as at october 31, 2018 - rbc.com · ab roy perf clie cap mill our and fun and func ca our fina (bc...

TRANSCRIPT

Royal Pillar

As at O

l Bank

3 Rep

ctober 3

k of Ca

port

31, 2018

anada

8

a

TA

CAU

ABO

CAP

DISC

OVE

KOO

LINK

L

LL

CRE

CCCCCCCCCCC

CCC

COU

CCCCCCCCC

SEC

SSSSS

MAR

MMMMMM

OPE

INTE

Royal Ban

BLE OF CON

UTION REGARD

OUT ROYAL BA

PITAL FRAMEW

CLOSURE MAP

ERVIEW OF KEY

KM1: Key CapitaOVA: Bank risk mOV1: Overview o

KAGES BETWE

LI1: Differences bcategories ...

LI2: Main sourceLIA: Explanations

EDIT RISK .........

CRA: General quCR1: Credit qualCR2: Changes inCRB: Additional dCRC: QualitativeCR3: Credit risk CRD: QualitativeCR4: StandardizeCR5: StandardizeCRE: QualitativeCR6: IRB – Cred

CR6: Memo ICR7: IRB – EffecCR8: RWA flow sCR9: IRB – Back

UNTERPARTY C

CCRA: QualitativCCR1: Analysis oCCR2: Credit valCCR3: StandardCCR4: IRB – CCCCR5: CompositCCR6: Credit deCCR7: RWA flowCCR8: Exposure

CURITIZATION ..

SECA: QualitativSEC1: IRB – SecSEC2: IRB – SecSEC3: SecuritizaSEC4: Securitiza

RKET RISK .......

MRA: QualitativeMRB: QualitativeMR1: Market riskMR2: RWA flow sMR3: IMA valuesMR4: Compariso

ERATIONAL RIS

EREST RATE R

nk of Cana

NTENTS

DING FORWARD

ANK OF CANAD

WORK .................

P .........................

Y METRICS, RIS

al and Leverage mmanagement appof risk weighted a

EEN FINANCIAL

between accoun..........................s of differences bs of differences b

...........................

ualitative informaity of assets ......

n stock of defaultdisclosure relate

e disclosure requmitigation techni

e disclosures on bed approach – ced approach – e disclosures rela

dit risk exposurestem: Retail Insur

ct on RWA of crestatements of crektesting of probab

CREDIT RISK ....

ve disclosure relaof counterparty cluation adjustmeized approach –

CR exposures by tion of collateral frivatives exposu

w statements of Ces to central coun

...........................

ve disclosure reqcuritization exposcuritization exposation exposures iation exposures i

...........................

e disclosure reque disclosures for k under standardstatements of mas for trading portfon of VaR estima

SK ......................

RISK IN THE BAN

ada Pillar 3

D-LOOKING STA

A .......................

..........................

..........................

SK MANAGEME

metrics (at consoproach ...............assets (RWA) ....

L STATEMENTS

ting and regulato..........................between regulatobetween account

..........................

ation about credit..........................ted loans and de

ed to the credit quirements related ques – overviewbanks' use of extredit risk exposuxposures by ass

ated to internal riss by portfolio andred Exposures ...edit derivatives usedit risk exposurebility of default (P

..........................

ated to counterpacredit risk (CCR) nt (CVA) capital CCR exposuresportfolio and PDfor CCR exposurres ....................

CCR exposures unterparties .........

..........................

uirements relatedsures in the banksures in the tradin the banking bon the banking bo

..........................

irements relatedbanks using the ized approach ...arket risk exposufolios .................

ates with gains/lo

..........................

NKING BOOK ..

3 Report

ATEMENTS ......

..........................

..........................

..........................

ENT AND RWA ..

olidated group lev....................................................

AND REGULAT

ory scopes of con..........................ory exposure amting and regulato

..........................

risk .............................................bt securities ......uality of assets ..to credit risk mit

w .........................ternal credit ratin

ure and credit riskset classes and risk-based (IRB) md PD range ...................................sed as CRM teches under IRB .....PD) per portfolio

..........................

arty credit risk ....exposure by appcharge ..............

s by regulatory poD scale ...............re .................................................under the Interna..........................

..........................

d to securitizatioking book ...........ng book ............

ook and associatook and associat

..........................

to market risk ...internal models ..........................ures under an IM..........................sses ..................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

vel) ........................................................................

TORY EXPOSUR

nsolidation and m..........................

mounts and carryiory exposure amo

..........................

..........................

..........................

..........................

..........................tigation technique..........................

ngs under the stak mitigation (CRMisk weights ........

models ...................................................................hniques .................................................................

..........................

..........................proach .........................................ortfolio and risk w..............................................................................

al Model Method ..........................

..........................

n exposures ..........................................................ted regulatory cated capital requir

..........................

..........................approach (IMA) ...........................

MA ...........................................................................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

RES ..................

mapping of finan..........................ing values in finaounts ................

..........................

..........................

..........................

..........................

..........................es ...............................................andardized approM) effects ................................................................................................................................................................................................

..........................

..........................

..........................

..........................weights ............................................................................................ (IMM) ........................................

..........................

..........................

..........................

..........................apital requiremenrements – bank a

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

cial statement ca..........................ancial statements..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................oach for credit ris................................................................................................................................................................................................................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................nts – bank actingacting as investo

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

ategories with re..........................s ..................................................

..........................

..........................

..........................

..........................

..........................

..........................

..........................sk .......................................................................................................................................................................................................................................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

.......................... as originator or

or ........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

Q4 2018

....................... 1

....................... 1

....................... 1

....................... 3

....................... 8

....................... 8

....................... 9

..................... 10

..................... 11

egulatory risk ..................... 11..................... 12..................... 13

..................... 14

..................... 14

..................... 15

..................... 15

..................... 15

..................... 19

..................... 20

..................... 20

..................... 21

..................... 22

..................... 23

..................... 26

.....................29

..................... 30

..................... 30

..................... 31

..................... 34

..................... 34

..................... 35

..................... 35

..................... 35

..................... 36

..................... 37

..................... 37

..................... 37

..................... 38

..................... 39

..................... 39

..................... 40

..................... 41as sponsor .. 42..................... 43

..................... 44

..................... 44

..................... 45

..................... 47

..................... 47

..................... 48

..................... 49

..................... 50

..................... 50

Ca

Fro“safsecCantypi“pronaturiseassreadmatbe frespExcfrom Ab

Royperfcliecapmill OurandFunandfunc Ca

OurFina(BC The

Undexpregurequapp

In JdiscregurequOSFimpfirst

Royal Ban

aution regard

m time to timefe harbour” pr

curities legislatinadian regulatocally identified

oject” and simiure, forward-lo

e to the possibiumptions may ders not to platerially from thefound in the rispect to us, invecept as requiredm time to time b

bout Royal B

yal Bank of Cformance. Our nts thrive and

pitalization, we ion clients in C

r business segd Capital Markenctions. Technod services to octional groups.

apital framew

r consolidated ancial Institutio

CBS).

e Basel III fram

Pillar 1 pfor calcul

Pillar 2 rethe risk p

Pillar 3 eacross ju

der Basel III, bposure types iulatory leveraguirements. Re

proaches. Refe

Credit Ri Counterp Market R Operatio Securitiza

January 2015, cipline through ulatory capitaluirements in thFI mandated t

portant banks (Dt phase of the R

nk of Cana

ding forward

e, we make wrirovisions of theon. We may mors or the SEC

d by words sucilar expressionoking statemenlity that our prenot be correct

ace undue rele expectations sk sections of estors and othd by law, we doby us or on our

Bank of Cana

Canada is a gsuccess come

d communitieshave a divers

Canada, the U.S

gments include ets. Our busineology & Operaour clients, wh

work

regulatory capons (OSFI), wh

ework integrate

prescribes minilating risk-weigequires the estprofile and capienhances the

urisdictions for m

banks use definncluding cred

ge ratio based oefer to the “Car to the followin

sk party Credit RisRisk nal Risk ation Exposure

the BCBS pubregulatory dis

l including ouhe areas of crethe domestic iD-SIBs) for theRevised Standa

ada Pillar 3

d-looking sta

itten or oral fore United State

make forward-loC, in other repch as “believe”ns of future or nts require us edictions, forect and that our iance on thesexpressed in sour 2018 Annuers should caro not undertaker behalf.

ada

global financiaes from the 84, prosper. As

sified business S. and 34 other

Personal & Cess segments ations provides ile Functions i

pital requiremeich are based

es three “Pillar

imum capital reghted assets (Rtablishment of tal adequacy oconsistency a

market particip

ned approacheit, counterparton OSFI’s Levapital manageng sections in t

sk

es

blished the “Resclosure requireur methodologdit risk, countemplementation

e reporting perioards.

3 Report

atements

rward-looking ses Private Secooking statemeports to shareh”, “expect”, “foconditional ve

to make assumcasts, projectiofinancial perfoe statements such forward-loual Report. Wrefully considere to update an

al institution w,000+ employeCanada’s bigmodel with a

r countries.

