-2014 demand growth of 5.6%, the strongest period of growth in over two decades.

Supply growth will be slow through to 2014. This strong period of demand will coincide with the lowest rate of supply increases witnessed during the past 20 years. Consensus believes that the Middle East will continue to build additional capacity, and that China will continue to increase upstream self-sufficiency. By contrast, we believe that quotas of cheap natural gas in the Middle East (ex Qatar) are being exhausted, while China increasingly accepts that it will struggle to raise petrochem self-sufficiency (with downstream chemicals its focus to address its chemical trade deficit).

22

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Potential Catalysts

Start-up of new petrochemical plants The last slug of new facilities are likely to commence production during 1Q 2011, when we expect 3.3 million tons of ethylene capacity to enter the market, which represents 2.3% of global capacity. Such a supply increase will likely result in some moderation of prices in Asia, which will feed through worldwide. Once we have experienced these capacity increases, we expect industry utilization rates to tighten for the next 4-5 years.

Utilisation rates to rise to 90% in 2013. With supply increases between 2010 and 2014 set to average just 2.8% – half the rate of demand growth – global utilisation rates are set to tighten from 84% in 2009 to above 90% from 2013. Such a tightening will be a favourable tailwind for the global industry. In the short term, we could see some easing of utilisation rates in 1H 2011, driven by the last of the current phase of capacity expansions (largely in Thailand), but we see the situation tightening again as 2011 develops.

Investor sentiment is driven by petrochemical margins for BASF. Chemicals and Plastics, BASF’s two upstream divisions most exposed to the petrochemical cycle, account for ~32% of group sales and 36% of EBIT. BASF sells very limited quantities of upstream petrochemicals to external customers, but essentially crystalises the petrochemical margin within its integrated structure. The group is not heavily

geared to petrochemical margins, but it is a strong influence on investor sentiment, so will likely provide support for the stock in 2011.

SABIC is the purest play on rising petrochemical prices. Within our Europe and EEMEA coverage, SABIC is the company with the greatest exposure to strong petrochemical prices driven by rising utilisation rates. With a relatively fixed feedstock base (at attractive rates), it will also benefit from a broadly rising oil price environment. Petrochemical activities account for 85% of sales and 76% of EBIT, and our bull case pricing assumptions (based on 98% utilisation by 2014) would drive 63% upside to our 2013 EPS forecasts.

Exhibit 2

Petrochemical industry ROCE still below mid-cycle

10%

12%

14%

16%

18%

20%

22%

2004 2006 2008 2010e 2012e 2014e

RO

CE

(%

)

Bull Bear Base

Source: Company data, Morgan Stanley Research estimates (e)

Exhibit 1

Risk/reward for global petrochemical stocks

31% 26%16% 14% 13% 11% 7% 4%

PT

BASE

BEAR

BULL

-60%

-40%

-20%

20%

40%

60%

80%

100%

LyondellBasell DowChemical

LG Chem PTTChemicals

SABIC RelianceIndustries

BASF FormosaPlastics Corp.

LyondellBasell, and The Dow Chemical Company are covered by Paul Mann; Reliance Industries and PTT Chemicals are covered Vinay Jaising; LG Chem is by Harrison Hwang; Formosa Plastics is covered by Jeremy Chen. For valuation methodology and risks associated with any other price targets above, please email [email protected] with a request for valuation methodology and risks on a particular stock. Source: FactSet, Morgan Stanley Research estimates

23

M O R G A N S T A N L E Y R E S E A R C H

Big Debates: 2011December 8, 2010

Clean Energy EDP Renovaveis: Further Capex Cuts Could Crystallize Value Morgan Stanley & Co.

