(approved by aicte, new delhi. & affiliated to sri

TRANSCRIPT

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 1

UNIT – I

INVESTMENT MANAGEMENT

Who is investor: The investor who is having extra cash could invest it in securities or in any

other assets like gold or real estate or could simply deposit in his bank account. The person who

invest his savings in to company investment.

Objective of Investor:

To minimize the risk involved in investment and maximise the return

Investment:

In General Sense,

“Investment as the process of sacrificing something now for the prospect of gaining something later”

The above definition we can infer that it contains three dimensions to an investment.

Time

Today’s sacrifice and

Prospect of gain.

Investment:

Investment is the employment of funds on assets with the aim of earning income or capital

appreciation.

To the Economist,

Investment is the net addition made to the nation’s capital stock that consists of goods

and services that are used in the production process. example:- new constructions of

plants and machines, inventories and etc .

Financial Investment

It is the allocation of money to assets that are expected to yield some gain over a period of

time. It is an exchange of financial claims such as stocks and bonds for money. They are expected to

yield returns and experience capital growth over the years.

Financial and Economic Meaning of Investment

In the financial sense investment is the commitment of a person’s fund to derive future income

in the form of income. dividend premium , pension benefit , or appreciation , in the value of their

capital example :- purchasing of shares , debentures , post office saving certificates , insurance

policies are all investments in the financial sense such investment generates financial assets.

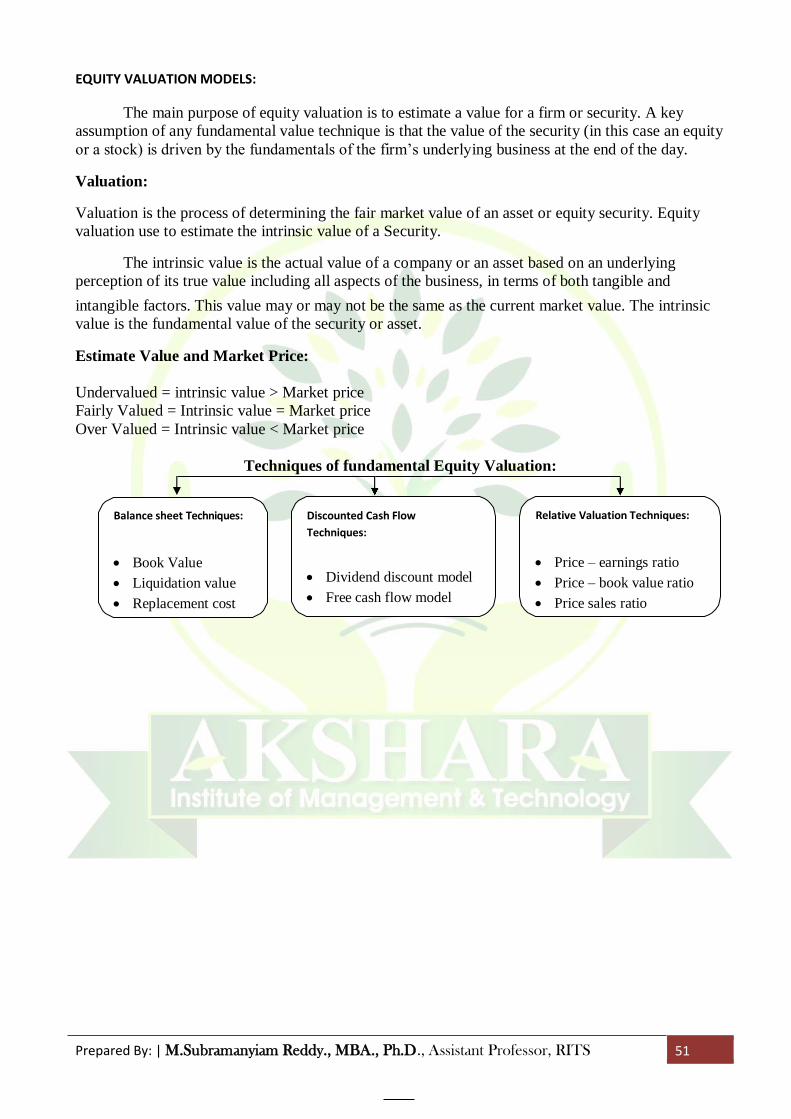

Classification of Investment:

A Major classification is physical and financial investment.

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 2

Physical Investment:

If saving are used to acquired Physical assets, useful for consumption or production. It cannot

be marketability. Physical investment are fixed and movable assets. Such as house, Land, building,

flats, gold, silver and other consumer durables.

Financial Investment:

It is nothing but different types of investments. It consist of marketable and non – marketable

securities. It can be easily transferable.

Marketable Securities: can be easily converted to cash such as government bonds, common stock or

certificates of deposits etc.

Non – Marketable Securities: cannot be easily converted to cash like Bank deposits, Provident Fund

and pension Funds etc.

Characteristics of Investment:

The Characteristics of investment are:

Risk

Return

Safety

Liquidity

Marketability

Risk: at the time of investment. The investor gathering information regarding how much risk

involved in the investment.

Return: The difference between purchasing price and selling price is called capital appreciation or

income or Return.

Safety: the safety of capital is the certainty of return on capital, without loss of money or time

involved.

Liquidity: Investment can be easily realizable, saleable or marketable. Then it said to be liquidity.

Marketability: this refers to transferability or saleability of an assets.

SPECULATION

Speculation means taking up the business risk in the hope of getting short term gain.

Speculation essentially involves buying and selling activities with the expectation of getting profit

from the price. This can be explained with an example. If a spouse buys a stock for its dividend, she

Investment

Physical Investment Financial Investment

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 3

may be termed as an investor. If she buys with the anticipation of price rise in the near future and the

hope of selling it at a gain price she would be termed as a speculator. The dividing line between

speculation and investment is very thin because people buy stocks for dividends and capital

appreciation.

Difference between the Investor and the Speculator

Investment Speculation

Time Horizon Plans for a longer time horizon. His holding

period may be from one year to few years.

Plans for a very short period. Holding Period

varies from few days to months

Risk Assumes moderate Risk Willing to undertake high Risk

Return Likes to have moderate rate of return

associated with limited risk

like to have high returns ofr assuming high risk

Decision

Considers fundamental factors and

evaluates the performance of the company regularly.

Considers inside information, here says and market behaviour

Funds Uses his own funds and avoids borrowed

funds.

Uses borrowed funds to supplement his

personal resources.

Objectives of Investment:

The main investment objectives are increasing the rate of return and reducing the risk. Other

objectives like Liquidity, Safety and Hedge against inflation.

Return: investors always expect a good rate of return from their investment. Rate of return could be

defined as the total income the investor receives during the holding period stated as a percentage of

the purchasing price at the beginning of the holding period.

Return =

Risk: Related with the probability of actual return. Investment risk is as important as measuring its

expected rate of return.

Liquidity: Marketability of the investment provides the liquidity to the investment. The liquidity

depends on the marketing and trading facility.

Hedge against Inflation: Since there is inflation in almost all the economy. The rate of return should

ensure a cover against the inflation. The return rate should be higher than the rate of inflation.

Safety: The selected Investment avenues should be under the legal and regulatory framework.

Approval of law itself adds a flavour of safety.

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 4

Real and Financial Assets:

Financial Assets:

Cash

Bank Deposits

Provident Fund

LIC Schemes

Post Office

Certificate &

Deposits

Saver

Investor

Real Assets:

House, Land,

Buildings and Flats.

