b a c kn e x t h o m e copyright 2001 mcgraw-hill ryerson limited. all rights reserved. 2&3...

TRANSCRIPT

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

2&3Please read and take BRIEF notes on the following Power-Point presentation.

CHAPTER

Analyzing and Recording Transactions

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

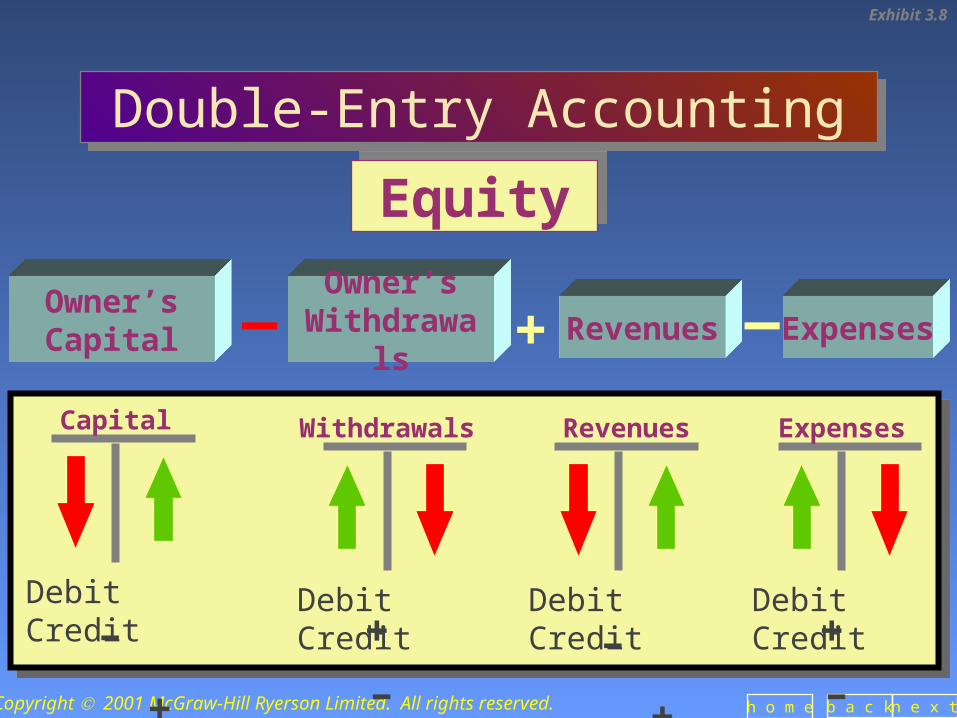

The expanded basic equation is:Assets = Liabilities + Capital - Drawings + Revenues

- Expenses

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Debit Credit

Capital

- +

EquityEquity

_Revenues Expenses

Owner’s Capital

Owner’s Withdrawals + _

Debit Credit

Withdrawals

+ -Debit Credit

Expenses

+ -Debit Credit

Revenues

- +

Double-Entry AccountingDouble-Entry Accounting

Exhibit 3.8

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Exhibit 3.1

Overview of the Accounting CycleOverview of the Accounting Cycle

1. Analyze transactions

based on source

documentsChapter 1 and 2

2. JournalizeChapter 3

3. PostChapter 3

9. Prepare post-closing trial balance

Chapter 5

8. CloseChapter 5

7. Prepare financial

statements Chapter 2 through 5

6. Prepare adjusted trial

balanceChapter 4

5. AdjustChapter 4

4. Prepare unadjusted trial

balanceChapter 3

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Sales Invoices

Bank Statement

Purchase Orders

Cheques

Source DocumentsSource Documents

Source documents identify and describe transactions

and events and are the source of accounting

information.

