appraisal process reading material 1 ©joe walsh - do not distribute without explicit permission

TRANSCRIPT

Appraisal Process

Reading Material

1

©Joe Walsh - Do not distribute without explicit permission.

Reading and Resources• The Appraisal of Real Estate, 13th Edition, Appraisal

Institute, 2008 (on reserve)– Chapter 7, The Valuation Process– Chapter 12, Highest and Best Use Analysis, pp. 277-289

• Appraisal Terms handout

2

©Joe Walsh - Do not distribute without explicit permission.

Outline

• What drives property value?– The economics behind real estate value

• Why appraisals?– Estimating the value when it’s not readily apparent

• The Appraisal Process– Forensic investigation and analysis of market evidence– Value Opinion

• Appraisal Process – Step by Step

3

©Joe Walsh - Do not distribute without explicit permission.

Economics ofReal Estate Value

• Economic Entities (Firms) in an Economic System– Cash flow cycle based on production function of activities– Economic inputs: land, capital, labor and knowledge

• Real estate: land and capital (i.e. buildings)– Inputs have economic productivity/utility within the entity’s production function

(unique to entity and production function/use)– Assume firms and households seek to maximize utility/profit

• Urban economics– Physical geography and locational issues impact the firm’s production

function– Locational attributes of property impact productivity/utility of land and

buildings specific to a firm’s production function• Example: Bottling Plant

4

©Joe Walsh - Do not distribute without explicit permission.

Transactions vs. Appraisals• Markets (buyers and sellers) set value/prices through competitive bidding• Appraisers estimate value through forensic investigation and analysis of

data• Results of the bidding process are not observable

– Unique Properties– Infrequent Transactions– (Stocks vs. Real Estate)

• Appraisal is forensic investigation of market evidence in the absence of direct observation of values– Requires thorough understanding of the “process” by which buyers and sellers establish

values

5

©Joe Walsh - Do not distribute without explicit permission.

Appraisal Process

• Standardized methodology for estimating value– Rigorous, exhaustive approach to gathering and analyzing data– Applicable to all property types– Not formulaic, requires judgment, adaptation

6

©Joe Walsh - Do not distribute without explicit permission.

Appraisal Process• Step 1: Identification of the Problem• Step 2: Scope of Work Definition• Step 3: Data Collection and Property Description

– Market Area Data– Subject Property Data– Comparable Property Data

• Step 4: Data Analysis– Market Analysis– Highest and Best Use Analysis

• Step 5: Site Value Opinion• Step 6: Application of Approaches to Value

– Sales Comparison– Cost– Income Approach

• Step 7: Reconciliation of Value Indications and Final Opinion of Value• Step 8: Report of Defined Value

(See Appraisal of Real Estate, Figure 7.1, page 131)

7

©Joe Walsh - Do not distribute without explicit permission.

Step 1:Identification of the Problem

• Identify client and intended users– Disclosure and identification to avoid misunderstandings and

misuse of the analysis

8

©Joe Walsh - Do not distribute without explicit permission.

Step 1:Identification of the Problem

• Identify the intended use– Helps determine necessary scope of work

• Common Uses of Appraisals– Financing– Determine Listing Price– Supporting a Sales Price– Property Taxation– Condemnation Appraisal– Lease vs. Buy Decisions– New Project Feasibility– Litigation of Property Rights and Interests– Project Performance Measuring (Capital Appreciation)– Fire and Casualty Insurance

9

©Joe Walsh - Do not distribute without explicit permission.

Step 1:Identification of the Problem

• Value Definition and Purpose of the Assignment• Common Types of Value

– Market Value– Investment value– Value in Use– Assessed value– Insurable value– Going – Concern value– Salvage Value– Book Value– Mortgage Loan Value (no definition in handout)– Liquidation Value– Business Enterprise Value (added definition)

•

10

©Joe Walsh - Do not distribute without explicit permission.

