apicorp activities in 2012 2012 apicorp activities.pdfarab company for detergent chemicals (aradet)...

TRANSCRIPT

APICORP Activities in 2012

PROjECT AND TRADE FINANCE

Lending ActivityThe early signs of a slow recovery in project finance activity in the Gulf region during 2011 were confirmed in 2012, while in North Africa and the Levant, activity remained flat.

Overall, sponsors and developers continued to be cautious due to the prevailing economic and political environment with its lack of visibility. Furthermore, the closing of landmark transactions has taken much longer than in the past, due mainly to the large variety of financing sources that need to be mobilised. Consequently, most of the project finance transactions launched by sponsors in the first half of 2012 were still in progress at the year-end.

In contrast, trade and commodity finance activity remained steady, with APICORP taking advantage of favourable market conditions to confirm its position as a major regional player in this business line. Despite a persistently difficult environment, the Corporation was able to secure mandates for arranging both project finance, and structured trade and commodity finance; and played a pivotal role in some of the transactions that were concluded during the year (see opposite page). Significantly, despite the political turbulence in several countries where the Corporation is active, the performance of the loan portfolio remained excellent, with no delinquent loans being reported.

New ProductsThe year was also marked by the launch of new products. In the last quarter of 2012, APICORP started to offer a complete suite of trade finance products and services, including the issuance of letters of credit and SBLC/guarantees; and the handling of export letters of credit, including advising, negotiation and confirmation. Furthermore, in order to ensure the highest quality of service to its clients, the Corporation entered into a back office trade processing arrangement with JP Morgan. Following the launch of the APICORP Petroleum Shipping Fund, the Corporation introduced a new instrument in its range of asset-based financing products, namely residual value guarantees. The Corporation also broadened its range of structured trade finance products to include transactional financings, inventory financings, borrowing base facilities and prepayment facilities. These are in addition to arranging pre-export financings in which the Corporation has been involved for more than 10 years.

Financial AdvisoryThe year was marked by a scarcity of financial advisory opportunities due to the cautiousness of sponsors and developers. Accordingly, the Corporation was not able to secure financial advisory mandates in 2012, despite the close follow-up of several opportunities that failed to materialise.

Overall PerformanceIn 2012, the Corporation successfully maintained the growth of its loan portfolio that had resumed the previous year, following two years of stagnation. As at the end of 2012, net loan assets amounted to US$ 2.9 billion. Net income generated by project and trade finance activities reached an historical record of US$ 44.5 million, compared with US$ 30.75 million in 2011. To conclude, in an environment that remained very challenging, the Corporation confirmed its ability to increase profitability and preserve the high quality of its portfolio of loans, as well as offering new products to its clients.