Gold, Silver and

other Metals

Consumer Durables Marketable Assets:

Shares, Bonds & Govt. Securities etc.,

Mutual Funds Schemes, UTI Units etc.,

Stock & Capital Market

Primary Market – New Issue Shares

Secondary Market – Secondary sale of

securities.

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 5

Characteristics of Real and Financial Assets:

Currency: Financial assets are exchange documents with an attached value. Their values are

dominated in currency with determined by the Govt. Of an economy. A note or a coin

representing cash or money is a financial asset with an attached face value and is represented

in terms of the currency unit of a country.

Convertibility: financial assets are convertible into any other type of assets.

Divisibility: Financial instruments are divisible into smaller units. The total value is

represented in terms of divisions that can be handled in a trade.

Reversibility: This implies that a financial instrument can be exchanged for any other assets

and logically the so formed asset may be transferred back into the original financial

instrument.

Liquidity: This is the immediate need value of the financial instrument.

Cash Flow: The holding of the financial instrument results in a stream of cash flows that are

the benefits. Accruing to the holder of the financial instrument. Example: 1) A deposit with a

bank gives an inflow of interest to the deposit holder. 2) Shares give the holder dividend or

bonus.

Financial Markets:

A financial market is a market in which people trade financial securities, commodities, and

value at low transaction costs and at prices that reflect supply and demand. Securities include stocks

and bonds, and commodities include precious metals or agricultural products.

Financial market can be refers to those centres and arrangements which facilitate to buying

and selling of financial assets, claims and services.

Financial Markets

Capital Market:

Capital Market is market for financial assets which have a long or indefinite maturity.

Generally, it deals with long term securities which have a maturity period of above one year. Capital

market may be further divided into three namely:

Industrial Securities Market:

As the very name implies, it is a market for industrial securities namely – Equity shares or

Capital Market Money Market

Industrial

Securities market

Govt. Securities

Market

Long Term

Loan Market

Call Money

Market

Short- Term

Market

Commercial

Bill Market

Treasury

Bill Market Primary Market Secondary Market

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 6

Ordinary shares, Preference shares and Debentures or bonds. It is a market where industrial concerns

raise their capital or debt by issuing appropriate instruments. It can be further subdivided into two.

They are: 1. Primary Market or New Issue Market.

2. Secondary Market or Stock exchange.

Government Securities Market:

Government Securities Market are traded in govt. In india many kinds of securities like Short

term and long term securities are traded in this market and short term securities are traded in money

market. The govt. Securities are issued by Central Government, State Government and semi

Government like city corporation authorised by government.

Stock Certificates

Promissory Note

Bearer Bonds etc..

Long – Term Loan Market:

Development banks and commercial banks play a significant role in this market by supplying

long term loans to corporate customers. Long – term loans market may further be classified into:

Term loans Market

Mortgages Market

Financial Guarantees Market

Money Market:

Money Market is a market for dealing with financial assets and securities which have a

maturity period of up to one year. In other words it is a market for purely short term funds. The

Money Market may sub divided in to four. They are:

Call Money Market

Commercial Bills Market

Treasury Bills Market

Short Term Loan Market

Call Money Market:

Call Money Market is a market for extremely short period loans. So one day to fourteen days.

So it is highly liquidity.

Commercial Bills Market:

It is market for bills of exchange arising out of genuine trade transactions. In case credit sales

seller draw a bill of exchange on the buyer. Time period are – 3 Months or 6 Months.

Treasury Bills Market:

It is market for treasury bill which have short term maturity. A Treasury bill is a promissory

Bill or financial bill issued by Government.

Short Term Loan Market:

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 7

It is market where short term loan are given to corporate customer for meeting their working

capital requirements.

Taxation of Income from Investments:

The taxation of your investment income depends on several factors, including the type of investment

income you have (e.g., tax exempt, ordinary, capital gain, or tax deferred).

While investing in a tax-saving instrument or for that matter any investment, it's important to keep an

eye on the taxability of its income. If the income earned is taxable, the scope to build wealth over

long term gets constrained as taxes will eat into the returns.

In the tax saving instruments such as National Savings Certificate (NSC), Senior Citizen Savings

Scheme (SCSS), 5-year time deposits in bank and post office, the interest amount gets added to one's

income and hence is liable to be entirely taxable. so, even though they help you save tax for the

current year, the interest income becomes a tax liability in each year till the tenure ends. Anil Rego,

CEO & Founder of Right Horizons, says, "One must note that (taxable tax savers) instruments will

help in saving the tax to an eligible limit both on investments and on maturity. Since they provide the

tax benefits, the returns on them are likely to be below the market returns."

The post-tax return in them, therefore, comes down after factoring in the tax. For example, for

someone who pays 30.9 percent tax, the post-tax return on a 5-year bank FD of 7 per cent is 4.8 per

cent per annum!

They can still be tax-exempt income if even after adding the interest income, the individual's total

income remains within the exemption limit as provided by income tax rules. Illustratively, a taxpayer

between ages 60-80 earns only interest income from such taxable investments of about Rs 3 lakh a

year. Since the income for such individuals is exempted till Rs 3 lakh, even the interest earned from

investment in taxable products does not translate into tax liability for them.

But, for most others especially those earning a salary or having income from business or profession,

choosing tax savers that come with E-E-E status helps. The investment in these get EEE benefit i.e.

exempt- exempt- exempt status on the income earned. The principal invested qualifies for deduction

under Section 80C of the Income Tax Act, 1961 and the income in all of them is tax exempt under

Section 10.

Here are few such tax savers that not only help you save tax but also help you save tax but also help

you earn tax-free income. But, not all are the same in terms of features and asset-class, so making the

right choice is essential.

TRADING ON STOCK EXCHANGES:

STOCK EXCHANGE

Definition of Stock Exchange: The securities regulation act of 1956 defined stock exchange

as “an association , organization , or a individual which is established for the purpose of assisting ,

regulating , and controlling business in buying ,selling and dealing in securities.”

Meaning: This comes under treasury sector, which provides service to stock brokers & traders to

trade stocks, bonds and securities. A stock exchange helps the companies to raise their fund.

Therefore the companies needs to list themselves in the Stock Exchange and the shares will be

issued which is known as equity or a ordinary share and these shareholders are the real owners of the

company the Board of Directors of the Company are elected out of these Equity Shareholders only.

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 8

FEATURES OF STOCK EXCHANGE

It is an organized market

It is a securities market

It is an important constituent of capital market i.e., market for long- term finance

It is a voluntary association of persons desirous of dealing in securities

Stock exchange is a voluntary association, its membership is not open to everybody

In a stock exchange, only the members can deal in i.e., buy & sell securities

The members of a stock exchange can buy and sell securities either as brokers for & on behalf

of their clients

The dealings in a stock exchange are under certain accepted code of conduct i.e., rules

and regulations

IMPORTANT FUNCTION OF STOCK EXCHANGE

Provide central and convenient meeting places for sellers and buyer of securities

Increase the marketability and liquidity of securities

Contribute to stability of prices of securities

Equalization of price of securities

Smoothen price movement

Help the investors to know the worth of their holdings

Promote the habit of saving and investment

Help capital formation

Help companies and government to raise funds from the investors

Provide forecasting service

History of Stock Exchange

th The stock exchange was established by “East India company” in 18 century . In India it

was established in 1850 with 22 stock brokers opposite to town hall Bombay .This stock exchange is

known as oldest stock exchange of Asia.