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

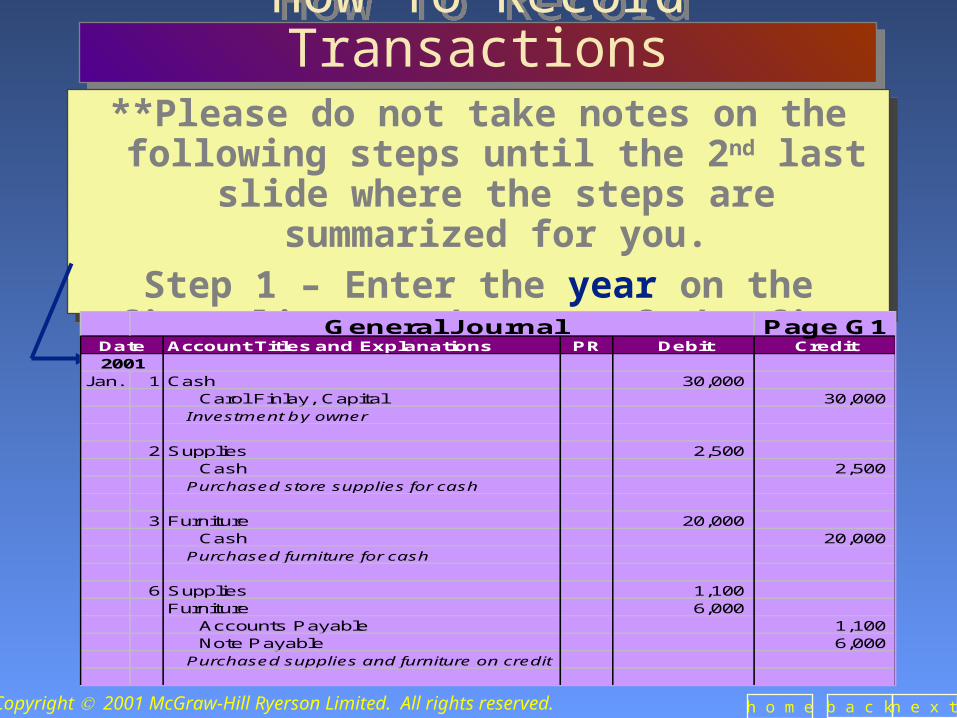

Recording TransactionsRecording Transactions

Entries are originally recorded in a journal. The process of recording the transactions is called journalizing. An example follows:

Entries are originally recorded in a journal. The process of recording the transactions is called journalizing. An example follows:

Page G1Account Titles and Explanations PR Debit Credit

Jan. 1 Cash 30,000 Carol Finlay, Capital 30,000

Investment by owner

2 Supplies 2,500 Cash 2,500

Purchased store supplies for cash

3 Furniture 20,000 Cash 20,000

Purchased furniture for cash

6 Supplies 1,100 Furniture 6,000 Accounts Payable 1,100 Note Payable 6,000

Purchased supplies and furniture on credit

Date2001

General Journal

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

How To Record TransactionsHow To Record Transactions**Please do not take notes on the following steps

until the 2nd last slide where the steps are summarized for you.

Step 1 – Enter the year on the first line at the top of the first column.

**Please do not take notes on the following steps until the 2nd last slide where the steps are

summarized for you.Step 1 – Enter the year on the first line at the top

of the first column.Page G1

Account Titles and Explanations PR Debit Credit

Jan. 1 Cash 30,000 Carol Finlay, Capital 30,000

Investment by owner

2 Supplies 2,500 Cash 2,500

Purchased store supplies for cash

3 Furniture 20,000 Cash 20,000

Purchased furniture for cash

6 Supplies 1,100 Furniture 6,000 Accounts Payable 1,100 Note Payable 6,000

Purchased supplies and furniture on credit

Date2001

General Journal

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Recording TransactionsRecording Transactions

Step 2 and 3 – Enter the month in column one on the first line of the journal entry and the day in column two. Note that entries are recorded in

chronological order (by date).

Step 2 and 3 – Enter the month in column one on the first line of the journal entry and the day in column two. Note that entries are recorded in

chronological order (by date).Page G1

Account Titles and Explanations PR Debit Credit

Jan. 1 Cash 30,000 Carol Finlay, Capital 30,000

Investment by owner

2 Supplies 2,500 Cash 2,500

Purchased store supplies for cash

3 Furniture 20,000 Cash 20,000

Purchased furniture for cash

6 Supplies 1,100 Furniture 6,000 Accounts Payable 1,100 Note Payable 6,000

Purchased supplies and furniture on credit

Date2001

General Journal

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Recording TransactionsRecording Transactions

Step 4 – Enter the titles of accounts debited. Account titles are taken from the chart of accounts and are

aligned with the left margin of the Account titles and explanation column. Accounts to be debited are always entered before accounts being credited.

Step 4 – Enter the titles of accounts debited. Account titles are taken from the chart of accounts and are

aligned with the left margin of the Account titles and explanation column. Accounts to be debited are always entered before accounts being credited.