APICORP Annual Report 201220

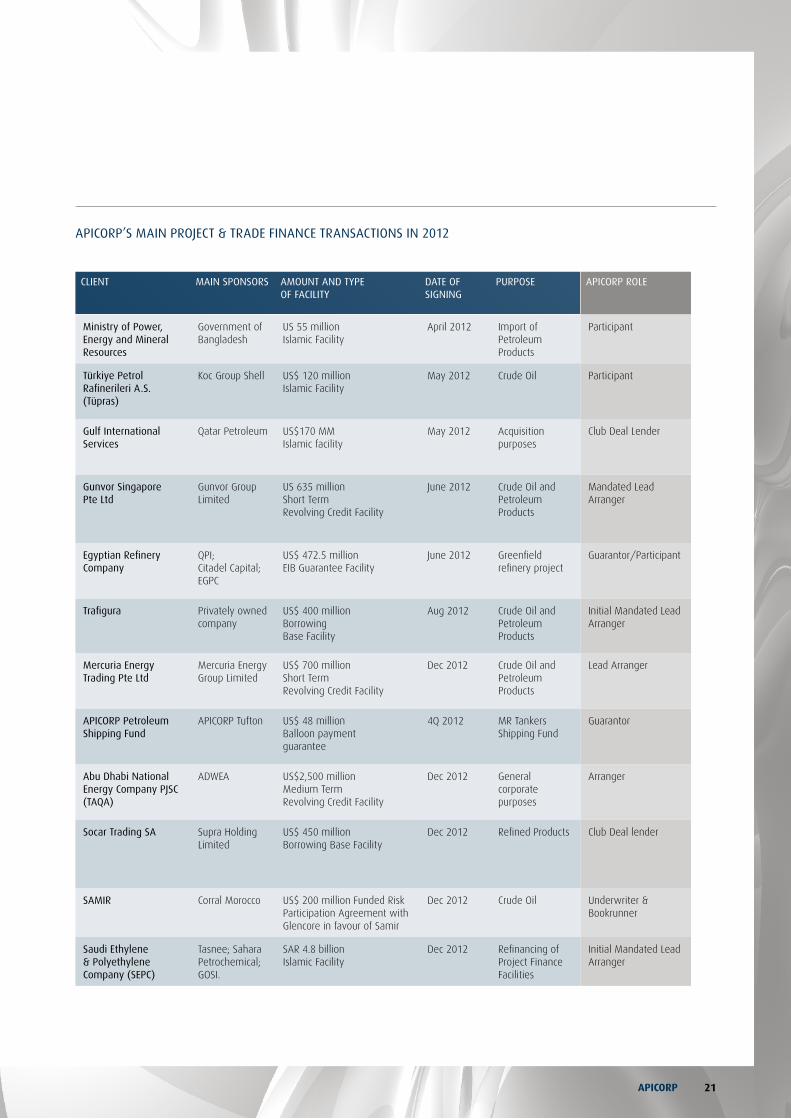

APICORP’S MAIN PROjECT & TRADE FINANCE TRANSACTIONS IN 2012

CLIENT MAIN SPONSORS AMOUNT AND TyPE OF FACILITy

DATE OF SIGNING

PURPOSE APICORP ROLE

Ministry of Power, Energy and Mineral Resources

Government of Bangladesh

US 55 million Islamic Facility

April 2012 Import of Petroleum Products

Participant

Türkiye Petrol Rafinerileri A.S. (Tüpras)

Koc Group Shell US$ 120 million Islamic Facility

May 2012 Crude Oil Participant

Gulf International Services

Qatar Petroleum US$170 MM Islamic facility

May 2012 Acquisition purposes

Club Deal Lender

Gunvor Singapore Pte Ltd

Gunvor Group Limited

US 635 million Short Term Revolving Credit Facility

June 2012 Crude Oil and Petroleum Products

Mandated Lead Arranger

Egyptian Refinery Company

QPI; Citadel Capital; EGPC

US$ 472.5 million EIB Guarantee Facility

June 2012 Greenfield refinery project

Guarantor/Participant

Trafigura Privately owned company

US$ 400 million Borrowing Base Facility

Aug 2012 Crude Oil and Petroleum Products

Initial Mandated Lead Arranger

Mercuria Energy Trading Pte Ltd

Mercuria Energy Group Limited

US$ 700 million Short Term Revolving Credit Facility

Dec 2012 Crude Oil and Petroleum Products

Lead Arranger

APICORP Petroleum Shipping Fund

APICORP Tufton US$ 48 million Balloon payment guarantee

4Q 2012 MR Tankers Shipping Fund

Guarantor

Abu Dhabi National Energy Company PjSC (TAQA)

ADWEA US$2,500 million Medium Term Revolving Credit Facility

Dec 2012 General corporate purposes

Arranger

Socar Trading SA Supra Holding Limited

US$ 450 million Borrowing Base Facility

Dec 2012 Refined Products Club Deal lender

SAMIR Corral Morocco US$ 200 million Funded Risk Participation Agreement with Glencore in favour of Samir

Dec 2012 Crude Oil Underwriter & Bookrunner

Saudi Ethylene & Polyethylene Company (SEPC)

Tasnee; Sahara Petrochemical; GOSI.

SAR 4.8 billion Islamic Facility

Dec 2012 Refinancing of Project Finance Facilities

Initial Mandated Lead Arranger

APICORP 21

At the end of 2012, APICORP’s total direct equity investments comprised seven petrochemical companies, three oil and gas services companies, and one gas products company in five Arab countries, with a total book value of US$ 318 million. Four petrochemical and one gas products company are located in Egypt; while Saudi Arabia hosts IBN ZAHR, IBN RUSHD, and YANSAB petrochemical companies. Two companies engaged in seismic services and oil drilling are located in Libya; while the remaining two companies

are based in Iraq and Tunisia. The range of the products provided by these companies consists of LPG, methanol, ethylene glycol, polyethylene, polypropylene, methyl tertiary butyl ether (MTBE), aromatics (BTX), linear alkyl benzene (LAB), nitrogen fertilizers (ammonia and urea), and synthetic fibers (poly acrylic).

1. ARAB DRILLING & WORKOVER COMPANy (ADWOC)APICORP share: 20%

ADWOC was established in 1978 to provide drilling and related operation services in Libya and nearby Arab markets. During 2012, the Company continued its efforts in restoring the majority of its drilling and maintenance fleet. By the end of December, 13 rigs were operational, and all company-owned rigs are expected to be operational by mid-2013. ADWOC recorded a net profit of LD 3.4 million in 2012 against a net loss of LD 14 million the previous year.

