arab petroleum investments corporation (“apicorp”) presentation - apicorp sukuk.pdf · neither...

TRANSCRIPT

October 2015

Arab Petroleum Investments Corporation

(“APICORP”)

Investor Presentation

2

Disclaimer

IMPORTANT: YOU ARE ADVISED TO READ THE FOLLOWING CAREFULLY BEFORE READING, ACCESSING OR MAKING ANY OTHER USE OF THE MATERIALS THAT FOLLOW.

The following applies to this document, the oral presentation of the information in this document by Arab Petroleum Investments Corporation (the “Company”) or any person on behalf of the Company, and

any question-and-answer session that follows the oral presentation (collectively, the “Information”). In accessing the Information, you agree to be bound by the following terms and conditions.

The Information has been prepared by and is the sole responsibility of the Company and has not been verified, approved or endorsed by any lead manager, bookrunner or underwriter retained by the

Company (the "Managers"). The Managers are acting exclusively for the Company and no one else, and will not be responsible for providing advice in connection with the Information to any other party.

Subject to applicable law, none of the Managers accepts any responsibility whatsoever and makes no representation or warranty, express or implied, for the contents of the Information, including its

accuracy, completeness or verification or for any other statement made or purported to be made in connection with the Company and nothing in this document or at this presentation shall be relied upon as

a promise or representation in this respect, whether as to the past or the future. The Managers accordingly disclaim all and any liability whatsoever, whether arising in tort, contract or otherwise (save as

referred above) which any of them might otherwise have in respect of the Information or any such statement.

The Information is an advertisement and does not constitute a prospectus for the purposes of the Prospectus Directive (as defined below). The Information does not constitute or form part or all of, and

should not be construed as, any offer of, or any invitation to sell or issue, or any solicitation of any offer to purchase, subscribe for, underwrite or otherwise acquire, or a recommendation regarding, any

securities of the Company, nor shall it or any part of it nor the fact of its presentation or distribution form the basis of, or be relied upon in connection with, any contract or any commitment whatsoever or any

investment decision. The Information is confidential and is being provided to you solely for your information and may not be reproduced, retransmitted or further distributed to any other person or published,

in whole or in part, for any purpose. If any such offer or invitation is made, it will be made through a separate and distinct documentation in the form of a prospectus, offering circular or other equivalent

document and any decision to purchase or subscribe for any securities pursuant to such offer or invitation should be made solely on the basis of such prospectus and not the Information.

The Information is only being distributed to and is only directed at: (A) persons in member states of the European Economic Area (other than the United Kingdom) who are “qualified investors” within the

meaning of Article 2(1)(e) of Directive 2003/71/EC (as amended and together with any applicable implementing measures in that member state, the “Prospectus Directive”) (“Qualified Investors”); (B) in

the United Kingdom, Qualified Investors who are investment professionals falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”) and/or

high net worth companies, and other persons to whom it may lawfully be communicated, falling within Article 49(2)(a) to (d) of the Order; and (C) such other persons as to whom the Information may be

lawfully distributed and directed under applicable laws (all such persons in (A) to (C) above together being referred to as “relevant persons”). Securities issued by the Company are only available to, and

any invitation, offer or agreement to purchase securities will be engaged in only with, relevant persons. Any person who is not a relevant person should not act or rely on the Information.

The Information contains data compilations, writings and information that are proprietary and protected under copyright and other intellectual laws and may not be redistributed or otherwise transmitted by

you to any other person for any purposes.

The Information should not be considered as a recommendation that any investor should subscribe for or purchase any securities. Any person who subsequently acquires securities must rely solely on the

final prospectus published by the Company in connection with such securities, on the basis of which alone purchases of or subscription for such securities should be made. In particular, investors should

pay special attention to any sections of the final prospectus describing any risk factors. Any such determination should involve, inter alia, an assessment of the legal, tax, accounting, regulatory, financial,

credit and other related aspects of the securities or such transaction.

The Information has not been independently verified and no responsibility is accepted, and no representation, undertaking or warranty is made or given, in either case, expressly or impliedly, by the

Company or any of its officers or advisers as to accuracy, reliability or completeness of the Information or as to the reasonableness of any assumptions on which any of the same is based or the use of any

of the same.

The Information is not intended for distribution or publication in the United States. Neither this document nor any part or copy of it may be distributed, directly or indirectly, in the United States. The

distribution of this document in certain jurisdictions may be restricted by law and persons in to whose possession this presentation comes should inform themselves about and observe any such restrictions.

By reviewing these materials, you represent and agree that you are located outside the United States and you are permitted under the laws of your jurisdiction to receive this presentation. This presentation

is not an offer to sell or a solicitation of any offer to buy the securities of the Company in the United States. The Company’s securities have not been and will not be registered under the Securities Act of

1933, as amended.

