apresentação do powerpoint - aes brasil

TRANSCRIPT

Corporate Presentation2017

Corporate Presentation2017

1

AES CorporationA Global Company

1 – Includes hydro, wind, solar, energy storage, and biomass; 2 – PV – Photovoltaic; 3 – Operating and under construction.

AES Corp is present in 17 countries and 4 continents

Natural gas and coal fired thermal plants25 GW of installed capacity

Over 8 GW ofRenewable sources¹

Distributed energy+104 MW of solar PV² projects in operation

World leader in Energy StorageTotal of 476 MW³

35 GWinstalled capacity

19thousand

employees

Providing services to over

9 million customers

2

• Solid participation in distribution and generation businesses

History in Brazil

1 – AES Sul was sold to CPFL Energia in June/2016.

1998

Privatization of AES

Eletropauloby a

consortium comprised by AES Corp and

other local and

international companies

1999

Privatization of AES Tietê

2000

AES Uruguaianabeginning of

operation

20012002

AES Corp increases its

interest in AES Eletropaulo

and AES Tietê

2003

Incorporation of CompanhiaBrasiliana de Energia and execution of shareholders agreement with BNDES

AES Corp acquired AES Sul through privatization

process

19971

Beginning of AES

Uruguaiana’sconstruction

1995

2016

AES Tietêmerged into

Cia Brasiliana and was renamedAES Tietê

Energia S.A.AES Brasil

+20 years ofpresence in

Brazil

3

AES Brasil Mission, Vision and Values

VisionTo be recognized by our customers and shareholders as the preferred partner for safe, innovative, reliable and affordable energy solutions

Values– Put safety first– Act with integrity– Honor commitments– Strive for excellence– Have fun through work

MissionTo promote the well being and development by providing secure, sustainable and reliable energy solutions

4

• Reservoirs repopulation

• Reforesting, borders and archeologicalmanagement programs

• Water quality monitoring

• Recycling and waste disposal programs

• Programs aiming to reduce CO2 emissions

• Risk Management and identification of opportunities related to climate change

AES Brasil Environmental Responsibility

5

AES Brasil Social Responsibility

• Access to reliable energy through social development

• Recycling incentive program as a means to pay the electricity bill - mitigation of delinquency

• Education for efficient and safe use of electricity

• Sustainable partnership – commitment with sustainable development at AES Brasil’s value chain

• AES Brasil Institute – Created in 2016 to promote social innovation and income generation initiatives impacting communities and people’s life based on four pillars: (i) shaping citizens, (ii) innovation for social development, (iii) entrepreneurship and (iv) volunteering.

6

AES Brasil Recognitions

AES Brasil AES Tietê

7

National Interconnected System

GENERATION

ThermalPlant

Hydroelectric and Solar Plant

Substation Transformer

TRANSMISSION

Substation Transformer

Distribution Substation

DISTRIBUTION

RESIDENTIAL CUSTOMERS

COMMERCIAL AND INDUSTRIAL CUSTOMERS

Renewable Energy

8

Energy Sector in Brazil: Business Segments

Sources: EPE, ANEEL, ONS, ABRADEE and Instituto Ascende Brasil.1 – Refers to May/2017 data; 2 – Refers to 2016 data; 3 – Includes HPP (hydro power plants) and SHP (small hydro plants).

• 4,660 power plants

• 160 GW of installed capacity

• System based on hydro plants (12643)

• Contracting environment: free and

regulated markets

Distribution²

• 63 distribution companies

• 327 TWh distributed energy

• 81 million consumer units

• Annual tariff adjustment

• Tariff reset every four or five years

• Regulated contracting environment

• 77 agents

• High voltage transmission (>230 kV)

• +100,000 km of lines (National

Integrated System)

• Regulated tariff (annually adjusted by

inflation)

Transmission²Generation¹

9

Ownership Structure

24.3% 28.3% 47.4% US$ 1.6 bi

Others1 Market Cap2

C = Common ShareP = Preferred ShareT = Total

C 50.00% + 1 shareP 0.00%T 46.15%

C 50.00% - 1 shareP 100.00%T 53.85%

C 100.00%T 100.00%

C 100.00%T 100.00%

AES Holdings Brasil

BrasilianaParticipações

AES Uruguaiana

C 99.42%T 99.42%

AES Elpa

C 50.52%P 0.00%T 16.84%

C 14.38%P 37.40%T 28.33%

C 61.57%P 0.04%T 24.28%

AES Tietê Energia

BNDESPar

AES Eletropaulo

C 22.56%P 16.82%T 18.73%

AES Ergos

1 – Includes 7.9% of Eletrobras shares; 2 – Base Date: 06/22/2017 (FX rate 3.3362 BRL/1 USD).