Broker and Jobber:

BROKER:He is one acts as a intermediary on behalf of others. A broker in a stock exchange is a

commission agent who transacts business in securities on behalf of non members.

JOBBER:He is not allowed to deal with the public directly .He deals with brokers who are engaged

with the investors. Thus, the securities are bought by the jobber from members and sells to members

who are operating on the stock exchange as broker.

Jobber Broker

1

A jobber is an independent dealer in securities,

purchasing or selling securities on his own

account

A broker deals with the jobber on behalf of his clients.

in other words, a broker is a middleman between a

jobber and clients

2

A jobber deals only with the brokers, does not deal with the general public

A broker is merely an agent, buying or selling securities on behalf of his clients.

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 9

3

A jobber earns profit from his operations i.e.,

buying and selling activities

A broker gets only commission for his dealings

4 Each jobber specializes in certain group of

securities

The broker deals in all types of securities

Speculation and Speculator:

SPECULATION:It is the transaction of members to buy or sell securities on stock exchange

with a view to make profits to anticipated raise or fall in price of securities.

SPECULATOR: The dealer in stock exchange who indulge in speculation are called

speculator. They do not take delivery of securities purchased or sold by them , but only pay or

rescue the difference between the purchase price and sale price . The different types of

speculators are

o BULL

o BEAR

o STAG

o LAME DUCK

Bull:

He is speculator who expects the future raise in price of securities he buys the securities to

sell them at future date at the higher price.

He is called as bull because his activities resembles as a bull , as the bull tends to throw its

victims up in the air through its horns. In simple the bull speculator tries to raise the price of securities

by placing a big purchase orders.

Bear:

He is speculator who expects future fall in prices, he does an agreement to sell securities at

future date at the present market rate. He is called as bear because his altitude resembles with bear , as

the bear tends to stamp its victims down to earth through its paws . In simple the bear speculator forces

of prices of securities to fall through his activities.

Stag:

He operates in new issue of market. He is just like a bull speculator . He applies large number

of shares in the issue market only by paying, application money and allotment money. He is not a

genuine investor because, he sells the allotted securities at the premium and makes profit. In simple

he is cautious in his dealings. He creates an artificial rise in prices of new shares and makes profits.

Lame Duck:

He is speculator when the bear operator finds it difficult to deliver the securities to the

consumer on a particular day as agreed upon , he struggles as a lame duck in fulfilling his

commitment . This happens when the prices do not fall as expected by the bear and the other party is

not willing to postpone the settlement to the next period.

Largest stock exchanges:

IN THE WORLD:

London Stock Exchange

New York Stock Exchange

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 10

Shanhai Stock Exchange

Australia Stock Exchange

Tokyo Stock Exchange

Hong Kong Stock Exchange

Toronto Stock Exchange

Deutsche Borse

Bm&F Bovespa

Nasdaq Omx Stock Exchange

London Stock Exchange

IN INDIA

National Stock Exchange

Bombay Stock Exchange

Calcutta Stock Exchange

Cochin Stock Exchange

Multi Commodity Exchange

Derivatives Exchange

Otc Exchange

Pune Stock Exchange

Interconnects Exchange

London Stock Exchange:

It was the first stock exchange established by east India company in 18th century in London.

The top gainer of LONDON STOCK EXCHANGE is “Blue chip shares.

Bombay Stock Exchange:

It is oldest and first stock exchange of India established in the year 1875. First it was started

under baniyan tree opposite to town hall of Bombay over 22 stock brokers. The top gainer in BSE is

100 companies in that GMR infra is first

National Stock Exchange of India (NSE Or NSEI):

The NSE of India is the leading stock exchange of India, covering 370 cities and towns in the

country. It was established in1994 as a TAX company. It was established by 21 leading financial

institutions and banks like the IDBI, ICICI, IFCI, LIC, SBI, etc...

Features of NSEI:

Nationwide coverage i.e., investors from all over country

Ring less i.e., it has no ring or trading floor

Screen-based trading i.e., trading in this stock exchange is done electronically.

Transparency, i.e., the use of computer screen for trading makes the dealings in securities

transparent.

Professionalization in trading, i.e., it brings professionalism in its functions

Securities and Exchange Board of India(SEBI):

The SEBI was constituted on 12th April, 1988 under a resolution of the Government of India.

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 11

On 31st january,1992, it was made a statutory body by the Securities and Exchange board of India

Act,1992.

The Companies (Amendment) Act, 2000 has given certain powers to SEBI as regards the

issues and transfer of securities and non-payment of dividend.

Function of SEBI:

Regulating the business in stock exchange and any other securities markets.

Promoting and regulating self-regulatory organization.

Registering and regulating the work of collective investment scheme, incluing mutual funds.

Prohibiting fraudulent and unfair trade practices relating to securities market.

Promoting education, and training of intermediaries of securities market

Power of SEBI:

Power to approve the bye-laws of stock exchange

Power to inspect the books of accounts

Power to grant license to any person for the purpose of dealing in certain areas.

Power to delegate powers exercisable by it.

Power to try directly the foliation of certain provision of the company Act

How To Deal and Invest In Stock Exchange:

In order to deal with a securities one as to have an account called Demat a/c or Trading a/c. It

is just like a bank account. Same procedure of opening the bank account is followed to open the a/c.

But all the banks does not give this facility of opening the account, only few banks provide this

facility. After demat a/c or Trading a/s is opened then the securities is bought and sold. The banks

which gives facility of demat a/c in India is

ICICI Bank,

Citi Bank, and

Bank of Baroda etc..

Market Prices:

Market Price (Market Value) = The price at which buyers and sellers trade the item in an open

market place.

Definition: Unique price at which buyers and sellers agree to trade in an open market at a particular

time. In formal markets (such stock exchanges):

The offer Price (selling price) which is higher and

Bid Price (buying price) that is lower.

The difference between these two price is called margin.

The price established in the market where buyers and sellers meet to buy and sell similar products a

In economics, market price is the economic price for which a good or service is offered in

the marketplace. It is of interest mainly in the study of micro economics. Market value and market

price are equal only under conditions of market efficiency, equilibrium, and rational expectations.

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 12

price determined by factors of supply and demand rather than by decisions made by management.

Market Price per Share and calculate:

The market price per share of stock or the price per share of stocks is a current measure of price not

an accounting or historical measure of the value of stock like the book value per share. Which is

based on the information from a company’s balance sheet.

The market price per share is a financial metric that inventors use to determine whether or not to

purchase a stock.

Calculation of Market Price per share:

There are several steps you must take in order to calculate the market price per share.

The First Step: is to determine the date on which you want to calculate the market price per share.

The Second Step: is to find the price on that particular date. You can look at the company’s

monthly, Quarterly or annual report to get the stock price on that particular date.

The Third Step: you must consider the preferred stock if any, that this company owns, if the

company owns and has paid dividends on its preferred stock subtract those dividends from the stock

price you have found form the financial report.

The Fourth Step: Determine the number of shares of stock. Outstanding by looking at the

Company’s quarterly or annual report.

Market Price Per Share =

the adjusted closing price is often used when examining historical returns or a stock’s price is

typically affected by supply and demand of market participants.

The difference between the cash dividends and stock dividend: examining historical return or

performing.

