automotive news europe - nxtbook media

TRANSCRIPT

2

AUTOMOTIVE NEWS EUROPE COVER STORY

www.autonewseurope.com JULY 2016

Knowledge built for market leadership

© 2016 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

From knowledge comes informed decisions. That’s why business leaders are looking for insight on today’s complex issues. And why we provide perspective on issues such as corporate governance, operations, regulation, talent, operations, cyber security, strategy and new platforms for growth. To gain additional insight on these and other issues of importance to your automotive business, visit www.pwc.com/auto

3

AUTOMOTIVE NEWS EUROPE

www.autonewseurope.comMARCH 2017

ISSUE HIGHLIGHTS

The European Commission is set to reshape the landscape of the global

auto industry later this year when it agrees on even more stringent carbon emission targets for the next decade. The new goals could mark the beginning of the end for vehicles powered by tra-ditional combustion engines in the EU, the world’s largest economic bloc. Our cover story assess the potential effects (Pages 6-10).

PSA Group CEO Carlos Tavares is con-cerned that the mayors of the world’s biggest cities -- especially those in Eu-rope -- will have a powerful say in which powertrains will rule the roads. Tavares supports making the air in cities cleaner, he just has a different idea on how to achieve the goal (Page 46).

Tavares is a very busy man. Having suc-cessfully turned around PSA, at press time he was aggressively pursuing a game-changing tie-up with General Mo-tors’ European brands, Opel and Vaux-hall. PSA and GM have been working together successfully for years, he said, pointing to the new Opel/Vauxhall Crossland X, which will spawn models for Peugeot and Citroen, as a prime ex-ample of what the companies could do if they merge. We look at the key events in Opel’s recent past that left it in posi-tion to part ways with GM after nearly a century together (Pages 16-17).

Clearing the air

Peugeot will highlight its autonomous driving technology at the Geneva auto show with a self-driving, shooting brake concept car called the Instinct. For a look at other key Geneva debuts, see our show preview on Pages 20-21.

SUVs and crossovers benefited most from Europe’s sales surge last year.

Combined sales of models such as the Renault Captur, Nissan Qashqai, BMW X1 and Jaguar F-Pace increased 22 percent to nearly 3.8 million units. That rise easily outpaced the overall mar-ket’s 6.5 percent increase to 15 million.

Our exclusive annual by-segment anal-ysis of the European market based on data from JATO Dynamics shows that SUVs and crossovers accounted for a quarter of the region’s total vehicle sales in 2015, up from 21 percent in 2015 and 20 percent in 2014. To find out which other segments are on the rise, and which ones are declining, see Pages 39-42. ANE

Sizzling SUVs

Our Latest Launches section showcases two brands -- Mini and Nissan -- that are counting on their newest models to shake things up (Pages 24 & 26).

Enjoy the issue!

Luca Ciferri,

Associate Publisher and Editor

Daimler’s new r&d boss, Ola Kaellenius, believes the auto industry is at a ma-jor crossroads as megatrends such as connectivity, autonomous drive, shared services and electrification combine to shape the future market. He shared his views on those key topics (Page 12).

Since creating the iconic looks of the first Audi TT, Peter Schreyer has dreamed of designing a true sports car. He joined Kia in 2006 and six years later he was promoted to Hyundai Motor Group vice president and chief design officer. Al-though this put him in control of styling at all the company’s brands, Schreyer’s sports car remained in a drawer. Then an opportunity arose to put that passion into a completely different project (Page 14).

Over the past two years, Renault has overtaken Ford and Opel to become the second-largest brand in Europe by unit sales, riding the momentum from a wave of stylish new models, especially in the hot crossover segment. But analysts say that success will be harder to maintain in 2017 (Page 18).

Hybrid and plug-in hybrid sales grew an impressive 30 percent to just over 400,000 in Europe last year, but the real impact in the midterm will be made by mild hybrids, analysts predict. By 2025 mild hybrids will capture 18 percent of the European market (Pages 22-23).

More on the WebPlease visit Automotive News Europe’s Geneva auto show Web page for the latest news and photos at:

autonewseurope.com/geneva

4

AUTOMOTIVE NEWS EUROPE

www.autonewseurope.com MARCH 2017

INSIDE THIS ISSUE

KEITH CRAINPublishing Director

KC CRAINGroup Publisher

JASON STEINPublisher

LUCA CIFERRIAssociate Publisher & Editor+39 348 274 00 [email protected]

DAVE VERSICALDirector of Group Editorial Operations+1 313 446 [email protected]

DOUGLAS A. BOLDUCManaging Editor+49 (0) 171 424 6373dbolduc@ autonews.com

PAUL MCVEIGHManaging Editor+49 (0) 176 7835 3951pmcveigh@ autonews.com

James Clark (UK), Nick Gibbs (UK), Christiaan Hetzner (Germany), David Jolley (Germany), Mary Raetz (U.S.), Heather Rowe (U.S.), Peter Sigal (France)Correspondents

ADVERTISINGEUROPE

THOMAS HERINGERCommercial Director Europe+ 49 (0) 8153 907 [email protected]

GEORGIA CHAPMANDirector of European Marketing and Events+49 (0) 89 5795 [email protected]

USA

KAREN RENTSCHLERManaging Director, Sales and Events+1 313 446 [email protected]

KOREA

JUNG-WON SUHSinsegi Media Inc.+82 2 785 [email protected]

CIRCULATIONJAMIE TUNISON Marketing Coordinator +1 313 446 1642 [email protected]

SUBSCRIPTION SERVICESInternational number +1 313-446-0450 Toll free from the US +1 877-812-1584 [email protected]

Published byCrain Communications Inc1155 Gratiot Ave. ❚ Detroit MI 48207. USA

All contents Copyright 2017. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic or mechanical, photocopying, recording or otherwise without the permission of the publisher.All rights reserved.