Commercial Banare supported the technolog

includes our fi

ents are determon the Basel I

s” to establish

equirements aRWA);

internal assessof banks; and comparabipants through m

es to calculate ty credit, mark

verage Requireement” sectionthis report for fu

evised Pillar 3 ements. The R

gies used in erparty credit rin of the first pod ending Octo

statements witcurities Litigati

ents in this Pillaholders and in oresee”, “forecaerbs such as “mptions and arons, expectatiormance and mas a number

ooking statemeWhen relying on

r these risk facy forward-look

with a purposeees who bring ogest bank, anfocus on inno

nking, Wealthby Corporate Sical and operanance, human

mined by guideII framework a

a robust found

nd addresses

sment process

lity of risk andmeaningful disc

their minimumket, operationments (LR) Gu

n of our 2018urther informat

Disclosure ReRevised Standacalculating cask and securiti

phase of the Rober 31, 2018.

hin the meaninion Reform Acar 3 Report, ouother commun

ast”, “anticipate“will”, “may”, “sre subject to inons or conclusimanagement ob

of risk factorsents. Additionan our forward-loctors as well asing statement,

e-driven, princour vision, valund one of the

ovation and pro

Management,Support, whichational foundatin resources, ri

elines issued badopted by the

dation for banki

capital adequa

ses and superv

d capital profilclosures.

m regulatory caal, and securuideline, which Annual Repotion on the resp

equirements” (ards require c

apital requiremization activitie

Revised Stand This Pillar 3 re

ng of certain sct of 1995 andur 2018 Annualnications. Forwe”, “intend”, “eshould”, “could

nherent risks aons will not probjectives will ns could cause al information aooking statemes other uncertawhether writte

ciples-led apprues and stratege largest in thoviding excepti

Insurance, Inv consists of Teion required tosk manageme

by the Office oBasel Commit

ing supervision

acy, including

visory review to

les between b

pital required tritizations expoh reflects the Bort for further pective approa

(Revised Standomprehensive

ments institutees are replacedards for Canaeport provides

ecurities laws,d any applical Report, in oth

ward-looking stestimate”, “goad” or “would”. nd uncertaintieove to be accuot be achievedour actual re

about certain risents to make dainties and poten or oral, that

roach to delivgy to life so wehe world baseional experienc

vestor & Treasechnology & Oo effectively deent, internal au

of the Superintttee on Banking

n and financial

standards

o evaluate

banks and

to support variosures. We dCBS Basel III information o

ches:

dards) to encodisclosure of

d under Pillad by the Reviseadian domesticdisclosures ref

Q4 2018

1

including the ble Canadian

her filings with tatements are al”, “plan” and

By their very es, which give urate, that our d. We caution sults to differ sk factors can decisions with tential events. may be made

vering leadinge can help oured on market ces to our 16

sury Services,perations andliver products

udit and other

endent of the g Supervision

stability:

ous risks and determine our leverage ratio

on calculation

ourage market our risks and r 1. Existing ed Standards. c systemically flective of this

Ca

In M– coBasdatefurth

Royal Ban

apital framew

March 2017, thonsolidated ansel III framewoe for the BCBSher information

nk of Cana

work (continu

e BCBS issuedd enhanced frark, including thS phase two dn on other upco

ada Pillar 3

ued)

d its second phamework”. The

he leverage andisclosure requ

oming regulato

3 Report

hase of the Pille disclosure stad liquidity ratioirements. Refery reforms.

lar 3 disclosureandard consoli

os disclosure teer to the “Capit

e requirementsidates all existemplates. OSFtal manageme

s entitled, “Pillating Pillar 3 disFI has not yet rent” section of

ar 3 disclosure sclosure requirereleased the imour 2018 Annu

Q4 2018

2

requirements ements of the

mplementation ual Report for

DI

Re

Ovem

man

Royal Ban

ISCLOSURE

Pillar 3 equirement

erview of key metrics, risk nagement and

RWA

K

O

O

nk of Cana

MAP

Pillar 3 Req

M1

VA

a) Business profile

b) Risk gove

c) Communicenforcementthe bank d) Scope andrisk measuree) Risk inform

f) Stress test

g) Strategiesapplied to mmitigate risks

OV1

ada Pillar 3

uirement

model and risk

ernance structure

cation and t of risk culture with

d main features of ement systems mation reporting

ting

s and processes anage, hedge and s

3 Report

2018 Annual R

Risk managem

Top and emerg

Enterprise risk

Enterprise risk

hin Enterprise risk

Enterprise risk

Enterprise risk Enterprise risk Market risk Systemic risk

Enterprise risk

Credit risk

Market risk

Liquidity and fu

Insurance risk

Operational risk

Regulatory comStrategic risk Reputation riskCompetitive risSystemic risk

Consolidated FStatements

Report section

ent - OverviewObPrRi

ging risks To

management

RiRiRiRi

management RiRi

management Ri

management Ri

management Rimanagement Ri

Stn/

management RiRiRiOvCrCrCrCrCrMapoVaRiStMaIntSINoris

unding risk

OvRiRiFuLiqIns

k OvOp

mpliance risk ReSt

k Rek Co

Sy

Financial

NoinsDepu

NoinsDetra

NoinsDe

Sub-sec

bjectives and Risk rinciples isk pyramid op and emerging risisk governance isk appetite isk measurement isk control isk governance isk control

isk conduct and cu

isk measurement

isk control – Reporisk measurement –tress tests /a isk appetite isk measurement isk control verview redit risk measuremredit risk assessmeredit risk mitigationredit risk approvalredit risk administraarket risk controls –ositions alue-at-Risk and Stisk tress tests arket risk controls –terest Rate Risk (SIRR measurementon-trading foreign esk verview isk control isk measurement unding quidity coverage rasurance risk verview perational risk framegulatory compliantrategic risk eputation risk ompetitive risk ystemic risk ote 8 – Derivative fstruments and hederivatives issued fourposes

ote 8 – Derivative fstruments and hederivatives issued foading purposes

ote 8 – Derivative fstruments and hederivative-related cr

ction

Management

sks

lture

rting – Stress testing

ment ent n

ation – FVTPL

tressed Value-at-

– Structural SIRR)

exchange rate

atio

mework nce risk

financial dging activities - or trading

financial dging activities - or other than

financial dging activities - redit risk

2018 Annual Report

Reference

49

50 50-51

52 53 53 54 52 54

55

53

55 53-54

67 87-88

53 53 54 56 56

57-58 59 59 59

67

67

67

69

69

70

72 73 73 75 79 83 83 83 85 85 85 87

87-88

171

171

173-174

Q4 2018

3

Frequency of Disclosure

Quarterly

Annual

Annual Annual Annual Annual Annual Annual Annual Annual

Annual

Annual

Annual Annual Annual Annual Annual Annual Annual Annual Annual Annual Annual Annual Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual Annual Annual Annual Annual Annual Annual Annual Annual Annual Annual Annual Annual

Annual

Annual

Annual

Quarterly

DI

Re

Linka

stare

C

Royal Ban

ISCLOSURE

Pillar 3 equirement

ages between financial tements and regulatory exposures

L

L

L

Credit risk

C

C

C

C

C

nk of Cana

MAP (contin

Pillar 3 Req

LI1

LI2

LIA

RA

a) Translatiomodel into ththe bank’s cr

b) Criteria anfor defining cmanagemensetting credit

c) Structure the credit riscontrol funct

d) Interactionrisk managecompliance afunctions

e) Scope andreporting on to the executand to the bo

R1

R2

RB

a) The scope“past due” anexposures upurposes anany, betweenpast due andaccounting apurposes. b) The extenexposures (mthat are not cimpaired andthis.

c) Descriptiofor determini

d) The bank’restructured

RC

a) Core featuprocesses foof the extentmakes use obalance shee

b) Core featuprocesses foevaluation an

c) Informatiocredit risk cothe credit risinstruments

ada Pillar 3

nued)

uirement

on of the business he components of redit risk profile

nd approach used credit risk t policy and for t risk limits

and organization ok management andion

n between the credment, risk control, and internal audit

d content of the credit risk exposurtive management oard of directors

e and definitions ofnd “impaired” sed for accounting d the differences, in the definition of d default for and regulatory

nt of past-due more than 90 days)considered to be d the reasons for

on of methods useding impairments.

’s own definition of exposure.

ures of policies andor, and an indicationt to which the bank of, on– and off–et netting

ures of policies andor collateral nd management

on about market or oncentrations underk mitigation used

3 Report

2018 Annual R

Credit risk

Enterprise risk

Credit risk

f d Enterprise risk

dit

Enterprise risk

re Enterprise risk

f

f Consolidated FStatements

) Consolidated FStatements

d Consolidated FStatements

a Consolidated FStatements

d n

Credit risk

Consolidated FStatements

Consolidated FStatements

d Credit risk

r Credit risk

Consolidated FStatements

Report section

Ov

Gr

management

Ri

Ri

Ri

Ri

Ov

Cr

Cr

Cr

management Ri

Ri

management Ri

management Ri

Ri

Financial

NoacjudDeCr(S

Financial NoacjudDe

Financial NoacjudAl

Financial NoacjudMo

Co

Financial NoinsDe

Financial Noan

Cr

Cr

Cr

Financial Noins

Sub-sec

verview

ross credit risk exp

isk governance

isk appetite

isk measurement

isk control - Author

verview

redit risk assessme

redit risk mitigation

redit risk approval

isk governance

isk control

isk governance

isk governance

isk control - Report

ote 2 – Summary occounting policies, dgments - efinition of defaultredit impaired finan

Stage 3)

ote 2 – Summary occounting policies, dgments - efinition of default

ote 2 – Summary occounting policies, dgments - llowance for credit ote 2 – Summary occounting policies, dgments -

Modifications

ounterparty credit r

ote 8 – Derivative fstruments and hederivative-related crote 30 – Offsetting nd financial liabilitie

redit risk mitigation

redit risk mitigation

redit risk approval -

ote 8 – Derivative fstruments and hed

ction

posure

rities and limits

ent

n

ting

of significant estimates and

ncial assets

of significant estimates and

of significant estimates and

losses of significant estimates and

risk

financial dging activities – redit risk

financial assets es

n - Collateral

n

- Credit risk limits

financial dging activities

2018 Annual Report

Reference

56

57

52

53

53

55

56

57-58

59

59

52

54

52

52

55

125

125

123-126, 129

126

58

173-174

207-208

59

59

59

170-178

Q4 2018

4

Frequency of Disclosure

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Semi-annual

Semi-annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

DI

Re

C(c

Coc

Royal Ban

ISCLOSURE

Pillar 3 equirement

Credit risk continued)

C

C

C

C

C

C

C

C

C

CR

ounterparty credit risk

CC

CC

CC

CC

CC

CC

CC

CC

CC

nk of Cana

MAP (contin

Pillar 3 Req

R3

RD

R4

R5

RE

R6

R7

R8

R9

R10

CRA

a) Risk manaand policies counterparty

b) The methothe operatingterms of intecounterpartyand for CCP

c) Policies reand other risassessmentscounterpartyexposures to

d) Policies wwrong-way re) The impacamount of cobank would bprovide givendowngrade