10

Corporate GovernanceKey for Investment Decisions

Operational and Investment Management Committee: robust capital allocation process

Corporate policy of Integrated Risk Management assessed monthly by the Companies’ Executive Officers and quarterly by the Fiscal Council and Board of Directors

Listed in B3:- TIET11 (units): Level II of Corporate Governance

ISE: Corporate Sustainability Index- Tag along rights

High level of commitment with monthly Board of Directors meetings

111 – Base: 06/22/2017. FX rate 3.3362 BRL/1 USD; 2 – SHPP – Small hydroelectric plant (installed capacity < 30MW); 3 – Amount of energy allowed to be contracted in the long term.

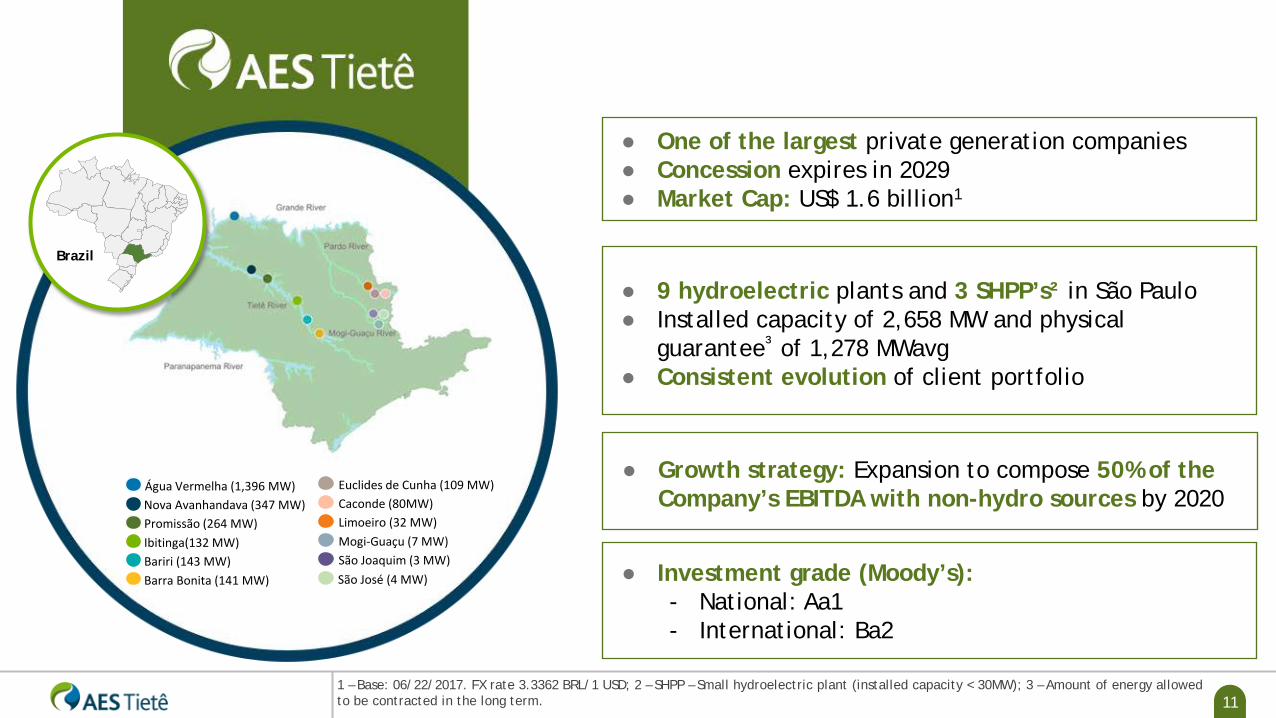

● One of the largest private generation companies● Concession expires in 2029● Market Cap: US$ 1.6 billion1

