appendix 2 appendix 2 28/08/2017 shire of collie khushwant ... · eft21395 07/07/2017 ingal civil...

TRANSCRIPT

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 128/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIAUSTRALIA POSTAP1 - AUSTRALIA POST24/07/2017 3,893.41JUL17

BENMUNIFINES ENFORCEMENT FEESFF1 - FINES ENFORCEMENT FEES25/07/2017 236.00JUL17

BENMUNIFINES ENFORCEMENT FEESFF1 - FINES ENFORCEMENT FEES28/07/2017 236.00JUL17

BENMUNIBANK FEESBF1 - BANK FEES31/07/2017 1,183.59JUL17

BENMUNIBOQ FINANCE-COMPUTER LEASEBQ1 - BOQ FINANCE-COMPUTER LEASE03/07/2017 3,729.76JUL17

BENMUNISCOPE-ADMIN COLOUR COPIER ($566.50)SC1 - SCOPE-ADMIN COLOUR COPIER ($566.50)

03/07/2017 566.50JUL17

BENMUNICAPITAL FINANCE-LIBRARY COPIER ($231.00)WM2 - CAPITAL FINANCE-LIBRARY COPIER ($231.00)

03/07/2017 231.00JUL17

BENMUNICANON FINANCE- ADMIN B&W COPIER LEASE ($233.20)CF1 - CANON FINANCE- ADMIN B&W COPIER LEASE ($233.20)

12/07/2017 233.20JUL17

BENMUNIFINES ENFORCEMENT FEESFF1 - FINES ENFORCEMENT FEES17/07/2017 59.00JUL17

BENMUNIKONICA-DEPOT COPIER LEASE ($115.50)KM1 - KONICA-DEPOT COPIER LEASE ($115.50)

19/07/2017 115.50JUL17

BENMUNICAPITAL FINANCE-ROCHE PARK COPIER ($123.23)WM1 - CAPITAL FINANCE-ROCHE PARK COPIER ($123.23)

21/07/2017 123.23JUL17

BENMUNIFINES ENFORCEMENT FEESFF1 - FINES ENFORCEMENT FEES21/07/2017 413.00JUL17

BENTRUSTPayment on behalf of Collie River Valley Visitor Centre for invoice A3799 - T465

Pak-it Computers20/07/2017 1,222.003140

BENTRUSTPayment on behalf of Collie River Valley Visitor Centre for invoice A3799 - T465

Pak-it Computers26/06/2017INV A3799 1,222.00

BENMUNICOMMISSIONS AND COSTS FOR DEBT RECOVERY - DEBTORS

AMPAC Debt Recovery (WA) Pty Ltd07/07/2017 902.00EFT21384

BENMUNICOMMISSIONS AND COSTS FOR DEBT RECOVERY - DEBTORS

AMPAC Debt Recovery (WA) Pty Ltd31/05/2017INV 39487 902.00

BENMUNIBCITF PAYMENT JUNE 2017BUILDING & CONSTRUCTION INDUSTRY07/07/2017 931.16EFT21385

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 228/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIBCITF PAYMENT JUNE 2017, BCITF COMMISSION JUNE 2017BUILDING & CONSTRUCTION INDUSTRY04/07/2017INV JUNE 17 931.16

BENMUNIBRB PAYMENT JUNE 2017BUILDING COMMISSION07/07/2017 1,040.70EFT21386

BENMUNIBRB PAYMENT JUNE 2017, BRB PAYMENT JUNE 2017BUILDING COMMISSION04/07/2017INV JUNE17 1,040.70

BENMUNITo supply PA system for Australia Day Award Ceremony on 26 January 2017.

B-TECH ELECTRONIC ENGINEERING07/07/2017 300.00EFT21387

BENMUNITo supply PA system for Australia Day Award Ceremony on 26 January 2017.

B-TECH ELECTRONIC ENGINEERING28/01/2017INV 20170899 300.00

BENMUNIReplacement wet weater jacket and vest due to damage to existing jacket

PETE'S07/07/2017 114.80EFT21388

BENMUNIReplacement wet weater jacket and vest due to damage to existing jacket

PETE'S06/06/2017INV 198887 114.80

BENMUNIReplace turntable jaws CO30167COLLIE TYRE & EXHAUST CENTRE07/07/2017 340.00EFT21389

BENMUNIPuncture repair to CO30167 Mitsubishi Prime Mover,COLLIE TYRE & EXHAUST CENTRE09/12/2016INV 00009339 50.00

BENMUNIReplace turntable jaws CO30167COLLIE TYRE & EXHAUST CENTRE23/01/2017INV 00009684 290.00

BENMUNICCTV maintenance and support, Wi-Fi internet to Central Park and Skate Park, Wi-Fi network maintenance and support to 31 August 2017.

CIPHERTEL07/07/2017 14,826.85EFT21390

BENMUNIReplacement lens/clean for CCTV cameraCIPHERTEL07/06/2017INV 00013100 220.00

BENMUNICCTV maintenance and support, Wi-Fi internet to Central Park and Skate Park, Wi-Fi network maintenance and support to 31 August 2017.,

CIPHERTEL07/06/2017INV 00013098 7,698.85

BENMUNIOutdoor Ruggedised high definition PTZ IP video camera x18 optical zoom - quote 13050v1.0

CIPHERTEL07/06/2017INV 00013050 6,468.00

BENMUNITraining for CCTV network useCIPHERTEL07/06/2017INV 00013099 440.00

BENMUNICleaning of public toilets and BBQ's for June 2017DAVES CLEANING SERVICE07/07/2017 5,930.00EFT21391

BENMUNICleaning of public toilets and BBQ's for June 2017DAVES CLEANING SERVICE01/07/2017INV 16 5,930.00

BENMUNICompletion of videography from opening night at Central Park and additional footage of new projects undertaken through the supertown project to be supplied on usb for Shire future use.

Drone and Dragons07/07/2017 1,000.00EFT21392

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 328/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNICompletion of videography from opening night at Central Park and additional footage of new projects undertaken through the supertown project to be supplied on usb for Shire future use.

Drone and Dragons30/06/2017INV 0017 1,000.00

BENMUNILEASE/RENTAL AGREEMENT REF C5076A9443 SHIRE ADMIN COPIER 16/7/17-15/8/17

FUJI XEROX AUSTRALIA PTY LTD07/07/2017 410.30EFT21393

BENMUNILEASE/RENTAL AGREEMENT REF C5076A9443 SHIRE ADMIN COPIER 16/7/17-15/8/17

FUJI XEROX AUSTRALIA PTY LTD21/06/2017INV QA944305 410.30

BENMUNIDoor lock - Maintenance Technician's workshopHENDERSON HARDWARE07/07/2017 37.50EFT21394

BENMUNIDoor lock - Maintenance Technician's workshopHENDERSON HARDWARE31/05/2017INV 224376 37.50

BENMUNI1 x C1050G fishtail end1 x C1060G bullnose endCo-op bridge

INGAL CIVIL PRODUCTS07/07/2017 154.00EFT21395

BENMUNI1 x C1050G fishtail end, 1 x C1060G bullnose end, Co-op bridgeINGAL CIVIL PRODUCTS09/05/2017INV 7039725 154.00

BENMUNIHire of room for community focus group to discuss the Positive Ageing Plan for the Shire of Collie on 22 September 2016.

NGALANG BOODJA COUNCIL ABORIGINAL CORP.

07/07/2017 120.00EFT21396

BENMUNIHire of room for community focus group to discuss the Positive Ageing Plan for the Shire of Collie on 22 September 2016.

NGALANG BOODJA COUNCIL ABORIGINAL CORP.

22/12/2016INV 1 120.00

BENMUNISHIRE OFFICE PREVENTATIVE SERVICE PLAN AND HELP DESK SUPPORT FOR MAY 2017

SCOPE BUSINESS IMAGING07/07/2017 1,637.15EFT21397

BENMUNISHIRE OFFICE PREVENTATIVE SERVICE PLAN AND HELP DESK SUPPORT FOR MAY 2017

SCOPE BUSINESS IMAGING31/05/2017INV 390324 1,637.15

BENMUNIHarmony Day signage in Central Park - as per information emailed.Existing sign to be re-skinned and erected prior to friday 9 March 2017.

Collie SignFX07/07/2017 302.50EFT21398

BENMUNIUpdating of honour boards for sport awards recipients.Collie SignFX28/03/2017INV INV-2172 27.50

BENMUNIHarmony Day signage in Central Park - as per information emailed., Existing sign to be re-skinned and erected prior to friday 9 March 2017.

Collie SignFX16/03/2017INV INV-2154 275.00

BENMUNI2 x face painters for Australia Day family entertainment and outdoor cinema evening and Harmony Day.

Stacie Skoda07/07/2017 320.00EFT21399

BENMUNI2 x face painters for Australia Day family entertainment and outdoor cinema evening and Harmony Day.

Stacie Skoda30/06/2017INV 300617 320.00

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 428/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIAlison Kononen clothing allowance 2016-17 - items from Totally Workwear

TOTALLY WORKWEAR BUNBURY07/07/2017 348.70EFT21400

BENMUNIAlison Kononen clothing allowance 2016-17 - items from Totally Workwear

TOTALLY WORKWEAR BUNBURY23/03/2017INV 007100188333 348.70

BENMUNIPHOTOCOPIER SES FORREST STREET 03/04/17-02/05/17WEST COUNTRY PRINT SYNC07/07/2017 114.72EFT21401

BENMUNIPHOTOCOPIER SES FORREST STREET 03/04/17-02/05/17WEST COUNTRY PRINT SYNC02/05/2017INV WA00334379 114.72

BENMUNI1 tonne bulka bags of wicket soilWESTERN AUSTRALIAN CRICKET ASSOCIATION

07/07/2017 5,610.00EFT21402

BENMUNI1 tonne bulka bags of wicket soilWESTERN AUSTRALIAN CRICKET ASSOCIATION

30/06/2017INV WFTI000487 5,610.00

BENMUNIWork clothing for Krys RobertsJacket, Jumper & blouse

PETE'S13/07/2017 184.00EFT21403

BENMUNIWork clothing for Krys Roberts, Jacket, Jumper & blousePETE'S06/06/2017INV 198909 184.00

BENMUNIEMPTY ORGANIC BINS JUNE 2017CLEANAWAY13/07/2017 34,931.92EFT21404

BENMUNIEMPTY WASTE BINS JUNE 2017, EMPTY ORGANIC BINS JUNE 2017, EMPTY RECYCLE BINS JUNE 2017

CLEANAWAY30/06/2017INV 9755589 33,871.09

BENMUNIRECYCLE BINS JUNE 2017CLEANAWAY30/06/2017INV 9751578 239.95

BENMUNIREPLACEMENT WASTE BINS AND DELIVERY JUNE 2017, REPLACEMENT ORGANIC BINS AND DELIVERY JUNE 2017, REPLACEMENT RECYCLE BINS AND DELIVERY JUNE 2017

CLEANAWAY30/06/2017INV 9755590 820.88

BENMUNISize D Rent on Acetylene Bottle 29/5/17-27/6/17BOC LIMITED13/07/2017 15.00EFT21405

BENMUNISize D Rent on Acetylene Bottle 29/5/17-27/6/17, Size C Rent on Acetylene Bottle 29/5/17-27/6/17

BOC LIMITED28/06/2017INV 4016491642 15.00

BENMUNIGROUP FITNESS INSTRUCTOR MUSIC KITS - REIMBURSEMENT

Deanne Lawrence13/07/2017 179.50EFT21406

BENMUNIGROUP FITNESS INSTRUCTOR MUSIC KITS - REIMBURSEMENT

Deanne Lawrence26/06/2017INV 260617 179.50

BENMUNI12 month renewal of Exterra termite protection system for 2017/18.GOLDEN WEST PEST & WEED CONTROL13/07/2017 880.00EFT21407

BENMUNI12 month renewal of Exterra termite protection system for 2017/18.GOLDEN WEST PEST & WEED CONTROL28/06/2017INV 2528 880.00

BENMUNICheck weight limiter switchGLOBAL AUTO ELECTRICAL AND AIR CONDITIONING SERVICES PTY LTD

13/07/2017 99.00EFT21408

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 528/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNICheck weight limiter switchGLOBAL AUTO ELECTRICAL AND AIR CONDITIONING SERVICES PTY LTD