Nothing contained in the Information shall be deemed to be a forecast projection or estimate of the Company's future economic performance. The Information contains forward-looking statements. These

forward-looking statements can be identified by the use of forward-looking terminology, including the terms “believes”, “estimates”, “projects”, “expects”, “intends”, “may”, “will”, “seeks” or “should” or, in each

case, their negative or other variations or comparable terminology, or by discussions of strategy, plans, objectives, goals, future events or intentions. Forward-looking statements are statements that are not

historical facts and include statements about the Company’s beliefs and expectations. These statements are based on current plans, estimates and projections and, therefore, undue reliance should not be

placed on them. Forward-looking statements speak only as of the date they are made. Although the Company believes that the beliefs and expectations reflected in such forward-looking statements are

reasonable, no assurance can be given that such beliefs and expectations will be realised.

By accepting the Information, you will be deemed to acknowledge and agree to the matters set forth above. FCA/ICMA stabilisation applies.

3

Agenda

Section 1 4 OVERVIEW OF APICORP

Section 2 11 FINANCIAL POSITION AND PERFORMANCE

Section 3 14 ASSET PROFILE

Section 4 18 FUNDING OVERVIEW

Section 5 21 LIQUIDITY, CAPITAL ADEQUACY & RISK FRAMEWORK

Section 6 24 PEER GROUP ANALYSIS

Section 7 26 KEY CREDIT STRENGTHS

Section 8 28 STRUCTURE OVERVIEW

4

OVERVIEW OF APICORP

Section 1

5

APICORP - Introduction

Arab Petroleum Investments Corporation (APICORP) is a multilateral development bank established on

23 November 1975 under the terms of an agreement signed by the ten Member States of the Organization of Arab

Petroleum Exporting Countries (OAPEC)

APICORP’s mission is to contribute to the development and the

transformation of the Arab hydrocarbon and energy industries through equity

and debt financing, advisory and research.

Mission

Net Worth US$ 1.94 billion

Capital Adequacy Ratio 29.31%

Moody’s Rating Aa3

Key Highlights (as at 30 June 2015)

APICORP is wholly owned by member states of the OAPEC

Kuwait 17%

Saudi Arabia 17%

UAE 17%

Libya 15%

Iraq 10%

Qatar 10%

Algeria 5%

Egypt 3%

Bahrain 3%

Syria 3%

Algeria Libya Egypt

Saudi Arabia

UAE

Qatar

Bahrain

Kuwait

Iraq

Syria

6

APICORP’s Board of Directors

10 Directors representing each of the 10 member states. Board members represent their country’s interest in

APICORP

The Board elects its Chairman. Membership of the Board is for a term of four years and can be renewed for any

number of successive terms.

Algeria

Mr. Farid Baka Member, Audit & Compensation

Committee

Iraq

Nihad A. Moosa Engineer

Egypt

Sherin Ahmed Mohamed Engineer

Saudi Arabia

Dr. Aabed A. Al-Saadoun Chairman of the Board

Chairman of Remuneration &

Nomination Committee

Libya

Mr. Khaled Amr Al-Qunsul Deputy Chairman of the Board

Member of Remuneration &

Nomination Committee

Kuwait

Shaikh Talal Naser A. Al-Sabah Chairman of Audit & Risk Committee

Member of Remuneration &

Nomination Committee

Bahrain

Mr. Mahmood Hashim Al-

Kooheji Member of Remuneration &

Nomination Committee

Qatar

Mr. Mohamed Khalid Al-

Ghanem Member of Audit & Risk Committee

United Arab Emirates

Dr. Matar Al-Neyadi Deputy Chairman of Audit & Risk

Committee

Syria

H.E. Eng. Suleiman Al-Abbas

7

APICORP’s Governance and Organizational Structure

Organizational Structure

Board Remuneration

& Nomination

Committee

Board of Directors

Chief Executive &

General Manager

Board Audit & Risk

Committee

CE&GM Office

PA’s

Advisors

Corporate Business

Strategy & PMO

Deputy Chief

Executive & General

Manager

Corp

Communication

& CSR

Operations IT Administration

Human

Resources Finance

Investments Corporate

Finance

Treasury &

Capital

Markets

Internal Audit

Manager

Governance

Group

Legal

Risk

Management

Compliance

Energy

Research

Dr. Raed Al-Rayes

Deputy Chief Executive and General Manager

Mr. Bennie Burger

Head of Corporate Strategy & PMO, Acting Head of Investments

Mr. Nicolas Thévenot

Head of Corporate Finance

Mr. Hesham Farid

Head of Treasury & Capital Markets

Mr. Ayman Zeyada

Head of Financial Control

Mr. Ali Hassan Fadel

General Counsel & Board Secretary and Compliance Officer

Mr. Ajay Kumar Jha

Head of Risk Management

Mr. Mohammed Al-Mubarak

Head of Operations

Mr. Hamdi Said Bata

Head of Human Resources & Administration

Mr. Raed Sirhan

Head of Information Technology

8

Making Sound Progress Across All Core Business Lines

All three core business lines namely Investments, Corporate Finance and Treasury and Capital Markets recorded

significant growth in 2014.