2. ARAB COMPANy FOR DETERGENT CHEMICALS (ARADET)APICORP share: 32%

ARADET was established in 1981 to produce 50,000 tons/yr each of linear alkyl benzene (LAB) and sodium tripoly phosphate (STPP). The LAB complex at Baiji was successfully constructed and commissioned in 1987; however, the STPP project has not materialised. The LAB complex includes an aromatics line with a capacity of 30,000 tons/yr of benzene and toluene. In 2012, ARADET’s revenues from the sale of LAB and other by-products amounted to US$ 81.9 million (out of which 70% were LAB revenues). The Company achieved a net profit of US$ 4.2 million compared to US$ 7.9 million during 2011.

3. TANKAGE MéDITERRANéE (TANKMED)APICORP share: 20%

TANKMED was established in 1984 to provide storage services for petroleum products at La Skhira terminal in Tunisia. Total storage capacity stands at 475,000 cubic metres, and the company is in the process of starting commercial operations of its expansion project III (to add another 60,000 cubic metres). In 2012, revenues were TD 22.7 million against TD 17.79 million in 2011. TANKMED posted a net profit of around TD 11 million compared with around TD 9 million the previous year.

DIRECT EQUITy INVESTMENTS

A brief summary of each of direct equity investment’s performance and profitability in 2012 is provided below:

APICORP Activities in 2012

APICORP Annual Report 201222

4. ARAB GEOPHySICAL EXPLORATION SERVICES COMPANy (AGESCO)APICORP share: 16.67%

AGESCO was established in 1985 to provide advanced seismic services in Libya and the Arab world. The Company’s seismic crew AG-03 resumed operations at the end of February 2012, while AG-02 resumed operations in May 2012. AGESCO recorded a net profit of LD 1.03 million in 2012 compared to net loss of LD 6.4 million in 2011.

5. THE SAUDI EUROPEAN PETROCHEMICAL COMPANy (IBN ZAHR)APICORP share: 10%

IBN ZAHR, established in 1985 in Jubail, has the capacity to produce 1.3 million tons/yr of methyl tertiary butyl ether (MTBE) – a gasoline octane booster, and 1.1 million tons/yr of polypropylene. During 2012, the Company produced 1.48 million tons of MTBE and 1.09 million tons of PP; and sold 1.48 million tons and 1.07 million tons, respectively. IBN ZAHR achieved a record net profit of US$ 850.5 million in 2012 compared to US$ 742.5 million the previous year.

6. THE ARABIAN INDUSTRIAL FIBERS COMPANy (IBN RUSHD)APICORP share: 3.45%

IBN RUSHD was established in 1993 at Yanbu, Saudi Arabia. Its integrated petrochemical complex comprises three plants for the production of aromatics (730,000 tons/yr), purified terephthalic acid (PTA - 350,000 tons/yr) and polyester (400,000 tons/yr). The Company’s expansion II project (to double PTA/PET production) is expected to be completed by the third quarter of 2013. As at end- December 2012, IBN RUSHD recorded a net loss of SR 556 million compared to SR 293 million in 2011.

7. ALEXANDRIA ACRyLIC FIBERS COMPANy (AFCO)APICORP share: 10%

AFCO was established in late 2003 in Egypt, to construct and own a poly acrylic fiber plant with a nameplate capacity of 18,000 tons/yr. Successfully commissioned in February 2006, the plant is currently in the process of being expanded to 54,000 tons/yr. Poly acrylic fibers are used mainly in the manufacture of carpets and blankets. During 2012, the Company produced and sold around 28 KMT of acrylic fibers. AFCO recorded net loss of US$ 9.64 million in 2012 compared to a marginal net profit of US$ 250,000 in 2011.

APICORP 23

8. yANBU NATIONAL PETROCHEMICAL COMPANy (yANSAB) APICORP share: 1.42%

YANSAB was established in early 2005 by SABIC with a paid up capital of SR 5,625 million. The Company is owned 55% by SABIC and 10% by SABIC’s partners in IBN RUSHD and TAIF, with the remaining shares being held by the general public. The complex is designed to produce 900,000 tons per year of low and high polyethylenes, 700,000 tons per year of ethylene glycols, 400,000 tons per year of polypropylene. YANSAB reported a net profit of SR 2.45 billion (around US$ 653 million) in 2012 compared to SR 3.17 billion the previous year.

9. EGyPTIAN METHANOL COMPANy (E-METHANEX) APICORP share: 7%

Methanex Corporation, Egyptian Petrochemicals Holding Company (ECHEM), Egyptian Natural Gas Holding Company (EGAS), Egyptian Natural Gas Company (GASCO) and APICORP established E-Methanex in 2006. The partners committed equity of US$ 215 million to build a US$ 1 billion methanol production facility in Damietta, Egypt, with a nameplate capacity of 1.26 million tons per year. In 2012, the company produced around 929 KMT of methanol and sold around 956 KMT. E-Methanex reported total revenues of US$ 280 million and net profits of US$ 44.1 million in 2012 compared to US$ 45.1 million during 2011.