23/02/2017INV 00006839 99.00

BENMUNIREIMBURSE UNIFORM 2016-2017ELFI JAMES13/07/2017 49.00EFT21409

BENMUNIREIMBURSE UNIFORM 2016-2017ELFI JAMES29/06/2017INV 290617 49.00

BENMUNIJUNIOR PROGRAM UMPIRINGJames Abbott13/07/2017 22.50EFT21410

BENMUNIJUNIOR PROGRAM UMPIRINGJames Abbott10/07/2017INV 100717 22.50

BENMUNIUNIFORM REIMBURSEMENT FOR 2016-2017JANET PATMORE13/07/2017 211.81EFT21411

BENMUNIUNIFORM REIMBURSEMENT FOR 2016-2017JANET PATMORE30/06/2017INV 300617 211.81

BENMUNIREIMBURSEMENT OF AIBS REGISTRATION MEMBER RENEWAL

LES CRAKE13/07/2017 499.00EFT21412

BENMUNIREIMBURSEMENT OF AIBS REGISTRATION MEMBER RENEWAL

LES CRAKE12/07/2017INV 120717 499.00

BENMUNIBusiness copying music licence - Z for period 1/7/2017 to 30/6/2018PHONOGRAPHIC PERFORMANCE COMPANY OF AUSTRALIA

13/07/2017 141.84EFT21413

BENMUNIBusiness copying music licence - Z for period 1/7/2017 to 30/6/2018PHONOGRAPHIC PERFORMANCE COMPANY OF AUSTRALIA

01/06/2017INV 3035831 141.84

BENMUNICharger and rechargable batteriesCOLLIE BETTA HOME LIVING13/07/2017 228.00EFT21414

BENMUNICharger and rechargable batteriesCOLLIE BETTA HOME LIVING22/05/2017INV 10077217 228.00

BENMUNIChain sharpener chain guideCOLLIE MOWERS AND MORE13/07/2017 296.20EFT21415

BENMUNIRectify BT121 auger run faultCOLLIE MOWERS AND MORE08/06/2017INV 72677 141.20

BENMUNIChain sharpener chain guideCOLLIE MOWERS AND MORE10/06/2017INV 72754 155.00

BENMUNI15 x Boxes A4 Reflex White Photocopier PaperSTAPLES AUSTRALIA13/07/2017 1,148.99EFT21416

BENMUNI15 x Boxes A4 Reflex White Photocopier PaperSTAPLES AUSTRALIA12/05/2017INV 9021155732 411.84

BENMUNI10 x Boxes of Reflex A4 Photocopier Paper, 3 x Reams of Reflex A3 Photocopier Paper

STAPLES AUSTRALIA13/04/2017INV 9020934772 325.31

BENMUNI15 x Boxes of A4 Reflex White Photocopier Paper.STAPLES AUSTRALIA13/06/2017INV 9021423062 411.84

BENMUNIWA Ranger Association Polo ShirtWA RANGER SERVICES13/07/2017 37.40EFT21417

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 628/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIWA Ranger Association Polo ShirtWA RANGER SERVICES31/08/2016INV 71 37.40

BENMUNIPayroll deductionsAUSTRALIAN SERVICES UNION17/07/2017 411.75EFT21418

Payroll Deduction for DAVID THOMAS ADDISON 11/07/2017, Payroll Deduction for JOHN ANTONI BAJOR 11/07/2017, Payroll Deduction for MAURICE LEO DHUE 11/07/2017, Payroll Deduction for HELENA ANNA GRYCZALOWSKI 11/07/2017, Payroll Deduction for ALEC SUTHERLAND 11/07/2017, Payroll Deduction for BRIAN JOHN MACINTYRE 11/07/2017, Payroll Deduction for STEPHEN GREGORY BOARD 11/07/2017, Payroll Deduction for MARK PIAVANINI 11/07/2017, Payroll Deduction for GARY BISHOP 11/07/2017, Payroll Deduction for SHANNON BARBER 11/07/2017, Payroll Deduction for DAYLE LYNETTE HOLLINS 11/07/2017, Payroll Deduction for PETER MILES 11/07/2017, Payroll Deduction for CHRISTINE SZOSTAK 11/07/2017, Payroll Deduction for STEVEN CRUICKSHANK 11/07/2017, Payroll Deduction for FRANCIS JOHN BECKER 11/07/2017

AUSTRALIAN SERVICES UNION11/07/2017INV DEDUCTION 411.75

BENMUNIPayroll deductionsCHILD SUPPORT AGENCY17/07/2017 701.00EFT21419

Payroll Deduction 11/07/2017, Payroll Deduction 11/07/2017, Payroll Deduction 11/07/2017

CHILD SUPPORT AGENCY11/07/2017INV DEDUCTION 701.00

BENMUNIAPRA music licencing for period1/7/2017 to 30/9/2017AUSTRALASIAN PERFORMING RIGHT ASSOCIATION LIMITED

20/07/2017 388.08EFT21420

BENMUNIAPRA music licencing for period1/7/2017 to 30/9/2017AUSTRALASIAN PERFORMING RIGHT ASSOCIATION LIMITED

28/06/2017INV 02299663/00013 388.08

BENMUNIManufacture 6mm x 10m winch line with thimble on one endBULLIVANTS20/07/2017 217.80EFT21421

BENMUNIManufacture 6mm x 10m winch line with thimble on one endBULLIVANTS16/06/2017INV DMI400701039 217.80

BENMUNI12 x small to medium sized shacklesStatewide Bearings20/07/2017 99.00EFT21422

BENMUNI12 x small to medium sized shacklesStatewide Bearings19/06/2017INV INV2484400 99.00

BENMUNI20 x plough bolts and nutsCoalfields Wearparts Pty Ltd20/07/2017 110.00EFT21423

BENMUNI20 x plough bolts and nutsCoalfields Wearparts Pty Ltd15/06/2017INV 00001582 110.00

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 728/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNISHIRE OF COLLIE WEBSITE : I"M ALERT FOOD SAFETY PROGRAM: 1/7/17 - 30/6/18

Environmental Health Australia (New South Wales) Incorporated

20/07/2017 550.00EFT21424

BENMUNISHIRE OF COLLIE WEBSITE : I"M ALERT FOOD SAFETY PROGRAM: 1/7/17 - 30/6/18

Environmental Health Australia (New South Wales) Incorporated

15/06/2017INV 1371 550.00

BENMUNIRepair work light to Hino Truck CO17693GLOBAL AUTO ELECTRICAL AND AIR CONDITIONING SERVICES PTY LTD

20/07/2017 722.74EFT21425

BENMUNICarry out diagnostics with laptop and rectifyGLOBAL AUTO ELECTRICAL AND AIR CONDITIONING SERVICES PTY LTD

15/06/2017INV 00007690 222.20

BENMUNIRepair work light to Hino Truck CO17693, 3 x find fault with trailers supply 3 x Trailer 7 pin plugs for (1TIR794, 1TNN796, 1TAJ796)

GLOBAL AUTO ELECTRICAL AND AIR CONDITIONING SERVICES PTY LTD

16/06/2017INV 00007702 500.54

BENMUNIREIMBURSEMENT TO REPLACE FLAT/BALD TYRE - 106CO - BOB JANE T-MARTS INVOICE 95672

GEOFF KLEM20/07/2017 195.00EFT21426

BENMUNIREIMBURSEMENT TO REPLACE FLAT/BALD TYRE - 106CO - BOB JANE T-MARTS INVOICE 95672

GEOFF KLEM04/07/2017INV 040717 195.00

BENMUNIReplace two tyresIAN GUPPY & CO SMASH REPAIRS20/07/2017 945.40EFT21427

BENMUNIInsurance excess 117CO, Replace two tyresIAN GUPPY & CO SMASH REPAIRS21/06/2017INV 58346 945.40

BENMUNIREIMBURSE PAYMENT FOR GAS BOTTLES PURCHASED TO REPLACE STOLEN BOTTLES AT CHANGE ROOMS NEAR VELODROME AS PER INSTRUCTIONS FROM DAVID BLURTON

JEFF SHEPPARD20/07/2017 250.00EFT21428

BENMUNIREIMBURSE PAYMENT FOR GAS BOTTLES PURCHASED TO REPLACE STOLEN BOTTLES AT CHANGE ROOMS NEAR VELODROME AS PER INSTRUCTIONS FROM DAVID BLURTON

JEFF SHEPPARD15/07/2017INV 150717 250.00

BENMUNI1 x 7021284 water valve1 x 7021286 coil

Bucher Municipal20/07/2017 194.98EFT21429

BENMUNI1 x 7021284 water valve, 1 x 7021286 coilBucher Municipal16/06/2017INV 863796 194.98

BENMUNI6 x chainsaw chains (4 x polesaw, 1 x 441 and 1 x 066)COLLIE MOWERS AND MORE20/07/2017 706.10EFT21430

BENMUNISet of Blades for Victa mowerCOLLIE MOWERS AND MORE16/06/2017INV 72949 19.00

BENMUNI6 x chainsaw chains (4 x polesaw, 1 x 441 and 1 x 066)COLLIE MOWERS AND MORE19/06/2017INV 73006 265.60

BENMUNI5 litre Stihl HP Ultra two stroke oilCOLLIE MOWERS AND MORE23/05/2017INV 72146 146.00

BENMUNI5 litre Stihl HP Ultra two stroke oilCOLLIE MOWERS AND MORE18/05/2017INV 71987 74.50

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 828/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNI5 litre Stihl HP Ultra two stroke oilCOLLIE MOWERS AND MORE18/05/2017INV 71982 92.00

BENMUNIBlade Sharpen HS 45 for Parks and GardensCOLLIE MOWERS AND MORE19/05/2017INV 72036 109.00

BENMUNITint office windows due glare in officesCollie SignFX20/07/2017 610.00EFT21431

BENMUNITint office windows due glare in officesCollie SignFX19/06/2017INV INV-2376 610.00

BENMUNIFuel Cap for Isuzu Water CartSouthwest Isuzu20/07/2017 82.29EFT21432

BENMUNIFuel Cap for Isuzu Water CartSouthwest Isuzu16/06/2017INV 518947 82.29

BENMUNI20 litre drums of add blue AQUEOUS UREA SOLUTIONTRUCKLINE20/07/2017 151.05EFT21433

BENMUNI20 litre drums of add blue AQUEOUS UREA SOLUTIONTRUCKLINE20/06/2017INV 5988736 151.05

BENMUNI12.5 80-18 (16ply) tyresTYREPOWER20/07/2017 1,670.00EFT21434

BENMUNICall out - replace truck tyreTYREPOWER16/06/2017INV 3207345 470.00

BENMUNITwo replacement batteries for jump starterTYREPOWER15/06/2017INV 3207238 380.00

BENMUNI12.5 80-18 (16ply) tyresTYREPOWER20/06/2017INV 3207487 820.00

BENMUNIGFEE FOR PERIOD ENDING 30 JUNE 2017WA TREASURY CORPORATION20/07/2017 4,619.08EFT21435

BENMUNIGFEE FOR PERIOD ENDING 30 JUNE 2017, GFEE FOR PERIOD ENDING 30 JUNE 2017, GFEE FOR PERIOD ENDING 30 JUNE 2017, GFEE FOR PERIOD ENDING 30 JUNE 2017, GFEE FOR PERIOD ENDING 30 JUNE 2017

WA TREASURY CORPORATION30/06/2017INV GFEE JUN17 4,619.08

BENMUNIJune 2017 rental on Air Liquide gas bottles Size D, E & GAIR LIQUIDE WA PTY LTD27/07/2017 75.68EFT21436

BENMUNIJune 2017 rental on Air Liquide gas bottles Size D, E & GAIR LIQUIDE WA PTY LTD30/06/2017INV UB4323 75.68

BENMUNIACQUITTAL AUDIT OF FINAL REPORT - COLLIE CBD REVITALISATION PROJECT - 000-0432-1 FOR THE YEAR PERIOD ENDED 30 JUNE 2017

AMD AUDIT & ASSURANCE PTY LTD27/07/2017 2,750.00EFT21437

BENMUNIACQUITTAL AUDIT OF FINAL REPORT - COLLIE CBD REVITALISATION PROJECT - 000-0432-1 FOR THE YEAR PERIOD ENDED 30 JUNE 2017

