asset tangibility and cash holdings (2015 fma) · asset tangibility and cash holdings ... spectrum...

TRANSCRIPT

Asset Tangibility and Cash Holdings

Current Version: January 15, 2015

Abstract The paper underscores the role of financial development in shaping corporate financing policy through a collateral channel, providing cross-country evidence that asset tangibility significantly affects corporate cash holdings negatively. This paper shows that firms in countries with higher levels of financial development exhibit less sensitivity of cash holdings to asset tangibility, which suggests that the collateral role of tangible assets is substituted by higher-standard financial institutions, proxied by creditor rights protection and information sharing among creditors. The results imply that the development of financial markets and institutions helps lower borrowing costs and mitigate corporate financial constraints and precautionary savings concerns, thereby promoting corporate investments and economic growth. This study confirms the view that risky firms tend to pledge more tangible collateral and the collateral spread declines with improvements in the quality of institutions. The study also shows that asset salability enhances the collateral role of tangible assets.

Asset Tangibility and Cash Holdings

Abstract

The paper underscores the role of financial development in shaping corporate financing policy through a collateral channel, providing cross-country evidence that asset tangibility significantly affects corporate cash holdings negatively. This paper shows that firms in countries with higher levels of financial development exhibit less sensitivity of cash holdings to asset tangibility, which suggests that the collateral role of tangible assets is substituted by higher-standard financial institutions, proxied by creditor rights protection and information sharing among creditors. The results imply that the development of financial markets and institutions helps lower borrowing costs and mitigate corporate financial constraints and precautionary savings concerns, thereby promoting corporate investments and economic growth. This study confirms the view that risky firms tend to pledge more tangible collateral and the collateral spread declines with improvements in the quality of institutions. The study also shows that asset salability enhances the collateral role of tangible assets.

JEL Classifications Numbers: G32, G21, G33, O16 Keywords: Asset Tangibility; Cash Holdings; Financial Development; Asset Redeployability

1

1. Introduction

Considerable attention has been paid to the record-high cash holdings of U.S. firms. For

instance, Bates, Kahle, and Stulz (2009) document that the average cash-to-assets ratio of U.S.

firms more than doubles from 10.5% in 1980 to 23.2% in 2006. The Wall Street Journal

stated in June 2010, “Nonfinancial companies had socked away $1.84 trillion in cash and

other liquid assets as of the end of March, up 26% from a year earlier and the largest-ever

increase in records going back to 1952. Cash made up about 7% of all company assets, the

highest level since 1963.”1 Prior work on determinants of cash holdings suggests that firms

accrue cash for various reasons such as the transaction cost motive, the precautionary motive,

the repatriation tax motive, and the managerial agency cost motive.2

Bates, Kahle, and Stulz (2009) also find that the average cash ratio of high-tech firms is

significantly greater than the average cash ratio of manufacturing firms. This evidence

provides empirical support for the precautionary motives that drive firms, for example, in

computers, electrical equipment, and pharmaceutical sectors, to sit on huge amounts of

unspent corporate cash. One reason is that these firms may be concerned about potential

difficulties in continuously funding their costly on-going R&D projects (Brown and Petersen,

2011) and they often face higher financing and refinancing costs due to the lack of sufficient

tangible assets pledged as collateral for loans.

While asset tangibility is a major factor in determining capital structure,3 much less

attention has been directed to understanding the collateral channel through which asset

1 Justin Lahart, “U.S. Firms Build Up Record Cash Piles,” The Wall Street Journal, June 10, 2010. 2 Studies by Kim, Mauer, and Sherman (1998), and Opler, Pinkowitz, Stulz, and Williamson (1999) show the pecking order and trade-off models of benefits and costs of cash holdings, and report that firm characteristics such as firm size, growth opportunities, and volatility of future cash flows determine the optimal investment in liquidity in the presence of capital market frictions. Almeida, Campello, and Weisbach (2011) present a model of inter-temporal investment decisions with costs of external financing and show that firms hold more cash today if they anticipate tighter financing constraints in the future. Bates, Kahle, and Stulz (2009) conduct an excellent review of the literature on cash holdings. 3 See, e.g., Kiyotaki and Moore (1997), Campello and Giambona (2013), and Rampini and Viswanathan (2013) for the positive link between fixed assets and leverage, and Rajan and Zingales (1995) for some international evidence on the interplay between asset tangibility and capital structure.

2

tangibility affects corporate cash holding policy.4 This paper attempts to fill this gap in the

cash holding literature by exploring in detail the association between asset tangibility and

cash holdings. The argument is that since tangible assets can be used as collateral to alleviate

firms’ financial constraints by reducing borrowing costs, firms with low asset tangibility tend

to hold more cash from a precautionary motive standpoint.

To motivate the argument, I first present time-series evidence from U.S. data as a point

of departure. The reason is that a large body of literature on cash holdings has been devoted

to explaining the evolution of cash holdings for U.S. firms over the past three decades (see,

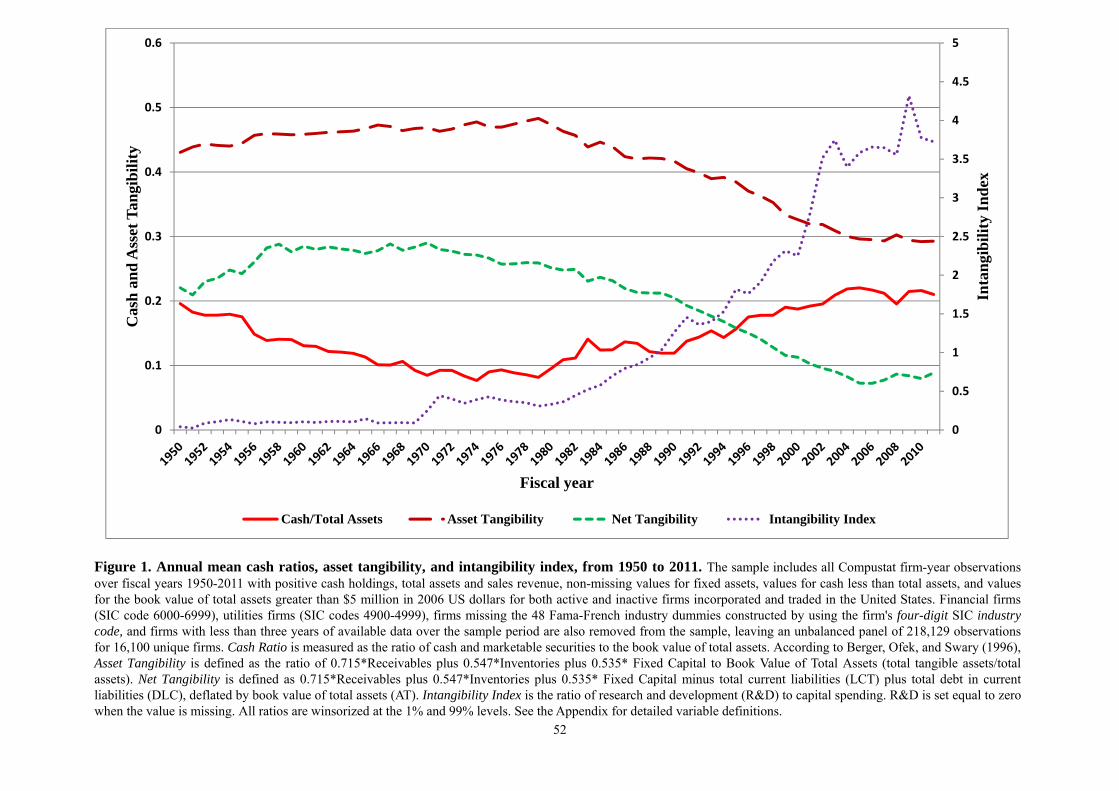

e.g., Opler, Pinkowitz, Stulz, and Williamson, 1999; Bates, Kahle, and Stulz, 2009). Figure 1

depicts two important stylized facts about the evolution of annual mean cash-to-assets ratio

and asset tangibility along with net tangibility and intangibility index over fiscal years 1950-

2011 from U.S. data.5

[Figure 1 about here]

First, Figure 1 reveals that not only cash holdings have not been increasing dramatically

until late 1970s, but both asset tangibility and net tangibility take on an almost reverse trend

against cash over the whole sample period, a pattern that has not been documented in the cash

holdings literature. To put it into perspective, in contrast to cash holdings, asset tangibility has

been plummeting since the early 1980s, representing merely 29.3% of the total assets in fiscal

year 2011, a 38.2% drop from 47.3% in 1980. A plausible explanation for this trend is that the

4 John (1993) shows that the liquidity ratio, measured as the ratio of cash and marketable securities to total assets, is decreasing in the ratio of inventory plus gross plant and equipment to total assets, a proxy for the liquidity costs of asset restructuring (the collateral value of the assets) suggested by Titman and Wessels (1988). Klasa, Maxwell, and Ortiz-Molina (2009) also consider the tangibility of a firm’s assets, measured as the ratio of net property, plant, and equipment to book assets, as a determinant of its cash holdings. 5 Throughout the paper, I measure the degree of asset tangibility by using the ratio of 0.715*Receivables plus 0.547*Inventories plus 0.535*Fixed Capital to Book Value of Total Assets, which is developed in Berger, Ofek, and Swary (1996). Net tangibility is calculated as 0.715*Receivables plus 0.547*Inventories plus 0.535*Fixed Capital minus total current liabilities (LCT) and plus total debt in current liabilities (DLC), deflated by book assets. Intangibility index is the ratio of research and development (R&D) to capital spending.

3

reduction in asset tangibility lowers the overall collateralizable value of firms’ assets, and

therefore reduces the availability of external debt finance. Consequently, firms, especially

those that are prone to being financially constrained, tend to stockpile large amounts of cash

to reduce potential borrowing costs, consistent with the precautionary motive for cash

holdings.

Second, the figure also illustrates another important fact. Specifically, the growth rate

of asset intangibility index (a flow measure) starts to accelerate around early 1980s, about the

same period when cash holdings start to increase. The mean capital input ratio between

intangible assets and tangible assets has been sharply rising to 3.72 in fiscal year 2011, more

than 10 times from 0.33 in 1980. As firms pour more funds in intangibles, the increasingly

intensified precautionary demand for cash plays a more critical role than before. This stylized

fact resonates with the rapid development and innovation in technology across the entire

spectrum of firms over the past three decades.

Undertaking a standard regression approach similar to the Tables III and V of Bates,

Kahle, and Stulz (2009), I show in unreported tables that 1) asset tangibility affects corporate

cash holdings negatively, which is robust to OLS regressions using variables in levels and

changes, Fama-MacBeth regressions, and specifications with firm fixed effects; and 2) asset

tangibility is the most important determinant of cash holdings in explaining the recent

dramatic increase in cash holdings in the U.S over the 2000s among a host of well-known

determinants such as industry sigma and cash flow documented in the literature.

After showing a negative link between cash and asset tangibility using U.S. data, I

further identify the collateral channel in a cross-country setting. The identification strategy is

motivated by a recent paper by Liberti and Mian (2010) who explore how the level of

financial development in a country affects the collateral cost of capital. Specifically, they

show that institutions such as creditor rights and information sharing that reflect/promote

4

financial development alleviate borrowing constraints by lowering the difference in

collateralization rates between high- and low-risk borrowers. They also document that firms

in better financially developed countries pledge a less amount and a wider range of assets

including firm-specific assets as collateral. Therefore, these findings imply that the

collateralization rates vary inversely with the quality of institutions. It further suggests that

the sensitivity of cash to asset tangibility should be smaller in countries with better

institutions.

