private health insurance report card 2018 - … private health... · 1 the private hospital system...

TRANSCRIPT

PRIVATE HEALTH INSURANCE REPORT CARD 2018

CONTENTSINTRODUCTION ..........................................................................................................................................1

PRIVATE HEALTH CARE IN AUSTRALIA ................................................................................................3

How health care is funded .................................................................................................................. 3

Premiums ............................................................................................................................................... 3

Cover ...................................................................................................................................................... 3

Policies with restrictions ..................................................................................................................... 4

Out of pocket costs related to doctors’ fees ................................................................................... 4

Medicare freeze .................................................................................................................................... 5

No gap and known gap ....................................................................................................................... 5

BUPA’s new gap arrangements in 2018 - reducing choice .......................................................... 6

BENEFIT SCHEDULES AND OUT OF POCKET COSTS (GAPS) ..........................................................7

Changes in benefits ...........................................................................................................................10

State-based comparison of gaps ....................................................................................................10

Gaps ......................................................................................................................................................12

PRIVATE HEALTH INSURANCE PERFORMANCE ...............................................................................14

Growth in profits ..................................................................................................................................14

Growth in exclusions ...........................................................................................................................14

Growth in complaints ..........................................................................................................................15

TREATMENT OF PRIVATE PATIENTS IN PUBLIC HOSPITALS ........................................................19

PUBLISHING DOCTORS’ FEES ...............................................................................................................19

MORE INFORMATION ABOUT PRIVATE HEALTH INSURERS AND THEIR PRODUCTS ..............20

AMAPRIVATE HEALTH INSURANCE REPORT CARD 2018

1

The private hospital system is a key pillar of the Australian health care system. Private health insurance offers many Australians greater choice when it comes to their doctors and their treatment.

Private health insurance premiums continue to rise year on year – far beyond the consumer price and wage price indices. If affordability is not addressed, membership rates will continue to fall, threatening the viability of the entire health system.

While affordability is important to consumers, value is critical to patients. There is a complex and confusing array of private health insurance policy offerings, many with low benefits, differing definitions, exclusions, and restrictions.

Too often, patients only find out they aren’t covered when they go to use their insurance – even sometimes after a surgical procedure has taken place. Allowing restrictions to be hidden in the fine print is unconscionable. Policies must cover patients in private hospitals, unless they are specifically and clearly identifiable as ‘public hospital only’ policies.

But, equally, patients must be entitled to use their private health insurance in public hospitals, if they choose to do so. This right must remain and be protected. Ensuring that private patients can use their insurance in public hospitals is particularly important for those Australians living in rural and remote areas, where there is limited access to private hospitals, and for Australians to access particular specialist services which might only be available in a public hospital.

Reforming the system, improving valueThe Federal Government is in its second year of reviewing the private health system. The Opposition has also announced its approach to addressing private health insurance value and affordability, which will include a Productivity Commission review.

The Government’s Private Health Ministerial Advisory Committee (PHMAC) has to date deliberated on how to: develop clearer consumer communication; introduce standardised clinical definitions; retain second tier and default benefits; and reduce out of pocket costs.

As a result of this work, the Government has indicated insurers will be required to categorise products under gold, silver, bronze, and basic labels, and use standardised clinical definitions, among other improvements.

The AMA has long called for the simplification of health insurance policies, so that consumers understand what their policies will, and will not, cover. But it will be important that the reforms are more than a ‘rebadging’ of complex polices with a new label. That will not ensure the ongoing viability of the private system, nor will it make insurance easier to understand.

To that end, the AMA has called for improved clarity on policy coverage and an end to junk policies – policies that are designed to avoid the Medicare surcharge, but which do not clearly explain that they are limited to low levels of coverage. The AMA has also argued that there should be mandatory minimum levels of cover, including cover for obstetrics from bronze upwards, and that both community rating and the private health insurance rebate should remain in place.

The Government has made a start at reforming the system in other ways as well – bolstering the power of the Private Health Insurance Ombudsman (PHIO), allowing upgrades for mental

INTRODUCTION

2

health cover, and finding savings through cuts to the amount paid by insurers for prostheses. However far more structural change will need to be made if the system is to remain affordable for Australians in the coming years.

The AMA Private Health Insurance Report Card 2018Private health insurance is one of the largest single discretionary purchases that families make each year to manage unanticipated financial burdens. Families need to be assured that in the event they need health care, they can afford the treatment they need, at the time they need it. Private health insurance is a significant financial commitment, and therefore achieving value for money is extremely important.

This is the third in the AMA’s annual series of Report Cards on private health insurance, and continues to be designed to assist patients/consumers by highlighting the differences in private health insurance policies and the operations of funds.

The Report Card provides consumers with some indicators to help choose the right cover, noting that what is important in a health insurance product differs for each individual or family1.

This year’s Report Card provides the latest comparison of what proportion of hospital and medical costs are covered by each fund, examples across a number of common procedures of the different levels of benefits provided by funds, and Government data on complaints made about funds. These features can help consumers see the likelihood of facing out of pocket costs, and the ease of interacting with a fund. These differences can have a significant impact on the support a patient might experience from their health fund when they undergo treatment.

The Report Card also provides an overview of the financial health of the private health insurance industry, and an overview of the change in exclusions in policies over time.

Just as importantly, the Report Card highlights to patients/consumers how the private health system is funded, and promotes greater health literacy by showing the impact of differing gap cover arrangements on patient out of pocket costs.

This report is a compilation of information gathered from a range of sources and is not tailored for individual circumstances. As with any insurance product, consumers should consider carefully which product is right for them and seek professional advice where necessary. This Report Card is not intended as a substitute for professional advice.

We hope the Report Card encourages people to review their private health insurance policy to ensure it meets their needs.

Dr Michael GannonPresidentMarch 2018

1 The information in the tables in this report are current as at 9 March 2018 and are based on a detailed review of the policies offered by private health insurers, benefit schedules published by private health insurers, and information reported by the Private Health Insurance Ombudsman at www.phio.gov.au and the Australian Prudential Regulation Authority www.apra.gov.au. These reports are updated throughout the year and the date of the publication is noted in the citation.

3

How health care is fundedWorking out the right private health insurance can be a difficult task. Private health insurance can be complex and, when buying a new policy or switching policies, it is important to try and understand what treatments are covered, and to what level.

Australian health care funding is complicated.

There are three key funders of the system:

1. The Federal Government, through the Medicare Benefits Scheme (MBS).

2. Private health insurance.

3. The patient (through ‘out of pocket’ costs).

To avoid surprises when it comes to settling medical bills, it is useful to understand which parts of medical fees are covered by each of the three key funders.

If patients are treated by a doctor outside of a hospital as a non-admitted patient, whether that be a general practitioner or another specialist, health insurance policies cannot be used to cover these costs.

There are three aspects of private health insurance for hospital treatment that are most commonly misunderstood:

1. Not all private health insurance policies cover every medical treatment.

2. What is covered by a purchased policy can change, often without notice.

3. Patients will sometimes have out of pocket costs, even when their policy covers the medical treatment they need.

PremiumsA ‘premium’ is the amount consumers pay for a contract of their insurance. Premiums are an income source for insurers, which help pay for their business costs. Once a premium is received from a consumer, the insurer is liable for providing coverage for claims according to the terms and conditions of their insurance policy. Each year in April, private health insurance premiums are adjusted to meet the increasing costs of providing health care. The Federal Government must approve the rate before it comes into effect.

CoverDoctors working in the private health system from time to time see patients who think they are covered for treatment under their private health insurance policies, only to find out they are not. This is understandable – people often assume, based on the significant premiums they pay, that they must be covered for everything. However, the term ‘cover’ does not always mean fully insured for all costs associated with a particular treatment or medical service.

PRIVATE HEALTH INSURANCE IN AUSTRALIA

4

For services delivered to privately insured patients admitted into hospital, private health insurance covers some, or all, of the cost difference between a doctor’s fee and 75 per cent of the MBS fee (rebate) paid by the Federal Government.

When a patient is treated as a private patient, either in a public or private hospital, each of the doctors who is involved with their care can charge a fee for their services. In addition, the hospital will also charge a fee for the hospital accommodation and any other services.

Policies with restrictionsThere have been cases where treatment is planned and surgery is booked only to be cancelled shortly beforehand because, when the hospital checks the patient’s health insurance policy, they find that the level of insurance does not cover the patient for that particular treatment. The patient then needs to either upgrade their policy and serve a defined waiting period, or go on the public hospital waiting list. In the worst case, the unfortunate result is they can’t have the treatment they need, when they need it. This can be traumatic for the patient. It can have adverse health consequences.