AMD AUDIT & ASSURANCE PTY LTD30/06/2017INV 800498 2,750.00

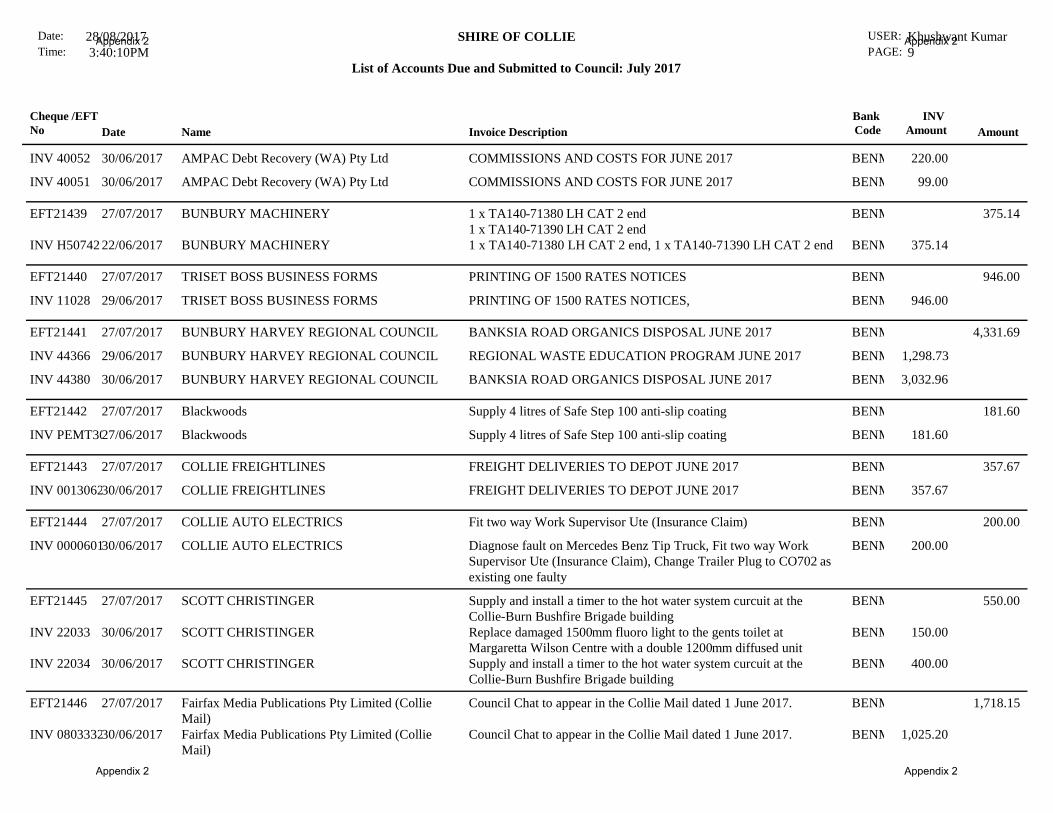

BENMUNICOMMISSIONS AND COSTS FOR JUNE 2017AMPAC Debt Recovery (WA) Pty Ltd27/07/2017 319.00EFT21438

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 928/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNICOMMISSIONS AND COSTS FOR JUNE 2017AMPAC Debt Recovery (WA) Pty Ltd30/06/2017INV 40052 220.00

BENMUNICOMMISSIONS AND COSTS FOR JUNE 2017AMPAC Debt Recovery (WA) Pty Ltd30/06/2017INV 40051 99.00

BENMUNI1 x TA140-71380 LH CAT 2 end1 x TA140-71390 LH CAT 2 end

BUNBURY MACHINERY27/07/2017 375.14EFT21439

BENMUNI1 x TA140-71380 LH CAT 2 end, 1 x TA140-71390 LH CAT 2 endBUNBURY MACHINERY22/06/2017INV H50742 375.14

BENMUNIPRINTING OF 1500 RATES NOTICESTRISET BOSS BUSINESS FORMS27/07/2017 946.00EFT21440

BENMUNIPRINTING OF 1500 RATES NOTICES,TRISET BOSS BUSINESS FORMS29/06/2017INV 11028 946.00

BENMUNIBANKSIA ROAD ORGANICS DISPOSAL JUNE 2017BUNBURY HARVEY REGIONAL COUNCIL27/07/2017 4,331.69EFT21441

BENMUNIREGIONAL WASTE EDUCATION PROGRAM JUNE 2017BUNBURY HARVEY REGIONAL COUNCIL29/06/2017INV 44366 1,298.73

BENMUNIBANKSIA ROAD ORGANICS DISPOSAL JUNE 2017BUNBURY HARVEY REGIONAL COUNCIL30/06/2017INV 44380 3,032.96

BENMUNISupply 4 litres of Safe Step 100 anti-slip coatingBlackwoods27/07/2017 181.60EFT21442

BENMUNISupply 4 litres of Safe Step 100 anti-slip coatingBlackwoods27/06/2017INV PEMT3038 181.60

BENMUNIFREIGHT DELIVERIES TO DEPOT JUNE 2017COLLIE FREIGHTLINES27/07/2017 357.67EFT21443

BENMUNIFREIGHT DELIVERIES TO DEPOT JUNE 2017COLLIE FREIGHTLINES30/06/2017INV 00130622 357.67

BENMUNIFit two way Work Supervisor Ute (Insurance Claim)COLLIE AUTO ELECTRICS27/07/2017 200.00EFT21444

BENMUNIDiagnose fault on Mercedes Benz Tip Truck, Fit two way Work Supervisor Ute (Insurance Claim), Change Trailer Plug to CO702 as existing one faulty

COLLIE AUTO ELECTRICS30/06/2017INV 00006017 200.00

BENMUNISupply and install a timer to the hot water system curcuit at the Collie-Burn Bushfire Brigade building

SCOTT CHRISTINGER27/07/2017 550.00EFT21445

BENMUNIReplace damaged 1500mm fluoro light to the gents toilet at Margaretta Wilson Centre with a double 1200mm diffused unit

SCOTT CHRISTINGER30/06/2017INV 22033 150.00

BENMUNISupply and install a timer to the hot water system curcuit at the Collie-Burn Bushfire Brigade building

SCOTT CHRISTINGER30/06/2017INV 22034 400.00

BENMUNICouncil Chat to appear in the Collie Mail dated 1 June 2017.Fairfax Media Publications Pty Limited (Collie Mail)

27/07/2017 1,718.15EFT21446

BENMUNICouncil Chat to appear in the Collie Mail dated 1 June 2017.Fairfax Media Publications Pty Limited (Collie Mail)

30/06/2017INV 0803332545 1,025.20

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 1028/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIAdvert in the Collie Mail dated 1 June 2017 in the Public Notice Section - Expressions of Interest - Disposal of Vehicles

Fairfax Media Publications Pty Limited (Collie Mail)

30/06/2017INV 0803332753 115.20

BENMUNIAdvert in the Collie Mail dated 8 June 2017 in the Public Notice Section - Expressions of Interest - Disposal of Vehicles

Fairfax Media Publications Pty Limited (Collie Mail)

30/06/2017INV 0803365489 115.20

BENMUNIAdvert in the Collie Mail dated 8 June 2017 in the Death Notices Section.

Fairfax Media Publications Pty Limited (Collie Mail)

30/06/2017INV 0803365497 65.78

BENMUNIAdvert in the Collie Mail dated 8 June 2017 in the Death Notices Section.

Fairfax Media Publications Pty Limited (Collie Mail)

30/06/2017INV 0803365539 51.17

BENMUNIDisability Access and Inclusion Plan Review - Community consultation.

Fairfax Media Publications Pty Limited (Collie Mail)

30/06/2017INV 0803400158 115.20

BENMUNIAdvert in the Collie Mail dated 22 June 2017 in the Tenders Section - Tender 09/2017 Mechanical Fuel Reduction of Reserve 36801.

Fairfax Media Publications Pty Limited (Collie Mail)

30/06/2017INV 0803442545 115.20

BENMUNIAdvert in the Public Notices Section of the Collie Mail dated 29 June 2017 - Imposition of Fees and Charges Coalfields Museum Entrance Fees.

Fairfax Media Publications Pty Limited (Collie Mail)

30/06/2017INV 0803478266 115.20

BENMUNIWork uniform clothingPETE'S27/07/2017 158.00EFT21447

BENMUNIWork uniform clothingPETE'S24/06/2017INV 199292 158.00

BENMUNIAdvertisement in Beautiful South accommodation and tourist guide.COLLIE VISITOR CENTRE27/07/2017 165.00EFT21448

BENMUNIAdvertisement in Beautiful South accommodation and tourist guide.COLLIE VISITOR CENTRE30/06/2017INV 7717 165.00

BENMUNIFREIGHT DELIVERIES TO DEPOT 26-28/6/17COURIER AUSTRALIA27/07/2017 135.74EFT21449

BENMUNIFREIGHT DELIVERIES TO DEPOT 26-28/6/17COURIER AUSTRALIA30/06/2017INV 0318 64.36

BENMUNIFREIGHT DELIVERIES EMERGENCY SERVICES 21-23/6/17, FREIGHT DELIVERIES EMERGENCY SERVICES 21-23/6/17

COURIER AUSTRALIA23/06/2017INV 0317 71.38

BENMUNIWater separator cover assemblyCOLLIE TYRE & EXHAUST CENTRE27/07/2017 75.00EFT21450

BENMUNIWater separator cover assemblyCOLLIE TYRE & EXHAUST CENTRE23/06/2017INV 00011064 75.00

BENMUNIPlease extend lighting and install 2 batten holders. Extend power supply and install 2 extra GPO's to museum

COLLIE ELECTRICAL SERVICE27/07/2017 675.29EFT21451

BENMUNIPlease extend lighting and install 2 batten holders. Extend power supply and install 2 extra GPO's to museum

COLLIE ELECTRICAL SERVICE29/06/2017INV 00006364 558.14

BENMUNIFault find library powerpoint and replace faulty GPOCOLLIE ELECTRICAL SERVICE26/06/2017INV 00006377 117.15

BENMUNIALLANSON BFB FUEL PURCHASES JUNE 2017CALTEX COLLIE SERVICE CENTRE27/07/2017 91.52EFT21452

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 1128/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIALLANSON BFB FUEL PURCHASES JUNE 2017CALTEX COLLIE SERVICE CENTRE01/07/2017INV 01JUL2017ACC12 91.52

BENMUNIRoad and Drainage Upgrade Rowe Street Collie as Per Contract 03/2017

Carbone Bros Pty Ltd27/07/2017 206,331.15EFT21453

BENMUNIRoad and Drainage Upgrade Rowe Street Collie as Per Contract 03/2017, Variation to Complete stormwater adjustments as per latest Rev C drawings

Carbone Bros Pty Ltd27/06/2017INV I79326 206,331.15

BENMUNIDays hire of multi tyred rollerCOALCLIFF PLANT HIRE PTY LTD27/07/2017 2,277.00EFT21454

BENMUNIDays hire of side tipper trailerCOALCLIFF PLANT HIRE PTY LTD30/06/2017INV 2260-43-48 1,045.00

BENMUNIDays hire of multi tyred rollerCOALCLIFF PLANT HIRE PTY LTD30/06/2017INV 2396-1-1 1,232.00

BENMUNISupply of Engineering Services for the upgrading of the Collie Motorplex facility in accordance with the respondents offer dated the 14th October 2016.

Calibre Consulting (Aust) Pty Ltd27/07/2017 3,797.97EFT21455

BENMUNISupply of Engineering Services for the upgrading of the Collie Motorplex facility in accordance with the respondents offer dated the 14th October 2016.

Calibre Consulting (Aust) Pty Ltd30/06/2017INV 019028 3,797.97

BENMUNIAdvertising of Australia Day family entertainment and outdoor cinema evening with South32 sponsorship.

COLLIE COMMUNITY BROADCASTING ASSOCIATION

27/07/2017 150.00EFT21456

BENMUNIAdvertising of Australia Day family entertainment and outdoor cinema evening with South32 sponsorship.