Specifically, I exploit the cross-country variation in a country’s characteristics such as

financial development to identify the collateral channel through which asset tangibility affects

cash holdings around the world. To this end, I proceed with a cross-country analysis by

collecting data on a commonly-used proxy for financial development (the value of credits by

financial intermediaries to the private sector, divided by GDP) from Beck and Demirgüç-

Kunt (2009), and data on cash holdings and asset tangibility from Compustat for fiscal years

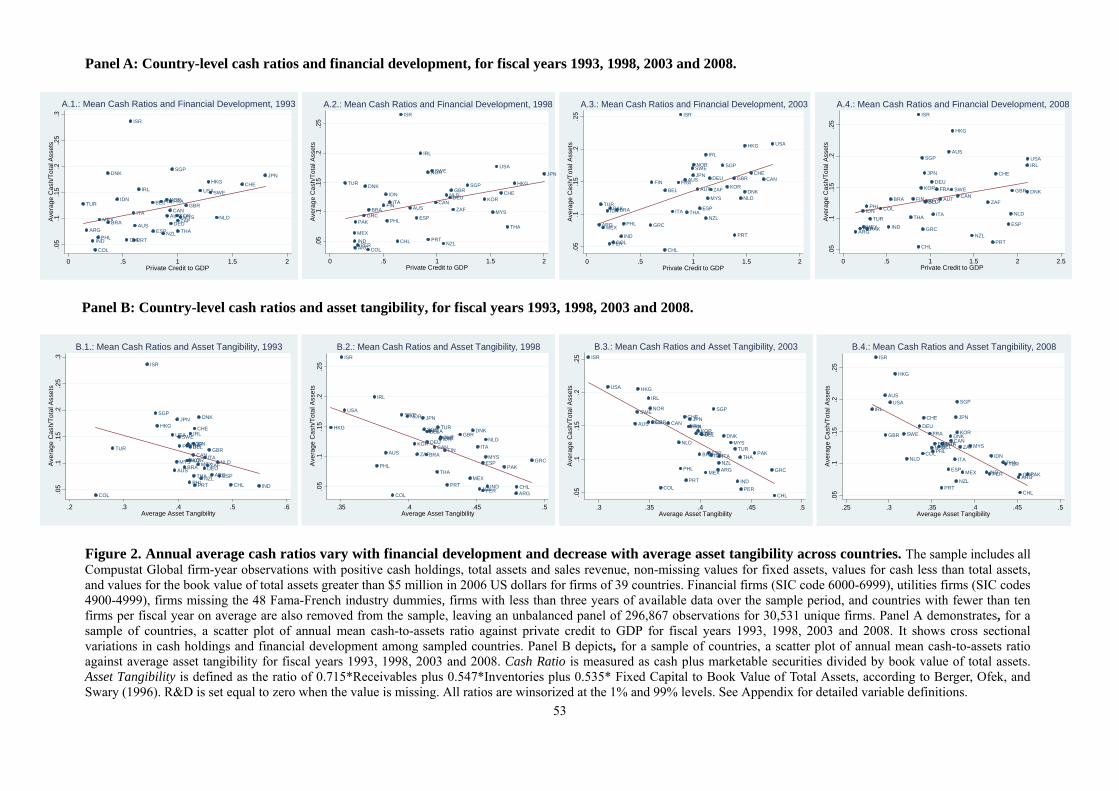

1993, 1998, 2003, and 2008 across 39 countries.

Panel A of Figure 2 plots the annual average cash-to-assets ratio against private credit

to GDP for fiscal years 1993, 1998, 2003 and 2008. Panel B plots the average asset tangibility

on the horizontal axis. Two facts stand out from Figure 2: (Fact 1) there exist significant

cross-national variations in cash holdings and financial development, as well as a slight

positive association between the two over time in Panel A.6 (Fact 2) the cross-sectional

average of cash holdings are decreasing in asset tangibility across countries and the

relationship has persisted throughout the sample period, as demonstrated in Panel B.

[Figure 2 about here]

6 Studies that positively link financial development (measured by private credit to GDP) and cash holdings in a cross-country setting include Dittmar, Mahrt-Smith, and Servaes (2003) and Kalcheva and Lins (2007). Khurana, Martin, and Pereira (2006) document that the sensitivity of cash holdings to cash flows decreases with financial development.

5

The work of Liberti and Mian (2010) is related to a large body of literature in law and

finance that has documented an important relationship between a country’s legal system and

the development of its financial markets. Prior work in this strand of literature by La Porta,

Lopez-de-Silanes, Shleifer, and Vishny (1997, 1998; henceforth LLSV) shed light on the

critical role of financial development as well as legal and institutional environment in

reducing the costs of collateral evaluation, processing, and liquidation.7 Importantly, LLSV

(1998) explore the role of two financial market mechanisms in economic development. They

conclude that both creditor rights and information sharing help promote capital market

development, which in turn contributes to economic growth.

The first mechanism is creditor’s rights, which refers to the contracting environment

between borrowers and lenders and the protection of creditors’ ability to collect the money

from borrowers defaulting on a debt obligation. A strand of literature on creditor rights

documents that strong creditor protection promotes credit market development (e.g., Djankov,

McLiesh, and Shleifer, 2007; Haselmann, Pistor, and Vig, 2010). In line with this view,

several studies also show that loans under strong creditor protection have lower interest rates,

lower contracting costs of financing, and favorable terms (Qian and Strahan, 2007). Stronger

creditor rights also reduce interest rate spread on loans to borrowers (Bae and Goyal, 2009).

Therefore, lenders (creditors) are willing to extend credit and take risk when they are less

exposed to borrower (debtors) expropriation, resulting in borrowing firms having more

external finance. The collateralization of loans is also lower in financially developed markets.

Moreover, LLSV (1998) construct an index aggregating the rights of secured lenders

based on restriction on reorganization, no automatic stay, no management stay, and secured

debt paid first. They show that countries with stronger legal protection of creditors have

7 In a similar spirit, Rajan and Zingales (1998) find that financial-sector development proxied by private credit to GDP, stock market capitalization, and accounting standards reduces the costs of external finance to firms.

6

deeper credit markets and that creditor rights act as a substitute for collateral in mature

markets.8 For example, restrictions on reorganization such as creditors’ consent or minimum

dividend are imposed when a debtor decides to file for reorganization. This restriction

decreases the likelihood that debtors use bankruptcy as a strategic way of avoiding debt.

Similarly, the “no automatic stay” or asset freeze imposed by the court protects creditor’s

ability to seize collateral after the petition for reorganization is approved. Finally, the “no

management stay” provides powers to an administrator rather than the incumbent

management that is in control of property pending and responsible for running the business

during the reorganization. Therefore, creditor rights weaken the role of tangible assets as

collateral for secured credit in restricting debtors from risk-taking and risk-shifting. I expect

that creditor rights protection should attenuate the cash-tangibility sensitivity.

The second mechanism that LLSV (1998) discuss is public and private information

sharing among lenders about the creditworthiness of loan applicants. Information sharing

attenuates adverse selection and moral hazard and therefore facilitates lending. A stream of

studies on creditor information sharing further shows that information exchange improves

credit availability (Pagano and Jappelli, 1993; Padilla and Pagano, 1997, 2000), lowers the

cost of credit to firms (Brown, Jappelli, and Pagano, 2009), motivates loan repayments

(Brown and Zehnder, 2007), and reduces default rates (Jappelli and Pagano, 2002).

In addition, bank lending literature suggests that collateral may be required simply to

reduce information asymmetry because lenders can obtain additional information about the

borrower by evaluating the quality and nature of the collateral (e.g., Picker, 1992) and assess

the borrower’s repayment prospects. Therefore, collateral-based lending is typically used to

provide credit availability in the opaque information environment of an emerging market

where information sharing and financial transparency are not available or extremely limited.

8 This is consistent with power theories of credit, based on the transfer of control rights upon default (Aghion and Bolton, 1992; Hart and Moore, 1998).

7

However, the improvement in the quality of creditor information through informational

infrastructure such as information sharing eliminates asymmetric information between

lenders and borrowers. Consequently, it directly decreases creditors’ effort and costs of

screening firms and encourages lenders to make use of substitutes for physical collateral to

provide credits. For example, the alternative types of loans may include unsecured loans or

loans secured by reputation collateral or restrictive covenants which limit borrowing firms’

actions prior to default and therefore provide ex ante protection for creditors, as argued by

Miller and Reisel (2012). Therefore, the role of collateral stipulated in the debt contract

becomes less significant in countries with credit information sharing systems through public

credit registries and private credit bureaus. I expect that information sharing should also

attenuate the cash-tangibility sensitivity.

The main results confirm the expectation that both creditor rights and information

sharing independently weaken the impact of asset tangibility on cash holdings after

controlling for the effects of economic development. Specifically, I estimate regressions that

include the interaction effects of asset tangibility with proxies for financial development

while also controlling for the interaction of asset tangibility with the log of gross domestic

product (GDP) per capita, along with country, industry, and time fixed effects. The main

results are robust to alternative measures of financial development, including weighted least

squares regressions where each country receives equal weight in the estimation, and

subsamples excluding the U.S. and Japan.

Having shown that creditor right protection substitutes for collateral, lowers the

importance of tangible assets in reducing a firm’s financial constraint, and hence reduces the

cash-tangibility sensitivity, I turn to further investigate whether the differences in laws and

enforceability of contracts also matter for the effect of creditor right protection on the cash-

tangibility sensitivity. This approach is motivated by Bae and Goyal (2009). I show that both

8

the existence of creditor rights per se and the quality of their legal enforcement are important

to the contracting and bank-lending process. I use four proxies including contract

enforcement speed and cost, legal formalism, and judicial efficiency for law enforcement of

the creditors’ rights to further identify the channel through which creditor rights substitute for

tangible assets as collateral.

The economic intuition is that strong legal protection that better ensures creditors to

repossess collateral impose a credible threat and greater costs upon a borrower in the case of

default. As a result, borrowers would be less willing to take on extra risk.9 Therefore I

anticipate that the expected realized value of collateral would increase with creditor

protection. It then follows that stronger (weaker) legal enforcement of creditors’ rights makes

creditor rights more (less) effective, leading to a more (less) pronounced attenuating effect of

creditor rights on the cash-tangibility sensitivity.

Having shown the attenuating impact of information sharing on the cash-tangibility

sensitivity, I next turn to further explore how the effect of information sharing on cash-

tangibility sensitivity varies with the opacity of a company. To this aim, I split the sample

according to firm characteristics – age, size, and growth opportunities. The estimates suggest

that only young, small, and high-growth firms, which arguably suffer most from financial

market imperfections such as asymmetric information and hence financial constraints, benefit

most from the establishment of information sharing. This result implies that information

sharing reduces the role of tangible assets as collateral and loosens the borrowing constraints

of informationally opaque firms. Hence, it provides additional support for the argument that

creditor information sharing substitutes for collateral in countries with high transparency of

credit markets.

9 Supporting to the view that borrowers are less willing to take risks when creditors are better protected, Acharya, Amihud, and Litov (2011) find international evidence that stronger creditor rights tend to reduce corporate risk taking. The right to repossess collateral gives lenders an essential threat to ensure that borrowers will not use the money borrowed unproductively.

