apollo global management - wordpress.com

TRANSCRIPT

APOLLOGlobal Management

Jonathan Dybka

Recommendation: BUY

Current Price: $48.05

Target Price: $67.55

Upside: 40%

Downside: 21%

Notes: Information as of January 21, 2021.

Source: Wikipedia, Yahoo Finance, Annual Report

SHARE PRICE PERFORMANCE

BUSINESS MIX FY2019

COMPANY OVERVIEW

0

10

20

30

40

50

60

20

18

-10

-01

20

18

-11

-01

20

18

-12

-01

20

19

-01

-01

20

19

-02

-01

20

19

-03

-01

20

19

-04

-01

20

19

-05

-01

20

19

-06

-01

20

19

-07

-01

20

19

-08

-01

20

19

-09

-01

20

19

-10

-01

20

19

-11

-01

20

19

-12

-01

20

20

-01

-01

20

20

-02

-01

20

20

-03

-01

20

20

-04

-01

20

20

-05

-01

20

20

-06

-01

20

20

-07

-01

20

20

-08

-01

20

20

-09

-01

20

20

-10

-01

20

20

-11

-01

20

20

-12

-01

Share Price in USD

2

AB

C

D

COVID-19

F

E

H

G

A Oct-Dec: S&P market correction; down 19.6%. Apollo's PE holdings decline 29.1% in value . $400M loss in carried interest income.

E Mar 26: U.S. Senate approves $2 Trillion stimulus packages in response to COVID-19 pandemic

B Apr 16: Smart & Final agrees to be aquired by Apollo. All outstanding shares will be purchased for $6.50/share representing a 25% premium

F Jun 18: Apollo announces plans to expand U.S insurance business. Athene holdings made a $500M equity investment for an 11% stake in Jackson National Life Insurance

C Aug 29: Apollo & Athene announced plans to acquire PK AirFinance from GE's Air-Finance unit. Estimated to be a $4B deal

G Oct 12: NY Times publishes article accusing Leon Black of having closer ties to Epstein than originally claimed

D Feb 17: Second confirmed death in U.S from COVID-19 H Nov 3: Market rallies on U.S. Election news

47%

44%

9%

Private Equity Credit Real Assets

AUM by Segment Revenues by sector

▪ $331M in AUM with a net IRR of 24% since inception

▪ Investment strategy

▪ Pursue investments that competitors avoid

▪ Seek complex structures

▪ Invest during uncertainty

▪ Operating Segments:

▪ Credit: Managing a leveraged, high-yield bond portfolio with

$173B in fee generating AUM

▪ Private Equity: $44B fee generating AUM

▪ Real Assets: Acquiring and recapitalizing assets in a distressed-

for-control context. $30B in fee generating AUM.

APOLLO

65%

23%

12%

Credit Private Equity Real Assets

Notes: Information as of January 21, 2021.

Source: Wikipedia, Yahoo Finance, Annual Report

DIVERSIFICATION ACROSS KEY ATTRIBUTES

3

INVESTOR BASE BY GEOGRAPHY

▪ Firm is becoming more geographically diversified since 2015

▪ Europe, and Middle Eastern regions showing strong growth

▪ Public pensions, Insurance, and Sovereign governments make

up 64% of Apollo’s investor base

25%

20%

19%

10%

9%

8%

7% 2%

Public Pension Finance/ Insurance

Sovereign Government Other

HNW / Retail Corporate Pensiond

Fund of Fund Endowment or Foundation

LP PROFILE

65%

12%15%

7%1%

60%

17%11% 11%

1%0%

10%

20%

30%

40%

50%

60%

70%

North America Europe Asia &Australia

Middle East Latin America

2015 2019

Apollo is diversified across geographies, vintage years, and institutions.

17,400

12,723

21,135

32,506

23,183

6,163

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Fund I,II,III,IV, and MIA

Fund V Fund VI Fund VII Fund VIII Fund IX

<2001 2001 2006 2008 2013 2018

Tota

l Val

ue

($ T

ho

usa

nd

s)

VINTAGE YEAR

APOLLO

77

216

39

Private Equity Credit Real Assets

BY SEGMENT ($B)

Notes: Information as of January 21, 2021.

Source: 1.IBIS World. 2.Institutional Investor. 3. FRED St Louis

MACRO OVERVIEW

4

-6.86%

4.84% 4.60%

7.55%

3.55% 3.63%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

2020 2021 2021E 2022E 2023E 2024E

GROWING DEMAND FROM PENSION FUNDS

0.0

50.0

100.0

150.0

200.0

250.0

300.0

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

E

20

22

E

20

23

E

20

24

E

20

25

E

20

26

E

INDUSTRY REVENUES – PRIVATE EQUITY ($B)

The private equity industry is expected to continue growing as institutions seek higher returns in a low interest rate environment.

▪ Institutional investors are expected to increase their

allocation in PE to achieve higher returns and diversification

▪ Industry profitability is expected to increase from 26% in

2020 to 36% in 2025

APOLLO

Notes: Information as of January 21, 2021.

Source: 1.IBIS World. 2.Institutional Investor. 3. FRED St Louis

MACRO OVERVIEW

5

-0.77

-1.34

0.28 0.31

0.170.13 0.13

-1.5

-1.3

-1.1

-0.9

-0.7

-0.5

-0.3

-0.1

0.1

0.3

YIELD ON 10 YR TREASURY NOTE

1100

1150

1200

1250

1300

1350

1400

1450

1500

1550

▪ Interest rates in the US are expected to remain close to 0% until

2023

BOFA HIGH YIELD TOTAL RETURN INDEX3

Apollo’s credit segment is affected on the high-yield bond market and interest rates.

▪ Low interest rates are good for PE firms as investors have

fewer alternative investment options2

▪ BofA Index is a good proxy for the performance of the high

yield bond market

APOLLO

Notes: Information as of January 21, 2021.