Page G1Account Titles and Explanations PR Debit Credit

Jan. 1 Cash 30,000 Carol Finlay, Capital 30,000

Investment by owner

2 Supplies 2,500 Cash 2,500

Purchased store supplies for cash

3 Furniture 20,000 Cash 20,000

Purchased furniture for cash

6 Supplies 1,100 Furniture 6,000 Accounts Payable 1,100 Note Payable 6,000

Purchased supplies and furniture on credit

Date2001

General Journal

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Recording TransactionsRecording Transactions

Step 5 – Enter the debit amount in the Debit column on the same line as the

accounts to be debited.

Step 5 – Enter the debit amount in the Debit column on the same line as the

accounts to be debited.Page G1

Account Titles and Explanations PR Debit Credit

Jan. 1 Cash 30,000 Carol Finlay, Capital 30,000

Investment by owner

2 Supplies 2,500 Cash 2,500

Purchased store supplies for cash

3 Furniture 20,000 Cash 20,000

Purchased furniture for cash

6 Supplies 1,100 Furniture 6,000 Accounts Payable 1,100 Note Payable 6,000

Purchased supplies and furniture on credit

Date2001

General Journal

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Recording TransactionsRecording Transactions

Step 6 – Enter the titles of accounts credited. Account titles are indented from the left margin of the Account Titles and Explanation column

to distinguish them from debits.

Step 6 – Enter the titles of accounts credited. Account titles are indented from the left margin of the Account Titles and Explanation column

to distinguish them from debits.Page G1

Account Titles and Explanations PR Debit Credit

Jan. 1 Cash 30,000

Carol Finlay, Capital 30,000 Investment by owner

2 Supplies 2,500 Cash 2,500

Purchased store supplies for cash

3 Furniture 20,000 Cash 20,000

Purchased furniture for cash

6 Supplies 1,100 Furniture 6,000 Accounts Payable 1,100 Note Payable 6,000

Purchased supplies and furniture on credit

Date2001

General Journal

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Recording TransactionsRecording Transactions

Step 7 – Enter the credit amount in the Credit column on the same line as the

accounts to be credited.

Step 7 – Enter the credit amount in the Credit column on the same line as the

accounts to be credited.Page G1

Account Titles and Explanations PR Debit Credit

Jan. 1 Cash 30,000

Carol Finlay, Capital 30,000 Investment by owner

2 Supplies 2,500 Cash 2,500

Purchased store supplies for cash

3 Furniture 20,000 Cash 20,000

Purchased furniture for cash

6 Supplies 1,100 Furniture 6,000 Accounts Payable 1,100 Note Payable 6,000

Purchased supplies and furniture on credit

Date2001

General Journal

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Recording TransactionsRecording Transactions

Step 8 – Write a brief explanation of the transaction on the line below the entry.

Step 8 – Write a brief explanation of the transaction on the line below the entry.

Page G1Account Titles and Explanations PR Debit Credit

Jan. 1 Cash 30,000 Carol Finlay, Capital 30,000

Investment by owner

2 Supplies 2,500 Cash 2,500

Purchased store supplies for cash

3 Furniture 20,000 Cash 20,000

Purchased furniture for cash

6 Supplies 1,100 Furniture 6,000 Accounts Payable 1,100 Note Payable 6,000

Purchased supplies and furniture on credit

Date2001

General Journal

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Recording TransactionsRecording Transactions

Step 9 – Skip a line between each journal entry for clarity.

Step 9 – Skip a line between each journal entry for clarity.

