assessing international diversification of west german

TRANSCRIPT

Strategic Management Journal, Vol. 8, 25-37 ( I 987)

/ ASSESSING INTERNATIONAL DIVERSIFICATION OF WEST GERMAN CORPORATIONS

L

ROLF BUHNER University of Passau, Passau, West Germany c

While product diversity has primarily attracted strategic management scholars, this paper examines the performance of corporate international diversif cation f r o m a market point of view. The results indicate that in a highly industrialized, but relatively small, West German market, companies going abroad create shareholder wealth.

INTRODUCTION

The purpose of the present study is to analyze the effects of international diversification of firms in Western Germany on market performance. If international corporate diversification has value to shareholders, a revaluation of the shares of those companies expanding in foreign markets should be observed. On a priori grounds, international diversification allows application of firm-specific know-how to penetration of prospective foreign markets and allows extension of the business which the firm knows best. Also, German manufacturing markets are relatively small; therefore firms diversifying internationally could profit from economies of large-scale pro- duction.

There are some attempts in modern financial theory to study aspects of international diversifi- cation. The financial argument is based on the internationalization of the capital market function as the rationale for diversification. In contrast, strategic management scholars are more inter- ested in economies from product-investment

* An earlier version of this paper was presented at the Fourth Annual Strategic Management Society Conference, October l(k13, 1984, Philadelphia, Pennsylvania.

decisions concerning core skill factors as central to the logic of corporate diversification. However, the strategic management perspective has been limited to product diversity and there has been no comprehensive attempt to explain international diversification. Hence, in analyzing international diversification it seems promising to incorporate finance theory into a strategic management view, highlighting the diversification issue of international corporate diversification as an investment option creating probable share- holder wealth.

The international diversification move has become an increasingly important aspect of corporate strategy of German corporations. Exports have nearly doubled (1982: DM 428 billion) and foreign direct investments have more than doubled from DM 43 billion to DM 95 billion during the period from 1976 through 1982. In particular, the large U.S. market has attracted German firms’ investment decisions.

As reported in a questionnaire study about the motives of international diversification (Ruppert, 1979), business executives gave, as the primary motive, ‘protect foreign sales through closer market representation’. The motive ‘wage cost differences’ followed in second place. The motives ‘evade import restrictions’, ‘transport cost advan-

0 143-2095/87/010025-13$06.50 0 1987 by John Wiley & Sons, Ltd.

Received 9 November 1984 Revised 22 July 1985

26 R. Buhner

tages’, and ‘exchange risk avoidance’ followed in order. However, smaller firms stressed wage cost differences, whereas larger firms (with more than 1000 employees) stressed securing sales.

INVESTOR INTERNATIONAL DIVERSIFICATION VERSUS CORPORATE INTERNATIONAL DIVERSIFICATION

To the extent that economic activity in different countries is less than perfectly correlated, diversi- fication across international boundaries should improve investors’ risk-return opportunities. As several empirical studies have suggested, individ- ual investors benefit from international portfolio diversification (Grubel, 1968; Levy and Sarnat, 1970; Grubel and Fadner, 1971; Solnik, 1974; Lessard, 1976; Rugman, 1976; Atherton and Yap, 1979; Barnett, 1979). According to the risk-return characteristics of investments, the benefits come in the form of risk reduction without diminishing expected returns or through risk-adjusted returns outperforming an achievable nationally diversified portfolio. However, the realization of potential benefits at the shareholder level depends upon capital market imperfections that prevent an arbitrage process from functioning (Cohn and Pringle, 1973). Among the factors responsible for imperfect and partially segmented markets are certain official restrictions such as controls on portfolio capital flows, differential trading costs, tax differences, exchange rate risks, and perhaps even more important, the bounded rationality of investors and the cost of information on foreign securities. Hence investors may actu- ally not be diversifying internationally; thus firms going abroad may perform a diversification service for investors. If so, shareholders can gain some benefits of international portfolio diversification from an investment in firms engaged in foreign activities that cannot be achieved through a similar investment in purely domestic firms.

Evidence concerning international diversifi- cation at the corporate level as a wealth-increasing strategy for shareholders is controversial and sparse. In a partial and indirect test of whether the international composition of a firm’s operations is reflected in the market behavior of its securities, the results of Agmon and Lessard (1977) show

significant differences between the market- assigned risk measures of U.S. firms with different degrees of international involvement. In contrast, a study by Jacquillat and Solnik (1978) unexpect- edly shows limited influence of foreign factors on the systematic market risk measures of U.S. multinational firms compared to the extent of the firms’ foreign activities. What the authors contend is that investing in U.S. multinational firms cannot be regarded as a valid substitute to international portfolio diversification.

Assessing shareholders wealth position it is necessary to measure both risk and return. Hughes, Logue and Sweeney (1975) have tested the proposition that if investors recognize the diversification aspects of multinational firms, and they are willing to pay something for this, then the distribution of risk-return performance for multinational firms should exceed the correspond- ing distribution for domestic firms. They found that when risk was measured using a domestic market index, the performance of multinational firms was significantly superior to comparable domestic firms. As the performance differential was fading using a world market index, it was suspected that assets were priced internationally rather than domestically. However, empirical stud- ies by Agmon (1972) and Stehle (1977) indicate that neither the national segmented nor the international one-market pricing hypotheses can be rejected in favor of the other.

Controversial evidence has come from recent studies. While Brewer (1981) found no statistical difference in the risk-adjusted performance of multinational and national firm stocks, some more support to a superior market performance through firms’ international diversification move- ment is given by Mikhail and Shawky (1979), and recently by Errunza and Senbet (1984).

PRODUCT DIVERSIFICATION VERSUS INTERNATIONAL DIVERSIFICATION

Empirical studies about the performance of product diversification strategy are somewhat ambiguous. As proposed by the seminal work of Rumelt (1974) a related-constrained strategy performed best on the average. Controlling for industry effects or market structure variables, pursuing studies by Christensen and Montgomery (1981), Bettis and Hall (1982), as well as

International Diversification in West Germany 27

by Rumelt (1982) shows results supporting a ‘defensive diversification’ conclusion. Diversifi- cation is thereupon a strategy avoiding adverse effects on profitability from developments taking place in the firm’s traditional product market areas preserving the values of ongoing organiz- ations and restoring the earning power of the entity (Weston and Mansinghka, 1971). The defensive nature of diversification is embedded in life cycle considerations (Mueller, 1972). Depending on the stage of a firm’s development there is a point where diversification offers a more profitable way to reinvest earned cash flow than traditional lines of business do. If there is no alternative use of assets, profit-maximizing firms will repurchase stock.