Source:Factset, Annual Report

FINANCIAL OVERVIEW

6

1,087

2,011

2,660

1,164

2,834

1,874

2,340

85%

32%

-56%

143%

-34%

25%

-100%

-50%

0%

50%

100%

150%

200%

0

500

1,000

1,500

2,000

2,500

3,000

2015 2016 2017 2018 2019 2020E 2021E

Revenue ($mm) % Growth

REVENUE FEE GENERATING VS TOTAL AUM

▪ During times of increased volatility and market dislocation, carried interest will be several impacted. The result of this can be seen in 2015, 2018 and 2020 as each year had a market correction

▪ Fee generating AUM makes up 77% of Total AUM on average

138 151169

214246

342372

170192

249

280

331

411

476

81%79%

68%

76% 74%83%

78%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

100

200

300

400

500

600

2015 2016 2017 2018 2019 2020E 2021E

Fee AUM ($B) Total AUM ($B) Fee AUM as % of total

Most of Apollo’s revenues come from management fees.

APOLLO

Notes: Information as of January 21, 2021.

Source:1.Investor Presentation. 2,Factset

FINANCIAL OVERVIEW

7

FRE MARGIN ($MM) MANAGEMENT FEES VS CARRIED INTEREST ($MM)

▪ Fee Related Earnings (FRE) margins are a key industry metric. Apollo’s FRE margin has been rising over the past five years by keeping costs consistent but growing revenues.

▪ 90% of Fee Related Earnings come from management fees.1

• Management fees are a more stable source of revenues. Carried interest is highly affected by market conditions.

FRE represents a stable and predictable revenue stream for Apollo.

APOLLO

960

1,1251,200

1,394

1,6141700

2125

422530

624

771

902 865

1081

44%

47%

52%55% 56% 56% 56%

0%

10%

20%

30%

40%

50%

60%

0

500

1,000

1,500

2,000

2,500

2015 2016 2017 2018 2019 2020E 2021E

Fee Related Revenue ($mm) Fee Related Earnings ($mm) FRE Margin

9301,044

1,155

1,345

1,576

1,240

97

780

1,338

(400)

1,057

(350)

-500

0

500

1,000

1,500

2015 2016 2017A 2018A 2019A Q3/2020

Management fee Carried int

Notes: Information as of January 21, 2021.

Source:1.Yahoo Finance

INVESTMENT THESIS

8

GROWING AUM

SHORT TERM: TRADING AT A DISCOUNT TO PEERS1:

45

65

85

105

125

145

APO KKR Ares Hamilton Lane

0

50

100

150

200

250

300

350

400

2015 2016 2017 2018 2019 2020E 2021E

LONG TERM:

GEOGRAPHIC EXPANSION

MARKET VOLATILITY DUE TO COVID-19

CREATING BUYING OPPORTUNITIES

Apollo is an attractive investment because of its AUM growth, buying opportunities, all while trading at a discount.

APOLLO

Notes: Information as of January 21, 2021.

Source:1.Cambridge Associates. 2.Annual Presentation

INVESTMENT THESIS – LONG TERM

9

YEARLY AUM GROWTH

0%

5%

10%

15%

20%

25%

30%

35%

2016 2017 2018 2019 Q3 2020

APO Ares KKR Hamilton

APO: 20.6%

HLNE: 15.8%

KKR: 14.3%

ARES: 13.8%

CAGR:

▪ Apollo grew its AUM at 26.6% CAGR in 5 years, higher than

any of its peers

INDUSTRY LEADING RETURNS1

13.8% 12.8%

18.34%

12.6%

39%

24%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

10 years 25 years 10 years 25 years PE Gross IRR PE Net IRR

US Private Equity Index

Top Quartile

Apollo IRR since inception

▪ This can be attributed to its industry leading returns, with a

net IRR of 24% since inception2

Fastest growing AUM in the industry due to a history of exceptional returns.

APOLLO

Notes: Information as of January 21, 2021.

Source:1.Annual Presentation. 2.Annaul Report 2019

INVESTMENT THESIS – SHORT TERM

10

DRY POWDER1 ($B)

Used the COVID induced stress to make strategic acquisitions and leveraged their advantage in credit to drive growth

▪ $45.8B in dry powder

▪ $50B in purchases during pandemic

▪ 14% of Fund IX committed to distressed opportunities

APOLLO

14.5

27.6

3.7

Credit Private Equity Real Assets

INDUSTRY LEADER IN CREDIT2

Credit Type Growth 1yr Net Returns 2019

Corporate Credit 13% 9.50%

Structured Credit 24% 10.00%

Direct Origination 45% 8.20%

▪ $300B in AUM. The largest alternative credit platform in the

industry

▪ Utilizing their scale to offer uncorrelated investment

opportunities

▪ Their success can be seen in the growth of the direct

origination segment

▪ 52% of management fees come from credit, therefore growth

in this segment is key

Notes: Information as of January 21, 2021.

Source: Factset. Annual Reports of each firm (2019)

VALUATION – COMPARABLE FIRMS

11

▪ Apollo had the highest growth in AUM at 34%

▪ Management fee margin is bellow industry average of 63%

▪ Apollo is valued at a discount compared to peers based on the P/FRE at 20.6x vs

industry average of 31.5x

▪ Trading at a discount compared to its historical 3 year average of 22.3x

Apollo is trading at a relative discount in P/FRE multiple to its peers. This is due to its low management fee ratio, despite having the highest AUM growth in the industry.

APOLLO

Company Market CapEnterprise

Value

Div

Yield

Fee AUM

($mm)

