berkshire hills bancorp, inc

TRANSCRIPT

BERKSHIRE HILLS BANCORP, INC.STRATEGIC TRANSFORMATION LAUNCH

MAY 18, 2021

FORWARD-LOOKING STATEMENTS

This document contains “forward-looking statements” within the meaning of section 27A of the Securities Act of 1933, as amended, and section 21E of the SecuritiesExchange Act of 1934, as amended. You can identify these statements from the use of the words “may,” “will,” “should,” “could,” “would,” “plan,” “potential,” “estimate,”“project,” “believe,” “intend,” “anticipate,” “expect,” “target” and similar expressions. There are many factors that could cause actual results to differ significantly fromexpectations described in the forward-looking statements. For a discussion of such factors, please see Berkshire’s most recent reports on Forms 10-K and 10-Q filedwith the Securities and Exchange Commission and available on the SEC’s website at www.sec.gov.

Further, given its ongoing and dynamic nature, it is difficult to predict what continued effects the novel coronavirus (COVID-19) pandemic will have on our business andresults of operations. The pandemic and the related local and national economic disruption may result in a continued decline in demand for our products and services;increased levels of loan delinquencies, problem assets and foreclosures; an increase in our allowance for credit losses; a decline in the value of loan collateral,including real estate; a greater decline in the yield on our interest-earning assets than the decline in the cost of our interest-bearing liabilities; and increasedcybersecurity risks, as employees increasingly work remotely. Accordingly, you should not place undue reliance on forward-looking statements, which reflect ourexpectations only as of the date of this document. Berkshire does not undertake any obligation to update forward-looking statements.

NON-GAAP FINANCIAL MEASURES

This presentation contains both financial measures based on accounting principles generally accepted in the United States (“GAAP”) and non-GAAP based financialmeasures, which are used where management believes them to be helpful in understanding the Company’s results of operations or financial position. Reconciliationsof these non-GAAP financial measures to the most comparable GAAP measures are included in the Appendix to this presentation. These disclosures should not beviewed as a substitute for operating results determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures that maybe presented by other companies.

2

KEY MESSAGES

3

New executive leadership team, talented hires and promotions in key roles; Creating renewed energy and focus across the organization

Becoming the leading “Socially Responsible Community Bank” in the communities we serve by embracing changing customer preferences

Sharper focus and sense of urgency to enhance stakeholder value; effective capital allocation in support of strategic choices to improve return on capital

1

2

3

* *

BERKSHIRE HILLS BANCORP (NYSE: BHLB) AT-A-GLANCE

Serving key needs of consumer, small business & commercial clients in New England / New York.

4

Key Statistics

Headquarters Boston, MA

Founded 1846

Market CapitalizationAs of 5/8/21

$1.27B

Total BranchesExcluding branches to be consolidated or sold

106

Total AssetsAs of 3/31/21

$12.8B

Total DepositsAs of 3/31/21

$10.2B

Loan-to-depositsAs of 3/31/21

75%

Capital (CET1)As of 3/31/21

14%

Customer RelationshipsAs of 5/8/21

350,000+

23%

47%

22%

8% C&I

CRE

Residential

Consumer

Loans

New England / New York FootprintDiversified Balance Sheet (EOP 3/31/21)

27%

18%

10%

24%

21%

Non Int. Bearing DDA

NOW & Other

Savings

Money Market

CDs

Deposits *Mid-Atlantic branches held for sale

• Top 25 SBA 7(a) Lender in the Nation

• ~$1B in PPP Loans to 7,000+ small businesses1

• $773M Small Business loan balances; helping ~10k businesses2

• $21M Foundation Giving over the last 10 years

• 383k+ hours of employee volunteer service since 2009

• 1k+ company-sponsored volunteer events in the last 5 years

• 86k+ people benefited from financial literacy programs

• Inclusive mainstream banking3

• 70% higher reinvestment in our neighborhoods than industry banking4

• $38M in renewable energy loans

• Transitioning electricity supply towards 100% renewable

• Strong policies govern lending activities to protect the environment

BERKSHIRE HILLS BANCORP – A LEADER IN SOCIAL RESPONSIBILITY

5

Local

Business

Community

Contribution

Financial

Inclusion

Environmental

1 Originated and referred loans 2 Balances as of 12.31.203 With products such as MyCheck, MyFreedom Checking, and Teen Checking4 Mighty Deposits: $76 of every $100 is reinvested back in local communities

