anticipating restructuring in the european defence industry

TRANSCRIPT

December 13&14, 2007

© BIPE 2007

Anticipating restructuring in the European defence industry

Overview of the studycoordinated by Dr. E. Waelbroeck-Rocha

at BIPE, with contributions fromProfessor Dr. H. Wulf, Dr. P. Wilke,

Mr. O. Bergstrom, Mr. D. Sellier, Mr. F. Bruggeman and J. Ganczewski

Final report overview2© BIPE 2007

Outline

Developments during the past decade and present industry structureDefining the defence industryOverview of demand trends: budgets, procurement, R&D expenditure, trade, competitiveness and market access conditionsTrend in employmentOrganisation of supply and changes therein: activities covered, key European defence producers, production location and country specialisations, trend in M&A, ownership structure, cross-border collaboration

ChallengesOutlook

Key factors influencing the futurePossible future scenarios

Anticipating change: examples of innovative practices

Final report overview3© BIPE 2007

Defining the defence industry

The defence sector is not a clearly defined industrial branch:In the literature, “defence” companies are said to produce “weapon systems”, “defence products”, “military equipment”, “arms” or “dual-use goods”, as well as components of these products and associated servicesThe term “dual-use” indicates that the defence sector borders with other sectors (civil aviation, vehicles, ship building, electronics, IT and others)

As illustrated on the next page, companies can be prime contractors (lead system integrators, platform producers and producers of weapon systems), sub-contractors (producers of sub-systems or major components) and third tier contractors (producers of components), usually SMEs, often producing dual-use goodsSMEs involved in defence produce small arms and ammunitions, low calibre artillery, military vehicles, small ships, military electronics, subsystems for weapons and componentsMany defence producers – mainly large but also some small - are involvedat several levels of the supply chain

Final report overview4© BIPE 2007

Organisation of the supply chain: the defence industry’s tier structure

LEAD SYSTEM INTEGRATORSAeronautics

System developersand platformassemblers

Engines / propulsion

manufacturers

Specialised systems producers(electronics, …)

Space & missilesSystem developers

and platformassemblers

Land defenceSystem developers

and platformassemblers

Naval industrySystem developers

and platformassemblers

Complete sub-systemsproducers & assemblers

Electrical & electronicequipment

Mechanicalengineering

Metal working, casts & moulds Etc…

Commoditysuppliers

General servicesuppliers

Basic economicinfrastructure

Prime contractors

Tier 1contractors

Tier 2contractors

Tier 3contractors

Final report overview5© BIPE 2007

There are several tiers of contractors

Prime contractors produce weapon systems:These are mainly large companies specialised on defence production and servicesSome are Lead System Integrators, i.e. assemble defence systems from several defence domains (ex: aircraft carrier), others are specialised in only one area (aerospace for example)Examples in the EU are BAE Systems (UK), EADS (Netherlands), Thales (France) and Finmeccanica (Italy), the later specialised in helicopters and armoured vehicles, and Saab (Sweden) for fighter aircraft, Nexter (France) and Krauss-Maffei-Wegmann(Germany) in major battle tanks, Thyssen Krupp (Germany), Fincantieri (Italy) and DCNS (France) in naval vessels.

Tier 1 contractors produce complete sub-systems or major components. Often, these are also risk sharing partners:

These are often specialized firms (engines, electronics,…), subcontracted by the prime contractors. Examples are Rolls Royce (UK), Groupe Safran (France), MTU (Germany) and Indra(Spain)

Tier 2 contractors produce components and supply servicesUsually small and medium enterprises (SME) or subsidiaries of the major defence producers (prime contractors and sub-contractors), these often produce dual-use goods or services These companies are not always listed as defence producers since they operate at the margin of the defence sector

Tier 3 contractors are commodity suppliers or supply generalist services. This levelalso includes all providers of « general economic infrastructure » services (transport network and services, communications, externalised training, etc.)