P/

Fee-AUMP/FRE

Management Fee to

Carried Interest RatioAUM Growth LTM EV/EBITDA NTM

Hamilton Lane 4,271 4,342 1.53% 38,700 11.2% 42.8x 7.48 8% 27.4x

Blackstone Group 73,602 84,480 3.02% 408,000 18.8% 39.5x 5.24 5% 19.7x

Carlyle Group 11,520 17,938 2.97% 161,000 6.4% 31.8x 3.38 4% 13.2x

Ares Management Corp 24,160 35,129 3.54% 96,900 6.7% 30.3x 1.57 24% 31.3x

KKR & Co 23,098 72,326 1.33% 152,997 14.1% 12.9x 0.40 11% 10.8x

Average 27,330 42,843 2.48% 171,519 11.4% 31.5x 3.62 10% 20.5x

Median 23,098 35,129 2.97% 152,997 11.2% 31.8x 3.38 8% 19.7x

Apollo Global 19,159 31,750 4.82% 246,446 8.0% 20.6x 1.49 34% 18.4x

Firm P/AUM AUM growth LTM

Brookfield 25% 6%

EQT 44% -1%

Partners Group 32% 2%

Intermediate Partners11% 14%

Average 28% 5%

Median 29% 4%

Apollo 8% 34%

COMPARED TO CNID CHALLENGE

12

INVESTMENT THESIS – DISCOUNT TO PEERS

▪ A linear relationship between Management Fee ratio and the multiple the firm

trades at

▪ A higher management fee relative to carried interest fee indicates the firm has a

more stable cash flow

MANAGEMENT FEE : CARRIED INTEREST RATIO

APOLLO

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2017 2018 2019 2020

APO Blackstone Carlyle Hamilton Ares

PRICE / FRE MULTIPLE

APO: 20.6x

BX: 39.5x

HLNE: 42.5x

CG: 31.8x

ARES: 30.3x

▪ The discount is due to the media’s accusations that CEO Leon Black had closer

ties to Jeffrey Epstein

▪ The company will continue trading at a discount until the independent committee

releases its decision

Apollo is trading at a discount to its peers due to a relatively lower management fee ratio and the current Epstein scandal.

Notes: Information as of January 21, 2021.

Source: Factset

7.5

5.2

3.4

1.6

0.4

1.5 1.5

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

10.0 15.0 20.0 25.0 30.0 35.0 40.0 45.0

Man

agm

ent

Fee

to C

arri

ed In

tere

st R

atio

P / FRE

APO (20x)

2020

KKR

HLNE

CG

ARES

BX

APO (25x)

2018

VALUATION – REVENUE FORECAST

13

REVENUE FORECAST

AUM Forecasts

2013 2014 2015 2016 2017 2018 2019 Q3 2020 2021E 2022E 2023E 2024E

Fee Rev ($B) 0.67 0.85 0.93 1.04 1.15 1.35 1.58 1.70 2.12 2.66 3.19 3.82

AUM ($B) 161 160 170 192 249 280 331 433 430 537 655 786

AUM Growth-0.62% 6.25% 12.94% 29.69% 12.45% 18.21% 30.82% -0.77% 25.00% 21.96% 20.00%

Fee Revenue as % of AUM

0.42% 0.53% 0.55% 0.54% 0.46% 0.48% 0.48% 0.39% 0.49% 0.49% 0.49% 0.49%

▪ Fee revenue remains constant at 0.5% of total

AUM.

▪ Based on the AUM growth of Q3/2020 of 30.8%,

AUM growth will slow over the next four years

▪ Having AUM forecasts, we can derive fee

revenues, assuming they remain at a constant %

of AUM

▪ Total revenues are expected to grow at 11.3%

CAGR until 2024

▪ 2020 will see a contraction due to COVID and the

resulting economic slowdown

▪ Economic activity is expected to return to normal

by 2021 and revenue growth will continue at

historical levels

1.58 1.702.12

2.663.19

3.82

-7.7%

17.5% 17.9%

15.1%15.9%

-10%

-5%

0%

5%

10%

15%

20%

-1

1

2

3

4

5

6

7

2019A 2020E 2021E 2022E 2023E 2024E

Management fees from affiliates Advisory and transaction fees from affiliates, net

Carried interest income from related parties Principal investment income / loss

Growth

APOLLONotes: Information as of January 21, 2021.

Source:

VALUATION – DISCOUNTED CASH FLOW MODEL

14

Fiscal Year 2017A 2018A 2019A Q1A Q2A Q3A Q4E 2020E 2021E 2022E 2023E 2024E

Fiscal Year End Date 12-31-17 12-31-18 12-31-19 3-31-20 6-30-20 9-30-20 12-31-20 12-31-20 12-31-21 12-31-22 12-31-23 12-31-24

Revenue 2,610,173 1,093,065 2,931,849 (1,469,086) 1,508,335 1,018,274 802,018 2,705,120 3,179,643 3,749,226 4,316,739 5,003,416

Revenue Growth % -58.1% 168.2% -32.5% -21.2% -7.7% 17.5% 17.9% 15.1% 15.9%

EBIT 1,412,014 80,406 1,537,955 (2,354,938) 1,123,098 686,953 749,455 1,724,046 2,071,550 2,410,008 2,747,236 3,155,273

EBIT Margin % 7.4% 52.5% 74.5% 67.5% 93.4% 63.7% 65.2% 64.3% 63.6% 63.1%

EBITDA 1,339,094 (77,589) 1,364,065 (2,402,582) 1,067,749 650,285 714,293 1,549,223 1,894,190 2,200,877 2,506,449 2,876,184

EBITDA Margin % -96.5% 88.7% 102.0% 95.1% 94.7% 95.3% 89.9% 91.4% 91.3% 91.2% 91.2%

Tax Rate % 18.4% 81.7% -9.2% 11.5% 12.3% 11.7% 11.8% 11.8% 11.8% 11.8% 11.8% 11.8%

EBIAT 660,875 1,520,608 1,827,107 2,125,627 2,423,062 2,782,951

(+) D&A 3,335 24,942 29,317 34,569 39,801 46,133

(-) CAPEX (16,028) (64,112) (64,112) (64,112) (64,112) (64,112)

(-) Change in NWC (1,089,270) (127,002) 126,917 (15,907) (15,958) (13,034)

Unlevered Free Cash Flows 1,737,452 1,608,440 1,665,395 2,111,991 2,414,709 2,778,005

Discount Factor 1% 101% 201% 301% 401%

Present Value of UFCFs 1,737,452 1,607,428 1,486,115 1,682,812 1,717,975 1,764,792

ASSUMPTIONS:

▪ Revenue will grow at a 9.2% CAGR for the next 4

years

▪ D&A will remain constant at 0.9% of revenues

▪ CAPEX will remain constant

▪ WACC of 11.99%

APOLLO

PERPETUITY: 75%

EXIT EBITDA: 25%

WEIGHTED AVERAGE

VALUE PER SHARE: $67.55

UPSIDE: 40% (from current $48.29)

Notes: Information as of January 21, 2021.