www.autonewseurope.com

INSIDE THE JANUARY & 1-MONTH NUMBERS

29 European sales by country and brandNetherland, Latvia, Poland were big monthly winners

30 European top 50 Ford Fiesta, VW Tiguan make solid gains

31 Top 10 sellers in key markets New feature shows leaders in 27 countries

33 European sales by modelBMW X1, Fiat Tipo, Hyundai SantaFe help lift their brands

39 Segment stars of 2016SUV sales surge to a landmark high

26 Goal-oriented Nissan plots Micra’s return to top 10 in subcompact segment

SUPPLIERS27 Tailored solution

Tata Steel looks to expand high-margin product to volume brands

28 CutawaySee who has parts in the new Land Rover Discovery

FINAL WORD46 Power players

Why city mayors may dictate which cars will rule the roads

43 European production by brandAston Martin, Maserati, DS make double-digit gains

44 Turkey salesJanuary sales rise 9%; Renault models benefit

45 Russia salesJanuary sales fall 5%; Kia Rio takes early lead

CONTENTS3 Issue highlights

COVER STORY6 Brave new world

Tougher EU emissions rules put the traditional engine’s future in doubt

Q&A12 Trend tracker

Daimler r&d boss outlines Mercedes’ self-driving, EV, connectivity plans

14 Design drivenHow Peter Schreyer channeled his passion to make a sports car into Kia’s new sedan

AUTOMAKERS16 Finding the right fit

How Opel/Vauxhall and PSA are already successfully cooperating

18 Holding its ground Renault faces tough task staying Europe’s No. 2 brand as product push slows

20 Showtime in Geneva DS 7 Crossback, Range Rover Velar, Seat Ibiza among crucial unveilings

22 Gaining ground Full-, plug-in hybrid sales rise fast but new tech could shake up sector

LATEST LAUNCHES24 Size matters

Mini maxes out with Countryman premium compact SUV

COVER DESIGN: Joerg Hunner/iStock

Hyundai Motor Chief Design Officer Peter Schreyer

14

@autonewseurope

45

AUTOMOTIVE NEWS EUROPE DATA

www.autonewseurope.com

MARCH 2017

AvtoVAZ ................... 16,334 15,577 5% 16,334 15,577 5%

Datsun ....................... 1,107 1,001 11% 1,107 1,001 11%

Infiniti ....................... 379 298 27% 379 298 27%

Nissan ........................ 4,230 4,494 –6% 4,230 4,494 –6%

Renault ..................... 5,208 5,014 4% 5,208 5,014 4%

RENAULT-NISSAN ...... 27,258 26,384 3% 27,258 26,384 3%

KIA ............................. 10,306 9,049 14% 10,306 9,049 14%

Audi .......................... 935 905 3% 935 905 3%

Skoda ........................ 3,571 3,556 0% 3,571 3,556 0%

Volkswagen .............. 4,581 4,455 3% 4,581 4,455 3%

Volkswagen vans ..... 305 323 –6% 305 323 –6%

VW GROUP ................ 9,392 9,239 2% 9,392 9,239 2%

Genesis ...................... 6 0 – 6 0 –

Hyundai .................... 6,694 8,010 –16% 6,694 8,010 –16%

HYUNDAI GROUP ...... 6,700 8,010 –16% 6,700 8,010 –16%

Lexus ......................... 1,000 1,085 –8% 1,000 1,085 –8%

Toyota ....................... 3,831 6,064 –37% 3,831 6,064 –37%

TOYOTA GROUP ........ 4,831 7,149 –32% 4,831 7,149 –32%

Mercedes-Benz ......... 2,471 3,206 –23% 2,471 3,206 –23%

Mercedes-Benz vans 246 260 –5% 246 260 –5%

Smart ......................... 20 12 67% 20 12 67%

DAIMLER .................... 2,737 3,478 –21% 2,737 3,478 –21%

GAZ LCV ..................... 2,307 1,851 25% 2,307 1,851 25%

FORD .......................... 2,253 2,242 1% 2,253 2,242 1%

BMW ......................... 1,758 1,919 –8% 1,758 1,919 –8%

Mini ........................... 70 76 –8% 70 76 –8%

BMW GROUP ............. 1,828 1,995 –8% 1,828 1,995 –8%

Cadillac ..................... 78 48 63% 78 48 63%

Chevrolet .................. 1,734 1,201 44% 1,734 1,201 44%

GM ............................. 1,812 1,249 45% 1,812 1,249 45%

UAZ ............................ 1,735 1,930 –10% 1,735 1,930 –10%

MAZDA ...................... 1,513 1,411 7% 1,513 1,411 7%

MITSUBISHI ................ 1,076 1,323 –19% 1,076 1,323 –19%

LIFAN .......................... 929 1,244 –25% 929 1,244 –25%

Jaguar ....................... 134 34 294% 134 34 294%

Land Rover ............... 401 500 –20% 401 500 –20%

JAGUAR LAND ROVER 535 534 0% 535 534 0%

Citroen ...................... 265 220 21% 265 220 21%

Peugeot .................... 227 196 16% 227 196 16%

PSA GROUP ................ 492 416 18% 492 416 18%

RAVON ....................... 445 0 – 445 0 –

SUBARU ..................... 303 422 –28% 303 422 –28%

SUZUKI ....................... 265 571 –54% 265 571 –54%

Alfa Romeo .............. 0 2 – 0 2 –

Chrysler ..................... 0 3 – 0 3 –

Fiat ............................ 122 164 –26% 122 164 –26%

Jeep ........................... 92 76 21% 92 76 21%

FIAT CHRYSLER .......... 214 245 –13% 214 245 –13%

CHERY ........................ 205 280 –27% 205 280 –27%

PORSCHE .................... 151 311 –51% 151 311 –51%

Acura ......................... 0 47 – 0 47 –

Honda ....................... 123 190 –35% 123 190 –35%

HONDA GROUP ......... 123 237 –48% 123 237 –48%

GEELY ......................... 120 555 –78% 120 555 –78%

CHANGAN .................. 93 34 174% 93 34 174%

VOLVO ....................... 72 16 350% 72 16 350%

DFM ............................ 54 91 –41% 54 91 –41%

ISUZU ......................... 41 57 –28% 41 57 –28%

IVECO ......................... 35 47 –26% 35 47 –26%

FAW ........................... 33 35 –6% 33 35 –6%

ZOTYE ........................ 28 0 – 28 0 –

BRILLIANCE ................ 13 114 –89% 13 114 –89%

BAW ........................... 10 13 –23% 10 13 –23%

HYUNDAI LCV ............ 4 0 – 4 0 –

FOTON ....................... 3 0 – 3 0 –

SSANGYONG ............. 0 153 – 0 153 –

HAIMA ....................... 0 40 – 0 40 –

DAEWOO ................... 0 1,269 – 0 1,269 –

Total ........................... 77,916 81,994 –5% 77,916 81,994 –5%

Russia vehicle sales by manufacturer – January

Jan. Jan. Percent 1 mos. 1 mos. Percent

2017 2016 change 2017 2016 change

1 Kia Rio

5,693 2 Lada Granta

4,624 3 Lada Vesta

4,088 4 Hyundai Solaris

2,886 5 Hyundai Creta

2,565 6 VW Polo

2,550 7 Skoda Rapid

1,981 8 Renault Duster

1,848 9 Chevrolet Niva

1,67010 Lada 4x4

1,62711 Lada X-ray

1,57812 Kia Sportage

1,56513 Lada Largus

1,56214 Renault Kaptur

1,51915 Toyota Camry

1,32716 VW Tiguan

1,28817 Skoda Octavia

1,24818 Nissan X-Trail

1,20619 Toyota RAV4

1,15020 Lada Priora

1,14321 Mazda CX-5

1,11522 Lada Kalina

1,02523 Datsun On-Do

1,01424 Nissan Qashqai

1,01025 Mitsubishi Outlander

943

January 2017 Top 25 Sellers Ranking based on new car and LCV sales in Russia

Source: AEB Automobile Manufacturers Committee

1 Lada Granta 7,377

2 Hyundai Solaris 5,626

3 Kia Rio

3,553 4 Toyota RAV4

2,816 5 VW Polo

2,655 6 Kia Sportage

2,407 7 Renault Duster

2,379 8 Lada Largus

2,065 9 Lada Vesta

1,64310 Lada 4x4

1,60911 Skoda Rapid

1,56012 Renault Logan

1,48113 Lada Priora

1,38614 Skoda Octavia

1,36515 Kia Cee’d

1,19616 Chevrolet Niva

1,18217 Toyota Camry

1,14618 Lada Kalina

1,14019 Nissan Qashqai

1,07320 Renault Sandero

1,04321 Toyota Land Cruiser

1,01422 Mazda CX-5

97523 Daewoo Gentra

95724 UAZ Patriot

85625 Nissan Almera

854

January 2016 Top 25 Sellers Ranking based on new car and LCV sales in Russia

5

AUTOMOTIVE NEWS EUROPE COVER STORY

www.autonewseurope.com MARCH 2017

6

AUTOMOTIVE NEWS EUROPE COVER STORY

www.autonewseurope.com MARCH 2017

Why tougher EU emissions rules put the combustion engine’s future in doubt

CHRISTIAAN [email protected]

The European Commission is set to reshape the landscape of the global

auto industry later this year when it agrees on even more stringent carbon emission targets for the next decade that could mark the beginning of the end for traditional combustion-pow-ered vehicles in the world’s largest economic bloc.

Experts believe regulators, most likely in the third quarter, could dramatically slash the future amount of greenhouse gases produced by new passenger cars in a bid to reverse rising emissions from the road transport sector in time for the European Union to meet its 2030 target. Brussels has committed to a binding CO2 cut of at least 40 percent on 1990 levels as part of the first global pact to combat climate change signed in Paris. Automakers currently must reduce their CO2 emissions in Europe to 95 grams per kilometer by 2021.

Major powertrain trends such as down-sizing and turbocharging were the result of pressure from EU regulators in the past. It’s fair to say the next round of tar-gets, which could include limits for both 2025 and 2030, will have an even more

drastic effect on the automakers’ pow-ertrain strategies.

Major metropolitan areas such as Paris, Madrid, Athens and Oslo are already planning to ban diesels in the city cen-ters in the coming years to tackle smog problems. By the end of the next de-cade, European new-car sales of mod-els with full or partially electrified drive-trains are expected to surpass those of vehicles with traditional combustion engines (see graphic, Page 7).

Speaking on behalf of vehicle manu-facturers in his role as president of in-dustry association ACEA, Daimler CEO Dieter Zetsche sounded worried last month when the conversation turned to the further de-carbonization of road transport.

“We need to pull every lever at our dis-posal, including hybrids, fuel cell, gas and battery-electric vehicles,” he said during ACEA’s annual reception in Brus-sels last month.

Electric powerThe move toward electromobility comes at a time when manufacturers are al-ready pouring billions of euros into de-veloping autonomous and connected cars. Alternative drivetrains will require

investments of more than 40 billion euros by 2020 by the German auto in-dustry alone, according to the VDA, the country’s auto association, making the push to reducing carbon emissions the greatest challenge facing automakers.

While new business models can be created by selling mobility-on-demand packages, real-time parking information or robotized ride-hailing services, the po-tential to generate fresh revenue growth simply by offering cleaner, eco-friendly cars is largely non-existent. Customers are unwilling to pay extra solely to im-prove ambient air quality, despite the es-timated 100 million euros in incremental costs per each gram of CO2 reduction undertaken by carmakers such as the Volkswagen Group.

Currently, each manufacturer is subject to weight-based limits that require the fleet CO2 average to reach 95g/km by 2021 based on New European Driving Cycle (NEDC) guidelines.

By comparison the ceiling for 2015 was 130g/km, which the industry easily met with a level of 119.5g/km even though plug-in hybrids and battery-electric ve-hicles comprised only 1 percent of the overall new car fleet at the time. Under new regulations, this target could poten-

Under new regulations, automakers may have to slash CO2 emissions to as low as 68g/km by 2025. Such a move would put automakers under pressure to switch to powertrains that emit very few tailpipe pollutants.

Brave new world

Phot

o: iS

tock

phot

o

7

AUTOMOTIVE NEWS EUROPE COVER STORY

www.autonewseurope.comMARCH 2017

tially sink as low as 68g/km for 2025 – a reduction by half in the space of just a decade. That’s roughly the same amount of time between the initial development of a new car and the end of the model’s life cycle. Meeting such a limit would undoubtedly require a substantial pen-etration of electrified cars, tough even for a company such as Toyota with its fuel-efficient fleet of gasoline-electric hybrids. The VW brand, for example, estimates it would have to sell 1 million battery-electric vehicles in 2025 alone, compared with the tens of thousands it currently sells, to meet future emissions targets around the world.

