automotive retail executive-lender-summitd · ©2015 dealertrack, inc. 6 us distribution of...

TRANSCRIPT

1Copyright © 2015 Dealertrack, Inc. All rights reserved.

Raj Sundaram

Co-President | Dealertrack Technologies

Automotive Retail Trends

2Copyright © 2015 Dealertrack, Inc. All rights reserved.

Key Trends Impacting Auto RetailersShopping Process

� Shopping Process Internet and mobility has transformed shopping.� Shoppers demand transparency, speed, no hassle.� “Pride of ownership” replaced by ease/utility/experience.

Macro Factors� Macro-factors predict strong demand, most retailers expect more opportunity in used cars and limited growth in new vehicle

sales.� Credit availability strong across all tiers, but interest rate increases and delinquencies may dampen growth rates.� Pricing pressure will increase as used supply increases and OEM capacity comes online.

Regulations� Franchise laws will continue to be the norm.� Lending regulation (CFPB) and compliance requirements will increase, pressuring F&I gross.

Dealership Structure� Continued consolidation into National and Regional super groups. � Increasing trend to centralize operations and drive scale.

Connected Car� Internet connectivity to console will usher game changing applications and opportunities to engage consumer post sale.

3©2015 Dealertrack, Inc.

U.S. Light Vehicle Sales and Forecast

Source: Deutsche Bank, Wards Inc.

17.3 17.116.8 16.6

16.9 16.916.5

16.1

13.2

10.4

11.6

12.7

14.4

15.5

16.417

17.5

10

11

12

13

14

15

16

17

18

19

20

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E 2016E

12 Month Moving Average

4Copyright © 2015 Dealertrack, Inc. All rights reserved.

Dealer Optimism Index vs. Vehicle SalesPragmatism settles in… but optimism holds.

5©2015 Dealertrack, Inc.

New cars become used cars…

Source: ALG Used Supply study, Q1 2015

6©2015 Dealertrack, Inc.

US Distribution of Vehicles in Operation

46% of used cars are 11 years old, or older.

7©2015 Dealertrack, Inc.

Franchise Dealer Count Begins to Rebound

22.8 22.7 22.3 21.7 21.520.0

17.5 17.9

1993 1996 1999 2002 2005 2008 2011 2014

Franchised Dealer Count(in thousands)

Source: NADA

8©2015 Dealertrack, Inc.

In 2015-16, leading dealers and dealer groups will…

■ Embrace digital more fully – online and in-store.

■ Seize the continuing opportunity in used cars.

■ Redefine the service experience to drive retention.

Opportunities Remain Plentiful

9©2015 Dealertrack, Inc.

Industry RecapTransformAuto Retail©2015 Dealertrack, Inc.

Leveraging Technology to…

10Copyright © 2015 Dealertrack, Inc. All rights reserved.

Factors and Changes Implications

• Internet and mobility has transformed shopping

• Shoppers demand transparency, speed, no hassle

• “Pride of ownership” replaced by ease and utility

• Industry will rapidly shift marketing spend to digital

• Industry will Improve online to in-store experience via tech.

• Dealers will prioritize self-branding and experience

*2014 Deloitte Automotive Consumer Study

9 10outof

The Shopping Process is Changing

Consumers want an extremely efficient purchase process.*

11Copyright © 2015 Dealertrack, Inc. All rights reserved.

The Funnel is now a Shot Glass2008 2013

6 Months29.9 Million People

16.9 Million Buyers 15.6 Million Buyers*

Media UsedTVRadioMagazinesNewspaperLocal MagazinesOnline

Dreaming�

Thinking�

Researching�

Deciding

Media UsedSocial Media

OnlineMobileVideo

3 Months20.9 Million People

2013 Borrell Inc. Report

12Copyright © 2015 Dealertrack, Inc. All rights reserved.

It’s Just the Start: 80M Gen Y Consumers Will Soon Dominate the Buying Landscape

Millennials/Gen YBy 2015, their annual spending is expected to be $2.45 trillion and by 2018, they will eclipse boomers in spending power at $3.39 trillion. [Oracle]

(2014 Deloitte Automotive Consumer Study)

13Copyright © 2015 Dealertrack, Inc. All rights reserved.