Source:

MANAGEMENT FEE REVENUE 2020

COST OF CAPITAL

COMPENSATION EXPENSE 2020

BETA

SENSITIVITY ANALYSIS

15

54.00

56.00

58.00

60.00

62.00

64.00

1,599,711 1,649,711 1,699,711 1,749,711 1,799,711

40.00

60.00

80.00

100.00

120.00

16% 14% 11.99% 10% 8%

50.00

55.00

60.00

65.00

70.00

1.9 1.8 1.7 1.6 1.5

Stock

Price ($)

58.00

59.00

60.00

61.00

(1,457,706) (1,157,706) (857,706) (557,706) (257,706)

55.00

94.55

48.87

19.46

64.64

102.76

74.97

55.38

0.00

20.00

40.00

60.00

80.00

100.00

120.00

DCF value at 0.7-2.7%perpetuity range

DCF value at 19.5-21.5x exitEBITDA range

DCF value at 10-14% WACCrange

52 week market high/low

FOOTBALL FIELD

How does the model react to different parameters?

APOLLONotes: Information as of January 21, 2021.

Source:

WORST CASE SCENARIO

SCENARIO ANALYSIS

16

Fiscal Year 2021E 2022E 2023E 2024E

Base Case

Total Revenue Forescast ($ Thousands) 3,179,643 3,749,226 4,316,739 5,003,416

EBIT 2,071,550 2,410,008 2,747,236 3,155,273

Bear Case:

Management fees from affiliates 2,124,639 2,655,799 3,186,959 3,824,350

EBIT 1,016,546 1,316,581 1,617,456 1,976,208

Unlevered FCF 734,882 1,147,588 1,418,243 1,738,070

Undistributed Performance Fees ($mm)1

Potential Clawback($mm)

Credit 359.7 381.2

Private Equity 610.3 1,294.6

Real Assets 145.7 338.8

Total 1,115.7 2,014.6

▪ Represents the maximum fees that could be returned if the

remaining funds were to become worthless

The worst case scenario, going forward Apollo does not do make any new deals and its only source of revenue are existing management fees. This would result in a 21% decline in their stock price.

Base Case:$67.55

40% Upside

Bear Case:$39.98

21% Downside

APOLLO

Extreme Bear Case:$30.30

38% Downside

Assumes growth in AUM and multiple

sources of revenue

▪ If the firm only generated management fees

▪ This represents a 28% drop in revenues and a 43% decline in

EBIT

Firm loses all future deals, and its only

source of revenue comes from existing

management fees

Only source of revenue comes from

management fees and firm must repay

the maximum clawback

Notes: Information as of January 21, 2021.

Source:1.Annual Report 2019

REGULATION INCREASED MARKET VOLATILITYLOSS OF KEY PERSONNEL

RISKS

17

VIX APO S&P

August 2011 43 -42% -17%

December 2018 30 -34% -18%

March 2020 66 -47% -32%

36

38

40

42

44

46

48

20

20

-10

-01

20

20

-10

-03

20

20

-10

-05

20

20

-10

-07

20

20

-10

-09

20

20

-10

-11

20

20

-10

-13

20

20

-10

-15

20

20

-10

-17

20

20

-10

-19

20

20

-10

-21

20

20

-10

-23

20

20

-10

-25

20

20

-10

-27

20

20

-10

-29

20

20

-10

-31

20

20

-11

-02

-22%

▪ October 12: NY Times accuses Leon Black

accused of having deeper times to Epstein

than originally claimed. Apollo stock falls 22%

on the news

▪ If the company were to lose at least two MP’s,

certain funds will be terminated, this would

severely impact revenues from the loss of fees

Sector Impact

Technology -9.20%

Health care -8.40%

Communication -8.2

Consumer discretionary -7.50%

Financials -6.50%

▪ Biden proposal: raise corporate tax rate from

21% to 28%

EXPECTED EARNINGS HIT FROM TAXES

Notes: Information as of January 21, 2021.

Source: 1. Annual Report, 2. CNBC, 3. Investopedia, 4.Bloomberg

▪ Increased market volatility could impact the

value of Apollo’s private equity, and credit

holdings

APOLLO SHARE PRICE ADVERSELY AFFECTED

WITH INCREASED VOLATILITY2

▪ Clawback:

▪ Performance fees that may need to be

repaid

▪ Future losses can result in unjustified

performance fees

The greatest risks to the firm are the Epstein scandal, and the potential for increased taxes on carried interest.

APOLLO

Price per share

Notes: Information as of January 21, 2021.

Source:1.Annual Report. 2. Factset.

EXECUTIVE COMPENSATION 2019GOVERNANCE

18

57%

43%

Independent Insider

Insider Ownership

Management: 10.16%

Board: 7.4%

INDEPENDENT DIRECTORS2

▪ Class B & C shares1:

▪ 100% owned by managing partners

▪ Used to limit influence of class A shareholders

▪ Sole authority to remove and replace directors

▪ Anti-Takeover Provisions:

▪ Limited voting rights for class A shareholders

▪ “BRH” directors have more votes

▪ Supermajority required for amendments

Stock compensation keeps management’s interests aligned with class A shareholders.

APOLLO

Name Insider HoldingsStock

CompensationTotal Annual

Compensation ($)

Leon Black 4.48% 80,000,000 260,175

Joshua Harris - 45,832,643 -

Marc Rowan 3.80% 32,481,402 -

James Zelter 1.20% - -

Scott Kleinman 0.80% - 18,615,204

Martin Kelly 0.13% 2,597,962 5,507,979

John Suydam 0.30% 577,539 4,181,695

17%

83%

Women Men

BOARD GENDER DISTRIBUTION

INVESTING SUSTAINABLY

Notes: Information as of January 21, 2021.

Source:1.Apollo. 2.Lumileds, Verallia, Hexion, Change For Kids

ENVIRONMENT & SOCIAL

19

INVESTING IN THE NEXT GENERATION

Through its investments and donations, Apollo is taking a proactive approach to corporate responsibility.