During a speech in January, VW brand sales chief Juergen Stackmann told his German dealers at a gathering in Bonn that “global environmental standards are expected to be intensified drasti-cally” starting in the next decade.

Another challenge facing automakers in Europe is that they will need to comply with the so-called Real Driving Emissions (RDE) test procedure starting in Septem-ber (see box, Page 10). Originally intro-duced to address excess nitrogen oxide (NOx) emissions from diesels, now ex-perts believe the RDE test can also help with reducing CO2. Certified NEDC fuel consumption for plug-in hybrids for ex-ample is about 30 percent to 40 percent lower than in real life use.

As a consequence, German supplier Schaeffler estimates that half of the 111 million vehicles produced globally in 2025 will no longer be powered purely

by internal combustion engines as out-put of hybrids gains speed. Over the fol-lowing five years, the share of battery-electric vehicles produced is expected to double, reaching 30 percent in 2030 and matching the number of vehicles made with combustion engines by then.

Schaeffler ally Continental acknowl-edges that the two companies may be able to increase sales of their fuel-saving solutions, such as their 48-volt mild hy-brids, as automakers race to reach the new targets but Continental CEO Elmar Degenhart refutes speculation the com-panies will profit from this.

“We all are sitting in the same boat,” De-genhart told Automotive News Europe. “What’s not good for our customers can-not be good for us suppliers.”

Cost dilemmaThe problem is when it comes time to pass on the added costs from carbon emissions compliance, even aspirational brands struggle. Porsche said last year its affluent car buyers won’t open their

wallets wider to pay the extra 10,000 euros needed to build a plug-in hybrid version of the Panamera or Cayenne, forcing the company to swallow a chunk of the costs itself. Daimler r&d chief Ola Kaellenius, Zetsche’s likely successor as CEO, said the automaker had little choice but to offer the plug-in hybrid version of its flagship Mercedes-Benz S class at the same price as the equivalent version with a traditional powertrain. Customers pay for horsepower, not CO2 savings, he said, underlining that the added complexity is the carmaker’s problem. Industry analysts say one key reason for that is that the fuel-usage levels touted by automakers can only be achieved in the utopian world of labora-tory test benches.

“Given the urgency and ambition of the Paris [Agreement] commitments, legisla-tion should be designed in a way that in-centivizes manufacturers to optimize tech-nology to lower CO2 emissions in reality rather than adapting to the test cycles,” scientists wrote in a report sent to the Eu-ropean commission last November.

In its annual Mind the Gap study, Brus-sels-based advocacy group Transport & Environment refuted official EU statistics that showed a continued improvement in CO2 emissions from new cars. Analyzing third-party fuel consumption data, T&E argued that only Toyota would have met its 2015 target in real life. T&E concluded that roughly two-thirds of the improve-ment in CO2 emissions over 2008 levels existed only on paper because of testing-procedure loopholes, blasting the results as “no longer having any credibility” and estimating the hidden fuel costs to mo-torists at 549 euros a year.

New testsTo address this weakness, the EU is phasing in a new method to measure emissions to create “a strong incentive for the deployment of low-carbon mobil-

NOx goals Nitrogen oxide emissions limits for diesel vehicles

2014 80mg/km2009 180mg/km2005 250mg/km2000 500mg/km

Tougher targets Automakers may be required to nearly halve their CO2 fleet average in 2025 compared with 2015

2025 68 to 78g/km*2021 95g/km2015 130g/km

*EU Parliament proposal

25

Powertrain mix estimate all cars Europe 2015 to 2030 assuming lowest TCO to achieve expected CO2 targets, registration of new cars (%)

Overall shift to electrified vehicles by 2030 replacing diesel which is expected to have a small share of additional sales post 2030

www.alixpartners.com

Key model findings

• By 2030, alternative powertrains will significantly substitute conventional powertrains.

• Diesel will lose high share to alternative powertrains from 2020 –not cheap enough to compete with gasoline and not clean enough to compete with APVs.

• Hybrids will gain significant share from 2020, PHEVs and EVs from 2025 as battery cell costs fall and charging infrastructure rolls out.

Source: AlixPartnersNote: * Based on 2016 testing procedure

120 95 78 60Average CO2 [g/km]*

20%

18%

28%

9%

25%

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

-202520202015

Gasoline

Diesel

Hybridgasoline

PHEVgasoline

EV

2030

Market mix changes

Source: AlixPartnersNote: * Based on 2016 testing procedure

120 95 78 60Average CO2 [g/km]*

20%

18%

28%

9%

25%

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

-202520202015

Gasoline

Diesel

Hybridgasoline

PHEVgasoline

EV

2030

Dramatic shift Electrified powertrains are forecast to have a 66% share of the European new-car market by 2030

8

AUTOMOTIVE NEWS EUROPE COVER STORY

www.autonewseurope.com MARCH 2017

ity technologies,” according to Brussels. Starting this September, it will begin re-placing the outdated and largely discred-ited NEDC cycle with the more robust Worldwide harmonized Light vehicles Test Procedure (WLTP) that better cap-tures real driving behavior.

This, however, complicates things since the post-2021 targets are therefore no longer directly comparable. T&E, for ex-ample, argues the Commission should propose a 2025 target of 80g/km based on the more strenuous WLTP guidelines, complemented by an additional real driv-ing test that ensures CO2 emissions are no higher than 10 percent above lab conditions rather than the 40 percent discrepancy of today.

One German official argued that the EU should only impose relative targets on each carmaker rather than an absolute figure given the lack of experience with the new cycle. The problem is none of this is really helping the overarching goal of reducing greenhouse gas emissions within the EU.

Although new cars are becoming cleaner each year, the overall carbon footprint from road transport has been growing since 1990, making it the only major sector of the economy heading in the wrong direction. According to the most current data from the European Envi-ronmental Agency published last June, road transport increased its CO2 output by 6.6 million metric tons in 2014 com-pared with 2013.

That was the largest increase of any sec-tor of the EU’s economy that year and meant that road transport was respon-sible for about 20 percent of total green-house gas emissions across the bloc. While part of this is due to the weakness of the NEDC system in measuring on-road emissions, another factor is that EU roads have an existing fleet of 250 million cars, which are estimated to be 9.7 years old on average.

“We would like to see proposals which do not only concentrate on new cars but also on the whole fleet,” said VDA President Matthias Wissmann, hoping to shift some of the burden away from manufacturers.

One failed proposal involved including road transport in Europe’s cap-and-trade system, effectively forcing drivers to pay for it in the form of higher fuel prices.

Currently, ACEA is calling for incentives to renew the aging car fleet or receive cred-its for Intelligent Transportation Systems

(ITS) such as truck platooning – it even has a website called reducingCO2together.eu.

German influenceWissmann, who is a former transportation minister from Chancellor Angela Merkel’s political party, used to have an easier lob-

bying job. When the 95g/km target was due to be passed during an EU summit in June 2013, Merkel intervened at the last minute on behalf of Wissmann’s au-tomotive members. She pushed for more lenient limits that would protect the sale of large premium sedans and SUVs -- the hallmark of companies such as BMW and Mercedes. Merkel, however, has since signed up to the Paris Agreement and must deliver on her own CO2 commit-ments, prompting T&E’s Greg Archer to say that he doesn’t expect any last-sec-ond changes to the new emissions regu-lations for automakers.

“There is no way that Germany can achieve its own targets on transport for 2030 unless there are significant im-provements in the efficiency of conven-tional vehicles,” Archer told Automotive News Europe. “The position of Germany is likely going to be much more nuanced than it has been in the past simply be-cause it has its own climate plan.”

Making matters worse is the negative backlash against all automakers in the wake of VW Group’s cheating on emissions tests. The scandal revealed the industry-wide use of legal loopholes to circumvent tailpipe emission limits as soon as vehicles are off the test bench and on the road. As a result, all vehicle emissions -- nitrogen

A portable emissions measurement system (PEMS) is pictured on the Citroen C4 during testing near Paris. The system is used to calculate a car’s fuel consumption, CO2 and NOx during real world driving.

Public health is at stake. We have no time to lose.