It should be easy for consumers to know what their policy covers them for, and to be able to review it every year, to make sure it meets their changing needs and will continue to do so in the future.

Out of pocket costs related to doctors’ feesA long-standing concern for consumers is that they may face out of pocket costs for doctors’ fees for their treatment.

Doctors who treat patients will send them a bill for their services (a fee). Doctors, like other highly trained professionals, are free to set their fees at a level they believe is fair and reasonable. These fees take into account the cost of running a practice, including professional indemnity and other insurance, wages, rent, consumables, and other equipment costs.

If a patient is admitted to hospital (public or private), and they choose to be treated as a private patient, Medicare will pay for 75 per cent of the MBS fee for each service provided by a hospital doctor.

The out of pocket cost is the difference between the fees charged by the doctor and the combined MBS benefit and private health insurance benefit.

By law, private health insurers must top up the Medicare payment by least 25 per cent of the relevant MBS fee. Insurers can pay a higher level of benefit than this in particular circumstances. These circumstances are explained under the heading ‘no gap and known gap’ on page 5.

5

Medicare freezeThe Medicare freeze has effectively been in place since 2013. What this means is that the MBS rebate to the patient has been the same for more than five years. There has been no indexation of the MBS fee that the Government will fund or reimburse for a patient’s procedure. In the meantime, the cost of running a medical practice has increased year on year just like other private businesses. Over the years, the lack of MBS indexation has had a flow-on effect, which contributes to out of pocket costs.

Finally, after prolonged and consistent advocacy from the AMA , the Government agreed that on 1 July 2018 the Medicare freeze will be lifted for consultations. On 1 July 2019, the rebates for surgery and other procedures will be indexed. Indexation for the majority of pathology and diagnostic imaging items will remain frozen.

It is very important to note that when indexation recommences it will not be backdated to 2014 – meaning the Medicare rebates will continue to lag behind the true cost of providing a medical service.

No gap and known gapWhether or not a health insurer pays more than the minimum 25 per cent of the MBS fee required by law is something consumers need to check. It should be clearly and explicitly explained in every policy holder’s health insurance policy brochure.

No gap arrangement

Most private health insurers offer ‘no gap’ arrangements. This occurs when the doctor agrees with the insurer to charge the exact same amount that the insurer has agreed to pay for that medical service. In many cases, doctors provide the service at ‘no gap’2 and patients will not incur an out of pocket cost for this medical service. The agreed no gap fee is generally higher than the MBS fee.

Known gap arrangement

Some insurers will pay a benefit that includes a ‘known gap’. This is where the insurer will allow the doctor to charge a fee that is a set amount above the insurer’s total benefit amount (often a maximum of $400 - $500 above the agreed fee). The patient pays an out of pocket amount at the ‘known gap’ rate for the medical service.

No arrangement

When there is no arrangement between a doctor and an insurer, or the doctor charges more than the known gap, the difference between 100 per cent of the MBS rate and the doctor’s fee is made up by the patient’s out of pocket costs, which can increase significantly.

This is because the insurer in this situation will only pay the minimum benefit amount required - 25 per cent of the MBS fee.

2 APRA: Medical Gap Statistics December 2017 – 88.1 per cent of services delivered at no gap

6

3 https://media.bupa.com.au/faq-what-do-changes-to-the-medical-gap-scheme-mean-for-bupa-members/

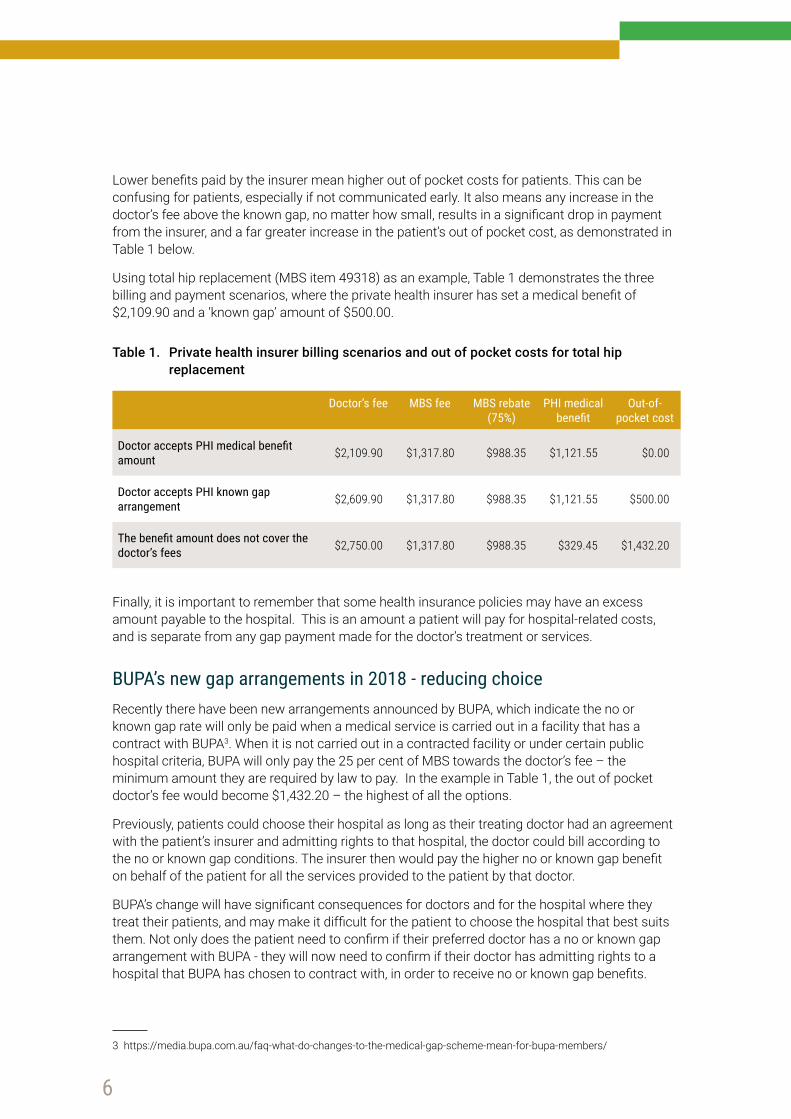

Lower benefits paid by the insurer mean higher out of pocket costs for patients. This can be confusing for patients, especially if not communicated early. It also means any increase in the doctor’s fee above the known gap, no matter how small, results in a significant drop in payment from the insurer, and a far greater increase in the patient’s out of pocket cost, as demonstrated in Table 1 below.

Using total hip replacement (MBS item 49318) as an example, Table 1 demonstrates the three billing and payment scenarios, where the private health insurer has set a medical benefit of $2,109.90 and a ‘known gap’ amount of $500.00.

Table 1. Private health insurer billing scenarios and out of pocket costs for total hip replacement

Doctor’s fee MBS fee MBS rebate (75%)

PHI medical benefit

Out-of-pocket cost

Doctor accepts PHI medical benefit amount $2,109.90 $1,317.80 $988.35 $1,121.55 $0.00

Doctor accepts PHI known gap arrangement $2,609.90 $1,317.80 $988.35 $1,121.55 $500.00

The benefit amount does not cover the doctor’s fees $2,750.00 $1,317.80 $988.35 $329.45 $1,432.20

Finally, it is important to remember that some health insurance policies may have an excess amount payable to the hospital. This is an amount a patient will pay for hospital-related costs, and is separate from any gap payment made for the doctor’s treatment or services.

BUPA’s new gap arrangements in 2018 - reducing choice Recently there have been new arrangements announced by BUPA, which indicate the no or known gap rate will only be paid when a medical service is carried out in a facility that has a contract with BUPA3. When it is not carried out in a contracted facility or under certain public hospital criteria, BUPA will only pay the 25 per cent of MBS towards the doctor’s fee – the minimum amount they are required by law to pay. In the example in Table 1, the out of pocket doctor’s fee would become $1,432.20 – the highest of all the options.

Previously, patients could choose their hospital as long as their treating doctor had an agreement with the patient’s insurer and admitting rights to that hospital, the doctor could bill according to the no or known gap conditions. The insurer then would pay the higher no or known gap benefit on behalf of the patient for all the services provided to the patient by that doctor.

BUPA’s change will have significant consequences for doctors and for the hospital where they treat their patients, and may make it difficult for the patient to choose the hospital that best suits them. Not only does the patient need to confirm if their preferred doctor has a no or known gap arrangement with BUPA - they will now need to confirm if their doctor has admitting rights to a hospital that BUPA has chosen to contract with, in order to receive no or known gap benefits.