● 9 hydroelectric plants and 3 SHPP’s² in São Paulo● Installed capacity of 2,658 MW and physical

guarantee³ of 1,278 MWavg● Consistent evolution of client portfolio

● Investment grade (Moody’s):- National: Aa1- International: Ba2

Brazil

Água Vermelha (1,396 MW)Nova Avanhandava (347 MW)Promissão (264 MW)

Bariri (143 MW)Barra Bonita (141 MW)

Ibitinga(132 MW)

Euclides de Cunha (109 MW)Caconde (80MW)Limoeiro (32 MW)Mogi-Guaçu (7 MW)São Joaquim (3 MW)São José (4 MW)

● Growth strategy: Expansion to compose 50% of the Company’s EBITDA with non-hydro sources by 2020

12

Power plants modernization process, aiming for continuous improvement inoperational conditions and ensuring availability in its generation plants

Investment focused on power plants modernization

186 168

101 114

81

47

69 89

ActualExpected1

2014 2015 2018(e) 2019(e)2016 2020(e)2017(e) 2021(e)

Investment Program (in R$ million)

1 – Nominal terms.

13

Lower generated energy reflects ONS’ lower dispatch

1 – National System Operator; 2 – Generated energy divided by the amount of hours.

● Hydropower plants are dispatched by ONS1

● Dispatch is also related to hydrological conditions: − Low hydrology translates into low

generation levels

905848

1Q17

1,445

1,6751,492

1Q16

Generation - MWavgGeneration / Physical Guarantee

2014 20162015

117%

71%67%

117%

147%

Generated Energy (Mwavg²)

14

Level of reservoirs below the long term average

1 – Base date: Jan – May / 2017.

Historical Data since 2001

87%81% 89% 71%SIN’s Average

Annual Inflow:

20162014 2015 20171

2014 2015 2016 2017

0

2

4

6

8

10

12

14

16

18

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Q1 Q22Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2011 2012 2013 2014 2015 2016 2017

Thermal Dispatch Reservoirs

Reservoirs (%) vs. Thermal Dispatch (GWavg)Historical Level of Brazilian Reservoirs (%)

4339 40 43 42 43 40

3429 23

20 2221 2330

35 37 3841

3632 29 28 29

4250

57 56 55 53 4944

3834 31 32

35 3839 40 42

0102030405060708090

100

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

15

Out of order dispatch continues elevated

1 – Source: ONS (PEN 2016).

R$/MWh(Spot Price SE/MW

Thermal Dispatch out of the Order of Merit Thermal Dispatch in the Order of Merit + Inflexibility Total Thermal Dispatch Spot Price – SE/MW

411371

12116614783763836203227240

387388

805729593

807823

378216

388

GWavg¹

Increase in Thermal Dispatch out of Order of Merit

13

16 16 15

16 15 15

16 16 17 17 17 17 17 17 16 15

16 14 15

16 14

15 14 13

12 10

12 10 11 10

12 13 13 12

10 10 9 11

12 12

-

2

4

6

8

10

12

14

16

18

20

jan/14 mar/14 may/14 jul/14 sep/14 nov/14 jan/15 mar/15 may/15 jul/15 sep/15 nov/15 jan/16 mar/16 may/16 jul/16 sep/16 nov/16 jan/17 mar/17 may/17

16

Energy Reallocation Mechanism (ERM) for hydrological risk sharing

1– GE: Generated Energy; 2 – PG: Physical Guarantee; 3 – Enough to cover variable O&M costs.

Key drivers for hydrological risk● Generated Energy

(hydro) in the entire system (ERM) -influenced by hydrology

● Spot Price - marginal cost influenced by hydrology and thermal dispatch

AssuredEnergy

MREGenerated Energy

PG2

Genco A

1) Equilibrium (GE1 = PG2)

Buy at MRE3

PG2

Genco A

2A) Deficit (GE1 < PG2)

Buy at MRE3 Buy at Spot

PG2

Genco B

2B) Surplus (GE1 > PG2)

Sell at MRE3

Buy at Spot

AssuredEnergy

MREGenerated Energy

AssuredEnergy

MREGenerated Energy

- System GSF = 1.0- PPA = PG

- System GSF < 1.0- PPA = PG

- System GSF < 1.0- PPA = PG

● A physical guarantee (assured energy) is assigned to support contracts

● Energy dispatch optimized by centralized system operator (ONS) on a tight pool

17

Growth Perspectives

1 – Close to Água Vermelha HPP, an existing AES Tietê hydro power plant on the border of the states of Minas Gerais and São Paulo; 2 Business model considers the payment of the plant using the economy from the distribution consumption; 3 – According to ANEEL.