Page G1Account Titles and Explanations PR Debit Credit

Jan. 1 Cash 30,000 Carol Finlay, Capital 30,000

Investment by owner

2 Supplies 2,500 Cash 2,500

Purchased store supplies for cash

3 Furniture 20,000 Cash 20,000

Purchased furniture for cash

6 Supplies 1,100 Furniture 6,000 Accounts Payable 1,100 Note Payable 6,000

Purchased supplies and furniture on credit

Date2001

General Journal

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

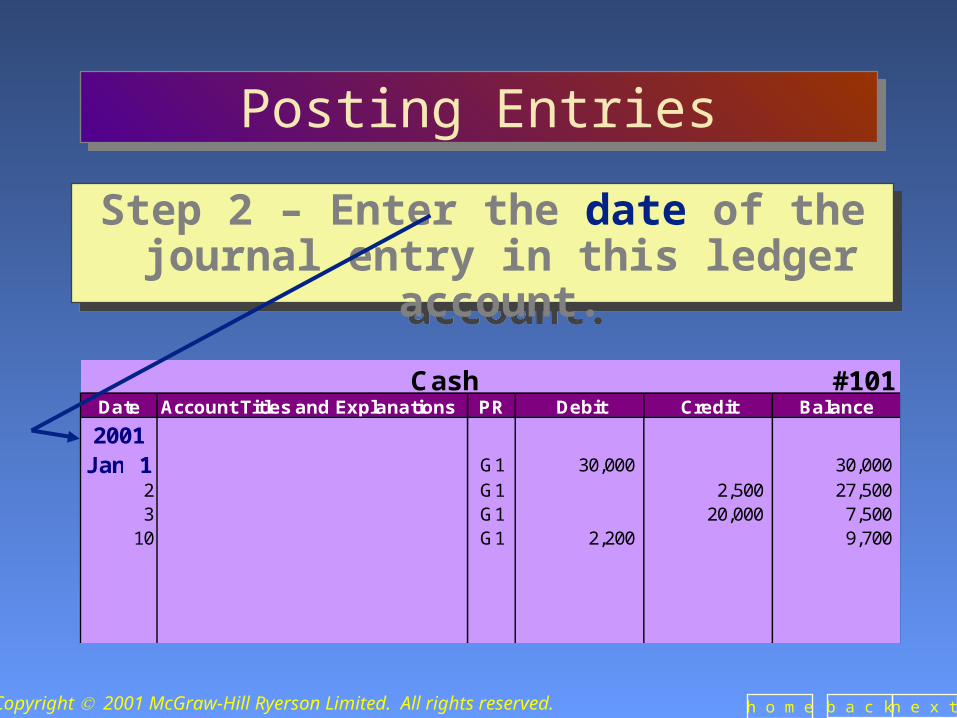

Posting EntriesPosting Entries

Entries are then posted from the journal into the general ledger on a transaction by transaction

basis; first the debit, then the credit.

Entries are then posted from the journal into the general ledger on a transaction by transaction

basis; first the debit, then the credit.

#101Account Titles and Explanations PR Debit Credit Balance

Jan. 1 G1 30,000 30,000 2 G1 2,500 27,500 3 G1 20,000 7,500

10 G1 2,200 9,700

Cash Account in the General LedgerDate2001

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Posting EntriesPosting Entries

Step 1 – Identify the ledger account that was debited in the journal entry and find it in the

general ledger. Example – first entry on Jan. 1 had a debit to the cash account for $30,000.

Step 1 – Identify the ledger account that was debited in the journal entry and find it in the

general ledger. Example – first entry on Jan. 1 had a debit to the cash account for $30,000.

#101Account Titles and Explanations PR Debit Credit Balance

Jan. 1 G1 30,000 30,000 2 G1 2,500 27,500 3 G1 20,000 7,500

10 G1 2,200 9,700

Cash Date2001

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Posting EntriesPosting Entries

Step 2 – Enter the date of the journal entry in this ledger account.

Step 2 – Enter the date of the journal entry in this ledger account.

#101Account Titles and Explanations PR Debit Credit Balance

Jan. 1 G1 30,000 30,000 2 G1 2,500 27,500 3 G1 20,000 7,500

10 G1 2,200 9,700

Cash Date

2001

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Posting EntriesPosting Entries

Step 3 – Enter the amount debited from the journal entry into the Debit column of the

ledger account.

Step 3 – Enter the amount debited from the journal entry into the Debit column of the

ledger account.

#101Account Titles and Explanations PR Debit Credit Balance

Jan. 1 G1 30,000 30,000 2 G1 2,500 27,500 3 G1 20,000 7,500

10 G1 2,200 9,700

Cash Date2001

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Posting EntriesPosting Entries

Step 4 – Enter the source of the debit in the PR (post-reference) column. The letter G indicates

the entry came from the general journal.

Step 4 – Enter the source of the debit in the PR (post-reference) column. The letter G indicates

the entry came from the general journal.

#101Account Titles and Explanations PR Debit Credit Balance

Jan. 1 G1 30,000 30,000 2 G1 2,500 27,500 3 G1 20,000 7,500

10 G1 2,200 9,700

Cash Date2001

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Posting EntriesPosting Entries

Step 5 – Compute and enter the account’s new balance in the Balance column. Remember, a debit balance would be increased by a debit

and decreased by a credit.

Step 5 – Compute and enter the account’s new balance in the Balance column. Remember, a debit balance would be increased by a debit

and decreased by a credit.