9

The results also complement the findings of Liberti and Mian (2010). Specifically, I

relate the average collateral spread, proxied by the differential cash-tangibility sensitivity

between high- and low-risk borrowers, to improvements in the quality of institutions. I first

show that firms with higher ex ante credit risk or default probability tend to have lower cash-

tangibility sensitivity. This implies that in order to obtain the same dollar worth of secured

loans, high default risk firms have to post more tangible assets as non-cash collateral. These

results are in line with the sorting-by-observed-risk paradigm which claims that observably

risky low quality borrowers are required to pledge collateral while observably safe borrowers

are not required or pledge less (e.g. Berger and Udell, 1990). More importantly, I demonstrate

that the differential cash-tangibility sensitivity between high- and low-risk borrowers declines

with improvements in the quality of institutions. This finding suggests that financial

development closes the wedge in collateralization rates between high- and low-risk

borrowers.

Finally, this paper is also closely related to the asset salability literature (Shleifer and

Vishny, 1992; Berger, Ofek, and Swary, 1996; Stromberg, 2001; Acharya, Bharath, and

Srinivasan, 2007; Benmelech, 2009; Campello and Giambona, 2013). Using three industry-

level measures of asset salability (industry competitiveness, industry asset non-specificity,

and industry liquidity), I first identify the cash-tangibility link through the effect of changes

in the liquidation values of redeployable tangible assets on liquidity management after

controlling for both institutional and economic impact. I show that higher industry-level

salability enlarges the negative impact of asset tangibility on cash holdings. The result is in

accordance with the argument in asset salability literature that the combination of the effects

of physical attributes of an asset and the sheer number and financial strength of its potential

buyers in the secondary market determines liquidation values of assets. I further show that

country-level salability, proxied by log of GDP per Capita, strengthens the industry-level

10

salability effect on the cash-tangibility sensitivity. The argument is that tangible assets are

more salable in countries with more economic activities (i.e., higher GDP per capita).10

Intuitively, an economic boom spurs firms’ investments and leads to high demand for

collateralizable tangible assets in the secondary market. It becomes faster and easier for

economic agents to trade financial instruments in asset markets. This then causes a surge in

the salability of tangible assets. Consequently, the liquidation value of the collateralizable

tangible assets rises. Overall, the results support the findings of Benmelech (2009) and

Campello and Giambona (2013) and complement their work by providing some new cross-

country evidence of the effects of asset tangibility on collateral value for lenders.

This paper contributes to the cash holding literature. I show that asset tangibility

explains the evolution of firms’ cash holdings across countries as a major neglected

determinant of cash holdings. In addition, to the best of my knowledge, this paper is the first

to explore how financial development affects a firm’s cash-tangibility sensitivity. This paper

contributes to the growing literature on the role of institutions in corporate finance by

analyzing their importance in improving firms’ access to external financing and shaping

corporate cash holdings across a large number of countries. Specifically, I argue and provide

evidence that both creditor rights and creditor information sharing substitute the collateral

role of tangible assets and exert attenuating effects on the negative cash-tangibility sensitivity,

but for different reasons. Creditor rights are an effective means for imposing disciplinary

restrictions on a borrowing firm’s action, especially when creditor rights are well enforced by

laws. In contrast, information sharing helps lenders easily gather accurate and timely

information about borrowers while appraising the loans. It assists lenders to provide credit to

financially constrained firms such as small technology firms that previously suffered from

10 Campello and Giambona (2013) show that the relationship between leverage and tangible assets is stronger when federal funds rate is higher, suggesting that redeployability is more important during credit contractions. Because higher FED funds rate is typically associated with economic booms, my arguments are consistent with theirs.

11

information asymmetry. Overall, with better institutions, firms have easy and multiple access

to extensions of credit from the financial system. Therefore, both creditor rights and

information sharing help promote capital market development and effectively allocate

economic resources, which in turn contributes to economic growth. These findings suggest

that the development of financial markets and institutions is a critical part of the growth

process. It is not simply an inconsequential side show that the financial system responds

automatically to demands for financial arrangements created by economic development

(Levine, 1997).

The paper proceeds as follows. Section 2 discusses the related literature and develops

hypotheses. Section 3 briefly describes the cross-country data and econometric framework.

Section 4 reports empirical evidence on the negative link between cash holdings and asset

tangibility and how institutional variables as well as industry- and country-level factors that

determine asset salability identify the link. Section 5 offers conclusions. Appendix contains

detailed definitions and sources of variables used in the study.

2. Hypothesis Development

2.1 Asset Tangibility and Cash Holdings

Economic theory and empirics suggest that collateral is commonly used in loan contracts to

reduce credit risks through decreasing expected default rates and increasing expected

recovery rates. There are two main functions of collateral.

The first is the disciplinary role of collateral. Collateral requirements provide secured

lenders the right to repossess collateral conditional on default. Therefore, collateral can be

used by lenders to restrict borrowers from asset substitution (Jensen and Meckling, 1976).

The second is the informational role of collateral. Lenders can obtain additional

information about the borrower by evaluating the quality and nature of the collateral (Picker,

12

1992) and assess the borrower’s repayment prospects. Moreover, collateral allows lenders to

sort observationally equivalent loan applicants through signaling and help attenuate the

problems of adverse selection and credit rationing (Besanko and Thakor, 1987a, 1987b;

Stiglitz and Weiss, 1981). It also reduces moral hazard by aligning the interests of both

lenders and borrowers (Boot, Thakor, and Udell, 1991; Holmstrom and Tirole, 1997).

Tangible assets can serve as collateral in secured lending. Therefore, asset tangibility

increases the recovery value for lenders in default states and is positively linked to the ease

with which borrowers can obtain external financing. For example, the recent work of

Campello and Giambona (2013) shows that redeployability of tangible assets is a main

determinant of corporate leverage.

Therefore, I hypothesize that when a firm's borrowing capacity from its existing asset

base increases with asset tangibility, the firm tends to have lower precautionary demand for

holding cash. I propose and empirically test the following hypothesis in alternative form:

HYPOTHESIS 1: Firms with higher asset tangibility face lower borrowing costs, and therefore

should hold lower levels of cash holdings from a precautionary standpoint,

ceteris paribus.

2.2 The Effects of Institutional Variables on Cash-Tangibility Sensitivity

Financial development reduces firms’ reliance on tangible assets as collateral in corporate

borrowing and therefore decreases the precautionary motive of cash savings through the

collateral channel. There has been a rich literature focusing on the determinants of financial

development and the potential role played by both financial intermediaries and markets in the

process of economic growth and development (see Levine (2005) for a useful survey).

Arguing for the benefits of financial development, financial sectors improve efficiency

13

in financial resource allocation in the economy (Boyd and Prescott, 1986), facilitate trading

and hedging in stock markets (Holmstrom and Tirole, 1993), lower liquidity risk (Diamond

and Dybvig, 1983), ameliorate information asymmetries, and hence reduce contract

enforcement costs, transactions frictions, and costs of external finance (Rajan and Zingales,

1998).11 Therefore, I anticipate that with deep capital markets, firms can take advantage of

easy and costless access to extensions of credit from the financial system. The collateral role

of tangible assets becomes less significant.

The law and finance literature also suggests that better legal systems foster the

protection of creditors and shareholders legal rights, reduce contracting costs, and improve

information infrastructure, such as public registries or private credit bureaus for sharing credit

information across financial institutions. Better institutions therefore reinforce the liquidity

provision by financial intermediaries.

The strength of creditor rights affects the contracting environment constituting an

essential ingredient of financial development. For example, LLSV (1997) show that countries

with stronger legal protection of creditors have deeper credit markets and that creditor

protection acts as a substitute for collateral in mature markets.

Creditors also provide finance to firms largely because the law protects their rights

(LLSV, 1998). When creditors have more bargaining power (such as being able to take

control of a firm in bankruptcy), they are more willing to grant credit on favorable terms

(such as longer maturities and lower interest rates). Thus, stronger creditor rights should

result in an environment in which firms are relatively less financially constrained because

there would be less credit rationing and lower costs of external finance.

Creditor rights protection also has a number of important influences on lender’s and

11 Financial development, however, does come with costs. Excessive financial liberalization may result in an unduly large expansion of credit to risky firms with unviable projects and limited monitoring of regulatory agencies (Aghion, Bacchetta, and Banerjee (2004)).

14

borrower’s risk incentives. Better creditors’ rights over the collateral stipulated in the debt

contract will make it easier for secured creditors to seize and liquidate assets in the event of

bankruptcy. Therefore the power of secured lenders in bankruptcy is likely to have effects on

over-borrowing, effective use of borrowed funds, the likelihood of bankruptcy including

strategic bankruptcy, and the recovery rates in bankruptcy.

Along these lines, Liberti and Mian (2010) argue that because both the expected

realized value of collateral and the expected costs on a borrower for default or any deviations

from the agreed upon contract increase with creditor protection, lenders can afford to reduce

collateral spread in stronger legal regimes. Moreover, creditor rights protection reduces

borrowers’ credit risks and restricts borrowers from strategic defaults, risk-taking (Acharya,

Amihud, and Litov, 2011) and risk-shifting.

These argument and findings are consistent with the view that creditor rights serve as a

substitute for asset tangibility. In other words, creditors in poor creditor protection countries

require more collateral to ensure smaller potential losses when they make loans.

In financially developed countries where information sharing among creditors is

available, lenders have a good knowledge of borrowers’ characteristics, past behavior, current

debt exposure, and possible subsequent indebtedness. Therefore, credit information sharing is

expected to reduce moral hazard and adverse selection in credit markets which can lead to

credit rationing and underinvestment (Pagano and Jappelli, 1993). Credit information sharing

also increases borrowers’ incentives to repay their debts as a strong disciplining device

because information about defaults becomes available to all lenders (Padilla and Pagano,

2000; Brown and Zehnder, 2007; Hertzberg, Liberti, and Paravisini, 2010), and reduces over-

borrowing and default rates (Jappelli and Pagano, 2002; Brown, Jappelli, and Pagano, 2009;

Bennardo, Pagano, and Piccolo, 2014).

Arguably, creditors in countries with greater information sharing are more likely to

15

exploit soft information obtained from other creditors so as to accept alternative intangible

collateral such as patents, trademarks, and borrower’s reputation and credit scores. Creditor

information sharing enables lenders to switch loan contracts from using collateral based

lending technologies to using other softer lending technologies such as restrictive financial

covenants which specify operating performance, balance sheet ratios, and limits to which the

borrower must adhere and hence provide ex ante protection on creditors prior to default.

Lenders may also underwrite unsecured loans using soft information on risk of

borrower default, credit worthiness, current and future earnings prospects, etc., to opaque

technology companies. Therefore, information sharing also substitutes the role of tangible

assets as collateral in providing useful hard information about borrowers. Hence it reduces

moral hazard and adverse selection as well as raising the discipline on borrowers. The second

hypothesis is:

HYPOTHESIS 2: The negative effect of asset tangibility on cash holdings is attenuated for firms

operating in countries with higher-standard financial institutions, ceteris

paribus; the disciplinary role of tangible assets in loan contracts is

substituted by creditor right protection and the informational role of tangible

assets is replaced by information sharing among creditors through

alternative softer lending instruments.

