assessing the investment case for australian private …

TRANSCRIPT

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 1

Research by Revolution Asset Management | June 2018

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN

PRIVATE DEBT

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 2

CONTENTS

EXECUTIVE SUMMARY ........................................................................................................ 3

AUSTRALIAN PRIVATE DEBT – HISTORY AND BACKGROUND ...................................... 5

PRIVATE DEBT

KEY ATTRIBUTES ................................................................................................................. 9

THE ROLE WITHIN PORTFOLIO CONSTRUCTION........................................................... 12

GLOBAL MARKET DYNAMICS – THE AUSTRALIAN OPPORTUNITY .............................. 14

AUSTRALIAN PRIVATE DEBT

CURRENT ATTRACTIVE SUB-SECTORS .......................................................................... 18

SIZE OF THE INVESTABLE & ATTRACTIVE SUB-SECTORS ........................................... 24

RELATIVE VALUE VS GLOBAL EQUIVALENTS ................................................................ 27

BARRIERS TO ENTRY ........................................................................................................ 30

THE ROLE IN A ‘LATE CYCLE’ PHASE .............................................................................. 32

CONCLUSION ...................................................................................................................... 34

GLOSSARY .......................................................................................................................... 35

CONTACT INFORMATION .................................................................................................. 37

This paper is for institutional and professional investors only and has been prepared by the Investment Manager, Revolution Asset Management Pty Ltd ACN 623 140 607 Authorised Representative No:1262909 (Revolution). Channel Capital Pty Ltd ACN 162 591 568 (Channel) is Revolution’s non-investment services provider. This paper is supplied on the following conditions which are expressly accepted and agreed to by each interested party (Recipient). The information in this paper is not financial product advice and has been prepared without taking into account the objectives, financial situation or needs of any particular person. The information is not intended for any general distribution or publication and must be retained in a confidential manner. Information contained herein consists of confidential proprietary information constituting the sole property of Revolution and respecting Revolution and its investment activities; its use is restricted accordingly. All such information should be maintained in a strictly confidential manner. This information does not purport to contain all of the information that may be required to evaluate Revolution or its investment strategy and the Recipient should conduct their own independent review, investigations and analysis of Revolution and its investment strategy and of the information contained or referred to in this paper. Neither Revolution nor Channel nor their related bodies corporate, representatives and respective employees or officers (collectively, the Beneficiaries) make any representation or warranty, express or implied, as to the accuracy, reliability or completeness of the information contained in this paper or subsequently provided to the Recipient or its advisers by any of the Beneficiaries, including, without limitation, any historical financial information, the estimates and projections and any other financial information derived there from, and nothing contained in this paper is, or shall be relied upon, as a promise or representation, whether as to the past or the future. Past performance is not a reliable indicator of future performance. The information in this paper has not been the subject of complete due diligence nor has all such information been the subject of proper verification by the Beneficiaries. Except insofar as liability under any law cannot be excluded, the Beneficiaries shall have no responsibility arising in respect of the information contained in this paper or subsequently provided by them or in any other way for errors or omissions (including responsibility to any person by reason of negligence).

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 3

EXECUTIVE SUMMARY

This paper serves to provide information on the Australian and New Zealand private debt

markets and why this growing asset class provides a compelling investment case, particularly

given current and likely future market conditions.

Australian private debt is not a new asset class, nor is it a small one. At over A$2.8 trillion1, it is

actually larger than each of the Bloomberg AusBond Composite Index, the S&P/ASX200 Index and

the Australian superannuation savings pool and has been growing at a compound annual growth rate

(CAGR) of 7.6%2 since 2003. The new and evolving aspect of Australian and New Zealand private

debt is the ability for institutional investors and high net worth individuals to access a larger portion of

this market that historically has been the domain of banks.

The opportunity in Australian and New Zealand private debt is being driven by a number of macro-

economic tailwinds, the most substantial of which relates to recent changes to bank regulations.

These changes have resulted in the local big four Australian banks being required to hold additional

capital against mortgages, derivatives (such as interest rate and cross currency swaps) and

securitisation assets, which is resulting in capital being rationed amongst internal business units

within the banks. This has created an opportunity for non-bank lenders (such as private debt

funds/investment managers) to fill the gap left by the banks as they withdraw from certain sub-sectors

of the domestic lending market. Other factors supporting the opportunity include the current low

interest rate environment resulting in low absolute yields, and recent increases in public market

volatility. Coupled with these factors is a general acknowledgement that fixed income return drivers

have changed, with interest rate duration no longer being a tailwind and inflation concerns increasing.

These factors combine to create a compelling backdrop for investors to consider allocations to the

Australian private debt sector.

Private debt also affords portfolios a number of attractive structural protections through seniority,

security and covenants, which combine to mitigate the risk of the investment and is particularly

important given the stage in the current credit cycle. Being largely illiquid, private debt also exhibits

lower volatility than other major asset classes, and stable returns. Additional diversification benefits

are achieved by private markets offering access to companies and industries that may not be

available in public markets, whilst also offering exposure away from the Australian financial sector,

which is an existing material component of investors’ Australian equity and fixed income portfolios.

Importantly, quarterly or monthly contracted coupons provide portfolios with regular income streams,

while their floating rate nature provides protection from inflation and future interest rate increases. In

private debt there is a contractual loan agreement for the life of the investment that stipulates the

interest rate to be paid by the borrower to the lender and the frequency of the payments (these are

based on a floating rate plus a credit margin). As such, private debt has a very attractive attribute of a

steady income stream rather than relying on capital gains as is the case in other asset classes.

From a portfolio construction perspective, Australian and New Zealand private debt exhibits several

compelling characteristics. The Revolution Private Debt Reference Benchmark3 exhibits a low

negative (-0.26) correlation to the S&P/ASX200 Accumulation Index and a low positive (+0.34)

correlation to the Australian Ausbond Composite Index over the most recent 10 years ending April

2018. This provides an important portfolio building block which offers diversification, high income, low

volatility and a floating interest rate. Additionally, adding Australian and New Zealand private debt to a

balanced portfolio may increase returns, without additional volatility, resulting in a higher Sharpe ratio.

1 Reserve Bank of Australia (RBA).

2 Reserve Bank of Australia (RBA).

3 The Revolution Private Debt Reference Benchmark is based on 1-month BBSW plus a gross credit spread of 450 basis

points, less 50 points of modelled credit losses (consistent with bank loan books) and is provided for illustrative purposes only.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 4

In looking at the spectrum of what is included in the private debt universe, the most attractive sub-

sectors have been identified (against the current market backdrop), which include leveraged buyout

and private company debt, private and public Asset-Backed Securities (ABS) and loans to stabilised

commercial real estate assets. The relative attraction of these sub-sectors is driven by numerous

factors, such as their size and the relative value on offer.

While the total Australian private debt market is very large, at over A$2.8 trillion, the above mentioned

key sub-sectors that are the most attractive are also importantly large in their own right. In aggregate,

the annual issuance across the three key sub-sectors (leveraged buyout and private company debt,

private and public ABS and loans to stabilised commercial real estate assets) totals A$180-195

billion4. Accordingly, manager selection is critical to ensure deep and wide origination networks to

take advantage of transactions that display the best risk-adjusted returns, while maintaining credit

discipline.

It is beneficial to have a large investable universe in asset classes that exhibit low correlation to other

major asset classes, however the real question is whether the asset class offers compelling relative

value. The relative value in the Australian private debt market is evidenced through the current wide

(and stable) spreads on offer in the Australian leveraged loan market, which is also echoed in

Australian ABS. The Australian leveraged loan market currently prices transactions circa 200 basis

points wider than an equivalent-rated US leveraged loan transaction. When compared to US

Collateralised Loan Obligations (CLO’s) (which offer the greatest credit margin for global ABS),

Australian public market ABS are currently trading 50-125 basis points wider, with Australian private

ABS being another 100 basis points wider again (150-225 basis points wider than US BBB-rated

CLOs) with a much shorter maturity.

One may wonder why such a large asset class offering such strong relative value has not been

inundated with institutional participants (i.e. private debt funds and investment managers), and this is

largely due to a number of barriers to entry. These barriers include the requirement to hold a mandate

to invest in illiquid and unrated instruments, while establishing and maintaining relationships with

sponsors, banks and advisory firms. Expertise is a key barrier, with participants requiring specialist

expertise in negotiating and documenting transactions, as well as the ability to analyse industries,

businesses and financial statements and create detailed financial models for scenario analysis. Local

knowledge is also critical – i.e. local knowledge of regulations, industries, the political landscape and

market dynamics. Lastly, offshore participants would most likely seek to hedge the exposure to an

Australian dollar position, which is made difficult by Australian private debt typically being callable in

nature and incorporating both unscheduled amortisation and cash flow sweeps, which make the

variable nature of the foreign currency cash flow difficult to hedge.

Being late in the cycle, a number of factors combine to make Australian private debt a relatively

attractive asset class when compared to domestic and offshore, investment grade and high yield

bonds and US leveraged loans. Australian private debt offers seniority, security, covenants, protection

from M&A activity and cash flow leakage, as well as demonstrating attractive relative value. These

key characteristics help to provide capital stability and protection in this late cycle phase.

This paper presents empirical evidence on the relative value of the Australian private debt market

versus notable offshore markets and make a case as to why this asset class is worthy of

consideration within a diversified portfolio construction framework. Furthermore, a rationale

supporting an allocation to the private debt asset class at this late phase of an unprecedented period

of economic growth in Australia spanning 26 years is also discussed.