Capitalizing on the widespread adoption

of LEDs. They are more energy efficient,

have longer lifespans and contain fewer

toxic materials1

Manufactures glass products. Glass can

be recycled infinitely thus reducing the

carbon footprint of glass products

Developed a low temperature curing

powder, reducing its customers’ energy

consumption by 20%

Apollo Women Empower

(AWE) was established to

help facilitate networking and

mentorship opportunities and

advance talented women to

leadership roles

Providing school supplies,

reading lessons, and field

trips to underprivileged kids

in New York

APOLLO

DIVERSIFIED ACROSS

KEY ATTRIBUTES

Notes: Information as of January 21, 2021.

Source:

SUMMARY

20APOLLO

GROWING AUM

DISCOUNT TO PEERS

▪ Providing an attractive return to investors since inception

▪ Using size to their advantage, economies of scale will help keep

costs down and maintain high returns going forward

▪ Industry leader in alternative credit, with a diverse array of

uncorrelated products

▪ Demand from different countries and institutions will ensure stable

growth in a wide variety of market conditions

▪ Trading at a discount to peers and their historical valuation

▪ If the independent committee clears Leon Black, Apollo will go

back to trading at its historical valuation of 25x P/FRE

▪ This provides an excellent buying opportunity in the short term

21

Thank you

Questions?

References:

Intro:https://oneunpark.com/teamhttps://www.genium360.ca/en-us/job/financial-analsyt-2257/

Macrohttps://www.institutionalinvestor.com/article/b1nf5v5h2h97jd/Ultra-Low-Interest-Rates-Are-Driving-Insurers-Into-the-Arms-of-Private-Equityhttps://my-ibisworld-com.lib-ezproxy.concordia.ca/us/en/industry/52599/industry-performancehttps://fred.stlouisfed.org/series/BAMLHYH0A0HYM2TRIV

Limited Partners:https://www.apollo.com/~/media/Files/A/Apollo-V2/documents/events/2015/apollo-investor-presentation-november-2015.pdfhttps://www.apollo.com/~/media/Files/A/Apollo-V2/reports-and-presentations/apollo-global-management-november-2020-investor-presentation-vfinal.pdf

Financial Overview:https://www.apollo.com/~/media/Files/A/Apollo-V2/reports-and-presentations/apollo-global-management-august-2020-investor-presentation.pdf

Investment thesis – Long Termhttps://www.ey.com/en_in/private-equity/how-india-is-emerging-as-one-of-the-leading-destinations-for-global-pe-vc-capitalhttps://www.cambridgeassociates.com/wp-content/uploads/2020/11/WEB-2020-Q2-USPE-legacy-Benchmark-Book.pdfhttps://my-ibisworld-com.lib-ezproxy.concordia.ca/us/en/industry/52599/industry-performanceCyprus, Michael. Kaloostian, Peter. (November 6, 2020). Compelling Value; Upgrade to Overweight. Morgan Stanley Research. Retrieved from ThomsonONE

Risks:https://www.cnbc.com/2021/01/08/how-joe-bidebsproposals-also-have-the-potential-to-affect-holders-of-stocks-and-bonds.htmlhttps://www.investopedia.com/terms/1/3c7.asphttps://www.subpng.com/png-9nyhi5/download.htmlhttps://www.bloomberg.com/news/articles/2020-05-01/apollo-takes-hit-with-asset-values-sinking-in-global-rout

Environment & Social:https://www.france-quintessence.fr/event/exhibitors/veralliahttps://www.avnet.com/wps/portal/silica/manufacturers/m/lumileds/https://www.hexion.com/https://www.vhv.rs/viewpic/ihTwoii_diversity-hands-hd-png-download/https://secure.givelively.org/donate/change-for-kids-inc/cfk-penguin-party-2020/courtney-seamon

Graphs generated using data from FactSet, Yahoo finance and Yearly Presentations

Appendix:https://en.wikipedia.org/wiki/Cox_Media_Grouphttps://en.wikipedia.org/wiki/ADT_Inc.https://en.wikipedia.org/wiki/Qdobahttps://financialpost.com/news/fp-street/apollo-casino-deal-is-approved-after-bid-lifted-to-1-9-billionhttps://ca.finance.yahoo.com/news/apollo-advanced-talks-buy-orbia-021512181.htmlhttps://www.travelpulse.com/suppliers/airlines/united-airlines.htmlhttps://www.archyde.com/apollo-buys-some-of-the-united-airlines-credit-banks-that-are-to-be-dropped/https://www.ft.com/content/1504dda4-ff2e-11e4-8dd4-00144feabdc0https://en.wikipedia.org/wiki/The_Blackstone_Grouphttps://www.aresmgmt.com/https://www.crunchbase.com/organization/kkrhttps://www.acpm.com/ACPM/files/4d/4de27d9d-2a43-4289-a3b6-1105bc845b1b.pdfhttps://en.wikipedia.org/wiki/Kohlberg_Kravis_Robertshttps://en.wikipedia.org/wiki/Apollo_Global_Management#Ares_Managementhttps://en.wikipedia.org/wiki/The_Carlyle_Grouphttp://ir.hamiltonlane.com/investors/financial-information/default.aspx

22

Appendix

24

APPENDIX - SEGMENTSCredit Private Equity Real AssetsCredit AUM($mm)

• Real Estate:

• $22.9B fee generating AUM

• Investing in asset classes such as: hospitality, office

space, industrial, retail healthcare, and residential

• Apollo Commercial Real Estate Finance Inc (ARI) publicly

traded commercial real estate trust

• Debt activities: first mortgage, mezzanine financing,

preferred equity, loans and mortgage-backed securities

• European Principal Finance (EPF) Funds:

• $5.1B fee generating AUM

• European residential, commercial, nonperforming loans,

unsecured loans, and distressed assets

• Moat: capital intensive and illiquid nature of investment

results in low competition in this sector

• Infrastructure:

• $1.7B fee generating AUM

• Midstream energy, renewables, and transportation

• Long lived assets, consistent cash flows, and limited

downside protection

• Focus on investments’ position in capital structure and

current yield

• Distressed buyouts, Debt, and Other Investments:

• Exploit market mispricing and volatility to build up a

position in distressed debt.