2.3 The Effects of Changes in Asset Salability on Cash-Tangibility Sensitivity

With liquid capital markets, firms have easy access to extensions of credit from the financial

system and can easily redeploy their tangible assets at low costs. Benmelech (2009) uses the

term “salability” to describe how the combination of the effects of physical attributes of an

asset and the sheer number and financial strength of its potential buyers in the secondary

16

market determine liquidation values. Therefore, tangible assets are more salable in industries

with more financially strong buyers and transferable tangible assets.

In addition, firms tend to supply more tangible assets that are desirable to creditors in

order to get favorable terms (e.g. low interest rates and long maturities on loans) if their

tangible assets are more redeployable. Since asset salability is determined jointly by the

redeployability of tangible assets and the liquidity of market for assets, firms can more easily

redeploy their tangible assets at low costs in countries with more economic activity (i.e.,

higher GDP per capita).

Intuitively, during economic booms, the profitability of capital and demand for funds is

high and firms also tend to invest a lot. The rise of investment and demand for assets by firms

is associated with high asset liquidity. Tangible assets are more salable. Therefore, it implies

that economic development complements for the role of redeployable tangible collateral,

thereby strengthening the cash-tangibility sensitivity. Economic agents are then less

concerned about possible restrictions on future access to capital markets.

Specifically, I investigate the second approach for identifying the cash-tangibility link

through the effect of changes in the liquidation values of redeployable tangible assets on

liquidity management by exploiting the heterogeneity in industry and economic

characteristics across countries. The third hypothesis is:

HYPOTHESIS 3: The negative effect of asset tangibility on cash holdings is larger for firms

operating in markets with higher asset salability, ceteris paribus; the

liquidation value of tangible assets is positively associated with asset

salability.

17

3. Data and Empirical Methods

This section presents the properties of the data and methods I use for empirically identifying

and evaluating the proposed collateral channel through which asset tangibility affects

corporate cash holdings.

3.1. Sample and Variable Construction

I draw firm-level data for U.S. and non-U.S. firms from the Compustat North America and

Compustat Global Fundamentals Annual database for the period 1989-2009. These data

include active and inactive firms that appear on Compustat at any time in the sample period. I

remove the following sets of firms from the sample: 1) financial firms (SIC code 6000-6999)

and utility firms (SIC codes 4900-4999); 2) firms missing the 48 Fama-French industry

dummies constructed by using the firm's four-digit SIC industry code; 3) firms that cross-list

in other markets of the world; 4) firms that do not prepare consolidated financial statements;

5) firms that have less than three years of available data over the study period; 6) firms for

which cash and equivalents, asset tangibility, and/or total assets are missing; and 7) all firm-

year observations with negative cash holdings, total assets and sales revenue, values for cash

less than total assets, and values for the book value of total assets less than $5 million,

inflation-adjusted in 2006 U.S. dollars. Finally, I further exclude countries with less than ten

firms per fiscal year on average. The remaining sample consists of 29,130 unique firms

representing 235,089 firm-year observations from 39 countries.

In this study, the dependent variable is the cash and equivalents divided by the book

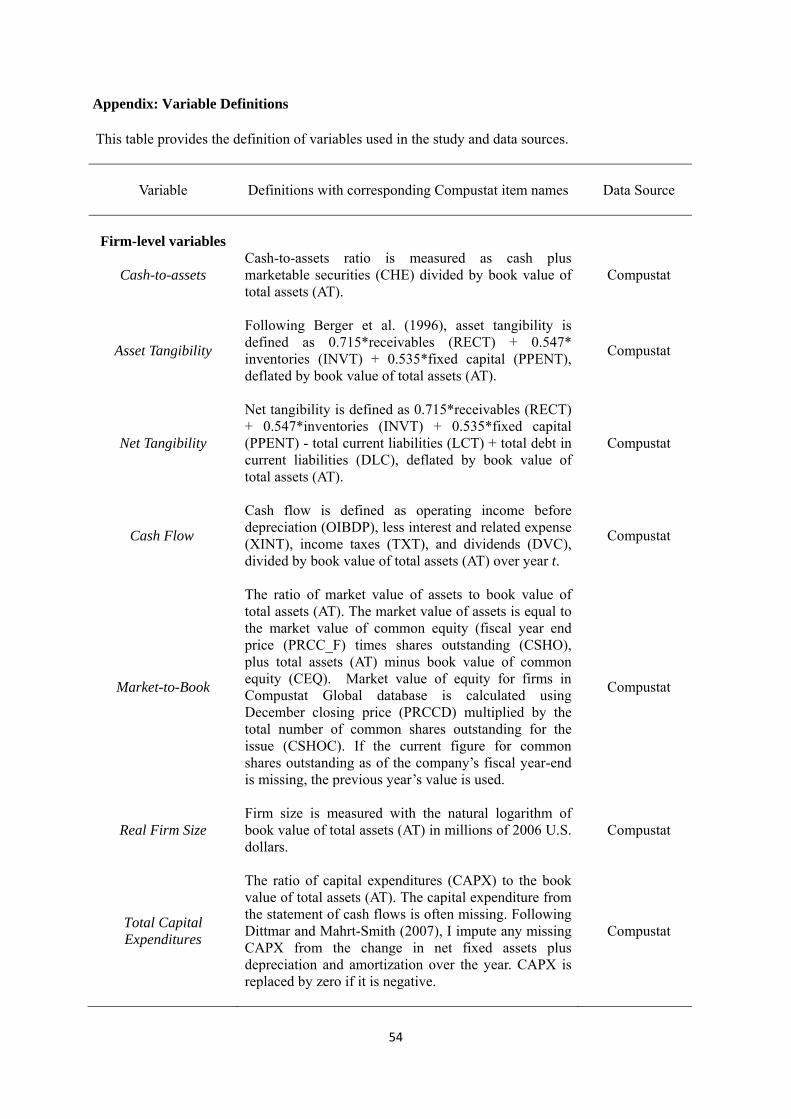

value of total assets. The baseline proxy for firm-level asset tangibility is computed using the

liquidation values of firm assets in discontinued operations and asset fire sales contained in

Berger, Ofek, and Swary (1996). Asset tangibility is defined as 0.715*receivables plus

0.547*inventories plus 0.535*fixed capital, deflated by book value of total assets. The proxy

measures the expected liquidation (resale) value of firms’ main categories of operating assets

18

such as fixed assets, accounts receivable, and inventories. Higher asset tangibility implies

higher asset redeployability and liquidity, and hence higher recover/exit value for creditors.

In addition, this measure allows us to examine how changes in fixed assets along with

changes in account receivables (or net of payables) and inventories explain the evolution of

cash holdings across the world.

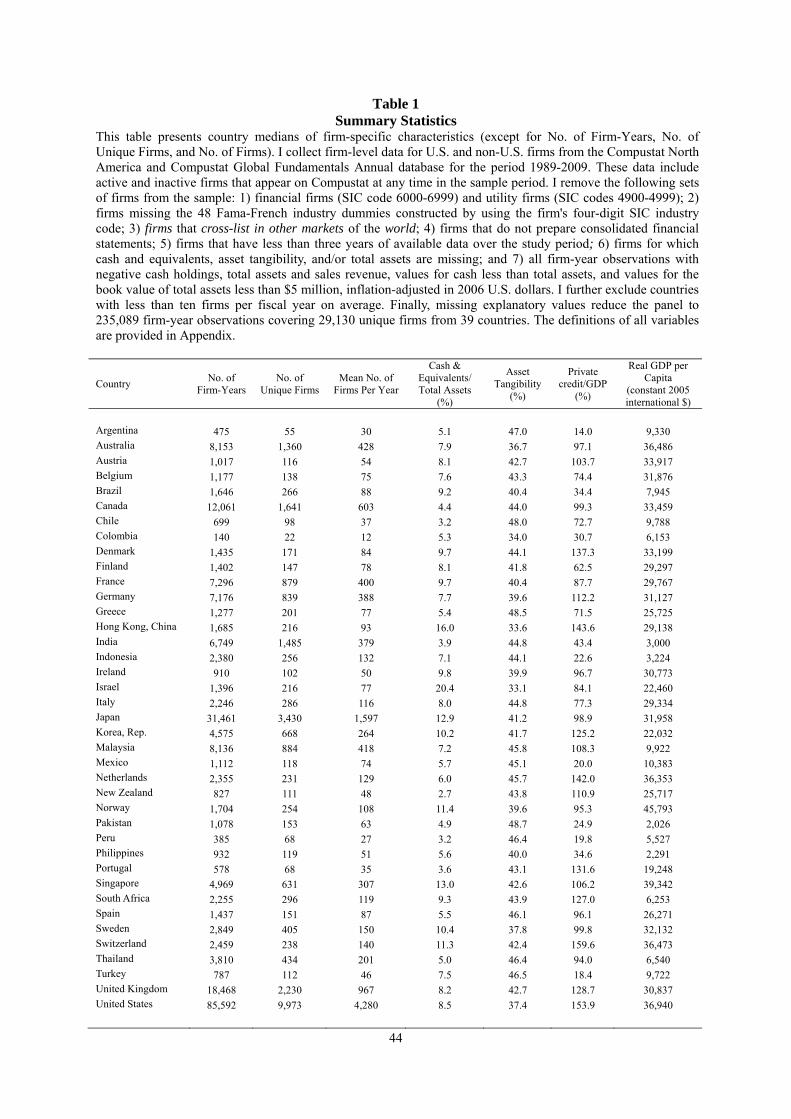

3.2. Summary Statistics

Table 1 presents country medians of some key variables employed in the analysis. In column

2, I observe that Japan has the second largest total firm-year observations and number of

unique firms behind the U.S., while Columbia has the smallest. There is a wide variation in

the cash ratios as displayed in column 5. The median firm in Israel and Hong Kong has a cash

ratio of 20.4% and 16.0%, respectively, while the median firm in New Zealand, Chile, and

Peru has a value of only 2.7%, 3.2%, and 3.2%, respectively. In contrast, as shown in column

6, the asset tangibility of the median firm in Israel and Hong Kong is merely 33.1% and

33.6%, respectively, whereas the value for the median firm in New Zealand, Chile, and Peru

is 43.8%, 48.0% and 46.4%, respectively. I again observe a negative relation between cash

holdings and asset tangibility in worldwide data.

[Table 1 about here]

I also gather aggregate country-specific data from 39 countries on private credit to GDP

from Beck and Demirgüç-Kunt (2009) and on GDP per capita from the World Bank’s World

Development Indicators (WDI) database. The last two columns of Table 1 report the country

medians for private credit creation and per capita GDP. In particular, the data show

substantial variability in private credit to GDP and country wealth. Consistent with previous

19

literature, I use private credit to GDP, the total amount of credit by deposit money banks and

other financial institutions to the private sector, divided by GDP, as the main measure of

financial development or financial depth in the baseline regression model to identify the

collateral channel, and I save other alternative proxies such as liquid liabilities per GDP and

commercial-central bank for sensitivity tests. The median private credit measured over the

period 1989–2009 ranges from values of 159.6% in Switzerland, 153.9% in the United States,

143.6% in Hong Kong, and 142.0% in Netherlands, to values below 30% in Argentina,

Turkey, Peru, and Mexico. Similarly, because the sample covers both developing and

advanced countries, the median gross national income level per capita varies from well above

$30,000 to as low as about $2,000 per annum, where GDP per capita is converted to 2005

international dollars using purchasing power parity (PPP) rates. This tremendous cross-

country variation in economic development helps us identify the channel through which asset

tangibility affects cash holdings.

