avoid the trap: how to make it through college without becoming a financial prisoner

TRANSCRIPT

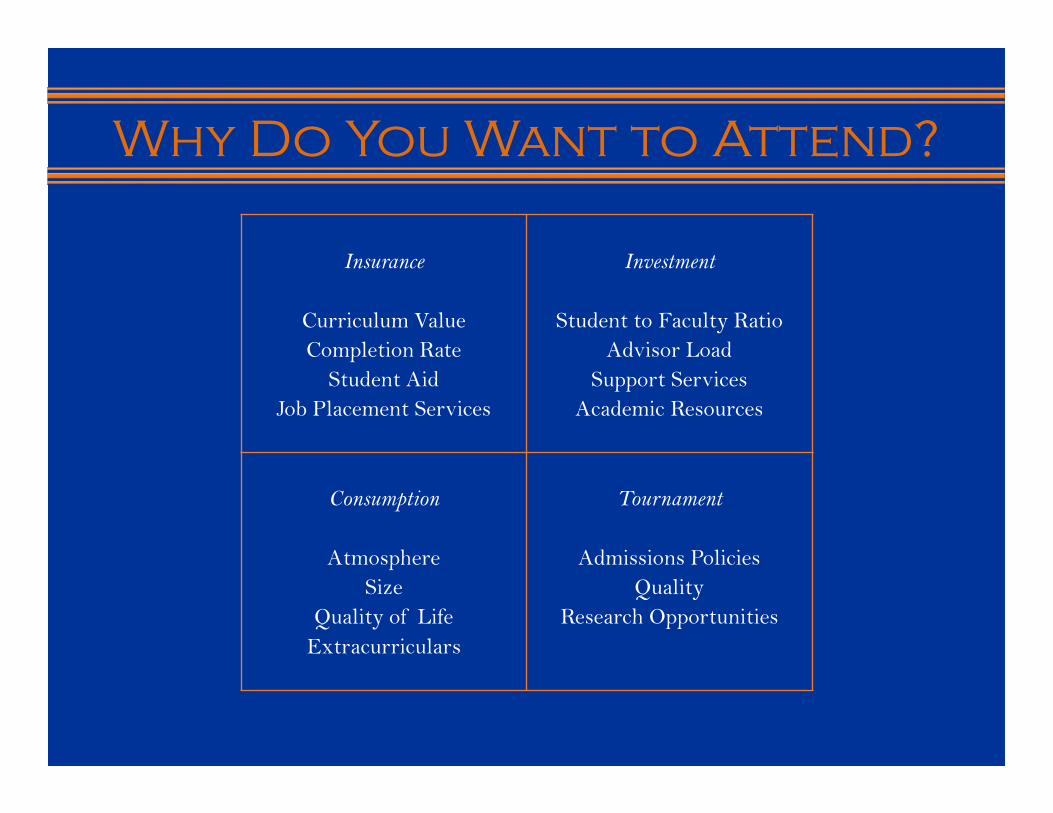

Why Do You Want to Attend?