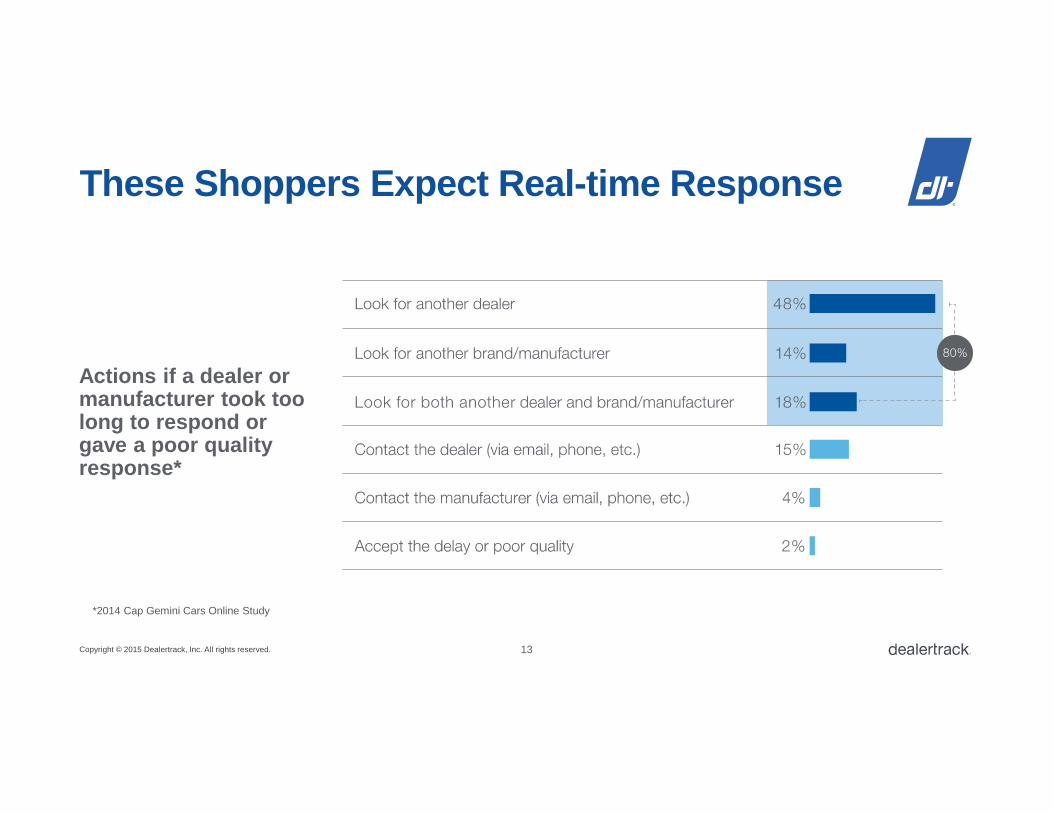

These Shoppers Expect Real-time Response

Actions if a dealer ormanufacturer took too long to respond or gave a poor quality response*

*2014 Cap Gemini Cars Online Study

14Copyright © 2015 Dealertrack, Inc. All rights reserved.

Interest in Buying Cars Online is Increasing

*2014 Cap Gemini Cars Online Study

Better price and speed cited as the top two perceived benefits*

=2013 =2014

15©2015 Dealertrack, Inc.

Interest in Buying Cars Online is Increasing

*2014 Cap Gemini Cars Online Study

54% consumers state that getting an actual price and payment is their largest unmet need online

- Edmunds.com

16©2015 Dealertrack, Inc.

Other industries are raising customers’ expectations regarding experience

Address all senses

Consistent appearance and

customer service

Everywhere [i.e. convenience]

Example: Starbucks

Virtual experience

Simplified POS[i.e. on demand)

Where I want, When I wantExample: Uber

Premiumsurroundings

Exclusive service

Pampering convenience

Example: Four Seasons Hotels

Personalized experiences

Deep product knowledge

Exclusive locations

Interconnected personal profile

Example: Apple Store

Source: Roland Berger

17©2015 Dealertrack, Inc. ©2015 Dealertrack, Inc.

Portals are evolving.Focusing on evolving consumer demands.

Dealer groups are investing in new areas.Progressive dealers investing in reinventing their business models.

OEMs are engaged around customer experience.Focusing on evolving consumer demands.

Startups trying to simplify shopping.Venture capital investors investing $100m+ in startups

What we’re seeing…

18©2015 Dealertrack, Inc.

MakeMyDeal

Cox Automotive’s online negotiation start-up. Dealer website plug-in displays monthly payments based on credit and trade info, centralized “Dealbook” negotiation portal lets consumers work deals from multiple dealers.

19©2015 Dealertrack, Inc.

TrueCar

Over half TrueCar’s traffic is from mobile devices, f ocusing on development on mobile solutions. Starting to beta elements of TrueTrade, guaranteed trade-in price so lution, released “Sell My Car” app in February.

20©2015 Dealertrack, Inc.

Concierge new-car buying service. Configure a vehicl e and find matches at participating dealers. Roadster rep negotiates price/trade, handles financing/paperwork , and delivers car to buyer

“Skip the dealership”

Roadster

$1.8m+ Funding

21©2015 Dealertrack, Inc.