From the policy perspective the key issues are whether or not a firm’s businesses are related due to its distinctive properties, and the extent to which those special skills are involved in various diversification moves. In an amalgamation with the market failures argument, asset speci- ficity arising either in the form of proprietary know-how or of indivisible physical assets circum- scribes impacts of shared input factors on the efficiency of the multiproduct firm (Williamson, 1975, 1981; Teece, 1980; Dundas and Richardson, 1980). From this point of view the transfer of proprietary know-how to alternative activities and the shared use of indivisible assets yielding scale economies are likely to generate scope economies (Panzar and Willig, 1981), if disecon- omies of organizational implementation are not seriously countereffective. Consequently, a firm possessing primarily specific intangible assets- such as innovative product or process knowledge, trademark, quality expertise, sales promotions techniques etc.-is supposed to be a successful one in its national market and to be able to use these capabilities in foreign markets. Whether export, licensing, or direct investment, inter- national corporate diversification offers the opportunity to exhaust all economies of scale in the distinctive domain without the necessity to resort to product diversity in order to obtain increased utilization of the generic asset base. Therefore performance effort by international real asset diversification seems not so much confounded by effects of diseconomies of organiz- ational scale as obviously associated with increased product diversity. In the same vein it is more rational to go abroad rather than battling

for marginal market shares or new product market areas at home (Delacroix, 1984). The rationale is that the opportunity cost of using the core skills in new markets is close to zero, and can be considered underutilized as long as the earned marginal revenue is positive.

omics that firms most likely operating on a multinational basis are those in industries charac- terized by high technological capability (e.g. Horst, 1972; Wolf, 1977). Furthermore the international move receives impetus from special product supply for differentiated market segments or size-related standard products with global economies of manufacturing and marketing scale (Johnson, 1970; Caves, 1971; Caves et al . , 1980). While the product differentiation motive is exemplified by German automobile firms, or machine producers serving the U.S. market, the second global strategy is pursued by giant chemical or electrical firms.

Since economies of scale are exhausted more fully in a country with a large and geographically diversified market, firms in such countries, and in industries where economies of scale are substantial, may stay at home and will not serve foreign markets. Testing West German corporations from this aspect it could be that gains from diversification are culture-specific due to the smaller geographic and economic size of the home market. Conversely, the large and regionally well diversified U.S. market might be attractive for scale-sensitive foreign firms since they can obtain efficient scale more fully.

There is ample evidence from industrial econ- ~

DATA, MEASURES, AND METHODS

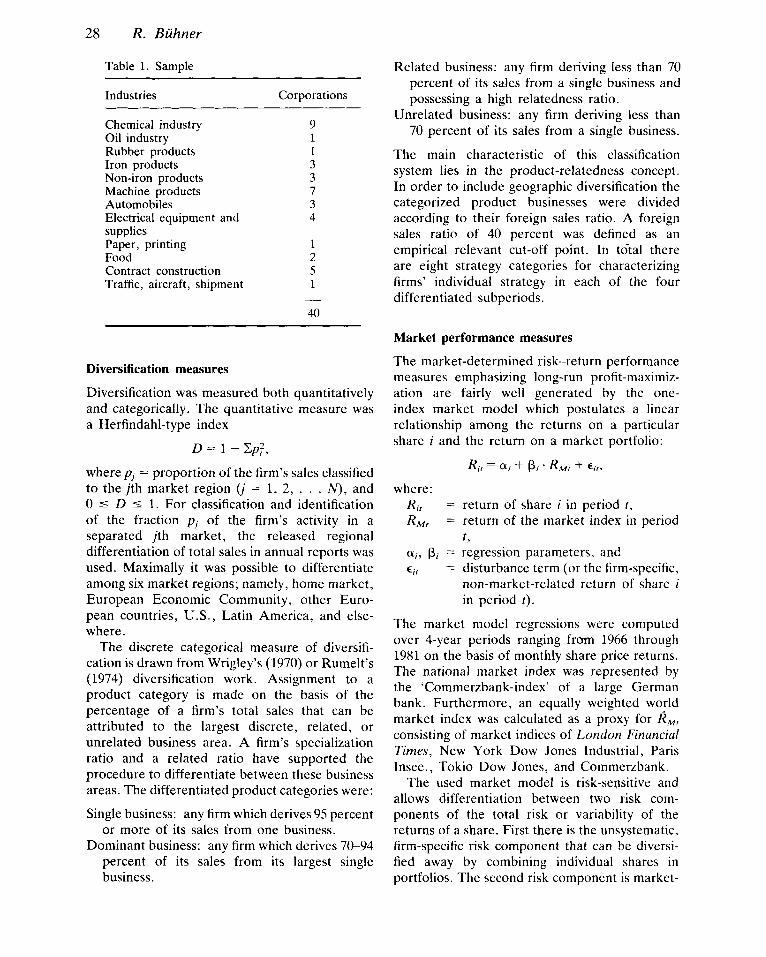

The study is based on data from a sample consisting of 40 large West German corporations of the top 300 firms in Western Germany. Selection criteria were related to published information in the annual reports about diversifi- cation measurement requirements. The sample firms spread over the major industries and are all stock exchange noted in Frankfurt. The sample corporations with their major industries in terms of the German SIC categories are shown in Table 1. The time period under study ranges from 1966 through 1981. The calculations of the following measures are based on equidistant 4-year sub- periods.

28 R. Buhner

Table 1. Sample

Industries Corporations

Chemical industry Oil industry Rubber products Iron products Non-iron products Machine products Automobiles Electrical equipment and supplies Paper, printing Food Contract construction Traffic, aircraft, shipment

9 1 1 3 3 7 3 4

1 2 5 1

40 -

Related business: any firm deriving less than 70 percent of its sales from a single business and possessing a high relatedness ratio.

Unrelated business: any firm deriving less than 70 percent of its sales from a single business.

The main characteristic of this classification system lies in the product-relatedness concept. In order to include geographic diversification the categorized product businesses were divided according to their foreign sales ratio. A foreign sales ratio of 40 percent was defined as an empirical relevant cut-off point. In total there are eight strategy categories for characterizing firms’ individual strategy in each of the four differentiated subperiods.