TRANSFORMING AND ADAPTING TO CHANGES IN BANKING SECTOR

6

Macro-economic Factors Preferences/Expectations Technology/Digitization Competition/Disruption

Low rates in the

short-to-medium term

Improving credit outlook

after a period of heightened

volatility

Higher standards for digital

experience across customer

journeys

Expectations for new ways

of working, such as work

from home

FinTech/PaaS Tech

acceleration, requiring

core systems platform

modernization & API

enablement

Need to reduce costs

increasing drive for

efficiency and scale;

accelerated M&A

Increasing competition from

Neo-Banks and FinTechs

Focused on Improving Drivers of Past Financial Underperformance

BHLB: WHY DO WE NEED TO TRANSFORM?

7

Improve Revenue Mix

Grow fees/revenue ratio

through growth in SBA,

Mortgage Banking, Treasury &

Wealth Management revenues

2020 Baseline Performance Gap vs. Peers

1 Adjusted basis – excludes non-operating gains/losses, and expenses, including $554 million pre-tax Goodwill write-off as well as discontinued operations. See reconciliation at the end of this presentation. 2 Peers: ABCB, AUB, BXS, CBU, CUBI, FFBC, FRME, FMBI, GWB, HTLF, HOMB, INDB, NBTB, ONB, RNST, SFNC, SSB, TOWN, TRMK, UBSI, UCBI, and WSBC

Source: S&P Global Market Intelligence (“SPGMI”); FactSet

Improve & Grow

Balances

Optimize Deposit and Loan

mix while growing overall

balances

Improve Margins

Higher DDA penetration,

loan pricing

improvements

& wholesale funding

Improve Asset Mix

Better C&I and Small Business

concentration in Commercial;

prudent allocation to Consumer

Lending Growth

Improve NPS &

Relationship Depth

Track/improve Net Promoter

Score; drive up account

primacy, products and

services per relationship

Strengthen & Promote

ESG Performance

Leverage the purpose-driven,

community-dedicated

programs to promote and

strengthen ESG performance

0.24% 3.2% 69.0%

1.0% 8.0% 56.0%

ROA ROTCEEfficiency

Ratio

14%

12%

CET1

BHLB¹

Peer Median2

INTRODUCING OUR “BEST” PLAN

8

Berkshire’s Exciting Strategic Transformation (BEST)

B E S T PILLARS

OPTIMIZE DIGITIZE ENHANCE

Optimize Products/Pricing and

Balances Mix for improved ROE

Digitize Account

Opening & Customer

Journeys

Digitize Marketing and

Customer Insights/Service

Enable API integrations with

FinTech/Sales Partners

Optimize

Physical footprint

Optimize

Processes &

Procurement

Grow profitable

originations and

balances

Enhance banker and

customer engagement

Enhance Capital allocation &

deployment for improved ROE

STRATEGIC CHOICE DOING MORE DOING LESS

PARTICIPATION

+ Accelerate growth in Business Banking, SBA Lending, Asset Based Lending,

Wealth Mgmt and MyBanker program

+ Increase Consumer Balances/ROE, while retaining ~65% Commercial mix

- Physical footprint (e.g. Branches, Hub Sites)

- High Risk, Non-relationship Lending

POSITIONING

+ “Socially Responsible Community Bank”

+ “Digi-Touch” Relationship Banking; driving up DDA penetration and account

primacy

- Physical footprint (e.g. Reevx brick & mortar)

- Decentralized sponsorships

ORGANIZATION

+ Improved alignment of incentive compensation with structured performance

management to drive shareholder value

+ Centralize Services that create efficiency (e.g., Procurement)

- Decentralized operations

- Limited spans of control

RISK+ Strengthen risk governance and higher focus on risk-adjusted-return on capital

+ Consumer Lending & FinTech Partnerships

- Pricing below RaRoC (Risk adjusted return)

- Manual underwriting for small $ originations

TECHNOLOGY+ Enhanced customer and banker experience

+ Streamlined operating and data platforms through cloud migration

- Number of applications to ‘run-the-bank’

(to invest in ‘change-the-bank’ initiatives)