11

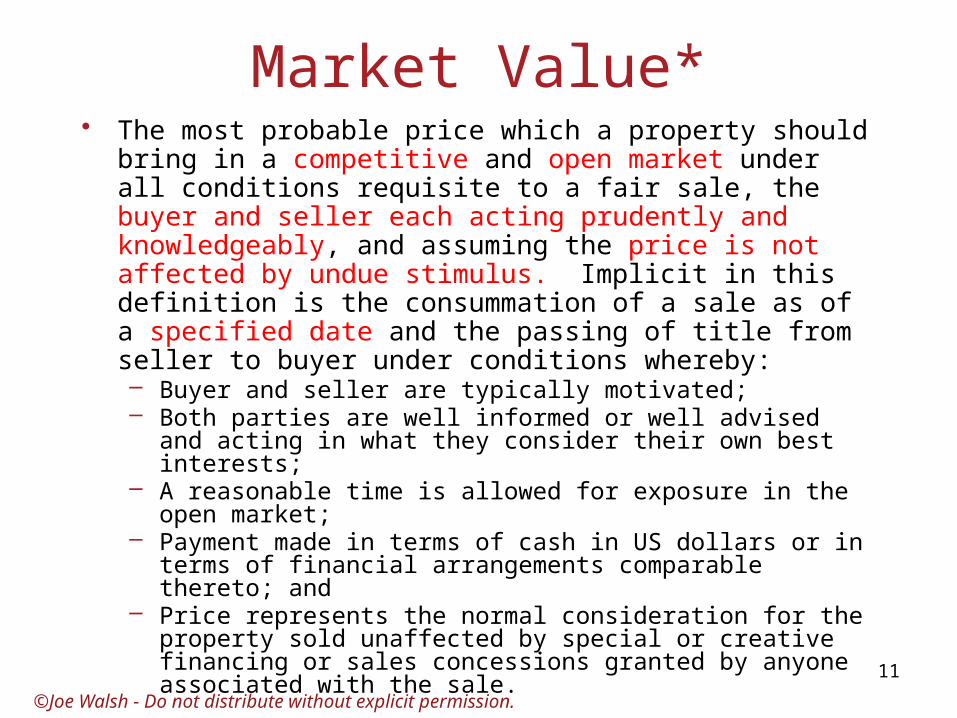

Market Value*• The most probable price which a property should bring in a

competitive and open market under all conditions requisite to a fair sale, the buyer and seller each acting prudently and knowledgeably, and assuming the price is not affected by undue stimulus. Implicit in this definition is the consummation of a sale as of a specified date and the passing of title from seller to buyer under conditions whereby: – Buyer and seller are typically motivated;– Both parties are well informed or well advised and acting in what

they consider their own best interests;– A reasonable time is allowed for exposure in the open market;– Payment made in terms of cash in US dollars or in terms of

financial arrangements comparable thereto; and– Price represents the normal consideration for the property sold

unaffected by special or creative financing or sales concessions granted by anyone associated with the sale.

• * Definition of “market value” used by agencies that regulate federally insured financial institutions in the United States. The Dictionary of Real Estate Appraisal, Fourth Edition, Appraisal Institute, 2002.

©Joe Walsh - Do not distribute without explicit permission.

Step 1:Identification of the Problem

• Identify the Effective Date of Value– Current date – most typical– As of completion of construction– As of stabilization– As of historic date – perhaps for litigation appraisal– As of effective date of taking – eminent domain appraisal

• Why does the date matter?– Value changes with time– Appraisal is snapshot of value at single point in time

12

©Joe Walsh - Do not distribute without explicit permission.

Step 1:Identification of the Problem

• Identification of Property Characteristics– Legal description– Identification of Property Rights

• Fee simple• Leased fee interest• Leasehold interest• Sub-leasehold interest• Sandwich interest• Easement• Life estate• Condominium ownership• Cooperative ownership• Timeshare

13

©Joe Walsh - Do not distribute without explicit permission.

