beacon economics inland empire forecast

DESCRIPTION

Annual forecast of economic conditions in Riverside and San Bernardino countiesTRANSCRIPT

2014Riverside/San BernardinoEconomicForecast

Presented byBeacon Economics, LLCUniversity of California at Riverside, School of Business Administration

Volume 7 Number 1 October 2014

This publication was prepared by:

Beacon Economics

Christopher Thornberg, Founding Partner Jordan G. Levine, Economist5777 West Century Boulevard, Suite 895 5777 West Century Boulevard, Suite 895Los Angeles, California 90045 Los Angeles, California 90045310.571.3399 [email protected] [email protected]

For further information about this publication, or about Beacon Economics, please contact:

Victoria Pike BondDirector of CommunicationsBeacon [email protected]

Or visit our website at www.BeaconEcon.com.

Reproduction of this document or any portion therein is prohibited without the expressed written permission of Beacon Economics.

Copyright ©2014 by Beacon Economics LLC.

School of Business Administration and The A. Gary Anderson Graduate School of Management

Anderson Hall

Riverside, CA 92521

Greetings,

The UC Riverside School of Business Administration is proud to partner with Beacon Economics

to bring you the fifth-annual economic forecast conference for the Riverside/San Bernardino

region. This important community event provides a platform for Inland Southern California’s top

business leaders to discuss and provide insight on the economy.

For the Sake of Growth: Building Entrepreneurs and Companies in the Inland Empire will be the

topic of this year’s expert panel. This insightful discussion will examine ways in which the public

and private sectors can work collaboratively to foster an environment that allows for greater

economic growth.

In fact, “Leading Thinkers Leading Growth” is our motto at the School of Business

Administration. It reflects our commitment to Inland Southern California’s economic

development—and to providing leadership as we navigate through the region’s continued

economic recovery. Toward this end, we are pleased to share that we have made significant

strides in the development of a UCR-housed Forecasting Research Center and look forward to

partnering with many of you on this initiative.

Additionally, we are proud to report that our school, accredited by the Association to Advance

Collegiate Schools of Business, was again named one of Princeton Review’s best 296 business

schools in the nation and one of the best in the west in 2013. In addition to the largest

undergraduate business program in the UC-system, we offer MBA, Ph.D., Master of Professional

Accountancy, Flex MBA and Master of Finance programs.

We are growing and, much like the region, are on the upward path to sustained excellence.

Thank you for your support of this year’s conference. I hope you enjoy the program.

Yunzeng Wang, Ph.D.

Dean

UCR School of Business Administration

Tel 951.827.6329 ͻ Fax 951.827.3970 ͻ www.soba.ucr.edu

SponsorsBeacon Economics would like to extend our deepest gratitude to our partners and sponsors, without whom thispublication would not have been possible.

Gold

Media

Silver

Bronze

Exhibit Booth

• Accredited by the Association to Advance Collegiate Schools of Business (AACSB). Less than 5% of business schools in the world have earned AACSB accreditation. • Listed by The Princeton Review among the top 296 “Best Business Schools” in the nation.• Ranked in the top 100 “Best Graduate Schools” of 2013 by U.S. News & World Report (97th out of 441 schools)

Contact Us:AGSM Graduate Business Programs Phone: (951) 827-6200Email: [email protected]

Earn your Master’s Now

MBAFlex MBA

Master of Professional AccountancyMaster of Finance

LEADING THINKERS LEADING GROWTH

agsm.ucr.edu

Qualified applicants may receive tuition assistance

Join our upcoming events athttp://agsm.ucr.edu/calendar/

Alzheimer’s ResearchCancer PreventionCalifornia’s newest public School of MedicineCharter Member: University Innovation Alliance www.universityinnovationalliance.org

Explore more health impactspromise.ucr.edu

Health Sustainability Policy Technology

By studying how the human immune system is

affected over a lifetime by diet and aging,

UCR immunologist Ilhem Messaoudi can develop

more effective vaccines for older populations.

LIVING THE PROMISE

Real World SolutionsO U R P R O M I S E :

The A. Gary Anderson Family Foundationis proud to support Children’s Fund and their mission

to provide for at-risk and abused children at their:

23rd AnnualA. GARY ANDERSONMemorial Golf Classic

June 8, 2015Red Hill Country Club

Rancho Cucamonga, CA

For more information about Children’s Fund,please visit their website at:

www.childrensfundonline.org

f a m i l y f o u n d a t i o nA. GARY ANDERSON

Is proud to support the 2014 Riverside/San Bernardino

Economic Forecast Conference and UC Riverside’s

School of Business Administration

Bank of America is honored to support UCR and the Beacon Economic Forecast Conference

Thank you for all that you do in the Inland Empire. Your presence here creates connections that enrich our entire community, and we are honored to support the great work you are doing.

Visit us at bankofamerica.com/local Life’s better when we’re connected®

©2014 Bank of America Corporation | ARH46WCM

Delivering Superior Engineering, Architecture & CM results in:

CLEAN ENERGYBuilding, utility and energy infrastructure designs that lower

your total cost.

COMPREHENSIVE BUILDING DESIGNComplex and mission critical structures.

877.725.2755 www.salasobrien.com

Contents

U.S. Forecast 1

California Forecast 9

Inland Empire Forecast 19

Employment 27

Business Activity 35

Residential Real Estate 47

Commercial Real Estate 57

Demographics and Quality of Life 75

Inland EmpireMetropolitan Statistical Area

Riverside

San Bernardino

California

Temecula

Wildomar

Murrieta

BlytheCoachella

La Quinta

Indian WellsLake Elsinore

Hemet

Indio

Idyllwild-Pine CovePalm Desert

Rancho MirageSan JacintoPerrisAnaheim

Cathedral CityCorona

Yorba Linda

Palm Springs

Beaumont

NorcoMoreno Valley

Desert Hot SpringsCalimesa

RiversideChino Hills

BanningDiamond BarChino Yucaipa

Ontario ColtonRedlands

Pomona

Highlandd

ClaremontRancho Cucamonga

RialtoFontana

Yucca Valley Twentynine PalmsSan

Bernardino

Lake Arrowhead

Hesperia

Victorville

Apple Valley

Adelanto

NeedlesBarstow

n

Searles Valley

Lake Havasu City

Canyon LakeSun City

Winchester

Nuevo

WoodcrestMarch AFB

Pedley Cherry ValleyMira Loma Rubidoux

Glen AvonLoma Linda Mentone Morongo Valley

Joshua Tree

Big River

CrestlineParker Strip

Big Bear Lake

BEACONECONOMICS

U.S. Forecastby Christopher Thornberg

ContentsZero To Hero 2Curb Your Enthusiasm 2The Bounce In Our Step 3On Policy and Prices... 7

U.S. Forecast

Zero To Hero

In 2008 the U.S. economy sunk into the deepest down-turn since the Great Depression. By the end of thatyear most of the globe had followed the United Statesinto recession and in 2009 global output shrank byover 2%, the first time that has happened since WorldWar II ended. TheUnited Stateswas not the only coun-try with a large housing bubble, nor were U.S. banksthe only to indulge in over-leveraging even as they in-vested in highly risky assets. Nevertheless, it was clearthat the United States was at the heart of the problem.

Today, the global economy is weak again. Europe hasyet to fully pull out of the recession, led by sovereigndebt crisis, that it experienced last year. The BRICS(an acronym for an association of five major emerg-ing national economies: Brazil, Russia, India, China,and South Africa) are also showing signs of trouble.China, while still growing, has slowed and its realestate markets are showing signs of distress. Brazilhas slipped into a mild recession due to sagging com-modity prices. Sanctions on Russia are clearly havingan impact on that nation and India has also slowedsharply. The World Bank and the IMF have both hadto scale back their growth outlook numerous times inthe last few months.

But this time the United States is no longer at thecore of the problem; quite the opposite, the U.S. econ-omy will be an important source of strength glob-ally as these nations work to reverse course and getback onto a growth trajectory. Nearly every part ofthe U.S. economy is showing real signs of slow butsteady improvement, fromhousing to public spendingto credit. The only portion of the economy that is act-ing as a drain on the nation is the export sector—for allthe aforementioned global reasons. That said, the U.S.economy will keep growing this year, but at slightlybelow 3%, a bit slower than last year. Next year, ex-pect the U.S. economy to grow at a pacemodestly over3%,with the following year improving evenmore—the

growing momentum will be driven by improving fun-damentals.

As for major risks, they remain largely external – al-though there is nothing on the international frontthat could seriously derail the nation’s economy. Theglobal economy remains the swing item. If there is abetter recovery than expected, then next year will bebetter than Beacon Economics’ current forecast. If itis significantly worse, then growth will likely dip intothe low 2% range. Regardless, the U.S. economy willcontinue to expand for the foreseeable future.

Curb Your Enthusiasm

The U.S. economy’s 4.6% growth rate in the secondquarter of 2014 came as a relief to many policymak-ers after the -2% hit taken during the first quarter ofthe year. Data from the third quarter have simply con-firmed Beacon Economics’ interpretation of the firstquarter as a blip. Beacon’s monthly GDP estimate sug-gests that growth in the third quarter will come inat 3.6%. Combine this with better labor market num-bers—on average 220,000 jobs were added per monthover the last year and the official unemployment ratehas dropped to below 6% for the first time since 2007—and suddenly the economy looks like a talking pointfor the Democrats rather the Republicans. Althoughthis does not seem to be having any impact on the out-look for the midterm elections.

Still, while there is little doubt the mid-year num-bers look good, these big numbers are really just abounce from the weak first quarter – a quarter thatwas largely an artifact of the extreme weather expe-rienced in many parts of the nation and of a big runoff in inventories (likely also related to weather). Thesecond and third quarters were largely mirror imagesof the first, as growing inventories and a bounce inconsumer spendingmade up for ground lost earlier inthe year. Average the three quarters out and growthis running at about 2%.

2 2014 Riverside/San Bernardino Economic Forecast

U.S. Forecast

One small part of the slowing is in the estimates ofconsumer health care expenditures. This seems odd,given that other numbers on consumer spending, in-cluding retail sales, auto sales, and other more eas-ily measured forms of spending, are rising. Addition-ally, by all accounts, approximately 7 to 8millionmoreAmericans have health insurance today compared toone or two years ago. If anything, health care expen-ditures would be expected to increase. And healthcareemployment continues to grow at a steady 2% annualpace. Add it up and it seems this is more likely a glitchin the U.S. Bureau of Economic Analysis’ (BEA) esti-mates rather than a real phenomena.

The real reason for the deceleration is the nation’sexternal accounts, with a sudden widening of thetrade deficit. Beacon Economics’ initial outlook forGDP growth in the 3% range in 2014 was based largelyon the assumption that the trade deficit would con-tinue to close. But this didn’t happen. Instead, a weakglobal economy slowed export growth sharply, evenas stronger demand in the United States caused im-port growth to accelerate.