4 APRA, Macquarie Group, Westpac, RBA, Thompson Reuters LPC, Revolution Asset Management.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 5

AUSTRALIAN PRIVATE DEBT

HISTORY AND BACKGROUND

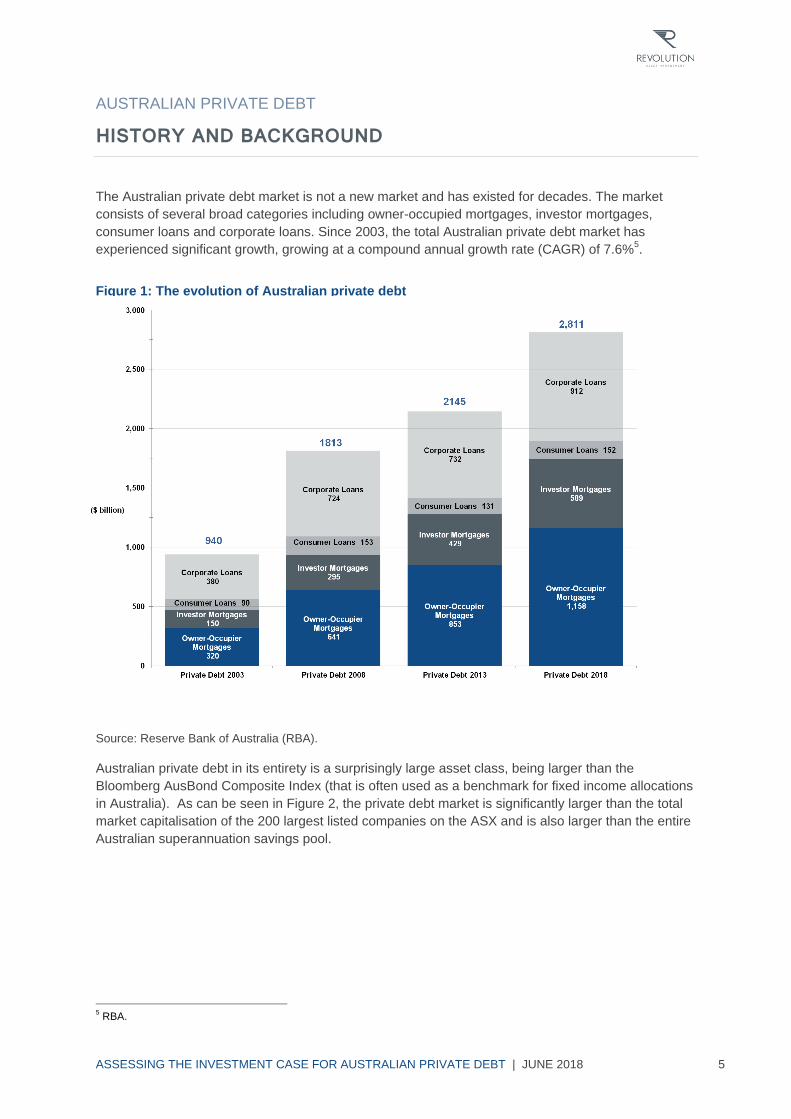

The Australian private debt market is not a new market and has existed for decades. The market

consists of several broad categories including owner-occupied mortgages, investor mortgages,

consumer loans and corporate loans. Since 2003, the total Australian private debt market has

experienced significant growth, growing at a compound annual growth rate (CAGR) of 7.6%5.

Figure 1: The evolution of Australian private debt

Source: Reserve Bank of Australia (RBA).

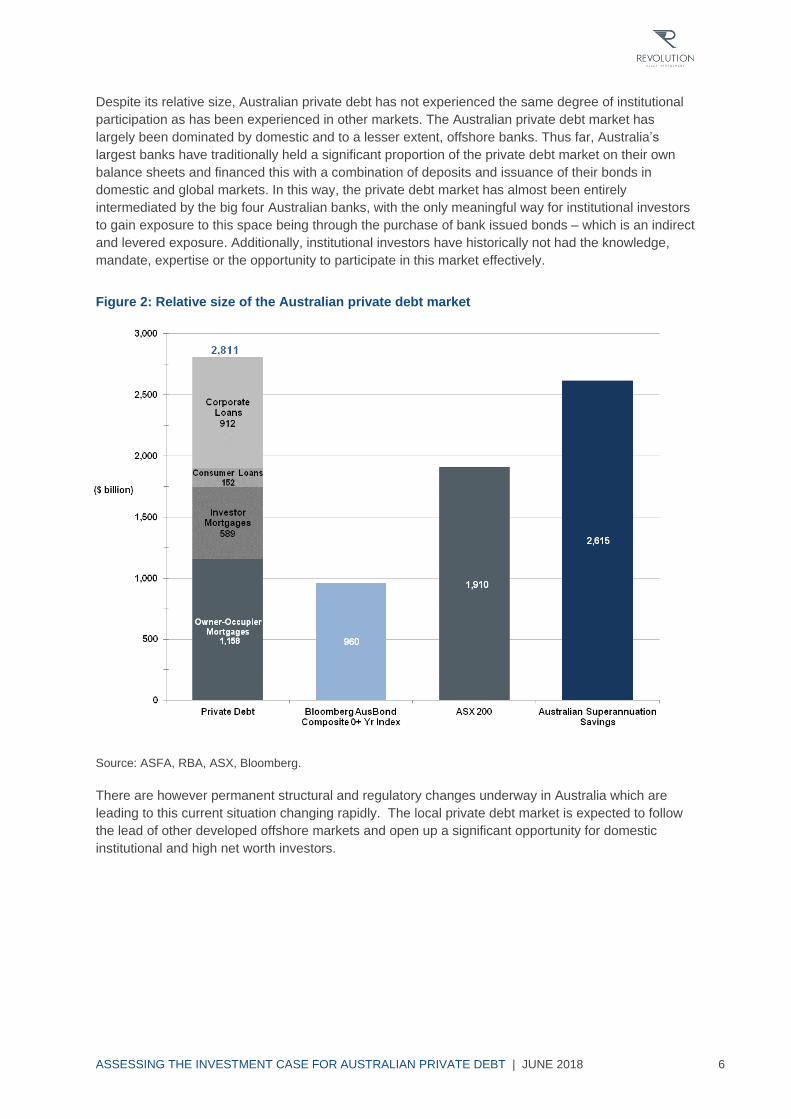

Australian private debt in its entirety is a surprisingly large asset class, being larger than the

Bloomberg AusBond Composite Index (that is often used as a benchmark for fixed income allocations

in Australia). As can be seen in Figure 2, the private debt market is significantly larger than the total

market capitalisation of the 200 largest listed companies on the ASX and is also larger than the entire

Australian superannuation savings pool.

5 RBA.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 6

Despite its relative size, Australian private debt has not experienced the same degree of institutional

participation as has been experienced in other markets. The Australian private debt market has

largely been dominated by domestic and to a lesser extent, offshore banks. Thus far, Australia’s

largest banks have traditionally held a significant proportion of the private debt market on their own

balance sheets and financed this with a combination of deposits and issuance of their bonds in

domestic and global markets. In this way, the private debt market has almost been entirely

intermediated by the big four Australian banks, with the only meaningful way for institutional investors

to gain exposure to this space being through the purchase of bank issued bonds – which is an indirect

and levered exposure. Additionally, institutional investors have historically not had the knowledge,

mandate, expertise or the opportunity to participate in this market effectively.

Figure 2: Relative size of the Australian private debt market

Source: ASFA, RBA, ASX, Bloomberg.

There are however permanent structural and regulatory changes underway in Australia which are

leading to this current situation changing rapidly. The local private debt market is expected to follow

the lead of other developed offshore markets and open up a significant opportunity for domestic

institutional and high net worth investors.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 7

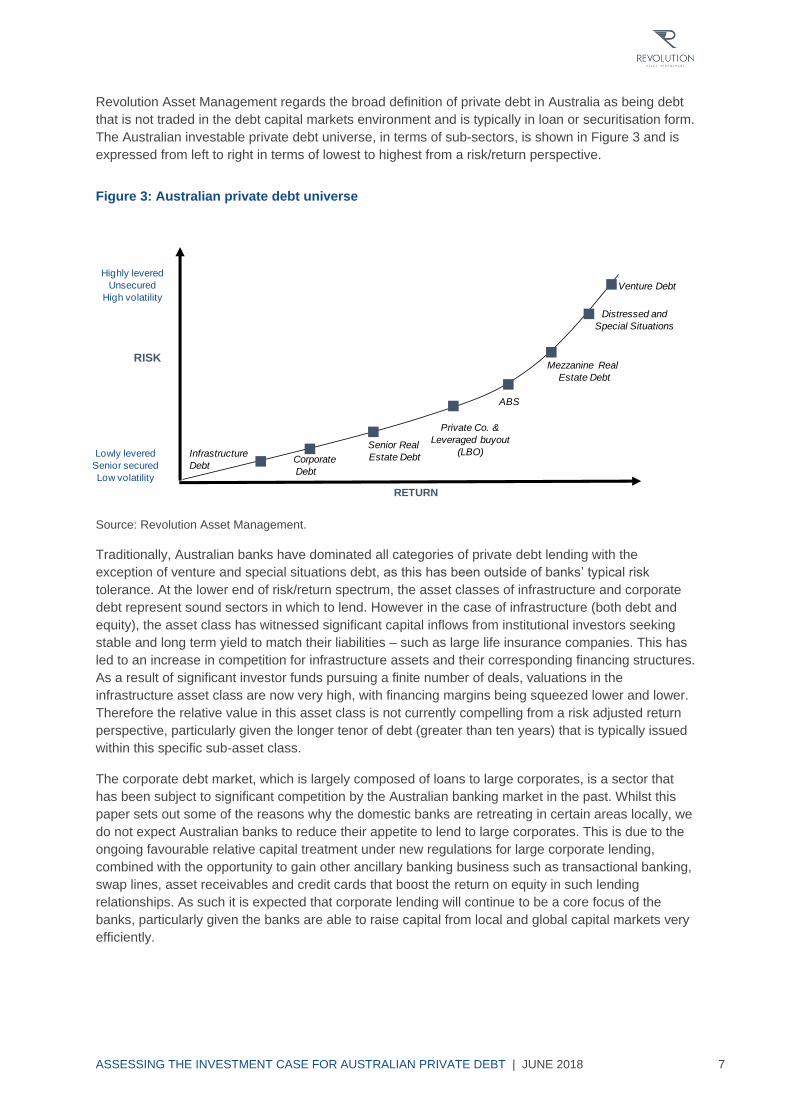

Revolution Asset Management regards the broad definition of private debt in Australia as being debt

that is not traded in the debt capital markets environment and is typically in loan or securitisation form.

The Australian investable private debt universe, in terms of sub-sectors, is shown in Figure 3 and is

expressed from left to right in terms of lowest to highest from a risk/return perspective.

Figure 3: Australian private debt universe

Source: Revolution Asset Management.

Traditionally, Australian banks have dominated all categories of private debt lending with the

exception of venture and special situations debt, as this has been outside of banks’ typical risk

tolerance. At the lower end of risk/return spectrum, the asset classes of infrastructure and corporate

debt represent sound sectors in which to lend. However in the case of infrastructure (both debt and

equity), the asset class has witnessed significant capital inflows from institutional investors seeking

stable and long term yield to match their liabilities – such as large life insurance companies. This has

led to an increase in competition for infrastructure assets and their corresponding financing structures.

As a result of significant investor funds pursuing a finite number of deals, valuations in the

infrastructure asset class are now very high, with financing margins being squeezed lower and lower.

Therefore the relative value in this asset class is not currently compelling from a risk adjusted return

perspective, particularly given the longer tenor of debt (greater than ten years) that is typically issued

within this specific sub-asset class.

The corporate debt market, which is largely composed of loans to large corporates, is a sector that

has been subject to significant competition by the Australian banking market in the past. Whilst this

paper sets out some of the reasons why the domestic banks are retreating in certain areas locally, we

do not expect Australian banks to reduce their appetite to lend to large corporates. This is due to the

ongoing favourable relative capital treatment under new regulations for large corporate lending,

combined with the opportunity to gain other ancillary banking business such as transactional banking,

swap lines, asset receivables and credit cards that boost the return on equity in such lending

relationships. As such it is expected that corporate lending will continue to be a core focus of the

banks, particularly given the banks are able to raise capital from local and global capital markets very

efficiently.