COLLIE COMMUNITY BROADCASTING ASSOCIATION

29/06/2017INV 20170501 150.00

BENMUNISupply and install footpath to plans provided - bridge access path access

Collie Concreting Pty Ltd27/07/2017 38,185.88EFT21457

BENMUNISupply and install footpath to plans provided - bridge access path access

Collie Concreting Pty Ltd20/06/2017INV IV0000000852 38,185.88

BENMUNIKidsport Reimbursement - Collie Eagles JFC3 participants

COLLIE EAGLES JUNIOR FOOTBALL CLUB INC

27/07/2017 325.00EFT21458

BENMUNIKidsport Reimbursement - Collie Eagles JFC, 3 participantsCOLLIE EAGLES JUNIOR FOOTBALL CLUB INC

22/06/2017INV KS011599 325.00

BENMUNICATERING SERVICES SHIRE OF COLLIE SENIORS LUNCHEON OCTOBER 2016

Community Home Care (Collie)27/07/2017 300.00EFT21459

BENMUNICATERING SERVICES SHIRE OF COLLIE SENIORS LUNCHEON OCTOBER 2016

Community Home Care (Collie)30/06/2017INV COL79 300.00

BENMUNICONSOLIDATED MINING TENEMENT ROLLLANDGATE27/07/2017 1,063.94EFT21460

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 1228/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIGRV CHARGEABLE SCHEDULE NO: G 2017/6 DATED 21/5/17 TO 18/6/17

LANDGATE27/06/2017INV 331666-10000927 76.94

BENMUNICONSOLIDATED MINING TENEMENT ROLLLANDGATE22/06/2017INV 331462-10000927 987.00

BENMUNISupply and apply prime seal to river Avenue shoulder.FULTON HOGAN INDUSTRIES27/07/2017 5,244.58EFT21461

BENMUNISupply and apply prime seal to river Avenue shoulder.FULTON HOGAN INDUSTRIES30/06/2017INV 10739065RI 5,244.58

BENMUNIPair of steel capped safety bootsCOLLIE SHOELAND27/07/2017 230.00EFT21462

BENMUNIPair of steel capped safety bootsCOLLIE SHOELAND23/06/2017INV 00002040 230.00

BENMUNIRectify communication failure between traffic signal trailers CO16885 & CO16884

GLOBAL AUTO ELECTRICAL AND AIR CONDITIONING SERVICES PTY LTD

27/07/2017 396.00EFT21463

BENMUNIRectify communication failure between traffic signal trailers CO16885 & CO16884

GLOBAL AUTO ELECTRICAL AND AIR CONDITIONING SERVICES PTY LTD

22/06/2017INV 00007721 297.00

BENMUNIDiagnose low oil pressure electrical fault and reportGLOBAL AUTO ELECTRICAL AND AIR CONDITIONING SERVICES PTY LTD

09/05/2017INV 00007431 99.00

BENMUNI3 bags general purpose cement, 1 padlock and 1 latch to suit padlockHENDERSON HARDWARE27/07/2017 118.60EFT21464

BENMUNI3 bags general purpose cement, 1 padlock and 1 latch to suit padlockHENDERSON HARDWARE29/06/2017INV 226743 64.40

BENMUNISupply 1 pkt 100mm t-hinge and 4 litre mineral turpsHENDERSON HARDWARE28/06/2017INV 226624 19.40

BENMUNISupply 2 pkts of nuts and bolts and 2 pkts of nyloc nutsHENDERSON HARDWARE29/06/2017INV 226765 14.80

BENMUNISupply 1 ten litre bucket and 1 20kg bag of grey mortar for repairing walls to toilet

HENDERSON HARDWARE28/06/2017INV 226627 20.00

BENMUNIRelief Ranger WE 02/07/2017Hays Specialist Recruiting (Australia) Pty Ltd27/07/2017 2,878.26EFT21465

BENMUNIRelief Ranger WE 02/07/2017Hays Specialist Recruiting (Australia) Pty Ltd05/07/2017INV 6695015 2,878.26

BENMUNISynergy Soft Upgrade (v11.1.86)IT VISION27/07/2017 1,743.50EFT21466

BENMUNIUniverse Upgrade, Synergy Soft Upgrade (v11.1.86)IT VISION30/06/2017INV 28374 1,743.50

BENMUNIOVERCALLS FEE FOR CONTRACT CA0184 FOR JUNE 2017INSIGHT CCS27/07/2017 306.02EFT21467

BENMUNIOVERCALLS FEE FOR CONTRACT CA0184 FOR JUNE 2017INSIGHT CCS15/07/2017INV 00088018 306.02

BENMUNIACCOUNT 1706061 NBN DATA PLAN 1/6/17-1/7/17Interphone27/07/2017 130.90EFT21468

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 1328/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIACCOUNT 1706061 NBN DATA PLAN 1/6/17-1/7/17Interphone05/07/2017INV 2341966 130.90

BENMUNIWaste Management Review as per Alternative Offer vide RFQ 03/2017 submitted by IWPROJECTS May - June 2017

IW PROJECTS27/07/2017 19,250.00EFT21469

BENMUNIWaste Management Review as per Alternative Offer vide RFQ 03/2017 submitted by IWPROJECTS May - June 2017

IW PROJECTS30/06/2017INV 878 19,250.00

BENMUNICoombes Street Collie Bridge No 3526: teat 40 Piles, Treat outside stringers, End Grain Treatment, Tighten and Maintain all bolts and fixings

JOMAR CONTRACTING27/07/2017 51,711.00EFT21470

BENMUNIPowerhouse Road Collie Burn Bridge No 3520: teat 28 Piles, Treat outside stringers, End Grain Treatment, Tighten and Maintain all bolts and fixings, Mungalup Road Collie Bridge No 3523: teat 32 Piles, Treat outside stringers, End Grain Treatment, Tighten and Maintain all bolts and fixings, Coombes Street Collie Bridge No 3526: teat 40 Piles, Treat outside stringers, End Grain Treatment, Tighten and Maintain all bolts and fixings, Demobilisation for works to all Bridges (Powerhouse Bridge, Mungalup Bridge & Coombes Street Bridge)

JOMAR CONTRACTING23/06/2017INV 00002733 51,711.00

BENMUNI11 X 15.9LTR BOTTLE SPRINGWATERLIVING SPRINGS27/07/2017 121.00EFT21471

BENMUNI11 X 15.9LTR BOTTLE SPRINGWATERLIVING SPRINGS30/06/2017INV INV-2700 121.00

BENMUNIHeritage Advisory Services for April-June 2017Leigh Barrett Heritage Advisory Services27/07/2017 529.75EFT21472

BENMUNIHeritage Advisory Services for April-June 2017Leigh Barrett Heritage Advisory Services30/06/2017INV COL020_1 APRIL-JUNE 2017 529.75

BENMUNIFire hazard level assessment - future devlopment areasLUSH FIRE & PLANNING27/07/2017 2,420.00EFT21473

BENMUNIFire hazard level assessment - future devlopment areasLUSH FIRE & PLANNING06/07/2017INV LFP163 2,420.00

BENMUNIREIMBURSE PURCHASE OF DOOR LOCK FOR POUND DOOR - REPAIRED AFTER BREAK IN

Leigh O'Connor27/07/2017 17.00EFT21474

BENMUNIREIMBURSE PURCHASE OF DOOR LOCK FOR POUND DOOR - REPAIRED AFTER BREAK IN

Leigh O'Connor24/07/2017INV 240717 17.00

BENMUNIHireof chlorine drum 920kg and 70kg cylinder for Collie swimming pool 01-30.06.2017

IXOM Operations Pty Ltd27/07/2017 209.55EFT21475

BENMUNIHireof chlorine drum 920kg and 70kg cylinder for Collie swimming pool 01-30.06.2017

IXOM Operations Pty Ltd30/06/2017INV 5842507 209.55

BENMUNIWorks to construct intersection upgrade to Princep & Forrest Streets.Picton Civil Pty27/07/2017 54,890.35EFT21476

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 1428/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIWorks to construct intersection upgrade to Princep & Forrest Streets.Picton Civil Pty20/06/2017INV P07192 54,890.35

BENMUNIHarmony Day - playing of drums by PCYC participants in the drumming program for Harmony Day 2017.

Collie Police & Community Youth Centre27/07/2017 220.00EFT21477

BENMUNIHarmony Day - playing of drums by PCYC participants in the drumming program for Harmony Day 2017.

Collie Police & Community Youth Centre30/06/2017INV SINV12593 220.00

BENMUNIInstall tie down points on truck tray CO 17693PIAVANINI WELDING27/07/2017 841.50EFT21478

BENMUNIInstall tie down points on truck tray CO 17693PIAVANINI WELDING30/06/2017INV 00008468 841.50

BENMUNIPROCESSING OF RECYCLABLES MAY 2017SUEZ Recovery & Recycling (Perth) Pty Ltd (Perthwaste)

27/07/2017 4,119.84EFT21479

BENMUNIPROCESSING OF RECYCLABLES JUNE 2017SUEZ Recovery & Recycling (Perth) Pty Ltd (Perthwaste)

30/06/2017INV 21175651 1,935.37

BENMUNIPROCESSING OF RECYCLABLES MAY 2017SUEZ Recovery & Recycling (Perth) Pty Ltd (Perthwaste)

31/05/2017INV 20693385 2,184.47

BENMUNIKidsport Reimbursement - Riding for the Disabled Association - Collie1 Participant

COLLIE RIDING FOR THE DISABLED27/07/2017 200.00EFT21480

BENMUNIKidsport Reimbursement - Riding for the Disabled Association - Collie, 1 Participant

COLLIE RIDING FOR THE DISABLED30/06/2017INV KS011876 200.00

BENMUNIRepairs to pole saw chain oil pumpCOLLIE MOWERS AND MORE27/07/2017 201.90EFT21481

BENMUNIRepairs to pole saw chain oil pumpCOLLIE MOWERS AND MORE28/06/2017INV 73310 160.90

BENMUNISets of edger bladesCOLLIE MOWERS AND MORE22/06/2017INV 73132 41.00

BENMUNIScheduled Service EMTS 100COSTATION MOTORS 197427/07/2017 956.80EFT21482

BENMUNINew key and reprogramme for 117COSTATION MOTORS 197428/06/2017INV R32096 430.00

BENMUNIScheduled Service EMTS 100COSTATION MOTORS 197422/06/2017INV R32031 526.80

BENMUNIRP0001-BLU LO LOGISTICS OFFICERSTEWART & HEATON CLOTHING CO PTY LTD

27/07/2017 72.90EFT21483

BENMUNIRP0001-BLU LO LOGISTICS OFFICERSTEWART & HEATON CLOTHING CO PTY LTD

22/06/2017INV SIN-2753818 36.45

BENMUNIRP0001-GLD PO PLANNING OFFICERSTEWART & HEATON CLOTHING CO PTY LTD

23/06/2017INV SIN-2754391 36.45

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 1528/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNISupply of sausages and chops for EOFY BBQ and presentation depotSPRY'S MEAT MARKET27/07/2017 200.30EFT21484

BENMUNISupply of sausages and chops for EOFY BBQ and presentation depotSPRY'S MEAT MARKET29/06/2017INV 36 200.30

BENMUNISupply the following Drum Units on Konica Minolta BizHub C284 photocopier at Roche Park1 x Cyan1 x Magenta1 x Yellow

SCOPE BUSINESS IMAGING27/07/2017 3,804.31EFT21485

BENMUNISupply Waste Toner box on Konica Minolta BizHub C284 photocopier at Roche Park, , Supply the following Drum Units on Konica Minolta BizHub C284 photocopier at Roche Park, 1 x Cyan, 1 x Magenta, 1 x Yellow

SCOPE BUSINESS IMAGING29/06/2017INV 392770 2,041.60

BENMUNISHIRE ADMIN OFFICE PREVENTATIVE SERVICE PLAN AND HELP DESK SUPPORT JUNE 2017

SCOPE BUSINESS IMAGING30/06/2017INV 393207 1,444.20

BENMUNIPREVENTATIVE SERVICE PLAN AND HELP DESK SUPPORT JUNE 2017

SCOPE BUSINESS IMAGING30/06/2017INV 393206 94.35

BENMUNILibrary photocopier maintenance plan and copy charges June 2017SCOPE BUSINESS IMAGING30/06/2017INV 393205 224.16

BENMUNIVarious reticulation tools (Quote 27162)TBS RURAL & HARDWARE27/07/2017 374.60EFT21486

BENMUNIVarious reticulation tools (Quote 27162)TBS RURAL & HARDWARE30/06/2017INV OEI87885 287.90

BENMUNID size batteriesTBS RURAL & HARDWARE23/06/2017INV OEI87829 32.00

BENMUNI9 x lengths of 25mm PVC pipe, 5 x 25mm PVC fittings, 5 x 20mm poly risers, 20 x 20mm poly elbows

TBS RURAL & HARDWARE23/06/2017INV OEI87836 54.70

BENMUNIBooks for apprentices from SWTAFE bookshopUniversity Co-op Bookshop Ltd27/07/2017 324.00EFT21487

BENMUNIBooks for apprentices from SWTAFE bookshopUniversity Co-op Bookshop Ltd04/04/2017INV 51343831 324.00

BENMUNIPre-employment medical for Tania Roberts - appointment with Guardian

COLLIE RIVER VALLEY MEDICAL CENTRE27/07/2017 240.00EFT21488

BENMUNIPre-employment medical for Tania Roberts - appointment with Guardian

COLLIE RIVER VALLEY MEDICAL CENTRE29/06/2017INV 251884BM 240.00

BENMUNIEQUIP 38926 SES COPIER CHARGES 2/6/17-2/7/17WEST COUNTRY PRINT SYNC27/07/2017 178.72EFT21489

BENMUNIEquipment 29795 Shire Office Copier charges 01/06/17-03/07/17WEST COUNTRY PRINT SYNC04/07/2017INV WA00344224 73.67

BENMUNIEQUIP 38926 SES COPIER CHARGES 2/6/17-2/7/17WEST COUNTRY PRINT SYNC04/07/2017INV WA00344225 105.05

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 1628/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNISupply and empty skip bins 1 x Minninup Pool, 1 x east end entrance, 1 x Black Diamond - June 2017 empties

COLLIE BIN HIRE27/07/2017 572.00EFT21490

BENMUNISupply and empty skip bins 1 x Minninup Pool, 1 x east end entrance, 1 x Black Diamond - June 2017 empties

COLLIE BIN HIRE30/06/2017INV 5883 572.00

BENMUNIRyan-Tracaire 72" tractor mounted aeratorWESTERN AG27/07/2017 22,561.00EFT21491

BENMUNIRyan-Tracaire 72" tractor mounted aerator, Spare and alternate parts, 20 x hollow tynes, 100 x spoon tynes, 100 x slicing tynes

WESTERN AG22/06/2017INV 00061737 22,561.00

BENMUNIAdvertisement in the SW Times - Public Notices Section on 1 June and 8 June 2017. Expressions of Interest - Disposal of Vehicles.