Contributions to Real GDP GrowthComponent Q1-14 Q2-14 Q3-14 Avg. Diff.

Real GDP -2.1 4.60 3.60 −1.09

Consumption 0.83 1.75 1.50 −0.54

Durable goods 0.23 0.99 0.79 0.24

Nondurable goods 0.00 0.34 0.26 −0.19

Services 0.60 0.42 0.46 −0.59

Private Domestic Inv. -1.13 2.87 1.21 −0.33

Structures 0.08 0.35 0.17 0.08

Equipment -0.06 0.63 0.51 0.01

IP products 0.18 0.21 0.26 0.11

Residential -0.17 0.27 0.27 −0.08

Change in Inventories -1.16 1.42 0.00 −0.45

Net Exports -1.66 -0.34 0.78 −0.67

Exports -1.30 1.43 0.89 −0.33

Imports -0.36 -1.77 -0.11 −0.34

Government -0.15 0.31 0.13 0.44

Federal -0.01 -0.06 0.06 0.48

State/Local -0.14 0.38 0.07 −0.03

Source: U.S. Bureau of Economic Analysis

Right now the United States still doesn’t have the‘umph’ to close the output gap that opened during thecourse of the downturn. And while the labor marketsaremodestly stronger, the operative word is ‘modest’.Participation rates are still under 63%, far below the66% level prior to the recession.Wage growth remainstepid—even if other sorts of income are doing better.And none of this suggests that there will be a dramaticshift in Federal Reserve policy any time in the near fu-ture.

The Bounce In Our Step

The current trends do seem to be a frustrating re-peat of the last few years—three steps ahead, two stepsback. But in reality there are plenty of indications thatthe United States is shifting towards being in a highergrowth regime, with many economic indicators pick-ing up steam on many fronts. Indeed there is enoughmomentum in the nation’s economy to push us pastthe problems in the broader global economy. Follow-ing is an overview of some of the brighter spots in theU.S. economy—consumer spending, construction andbusiness investment—followed by a look at trade andpublic spending, two areas that are preventing evenbetter growth rates.

Consumer Spending

Consumer spending, outside of healthcare, has beengrowing at a steady pace since the start of 2014. Autosales have hit a 17 million annual pace in recentmonths—the best showing since before the recession.Retail sales have been growing at a nominal 4.5% an-nualized pace in recent months. And there are plentyof indications that the pace of growth will at least bemaintained over the next year.

The labor market is showing some of the strongestgrowth since the end of the recession, expanding at apace of 200,000 plus jobs per month over the last year.Moreover, the nation’s headline unemployment has

2014 Riverside/San Bernardino Economic Forecast 3

U.S. Forecast

dropped below 6%. And while there are still a higherthan normal number of distressed workers (long termunemployed, discouraged, or under employed) thetrend in unemployment is clearly on a downward tra-jectory. The labor markets may start to look ‘normal’againwithin two years. Also encouraging, personal in-comegrowthhas been expanding at a better pace. Realaggregate disposable personal income is growing at a2.7% pace, after running flat for most of 2013.

-4.0

-2.0

0.0

2.0

4.0

Y-o-

Y G

row

th (%

)

0

5,000

10,00

015

,000

20,00

0

Wor

kers

(000

s)

Jan-04 Jan-06 Jan-08 Jan-10 Jan-12 Jan-14year

LT Unemployed PT EconomicMarginal DiscouragedDisposable Income Growth

Source: Bureau of Labor Statistics

United States, Jan-04 to Sep-14Distressed Workers and Real Disposable Income Growth

Another bit of good news comes from consumercredit. Outside of student debt, consumer creditgrowth has been very subdued in recent years. Butin 2014 things have started to shift. Consumers havebecome more comfortable with borrowing as their fi-nancial confidence and net worth has expanded, andthe banking systemhas beenmorewilling to add loansto their balance sheets. The pace of expansion is nowover 6% per year. And with the savings rate remain-ing at a sufficient level, there is little sign of Americansover-extending themselves like they did in themiddleof last decade.

-10

-5

0

5

Year

-Ove

r-Yea

r Gro

wth

(%)

1,600

1,700

1,800

1,900

2,000

$ Bi

llions

Q1-07 Q1-08 Q1-09 Q1-10 Q1-11 Q1-12 Q1-13 Q1-14

Total Y-o-Y Growth

Source: Federal Reserve

Q1-07 to Q2-14Non-Education Consumer Credit

Construction

Construction is one of the big shortfalls in the U.S.economy (as noted in past years’ reports). Prior to thedownturn, close to 8% of U.S. GDP went to residentialand nonresidential investments. Today, that figure is6%, and with multiplier effects, explains close to halfthe output gap in the U.S. economy. Housing permitsremain stuck at one million units, with disappointingsales of new homes constraining construction of newsingle-family structures. Existing home sales have alsosoftened this year, leading some to predict anotherslump in the market. There are, however, other sig-nals that housing is not in a slump—but rather at thefront end of a solid expansion.

While sales of existing homes have slowed, this ap-pears to be largely due to a decline in the number offoreclosures rather than a pull back in what mightbest be termed ‘retail’ demand—move-up owner-occupants shifting to new properties. Indeed, otherindicators continue to suggest the market is not ‘soft’by any traditional measure. Inventories of units forsale remain tight and prices are still rising, albeit ata slower rate than earlier in the year. Rather, the pullback by investors has not yet beenmade up for by bet-ter retail buyer demand.

But that increased retail demand looks to be on thehorizon. The recent growth in home prices has addedsubstantially to home equity—which is now close to

4 2014 Riverside/San Bernardino Economic Forecast

U.S. Forecast

$14 trillion, up from $8 trillion at the bottom of theslump. Credit has also been a problem, but again, con-ditions are easing. Recent Fannie Mae data shows adecline in the average FICO score for new borrowers.Data from the Federal Reserve’s Senior Loan OfficerSurvey indicates that banks are starting to ease creditconditions for primemortgage loans. And data on out-standing mortgage debt held directly by the bankingsystem is beginning to grow slowly for the first time inyears. The coming increase in retail demand impliesmore need for new product—which should give newhome construction a nice lift in 2015.

Beacon Economics expects the second half of 2014to show distinct improvement in terms of sales andbuilding permits over the first half. Preliminary statis-tics for the first two months of the third quarterappear to back this up—existing home sales havestarted to increase again, and new home sales havealso jumped somewhat.

3,000

4,000

5,000

6,000

7,000

8,000

Sale

s (0

00s,

SAA

R)

Q1-04 Q3-06 Q1-09 Q3-11 Q1-14Source:

United States, Q1-04 to Q2-14Traditional Sales

Non-residential spending has also started to rampup in recent months. Much of the growth contin-ues to be in ‘alternative’ projects such as private in-frastructure and manufacturing. But traditional com-mercial projects—retail, office, hotel, and industrialspace—are also starting to expand rapidly, despitethe relatively high vacancy rate in these markets. Al-though overall vacancy rates are higher, there arepockets of high-demand and specialty type productsthat are in short supply. Demand in these areas has

pushed rent prices towards pre-recession levels andthe net result has been a new wave of construc-tion—either of new structures or to repurpose exist-ing ones into more high-demand products. With busi-ness activity continuing to grow, this trend will verylikely continue for the next few years.

Business Investment

Corporate profits and proprietor incomes havebounced back faster than almost any other part ofthe economy since the recession came to an end.They are now 35% higher than before the downturnbegan. Low interest rates, benign wage growth, and aweak dollar have all contributed. Still, recent reportshave suggested that businesses have not used thepositive environment to expand real investment.Rather, the story goes, they are only interested invarious financial maneuvers, from buying back stockto purchasing other firms to finding interesting waysto avoid paying taxes.

Actually the idea of declining investment by businessisn’t true—it is an illusion caused by the declining costof various sorts of investment, particularly informa-tion technology. Real (price adjusted) investments inequipment or intellectual property as a share of U.S.GDP are currently at record high levels. And there isplenty of reason to believe the level of investmentwill continue to grow. In the short term, orders andshipments of durable capital goods have risen sharplyand the third quarter will likely show solid growthdriven by spending. Capacity utilization has contin-ued to rise, a good leading indicator of more busi-ness investment for the near term. And the ISM in-dexes for manufacturing and non-manufacturing ac-tivity are also strongly in the black.

2014 Riverside/San Bernardino Economic Forecast 5

U.S. Forecast

2.5

3.0

3.5

4.0

4.5

5.0

Publ

ic In

vest

men

ts (%

of G

DP)

10

12

14

16

18

20

Priv

ate

Inve

stm

ents

(% o

f GD

P)

Q1-05 Q1-07 Q1-09 Q1-11 Q1-13

Private Investment Public Investment

Source: Bureau of Economic Analysis

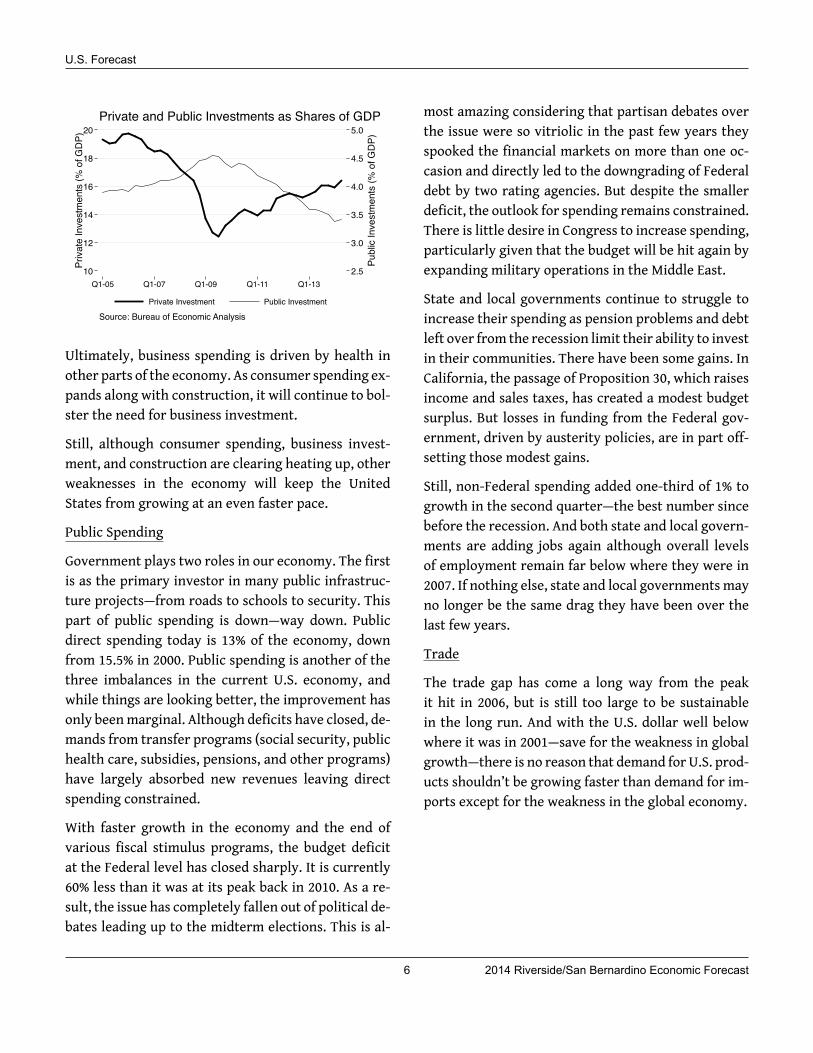

Private and Public Investments as Shares of GDP

Ultimately, business spending is driven by health inother parts of the economy. As consumer spending ex-pands along with construction, it will continue to bol-ster the need for business investment.