10. MISR OIL PROCESSING COMPANy (MOPCO) APICORP share: 3.03%

In January 2009, MOPCO officially became the full owner of EAgrium, and its issued and paid up capital was doubled from LE 996 million to LE 1,992 million. As a result of this acquisition, APICORP’s share, which was previously 7% in EAgrium, was diluted to 3.03%. MOPCO successfully commissioned its first ammonia/urea plant (MOPCO 1) in Damietta with 400,000/635,000 t/pyr capacity in July 2008. After nearly 10 months of forced shutdown, MOPCO 1 resumed operations on August 25, 2012, and has since operated smoothly.

MOPCO’s expansion project (ex. EAgrium) consists of two identical and integrated plants (MOPCO 2&3), each with a capacity similar to MOPCO 1. Upon completion, the Company’s total capacity will increase to 1.2 million tons/yr and 1.9 million tons/yr of ammonia and urea, respectively. Expansion works at the site have been at a standstill since November 2011 due to some opposition from neighbouring communities, although the construction had reached 88% progress by then.

During 2012, the company produced 236 KMT of urea, with the majority being sold. MOPCO recorded a net profit of LE 238 million (c. US$ 38 million) compared to a net profit of LE 659 million in 2011.

APICORP Activities in 2012

APICORP Annual Report 201224

11. EGyPTIAN BAHRAINI GAS DERIVATIVES COMPANy (EBGDCO)APICORP share: 20%

The Egyptian Natural Gas Holding Company (EGAS), Danagas of Bahrain and APICORP established EBGDCO in early 2007 in Egypt with a share capital of US$ 25 million. Following construction of a US$ 125 million facility at Ras Shakair for propane and butane recovery from 150 million cfd of associated natural gas feed, EBGDCO commenced pre-commercial operations on August 7, 2012. The company recorded total revenues of US$ 8.1 million and net loss of US$ 9.1 million at the end of the year.

12. APICORP SHIPPING FUNDEstablished by APICORP in 2012, APSF is the Corporation’s first investment fund, and also the first of its kind in the region. Capitalised at US$ 150 million with a Shariah-compliant structure, the Fund targets the specific category of medium-range petroleum products vessels. Five tankers have been acquired for employment in the regional and international tanker market for five years, in order to help meet the projected upsurge in demand for petroleum product carriers. The Fund is co-managed by Tufton Oceanic, a leading global fund manager in the maritime and energy-related industries.

NB: In line with its new strategy, which encourages exit from some of its investment portfolio companies and the recycling of the resulting profits in new investment opportunities, APICORP sold its share (14%) in Oriental Petrochemicals Company (OPC) to Carbon Holdings on November 21, 2012.