Infrastructure

Debt

RISK

RETURN

Distressed and

Special Situations

Venture Debt

Mezzanine Real

Estate Debt

Senior Real

Estate Debt

Private Co. &

Leveraged buyout

(LBO)Corporate

Debt

Lowly levered

Senior secured

Low volatility

Highly levered

Unsecured

High volatility

ABS

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 8

At the other end of the risk/return continuum are the sub-sectors of venture debt and

distressed/special situations debt. These sub-sectors have merit in the construction of a balanced

portfolio within a higher risk/return seeking allocation, however Revolution Asset Management

believes it is important that investors seek out the best specialist managers with strong track records

within these particular higher risk/return sub-markets. It is generally accepted that different skills are

required by managers to invest in par loans (with a view of holding these investments to maturity), as

opposed to purchasing a deeply distressed loan at a heavily discounted rate and looking to exit in a

much shorter timeframe. Investors should be wary of core strategies that seek to invest in

distressed/special situations debt together with par loans in the same vehicle.

Throughout the remainder of the paper we will focus on the areas of the private debt market that

Revolution Asset Management believes represent the highest relative risk adjusted return within the

Australian private debt market whilst maintaining the core defensive attribute of capital preservation.

These areas include commercial real estate debt, private and LBO debt and ABS.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 9

PRIVATE DEBT

KEY ATTRIBUTES

There are a number of key attributes that have led to the private debt asset class becoming firmly

entrenched in global developed markets. These include higher relative levels of structural protection,

lower volatility, inflation hedging, a stable income stream and diversification. Each of these attributes

are further described below.

Structural Protection

Private debt offers a number of structural features that can help to protect and preserve investor

interests if performance is not as expected. These features include the protections afforded by

seniority in the capital structure (as illustrated in Figure 4), security and covenants, which are

particularly important from a fixed income perspective. When these attributes are combined (as they

are in private debt), they help to mitigate any potential loss for investors.

Seniority refers to investors’ relevant position in the capital structure. The most senior lenders within a

capital structure receive priority repayment of cash flows, meaning that any principal and/or interest

on senior instruments are paid before any less senior instruments further down the capital structure.

Seniority at its core enables investors to protect themselves from a scenario where a borrower might

have insufficient funds to honour its commitments and results in a senior or preferential position

relative to any junior or subordinated debt.

Figure 4: Example of typical capital structure

Source: Revolution Asset Management.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 10

Security (which is legally documented in loan contracts), also known as a lien in the US, allows

lenders to have rights over certain or all of the borrower’s assets should they be unable to meet their

repayment obligations. Furthermore, it grants the legal right of a creditor to take control of the property

from a borrower that has failed to repay the creditor, with the creditor having the ability to sell the

assets or property if the loan is not repaid.

Secured lending is where a borrower pledges its assets (collateral) against the value of the loan to

reduce risk to the lender. This provides lenders with a greater degree of confidence in recovering the

value of their investment should the borrower default (or their cash flows come under stress resulting

in a covenant breach).

In the Australian market context, a senior secured loan is one where the lender has first ranking

security and priority in the capital structure. This senior security can be over a business (which

includes all of its assets) or an asset or group of assets (in the case of real estate lending). This is the

equivalent of first lien lending in US parlance.

One may also have a junior secured position in a capital structure, or second ranking security. This is

the equivalent of second lien lending in US parlance. In this case, the debt holder still holds a security

interest, though in the event of default, these junior secured or second lien debt holders would only

receive payment after all senior or first lien debt holders are paid in full. An example of lending in this

context could include lending to a real estate asset or group of assets where there is senior secured

(or first lien) debt together with junior secured (or second lien) debt.

Covenants are binding commitments that require the borrower to fulfil certain conditions or which may

forbid the borrower from engaging in certain actions. Covenants allow lenders to monitor borrowers’

performance and provide an early warning sign for deterioration in their creditworthiness. Importantly,

they can allow lenders to take action to ensure the weak performance is rectified. Covenants may

include ratios such as leverage (debt/EBITDA), interest coverage (a measure of how many times

EBITDA covers the interest cost), debt service coverage (a cash flow measure of principal and

interest cover), and loan to value ratio (LVR).

These structural protections afforded via the attributes of private debt exposures should be of

particular interest to investors considering their allocations at this advanced stage of the credit cycle.

Low volatility

The private debt market exhibits lower levels of volatility (beta) and low correlation to equities and

liquid credit markets, by virtue of the fact that it is a floating rate investment and the return is private in

nature and not a daily liquid investment. As shown in the correlation matrix studies in Tables 1 and 2

(in the section titled The Role of Private Debt in Portfolio Construction), the lower volatility attribute is

a significant reason why private debt has experienced significant growth in offshore markets,

particularly for institutional clients.

Inflation hedge

Private debt investments are made on a floating interest rate plus a margin for the term of the

instrument. This has the effect of immunising the capital value of the instrument to any resultant

changes in interest rates or any changes in inflation. In this way, the asset class may be construed as

defensive and is attractive in periods of rising rates and inflation as the rate of interest on the

underlying investments moves up with any interest rate rises.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 11

Stable income stream

All private debt investments, whether they are in loan or ABS format, have contractual obligations

underpinning their interest payments on a monthly or quarterly basis. The effect of this is that an

investment in private debt provides a stable and regular income stream that is immunised to the

macro-economic cycle. The stable income attribute of the private debt asset class sets it apart from

many others like equities, real estate equity and private equity where income paid to underlying

investors is subject to much higher discretion by the underlying management team of the company

invested in or the manager in charge of the fund. In private debt, there is a contractual loan

agreement for the life of the investment that stipulates the interest rate to be paid by the borrower to

the lender and the frequency of the payments (these are based on a floating rate plus a credit

margin). As such, private debt offers a steady income stream, differing to other asset classes that

may rely on capital gains and manager discretion.

Diversification

Diversification benefits are achieved by private markets offering access to companies and industries

that may not be available in public markets, while also offering exposure away from the Australian

financial sector, which is a material component of both Australian equity and fixed income benchmark

portfolios.

Private debt provides investors access to a more diverse range of industries and sectors that have

traditionally only been available to banks. An example of this was that prior to the listing of Ingham’s

on the ASX, the ability for investors to gain access to the Australian poultry market (through either

debt or equity) did not exist. Other examples of companies and industries that were only accessible

via private debt include Primo (Australian smallgoods) and Ticketek (Australian live entertainment).

The traditional equity and debt capital markets have been dominated by banks and financial exposure

– making up a high weighting on both the S&P/ASX200 Index and Bloomberg AusBond Composite

Bond Index. An allocation to private debt allows investors to further diversify from this banking and

financial exposure.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 12

PRIVATE DEBT

THE ROLE WITHIN PORTFOLIO CONSTRUCTION

The US Experience

The private debt asset class has become accepted and entrenched in US and European markets by

non-banks seeking to invest in the asset class due to the favourable attributes discussed in the

previous section of this paper. From an asset allocation context, there are compelling reasons to

include private debt as a key component in a balanced portfolio.

Table 1 shows the results of a correlation study completed by JP Morgan over a 15 year period. The

correlation matrix compares the US leveraged loan market (as a proxy for private debt) to a number of

other investable asset classes, for the fifteen years ending December 2017.

Table 1: Risk and return of various assets – fifteen years ending 29 December 2017

Source: JP Morgan, S&P Leveraged Commentary and Data.

Most notably, leveraged loans have a negative correlation coefficient of -0.38 versus 10-year

Treasuries, and exhibit a low correlation to the investment grade bond market (JULI High Grade

Index) and international equities (S&P 500). It is worth highlighting that these negative and low

correlations result in private debt being an attractive allocation when constructing optimal portfolios to

maximise return without additional volatility – thereby increasing overall portfolio Sharpe ratios.

The Australian Opportunity

From a portfolio perspective, Australian private debt exhibits several characteristics which increase its

relevance in portfolio construction. The Revolution Private Debt Reference Benchmark6 exhibits a low

negative (-0.26) correlation to the S&P/ASX200 Accumulation index and a low positive (+0.34)

correlation to the Australian Ausbond Composite Index over the most recent ten years ending in April

2018. This is illustrated in Table 2.

6 The Revolution Private Debt Reference Benchmark is based on 1-month BBSW plus a gross credit spread of 450 basis

points, less 50 basis points of modelled credit losses (consistent with bank loan books) and is provided for illustrative purposes only.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 13

Table 2: Correlation of Australian private debt

S&P/ASX200

Accumulation

Index

Bloomberg

AusBond

Composite

0+Yr Index

Revolution

Private Debt

Reference

Benchmark

S&P/ASX200

Accumulation Index 1

Bloomberg AusBond

Composite 0+Yr Index -0.29 1

Revolution Private Debt

Reference Benchmark -0.26 0.34 1

Source: Revolution Asset Management, Citi, Morningstar. Past performance is not indicative of future

performance.

Being floating rate and largely illiquid, private debt also exhibits lower volatility and stable returns,

which results in a superior Sharpe ratio when incorporated into a portfolio of Australian equities and

fixed income (as seen in Table 3). Importantly, quarterly or monthly (in the case of ABS) coupons,

provide portfolios with regular income streams, while their floating rate nature provides protection from

inflation and future interest rate increases.

Table 3: The addition of Australian private debt to portfolios

A B C A:B:C A:B:C A:B:C A:B:C

S&P/ASX200

Accumulation

Index

Bloomberg

AusBond

Composite

0+Yr Index

Revolution

Private

Reference

Benchmark

100%:

0%:0%

60%:

40%:0%

60%:

20%:20%

60%:

0%:40%

1 year return 5.7% 2.0% 5.7% 5.7% 4.2% 4.9% 5.7%

3 year return 5.8% 2.7% 5.8% 5.8% 4.7% 5.3% 5.9%

5 year return 7.7% 3.8% 6.1% 7.7% 6.2% 6.7% 7.1%

7 year return 7.8% 5.9% 7.1% 7.8% 7.2% 7.4% 7.6%

10 year return 4.8% 5.8% 7.2% 4.8% 5.6% 5.9% 6.1%

10 year

volatility 14.0% 3.0% 0.5% 14.0% 8.3% 8.2% 8.4%

10 year

sharpe ratio

0.34 0.68 0.71 0.73

Source: Revolution Asset Management, Citi, Morningstar.

Past performance is not indicative of future performance.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 14

PRIVATE DEBT

GLOBAL MARKET DYNAMICS – THE AUSTRALIAN OPPORTUNITY

There are four key drivers that have been the catalyst for the significant growth of the private debt

asset class globally including global banking changes, a change in traditional fixed income drivers, a

rise in public market volatility and low interest rates, as illustrated in Figure 5.