7

The change will also have a significant impact on the contracting relationship between hospitals and insurers.

But of most concern to the AMA is that it will likely drive increased out of pocket costs for patients – as many may struggle, or be unaware they may only use their policies in the hospitals with which their insurer has a contract (or under specific conditions in a public hospital) in order to receive the full benefit of their insurance cover.

When insurance is already complicated, and when out of pocket costs are already an issue, this change by BUPA will only damage the value proposition of private health insurance further. It has the potential to remove patient choice, and it undermines the private health insurance reform efforts to date.

BENEFIT SCHEDULES AND OUT OF POCKET COSTS (GAPS)Each insurer has its own schedule of benefits for admitted medical services, but this is not always publicly available.

For admitted hospital treatments, the level of benefits paid by the insurer will depend on the insurer, the particular insurance policy, and the insurer’s arrangements with the treating doctor, and, after the latest insurer initiated changes, the treating hospital.

Private health insurers will generally aim to set premium levels to cover the expected costs of benefits plus the insurer’s management costs. However, the benefit that a insurer may agree to pay varies by insurer, policy, and procedure.

As discussed earlier, when there is a difference between the doctor’s fee and the insurance benefit, an out of pocket cost can occur. It is a common misunderstanding that the doctor’s fee is the reason for an out of pocket cost. Yet, as Table 2 demonstrates, there can be a significant difference in the amount an insurer will pay towards a medical service, and it varies insurer to insurer and procedure to procedure. Occasionally it varies from State to State, as outlined in Table 3.

Table 2 shows the different benefit amounts paid by insurers for a select range of common procedures. Red indicates the lower level of benefits paid and green shows which insurers pay a higher level of benefits. The scale is relative to the other benefits paid for the same procedure across the listed insurers.

It is important to note that not all private health insurers are listed in Table 2, and therefore the table does not represent the entire industry. Note these payments relate to the relevant item and insurer description and, as such, there may be additional items used for any particular procedure or service (i.e. pathology, diagnostic imaging, anaesthetics), or for any other doctors involved.

Generally speaking, the greater the benefits, the less likelihood of out of pocket costs.

8

Table 2: Varying benefit amounts paid by private health insurers in 2018

MBS Item MBS Description MBS Fee

ahm Health

InsuranceBUPA Pty

Ltd HCF

Medibank Private

Ltd

Mildura Health Fund

NIB Health Funds

LtdSt.Lukes Health AHSA

12203Overnight Investigation for sleep apnoea

588.00 694.25 703.45 758.50 694.25 735.00 713.00 709.45 684.40

13918 Cytotoxic Chemotherapy 97.95 115.55 118.05 128.30 115.55 122.45 111.40 119.90 108.00

16519 Uncomplicated Delivery (of baby) 693.95 1,886.95 2,057.05 2,058.95 1,886.95 1,353.25 1,550.95 1,995.50 1,610.00

16522 Complicated Delivery (of baby) 1,629.35 2,198.50 2,406.65 2,408.00 2,198.50 2,199.65 2,299.50 2,316.55 2,118.20

30445 Cholecystectomy 739.35 1,012.45 1,061.15 1,083.15 1,012.45 1,012.95 1,001.20 1,049.00 1,100.10

30572 Appendicectomy 445.40 609.95 639.25 652.50 609.95 610.20 602.00 631.85 636.40

30609 Femoral on Inguinal Hernia 464.50 636.05 666.65 680.50 636.05 636.40 627.80 660.10 920.00

31500Breast, benign lesion surgical biopsy or excision

260.05 355.30 382.95 380.95 355.30 356.30 351.45 368.65 358.60

32090 Colonoscopy 334.35 442.50 472.95 473.10 442.50 441.35 432.65 463.65 437.30

32139 Haemorrhoidectomy 367.75 503.80 520.20 520.35 503.80 485.45 475.90 526.70 608.40

32500 Varicose Veins 109.80 160.70 165.55 165.80 160.70 153.75 149.50 169.85 166.10

35657 Vaginal Hysterectomy 674.70 986.20 1,084.85 1,129.45 986.20 944.60 1,017.10 1,029.15 1,075.30

37623 Vasectomy 229.85 348.95 355.60 360.85 348.95 326.40 351.05 367.75 346.40

38306 Stent for Coronary artery 762.35 1,111.65 1,104.55 1,111.75 1,111.65 1,090.20 1,028.10 1,142.95 1,270.60

38500 Coronary Artery Bypass 2,200.00 3,265.15 3,316.75 3,432.00 3,265.15 3,080.00 3,090.55 3,419.80 3,820.00

39331 Carpal Tunnel Release 276.80 404.90 457.30 469.20 404.90 387.55 419.65 428.80 444.00

39709 Craniotomy 1,586.75 2,322.10 2,622.35 2,689.55 2,322.10 2,221.45 2,405.65 2,454.65 2,440.20

41789 Tonsils or Tonsils and Adenoids 295.70 472.35 485.00 561.85 472.35 425.85 443.55 496.40 519.00

42702 Cataract Surgery 760.65 1,126.25 1,192.65 1,293.10 1,126.25 1,064.95 1,150.60 1,168.45 1,250.80

49318 Hip Replacement 1,317.80 2,000.75 2,109.90 2,503.80 2,000.75 1,844.95 2,024.25 2,330.95 2,235.30

49518 Knee Replacement 1,317.80 2,000.75 2,109.90 2,503.80 2,000.75 1,844.95 2,024.25 2,330.95 2,592.30

Highest benefit paid Lowest benefit paid

1 2 3 4 5 6 7 8

Known Gap Arrangements - AHM up to a max. $500.00/claiming provider, BUPA up to $500.00/episode of care, HCF varies according to HCF known gap schedule, Medibank Private up to $500.00/doctor/claim, NIB not available, St Lukes within 10 per cent of their benefits schedule, AHSA up to $400.00 per item.This table was compiled from the Private Health Insurance Ombudsman’s (PHIO) List of the Health Funds with data from the Private Health Insurers’ own websites on 9 March 2018. While every care has been taken to provide accurate information, the AMA does not warrant the accuracy or currency of the information provided. Insurers can provide different benefits depending on the State where the procedure is performed. The NSW benefits lists for BUPA and AHSA were used. AHSA represents; ACA Health Benefits Funds, Australian Unity Health Ltd, CBHS Corporate Health Pty Ltd, CBHS Health Fund Ltd, CUA Health Ltd, Defence Health, Emergency Services Health Pty Ltd, GMHBA (Budget Direct Health Insurance & Frank Health Insurance), GU Health, HBF Ltd (except WA where a different schedule is used), Health Care Insurance Ltd, Health.com.au, Health Insurance Fund of Australia Ltd, Health Partners, MyOwn, Navy Health, Nurses & Midwives Health Pty Ltd, OneMediFund, Peoplecare Health Insurance, Phoenix Health Fund, Police Health Ltd, Queensland Country Health Fund Ltd (Territory Health Fund), Reserve Bank Health Society Ltd, RT Health Fund, Teachers Health (UniHealth Insurance), Teachers Union Health, The Doctors’ Health Fund Pty Ltd, Transport Health, Westfund. Insurers who have not published an online benefits schedule were not included.