APICORP 25

COMPANy NAMEPAID-UP CAPITAL

PARTICI-PATION

OTHER MAjOR SHAREHOLDERS ACTIVITIES

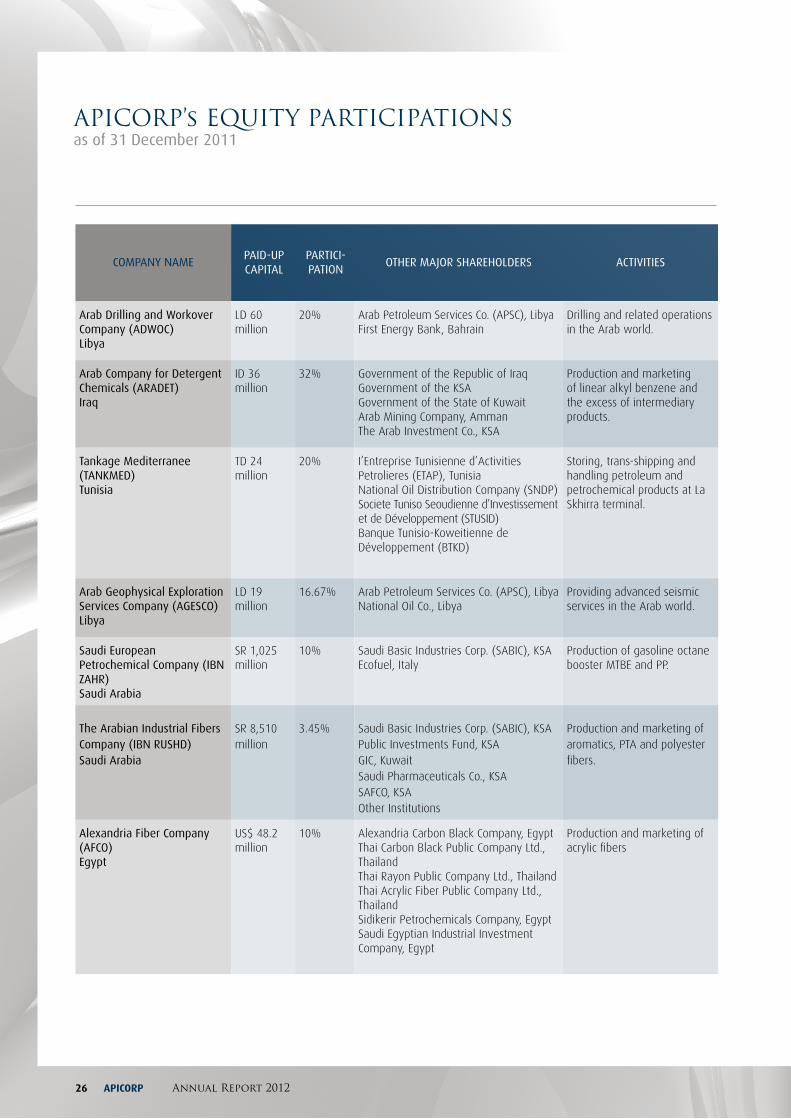

Arab Drilling and Workover Company (ADWOC)Libya

LD 60million

20% Arab Petroleum Services Co. (APSC), LibyaFirst Energy Bank, Bahrain

Drilling and related operations in the Arab world.

Arab Company for Detergent Chemicals (ARADET)Iraq

ID 36 million

32% Government of the Republic of IraqGovernment of the KSAGovernment of the State of KuwaitArab Mining Company, AmmanThe Arab Investment Co., KSA

Production and marketing of linear alkyl benzene and the excess of intermediary products.

Tankage Mediterranee (TANKMED)Tunisia

TD 24million

20% I’Entreprise Tunisienne d’Activities Petrolieres (ETAP), TunisiaNational Oil Distribution Company (SNDP)Societe Tuniso Seoudienne d’Investissement et de Développement (STUSID)Banque Tunisio-Koweitienne de Développement (BTKD)

Storing, trans-shipping and handling petroleum and petrochemical products at La Skhirra terminal.

Arab Geophysical Exploration Services Company (AGESCO)Libya

LD 19 million

16.67% Arab Petroleum Services Co. (APSC), LibyaNational Oil Co., Libya

Providing advanced seismic services in the Arab world.

Saudi European Petrochemical Company (IBN ZAHR)Saudi Arabia

SR 1,025 million

10% Saudi Basic Industries Corp. (SABIC), KSAEcofuel, Italy

Production of gasoline octane booster MTBE and PP.

The Arabian Industrial Fibers Company (IBN RUSHD)Saudi Arabia

SR 8,510 million

3.45% Saudi Basic Industries Corp. (SABIC), KSAPublic Investments Fund, KSAGIC, KuwaitSaudi Pharmaceuticals Co., KSASAFCO, KSAOther Institutions

Production and marketing of aromatics, PTA and polyester fibers.

Alexandria Fiber Company(AFCO)Egypt

US$ 48.2 million

10% Alexandria Carbon Black Company, EgyptThai Carbon Black Public Company Ltd., ThailandThai Rayon Public Company Ltd., ThailandThai Acrylic Fiber Public Company Ltd., ThailandSidikerir Petrochemicals Company, EgyptSaudi Egyptian Industrial Investment Company, Egypt