Figure 5: Four key drivers of growth in private debt globally

Global banking changes

In the aftermath of the global financial crisis (GFC) of 2007-2009, the Basel Committee on Banking

Supervision outlined measures aimed specifically to strengthen the regulation, supervision and risk

management of banks under guidelines known as the Basel III regulatory reforms. These standards

and reforms are minimum requirements that apply to all active global banks which were designed to

restore the confidence in the banking system. Under Basel III, and soon to be progressively

implemented Basel IV, guidelines set forth by the Committee standardised the calculation of bank

Risk Weighted Assets (RWA) in order to improve the comparability of banks’ capital ratios, across and

within different markets.

The most profound impact of these guidelines was felt by US and European banks that found

themselves with significantly higher leverage and as a result lower capital ratios than the Basel III

allowable threshold. From 2010 onwards, these banks proactively set about simultaneously reducing

their leverage and boosting their equity capital bases. They did this by reducing proprietary trading,

originating lower volumes of loans and securitisation transactions, selling capitally intensive portions

of their existing balance sheets to institutional investors and issuing new equity capital. As a result,

bank leverage in the US and Europe decreased (equity to assets increased) considerably over the

period from 2009 to 2015.

Lowinterest rates

Global banking changes

Change in fixed income

return drivers

Public market volatility

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 15

Figure 6: Equity to assets ratio of banks in the United States from 2000 to 2017

Source: FFIEC, St. Louis Fed, Statista.

As banks in the US and Europe retreated considerably from proprietary trading and also sub-sectors

of the private debt market that were formerly core strategies, it left a considerable opportunity that

was quickly seized upon by non-bank institutional investors. These investors were attracted to the

private debt market due to key attributes that will be discussed further below.

The experience in Australia has been in significant contrast to that of the US and Europe despite the

Basel reforms applying to all active global banks. This was due to the fact that the big four Australian

banks (CBA, Westpac, NAB and ANZ) had very different balance sheets and were amongst the

strongest in the world following the GFC, retaining their strong capital ratios and ‘AA’ credit ratings. As

a result they were not forced to undertake the same urgent reforms in order to bolster their equity

capital and reduce leverage.

This ultimately led to Australian banks continuing to focus on increasing their market share, driving

revenue and growing their overall balance sheet rather than reducing asset growth and increasing

capital ratios. That was until a number of key announcements. In July 2015, The Australian Prudential

Regulation Authority (APRA) announced a significant increase in the amount of capital required for

Australian residential mortgage exposures by authorised deposit-taking institutions (ADIs) accredited

to use the internal ratings-based (IRB) approach to credit risk. The average risk weight on Australian

residential mortgage exposures increased from approximately 16% to at least 25%7. Then in July

2017, APRA announced new minimum core equity tier 1 (CET1) of 10.5% for the big four banks –

designed specifically to ensure that they got to an ‘unquestionably strong’ position. On 7 December

2016, APRA released the final guidelines in relation to ADI’s adopting prudent guidelines to manage

the risks associated with securitisation, called APS 120. Whilst these guidelines were announced in

2016 they came into force on 1 January 2018.

7 APRA Media Release July 2015.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 16

The effect of these key announcements by APRA (and their subsequent adoption) has been

significant on the four Australian banks. Given approximately two thirds of the big four banks’ balance

sheets are composed of mortgages, there has been a dramatic increase in the capital required to

support this activity. This has had the effect of ‘starving’ other areas of capital required to support

lending activities attracting higher capital charges due to the rationing of a finite capital base.

As a result of these regulatory changes there is now a significant opportunity in the Australian private

debt market, where the banks have been forced to retreat and where institutional investors have

emerged to fill the void – these specific opportunities will be highlighted in subsequent sections of this

paper.

Other changes to bank capital requirements have had some profound impacts on the liquidity of the

debt capital markets. Over time global banking regulators have made it more capitally intensive for

banks to provide a balance sheet for proprietary trading and market making. This has resulted in far

less liquidity than was previously the case for corporate and financial bonds. The effect of these

regulations has been that investment funds that offer ‘daily liquidity’ may find it more challenging to

liquidate their portfolios in the current market and especially in times where there is a high demand for

liquidity. Additionally, it has been reported that banks have reduced bond inventories by about 70%8

because of these tighter regulations, contributing to less liquidity in debt capital markets. Accordingly,

so called liquid markets may not be as liquid if and when that liquidity is required.

Change in fixed income return drivers

The fixed income asset class has been a beneficiary of a long term secular rally in global interest rate

markets that has proven to be a tailwind for performance (this is illustrated in Figure 7). Over a shorter

timeframe, the global credit markets (both investment grade (IG) and high yield (HY)) have also

benefited from significant compression in credit spreads as shown below. With the US economy

significantly more robust as evidenced by lower unemployment and consistently higher non-farm

payrolls feeding through into GDP growth, the US Federal Reserve (Fed) has embarked on a

tightening cycle. The effect of this is that interest rate duration is not expected to be a significant

positive driver of performance for fixed income going forward, as it will be more difficult to predict the

direction and magnitude of any changes in rates markets.

Figure 7: US 10-year Treasury Yield

Source: JP Morgan.

8 Mark Carney: The Future of Financial Reform (speech by Mark Carney, Governor of the Bank of England and Chairman of the

Financial Stability Board, at the 2014 Monetary Authority of Singapore lecture, Singapore, 17 November 2014.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 17

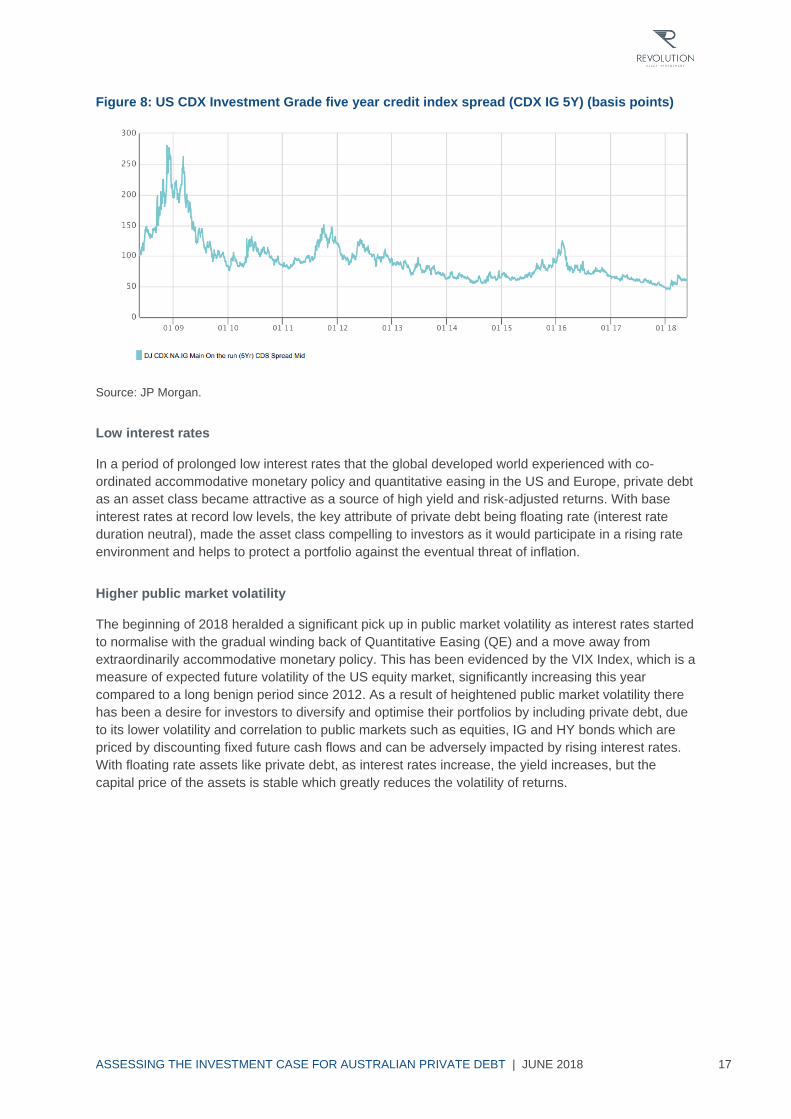

Figure 8: US CDX Investment Grade five year credit index spread (CDX IG 5Y) (basis points)

Source: JP Morgan.

Low interest rates

In a period of prolonged low interest rates that the global developed world experienced with co-

ordinated accommodative monetary policy and quantitative easing in the US and Europe, private debt

as an asset class became attractive as a source of high yield and risk-adjusted returns. With base

interest rates at record low levels, the key attribute of private debt being floating rate (interest rate

duration neutral), made the asset class compelling to investors as it would participate in a rising rate

environment and helps to protect a portfolio against the eventual threat of inflation.

Higher public market volatility

The beginning of 2018 heralded a significant pick up in public market volatility as interest rates started

to normalise with the gradual winding back of Quantitative Easing (QE) and a move away from

extraordinarily accommodative monetary policy. This has been evidenced by the VIX Index, which is a

measure of expected future volatility of the US equity market, significantly increasing this year

compared to a long benign period since 2012. As a result of heightened public market volatility there

has been a desire for investors to diversify and optimise their portfolios by including private debt, due

to its lower volatility and correlation to public markets such as equities, IG and HY bonds which are

priced by discounting fixed future cash flows and can be adversely impacted by rising interest rates.

With floating rate assets like private debt, as interest rates increase, the yield increases, but the

capital price of the assets is stable which greatly reduces the volatility of returns.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 18

AUSTRALIAN PRIVATE DEBT

CURRENT ATTRACTIVE SUB-SECTORS

Across the spectrum of Australian private debt, there are a number of sub-sectors that have

presented, and continue to present, stronger risk-adjusted returns. These sub-sectors include:

Leveraged buyout and private company debt;

Private and public Asset-Backed Securities (ABS) to various commercial and consumer loan

pools; and

Loans to stabilised (non-construction/development) commercial real estate assets with

underlying lease cashflow streams.

Figure 9: Attractive sub-sectors of Australian private debt

Source: Revolution Asset Management.

These sub-sectors are explained in detail below.

Senior Real Estate Debt

This sub-sector is involved in providing loans to stabilised commercial (office, retail and industrial)

properties and portfolios of properties. This lending is based on a combination of cash flows

generated by the properties and the underlying value of the asset/s in question. This type of lending is

viewed as relatively low risk due to the fact that the properties have long, stable tenant profiles

(supporting cash flow generation) and are generally geared to less than 70% providing a material

equity cushion.

Real estate lending can itself be considered quite a broad category, with opportunities spanning

everything from residential apartment development right through to stabilised properties with high

occupancy, long Weighted Average Lease Expiry (WALE) and low gearing. While the former may

offer double-digit returns in benign market conditions, this could rapidly change with a potentially high

loss-given-default (consider, for example, the value of an off the plan apartment when banks are

tightening their lending standards).