Still, although consumer spending, business invest-ment, and construction are clearing heating up, otherweaknesses in the economy will keep the UnitedStates from growing at an even faster pace.

Public Spending

Government plays two roles in our economy. The firstis as the primary investor in many public infrastruc-ture projects—from roads to schools to security. Thispart of public spending is down—way down. Publicdirect spending today is 13% of the economy, downfrom 15.5% in 2000. Public spending is another of thethree imbalances in the current U.S. economy, andwhile things are looking better, the improvement hasonly beenmarginal. Although deficits have closed, de-mands from transfer programs (social security, publichealth care, subsidies, pensions, and other programs)have largely absorbed new revenues leaving directspending constrained.

With faster growth in the economy and the end ofvarious fiscal stimulus programs, the budget deficitat the Federal level has closed sharply. It is currently60% less than it was at its peak back in 2010. As a re-sult, the issue has completely fallen out of political de-bates leading up to the midterm elections. This is al-

most amazing considering that partisan debates overthe issue were so vitriolic in the past few years theyspooked the financial markets on more than one oc-casion and directly led to the downgrading of Federaldebt by two rating agencies. But despite the smallerdeficit, the outlook for spending remains constrained.There is little desire in Congress to increase spending,particularly given that the budget will be hit again byexpanding military operations in the Middle East.

State and local governments continue to struggle toincrease their spending as pension problems and debtleft over from the recession limit their ability to investin their communities. There have been some gains. InCalifornia, the passage of Proposition 30, which raisesincome and sales taxes, has created a modest budgetsurplus. But losses in funding from the Federal gov-ernment, driven by austerity policies, are in part off-setting those modest gains.

Still, non-Federal spending added one-third of 1% togrowth in the second quarter—the best number sincebefore the recession. And both state and local govern-ments are adding jobs again although overall levelsof employment remain far below where they were in2007. If nothing else, state and local governments mayno longer be the same drag they have been over thelast few years.

Trade

The trade gap has come a long way from the peakit hit in 2006, but is still too large to be sustainablein the long run. And with the U.S. dollar well belowwhere it was in 2001—save for the weakness in globalgrowth—there is no reason that demand for U.S. prod-ucts shouldn’t be growing faster than demand for im-ports except for the weakness in the global economy.

6 2014 Riverside/San Bernardino Economic Forecast

U.S. Forecast

80

90

100

110

120

Inde

x M

ar-7

3 =

100

(NSA

)

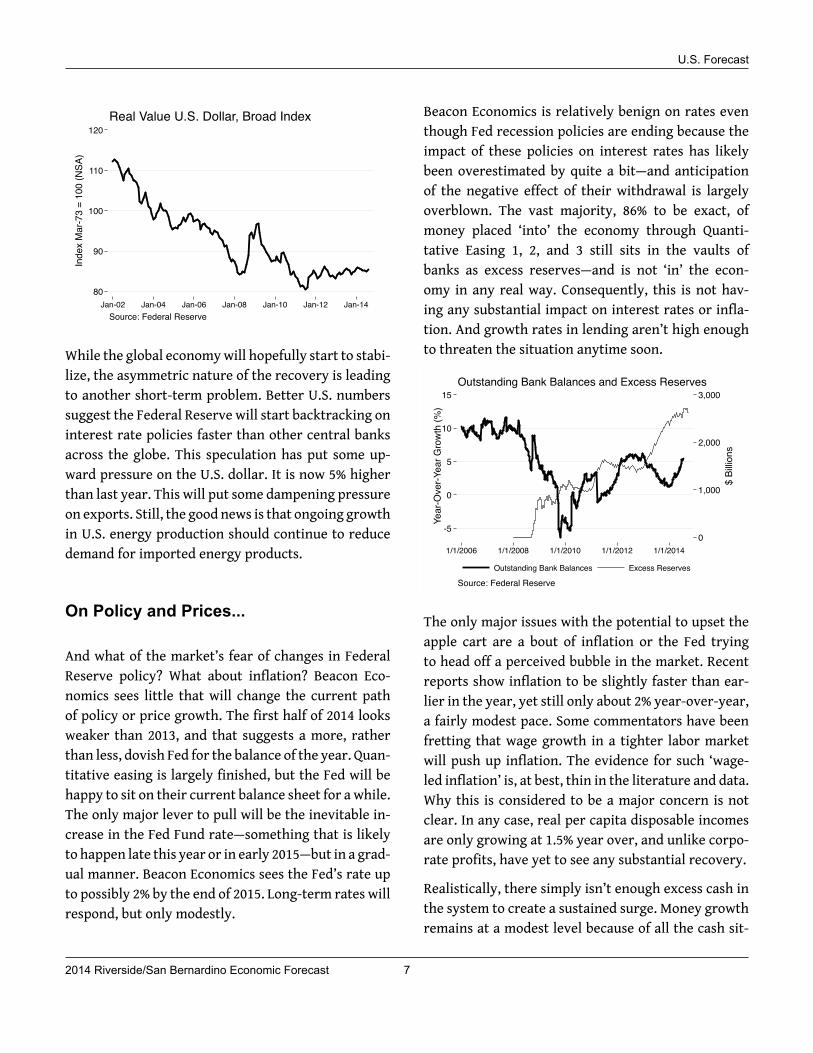

Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Jan-12 Jan-14Source: Federal Reserve

Real Value U.S. Dollar, Broad Index

While the global economywill hopefully start to stabi-lize, the asymmetric nature of the recovery is leadingto another short-term problem. Better U.S. numberssuggest the Federal Reserve will start backtracking oninterest rate policies faster than other central banksacross the globe. This speculation has put some up-ward pressure on the U.S. dollar. It is now 5% higherthan last year. This will put some dampening pressureon exports. Still, the good news is that ongoing growthin U.S. energy production should continue to reducedemand for imported energy products.

On Policy and Prices...

And what of the market’s fear of changes in FederalReserve policy? What about inflation? Beacon Eco-nomics sees little that will change the current pathof policy or price growth. The first half of 2014 looksweaker than 2013, and that suggests a more, ratherthan less, dovish Fed for the balance of the year. Quan-titative easing is largely finished, but the Fed will behappy to sit on their current balance sheet for a while.The only major lever to pull will be the inevitable in-crease in the Fed Fund rate—something that is likelyto happen late this year or in early 2015—but in a grad-ual manner. Beacon Economics sees the Fed’s rate upto possibly 2% by the end of 2015. Long-term rates willrespond, but only modestly.

Beacon Economics is relatively benign on rates eventhough Fed recession policies are ending because theimpact of these policies on interest rates has likelybeen overestimated by quite a bit—and anticipationof the negative effect of their withdrawal is largelyoverblown. The vast majority, 86% to be exact, ofmoney placed ‘into’ the economy through Quanti-tative Easing 1, 2, and 3 still sits in the vaults ofbanks as excess reserves—and is not ‘in’ the econ-omy in any real way. Consequently, this is not hav-ing any substantial impact on interest rates or infla-tion. And growth rates in lending aren’t high enoughto threaten the situation anytime soon.

0

1,000

2,000

3,000

$ Bi

llions

-5

0

5

10

15

Year

-Ove

r-Yea

r Gro

wth

(%)

1/1/2006 1/1/2008 1/1/2010 1/1/2012 1/1/2014

Outstanding Bank Balances Excess Reserves

Source: Federal Reserve

Outstanding Bank Balances and Excess Reserves

The only major issues with the potential to upset theapple cart are a bout of inflation or the Fed tryingto head off a perceived bubble in the market. Recentreports show inflation to be slightly faster than ear-lier in the year, yet still only about 2% year-over-year,a fairly modest pace. Some commentators have beenfretting that wage growth in a tighter labor marketwill push up inflation. The evidence for such ‘wage-led inflation’ is, at best, thin in the literature and data.Why this is considered to be a major concern is notclear. In any case, real per capita disposable incomesare only growing at 1.5% year over, and unlike corpo-rate profits, have yet to see any substantial recovery.

Realistically, there simply isn’t enough excess cash inthe system to create a sustained surge. Money growthremains at a modest level because of all the cash sit-

2014 Riverside/San Bernardino Economic Forecast 7

U.S. Forecast

ting in excess reserves. And the Federal Reserve cansee the situation forming long before it becomes aproblem. Beacon Economics doesn’t see inflation as aproblem.

-4

0

4

8

12

Year

-Ove

r-Yea

r Gro

wth

(%, S

moo

thed

)

Q1-80 Q1-85 Q1-90 Q1-95 Q1-00 Q1-05 Q1-10Source: Federal Reserve

Money Supply (M2)

The only real fear is that the Federal Reserve startpushing rates up sharply in response to a perceivedfinancial bubble—the way it did between 2004 and2006—with little impact on the bubble it should benoted. Beacon Economics doesn’t believe the marketsare too high at this point, so it is too early tomake sucha forecast. But, one bit of irony is that Wall Street’sown irrational fear of the Federal Reserve may well bethe thing that prevents the Fed from having to act.

8 2014 Riverside/San Bernardino Economic Forecast

California Forecastby Jordan G. Levine

ContentsCalifornia Overview 10What’s Right Cyclically? 10What’s Wrong Cyclically? 13What’s Right Structurally? 14What’s Wrong Structurally? 15The Forecast 16

California Forecast

California Overview

With the Great Recession firmly in the rear-view mir-ror, and California’s economy well into its recovery,it’s a good time to assess both what is working in thestate, and the greatest challenges that still lay ahead.The following forecast focuses on what’s right in to-day’s California, which areas need improvement, andwhere the state’s economy is headed over the next fiveyears.

What’s Right Cyclically?

Froma cyclical standpoint,many things are goingwellin California’s economy.

Labor Markets: Employment in the state is growingconsistently. In June 2014, California finally surpassedits pre-recession employment peak, recovering all ofthe 1.35 million jobs lost during the downturn andreaching the state’s highest level of nonfarm jobs onrecord. Through August 2014, California added an ad-ditional 75,700 jobs and now has nearly 90,000 morejobs than it did at the height of the previous bubble.