Final report overview6© BIPE 2007

Many sectors and sub-sectors are involvedalong the supply chain. Some are highlyspecialised, others are commodity producers

The example of an aeronautics clusterAssemblage etConstructionaéronautique

Fabrication demoteurs et turbines

Fabrication et rechapage depneumatiques

Colles, adhésifs

CaoutchoucNaturel et

synthétique

Aluminium

Servicesaéroportuaires

Matériauxd’emballage

Infrastructures deTransport

PRODUITSSERVICES CLES

MACHINES ETEQUIPEMENTS

PRODUITS INTERMEDIAIRES

INDUSTRIESDE BASE

INDUSTRIES ETSERVICES DESUPPORT

INFRASTRUCTUREÉCONOMIQUE DEBASE

Composantsaéronautiques

Pompes,Compresseur,

Syst. hydrauliques

Transformation dematières plastiques

Industrie textile/confection

Métaux ferreux

Marketing/Publicité

Universités,centres de formation

Peintures,Vernis

Rénovation(Niveau 6)

Fabricationde verre plat et de

fibres de verre

Industrie du bois

Forge,emboutissage,

estampage

Design, R&D

Laboratoires derecherche

Produitsd’entretien

Robots,Machines outils

Entretienmaintenance

Fabrication de Céramiques

avancées

Production desPlastiques de base

Laminage,Profilage,tréfilage

Distributiontransport

Fédérationsprofessionnelles,

syndicats

Huiles,Lubrifiants

Equip. électriqueset électroniques

Injection deplastiques

Ferro-alliages

Evironnementinstitutionnel

Equipement delevage

manutention

Cables, tuyaux,Petit matériel

Services financiers

Bureaux d’étude LogistiqueServices de transport

Services auxentreprises

Final report overview7© BIPE 2007

The risk-sharing partner concept

« Risk- and revenue-sharing » is a system whereby the developmentcosts of new systems or equipments is distributed across the prime contractor and its « partners »Under this system, prime contractors delegate the responsibility for conceptualising, designing, developing and producing the new system, as well as the responsibility for financing the development costsThe associated expenditures are, by nature, investment costs, yet in accounting terms these are considered to be operating costs (there are activation methods)The costs are paid back by the prime contractor to the risk-sharing partners as sales are realised: the partnership, therefore, also impliescommercial risk sharingFor the partner, the depreciation (and reimbursement) of expenses istherefore uncertain, both in terms of the amount of pay-back and in terms of the duration of the financingFor major defence projects, development costs are typically financed by Governments

Final report overview8© BIPE 2007

Outline

Developments during the past decade and present industry structureDefining the defence industryOverview of demand trends: budgets, procurement, R&D expenditure, trade, competitiveness and market access conditionsTrend in employmentOrganisation of supply and changes therein: activities covered, key European defence producers, production location and country specialisations, trend in M&A, ownership structure, cross-border collaboration

ChallengesOutlook

Key factors influencing the futurePossible future scenarios

Anticipating change: examples of innovative practices

Final report overview9© BIPE 2007

On the demand side, the key factors of influence are both European and global

European:Changing role of force new demand mixStagnant or declining overall defence budgets within the EUShrinking national defence procurementComparatively low spending on R&D

Global:Lack of dynamism of world market demandDifficult entry conditions in the more dynamic markets

Final report overview10© BIPE 2007

The past trends in military budgets

The past trend in military expenditures has shaped the present structure of the European defence industry and the restructuring process that took place during the last decade and a half in the EU:

As a result of the ‘peace dividend’ in the first half of the 1990s, the defence industry suffered from the reduction of procurement orders (both national procurement as well as arms exports). World military expenditure decreased from a total of over 1 trillion US $ at the end of the Cold War to less than 800 billion US $ in the mid 1990sThe eastern European countries also suffered from the break-up of the Warsay TreatyAfter an adjustment period, world military budgets have constantly increased. They reached 1.2 trillion US $ in 2006.

