author’s name 03-19-07 author’s name financial services fraud jonathan b. wolfe, cpa director,...

TRANSCRIPT

Author’s Name

03-19-07

Author’s Name

Financial Services Fraud

Jonathan B. Wolfe, CPA Director, Accume Partners

2

Agenda Overview

Definition of Operational Fraud Fraud Statistics

Fraud within Financial Services Banking, Insurance, Investment Advisors/Broker Dealers Risk Factors

What can an internal auditor do? Fraud Risk Assessment Employ Best Practices

Fraud Resources

3

Financial Services Fraud

Overview

4

Definition of Occupational Fraud

The term “Occupational Fraud” may be defined as:

“The use of one’s occupation for personal enrichment through the deliberate misuse or misapplication of the employing organization’s resources or assets.”

5

Definition of Occupational Fraud

All occupational fraud schemes have four key elements in common. The activity: is clandestine; violates the perpetrator’s fiduciary duties to the victim

organization; is committed for the purpose of direct or indirect financial

benefit to the perpetrator; and costs the employing organization assets, revenue, or

reserves.

6

Occupational Fraud

All occupational frauds fall into one of three major categories:

Asset Misappropriations, which involve the theft or misuse of an organization’s assets.

Corruption, in which fraudsters wrongfully use their influence in a business transaction in order to procure some benefit for themselves or another person, contrary to their duty to their employer or the rights of another.

Fraudulent Statements, which generally involve falsification of an organization’s financial statements.

7

Fraud Statistics Source: 2006 Association of Certified Fraud Examiners

(ACFE) Report to the Nation

10- The Sum of Percentage in this chart exceeds 100% because in some cases respondents identified more than one detection method.

8

Fraud Statistics Source: 2006 ACFE Report to the Nation

9

Fraud Statistics Source: 2006 ACFE Report to the Nation

Banking and Financial Services Industry has the highest number of cases

Insurance was ranked 5th.

10

Fraud Statistics Source: 2006 ACFE Report to the Nation

Accounting, Finance and Executives represents 55% of the cases.

While frauds committed by those in the highest age groups were the most costly on average, over two-thirds of the frauds reported were committed by employees in the 31-50 age group. The median age among perpetrators was 42.

Most of the perpetrators were either employees (41.2%) or managers (39.5%). Owner/executives (19.3%).

Where is it happening?

11

Fraud Statistics – Median Loss Source: 2006 ACFE Report to the Nation

12

Financial Services Fraud

Fraud Within Financial Services

13

Fraud Within Financial ServicesSource: 2006 ACFE Report to the Nation

Not surprisingly, two of the three most common schemes in the banking and financial services industry were cash larceny and skimming. These schemes generally involve the physical theft of incoming cash and cash on hand (for example, in a vault).

Among the 23 non-cash cases in this industry, the most common type of scheme involved the theft of proprietary information about bank customers.

Of the 148 cases, 80% were prosecuted.