4.55.56.57.58.59.510.511.512.5

Une

mpl

oym

ent R

ate

(%, S

A)

12.012.513.013.514.014.515.015.516.0

Non

farm

Em

p. (M

illion

s, S

A)

Jan-90 Jan-95 Jan-00 Jan-05 Jan-10 Jan-15

Nonfarm Employment Unemployment Rate

Source: California Employment Development Department

Nonfarm Employment Reaches Record HighCalifornia Labor Markets, Jan-90 to Aug-14

Every major metropolitan area in California has ex-perienced a return to job growth, although some re-gions continue to do better than others. Similarly, ev-ery job sector, with the exception of Government and

Finance, has seen an uptick over the past four years,since the recession ended.

Moreover, as of August 2014, California had outpacedjob growth in the nation overall for 30 consecutivemonths. In August, California dipped from the 9thfastest growing state in the nation (June 2014) to the13th fastest. However, the number of jobs created wassecond only to Texas (314,000 vs. 395,000). In fact, oneout of every eight jobs created nationwide over thelast 12 months was created in California.

0.0

1.0

2.0

3.0

4.0

Gro

wth

(% Y

ear-o

ver-Y

ear,

SA)

Jan-1

3

Feb-13

Mar-13Apr-

13

May-13Ju

n-13Ju

l-13

Aug-13

Sep-13Oct-

13

Nov-13

Dec-13Ja

n-14

Feb-14

Mar-14Apr-

14

May-14Ju

n-14Ju

l-14

Aug-14

Source: U.S. Bureau of Labor Statistics

California Outpaces U.S. AverageNonfarm Employment Growth, 2013 to Current

California United States

Broader Economic Conditions: Virtually every keyeconomic indicator in California ismoving in the rightdirection: GDP is expanding in real terms, incomes arerising in the aggregate, consumer and business spend-ing is approaching its fifth year of consecutive growth,and the state’s unemployment rate has fallen from apeak of 12.4%, to 7.4% (August 2014) despite the factthat the labor force has expanded since the end of thedownturn.

California Economic IndicatorsIndicator 2012 2013

Real GSP Growth (%) 2.7 2.0Personal Income Growth (%) 5.0 2.8Taxable Sales Growth (%) 7.3 6.8Unemployment Rate (%) 10.4 8.9Labor Force (Millions) 18.52 18.60Source: Various

10 2014 Riverside/San Bernardino Economic Forecast

California Forecast

Fiscal Situation:California’s budget continues to healwith Governor Jerry Brown earning some nationalpraise for balancing the books.1 Although the budgetsituation is more nuanced than the headlines suggest,revenues have improved tremendously. With the pas-sage of Proposition 30, which raised income and salestaxes, General Fund receipts are up by more than 18%since hitting bottom in 2011-2012 when the previoustemporary sales tax increase expired. And, for the pasttwo years, receipts have actually outstripped expendi-tures, resulting in a $1.9 billion positive balance in thestate’s General Fund as of the end of fiscal year 2013-2014. This improvement is being felt at the local levelas both sales taxes and property taxes rise across Cal-ifornia.

60

70

80

90

100

110

Billio

ns

1998 2000 2002 2004 2006 2008 2010 2012 2014Fiscal Year Ending

Total Receipts Total Expenditures

Source: California State Controller's Office

Receipts Exceed Expenditures AgainCalifornia General Fund

Residential Real Estate: After precipitating many ofthe issues that drove the state and nation into reces-sion in the first place, California’s real estate marketsare also on a robust growth path. The median priceof an existing single-family home has been growingby double-digit percentages all across the state sinceJune 2012. The growth is due in part to limited inven-tory, which the California Association of Realtors esti-mate was at just 4.0 months of supply in August 2014.The numbers of distressed units coming onto themar-ket has also fallen as defaults and foreclosures haveplummeted in the wake of the recovery.

1Thomas Del Beccaro, "Jerry Brown Stands Atop California'sCollapsing House Of Cards", Forbes.com, July 8, 2014.

200

250

300

350

400

450

500

Med

ian

Pric

es ($

000s

, SA)

0

5

10

15

20

Mon

ths

of S

uppl

y (S

A)

Jun-05 Dec-06 Jun-08 Dec-09 Jun-11 Dec-12 Jun-14

Inventory Prices

Source: California Association of Realtors and DataQuick

Prices Rise Amidst Low InventoriesCalifornia Housing Market, 2005 to 2014

Home sales in California have been lackluster andlargely viewed as a disappointment by the marketsand in the media. Sales have indeed been weak on thesurface. However, the reason for the lackluster totalsales figures is due to the reduction in new foreclo-sures across California. When foreclosures are omit-ted from the equation, California home sales havebeen on the uptick in 2014. Although the headline fig-ures have disappointed some, they are the result ofvery positive trends.

40,000

60,000

80,000

100,000

120,000

Sale

s (S

A)

Q1-09 Q1-10 Q1-11 Q1-12 Q1-13 Q1-14

Sales Sales Less Foreclosures

Source: DataQuick

Sales Lag Due to Fewer ForeclosuresCalifornia Home Sales, 2005 to 2014

Residential Permits: New construction activity con-tinues to grow as builders are enticed by rising pricesand limited inventories.Multi-family propertiesmakeup the majority of new residential units being builtin the state, driven by demand, as the renter popula-tion has increased significantly since the foreclosure

2014 Riverside/San Bernardino Economic Forecast 11

California Forecast

crisis. And unlike many other states, the vacancy ratefor both ownership (1.2%) and rental properties (5.2%)is very low, which should continue to drive new con-struction permits for both single- and multi-familyproperties into the future.

California Residential Permitting

Indicator Aug-13 Aug-14 ChangeYTD YTD (%)

CaliforniaMulti-Family 27,179 26,730 -1.7Single-Family 24,867 25,768 3.6

52,046 52,498 0.9

United StatesMulti-Family 219,274 256,523 17.0Single-Family 428,989 426,681 -0.5

Total 648,263 683,204 5.4Source: U.S. Census Bureau

Commercial Real Estate: The commercial side of thereal estate market was much slower out of the 're-covery' gate than were residential properties. How-ever, California’s nonresidential market is experienc-ing progress. Vacancies for office space in particular,while remaining high, have begun to decline. Indus-trial properties in California stand out as the healthi-est part of the commercial market with vacancy ratesnow in the low single-digits in most major metropoli-tan areas.

Nonresidential Permits: Improvements in the com-mercial real estate market have spawned new com-mercial development projects. Through August 2014,nonresidential permit values were up 17.7%, withgains spread between the development of new office,hotel, and retail space, and alterations/additions toexisting structures. The increased activity, coupledwith improving residential market conditions, shouldhelp drive additional job growth in Construction overthe next few years.

California Nonresidential Permitting

Indicator Aug-14 YTD Change($Mill.) (%)

New Commercial 4,632 49.9Office 1,183 48.4Retail 1,835 29.2Hotel 548 204.4

Industrial 522 -16.2Other Nonres. 2,386 -18.4Nonres. Alts./Adds. 7,940 21.9

Total Nonres. 15,479 17.7Source: California Homebuilding Foundation

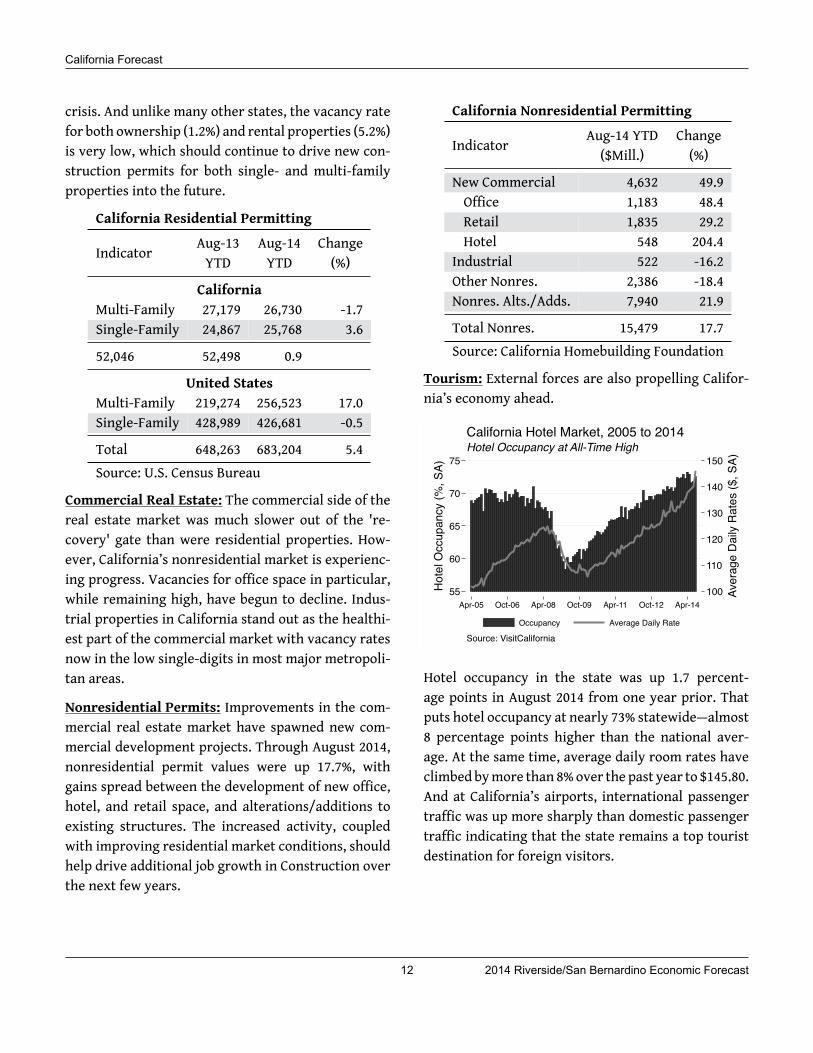

Tourism: External forces are also propelling Califor-nia’s economy ahead.

100

110

120

130

140

150

Aver

age

Daily

Rat

es ($

, SA)

55

60

65

70

75

Hote

l Occ

upan

cy (%

, SA)

Apr-05 Oct-06 Apr-08 Oct-09 Apr-11 Oct-12 Apr-14

Occupancy Average Daily Rate

Source: VisitCalifornia

Hotel Occupancy at All-Time HighCalifornia Hotel Market, 2005 to 2014

Hotel occupancy in the state was up 1.7 percent-age points in August 2014 from one year prior. Thatputs hotel occupancy at nearly 73% statewide—almost8 percentage points higher than the national aver-age. At the same time, average daily room rates haveclimbed bymore than 8%over the past year to $145.80.And at California’s airports, international passengertraffic was up more sharply than domestic passengertraffic indicating that the state remains a top touristdestination for foreign visitors.

12 2014 Riverside/San Bernardino Economic Forecast

California Forecast

What’s Wrong Cyclically?

Although the cyclical effects of the recent recessioncontinue to fade, that progress has not been spreadevenly across the population base. Some Californiansare doing much better in the current economic envi-ronment than others.