Insurance Investment

Curriculum Value Student to Faculty Ratio

Completion Rate Advisor Load

Student Aid Support Services

Job Placement Services Academic Resources

Consumption Tournament

Atmosphere Admissions Policies

Size Quality

Quality of Life Research Opportunities

Extracurriculars

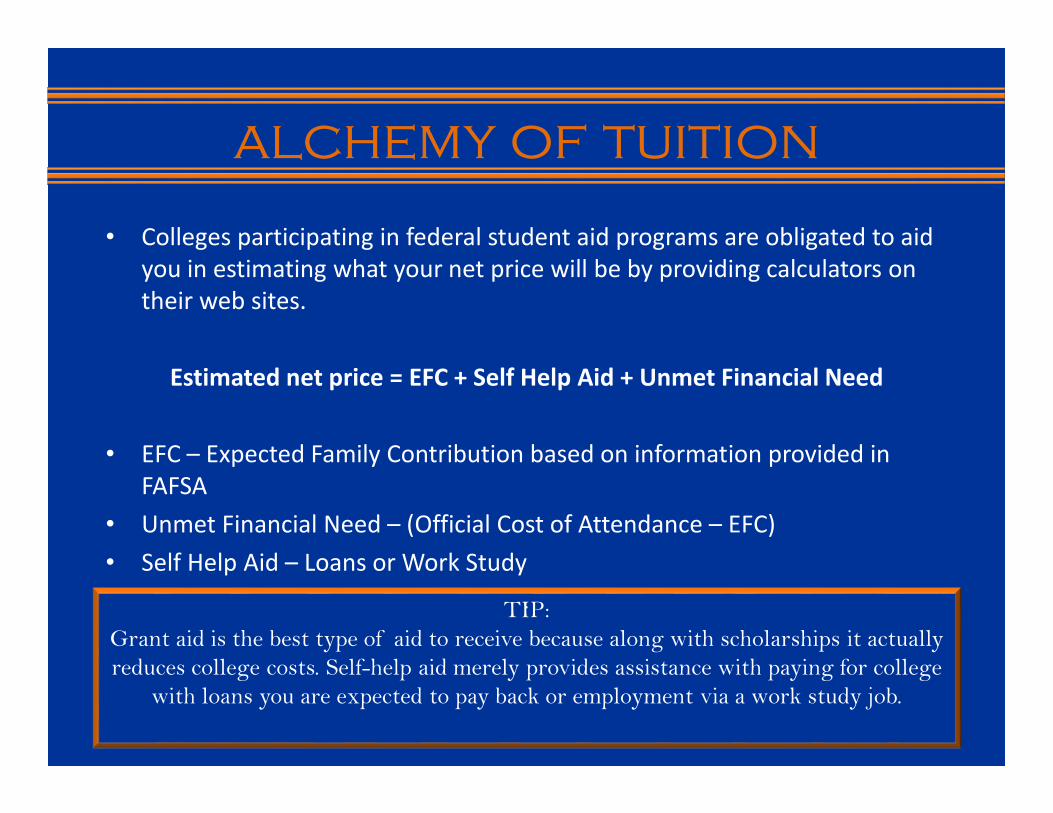

alchemy of tuition

• Colleges participating in federal student aid programs are obligated to aid

you in estimating what your net price will be by providing calculators on

their web sites.

Estimated net price = EFC + Self Help Aid + Unmet Financial Need

• EFC – Expected Family Contribution based on information provided in

FAFSA

• Unmet Financial Need – (Official Cost of Attendance – EFC)

• Self Help Aid – Loans or Work Study

.TIP:Grant aid is the best type of aid to receive because along with scholarships it actually

reduces college costs. Self-help aid merely provides assistance with paying for college

with loans you are expected to pay back or employment via a work study job.

options.

Financial AID Shopping

Sheet

• The financial aid shopping sheet is a helpful tool to aid

comparisons of the packages of schools you are considering.

• The sheet provides a standard format for colleges to

summarize their Cost of Attendance and Financial Aid offers

so you can you can easily compare the colleges you are

interested in.

• Currently over 2000 schools report on their aid packages with

the format.

Tip:

Adoption of the sheet is voluntary so it is possible some of the schools

you are interested in won’t provide a sheet with their financial aid offer.

The Consumer Financial Protection Bureau maintains a comparison tool so you can

easily compare schools you are interested in that have not adopted the sheet.

Free Application for federal

student aid

• File your FAFSA as close to October 1 during your senior year as possible.

Filing early maximizes your chances for receiving aid.

• If you are filing to attend a state school in your state of residence make

sure to list it first in your FAFSA. In many states this is a requirement to be

considered for state aid.

• Both students and parents will need to establish an FSA, Federal Student

Aid, ID prior to filing. The FSA ID is used to sign government financial aid

documents electronically.

• List the other schools alphabetically so it does not appear you have a

preference for one

Tip:

Use the IRS Data Retrieval Tool to automate the process of

including the required financial information in your FAFSA filing.

It is accessible for the prior tax year starting the first Sunday in February.

Student aid report

• Provides a summary of your eligibility for federal student aid

and provides a record of the answers in your FAFSA filing.

• Expected Family Contribution (EFC) is the primary factor in

determining how much aid you will be offered.

• It is calculated using the details provided regarding assets and

income in your FAFSA application.

• Represents the minimal amount you can expect to pay to

attend college

• Colleges use this figure to determine your eligibility for aid.

TIP:

The lower the EFC the more grant aid you will be eligible for. If you have a

high EFC expect most of the offered package to be loan aid.