Infrastructure

Debt

RISK

RETURN

Distressed and

Special Situations

Venture Debt

Mezzanine

Real Estate Debt

Corporate

Debt

Lowly levered

Senior secured

Low volatility

Highly levered

Unsecured

High volatility

Senior Real

Estate Debt

Private Co.

& Leveraged Buyout (LBO)

ABS

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 19

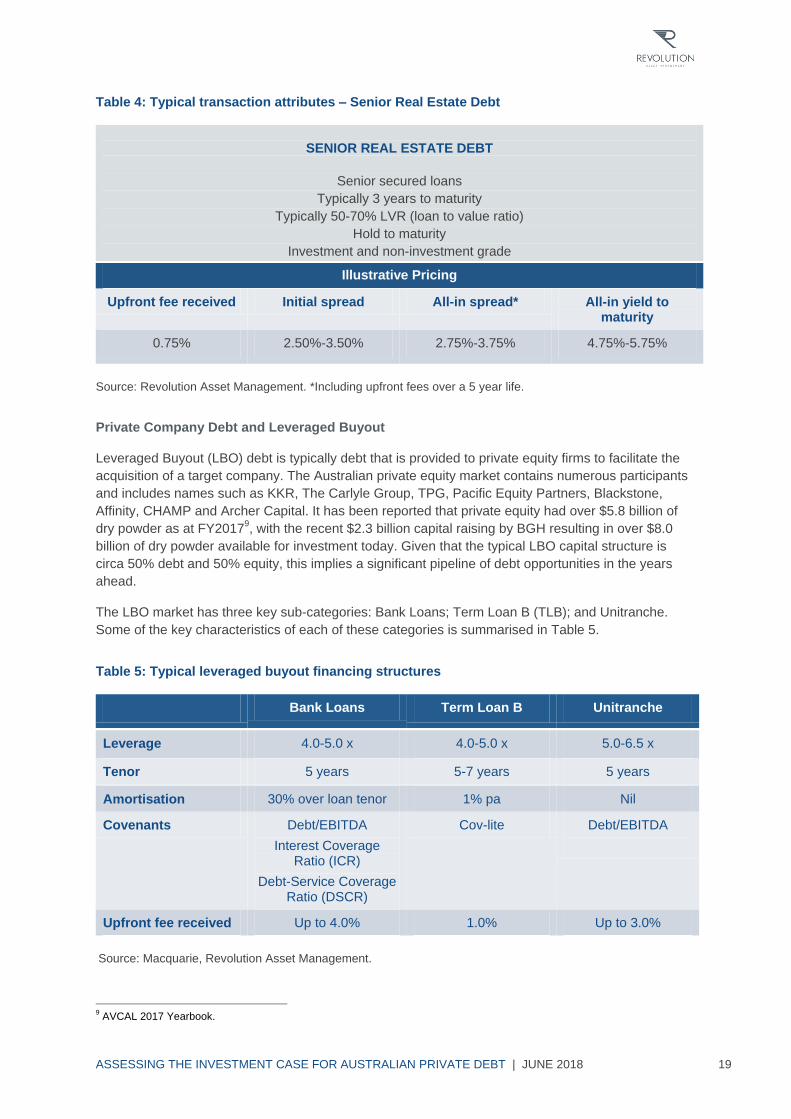

Table 4: Typical transaction attributes – Senior Real Estate Debt

SENIOR REAL ESTATE DEBT

Senior secured loans

Typically 3 years to maturity

Typically 50-70% LVR (loan to value ratio)

Hold to maturity

Investment and non-investment grade

Illustrative Pricing

Upfront fee received Initial spread All-in spread* All-in yield to maturity

0.75% 2.50%-3.50% 2.75%-3.75% 4.75%-5.75%

Source: Revolution Asset Management. *Including upfront fees over a 5 year life.

Private Company Debt and Leveraged Buyout

Leveraged Buyout (LBO) debt is typically debt that is provided to private equity firms to facilitate the

acquisition of a target company. The Australian private equity market contains numerous participants

and includes names such as KKR, The Carlyle Group, TPG, Pacific Equity Partners, Blackstone,

Affinity, CHAMP and Archer Capital. It has been reported that private equity had over $5.8 billion of

dry powder as at FY20179, with the recent $2.3 billion capital raising by BGH resulting in over $8.0

billion of dry powder available for investment today. Given that the typical LBO capital structure is

circa 50% debt and 50% equity, this implies a significant pipeline of debt opportunities in the years

ahead.

The LBO market has three key sub-categories: Bank Loans; Term Loan B (TLB); and Unitranche.

Some of the key characteristics of each of these categories is summarised in Table 5.

Table 5: Typical leveraged buyout financing structures

Bank Loans Term Loan B Unitranche

Leverage 4.0-5.0 x 4.0-5.0 x 5.0-6.5 x

Tenor 5 years 5-7 years 5 years

Amortisation 30% over loan tenor 1% pa Nil

Covenants Debt/EBITDA

Interest Coverage Ratio (ICR)

Debt-Service Coverage Ratio (DSCR)

Cov-lite Debt/EBITDA

Upfront fee received Up to 4.0% 1.0% Up to 3.0%

Source: Macquarie, Revolution Asset Management.

9 AVCAL 2017 Yearbook.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 20

As shown in Table 5, the key variables across the different categories include leverage, tenor and

covenants, with Bank Loans typically exhibiting the lowest leverage, shortest tenor and full covenant

packages.

LBO debt provides an attractive risk adjusted return with running yields (excluding any upfront fees) of

currently around 3.75%-4.75%, with TLB and Unitranche transactions typically pricing wider than this

to compensate for the additional leverage, tenor and lack of covenants. Covenants should only be

dispensed with for the most stable and robust credit profiles. In assessing TLB and Unitranche

transactions, investors should only be investing in these structures for the most attractive and

defensive industries and underlying business profiles.

Table 6: Typical transaction attributes – Private Company and Leveraged Buyout Debt

PRIVATE COMPANY AND LEVERAGED BUYOUT DEBT

Senior secured loans and some bonds

Typically 5 years to maturity

Floating interest rate

Hold to maturity

Non-investment grade

Illustrative Pricing

Upfront fee received Initial spread All-in spread* All-in yield to maturity

Up to 4% 3.75%-4.75% 3.95%-5.55% 5.95%-7.55%

Source: Revolution Asset Management. *Including upfront fees over a 5 year life.

Asset-Backed Securities (Private and Public)

Securitisation is the act of creating Asset-Backed Securities (ABS) from pools of underlying loans. It

begins with the formation of a special purpose vehicle (SPV), which is a company whose specific

purpose is to acquire assets and issue debt secured by those assets. ABS are the preferred way for

smaller banks and specialty finance companies to finance pools of familiar asset types, such as auto

loans, credit card receivables, mortgages, and business loans. Each underlying loan in a pool is a

contractual obligation to pay. Figure 10 illustrates this.

Figure 10: Securitisation and Asset-Backed Securities

Source: Revolution Asset Management.

Pool of Loan

Assets

Special Purpose

Vehicle (SPV)

Bond

Issuance

Bankruptcy

Remote & Insolvency

Proof

Class A

Senior

Class B

Subordinated

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 21

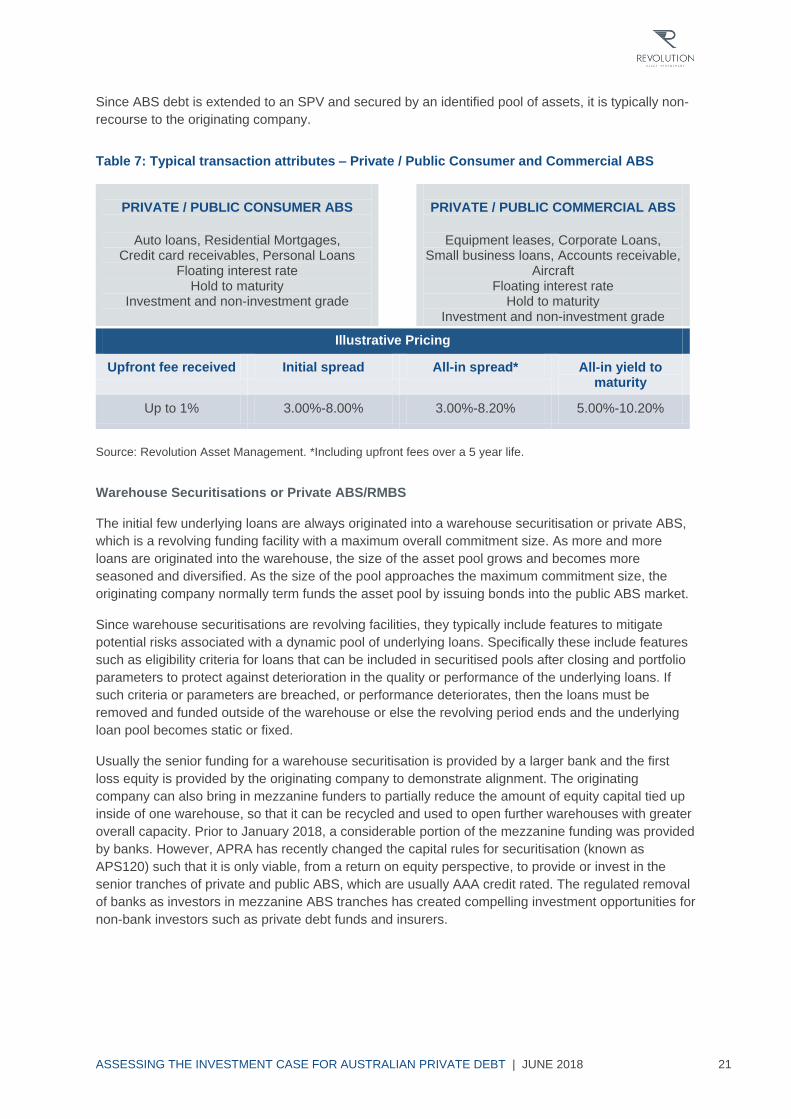

Since ABS debt is extended to an SPV and secured by an identified pool of assets, it is typically non-

recourse to the originating company.

Table 7: Typical transaction attributes – Private / Public Consumer and Commercial ABS

PRIVATE / PUBLIC CONSUMER ABS

Auto loans, Residential Mortgages, Credit card receivables, Personal Loans

Floating interest rate Hold to maturity

Investment and non-investment grade

PRIVATE / PUBLIC COMMERCIAL ABS

Equipment leases, Corporate Loans, Small business loans, Accounts receivable,

Aircraft Floating interest rate

Hold to maturity Investment and non-investment grade

Illustrative Pricing

Upfront fee received Initial spread All-in spread* All-in yield to maturity

Up to 1% 3.00%-8.00% 3.00%-8.20% 5.00%-10.20%

Source: Revolution Asset Management. *Including upfront fees over a 5 year life.