Workers Left Behind: California recently returned toits pre-recession peak employment level. However,the sectors that experienced the most growth dur-ing the recovery are not the same sectors that lostthe most jobs during the recession, and many work-ers continue to face difficulty finding work. For exam-ple, the Healthcare, Professional/Scientific/Technicalsector has at least 100,000 more jobs now than at thepeak of the bubble.

California Employment Levels

Industry Jul-07 Aug-14 Diff.Peak (Current) (000s)

Education/Health 1,919.6 2,405.3 485.7Leisure/Hospitality 1,562.6 1,721.7 159.1Prof/Sci/Tech 1,062.9 1,190.6 127.7Admin Support 999.7 1,025.9 26.2Management 207.2 226.0 18.9Other Services 514.2 524.6 10.4NR/Mining 26.7 31.5 4.8Logistics 511.7 512.1 0.4Information 471.4 471.7 0.3

Wholesale Trade 717.3 709.0 -8.3Real Estate 284.2 264.2 -20.0Retail Trade 1,691.6 1,626.9 -64.7Finance/Insurance 614.2 514.3 -99.9Government 2,498.0 2,389.3 -108.7Manufacturing 1,468.8 1,250.6 -218.2Construction 899.4 676.4 -223.0

Total Private 12,951.8 13,150.3 198.5

Total Nonfarm 15,449.8 15,539.6 89.8Source: California EDD

On the other hand, collectively, there are still 500,000fewer jobs in the Retail, Construction, and Manufac-turing sectors. Many former Retail and Constructionworkers are not in a position in terms of skill sets totap into the faster growing and higher wage Profes-sional job sector. As such, at least 25% of the state’sunemployed workers have been unemployed for oversix months—a point at which their skill levels and em-ployability begin to erode.

Rising Inequality: Given the uneven growth acrosshigher and lower wage job sectors, income inequalityin California has increased in the wake of the reces-sion.

0102030405060708090

100

Perc

ent o

f Tot

al In

com

e

0 10 20 30 40 50 60 70 80 90 100Income Percentile

Perfect Equality 20002012

Source: U.S. Census Bureau

Income Distributed More UnevenlyCalifornia Income Inequality

In 2012, the top 20% of income earners in the state ac-counted for 52.6% of all income earned. In 2000, thetop 20% of income earners accounted for just 50.1%of all income earned. Income has become increasinglyconcentrated and inequality has risen over the pastdecade as high-income earners have done better andmiddle-income earners have been more prone to mi-grate out of California in search of more affordablehousing.

Lackluster Wage Growth: Although nominal wageshave been rising over the past 15 years, so too hasthe cost of housing, goods, and services. Adjusting an-nual averagewages into real termswith the ConsumerPrice Index for the western region, and wage growthhas been lackluster at best.

2014 Riverside/San Bernardino Economic Forecast 13

California Forecast

-10

-5

0

5

10

YoY

Gro

wth

(%, S

A)

28,000

29,000

30,000

31,000

32,000

Rea

l Wag

es ($

, SA)

Q1-00 Q1-02 Q1-04 Q1-06 Q1-08 Q1-10 Q1-12 Q1-14

Real Wages GrowthAvg. Growth No Growth

Source: VisitCalifornia

Wage Growth Marginally Positive over Long TermCalifornia Real Wages

In fact, wage growth has only been slightly more pos-itive on a year-over-year basis than it has been nega-tive with growth dropping below zero in 23 of the past56 quarters. On average, real wages in California havegrown by 0.66% since 2000, and at the end of 2013, realwages are almost identical to what they were at theturn of the century, meaning that the quality of lifefor the average Californian has not improved much.

What’s Right Structurally?

In addition to itsmore recent recovery from the reces-sion, California’s many structural assets and advan-tages will also help stimulate economic growth overthe next five years.

Strategic Infrastructure: California is home to in-frastructure that will help generate jobs and eco-nomic activity as the state moves ahead. When com-bined, the Ports of Los Angeles and Long Beach are thesecond largest exporting ports in the nation, behindonly Houston. Add exports from Los Angeles Interna-tional Airport and more goods are shipped throughthe Southern California economy than from any otherport in the nation. While there have been concernsover the competitive threats associated with the ex-pansion of the Panama Canal, those fears are largelyoverblown. Although some firms may find it advan-tageous to circumvent West Coast ports in favor of

ports along the Gulf of Mexico, California will still re-main competitive for time-sensitive deliveries as wellas for the next generation of super-ships that will betoo large for even the widened Panama Canal to ac-commodate.

Educated Workers: California has long been home toa highly educated workforce.

0 10 20 30 40% of Pop. with a Degree or Higher

CaliforniaRhode Island

IllinoisWashington

MinnesotaNew York

New HampshireVirginia

VermontNew Jersey

MarylandConnecticut

ColoradoMassachusetts

Source: U.S. Census Bureau

California Still Relatively EducatedU.S. Educational Attainment, 2012

According to data from the U.S. Census Bureau, over30% of California residents hold at least a bachelor’sdegree. That ranks 15th nationwide, and represents asolid contingent of skilled workers who feed the high-tech industries synonymous with the state. Indeed,California has been ranked amongst the most innova-tive states in the entire union.2

Venture Capital: Perhaps as a result of the skill andeducational levels of California residents, the statecontinues to be a center for technology-based growthand new inventions. Venture capital funding has seenstrong, though bumpy, growth since hitting bottom in2009. Total venture capital funding in California ex-ceeded its pre-recession peak during the first quar-ter of 2014—nearly doubling over the first quarter of2013. Indeed, in 2013 California received more thanhalf of all venture capital investment in several high-tech categories including Semiconductors, Computers

2CNN Money, "10 most inventive states", October 24, 2012,http://money.cnn.com/gallery/smallbusiness/2012/10/24/states-patent-invention/.

14 2014 Riverside/San Bernardino Economic Forecast

California Forecast

and Peripherals, Telecommunications, Media and En-tertainment, Software, and IT Services.3

Venture Capital Investment in 2013

Industry California United CaliforniaStates Share (%)

Semiconductors 395 601 65.7Computers/Periphs. 327 517 63.2Telecomms. 390 644 60.7Media/Entertain. 1,753 2,963 59.2Software 6,206 11,074 56.0IT Services 1,017 1,965 51.8Retailing/Distribution 122 237 51.5Medical Devices/Equip. 980 2,102 46.6Healthcare Services 81 193 41.9Bus. Products/Svcs. 91 218 41.8Biotechnology 1,919 4,655 41.2Industrial Energy 601 1,491 40.3Consumer Prods./Svcs. 423 1,259 33.6Networking/Equipment 212 672 31.6Electronics Instrs. 95 326 29.1Financial Services 160 566 28.2Other 23 98 24.0

Total 14,793 29,580 50.0Source: PWC MoneyTree

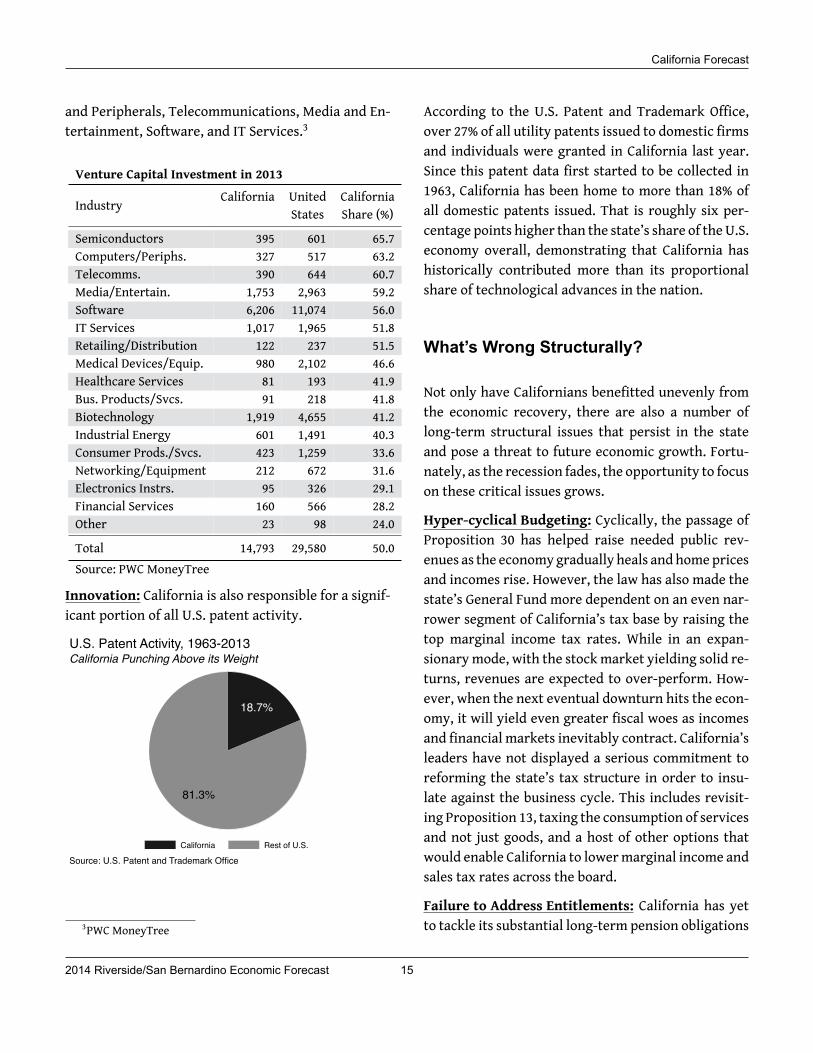

Innovation: California is also responsible for a signif-icant portion of all U.S. patent activity.

18.7%

81.3%

California Rest of U.S.

Source: U.S. Patent and Trademark Office

California Punching Above its WeightU.S. Patent Activity, 1963-2013

3PWC MoneyTree

According to the U.S. Patent and Trademark Office,over 27% of all utility patents issued to domestic firmsand individuals were granted in California last year.Since this patent data first started to be collected in1963, California has been home to more than 18% ofall domestic patents issued. That is roughly six per-centage points higher than the state’s share of the U.S.economy overall, demonstrating that California hashistorically contributed more than its proportionalshare of technological advances in the nation.

What’s Wrong Structurally?

Not only have Californians benefitted unevenly fromthe economic recovery, there are also a number oflong-term structural issues that persist in the stateand pose a threat to future economic growth. Fortu-nately, as the recession fades, the opportunity to focuson these critical issues grows.

Hyper-cyclical Budgeting: Cyclically, the passage ofProposition 30 has helped raise needed public rev-enues as the economygradually heals andhomepricesand incomes rise. However, the law has also made thestate’s General Fund more dependent on an even nar-rower segment of California’s tax base by raising thetop marginal income tax rates. While in an expan-sionarymode, with the stockmarket yielding solid re-turns, revenues are expected to over-perform. How-ever, when the next eventual downturn hits the econ-omy, it will yield even greater fiscal woes as incomesand financial markets inevitably contract. California’sleaders have not displayed a serious commitment toreforming the state’s tax structure in order to insu-late against the business cycle. This includes revisit-ing Proposition 13, taxing the consumption of servicesand not just goods, and a host of other options thatwould enable California to lowermarginal income andsales tax rates across the board.