Elzbieta BienkowskaEU Industry Commissioner

Continued on Page 10▼

9

AUTOMOTIVE NEWS EUROPE COVER STORY

www.autonewseurope.comMARCH 2017

10

AUTOMOTIVE NEWS EUROPE COVER STORY

www.autonewseurope.com MARCH 2017

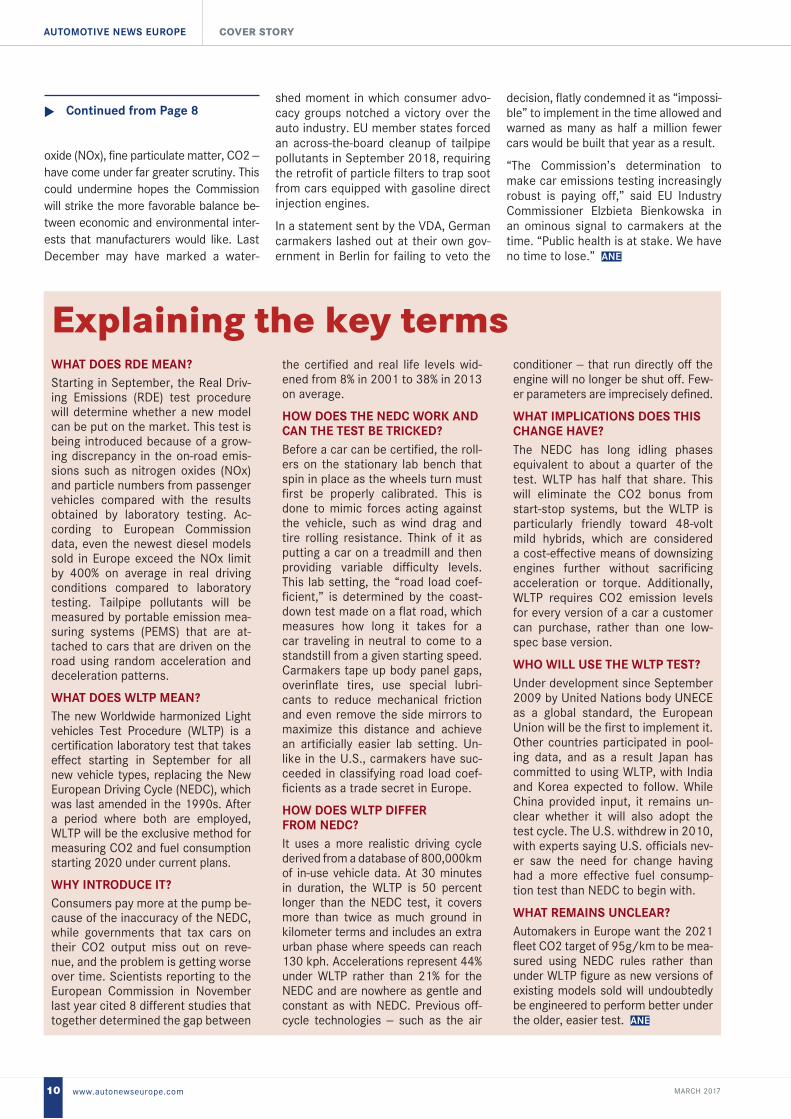

WHAT DOES RDE MEAN?Starting in September, the Real Driv-ing Emissions (RDE) test procedure will determine whether a new model can be put on the market. This test is being introduced because of a grow-ing discrepancy in the on-road emis-sions such as nitrogen oxides (NOx) and particle numbers from passenger vehicles compared with the results obtained by laboratory testing. Ac-cording to European Commission data, even the newest diesel models sold in Europe exceed the NOx limit by 400% on average in real driving conditions compared to laboratory testing. Tailpipe pollutants will be measured by portable emission mea-suring systems (PEMS) that are at-tached to cars that are driven on the road using random acceleration and deceleration patterns.

WHAT DOES WLTP MEAN?The new Worldwide harmonized Light vehicles Test Procedure (WLTP) is a certification laboratory test that takes effect starting in September for all new vehicle types, replacing the New European Driving Cycle (NEDC), which was last amended in the 1990s. After a period where both are employed, WLTP will be the exclusive method for measuring CO2 and fuel consumption starting 2020 under current plans.

WHY INTRODUCE IT?Consumers pay more at the pump be-cause of the inaccuracy of the NEDC, while governments that tax cars on their CO2 output miss out on reve-nue, and the problem is getting worse over time. Scientists reporting to the European Commission in November last year cited 8 different studies that together determined the gap between

the certified and real life levels wid-ened from 8% in 2001 to 38% in 2013 on average.

HOW DOES THE NEDC WORK AND CAN THE TEST BE TRICKED?Before a car can be certified, the roll-ers on the stationary lab bench that spin in place as the wheels turn must first be properly calibrated. This is done to mimic forces acting against the vehicle, such as wind drag and tire rolling resistance. Think of it as putting a car on a treadmill and then providing variable difficulty levels. This lab setting, the “road load coef-ficient,” is determined by the coast-down test made on a flat road, which measures how long it takes for a car traveling in neutral to come to a standstill from a given starting speed. Carmakers tape up body panel gaps, overinflate tires, use special lubri-cants to reduce mechanical friction and even remove the side mirrors to maximize this distance and achieve an artificially easier lab setting. Un-like in the U.S., carmakers have suc-ceeded in classifying road load coef-ficients as a trade secret in Europe.

HOW DOES WLTP DIFFER FROM NEDC?It uses a more realistic driving cycle derived from a database of 800,000km of in-use vehicle data. At 30 minutes in duration, the WLTP is 50 percent longer than the NEDC test, it covers more than twice as much ground in kilometer terms and includes an extra urban phase where speeds can reach 130 kph. Accelerations represent 44% under WLTP rather than 21% for the NEDC and are nowhere as gentle and constant as with NEDC. Previous off-cycle technologies -- such as the air

conditioner -- that run directly off the engine will no longer be shut off. Few-er parameters are imprecisely defined.

WHAT IMPLICATIONS DOES THIS CHANGE HAVE?The NEDC has long idling phases equivalent to about a quarter of the test. WLTP has half that share. This will eliminate the CO2 bonus from start-stop systems, but the WLTP is particularly friendly toward 48-volt mild hybrids, which are considered a cost-effective means of downsizing engines further without sacrificing acceleration or torque. Additionally, WLTP requires CO2 emission levels for every version of a car a customer can purchase, rather than one low-spec base version.

WHO WILL USE THE WLTP TEST?Under development since September 2009 by United Nations body UNECE as a global standard, the European Union will be the first to implement it. Other countries participated in pool-ing data, and as a result Japan has committed to using WLTP, with India and Korea expected to follow. While China provided input, it remains un-clear whether it will also adopt the test cycle. The U.S. withdrew in 2010, with experts saying U.S. officials nev-er saw the need for change having had a more effective fuel consump-tion test than NEDC to begin with.

WHAT REMAINS UNCLEAR?Automakers in Europe want the 2021 fleet CO2 target of 95g/km to be mea-sured using NEDC rules rather than under WLTP figure as new versions of existing models sold will undoubtedly be engineered to perform better under the older, easier test. ANE

Explaining the key terms

oxide (NOx), fine particulate matter, CO2 -- have come under far greater scrutiny. This could undermine hopes the Commission will strike the more favorable balance be-tween economic and environmental inter-ests that manufacturers would like. Last December may have marked a water-

shed moment in which consumer advo-cacy groups notched a victory over the auto industry. EU member states forced an across-the-board cleanup of tailpipe pollutants in September 2018, requiring the retrofit of particle filters to trap soot from cars equipped with gasoline direct injection engines.

In a statement sent by the VDA, German carmakers lashed out at their own gov-ernment in Berlin for failing to veto the

decision, flatly condemned it as “impossi-ble” to implement in the time allowed and warned as many as half a million fewer cars would be built that year as a result.

“The Commission’s determination to make car emissions testing increasingly robust is paying off,” said EU Industry Commissioner Elzbieta Bienkowska in an ominous signal to carmakers at the time. “Public health is at stake. We have no time to lose.” ANE

Continued from Page 8▼

11

AUTOMOTIVE NEWS EUROPE COVER STORY

www.autonewseurope.com MARCH 2017

12

AUTOMOTIVE NEWS EUROPE Q&A

www.autonewseurope.com MARCH 2017

Daimler r&d boss outlines Mercedes’ self-driving, EV, connectivity plans

Trend tracker QADaimler’s new r&d boss, Ola Kaelle-

nius, believes the auto industry is at a major crossroads as megatrends such as connectivity, autonomous drive, shared services and electrification com-bine to shape the future market. The Swedish executive succeeded Daimler’s long-serving r&d chief, Thomas Weber, in January and is considered a front-runner to succeed CEO Dieter Zetsche when his contract expires in 2019. Kaellenius has worked at Daimler since 1993. He is the former head of sales at Mercedes-Benz Cars and has also headed the compa-ny’s AMG performance unit. He recently spoke with Automotive News Europe As-sociate Publisher and Editor Luca Ciferri.

Do you believe the automotive indus-try is at a crossroads? Yes, we are in the middle of a transfor-mation process. There are four technical megatrends shaping this transforma-tion, we call them CASE, which is short for connectivity, autonomous drive, shared services and electrification. The breakthroughs that we have had in the last few years will lead to an actualiza-tion of these trends in the next five to 10 years and this could change the face of the auto industry.

Does Daimler expect to benefit from these trends? We’re in a strong position on every one and we are putting further resources into them to make sure Daimler remains one of the leading companies in the future.

Is artificial intelligence (AI) now the leading technology for autonomous driving and is it ready? I remember hearing a lot about artificial intelligence 20 or 25 years ago. Every-body was talking about it. Then it went quiet for 20 years, not least because writ-ing line code for every eventuality would end up creating a very thick book that would need computing power like there was no tomorrow. That’s why it stalled. In the last three to four years, there’s been an absolute breakthrough in how you can apply software to address this

problem. We couldn’t have done it the old way. Now the technological building blocks capable of taking on this chal-lenge are really coming together.

What do you need for AI in a car to be safe, redundant AI interfaces? In terms of the computing power to run the autonomous system, we will rely on one computer to make it simple. But, for some systems in the car, like steering and braking where in a case of the loss of electrical power you must use muscle power to make sure the car stays on the road, you are going to have to look at redundancies.