CR1

CR2

CR3

CR4

CR5

CR6

CR7

CR8 f) Exposurescounterpartie

ada Pillar 3

nued)

uirement

agement objectivesrelated to

y credit risk

od used to assign g limits defined in rnal capital for

y credit exposures exposures

elating to guaranteesk mitigants and s concerning y credit risk, includinowards CCPs

with respect to isk exposures ct in terms of the ollateral that the be required to n a credit rating

s to central es

3 Report

2018 Annual R

n/a

s

Credit risk

Consolidated FStatements

Consolidated FStatements

Credit risk

es

ng

Credit risk

Consolidated FStatements

Consolidated FStatements

Credit risk

Liquidity and fu

n/a

Report section

n/

CrCo

Financial NoinsDe

Financial Noacjud

CrCo

CrCo

Financial NoinsDe

Financial NoanCrCo

unding risk Cr

n/

Sub-sec

/a

redit risk assessmeounterparty credit rote 8 – Derivative fstruments and hederivative-related crote 2 – Summary occounting policies, dgements – Deriva

redit risk assessmeounterparty credit r

redit risk assessmeounterparty credit rote 8 – Derivative fstruments and hederivative-related crote 30 – Offsetting nd financial liabilitieredit risk assessmeounterparty credit r

redit ratings

/a

ction

ent – risk financial

dging activities – redit risk of significant estimates and

atives

ent – risk

ent – risk financial

dging activities – redit risk

financial assets es ent – risk

2018 Annual Report

Reference

n/a

58

173-174

126, 129, 133-134

58

58

173-174

207-208

58

78

n/a

Q4 2018

5

Frequency of Disclosure

Semi-annual

Annual

Semi-annual

Semi-annual

Annual

Semi-annual

Semi-annual

Quarterly

Annual

Semi-annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Semi-annual

Semi-annual

Semi-annual

Semi-annual

Semi-annual

Semi-annual

Quarterly

Semi-annual

DI

Re

Se

M

Royal Ban

ISCLOSURE

Pillar 3 equirement

ecuritization

SE

SE

SE

SE

SE

Market risk M

nk of Cana

MAP (contin

Pillar 3 Req

ECA

a) Objectivessecuritization

b) List of SPsponsor / prosupport

c) Accountinsecuritization

d) the namesassessment used for sectypes of secufor which eac

e) Use of Bapurposes

f) Use of othassessment

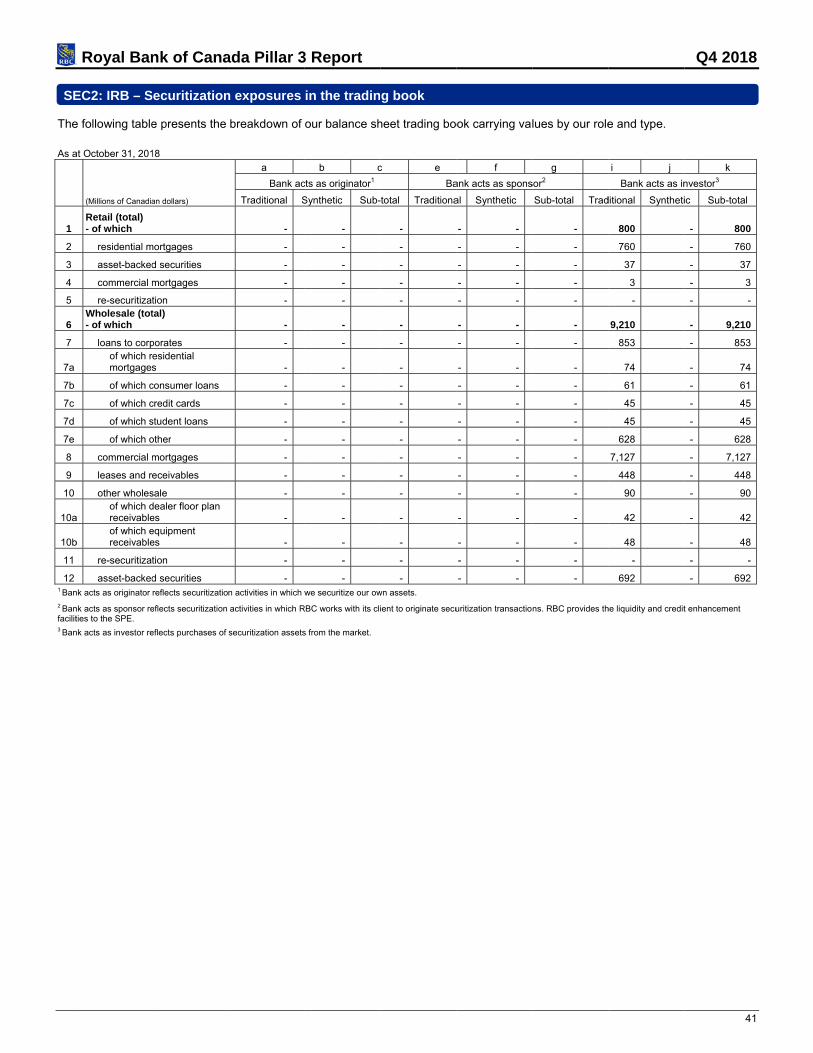

EC1 Securitizatiobanking boo

EC2 Securitizatiotrading book

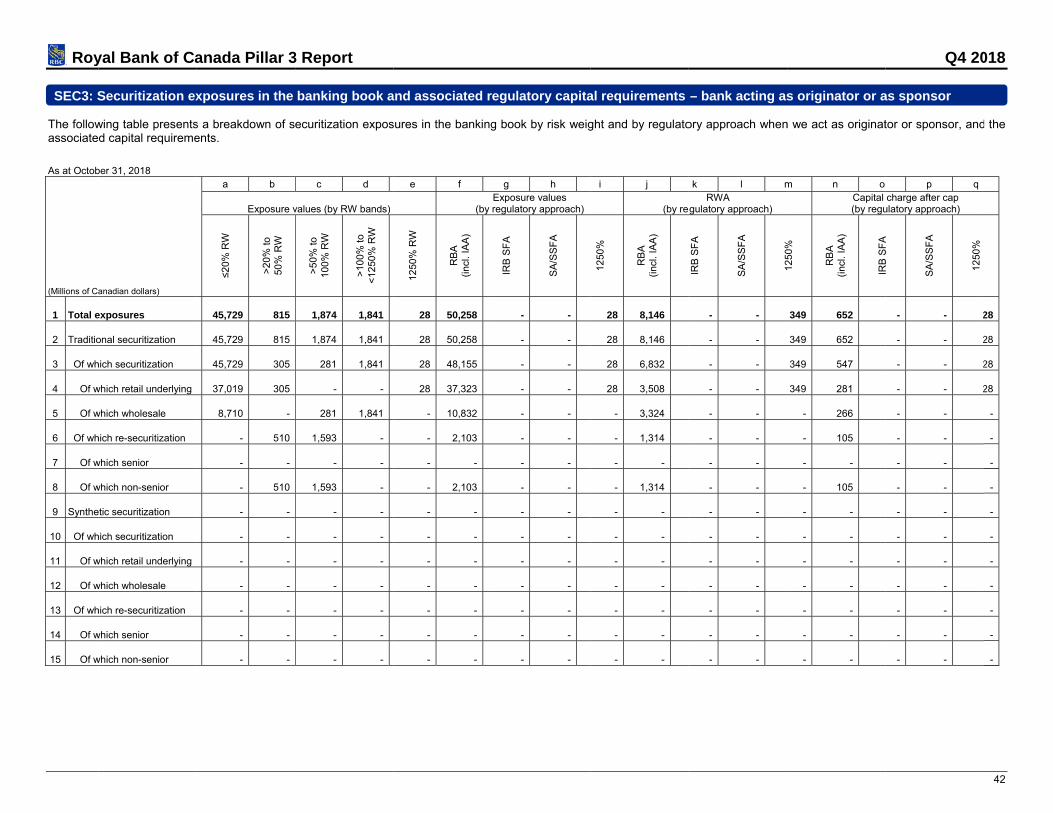

EC3

Securitizatiobanking booregulatory cabank acting asponsor

EC4

Securitizatiobanking boocapital requiracting as inv

RA

a) Processesidentify, meacontrol the b

Policies for hstrategies/prmonitoring theffectiveness

b) Descriptiogovernance established tstrategies anbank

Description oand the commechanismsdifferent partmarket risk m

ada Pillar 3

nued)

uirement

s in relation to n activities

Es where RBC is ovides implicit

g policies for n

s of external credit institution (ECAIs) uritizations and theuritization exposurech agency is used

asel IAA for capital

er internal for capital purposen exposures in the k n activities in the

k n exposures in the k and associated apital requirementsas originator or as

n exposures in the k and associated rements - bank

vestor

s implemented to asure, monitor and ank’s market risks

hedging risk and rocesses for he continuing s of hedges

on of the market risstructure to implement the nd processes of the

of the relationshipsmunication

s between the ties involved in management

3 Report

2018 Annual R

Off-balance shearrangementsConsolidated FStatements Consolidated FStatements

Consolidated FStatements

Consolidated FStatements

Critical accountand estimates

e e

Capital Manage(also refer to Cdocument)

Credit risk

Capital Manage

es Credit risk

s -

Market risk

Consolidated FStatements

k

e Enterprise risk

Enterprise risk

Report section

eet Of

Financial Noas

Financial No

Financial No

Financial

Noacjud

Noacjudfin

ting policies Co

ement RD in this

Rese

n/

ement Rese

Cr

MapoStMapoMaFVliaMaInt

SI

MaIntMama

Financial Noacjud

management

Ri

Ri

Ri

Ri

St

Ri

management

Ri

Ri

Sub-sec

ff-balance sheet ar

ote 6 – Derecognitissets

ote 7 – Structured

ote 7 – Structured

ote 2 – Summary occounting policies, dgments – Basis o

ote 2 – Summary occounting policies, dgments – Derecognancial assets

onsolidation of stru

egulatory capital apecuritization exposu

/a

egulatory capital apecuritization exposu

redit risk assessme

arket risk controls –ositions tress Tests arket risk measureositions arket risk measureVTPL positions – Aabilities of RBC Insuarket risk controls –terest Rate Risk (S