Diversification measures

Diversification was measured both quantitatively and categorically. The quantitative measure was a Herfindahl-type index

D = 1 - &I;,

where p, = proportion of the firm’s sales classified to the j th market region (j = 1, 2, . . . N), and 0 5 D 5 1. For classification and identification of the fraction p , of the firm’s activity in a separated jth market, the released regional differentiation of total sales in annual reports was used. Maximally it was possible to differentiate among six market regions; namely, home market, European Economic Community, other Euro- pean countries, U.S., Latin America, and else- where.

The discrete categorical measure of diversifi- cation is drawn from Wrigley’s (1970) or Rumelt’s (1974) diversification work. Assignment to a product category is made on the basis of the percentage of a firm’s total sales that can be attributed to the largest discrete, related, or unrelated business area. A firm’s specialization ratio and a related ratio have supported the procedure to differentiate between these business areas. The differentiated product categories were:

Single business: any firm which derives 95 percent or more of its sales from one business.

Dominant business: any firm which derives 70-94 percent of its sales from its largest single business.

Market performance measures

The market-determined risk-return performance measures emphasizing long-run profit-maximiz- ation are fairly well generated by the one- index market model which postulates a linear relationship among the returns on a particular share i and the return on a market portfolio:

R;, = CK; + p;. RM, + E;,, where:

Ri, =

RMr

Pi = - -

€it

return of share i in period t , return of the market index in period t , regression parameters, and disturbance term (or the firm-specific, non-market-related return of share i in period t ) .

The market model regressions were computed over 4-year periods ranging from 1966 through 1981 on the basis of monthly share price returns. The national market index was represented by the ‘Commerzbank-index’ of a large German bank. Furthermore, an equally weighted world market index was calculated as a proxy for I?,, consisting of market indices of London Financial Times, New York Dow Jones Industrial, Paris Insee., Tokio Dow Jones, and Commerzbank.

The used market model is risk-sensitive and allows differentiation between two risk com- ponents of the total risk or variability of the returns of a share. First there is the unsystematic, firm-specific risk component that can be diversi- fied away by combining individual shares in portfolios. The second risk component is market-

International DiversiJication in West Germany 29

related and it is this systematic risk portion of the return, or measured as ‘beta’ in the market model equation, that cannot be eliminated in a well-diversified portfolio.

It is the unsystematic risk component that does not matter from the point of view of a rational, risk-averse investor. But as Peavy (1984) has shown, this diversification effect of risk-reduction does not mean that unsystematic risk should go unmanaged from a corporate level. However, an individual stock’s beta depends on the total risk of the stock’s return. Therefore unsystematic risk affects beta. In that vein some researchers have suggested that the market-related beta risk component is affected by structured business factors such as operating and financial leverage (Beaver and Manegold, 1975; Montgomery and Singh, 1984).

The calculated risk-adjusted performance measure was adopted from Jensen (1969): Rir - R, = ai+ Pi(RMr - RF) + eir, where RF is a risk-free rate of return (interest rate of fixed deposits), and ‘&’ the proposed performance measure. Westerfield (1970) has suggested that &; is a good indicator of strategic relevant synergy effects, e.g. obtained by matching strategy and structure.

Investor buying and selling decisions are based on observable economic events, mainly released accounting numbers. Traditionally, return on assets and return on equity have appeal to shareholders in a sense of signalling a firm’s long- term future. The additional use of both measures will supplement the measured market prices, albeit published accounting data are prior subject to serious problems of misrepresenting firm’s performance.

Additional explanatory variables

Attempting to get a better understanding of the relationship between performance differentials and diversification strategy, some more variables with a priori explanatory power were modeled in a multiple regression approach:

First, size and growth variables reflecting differences in accounting profit which result, respectively, from superior firm efficiency and innovative effort, or from high market shares indicating high barriers to entry (e.g. Gale, 1972; Shepherd, 1972). Market power is not explicitly regarded because of the difficulties of classifying

highly diversified companies into one industry code, and unavailability of relevant data as a proxy for the multidivisional nature of this variable.

Second, growth models of diversification rec- ommend the attention of ownership structure and internal multidivisional M-form structure affecting agency costs induced by discretionary behavior of managers (Marris and Mueller, 1980; Williamson, 1981; Jensen and Meckling, 1976; Buhner, 1985). While multidivisional structure was identified by firm-specific chart information, a company was classified as owner-controlled if a party owned more than 25 percent of the equity. This requirement secures a legal influence of sharehol- ders’ meeting (Hauptversammlung) on the execu- tive board of directors (Vorstand).

Third, financial leverage was regarded as an observable risk factor influencing performance. Defining leverage as debt to equity ratio in book values, it is presumed that the diversification effect of combining two or more income streams probably leads to reduced bankruptcy risk (and the expected cost of bankruptcy) of the combined entity, ceteris paribus, raising bondholders’ wealth (Higgins and Schall, 1975).