• Focus on high quality operating companies with poor

balance sheets

• Downside protection by staying high in the capital

structure

• Distressed for control strategy: take control through

distressed debt, work with management in restructuring,

equitize debt positions and hold for 3-5 years

• Non-control distressed investment strategy: not able to

take control of the company, sell debt investments over

time, results in higher short-term IRR

• Corporate Carve-outs:

• Carving out a business from a larger corporate parent

• Business is typically poorly managed or overlooked,

leading to attractive purchase prices

• Transactions are labour intensive and requires deep

industry knowledge

• Hybrid Capital

• Help companies fund organic growth, acquisitions, or

build ups with customized capital solutions

• Senior unsecured debt, preferred equity securities,

typically linked with equity-linked upside

APOLLO

110.7

52.7

24.2

27.9

Corporate Credit Structured Credit

Direct Origination Advisory and Other

• Corporate credit & fixed income

• $92.6B fee generating AUM

• Investment grade corporate bonds, emerging markets,

and private placements

• Less liquid

• Collagenized Loan Obligations (CLOs):

• Seeking competitive yields, diversified assets with history

of low default rates

• Structured Credit & Funds

• Targets tranches of less liquid securities with protective

lending terms, predictable payments, diversified

portfolios, and low default fates

• Direct Origination:

• Advises clients investing in loans

• First-lien senior secured/unsecured loans, mezzanine

loans, private high-yield debt, asset backed loans etc

• MidCap:

• Middle market subsidy of Apollo, providing senior debt

solutions

• AINV:

• Closed end investment company

• Private financing for companies that don’t have access to

traditional sources of capital

• Advisory:

• ISGI subsidy provides asset allocation & risk management

services to financial institutions acquired by Apollo

FundVintage

YearCapital Raised

($B)Strategy

IX 2018 24.7 Buyout/Distressed

VIII 2013 18.4 Buyout/Distressed

VII 2008 14.7 Buyout/Distressed

VI 2006 10.1 Buyout/Distressed

V 2001 3.7 Buyout/Distressed

ANRP 2018 -- Energy Buyout

ANRP II 2016 3.5 Energy BuyoutSource: Credit Suisse

29.4

7.2

2.2

Real Estate Principal Finance Infrastructure

Notes: Information as of January 21, 2021.

Source: Annual Report 2019

APPENDIX - CREDIT

25

PERFORMANCE FEES ($MM) CREDIT AUM BY SEGMENT ($B)

556642

779

572

30

9

44

1418

28

21

16

0

100

200

300

400

500

600

700

800

900

2017 2018 2019 Q3/2020

Management fees Advisory and transaction fees Performance fees

▪ Corporate credit and direct origination drove growth

in the credit segment over the past three years

Segment Fee %

Management fees 9.6%

Advisory and transaction fees 0.5%

Performance fees 0.3%

Total 10.4%

Appreciation Required to

Achieve Performance Fees

Corporate Credit 3%

Structured Credit 17%

Direct Origination 5%

35 33

98

57

16

36

1825

58

0

20

40

60

80

100

2017 2018 2019

Corporate Credit Structured Credit Direct Origination

Notes: Information as of January 21, 2021.