Failure to Address Entitlements: California has yetto tackle its substantial long-term pension obligations

2014 Riverside/San Bernardino Economic Forecast 15

California Forecast

at the state and local level. Together, CalPERS andCalSTRS represent nearly $140 billion in unfunded li-abilities—even after accounting for the recent stockmarket surge—and are still 24% and 33% unfunded,respectively. Some form of compromise between re-tirees and state and local governments is badly neededas these unfunded obligations represent more thanone full year of General Fund receipts.

CEQA and Housing Costs: One of California’s biggestchallenges is the state’s high cost of housing. Theabuse of the well-intentioned California Environmen-tal Quality Act (CEQA) plays a large role in drivingup building costs by limiting and delaying construc-tion projects. And with the recent surge in the real es-tate market, California has grown even more expen-sive relative to other states. California’s most inex-pensive metro areas are on par with the most expen-sive metro areas in places like Texas, while Califor-nia’s most expensive markets are quickly approach-ing median prices of $1 million. That is well beyondthe reach of the average Californian, and as a result,the state has experienced more out-migration amonglower- and mid-income workers than among high-income workers. This worrisome trend deprives busi-nesses of a strong mid-skilled workforce and makes itdifficult to recruit talent because businesses can’t af-ford to pay wages that would offer a desired quality oflife (such as the ability to buy a home). Containing theexcessive cost of housing should be a top policy goal,and reforming CEQA should be at the heart of that pro-cess.

Education Gap Closing: California has historicallybeen a “barbell” statewithmany high- and low-skilledworkers, and a shrinking population of mid-skilledworkers. It has always, however, had a strong con-tingent of residents on the highly educated end ofthe scale. And while California remains a state witha relatively educated population base, over the pastdecade or so, that education gap has slowly been clos-ing as other states raise their levels of educational at-tainment more and faster. Striving to build and re-

tain the most skilled workforce is critical to Califor-nia maintaining its advantage in the high-tech sectorsthat drive so much of the state’s economic growth.

Educational Attainment LevelsPopulation with a Bachelor's or HigherLocation 2000 2012 Diff. (%)

California 26.6 30.9 4.3Rest of US 24.1 28.9 4.8

Education Gap (%) 2.5 2.0 -0.5Source: U.S. Census Bureau

Effects of Technological Change: Gauging and re-sponding to technological change will remain a long-term challenge for California and for all states. Com-mercial real estate provides a strong example. Withthe ubiquitous nature of the Internet, wireless tech-nology, laptops, smartphones, and tablets in today’sworld, traditional relationships between employmentand commercial absorption are breaking down asmore workers telecommute, work remotely, or workon-site for their clients. As such, the job growth thatused to propel new commercial construction activi-ties, is expected to have a smaller and smaller effecton commercial markets in California in the future.

The Forecast

Beacon Economics is forecasting ongoing improve-ment in California’s economy through the life of theforecast in 2019.

Employment growth will settle in at 2.5% by 2016and the unemployment rate is expected to dip be-low 6% by mid-2017.

Home prices will continue to grow over the nexttwo years, although growth will cool to a 4% to 6%pace that is more consistent with income growth.

16 2014 Riverside/San Bernardino Economic Forecast

California Forecast

As home equity rises and bank lending increases,home sales are also expected to turn around in2015, rising by double-digit percentages next year.

As the economy continues to heal, new construc-tion activity will be stimulated in the residen-tial market (190,000 new units forecast over thenext two years) and the nonresidential market (4%growth forecast this year).

Consumer spending is also forecasted to continueits upward trajectory, growing by roughly 4% overthe next two years.

Cyclically, things are improving. Whether focusingon employment, incomes, GDP, home prices, buildingpermits, or taxable sales (among many other indica-tors), California’s economy is in growth mode. In fact,despite the state’s many challenges, California contin-ues to lead the nation in many key ways.

California also faces critical challenges including edu-cation, infrastructure, housing costs, and the need toinvigoratemanufacturing. Tackled appropriately, Cal-ifornia could climb even higher in the state rankingsand become an even greater economic success.

2014 Riverside/San Bernardino Economic Forecast 17

California ForecastStateHistorical

Table

California

Q1-2012

Q2-2012

Q3-2012

Q4-2012

Q1-2013

Q2-2013

Q3-2013

Q4-2013

Q1-2014

Q2-2014

TotalN

onfarm

Empl.(Mill,SA)

14.56

14.64

14.73

14.90

15.01

15.10

15.21

15.29

15.34

15.45

Grow

th(%

,SAAR

)3.35

2.10

2.55

4.77

2.94

2.53

2.85

2.21

1.19

2.89

Unem

ploy

men

tRate(

%,SA

)10.83

10.67

10.37

9.83

9.37

9.03

8.90

8.43

8.10

7.60

Person

alIncome(

$Bill)

1,760.98

1,780.94

1,795.42

1,883.43

1,816.45

1,848.27

1,871.83

1,889.91

1,909.09

1,937.41

Grow

th(%

,SAAR

)15.68

4.61

3.29

21.10

-13.49

7.19

5.20

3.92

4.12

6.07

TaxableS

ales

($Bill,

SA)

136.50

137.55

139.69

143.93

147.04

149.36

148.88

151.51

152.31

155.27

Grow

th(%

,SAAR

)9.02

3.09

6.39

12.70

8.93

6.46

-1.29

7.27

2.14

7.99

Sing

le-Fam

ilyHo

meP

rices

($000s,SA)

251.18

263.10

274.87

296.50

308.59

336.76

350.23

361.20

368.06

373.57

Grow

th(%

,SAAR

)18.42

20.38

19.13

35.40

17.34

41.82

16.99

13.13

7.81

6.13

Sing

le-Fam

ilyHo

meS

ales

(000s,SA

)87.79

86.64

85.43

89.89

86.75

86.96

87.45

79.04

73.58

78.65

Grow

th(%

,SAAR

)32.62

-5.15

-5.43

22.55

-13.25

0.95

2.27

-33.26

-24.91

30.60

Sing

le-Fam

ilyPe

rmits

(000s,SA

)6.21

6.76

7.26

7.76

8.28

8.68

8.98

9.15

9.12

9.24

Grow

th(%

,SAAR

)25.61

39.69

33.12

30.65

29.77

20.94

14.23

8.19

-1.51

5.43

Multi-Family

Perm

its(000s,SA

)7.48

8.30

8.98

9.40

10.14

10.46

11.00

11.48

11.32

11.31

Grow

th(%

,SAAR

)24.63

51.83

37.03

20.06

35.51

13.15

22.36

18.67

-5.59

-0.05

Nonresiden

tialP

ermits

($Bill,

SA)

3.42

3.77

3.89

4.10

4.48

4.73

5.10

5.32

5.25

5.51

Grow

th(%

,SAAR

)14.51

47.66

13.32

22.96

42.48

24.33

35.63

18.38

-5.08

20.78

Popu

latio

n(M

ill)

37.79

37.87

37.95

38.04

38.12

38.20

38.29

38.38

38.47

38.56

Grow

th(%

,SAAR

)0.82

0.84

0.86

0.87

0.89

0.90

0.91

0.92

0.94

0.96

NetM

igratio

n(000s)

11.07

13.14

14.86

16.24

17.26

17.93

19.14

19.79

21.42

22.76

NaturalInc

rease(

000s)

65.72

65.70

65.84

66.15

66.62

67.26

67.72

68.28

68.82

69.58

StateForecastTa

ble

California

Q3-2014

Q4-2014

Q1-2015

Q2-2015

Q3-2015

Q4-2015

Q1-2016

Q2-2016

Q3-2016

Q4-2016

TotalN

onfarm

Empl.(Mill,SA)

15.52

15.60

15.70

15.79

15.88

15.98

16.08

16.18

16.28

16.39

Grow

th(%

,SAAR

)1.83

2.24

2.37

2.42

2.44

2.45

2.51

2.52

2.53

2.56

Unem

ploy

men

tRate(

%,SA

)7.40

7.26

7.10

6.96

6.82

6.69

6.55

6.42

6.30

6.18

Person

alIncome(

$Bill)

1,947.71

1,973.43

1,997.80

2,021.99

2,047.54

2,070.85

2,098.08

2,124.32

2,152.03

2,180.80

Grow

th(%

,SAAR

)2.14

5.39

5.03

4.93

5.15

4.63

5.36

5.10

5.32

5.46

TaxableS

ales

($Bill,

SA)

156.99

157.14

158.70

160.74

162.09

163.12

165.62

168.06

170.14

172.59

Grow

th(%

,SAAR

)4.51

0.39

4.04

5.23

3.41

2.57

6.28

6.01

5.04

5.89

Sing

le-Fam

ilyHo

meP

rices

($000s,SA)

378.31

383.44

388.75

394.15

399.67

405.08

410.62

416.17

421.77

427.46

Grow

th(%

,SAAR

)5.17

5.53

5.66

5.67

5.72

5.52

5.59

5.51

5.50

5.51

Sing

le-Fam

ilyHo

meS

ales

(000s,SA

)82.35

85.08

87.11

88.84

90.41

91.82

93.10

94.23

95.25

96.19

Grow

th(%

,SAAR

)20.19

13.93

9.87

8.19

7.27

6.37

5.69

4.95

4.42

4.00

Sing

le-Fam

ilyPe

rmits

(000s,SA

)9.86

10.55

11.24

12.17

13.15

14.14

15.14

16.11

17.08

18.01

Grow

th(%

,SAAR

)29.64

31.02

28.62

37.49

36.32

34.00

31.40

27.99

26.36

23.80

Multi-Family

Perm

its(000s,SA

)11.48

11.85

12.50

13.44

14.61

15.93

17.34

18.72

20.00

21.16

Grow

th(%

,SAAR

)6.05

13.62

23.50

33.81

39.74

41.37

40.11

35.87

30.47

25.13

Nonresiden

tialP

ermits

($Bill,

SA)

5.66

5.77

5.91

6.03

6.16

6.29

6.40

6.52

6.64

6.75

Grow

th(%

,SAAR

)11.28

8.17

9.83

8.82

8.60

8.46

7.76

7.50

7.26

6.93

Popu

latio

n(M

ill)

38.66

38.75

38.85

38.95

39.05

39.15

39.26

39.36

39.46

39.57

Grow

th(%

,SAAR

)0.99

1.00

1.02

1.03

1.04

1.04

1.05

1.06

1.06

1.06

NetM

igratio

n(000s)

24.76

25.95

26.92

27.61

28.13

28.49

28.73

28.91

29.02

29.06

NaturalInc

rease(

000s)

70.29

70.73

71.27

71.69

72.31

72.96

73.60

74.23

74.85

75.45

Forecastsb

yBe

acon

Econ

omics

18 2014 Riverside/San Bernardino Economic Forecast

Inland Empire Forecast

by Rafael De Anda

ContentsKey Chapter Findings 20The Third Recovery in 25 Years 20Population 22Employment 23Business Activity 24Real Estate 25

Inland Empire Forecast

Key Chapter Findings

In comparison with the last economic recovery, from 2001 to 2005, the current economic recovery haslacked support from the Construction and Retail Trade industries. However, both industries are startingto heat up, a good omen for the economy at large.