THE WEST AUSTRALIAN27/07/2017 1,452.00EFT21492

BENMUNIADVERTISEMENT FOR POSITON VACANT - SOUTH WEST TIMES - MUSEUM CUSTOMER SERVICE OFFICER 01.06.2017, ADVERTISEMENT FOR POSITON VACANT - SOUTH WEST TIMES - ACCOUNTANT MATERNITY LEAVE COVER 01.06.2017

THE WEST AUSTRALIAN30/06/2017INV 1025012620170630 629.20

BENMUNIAdvertisement in the SW Times - Public Notices Section on 1 June and 8 June 2017. Expressions of Interest - Disposal of Vehicles.

THE WEST AUSTRALIAN30/06/2017INV 1025012620170630 580.80

BENMUNIAdvertisement in the Tenders Section of the SW Times on Thursday 22 June 2017 - Tender 09/2017 Mechanical Fuel Reduction of Reserve 36801.

THE WEST AUSTRALIAN30/06/2017INV 1025012620170630 242.00

BENMUNIPayroll deductionsAUSTRALIAN SERVICES UNION27/07/2017 411.75EFT21493

Payroll Deduction for DAVID THOMAS ADDISON 26/07/2017, Payroll Deduction for JOHN ANTONI BAJOR 26/07/2017, Payroll Deduction for MAURICE LEO DHUE 26/07/2017, Payroll Deduction for HELENA ANNA GRYCZALOWSKI 26/07/2017, Payroll Deduction for ALEC SUTHERLAND 26/07/2017, Payroll Deduction for BRIAN JOHN MACINTYRE 26/07/2017, Payroll Deduction for STEPHEN GREGORY BOARD 26/07/2017, Payroll Deduction for MARK PIAVANINI 26/07/2017, Payroll Deduction for GARY BISHOP 26/07/2017, Payroll Deduction for SHANNON BARBER 26/07/2017, Payroll Deduction for DAYLE LYNETTE HOLLINS 26/07/2017, Payroll Deduction for PETER MILES 26/07/2017, Payroll Deduction for CHRISTINE SZOSTAK 26/07/2017, Payroll Deduction for STEVEN CRUICKSHANK 26/07/2017, Payroll Deduction for FRANCIS JOHN BECKER 26/07/2017

AUSTRALIAN SERVICES UNION26/07/2017INV DEDUCTION 411.75

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 1728/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIPayroll deductionsCHILD SUPPORT AGENCY27/07/2017 701.00EFT21494

Payroll Deduction 26/07/2017, Payroll Deduction 26/07/2017, Payroll Deduction 26/07/2017

CHILD SUPPORT AGENCY26/07/2017INV DEDUCTION 701.00

BENMUNICOFFEE MACHINEROCHE PARK RECREATION CENTRE07/07/2017 295.1541172

BENMUNIRCA STEREO LEAD AND TUB, EASTER SKATE ITEMS, SPORTS BOUNCE BALLS, SOCCER PENCILS, FROZEN CHIPS, TOMATO SAUCE, POTATO CRISPS, MILK, SUGAR, BISCUITS, COFFEE PODS, MOP HEADS WASHING, COFFEE MACHINE

ROCHE PARK RECREATION CENTRE28/06/2017INV PETTYCASH280617 295.15

BENMUNITELSTRA ACCOUNT 2265155000 SERVICE AND EQUIPMENT RENTAL TO 22/7/17

TELSTRA07/07/2017 67.6641173

BENMUNITELSTRA ACCOUNT 2265155000 SERVICE AND EQUIPMENT RENTAL TO 22/7/17

TELSTRA27/06/2017INV P633222551-0 67.66

BENMUNIREFUND FOR PENSION REBATE PAYMENT MADE ON 05/07/17

COMMISSIONER OF STATE REVENUE13/07/2017 6,772.8341174

BENMUNIREFUND FOR PENSION REBATE PAYMENT MADE ON 05/07/17

COMMISSIONER OF STATE REVENUE07/07/2017INV 070717 6,772.83

BENMUNIPayroll deductionsOUTSIDE SOCIAL CLUB17/07/2017 49.0041175

Payroll Deduction for DAVID THOMAS ADDISON 11/07/2017, Payroll Deduction for BRIAN JOHN MACINTYRE 11/07/2017, Payroll Deduction for STEPHEN GREGORY BOARD 11/07/2017, Payroll Deduction for MARK PIAVANINI 11/07/2017, Payroll Deduction for DENNIS MEREMA 11/07/2017, Payroll Deduction for RUSSELL TIERNEY 11/07/2017, Payroll Deduction for SHANE DOUGLAS COCKMAN 11/07/2017

OUTSIDE SOCIAL CLUB11/07/2017INV DEDUCTION 49.00

BENMUNIEMPLOYEE DEDUCTIONS PPE 12.7.2017EMPLOYEE DEDUCTIONS17/07/2017 65.0041176

EMPLOYEE DEDUCTIONS FOR PPE 12.7.2017EMPLOYEE DEDUCTIONS17/07/2017INV 12072017 65.00

BENMUNIMILK FROTHERROCHE PARK RECREATION CENTRE20/07/2017 286.1541177

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 1828/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIICE CUBE BAGS FOR ICE PACKS, CRAZY HAIR SKATE ITEMS/PRIZES, HOT CHOCOLATE, OIL AND CONFECTIONERY, COFFEE SUPPLIES, FROZEN CHIPS, MILK, MILK FROTHER, HULA HOOP - JNR PROGRAM ACTIVITY, HULA HOOP - JNR PROGRAM ACTIVITY, HULA HOOP - JNR PROGRAM ACTIVITY, DODGEBALL - JNR PROGRAM ACTIVITY, NETBALLS

ROCHE PARK RECREATION CENTRE18/07/2017INV PETTYCASH180717 286.15

BENMUNITELSTRA-ACCOUNT 0509899000TELSTRA20/07/2017 4,406.5541178

BENMUNIAllanson BFB Usage charges/ services & equipment rental to 1/8/17TELSTRA06/07/2017INV P323226461-6 52.10

BENMUNITELSTRA ACCOUNT 8260791400 HARRIS RIVER BFB SERVICE AND EQUIPMENT RENTAL TO 3/8/17

TELSTRA08/07/2017INV P208178051-6 32.33

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 1928/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIMobile Phones - Admin-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, Visitor Centre - Phone/Internet- TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, Server -TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, Health MUN-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, Waste MUN-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, Pool MUN-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, Roche Park MUN-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, Library MUN-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, Building MUN-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, PWO MUN-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, Land Lines-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, Internet-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, Supertowns Project-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, Ranger MUN-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, Health MUN-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, PWO MUN-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17, Bushfire Risk Planning Coordinator MUN-TELSTRA-ACCOUNT 0509899000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17

TELSTRA09/07/2017INV P456401251-9 4,192.17

BENMUNITELSTRA ACCOUNT 0500999000 USAGE CHARGES TO 1/7/17 SERVICE AND EQUIPMENT RENTAL TO 1/8/17

TELSTRA12/07/2017INV P670480151-8 129.95

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 2028/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIELECTRICITY ACCOUNT 261855670 11/5/17-11/7/17SYNERGY20/07/2017 2,203.4041179

BENMUNIELECTRICITY ACCOUNT 261855670 11/5/17-11/7/17SYNERGY11/07/2017INV 2040338094 1,459.90

BENMUNIELECTRICITY ACCOUNT 254858780 4/5/17-10/7/17SYNERGY10/07/2017INV 2180392260 743.50

BENMUNIWATER ACCOUNT 9006817397 SERVICE CHARGES 1/7/17-31/8/17

WATER CORPORATION20/07/2017 193.8741180

BENMUNIWATER ACCOUNT 9006817397 SERVICE CHARGES 1/7/17-31/8/17

WATER CORPORATION04/07/2017INV 0085 193.87

BENMUNITELSTRA ACCOUNT 2000550531048 SES 05/06/17-04/07/17TELSTRA27/07/2017 39.9541181

BENMUNITELSTRA ACCOUNT 2000550531048 SES 05/06/17-04/07/17TELSTRA09/07/2017INV 1263942648 39.95

BENMUNIELECTRICITY ACCOUNT 403265710 12/5/17-12/7/17SYNERGY27/07/2017 1,343.1041182

BENMUNIELECTRICITY ACCOUNT 403265710 12/5/17-12/7/17SYNERGY12/07/2017INV 2060342211 1,343.10

BENMUNIWATER ACCOUNT 9021475241 ANNUAL CHARGE 01/07/17-30/06/18

WATER CORPORATION27/07/2017 230.6141183

BENMUNIWATER ACCOUNT 9021475241 ANNUAL CHARGE 01/07/17-30/06/18

WATER CORPORATION04/07/2017INV 0003 230.61

BENMUNIPayroll deductionsOUTSIDE SOCIAL CLUB27/07/2017 49.0041184

Payroll Deduction for DAVID THOMAS ADDISON 26/07/2017, Payroll Deduction for BRIAN JOHN MACINTYRE 26/07/2017, Payroll Deduction for STEPHEN GREGORY BOARD 26/07/2017, Payroll Deduction for MARK PIAVANINI 26/07/2017, Payroll Deduction for DENNIS MEREMA 26/07/2017, Payroll Deduction for RUSSELL TIERNEY 26/07/2017, Payroll Deduction for SHANE DOUGLAS COCKMAN 26/07/2017

OUTSIDE SOCIAL CLUB26/07/2017INV DEDUCTION 49.00

BENMUNIEMPLOYEE DEDUCTIONS PPE 26.7.2017EMPLOYEE DEDUCTIONS27/07/2017 65.0041185

EMPLOYEE DEDUCTIONS FOR PPE 26.7.2017EMPLOYEE DEDUCTIONS27/07/2017INV 26072017 65.00

BENMUNIFuel Purchases - June 2017CALTEX ENERGY WA21/07/2017 2,940.37DD23097.1

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 2128/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIStarcard - Monthly Card Fee - June 2017, Fuel Purchases - Workshop - June 2017, Fuel Purchases - BFB Chief - T Hunter - June 2017, Fuel Purchases - BFB Chief - T Hunter - June 2017, Fuel Purchases - BFB Chief - T Hunter - June 2017, Fuel Purchases - BFB Chief - T Hunter - June 2017, Fuel Purchases - BFB Chief - T Hunter - June 2017, Fuel Purchases - BFB Chief - T Hunter - June 2017, Fuel Purchases - BFB Chief - T Hunter - June 2017, Fuel Purchases - BFB Chief - T Hunter - June 2017, Fuel Purchases - BFB Chief - T Hunter - June 2017, Fuel Purchases - BFB Chief - T Hunter - June 2017, Fuel Purchases - BFB Chief - T Hunter - June 2017, Fuel Purchases - BFB Chief - T Hunter - June 2017