9

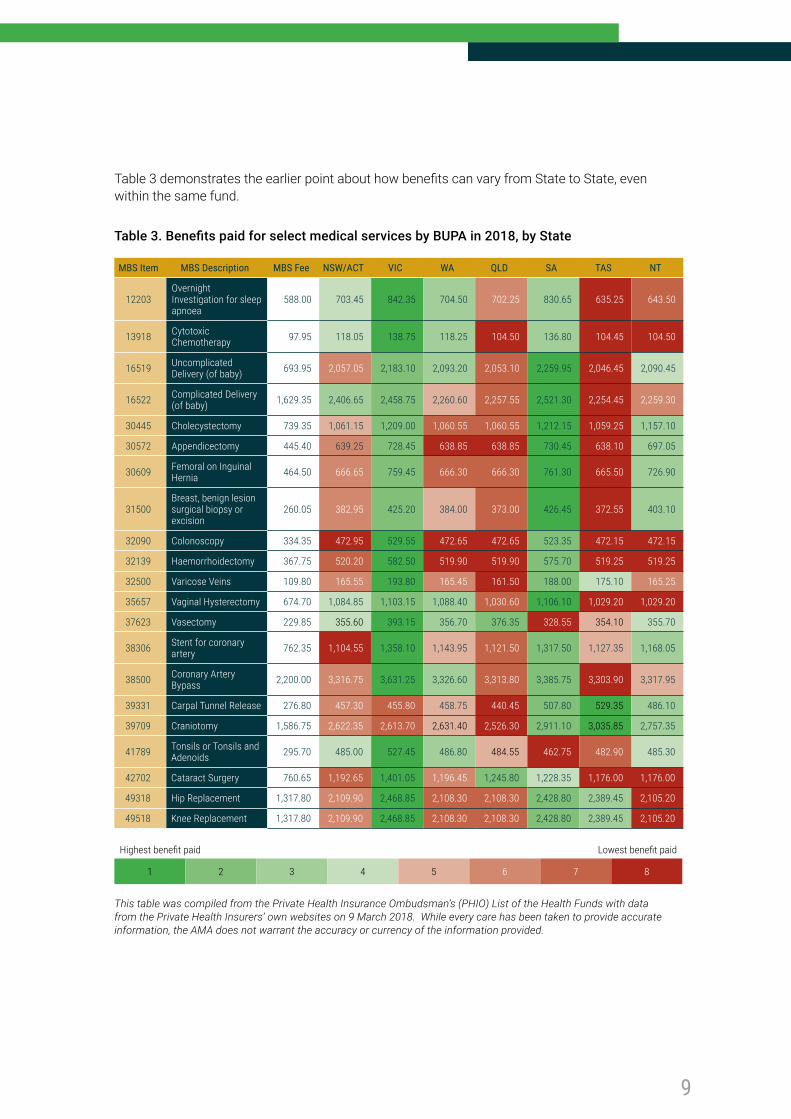

Table 3 demonstrates the earlier point about how benefits can vary from State to State, even within the same fund.

Table 3. Benefits paid for select medical services by BUPA in 2018, by State

MBS Item MBS Description MBS Fee NSW/ACT VIC WA QLD SA TAS NT

12203Overnight Investigation for sleep apnoea

588.00 703.45 842.35 704.50 702.25 830.65 635.25 643.50

13918 Cytotoxic Chemotherapy 97.95 118.05 138.75 118.25 104.50 136.80 104.45 104.50

16519 Uncomplicated Delivery (of baby) 693.95 2,057.05 2,183.10 2,093.20 2,053.10 2,259.95 2,046.45 2,090.45

16522 Complicated Delivery (of baby) 1,629.35 2,406.65 2,458.75 2,260.60 2,257.55 2,521.30 2,254.45 2,259.30

30445 Cholecystectomy 739.35 1,061.15 1,209.00 1,060.55 1,060.55 1,212.15 1,059.25 1,157.10

30572 Appendicectomy 445.40 639.25 728.45 638.85 638.85 730.45 638.10 697.05

30609 Femoral on Inguinal Hernia 464.50 666.65 759.45 666.30 666.30 761.30 665.50 726.90

31500Breast, benign lesion surgical biopsy or excision

260.05 382.95 425.20 384.00 373.00 426.45 372.55 403.10

32090 Colonoscopy 334.35 472.95 529.55 472.65 472.65 523.35 472.15 472.15

32139 Haemorrhoidectomy 367.75 520.20 582.50 519.90 519.90 575.70 519.25 519.25

32500 Varicose Veins 109.80 165.55 193.80 165.45 161.50 188.00 175.10 165.25

35657 Vaginal Hysterectomy 674.70 1,084.85 1,103.15 1,088.40 1,030.60 1,106.10 1,029.20 1,029.20

37623 Vasectomy 229.85 355.60 393.15 356.70 376.35 328.55 354.10 355.70

38306 Stent for coronary artery 762.35 1,104.55 1,358.10 1,143.95 1,121.50 1,317.50 1,127.35 1,168.05

38500 Coronary Artery Bypass 2,200.00 3,316.75 3,631.25 3,326.60 3,313.80 3,385.75 3,303.90 3,317.95

39331 Carpal Tunnel Release 276.80 457.30 455.80 458.75 440.45 507.80 529.35 486.10

39709 Craniotomy 1,586.75 2,622.35 2,613.70 2,631.40 2,526.30 2,911.10 3,035.85 2,757.35

41789 Tonsils or Tonsils and Adenoids 295.70 485.00 527.45 486.80 484.55 462.75 482.90 485.30

42702 Cataract Surgery 760.65 1,192.65 1,401.05 1,196.45 1,245.80 1,228.35 1,176.00 1,176.00

49318 Hip Replacement 1,317.80 2,109.90 2,468.85 2,108.30 2,108.30 2,428.80 2,389.45 2,105.20

49518 Knee Replacement 1,317.80 2,109.90 2,468.85 2,108.30 2,108.30 2,428.80 2,389.45 2,105.20

Highest benefit paid Lowest benefit paid

1 2 3 4 5 6 7 8

This table was compiled from the Private Health Insurance Ombudsman’s (PHIO) List of the Health Funds with data from the Private Health Insurers’ own websites on 9 March 2018. While every care has been taken to provide accurate information, the AMA does not warrant the accuracy or currency of the information provided.

10

4 The Private Health Insurance Ombudsman report, State of the Health Funds 2017, states on page 20 that this data includes: charges for hospital accommodation, theatre costs, prostheses and specialist fees (not including the Medicare benefit) and associated benefits (after any excesses and co-payments are deducted).

Changes in benefitsConsumers should check any information that they receive from their insurer. Consumers can experience a change to benefits in a number of ways, including through a change to an insurer’s rules or a change to an insurer’s arrangements with health care service providers.

Benefit changes are widespread and the Australian Competition and Consumer Commission (ACCC) suggests that these changes are increasing over time. Private health insurers should inform consumers clearly and promptly of any relevant changes to their benefits.

Unexpected changes to policies and benefits continue to be a concern for consumers, the medical profession, and government regulators. In 2016, the ACCC instituted proceedings against Medibank, alleging that Medibank made false, misleading, or deceptive representations and engaged in unconscionable conduct.

The ACCC alleged that Medibank failed to notify its members, and members of ahm (a subsidiary brand), of the decision to limit benefits for in-hospital pathology and radiology services, despite describing in some marketing materials that it would.

While the Medibank case was dismissed by the Federal Court, the ACCC has responded by lodging an appeal.

State-based comparison of gapsAs with the 2017 AMA Private Health Insurance Report Card, this report provides information on two different measures of insurance benefits:

• The percentage of hospital related charges covered (this includes accommodation at the hospital, provision of nursing care, and the cost of any prostheses)4 (see Tables 4 & 5).

• The percentage of medical services provided at no gap. This is the percentage of the doctor’s fees paid by that insurer that are provided with no gap (See Tables 6 & 7).

As demonstrated in Tables 4-7, this information is broken down by private health insurer on a State basis because the value of some insurers’ gap schemes and benefits schedules can differ between States, and these differences are not apparent in the national figures.

11

Table 4: Percentage of hospital related charges covered by State - Open membership funds

ACT NSW VIC QLD SA WA TAS NT

Australian Unity 85.1 87.4 90.7 88.6 92.1 88.8 90.0 83.6

BUPA 82.9 88.8 93.2 91.0 95.5 88.4 93.6 89.9

CBHS Corporate n/a 59.8 100.0 100.0 n/a n/a n/a n/a

CDH n/a 95.7 94.0 95.1 85.2 94.4 95.2 n/a

CUA Health 74.0 88.8 91.1 92.5 90.4 89.5 91.8 93.5

GMHBA 71.2 81.1 89.0 84.8 87.0 86.6 90.0 80.6

GU Corporate 85.8 86.5 90.4 87.9 87.9 87.9 88.2 81.5

HBF 83.8 89.4 93.8 91.6 93.3 96.0 95.1 91.2

HCF 87.5 93.1 93.8 92.4 95.3 90.1 93.7 88.8

HCI 84.4 88.3 94.2 89.2 94.7 95.7 95.8 95.3

Health.com.au 77.5 80.9 84.9 84.5 87.1 83.3 87.2 87.1

Health Partners 82.0 89.3 93.2 93.2 95.7 72.9 95.9 96.3

HIF 73.4 88.2 90.8 91.1 92.2 92.6 95.0 93.6

Latrobe 78.8 88.3 92.4 91.0 91.0 92.3 92.1 93.0

MDHF 84.7 93.1 93.6 93.2 91.8 94.3 89.9 95.4

Medibank 83.7 89.5 92.8 90.3 94.1 90.5 93.6 90.3

NIB 76.0 87.6 86.0 84.5 90.7 84.4 90.3 82.7

Onemedifund 97.8 93.0 95.3 92.8 96.8 95.1 96.6 n/a

Peoplecare 75.6 91.2 92.8 91.5 91.8 93.2 93.2 95.8

Phoenix 87.5 95.2 95.4 94.0 97.3 95.6 95.1 100.0

QCH 86.8 93.0 93.9 89.8 94.3 90.9 100.0 90.4

St Lukes 93.9 93.3 93.5 91.3 93.8 91.5 94.8 92.0

Transport Health 76.0 90.9 94.9 90.1 91.4 95.1 95.7 n/a

Westfund 87.3 93.8 95.7 92.2 97.3 96.3 96.1 91.6

Source: Private Health Insurance Ombudsman (PHIO): State of the Health Funds Report 2017