RESULTS

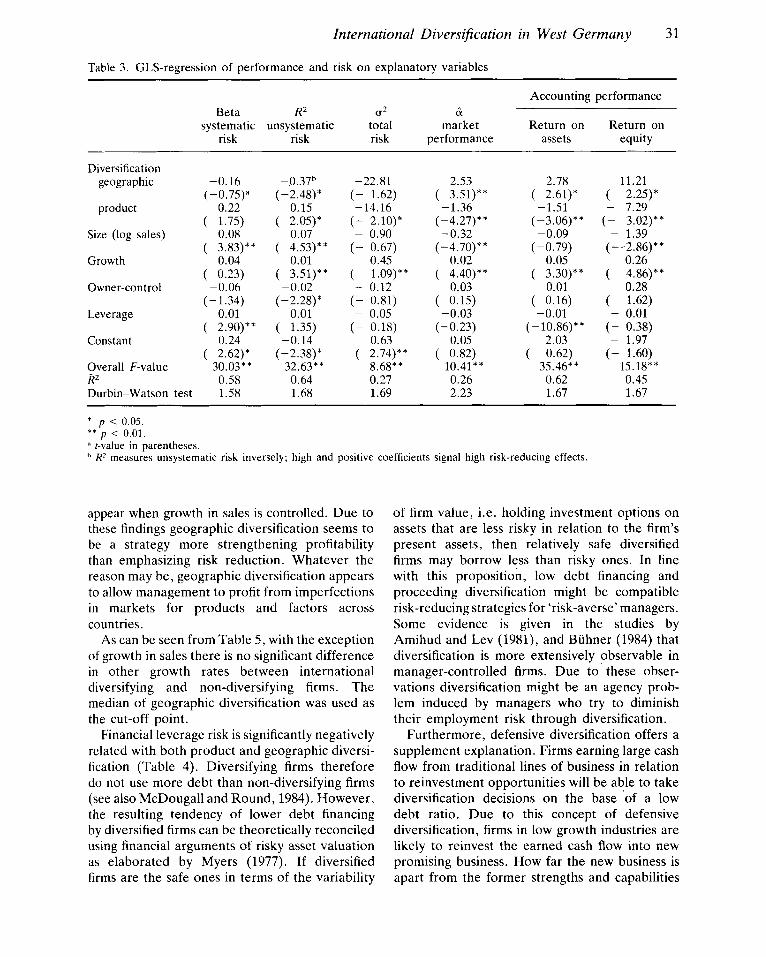

Table 3 reports results of a multiple regression analysis of strategy and structure features on performance measures. Since Spearman tests (Johnston, 1963) indicated heteroscedasticity in OLS estimates, appropriately weighted least squares found by Park’s procedure were calcu- lated. On the other hand, autocorrelation of the error terms could be rejected by the Durbin-Watson statistic. The results show sig- nificant positive relationships between geographic diversification and both market and accounting performance. In contrast there are significant negative relationships of product diversification and performance measures. Moreover, growth in sales is strongly positive related to performance, while more debt in the capital structure is negatively associated with performance. Finally, firm size is negatively linked with market perform- ance and return on equity.

The regression of Table 3 does not include the multidivisional M-form variable. Since there could be interaction effects with strategy, an

R. Buhner

Table 2 . Main variables and measures ~ ~~~

Variables Measures

Performance market-determined accounting-determined

Market risk total risk unsystematic risk

systematic risk

Jensen ‘tit ROA (Yo) ROE (Yo)

Variance of the returns of a share Market standard deviation of the residual return factor e, or as the proportion of variability in portfolio return that is attributable to variability in market returns (R2) Market model ‘beta’

Diversification

quantitative Herfindahl-type index product geographical 1 product categorical geographical } Rumelt-built categories with geographical extension

Size Log sales Growth

Ownership

M-form structure Chart information Leverage

Growth sales (YO) (see also Table 4) > 25 percent of the equity (legally determined)

Debt: equity (in book values)

interaction dummy (1 for related and unrelated companies with a multidivisional structure; 0 otherwise) was added in a separate regression (available on request). The results show, how- ever, significantly negative effects on market performance, so highly diversified multidivisional companies do not outperform less diversified functional structured companies (Buhner, 1985).

With reference to the market-determined risk meas,ures in Table 3, the results support, as expected, risk-reducing diversification effects on the unsystematic risk measure, and on the total variability of returns. The measured market related beta risk component is size- and leverage- induced. This result does conform with arguments implying that beta represents a firm’s intrinsic operating and financial leverage risk (e.g. Ham- ada, 1972; Rubinstein, 1973; Montgomery and Singh, 1984). Calculated accounting risks meas- ured by the variation coefficient of the prof- itability ratios are not shown, because these coefficients appeared to fluctuate by chance and there was not any systematic link with diversification.

The market results are all based on the used domestic market index. When the world index is used the regressions of diversification on performance are no more statistically significant. This might tentatively suggest that assets are priced internationally. However it is for the following analysis a fair procedure to utilize the predictive more powerful domestic index.

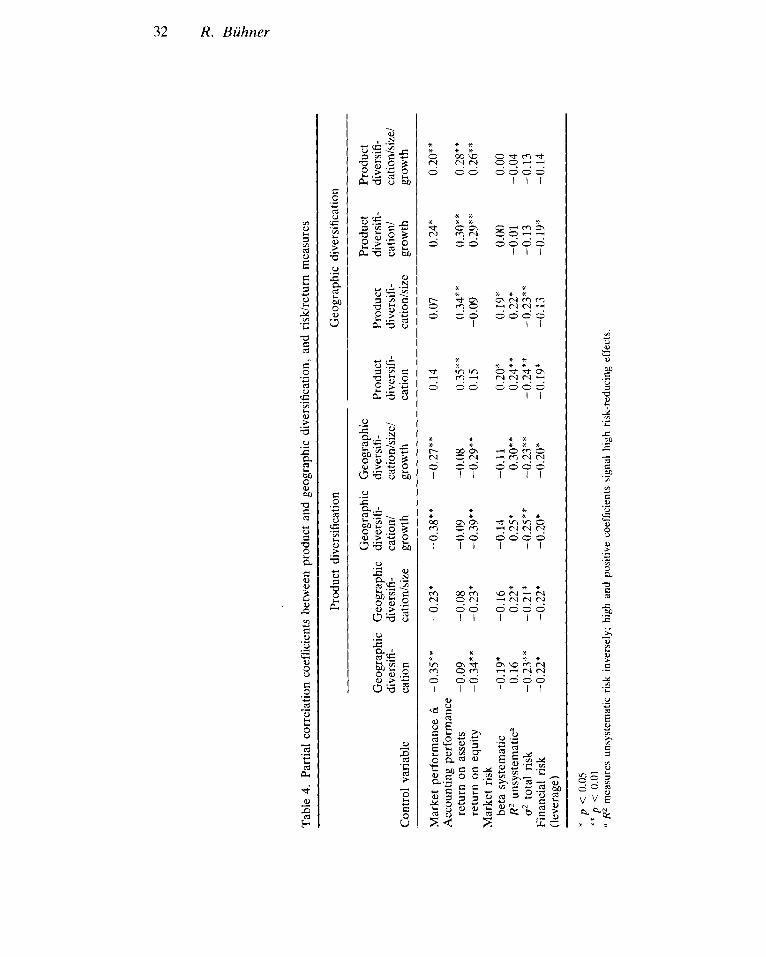

Table 4 shows the partial correlation coef- ficients among the risk and return measures and the explanatory measures controlling for product or geographic diversification, respectively. Con- trolling for geographic diversification, product diversification is significantly negative associated with risk, but also with market performance and rate of returns on equity. The relationships remain stable when additionally both size and growth are controlled. In contrast, the risk and return effects of geographic diversification appear to be contingent on growth in sales. If there is control for the growth variable, then the results show that geographic diversification is a strategy increasing firm’s performance. Furthermore, the risk effects of an international expansion dis-

International DiversiJcation in West Germany 31

Table 3 . GLS-regression of performance and risk on explanatory variables

Accounting performance Beta R2 a2 2

systematic unsystematic total market Return on Return on risk risk risk performance assets equity

Diversification geographic

product

Size (log sales)

Growth

Owner-control

Leverage

Constant

Overall F-value R 2

Durbin-Watson test

-0.16 (-0.75)”

0.22 ( 1.75)