- De-centralized Data Mgmt, Infosec

BEST – KEY STRATEGIC CHOICES TO POSITION BHLB FOR SUCCESS

9

+

+

++

+

+

+

+

+

+

BEST – OPTIMIZE INITIATIVES AND IMPACT

10

FOOTPRINT

Exit under-penetrated

markets

Branch consolidations

Hub site consolidations

Optimize Total Projected ROTCE Impact: ~300bps

PROCESSES

Centralized procurement

Enterprise process

mapping and

re-engineering

Automation and

outsourcing

BALANCE SHEET

Better Before Bigger –

improve asset/deposits mix

Reduce, eliminate

non-core/low-margin/

duplicative products

Optimize pricing

– deposit/treasury

repricing, loan relationship

RaROC pricing

HUMAN CAPITAL

Org structure and span of

control optimization

Redeployment of talent for

optimized outcomes

Optimize T&E expenses

BEST – DIGITIZE INITIATIVES AND IMPACT

11

CHANNELS

Omni-channel experience:

MyBanker, Virtual Branch

(ITM)

Digitized branches and

CRM platforms

Digital account opening –

Consumer, Small Business

Digitize Total Projected ROTCE Impact: ~75bps

CUSTOMER

EXPERIENCE

Mobile-first, responsive

design across digital

experience

Mobile/digital app rating

& customer experience

enhancement

Increase digital capabilities

to enhance self-service

options

MARKETING/

CUSTOMER OUTREACH

Leverage and enhance

CRM functionality/

integration

Data warehouse and

analytics for improving

marketing ROI

Customer alerts and

insights for relationship

deepening

PARTNERSHIPS

API-enabled integrations

with FinTech and other

partners

New customer

originations for consumer

and business banking

Consolidate digital

interfaces for single-view,

single sign-on

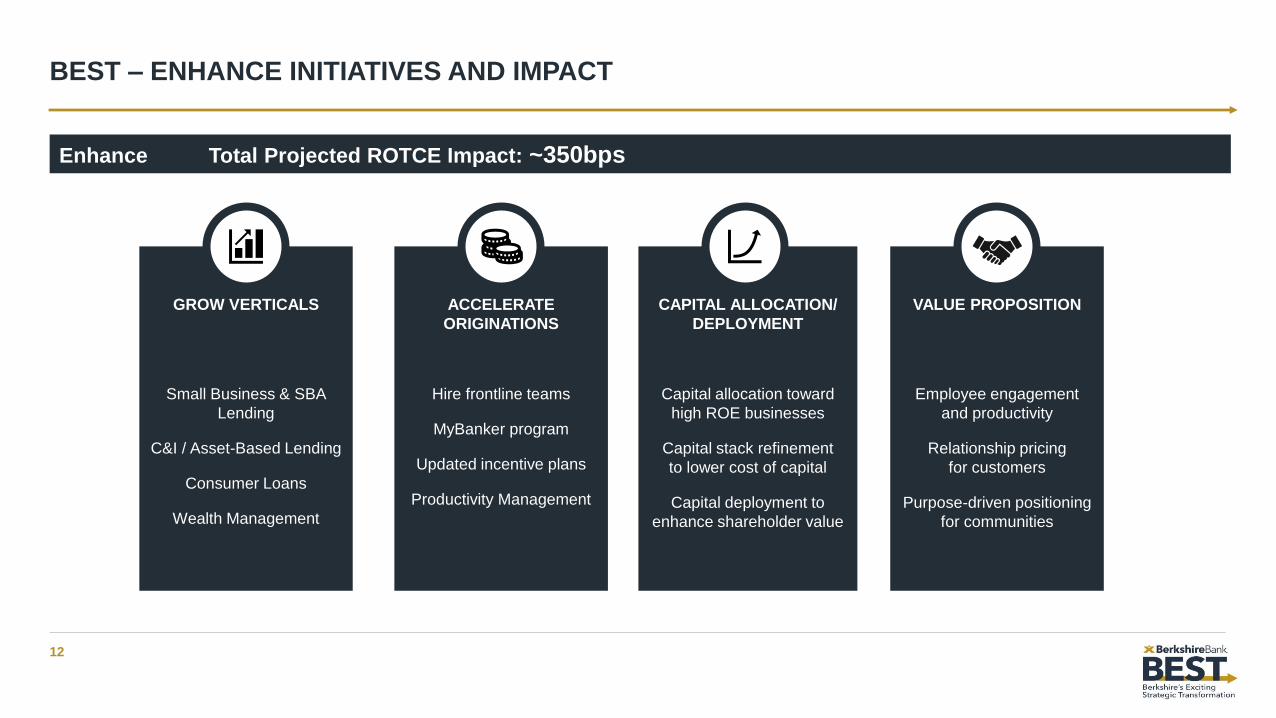

BEST – ENHANCE INITIATIVES AND IMPACT

12

GROW VERTICALS

Small Business & SBA

Lending

C&I / Asset-Based Lending

Consumer Loans

Wealth Management

Enhance Total Projected ROTCE Impact: ~350bps

ACCELERATE

ORIGINATIONS

Hire frontline teams

MyBanker program

Updated incentive plans

Productivity Management

CAPITAL ALLOCATION/

DEPLOYMENT

Capital allocation toward

high ROE businesses

Capital stack refinement

to lower cost of capital

Capital deployment to

enhance shareholder value

VALUE PROPOSITION

Employee engagement

and productivity

Relationship pricing

for customers

Purpose-driven positioning

for communities

BEST – KEY SUCCESS METRICS OVER 3 YEARS

13

Through effective execution of BEST program over the next 3 years, we project to deliver…

*PPNR is a Non-GAAP number representing GAAP revenues minus GAAP expenses excluding credit provision expense and tax expense