Source: Annual Report 2019

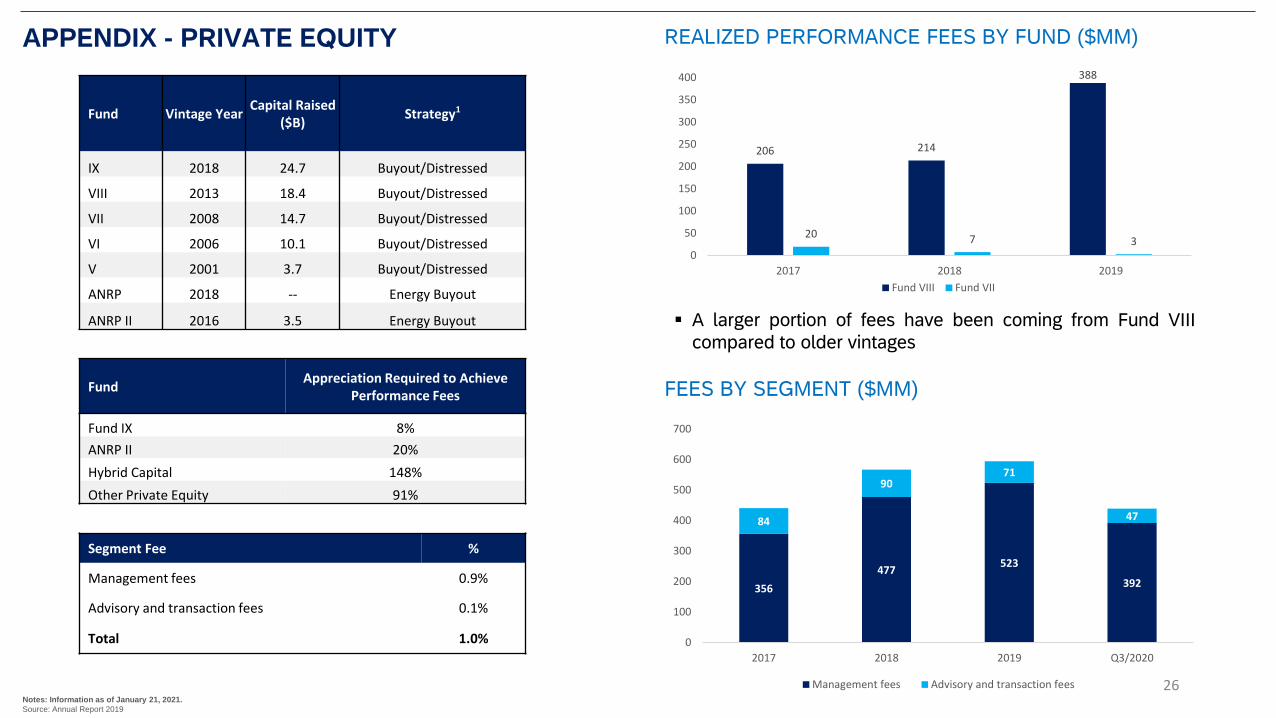

REALIZED PERFORMANCE FEES BY FUND ($MM)APPENDIX - PRIVATE EQUITY

26

206 214

388

20 7 30

50

100

150

200

250

300

350

400

2017 2018 2019

Fund VIII Fund VII

Fund Vintage YearCapital Raised

($B)Strategy1

IX 2018 24.7 Buyout/Distressed

VIII 2013 18.4 Buyout/Distressed

VII 2008 14.7 Buyout/Distressed

VI 2006 10.1 Buyout/Distressed

V 2001 3.7 Buyout/Distressed

ANRP 2018 -- Energy Buyout

ANRP II 2016 3.5 Energy Buyout

Fund Appreciation Required to Achieve

Performance Fees

Fund IX 8%

ANRP II 20%

Hybrid Capital 148%

Other Private Equity 91%

Segment Fee %

Management fees 0.9%

Advisory and transaction fees 0.1%

Total 1.0%

356

477523

392

84

9071

47

0

100

200

300

400

500

600

700

2017 2018 2019 Q3/2020

Management fees Advisory and transaction fees

FEES BY SEGMENT ($MM)

▪ A larger portion of fees have been coming from Fund VIII

compared to older vintages

Notes: Information as of January 21, 2021.

Source: Annual Report 2019

REAL ASSETS AUM ($B)

APPENDIX - REAL ASSETS

27

29.4

7.2

2.2

Real Estate Principal Finance Infrastructure

REAL ASSETS FEE RELATED REVENUES ($MM)

171163

189

140

3 13

7

6

0

50

100

150

200

250

2017 2018 2019 Q3/2020

Management fees Advisory and transation feesSegment Fee %

Management fees 1.86%

Advisory and transaction fees 0.07%

Total 1.93% ▪ Minimum appreciation required to achieve performance fees: 250

bps

Notes: Information as of January 21, 2021.

Source: Annual Report 2019

APPENDIX – DISCOUNTED CASH FLOW MODEL

28

Perpetuity approach

Normalized FCF in last forecast period 3,180,935

Normalized FCFt+1 3,234,056

Long term growth rate (g) 1.67%

Terminal value 31,328,130

Present value of terminal value 19,901,922

Present value of stage 1 CF 8,259,124

Enterprise value 28,161,046

Implied TV exit EBITDA multiple 10.9x

Enterprise value 28,161,046

Less: net debt (1,727,329)

Less: trapped cash (17,694)

Equity value 26,416,022

Diluted shares (000) 445,188

Equity value per share $ 59.34

Market premium/ (discount) to fair value (18.6)%

Exit EBITDA multiple approach

Terminal year EBITDA 2,876,184

Terminal value EBITDA multiple 20.47x

Terminal value 58,875,484

Present value of terminal value 37,402,019

Present value of stage 1 CF 8,259,124

Enterprise value 45,661,143

Implied TV perpetual growth rate 6.6%

Enterprise value 45,661,143

Less: net debt (1,727,329)

Less: trapped cash (17,694)

Equity value 43,916,119

Diluted shares (000) 445,188

Equity value per share $ 98.65

Market premium/ (discount) to fair value (51.0)%

WACC = 11.99%

▪ Using a WACC of 11.99% and long term growth rate of

1.67% an equity value of $59.32 was derived

▪ At this valuation, we can imply an exit multiple of 10.9x

EV/EBITDA

▪ Using the industry average EV/EBITDA exit multiple of

20.47x, we can derive an equity value of $98.65

▪ This method implies a higher value per share because

the industry average is higher than Apollo current

multiple of 18.4x

APOLLO

APPENDIX – GENERAL COMPS

Company EV/EBITP/E

NTM

P/B

NTM

P/CF

NTM

Hamilton Lane 29.1x 36.0x 11.4x 22.2x

Blackstone Group 15.9x 20.8x 8.1x 19.5x

Carlyle Group 15.0x 15.0x 5.3x 32.1x

Ares Management Corp 31.8x 21.6x 7.7x 20.5x

KKR & Co 11.8x 18.7x 1.7x 10.9x

Average 20.7x 22.4x 6.8x 21.1x

Median 15.9x 20.8x 7.7x 20.5x

Apollo Global 19.9x 18.4x 8.6x 19.0x

Notes: Information as of January 21, 2021.

Source: Factset

APPENDIX – PEER GROUP

Notes: Information as of January 21, 2021.

Source: Wikipedia, Archyde, Orbia. Wikipedia. Hamilton Lane Investor Relations. FactSet

One of the largest investors in leveraged buyouts and heavily involved in commercial

real estate. It is the largest of the whole cohort in terms of market cap. Operates in:

Private Equity, Real Estate, Hedge Fund Solutions and Credit.

Operates in private equity, energy, infrastructure, real estate, credit, and strategic

hedge funds. Trades at a lower multiple because its primary source of revenues are

not management fees but investment income which is riskier.

Initially established as a segment of Apollo’s collateralized debt obligations. In 2002 it

was spun out from Apollo and has operated as an independent business development

company.

Operates in corporate private equity, real assets, and private credit. It is the second

largest private equity firms in terms of capital raised.

Designs customized portfolios, design and invest in specialized funds, provide advisory

services in asset allocation and strategic plan creation. Because they have a more

service-based offering, they get a higher % of revenues from management fees.

APPENDIX - STRATEGIES

Strategy Description

ADIP Apollo/Athene Dedicated Investment Program. $10M unfunded.

Infrastructure EquityPart of real assets. Acquisition and recapitalization of realestate and infrastructure assets, portfolios, platforms and operating companies.

Aircraft Lending Acquired PK AirFinance in December 2019. PK AirFinance, a aircraft lending business, acquired the PK AirFinance aircraft lending platform and Athene acquired PK AirFinance’s existing portfolio of loans.

Hybrid Value

Launched in 2018. Pursues the provision to companies of: rescue financing or customized capital solutions, including senior secured and unsecured debt or preferred equity securities, often with equity-linked or equity-like upside. Typically, in these scenarios, companies are looking for an equity partner to fund initiatives such as organic growth, acquisitions, deleveraging or build-ups.