DIVIDEND:

The dividend paid to the shares holders are out of the firm’s profits. Dividends in a firm are

paid according to the policies and decisions of the management. Regarding the retained earnins of the

firm.

The directors of a firm to retain some part of the income and to give the other part of the income and

to give the other part as dividends to the owners of the firm called shareholders.

Which can be classified as:

Cash Dividend

Stock Dividend

Scrip Dividend

Property Dividend

Bond Dividend

Special Dividend

Optional Dividend

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 13

Depreciation Dividend

Dividends from capital surplus

Dividend from Appreciation

Liquidation Dividend

If the company does not find sufficient amount to pay cash dividend. Effective technique of raising

capital. It also helps in raising future dividends of existing shareholders.

Stock Splits:

When the company pays a stock dividend it may also offer the stock split up. Effective stock

split up is only an increase in the number of shares that are outstanding. The change does not affect

the stated value of a stock or its surplus.

Reduction of the market Price

Future Growth

Reverse split

Re – Purchase of stock

Right Issue:

Right issue is an offer to the existing shareholders to subscribe for more shares, in proportion to their

existing shareholding usually at a relatively chep price.

In these rights offerings companies grant shareholders a chance to buy new shares at a discount to the

current trading price.

A rights issue is an invitation to existing shareholders to purchase additional new shares in the

company.

Ex: Mr. A have 100 shares of X company @ rs. 400 = 40, 000 1:1 subscription right issue at offring

price of Rs 200 offer price is 100 shares @ Rs. 100 = 20, 000 Average price cost of acquisition for

the 200 shares to Rs. 300 shares.

=40, 000 + 20,000/200 = 300.

Ad of right issue: it gives existing shareholders securities called “Rights” which give the shareholders

the right to purchase new shares at a discount to the market price.

Bonus Issue:

The term bonus in relation to share capital refers to an extra dividend to the shareholders from

surplus profits. When a company has accumulated profits which are in excess of its need then the

excess amount can be distributed by way of bonus share among existing shareholders.

What is an 'Adjusted Closing Price'

An adjusted closing price is a stock's closing price on any given day of trading that has been amended

to include any distributions and corporate actions that occurred at any time prior to the next day's

open. The adjusted closing price is often used when examining historical returns or performing a

detailed analysis on historical returns.

A stock's price is typically affected by supply and demand of market participants. However, there are

some corporate actions that affect a stock's price, which needs to be adjusted in the event of these

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 14

actions. The adjusted closing price is a useful tool when examining historical returns because it gives

analysts an accurate representation of the firm's equity value beyond the simple market price. It

accounts for all corporate actions such as stock splits, dividends/distributions and rights offerings.

Investors should understand how corporate actions are accounted for in a stock's adjusted closing

price.

Adjusting Prices for Stock Splits

A stock split is a corporate action that is usually done by companies to make their share prices more

marketable. A stock split does not affect a company's total market capitalization, but it does affect the

company's stock price. Consequently, a company undergoing a stock split must adjust its closing

price to depict the effect of the corporate action.

For example, a company's board of directors may decide to split the company's stock three-for-one.

Therefore, the company's shares outstanding increase by a multiple of three, while its share price is

divided by three. If a stock closed at $300 the day prior to its stock split, the closing price is adjusted

to $100, or $300 divided by 3, per share to show the effect of the corporate action.

Adjusting for Dividends

Common distributions that affect a stock's price include cash dividends and stock dividends. The

difference between cash dividends and stock dividends is shareholders are entitled to a predetermined

price per share and additional shares, respectively. For example, assume a company declared a $1

cash dividend and is trading at $51 per share on the ex-dividend date. On the ex-dividend date, the

stock price is reduced by $1 and the adjusted closing price is $50.

Adjusting for Rights Offerings

A stock's adjusted closing price also reflects rights offerings that may occur. A rights offering is an

issue of rights given to existing shareholders, which entitles the shareholders to subscribe to the

rights issue in proportion to their shares. For example assume a company declares a rights offering, in

which existing shareholders are entitled to one additional share for every two shares owned. Assume

the stock is trading at $50 and existing shareholders are able to purchase additional shares at a

subscription price of $45. On the ex-date, the adjusted closing price is calculated based on the

adjusting factor and the closing price.

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 15

UNIT – II

FIXED INCOME SECURITES

A fixed income security is an investment that provides a return in the form of fixed periodic

payments and the eventual return of principal at maturity. Unlike a variable-income security, where

payments change based on some underlying measure such as short-term interest rates, the payments

of a fixed-income security are known in advance.

Security is an evidence of property right. Like equity shares, preference shares, debentures, bonds

and other marketable instruments are called as securities.

Classification of Securities are:

Fixed Income Securities – Earn interest / dividend at fixed rate.

Variable Income Securities – Earn dividend at variable rate.

Fixed Income Securities:

FI Securities are investment where the cash flows are according to a pre determined amount

of interest, paid on a fixed schedule. Unlike a variable-income security, where payments

change based on some underlying measure such as short term interest rates, the payments of

a fixed-income security are known in advance. Popularly known as Debt instrument

Types of Fixed income securities:

The different types of fixed income securities include government securities, corporate bonds,

Treasury Bills, Commercial Paper, Strips etc.

Bank Deposits

Company Deposits

Small Saving Schemes

Debentures / Bonds

Bank Deposits: - Fixed deposit in the bank

Safest

Highly liquid as they can be encashed premature at 1% less on interest rate.

Neither tradable and nor transferable

Nomination facility.

Company Deposits:

Her, instead of deposits with bank, we deposit with NBFC’s and Manufacturing companies

Offer max interest rate than bank.

Neither secured nor guaranteed by RBI

Neither tradable nor transferable

No Nomination facilities is available

Small Saving Schemes:

Initial investment get double in 5 – 6 years

Neither tradable

Accepted as collateral

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 16

Debentures or Bonds:

Long term debt instruments

Higher rate of interest

Safer or unsafe (credit rating agency loss to decide)

Liquidity is very light

Tradable and transferable

Advantages of Fixed income securities:

Max return (revenue gain), Capital gain

Less risk

Tax advantages

Disadvantages of fixed income securities:

Return is fixed. Cannot earn more

Due to inflation, fixed return become very less in real value

Difficult to sell at attractive price

Real and Rates of Return:

A real rate of return is the annual percentage return realized on an investment, which is

adjusted for changes in prices due to inflation or other external effects. This method expresses

the nominal rate of return in real terms, which keeps the purchasing power of a given level of capital

constant over time. Adjusting the nominal return to compensate for factors such as inflation allows

you to determine how much of your nominal return is actually real return.

Nominal Interest Rate:

Nominal interest rate refers to the interest rate before taking inflation into account. Nominal can also

refer to the advertised or stated interest rate on a loan, without taking into account any fees or

compounding of interest. Finally, the federal funds rate, the interest rate set by the Federal Reserve,

can also be referred to as a nominal rate.

Difference between Nominal and Real Interest Rates

Unlike the nominal rate, the real interest rate takes the inflation rate into account. The equation that

links nominal and real interest rates can be approximated as:

Nominal rate = Real interest rate + Inflation rate,

or

Nominal rate - Inflation rate = Real rate.