CALTEX ENERGY WA30/06/2017INV 01057522500 2,940.37

BENMUNILitres of dieselCALTEX AUSTRALIA21/07/2017 16,894.87DD23097.2

BENMUNILitres of dieselCALTEX AUSTRALIA07/06/2017INV 9419218775 8,018.44

BENMUNILitres of dieselCALTEX AUSTRALIA21/06/2017INV 9419272790 1,771.31

BENMUNIDIESELCALTEX AUSTRALIA28/06/2017INV 9419298377 3,482.16

BENMUNILitres of dieselCALTEX AUSTRALIA15/06/2017INV 9419246104 3,622.96

BENMUNISuperannuation contributionsWA SUPER11/07/2017 22,656.93DD23114.1

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 2228/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNISuper. for DAVID THOMAS ADDISON 2384 11/07/2017, Super. for DAVID THOMAS ADDISON 2384 11/07/2017, Super. for JOHN ANTONI BAJOR 2386 11/07/2017, Super. for MAURICE LEO DHUE 3525 11/07/2017, Super. for MAURICE LEO DHUE 3525 11/07/2017, Super. for HELENA ANNA GRYCZALOWSKI 2387 11/07/2017, Super. for HELENA ANNA GRYCZALOWSKI 2387 11/07/2017, Super. for ALEC SUTHERLAND 4201 11/07/2017, Super. for BRIAN JOHN MACINTYRE 5260 11/07/2017, Super. for BRIAN JOHN MACINTYRE 5260 11/07/2017, Super. for STEPHEN GREGORY BOARD 5589 11/07/2017, Super. for MARK PIAVANINI 25684 11/07/2017, Super. for MARK PIAVANINI 25684 11/07/2017, Super. for VICKY LORRAINE CARTER 24952 11/07/2017, Super. for GARY BISHOP 8443 11/07/2017, Super. for GARY BISHOP 8443 11/07/2017, Super. for JANET ALISON KIDMAN 8442 11/07/2017, Super. for JANET ALISON KIDMAN 8442 11/07/2017, Super. for DENNIS MEREMA 8336 11/07/2017, Super. for GREGORY MALCOLM MCLAUGHLAN 219994 11/07/2017, Super. for SARA-JANE COLE 222172 11/07/2017, Super. for BRIAN ERNEST STUDSOR 223268 11/07/2017, Super. for MICHAEL GRAEME SEWELL 225805 11/07/2017, Super. for RUSSELL TIERNEY 225807 11/07/2017, Super. for DAVID LAWRENCE BLURTON 21399 11/07/2017, Super. for DAVID LAWRENCE BLURTON 21399 11/07/2017, Super. for SHANE DOUGLAS COCKMAN 230208 11/07/2017, Super. for SHANE DOUGLAS COCKMAN 230208 11/07/2017, Super. for ELFRIEDE JAMES 235180 11/07/2017, Super. for ELFRIEDE JAMES 235180 11/07/2017, Super. for SUZANNE JANE CUMING 237910 11/07/2017, Super. for TAMRON GRIBBLE 226627 11/07/2017, Super. for LINDSAY JOHN HEMLEY 242534 11/07/2017, Super. for PAMELA JOAN AHLIN 242905 11/07/2017, Super. for PAMELA JOAN AHLIN 242905 11/07/2017, Super. for DAYLE LYNETTE HOLLINS 242909 11/07/2017, Super. for CATHERINE CURRAN 242907 11/07/2017, Super. for JAYNE GREEN 13624 11/07/2017, Super. for ZAC SKWIROWSKI 246754 11/07/2017, Super. for ALLISON FERGIE 247092 11/07/2017, Super. for ALLISON FERGIE 247092 11/07/2017, Super. for PETER MILES 247386 11/07/2017, Super. for PETER MILES 247386 11/07/2017, Super. for JULIA LARKING 251868 11/07/2017, Super. for JULIA LARKING 251868

WA SUPER11/07/2017INV SUPER 18,682.58

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 2328/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

11/07/2017, Super. for ALISON KONONEN 2010023499 11/07/2017, Super. for CHRISTINE SZOSTAK 250128 11/07/2017, Super. for SHIRLEY COCKMAN 250945 11/07/2017, Super. for BRENDEN MEREMA 248063 11/07/2017, Super. for REBECCA O'CONNOR 251858 11/07/2017, Super. for BELINDA DENT 26456 11/07/2017, Super. for BELINDA DENT 26456 11/07/2017, Super. for STEVEN CRUICKSHANK 252356 11/07/2017, Super. for STEVEN CRUICKSHANK 252356 11/07/2017, Super. for ALEXANDER THOMAS SCADE 253913 11/07/2017, Super. for DEAN ALLAN BROWN 254688 11/07/2017, Super. for BRETT THOMAS LOWCOCK 253338 11/07/2017, Super. for BRETT THOMAS LOWCOCK 253338 11/07/2017, Super. for RICHARD JOHN SUMMERFIELD 3504 11/07/2017, Super. for RICHARD JOHN SUMMERFIELD 3504 11/07/2017, Super. for GEOFFREY VINCENT KLEM 228460 11/07/2017, Super. for KELLY BEAUGLEHOLE 234466 11/07/2017, Super. for MARIE MICHAEL 257532 11/07/2017, Super. for DEANNE MAREE LAWRENCE 6118 11/07/2017, Super. for SANDY MARSHALL 259103 11/07/2017, Super. for PHILLIP ARTHUR SCHENBERG 259102 11/07/2017, Super. for DAMIAN SCOTT SAUNDERS 260463 11/07/2017, Super. for TERRESA KIM BRIGGS 260501 11/07/2017, Super. for JULIE ANNE PELLICIARI 260497 11/07/2017, Super. for JULIE ANNE PELLICIARI 260497 11/07/2017, Super. for LES CRAKE 002302 11/07/2017, Super. for LES CRAKE 002302 11/07/2017, Super. for KOHDY JAMES FLYNN 261884 11/07/2017, Super. for KOHDY JAMES FLYNN 261884 11/07/2017, Super. for HASREEN SYED MAULE 263307 11/07/2017, Super. for HASREEN SYED MAULE 263307 11/07/2017, Super. for TRISTAN PETER GULVIN 263910 11/07/2017, Super. for AARON WILLIAM SHEPPARD 264320 11/07/2017, Super. for CHARLEE MAI WESTWOOD TBA 11/07/2017, Super. for JORDAN WILLIAM JACKSON 264683 11/07/2017, Super. for JODIE MICHELLE PILATTI 264794 11/07/2017, Super. for TERRESA KIM BRIGGS 260501 11/07/2017, Super. for ANDREW DOVER 253436 11/07/2017, Super. for ANDREW DOVER 253436 11/07/2017, Super. for JOHN OSVALDO BERNARDI TBA 11/07/2017, Super. for SHELBY LEE LATHAM 267087 11/07/2017, Super. for NATHAN ROBERT HUNT TBA 11/07/2017

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 2428/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIPayroll Deduction for DAVID THOMAS ADDISON 11/07/2017WA SUPER11/07/2017INV DEDUCTION 660.93

BENMUNIPayroll Deduction for MAURICE LEO DHUE 11/07/2017, Payroll Deduction for HELENA ANNA GRYCZALOWSKI 11/07/2017, Payroll Deduction for BRIAN JOHN MACINTYRE 11/07/2017, Payroll Deduction for MARK PIAVANINI 11/07/2017, Payroll Deduction for RUSSELL TIERNEY 11/07/2017, Payroll Deduction for ELFRIEDE JAMES 11/07/2017, Payroll Deduction for PAMELA JOAN AHLIN 11/07/2017, Payroll Deduction for ALLISON FERGIE 11/07/2017, Payroll Deduction for STEVEN CRUICKSHANK 11/07/2017, Payroll Deduction for JULIE ANNE PELLICIARI 11/07/2017, Payroll Deduction for LES CRAKE 11/07/2017, Payroll Deduction for HASREEN SYED MAULE 11/07/2017

WA SUPER11/07/2017INV DEDUCTION 1,932.12

BENMUNIPayroll Deduction for JANET ALISON KIDMAN 11/07/2017WA SUPER11/07/2017INV DEDUCTION 340.00

BENMUNIPayroll Deduction for SARA-JANE COLE 11/07/2017WA SUPER11/07/2017INV DEDUCTION 20.00

BENMUNIPayroll Deduction for SHANE DOUGLAS COCKMAN 11/07/2017WA SUPER11/07/2017INV DEDUCTION 113.05

BENMUNIPayroll Deduction for PETER MILES 11/07/2017, Payroll Deduction for BELINDA DENT 11/07/2017, Payroll Deduction for KOHDY JAMES FLYNN 11/07/2017

WA SUPER11/07/2017INV DEDUCTION 285.94

BENMUNIPayroll Deduction for JULIA LARKING 11/07/2017WA SUPER11/07/2017INV DEDUCTION 218.67

BENMUNIPayroll Deduction for RICHARD JOHN SUMMERFIELD 11/07/2017

WA SUPER11/07/2017INV DEDUCTION 355.87

BENMUNISuper. for KAREN VAN ASSELT 259013 11/07/2017WA SUPER11/07/2017INV SUPER 47.77

BENMUNISuperannuation contributionsAMP FLEXIBLE LIFETIME SUPERANNUATION

11/07/2017 191.87DD23114.2

BENMUNISuper. for FRANCIS JOHN BECKER 9552460058 11/07/2017AMP FLEXIBLE LIFETIME SUPERANNUATION

11/07/2017INV SUPER 191.87

BENMUNISuperannuation contributionsREST PERSONAL DIVISION11/07/2017 227.06DD23114.3

BENMUNISuper. for TAMMY JOY JOHNSON 711282615 11/07/2017REST PERSONAL DIVISION11/07/2017INV SUPER 227.06

BENMUNISuperannuation contributionsNETWEALTH SUPERANNUATION MASTER FUND

11/07/2017 393.01DD23114.4

BENMUNISuper. for STEPHEN MURRAY TUCK 0001070395 11/07/2017, Super. for CRAIG RICHARD MORTON 0001067567 11/07/2017

NETWEALTH SUPERANNUATION MASTER FUND

11/07/2017INV SUPER 393.01

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 2528/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

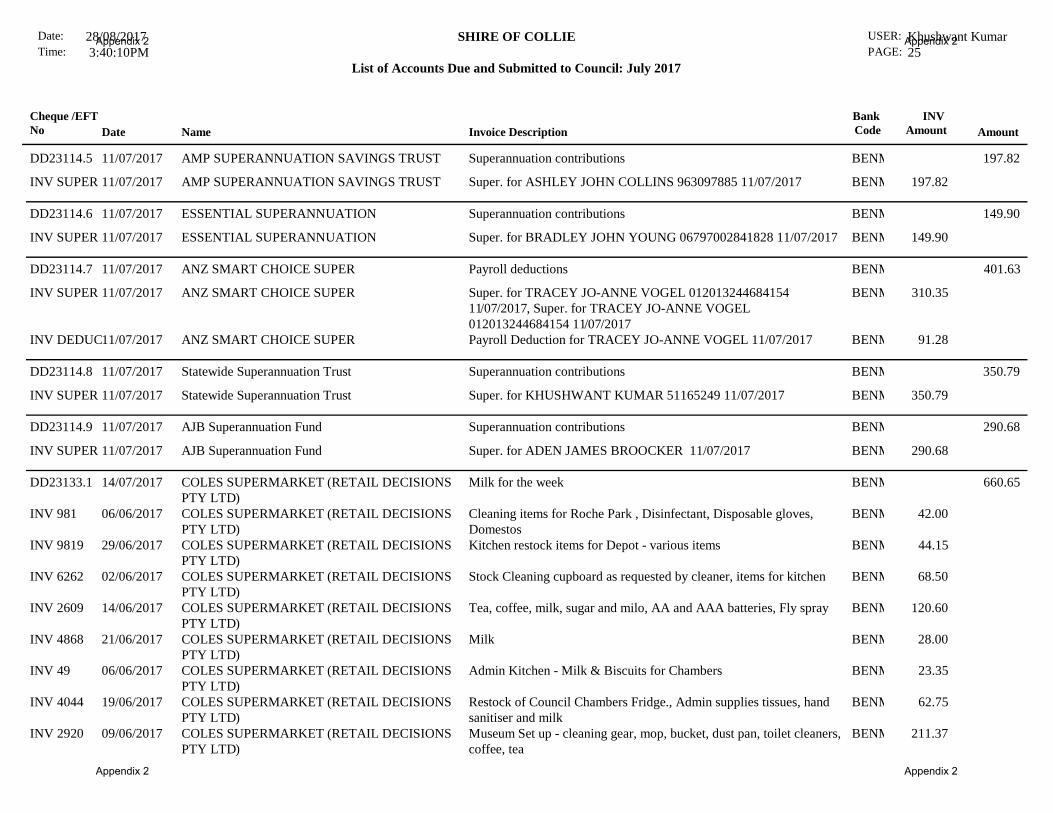

BENMUNISuperannuation contributionsAMP SUPERANNUATION SAVINGS TRUST11/07/2017 197.82DD23114.5