0.08 ( 3.83)**

0.04 ( 0.23)

-0.06 (-1.34)

0.01 ( 2.90)**

0.24 ( 2.62)*

30.03 * * 0.58 1.58

-0.37h

0.15 ( 2.05)*

0.07

0.01 ( 3.51)** -0.02

( - 2.28) * 0.01

-0.14 ( - 2.38) *

(-2.48)*

( 4.53)**

( 1.35)

32.63* * 0.64 1.68

-22.81 (- 1.62) - 14.16

- 0.90 (- 0.67)

(- 2.10)*

0.45 ( 1.09)** - 0.12

- 0.05 (- 0.81)

(- 0.18) 0.63

( 2.74)** 8.68** 0.27 1.69

2.53 ( 3.51)** -1.36

( - 4.27) * * -0.32

(-4.70) * * 0.02

( 4.40)** 0.03

( 0.15) -0.03

(-0.23) 0.05

( 0.82) 10.41** 0.26 2.23

2.78 ( 2.61)” -1.51

( - 3.06) * * -0.09

(-0.79) 0.05

( 3.30)** 0.01

( 0.16) -0.01

( - 10.86) * * 2.03

35.46** 0.62 1.67

( 0.62)

11.21 ( 2.25)* - 7.29

(- 3.02)** - 1.39

0.26 ( 4.86)**

0.28 ( 1.62) - 0.01

(- 0.38) - 1.97

(- 1.60)

(--2.86)**

15.18** 0.45 1.67

* p < 0.05.

a r-value in parentheses. * * p < 0.01.

RZ measures unsystematic risk inversely; high and positive coefficients signal high risk-reducing effects

appear when growth in sales is controlled. Due to these findings geographic diversification seems to be a strategy more strengthening profitability than emphasizing risk reduction. Whatever the reason may be, geographic diversification appears to allow management to profit from imperfections in markets for products and factors across countries.

As can be seen from Table 5 , with the exception of growth in sales there is no significant difference in other growth rates between international diversifying and non-diversifying firms. The median of geographic diversification was used as the cut-off point.

Financial leverage risk is significantly negatively related with both product and geographic diversi- fication (Table 4). Diversifying firms therefore do not use more debt than non-diversifying firms (see also McDougall and Round, 1984). However, the resulting tendency of lower debt financing by diversified firms can be theoretically reconciled using financial arguments of risky asset valuation as elaborated by Myers (1977). If diversified firms are the safe ones in terms of the variability

of firm value, i.e. holding investment options on assets that are less risky in relation to the firm’s present assets, then relatively safe diversified firms may borrow less than risky ones. In line with this proposition, low debt financing and proceeding diversification might be compatible risk-reducing strategies for ‘risk-averse’ managers. Some evidence is given in the studies by Amihud and Lev (1981), and Biihner (1984) that diversification is more extensively observable in manager-controlled firms. Due to these obser- vations diversification might be an agency prob- lem induced by managers who try to diminish their employment risk through diversification.

Furthermore, defensive diversification offers a supplement explanation. Firms earning large cash flow from traditional lines of business in relation to reinvestment opportunities will be able to take diversification decisions on the base ‘of a low debt ratio. Due to this concept of defensive diversification, firms in low growth industries are likely to reinvest the earned cash flow into new promising business. How far the new business is apart from the former strengths and capabilities

Tabl

e 4.

Par

tial

corr

elat

ion

coef

ficie

nts

betw

een

prod

uct

and

geog

raph

ic d

iver

sific

atio

n, a

nd r

iskh

etur

n m

easu

res

Prod

uct

dive

rsifi

catio

n G

eogr

aphi

c di

vers

ifica

tion

Geo

grap

hic

Geo

grap

hic

Prod

uct

Prod

uct

Geo

grap

hic

Geo

grap

hic

dive

rsifi

- di

vers

ifi-

Prod

uct

Prod

uct

dive

rsifi

- di

vers

ifi-

dive

rsifi

- di

vers

ifi-

catio

n1

catio

nkiz

el

dive

rsifi

- di

vers

ifi-

catio

n/

catio

nlsi

zel

Con

trol

var

iabl

e ca

tion

catio

nlsi

ze

grow

th

grow

th

catio

n ca

tionh

ize

grow

th

grow

th

Mar

ket

perf

orm

ance

&

-0.3

5**

-0.2

3*

-0.3

8**

-0.2

7**

0.14

0.

07

0.24

* 0.

20**

A

ccou

ntin

g pe

rfor

man

ce

retu

rn o

n as

sets

-0

.09

-0.0

8 -0

.09

-0.0

8 0.

35**

0.

34**

0.

30**

0.

28**

re

turn

on

equi

ty

-0.3

4**

-0.2

3*

-0.3

9**

-0.2

9**

0.15

-0

.09

0.29

**

0.26

**

Mar

ket

risk

beta

sys

tem

atic

-0

.19*

-0

.16

-0.1

4 -0

.11

0.20

* 0.

19*

0.00

0.

00

R2 u

nsys

tem

atic

" 0.

16

0.22

* 0.

25*

0.30

**

0.24

**

0.22

* -0

.01

-0.0

4 u2

tota

l ris

k -0

.23*

* -0

.21*

-0

.25*

* -0

.23

* *

-0.2

4**

-0.2

3**

-0.1

3 -0

.13

Fina

ncia

l ris

k -0

.22*

-0

.22*

-0

.20*

-0

.20*

-0

.19*

-0

.13

-0.1

9*

-0.1

4 (le

vera

ge)

* p

< 0

.05

** p

< 0

.01

a R

2 m

easu

res

unsy

stem

atic

ris

k in

vers

ely;

hig

h an

d po

sitiv

e co

effic

ient

s si

gnal

hig

h ris

k-re

duci

ng e

ffec

ts

International Diversification in West Germany 33

Table 5. A comparison of the rates of growth in sales, assets and profitability ratios of international diversifying and non-diversifying firms

International International t non-diversifying diversifying

Sales 1.08 1.10 -2.49" Assets 1.05 1.06 - 1.04 Return on assets 0.96 0.98 -1.15 Return on equity 0.95 0.96 -0.65 Market return a 0.92 0.96 -0.88

* p < 0.05.