12

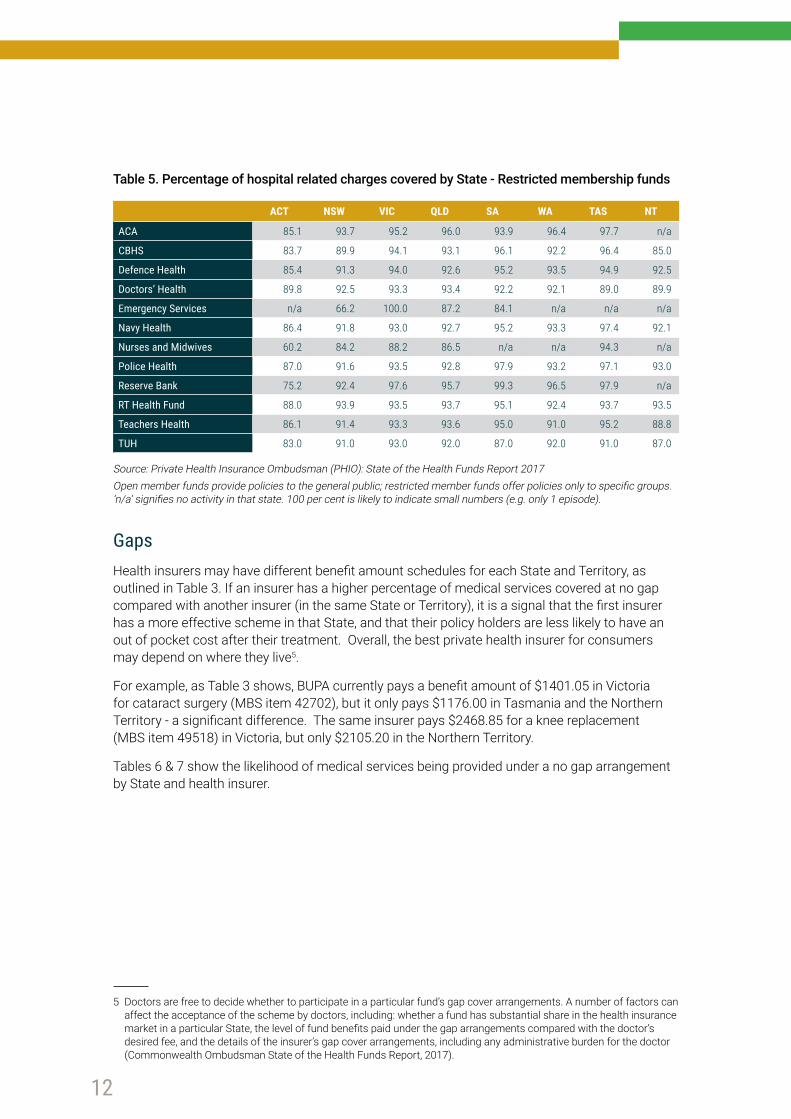

Table 5. Percentage of hospital related charges covered by State - Restricted membership funds

ACT NSW VIC QLD SA WA TAS NT

ACA 85.1 93.7 95.2 96.0 93.9 96.4 97.7 n/a

CBHS 83.7 89.9 94.1 93.1 96.1 92.2 96.4 85.0

Defence Health 85.4 91.3 94.0 92.6 95.2 93.5 94.9 92.5

Doctors’ Health 89.8 92.5 93.3 93.4 92.2 92.1 89.0 89.9

Emergency Services n/a 66.2 100.0 87.2 84.1 n/a n/a n/a

Navy Health 86.4 91.8 93.0 92.7 95.2 93.3 97.4 92.1

Nurses and Midwives 60.2 84.2 88.2 86.5 n/a n/a 94.3 n/a

Police Health 87.0 91.6 93.5 92.8 97.9 93.2 97.1 93.0

Reserve Bank 75.2 92.4 97.6 95.7 99.3 96.5 97.9 n/a

RT Health Fund 88.0 93.9 93.5 93.7 95.1 92.4 93.7 93.5

Teachers Health 86.1 91.4 93.3 93.6 95.0 91.0 95.2 88.8

TUH 83.0 91.0 93.0 92.0 87.0 92.0 91.0 87.0

Source: Private Health Insurance Ombudsman (PHIO): State of the Health Funds Report 2017Open member funds provide policies to the general public; restricted member funds offer policies only to specific groups. ‘n/a’ signifies no activity in that state. 100 per cent is likely to indicate small numbers (e.g. only 1 episode).

GapsHealth insurers may have different benefit amount schedules for each State and Territory, as outlined in Table 3. If an insurer has a higher percentage of medical services covered at no gap compared with another insurer (in the same State or Territory), it is a signal that the first insurer has a more effective scheme in that State, and that their policy holders are less likely to have an out of pocket cost after their treatment. Overall, the best private health insurer for consumers may depend on where they live5.

For example, as Table 3 shows, BUPA currently pays a benefit amount of $1401.05 in Victoria for cataract surgery (MBS item 42702), but it only pays $1176.00 in Tasmania and the Northern Territory - a significant difference. The same insurer pays $2468.85 for a knee replacement (MBS item 49518) in Victoria, but only $2105.20 in the Northern Territory.

Tables 6 & 7 show the likelihood of medical services being provided under a no gap arrangement by State and health insurer.

5 Doctors are free to decide whether to participate in a particular fund’s gap cover arrangements. A number of factors can affect the acceptance of the scheme by doctors, including: whether a fund has substantial share in the health insurance market in a particular State, the level of fund benefits paid under the gap arrangements compared with the doctor’s desired fee, and the details of the insurer’s gap cover arrangements, including any administrative burden for the doctor (Commonwealth Ombudsman State of the Health Funds Report, 2017).

13

Table 6. Percentage of medical services with no gap – Open member funds

ACT NSW VIC QLD SA WA TAS NT

Australian Unity 83.6 90.9 92.7 92.0 93.4 88.7 92.7 86.6

BUPA 78.5 84.2 86.4 82.1 85.4 73.4 86.6 80.2

CBHS Corporate n/a 70.0 100.0 100.0 n/a n/a n/a n/a

CDH n/a 87.4 n/a n/a n/a n/a n/a n/a

CUA Health 86.2 90.5 91.3 93.4 85.4 87.7 92.8 85.1

GMHBA 58.3 76.3 76.9 81.9 77.0 71.5 74.9 74.1

GU Corporate 78.7 87.8 92.1 88.3 92.3 85.5 92.3 93.6

HBF 55.4 65.4 66.1 66.2 57.7 87.8 62.1 46.2

HCF 80.9 91.0 89.3 92.0 90.3 85.2 90.8 86.3

HCI 86.3 88.8 90.4 89.4 90.4 93.0 93.9 97.0

Health.com.au 74.4 84.6 87.4 87.2 84.0 84.2 91.1 85.1

Health Partners 76.7 88.3 91.5 93.0 93.8 85.2 81.5 94.0

HIF 74.6 84.1 88.2 89.0 88.8 87.0 92.7 88.9

Latrobe 50.8 75.7 79.9 81.4 76.7 76.3 68.0 58.0

MDHF 83.2 80.6 81.8 83.0 86.3 72.3 61.5 69.4

Medibank 79.8 88.4 84.6 87.6 90.3 73.6 92.2 81.6

NIB 67.5 88.8 82.2 84.1 91.7 74.7 82.9 80.2

Onemedifund 87.6 89.4 90.0 91.2 91.1 85.9 94.2 n/a

Peoplecare 74.9 92.4 91.2 91.4 89.9 89.3 94.4 82.7

Phoenix 74.1 92.2 91.2 92.2 94.3 86.5 95.4 100.0

QCH 31.6 92.2 92.1 91.8 89.9 85.7 92.7 86.1

St Lukes 77.3 81.3 80.8 80.3 79.9 71.3 91.8 93.3

Transport Health 59.3 87.4 92.2 89.3 89.9 59.0 99.1 n/a

Westfund 66.9 86.0 84.6 85.4 91.3 86.2 76.9 62.9

Source: Private Health Insurance Ombudsman (PHIO) – State of the Health Funds Report 2017This table shows the average for the listed health funds, but individual results vary.