Natural Gas Power Plants & Cogen~1.5GW of dispatchable source

● 2 natural gas combined cycle power plants ready to go to energy auctions

● Cogeneration: distributed generation based on natural gas solutions

● Assessing M&A opportunities

Renewable EnergySolar and Wind

● 150 MW solar projects in São Paulo¹.

● Assessing M&A opportunities

● Distributed generation²: AES owns globally 104 MW and Brazil’s potential is 4.5 GW up to 2024³

Energy Storage

● AES Corp is the world leader in battery-based energy storage (patented system): Operations in 7 Countries (+476 MW capacity; + 10 years experience)

● Medium and large size systems: utilities and behind the meter (industrial and commercial)

18

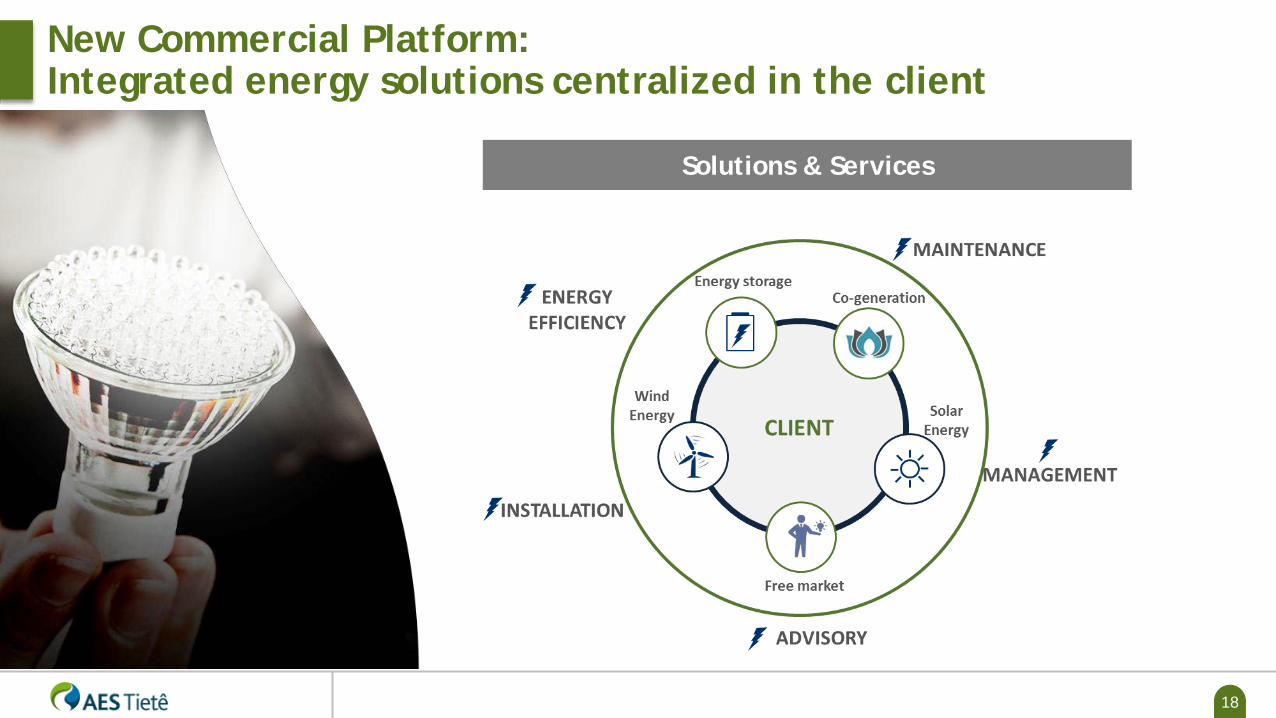

New Commercial Platform: Integrated energy solutions centralized in the client

Solutions & Services

19

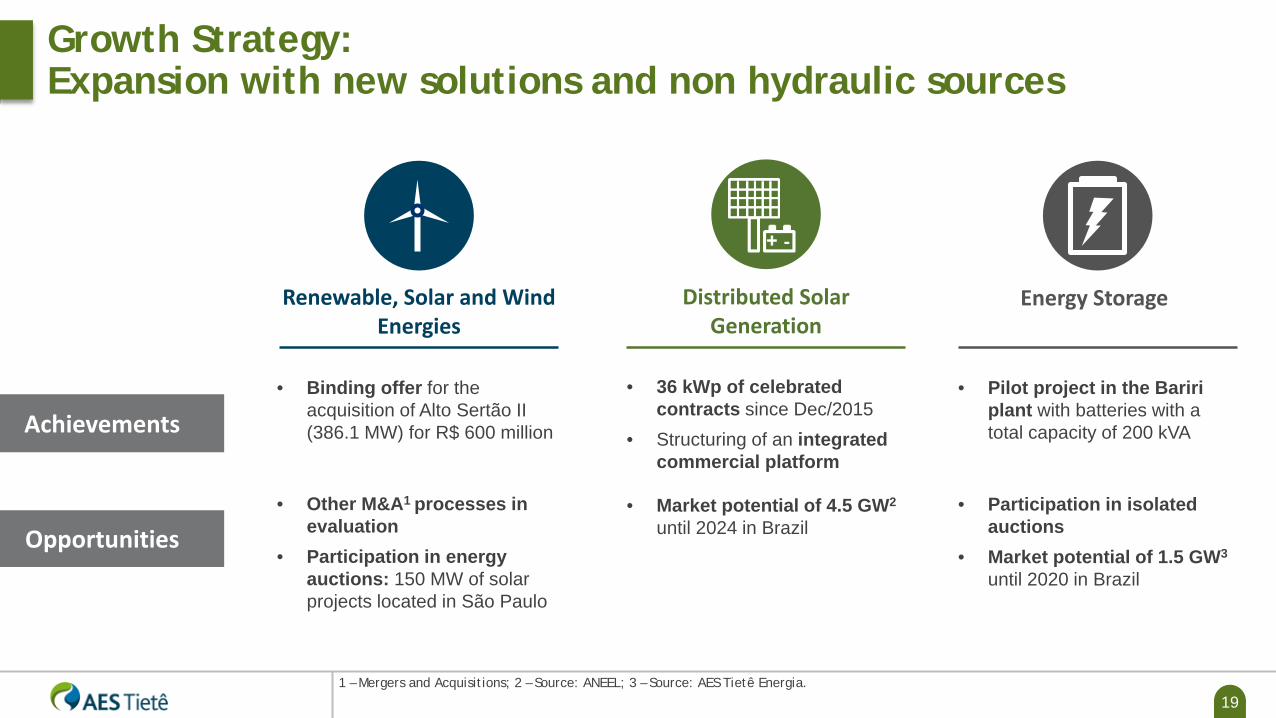

• Binding offer for the acquisition of Alto Sertão II (386.1 MW) for R$ 600 million

Distributed Solar Generation

• 36 kWp of celebrated contracts since Dec/2015

• Structuring of an integrated commercial platform

• Pilot project in the Baririplant with batteries with a total capacity of 200 kVA

Renewable, Solar and Wind Energies

Energy Storage

Achievements

Opportunities• Other M&A1 processes in

evaluation• Participation in energy

auctions: 150 MW of solar projects located in São Paulo

• Market potential of 4.5 GW2

until 2024 in Brazil• Participation in isolated

auctions• Market potential of 1.5 GW3

until 2020 in Brazil

Growth Strategy:Expansion with new solutions and non hydraulic sources

1 – Mergers and Acquisitions; 2 – Source: ANEEL; 3 – Source: AES Tietê Energia.

20

Acquisition:Purchase of Alto Sertão II Wind Park

Location: Caetité, Bahia

Installed Capacity: 386.1 MW

PPA’s: LER¹ 2010 (valid until 2033) / LEN² 2011 (valid until 2035)

Acquisition Price: R$ 600 million

Up to R$ 100 million as earn-out³

Assumption of R$ 1,150 million in debts

Pending Items: Creditor Approval

Alto Sertão II Wind Park

1 – Reserve Energy Auction; 2 – New Energy Auction; 3 – Addition of up to R$ 100 million as earn out depending on the park’s performance in comparison with a minimum reference.