Population growth, one of the underlying components of long-term economic growth, is projected tobounce back over the next five years.

Employment growthwas strong in 2013, and 2014 is shaping up to be a good year as well. Yet a fair numberof skilled and educated workers are still looking for work.

Auto sales and tourism are supporting local economic growth.

Although home prices have improved, there is plenty of room for growth.

The Third Recovery in 25 Years

With the economy experiencing its third recovery in25 years, many Inland Empire businesses and resi-dents are starting to feel at ease as the aftereffectsof the dreadful Great Recession fade. As has beenwell documented, the economic recovery has beenpainfully slow by historical standards and more slug-gish than the upturns in neighboring coastal commu-nities. However, other inland regions throughout thestate were equally bullied by the downturn and haverecovered at a similarly slow pace—with the excep-tion of the energy-rich Bakersfield metropolitan area,which has seen robust economic growth.

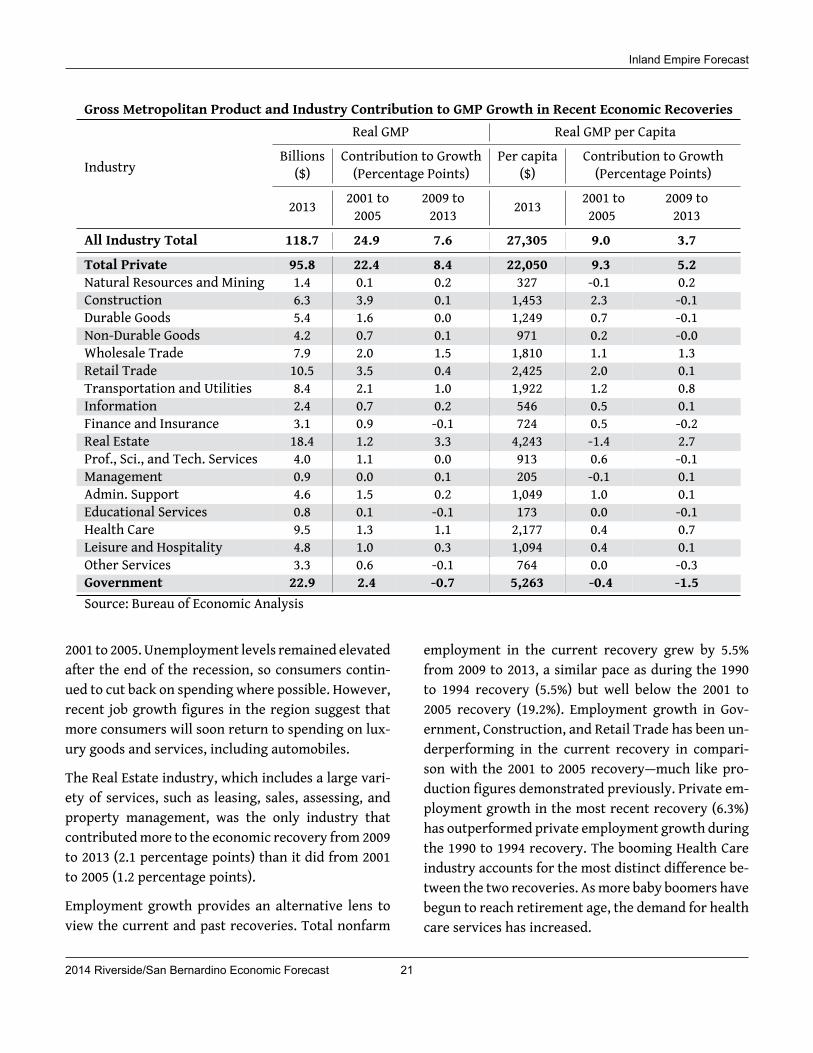

There are key differences between the Inland Empire’scurrent economic recovery and the recovery in theearly 2000s. First, in this recovery, the Governmentsector has not contributed to economic growth, owingto forces outside local leaders’ control. The Govern-ment sector’s contribution to growth in economic out-put, as measured by the region’s gross metropolitanproduct (GMP), was 2.4 percentage points of the total24.9% GMP growth from 2001 to 2005. In comparison,the Government contribution to economic growth ineconomic output from 2009 to 2013 was a negative 0.7percentage points. In dollar value, that equates to a

$3.6 billion difference, which is augmented by the in-direct and induced impacts that affect other indus-tries to a varying degree.

Through 2013, the current economic recovery alsolacked a lift from the Construction industry, a strongcontributor to the recovery in 2001 to 2005. BeaconEconomics has long held the position that housingthroughout the state is undersupplied, yet with homeprices slashed in half over the course of two years andwith commercial vacancy rates shooting upward inthe aftermath of the recession,many investors and de-velopers were discouraged from building newhousingand commercial structures. The Construction indus-try contributed 0.1 percentage points to GMP growthfrom 2009 to 2013. In comparison, Construction added3.9 percentage points to GMP growth from 2001 to2005. Yet with investment now starting to pick up,particularly for massive warehouses and large-scaleresidential developments, we expect Construction tobe one of the largest contributors to economic growthmoving forward.

The current economic recovery has also lacked a sig-nificant contribution from the Retail Trade industry.From 2009 to 2013, Retail Trade accounted for 0.4 per-centage points of GMP growth, compared with the 3.5percentage point contribution to GMP growth from

20 2014 Riverside/San Bernardino Economic Forecast

Inland Empire Forecast

Gross Metropolitan Product and Industry Contribution to GMP Growth in Recent Economic Recoveries

Industry

Real GMP Real GMP per CapitaBillions Contribution to Growth Per capita Contribution to Growth

($) (Percentage Points) ($) (Percentage Points)

2013 2001 to 2009 to 2013 2001 to 2009 to2005 2013 2005 2013

All Industry Total 118.7 24.9 7.6 27,305 9.0 3.7Total Private 95.8 22.4 8.4 22,050 9.3 5.2Natural Resources and Mining 1.4 0.1 0.2 327 -0.1 0.2Construction 6.3 3.9 0.1 1,453 2.3 -0.1Durable Goods 5.4 1.6 0.0 1,249 0.7 -0.1Non-Durable Goods 4.2 0.7 0.1 971 0.2 -0.0Wholesale Trade 7.9 2.0 1.5 1,810 1.1 1.3Retail Trade 10.5 3.5 0.4 2,425 2.0 0.1Transportation and Utilities 8.4 2.1 1.0 1,922 1.2 0.8Information 2.4 0.7 0.2 546 0.5 0.1Finance and Insurance 3.1 0.9 -0.1 724 0.5 -0.2Real Estate 18.4 1.2 3.3 4,243 -1.4 2.7Prof., Sci., and Tech. Services 4.0 1.1 0.0 913 0.6 -0.1Management 0.9 0.0 0.1 205 -0.1 0.1Admin. Support 4.6 1.5 0.2 1,049 1.0 0.1Educational Services 0.8 0.1 -0.1 173 0.0 -0.1Health Care 9.5 1.3 1.1 2,177 0.4 0.7Leisure and Hospitality 4.8 1.0 0.3 1,094 0.4 0.1Other Services 3.3 0.6 -0.1 764 0.0 -0.3Government 22.9 2.4 -0.7 5,263 -0.4 -1.5Source: Bureau of Economic Analysis

2001 to 2005. Unemployment levels remained elevatedafter the end of the recession, so consumers contin-ued to cut back on spending where possible. However,recent job growth figures in the region suggest thatmore consumers will soon return to spending on lux-ury goods and services, including automobiles.

The Real Estate industry, which includes a large vari-ety of services, such as leasing, sales, assessing, andproperty management, was the only industry thatcontributedmore to the economic recovery from 2009to 2013 (2.1 percentage points) than it did from 2001to 2005 (1.2 percentage points).

Employment growth provides an alternative lens toview the current and past recoveries. Total nonfarm

employment in the current recovery grew by 5.5%from 2009 to 2013, a similar pace as during the 1990to 1994 recovery (5.5%) but well below the 2001 to2005 recovery (19.2%). Employment growth in Gov-ernment, Construction, and Retail Trade has been un-derperforming in the current recovery in compari-son with the 2001 to 2005 recovery—much like pro-duction figures demonstrated previously. Private em-ployment growth in the most recent recovery (6.3%)has outperformed private employment growth duringthe 1990 to 1994 recovery. The booming Health Careindustry accounts for the most distinct difference be-tween the two recoveries. Asmore baby boomers havebegun to reach retirement age, the demand for healthcare services has increased.

2014 Riverside/San Bernardino Economic Forecast 21

Inland Empire Forecast

The economy is poised to accelerate in the com-ing years. The industries that provided the largestcontributions to the economic recovery in 2001 to2005—Construction and Retail Trade—have picked upthe pace of hiring through 2014. The recovery willalso be supported by logistics firms that are appear-ing throughout the region and by health care facilitiesthat are expanding.

Employment and Industry Employment Growth inRecent Economic Recoveries

Industry

Emp. Contribution to Growth(000s) (Percentage Points)

2013 1990 to 2001 to 2009 to1994 2005 2013

Total Nonfarm 1,226 5.5 19.2 5.5

Total Private 1,001 4.5 17.2 6.3NR/Mining 1 0.0 0.0 0.0Construction 69 -2.5 3.3 0.1Non-Durable Goods 30 0.4 0.0 -0.1Durable Goods 57 0.5 0.2 -0.1Wholesale Trade 56 0.3 0.8 0.6Retail Trade 165 0.8 3.1 0.7Transport 79 1.2 1.5 1.0Information 11 -0.1 0.0 -0.2Financial Activities 42 0.2 1.1 0.0Prof., Sci., and Tech. Svc. 38 -0.6 1.0 0.0Management 9 0.2 0.1 0.0Admin Support 86 1.2 1.9 0.6Health Care 165 1.9 1.8 2.3Leisure and Hospitality 136 0.7 1.7 1.1Other Services 41 0.4 0.3 0.3Government 225 1.1 1.9 -0.9Source: California Employment Development Dept.