Maximizing Aid Eligibility

• To maximize the quantity and quality of aid you receive

minimize your EFC

• Two options to lower EFC

– Reduce income in years when you are seeking aid

– Increase your allowance of protected assets.

• The less assets a student has in their name the better their

prospects for aid

• Check out this FinAid calculator to evaluate EFC reduction

strategies

TIP

To reduce income included in FAFSA make larger contributions to retirement

funds

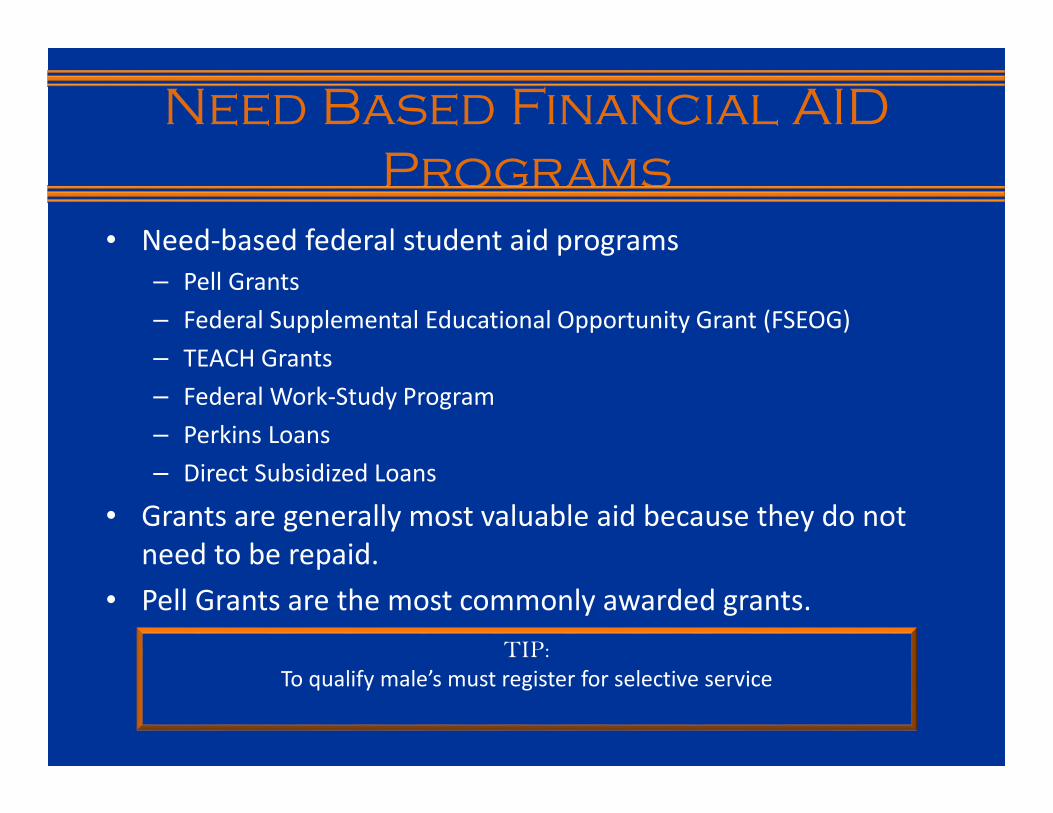

Need Based Financial AID

Programs

• Need-based federal student aid programs

– Pell Grants

– Federal Supplemental Educational Opportunity Grant (FSEOG)

– TEACH Grants

– Federal Work-Study Program

– Perkins Loans

– Direct Subsidized Loans

• Grants are generally most valuable aid because they do not

need to be repaid.

• Pell Grants are the most commonly awarded grants.

TIP:

To qualify male’s must register for selective service

Loans for students

• Federal Student Loan Programs

– Perkins Loans

– Direct Subsidized Loans

– Unsubsidized Loans

• Private Loans

*State Loans are considered private because they are not sponsored by

federal government

• Institutional Loan Funds

TIP:

Generally, students should leverage federal loans first because federal

student loans are the safest type of loan to take for financing an education.

They tend to have the lowest interest rate, are readily available, and have

better repayment terms than other loan types.

Loans for Parents

• PLUS loans are federal loans parents of dependent

undergraduate students can use to help pay for education

expenses not covered by financial aid.