Step 1:Identification of the Problem

• Assignment Conditions – Extraordinary Assumptions– An assumption which, if found to be false, could alter the appraisers opinion or

conclusions (See definitions)– For example, in appraising new construction, the appraisal assignment may

require estimating the value of the property upon completion. The appraiser would assume that construction will be completed as planned at a specific date.

• Assignment Conditions – Hypothetical Conditions – An assumption contrary to what actually exists but is supposed for the purpose of

analysis. (See definitions)– For example, for litigation purposes, the appraisal assignment may require

estimating the value of a property if an adjacent property had been built.

14

©Joe Walsh - Do not distribute without explicit permission.

Step 1:Identification of the Problem

• Limiting Conditions and Assumptions– Assumptions made by the appraiser beyond their level of expertise or scope that

may have an impact on the value of property is different than assumed– Limitations on the use or reliance of the report– In effect, they are “extraordinary assumptions” to limit appraisers liability

• Typical assumptions include– Legal description is accurate– Property title is free and clear of liens and encumbrances– Competent management– Engineering studies are correct– No hidden or other unapparent conditions– Property is in compliance with applicable laws– Property conforms to zoning– Licenses, certificates of occupancy, consents and other permits in place– No hazardous materials or environmental contamination

15

©Joe Walsh - Do not distribute without explicit permission.

Step 1:Identification of the Problem

• Typical limiting conditions include;– Reliance limited to client and purpose– Reliance on allocation of value to components– Limited rights regarding publication– Opinion of value applied to entire property valued, with no reliance on

pro ration or division of interests– Forecast based on current market conditions

16

©Joe Walsh - Do not distribute without explicit permission.

Step 2:Scope of Work Definition

• Description of Scope of Appraisal– A brief description of the amount and type of information

research and analysis applied in an assignment– Includes information regarding

• Property inspection date and details of inspection• Area search to gather data• Degree of completeness of analysis• Names and experience of personnel performing appraisal

17

©Joe Walsh - Do not distribute without explicit permission.

Step 3: Data Collection and Property Description

• Market analysis– General regional economic trends– Demand trends for property types– Supply trend for property types– Market rents and vacancy for various property uses

18

©Joe Walsh - Do not distribute without explicit permission.

Step 3: Data Collection and Property Description

• Site data– Definition of site boundaries – legal description– Zoning and land-use information– Physical characteristics of site– Utilities and infrastructure– Characteristics of adjacent property and neighborhood

• Improvement data– Structural description– Spatial layout– Equipment and mechanical systems– Architectural style– Functional utility– Quality and condition– Deferred maintenance

19

©Joe Walsh - Do not distribute without explicit permission.

Step 3: Data Collection and Property Description

• Comparable property data– Income approach

• Rent/Lease comparables• Operating expense comparables• Capitalization rate comparables

– Sales comparison approach• Sale comparables

– Cost approach• Land sales comparables

20

©Joe Walsh - Do not distribute without explicit permission.

Step 4: Data AnalysisMarket Analysis

• Supply, Demand and Marketability Studies• Conclusions, specific to subject property:

– Market Rent– Vacancy and absorption expectations

21

©Joe Walsh - Do not distribute without explicit permission.

Step 4: Data AnalysisHighest and Best Use Analysis

• Economics– Firms are profit maximizing – Landlords/Sellers seek highest price– Competitive bidding of alternative uses establishes prices– “Winning” use reflects the use having greatest productivity/utility of property– Subject to physical and legal constraints

• Filtering Process– Physically possible– Legally permissible– Financially feasible– Maximally productive (i.e. highest price)

• Two fundamentally different Options/Scenarios– HBU is continued use of property as built (as improved), or– HBU is to demolish improvement and build something else (as if vacant)

22

©Joe Walsh - Do not distribute without explicit permission.