IRR measurement

arket risk measureterest Rate Sensitiarket risk measureaterial non-trading

ote 2 – Summary occounting policies, dgements – Hedge

isk Governance

isk Appetite

isk Measurement

isk Control

tress Testing

isk Conduct and Cu

isk governance

isk Control

ction

rrangements

ion of financial

entities

entities

of significant estimates and

of consolidation

of significant estimates and gnition of

uctured entities

pproach for ures

pproach for ures

ent

– FVTPL

es – FVTPL

es for other Assets and urance – Structural

SIRR) positions

es – Structural vities

es for other portfolios

of significant estimates and

e accounting

ulture

2018 Annual Report

Reference

47-49

166

167-170

167-170

121-122

133

102

98-99

56-59

98-99

57-58

67

67

68

69

69

69

69

70

134

52

53

53

54

53-54

55

52

54

Q4 2018

6

Frequency of Disclosure

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Semi-annual

Semi-annual

Semi-annual

Semi-annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

DI

Re

M(c

Royal Ban

ISCLOSURE

Pillar 3 equirement

Market risk continued)

M(cont

M

M

M

M

M

Operational risk

Interest rate risk i

nk of Cana

MAP (contin

Pillar 3 Req

RA tinued)

c) Scope andreporting andsystems

RB

c) General dmodels (VaR

g) Descriptioapplied to thparameters

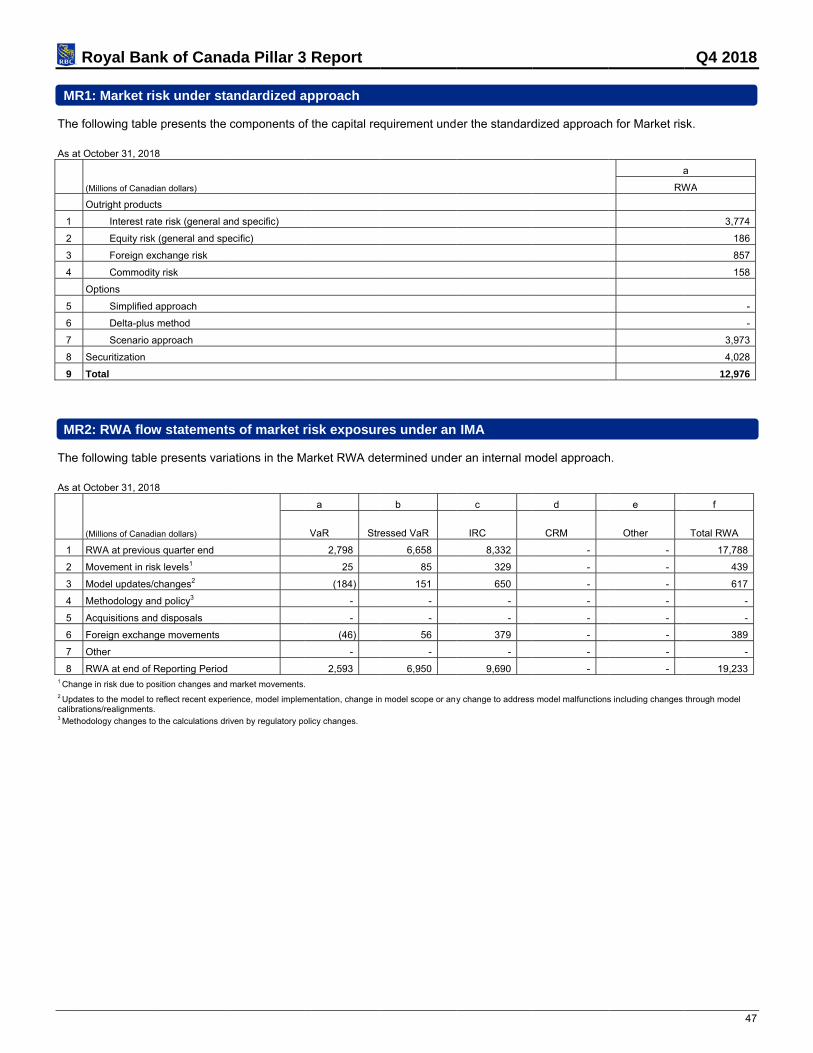

MR1 MR2

MR3

MR4

a) Details of operational rassessment qualifies

b) Descriptiomeasuremenoperational r

c) Descriptioinsurance fomitigating op

in the banking book

ada Pillar 3

nued)

uirement

d nature of risk d/or measurement

escription of the R/stressed VaR)

on of stress testing e modelling

the approach for risk capital for which the bank

on of the advanced nt approaches for risk (AMA)