Table 7. Percentage of medical services with no-gap – Restricted member funds

ACT NSW VIC QLD SA WA TAS NT

ACA 83.3 90.8 93.6 93.4 96.4 91.0 93.7 n/a

CBHS Health 80.4 88.7 91.4 92.4 90.8 86.8 95.2 82.7

Defence Health 79.3 89.2 91.7 92.7 90.7 88.2 93.3 88.5

Doctors’ Health 88.7 92.1 93.7 94.4 92.8 89.1 93.3 76.1

Emergency Services n/a 60.0 n/a 51.9 100.0 n/a n/a n/a

Navy Health 78.7 89.8 92.1 91.3 92.7 87.1 92.6 89.0

Nurses and Midwives 100.0 85.7 76.1 38.2 n/a n/a 100.0 n/a

Police Health 83.5 91.0 88.7 88.9 91.8 84.3 93.0 85.8

Reserve Bank 58.1 89.9 93.5 94.0 96.1 90.6 92.2 n/a

RT Health Fund 81.5 92.9 92.1 93.3 94.2 86.3 93.3 87.7

Teachers’ Health 84.6 90.2 91.1 92.9 91.1 85.4 94.4 91.5

TUH 78.3 88.8 92.0 92.6 90.6 89.5 91.9 80.9

Source: Private Health Insurance Ombudsman (PHIO) – State of the Health Funds Report 2017This table shows the average for the listed health funds, but individual results vary. ‘n/a’ signifies no activity or very low activity in that State. 100 per cent is likely to indicate small numbers of services provided (i.e. only one episode).

14

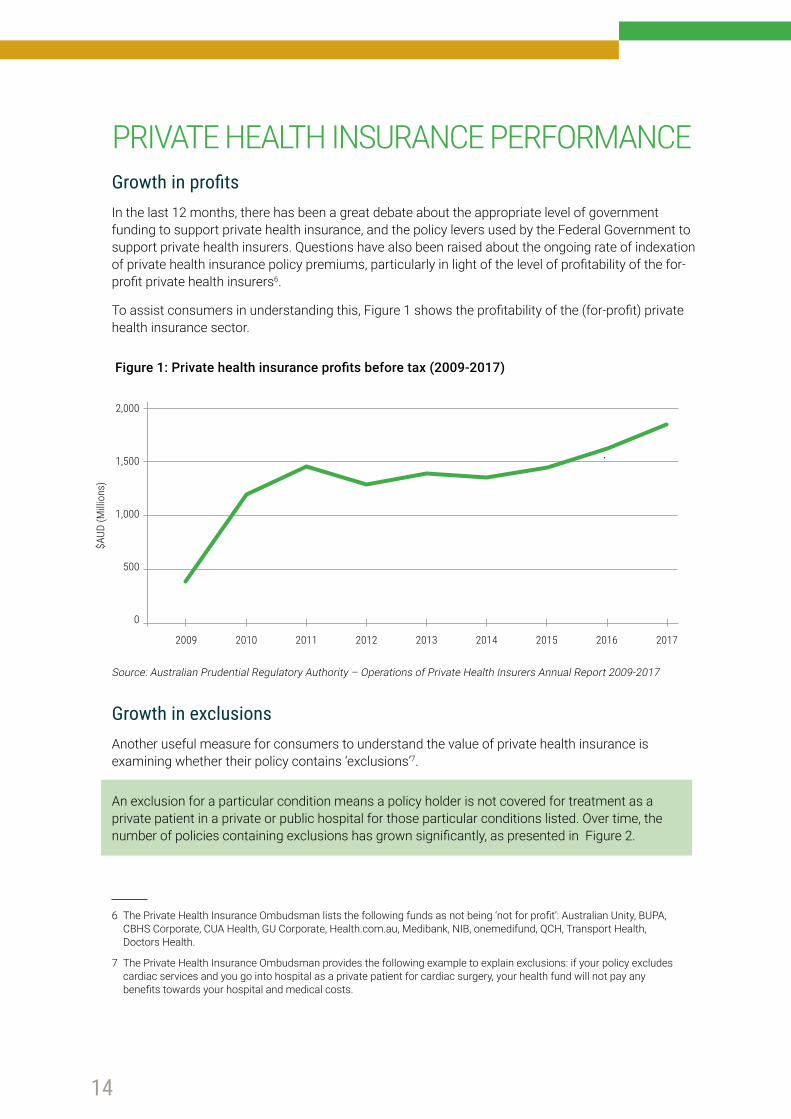

PRIVATE HEALTH INSURANCE PERFORMANCE Growth in profits In the last 12 months, there has been a great debate about the appropriate level of government funding to support private health insurance, and the policy levers used by the Federal Government to support private health insurers. Questions have also been raised about the ongoing rate of indexation of private health insurance policy premiums, particularly in light of the level of profitability of the for-profit private health insurers6.

To assist consumers in understanding this, Figure 1 shows the profitability of the (for-profit) private health insurance sector.

Figure 1: Private health insurance profits before tax (2009-2017)

Source: Australian Prudential Regulatory Authority – Operations of Private Health Insurers Annual Report 2009-2017

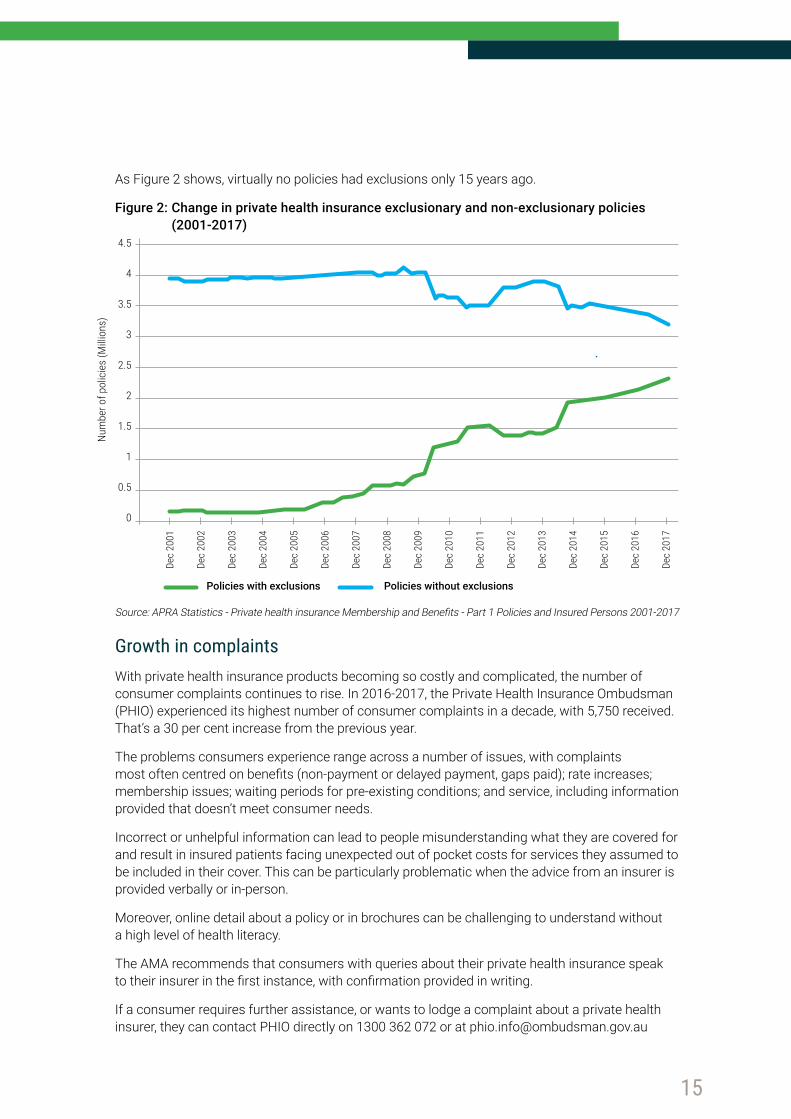

Growth in exclusionsAnother useful measure for consumers to understand the value of private health insurance is examining whether their policy contains ‘exclusions’7.