Combined EU MS’ military expenditures amount to below €200 billion annually, of which more than €80 billion worth of procurement, R&D and maintenance expenditureIn contrast to the United States, procurement expenditure in the EU has remained fairly stable in recent years. The increase of procurement budgets in Europe between 2000 and 2006 was minimalThe US military budget amounts to US $550 billion, more than double the combined defence budget of the 27 EU countries

Final report overview11© BIPE 2007

World military budgets

0

200

400

600

800

1000

1200

1985 1990 1995 2000 2006

World totalEU

in billion US $ (constant)

Source: SIPRI

Final report overview12© BIPE 2007

Trend in procurement budgets

0

20

40

60

80

100

120

140

2000 2001 2002 2003 2004 2005 2006

USA NATO-Europe

in billion US $ (2005 prices and exchange rates)

Source: SIPRI

Note:

NATO-Europe is not a single entity, hence the trend illustrated reflectsthe sum of national budgets

Final report overview13© BIPE 2007

Overview of 2005 shares of worlddefence budgets

31%Rest of the world(165 countries, includingChina, Russia, Indiaand Japan)

42522%EU

1 38347%US

Defence expenditureper capita (in US$)

Budget share of world total defence budgets

Final report overview14© BIPE 2007

In the future, the EU-27 defence budgets willgrow between 0.5 and 2% per year in real terms

Possible trend in the EU-27 total defence budgets between 2006 and 2015, in billion € at constant 2006 prices

-

50

100

150

200

250

300

2006 2015

+ 0,5%

+ 2,0%

Based on constant defence budget shares

Based on trend-defence budget shares

Source: national statistics, BIPE forecast

Final report overview15© BIPE 2007

The defence budget shares currentlyvary susbstantially across the EU-27

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

Greece

United Kingdom

France

Bulgaria

Portugal

TOTALRomania Ital

yPolan

dDenmark

Czech Republic

Slovakia

Latvia

Netherl

andsSwedenHungarySloven

iaEsto

niaGerm

anyFinlan

dCyprus

LithuaniaSpain

Belgium

Austria

LuxemburgMaltaIrel

and

Share of GDP in 2006 Share of GDP in 2015 - no change Share of GDP in 2015 - trend growth in budget

Defence budget as a % of GDP per country, in 2006 and two assumptions for 2015

Source: national statistics, BIPE forecast

Final report overview16© BIPE 2007

At best, the defence budgets will amountto 255 billion € in 2015, at 2006 prices

By 2015, depending on the trends in national budget spending, the share of expenditures on defence will bebetween 1.6% and 2.1% of total EU-27 GDPThis is equivalent to an annual growth of total defencebudgets between 0.5% and 2% in real termsThe total value of 2015 budget at 2006 prices will at most be250 billion €A figure of 221 billion €, barely 5% above the 2006 level in real terms, is, however, also possible

Final report overview17© BIPE 2007

Trend in RTD expenditures

RTD expenditures are an investment into the futureR&T expenditures are a subset of R&D spent which apply to expenditure for basic research, applied research and technology demonstration for defence purposes

In 2005, the EU countries spent approximately € 2.2 billion on defence RTD. In 2006, the figure increased to € 2.5 billion This amounts to one-sixth of the US RTD expenditure on defence On average, the EU Member States allocate 1.14% of their military budget to RTD expenditures, compared with 3.31% in the United States

Final report overview18© BIPE 2007

International comparison of R&T spent

Source: EDA

Final report overview19© BIPE 2007

Comparison of European and US R&T expenditure

Note that the EU is not a single entity but composed of 27 separate markets – which increases the gap with the USA

Final report overview20© BIPE 2007

Trend in world arms trade

European companies play a major role in world trade: combined EU exports of all MS (before correction for intra-EU trade) presently account for close to 25/% of the world totalThe global arms trade dropped considerably after the end of the ColdWarThe western European countries were not affected to the same extent as other producers, especially from the former Soviet Union and eastern Europe. The latter countries suffered both from the decline in world trade and from the collapse of the Warsaw PactTotal arms transfers fluctuated in the mid 1990s and early 2000s. Since 2002, the trend is again clearly upward oriented.Based on official sources1, the value of arms exports was over 15 billion US $ in 2005 (the last year of reporting).