• The maximum loan amount that can be borrowed reflects the

difference between the student’s cost of attendance minus

any other financial aid received.

• To be considered a parent for purposes of the PLUS program

the student must be the biological or legally adopted child of

the parent

TIP:

It is generally best to exhaust loans available to the student first and assist

them with payment if needed. Federal student loans have lower interest

rates and fees than PLUS loans.

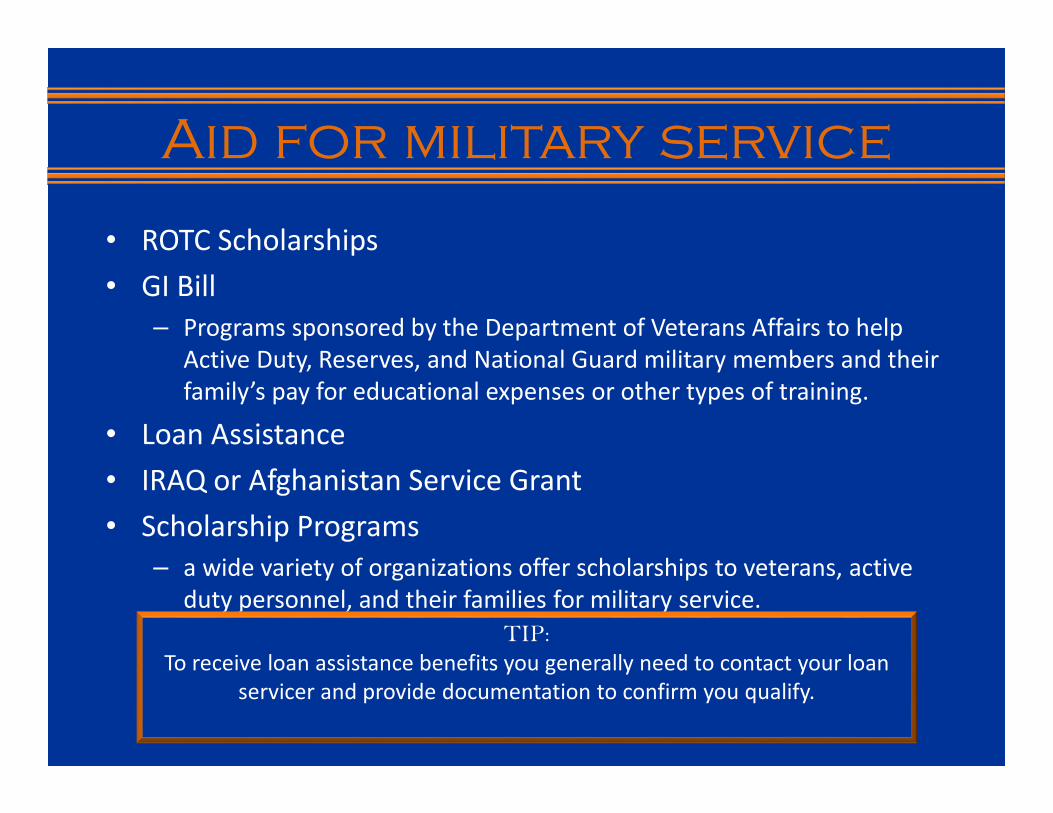

Aid for military service

• ROTC Scholarships

• GI Bill

– Programs sponsored by the Department of Veterans Affairs to help

Active Duty, Reserves, and National Guard military members and their

family’s pay for educational expenses or other types of training.

• Loan Assistance

• IRAQ or Afghanistan Service Grant

• Scholarship Programs

– a wide variety of organizations offer scholarships to veterans, active

duty personnel, and their families for military service.

TIP:

To receive loan assistance benefits you generally need to contact your loan

servicer and provide documentation to confirm you qualify.

Other Ways to Fund

educational expenses

• Work Study Employment

– Offered in work related to course of study to those who demonstrate financial need on

FAFSA.

• Working Part Time

– Generally better paying than work study opportunities

• Tuition Waivers

– Resident Assistant

– Exchange programs for out of state students

– Other State Programs

– Varies by university ask for a list of programs offered

TIP:

Scholarships from organizations outside of the University you are attending

reduce the aid you are awarded. Because colleges are required to reduce

your financial need. Colleges that reduce gift aid only after loan aid has been

subtracted are preferable to ones that reduce them equally.