#101Account Titles and Explanations PR Debit Credit Balance

Jan. 1 G 30,000 30,000 2 G 2,500 27,500 3 G 20,000 7,500

10 G 2,200 9,700

Cash Account (in general ledger)Date2001

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Recording TransactionsRecording Transactions

Step 6 – Finally, enter the ledger account number in the PR column of the journal entry.

Step 6 – Finally, enter the ledger account number in the PR column of the journal entry.

Page G1Account Titles and Explanations PR Debit Credit

Jan. 1 Cash 101 30,000 Carol Finlay, Capital 30,000

Investment by owner

2 Supplies 2,500 Cash 2,500

Purchased store supplies for cash

3 Furniture 20,000 Cash 20,000

Purchased furniture for cash

6 Supplies 1,100 Furniture 6,000 Accounts Payable 1,100 Note Payable 6,000

Purchased supplies and furniture on credit

Date2001

General Journal

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

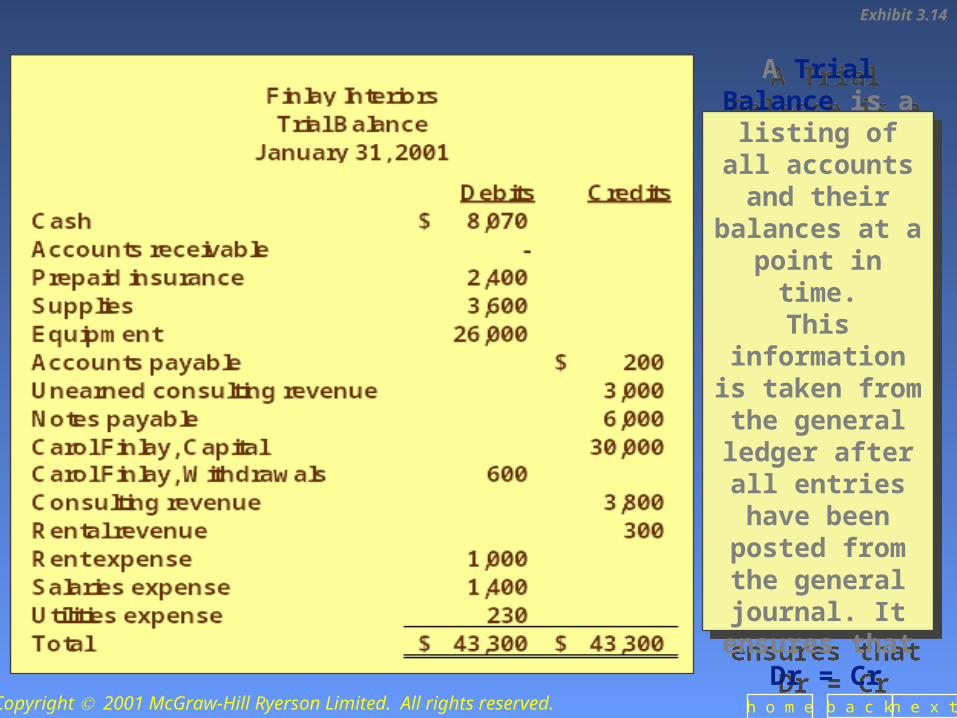

A Trial Balance is a listing of all accounts and

their balances at a point in time.

This information is taken from the general

ledger after all entries have been posted

from the general journal. It

ensures that Dr = Cr

A Trial Balance is a listing of all accounts and

their balances at a point in time.

This information is taken from the general

ledger after all entries have been posted

from the general journal. It

ensures that Dr = Cr

Exhibit 3.14

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Posting Steps SummarizedPosting Steps Summarized

General Journal Entry – Steps:• Record the date• Account debited – record amount• Account credited – record amount• Brief explanation of transaction• Skip a line before next entry

General Ledger Entry – Steps:• Find the ledger account affected – the debit account then the credit

account and then do the following:• Record date• Record amount• Record source in PR column (G indicates from GJ)• Calculate the new ledger account balance• Enter the ledger account number in the PR column of the journal

entry

b a c k n e x th o m eCopyright 2001 McGraw-Hill Ryerson Limited. All rights reserved.

Accounting Cycle Step #3Accounting Cycle Step #3

Prepare an unadjusted trial balance sheet.This is the end of Chapters 2 & 3.

Next we will: Take the 10 min. quiz Review GAAPS Review the 3 adjusting entries you learned last year and

introduce 2 new entries!