**Reflects improvement over FY2020 non-GAAP financials

***ESG Index ratings: MSCI, ISS-ESG, Sustainalytics, Bloomberg

ROA

Increase ROA

by 76-81bps**

PPNR*

Increase PPNR

by $71-91M**

ROTCE

Increase ROTCE

by 680-880bps*

ESG

Be recognized as a top

quartile bank by

leading ESG indexes

in the US***

NPS

Become a top quartile

NPS (Net Promoter

Score) bank in

New England

100-105 bps10-12% Top 25%Top 25%$180-200M

BEST – YEAR 3 ROTCE IMPACT

14

Optimize Digitize Enhance

Projected ROTCE

10–12%~100bps

3.2%

~300bps~75bps

~350bps

~100bps

11–13%

2020A ROATCE Optimize Digitize Enhance Credit Normalization& Return Capital

Year3 ROATCE Upside from higherrates

Normalized Credit and Capital Return

2020

Adj. ROTCE¹Optimize Digitize Enhance

Normalized

Credit and

Capital Return

Year 3

ROTCE

Upside with

higher rates

Year 3

ROTCE

with higher rates

1 BEST program scheduled to start in July 2021

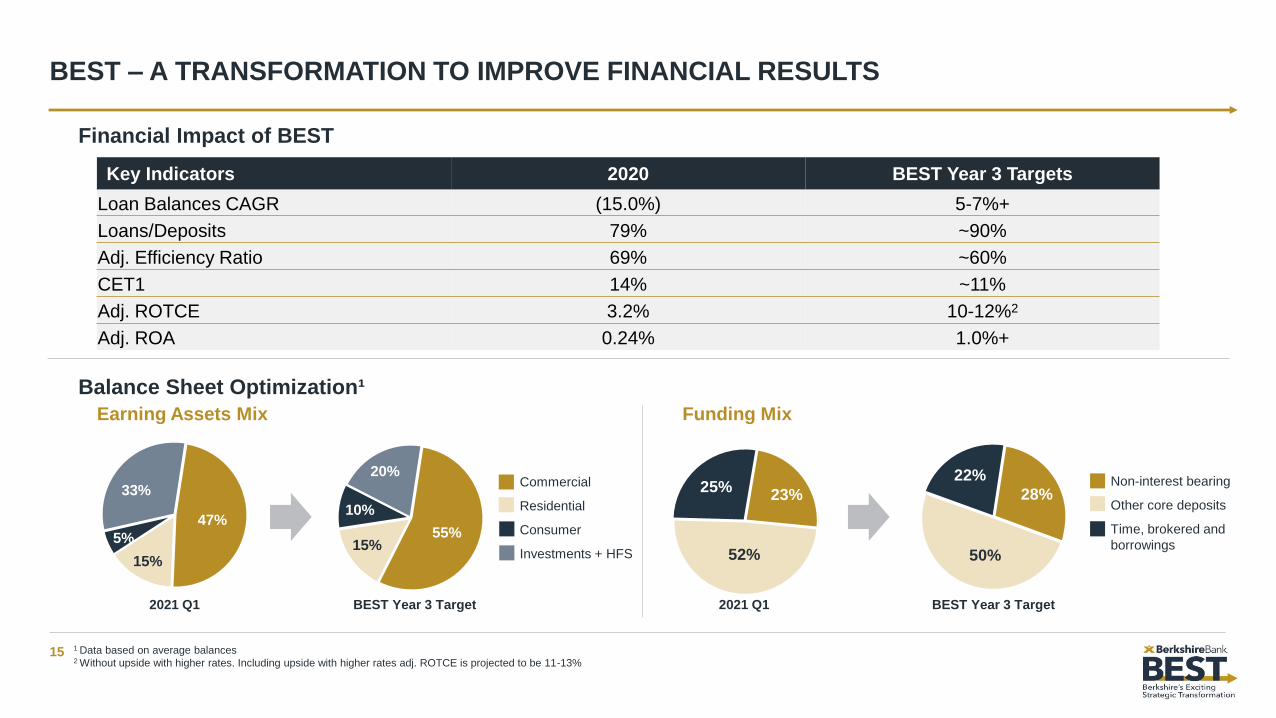

BEST – A TRANSFORMATION TO IMPROVE FINANCIAL RESULTS

15

Key Indicators 2020 BEST Year 3 Targets

Loan Balances CAGR (15.0%) 5-7%+

Loans/Deposits 79% ~90%

Adj. Efficiency Ratio 69% ~60%

CET1 14% ~11%

Adj. ROTCE 3.2% 10-12%2

Adj. ROA 0.24% 1.0%+

1 Data based on average balances2 Without upside with higher rates. Including upside with higher rates adj. ROTCE is projected to be 11-13%

Financial Impact of BEST

Earning Assets Mix

47%

15%

5%

33%

55% 15%

10%

20%

Funding Mix

28%

50%

22%Commercial

Residential

Consumer

Investments + HFS

2021 Q1 BEST Year 3 Target 2021 Q1 BEST Year 3 Target

Balance Sheet Optimization¹

Non-interest bearing

Other core deposits

Time, brokered and

borrowings

23%

52%

25%

BEST – EXECUTION PLAN AND GOVERNANCE

16

DIGITIZE ENHANCEOPTIMIZEBEST Pillars

16 workstreams to support BEST Pillars to drive initiatives to track and achieve financial goalsWorkstreams

Governance

and Support