Banking and Financial Services Fraud

14

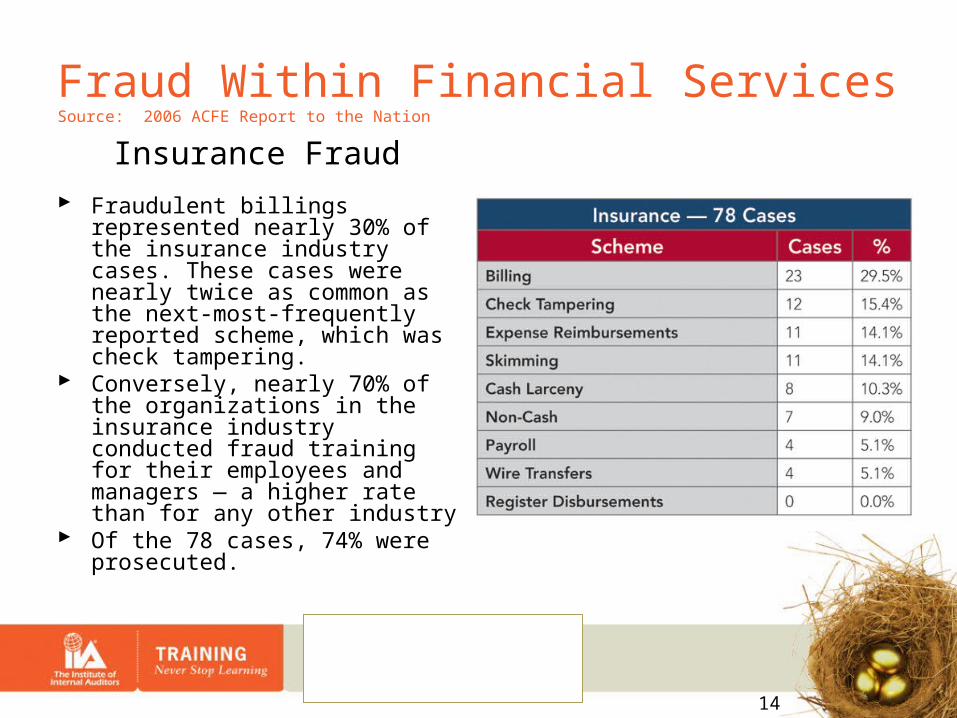

Fraud Within Financial ServicesSource: 2006 ACFE Report to the Nation

Fraudulent billings represented nearly 30% of the insurance industry cases. These cases were nearly twice as common as the next-most-frequently reported scheme, which was check tampering.

Conversely, nearly 70% of the organizations in the insurance industry conducted fraud training for their employees and managers — a higher rate than for any other industry

Of the 78 cases, 74% were prosecuted.

Insurance Fraud

15

Risk Factors

1. Incentives or pressures

2. Opportunities

3. Attitudes or rationalizations

16

Industry Fraud – Banking & Mortgage Banking

Notary Volume pressures – Loans, Deposits

Appraisers Artificially inflating home values

Check Fraud Participating financial institutions can report all checking accounts

"closed for cause" to a central database, called ChexSystems. This program prevents people, who have outstanding checks due to retailers, from opening new accounts.

Black Market Peso Peso brokers laundering monies through the purchase of foreign

goods.

17

Industry Fraud - Insurance Premium Fraud

Premium fraud occurs when employers fraudulently misstate the number of employees or the nature of their work, such as reporting a roofer as an office worker.

Billing Fraud Ohio pain management specialist threatened to deny desperate patients

painkillers unless they let him use their names to bill insurance companies more than $60 million in narcotic drugs and expensive diagnostic tests he never gave. Some patients grew addicted, and two died of overdoses. He also fraudulently billed insurers for more than 100 patients a day for years. He received life in federal prison.

Employer or Insurance Carrier Fraud In this type of fraud, employers or employees of an insurance carrier will

make a false statement regarding a workers entitlement to benefits. The statement is designed to discourage the worker from pursuing a legitimate claim

18

Industry Fraud – Investment Advisors and Broker Dealers Churning – Excessive Commission Scams

Discretionary Accounts 3% or more commissions Breakpoint Sales – Fee Scales

Over Concentration - brokers are obligated to advise their clients to diversify in order to decrease risk.

House Stocks - A "house stock" is essentially a stock that the firm wants people to buy in order to artificially increase its value.

Failure to Place an Order - broker is trying to inflate the value of a stock as part of an unethical investment scheme, it may be against his interests to sell the stock.

Unauthorized Trades - brokers who have had discretionary trading contracts with their clients may take advantage of their freedom and purchase "house stocks", or engage in other illicit trading practices designed to increase their earnings at the expense of their client.

19

Financial Services Fraud

What can an Internal Auditor do?

20

What can an Internal Auditor do?

Systematic Rather Than Haphazard or Informal Address

Financial reporting Misappropriation of assets Expenditures and liabilities for improper purposes Fraudulently obtained revenues and assets, and costs and expenses

avoided by fraud Fraud by senior management

Extend to Business Unit and Significant Account Levels Likelihood: Identify Fraud Risks That Are “More Than Remote” Significance: Identify Fraud Risks That Are “More Than

Inconsequential in Amount: Consider Risks of Management Override

Fraud Risk Assessment

21

What can an Internal Auditor do?

Develop a Fraud Policy Enhance Audit Programs Leverage your Sarbanes Oxley work Educate Audit Committee and Boards Evaluate Code of Ethics Provide annual training programs Integrate fraud monitoring into your enterprise risk management

program Implement a whistle blower policy Discuss SAS 99 with your external auditors Outside resources – CFEs, consultants Technology – ACL, data mining

Employ Best Practices

22

Does Internal Audit Make a Difference? YES! Source: 2006 ACFE Report to the Nation

Internal audits had a positive correlation with both time to detection and median loss. Fifty-nine percent of victim organizations had an internal audit or fraud examination department at the time of the fraud.

Similarly, organizations with internal audit departments detected their frauds in 18 months, as opposed to 24 months for those without internal audit departments.

23

Fraud Resources

The Institute of Internal Auditors www.theiia.com

Association of Certified Fraud Examiners www.cfenet.com

Securities and Exchange Commission www.sec.gov

The Treasury Department www.treas.gov

National White Collar Crime Center www.nw3c.org

24

Financial Services Fraud

Questions?