3.3. Empirical Strategy

I look for international evidence to support the negative link between cash holdings and asset

tangibility hypothesized in Section 2, and estimate a model of cash holdings by using pooled

least squares regressions. The additional firm-level explanatory variables that I incorporate in

the cross-country analysis are similar to those used by Dittmar, Mahrt-Smith, and Servaes

(2003), and Kalcheva and Lins (2007). Specifically, the following regression model is use to

test the first hypothesis:

, , , , , 1

where i, c, j, and t denote firm, country, industry, and year, respectively; Cash is cash and

20

equivalents deflated by the book value of total assets; Asset Tangibility is defined as

0.715*receivables plus 0.547*inventories plus 0.535*fixed capital deflated by book value of

total assets, following the metric introduced in Berger, Ofek, and Swary (1996). The

estimated coefficient on asset tangibility delivers the prediction about the collateral channel –

the direct effect of asset tangibility on cash holdings through changes in a firm’s collateral

values of tangible assets. The higher the value of the tangible collateral, the less incentives

there are for firms to hold cash. Therefore, I expect the marginal effect of asset tangibility on

cash holdings to be negative and statistically significant ( 0). I also note that asset

tangibility as a stock variable is a better proxy for debt capacity than capital expenditure

which is considered as a very lumpy flow variable. , is a set of firm-level covariates,

which includes Market-to-Book, Firm Size which is measured by the natural logarithm of

book value of total assets in millions of 2006 U.S. dollars, Cash Flow/Total Assets, Total

Capital Expenditures/Total Assets, Total Book Leverage, R&D Expenses/Sales, and Dividend

Dummy Variable. , are distributed independently across firms with zero mean. The baseline

regression also controls for unobservable time-invariant country level heterogeneity ,

industry-specific factors that capture systematic differences in liquidity management

across industries, and year effects of common macroeconomic shocks that might affect

firms’ cash decisions. Standard errors are clustered at both the firm and year levels to obtain

standard-error estimates that are more conservative, as suggested by Petersen (2009) and

Thompson (2011).12 Details on the construction of all variables are provided in the Appendix.

Next, I exploit the heterogeneity in financial and economic development and

12 Following Bates et al. (2009), I use the double-clustered (or Rogers) standard errors suggested by Petersen (2009), Moulton (1986), and Thompson (2011) to account for unobserved time and firm effects. Petersen (2009) finds that standard errors clustered by time are much larger than standard errors clustered by firm, and recommends clustering by time. Clustering by the higher level of aggregation (in my case, by country) is generally preferable (Cameron, Gelbach, and Miller, 2006), but it can give rise to distortions if the number of clusters is small and the cluster size is uneven, as is the case with my sample (Nichols and Shaffer, 2007). Specifically, since the number of observations for each country in my data set is not even, I use standard errors clustered by firm rather than country.

21

contractual environment across countries and over time to identify the channel through which

asset tangibility affects corporate cash holdings. Specifically, I test hypotheses (2) and (3)

using the following regression model,

, , , ,

, , ,

, ,

2

where i, c, j, and t denote firm, country, industry, and year, respectively. Financial

development is measured by private credit to GDP, a popular proxy for the development of

financial intermediaries that captures the demand-side effect for collateralizable tangible

assets from financial systems. Since private credit to GDP might be an outcome of financial

institutions, I use creditor rights and information sharing as proxies for financial development.

I anticipate a positive sign on the interaction of asset tangibility with financial development

( 0). Since a reduction in the potential liquidation costs, which stem from economic

booms, increases the redeployability of tangible assets, I expect a negative sign on the

interaction term between asset tangibility and economic development proxied by GDP per

capita ( 0).

4. Empirical Results on Asset Tangibility and Cash Holdings

In this section, I first provide international evidence on the tangibility-cash link and identify

this collateral channel through cross-country variations in financial and economic

development. Second, I employ alternative country-level measures – the quality of

institutions and the redeployability of tangible assets – to investigate how these measures

influence the cash-tangibility sensitivity. Third, I evaluate how a firm’s default risk affects

collateralization rates and how the quality of institutions affects collateral spread. Fourth, I

22

utilize industry-level measures of asset salability to further identify the collateral channel.

Finally, I conclude with a series of robustness tests.

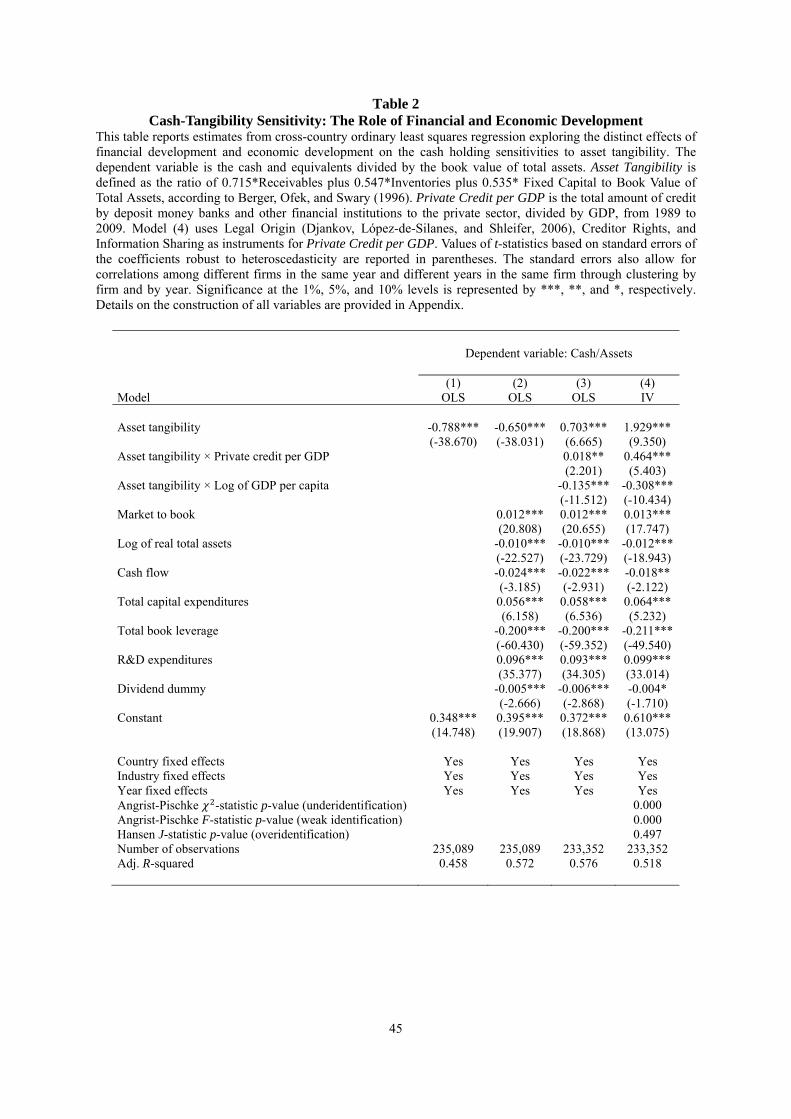

4.1. The Effect of Financial and Economic Development on Cash-Tangibility Sensitivity

Table 2 presents estimates from cross-country ordinary least squares regression exploring the

distinct effects of financial development and economic development on the cash holding

sensitivities to asset tangibility. Financial development is proxied by Private Credit per GDP.

I use the natural logarithm of country real gross domestic product per capita to measure the

overall status of a country’s economic development and activity.

In Model 1 of Table 2, I begin the assessment of whether the redeployability measure of

asset tangibility alone can explain variations in cash holdings. Only controlling for country,

industry and year fixed effects, I find that the coefficient on asset tangibility is negative and

statistically significant at the 1% level. This result indicates that having a high value of

potential collateralizable tangible assets substantially and significantly decreases corporate

cash holdings.

Model 2 presents estimates of the regression model Eq. (1). The result reveals that the

effect of asset tangibility on cash holdings becomes somewhat smaller after controlling for

covariates. The coefficient on asset tangibility is -0.650 and still significant at the 1% level.13

The size of the effect is nontrivial and I interpret the economic meaning of the estimated

coefficient on asset tangibility as follows. All else equal, a move from the 25th percentile of

the asset tangibility ratio (0.291) to the 75th percentile (0.484) decreases cash holdings by

about 12.6%, which corresponds to a decrease of 47.5% relative to the sample mean effect of

-0.265. In other words, if the firm decreases its tangibility ratio by one-interquartile range

(IQR), it has to hold 47.5% more cash ratio relative to its mean value. Alternatively,

13 The results remain qualitatively unchanged when I use alternative definitions of the cash ratio, including cash to net assets, and log of cash to net assets, and when I replace asset tangibility by net tangibility.

23

interpreting the coefficient at the sample mean, for a $1.00 decrease in tangible assets, ceteris

paribus, I expect to see a 65-cent increase in cash holdings. The negative connection between

tangibility and cash simply reflect the redeployability of tangible assets pledged as

collateral.14

[Table 2 about here]

Model 3 presents estimates of the baseline regression model Eq. (2) in which I combine

the two avenues that influence the sensitivity of cash holdings to asset tangibility. The results

also indicate that first, the coefficient on the interaction of financial development with asset

tangibility is positive and significant at the 5% level, suggesting that the collateral role of

tangible assets on cash holdings is less pronounced in financially developed countries. These

results confirm the second hypothesis and provide support for the benefits of financial

development. It suggests that the ease of raising money may actually lead firms to hold less

cash in financially developed countries. The results are also consistent with findings in

Liberti and Mian (2010) that creditors in countries with better financial development demand

lower collateralization rates, implying that creditors may be able to use alternative

instruments to constraint firms from risk-taking behavior.

Second, I find that the coefficient on the interaction term between asset tangibility and

log of GDP per capita is negative and significant. It suggests that the effect of firms’ supply

of collateralizable tangible assets on cash-tangibility sensitivity is most pronounced in

countries with high economic development where there are more economic activities and

where the markets for assets are presumably more liquid. This confirms the third hypothesis

that tangible assets are more salable in countries with more economic activities and the

increase in salability enlarges the negative effect of asset tangibility on cash holdings.

14 Note that the negative relation between cash and the chosen measure of asset tangibility may not be mechanical, because in the regression I do not simultaneously control for Compustat balance sheet (asset side) items ACO, IVAEQ, IVAO, INTAN and AO (Other Current Assets, Investment and Advances in Equity, Other Investment and Advances, Intangible Assets, and Other Assets, respectively). Moreover, the results are robust to exclusion of total book leverage as firm-specific control variables.

24

The findings also show that, all else equal, a one-IQR decrease in asset tangibility ratio

of 0.193 translates to a 13.0% (=0.193*(0.703) + 0.193*(0.018*1.202) + 0.193*(-

0.135*10.381)) increase in the cash ratios in countries with private credits per GDP and per

capita GDP equal to the sample median. All the controls have the predicted signs and have

significant coefficients.

Model 4 shows that the results are also robust to instrumental variable estimation for

private credit per GDP. Specifically, I use legal origin, creditor rights, and information

sharing as instruments for private credit per GDP. The instrumental variables pass

underidentification, weak identification, and overidentification tests.

