attachment 11 diamond analysis example

DESCRIPTION

ÂTRANSCRIPT

Attachment 11 Diamond Analysis: Benin Cashew Value Chain Example

1 | P a g e

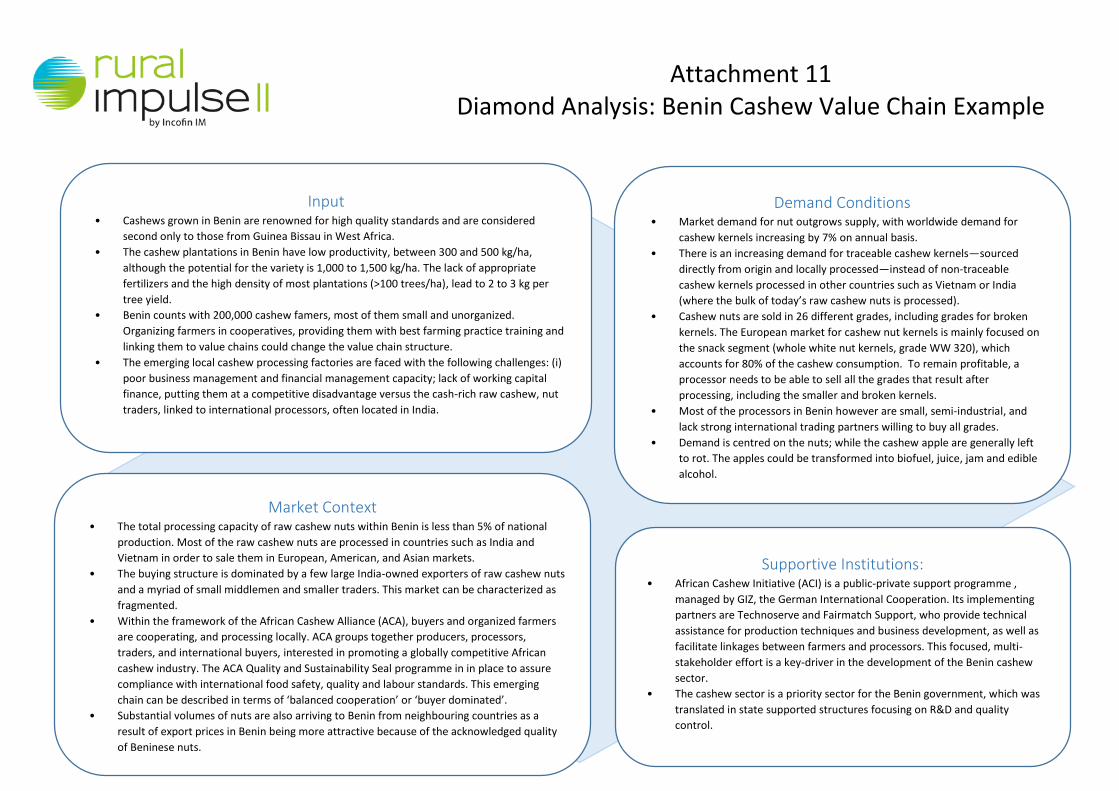

Demand Conditions • Market demand for nut outgrows supply, with worldwide demand for

cashew kernels increasing by 7% on annual basis.

• There is an increasing demand for traceable cashew kernels—sourced

directly from origin and locally processed—instead of non-traceable

cashew kernels processed in other countries such as Vietnam or India

(where the bulk of today’s raw cashew nuts is processed).

• Cashew nuts are sold in 26 different grades, including grades for broken

kernels. The European market for cashew nut kernels is mainly focused on

the snack segment (whole white nut kernels, grade WW 320), which

accounts for 80% of the cashew consumption. To remain profitable, a

processor needs to be able to sell all the grades that result after

processing, including the smaller and broken kernels.

• Most of the processors in Benin however are small, semi-industrial, and

lack strong international trading partners willing to buy all grades.

• Demand is centred on the nuts; while the cashew apple are generally left

to rot. The apples could be transformed into biofuel, juice, jam and edible

alcohol.

Input • Cashews grown in Benin are renowned for high quality standards and are considered

second only to those from Guinea Bissau in West Africa.

• The cashew plantations in Benin have low productivity, between 300 and 500 kg/ha,

although the potential for the variety is 1,000 to 1,500 kg/ha. The lack of appropriate

fertilizers and the high density of most plantations (>100 trees/ha), lead to 2 to 3 kg per

tree yield.

• Benin counts with 200,000 cashew famers, most of them small and unorganized.

Organizing farmers in cooperatives, providing them with best farming practice training and

linking them to value chains could change the value chain structure.

• The emerging local cashew processing factories are faced with the following challenges: (i)

poor business management and financial management capacity; lack of working capital

finance, putting them at a competitive disadvantage versus the cash-rich raw cashew, nut

traders, linked to international processors, often located in India.

Market Context • The total processing capacity of raw cashew nuts within Benin is less than 5% of national

production. Most of the raw cashew nuts are processed in countries such as India and

Vietnam in order to sale them in European, American, and Asian markets.

• The buying structure is dominated by a few large India-owned exporters of raw cashew nuts

and a myriad of small middlemen and smaller traders. This market can be characterized as

fragmented.

• Within the framework of the African Cashew Alliance (ACA), buyers and organized farmers

are cooperating, and processing locally. ACA groups together producers, processors,

traders, and international buyers, interested in promoting a globally competitive African

cashew industry. The ACA Quality and Sustainability Seal programme in in place to assure

compliance with international food safety, quality and labour standards. This emerging

chain can be described in terms of ‘balanced cooperation’ or ‘buyer dominated’.

• Substantial volumes of nuts are also arriving to Benin from neighbouring countries as a

result of export prices in Benin being more attractive because of the acknowledged quality

of Beninese nuts.

Supportive Institutions: • African Cashew Initiative (ACI) is a public-private support programme ,

managed by GIZ, the German International Cooperation. Its implementing

partners are Technoserve and Fairmatch Support, who provide technical

assistance for production techniques and business development, as well as

facilitate linkages between farmers and processors. This focused, multi-

stakeholder effort is a key-driver in the development of the Benin cashew

sector.

• The cashew sector is a priority sector for the Benin government, which was

translated in state supported structures focusing on R&D and quality

control.