An exclusion for a particular condition means a policy holder is not covered for treatment as a private patient in a private or public hospital for those particular conditions listed. Over time, the number of policies containing exclusions has grown significantly, as presented in Figure 2.

2,000

1,500

1,000

500

0

2009

$AUD

(Milli

ons)

2010 2011 2012 2013 2014 2015 2016 2017

6 The Private Health Insurance Ombudsman lists the following funds as not being ‘not for profit’: Australian Unity, BUPA, CBHS Corporate, CUA Health, GU Corporate, Health.com.au, Medibank, NIB, onemedifund, QCH, Transport Health, Doctors Health.

7 The Private Health Insurance Ombudsman provides the following example to explain exclusions: if your policy excludes cardiac services and you go into hospital as a private patient for cardiac surgery, your health fund will not pay any benefits towards your hospital and medical costs.

15

As Figure 2 shows, virtually no policies had exclusions only 15 years ago.

Figure 2: Change in private health insurance exclusionary and non-exclusionary policies (2001-2017)

Source: APRA Statistics - Private health insurance Membership and Benefits - Part 1 Policies and Insured Persons 2001-2017

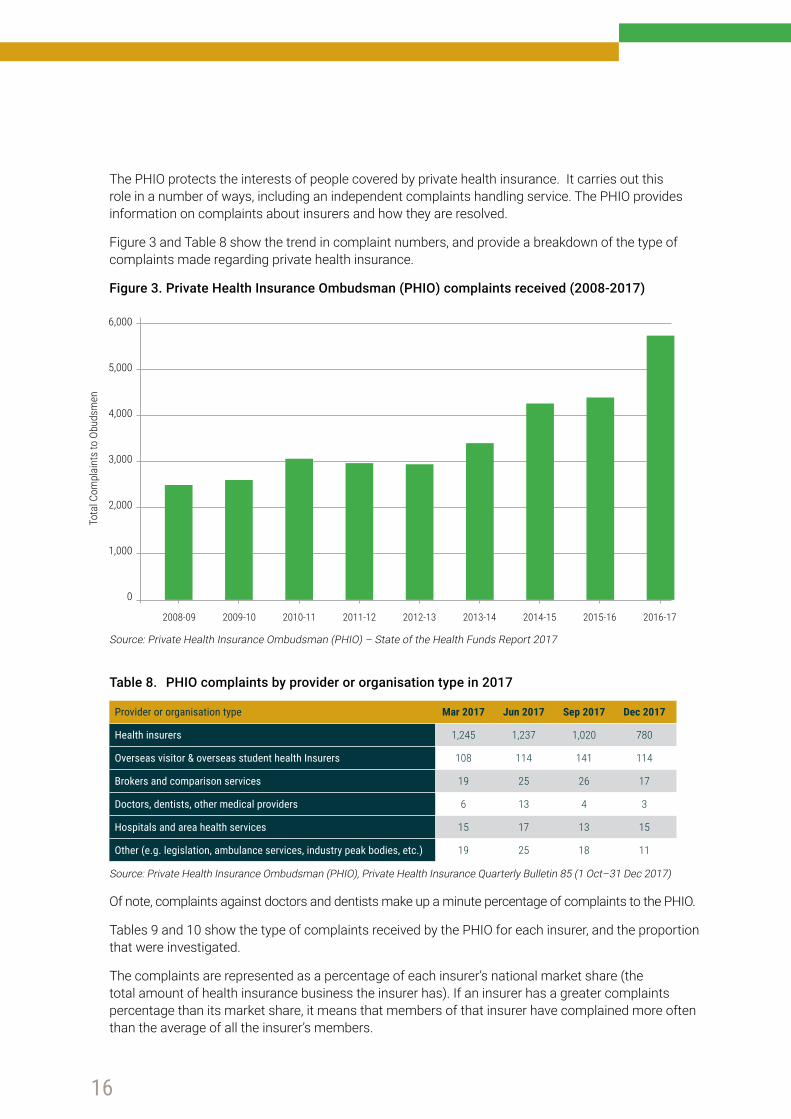

Growth in complaintsWith private health insurance products becoming so costly and complicated, the number of consumer complaints continues to rise. In 2016-2017, the Private Health Insurance Ombudsman (PHIO) experienced its highest number of consumer complaints in a decade, with 5,750 received. That’s a 30 per cent increase from the previous year.

The problems consumers experience range across a number of issues, with complaints most often centred on benefits (non-payment or delayed payment, gaps paid); rate increases; membership issues; waiting periods for pre-existing conditions; and service, including information provided that doesn’t meet consumer needs.

Incorrect or unhelpful information can lead to people misunderstanding what they are covered for and result in insured patients facing unexpected out of pocket costs for services they assumed to be included in their cover. This can be particularly problematic when the advice from an insurer is provided verbally or in-person.

Moreover, online detail about a policy or in brochures can be challenging to understand without a high level of health literacy.

The AMA recommends that consumers with queries about their private health insurance speak to their insurer in the first instance, with confirmation provided in writing.

If a consumer requires further assistance, or wants to lodge a complaint about a private health insurer, they can contact PHIO directly on 1300 362 072 or at [email protected]

4.5

4

3.5

3

2.5

2

1.5

1

0.5

0

Dec

2001

Dec

2002

Dec

2003

Dec

2004

Dec

2005

Dec

2006

Dec

2007

Dec

2008

Dec

2009

Dec

2010

Dec

2011

Dec

2012

Dec

2013

Dec

2014

Dec

2015

Dec

2016

Dec

2017

Num

ber o

f pol

icie

s (M

illion

s)

Policies with exclusions Policies without exclusions

16

The PHIO protects the interests of people covered by private health insurance. It carries out this role in a number of ways, including an independent complaints handling service. The PHIO provides information on complaints about insurers and how they are resolved.

Figure 3 and Table 8 show the trend in complaint numbers, and provide a breakdown of the type of complaints made regarding private health insurance.

Figure 3. Private Health Insurance Ombudsman (PHIO) complaints received (2008-2017)

Source: Private Health Insurance Ombudsman (PHIO) – State of the Health Funds Report 2017

Table 8. PHIO complaints by provider or organisation type in 2017

Provider or organisation type Mar 2017 Jun 2017 Sep 2017 Dec 2017

Health insurers 1,245 1,237 1,020 780

Overseas visitor & overseas student health Insurers 108 114 141 114

Brokers and comparison services 19 25 26 17

Doctors, dentists, other medical providers 6 13 4 3

Hospitals and area health services 15 17 13 15

Other (e.g. legislation, ambulance services, industry peak bodies, etc.) 19 25 18 11

Source: Private Health Insurance Ombudsman (PHIO), Private Health Insurance Quarterly Bulletin 85 (1 Oct–31 Dec 2017)

Of note, complaints against doctors and dentists make up a minute percentage of complaints to the PHIO.