Warehouse Securitisations or Private ABS/RMBS

The initial few underlying loans are always originated into a warehouse securitisation or private ABS,

which is a revolving funding facility with a maximum overall commitment size. As more and more

loans are originated into the warehouse, the size of the asset pool grows and becomes more

seasoned and diversified. As the size of the pool approaches the maximum commitment size, the

originating company normally term funds the asset pool by issuing bonds into the public ABS market.

Since warehouse securitisations are revolving facilities, they typically include features to mitigate

potential risks associated with a dynamic pool of underlying loans. Specifically these include features

such as eligibility criteria for loans that can be included in securitised pools after closing and portfolio

parameters to protect against deterioration in the quality or performance of the underlying loans. If

such criteria or parameters are breached, or performance deteriorates, then the loans must be

removed and funded outside of the warehouse or else the revolving period ends and the underlying

loan pool becomes static or fixed.

Usually the senior funding for a warehouse securitisation is provided by a larger bank and the first

loss equity is provided by the originating company to demonstrate alignment. The originating

company can also bring in mezzanine funders to partially reduce the amount of equity capital tied up

inside of one warehouse, so that it can be recycled and used to open further warehouses with greater

overall capacity. Prior to January 2018, a considerable portion of the mezzanine funding was provided

by banks. However, APRA has recently changed the capital rules for securitisation (known as

APS120) such that it is only viable, from a return on equity perspective, to provide or invest in the

senior tranches of private and public ABS, which are usually AAA credit rated. The regulated removal

of banks as investors in mezzanine ABS tranches has created compelling investment opportunities for

non-bank investors such as private debt funds and insurers.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 22

Figure 11 illustrates how the warehouse process works for a Residential Mortgage Backed Security

(RMBS), which is a specific instance of an ABS where the underlying pool of loans consists of

residential mortgages.

Figure 11: Warehouse process for a Residential Mortgage Backed Security

Source: Westpac, Revolution Asset Management.

The principal job of ABS investors is to analyse the cash flows from the pool of underlying assets to

assess value and the possibility of loss, rather than relying on current market prices or an external

credit rating. From a historical perspective, the performance of Australian RMBS and ABS has been

strong, with Standard & Poors (S&P) confirming that in the 30 plus year history of the market, all

gross losses to date have been covered by lenders‘ mortgage insurance (LMI) claims paid and by

excess spread in the underlying pools. The strong performance can be attributed to the quality of

credit underwriting and the strong alignment of interest for loan originators through them being the

first to suffer from any credit losses.

Loans sold into warehouse

Bank funded

mortgage warehouse

Class A

Class B

Once the warehouse has

reached capacity, loans are

termed out via RMBS

Loans can again be sold

into the now empty

warehouse

Bank funded

mortgage warehouse

Term RMBS

issue

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 23

Figure 12 compares residential mortgages in Australia versus different European countries, and

illustrates the outstanding long term performance of the Australian market in a global context.

Figure 12: International Arrears

Source: Westpac, S&P.

The US mortgage market is not shown in the chart above because it is unique compared to all others.

The vast majority of US conforming mortgages ultimately end up being funded via one of the three

major government agencies (Ginnie Mae, Fannie Mae and Freddie Mac). The agencies guarantee the

credit risk of all the underlying loans which makes US RMBS essentially an interest rate product

because the underlying loans are all fixed rate and pre-payable. The US subprime mortgage market

was the epicentre of the GFC. It was a niche sub-sector of the US mortgage market outside of the

government agencies, targeting very high risk borrowers with poor credit histories and low incomes.

US subprime is only a fraction of the size it was before the GFC and its problems can be traced back

to extremely poor underwriting of credit risk as a result of poor alignment of interest with the loan

originators who were incentivised by volume alone.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 24

AUSTRALIAN PRIVATE DEBT

SIZE OF THE INVESTABLE & ATTRACTIVE SUB-SECTORS

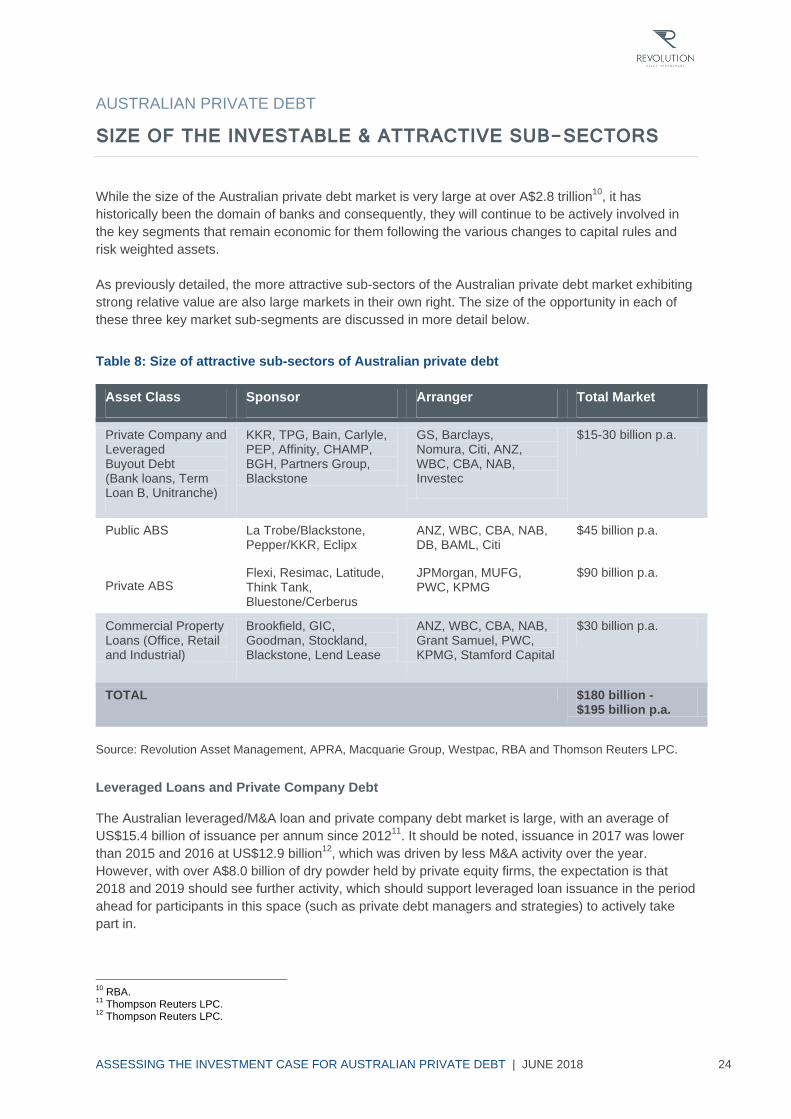

While the size of the Australian private debt market is very large at over A$2.8 trillion10

, it has

historically been the domain of banks and consequently, they will continue to be actively involved in

the key segments that remain economic for them following the various changes to capital rules and

risk weighted assets.

As previously detailed, the more attractive sub-sectors of the Australian private debt market exhibiting

strong relative value are also large markets in their own right. The size of the opportunity in each of

these three key market sub-segments are discussed in more detail below.

Table 8: Size of attractive sub-sectors of Australian private debt

Asset Class Sponsor Arranger Total Market

Private Company and Leveraged Buyout Debt (Bank loans, Term Loan B, Unitranche)

KKR, TPG, Bain, Carlyle, PEP, Affinity, CHAMP, BGH, Partners Group, Blackstone

GS, Barclays, Nomura, Citi, ANZ, WBC, CBA, NAB, Investec

$15-30 billion p.a.

Public ABS

Private ABS

La Trobe/Blackstone, Pepper/KKR, Eclipx

Flexi, Resimac, Latitude, Think Tank, Bluestone/Cerberus

ANZ, WBC, CBA, NAB, DB, BAML, Citi

JPMorgan, MUFG, PWC, KPMG

$45 billion p.a.

$90 billion p.a.

Commercial Property Loans (Office, Retail and Industrial)

Brookfield, GIC, Goodman, Stockland, Blackstone, Lend Lease

ANZ, WBC, CBA, NAB, Grant Samuel, PWC, KPMG, Stamford Capital

$30 billion p.a.

TOTAL $180 billion - $195 billion p.a.

Source: Revolution Asset Management, APRA, Macquarie Group, Westpac, RBA and Thomson Reuters LPC.

Leveraged Loans and Private Company Debt

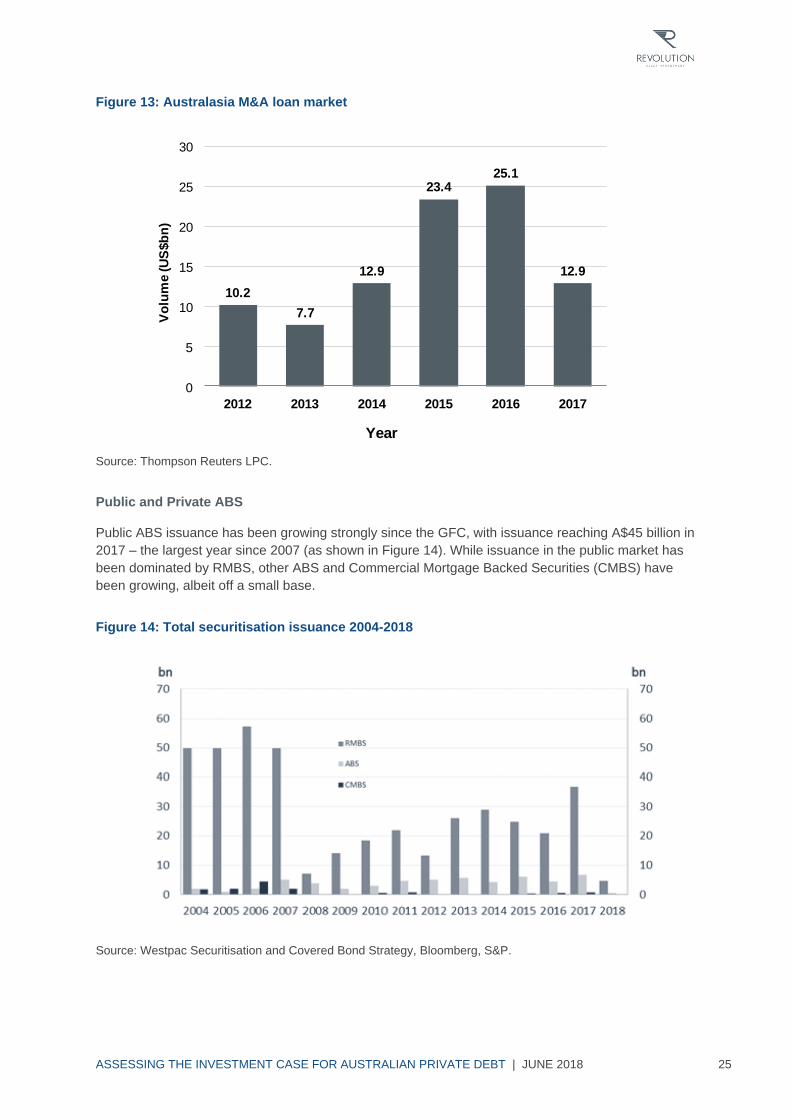

The Australian leveraged/M&A loan and private company debt market is large, with an average of

US$15.4 billion of issuance per annum since 201211

. It should be noted, issuance in 2017 was lower

than 2015 and 2016 at US$12.9 billion12

, which was driven by less M&A activity over the year.