Dividend income generated by direct equity investment portfolio reached

US$ 91 million, in 2014, 26% higher

than income generated in 2013

Share of Islamic finance assets grew to

29% of total loan portfolio in 2014 from

27% in 2013

Key Achievements of 2014 and 2015 YTD

Awarded Best Dual Syndicated Loan Deal of 2014 from Islamic Finance News for

APICORP’s active management of financial obligations, extending tenors, reducing

funding costs and diversifying investor base

APICORP’s direct equity investments portfolio

comprises of seven petrochemical companies, four oil

and gas field service companies, one LPG extraction

company, one engineering products manufacturer and

one petroleum products storage company in six Arab

countries.

Direct equity investments increased from US$866

million at end 2014 to US$944 million at June 30, 2015.

In 2014, APICORP was involved in the acquisition of

National Petroleum Services (NPS), which represents

one of the largest regional private equity transactions

of 2014.

APICORP also committed capital to the Powervest

Fund, the first Shariah compliant specialised

infrastructure fund to be established in Saudi Arabia,

and acquired a 15% shareholding in Saudi Mechanical

Industries (SMI), a Saudi Arabian engineering

company engaged in manufacturing products with a

focus on fluid flow and control equipment in 2015.

The Corporate Finance business arranges financing

through loans and credit for projects developed by

local, regional and international sponsors in the energy

and hydrocarbon sectors.

Total income generated by corporate finance activities

in 2014 amounted to US$59 million and US$ 29 million

for the six months ending 30 June 2015

Average loan balance at June 30, 2015 remained

stable at US$2.86 billion compared with US$2.94 billion

at end 2014, in line with its strategy to re-balance the

asset composition of the balance sheet.

APICORP concluded 15 transactions in 2014 totaling

over US$608 million ensuring active presence of the

corporation in both project and trade finance and

increased its support to key clients comprising top 10

energy commodity players worldwide. During H1 2015,

APICORP concluded 12 transactions totaling US$ 355

million.

The Treasury and Capital Markets business is to

ensure that APICORP is adequately funded, market

risks are proactively managed and the investment

portfolio provides enhanced earnings not correlated to

APICORP’s other two cyclical business lines.

Total income generated by treasury and

capital markets activities in 2014 amounted to

US$ 36.9 million and US$ 18 million for the six months

ending 30 June 2015

Total market value of investments in the

fixed income securities portfolio amounted to

US$1.12 billion at end June 2015 and continued to

remain focused on strong credits with an average

portfolio rating of ‘A’.

Treasury and capital market assets recorded at US$

1.9 billion at end June 2015.

As at 30 June 2015, APICORP had six fully drawn

bank term loans and one issue of debt securities

outstanding.

Investments Corporate Finance Treasury and Capital Markets

9

Rating Agency Review of APICORP

APICORP’s asset quality and capital adequacy remain strong, despite the drop in global oil prices.

APICORP’s shareholders have explicitly committed to support the institution on a “joint and several” basis.

“The Member States undertake, jointly and severally, to support the corporation, protect it and embrace its causes in every way

that ensures the protection of its rights and interests internationally and otherwise and undertake to facilitate all the activities

related to its objectives and to adopt all possible measures to that end.”