Production and marketing of acrylic fibers

APICORP’s EQUITY PARTICIPATIONSas of 31 December 2011

APICORP Annual Report 201226

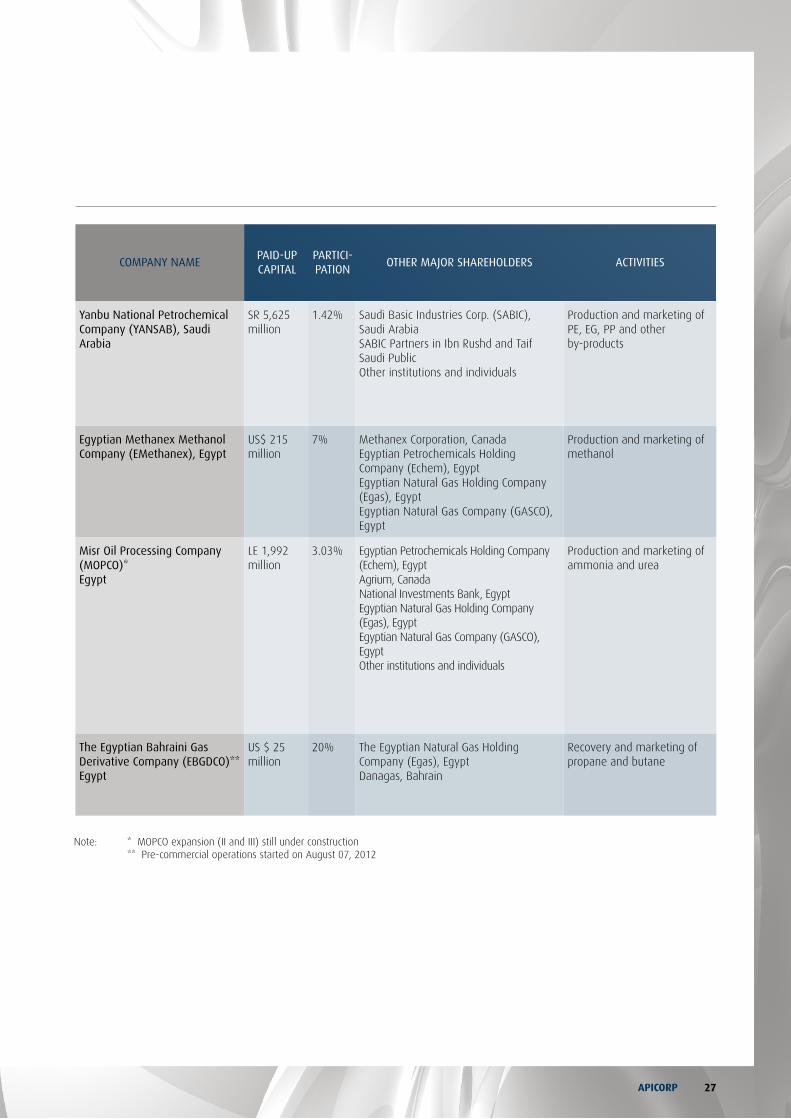

Note: * MOPCO expansion (II and III) still under construction ** Pre-commercial operations started on August 07, 2012

COMPANy NAMEPAID-UP CAPITAL

PARTICI-PATION

OTHER MAjOR SHAREHOLDERS ACTIVITIES

yanbu National Petrochemical Company (yANSAB), Saudi Arabia

SR 5,625 million

1.42% Saudi Basic Industries Corp. (SABIC), Saudi ArabiaSABIC Partners in Ibn Rushd and Taif Saudi PublicOther institutions and individuals

Production and marketing of PE, EG, PP and other by-products

Egyptian Methanex Methanol Company (EMethanex), Egypt

US$ 215million

7% Methanex Corporation, CanadaEgyptian Petrochemicals Holding Company (Echem), EgyptEgyptian Natural Gas Holding Company (Egas), EgyptEgyptian Natural Gas Company (GASCO), Egypt

Production and marketing of methanol

Misr Oil Processing Company (MOPCO)*Egypt

LE 1,992million

3.03% Egyptian Petrochemicals Holding Company (Echem), EgyptAgrium, CanadaNational Investments Bank, EgyptEgyptian Natural Gas Holding Company (Egas), EgyptEgyptian Natural Gas Company (GASCO), EgyptOther institutions and individuals

Production and marketing of ammonia and urea

The Egyptian Bahraini Gas Derivative Company (EBGDCO)**Egypt

US $ 25 million

20% The Egyptian Natural Gas Holding Company (Egas), EgyptDanagas, Bahrain

Recovery and marketing of propane and butane

APICORP 27

TREASURy & CAPITAL MARKETS

The year 2012 continued to be another challenging period for the global financial sector with a continuation of the unresolved issues of 2011. These include the Eurozone sovereign debt crisis; the US debt ceiling; fiscal austerity in developed world and its drag on global growth; the inability of developed markets to address high unemployment rates; the slow-down in emerging economies including China; and instability in the Middle East and Africa. Such issues caused frequent volatilities in the financial markets across the globe, and troubled the fragile global banking system.

APICORP’s strategy during 2012 was focused on prioritising liquidity management and minimising funding risks. In its endeavour to increase its medium-term funding, the Corporation concluded its first-ever Shariah-compliant SAR 2.5 billion (US$ 667 million) three-year syndicated Murabaha loan financing in January 2012, arranged by a number of leading Saudi banks. In addition, APICORP concluded two additional five-year Shariah-compilant Murabaha term loans amounting to SAR 940 million (US$ 250 million) during May and July 2012. A US$400 million term loan that matured in May 2012 was repaid. As at 31 December 2012, the Corporation’s medium-term borrowings, including outstanding bonds of SAR 2 billion (US$ 530 million) maturing in 2015, stood at US$ 1,437 million.

Treasury & Capital Markets assets continued to grow. As at 31 December 2012, total assets were US$ 1,709 million compared to US$ 1,456 million at the end of the previous year. APICORP’s liquidity, as measured by cash and placements, amounted to a comfortable US$ 756 million at the year-end against US$ 662 million as at 31 December 2011. Total market value of investments in the fixed income securities portfolio at the end of 2012 amounted to US$ 953 million compared with US$ 794 million as at 31 December 2011; and continues to be focused on strong credits, with an average portfolio rating of A+. During 2012, Treasury & Capital Markets achieved a higher gross income than the previous year. Total income increased to US$ 32.9 million against US$ 26.9 million for 2011.