on of the use of r the purpose of

perational risk

k

3 Report

2018 Annual R

Enterprise risk

Market risk

Market risk

Market risk

k

Operational risk

Capital manage

Operational risk

Capital manage

Operational risk

Market risk

Report section

management

Ri

Ri

St

Mapo

St

Mapo

MaFVlia

MaInt

SI

MaInt

Mama

Mapo

St

k Op

ement Atbu

k Op

ement Atbu

k Op

Ma

Sub-sec

isk Measurement

isk Control

tress Testing

arket risk controls –ositions

tress Tests

arket risk measureositions

arket risk measureVTPL positions - Aabilities of RBC Insu

arket risk controls –terest Rate Risk (S

IRR measurement

arket risk measureterest Rate Sensiti

arket risk measureaterial non-trading

arket risk controls –ositions

tress Tests

perational risk capi

ttributed capital in tusiness activities

perational risk capi

ttributed capital in tusiness activities

perational risk capi

arket risk

ction

– FVTPL

es – FVTPL

es for other Assets and urance

– Structural SIRR) positions

es – Structural vities

es for other portfolios

– FVTPL

ital

the context of our

ital

the context of our

ital

2018 Annual Report

Reference

53

54

53-54

67

67

68

69

69

69

69

70

67

67

84

97-98

84

97-98

84

67-72

Q4 2018

7

Frequency of Disclosure

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Annual

Semi-annual

Quarterly

Semi-annual

Semi-annual

Annual

Annual

Annual

Annual

Annual

Annual

OV

KM

1

2

3

4

5

6

7

8

9

10

11

12

13

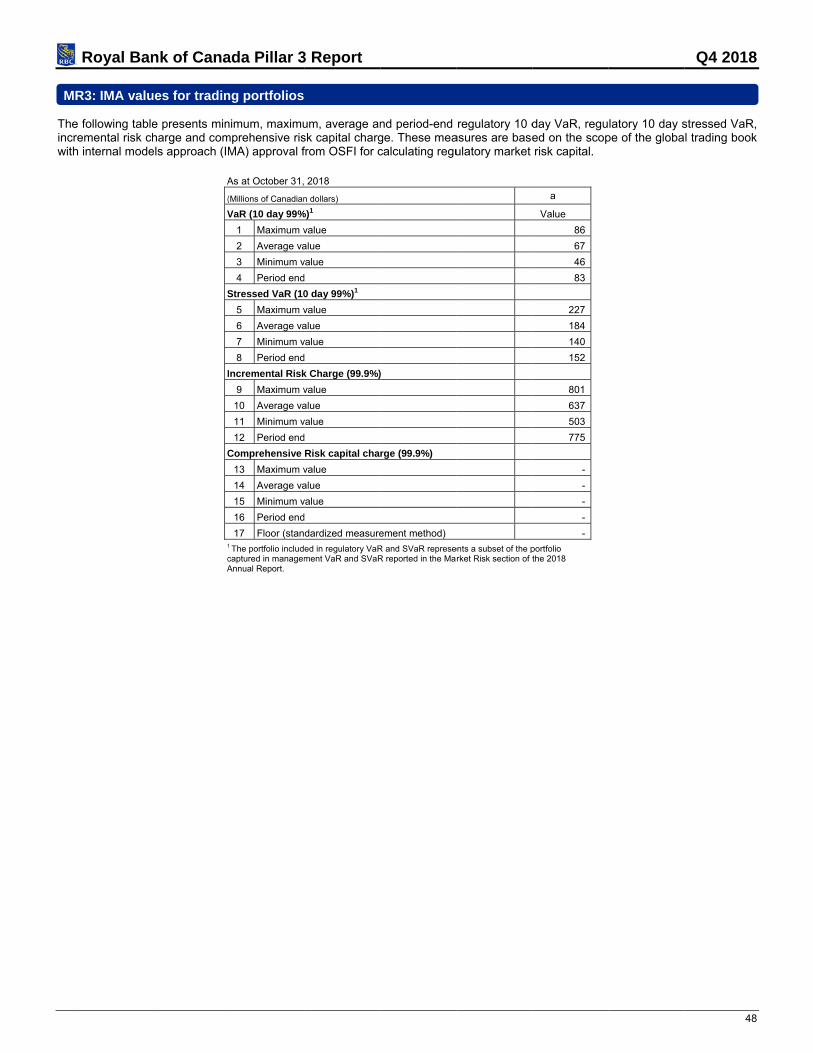

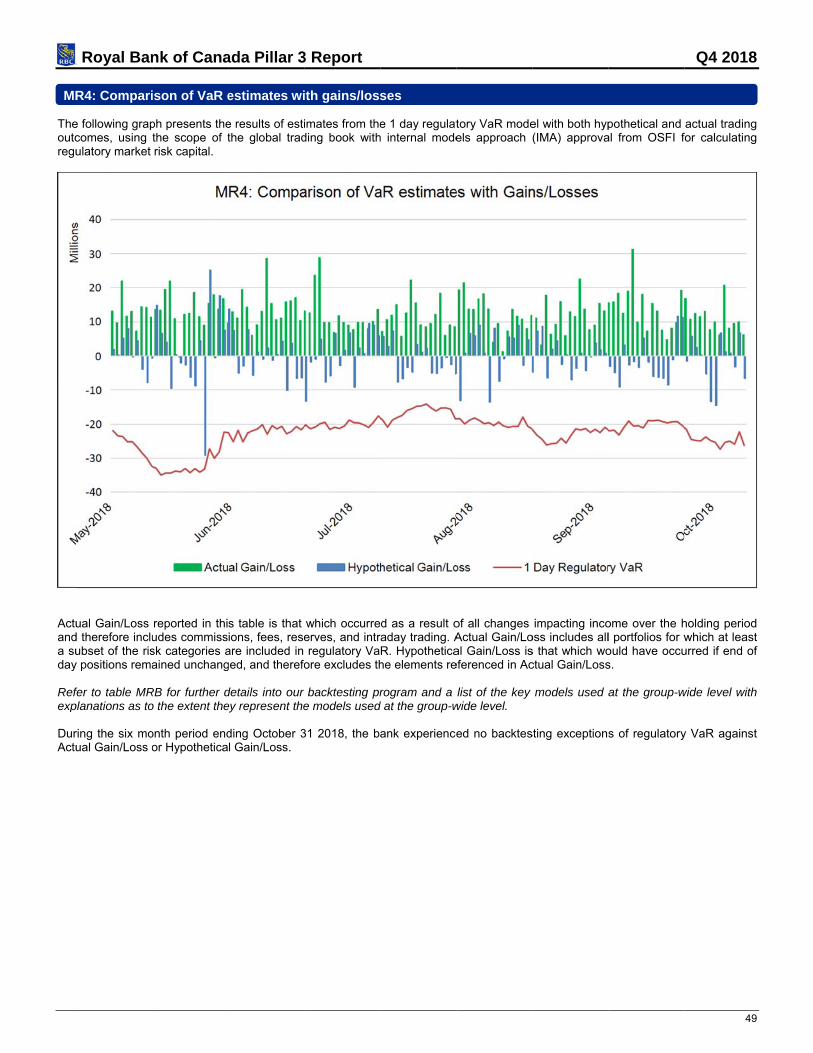

14 1 8%

Royal Ban

VERVIEW OF

M1: Key Cap

(Millions of Cana

Available capi

Common Equit

Tier 1

Total capital

Risk-weighted

Total risk-weig

Risk-based ca

Common Equit

Tier 1 ratio

Total capital ra

Additional CE

Capital conserv

Countercyclica

Bank G-SIB an

Total of bank C

CET1 available

Basel III levera

Total Basel III l

Basel III levera

reflects minimum ca

nk of Cana

F KEY METR

pital and Leve

dian dollars)

ital (amounts)

ty Tier 1 (CET1)

d assets (amount

hted assets (RWA

apital ratios as a

ty Tier 1 ratio

atio

ET1 buffer require

vation buffer requ

al buffer requireme

nd/or D-SIB additio

CET1 specific buff

e after meeting the

age ratio

leverage ratio exp

age ratio (row 2 / r

apital requirements w

ada Pillar 3

RICS, RISK M

erage metric

ts)

A)

percentage of R

ements as a perc

irement

ent

onal requirements

fer requirements (

e bank's minimum

posure measure

row 13)

which includes D-SIB

3 Report

MANAGEMEN

cs (at consoli

RWA

centage of RWA

s

row 8 + row 9 + ro

m capital requirem

B/G-SIB surcharge. R

NT AND RWA

idated group

ow 10)

ents (row 5 - 8%)

Refer to our Capital

A

p level)

)1

Management sectio

a

October 31

2018

57,001

63,279

72,494

496,459

11.5%

12.8%

14.6%

2.5%

-

1.0%

3.5%

3.5%

1,450,769

4.4%

n of our 2018 Annua

b

July 31

2018

55,054

61,332

70,525

498,896

11.1%

12.3%

14.1%

2.5%

-

1.0%

3.5%

3.1%

1,413,899

4.3%

al Report

Q4 2018

8

c

Change

1,947

1,947

1,969

(2,437)

0.4%

0.5%

0.5%

0.4%

36,870

0.1%

OV

Theincohttp

a)

b)

c)

d)

e)

f)

g)

Royal Ban

VA: Bank ris

e table below porporated by rp://www.rbc.com

Pillar 3 disclos

Business model

Risk governance

Communication culture within the

Scope and mainmeasurement syRisk information

Stress testing

Strategies and pmanage, hedge

nk of Cana

sk manageme

presents an ovreference into m/investorrelat

sures requireme

and risk profile

e structure

and enforcement e bank

features of risk ystems

reporting

processes applied and mitigate risks

ada Pillar 3

ent approach

verview of Pillathis Pillar 3

ions

nt RBC

Risk ma

Top and

Enterpr

Enterpr

of risk Enterpr

Enterpr

EnterprEnterprMarket System

to s

Enterpr

Credit r

Market

Liquidity

Insuran

Operatio

RegulatStrategiReputatCompetSystem

Consoli

3 Report

h

r 3 disclosure report. Our 2

C 2018 Annual Re

anagement overvi

d emerging risks

ise risk managem

ise risk managem

ise risk managem

ise risk managem

ise risk managemise risk managemrisk ic risk

ise risk managem

isk

risk

y and funding risk

ce risk

onal risk

tory compliance riic risk tion risk titive risk ic risk

dated Financial S

requirements 2018 Annual R

eport section

ew

ment

ment

ment

ment

ment ment

ment

k

sk

Statements

that have beeReport is avai

Objectives and RRisk pyramid Top and emerginRisk governanceRisk appetite Risk measuremeRisk control Risk governanceRisk control

Risk conduct an

Risk measureme

Risk control – RRisk measuremeStress tests n/a Risk appetite Risk measuremeRisk control Overview Credit risk measCredit risk assesCredit risk mitigaCredit risk approCredit risk adminMarket risk contValue-at-Risk anStress tests Market risk contpositions SIRR measuremNon-trading foreOverview Risk control Risk measuremeFunding Liquidity coveragInsurance risk Overview Operational risk Regulatory compStrategic risk Reputation riskCompetitive riskSystemic risk Note 8 - DerivatiDerivatives issueNote 8 - DerivatiDerivatives issueNote 8 - DerivatiDerivative-relate

n met within oilable free of

Sub-se

Risk Managemen

ng risks e

ent

e

d culture

ent

Reporting ent – Stress testin

ent

surement ssment ation oval nistration rols – FVTPL posnd Stressed Value

rols – Structural In

ment eign exchange rate

ent

ge ratio

framework pliance risk

k

ive financial instrued for trading purpive financial instrued for other-than-ive financial instru

ed credit risk

our 2018 Annuacharge on ou

ection

t Principles

ng

sitions e-at-Risk

nterest Rate Risk

e risk

uments and hedgirposes

uments and hedgi-trading purposesuments and hedgi

Q4 2018

9

al Report andur website at

(SIRR)

ng activities –

ng activities –

ng activities –

OV

The

1

2

3

4

4a

4b

5

6

7

8

9

10

11

12

12a

13

14

15

16

17

18

19

20

21

22

23

24

25 1 Amoamou2 Amo3 Amo

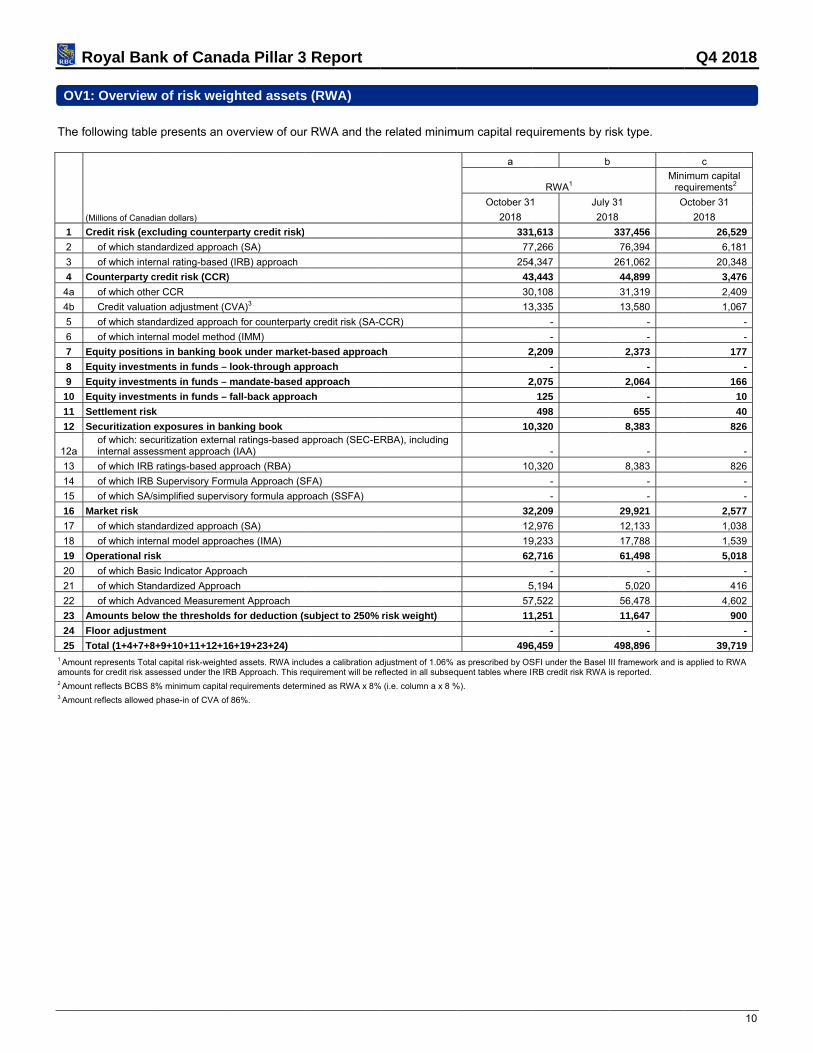

Royal Ban

V1: Overview

e following table

(Millions of Canad

Credit risk (ex

of which stan

of which inte

Counterparty c

of which othe

Credit valuat

of which stan

of which inte

Equity positio

Equity investm

Equity investm

Equity investm

Settlement ris

Securitization

a of which: secinternal asse

of which IRB

of which IRB

of which SA/

Market risk

of which stan

of which inte

Operational ris

of which Bas

of which Sta

of which Adv

Amounts below

Floor adjustme

Total (1+4+7+8

ount represents Totaunts for credit risk as

ount reflects BCBS 8

ount reflects allowed

nk of Cana

w of risk weig

e presents an o

dian dollars)

cluding counterp

ndardized approac

ernal rating-based

credit risk (CCR)

er CCR

tion adjustment (C

ndardized approac

ernal model metho

ns in banking bo

ments in funds –

ments in funds –

ments in funds –

k

exposures in bacuritization externessment approach

B ratings-based ap

B Supervisory Form

/simplified supervi

ndardized approac

ernal model approa

sk

sic Indicator Appro

ndardized Approa

vanced Measurem

w the thresholds

ent

8+9+10+11+12+1

al capital risk-weightessessed under the IR

8% minimum capital

d phase-in of CVA of

ada Pillar 3

ghted assets

overview of our

party credit risk)

ch (SA)

(IRB) approach

)

CVA)3

ch for counterpart

od (IMM)

ook under marke

look-through ap

mandate-based

fall-back approa

anking book

al ratings-based ah (IAA)

pproach (RBA)

mula Approach (S

isory formula appr

ch (SA)

aches (IMA)

oach

ach

ment Approach

s for deduction (s

6+19+23+24)

ed assets. RWA inclRB Approach. This re

requirements determ

f 86%.