Will we see a mid-cycle face-lift of the S class this summer and will there be new autonomous driving features added to your flagship? We’re coming with more new features on the next S class. For example, I think this is the first time any production car links the map to the sensor data in an in-telligent way for an application that you can actually buy.

Could you explain? Let me give you one example: Take a curvy highway somewhere in the U.S. where the speed limit is 55 mph (about 80 kph). This highway might have some corners that are so tight that it wouldn’t be very comfortable to go through them at 55 mph. Maybe you should go through at 50 mph or at 45 mph. As a driver, you would just slow down. Most assistance systems up to this point, however, can’t do that. That’s why we have linked the sensors to the map material. The map knows that you’re getting to this corner so it automatically slows the car to the appropriate speed to take the corner and then accelerates to the set speed once you are through the curves.

How good is your current semi-auton-omous technology at handling curves?

One of the challenges with semi-auto-mated drive is radius as a course and exactness. Clearly you don’t want to be a meter off and end up with half of your

car on the other side of the road. The narrower the corner, the more difficult this is. Our current level of our driver assistance systems, especially at high speeds, could do 80 percent of all au-tobahns in Germany and maybe 10 to 20 percent of the smaller roads. The new system, where we have worked up even sharper cornering ability and further devel-oped our sensing technology, can now do approximately 80 percent of the smaller highways in Germany as well. ANE

Meet r&d boss❚ NAME: Ola Kaellenius

❚ TITLE: Daimler Board Member for Group Research and Mercedes-Benz Cars Development

❚ AGE: 47

❚ MAIN CHALLENGES: Keep-ing Daimler ahead of sweeping changes around connectivity, autonomous driving and electrifi-cation; managing the expansion of Mercedes’ portfolio to more than 40 models.

13

AUTOMOTIVE NEWS EUROPE COVER STORY

www.autonewseurope.com MARCH 2017

14

AUTOMOTIVE NEWS EUROPE Q&A

www.autonewseurope.com MARCH 2017

How Schreyer channeled his passion to make a sports car into the Kia Stinger

Design driven QAPeter Schreyer, the man responsible

for the iconic looks of the first Audi TT coupe, has dreamed of designing a true sports car for Kia since the Korean auto-maker hired him away from the Volkswa-gen Group in 2006. Despite his success at Kia, which in 2012 earned him a promo-tion to Hyundai Motor Group vice presi-dent and chief design officer and put him in control of styling at all the company’s brands, Schreyer’s sports car remained in a drawer. Then an opportunity arose to put that passion into a completely differ-ent project. The result is the Kia Stinger. Schreyer discussed the sport sedan’s gen-esis with Automotive News Europe Associ-ate Publisher and Editor Luca Ciferri at the Stinger’s European preview in Milan, Italy.

How did you start with the Stinger?I had a sports car on my mind for years. It was almost a dream for me [since I arrived at Kia]. I had hoped to use a rear-wheel-drive layout for the car be-cause you can get completely different proportions that way. After we did the South Korea-only K9 large sedan with rwd [Kia Europe design boss) Gregory Guillaume said we should collaborate on something based on this architec-ture because we are both passionate about sports cars. The result was the Stinger, which is something special. It is the first rwd sporty sedan from Kia that was designed since day one for in-ternational markets.

Where did you look for inspiration?In the 1970s you had fantastic Gran Tur-ismo models from Maserati, such as the Ghibli, that offered performance, com-fort and style. The idea was to make a modern interpretation of the GT.

Was the first example of this the GT concept unveiled at the 2011 Frank-furt auto show?Yes, it was so well received by the media, dealers and customers that the top management in Korea started to consider making a business case for the car so we started to work to-ward production.

Is it fair to say the Stinger is a real-ity because the design of the concept was so compelling?Absolutely. And after seeing it the busi-ness side of the company became ex-cited and really wanted to make it hap-pen. For us it was a dream come true. I became more and more hopeful the car would make it to production when I kept seeing big smiles on the faces of top management when we presented the various evolutions of the project.

Why was it called the “red model” within Kia?The code-name was CK but after we had presented the styling model painted in a special shade of red that everyone liked it became known as the red model with-in the entire company.

As a car goes from concept to produc-tion the design is usually toned down. Did that also happen with the Stinger?Designers always aspire to make the production car as close to the concept as possible, but you face a lot of tech-nical and safety issues, ranging from pedestrian protection requirements to C-pillar visibility. Overall, I am happy with the Stinger’s final look. I also have to admit that the front of the production car is better than the concept because we had more time to refine it.

Will there be black stripes on the hoods on all models? If so, isn’t that just decoration?They are on all models and I do not see them as decoration. You need to differen-tiate your design from your competitors and graphic elements are needed some-times, otherwise you just make a box.

Which of the Stinger’s design charac-teristics will be transferred to future Kia models? Every new model influences the next ones. You will see some sportier Kia cars in the future.

Will China get the Stinger?China is such a big market with different

demands and sports sedans like this are also going to work there, sooner or later.

Will there be a Stinger wagon?A wagon is not planned at the moment.

Do you still dream of one day penning a roadster for Kia, Hyundai or eventu-ally Genesis?Yes, it would be nice to have something like this, but it is much more difficult to get approval [for a roadster] because you will never sell it in high volumes. The Stinger has the potential to sell in signifi-cant numbers. ANE

Meet the design boss❚ NAME: Peter Schreyer

❚ TITLE: Hyundai Motor Group President and Chief Design Officer

❚ AGE: 63

❚ MAIN CHALLENGE: Differentiat-ing the styling of Hyundai, Kia and Genesis brands.

15

AUTOMOTIVE NEWS EUROPE COVER STORY

www.autonewseurope.com MARCH 2017

Your Latest Features on Full Display

It can stream rear video to optimize the rearward view. Run home automation scenes

with the push of a button. Display ADAS alerts in the ideal, heads-up location.

Automatically pay tolls and facilitate transactions.

The Full Display Mirror®. It’s not just high-tech, it’s Gentex. www.gentex.com/fdm

HomeLink® car-to-home automation

Mirror-integrated LCD display

LCD adjustment controls

ADAS alerts and driver information

Integrated toll payment module

16

AUTOMOTIVE NEWS EUROPE AUTOMAKERS

www.autonewseurope.com MARCH 2017

Finding the right fitHow Opel/Vauxhall and PSA are already successfully cooperating

CHRISTIAAN [email protected]

The new Crossland X, which Opel/Vauxhall is taking on tour around Eu-

rope this month, shares many character-istics found in the brand’s other cars. The so-called “floating roof” comes from the Adam, ergonomic seats are also found in the Insignia and the OnStar concierge service derives from parent General Mo-tors. Engineers claim the crossover drives like a German car too, meaning it is stable in the curves without sacrificing comfort.

Underneath, however, the mechanical innards are all French. To save costs, essentially every part in the Cross-land X that the customer doesn’t see is shared with the new Citroen C3 Air-cross. Not even the 1.6-liter diesels come from Opel.

If it’s up to GM CEO Mary Barra, the Crossland X will mark a new beginning for Opel and Vauxhall – one without GM. The U.S. carmaker looks to extricate itself from Europe by offloading its two brands onto Citroen’s parent, the PSA Group. Im-mediately following the announcement that in 2016 it took a $257 million loss at Opel/Vauxhall, this time on the back of Brexit-related currency headwinds, Barra voiced her frustration at yet an-

other breakeven target GM’s European arm failed to achieve. Despite nearly two decades of restructuring programs, cut-backs and plant closures, Opel/Vauxhall remained mired in red ink. Meanwhile once-struggling rivals Ford of Europe and PSA have been able to return to profit.

‘Not satisfied’“We’re not satisfied with these results and the team is focused on mitigating the effects,” Barra told investors last month, just days before it was revealed she and GM were in advanced talks with Opel’s platform provider over a sale to the French parent. PSA Group CEO Car-los Tavares says the Crossland X is the blueprint for how the two companies can successfully work together, which he says they have been doing without any problems for four years. He believes those benefits would only expand from closer cooperation, something the two companies have been discussing since last November.

Tavares is confident PSA can make a dif-ference. “We think we could help Opel because three years ago PSA was in a similar position,” the CEO said. “Opel is ready to listen to us.”

Another key factor pushing Opel toward

PSA is that Europe’s car market is ex-pected to stagnate this year on the back of a forecast decline for UK sales due to uncertainty about the country’s exit from the EU, ensuring further losses for Opel this year. In addition, major elections are being held across the EU that could de-termine the fate of the single currency, especially if Marine Le Pen, who has said she would hold a referendum on whether to abandon the euro, is elected French President in May. An expected sales re-bound in Russia this year also won’t help because Opel pulled out of the market in 2015 to prevent further losses.

Forecaster IHS Markit highlighted late last month the harsh reality, saying the industry risk in mature markets is at the highest level it has been since the Lehm-an Brothers collapse in 2008, which helped spark the global economic crisis. “Political uncertainty could cause a sig-nificant rift in light vehicle sales both in the U.S. and Europe, as both regions are undergoing fluctuations in policy, leader-ship and other dynamics,” said Henner Lehne, senior director, global vehicle group for IHS Markit.