International plc+

Allen Wells [email protected]

Andrew Humphrey [email protected]

Our View Market View

We believe further capex cuts at EDPR are possible and would be taken positively by the market. We think the market is too bearish on macro and regulatory drivers. Concerns over potentially dilutive expansion are real, though we see a possibility that further capex cuts in 2011 could crystallize value in the shares. We believe the shares would generate a Free Cash Flow Yield of 11% in 2012 and 13% in 2013, assuming management cuts all growth capex, other than for those assets currently under construction. Our assumptions on power prices are conservative, and we see the regulatory outlook as unlikely to deteriorate further.

The market is cautious on tariff cuts and growth dilution. Investors have been cautious on the Spanish government’s proposals to cut wind tariffs. Uncertainty persists here, but resolutions proposed to date have been fairly benign for the wind sector. We believe the shares are pricing in a 25% cut to Spanish tariffs (fixed, tariff, premium and tariff floor), and only inflationary increases in US power prices. Alternatively, we estimate the shares are pricing in cost of equity of 12.5%, or a blended WACC of 8.9%. While debt costs should rise over coming years, this is already reflected in our long-term cost of capital estimates, and we think this view is too bearish.

What’s in the Price The stock is pricing in a 25% reduction to Spanish tariffs and downside to US power prices

€7.40 (+91%)

€ 3.87€4.7 (+22%)

€8.4 (+117%)

0

1

2

3

4

5

6

7

8

9

Dec-09 Jun-10 Dec-10 Jun-11 Dec-11

€

Price Target (Dec-11) Historical Stock Performance Current Stock Price Risk-Reward Scenarios

€4.7 Bear Case

20x P/E on Bear Case

C2011 Adj. EPS of €0.239

€7.4 Base Case

30x P/E on Base Case

C2011 Adj. EPS of €0.249

€8.4 Bull Case

34x P/E on Bull Case

C2010 Adj. EPS of €0.244

Value of operating assets. No new capacity after 2010, fair value equals value of assets as of Dec-10. LT Spanish pool prices of €42 per MWh.

Solid growth, muted power price outlook. New capacity at ~1.2GW in 2010-12. Power hedges protect earnings in Spain from low pool prices in 2010. LT Spanish prices at €65/MWh. 20-27% EPS growth in 2010-12 on the impact from new capacity and higher power prices.

Accelerating new capacity growth, bullish power price recovery. 1.5-1.6GW pa installed in 2010-15. LT Spanish prices at €82/MWh by 2018, solid power prices across other regions.

Source: FactSet (price data), Morgan Stanley Research estimates

24

M O R G A N S T A N L E Y R E S E A R C H

The Big Debates: 2011December 8, 2010

Potential Catalysts

Early 2011 Spanish government to finalise tariff package for existing renewable energy assets, following discussion with the industry. Early draft already published

Mid-late 2011 Further capex cuts in 2011 and 2012 from wind developers. While this would naturally slow long-term growth, we believe it could substantially improve near-term cash generation

The market is too bearish on Spanish tariffs, in our view. While the issue of regulated tariffs for Spanish wind assets remains unresolved, we believe the market is pricing in too bearish a scenario. On our estimates, the shares reflect a 25% reduction to the tariff premium, fixed-tariff option, and to the guaranteed floor for wind, applied to all assets in the portfolio. Furthermore, the shares are pricing in no upside to average 2010 US power prices, which are ~10% lower than current blended levels reported by the company. While US wind farms currently selling power on the merchant market are not earning their cost of capital, we believe this is too bearish an expectation for the long term. Looked at another way, the current share price reflects a value for only the existing wind assets of €1.1m/MW – roughly 10% below replacement cost.

Further capex cuts are likely in this scenario. If the scenario outlined above plays out, we believe EDPR management would cut capex, rather than pursue dilutive capacity expansion. On our estimates, cutting capex to a minimum would put the shares on a FCF yield of 11% in 2012 and 13% in 2013, which we believe would be highly attractive for investors. Management has already cut capex materially in 2010, but it could instigate further cuts in the event that the broader macro environment does not improve (i.e. the Spanish government introduces larger cuts, or PPAs are not signed in the US). We view this as a potential catalyst for sentiment turning more positive on the shares.