Strong Capital Adequacy

High Quality Asset Portfolio

Relatively Low Leverage

Benefits from de facto preferred creditor status

Strong ability of shareholders to support

Rated Aa3, Stable Outlook Since September 2012

Reconfirmed in September 2015

Provisional (P)Aa3 senior unsecured MTN rating on APICORP Sukuk Limited’s US$

3.0billion Trust Certificate Issuance Programme assigned in June 2015

10

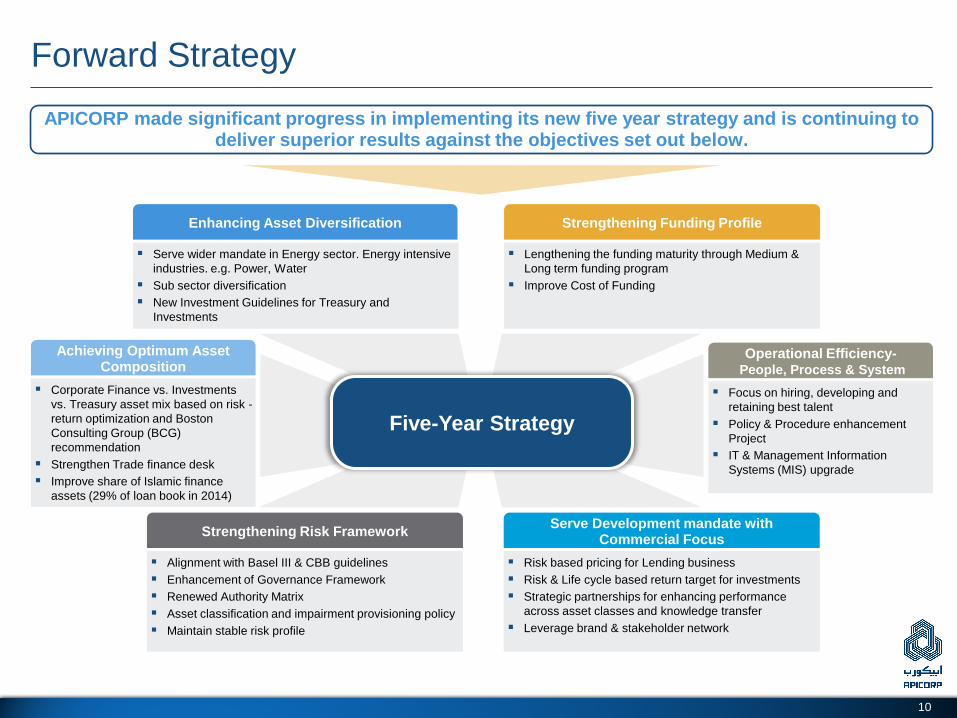

Forward Strategy

APICORP made significant progress in implementing its new five year strategy and is continuing to deliver superior results against the objectives set out below.

Focus on hiring, developing and

retaining best talent

Policy & Procedure enhancement

Project

IT & Management Information

Systems (MIS) upgrade

Operational Efficiency- People, Process & System

Risk based pricing for Lending business

Risk & Life cycle based return target for investments

Strategic partnerships for enhancing performance

across asset classes and knowledge transfer

Leverage brand & stakeholder network

Serve Development mandate with Commercial Focus

Alignment with Basel III & CBB guidelines

Enhancement of Governance Framework

Renewed Authority Matrix

Asset classification and impairment provisioning policy

Maintain stable risk profile

Strengthening Risk Framework

Corporate Finance vs. Investments

vs. Treasury asset mix based on risk -

return optimization and Boston

Consulting Group (BCG)

recommendation

Strengthen Trade finance desk

Improve share of Islamic finance

assets (29% of loan book in 2014)

Achieving Optimum Asset Composition

Enhancing Asset Diversification

Serve wider mandate in Energy sector. Energy intensive

industries. e.g. Power, Water

Sub sector diversification

New Investment Guidelines for Treasury and

Investments

Strengthening Funding Profile

Lengthening the funding maturity through Medium &

Long term funding program

Improve Cost of Funding

Five-Year Strategy

11

FINANCIAL POSITION AND

PERFORMANCE

Section 2

12

Increasing Profitability Amidst Growing Asset Base

Continuous growth in profits leading to a growing asset portfolio while maintaining low leverage

Increasing Profitability coupled with Stable Efficiency Ratio (Gross Income US$ mn, Efficiency Ratio: Operating Expenses/ Gross Income)

Profitable Institution with a Healthy Balance Sheet

APICORP continues to remain profitable despite challenging

economic environment with gross income rising 4% to US$ 156

million in 2014

Net income recorded at US$ 105 million as an investment provision

was built in 2014 on the back of uncertain geopolitical outlook for the

MENA region.

Similarly, APICORP’s total assets reached US$ 5.64 billion as on

June 30, 2015 vs. US$ 5.67 billion on 31 December 2013.

Total liabilities dropped to US$ 3.70 billion as on 30 June 2015 from

US$ 4.02 billion at end 2014, while equity reached US$ 1.93 billion on

June 30, 2015 from US$ 1.85 billion at end 2014

4,119 4,312 4,629

5,078 5,675 5,884 5,643

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2009 2010 2011 2012 2013 2014 30-Jun-15

3,117 3,171 3,411

3,768 3,868 4,025 3,707

1,002 1,141 1,219 1,309

1,807 1,859 1,936

0

1,000

2,000

3,000

4,000

5,000

2009 2010 2011 2012 2013 2014 30-Jun-15

Liabilities Equity

Total Assets (US$ mn) Total Liabilities and Equity (US$ mn)