The foreign branch of APICORP which started its operations as an investment bank in Bahrain during last quarter of 2006, continues to complement all the Treasury & Capital Markets activities of APICORP’s Head Office. The Corporation continues to place emphasis on further expanding and diversifying its funding base, which is vital for financing core activities and maintaining sufficient liquidity levels.

APICORP Activities in 2012

THE DEPARTMENT OF ECONOMICS & RESEARCH

The Economics & Research Department is dedicated to the study of economic and policy issues relevant to APICORP’s growth and diversification strategy. To address and discuss these issues, the Department continued to focus on three separate but interdependent areas in 2012:

1. The scanning of the Corporation’s business environment and trends in the context of the lagged global financial crisis, highlighting impacts on the money, credit and energy markets

2. The recalibration, in the wake of the so-called ‘Arab Spring’ and the turmoil it has created, of the key attributes of APICORP’s in-house “perceptual mapping” of the energy investment climate in the Arab (MENA) world

3. The extension of the review of the Arab (MENA) energy investment outlook to incorporate the full scope and scale of the power sector

APICORP has earned a widespread reputation for the quality of its economic research and policy analysis. The Corporation’s annual Review of Energy Investments in the Arab/MENA world has become a trusted source of analysis and insight in the field. Publication of the review, year after year, has made trend studies possible, thus offering a useful tool for policy analysis.At the same time, the timely and broad dissemination of APICORP’s research findings through its monthly Economic Commentary (see Box), has consistently added value to the region’s economic and energy policy debate. In addition, growing uptake of the Corporation’s research through numerous presentations of findings in international forums has helped shape and influence some of the key policy issues that are relevant to APICORP’s shareholders.

APICORP Annual Report 201228

2012 Issues of APICORP’s Economic CommentaryAll issues have been wrapped up in a single eBinder on www.apicorp-arabia.com/Research/Commentaries/EC_2012_Binder.pdf

• ‘APICORP’s Review of MENA Energy Investment: Sustained Outlook despite Lingering Uncertainty’, January 2012.

• ‘ IEA’s World Energy Outlook: Review and Discussion of MENA Deferred Investment Case’, February 2012.• ‘MENA Energy Investment in a Global Setting Assessment and Implications for Policy and Long-term Planning’,

March 2012.• ‘ MENA Power Reassessed: Growth Potential, Investment and Policy Challenges’, April-May 2012.• ‘Is the Anticipated Rise in Long-term Oil Price Inevitable?’, June 2012.• ‘Global Trends in Renewable Energy Investment: A Review of the Frankfurt School-UNEP’s Report and Discussion

of the MENA Case’, July 2012.• ‘Fiscal Break-even Prices Revisited: What More Could They Tell Us About OPEC Policy Intent?’, August –September

2012. • ‘MENA Energy Investment Outlook: Capturing the Full Scope and Scale of the Power Sector’, October 2012.• ‘Strait of Hormuz: Alternate Oil Routes Not Enough’, November 2012.• ‘MENA Natural Gas Endowment Is Likely To Be Much Greater Than Commonly Assumed’, December 2012.

CONFERENCES AND SEMINAR 2012

Effective Negotiations: Strategies and Tactics A training seminar for APICORP staff was held at the Corporation’s Head Office in Khobar, Saudi Arabia, on 21-22 February 2012. It was conducted by Professor Joseph Harbaugh, a legal expert and Ex-Dean of the School of Law at Northeastern State University, USA.

Energy Institute of Iraq Visit to APICORPIn response to an invitation by APICORP, a delegation from the Iraq Energy Institute visited the Corporation’s Bahrain Banking Branch on 4 March 2012. The purpose of the visit was to identify investment opportunities in the oil and energy projects that the Iraqi Government is planning to implement, and APICORP’s participation in such projects. The delegation gave a presentation on the future of the oil, gas and energy industries in Iraq.

The Arab Energy Club, DubaiAPICORP participated in this year’s Arab Energy Club sessions held in Dubai, UAE on 8 January 2012. The Club brainstormed on economic diversification in relation to the petroleum industry, with a focus on human capital development, local content creation, and the incentive structure needed to move away from rent-seeking to value-adding manufacturing.

Brookings Doha Energy ForumAPICORP participated in the winter meeting of the Arab Energy Club which was organised and hosted by the Brookings Doha Centre on 20-21 February 2012. The theme was ‘At the energy fault-line: what shifts in global economics and local politics mean for Middle East suppliers and their customers’.