Under that scenario, perhaps it is wise for GM not to have Opel and Vauxhall, although the automaker balked at the chance to discard the brands eight years

Illus

trat

ion:

Aut

omot

ive

New

s Eu

rope

/iSt

ockp

hoto

17

AUTOMOTIVE NEWS EUROPE AUTOMAKERS

www.autonewseurope.comMARCH 2017

ago because management wanted to maintain a presence in Europe. When the U.S. automaker found itself insol-vent in 2009 and unable to fund Opel, the subsidiary was put up for sale at the insistence of the German govern-ment. Once GM emerged financially strengthened from its pre-packaged bankruptcy, however, it called off the disposal. The uncertainty over Opel/Vauxhall’s future, however, left a per-manent mark on the business.

Positive signalsWhen Opel CEO Karl-Thomas Neumann joined in March 2013, the year European new-car sales hit bottom, the GM sub-sidiary had just postponed yet another breakeven target after losses soared to $1.9 billion in the previous year. With Neumann in charge, GM agreed to fund 4 billion euros worth of investments through 2016. It even held its first board of directors meeting in Opel’s German headquarters to demonstrate the par-ent’s steadfast commitment.

In return Neumann pledged that by 2022 Opel/Vauxhall would deliver an 8 percent European market share and an operating margin of 5 percent. The first test of that goal was attaining profitability last year. While Opel failed, it was a lot closer to making money than it had been in nearly two decades. Since Neumann joined four years ago, Opel managed to halt a market share slide it had suffered since Europe-an car sales peaked in 2007.

Key new models such as the Astra were winning important prizes, sales were slowly growing, and Opel’s once-disas-trous image in Germany was on the mend, helped by ads that took advantage of Opel’s underdog status.

Turning around a chronic money-loser such as Opel/Vauxhall is no small feat. Whether it is Fritz Henderson, Carl-Pe-ter Forster, Nick Reilly, Karl-Friedrich Stracke, Steve Girsky or Neumann – the list of executives that had their shot at making GM’s European operations prof-itable is long. And all ultimately failed.

Said Tavares: “I have a high respect for the work that Neumann and his team did at Opel, but you cannot continue to lose money for more than a decade and

burn 1 billion euros in cash each year.” He added that he doesn’t think you can plan the future if you do not manage to deliver results in the short term.

Model offensiveAs talks continue about Opel/Vauxhall’s future without GM the company has start-ed the biggest model offensive in its his-tory, with seven launches this year that are expected to help it become Europe’s second-largest automaker by sales next year, according to an IHS forecast (see chart, left). The new models include the revamped Insignia sedan as well as the Ampera-e, a purpose-built full-electric car with a certified range of more than 500 km. Largely based on the Chevrolet Bolt, the Ampera-e beats Volkswagen brand’s ID electric car to market by three years. At press time, Neumann was re-portedly mapping out the transformation of Opel into an electric car brand. Perhaps that is why the otherwise Twitter-friendly CEO only could muster a tepid endorse-ment for the deal on social media: “In principle, an affiliation with PSA makes sense,” he tweeted, even though he nev-er once supported deeper ties with the French carmaker in the past when asked.

Despite Neumann’s possible reserva-tions about the deal, Tavares believes the combined entity could sell 5 million units a year in the midterm and reach a profitability level close to PSA’s cur-rent target, which is a 6 percent margin. “There is an opportunity to create a Eu-ropean car champion resulting from the combination of a French company and a German company with a strong UK brand,” he said.

-- Luca Ciferri and Peter Sigal contributed

Race for second placeOpel/Vauxhall is expected to rise to No. 2 in European sales next year but slide into 4th place behind the Renault and Ford brands by 2021

Source: IHS Automotive

5002017 2018 2019 2020 2021

1,000

1,500

2,000

The Opel/Vauxhall Crossland X shares its platform with the Citroen C3 Air-cross. The small crossover, which is made at Opel’s plant in Zaragoza, Spain, is one of seven new models Opel will launch in 2017.

Volkswagen

FordRenaultOpel

in ’000s

18

AUTOMOTIVE NEWS EUROPE AUTOMAKERS

www.autonewseurope.com MARCH 2017

Holding its groundRenault faces tough task staying Europe’s No. 2 brand as product push slows

PETER [email protected]

Over the past two years, Renault has overtaken Ford and Opel to become

the second-largest brand in Europe by unit sales, riding the momentum from a wave of stylish new models, especially in the hot crossover segment. But ana-lysts say that success will be harder to maintain in 2017 as growth in the overall European market slows and the product pipeline empties out. The European auto market is widely expected to increase by only about 2 percent in 2017, compared with 6.5 percent last year.

“It’s probably easier to have strong growth when the market is growing it-self,” said Alexis Albert, a Paris-based analyst on the automotive sector at Bar-clays. “The market will be less support-ive than it was in 2016.”

Ian Fletcher, a principal analyst at IHS Automotive, said: “I don’t think it’s nec-essarily going to be an easy time for them, but given the foundations that have been put in place now going to-ward the next decade, they are looking reasonably positive.”

IHS forecasts that Renault will finish as Europe’s second-largest brand again in 2017 with a volume of 1.17 million, fol-lowed by Ford (1.04 million) and Opel/Vauxhall (997,650).

Last year Renault sold a company-re-cord 1,100,880 vehicles in Europe, a 13 percent gain over 2015, according to industry association ACEA. That left it behind No. 1 Volkswagen brand’s 1.72 million sales but ahead of Ford and Opel/Vauxhall. Renault’s rise last year followed an 11 percent increase in 2015 and a 9 percent increase in 2014.

Last month Renault also reported a 38 percent surge in operating profit to 3.28 billion euros in 2016 on 51.2 billion euros in revenue. That helped Renault increase its profit margin to 6.4 percent from 5.2 percent in 2015, meeting a key target one year early. The success caused Renault to set new goals, includ-ing a 7 percent operating margin and 70 billion euros in revenue by 2022.

No blockbusters in ’17While Renault will continue to benefit in its home region from recently launched products such as the new Scenic, which is one of Europe’s top-selling minivans, there are no “blockbuster” new models planned for 2017, Albert said. He added that the downside to introducing so many models in a short time span is that it can overwhelm the sales force, which then fo-cuses on selling the vehicles that are easi-est to move, such as the Kadjar compact crossover. Similarly, he said, “once you get your sales force and customers used to so many new cars, it becomes more difficult to sustain that kind of growth rate.”

In addition, Renault’s closest competi-tors are keeping up the pressure. Prod-ucts such as the Opel/Vauxhall Grand-land X and Crossland X crossovers, which are built under a 4-year-old joint development deal between the General Motors subsidiary and PSA Group, are scheduled to reach the market starting this year. Ford, which posted a record $1.2 billion profit in Europe in 2016, will also continue to make a strong push in SUVs, said Dominic O’Brien, an analyst at Exane BNP Paribas in London. “The competition’s not going to get any eas-

ier,” O’Brien said. “You could probably imagine that this will be an incrementally more competitive year [for Renault].”

Brexit & diesel probeThat could be complicated somewhat by geopolitical events, including close-ly watched presidential elections in France, the Netherlands and Germany, and the effects of Britain’s exit from the European Union. And in the wake of the Volkswagen Group’s emissions-cheating scandal, combined with increased pres-sure from France and other European countries to further reduce emissions, the region’s consumers are starting to turn away from diesel engines. Renault is vulnerable to the trend, as about 54 per-cent of the company’s sales in France, and 51 percent in Europe, are diesel powered, a spokeswoman said. Renault has also come under scrutiny by French authorities, who have opened an investi-gation into suspected cheating on emis-sions testing. The company has denied any wrongdoing, and analysts urged cau-tion about the matter. “We don’t know the full details, let alone which way this is going to come out,” O’Brien said. “We have no reason to believe this is on the same scale as Volkswagen.” ANE

Helped by the Clio, Europe’s best-selling subcompact, Renault raced past Ford to No. 2 in sales behind the VW brand.

19

AUTOMOTIVE NEWS EUROPE COVER STORY

www.autonewseurope.com MARCH 2017

We’re moving millions – increasingly clean and efficient.

borgwarner.com

There is no more important technological challenge for the automotive industry today than the commitment of building more eco-friendly vehicles. Therefore, improving fuel economy and reducing emissions are the main objectives within our technology development of combustion engines. Whether new combustion processes, automatic start-stop systems or increasingly strict emissions requirements – we have innovative solutions ready for every technological challenge.

20

AUTOMOTIVE NEWS EUROPE AUTOMAKERS

www.autonewseurope.com MARCH 2017

Show starsFast cars in spotlight at Geneva

Citroen Citroen will compete in the hot-selling subcompact SUV/crossover segment with the C-Aircross, which is based on the new C3 hatchback. The concept previews the produc-tion car that will replace the C3 Picasso small minivan. The production C-Aircross will be built in Opel’s plant in Zaragoza, Spain, alongside its siblings, the Opel/Vauxhall Crossland X and a Peugeot version.

DS Automobiles DS Automobiles will unveil a new flagship, the DS 7 Cross-back. The compact crossover is expected to go on sale in Europe later this year as a rival to German premium models. It shares its EMP2 platform with the Peugeot 3008 and up-coming Opel/Vauxhall Grandland X. The DS 7 Crossback is also likely to have all-wheel-drive and plug-in hybrid versions.