Step 4: Data AnalysisHighest and Best Use Analysis

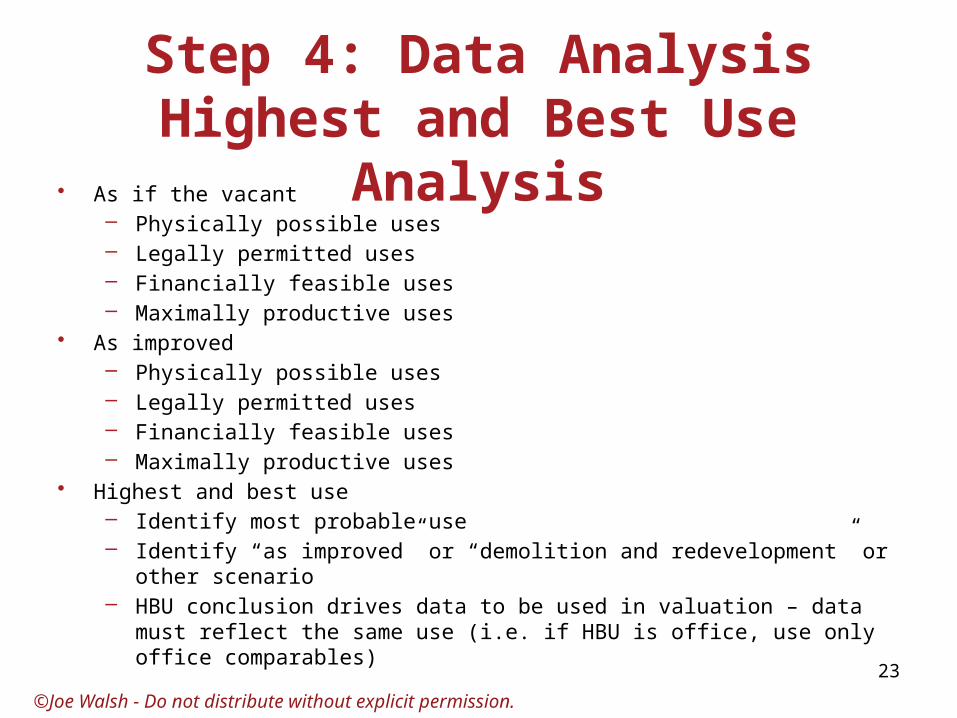

• As if the vacant– Physically possible uses– Legally permitted uses– Financially feasible uses– Maximally productive uses

• As improved– Physically possible uses– Legally permitted uses– Financially feasible uses– Maximally productive uses

• Highest and best use– Identify most probable use– Identify “as improved” or “demolition and redevelopment” or other scenario– HBU conclusion drives data to be used in valuation – data must reflect the same

use (i.e. if HBU is office, use only office comparables)

23

©Joe Walsh - Do not distribute without explicit permission.

Step 5: Site Value Opinion• Purpose

– Necessary for HBU analysis– Necessary for cost approach

• Approaches– Sales comparison– Extraction– Allocation– Subdivision development– Land residual– Ground rent capitalization

24

©Joe Walsh - Do not distribute without explicit permission.