1: EU Member States governments

Final report overview21© BIPE 2007

Trends in arms exports by the main EU producing countries (Germany, France, UK, Netherlands, Italy, Sweden, Spain)

0

5

10

15

20

25

30

35

40

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

globalEU

SIPRI data refer to actual deliveries, allowing for comparisons between transfers of different weapons. SIPRI uses a trend-indicator value and not the actual financial value of a transfer.

SIPRI trend indicator, in million US $ (major conventional weapons only)

Note: the EU is not a single entity. EU data applies to the sum of country figures

Final report overview22© BIPE 2007

Global arms transfers : world market shares (2002-2006 – major conventional weapons)

30%

29%

31%

10%

USARussiaEUOthers

The shares in world markets (including sale of used weapons) of the US, Russia and the EU Member States are of comparable size

Final report overview23© BIPE 2007

Value of arms exports by the major EU producers

970831480Italy

8912

419

682

925

1630

3016

3711

2005

845624Spain

95559938EU total

808406Netherlands

1129780Sweden

11641129Germany

23842975UK*

39786952France

20062004In million €

Source: Official Journal of the EU: 7th, 8th and 9th Annual Report on Arms Exports•For the UK = value of licenses; all others : value of exports•http://www.consilium.europa.eu/cms3_fo/showPage.asp?id=408&lang=en&mode=g#exp4

Final report overview24© BIPE 2007

The EU competitiveness status

One indication of the relative competitiveness of EU-based defence producers is the origin of imports of major equipmentAn analysis of the origin of imports of three categories of major conventional weapons (naval vessels, combat aircraft and major battle tanks) shows that US companies have a technological dominance in certain areas of the defence sector, but not in allThe European Defence Technology Industrial Base (EDTIB) seeks to address some of those concernsIt is not only the technological dominance of the US industry which is responsible for the imbalance in transatlantic trade. It is also due to trade restrictions in the United States (US Buy America Act) which make entry into the largest defence market of the world difficult for foreign firmsThe US dominance is also reflected in the fact that European companies have captured only a small margin of the US procurement market, while US companies won about one quarter of the European market

Final report overview25© BIPE 2007

Sources of imported military equipment

89

EUNon-EU

52

102

EUNon-EU

2

779

EUNon-EU

Naval Vessels Combat Aircraft Major Battle Tanks

From 2001 to 2006, more than half of the imported naval vessels (national production not included), two-thirds of all imported combat aircraft and only 2 of a

total of 781 major battle tanks were imported from non-EU countries.

Final report overview26© BIPE 2007

The changes in market accessconditions within the EU

A range of political and legal guidelines have been designed, and institutions founded, to improve coordination, internationalise procurement and encourage competition:

In 1991, the Maastricht Treaty laid the ground for an Intergovernmental Arms Agency, OCCAR was createdMore recently, the EDA has been formed

The joint efforts to coordinate procurement, increase competition and overcome protectionism have included, among others:

the Letter of Intent (LoI), the Framework Agreement, the Harmonisation of Military Requirements (HMR), the European Headline Goalsthe creation of a joint 55 million € Joint Investment Programme on Force ProtectionThe Code of Conduct to establish a voluntary, non-binding intergovernmental regime

However, despite all efforts, one is far from a Single European Defence MarketStill less than one fifths of procurement is spent in collaboration projects in which at least two EU members participate.

Final report overview27© BIPE 2007

The conditions of Article 296

Article 296 TEC allows Member States to derogate from Internal Market rules when their essential security interests are at stake:

Article 296(1)(b) allows for measures "connected with the production of or trade in arms, munitions and war material", specified in a list. According to a court ruling Article 296(1)(b) TEC "is not intended to apply to activities relating to products other than the military products identified on [that] list".