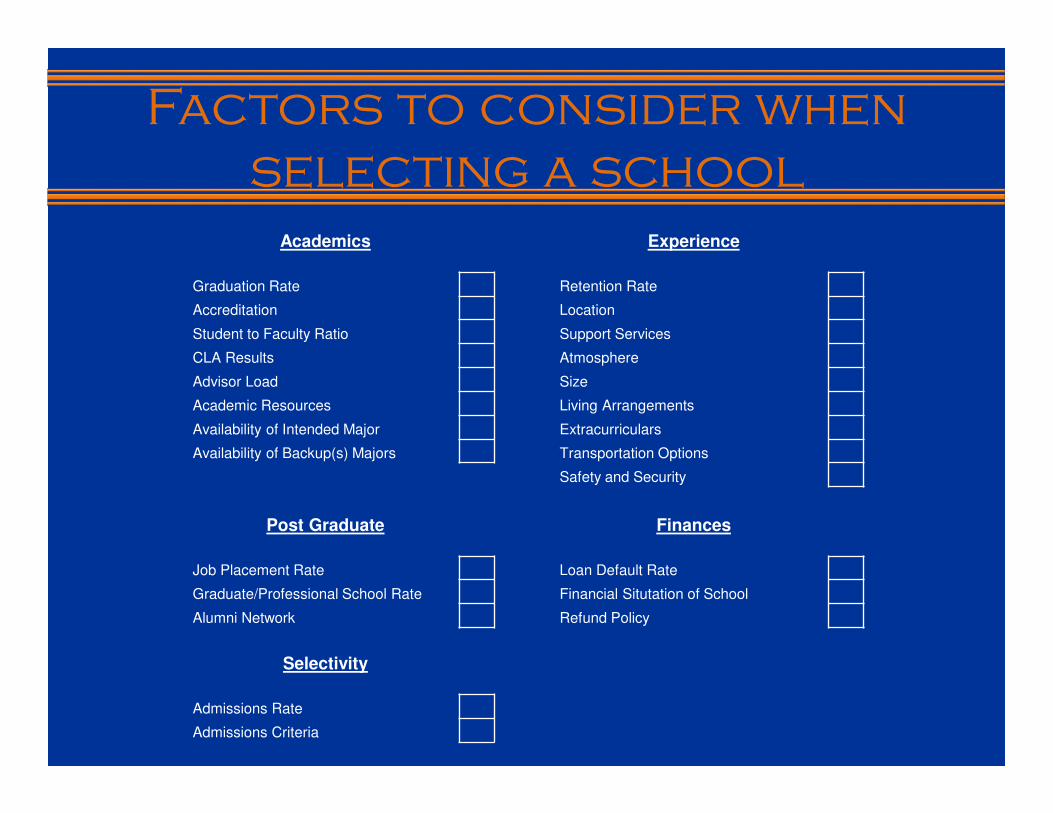

Factors to consider when

selecting a school

Academics Experience

Graduation Rate Retention Rate

Accreditation Location

Student to Faculty Ratio Support Services

CLA Results Atmosphere

Advisor Load Size

Academic Resources Living Arrangements

Availability of Intended Major Extracurriculars

Availability of Backup(s) Majors Transportation Options

Safety and Security

Post Graduate Finances

Job Placement Rate Loan Default Rate

Graduate/Professional School Rate Financial Situtation of School

Alumni Network Refund Policy

Selectivity

Admissions Rate

Admissions Criteria

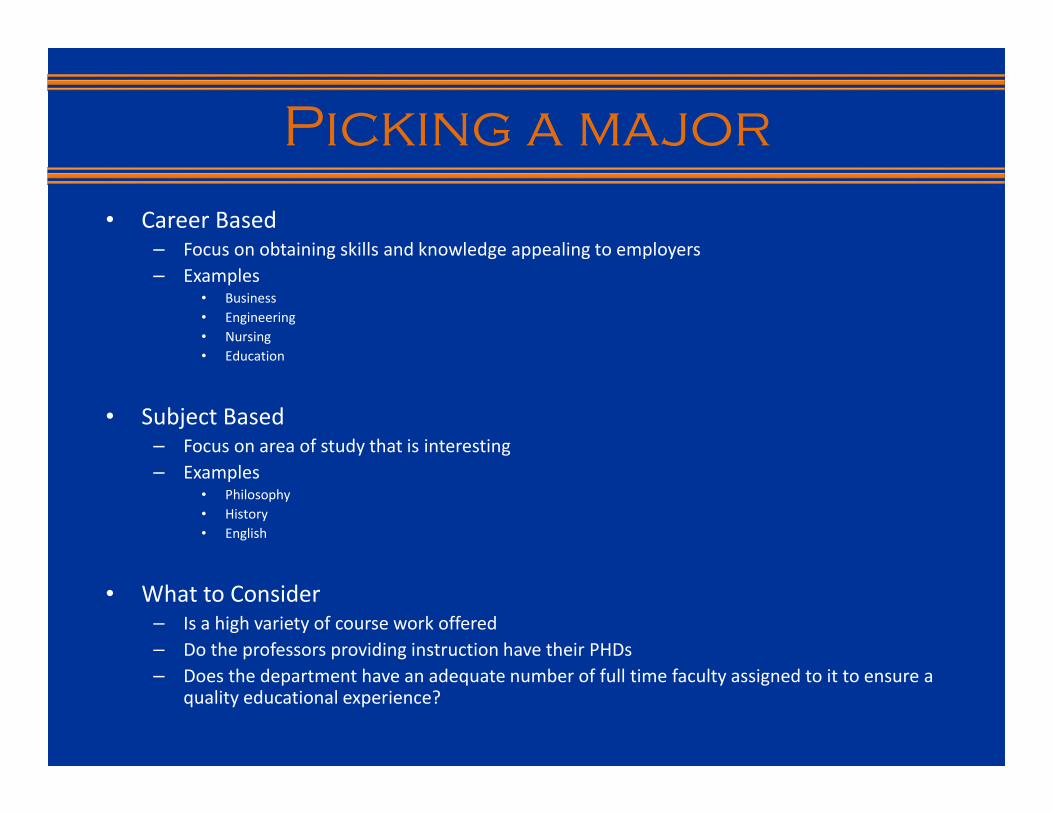

Picking a major

• Career Based

– Focus on obtaining skills and knowledge appealing to employers

– Examples • Business

• Engineering

• Nursing

• Education

• Subject Based

– Focus on area of study that is interesting

– Examples• Philosophy

• History

• English

• What to Consider

– Is a high variety of course work offered

– Do the professors providing instruction have their PHDs

– Does the department have an adequate number of full time faculty assigned to it to ensure a quality educational experience?

College prep checklist

Pre Application

Set Up FSA ID (Student)

Implement EFC Reduction Strategies

Application

Obtain FAFSA Deadline for State School

File FAFSA

File CSS Profile (if required)

Review Student Aid Report

Release SAR to schools not included in FAFSA filing

Selecting a School College One College Two College Three