Nominal & Real Rates of Return:

Investors are more concerned with the real rate of return – the return adjusted for the effects

of inflation. Inflation affects the value of money by reducing spending power. Thus:

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 17

Real Return = Nominal Rate – Annual calculated Rate of Return

Example: Assume the return is 100% taxable, an investor with a return of 10%, having a tax rate of

30%, would have an after tax return of 7%, calculated as 10% X (100% – 30%).

Taking inflation into account (at 2%), the investor’s approximate real return would be 5% (7% –

2%).

Computation of Risk and Return:

Risk:

Risk is a measure of future uncertainties in achieving program performance goals and objectives within

defined cost, schedule and performance constraints. Risk can be associated with all aspects of a program

(e.g., threat, technology maturity, supplier capability, design maturation, performance against plan,) as

these aspects relate across the Work Breakdown Structure (WBS) and Integrated Master Schedule (IMS).

Risk addresses the potential variation in the planned approach and its expected outcome. While such

variation could include positive as well as negative effects, this guide will only address negative future

effects since programs have typically experienced difficulty in this area during the acquisition process.

Risk is the possibility of loss or injury

Investor thinks minimize the risk and maximise the Return

Risk is inter changeable used with uncertainty

Components of Risk Risks have three components:

A future root cause (yet to happen), which, if eliminated or corrected, would prevent a

potential consequence from occurring,

A probability (or likelihood) assessed at the present time of that future root cause occurring,

and

The consequence (or effect) of that future occurrence.

A future root cause is the most basic reason for the presence of a risk. Accordingly, risks should be tied to future root causes and their effects.

Risk mainly consists of two components:

RISK

Systematic Risk:

The systematic risk affects the entire market. Often we read in the newspaper that the stock

market is in the bear hug or in the bull grip. This indicates that the entire market is moving in a

particular direction either upward and downward.

The economic conditions, political situations and Sociological changes affect the security

market.

Systematic Risk Unsystematic Risk

Market Risk Business Risk Financial Risk

Intangible Events Tangible Events

Purchasing Power Risk Interest Rate Risk

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 18

1988 recession experienced by developed and developing countries has affected the stock

market all over the world.

The systematic risk is further sub – divided into:

Market Risk

Interest Rate Risk

Purchasing Power Risk

Market Risk:

Jack Clark Francis defied market risk is portion of total variability of return caused by the

alternating forces of Bull and Bear Markets.

When the security index moves upward haltingly for a significant period of time, it is known

as Bull Market.

When the security index moves downward, it is known as Bear Market. Bear market is just a

reverse to the bull market.

Market risk can be sub divided into:

Tangible Events – it is Real events like Earthquakes, war, political uncertainty and fall in the

value of currency as the Recession time.

Intangible Events – Market Psychology – 1994 LPG due to market psychology is positive

and 1988 it is a recession at the time Market psychology is negative.

1998 recession at this time market is falls down – Rush to sell the share in the market in this the price

of the scrip’s fall below their intrinsic values.

Interest Rate Risk:

The variation in the single period rate of returns caused by the fluctuation in the market

interest Rates.

The most commonly interest rate risk affects the price of bonds, debentures and stocks.

The fluctuations in the interest rate are caused by the changes in Govt. Monetary Policy.

Change interest rates of Treasury bills and govt. bounds etc..

Purchasing Power Risk:

The Variation in the returns an caused also by the loss of purchasing power of currency.

Inflation is the reason behind the loss of purchasing power.

Purchasing power risk is the probable loss in the purchasing power of the returns to be

received.

The inflation may be Demand pull or cost push inflation.

Unsystematic Risk:

It is the factors are specific, unique and related to the particular industry or company.

Unsystematic risk stems from managerial inefficiency, technological change in the production

process, availability of raw material, changes in the consumer preference and labour problem.

Unsystematic risk can be classified into:

Business Risk

Financial Risk

Business Risk:

Business risk is that portion of the unsystematic risk caused by the operating environment of

the business. Variation that occurs in the operating environment is reflected on the operating income

and expected dividends.

Business risk can be sub – divided into:

Internal Business Risk

External Business Risk

Internal Business risk:

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 19

Fluctuations in the sales

Research and Development

Personnel Management

Fixed cost

Single product

External Business Risk:

Social and regulatory factors

Political risk

Business Cycle

Financial Risk:

It refers to the variability of the income to the equity capital due to the debt capital. Financial

risk in a company is associated with the capital Structure of the company.

Capital Structure of the company consists of Equity funds and borrowed funds.

The presence of debt and preference capital results in a commitment of paying interest or pre

fixed rate of dividend.

Return:

Return is the primary motivating force that drives investment. It represents the reward for

undertaking investment. Since the game of investing is about returns (after allowing for risk),

measurement of realised (historical) returns is necessary to assess how well the investment manager

has done. In addition, historical returns are often used as an important input in estimating future

(prospective) returns.

It is a Reward for the undertaking investment.

Measurement of realised return

The return of an investment consists of two components:

Current Return

Capital Return

Current Return:

The first component that often comes to mind when one is thinking about return is the

periodic cash flow (income or interest), such as dividend or interest, generated by the investment.

Current return is measured as the periodic income in relation to the beginning price of the investment.

Capital Return:

The second component of return is reflected in the price change called the capital return. It is

simply the price appreciation or depreciation divided the beginning price of the asset. For assets like

equity stocks, the capital return predominates.

The total return for any security is defined as:

Total return = Current return + Capital return

The current return can be zero or positive, whereas the capital return can be negative.

Measuring Historical Return:

The total return on an investment for a given period is:

Total Return =

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 20

Where:

C= Cash inflow PE

= Ending price

PB = Beginning Price

BOND:

A Bond is a contract that requires the borrower to pay the interest income to the lender. It

resembles the promissory note and issued by the government and corporate. The par value of the

bond indicates the face value of the bond. i.e. the value stated on the bond paper.

Most of the bonds make fixed interest payment till the maturity period. This specific rate of interest is

known as coupon rate paid quarterly, semi – annually and annually. At the end of the maturity period

the value is repaid.

A long-term debt instrument (a legal contract) in which a borrower agrees to make payments

of principal and interest, on specific dates, to the holders of the bond.

It is a Debt instrument issued by Govt. and Public Sector companies.

Features of Bonds:

The features of bonds are:

1. Face Value:

a. Value printed on the bond

b. Basis for payment of interest

c. We may or not issue at face value or par, premium and Discount value.

2. Redemption Value:

a. Value of buying back of the bonds

b. Max the face value – premium, less than face value – discount and equal to face value

– Re demand at par

3. Coupon rate:

a. Rate of interest to be paid

4. Maturity Period:

a. Period for which bond is issued

b. Pay interest only to maturity period

c. After that no interest is paid

5. Collateral:

a. Security against which the bonds an issued to the bond holder. If interest is not paid

then “bond trustee” dispose this collateral to pay interest.

6. Bond Indent:

a. Agreement among – bond holders, company and bond trustee.

Contains terms and conditions on the above said features and rights of the each party.

TYPES OF BONDS:

Bonds are classified as:

1. Convertible Bonds: - bond for some time than it become convertible to shares. Ex: after 5

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 21

years the bond can be convertible bond Rs. 100. With coupon rate 10% which will be

converted into 2 equity shares of Rs, 50. Each.

2. Non – Convertible Bonds: - Continue as bond through the maturity period.

3. Redeemable Bonds: - Specified about the redemption period then it will buy back at

Premium or discount

4. Irredeemable bonds: - No Specification about maturity to bond holders get interest till the

company buys it back.