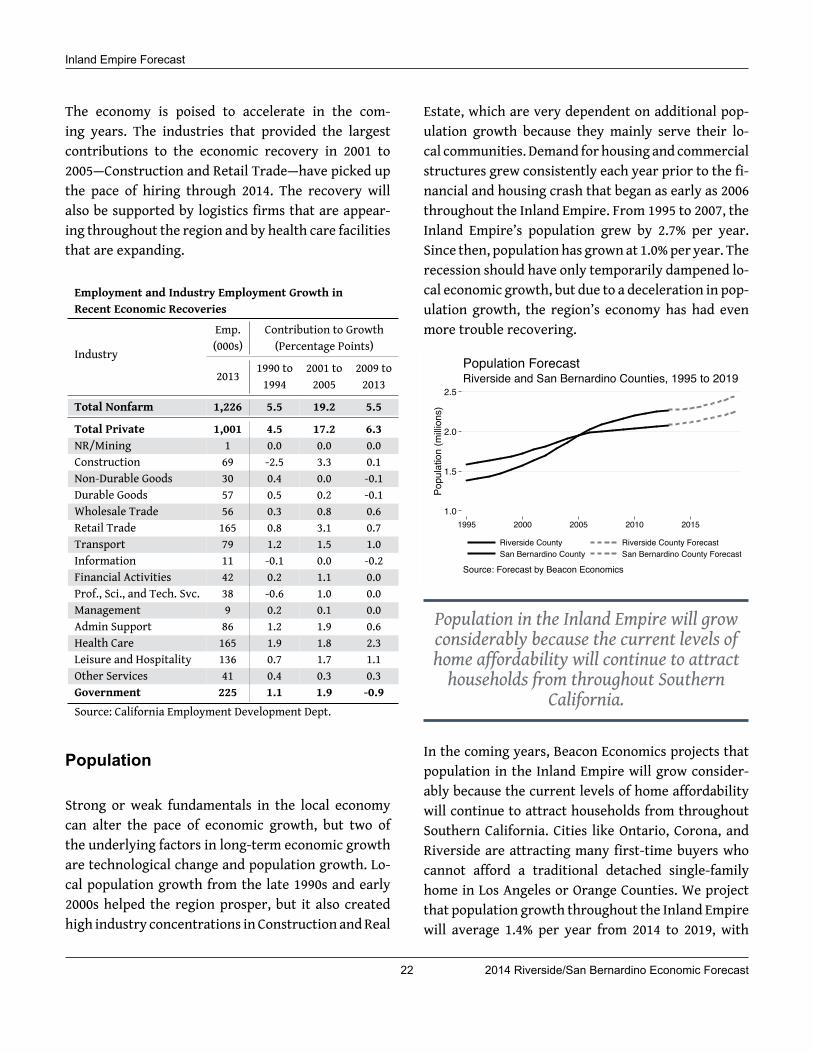

Population

Strong or weak fundamentals in the local economycan alter the pace of economic growth, but two ofthe underlying factors in long-term economic growthare technological change and population growth. Lo-cal population growth from the late 1990s and early2000s helped the region prosper, but it also createdhigh industry concentrations in Construction andReal

Estate, which are very dependent on additional pop-ulation growth because they mainly serve their lo-cal communities. Demand for housing and commercialstructures grew consistently each year prior to the fi-nancial and housing crash that began as early as 2006throughout the Inland Empire. From 1995 to 2007, theInland Empire’s population grew by 2.7% per year.Since then, population has grown at 1.0%per year. Therecession should have only temporarily dampened lo-cal economic growth, but due to a deceleration in pop-ulation growth, the region’s economy has had evenmore trouble recovering.

1.0

1.5

2.0

2.5

Popu

latio

n (m

illion

s)

1995 2000 2005 2010 2015

Riverside County Riverside County ForecastSan Bernardino County San Bernardino County Forecast

Source: Forecast by Beacon Economics

Riverside and San Bernardino Counties, 1995 to 2019Population Forecast

Population in the Inland Empire will growconsiderably because the current levels ofhome affordability will continue to attracthouseholds from throughout Southern

California.

In the coming years, Beacon Economics projects thatpopulation in the Inland Empire will grow consider-ably because the current levels of home affordabilitywill continue to attract households from throughoutSouthern California. Cities like Ontario, Corona, andRiverside are attracting many first-time buyers whocannot afford a traditional detached single-familyhome in Los Angeles or Orange Counties. We projectthat population growth throughout the Inland Empirewill average 1.4% per year from 2014 to 2019, with

22 2014 Riverside/San Bernardino Economic Forecast

Inland Empire Forecast

a strong return in domestic migration to the region.Furthermore, we project that both Riverside Countyand San Bernardino County will grow equally, eventhough recent population growth has favored River-side County (1.1% in 2014) more than San BernardinoCounty (0.8% in 2014).

As a result, a strong return in population growth willlead to output growth that more closely resemblespre-recession levels.

-7.5

-5.0

-2.5

0.0

2.5

5.0

7.5

Annu

al G

rowt

h (%

)

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Source: Bureau of Economic Analysis

California and Inland Empire, 2002 to 2013Annual Economic Output Growth

California GSP Inland Empire GMP

Employment

Our headline from a year ago noted that employ-ment was “slowly” moving forward. As we ex-pected, the California Employment Development De-partment produced revised employment numbersthat showed even better job growth than previouslyreported—upwards of 4% from August 2012 to Au-gust 2013. Employment growth in the Inland Empirethrough 2014 has continued to flourish, helping bringdown the region’s unemployment rate from 10.0% inAugust 2013 to 8.7% in August 2014.

Over the next five years, Beacon Economics projectsemployment growth to continue to remain elevated.One reason our projection remains optimistic is thatthere are plenty of unemployed workers available tobusinesses that are now looking to expand. The un-

employment rates in the Cities of San Bernardino andMoreno Valley were estimated at 16.6% and 13.9%, re-spectively, in 2013. And many of these workers arewell qualified and well educated. In the City of SanBernardino, 3,370 unemployed workers (35%) look-ing for work had attended college or received an as-sociate’s degree or higher, while 2,760 unemployedworkers (30%) in the City of Moreno Valley had thesame qualifications.

The Logistics industry is particularly likely to expand.Widespread developments of warehouses and distri-bution centers have been appearing over the last fewyears, and more are coming online over the course ofthe next year. Jobs at logistics centers require skillsand training, and thus pay livable wages. In 2013, theaverage wage at Transportation and Warehousing es-tablishments was 9.7% higher than in all private in-dustries ($41,340 per year).

0

5

10

15

Une

mpl

oym

ent R

ate

(%, S

A)

600

900

1,200

1,500

Non

farm

Em

ploy

men

t (00

0s, S

A)

Q1-01 Q1-04 Q1-07 Q1-10 Q1-13 Q1-16 Q1-19

Nonfarm Employment Nonfarm Employment ForecastUnemployment Rate Unemployment Rate Forecast

Source: Forecast by Beacon Economics

Inland Empire, Q1-01 to Q4-19Employment and Unemployment Rate Forecast

Jobs in the Health Care industry are also projected tocontinue to grow over the next five years, though notall of these jobs require advanced degrees. For exam-ple, 15.3% of jobs in the Health Care industry are inoffice and administrative support occupations, 3.5% ofjobs are in management occupations, 3.0% of jobs arein food preparation or serving-related jobs, and 2.5%of jobs are in building and grounds cleaning andmain-tenance occupations, according to national statisticspublished by the U.S. Bureau of Labor Statistics.

2014 Riverside/San Bernardino Economic Forecast 23

Inland Empire Forecast

Beacon Economics projects that totalnonfarm employment will grow by 3.2% from

the second quarter of 2014 to the secondquarter of 2015.

With major contributions from these key industries,Beacon Economics projects that total nonfarm em-ployment will grow by 3.2% from the second quarterof 2014 to the second quarter of 2015. In the followingyears, we expect that employment growth will followat about the same clip butmore likely average 3.4% an-nual growth through 2019. By these projections, non-farm employment will surpass the 1.5 millionmark bythe end of 2019, adding more than 250,000 jobs overthe course of five years.

Business Activity

Many businesses in the Inland Empire have been ex-panding their workforce and production levels overthe last few years, helping taxable sales in the two-county region rebound from the recession. Yet com-pared to the 2001 to 2005 recovery, when taxable salesgrew by 39% after inflation adjustments, taxable salesonly grew by 23% from 2009 to 2013.4

Through the second quarter of 2014, taxable salesgrowth appears to be decelerating. During the 2014fiscal year, total taxable sales grew by 5.7%, a slowerpace than in the 2013 fiscal year (8.3%) and the 2012fiscal year (9.8%).5 A large portion of the previousgrowth is in part attributable to major constructionprojects, such as the Genesis Solar Energy Project byNextEra Energy Resources. These types of projectsprovided a boost to the local economy when it neededit most, but they are now near completion.

4Prior to adjustments for inflation, taxable sales from 2001 to2005 grew by 53%, while taxable sales from 2009 to 2013 grew by34%.

5These figures are not adjusted for inflation.

Moving forward, more traditional means of consumeractivity will help the Inland Empire continue to ex-pand its taxable sales base. Auto sales, in particular,have been providing the local economy with an addedlayer of support, as pent-up demand for automobileshas helped tax receipts from autos and transportationgrow by 11.2% in Riverside County and 6.5% in SanBernardino County from the second quarter of 2013to the second quarter of 2014. San Bernardino Countyhas seven new automobile dealers that opened theirdoors between the first quarter of 2013 and the firstquarter of 2014, according to the California Employ-ment Development Department.

Hotel occupancy rates throughout the InlandEmpire picked up by 3.5 percentage points

from the first five months of 2013 to the sameperiod in 2014.

Tourism has also been strong throughout the region,helping bring in money from outside of the area. Andthe number of tourists who stayed in local hotels con-tinued to grow. Hotel occupancy rates throughoutthe Inland Empire picked up by 3.5 percentage pointsfrom the first fivemonths of 2013 to the sameperiod in2014, reaching a healthy 71.2%, according to PKF Con-sulting. Gross receipts from restaurants and hotels,which include local spending as well, grew by 5.5% inRiverside County and 7.2% in San Bernardino Countyfrom the second quarter of 2013 to the second quarterof 2014. In addition, the number of passengers flyingthrough Ontario International Airport finally grew af-ter years of decline.

Overall, economic activity indicators are heading inthe right direction for the Inland Empire, and theeconomy is poised for further growth. Beacon Eco-nomics projects taxable sales in the region to grow by5.1% from the second quarter of 2014 to the secondquarter of 2015. Afterwards, with help from under-lying growth in population counts throughout River-side and San Bernardino Counties, taxable sales are

24 2014 Riverside/San Bernardino Economic Forecast

Inland Empire Forecast

expected to grow from 6.5% to 7.5% annually through2018.

0

5

10

15

20

25

Taxa

ble

Sale

s ($

Milli

ons,

SA)

Q1-01 Q1-04 Q1-07 Q1-10 Q1-13 Q1-16 Q1-19

Actual Forecast

Source: Forecast by Beacon Economics

Inland Empire, Q1-01 to Q4-19Taxable Sales Forecast