4.2. The Effect of Institutional Variables on Cash-Tangibility Sensitivity

There is a growing body of research that investigates laws as well as regulatory and

supervisory practices determining financial development. For example, Djankov, McLiesh,

and Shleifer (2007) find that improvements in creditor protections from both the legal system

and information sharing institutions that affect the ability of borrowers to use collateral are

strongly positively linked to higher ratios of private credit to GDP. It might be the quality of

institutions underlying financial development that shapes the financial system. Therefore, I

conjecture that, at a more primitive level, higher financial development is an outcome of

institutional development.

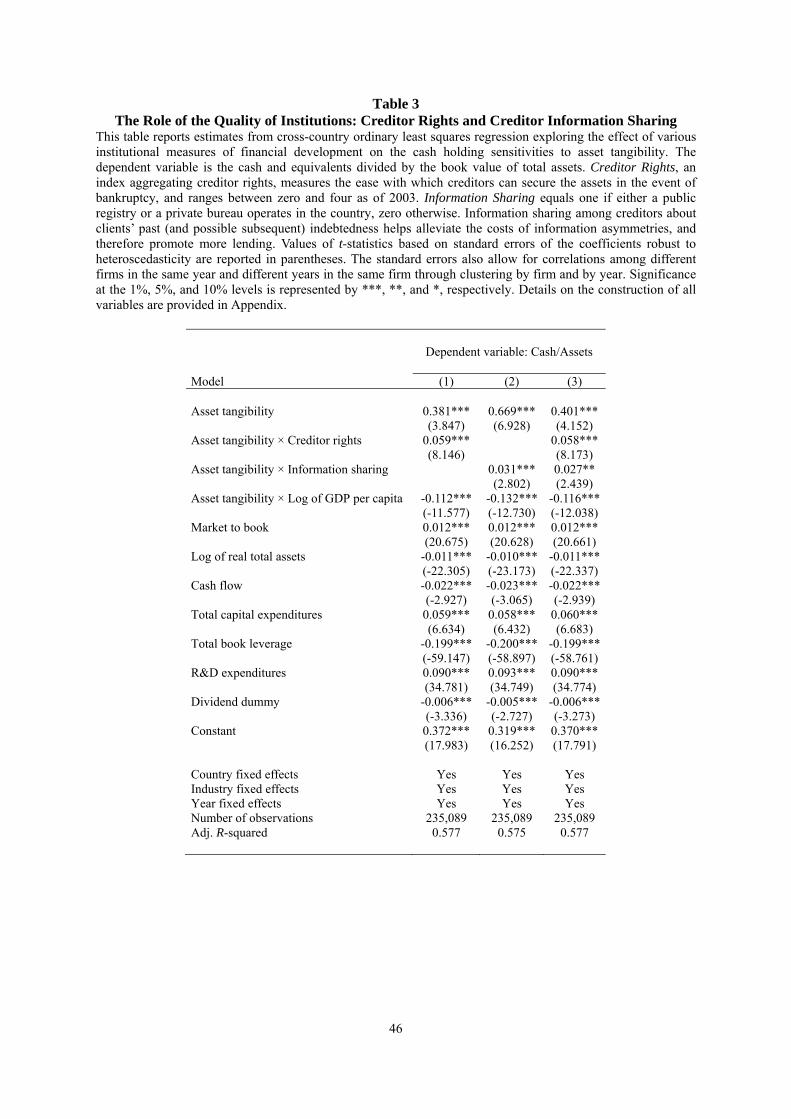

To this end, I now turn to use two sets of direct cross-country indicators of financial

development to measure the quality of institutions: creditor rights and information sharing.

The creditor rights index, constructed by LLSV (1997), measures the ease with which

creditors secure assets in the event of a default. Information sharing is a time-varying

indicator variable that equals one if either a public registry or a private bureau operates in the

country, zero otherwise.

25

[Table 3 about here]

Table 3 reports estimates from cross-country ordinary least squares regressions that

evaluate the effect of institutional measures of financial development – creditor rights and

information sharing – on the sensitivity of cash holding to asset tangibility. The estimates

indicate that both creditor rights and information sharing attenuate the negative effect of asset

tangibility on cash holdings. As shown in Models 1 and 2, the positive and significant

estimated coefficients on interaction terms Asset Tangibility × Creditor Rights and Asset

Tangibility × Information Sharing indicate that the negative effect of asset tangibility on cash

holdings is less pronounced in countries with institutions of better quality.

In Model 3, I simultaneously control for the interactive effects of both institutional

variables on cash-tangibility sensitivity. It turns out that creditor rights and information

sharing have independent and significant attenuating effects on the negative link between

cash and tangibility. These results confirm the second hypothesis in section 2. The finding

suggests that better institutions substitute for collateral, thereby lowering the importance of

tangible assets in reducing a firm’s financial constraint.

Throughout Table 3, I control for the impact of economic development on cash-

tangibility sensitivity following the same argument for Model 3 of Table 2: The liquidity of

the market for corporate assets is often a function of its GDP per capita, which might affect

the redeployability of tangibles. Compared with the results in Model 3 of Table 2, the

estimated coefficient on Asset Tangibility × Log of GDP per Capita in Table 3 remains

negative and significant after replacing private credit per GDP by two more precise measures

of financial development. This important finding suggests that even though a country’s level

of financial development may be closely related to its economic development, which implies

that a higher level of national economic development might be associated with higher-quality

26

institutions that facilitate private contracting (e.g. Claessens and Laeven, 2003), financial

development and economic development are somewhat different and exert opposite impacts

on the cash-tangibility sensitivity.

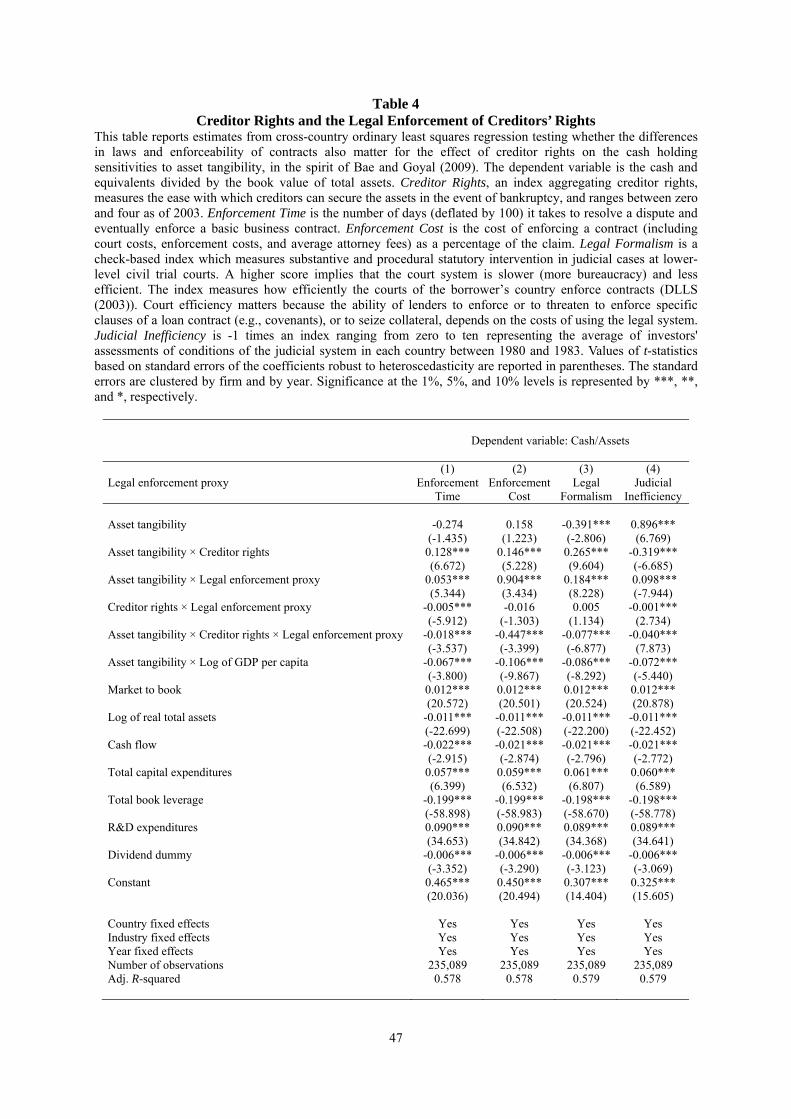

4.3. Creditor Rights and the Legal Enforcement of Creditors’ Rights

Given the important role of creditor rights in the cash-tangibility sensitivity, I further identify

the effect of creditor rights on the cash-tangibility sensitivity. Specifically, I assess whether

cross-country differences in the efficiency of contract enforcement also matter.

The rationale is that strong legal protection that better ensures creditors to repossess

collateral imposes a credible threat and greater costs upon a borrower in the case of default.

As a result, borrowers would be less willing to take on extra risk and use borrowed funds

unproductively. Therefore I anticipate that the expected realized value of collateral would

increase with creditor rights protection. It then follows that better legal enforcement of

creditors’ rights makes them more effective, leading to a more pronounced attenuating effect

of creditor rights on the cash-tangibility sensitivity.

Therefore, what really matters for the incentives for loan activities and viability of

private credit is the effective power of creditors through legal enforcement. For example,

lenders in developing countries will be reluctant to accept collateral unless the legal

environment clearly defines and effectively enforces creditor rights. As a result, the value of

collateral demanded for every dollar lent out (the collateralization rate) is significantly higher

in developing countries. On the other hand, lenders in developed countries presumably enjoy

a better legal environment and demand less collateral. It explains the observation that the

incidence and degree of collateral are higher in emerging markets than in mature markets. For

example, Bae and Goyal (2009) find that the differences in laws and enforceability of

contracts matter for bank loan size and maturity and loan spreads, whereas creditor rights

27

matter only for loan spreads.

In the spirit of their work, I use four proxies for the legal enforcement of creditors’

rights and document that the differences in laws and enforceability of contracts also matter

for the effect of creditor rights on the sensitivity of cash holding to asset tangibility. My

finding suggests that not only the strength of creditor rights but also the ownership of

collateralizable assets in bankruptcy and superior legal enforceability of creditor rights are an

essential part of the contracting and lending process.

The first proxy for legal enforcement of creditors’ rights is enforcement time, which is

the number of days (deflated by 100) it takes to resolve a dispute and eventually enforce a

basic business contract. The second proxy is enforcement cost, which is the cost of enforcing

a contract (including court costs, enforcement costs, and average attorney fees) as a

percentage of the claim. Both enforcement time and cost are proxies for the efficiency of

courts. The third proxy is Legal Formalism, which is a check-based index which measures

substantive and procedural statutory intervention in judicial cases at lower-level civil trial

courts. A higher score implies that the court system is slower (more bureaucracy) and less

efficient. The last proxy is judicial inefficiency, which is -1 times an index ranging from zero

to ten representing the average of investors' assessments of conditions of the judicial system

in each country between 1980 and 1983. The judicial system efficiency index, taken from

LLSV (1998), measures the efficiency of debt enforcement. The index is quantified based on

local practitioner’s evaluations of a hypothetical case of a debt default and insolvency.

[Table 4 about here]

Table 4 show that the coefficient on the three-way interaction term, Asset Tangibility ×

Creditor Rights × Legal Enforcement Proxy is negative and statistically significant,

28

suggesting that the attenuating effect of creditor rights on cash-tangibility sensitivity is

weaker when a country has a weaker law and order system. This implies that higher

enforcement speed, lower enforcement costs, and more efficient judicial system would make

creditor rights a more effective substitute for tangible assets as collateral.