5. Secured Bond:- company mortgagers some of it assets. Ex: building, land etc. With the

trustee if co. fails to pay interest, trustee will sell these assets to make payment.

6. Unsecured Bond:- No such a mortgages

7. Callable Bonds: - company has the right redeem before maturity period. When market

interest rate < coupon.

8. Put able Bonds: - Bond holders have the right to redeem before maturity period. When

market interest rate >Coupon rate

9. Junk Bonds:- high coupon rate and not secured by an asset. More risk of default, speculators

prefer than bonds.

10. Zero Bonds:- no coupon rate but compulsory converted into equity share. Within the 3 years

of issue.

11. Deep Discount bonds: - it is a zero coupon bond without compulsion to convert, issue at

discount.

BOND CHARACTERISTICS:

A bond obligates the issuer to make specified payments (interest and principal) to the

bondholder. There are: -

Par value,

Coupon Rate and

Maturity Data.

Par Value: the par value is the value stated on the face of bond. It represents the amount the issuer

promises to pay at the time of the maturity.

Coupon Rate: the coupon rate is the interest rate payable to the bond holder.

Maturity Date: the maturity date is the date when the principal amount is payable to the bond

holder.

BOND YIELD:

Bond yield is the return on a bond made up of 3 components.

Coupon Rate

Capital Gain

Interest on Maturity

Generally classified in to 2 components

Capital Gain

Revenue Gain

Factors affecting bond yield or Bond Risk:

Generally stocks are considered to be risky but bonds are not. This is not fully correct. Bonds

do have risk but the nature and types of risks may be different. The risks are interest rate, default,

marketability and call ability risk.

Interest rate risk:

o Variability in the return from the debt instruments to investors is caused by the changes in the market interest rate.

o This is known as interest rate risk. changes that occur in interest rate affect the bonds more directly then the equity.

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 22

o There is a relationship between the coupon rate and market interest rate.

o If the market interest rate move up, the price of the bond declines and vice versa. Inflation rate risk:

o The uncertainty over the future value of our investment o Suppose bond is of Rs. 100 and offers 12% P.A and have a maturity of 1 year then be

gets rs.112 after one year.

Default Risk:

o If the company which has issued bond and fails to pay interest or pay redemption value.

o Due to micro and macro environmental factors. Call Risk:

o If the bond is callable bond, then the company has the option to call the bonds before maturity period.

o We lose the opportunity to earn

o This happen when interest rate in the market > coupon rate. Liquidity Risk:

o Few bonds are not preferred by the investor to buy or when we want to sell. So it is difficult to exit from their debt investment.

Reinvestment Risk:

o When a bond pays periodic interest there is a risk that the interest payments may have to be reinvested at a lower interest rate. Called reinvestment risk.

Foreign Exchange Risk:

o If a bond has payments that are denominated in a foreign currency its repee cash flows are uncertain.

Methods or Measures of Bond Yield:

The methods of Bond Yield are:

Current Yield

Holding Period Yield

Yield to Maturity

Approximate Yield to Maturity

Yield to Call

Current Yield:

it is the current return on the investments

Holding Period Yield:

Holding period return an investor buy a bond and sells it after holding for a period. The rate of return

in that holding period is:

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 23

Where:

I = Interest/ income/ coupon

amount P0= Current Market Price

Pn= Redemption Value or par Value

Yield to Maturity (YTM):

It is the rate at which NPV (net present value) of the bond = 0 or it is the discount rate at

which present value of cash inflow (PVCI) of bond in feature = PV Of cash outflow of bond PVCO.

Approximate Yield to Maturity:

It is a lengthy process to find the YTM by using IRR Method. Hence an approximation is

made to it in the form of a formula. It is called AYTM.

Where:

I = Interest or income or coupon

amount. P0= Current market price

Pn= Redemption value / Par value

N = Maturity Period

Where:

RL = Lower Rate

RH = High Rate

VL = Value at lower rate VH

= Value at Higher rate O = Out flow

Yield to Call (YTC):

If the bond is callable then the issuer has the right to redeem before maturity period.

YTC formula is some as AYTM but n = call period ≠ Maturity period.

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 24

I = Interest or income or coupon

amount. P0= Current market price

Pn= Redemption value / Par value N = Callable Period

BOND PRICE:

The value of bond or any asset, real or financial is equal to the present value of the cash flows

expected from Bond.

The value of a bond requires:

An estimate of expected cash flows

As estimate of the required returns

Bond Valuation:

It refers to the process of determining the value or price of a bond.

As the cash flows are spread over a period of years in the future. All the future cash flow have

to be converted into present to determine the value of the bond.

Where:

T= time period when the payment is

received P = Value of the bond at present.

C = Coupon rate or annual interest

payment M = Maturity value

N = no – of years

R = Discount rate or interest rate in the market.

Where:

P=value of bond

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 25

C/2=semi annual interest

payment r/2=the discount rate of

year

m= maturity value

2n= maturity

period

T=time period when the payment is received

YIELD CURVE:

The bond portfolio manager is often concerned with two aspects of interest rates: the level of

interest rate and the term structure of interest rate. The relationship between the yield and time or

years to maturity is called term structure.

The term structure is also known as yield curve. In analysing the effect of maturity on yield all other

influences are held constant. Usually pure discount instruments are selected to eliminate the effect of

coupon payments.

The bonds chosen do not have early redemption features. The maturity date are different but the

risks, tax liabilities and redemption possibilities are similar.

Its shows YTM is related to term to maturity for bonds that are similar in all aspects excepting

maturity.

The following data for government securities:

Face

Value

Interest

rate

Maturity

years

Current

Price YTM

100000 0 1 88.968 12.40

100000 12.75 2 99.367 13.13

100000 13.50 3 100.352 13.35

100000 13.50 4 99.706 13.60

100000 13.75 5 99.484 13.90

BOND DURATION:

Duration of a bond is generally mean that maturity period. But it is a wrong measure because

Zero coupon bond and 10% coupon bond of same maturity and have some duration but 10% coupon

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 26

bond recover “Purchase Price” Exactly the Zero Coupon.

There four measure of life of a bond must consider not only timing of cash flows but also size

of cash inflow.

Fredrick R Maculay: in 1983 has given such a measure for life of a bond and it is popularly known

as Maculay’s Duration of a bond.

Definition:

Maculay’s Duration is the weighted average maturity of a bonds cash flows on a present value basis.

MD’s is number of years needed to fully recover purchase price of a bond taking present values of its

cash inflows.

Procedure to Calculate Maculay’s Duration:

1. List out the years in which cash inflows are realized.

2. List out cash flows realized in respective years.

3. List out present value factor’s for each years cash flow taking discount rate (YTM).

4. Multiply (PVF) and (CF) to get present value of each cash flow

5. Then add all PVCI i.e. ∑ PVCI (present value cash inflow) = P0

6. Find the weight of patch cash flow in ∑ PVCI. Wt =

7. Multiply weight and years of cash inflow 8. Add all the above (weight X years) to get maculay’s Duration.

Maculay’s Duration (MD) = ∑Wt (t) Where:

Wt = Weight of cash flow T

= time period in years

Years CI PVAF PVCI PVCI /

P0 = Wt

Wt X t

P0 MD = ?

IMMUNISATION:

Immunisation is a technique that makes the bond portfolio holder to be relatively certain

about the promised stream of cash flows. The bond interest rate risk raises form the changes in the

market interest rate.