However, with over A$8.0 billion of dry powder held by private equity firms, the expectation is that

2018 and 2019 should see further activity, which should support leveraged loan issuance in the period

ahead for participants in this space (such as private debt managers and strategies) to actively take

part in.

10

RBA. 11

Thompson Reuters LPC. 12

Thompson Reuters LPC.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 25

Figure 13: Australasia M&A loan market

Source: Thompson Reuters LPC.

Public and Private ABS

Public ABS issuance has been growing strongly since the GFC, with issuance reaching A$45 billion in

2017 – the largest year since 2007 (as shown in Figure 14). While issuance in the public market has

been dominated by RMBS, other ABS and Commercial Mortgage Backed Securities (CMBS) have

been growing, albeit off a small base.

Figure 14: Total securitisation issuance 2004-2018

Source: Westpac Securitisation and Covered Bond Strategy, Bloomberg, S&P.

10.2

7.7

12.9

23.425.1

12.9

0

5

10

15

20

25

30

2012 2013 2014 2015 2016 2017

Vo

lum

e (U

S$b

n)

Year

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 26

Figure 15: Estimated Non-ADI share of housing credit

Source: APRA, RBA.

The private ABS market is significantly larger than the public market, with Revolution Asset

Management estimating around A$90 billion of transactions in 2017 – approximately double that of

the public ABS market. This market is expected to continue to see strong transaction flow in the

coming years, largely supported by several large private equity funds investing into non-bank

originators13

. These non bank lenders will be armed with large amounts of equity capital to fund their

growth ambitions. At the same time banks will face increased regulatory pressure in the form of higher

risk weights, limits on investor and interest only loans and the recommendations from the recent

Royal Commission (Misconduct in the Banking, Superannuation and Financial Services Industry).

Overall, these factors are likely to see market share of housing credit shift from banks to non-bank

lenders, as they seek to regain the market share they lost following the GFC.

Commercial Real Estate Debt

The debt market for commercial real estate in Australia is material, with APRA figures as at 31

December 2017 showing that Authorised Deposit-taking Institutions (ADIs) had circa A$200 billion of

office, retail, and industrial property debt exposure. While commercial real estate loans are generally

3-7 years in tenor, this could see $30-70 billion in existing loans maturing each year. Additionally,

there are other opportunities such as new transactions that will require funding, as well as the

aforementioned impacts of increasing risk weights and capital charges on banks. This will likely result

in the banks lending on a lower loan to value ratio basis or, in some instances, not being willing to

refinance a loan and consequently requiring a third party to provide funding. Accordingly, it is

conservatively estimated that any given year will see around A$30 billion of commercial real estate

debt opportunities.

Overall, one can see that the markets for the most attractive sub-sectors of the Australian private debt

market are significant, with an aggregate size of approximately A$180-195 billion14

of issuance per

annum. In this regard, manager selection remains critical to ensure deep and wide origination

networks to take advantage of transactions that display the best risk-adjusted returns, while

maintaining credit discipline.

13

Examples here include Cerberus Capital Management acquiring Bluestone, KKR acquiring Pepper and Blackstone acquiring La Trobe financial.

14 Revolution Asset Management, APRA, Macquarie Group, Westpac, RBA and Thomson Reuters LPC.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 27

AUSTRALIAN PRIVATE DEBT

RELATIVE VALUE VS GLOBAL EQUIVALENTS

The relative attraction to the aforementioned sub-sectors is further supported by the relative value

they currently offer when compared to their offshore equivalents.

Figure 16 shows the US BB and B credit rated leveraged loan spreads15

versus the equivalent

indicative Australian loan spreads. Some of the key features highlighted here include the volatility of

the US market, especially when compared to the Australian market, and the spread comparison,

noting that the US B-rated index is currently tighter than Australian BB-rated indicative spreads.

Figure 16: Credit Suisse US Leveraged Loan Index – BB and B spreads

Source: Credit-Suisse, Loan Connector.

As can be seen in Figure 16, spreads in the Australian private debt market have been remarkably

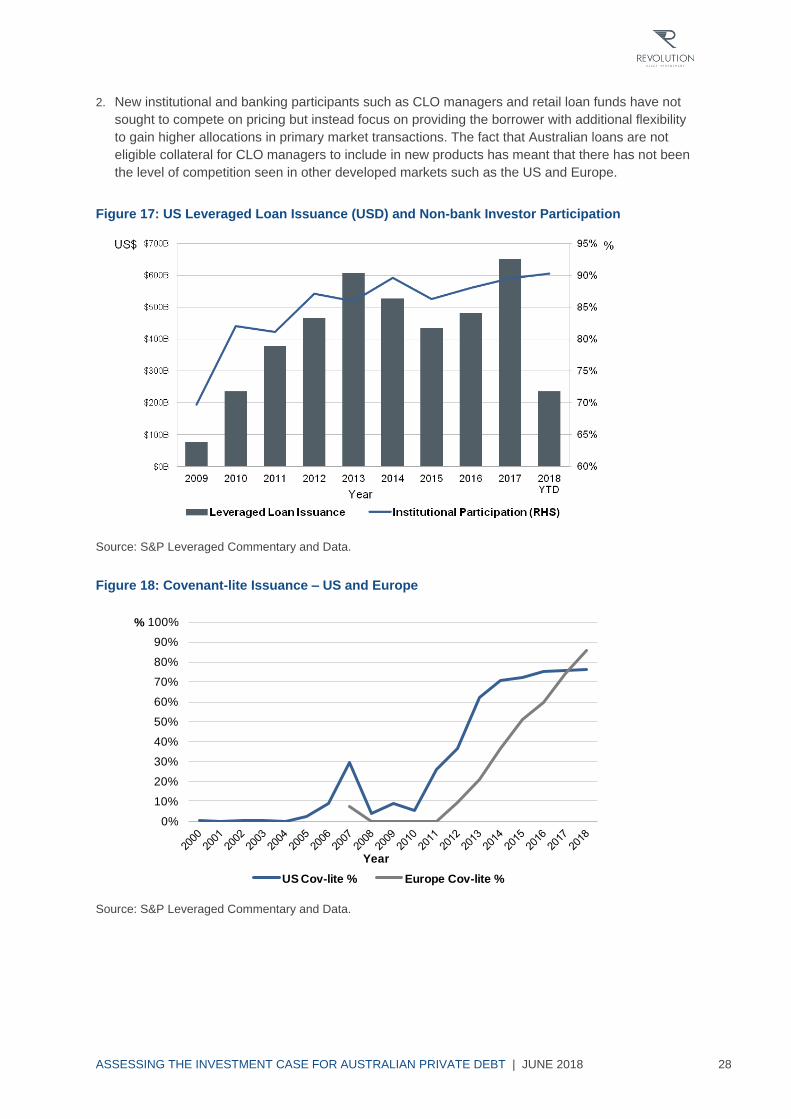

stable over a long period of time. This has been largely driven by two main factors:

1. The Australian leveraged loan market remains very much bank dominated with very low

institutional investor participation. This has allowed banks to maintain pricing discipline for given

credit risk over time. It is important to remember that banks are ultimately leveraged investors via

the ongoing regulatory capital framework, so their conservatism locally with respect to credit risk is

understandable. In other markets such as the US and Europe, participation is dominated by

institutional investors (see Figure 17) and banks play more of an intermediary role. The intense

competition for loan assets overseas has seen credit spreads fall sharply coupled with the

increasing sacrifice of structural protections for loan investors in the form of lending covenants

(see Figure 18).

15

Source: Credit Suisse.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 28

2. New institutional and banking participants such as CLO managers and retail loan funds have not

sought to compete on pricing but instead focus on providing the borrower with additional flexibility

to gain higher allocations in primary market transactions. The fact that Australian loans are not

eligible collateral for CLO managers to include in new products has meant that there has not been

the level of competition seen in other developed markets such as the US and Europe.

Figure 17: US Leveraged Loan Issuance (USD) and Non-bank Investor Participation

Source: S&P Leveraged Commentary and Data.

Figure 18: Covenant-lite Issuance – US and Europe

Source: S&P Leveraged Commentary and Data.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

US Cov-lite % Europe Cov-lite %

Year

%

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 29

This relative value is also evident in Australian ABS as illustrated in Figure 19. When compared to US

BBB rated CLOs (which offer the greatest credit margin for global ABS), Australian public market BBB

rated ABS are currently trading 50-125 basis points wider (at a spread of around 325 basis points to

400 basis points). The Australian and New Zealand private ABS warehouse market is generally

another 100 basis points wider again (150-225 basis points wider than US BBB-rated CLOs) with a

much shorter maturity. This represents outstanding global relative value given the exceptional long

term performance of the underlying pools.

Figure 19: Global Asset-Backed Securities (ABS) relative value

Source: Westpac, National Australia Bank, Wells Fargo.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 30

AUSTRALIAN PRIVATE DEBT

BARRIERS TO ENTRY

Local market attributes While it has already been recognised that the Australian private debt market is large and well-

established, there have been several barriers that have resulted in this asset class experiencing a low

level of institutional participation. These are explained in detail below.

Mandates

Being a largely illiquid asset class, market participants must be able to tolerate this key feature and

have a specific illiquid mandate in order to exploit the opportunities currently available in the local

market. This has resulted in more traditional fixed income managers, which usually promote the liquid

feature of their product, not being able to participate. Additionally, most traditional fixed income

products typically require an external credit rating from a credit rating agency such as Standard &

Poor’s, Moody’s or Fitch. With the Australian private debt market typically consisting of unrated

transactions, most traditional fixed income managers are unable to explore opportunities that have not

been rated by an external credit rating agency, limiting their ability to participate in the private debt

market.

Relationships – Origination

Relationships are critical when it comes to markets that are private in nature, due to transactions

being sourced from these key relationships. In this instance, participants require relationships with a

number of firms such as:

Sponsors: typically includes private equity firms for leveraged loans and non-bank lenders for ABS

transactions;

Banks: this would include the banks that arrange and syndicate transactions; and

Advisory firms: this includes a number of firms that are involved in debt advisory. These firms

typically have unique client bases that would require private debt solutions.

