asociación de industrias químicas y de proceso de asturias brussels, 13th february, 2008 1/16...

TRANSCRIPT

Asociación de Industrias Químicas y de Proceso de Asturias

Brussels, 13th February, 2008

1/16

Emerging Chemical Markets from

a European Downstream User Perspective

Asociación de Industrias Químicas y de Proceso de Asturias

Brussels, 13th February, 2008

2/16

Asociación de Industrias Químicas y de Proceso de Asturias

Some Facts and Figures . . .

Market Share: 32 % (EU27)

World’s leading exporter and importer of Chemicals Main trading partners: North America, Central and Eastern Europe, Asia Euro / US dollar exchange, undermines Europe’s competitive position

96 % SMEs

12 of the 25 biggest chemical companies, based in Europe

Brussels, 13th February, 2008

3/16

Asociación de Industrias Químicas y de Proceso de Asturias

Some Facts and Figures . . .

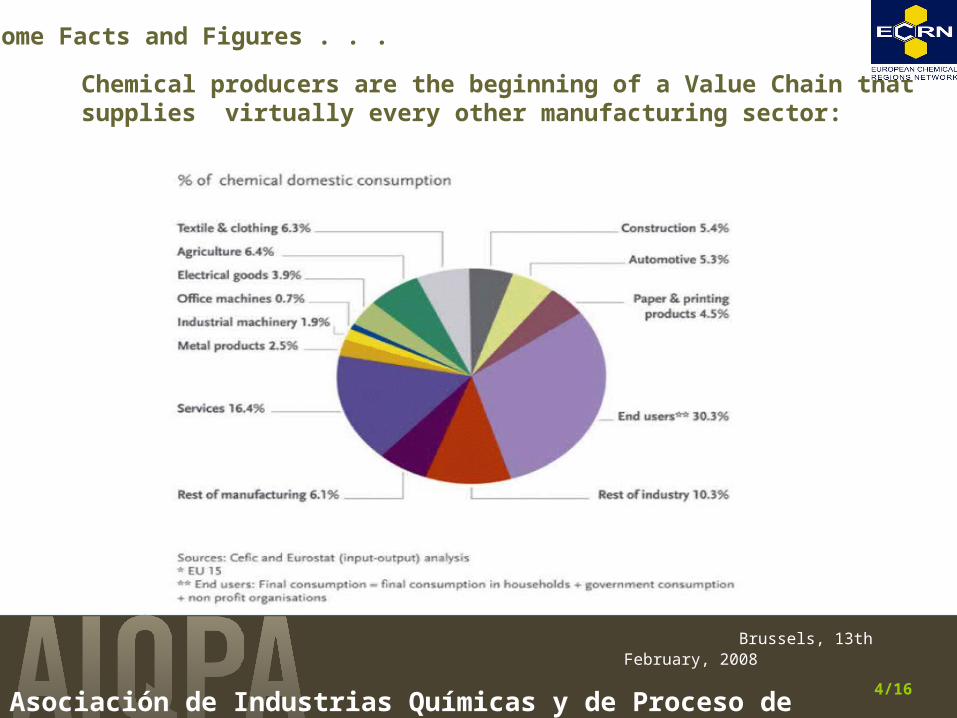

Chemical producers are the beginning of a Value Chain that supplies virtually every other manufacturing sector:

Brussels, 13th February, 2008

4/16

Some Facts and Figures . . .

Asociación de Industrias Químicas y de Proceso de Asturias

Brussels, 13th February, 2008

5/16

Asociación de Industrias Químicas y de Proceso de Asturias

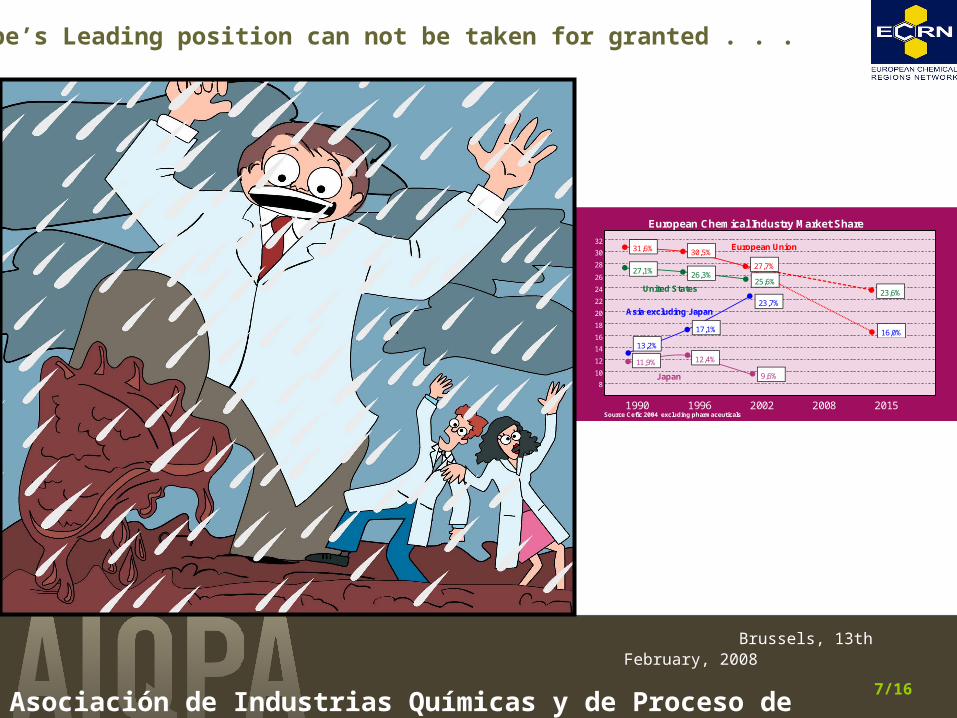

Europe’s Leading position can not be taken for granted . . .