Obtain Copy of Financial Aid Shopping Sheet

Research State Aid Programs

Research State Loan Programs

Research Availability of Institutional Loan Funds

Compare Costs Between Schools

Identify Differences in Your Cost of Attendance Versus Average Student

Research Economic Value of Major(s)

Estimate Your ROI

Post Decision

Register for Selective Service (Males)

Complete Entrance Counseling for Loans

Sign Promissory Note

To modify the checklist copy it from Google Sheets here.

Get This Book NowGet This Book NowGet This Book NowGet This Book Now

Remember:

College is about expanding your options while taking on debt narrows them. Every

dollar you have to take on in debt to finance your education narrows your choices

after school and should not be taken lightly.

For notices of book revisions and recommendations along with article updates and exclusive

subscriber only content

About the Author

As a thank you for subscribing you’ll receive a copy of the over 8000 word report

The Snowball Effect: How to Eliminate Your Debts While Maintaining Your Lifestyle.

sign up for his newsletter

Visit the Author at DebtMD.com

Steve Miller

Steve is a CFA® Charterholder and founder of DebtMD.com. A site devoted

to helping people discern insights into their finances. The CFA designation is

globally recognized and attests to a charterholder’s success in a rigorous and

comprehensive study program in the field of investment management and

research analysis.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

On Twitter @DebtMD