82

119

159

131

150 156

81

58

95 105 109 112 105

56

27%

21% 23%

22%

26% 26%

24%

10%

15%

20%

25%

30%

35%

0

20

40

60

80

100

120

140

160

180

2009 2010 2011 2012 2013 2014 30-Jun-15

Gross Income Net Income Efficiency Ratio

13

Track Record of Strong Shareholders Support

In addition to the five capital increases, shareholders’ decision not to receive dividends for 6 years from 2008-2010

& 2012-2014 evidences strong shareholder support. Capital Adequacy Ratio of 29.3% at end June 2015 is

significantly higher than the Basel III requirement of 13%

Capital Adequacy Ratio (%)

25.7%

29.2%

28.4%

27.2%

28.7% 28.8% 29.3%

23%

24%

25%

26%

27%

28%

29%

30%

2009 2010 2011 2012 2013 2014 30-Jun-15

Shareholders’ Equity (US$ mn) Shareholders’ Deposits (US$ mn)

370

222

103 104 105 106 107

1,000

0

200

400

600

800

1,000

1,200

2009 2010 2011 2012 2013 2014 30-Jun-15 Approved Amount

1,002 1,141 1,219 1,309

1,807 1,859 1,936

0

500

1,000

1,500

2,000

2,500

2009 2010 2011 2012 2013 2014 30-Jun-15

Authorized

Capital

Subscribed

Capital

Issued and

Fully Paid

Callable

Capital

2,400 1,500 1,000 500

APICORP’s Capital Structure – 30 June 2015 (US$ mn)

14

ASSET PROFILE

Section 3

15

Distribution of Group’s Assets

Despite APICORP’s growing asset base, focus on GCC states and the petroleum industry is maintained

Asset Class Breakdown Focus on GCC Region and the Petroleum Industry Maintained

Majority of APICORP’s assets are in syndicated and direct loans

followed by available for sale securities and direct equity investments

at 46%, 20% and 17% respectively of total assets as of end June

2015

APICORP’s net cash position remained strong with total cash and

bank placements of US$ 769 million recorded at end June 2015

APICORP’s majority assets (82%) are based out of the GCC region,

with 35% of total assets based out of the Kingdom of Saudi Arabia

itself

Geographical Distribution of Assets – 30 June 2015 Industry Distribution of Assets – 30 June 2015

16% 10% 17% 14%

57% 52%

46% 47%

6% 15% 15% 17%

19% 21% 20% 20%

0%

20%

40%

60%

80%

100%

2012 2013 2014 30-Jun-15

Cash&Bank Placements Loans Equity AFS Securities PP&E Other Assets

35%

23%

24%

6%

4% 2%

2% 4% KSA (35%)

Qatar (23%)

Other GCC (24%)

Egypt and North Africa (6%)

Europe (4%)

Asia pacific (2%)

United States (2%)

Other North and South America (4%)

11%

11%

3%

2%

23%

1% 8%

9%

13%

4%

15%

Refineries

Oilfield production development services

Floating production, storage and offloading Facilities

Liquefied natural gas (LNG) plants

Petroleum and petrochemicals

Maritime transportation

Power generation

Other petroleum

Banks and financial institutions

Other industries

Governments and public sector

16

Focus on GCC States Across All Asset Classes

Represents 46% of total assets (H1 2015)

Directed towards large corporates and real

projects backed by strong sponsors and/ or

governments

Similar to total assets, majority loans are in

the GCC region with focus on the petroleum

sector

Investment Securities Loan Portfolio Direct Equity Investment

Represents 20% of total assets (H1 2015)

Average rating for the fixed income portfolio is

A, mainly comprised of fixed and floating rate

securities

GCC exposure is the maximum at 76%

followed by Europe at 17% and US at 7%

Total investment in direct equity reached US$

944 million as on 30 June 2015, representing

17% of total assets

Dividend income generated by the portfolio

reached US$ 91 million in 2014 equal to 58%

of APICORP’s total income in 2014. In H1

2015, dividend income reached US$ 49

million

Breakdown by Security Type (30 June 2015) Breakdown by Sector (30 June 2015) Breakdown by Security Type (30 June 2015)

18%

6%

22%

1% 22%

15%

16%

Oilfield production development services Floating production, storage and offloading Facilities Petroleum and petrochemicals

Maritime transportation

Refineries

Power generation

Other petroleum

69%

15%

1%

15% Fixed-rate bonds

Floating-rate bonds

Structured notes

Funds & Equities 90%

10%

Unlisted Equities

Listed Equities

Breakdown by Geography (30 June 2015) Breakdown by Geography (30 June 2015) Breakdown by Geography (30 June 2015)

40%

25%

23%

4% 4% 4% KSA

Qatar

Other GCC

Egypt and North Africa

Europe

Asia Pac.