CLOsEmploys structured credit and performing credit strategies with the goal of providing investors with competitive yields achieved through highly diversified pools of historically low defaulting assets

Asia real estate equity funds

Primary focus on investing in China, India and Southeast Asia, while executing Apollo’s strategy of opportunistic value investing.

Notes: Information as of January 21, 2021.

Source: Annual Report 2019

APPENDIX – HOLDINGS

American media

conglomerate. Owned by

Apollo and Cox Enterprises.

Operates radio and TV

stations serving the pacific,

south, Eastern Midwest and

North East of the US.

Acquired in December 2019

for $3.1B

Provides residential and

business security solutions.

Fire alarms and other

monitoring services. Acquired

by Apollo in February 2016

for $6.9B in a leveraged

buyout. It was purchased at a

premium of 56% above ADT’s

share price.

Notes: Information as of January 21, 2021.

Source: Wikipedia

Fast casual chain of restaurants

operating in the US and

Canada. Offering Mexican style

dishes. In 2018 they operated

over 700 locations. Acquired by

Apollo in March 2018 for

$305M.

APPENDIX – RECENT & ONGOING DEALS

Operates 25 properties of

casinos, horse tracks and

gaming centers. Also runs

hotels and restaurants. Apollo

acquired the Canadian

company in December of

2020 for $1.9B of 45$ per

share. Apollo plans to bolster

growth through loyalty

programs. This complements

Apollo’s existing gaming

holdings such as Caesars

Entertainment.

Headquartered in Mexico city.

Orbia operates five brands

focusing on food security,

water scarcity, and health &

wellness through materials.

Apollo is currently in talks to

purchase Orbia’s vinyl

business. The business unit is

estimated to be worth $2B.

Apollo has existing operations

in companies with its holdings

of Lyondell.

The COVID -19 pandemic put

airlines in a strained position

to maintain liquidity. Apollo

sensed this opportunity and in

March 2020, they purchased

part a $2B bank loan. This fits

in with their investment

strategy of buying during

times of uncertainty.

Notes: Information as of January 21, 2021.

Source: Wikipedia, Archyde, Orbia

Notes: Information as of November 30, 2020.

Source:1.EY

34

67%

80%

59%

52%

83%

58%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2014 2015 2016 2017 2018 2019

Expense margin

Expense Margin

55%

89%

53%44%

123%

54%

0%

20%

40%

60%

80%

100%

120%

140%

2014 2015 2016 2017 2018 2019

Management Fee margin

EXPANSION TO INDIA

0.72 2

4.1

11.6

2.2

1.91

6.3

4.6

0

2

4

6

8

10

12

14

16

18

2015 2016 2017 2018 2019

Real Estate & Infrastructure Buyouts Traditional PE buyouts

▪ PE/VC investments in India have grown at a CAGR of

44%1

▪ Apollo is establishing a foothold in this fast growing

market through its ARCION Revitalization Private Limited

and AION India Opportunities Trust

BUYOUT ACTIVITY IN INDIA

APPENDIX - MISCELANIOUS

REGULATION INCREASED MARKET VOLATILITYLOSS OF KEY PERSONNEL

APPENDIX - RISKS

35

VIX APO S&P

August 2011 43 -42% -17%

December 2018 30 -34% -18%

March 2020 66 -47% -32%

36

38

40

42

44

46

48

20

20

-10

-01

20

20

-10

-03

20

20

-10

-05

20

20

-10

-07

20

20

-10

-09

20

20

-10

-11

20

20

-10

-13

20

20

-10

-15

20

20

-10

-17

20

20

-10

-19

20

20

-10

-21

20

20

-10

-23

20

20

-10

-25

20

20

-10

-27

20

20

-10

-29

20

20

-10

-31

20

20

-11

-02

-22%

▪ October 12: NY Times accuses Leon Black accused of having

deeper times to Epstein than originally claimed. Apollo stock

falls 22% on the news

▪ This shows simple accusations can have a severe impact on

the stock price in the short term

▪ Three managing partners at Apollo1:

▪ Leon Black

▪ Joshua Harris

▪ Marc Rowan

▪ Company does not carry “key man” insurance in the case of

death or disability for any MP

▪ If the company were to lose at least two MP’s, certain funds

will be terminated, this would severely impact revenues from

the loss of fees

▪ This is true for example of Fund VIII and Fund IX

Sector Impact

Technology -9.20%

Health care -8.40%

Communication -8.2

Consumer discretionary -7.50%

Financials -6.50%

▪ With Democrats controlling the white house and congress,

there are concerns of increased regulation and taxes2

▪ Biden proposal: raise corporate tax rate from 21% to 28%

EXPECTED EARNINGS HIT FROM TAXES

▪ Investment Company Act: as a private equity firm, Apollo

qualifies for the 3C7 exemption:

▪ Allows them more freedom to take on leverage

▪ If they were to lose this exemption status, the

increased restrictions could impact revenues3

Notes: Information as of November 30, 2020.

Source:

1. Annual Report, 2. CNBC, 3. Investopedia, 4.Bloomberg

▪ Increased market volatility could impact the value of Apollo’s

private equity, and credit holdings

▪ During COVID-19 pandemic4:

▪ Private equity holdings declined 22%

▪ Athene holdings declined 47%

APOLLO SHARE PRICE ADVERSELY AFFECTED

WITH INCREASED VOLATILITY2

▪ Clawback:

▪ Performance fees that may need to be repaid

▪ Future losses can result in unjustified performance

fees

APPENDIX – GOVERNANCE

Leon BlackFounder

CEO

Josh HarrisCo-Founder

Marc RowanCo-Founder

Managing Director

James ZelterCo-President

CIO, Credit

Experience as an

entrepreneur, running

seven different

companies. Former

employee of Drexel

Durham. Leader at

Apollo for 31 years.

Founded five different

companies. Sits on the

board of 11 other

companies. Member of

Apollo’s board for 31

years.

Co-founder of Apollo

and held a seat on the

board of directors for 31

years. Board member of

16 other companies.

Also holds a leadership

role in the Youth

Renewal Fund.

Held a leadership

position at Apollo for

15 years. Prior CIO to

Citigroup Alternative

Investments and a

trader at Goldman

Sachs.

Notes: Information as of November 30, 2020.

Source: FactSet, Apollo Website