As a result, Europe's defence sector remains fragmented at national level, with 27 different customers and 27 different regulatory frameworks.Article 296 creates extra costs and inefficiencies, and thus has a negative impact on the competitiveness of Europe's Defence Industrial and Technological Base as well as on Member States' efforts to equip their armed forces adequately.

Final report overview28© BIPE 2007

Outline

Developments during the past decade and present industry structureDefining the defence industryOverview of demand trends: budgets, procurement, R&D expenditure, trade, competitiveness and market access conditionsTrend in employmentOrganisation of supply and changes therein: activities covered, key European defence producers, production location and country specialisations, trend in M&A, ownership structure, cross-border collaboration

ChallengesOutlook

Key factors influencing the futurePossible future scenarios

Anticipating change: examples of innovative practices

Final report overview29© BIPE 2007

Different categories of employment have to distinguished – all of which are related to defence industries

Direct employmentin prime contractors,

exclusivelyrelated to

defence activities

Direct employmentin tier 1 contractors,exclusively related to

defence activities

Part of employmentin tier 2 contractors,

linked to thedefence contracts

Direct employmentin prime contractors,In civilian activities

Direct employmentin tier 1 contractors,In civilian activities

Otheremployment

in tier 2contractors

Indirect employment = employment in related (tier 3 and higher) industries

Final report overview30© BIPE 2007

Estimates of direct employment vary between350 000 and 750 000. Including indirect employment, 1 640 000 persons are concerned

In 2003, the direct employment in defence industries in the EU-27 was estimated at approximately 750,000 employees, less than half theemployment level at the end of the Cold War (1.5 million in 1993) The ASD estimates total employment in aerospace (incl. civilian aeronautics), and defence at 594 000 in the EU-27 in 2005. This, however, mainly covers the prime and tier 1 contractors.In the Defence Communication, the EC quotes 300,000 employees, based on the ASD estimate, of which 98 000 are employed in land defence industries; 63,000 in the naval industries and 150 000 in military aeronautics industriesBottom-up calculations indicate that the above numbers underestimate employment in subcontractor and related industries. For example:

In the UK, official figures indicate 170 000 direct jobs in defence industries, plus 140 000 indirect jobs, totalling 310 000 jobs in 2005In the Midi-Pyrénées region of France, there are more than 1,000 industrial SMEs working as subcontractors. Of the 94 000 jobs in the region, 50 000 are subcontracted jobs.In the Navantia shipyard (Ferrol), in Spain, there are 2 500 jobs in companies subcontracted by Navantia, which itself counts 5,560 jobs in 2005, a ratio of 1 to 2.

Final report overview31© BIPE 2007

Estimates of direct employment vary between350 000 and 750 000. Including indirect employment, 1 640 000 persons are concerned

The next side shows the estimated number of jobs directly or indirectly concerned by trends in the defence industry.The figures are bottom-up estimates and subject to revisions, given the difficulty in allocating employment between defence and civilian activities within a given companyIn summary, one estimates that there are approximately 405 000 jobs in prime and tier 1 defence companies that are directly involved in the production of defence industry products, and 418 000 jobs in the civilanpart of the prime and tier 1 companies.There is likely to be another 350 000 jobs in tier 2 companies, i.e. working on the production of goods and services used by Tier 1 and primecontractors, and close to 470 000 additional employments in related industries (essentially commodity goods and services producers). In total, 1 644 000 persons are concerned, directly or indirectly, by trends in defence markets and European defence production

Use of I-O tables indicates an average employment multiplier of 0.45 in equipment goods producing industries, used to estimate the employment estimate in Tier 2 and higher companiesTier 2 employment directly related to defence production is based on an multiplier of 0.4, and that in civilian activites of 0.45. The figure are consistent with estimates for France and the UK.