Table 6. Risk and return measures of strategies

Accounting performance Beta R2 a2 &

systematic unsystematic total market Return on Return on risk risk" risk performance assets equity

Single-parent Single-foreign Dominant-parent Dominant-foreign Related-parent Related-foreign Unrelated-parent Unrelated-foreign

0.94 1.09 0.94 1.09 0.92 0.96 1.04 1.12

0.31 0.43 0.38 0.45 0.36 0.48 0.49 0.51

56.8 44.6 42.8 33.4 47.9 32.4 46.6 43.9

0.69 0.90 0.29 0.98 0.68 0.36 0.59

-0.54

1.55 2.09 1.51 1.00 2.88 1.77 1.04 1.66

9.49 12.12 5.59 6.29 6.33 7.37 7.19

-3.85

Overall means 0.99 0.42 43.2 0.54 1.84 7.39 F-values 3.71** 10.8*" 12.6"" 2.41" 2.25' 5.12**

* p < 0.05 * * p < 0.01 RZ measures unsystematic risk inversely

depends on diversification strategy and manag- ement's ability to understand the diversification move.

Table 6 shows the risk and return values for different diversification strategies. In comparison to the domestic product-diversified firms, the additional international involvement leads in total to additional risk-reducing effects. As the partial correlation analysis has revealed, the total and component risk effects are growth-induced.

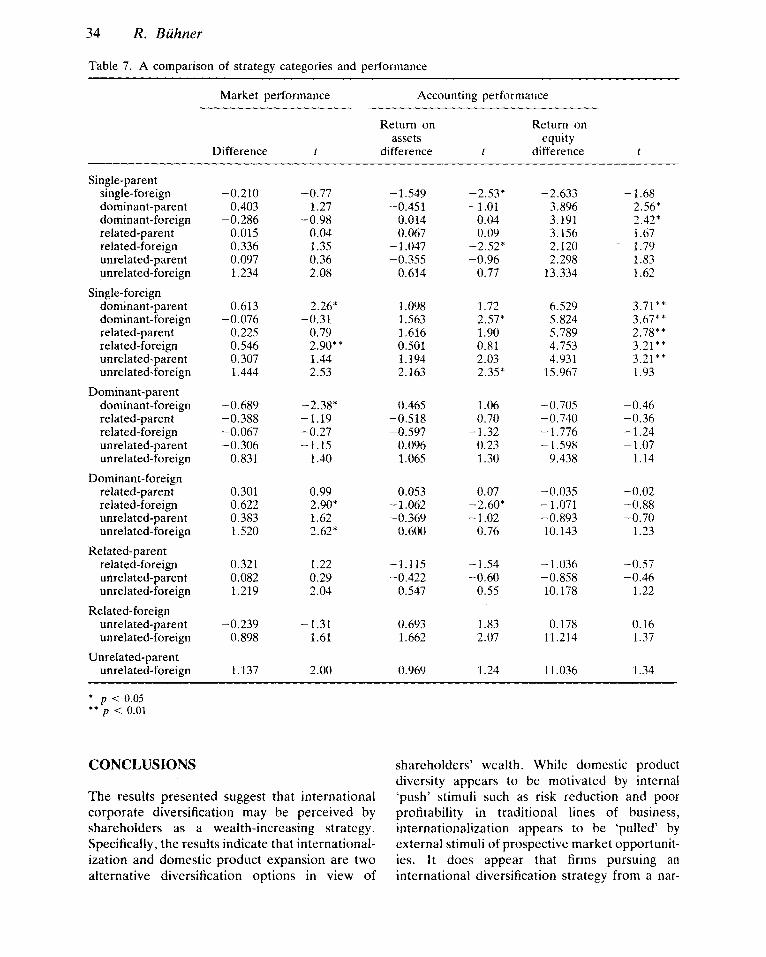

A one-way analysis of variance was used to test for differences among the pairs of diversification strategies for each risk and return variable. The pairwise test results for the market and accounting performance across the strategy categories are shown in Table 7. The results do

not indicate any consistent reward of a firm's foreign strategy involvement. The risk-adjusted market performance differences suggest that the market has selectively rewarded a firm's foreign strategy in dependence on the product diversity level. Firms involved in less product diversity which went abroad outperformed firms within the related foreign and unrelated foreign category. This interpretation is largely supported by the accounting-determined rate of returns on equity. In comparison, strategy performance differences in rate of returns on asset are statistically less evident, probably for reasons of financial leverage. Overall, firms in the single-foreign category appear to be the strongest performers in the sample.

34 R. Buhner

Table 7. A comparison of strategy categories and performance

Market performance Accounting performance

Return on Return on assets equity

Difference t difference t difference t

Single-parent single-foreign dominant-parent dominant-foreign related-parent related-foreign unrelated-parent unrelated-foreign

dominant-parent dominant-foreign related-parent related-foreign unrelated-parent unrelated-foreign

Dominant-parent dominant-foreign related-parent related-foreign unrelated-parent unrelated-foreign

Dominant-foreign related-parent related-foreign unrelated-parent unrelated-foreign

related-foreign unrelated-parent unrelated-foreign

unrelated-parent unrelated-foreign

unrelated-foreign

Single-foreign

Related-parent

Related-foreign

Unrelated-parent

-0.210 0.403

-0.286 0.015 0.336 0.097 1.234

-0.77

-0.98 1.27

0.04 1.35 0.36 2.08

-1.549 -0.451

0.014 0.067

-1.047 -0.355

0.614

-2.53’ -1.01

0.04 0.09

-2.52* -0.96

0.77

-2.633 3.896 3.191 3.156 2.120 2.298

13.334

-1.68 2.56* 2.42* 1.67 1.79 1.83 1.62

0.613

0.225 0.546 0.307 1.444

-0.076 2.26*

-0.31 0.79 2.90** 1.44 2.53

1.098 1.563 1.616 0.501 1.194 2.163

1.72 2.57* 1.90 0.81 2.03 2.35*

6.529 5.824 5.789 4.753 4.931

15.967

3.71** 3.67** 2.78** 3.21** 3.21** 1.93

-0.689 -0.388 -0.067 -0.306

0.831

-2.38* -1.19 -0.27 -1.15

1.40

0.465 -0.518 -0.597

0.096 1.065

1.06 0.70

- 1.32 0.23 1.30

-0.705 -0.740 - 1.776 -1.598

9.438

-0.46 -0.36 -1.24 - 1.07

1.14

0.301 0.622 0.383 1.520

0.99 2.90* 1.62 2.62*

0.053 -1.062 -0.369

0.600

0.07 -2.60” - 1.02

0.76

-0.035 -1.071 -0.893 10.143

-0.02 -0.88 -0.70

1.23

0.321 0.082 1.219

1.22 0.29 2.04

-1.115 -0.422

0.547

-1.54 -0.60

0.55

-1.036 -0.858 10.178

-0.57 -0.46

1.22

-0.239 0.898

-1.31 1.61

0.693 1.662

1.83 2.07

0.178 11.214

0.16 1.37

1.137 2.00 0.969 1.24 11.036 1.34

* p < 0.05 * * p < 0.01

CONCLUSIONS shareholders’ wealth. While domestic product diversity appears to be motivated by internal

T h e results presented suggest that international ‘push’ stimuli such as risk reduction and poor corporate diversification may be perceived by profitability in traditional lines of business, shareholders as a wealth-increasing strategy. internationalization appears to be ‘pulled’ by Specifically, t he results indicate that international- external stimuli of prospective market opportunit- ization and domestic product expansion are two ies. It does appear that firms pursuing an alternative diversification options in view of international diversification strategy from a nar-

International Diversification in West Germany 35

row product core skill level outperform purely domestic firms, and firms having a highly foreign product diversity.