Ferrari Ferrari’s 812 Superfast will be the brand’s most powerful se-ries production car to date. Its naturally aspirated 6.5-liter V-12 engine makes 798 hp and pushes the car to a top speed of 340 kph (211 mph) with acceleration from 0 to 100 kph (62 mph) in 2.9 seconds. It’s the first Ferrari to have electric power steering.

Ford The new Fiesta will get advanced safety features such as adap-tive cruise control and lane-keeping assist that are not yet common in subcompacts. The upscale equipment will help the Fiesta meet demand for advanced technology from custom-ers downsizing from larger models and will help distance the car from the new Ka Plus subcompact, which targets budget customers in Europe.

Hyundai Hyundai will debut the new i30 compact wagon. The wagon’s trunk capacity has grown to be among the biggest in the seg-ment at 602 liters, with space rising to 1,650 liters when the rear seats are folded flat. The car gets advanced active safety equipment already on the new i30 hatchback such as autono-mous emergency braking, smart cruise control and driver at-tention alert.

This year’s Geneva auto show will highlight a mix of super-cars, SUVs and mainstream models. PSA’s DS brand and

Land Rover’s Range Rover will show new SUVs aimed at buy-ers in a hot segment looking for luxury. Citroen’s C-Aircross concept previews the brand’s new entry in the subcompact crossover segment, while Porsche and Hyundai target practi-cal buyers with new wagons. Among the supercar highlights will be Ferrari’s most powerful series production model to date and Chinese-backed Techrules’ Tesla Model S fighter styled by Giorgetto Giugiaro.

Here are some key debuts:

Citroen C-Aircross concept

Ferrari 812 Superfast

DS 7 Crossback

Ford Fiesta Hyundai i30 wagon

21

AUTOMOTIVE NEWS EUROPE AUTOMAKERS

www.autonewseurope.comMARCH 2017

Italdesign Italdesign, Audi’s design and engineering subsidiary, will unveil the Zerouno supercar priced at 1.5 million euros ($1.6 mil-lion) plus taxes. The company’s new bespoke division, Italde-sign Automobili, intends to build five examples of the two-seat carbon-fiber car. It has a 5.2-liter V-10 engine also used in top-end versions of the Audi R8 and can accelerate from 0 to 100 kph (62 mph) in 3.2 seconds.

Kia Kia hopes customer loyalty, along with new connectivity and safety features, will help lift sales of the Picanto in the price-sensitive minicar segment. Picanto buyers are “extremely loy-al” to the brand compared with customers for other Kia cars and the market as a whole, Kia Europe Chief Operating Officer Michael Cole said. Kia is discontinuing the three-door version due to slowing demand.

Opel/Vauxhall Opel hopes the new Insignia’s advanced technology, ride com-fort and sleek design will help to stem the loss of midsize seg-ment customers to premium rivals such as the BMW 3 series. The sedan gets a new name, the Insignia Grand Sport. Opel says the car’s optional torque vectoring all-wheel-drive system that improves grip and handling is a segment first. The Insignia Grand Tourer wagon will also debut.

PorscheThe Panamera Sport Turismo, Porsche’s first wagon, will com-pete with the Mercedes-Benz CLS Shooting Brake to appeal to customers looking for luxury, a sporty drive and practicality. Porsche sees Europe as the main market for the wagon, which is based on the latest Panamera four-door variant, but it will also sell the car in the U.S. and China, where wagons are less popular.

Land Rover Land Rover will expand its Range Rover lineup with the Velar, a sporty SUV that will be a rival to the Porsche Macan. The Velar will be positioned between the entry-level Range Rover Evoque and the more expensive Range Rover Sport. The Velar is the first Land Rover to use Jaguar Land Rover’s D7A all-wheel/rear-wheel-drive platform that underpins the XE midsize sedan and F-Pace SUV sold by sister brand Jaguar.

Techrules Chinese startup Techrules’ supercar was styled by the Ital-ian father-son design team of Gior-getto and Fabrizio Giugiaro. The car has an aircraft-inspired three-seat cockpit design. It’s the production version of the 1,030-hp GT96 concept unveiled in Geneva last year. The car will be powered by a hybrid powertrain that uses a micro-turbine to generate electricity to charge a battery pack.

More on the WebPlease visit Automotive News Europe’s stand-alone Geneva auto show Web page for the latest news and photos at:

autonewseurope.com/geneva

stand-alone Geneva auto show Web page

Opel Insignia Grand Sport

Seat Ibiza

Range Rover Velar

PorschePanamera

KiaPicanto

Italdesign Zerouno

Techrules concept

sporty SUV that will be a rival to the Porsche Macan. The Velar will be positioned between the entry-level Range Rover Evoque and the more expensive Range Rover Sport. The Velar is the first Land Rover to use Jaguar Land Rover’s D7A all-wheel/rear-wheel-drive platform that underpins the XE midsize sedan and F-Pace SUV sold by sister brand Jaguar.

Techrules Chinese startup Techrules’ supercar was styled by the Ital-ian father-son design team of Gior-getto and Fabrizio Giugiaro. The car has an aircraft-inspired three-seat cockpit design. It’s the production version of the 1,030-hp GT96 concept unveiled in Geneva last year. The car will be powered by a hybrid powertrain that uses a micro-turbine to generate electricity to charge a battery pack.

Techrules concept

is based on the latest Panamera four-door variant, but it will also sell the car in the U.S. and China, where wagons are less popular.

Seat Ibiza

due to slowing demand.

PorscheThe Panamera Sport Turismo, Porsche’s first wagon, will com-

Land Rover Land Rover will expand its Range Rover lineup with the Velar, a

Range Rover Velar

PorschePanamera

for the latest news and photos at:

autonewseurope.com/geneva

Opel Insignia Grand Sport

Seat Seat’s latest Ibiza is the first Volkswagen Group model to use the MQB A0 architecture for smaller cars that will also under-pin the new VW Polo. The platform has enabled Seat to im-prove the car’s driving dynamics, ride quality and driving com-fort. Safety technology will include adaptive cruise control and traffic jam assist, which can accelerate and decelerate the car in traffic congestion.

22

AUTOMOTIVE NEWS EUROPE AUTOMAKERS

www.autonewseurope.com MARCH 2017

Gaining groundFull-hybrid, plug-in hybrid sales rise fast but new tech could shake up sector

NICK [email protected]

Hybrid and plug-in hybrid sales grew an impressive 30 percent to just

over 400,000 in Europe last year, but the real impact in the midterm will be made by mild hybrids, analysts predict. By 2025 mild hybrids will capture 18 per-cent of the European market, IHS Auto-motive forecasts. That’s compared with 6 percent for plug-in hybrids, 3 percent for full hybrids and 3 percent for full-elec-tric vehicles in the same time frame.

Currently, the big growth is in full hybrids, largely because of Toyota’s increasing success in Europe. Expanding a technol-ogy that is enormously successful in its home market of Japan, the automaker last year launched hybrid versions of the RAV4 and CH-R compact SUVs, which joined gasoline-electric versions of the Auris compact and Yaris subcompact hatchbacks already on sale in Europe.

Last year Toyota sold 232,699 hybrids across Europe, a rise of 47 percent from the year before, according to data from market researchers JATO Dynamics. Of those, 41,814 were the new RAV4 hybrid, putting it third behind the Yaris and Auris hybrid models. Lexus was the next biggest hybrid brand with sales of 41,372.

Apart from minicars, Toyota is commit-ted to offering hybrid variants through-out its entire range, Toyota Europe CEO Johan van Zyl told Automotive News Europe last summer. The automaker wants hybrids to account for half of its total European sales by 2020, up from 31 percent at the time of interview. Van Zyl said he expected 70 percent of C-HR sales to be hybrid. The car is not available with a diesel engine. Now that Peugeot is winding down its diesel hybrid program, Toyota’s rivals for hybrid sales in Europe are limited to Kia and Hyundai, which last year launched the Niro and Ioniq compacts, respectively. The Ioniq is also available as an EV.

Plug-in hybrids expandHyundai and Kia will add plug-in hybrid ver-sions of both cars later this year, further ex-panding a market that now offers far more choice to consumers than either the full

hybrid or EV segments. Plug-in hybrid sales in Europe rose by 19 percent to 112,300 last year as new models helped drive de-mand. Europe’s best-seller by a wide mar-gin was once again the Mitsubishi Out-lander PHEV, which has been the region’s leader in the fledgling niche since 2014. Demand for the car, however, dropped 33 percent to 21,149 last year as German automakers started to gain share in the sector (see table, above, right).

The Volkswagen Passat GTE rose to sec-ond from seventh in 2015 after sales climbed 176 percent. The Passat GTE also took advantage of a 37 percent drop for the former No. 2 in the sector, the GTE

version of the VW Golf, which fell to third. Also seeing strong growth in the segment were the Mercedes-Benz C 350 e, Volvo XC90 T8 Twin Engine, BMW 330e and BMW 225xe Active Tourer.

Sales of plug-in hybrids in Europe have already overtaken those of full-electric vehicles and will continue to grow more strongly than EVs in the near term, IHS Automotive powertrain analyst Vijay Subramanian believes. But he warns the growth is precarious.

The Mitsubishi Outlander remained Europe’s No. 1-selling plug-in hybrid in 2016 despite a 33% decline in sales.