21

Increase in Net Revenue reflects secondary energy verified in the quarter and higher average price of contracts

1 – Energy Reallocation Mechanism; 2 – Includes the selling to AES Eletropaulo at A-1 Auction.

Spot/CCEE Operations/OthersERM¹Regulated and Free Market

19

4012

+5%

1Q17

403

4

360

1Q16

383

352

302402418

940

2014

3,740

15,075

15,670

11,108

11,413

2015

14,485

2016

2,437

3,854

227

11,108

4,062

2,771

1,098

3,357

193

1Q16

2,638

-17%

1Q17

Regulated and Free Market² ERM1 Spot/CCEE Operations/Others

Billed Energy (GWh)Net Revenue (R$ million)

22

Contracting environment and opportunities

1 – Free Consumers (Conventional free consumer - demand above 3MW and connected to a line of 69kV – and incentivized/ special free consumer - demand above 0.5MW).

2016and

beyond

Regulated Market Free Market Spot Market

Existing Energy Auctions

Distribution companies

Via auctions organized by federal government

Via bilateral agreements

Bilateral contracts

Free Consumers¹

Non contracted energy

CCEE Settlement

Exposed to Spot Market price

23

Free MarketDynamic and competitive market

Long Term Marginal Expansion CostRegulated Market price

Medium Term Supply and demand

Short term Spot price (hydrology and reservoirs)

Price Formation Methodology

24

Termination of electric energy agreement in 2017 and 2018 in order to mitigate the hydrological risk

1 – Conventional energy only excluding losses and internal consumption; including energy purchase agreements to mitigate the hydrological risks; energy sale agreements firmed on Mar/17; excludes the physical guarantee of the Limoeiro power plant (incentivized energy);2 – Actual values as of March 2017.

157 161 160 151 145Average price2

(R$/MWh)

911598

443

219287

600755

164

1,034

20212020201920182017

1,056

2016

1,178

66

Energy available for sale Own energy already sold

95% 83% 76% 50% 37%Contracting Level

129

14%

Client Portfolio¹ (MWavg)