The findings are consistent with some previous studies concerning the financial role for corporate international diversification by presuming gains from completing the market services for investors, and also consistent with strategic management studies stressing core strengths of the firms and gains from excess economies of market- investment decisions. However, the prior gains from the management source may arise from the utilization of firm-specific assets and core skills in the production process assuming the accompanying costs of organizational diseconom- ies are down. Although there is still no consensus about efficient internal structures, guidelines from a contingency framework suggest that both product and geographic diversity, simultaneously, make good ‘fit’ structure design difficult (Stopford and Wells, 1972; Herbert, 1984; Daniels, Pitts, and Tretter, 1984).

It could be that the market premiums of the internationally diversified corporations go back to countercyclical effects during the downswing of a German economic cycle. Dividing the time under study in stock market boom periods (1966-69 and 1974-77) and slump periods (197CL73 and 1978-81) it is shown that during the slump the highly product diversified corporations were sold more enthusiastically. Internationally diversified corporations with a closely related product base performed best, while highly product and international diversified corporations were just equally priced during the boom periods. This implies that there is no positive valuation in the stock market for an efficient management of diversified activities in an economic downturn.

There are some practical implications of the findings: First, foreign diversification strategy allows easy realization of economies of scale and experience curve effects through sales growth and exploiting parent capacity. In particular, exporting suggests this implication (Ursic and Czinkota, 1984). Second, synergy appears to be an ambitious economic concept which is obviously hard to achieve across different product lines through organizational means. Foreign market penetration allows management to operate from a product know-how level which it understands best. There is no need to amalgamate different (product) cultures, member attitudes or behavior.

Going abroad primarily affects the marketing function, and largely requires modest organiz- ational adaptation. Third, internationalization delivers a strategy to increase sales volume rapidly which, on the other hand, helps to shorten payback time of investments, e.g. in research and development, product variety or process automation. Fourth, global strategy does not exclude a foreign differentiation, or niche strat- egy. It is remarkable that most German companies serve foreign markets with specialities. Fifth, companies which are present on the most important markets worldwide contest with the best competitors. This challenge promotes inno- vation, helps to ensure the closeness to customer needs, and protects against the underestimation of new potential market entrants.

The findings are limited to large firms residing in West Germany. The small geographic and economic size of this country might be responsible for imperfection in the goods and factor markets. Shareholders may have therefore benefited from international diversification to an extent depend- ing on the firm’s ability to bypass the imperfection through exploiting the firm’s distinctive capabil- ities. However, the resolution of international diversification problems requires further research.

REFERENCES

Agmon, T. ‘The relations among equity markets: a study of share price co-movements in the United States, United Kingdom, Germany and Japan’, Journal of Finance, 27, 1972, pp. 839-855.

Agmon, T. and D. R. Lessard. ‘Investor recognition of corporate international diversification’, Journal of Finance, 32, 1977, pp. 1049-1055,

Amihud, Y. and B. Lev. ‘Risk reduction as a managerial motive for conglomerate mergers’, Bell Journal of Economics, 12, 1981, pp. 605417.

Atherton, J. and D. C . L. Yap. ‘Risk reduction by international diversification’, Managerial Finance, 5 , 1979, pp. 18-28.

Barnett, G. A. ‘The best portfolios are international’, Economy, April 1979, pp. 165-171.

Beaver, W. and J. Manegold. ‘The association between market-determined and accounting-determined measures of systematic risk: some further evidence’, Journal of Financial and Quantitative Analysis, 10, 1975, pp. 231-284.

Bettis, R. A. and W. K. Hall. ‘Diversification strategy, accounting determined risk, and accounting deter- mined return’, Academy of Management Journal, 25, 1982, pp. 254264.

36 R . Biihner

Brewer, H. L. ‘Investor benefits from corporate international diversification’, Journal of Financial and Quantitative Analysis, 16, 1981, pp. 113-126.

Buhner, R. ‘Rendite-Risiko-Effekte der Trennung von Eigentum und Leitung im diversifizierten GroBunternehmen’, Zeitschrift fur betriebswirtsch- aftliche Forschung, 36, 1984, pp. 812-824.

Buhner, R. ‘Internal organization and returns: an empirical analysis of large diversified German corporations’, in Schwalbach, J. (ed.), Industry Structure and Performance, edition sigma rainer bohn verlag, Berlin, 1985.

Caves, R. E. ‘International corporations: the industrial economics of foreign investment’, Economica, 38,

Caves, R. E., M. E . Porter, A. M. Spence and J. T. Scott. Competition in the Open Economy, A Model Applied to Canada, Harvard University Press, Cambridge, MA, 1980.

Christensen, H. K. and C. A. Montgomery. ‘Corporate economic performance: diversification strategy ver- sus market structure’, Strategic Management Jour- nal, 2, 1981, pp. 327-343.

Cohn, R. A. and J. J. Pringle. ‘Imperfections in international financial markets: implications for risk premia and the cost of capital to firms’, Journal of Finance, 28, 1973, pp. 5%66.

Daniels, J. D. , R. A. Pitts and M. J. Tretter. ‘Strategy and structure of U.S. multinationals: an exploratory study’, Academy of Management Journal, 27, 1984,

Delacroix, J. ‘Export strategies for small American firms’, California Management Review, 26, 1984, pp. 138-153.

Dundas, K. N. M. and P. R. Richardson. ‘Corporate strategy and the concept of market failure’, Strategic Management Journal, 1, 1980, pp. 177--188.