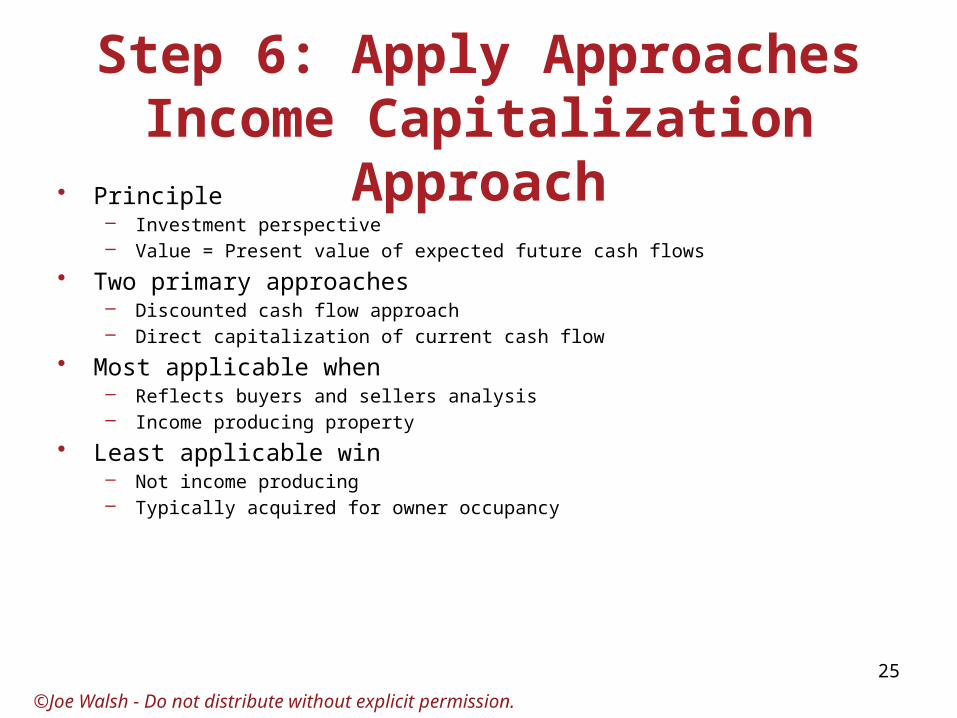

Step 6: Apply ApproachesIncome Capitalization Approach

• Principle– Investment perspective– Value = Present value of expected future cash flows

• Two primary approaches– Discounted cash flow approach– Direct capitalization of current cash flow

• Most applicable when– Reflects buyers and sellers analysis– Income producing property

• Least applicable win– Not income producing– Typically acquired for owner occupancy

25

©Joe Walsh - Do not distribute without explicit permission.

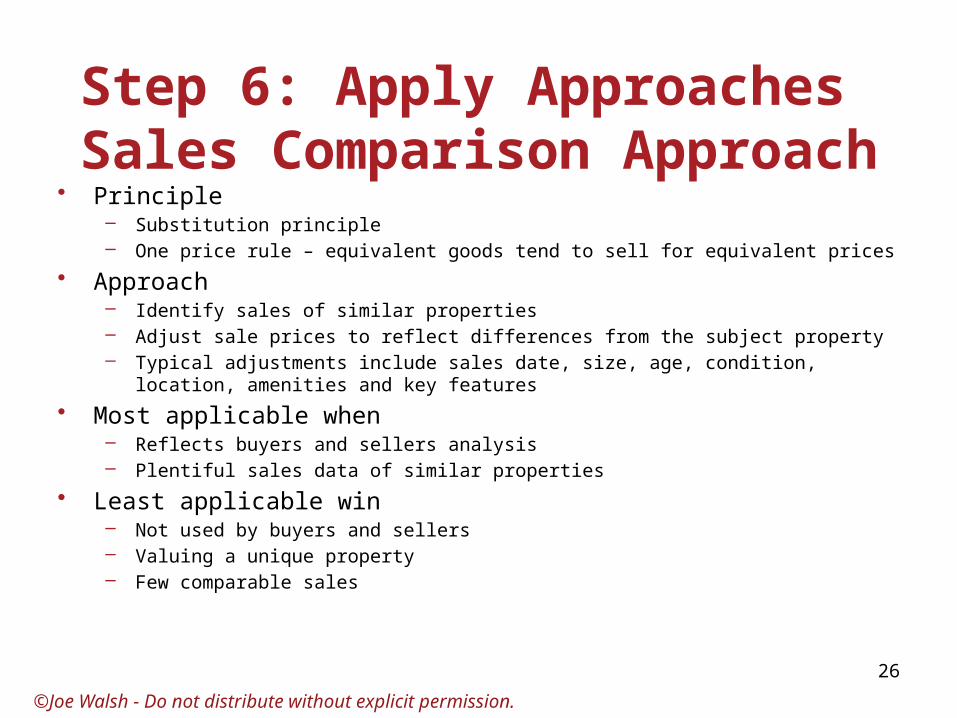

Step 6: Apply Approaches Sales Comparison Approach

• Principle– Substitution principle– One price rule – equivalent goods tend to sell for equivalent prices

• Approach– Identify sales of similar properties– Adjust sale prices to reflect differences from the subject property– Typical adjustments include sales date, size, age, condition, location, amenities and key

features

• Most applicable when– Reflects buyers and sellers analysis– Plentiful sales data of similar properties

• Least applicable win– Not used by buyers and sellers– Valuing a unique property– Few comparable sales

26

©Joe Walsh - Do not distribute without explicit permission.