Mixed results European sales of all electrically as-sisted cars in 2016; change from 2015

Full hybrids 294,800 +37%Plug-in hybrids 112,300 +19%Electric vehicles 89,500 +4.8%Extended-range EVs 6,900 -4.1%Fuel-cell cars 108 -2.7%

Source: JATO Dynamics

The leaders Europe’s top-selling plug-in hybrids

1. Mitsubishi Outlander 21,149 -33% 2. VW Passat GTE 13,327 176% 3. VW Golf GTE 11,104 -37% 4. Mercedes C 350 e 10,056 73% 5. Volvo XC90 T8 9,777 236% 6. BMW 330 e 8,708 new 7. Audi A3 e-tron 6,589 -46% 8. BMW 225xe 6,047 new 9. BMW X5 xDrive 40e 5,664 202%10. Audi Q7 e-tron 3,732 new

Source: JATO Dynamics

23

AUTOMOTIVE NEWS EUROPE AUTOMAKERS

www.autonewseurope.comMARCH 2017

Changing incentivesThe Netherlands was by far the biggest European market for plug-in hybrids in 2015, but last year the country slipped below the UK and Norway after sales halved. The collapse was because the government withdrew generous incen-tives for company car drivers on discov-ering from fuel-card data that drivers weren’t plugging them in. Instead of re-ducing CO2 levels, the incentives were in danger of increasing them.

Incentives are important because plug-in hybrids are more expensive than con-ventional models. In the UK, the largest market in Europe for both conventional and plug-in hybrids, the new Toyota Prius plug-in hybrid starts at 34,895 pounds [40,800 euros] before a 2,500-pound government incentive is applied. The Prius hybrid starts at 24,100 pounds.

Despite the high purchase price, plug-in hybrids are popular in the UK and

other markets because the current EU-wide NEDC fuel-economy testing cycle is very generous to plug-in models. The low CO2 figure it generates for plug-in hybrids make them eligible for attrac-tive tax incentives. Those perks could be reduced if the forthcoming real-driv-ing emissions (RDE) element of the re-vamped fuel economy test records more realistic figures.

“The dramatic fall in PHEV [plug-in hybrid electric vehicle] demand in the Nether-lands confirms how dependent they are on incentives,” JATO analyst Felipe Mu-noz said. “The only real advantage they have is the incentive they can get.”

Automakers are responding by accen-tuating the other positives of plug-in hy-brid models, such as performance.

“It has this additional boost that comes on top of the gasoline propulsion that really gives you an edge. It’s fantastic,” BMW’s board member responsible for

the Mini brand, Peter Schwarzenbauer, said about the new Mini Countryman plug-in hybrid, the brand’s first. The car uses a version of the drivetrain found on the BMW 225xe Active Tourer.

Even so, Schwarzenbauer admits that adding the variant to the Countryman’s portfolio is a gamble. “We have studied all plug-in hybrids and cannot see a clear trend. In some markets it’s booming, other markets it’s zero,” he told Auto-motive News Europe at the Los Angeles auto show last November.

Rival technology Automakers and suppliers are clearer on the advantages of cheaper mild hybrids. In the first phase of the technology, a small 48-volt electric motor connects to the crankshaft to provide a low-cost power boost from a battery topped up with energy recovered during braking and deceleration.

The Suzuki Baleno and Ignis SVHS (Smart Hybrid Vehicle by Suzuki) were the first vehicles to offer a 48-volt mild hybrid in Europe, but Renault is about to make an even bigger splash with the imminent arrival of its first model with the technology, the Scenic Hybrid As-sist. Renault will extend the technology from its popular minivan to the Megane compact model line later this year. The vehicles will use a 48-volt system from supplier Continental, which pre-dicts the number of cars using these lower voltage hybrid drives will reach 4 million worldwide by 2020, rising to 25 million by 2025.

Renault will use them on diesel mod-els initially, but ultimately the technol-ogy will be applied to gasoline-powered cars to help reduce European auto-makers’ dependence on diesels. VW believes the technology will remove the need for the smaller 1.6-liter diesel engine altogether. “In a time not so far away, people will go for petrol engines in combination with a mild hybrid,” Volkswagen’s head of research and de-velopment, Frank Welsch, told the UK’s Autocar magazine in February.

The technology is cheap enough to be-come mainstream, Continental’s board member for its powertrain division, Jose Avila, told Automotive News Europe. “Typically a manufacturer says that an acceptable compromise for fuel econo-my versus cost is 50 euros per gram of CO2 savings,” he said. “This technology gets very close to that.” ANE

The VW Passat GTE rose to No. 2 on Europe’s list of top-selling plug-in hybrids last year because of a 176% sales rise.

European sales of plug-in hybrids climbed 19% last year with rising demand for models such as the Mercedes C 350 e.

24

AUTOMOTIVE NEWS EUROPE LATEST LAUNCHES

www.autonewseurope.com MARCH 2017

The Countryman gets more of an SUV look. Its classic Mini grille and headlights are less prominent.

Mini maxes out with CountrymanThe Mini Countryman has grown to

become the BMW subsidiary’s big-gest model to date and it is likely to re-main the marque’s maximum-sized car. “There will not be a larger Mini for the foreseeable future,” said the brand’s boss, Sebastian Mackensen.

The new Countryman is 200mm longer and 30mm wider than the first-gener-ation model and now competes in the compact class, the first Mini to do so. BMW’s board member for Mini, Peter Schwarzenbauer, said the Countryman will stand out against more practical compacts because of its distinctive look. “Mini is a style icon and the Countryman has lots of emotional appeal,” he said.

The Countryman, which first appeared in 2010, had to grow because customers, especially in the U.S. and China, wanted more room as well as additional safety equipment and comfort features.

The Countryman’s bigger size means more units of the model are likely to be sold for use as a sole family car rather than as a second or third car. The new Countryman has significantly more head and shoulder space for the driver and front seat passenger, along with ample room for three passengers in the rear. Its luggage compartment’s volume is 450 liters, 220 liters more than the pre-decessor, and the space can be extend-ed to 1,390 liters, up from 1,170 liters.

The Countryman shares parent BMW Group’s front-wheel/all-wheel drive plat-form with other models such as the BMW X1 and 2-series minivans. The Country-man will be the first Mini to get a plug-in hybrid version, which will have a 40km full-electric driving range when it goes on sale in June. That’s a few months af-ter the launch of the gasoline and diesel versions of the car.

Mini’s global sales increased 12 per-cent last year to a record 338,466 and BMW expects the Countryman to help increase the brand’s volume this year despite political uncertainty in key mar-kets such as the UK and U.S.

– Paul McVeigh

❚ Launch date: February (Europe); March (rest of world)

❚ Base price: 26,500 euros (Germany)

❚ Main rivals: Mercedes GLA, Audi Q2

❚ Where built: Born, Netherlands

❚ Lowest CO2 emissions: 118g/km (diesel); 49g/km (plug-in)

The Basics❚ Technology: Features include cam-era-based active cruise control, colli-sion warning with city braking func-tion, road sign detection. ❚ Connectivity: A personal mobility assistant will calculate the best de-parture time to drive to appointments based on address data and calendar information saved by the driver.

Fast Facts

❚ Novelty feature: A “picnic bench” that folds out of the luggage com-partment and seats two people.

25

AUTOMOTIVE NEWS EUROPE COVER STORY

www.autonewseurope.com MARCH 2017

OPTIMIZE

DES

IGN

CUT

T H E E X P E R T I S E T O D R I V E C H A N G E

You can’t deliver extraordinary products if you don’t excel atordinary operations. From design through product development to manufacturing, Lectra’s professional services and innovative technology optimize your manufacturing process for fabric and leather car interiors, as well as airbags. We ensure that you can sustain your performance and have the flexibility to surmount current and future challenges.

Those who demand more, demand Lectra.

TO OPERATIONAL EXCELLENCE.

ON THE ROAD

STAY ONE STEP AHEAD

Get more at demandmore.lectra.com

26

AUTOMOTIVE NEWS EUROPE LATEST LAUNCHES

www.autonewseurope.com MARCH 2017

Nissan gave the Micra an athletic design to lure more male buyers.

Nissan plots Micra’s return to top 10Nissan wants to re-establish the Mi-

cra as one of the 10 top-sellers in Europe’s biggest and most competitive segment after its predecessor slipped to a disappointing No. 18. Nissan also wants the new Micra to account for 4 percent of European subcompact sales, which last year were a Europe-best 2.8 million, according to market researcher JATO Dynamics (see the 2016 segment by-segment report, Pages 39-42).

Nissan is confident it can achieve both tar-gets because the car’s slow-selling prede-cessor was aimed at global markets, while the fifth-generation Micra was conceived, designed and engineered with European car buyers’ requirements in mind.

“If you compromise too much you lose cus-tomers,” Laurent Lamotte, Nissan Europe’s marketing product manager for the Micra, said when comparing the old car with the new one. “We cover more of the customers’ needs in the segment with this car.”

One key was giving the Micra a diesel, which comes from alliance partner Re-nault, something the fourth-generation car lacked. Nissan estimates that 20 percent of subcompacts sold in Europe have a diesel, but without the pow-ertrain Lamotte said Nissan would be at a disadvantage against rivals such as the Ford Fiesta and Volkswagen Polo. He said that while Nissan is not in the same league as those two cars when it