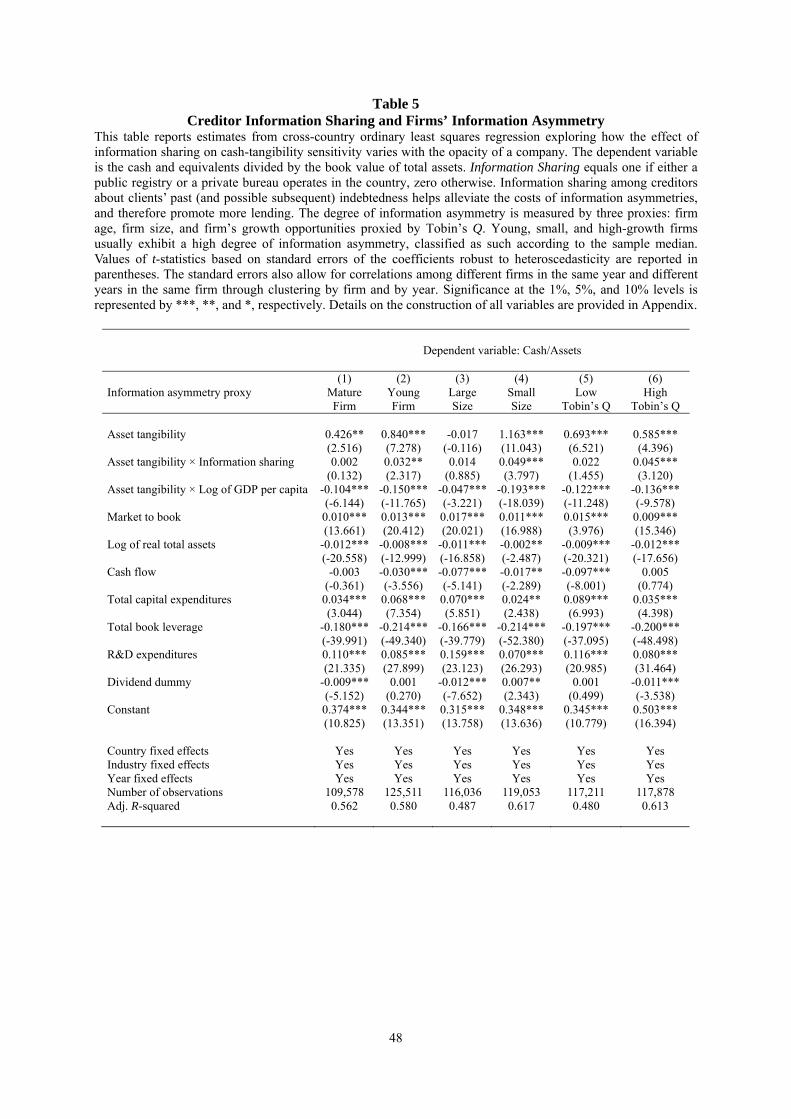

4.4. Creditor Information Sharing and Firms’ Information Asymmetry

I now turn to find further evidence in support of the conjecture that creditor information

sharing substitutes for the role of tangible collateral in reducing information asymmetry in

loan contracting.

Creditors typically use tangible assets as collateral to limit the risk-taking incentives of

debtors and reduce the higher credit risks of relatively small and young firms. Therefore,

tangible assets are relatively more important for these types of borrowing firms. However,

having access to more detailed information about borrowers via the improved institutional

mechanisms decreases the importance of tangible assets as a source for collateral. Creditors

could demand other forms of intangible collateral or even provide unsecured loans through

softer lending technologies based on factors such as borrowers’ credit history and reputation

or more restrictive financial covenants or indentures. As a result, I anticipate that the benefit

of better quality of creditor information sharing would be greater for informationally opaque

firms, as reflected through the impact of information sharing on the cash-tangibility

sensitivity.

[Table 5 about here]

Table 5 reports estimates to investigate how the effects of information sharing and

economic development on cash-tangibility sensitivity vary with the opacity of a company. I

provide direct results of regressions estimated on subsamples of firms that are classified as

29

having low or high information asymmetry by firm age, size, and firm’s growth opportunities.

Young, small, and high-growth firms usually exhibit a high degree of information

asymmetry, classified as such according to the sample median. I find positive and significant

coefficient estimates on Asset Tangibility × Information Sharing only for opaque firms. The

estimates suggest that only young, small and high-growth firms, suffering most from

financial market imperfections such as asymmetric information and hence financial

constraints, benefit from the establishment of information sharing. The result also implies that

a better quality of institutions is beneficial for opaque and distressed borrowing firms when

they have a limited amount of quality collateral. Moreover, firms that are opaque and costly

to screen gain greater access to credit through alternative lending instruments after the

introduction of a credit registry or bureau.

Table 5 also indicates that the estimated coefficient on Asset Tangibility × Log of GDP

per Capita is persistently negative and significant across various sample splits. The effect of

the level of economic development on cash-tangibility sensitivity for opaque firms is both

statistically and economically greater than that of transparent and usually unconstrained

firms. This result suggests that all types of firms take advantages of economic booms because

a booming economy enhances the redeployability of tangible assets through the collateral

channel. The rise in asset salability helps firms bolster their borrowing capacity, while opaque

and credit constrained firms benefit more from it.

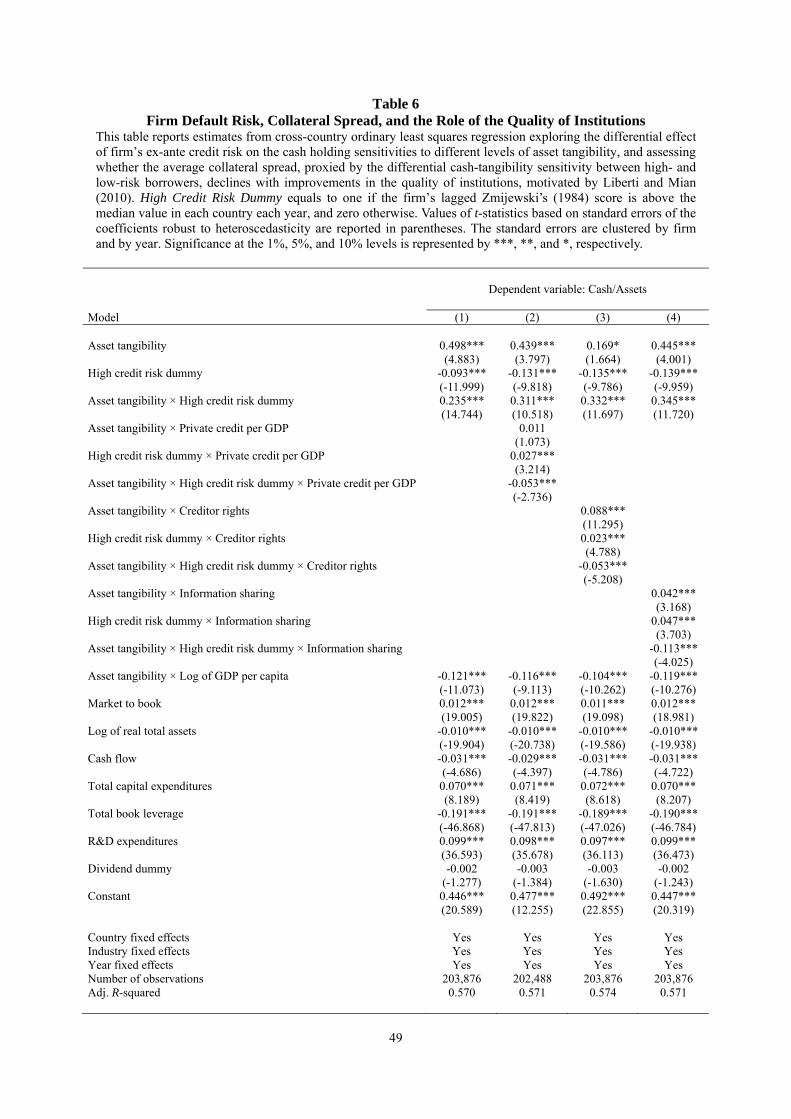

4.5. Firm Default Risk, Collateral Spread, and the Role of the Quality of Institutions

In this subsection, I complement some of the findings of Liberti and Mian (2010). Liberti and

Mian (2010) show that 1) as the predicted default or expected firm risk increases, the

collateralization rate rises as well. This implies a positive collateral spread in equilibrium

which is defined as the difference in collateralization rates between high- and low-risk

30

borrowers. Putting it differently, riskier borrowers pledge more collateralizable assets as

collateral to get the same amount of bank loans. This finding is consistent with the sorting-

by-observed-risk paradigm in the bank lending literature which claims that observably risky

borrowers are required to pledge collateral, while observably safe borrowers are not required

or pledge less (e.g. Berger and Udell, 1990); and 2) institutions that promote financial

development ease borrowing constraints by lowering the average collateral spread.

Motivated by their work, I use the differential cash-tangibility sensitivity between high-

and low-risk borrowers as a proxy for the average collateral spread, as indicated by the

estimated coefficient on the interaction term Asset Tangibility × High Credit Risk Dummy,

where the high credit risk dummy variable equals to one if the firm’s lagged Zmijewski’s

(1984) score, a proxy for the financial distress costs or probability of bankruptcy of a firm, is

above the median value in each country each year, and zero otherwise.15 A higher Zmijewski

-score value indicates a higher likelihood that a company will go bankrupt. The inputs to the

calculation of the Zmijewski-score are from the financial statements of fiscal years ending in

calendar year t−1, which ensures that these firm risk proxies are estimated on an ex-ante

basis.

[Table 6 about here]

In model 1 of Table 6, I focus the attention on the interaction term between asset

tangibility and high credit risk dummy. The interaction term tests whether riskier borrowers

pledge more collateral due to creditors’ reliance on secondary sources of hard or soft

information on collateral lien against the tangible collateral. I find that the sensitivity of cash

holdings to tangible collateral decreases with borrowing firms’ ex ante default risk, as

indicated by a positive and significant coefficient on Asset Tangibility × High Credit Risk

15 I find similar results by using Altman’s (1968) Z-score or Ohlson’s (1980) O-score as the distress measure.

31

Dummy. It implies that there exists a positive relationship between the amount of tangible

collateral pledged and borrower risk. This result is in accordance with the sorting-by-

observed-risk paradigm. Creditors usually demand higher collateral primarily to reduce the

higher credit risks of riskier firms because firms with greater default risk are more likely to

engage in risk-shifting for instance. Therefore, according to this view, tangible assets are less

effective in reducing financing constraints for high counterparty default risk firms.

Furthermore, the size of the coefficient on Asset Tangibility × High Credit Risk Dummy is

also economically significant. All else equal, riskier firms typically hold 4.54%

(=0.193*0.235) more in cash than relatively safer counterparts in response to a one-IQR

decrease in tangibility ratio of 0.193. It is consistent with the view of Liberti and Mian (2010)

that risker firms face higher collateralization rates.

More importantly, in Models 2 through 4, I explore whether the observed collateral

spread (the differential cash-tangibility sensitivity) between high- and low-risk borrowers

declines with financial development (Private credit per GDP) and improvements in the

quality of institutions (creditor rights and information sharing), respectively. As expected, I

find a negative and significant estimated coefficient on the three-way interaction in each

model. This provides additional cross-country evidence that financial development and

institutions close the wedge in collateralization rates between high- and low-risk borrowers.