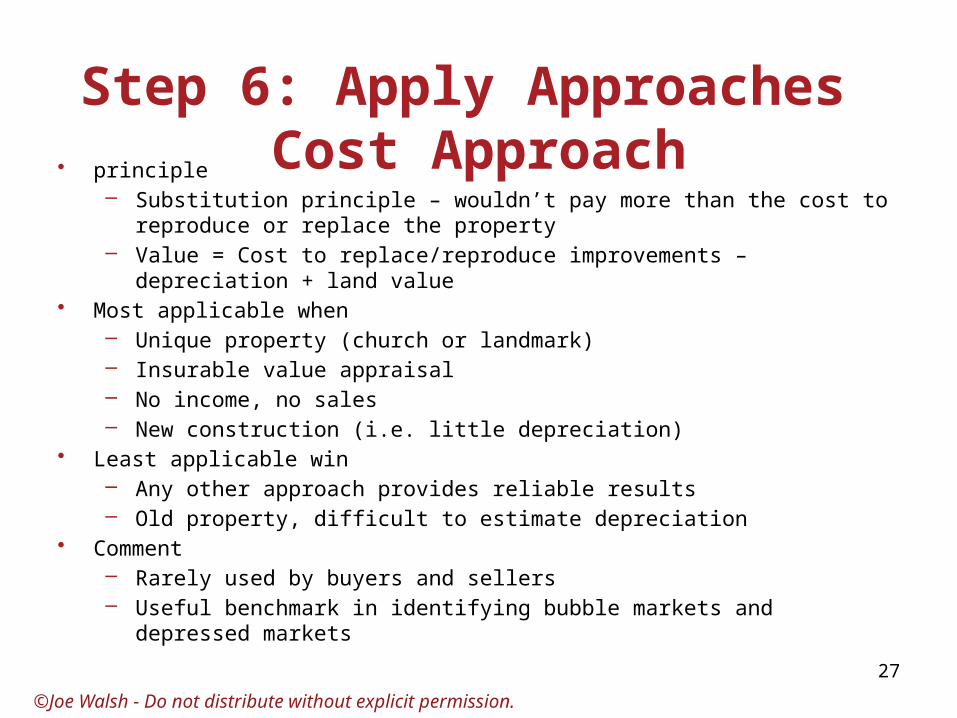

Step 6: Apply Approaches Cost Approach• principle

– Substitution principle – wouldn’t pay more than the cost to reproduce or replace the property

– Value = Cost to replace/reproduce improvements – depreciation + land value• Most applicable when

– Unique property (church or landmark)– Insurable value appraisal– No income, no sales– New construction (i.e. little depreciation)

• Least applicable win– Any other approach provides reliable results– Old property, difficult to estimate depreciation

• Comment– Rarely used by buyers and sellers– Useful benchmark in identifying bubble markets and depressed markets

27

©Joe Walsh - Do not distribute without explicit permission.