BENMUNISuper. for ASHLEY JOHN COLLINS 963097885 11/07/2017AMP SUPERANNUATION SAVINGS TRUST11/07/2017INV SUPER 197.82

BENMUNISuperannuation contributionsESSENTIAL SUPERANNUATION11/07/2017 149.90DD23114.6

BENMUNISuper. for BRADLEY JOHN YOUNG 06797002841828 11/07/2017ESSENTIAL SUPERANNUATION11/07/2017INV SUPER 149.90

BENMUNIPayroll deductionsANZ SMART CHOICE SUPER11/07/2017 401.63DD23114.7

BENMUNISuper. for TRACEY JO-ANNE VOGEL 012013244684154 11/07/2017, Super. for TRACEY JO-ANNE VOGEL 012013244684154 11/07/2017

ANZ SMART CHOICE SUPER11/07/2017INV SUPER 310.35

BENMUNIPayroll Deduction for TRACEY JO-ANNE VOGEL 11/07/2017ANZ SMART CHOICE SUPER11/07/2017INV DEDUCTION 91.28

BENMUNISuperannuation contributionsStatewide Superannuation Trust11/07/2017 350.79DD23114.8

BENMUNISuper. for KHUSHWANT KUMAR 51165249 11/07/2017Statewide Superannuation Trust11/07/2017INV SUPER 350.79

BENMUNISuperannuation contributionsAJB Superannuation Fund11/07/2017 290.68DD23114.9

BENMUNISuper. for ADEN JAMES BROOCKER 11/07/2017AJB Superannuation Fund11/07/2017INV SUPER 290.68

BENMUNIMilk for the weekCOLES SUPERMARKET (RETAIL DECISIONS PTY LTD)

14/07/2017 660.65DD23133.1

BENMUNICleaning items for Roche Park , Disinfectant, Disposable gloves, Domestos

COLES SUPERMARKET (RETAIL DECISIONS PTY LTD)

06/06/2017INV 981 42.00

BENMUNIKitchen restock items for Depot - various itemsCOLES SUPERMARKET (RETAIL DECISIONS PTY LTD)

29/06/2017INV 9819 44.15

BENMUNIStock Cleaning cupboard as requested by cleaner, items for kitchenCOLES SUPERMARKET (RETAIL DECISIONS PTY LTD)

02/06/2017INV 6262 68.50

BENMUNITea, coffee, milk, sugar and milo, AA and AAA batteries, Fly sprayCOLES SUPERMARKET (RETAIL DECISIONS PTY LTD)

14/06/2017INV 2609 120.60

BENMUNIMilkCOLES SUPERMARKET (RETAIL DECISIONS PTY LTD)

21/06/2017INV 4868 28.00

BENMUNIAdmin Kitchen - Milk & Biscuits for ChambersCOLES SUPERMARKET (RETAIL DECISIONS PTY LTD)

06/06/2017INV 49 23.35

BENMUNIRestock of Council Chambers Fridge., Admin supplies tissues, hand sanitiser and milk

COLES SUPERMARKET (RETAIL DECISIONS PTY LTD)

19/06/2017INV 4044 62.75

BENMUNIMuseum Set up - cleaning gear, mop, bucket, dust pan, toilet cleaners, coffee, tea

COLES SUPERMARKET (RETAIL DECISIONS PTY LTD)

09/06/2017INV 2920 211.37

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 2628/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNIMuseum Set up - broomsCOLES SUPERMARKET (RETAIL DECISIONS PTY LTD)

09/06/2017INV 2921 28.98

BENMUNICleaning spray & wipe/tissues for Transfer StationCOLES SUPERMARKET (RETAIL DECISIONS PTY LTD)

22/06/2017INV 5582 10.00

BENMUNIMilk for the weekCOLES SUPERMARKET (RETAIL DECISIONS PTY LTD)

26/06/2017INV 7638 20.95

BENMUNICONTRACT FEE BODYPUMP, BODYBALANCE, RPM, CXWORX, BODYCOMBAT 01/07/17-31/07/17

LES MILLS ASIA PACIFIC03/07/2017 831.46DD23135.1

BENMUNICONTRACT FEE BODYPUMP, BODYBALANCE, RPM, CXWORX, BODYCOMBAT 01/07/17-31/07/17

LES MILLS ASIA PACIFIC03/07/2017INV 857644 831.46

BENMUNIDeckhouse wall light plus postage and handling.SUBIACO RESTORATION14/07/2017 114.00DD23137.1

BENMUNIDeckhouse wall light plus postage and handling.SUBIACO RESTORATION23/06/2017INV 104815 114.00

BENMUNICSIRO Publishing14/07/2017 -24.95DD23137.2

BENMUNIREFUND FOR INV 252468 PAID BY CREDIT CARD AND EFTCSIRO Publishing05/06/2017INV 223786356 -24.95

BENMUNICREDIT CARD FEES JUNE 2017BENDIGO BANK CREDIT CARD29/07/2017 4.00DD23137.3

BENMUNICREDIT CARD FEES JUNE 2017BENDIGO BANK CREDIT CARD29/06/2017INV 30JUN2017 4.00

BENMUNIFLEET PARTNERS FUEL COSTS FOR JUNE 2017 1GBB194FLEET PARTNERS PTY LTD17/07/2017 2,461.08DD23147.1

BENMUNIFleet Partners Lease instalments 15/6/17-14/7/17 DLP5, Fleet Partners Lease instalments 15/6/17-14/7/17 1GBB194

FLEET PARTNERS PTY LTD01/07/2017INV LASH04721710A 2,203.60

BENMUNIFLEET PARTNERS FUEL COSTS FOR JUNE 2017 1GBB194FLEET PARTNERS PTY LTD01/07/2017INV FASH04721710A 257.48

BENMUNISuperannuation contributionsWA SUPER26/07/2017 24,600.83DD23155.1

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 2728/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNISuper. for DAVID THOMAS ADDISON 2384 26/07/2017, Super. for DAVID THOMAS ADDISON 2384 26/07/2017, Super. for JOHN ANTONI BAJOR 2386 26/07/2017, Super. for MAURICE LEO DHUE 3525 26/07/2017, Super. for MAURICE LEO DHUE 3525 26/07/2017, Super. for HELENA ANNA GRYCZALOWSKI 2387 26/07/2017, Super. for HELENA ANNA GRYCZALOWSKI 2387 26/07/2017, Super. for ALEC SUTHERLAND 4201 26/07/2017, Super. for BRIAN JOHN MACINTYRE 5260 26/07/2017, Super. for BRIAN JOHN MACINTYRE 5260 26/07/2017, Super. for STEPHEN GREGORY BOARD 5589 26/07/2017, Super. for MARK PIAVANINI 25684 26/07/2017, Super. for MARK PIAVANINI 25684 26/07/2017, Super. for VICKY LORRAINE CARTER 24952 26/07/2017, Super. for GARY BISHOP 8443 26/07/2017, Super. for GARY BISHOP 8443 26/07/2017, Super. for JANET ALISON KIDMAN 8442 26/07/2017, Super. for JANET ALISON KIDMAN 8442 26/07/2017, Super. for DENNIS MEREMA 8336 26/07/2017, Super. for GREGORY MALCOLM MCLAUGHLAN 219994 26/07/2017, Super. for SARA-JANE COLE 222172 26/07/2017, Super. for BRIAN ERNEST STUDSOR 223268 26/07/2017, Super. for MICHAEL GRAEME SEWELL 225805 26/07/2017, Super. for RUSSELL TIERNEY 225807 26/07/2017, Super. for DAVID LAWRENCE BLURTON 21399 26/07/2017, Super. for DAVID LAWRENCE BLURTON 21399 26/07/2017, Super. for SHANE DOUGLAS COCKMAN 230208 26/07/2017, Super. for SHANE DOUGLAS COCKMAN 230208 26/07/2017, Super. for ELFRIEDE JAMES 235180 26/07/2017, Super. for ELFRIEDE JAMES 235180 26/07/2017, Super. for SUZANNE JANE CUMING 237910 26/07/2017, Super. for TAMRON GRIBBLE 226627 26/07/2017, Super. for LINDSAY JOHN HEMLEY 242534 26/07/2017, Super. for PAMELA JOAN AHLIN 242905 26/07/2017, Super. for PAMELA JOAN AHLIN 242905 26/07/2017, Super. for DAYLE LYNETTE HOLLINS 242909 26/07/2017, Super. for CATHERINE CURRAN 242907 26/07/2017, Super. for JAYNE GREEN 13624 26/07/2017, Super. for ZAC SKWIROWSKI 246754 26/07/2017, Super. for ALLISON FERGIE 247092 26/07/2017, Super. for ALLISON FERGIE 247092 26/07/2017, Super. for PETER MILES 247386 26/07/2017, Super. for PETER MILES 247386 26/07/2017, Super. for JULIA LARKING 251868 26/07/2017, Super. for JULIA LARKING 251868

WA SUPER26/07/2017INV SUPER 20,061.76

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 2828/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

26/07/2017, Super. for ALISON KONONEN 2010023499 26/07/2017, Super. for CHRISTINE SZOSTAK 250128 26/07/2017, Super. for SHIRLEY COCKMAN 250945 26/07/2017, Super. for BRENDEN MEREMA 248063 26/07/2017, Super. for REBECCA O'CONNOR 251858 26/07/2017, Super. for BELINDA DENT 26456 26/07/2017, Super. for BELINDA DENT 26456 26/07/2017, Super. for STEVEN CRUICKSHANK 252356 26/07/2017, Super. for STEVEN CRUICKSHANK 252356 26/07/2017, Super. for CARLY RAE FORREST 253415 26/07/2017, Super. for ALEXANDER THOMAS SCADE 253913 26/07/2017, Super. for DEAN ALLAN BROWN 254688 26/07/2017, Super. for BRETT THOMAS LOWCOCK 253338 26/07/2017, Super. for BRETT THOMAS LOWCOCK 253338 26/07/2017, Super. for RICHARD JOHN SUMMERFIELD 3504 26/07/2017, Super. for RICHARD JOHN SUMMERFIELD 3504 26/07/2017, Super. for GEOFFREY VINCENT KLEM 228460 26/07/2017, Super. for KELLY BEAUGLEHOLE 234466 26/07/2017, Super. for MARIE MICHAEL 257532 26/07/2017, Super. for DEANNE MAREE LAWRENCE 6118 26/07/2017, Super. for SANDY MARSHALL 259103 26/07/2017, Super. for PHILLIP ARTHUR SCHENBERG 259102 26/07/2017, Super. for PAMELA ANNE PETERS 69122 26/07/2017, Super. for DAMIAN SCOTT SAUNDERS 260463 26/07/2017, Super. for TERRESA KIM BRIGGS 260501 26/07/2017, Super. for JULIE ANNE PELLICIARI 260497 26/07/2017, Super. for JULIE ANNE PELLICIARI 260497 26/07/2017, Super. for LES CRAKE 002302 26/07/2017, Super. for LES CRAKE 002302 26/07/2017, Super. for KOHDY JAMES FLYNN 261884 26/07/2017, Super. for KOHDY JAMES FLYNN 261884 26/07/2017, Super. for HASREEN SYED MAULE 263307 26/07/2017, Super. for HASREEN SYED MAULE 263307 26/07/2017, Super. for TRISTAN PETER GULVIN 263910 26/07/2017, Super. for AARON WILLIAM SHEPPARD 264320 26/07/2017, Super. for CHARLEE MAI WESTWOOD TBA 26/07/2017, Super. for JORDAN WILLIAM JACKSON 264683 26/07/2017, Super. for JODIE MICHELLE PILATTI 264794 26/07/2017, Super. for TERRESA KIM BRIGGS 260501 26/07/2017, Super. for ANDREW DOVER 253436 26/07/2017, Super. for ANDREW DOVER 253436 26/07/2017, Super. for JOHN OSVALDO BERNARDI TBA 26/07/2017, Super. for CREANA NARELLE GIBBS TBA 26/07/2017, Super. for SHELBY LEE