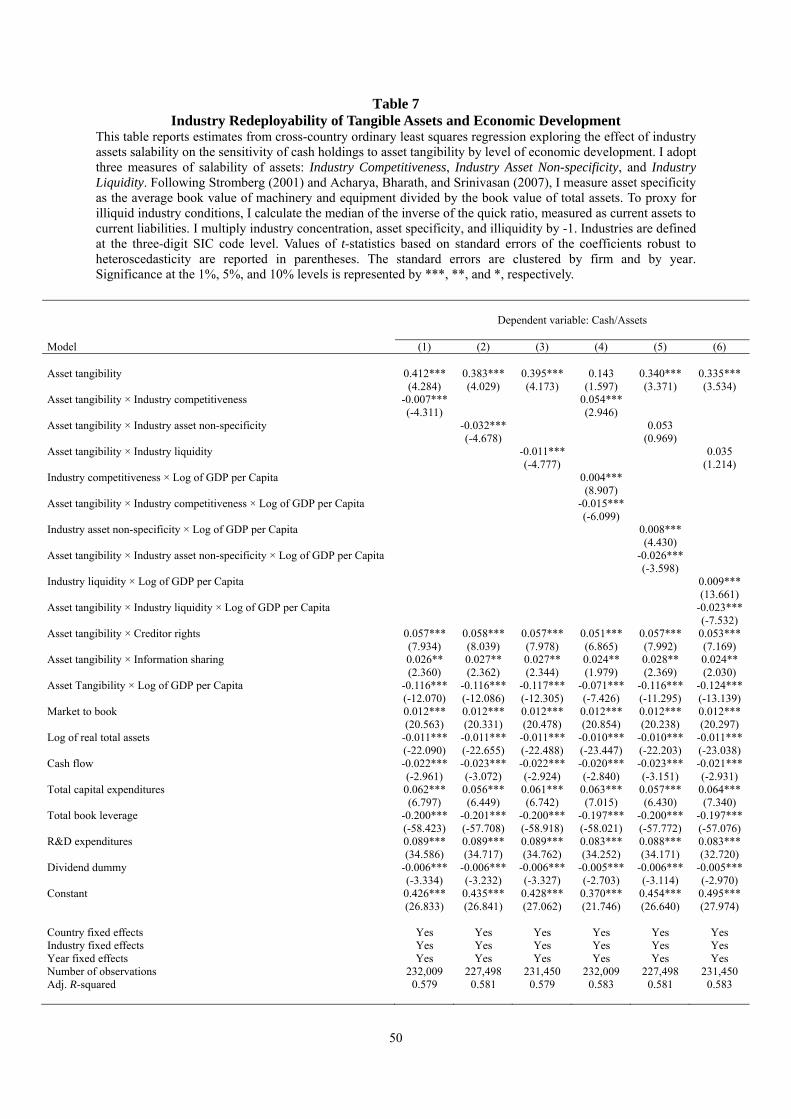

4.6. Industry Redeployability of Tangible Assets and Economic Development

In this subsection, I employ variations in industry-level and/or country- measures for the

liquidity of the market for corporate assets to identify the collateral channel through which

asset tangibility influences cash holdings.

32

4.6.1. Industry-Level Measures

I use three types of industry-level measures of asset salability.16 The first type is measured by

-1 times the industry concentration which is defined as the natural logarithm of asset-based

Herfindahl index. I deploy it to gauge the effect of market concentration on asset

redeployability. The reason is that firms in high-competition industries (low concentration

ratio) can possibly fetch a greater value when their assets are redeployed. That is, the

liquidation value of a firm’s assets decreases as the market becomes more concentrated,

partly due to fewer potential buyers of second-hand capital. This is consistent with the view

of Shleifer and Vishny (1992). Therefore, I expect that industry competition reinforces the

collateral role of tangibility in firms’ cash policies.

Second, I use -1 times the industry median ratio of the book value of machinery and

equipment relative to book value of total assets to measure asset redeployability, following

the literature (See, e.g., Berger, Ofek, and Swary, 1996; Stromberg, 2001; Acharya, Bharath,

and Srinivasan, 2007). Machinery and equipment, unlike buildings and land, are firm-specific

assets and not readily redeployable outside of the industry. They are likely to experience

lower liquidation values because they may suffer from ‘‘fire-sale” discounts in auctions for

asset sales, particularly when other firms in the industry are also in distress.

The last proxy for salability is calculated as -1 times the inverse of median Quick ratio,

which is the difference between current assets and inventories deflated by current liabilities,

following Acharya, Bharath, and Srinivasan (2007). Shleifer and Vishny (1992) also point out

that liquidation values decrease when potential buyers are likely to be financially constrained.

That is, the liquidity of redeployable assets drops when the potential buyers do not have

16 Some countries in the sample have a limited number of firm-year observations that makes it difficult to calculate accurate industry-level variables for each country in each year. Therefore, I follow the argument of Rajan and Zingales (1998) that for technological and economic reasons there exist some industry-specific characteristics and cross-industry differences that persist across countries. Specifically, I first calculate the industry-level variable for each Fama-French industry classified by the two-digit SIC code for the U.S. in each fiscal year, and then I extrapolate the median value to firms in other countries.

33

financial resources to afford paying for its services.

[Table 7 about here]

After controlling for the effects of financial institutions and economic development,

Models 1 through 3 indicate that cash-tangibility sensitivity becomes larger when firms

operate in industries with high asset salability, as indicated by the negative and significant

interaction terms of Asset Tangibility × Industry Asset Salability Proxy.

4.6.2. Country-Level Measures

I have shown that industry-level salability enlarges the negative impact of asset tangibility on

cash holdings. In Models 4 through 6, I continue to test whether variations in the level of

economic development exert differential impacts on this industry-level effect.

I show that a high level of GDP per capita (such as economic booms) facilitates the

liquidity of tangible assets and enlarges the strengthening impact of industry-level asset

salability on the negative cash-tangibility sensitivity after controlling for the effect of

financial institutions. Put differently, the greater the country-level asset salability of tangible

assets, the greater the impact of industry-level asset salability on the sensitivity of cash to

tangible assets. The results therefore complement the findings of Benmelech (2009) and

Campello and Giambona (2013) by supplying new international evidence on liquidation

values of pledged tangible assets for lenders. Therefore, this provides new insights on

corporate liquidity management and capital structure through the supply-side of redeployable

assets.

4.7. Robustness

In this subsection, I investigate the robustness of the key inference results presented thus far. I

show that the results stand up to alternative measures of financial development, the

34

decomposition of creditor right index, alternative measure of creditor information, the

weighted least squares (WLS) estimation method, and subsamples.

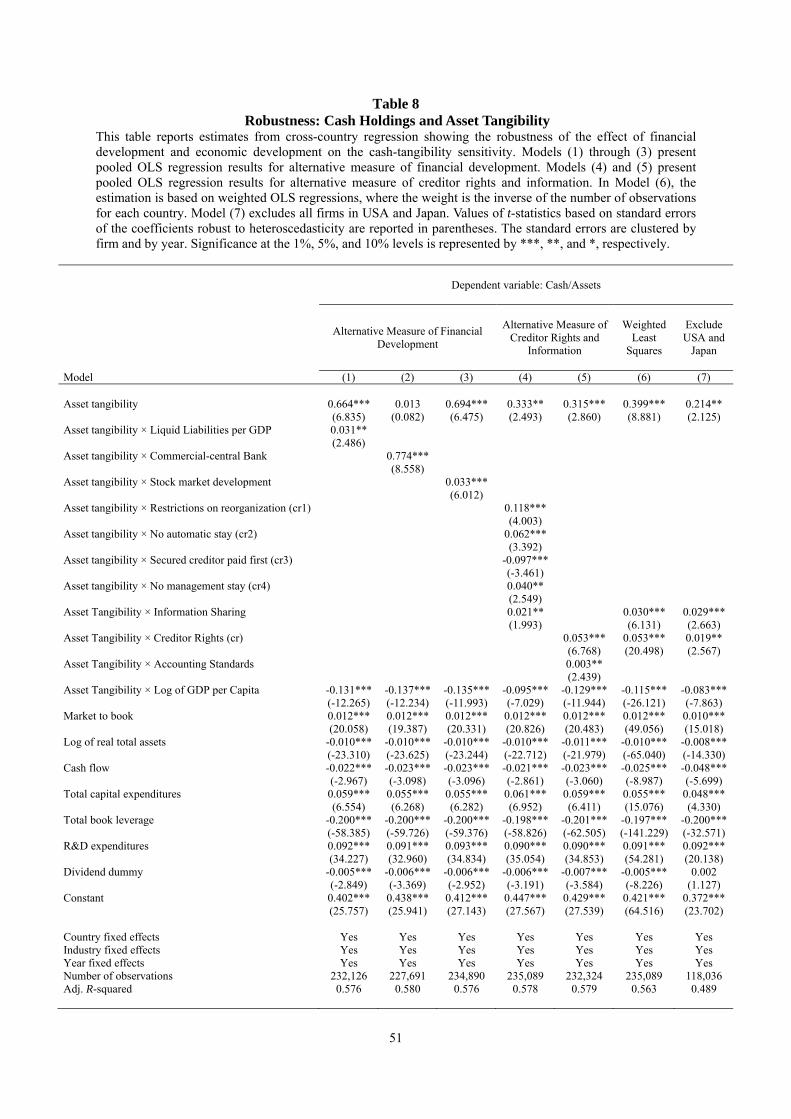

[Table 8 about here]

Table 8 contains robustness test results. In Models 1 through 3, following the financial

development and economic growth literature, I consider liquid liabilities per GDP,

commercial-central bank, and stock market development as alternative indicators of a

country’s level of financial development. The data are constructed by Beck and Demirgüç-

Kunt (2009) who obtain the raw data from the IMF's International Financial Statistics (IFS).

Liquid liabilities of the financial system are measured by currency plus demand and interest-

bearing liabilities of banks and non-bank financial intermediaries, divided by GDP. It is a

proxy for the overall size of the formal financial intermediary sector. Commercial-central

bank equals the ratio of deposit money banks’ claims on domestic nonfinancial real sector to

the sum of deposit money bank and central bank claims on domestic nonfinancial real sector.

It measures the extent to which commercial banks versus the central bank in mobilizing

savings and allocating credit. I use it to measure the financial intermediary development

because commercial banks are more likely to identify profitable investments, monitor

managers, facilitate risk management, and allocate society’s savings than central banks

(Levine, Loayza, and Beck, 2000). Stock market development is the ratio of market

capitalization over the gross domestic product (GDP). Models 1 through 3 provide

qualitatively similar results compared to what I document earlier in Model 3 of Table 2.

In Model 4, I decompose the creditor rights index into four components: Restrictions on

Reorganization (cr1), No Automatic Stay (cr2), Secured Creditor Paid First (cr3), and No

Management Stay (cr4). The negative and significant estimate on the interaction term Asset

35

Tangibility × Secured Creditor Paid First (cr3) is consistent with the view that the liquidation

value of tangible collateral increases when secured creditors are ranked first in the

distribution of proceeds of liquidating a bankrupt firm as opposed to other creditors such as

employees or government. The results for cr1, cr2 and cr4 are qualitatively similar to the