The market rate affects the coupon rate and the price of the bond. In the immunisation

process, the coupon rate risk and the price of the bonds fall.

At the same time the newly issued bonds offer higher interest rate.

The coupon can be reinvested in the bonds offering higher interest rate and losses that occur

due to the fall in the price of bond can be offset and the portfolio is said to be immunized.

The process the bond portfolio manager or investor has to calculate the duration of the promised

outflow of the funds and invest in a portfolio of bonds which has an identical duration.

The bond portfolio duration is the weighted average of the durations of the individual bonds

in the portfolio.

For Example: if an investor has invested equal amount of money in three bonds namely A,B

and C with a duration of 2, 3 and 4 years respectively, then the bond portfolio duration is

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 27

D = 1/3 x 2 + 1/3 x3 + 1/3 x 4

= 0.66 + 1+1.33

D = 2.99 or 3 years.

By matching the outflow duration with cash inflow duration from bond investment the bond manager

can offset the interest rate risk and price risk. the portfolio of money to be invested between the

different types of bonds also can be found. The equation is:

Investment outflow = (X1 x Duration of bond1) + (X2 x Duration of bond2)

X1, X2 is the proportion of the investment on bond 1 and 2.

(X1 x D1) + (X2 x D2) = 2

Where:

X1 = the proportion of the investment on bond A X2 = the proportion of the investment on bond B D1 = Duration of bond A

D2 = Duration of Bond B

Duration (MD) = ∑Wt (t) Where:

Wt = Weight of cash flow T = time period in years

Years CI PVAF PVCI PVCI / P0 = Wt Wt X t

P0 MD = ?

AKSHARA INSTITUTE OF MANAGEMENT & TECHNOLOGY.

(Approved by AICTE, New Delhi. & Affiliated to Sri Venkateswara University, Tirupati.)

Prepared by: Dr. M.A.Dhandapani., M.Com., MBA., M.Phil., Ph.D I-CET CODE :AMTT Page 28

Index Means:

UNIT – III

INDEX MODELS

pared By: | M.Subramanyiam Reddy., MBA., P h.D., Assistant Professor, RITS Pre 30

Alphabetically arranged list of items (such as names or terms) given at the end of a printed

text with page numbers on which the item can be found.

Indexes (indices) also measure up and down movement of industrial production, and of the

market prices of bonds, commodities, shares, etc. See also indexation.

An index is a statistical measure of the changes in a portfolio of stocks representing the

overall market.

What is Index:

An Index is a statistical aggregate that measures change. It is and indicator. Sensex and Nifty are

large capital index in India.

Uses of Index:

Indicator of market movement/returns

It reflects highly up-to-date information

Lead indicator of the economy

Stock Market:

A stock market is a physical place, where brokers gather to buy and sell stocks and other

securities. It enables the trading of stocks. Stock market indexes are meant to capture the overall

behaviour of equity markets

Types of Stock Index:

There are mainly three types of stock index

Market capitalization weighted index

Free-float market capitalization weighted index

Price weighted index

Index Futures: Index futures is one of the most successful financial innovation of financial market.

In 1982, the stock index futures is the futures contract made on the major stock market index. The

stock index futures has the following characteristics.

It is an obligation and not an option

Settlement value depends

o On the value of stock index and the price at which the original contract is struck and o On the specified time the difference between the index value at the last closing day of

the contract and the original price of the contract

Basis of the stock index futures is the specified stock market index. No physical delivery of

stock is made.

Importance of Index

Easy location

Save times and efforts

Efficiency Cross reference

Reduce cost

An index is a statistical measure of the changes in a portfolio of stocks representing the overall

market.

Risk Premium:

pared By: | M.Subramanyiam Reddy., MBA., P h.D., Assistant Professor, RITS Pre 31

A risk premium is the return in excess of the risk-free rate of return an investment is expected

to yield; an asset's risk premium is a form of compensation for investors who tolerate the extra risk,

compared to that of a risk-free asset, in a given investment. For example, high-quality corporate

bonds issued by established corporations earning large profits have very little risk of default.

Therefore, such bonds pay a lower interest rate, or yield, than bonds issued by less-established

companies with uncertain profitability and relatively higher default risk

Investors expect to be properly compensated for the amount of risk they undertake in the form

of a risk premium, or additional returns above the rate of return on a risk-free investment such as U.S.

government-issued securities. In other words, investors risk losing their money because of the

uncertainty of a potential investment failure on the part of the borrower in exchange for receiving

extra returns as a reward if the investment turns out to be profitable. Therefore, the prospect of

earning a risk premium does not mean investors can actually get it because it is possible the borrower

may default absent a successful investment outcome.

Portfolio Risk:

Portfolio Management is management of large investible funds with a view to maximizing

return and minimizing risk.

Though return of portfolio is the weighted average return of individual assets in the portfolio.

But risk of a portfolio is not a weighted average risk of individual assets. Because overall risk is

reduced by combining assets into one portfolio.

When two or more securities or assets are combined in portfolio, their covariance or interactive risk

is to be considered. Thus if the returns on two assets more together their co-variance is positive and

the risk is more on such portfolio. If on the other hand the returns more independently or in opposite

directions the co – variance is negative and the risk in total will be lower.

Where:

Cov xy = Covariance

Rx= Return on Security x1

Ry = Return on Security y1

Rx = Expected Return x Ry

= Expected Return y

N = No – of – Observations.

The co – efficient of correlation is another measure designed to indicated the similarity or

dissimilarity in the behaviour of two variables.

Correlation co – efficient of x and y as:

pared By: | M.Subramanyiam Reddy., MBA., P h.D., Assistant Professor, RITS Pre 32

Where:

The correlation of co – efficient indicates the similarity or dissimilarity in the behaviour of x

and y stocks. In correlation, co – variance is not taken as an absolute value but relative to the standard

deviation of individual securities. It shows, how much x and y vary together as a proportion of their

combined individual variations measured by Standard Deviation of x and standard deviation of y. In

our example the correlation co – efficient is -1.0 which indicates that there is a perfect negative

correlation and the returns move in the opposite direction. If the correlation is 1, means perfect

positive correlation exists between the securities and they tend to move in the same direction. If the

correlation co-efficient is Zero, the securities returns are independent. Thus, the correlation between

two securities depends upon the covariance between the two securities and the standard deviation of

each security.

Now, let us proceed to calculate the portfolio risk. Combination of two securities reduces the risk

factor if less degree of positive correlation exists between them.

Expected Return on Portfolio:

Where:

Rp = Return on the Portfolio

X1 = Proportion of total portfolio invested in security 1

R1 = Expected return of Security 1

Where:

MARKOWITZ PORTFOLIO SELECTION:

pared By: | M.Subramanyiam Reddy., MBA., P h.D., Assistant Professor, RITS Pre 33

Portfolio means:

A portfolio is a grouping of financial assets such as stocks, bonds, cash equivalents as well as

their mutual, exchange –traded and closed-fund counterparts. His choice depends upon the risk-return

characteristics of individual securities.

Phases of Portfolio Management

Building a Portfolio:

Step-1 : Use the Markowitz portfolio selection model to identify optimal combinations.

Step-2 : consider borrowing and lending possibilities.

Step-3 : choose the final portfolio based on your preferences for return relative to risk.

PORTFOLIO SELECTION:

• Goal: finding the optimal portfolio

• OPTIMAL PORTFOLIO: Portfolio that provides the highest return and lowest risk.