25

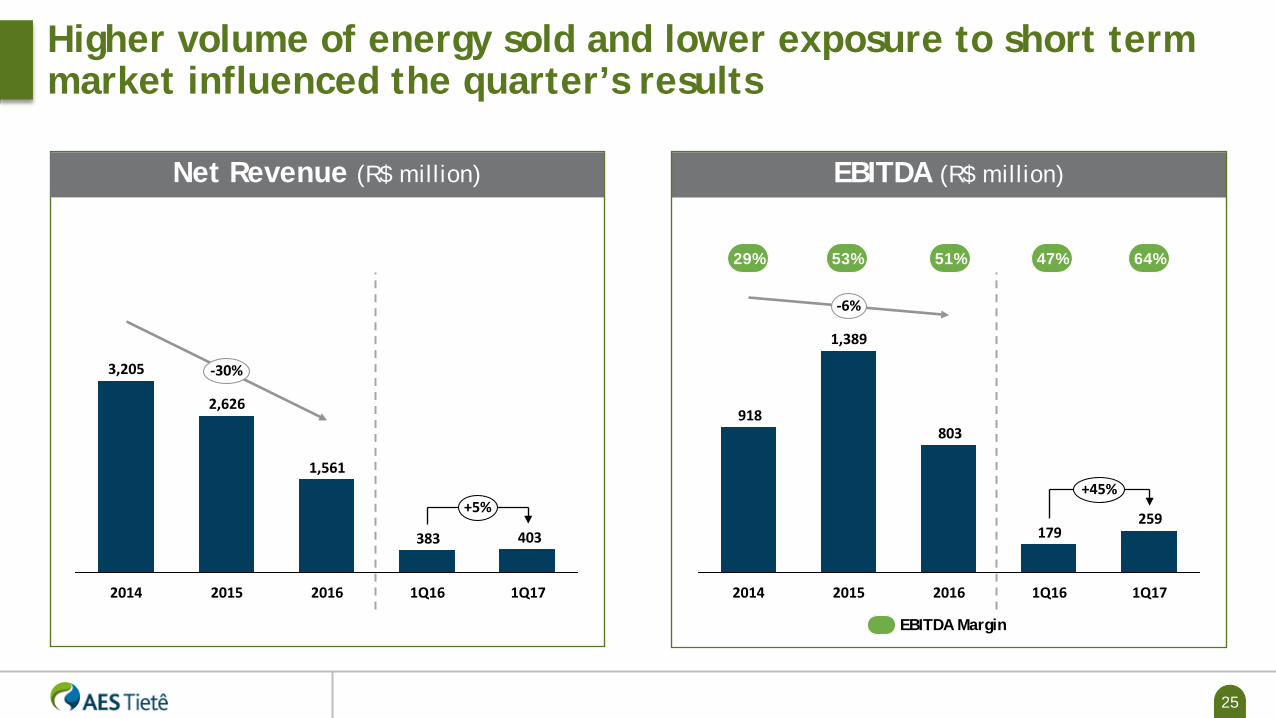

Higher volume of energy sold and lower exposure to short term market influenced the quarter’s results

EBITDA Margin

29% 53% 51%

403383

-30%

+5%

1Q171Q162016

1,561

2015

2,626

2014

3,205

259179

803918

1,389

2015 1Q16

+45%

-6%

1Q1720162014

47% 64%

EBITDA (R$ million)Net Revenue (R$ million)

26

And returns…

Minimum of 25% dividend payout of annual net income

according to bylaws

Distribution practice: quarterly basis

Average payout from 2008 to 2017¹: 108%

Average dividends since 2008: R$ 753 million/year

Management proposed the payment of R$ 133.3 million

in dividends for 1Q17

- Dividend yield of 2.3% and payout of 105.8%

12674

359

739

449

-11%

1Q172015 20162014 1Q16

+69%

Net Income (R$ million) & Dividend Distribution¹

1 – Does not consider Interest on Shareholders’ Equity; 2 – Until 1Q17.

27

Low leverage level…

1 – Adjusted to debt service; 2 – Flow comprised of principal amortization, accrued interests and balance of deferred amounts, as per "Explanatory Note 13" of the Company's Quarterly Financial Information. For 2018 considers debt classified as current liabilities.

Debt Amortization Schedule2Net Debt (R$ million)

743688

1Q17

0.8

1Q16

0.6

Net DebtNet Debt / Adjusted EBITDA¹

179

422

261

334

278

2021-20232019 202020182017

Amortization (R$ million)

Covenants• Net Debt / Adjusted EBITDA < 3.50x• Adjusted EBITDA / Financial Expenses > 1.75x

Debt Cost 1Q16 1Q17• Average cost (% CDI) 107% 114%• Average term (years) 2.7 2.5• Effective rate 14.9% 12.0%