These relationships are built over many years and many transactions, making it difficult for new

participants to be able to enter the market successfully.

Expertise – Track Record

Private debt requires a high level of relevant expertise. This expertise is required across every facet of

originating a transaction such as negotiating key terms and conditions, as well as conducting the

underlying credit analysis and monitoring individual transactions. This is particularly relevant to

offshore participants looking at entering Australia, with local industries often displaying different

regulations and structures compared to their offshore equivalents, making it more difficult for offshore

based analysts/portfolio managers to properly analyse and scenario model illiquid Australian

industries and companies.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 31

Local Industry Knowledge

Whilst many leveraged loan managers in offshore jurisdictions have strong and deep credit teams to

enable assessment of loans and ABS, the knowledge and experience that these teams possess is not

always relevant in the Australian market. An example of this would be healthcare. The Australian

healthcare industry has its own regulations and nuances and is unique hence a US healthcare

industry expert would have little or no familiarity with how the industry operates in an Australian

context. A company specific example of local industry knowledge would be where we have a

dominant player in an industry such as ‘Boost Juice’ where this company has effectively created its

own category for fresh juices and smoothies in the local market. When comparing the scale of this

franchise operation versus a US franchise model it would seem as though Boost Juice would appear

more like a small start up, rather than a leading player, however it represents an attractive risk

adjusted local opportunity nonetheless. In this way local knowledge and familiarity with companies

operating in Australia is a distinct advantage to local managers over foreign domiciled fund managers

looking to enter the Australian market.

Hedging

Foreign participants would typically require the AUD currency risk to be hedged, to ensure their return is not adversely impacted by fluctuations in the Australian dollar. Given that Australian private debt instruments are typically callable in nature and often include contracted amortisation and excess cash flow sweeps, the cash flows from the underlying instrument are variable, making them difficult to hedge, unlike a daily traded liquid bond, which does not include amortisation or cash flow sweeps.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 32

AUSTRALIAN PRIVATE DEBT

THE ROLE IN A ‘LATE CYCLE’ PHASE

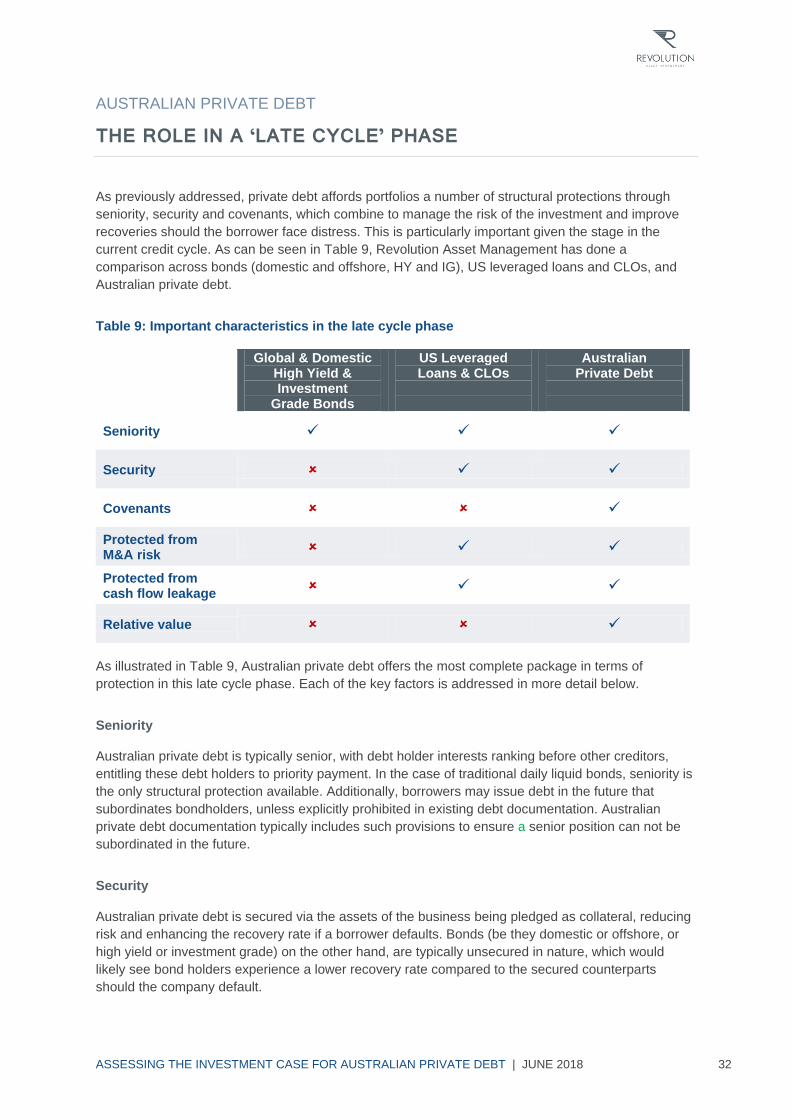

As previously addressed, private debt affords portfolios a number of structural protections through

seniority, security and covenants, which combine to manage the risk of the investment and improve

recoveries should the borrower face distress. This is particularly important given the stage in the

current credit cycle. As can be seen in Table 9, Revolution Asset Management has done a

comparison across bonds (domestic and offshore, HY and IG), US leveraged loans and CLOs, and

Australian private debt.

Table 9: Important characteristics in the late cycle phase

Global & Domestic High Yield & Investment

Grade Bonds

US Leveraged Loans & CLOs

Australian Private Debt

Seniority

Security

Covenants

Protected from M&A risk

Protected from cash flow leakage

Relative value

As illustrated in Table 9, Australian private debt offers the most complete package in terms of

protection in this late cycle phase. Each of the key factors is addressed in more detail below.

Seniority

Australian private debt is typically senior, with debt holder interests ranking before other creditors,

entitling these debt holders to priority payment. In the case of traditional daily liquid bonds, seniority is

the only structural protection available. Additionally, borrowers may issue debt in the future that

subordinates bondholders, unless explicitly prohibited in existing debt documentation. Australian

private debt documentation typically includes such provisions to ensure a senior position can not be

subordinated in the future.

Security

Australian private debt is secured via the assets of the business being pledged as collateral, reducing

risk and enhancing the recovery rate if a borrower defaults. Bonds (be they domestic or offshore, or

high yield or investment grade) on the other hand, are typically unsecured in nature, which would

likely see bond holders experience a lower recovery rate compared to the secured counterparts

should the company default.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 33

Covenants

Australian private debt transactions typically include covenants, which provide an early warning sign

in the event of any deterioration in creditworthiness. Importantly, covenants empower lenders (e.g.

private debt managers) to be able to engage with the company efficiently to ensure any weak

performance is rectified. This rectification could involve adjusting covenant levels to increase flexibility

(typically in exchange for a fee and/or an increase in the interest rate) for temporary issues, or closer

engagement with management to strengthen the balance sheet through a capital raising or asset

disposals for more challenging or permanent issues the business may encounter. This is something

that is generally not seen in the bond market or US leveraged loan market. In fact, around 80% of

leveraged loan issuance in the US and Europe have actually been covenant-lite16

, resulting in no or

minimal covenants to protect lenders. While this may be acceptable in a benign credit environment,

more challenging times will result in lenders being unable to intervene, driving a lower recovery rate.

M&A protection

Loan documentation typically includes limits on permitted acquisitions, resulting in the borrower not

being able to conduct M&A activity without the consent from the lending syndicate (which the private

debt manager would be the leader of or play a key part). Additionally, the documentation typically

contains change of control provisions, requiring all outstanding debt to be repaid should there be a

change of control event. This protects creditors in the event the borrower becomes a target and

becomes part of a more leveraged, less creditworthy company. Either outcome could involve the

consolidated entity holding materially more debt resulting in a weaker credit profile. Traditional daily

traded bonds do not offer such a protection, with numerous examples of multi-notch downgrades

which can impact bond prices following the announcement of M&A activity.

Protection from cash flow leakage

Cash flow leakage can occur in companies that issue daily liquid bonds, that may significantly affect

their credit worthiness and value. Examples would include a company paying out large dividends, a

special dividend or a share buyback. These are all equity-friendly initiatives which are considered

credit negative for the owner of daily liquid bonds due to the cash no longer being available to pay

debt holders. Australian public debt transactions typically trap all cash in the structure, resulting in

dividends generally not being able to be paid by the company, with any excess cash flow (that is,

cash flow after meeting operating expenses, principal and interest payments and any capital

expenditure) typically used to reduce outstanding debt. This is particularly important when looking at

publicly traded bonds (where company’s can pay large dividends or conduct share buy backs to the

detriment of the company’s credit profile) vs. the superior position in the capital structure of an

investment via private debt.

Relative value

As outlined above, Australian private debt offers attractive relative value, particularly across the three

sub-sectors identified, together with maintaining all the aforementioned protections.

The key factors identified above provide capital stability and security of income for investors via

Australian private debt which in summary offers seniority in the capital structure, security and

covenants, protection from M&A activity and cash flow leakage, as well as demonstrating attractive

superior relative value when compared to offshore markets.

16

S&P Leveraged Commentary and Data.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 34

CONCLUSION

Overall, Australian and New Zealand private debt offers a significant and immediate investment case

in the late market cycle for investors. The local private debt asset class is substantial at over A$2.8

trillion and is larger than the Bloomberg AusBond Composite Index and the S&P/ASX200 Index, and

comparable in size to the total Australian superannuation savings pool.

There are also a number of tailwinds supporting the asset class, while offering a number of portfolio

construction benefits such as low correlations to other asset classes together with diversification

benefits, structural protections (which have now diminished in offshore markets), lower volatility, a

steady income stream and inflation protection.

The investment universe is large with low levels of institutional investor participation, while offering

strong relative value. Australian private debt provides investors today with a compelling investment

opportunity.

ASSESSING THE INVESTMENT CASE FOR AUSTRALIAN PRIVATE DEBT | JUNE 2018 35

GLOSSARY

Asset-backed Securities (ABS)

An asset-backed security is a security that is backed by a pool of loans or receivables. These include

auto loans, consumer loans, commercial assets (e.g. aircraft and receivables), credit cards, home

equity loans and manufactured housing loans. ABS are essentially the same thing as a mortgage-

backed security except that the security backs assets such as personal loans, leases, credit card

debt, a company's receivables, royalties.

Collateralised Loan Obligation (CLO)

A collateralised loan obligation (CLO) is a security backed by a pool of debt, often low-rated corporate

loans. Collateralised loan obligations are similar to collateralised mortgage obligations (CMO), except

that the underlying loans are of a different type and character. With a CLO, the investor receives

scheduled debt payments from the underlying loans, assuming most of the risk in the event borrowers

default. In return for taking on the default risk, the investor is offered greater diversity and the potential

for higher-than-average returns.

Corporate Loans