3 Report

s (RWA)

r RWA and the

ty credit risk (SA-C

et-based approac

pproach

approach

ach

approach (SEC-E

SFA)

roach (SSFA)

subject to 250%

udes a calibration adequirement will be re

mined as RWA x 8%

e related minim

CCR)

ch

RBA), including

risk weight)

djustment of 1.06% eflected in all subseq

% (i.e. column a x 8 %

mum capital req

a

October 31

2018

331

77

254

43

30

13

2

2

10

10

32

12

19

62

5

57

11

496

as prescribed by OSquent tables where I

%).

uirements by r

b

RWA1

1 July

20

1,613

7,266

4,347

3,443

0,108

3,335

-

-

2,209

-

2,075

125

498

0,320

-

0,320

-

-

2,209

2,976

9,233

2,716

-

5,194

7,522

1,251

-

6,459

SFI under the Basel RB credit risk RWA

risk type.

b

Min req

y 31 O

18

337,456

76,394

261,062

44,899

31,319

13,580

-

-

2,373

-

2,064

-

655

8,383

-

8,383

-

-

29,921

12,133

17,788

61,498

-

5,020

56,478

11,647

-

498,896

III framework and is is reported.

Q4 2018

10

c

imum capital quirements2

October 31

2018

26,529

6,181

20,348

3,476

2,409

1,067

-

-

177

-

166

10

40

826

-

826

-

-

2,577

1,038

1,539

5,018

-

416

4,602

900

-

39,719

applied to RWA

LI

LIsta

Thewithfina As a

(MillioAsseCasInterSecu

TIn

AsseagreLoan

RW

A

SegOthe

CDPGOO

TotaLiabDep

PBB

SegOthe

AOOreDInO

SubTotaEqu

PCRO

NonTotaTota1 Colu2 Der

Royal Ban

NKAGES BE

1: Differencatement cate

e following tablh International ancial statemen

at October 31, 201

ons of Canadian dolets h and due from brest-bearing depurities rading

nvestment, net of a

ets purchased ueements and secns

Retail Wholesale

Allowance for loan

regated fund neter

Customers' liabilityDerivatives2

remises and equiGoodwill Other intangibles Other assets

al assets2 bilities and equityposits

ersonal usiness and goveank

regated fund neter

Acceptances Obligations relatedObligations relatedepurchase agreem

Derivatives2 nsurance claims a

Other liabilities

ordinated debenal liabilities2 ity attributable toreferred shares

Common shares Retained earnings Other components

n-controlling inteal equity

al liabilities and e

umn c to g reflect a f

rivative assets and lia

nk of Cana

ETWEEN FINA

es between egories with

e provides the Financial Rep

nts into regulato

18

lars)

banks posits with banks

applicable allowa

nder reverse repcurities borrowed

losses

t assets

y under acceptanc

pment, net

y

ernment

t liabilities

to securities sold to assets sold un

ments and securiti

and policy benefit l

ntures

o shareholders

of equity

rests

equity2

further breakout of c

abilities are subject t

ada Pillar 3

ANCIAL STA

accountingregulatory r

differences beorting Standarory risk categor

Cva

repf

sta

s

nce

purchase d

ces

1

d short nder es loaned

liabilities

1

1

olumn b by providing

to both counterparty

3 Report

ATEMENTS A

g and regularisk categorie

etween carryingrds (IFRS) andries.

a

Carrying alues as ported in ublished inancial atements

Cavalue

scoregu

conso

30,209 36,471

128,258 1

94,608 222,866 2

294,602 2

399,452 3180,278 1579,730 5

(2,912)576,818 5

1,368

15,641 94,039 2,832

11,137 4,687

44,064 172,400 1

1,334,734 1,3

270,154 2534,371 5

32,521 837,046 8

1,368

15,662 32,247

206,814 290,238 10,000 52,273

407,234 39,131

1,254,779 1,2

6,309 17,617 51,112 4,823

79,86194

79,9551,334,734 1,3

g the respective CAR

credit risk and mark

AND REGULA

atory scopeses

g values presed our regulatory

b c

rrying es under ope of ulatory olidation

Subjeccredit framew

30,207 3036,471 36

120,162

92,555 79212,717 8

294,602

399,167 389178,280 166577,447 556

(2,912)574,535 556

-

15,641 1594,125 2,829 2

11,137 4,603

45,480 37173,815 56322,347 759

270,154 534,492

32,521 837,167

-

15,662 32,247

206,814 90,238

- 51,077

396,038 9,131

242,336

6,309 17,617 51,114 4,877

79,91794

80,011322,347

R guideline framewo

ket risk framework –

ATORY EXPO

s of consol

ented in our finy exposures. I

d

C

ct to risk

work

Subject counterpa

credit risframewo

0,207 6,471

1,432 9,685 1,117

- 294,6

9,534 6,566 46,100 4

- 6,100 4

-

5,641 - 94,

2,829 - -

7,554 4,56,024 98,79,919 393,7

- - - --

- -

- 206,8- 90,2- - - 297,0- - 297,0

- - - - -- -- 297,0

orks utilized.

hence column b will

OSURES

lidation and

ancial statemet further break

e

Carrying values o

to arty sk ork

Subject to thsecuritizatio

framework

- -

- 18- 12,87- 13,05

602

- 479 6,47479 6,47

- 479 6,47

-

- 125

- - -

593 2718 2799 19,55

- - - --

- -

814 238

- -

052 -

052

- - - - -- -

052

not equal to the sum

mapping o

ents prepared iks down the am

f

f items:1

he n

Subject to the market risk framework

- -- -

87 118,54370 -57 118,543

- -

- -74 3,47774 3,477

- -74 3,477

- -

- -- 91,192- -- -- -

23 2,60823 93,80054 215,820

- -- -- -- -- -

- -- -

- -- 87,761- -- -- 87,761- -- 87,761

- -- -- -- -- -- -- -- 87,761

m of column c to g.

Q4 2018

11

of financial

n accordance mounts in our

g

Not subject to capital

requirements / or subject to

deduction from capital

- -

- - -

-

9,633 1,284

10,917 (2,912)8,005

-

- - -

11,137 4,603

702 16,442

24,447

270,154 534,492

32,521 837,167

-

15,662 32,247

- - -

51,077 98,986 9,131

945,284

6,309 17,617 51,114 4,877

79,91794

80,0111,025,295

LI2sta

Thecarr

As a

1

2

3

4

5

6

7

8

9

10

1 Am– hen2 Off-

Royal Ban

2: Main souatements

e following tabrying values as

at October 31, 201

(Millions of Canad

Asset carryingregulatory con

Liabilities carryof consolidation

Total net amouconsolidation

Off-balance she

Differences due

Differences duethose already in

Differences due

Differences due

Difference due securitizations a

Exposure amopurposes

ount reflects Table Lnce column a will no

-balance sheet amou

nk of Cana

urces of diffe

ble provides ths presented in o

18

dian dollars)

g value amount unsolidation (as pe

ing value amount n (as per template

nt under regulator

eet amounts2

e to Fair Value adj

e to different nettinncluded in row 2

e to consideration

e to prudential filte

to accounting andand other items

ounts considered

LI1 columns (c), (d), t equal to the sum of

unts reflect the applic

ada Pillar 3

erences betw

he key differenour financial sta

under scope of er template LI1)1

under regulatory e LI1)1

ry scope of

justment

ng rules, other tha

of provisions

ers

d risk treatment of

d for regulatory

(e) and (f) from the pf column b to e.

cation of credit conv

3 Report

ween regula

nces between atements that a

a

Tot

1,2

scope 2

1,0

1,1

an

f

2,1

previous page. Deriv

version factors.

atory exposu

the exposure are within the s

tal Credfram

297,900

297,052

000,848

114,918

299

995

306

-

5,195

122,561 1

vative assets and liab

ure amounts

amounts for scope of regula

b

dit risk mework

Secfra

759,919

-

759,919

306,189

299

995

306

-

3,626

1,071,334

bilities are subject to

s and carryi

regulatory puatory consolida

c

Items subject

curitization amework

C

f

19,554

-

19,554

42,215

-

-

-

-

1,569

63,338

o both counterparty c

ing values i

rposes and thation.

d

t to: ounterparty credit risk framework

393,799

297,052

96,747

766,514

-

-

-

-

-

863,261

credit risk and marke

Q4 2018

12

n financial

he accounting

e

Market risk framework

215,820

87,761

128,059

-

(3,429)

-

-

-

-

124,630

et risk framework

LIA

OurStathe In Tcate(colbalainsu In Tqua Ourdebundcon Regrevesecdiffediffeexp ThesecCAR OurprudReprisk

Royal Ban

A: Explanati

r consolidated ndards (IFRS) required regula

Template LI1: egories with reumn a in LI1) ance sheet, onurance subsidia

Template LI2: Mantify measurem

r banking bookbt securities cader the Credit version factors

gulatory carryinerse repurchas

curities loaned erences betweerences in allo

posure amount.

e regulatory cacuritization holdR guidelines C

r trading book dent valuation port - Risk Mank to selected ba

nk of Cana

ons of differ

balance sheeas issued by t

atory requirem

Differences begulatory risk c

and our regn which capital aries as prescr

Main sources oment difference

k regulatory cararried at fair va

risk frameworks and undrawn

ng values for ose agreementsare determineen the accountwed IFRS and.

arrying value odings as well ahapter 7 but ar

regulatory carrguidance requ

nagement sectalance sheet ite

ada Pillar 3

rences betwe

et (“accountingthe Internationents prescribed

between accoucategories, wegulatory capital

adequacy reqribed by OSFI’s

of differences bes other than re

rrying values realue through otk, are measuramounts.

our Counterpar and securitiesd using OSFI’sting and regula

d regulatory ne

of exposures as our securitizre not consider

rying values areuirements, as stion which provems.