28

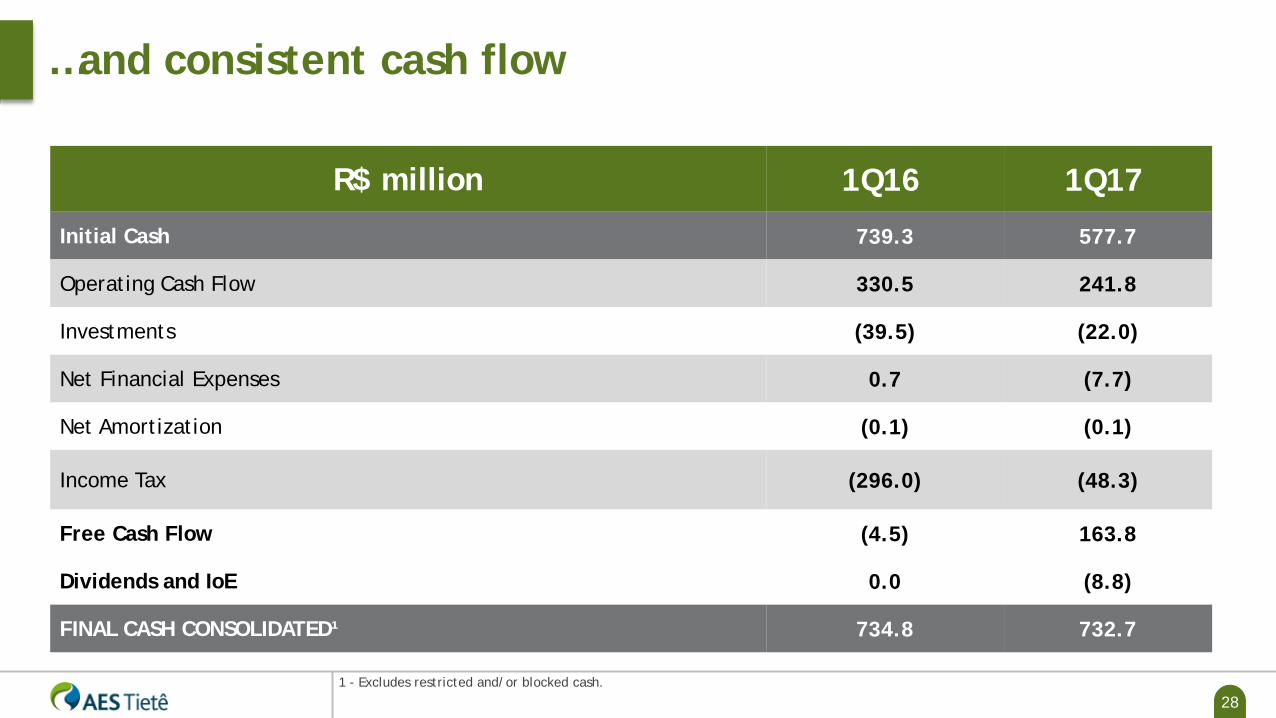

…and consistent cash flow

1 - Excludes restricted and/or blocked cash.

R$ million 1Q16 1Q17

Initial Cash 739.3 577.7

Operating Cash Flow 330.5 241.8

Investments (39.5) (22.0)

Net Financial Expenses 0.7 (7.7)

Net Amortization (0.1) (0.1)

Income Tax (296.0) (48.3)

Free Cash Flow (4.5) 163.8

Dividends and IoE 0.0 (8.8)

FINAL CASH CONSOLIDATED¹ 734.8 732.7

29

40

60

80

100

120

140

Feb-13 May-13 Aug-13 Nov-13 Feb-14 May-14 Aug-14 Nov-14 Feb-15 May-15 Aug-15 Nov-15 Feb-16 May-16 Aug-16 Nov-16 Feb-17 May-17

GETI4 GETI3 IEE IBOV TSR - GETI4 TIET11 TSR - TIET11

Capital Markets

1 – Base 100: from 01/01/2012 to 06/22/2017; 2 – Total Shareholders’ Return; 3 – Base date: 06/22/2017. FX rate 3.3362 BRL; 4 – Government program to reduce energy tariffs.

I

Market cap³: US$ 1.6 billion / R$ 5.4 billion

B3: TIET3 (common shares), TIET4 (preferred shares) and TIET11 (units)

Restricted ADR program (Reg “S” and 144-A)

Feb/2013: High thermoelectric dispatch to conserve water in the reservoirs increase spot pricesAug/2013: 2Q13 results above consensus due to higher-than-expected spot prices

Nov/2013: weak 3Q13 results affected by seasonality strategy

Feb/2014: 4Q13 results slightly below consensus but market show high expectations on 2014 commercialization strategy

May/2014: 1Q14 EBITDA above expectation benefited from seasonality strategy

A

B

C

D

E

Jan/2015: Hydrology for rainy season worse than expected

F

Dec/2015: Corporate Restructuring concluded

AES Tietê Energia x IEE x Ibovespa¹

G

H May/2016: AES Tietê’s stock returned to the MSCI Index

FE G HA CB I

I Aug/2016: Capital Increase

Oct/2016: Conclusion of Capital IncreaseJ

D J

Jan/2017: Company announced the offer to acquire Alto Sertão II Wind Park

K

K

May/2017: Political Event in BrazilL

L

30

● Asset Management - ISO 55001 certification, 1st Generation company in America

● AES Tietê Energia has been included in the Corporate Sustainability Index (ISE) since 2007

● Attractive returns to investors. Strong cash generation; Maximization of payout

● Cost efficiency and optimized capital allocation

● Established risk management capability

We have strong capabilities and corporate governance

31

AES BrasilInvestor Relations

Website:ri.aestiete.com.br

Phone: + 55 11 2195-7048Fax: + 55 11 2195-1004

Ave. Dr. Marcos Penteado de Ulhôa Rodrigues, 939 - 7th floorBarueri - SP – BrazilZIP code: 06460-040