The 13th International Energy Forum, KuwaitAPICORP participated in the 13th International Energy Forum, arranged by the State of Kuwait on 13-14 March 2012. As part of the work of the Energy Investment Committee, which was chaired by Prince Abdul-Aziz Bin Salam Bin Abdul-Aziz, Assistant Minister of Petroleum and National Resources, Kingdom of Saudi Arabia, APICORP presented a paper under the theme ‘Meeting Future Energy Demand: Planning and Investment for the Long-term’.

APICORP 29

CONFERENCES AND SEMINAR 2012 (continued)

Money and Ships – Finance and Investment in the International Shipping Market SeminarIn coordination with Tufton Oceanic (Middle East), APICORP arranged a seminar on ‘Money and Ships’ on 18-19 March 2012. This addressed the underlying context of the international shipping and oil services industry; and its different sectors and sub-sectors most relevant to the GCC region. In addition to the introduction to shipping and its historical context, the seminar also discussed the commercial/operational context of industry participants; legal and commercial structures typical in the industry; and sources of financing for the industry. The seminar also reviewed the shipping market outlook, and the overall investment opportunity in shipping; while providing specific transaction analysis based on debt and equity finance case studies.

KPMG Second Annual Energy ConferenceAPICORP participated in the KPMG Annual Energy Conference, held in Abu Dhabi, UAE on 16 October 2012 under the title ‘The Role of Energy Companies in Decision-Making in the Light of Uncertainty in the Region’.

GPCA Annual Forum Represented by a delegation led by the Chief Executive & General Manager, APICORP participated in the 7th Annual GPCA Forum organized by the Gulf Petrochemicals and Chemicals Association (GPCA), under the theme ‘Sustaining Competitiveness in a Rapidly Changing World’. The Forum took place in Dubai, UAE on 27-29 November 2012.

Abu Dhabi International Petroleum Exhibition & Conference (ADIPEC)APICORP participated in the 15th edition of the Abu Dhabi International Petroleum Exhibition and Conference (ADIPEC), which took place in Abu Dhabi, UAE on 11-14 November 2012, arranged by Abu Dhabi National Oil Company (ADNOC) and the Ministry of Energy in UAE. The theme for 2012 was ‘Meeting Increasing Oil and Gas Demand Through Innovation’.

APICORP Forum – The Transformation of the Global Energy SystemAt the Corporation’s head office in Khobar on 26 June 2012, APICORP held a Forum on the Shifts of the Global Energy System. It was presented by Professor Eicke R. Weber of the Frauhofer Institute for Solar Energy Systems ISE, Germany. The forum covered a number of aspects, including the future of the availability and sustainability of energy; the role of technology in the abundance of solar energy; the utilisation of other alternative energy systems; and the possibility of

energy storage. The Seminar was attended by a number of the Corporation’s senior employees.

Research and Economic Studies Volume # VIIAPICORP issued Volume VII of the Research and Economic Studies reports that contained the 12 monthly reports generated by the Corporation during the year.

The Oxford Energy ForumAPICORP participated in the Oxford Energy Policy Club as a member, where the following topics were discussed: • Oil Market Dynamics: is it the end of the supercycle?• Divergence in Global Gas Prices: what are the causes

and implications?• Iraq’s Energy Policy: how close is the country to

achieving its output targets?

Euromoney Annual Conference – Stability, Growth and jobsAPICORP attended, as an invited panellist, Euromoney’s Saudi Arabia Conference in Riyadh, on 22-23 May 2012. The Conference started with a keynote speech by Saudi policymakers (finance, economy and labour). Debated topics included the global economic and oil market issues; further reforms of the local capital market; housing policies and programmes; and how to address the employment gap among the younger generation of Saudis.

APICORP 2012 Symposium The APICORP 2012 Symposium is the first in a series of public events to be organised by the Corporation. The Symposium took place on 30 May 2012 in Manama, Bahrain, under the title ‘MENA Energy Investment in a Global Setting: Determinants and Policy Implications of Shifting Dynamics’. The event commenced with an opening speech by APICORP’s Chief Executive and General Manager, Mr. Ahmad Al-Nuaimi; and was moderated by Dr. Walid Khaddur, a Consultant at MEES. The main three topics of the Symposium started with an overview of oil demand/supply, shifting balances, and forecast on oil pricing, by Mr. Roberto Sieber, Chief Economist at Hess Corporation. The second topic was on the politics of oil, focusing primarily on the GCC, delivered by Mr. Bill-Farren Price, CEO at Petroleum Policy Intelligence. The third presentation, which was given by Mr. Ali Aissaoui, Senior Economic Consultant at APICORP, provided forecasts on energy investments in MENA for the coming five years, with the bulk of the presentation focused on the GCC.

APICORP Activities in 2012

APICORP Annual Report 201230