Flat fee concierge new-car buying service, just choo se a vehicle Cartelligent will source the car and negotia te the deal.

“Never set foot in a dealership”

Cartelligent

$ukn Funding

22©2015 Dealertrack, Inc.

Peer-to-peer online used-car marketplace. Performs pre-sale inspection/merchandising, delivers car to buyer. Purchases car from seller if buyer not found within 30 days, and offers buyers 10-day money back guarantee.

Beepi

$79m Funding

23©2015 Dealertrack, Inc.

Online used-car retailer, highlighting both vehicle features and any imperfections to build trust. 7-day test drive, vehicle pickup and/or delivery. No traditional dealerships, just hubs to distribute vehicles

“a car without the car salesman”

Carvana by DriveTime

24©2015 Dealertrack, Inc.

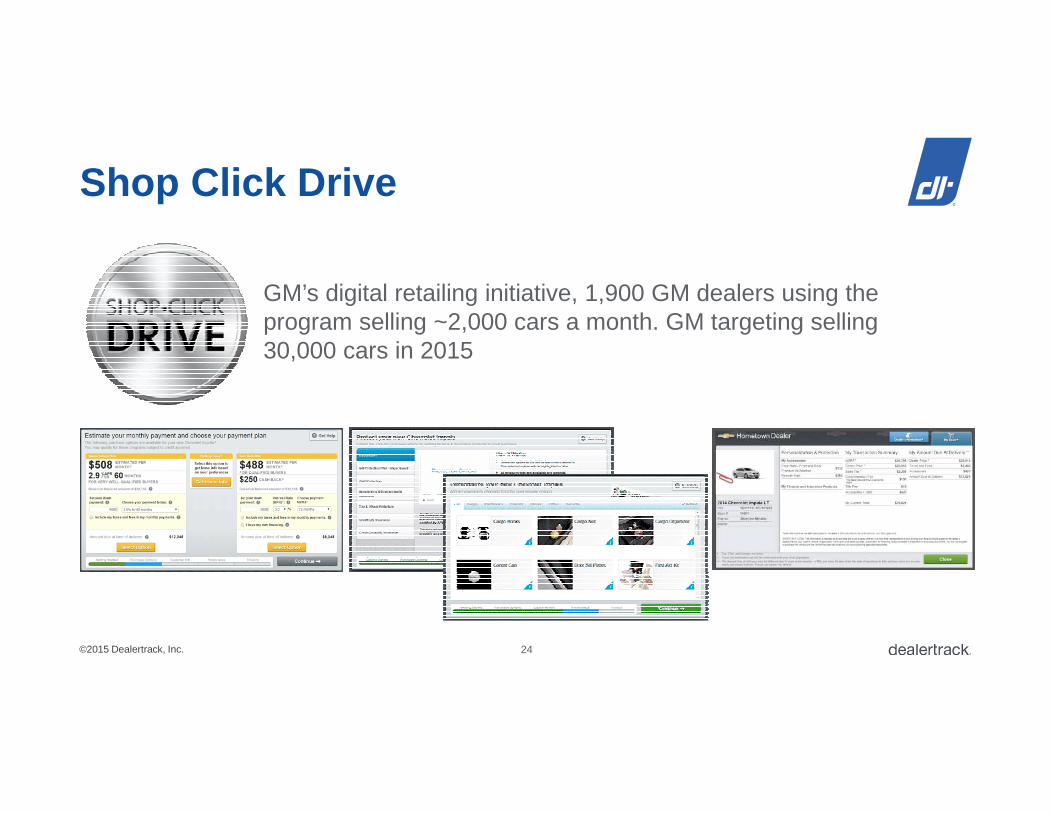

Shop Click Drive

GM’s digital retailing initiative, 1,900 GM dealers using the program selling ~2,000 cars a month. GM targeting selling 30,000 cars in 2015

Copyright © 2015 Dealertrack, Inc. All rights reserved.

Transforming Automotive Retail…

26Copyright © 2015 Dealertrack, Inc. All rights reserved.

Credit App.

Submit Lead/

Appointment

Auto Retail is Complex…

Cars that need to sell

Sales/InventoryManager

Narrowing Options

Additional Research

Website Visits

Contextual Ads

Marketing Manager

Shopper

Salesperson

F&IManager

Salesperson

Service Appointments

Create Campaign

Retargeting

DocumentExecution

Registration & Titling

Pencil deal, Negotiations, Credit Bureau

TestDrive

AppraiseTrade-in

Presentation and selection

Menu

Merchandise Inventory

Price and Prep Trade in

for Sale

$

Credit Decision

VehicleDelivery

Exchange Auction/

Wholesale

Service Marketing

Follow up, “Road to Sale”

process

Transaction in DMS/

Doc. Mgmt.