3 Report

een accounti

balance sheeal Accounting d by OSFI to d

unting and rege identify the dl consolidated uirements are s CAR guidelin

between regulaegulatory conso

eflect our IFRSther comprehered at amortize

rty credit risk rs borrowed ands CAR guidelinatory amounts etting rules, and

subject to thezed credit cardred securitized

e determined astated in CAR vides further in

ing and regu

et”) is prepareStandards Boaetermine our re

ulatory scopesdifferences betw

balance sheetdetermined, rees.

atory exposure olidation.

S accounting bansive income ed cost. Off-ba

related to our dd obligations renes Chapter 4 relate to regulad also applicat

e securitizationd exposures wfor the purpose

as prescribed uChapter 9 sec

nsight into how

ulatory expos

ed in complianard. We leveraegulatory capit

s of consolidaween our IFRSt (column b ineflects all of ou

amounts and c

alance sheet v(FVOCI) (availalance sheet r

derivative asseelated to assetSettlement an

atory inclusiontion of financia

n framework inhich meet the es of our IFRS

under the CARction 9.8 to ou

w we measure

sure amount

nce with Internage our accountal consolidated

ation and mapS consolidated

n LI1). Our regur consolidated

carrying values

values except flable for sale (regulatory asse

ets and liabilitiets sold under r

nd Counterpart of potential fu

al collateral in t

ncludes our onrisk transferen

S accounting ba

R guidelines Chur trading bookour market ris

ts

national Financnting balance sd balance shee

pping of financd accounting bgulatory capitald subsidiaries e

s in financial st

for our fair valu(AFS) under IAet values refle

es, assets purcrepurchase agrty risk framewouture exposure the calculation

n-balance shence requiremealance sheet.

hapter 9. We ek. Refer to our k and the linka

Q4 2018

13

cial Reporting sheet to applyet.

cial statement balance sheet consolidated except for our

tatements, we

ued loans and AS 39), which ect prescribed

chased under reements and ork. The main amounts and of regulatory

et third party nts under the

mploy OSFI’s 2018 Annual

age of market

CR

CR

Theincohttp

P

a)

b)

c)

d)

e)

Royal Ban

REDIT RISK

RA: General

e table below porporated by rp://www.rbc.com

Pillar 3 disclos

Translation ofinto the compcredit risk pro

Criteria and adefining creditpolicy and for limits

Structure andcredit risk mafunction

Interaction bemanagement,compliance anfunctions

Scope and coon credit risk executive manboard of direc

nk of Cana

qualitative in

presents an ovreference into m/investorrelat

sures requirem

f the business monents of the bfile

pproach used t risk managemsetting credit r

organization onagement and

etween the cred, risk control, nd internal aud

ontent of the reexposure to thenagement and

ctors

ada Pillar 3

nformation a

verview of Pillathis Pillar 3

ions

ment RBC

model bank’s Credit

for ment risk

Enterp

Credit

of the control Enterp

dit risk

dit Enterp

porting e to the

Enterp

3 Report

about credit

r 3 disclosure report. Our 2

2018 Annual R

t risk

prise risk mana

t risk

prise risk mana

prise risk mana

prise risk mana

risk

requirements 2018 Annual R

Report section

agement

agement

agement

agement

that have beeReport is avai

n

Overview

Gross credit

Risk govern

Risk appetit

Risk measu

Risk control

Overview

Credit risk a

Credit risk m

Credit risk a

Risk govern

Risk control

Risk govern

Risk govern

Risk control

n met within oilable free of

Sub-s

t risk exposure

ance

e

rement

- Authorities a

assessment

mitigation

approval

ance

ance

ance

- Reporting

our 2018 Annuacharge on ou

section

e

and limits

Q4 2018

14

al Report andur website at

CR

The

As a

1

2

3

4 1 Def2 Ref3 Off exclu

CR

Theand

For t

1

2

3

4

5

6

CR

Theincohttp

P

a)

b)

c)

d)

Royal Ban

R1: Credit qu

e following table

at October 31, 201

(Millions of Canad

Loans

Debt Securities

Off-Balance Sh

Total finition of default as pflects Stage 3 IFRS 9

balance sheet amouuded as per BCBS re

R2: Changes

e following tabld reductions in

the six months en

(Millions of Canad

Defaulted loan

Loans and debt

Returned to no

Amounts writte

Other changes

Defaulted loan

RB: Addition

e table below porporated by rp://www.rbc.com

Pillar 3 disclos

Definitions of exposures

Extent of past

Description ofdetermining im

Definition of aexposure

nk of Cana

uality of asse

e presents a co

18

dian dollars)

s

heet exposures3

per the CAR guidelin9 allowances only.

unts are before the aequirements.

s in stock of

e presents ourthe defaulted e

nded October 31, 2

dian dollars)

ns and debt secu

t securities that ha

n-defaulted status

n off

ns and debt secu

nal disclosur

presents an ovreference into m/investorrelat

sures requirem

past due and i

t due exposure

f methods usedmpairments

a restructured

ada Pillar 3

ets

omprehensive

a

Defaulted ex

nes.

application of credit c

defaulted loa

r defaulted expexposure balan

2018

urities at the end

ave defaulted sinc

s

urities at the end

re related to t

verview of Pillathis Pillar 3

ions

ment RBC

mpaired Cons

es Cons

d for Cons

Cons

3 Report

view of the cre

Gross carrying v

xposures1 N

2,027

-

289

2,316

conversion factors an

ans and deb

posure balancences due to writ

of the previous

ce the last reportin

of the reporting

the credit qu

r 3 disclosure report. Our 2

C 2018 Annual

solidated Finan

solidated Finan

solidated Finan

solidated Finan

edit quality of ou

b

values of

on-defaulted expo

5

2

8

nd reflect guarantees

t securities

s, the flows bete-offs.

reporting period

ng period

period

uality of asse

requirements 2018 Annual R

Report sectio

cial Statement

cial Statement

cial Statement

cial Statement

ur on- and off-b

Allowaosures

554,073

79,190

255,609

888,872

s given and irrevoca

etween non-def

d

ets

that have beeReport is avai

on

ts

Note 2 - Suestimates a"Definition "Credit imp

ts Note 2 - Suestimates a"Definition

ts Note 2 - Suestimates a"Allowance

ts Note 2 - Suestimates a"Modificatio

balance sheet

c

ances/impairments

7

7

able loan commitmen

faulted and de

n met within oilable free of

Sub-

ummary of signand judgmentsof default"

paired financial

ummary of signand judgmentsof default"

ummary of signand judgmentse for credit loss

ummary of signand judgmentsons”

assets.

s2 Net

(a

700

-

-

700

nts. Revocable loan

efaulted exposu

a

our 2018 Annuacharge on ou

-section

nificant accouns

assets (Stage

nificant accouns

nificant accouns ses"

nificant accouns

Q4 2018

15

d

values +b-c)

555,400

79,190

255,898

890,488

commitments are

ure categories

a

2,402

207

(148)

(841)

407

2,027

al Report andur website at

ting policies,

e 3)"

ting policies,

ting policies,

ting policies,

CR

(e) Theclas(EA As a

(Millio

Reta

R

Q

O

Who

A

A

B

C

C

O

F

F

Fo

G

In

In

In

M

P

R

O

Te

T

U

O

Tota

By G

C

U

E

O

Tota

By M

U

W

1

O

Tota1 Exc2 Off 3 Inclu4 Cou5 Inclu

Royal Ban

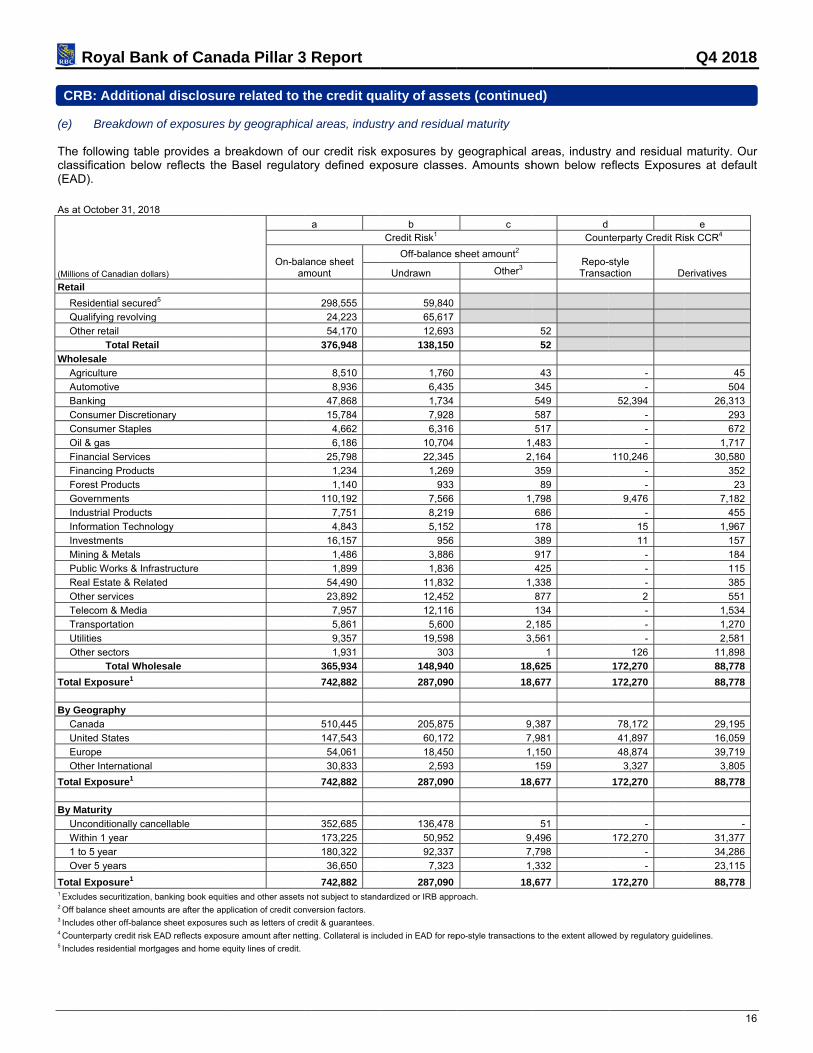

RB: Addition

Breakdown

e following tablssification beloAD).