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 2928/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

LATHAM 267087 26/07/2017, Super. for NATHAN ROBERT HUNT TBA 26/07/2017, Super. for ANDRIENA MICHELLE CIRIC 45175 26/07/2017

BENMUNIPayroll Deduction for DAVID THOMAS ADDISON 26/07/2017WA SUPER26/07/2017INV DEDUCTION 676.05

BENMUNIPayroll Deduction for MAURICE LEO DHUE 26/07/2017, Payroll Deduction for HELENA ANNA GRYCZALOWSKI 26/07/2017, Payroll Deduction for BRIAN JOHN MACINTYRE 26/07/2017, Payroll Deduction for MARK PIAVANINI 26/07/2017, Payroll Deduction for RUSSELL TIERNEY 26/07/2017, Payroll Deduction for ELFRIEDE JAMES 26/07/2017, Payroll Deduction for PAMELA JOAN AHLIN 26/07/2017, Payroll Deduction for ALLISON FERGIE 26/07/2017, Payroll Deduction for STEVEN CRUICKSHANK 26/07/2017, Payroll Deduction for JULIE ANNE PELLICIARI 26/07/2017, Payroll Deduction for LES CRAKE 26/07/2017, Payroll Deduction for HASREEN SYED MAULE 26/07/2017

WA SUPER26/07/2017INV DEDUCTION 1,960.85

BENMUNIPayroll Deduction for GARY BISHOP 26/07/2017WA SUPER26/07/2017INV DEDUCTION 500.00

BENMUNIPayroll Deduction for JANET ALISON KIDMAN 26/07/2017WA SUPER26/07/2017INV DEDUCTION 340.00

BENMUNIPayroll Deduction for SARA-JANE COLE 26/07/2017WA SUPER26/07/2017INV DEDUCTION 20.00

BENMUNIPayroll Deduction for SHANE DOUGLAS COCKMAN 26/07/2017WA SUPER26/07/2017INV DEDUCTION 115.95

BENMUNIPayroll Deduction for PETER MILES 26/07/2017, Payroll Deduction for BELINDA DENT 26/07/2017, Payroll Deduction for KOHDY JAMES FLYNN 26/07/2017

WA SUPER26/07/2017INV DEDUCTION 293.96

BENMUNIPayroll Deduction for JULIA LARKING 26/07/2017WA SUPER26/07/2017INV DEDUCTION 222.39

BENMUNIPayroll Deduction for RICHARD JOHN SUMMERFIELD 26/07/2017

WA SUPER26/07/2017INV DEDUCTION 360.87

BENMUNISuper. for KAREN VAN ASSELT 259013 26/07/2017WA SUPER26/07/2017INV SUPER 49.00

BENMUNISuperannuation contributionsAMP FLEXIBLE LIFETIME SUPERANNUATION

26/07/2017 201.49DD23155.2

BENMUNISuper. for FRANCIS JOHN BECKER 9552460058 26/07/2017AMP FLEXIBLE LIFETIME SUPERANNUATION

26/07/2017INV SUPER 201.49

BENMUNISuperannuation contributionsREST PERSONAL DIVISION26/07/2017 310.92DD23155.3

BENMUNISuper. for TAMMY JOY JOHNSON 711282615 26/07/2017, Super. for JAYENDRA SINGH BUNDELA 125935413 26/07/2017

REST PERSONAL DIVISION26/07/2017INV SUPER 310.92

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 3028/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNISuperannuation contributionsNETWEALTH SUPERANNUATION MASTER FUND

26/07/2017 421.87DD23155.4

BENMUNISuper. for STEPHEN MURRAY TUCK 0001070395 26/07/2017, Super. for CRAIG RICHARD MORTON 0001067567 26/07/2017

NETWEALTH SUPERANNUATION MASTER FUND

26/07/2017INV SUPER 421.87

BENMUNISuperannuation contributionsAMP SUPERANNUATION SAVINGS TRUST26/07/2017 202.95DD23155.5

BENMUNISuper. for ASHLEY JOHN COLLINS 963097885 26/07/2017AMP SUPERANNUATION SAVINGS TRUST26/07/2017INV SUPER 202.95

BENMUNISuperannuation contributionsESSENTIAL SUPERANNUATION26/07/2017 155.76DD23155.6

BENMUNISuper. for BRADLEY JOHN YOUNG 06797002841828 26/07/2017ESSENTIAL SUPERANNUATION26/07/2017INV SUPER 155.76

BENMUNIPayroll deductionsANZ SMART CHOICE SUPER26/07/2017 411.15DD23155.7

BENMUNISuper. for TRACEY JO-ANNE VOGEL 012013244684154 26/07/2017, Super. for TRACEY JO-ANNE VOGEL 012013244684154 26/07/2017

ANZ SMART CHOICE SUPER26/07/2017INV SUPER 317.71

BENMUNIPayroll Deduction for TRACEY JO-ANNE VOGEL 26/07/2017ANZ SMART CHOICE SUPER26/07/2017INV DEDUCTION 93.44

BENMUNISuperannuation contributionsStatewide Superannuation Trust26/07/2017 350.79DD23155.8

BENMUNISuper. for KHUSHWANT KUMAR 51165249 26/07/2017Statewide Superannuation Trust26/07/2017INV SUPER 350.79

BENMUNISuperannuation contributionsAJB Superannuation Fund26/07/2017 295.39DD23155.9

BENMUNISuper. for ADEN JAMES BROOCKER 26/07/2017AJB Superannuation Fund26/07/2017INV SUPER 295.39

BENMUNISuperannuation contributionsIOOF PURSUIT - SHAREN-LOUISE TAYLOR11/07/2017 110.92DD23114.10

BENMUNISuper. for SHAREN LOUISE TAYLOR 326958M-D2-01 11/07/2017IOOF PURSUIT - SHAREN-LOUISE TAYLOR11/07/2017INV SUPER 110.92

BENMUNISuperannuation contributionsAUSTRALIAN SUPER11/07/2017 1,788.65DD23114.11

BENMUNIPayroll Deduction for KRYSTYNA JULIANA ROBERTS 11/07/2017, Payroll Deduction for LEIGH JAMES O'CONNOR 11/07/2017, Payroll Deduction for DARRYL ELIZABETH KING 11/07/2017

AUSTRALIAN SUPER11/07/2017INV DEDUCTION 307.28

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 3128/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNISuper. for RUSSEL SAM KENT 65403228 11/07/2017, Super. for KRYSTYNA JULIANA ROBERTS 6385296 11/07/2017, Super. for SHANNON BARBER 64715006 11/07/2017, Super. for LEIGH JAMES O'CONNOR 700866290 11/07/2017, Super. for LEIGH JAMES O'CONNOR 700866290 11/07/2017, Super. for TEGAN MAREE SHEA 65414715 11/07/2017, Super. for DARRYL ELIZABETH KING 702046311 11/07/2017, Super. for DARRYL ELIZABETH KING 702046311 11/07/2017

AUSTRALIAN SUPER11/07/2017INV SUPER 1,366.76

BENMUNISuper. for JO-ANNE LESLEY GOLTZ 65355287 11/07/2017AUSTRALIAN SUPER11/07/2017INV SUPER 48.65

BENMUNISuper. for KRYSTYNA JULIANA ROBERTS 6385296 11/07/2017AUSTRALIAN SUPER11/07/2017INV SUPER 65.96

BENMUNISuperannuation contributionsCONSTRUCTION & BUILDING INDUSTRY SUPER

11/07/2017 183.69DD23114.12

BENMUNISuper. for RUSSELL TIERNEY 2739770 11/07/2017CONSTRUCTION & BUILDING INDUSTRY SUPER

11/07/2017INV SUPER 183.69

BENMUNISuperannuation contributionsCOMMONWEALTH BANK OF AUST11/07/2017 61.90DD23114.13

BENMUNISuper. for JANET PATMORE 187580030 11/07/2017COMMONWEALTH BANK OF AUST11/07/2017INV SUPER 61.90

BENMUNISuperannuation contributionsMTAA SUPERANNUATION FUND11/07/2017 201.56DD23114.14

BENMUNISuper. for CHRISTOPHER SPRIGG 6780718 11/07/2017MTAA SUPERANNUATION FUND11/07/2017INV SUPER 201.56

BENMUNISuperannuation contributionsIOOF PURSUIT - SHAREN-LOUISE TAYLOR26/07/2017 110.92DD23155.10

BENMUNISuper. for SHAREN LOUISE TAYLOR 326958M-D2-01 26/07/2017IOOF PURSUIT - SHAREN-LOUISE TAYLOR26/07/2017INV SUPER 110.92

BENMUNISuperannuation contributionsAUSTRALIAN SUPER26/07/2017 1,883.51DD23155.11

BENMUNIPayroll Deduction for KRYSTYNA JULIANA ROBERTS 26/07/2017, Payroll Deduction for LEIGH JAMES O'CONNOR 26/07/2017, Payroll Deduction for DARRYL ELIZABETH KING 26/07/2017

AUSTRALIAN SUPER26/07/2017INV DEDUCTION 316.04

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Date:

Time: 3:40:10PMSHIRE OF COLLIE USER: Khushwant Kumar

PAGE: 3228/08/2017

List of Accounts Due and Submitted to Council: July 2017

Cheque /EFT No Date Name Invoice Description

Bank Code Amount

INV Amount

BENMUNISuper. for RUSSEL SAM KENT 65403228 26/07/2017, Super. for KRYSTYNA JULIANA ROBERTS 6385296 26/07/2017, Super. for SHANNON BARBER 64715006 26/07/2017, Super. for LEIGH JAMES O'CONNOR 700866290 26/07/2017, Super. for LEIGH JAMES O'CONNOR 700866290 26/07/2017, Super. for TEGAN MAREE SHEA 65414715 26/07/2017, Super. for DARRYL ELIZABETH KING 702046311 26/07/2017, Super. for DARRYL ELIZABETH KING 702046311 26/07/2017

AUSTRALIAN SUPER26/07/2017INV SUPER 1,397.11

BENMUNISuper. for JO-ANNE LESLEY GOLTZ 65355287 26/07/2017AUSTRALIAN SUPER26/07/2017INV SUPER 98.56

BENMUNISuper. for KRYSTYNA JULIANA ROBERTS 6385296 26/07/2017AUSTRALIAN SUPER26/07/2017INV SUPER 71.80

BENMUNISuperannuation contributionsCONSTRUCTION & BUILDING INDUSTRY SUPER

26/07/2017 180.79DD23155.12

BENMUNISuper. for RUSSELL TIERNEY 2739770 26/07/2017CONSTRUCTION & BUILDING INDUSTRY SUPER

26/07/2017INV SUPER 180.79

BENMUNISuperannuation contributionsCOMMONWEALTH BANK OF AUST26/07/2017 54.28DD23155.13

BENMUNISuper. for JANET PATMORE 187580030 26/07/2017COMMONWEALTH BANK OF AUST26/07/2017INV SUPER 54.28

BENMUNISuperannuation contributionsMTAA SUPERANNUATION FUND26/07/2017 210.24DD23155.14

BENMUNISuper. for CHRISTOPHER SPRIGG 6780718 26/07/2017MTAA SUPERANNUATION FUND26/07/2017INV SUPER 210.24

TOTAL

BENDIGO BANK tBENTRUST

BENDIGO BANK mBENMUNI

TOTAL

636,720.60

1,222.00

637,942.60

REPORT TOTALS

Bank NameBank Code

CERTIFICATE OF Chief Executive Officer

This schedule of accounts to be passed for payment, covering vouchers as above which was submitted to each member of Council has been checked and is fully supported by vouchers and invoices which are submitted herewith and which have been duly certified as to the receipt of goods and the rendition of services and as to prices, computations, and costings and the amounts shown are due for payment

Chief Executive Officer

Appendix 2 Appendix 2

Appendix 2 Appendix 2

Var. $

(b)-(a)

Var. %

(b)-(a)/(a)

Note (Under)/Over (Under)/Over

Revenues $ $ $ $ %

General Purpose Funding 1 7,927,910 514,991 13,811 (501,180) (97.32%)

Governance 100,069 8,337 12,252 3,915 46.95%

Law, Order and Public Safety 264,573 22,188 16,345 (5,843) (26.33%)

Health 10,000 833 2,659 1,826 219.23%

Welfare 24,000 2,000 4,089 2,089 104.45%

Housing 7,800 650 0 (650) (100.00%)

Community Amenities 2 1,459,385 119,024 12,072 (106,952) (89.86%)