Manage Service

27Copyright © 2015 Dealertrack, Inc. All rights reserved.

From the Consumer Perception of Today…Linear in nature, not enjoyable, lack of trust, dis jointed, time intensive.

ShopAttract Structure Transact Manage

HookPitch Negotiate Close Neglect

28Copyright © 2015 Dealertrack, Inc. All rights reserved.

Attract• Audiences• Display• Retargeting• Paid Search• Organic Search• Merchandising

Shop• Research• Locate Vehicles• ‘Real Time’ Pricing

& Availability• Price & Vehicle

Compare

Structure• Trade Offer• Payoff Quote• Financing Options• Structure Deal• Credit

Transact• Aftermarket/Menu• Contract• Funding• Registration & Title • Insurance• Delivery / Pick-up• Service

ShopAttract Structure Transact Manage

Manage• Service• Loyalty• CRM

Evolving The Customer Journey

29©2015 Dealertrack, Inc.

Digital Retailing

1. Takes time out of the process of selling a car.

2. Dealer controlled.3. Meets customer needs.4. Delivers higher sales and

gross profits.

FinanceDriverPaymentDriver

TradeDriverMenuDriver

30©2015 Dealertrack, Inc.

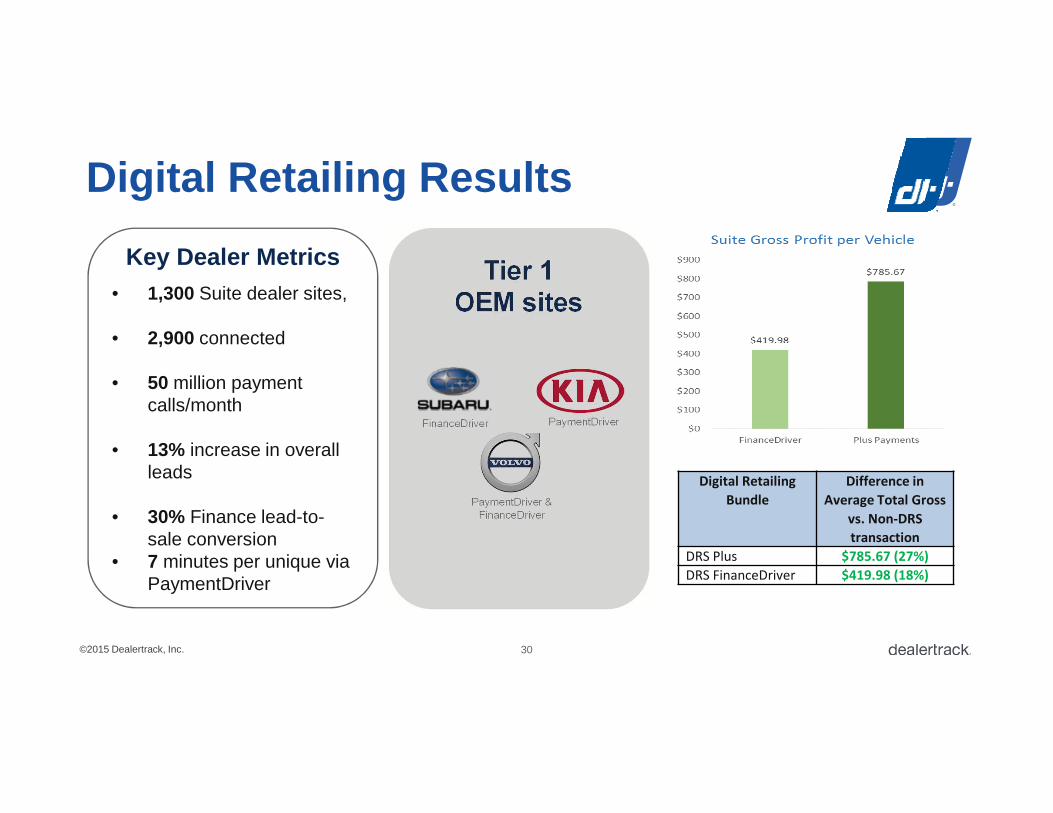

Digital Retailing: Results

Key Dealer Metrics• 1,300 Suite dealer sites,

• 2,900 connected

• 50 million payment calls/month

• 13% increase in overall leads

• 30% Finance lead-to-sale conversion

• 7 minutes per unique via PaymentDriver

Tier 1 OEM sites

FinanceDriver PaymentDriver

PaymentDriver &FinanceDriver

Digital Retailing Results

Digital Retailing

Bundle

Difference in

Average Total Gross

vs. Non-DRS

transaction

DRS Plus $785.67 (27%)

DRS FinanceDriver $419.98 (18%)

Copyright © 2015 Dealertrack, Inc. All rights reserved.

Thank you.