Errunza, V. R. and L. W. Senbet. ‘International corporate diversification, market valuation, and size-adjusted evidence’, Journal of Finance, 34,

Gale, B . T. ‘Market share and rate of return’, Review of Economics and Stutistics, 54, 1972, pp. 412-423.

Grubel, H. G. ‘Internationally diversified portfolios: welfare gains and capital flows’, American Economic Review, 58, 1968, pp. 1299-1314.

Grubel, H. G. and K. Fadner. ‘The interdependence of international equity markets’, Journal of Finance,

Hamada, R. S. ‘The effect of firm’s capital structure on systematic risk of common stocks’, Journal of Finance, 17, 1972, pp. 435-452.

Herbert, T. T. ‘Strategy and multinational organization structure: an interorganizational relationships per- spective’, Academy of Management Review, 12,

Higgins, R. S. and L. D. Schall. ‘Corporate bankruptcy and conglomerate merger’, Journal of Finance, 30, 1975, pp. 93-113.

Hill, C. W. L. ‘Conglomerate performance over the economic cycle’, Journal of Industrial Economics,

1971, pp. 1-27.

pp. 292-307.

1984, pp. 727-745.

26, 1971, pp. 89-94.

1984, pp. 259-271.

32, 1983, pp. 197-211.

Horst, T. ‘Determinants of the decision to invest abroad’, Review of Economics and Statistics, 54,

Hughes, J. S., D. E. Logue and R. J. Sweeney. ‘Corporate international diversification and market assigned measures of risk and diversification’, Journal of Financial and Quantitative Analysis, 10, 1975, pp. 627437.

poor tools for diversification’, Journal of Portfolio Management, Winter 1978, pp. 8-12.

Jensen, M. C. ‘Risk, the pricing of capital assets, and the evaluation of investment portfolios’, Journal of Business, 42, 1969, pp. 167-247.

Jensen, M. C. and W. H. Meckling. ‘Theory of the firm: managerial behavior, agency costs, and ownership structure’, Journal of Financial Econ- omics, 3, 1976, pp. 305-360.

Johnson, H. G. ‘The efficiency and welfare impli- cations of the international corporation’, in Kindle- berger, C. P. (ed.), The International Corporation, MIT Press, Cambridge, MA, 1970, pp. 35-56.

Johnston, J. Econometric Methods, McGraw-Hill, New York, 1963.

Lessard, D. R. ‘World, country, and industry relation- ships in equity returns. Implications for risk reduction through international diversification’, Financial Analysts Journal, 31, Jan.-Feb. 1976,

Levy, H. and M. Sarnat. ‘International diversification of investment portfolios’, American Economic Review, 60, 1970, pp. 668-685.

Marris, R. and D. C. Mueller. ‘The corporation, competition, and the invisible hand’, Journal of Economic Literature, 18, 1980, pp. 32-63.

McDougall, F. M. and D. K. Round. ‘A comparison of diversifying and nondiversifying Australian indus- trial firms’, Academy of Management Journal, 27, 1984, pp. 384-398.

Mikhail, A. D. and H. A. Shawky. ‘Investment performance of U.S.-based multinational corpora- tions’, Journal of International Business Studies, Spring-Summer 1979, pp. 53-66.

Montgomery, C. A. and H. Singh. ‘Diversification strategy and systematic risk’, Strategic Management Journal, 5, 1984, pp. 181-191.

Mueller, D. C. ‘A life cycle theory of the firm’, Journul of Industrial Economics, 20, 1972, pp. 199-219.

Myers, S. C . ‘Determinants of corporate borrowing’, Journal of Financial Economics, 5, 1977,

Panzar, J. and R. Willig. ‘Economies of scope’, American Economic Review, Papers and Proceed- ings, 71(2), 1981, pp. 268-272.

Peavy, J. W., 111. ‘Modern financial theory, corporate strategy, and public policy: another perspective’, Academy of Management Review, 9, 1984,

Rubinstein, M. E. ‘A mean-variance synthesis of corporate financial theory’, Journal of Finance, 28,

Rugman, R.. P. ‘Risk reduction by international

1972, pp. 258-266.

Jacquillat, B. and B. H. Solnik, ‘Multinationals are ’

-

pp. 32-38.

pp. 147-175.

pp. 152-157.

1973, pp. 167-181.

International Diversification in West Germany 37

diversification’, Journal of International Business Studies, 7, 1976, pp. 75-80.

Rumelt, R. P. Strategy, Structure, and Economic Performance, Division of Research, Harvard Busi- ness School, Boston, MA, 1974.

Rumelt, R. P. ‘Diversification strategy and profitabili- ty’, Strategic Management Journal, 3, 1982,

Ruppert, W. ‘Produktionsstandorte der Industrie im Urteil der Unternehmen’, Ifo-Schnelldienst, 19,

Shepherd, W. G. ‘The elements of market structure’, Review of Economics and Statistics, 54, 1972,

Solnik, B. H. ‘Why not diversify internationally rather than domestically?’, Financial Analysts Journal, 30,

Stehle, R. ‘An empirical test of the alternative hypotheses of national and international pricing of risky assets’, Journal of Finance, 32, May 1977,

Stopford, J. M. and L. T. Wells. Managing the Multin- ational Enterprise. Organization of the Firm and Ownership of the Subsidiaries’, Longmans, London, 1972.

pp. 359-369.

1979, pp. 7-15.

pp. 25-37.

July-Aug. 1974, pp. 48-54.

pp. 493-502.

Teece, D. J. ‘Economies of scope and the scope of the enterprise’, Journal of Economic Behavior and Organization, 1, 1980, pp. 223-247.

Ursic, M. L. and M. R. Czinkota. ‘An experience curve explanation of export expansion’, Journal of Business Research, 12, 1984, pp. 159-168.

Westerfield, R. ‘A note on the measurement of conglomerate diversification’, Journal of Finance, , 25, 1970, pp. 909-914.

Weston, J. F. and S. K . Mansinghka. ‘Tests of the efficiency performance of conglomerate firms’, Journal of Finance, 26, 1971, pp. 919-936.

Williamson, 0. E. Markets and Hierarchies: Analysis and Anti-trust Implications, Free Press; New York, 1975.

Williamson, 0. E. ‘The modern corporation: origins, evolution, attributes’, Journal of Economic Litera- ture, 19, 1981, pp. 1537-1568.

Wolf, B. M. ‘Industrial diversification and internation- alization: some empirical evidence’, Journal of Industrial Economics, 26, 1977, pp. 177-191.

Wrigley, L. ‘Divisional autonomy and diversification’. Unpublished DBA dissertation, Harvard Business School, 1970.