20%

11%

45%

17%

7% KSA

Qatar

Other GCC

Europe

US

66%

10%

24% KSA

Egypt and N. Africa

UAE

17

APICORP’s Direct Equity Investments

Investment in Direct Equity Reached US$ 944 million as on June 30, 2015

Paid-up capital: LD 60 million

APICORP Share: 20%

Drilling and related operations in the Arab world.

Arab Drilling and Workover

Company (ADWOC), Libya

www.adwoc.com

Paid-up capital: TD 30 million

APICORP Share: 20%

Storage and handling of petroleum products at La Skhira terminal.

Paid-up capital: LD 35 million

APICORP Share: 16.67%

Providing seismic services for the oil and gas industry in the Arab world.

Paid-up capital: SR 1,025 million

APICORP Share: 10%

Production and marketing of MTBE and Poly Propylene (PP).

Arab Company for Detergent

Chemicals (ARADET), Iraq

www.aradetco.com

Tankage Mediterranee

(TANKMED), Tunisia

www.tankmed.com

Arab Geophysical Exploration

Services Company (AGESCO),

Libya

www.agesco-ly.com

Saudi European Petrochemical

Company (IBN ZAHR), Saudi

Arabia

www.sabic.com

Paid-up capital: SR 8,510 million

APICORP Share: 3.45%

Production and marketing of aromatics, PTA and polyester fibers.

The Arabian Industrial Fibers

Company (IBN RUSHD), Saudi

Arabia

www.sabic.com

Paid-up capital: SR 5,625 million

APICORP Share: 1.32%

Production and marketing of poly ethylene, ethylene glycol, poly propylene and other by-products.

Paid-up capital: US$ 215 million

APICORP Share: 17%

Production and marketing of methanol.

Paid-up capital: LE 1,992 million

APICORP Share: 3.03%

Production and marketing of ammonia and urea.

Alexandria Fiber Company

(AFCO), Egypt

www.adityabirla.com

Yanbu National Petrochemical

Company (YANSAB), Saudi

Arabia

www.yansab.com.sa

Egyptian Methanex Methanol

Company (EMethanex), Egypt**

www.methanex.com

Misr Oil Processing Company

(MOPCO)*, Egypt

www.mopco-eg.com

Paid-up capital: SR 2 billion

APICORP Share: 5.86%

Energy and related sectors (drilling, geophysical, oil field services, seamless pipe manufacturing, industrial gases etc.)

Paid-up capital: US$ 370 million

APICORP Share: 28.33%

Well services and intervention, wireline logging, testing, drilling and work-over activities.

The Egyptian Bahraini Gas

Derivative Company

(EBGDCO)**, Egypt

www.danagas.com

The Industrialization & Energy

Services Company (TAQA),

Saudi Arabia

www.taqa.com.sa

National Petroleum Services

(NPS)

www.npsintl.com

Paid-up capital: US$ 25 million

APICORP Share: 20%

Recovery and marketing of propane and butane.

Paid-up capital: ID 36 million

APICORP Share: 32%

Production and marketing of linear alkyl benzene (LAB) and byproducts.

Paid-up capital: US$ 48.3 million

APICORP Share: 10%

Production and marketing of acrylic fibers.

AS AT 30 June 2015

* Mopco 1 and 2 (expansion projects) works are progressing which were stopped for 28 months. Line 1 has commissioned in 2015 while Line 2 is planned to commission in Q4 2015

** The project is still not passing the commercial test/operations. (pre-test operations done on August 07, 2012).

Paid-up capital: SAR 250 million

APICORP Share: 15%

Provides manufacturing, distribution, installation and maintenance services to numerous sectors

Saudi Mechanical Industries

Company, Saudi Arabia

www.smi.com.sa

18

FUNDING OVERVIEW

Section 4

19

Access to Diverse Funding Sources

Amount Signing Date Tenor Status

US$ 300 million 1997 5 yrs Matured

US$ 200 million 2000 5 yrs Matured

US$ 300 million 2002 5 yrs Matured

US$ 250 million 2005 5 yrs Matured

US$ 400 million 2007 5 yrs Matured

SAR 2.5 billion (US$ 667 million) 2012 3 yrs Matured

SAR 500 million(US$ 133 million) 2012 5 yrs Outstanding

SAR 400 million(US$ 117 million) 2012 5 yrs Outstanding

US$ 105 million 2012 6 yrs Outstanding

SAR 1.0 billion (US$ 267 million) 2014 5 yrs Outstanding

US$ 150 million 2014 3 yrs Outstanding

SAR 3.0 billion (US$ 800 million) 2014 5 yrs Outstanding

Issue Type Amount Signing Date Tenor Status

Floating Rate Notes SAR 2billion (US$ 533million) 25-Oct-10 5 yrs callable 3 yrs Outstanding

APICORP’s Debt Capital Market Financing

Accessed different pools of funding including term loans, deposits, repo activities and debt capital markets, in

addition to strong shareholder support, and is successfully diversifying its funding sources.