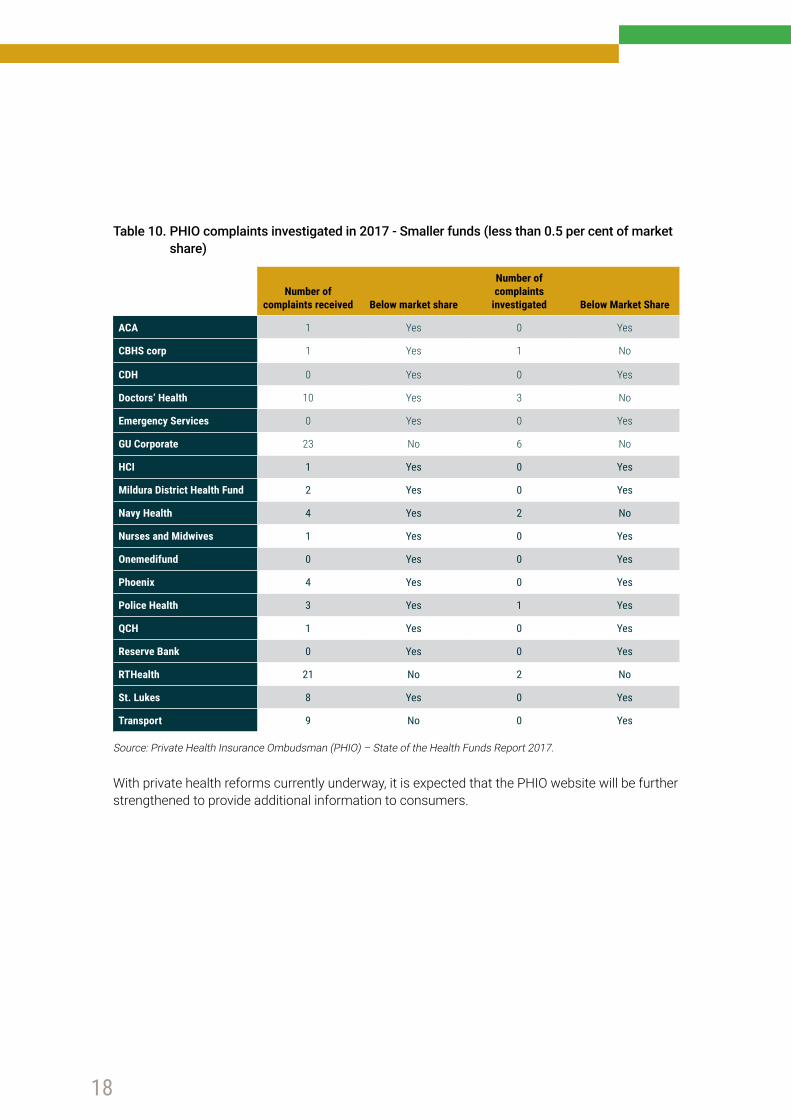

Tables 9 and 10 show the type of complaints received by the PHIO for each insurer, and the proportion that were investigated.

The complaints are represented as a percentage of each insurer’s national market share (the total amount of health insurance business the insurer has). If an insurer has a greater complaints percentage than its market share, it means that members of that insurer have complained more often than the average of all the insurer’s members.

6,000

5,000

4,000

3,000

2,000

1,000

0

Tota

l Com

plai

nts

to O

buds

men

2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17

17

Benefit complaints – e.g. non-payment or delayed payment, benefit level paid or gap paid by the fund’s member

Service complaints – e.g. quality of customer service provided by the fund, problems with premium payments

If the matter requires further intervention by the PHIO, it is lodged as a ‘complaints investigated’ and used as a measure of each funds’ internal complaints-handling processes.

It should be noted that the number of complaints received is small compared to overall insurer membership.

Table 9. PHIO complaints investigated in 2017 - Larger funds (greater than 0.5 per cent of market share)

Market Share

Complaints as a proportion of market share %

Benefits Service All ComplaintsComplaints investigated

Australian Unity 3 5.2 3.6 4.8 5.9

BUPA 26.9 21 9.9 17.6 27.4

CBHS 1.5 0.5 0.2 0.6 0.6

CUA Health 0.6 1.5 0.5 1.5 5

Defence Health 2 0.9 0.5 0.7 0.2

GMHBA 2.3 3.1 0.8 2 1.8

HBF 8 4.3 2.8 4.4 2.4

HCF 10.4 10.7 4.8 9.7 11.6

Health Partners 0.6 0.3 0.2 0.3 0.6

Health.com.au 0.6 2.1 0.3 1.2 2.8

HIF 0.9 0.4 0.3 0.6 0.2

Latrobe 0.7 0.4 0.1 0.2 0.4

Medibank 26.9 34.4 71.4 46.3 26.3

NIB 8.3 8.5 3 6.1 8.5

Peoplecare 0.5 0.3 0 0.2 0

Teachers Health 2.3 2.9 0.8 1.5 2.4

TUH 0.6 0.6 0 0.4 0.7

Westfund 0.7 0.1 0 0.1 0.6

Source: Private Health Insurance Ombudsman (PHIO) – State of the Health Funds Report 2017.

18

Table 10. PHIO complaints investigated in 2017 - Smaller funds (less than 0.5 per cent of market share)

Number of complaints received Below market share

Number of complaints

investigated Below Market Share

ACA 1 Yes 0 Yes

CBHS corp 1 Yes 1 No

CDH 0 Yes 0 Yes

Doctors’ Health 10 Yes 3 No

Emergency Services 0 Yes 0 Yes

GU Corporate 23 No 6 No

HCI 1 Yes 0 Yes

Mildura District Health Fund 2 Yes 0 Yes

Navy Health 4 Yes 2 No

Nurses and Midwives 1 Yes 0 Yes

Onemedifund 0 Yes 0 Yes

Phoenix 4 Yes 0 Yes

Police Health 3 Yes 1 Yes

QCH 1 Yes 0 Yes

Reserve Bank 0 Yes 0 Yes

RTHealth 21 No 2 No

St. Lukes 8 Yes 0 Yes

Transport 9 No 0 Yes

Source: Private Health Insurance Ombudsman (PHIO) – State of the Health Funds Report 2017.

With private health reforms currently underway, it is expected that the PHIO website will be further strengthened to provide additional information to consumers.

19

TREATMENT OF PRIVATE PATIENTS IN PUBLIC HOSPITALSThe Federal Government recently announced, as part of the ‘Heads of the Agreement between the Commonwealth and the States and Territories on public hospital funding and health reform’, there will be work undertaken to examine the underlying drivers of growth in the number of private patients in public hospitals. The Government will also review admission policies and practices, and examine the impact of changes to the Medicare principles.

The AMA continues to argue that it is vitally important that patients with private health insurance maintain the choice to be treated in a public hospital rather than a private hospital. These patients are able to choose their doctor, but, depending on their insurance cover, may not have the choice of a private room. As with the private system, there may be fees for the doctor and hospital accommodation costs.

There are a variety of reasons a privately insured patient may choose to be treated in a public hospital. These include:

• Their preferred doctor has a private practice at that hospital.• Their doctor is the only specialist in their area who treats their particular medical problem.• The public hospital may be the only hospital with the appropriate technology for the treatment

needed.• It may be the closest hospital to the patient’s home and family.• A public hospital may be the most cost effective choice of hospital for patients who are only

insured on policies with restricted benefits.

PUBLISHING DOCTORS’ FEESThe subject of publication of doctors’ fees has recently become an area of media and public interest, and is seen by some as an ‘easy way’ to tackle medical out of pocket costs.

In 2017, the Federal Government established a Ministerial advisory committee as part of a wider private health insurance review to address increasing concerns regarding out of pocket costs.

The committee’s stated role is to “ensure a collaborative approach in determining the best model to make information on out of pocket costs charged by doctors more transparent and to help consumers with private health insurance better understand out of pocket costs”.

The AMA is strongly committed to information sharing between a doctor and a patient to create an agreed treatment plan, and to understand its associated costs.

To that end, the AMA publishes extensive information on Informed Financial Consent, Billing Practices, guides, and suggested questions for patients to ask their doctor, so they fully understand their individual situation.

However, the publication via a website of potential fees for every doctor and every procedure is impractical, and potentially unhelpful.

20

A patient’s out of pocket costs are determined by numerous factors, including:

• which MBS item number is used for their particular operation; • whether they are actually covered for that procedure; • whether the doctor has an agreement with the health fund; • what other doctors and tests are involved; • whether the hospital has an agreement with the health fund; • the clinical terminology and the benefit rate set by the fund; and• what State they live in.

One specialist could use a large number of item numbers in their practice, which would make for a website with over a thousand figures listed for that doctor’s procedures, once the number of different funds and their differing benefit rates are taken into account.

Also, simply publishing one fee for a particular treatment or procedure may mislead consumers, as it ignores clinical factors like the complexity of the procedure for that patient, who may have other health issues.

It also has the potential to confuse if all of these factors are not taken into account. As demonstrated throughout this year’s Report Card, a patient’s out of pocket cost comes about from the doctor’s fee and by the benefit paid by a fund. These rates are not uniform across insurers, procedures, States, and hospital setting.

Given that the vast majority of services are provided by doctors at no additional cost to the patient, a comprehensive table of fees would not be meaningful.

A general practitioner who has an ongoing relationship with their patient is best placed to refer for appropriate specialist care. A doctor should be prepared to outline their estimated costs when contacted by patients, particularly for standard treatments or initial consultations.

MORE INFORMATION ABOUT PRIVATE HEALTH INSURERS AND THEIR PRODUCTSGovernment informationThe Australian Government hosts a website that provides:

• more detailed information about how private health insurance works; • a tool for comparing the features of policies; and • the Standard Information Statements for every policy.

Visit www.privatehealth.gov.au

More information about medical feesTo read more about how the health care system funds Australians’ medical care, visitwww.ama.com.au/article/guide-patients-how-health-care-system-funds-medical-care

To read more about Informed Financial Consent for medical bills, visit www.ama.com.au/article/ama-informed-financial-consent

21

22

42 Macquarie Street Barton ACT 2600Telephone: 02 6270 5400www.ama.com.au