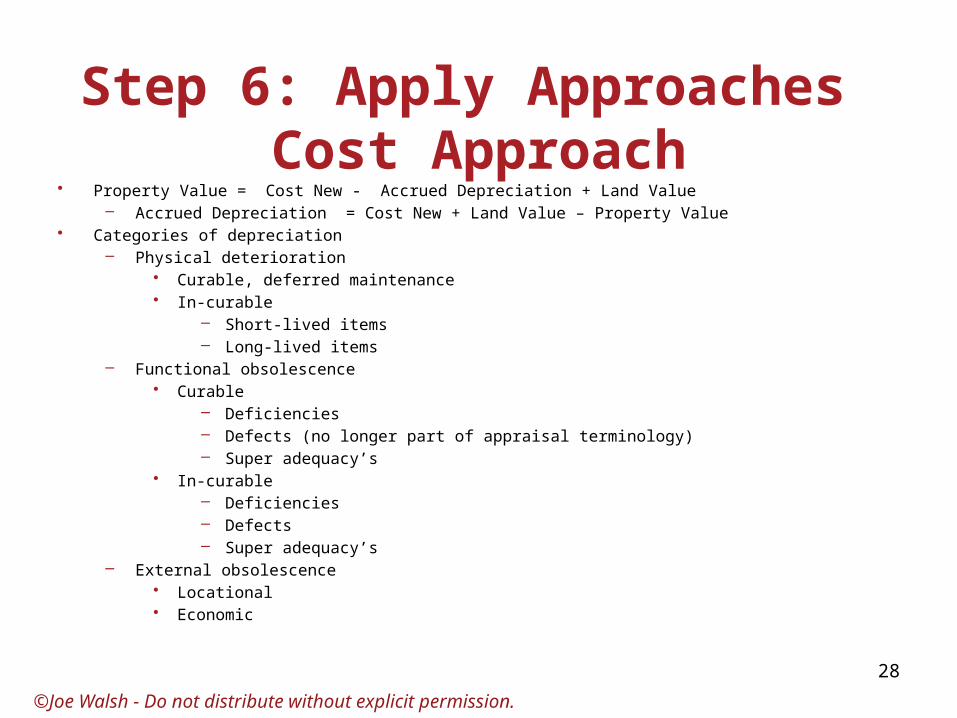

Step 6: Apply Approaches Cost Approach

• Property Value = Cost New - Accrued Depreciation + Land Value– Accrued Depreciation = Cost New + Land Value – Property Value

• Categories of depreciation– Physical deterioration

• Curable, deferred maintenance• In-curable

– Short-lived items– Long-lived items

– Functional obsolescence• Curable

– Deficiencies– Defects (no longer part of appraisal terminology)– Super adequacy’s

• In-curable– Deficiencies– Defects– Super adequacy’s

– External obsolescence• Locational• Economic

28

©Joe Walsh - Do not distribute without explicit permission.

Step 7: Reconciliation andFinal Opinion of Value

• Three approaches => Potentially three different value indications• Distribution curve, value range, or single value estimate?

– Economic reality => competitive bidding process that sets price in an imperfect market suggests a probabilistic range of values

• Normal or other distribution curve

– Business Reality => most appraisal assignments require a single value estimate• Most probable price – single value estimate

• Appraiser’s Judgment– “Direct Results” vs. “Process”– Methodology used by buyers and sellers in the market– Quantity, quality and reliability of data used in each approach– Understanding of economic drivers of value in the market

29

©Joe Walsh - Do not distribute without explicit permission.

Step 7: Reconciliation andFinal Opinion of Value

• “Direct Results”– What was the direct “result” from the market?– Use direct evidence from the market (e.g. the last 3 buildings

warehouses sold at prices ranging from $41.50 to $43.00psf)– Given good direct “results” data, a more reliable approach

• Ex. Litigation work• “Process”

– What methodology do buyers and sellers use in determining prices?

– Duplicate their “process” (e.g. DCF results in a value of $X) to estimate value

– Prone to errors in the estimates• Ex. Rent spikes

30

©Joe Walsh - Do not distribute without explicit permission.

Step 8: Appraisal Report

• Written* presentation of data analysis and results

• Report standards conform to scope and purpose of the appraisal– USPAP – Uniform Standards of Professional Appraisal Practice

• * Appraisals can be presented orally, but, as with legal contracts, generally not a good idea

31

©Joe Walsh - Do not distribute without explicit permission.