APICORP’s Term Loan Financing – 30 June 2015

20

Maturity Profile for Assets and Liabilities

Maturity Profile of Assets and Liabilities – 2014

Loans and liabilities maturities overview

Given the nature of APICORP’s development mandate and business

focus, over 70% of its assets have a long maturity

APICORP’s unique access to term funding, low leverage and solid net

worth position is effectively reducing the maturity gaps. In 2014,

APICORP successfully raised a SAR 3.0 billion Club Murabaha term

facility, for the repayment of SAR 2.5 billion maturities due in

January, 2015 which reduced the maturity mismatch significantly

Moreover, short-term mismatch between maturities of assets and

liabilities has substantially reduced as majority deposits from banks are

routinely rolled over on maturity

Assets and Liabilities Maturities – 30 June 2015 (US$ mn)

2014 (US$ mn) Up to 3 months 3 months to 1 year 1 year to 5 years 5 years and above Total

Total Assets 812.5 924.2 2,108.5 2,038.7 5,884.0

Total Liabilities and Equity (1,970.9) (1,282.9) (755.9) (1,874.3) (5,884.0)

Maturity Gap (1,158.4) (358.7) 1,352.6 164.4 -

Cumulative Maturity Gap (1,158.4) (1,517.0) (164.4) - -

Maturity Profile of Assets and Liabilities – 30 June 2015

2015 (US$ mn) Up to 3 months 3 months to 1 year 1 year to 5 years 5 years and above Total

Total Assets 596.1 697.1 1,762.4 2,587.5 5,643.1

Total Liabilities and Equity (1,267.5) (899.7) (1,539.6) (1,936.3) (5,643.1)

Maturity Gap (671.4) (202.6) 222.8 651.2 -

Cumulative Maturity Gap (671.4) (873.9) (651.2) - -

596 697

1,762

2,588

1,267

900

1,540

1,936

0

500

1,000

1,500

2,000

2,500

3,000

Up to 3 months 3 months to 1 year 1 to 5 years 5 years and over

21

LIQUIDITY, CAPITAL ADEQUACY & RISK

FRAMEWORK

Section 5

22

Improving Capital Adequacy Amidst High Liquidity

Profile

(US$ million) 2012 2013 2014 30 June 2015

Placement with Islamic Financial Institutions 90 54 328 192

Placements with conventional financial institutions 429 437 561 493

Reverse purchase agreements 265 52 25 0

Margin call accounts on securities sold under agreement to repurchase 8 2 3 6

Total Placement with Banks 792 546 918 691

Cash 17 25 65 77

Total Liquidity 809 571 983 768

APICORP monitors its capital based on capital adequacy ratios prescribed by the Basel Committee (Basel II)

As at 30 June 2015, Capital adequacy ratio reached 29.3%, significantly higher than the Basel III requirement

of 13%

(US$ million, except percentages) 2012 2013 2014 30 June 2015

Risk Weighted Exposures

On balance sheet assets 3,859 4,751 5,147 5,135

Off balance sheet exposures 536 412 275 443

Total risk weight exposures 4,395 5,164 5,422 5,578

Capital Adequacy Ratio

Tier 1 Capital* 1,097 1,208 1,313 1,369

Tier 2 Capital** 98 274 251 266

Qualifying Capital 1,195 1,482 1,564 1,635

Total Capital Adequacy Ratio 27.2% 28.7% 28.8% 29.3%

* Comprise share capital, legal and general reserves and retained earnings

** Comprises investments fair value reserve and collective impairment allowance

June 2015 from APICORP’s internal sources

Liquidity

Capital Adequacy

23

Conservative Risk Management

The Board of Directors have overall responsibility for the establishment and oversight of APICORP’s risk management framework and have established a Board

Audit and Risk committee which is responsible for developing and monitoring APICORP’s risk management policies.

In addition, the Risk and ALCO Committee, which is a management committee, is responsible for developing and monitoring APICOR’s risk management policies to

maintain effective oversight of the key risks faced.

Risk Governance

Liquidity Risk Credit Risk Operational Risk

APICORP has established policies, procedures and

limits established to control, monitor and manage all

credit risks namely:

Credit Evaluation of obligors and counterparties;

Robust rating model;

Consultative approval procedure;

Transactional strength and risk based pricing

methodology; and

Concentration by country, product, industry sub-

sector and risk grade reviewed regularly to avoid

excessive exposure and ensure a broad

diversification.

APICORP’s liquidity management policies are:

Aiming towards aligning liquidity risk

management policies with Basel III standards

during 2015;

Line of credit from shareholders amounting to

US$ 1billion. Unutilised funding from this credit

line was US$ 894 million at end June 2015;

Maintaining adequate level of quality liquid

assets, well diversified funding sources and

liquidity mismatches monitored on a proactive

basis; and

Liquidity stress testing under scenarios covering

both normal and more severe market conditions.