Structure

BEST Leadership

Decision and Execution Model

Forums, Meetings and Interaction Model

Transformation Office Workstreams

Transformation

Enablers

Communications

Change Management & Performance Management

BEST Impact

ROA PPNRROTCE ESG NPS

100-105

bps10-12%

Top

25%Top

25%

$180-

200M

EXPERIENCED EXECUTIVE LEADERSHIP TEAM

17

Broad and Deep Sector Experience…

Nitin

Mhatre

Chief Executive

Officer

Sean

Gray

Chief Operating

Officer

Subhadeep

Basu

Chief Financial

Officer

Tami

Gunsch

SEVP,

Consumer

Banking

Gregory

Lindenmuth

SEVP,

Chief Risk

Officer

George

Bacigalupo

SEVP,

Commercial

Banking

Deborah

Stephenson

SEVP,

Compliance &

Regulatory

Jason

White

EVP,

Chief

Information

Officer

Jacqueline

Courtwright

EVP,

Chief HR and

Culture Officer

Gordon

Prescott

EVP,

General

Counsel & Corp.

Secretary

Georgia

Melas

EVP,

Chief Credit

Officer

Jennifer

Carmichael

EVP,

Chief Internal

Audit Officer

Years of Combined Banking

Experience (avg. 27 years) 325+

…driven by purpose and passion to

empower everyone’s financial potential

Executive Volunteerism on Nonprofit Boards

BHLB – GETTING BETTER, STRONGER, FASTER

18

Becoming

the leading

socially-responsible,

omni-channel

community bank in

the communities

we serve

Adapting

to changing customer

preferences by

optimizing footprint

while enhancing &

digitizing customer

experience

Transforming

the company with a

new leadership team

and collective

organizational

resolve to deliver

high performance

1 2 3

Maximizing

stakeholder/

shareholder value

while maintaining

strong capital base &

balance sheet for

future growth

4

WE ARE COMMITTED TO

MAKING BERKSHIRE

BETTER, STRONGER…AND

FASTER

WE ARE COMMITTED TO

MAKING BERKSHIRE

BETTER, STRONGER…

FASTER

WE ARE COMMITTED TO

MAKING BERKSHIRE

BETTER, STRONGER…AND

FASTER

APPENDIX

NON-GAAP RECONCILIATION