at October 31, 201

ons of Canadian dol

ail

Residential secured

Qualifying revolving

Other retail Total Reta

olesale

Agriculture

Automotive

anking

Consumer Discretio

Consumer Staples

Oil & gas

inancial Services

inancing Products

orest Products

Governments

ndustrial Products

nformation Techno

nvestments

Mining & Metals

ublic Works & Infr

Real Estate & Rela

Other services

elecom & Media

ransportation

tilities

Other sectors

Total Who

al Exposure1

Geography

Canada

nited States

urope

Other International

al Exposure1

Maturity

nconditionally can

Within 1 year

to 5 year

Over 5 years

al Exposure1

cludes securitization,

balance sheet amou

udes other off-balan

unterparty credit risk

udes residential mor

nk of Cana

nal disclosur

n of exposures

e provides a bow reflects the

18

lars)

d5

g

ail

onary

s

ology

rastructure

ated

olesale

ncellable

banking book equiti

unts are after the app

ce sheet exposures

EAD reflects exposu

rtgages and home eq

ada Pillar 3

re related to t

by geographica

breakdown of oBasel regulato

On-balam

ies and other assets

plication of credit con

such as letters of cr

ure amount after net

quity lines of credit.

3 Report

the credit qu

al areas, indus

our credit risk ory defined ex

a

lance sheet mount

298,555

24,223

54,170

376,948

8,510

8,936

47,868

15,784

4,662

6,186

25,798

1,234

1,140

110,192

7,751

4,843

16,157

1,486

1,899

54,490

23,892

7,957

5,861

9,357

1,931

365,934

742,882

510,445

147,543

54,061

30,833

742,882

352,685

173,225

180,322

36,650

742,882

not subject to stand

nversion factors.

redit & guarantees.

tting. Collateral is inc

uality of asse

stry and residua

exposures by xposure classe

b

Credit Risk1

Off-balance s

Undrawn

59,840

65,617

12,693138,150

1,760

6,435

1,734

7,928

6,316

10,704

22,345

1,269

933

7,566

8,219

5,152

956

3,886

1,836

11,832

12,452

12,116

5,600

19,598

303148,940

287,090

205,875

60,172

18,450

2,593

287,090

136,478

50,952

92,337

7,323

287,090

dardized or IRB appr

cluded in EAD for rep

ets (continue

al maturity

geographical aes. Amounts sh

c

sheet amount2

Other3

1

2

1

1

2

3

18,

18,

9

7

1

18,

9

7

1

18,

roach.

po-style transactions

ed)

areas, industryhown below re

d

Coun

Repo-Transa

52

52

43

345

549

587

517

,483

,164

359

89

,798

686

178

389

917

425

,338

877

134

,185

,561

1

,625

,677

,387

,981

,150

159

,677

51

,496

,798

,332

,677

s to the extent allowe

y and residual eflects Exposu

terparty Credit Ri

-style action D

-

-

52,394

-

-

-

110,246

-

-

9,476

-

15

11

-

-

-

2

-

-

-

126

172,270

172,270

78,172

41,897

48,874

3,327

172,270

-

172,270

-

-

172,270

ed by regulatory guid

Q4 2018

16

maturity. Our res at default

e

sk CCR4

erivatives

45

504

26,313

293

672

1,717

30,580

352

23

7,182

455

1,967

157

184

115

385

551

1,534

1,270

2,581

11,898

88,778

88,778

29,195

16,059

39,719

3,805

88,778

-

31,377

34,286

23,115

88,778

delines.

CR

(f)

The As a

Impa(Millio

Can

R

W

STo

Unit

R

W

STo

Othe

R

W

STo

Tota

R

W

STota1 Geo2 Allo

Net (Millio

Can

R

W

Unit

R

W

Othe

R

W

Tota

R

W

Tota1 Geo2 Inclu

Royal Ban

RB: Addition

Amounts oallowances

e following table

at October 31, 201

aired exposures ons of Canadian dol

ada

Retail

Wholesale

ecurities

otal - Canada

ted States

Retail

Wholesale

ecurities

otal - United Stat

er International

Retail

Wholesale

ecurities

otal - Other Inter

al

Retail

Wholesale

ecurities

al impaired expos

ographic information

owance reflects only

write-offs by geo

ons of Canadian dol

ada

Retail

Wholesale

ted States2

Retail

Wholesale

er International

Retail

Wholesale

al

Retail

Wholesale

al net write-offs

ographic information

udes acquired credit

nk of Cana

nal disclosur

of impaired exs and write-offs,

es provide a br

18

by geography1 alars)

tes

rnational

sures

is based on residen

Stage 3 IFRS 9 allo

ography1 and po

lars)

is based on residen

t-impaired loans rela

ada Pillar 3

re related to t

xposures (acco, broken down

reakdown of im

and portfolio

nce of borrower.

wances.

rtfolio

nce of borrower.

ated to the acquisition

3 Report

the credit qu

ording to the by geographic

mpaired exposu

n of City National.

uality of asse

definition usecal areas and in

ures by geograp

Grosex

ets (continue

ed by the banndustry

phical areas an

ss impaired xposures

723

396

- 1,119

23

401

- 424

327

313

125

765

1,073

1,110

125

2,308

ed)

nk for account

nd industry.

Allowance2

For the ye

ting purposes)

2 Net ex

168

92

- 260

1

164

- 165

166

109

- 275

335

365

- 700

ear ended Octobe

Q4 2018

17

) and related

impaired posures

555

304

- 859

22

237

- 259

161

204

125

490

738

745

125

1,608

er 31, 2018

942

83

4

19

24

40

970

142

1,112

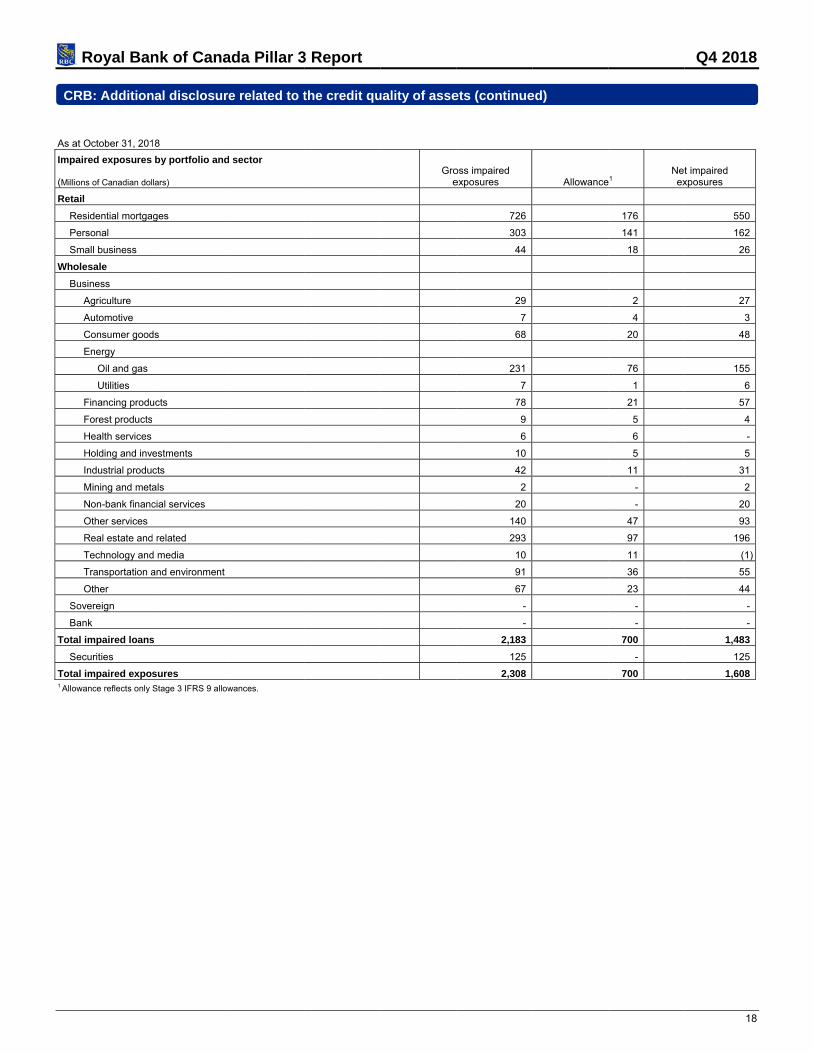

CR

As a

Impa (Millio

Reta

R

P

S

Who

B

S

B

Tota

S

Tota1 Allo

Royal Ban

RB: Addition

at October 31, 201

aired exposures

ons of Canadian dol

ail

Residential mortga

ersonal

mall business

olesale

usiness

Agriculture

Automotive

Consumer good

Energy

Oil and gas

Utilities

Financing produ

Forest products

Health services

Holding and inv

Industrial produ

Mining and meta

Non-bank financ

Other services

Real estate and

Technology and

Transportation a

Other

overeign

ank

al impaired loans

ecurities

al impaired expos

owance reflects only

nk of Cana

nal disclosur

18

by portfolio and

lars)

ages

ds

ucts

s

estments

cts

als

cial services

d related

d media

and environment

s

sures

Stage 3 IFRS 9 allow

ada Pillar 3

re related to t

d sector

wances.

3 Report

the credit quuality of asse

Groe

ets (continue

oss impaired exposures

726

303

44

29