European Chemical Industry Market Share

1990 1996 2002 2008 2015

32

30

28

26

24

22

20

18

16

14

12

10

8

Source Cefic 2004 excluding pharmaceuticals

31,6% 30,5%

27,7%

23,6%

16,0%

European Union

27,1% 26,3%25,6%

United States

13,2%

17,1%

23,7%Asia excluding Japan

11,9% 12,4%

9,6%Japan

Brussels, 13th February, 2008

6/16

Asociación de Industrias Químicas y de Proceso de Asturias

Europe’s Leading position can not be taken for granted . . .

European Chemical Industry Market Share

1990 1996 2002 2008 2015

32

30

28

26

24

22

20

18

16

14

12

10

8

Source Cefic 2004 excluding pharmaceuticals

31,6% 30,5%

27,7%

23,6%

16,0%

European Union

27,1%26,3%

25,6%United States

13,2%

17,1%

23,7%Asia excluding Japan

11,9% 12,4%

9,6%Japan

Brussels, 13th February, 2008

7/16

Asociación de Industrias Químicas y de Proceso de Asturias

Brussels, 12th, 13th February, 2008

15/21

Where European Competitors come from ? . . .

. . . Low Cost Countries (LCC)

15/21Asociación de Industrias Químicas y de Proceso de Asturias

. . . China and India

. . . BRIC: (Brazil, Russia, India, and China)

. . . Eastern Europe

. . . Middle East and North Africa

. . . The Next Eleven: (Bangladesh, Egypt, Indonesia, Iran, Korea, Mexico, Nigeria, Pakistan, Phillipines, Turkey, Vietnam )

Asociación de Industrias Químicas y de Proceso de Asturias

Brussels, 13th February, 2008

7/16

Asociación de Industrias Químicas y de Proceso de Asturias

Why Looking for Chemicals in Low Cost Countries ? . . .

. . . A better balance between cost and quality

. . . A more flexible production

. . . A stronger negotiation position

. . . Possitioning in fast growing markets

Brussels, 13th February, 2008

9/16

Asociación de Industrias Químicas y de Proceso de Asturias

Why continuing purchasing from Europe ? . . .

. . . Safeguard Intellectual Property

. . . Technological limitations

. . . Country related risks

. . . Be close to the users site

. . . Supply and deliveries risks

. . . Existing facilities Liabilities

. . . Costs of shifting into LCC

. . . Bad image costs in Home Countries

Brussels, 13th February, 2008

10/16

Asociación de Industrias Químicas y de Proceso de Asturias

Why Looking for Chemicals in Low Cost Countries ? . . .

Price Issues . . .

. . . Lower labour costs

. . . Lower capital investment costs

. . . Lower local sourcing costs

. . . Government incentives

. . . Higher productivity . . . A company purchasing in LCC

may get a 20 % - 40 % inmediate reduction in the cost of the goods

Brussels, 13th February, 2008

11/16

Asociación de Industrias Químicas y de Proceso de Asturias

Why Looking for Chemicals in Low Cost Countries ? . . .

Quality Issues . . .

. . . Low cost is not low quality

. . . Skill and motivated workers make quality improvements

. . . LCC offer are shifting into more added value products

Brussels, 13th February, 2008

12/16

Asociación de Industrias Químicas y de Proceso de Asturias

Why Looking for Chemicals in Low Cost Countries ? . . .

. . . Flexibility

. . . Increasing R&D Capabilities . . . . . . Integration to more Added Value Products . . . Transfer of Technology (patent issues)

Brussels, 13th February, 2008

13/16

Asociación de Industrias Químicas y de Proceso de Asturias

Why Looking for Chemicals in Low Cost Countries ? . . .

Regulatory Issues. . .

. . . The EU legal Framework

. . . What is the goal of every private company?

Brussels, 13th February, 2008

14/16

Asociación de Industrias Químicas y de Proceso de Asturias

Imports from Emerging Markets in Asturias 2000 – 2005 . . .

Total imports Imports of chemicals % Total imports

Imports of chemicals %

China 29.880.615 1.310.998 4,39 91.713.035 5.633.241 6,14 429,7

India 7.553.126 197.123 2,61 8.882.423 881.036 9,92 446,9

Taiwan 3.736.253 567 0,02 4.274.158 150.905 3,53 26614,6

South Korea 9.155.922 0 0,00 4.012.921 18.786 0,47

Vietnam 492.762 0 0,00 1.241.208 3.233 0,26

Hong Kong 741.717 1.234 0,17 1.618.042 1.624 0,10 131,6

Thailand 1.817.846 0 0,00 2.033.181 964 0,05

2000-2005 Growth %

(Source: SADEI)

(euros x 1000)

2000 2005

Brussels, 13th February, 2008

15/16

Asociación de Industrias Químicas y de Proceso de Asturias

Emerging Chemical Markets from

a European Downstream User Perspective

Thank you for your attention

Brussels, 13th February, 2008

16/16