• Method of portfolio selection: Markowitz model

The proper goal of portfolio construction would be to generate a portfolio that provides the

highest return and the lowest risk is called optimal portfolio. The process of finding the optimal

portfolio is described as Portfolio selection.

Efficient Set of Portfolio:

The concept of efficient portfolio - let us consider various combinations of securities and

designated them as portfolio 1 to n.

The risk of these portfolios may be estimated by measuring the standard deviation of portfolio

returns.

Feasible set of portfolio:

Also known as portfolio opportunity set.

With a limited no of securities an investor can create a very large no. of portfolios by

combining these’s securities in different proportions.

EFFICIENT PORTFOLIO

Portfolio

No

Expected

Return

Standard

Deviation

Portfolio Management

Security

Analysis

Portfolio

Analysis

Portfolio

Selection

Portfolio

Revision

Portfolio

Evaluatio

1. Fundamental Analysis

2. Technical Analysis

3. Market Hypothesis

Diversification 1. Markowitz Model

2. Sharpe’s Single

Index Model

3. CAPM

4. APT

1. Formula

Plans

2. Rupee Cost

Averaging

1. Sharpe’s Index

2. Treynor’s Measure

3. Jenson’s Measure

4. M2 Measure

pared By: | M.Subramanyiam Reddy., MBA., P h.D., Assistant Professor, RITS Pre 34

1 5.6 4.5

2 7.8 5.8

3 9.2 7.6

4 10.5 8.1

5 11.7 8.1

6 12.4 9.3

7 13.5 9.5

8 13.5 11.3

9 15.7 12.7

10 16.8 12.09

Compare 4 & 5 which have same standard deviation:

Portfolio

No

Expected

Return

Standard

Deviation

1 5.6 4.5 Higher return?? Pf no.5 gives higher

expected return which is more efficient

portfolio then Pf no. 4.

2 7.8 5.8

3 9.2 7.6

4 10.5 8.1

5 11.7 8.1

6 12.4 9.3

Compare 7 & 8 which have same Expected Return:

Portfolio

No

Expected

Return

Standard

Deviation

1 5.6 4.5

2 7.8 5.8

3 9.2 7.6

Lower standard deviation?? Pf no.7

which is more efficient portfolio then Pf

no. 8.

4 10.5 8.1

5 11.7 8.1

6 12.4 9.3

7 13.5 9.5

8 13.5 11.3 9 15.7 12.7

10 16.8 12.09

CRITERIA: EFFICIENT PROTFOLIO

Given 2 portfolio with the same expected return, the investor would prefer the one with the

lower risk.

Given 2 portfolio with the same risk, the investor would prefer the one with the higher

expected return.

Prepared By: | M.Subramanyiam Reddy., MBA., Ph.D., Assistant Professor, RITS 35

Grouping of financial stocks :

Stock

1

Stock

2

Compare Result

E F Same return but E has Less risk then F E has preferred C has minimum

risk and B has

maximum risk C E Same risk but E offer more return E has preferred Based on these

we drawing

efficient frontier

C A Same return but C less risk C has preferred

A B Same level of risk but B has higher

return.

B has preferred

Harry Max Markowitz Model:

Harry Max Markowitz (born August 24, 1927) is an American economist. He is best known for his

pioneering work in Modern Portfolio Theory. Harry Markowitz put forward this model in 1952.

Studied the effects of asset risk, return, correlation and diversification on probable investment

portfolio returns.

Essence of Markowitz Model “Do not put all your eggs in one basket”

An investor has a certain amount of capital he wants to invest over a single time horizon.

He can choose between different investment instruments, like stocks, bonds, options,

currency, or portfolio. The investment decision depends on the future risk and return.

The decision also depends on if he or she wants to either maximize the yield or Minimize the

risk.

Markowitz model assists in the selection of the most efficient by analysing various possible

Prepared By: | M.Subramanyiam Reddy., MBA., Ph.D., Assistant Professor, RITS 36

portfolios of the given securities.

By choosing securities that do not 'move' exactly together, the HM model shows investors

how to reduce their risk.

The HM model is also called Mean-Variance Model due to the fact that it is based on

expected returns (mean) and the standard deviation (variance) of the various portfolios.

Diversification and Portfolio Risk:

Diversification is a technique of reducing the risk involved in investment and in portfolio

management. This is a process of conscious selection of assets, instruments and scrips of

companies/government securities, in a manner that the total risks are brought down. This process

helps in the reduction of risk, under category of what is known as unsystematic risk and promotes the

optimisation of returns for a given level of risks in portfolio management.

Market risk versus Unique risk:

The portfolio risk does not fall below a certain level, irrespective of how wide the

diversification is why?. The answer lies in the following relationship which represents a basic insight

of modern portfolio theory.

Total Risk = Unique risk + Market Risk

The unique risk of a security represents that portion of its total risk which stems from firm – specific

factors like the development of a new product, a labour strike, or the emergence of a new competitor.

Events of this nature primarily affect the specific firm and not all firms in general. Hence the unique

risk of a stock can be washed away by combining it with other stocks. In a diversified portfolio,

unique risks of different stocks tend to cancel each other – a favourable development in one firm may

offset an adverse happening in another and vice versa. Hence, unique risk is also referred to as

diversifiable risk or unsystematic risk.

The Market Risk of a stock represents that portion of its risk which is attributable to economy – wide

factors like the growth rate of GNP, the level of government spending, money supply, interest rate

structure, and inflation rate. Since these factors affect all firms to a greater or lesser degree, investors

cannot avoid the risk arising from them, however diversified their portfolios may be. Hence, it is also

referred to as systematic risk or non – diversifiable risk.

Markowitz Model Assumptions:

An investor has a certain amount of capital he wants to invest over a single time horizon.

He can choose between different investment instruments, like stocks, bonds, options,

currency, or portfolio.

The investment decision depends on the future risk and return. The decision also depends on

if he or she wants to either maximize the yield or minimize the risk.

The investor is only willing to accept a higher risk if he or she gets a higher expected return.

Prepared By: | M.Subramanyiam Reddy., MBA., Ph.D., Assistant Professor, RITS 37

Tools of Selection of Portfolio – Markowitz Model:

1. Expected return (Mean):

Mean and average to refer to the sum of all values divided by the total number of values.

The mean is the usual average, so:

(13 + 18 + 13 + 14 + 13 + 16 + 14 + 21 + 13) ÷ 9 = 15

Expected Return on Portfolio:

(OR)

Where:

ER = The expected return on Portfolio

E(Ri) = The estimated return in scenario i

Wi = Weight of security i occurring in the port folio.

Rp = Return on the Portfolio

X1 = Proportion of total portfolio invested in security 1

R1 = Expected return of Security 1

(OR)

Where:

Rp = The expected return on Portfolio

R1= The estimated return in Security 1

R2= The estimated return in Security 1

W1= Proportion of security 1 occurring in the port folio

W2 = Proportion of security 1 occurring in the port folio

2. Variance & Co-variance

The variance is a measure of how far a set of numbers is spread out. It is one of several descriptors of

a probability distribution, describing how far the numbers lie from the mean (expected value).

Co-variance

Covariance reflects the degree to which the returns of the two securities vary or change

together.

A positive covariance means that the returns of the two securities move in the same direction.

A negative covariance implies that the returns of the two securities move in opposite

direction