APICORP has developed a framework and

methodology to identify and control APICORP’s

operational risks; including:

Internal audit function makes regular,

independent appraisals of the control

environment in all identified risk areas;

Incident management system developed to

report, assess and control operational risks

across the organisation; and

Adequately tested contingency arrangements

are in place to support operations in the event of

a possible disaster scenario.

Currency Risk Interest Rate Risk

APICORP’s funding is principally denominated in US Dollars and interest

rates are typically linked to U.S. dollar LIBOR

Exposure to interest rate fluctuations on certain financial assets and liabilities

are hedged by entering into interest rate swap agreements

Exposures in currencies other than US Dollars is hedged by entering into

forward contracts

Key Developments of 2014

Liquidity risk policy in line with Basel guidelines

developed for approval by Board

Established Asset Classification and impairment

provisioning policy Operational risk management practice developed

24

PEER GROUP ANALYSIS

Section 6

25

APICORP in Perspective

APICORP offers significant value versus similarly rated supranational peers. These include return on average

assets coupled with high liquidity levels

2013

Central

American Bank

for Economic

Integration

Corporacion

Andina de

Fomento

Arab

Petroleum

Investments

Corporation

Council of

Europe

Development

Bank

North America

Development

Bank

Caribbean

Development

Bank

Nordic

Investment

Bank

Islamic

Development

Bank

CABEI CAF APICORP CoE NADB CDB NIB IsDB

Issuer Rating A1 Aa3 Aa3 Aa1 Aa1 Aa1 Aaa Aaa

Weighted Median Shareholders Rating Ba1 Ba2 Aa3 – – Baa1 – –

Total Assets

(US$ million) 7,537 27,418 5,675 33,767 1,578 1,315 26,182 20,565

Return on Average Assets

(%) 1.57 0.79 2.00 0.5 0.5 0.20 0.9 1.4

Usable Equity / Gross Loans Outstanding +

Equity Operations*

(%)

42.0 42.9 46.9 19.3 51.7 71.8 – –

Gross NPLs / Gross Loans Outstanding **

(%) 0.6 0.0 2.3 0.0 0.7 0.5 0.2 1.0

ST Debt + CMLTD/ Liquid Assets***

(%) 63.8 69.3 10.0 49.3 0.0 44.1 67.0 47.9

Total Debt/ Discounted Callable Capital ****

(%) 546.8 1,910.2 360.9 488.6 40.9 87.1 329.7 121.7

Aaa Credits Aa3 Credits

Source: Moody’s Investor Service; Audited Financial Statements of the respective multilateral development bank

* Usable Equity is shareholder’s equity and excludes callable capital

** Non Performing Loans

*** Short term debt and current maturing long term debt

**** Callable capital pledge by members rated Baa3 or higher, discounted by Moody’s 30-year expected loss rates associated with ratings

26

KEY CREDIT STRENGTHS

Section 7

27

Key Credit Strengths

De facto Preferred Creditor

Status amidst Strong Ability

of Shareholders to Support

100% Sovereign Owned

Multilateral Development

Bank

Consistently Delivering

Superior Financial Results

Conservative leverage levels

with total liabilities divided

by total equity at 1.9 times

as at end June 2015

Highly Rated Institution with

Stable Outlook

High Grade Asset Portfolio

Coupled with Extremely Low

Leverage

Explicit Shareholder

Commitment on a “joint and

several” basis

Solid Capitalisation with

Capital Adequacy Ratio

determined in accordance

with Basel II methodology at

29.3% as at end June 2015

28

STRUCTURE OVERVIEW

Section 8

29

Structure Diagram

Special Purpose Vehicle

as Issuer and Trustee

APICORP

as Wakeel

APICORP

as Obligor /

Beneficiary

APICORP

as Purchaser

Investors

as Certificateholders

APICORP

as Seller Broker 1

Broker 2

Master Trust

Deed

Commodity

Purchase LOU

Commodity

Sale LOU

Master Murabaha

Agreement

Purchase / Sale

Undertaking Wakala Agreement

Master

Purchase

Agreement

8. Commodities

9. Cost Price (no

greater than 49%)

7. Commodities

Under Murabaha

Contract

10. Deferred

Payment

Price

14. Wakala

Assets

13. Exercise

Price

11. Principal

Revenues and

Income Revenues

5. Cost Price (no

greater than 49%)

6. Commodities 4. The Wakala

Assets

3. No less than

51% of Series

Issuance

1. Certificates 2. Series

Issuance

12. Periodic

Distribution

15. Dissolution

Amount

30

THANK YOU!