Final report overview32© BIPE 2007

Estimated employment by type of activity in EU-27

Direct employmentin prime contractors,

defence only:211 500

Direct employmentin tier 1 contractors,

defence only:193 500

Employmentin tier 2 contractors,

linked to defence:162 000

Direct employmentin prime contractors’

civil production:160 700

Direct employmentin tier 1 contractors,in civil production:

256 500

Otheremployment

in tier 2Contractors:

188 000

Indirect employment = employment in related (tier 3 and higher) industries470 000

Final report overview33© BIPE 2007

Trends in employment by country

Based on the BICC data, the decline in employment was particularly pronounced in the second half of the 1990s. The process has slowed down considerably in recent years: reductions are now due to efficiency gains in the production processDifferent groups of countries can be distinguished:

1st block : relatively stable employment levels between 1993-2003

Greece, Finland, Denmark2d block: major drop in employment between 1993-1998, followed by further reductions between 1998 and 2003

This block includes the LoI countries (except Sweden), plus Belgium3d block: continuous reduction in employment throughout the period:

In the eastern European countries, employment in the defence industries decreased in the range of 50-90 %Poland, Slovakia and Estonia were the worst hit

Final report overview34© BIPE 2007

Change in employment levels acrosscountries, base 1993=100

0102030405060708090

100France

United Kingdom

Germany

Italy

Spain

Sweden

Belgium

Bulgaria

Romania

HungaryCzech Republic

Estonia

Slovakia

Poland

Netherlands

Portugal

Austria

Denmark

Finland

Greece

199319982003

Final report overview35© BIPE 2007

151515Greece

151830Czech Republic

182660Romania

202550Spain

252775Bulgaria

252634Sweden

263550Italy

5070120Poland

8095160Germany

200280380UnitedKingdom

240266345France

200319981993

7729711522

n. a.: Cyprus, Ireland, Malta, Latvia, Lithuania, Luxemburg, Slovenia

227Hungary

334Austria

555Denmark

559Portugal

6815Belgium

72075Slovakia

101018Netherlands

101010Finland

102560Estonia

200319981993

Estimated workforce, in thousands

* All countries listed are members of the EU in 2007. Source: BICC Conversion Survey 2005, pp. 167-168

Despite the uncertainty on the exact employment levels, the overall trend has always been downward oriented

Final report overview36© BIPE 2007

In the UK, official statistics estimate indirect employment as 0.82% of total direct employment in the defence industries

1997/98 2000/01 2001/02 2002/03 2003/04 2004/05Total employment:Direct Indirect

340 160 180

300 155 145

295 155 140

305 165 140

315 170 145

310 170 140

Employment from MoD equipment expenditure: Direct Indirect

145 70 75

135 70 65

140 75 65

160 85 75

155 85 70

150 80 70

Employment from MoD Non-equipment expenditure: Direct Indirect

95 50 45

95 55 40

95 55 40

85 50 35

95 55 40

90 55 35

Employment from defence exports: Direct Indirect

110 45 65

70 30 35

60 30 30

60 30 30

65 30 30

65 35 35

Source: MoD/DASA (2006). Defence Statistics 2006, TSO, London

Employment in UK defence industries, in thousand

Final report overview37© BIPE 2007

In most countries, the fall in employment in defence industries was much more pronouncedthat that of total manufacturing employment

60

70

80

90

100

110

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Defence Industry in FranceMetal-working industries in FranceIndustry total (excl. Energy)

Trend in employment in France – 1993 = 100

Final report overview38© BIPE 2007

Other issues related to employment

Skill shortages are starting to develop in the easternEuropean countries, due to ageing of the workforce and emigration patternsThe age structure of workers in industry is skewed to the right, as for other manufacturing sectors: there will be a highnumber of departures for retirement The defence sector employs a comparatively high share of technical and high-skills level, which are also in short supplydue to overall socio-demographic changes and relative lack of attractiveness of industrial sectors compared to services

Final report overview39© BIPE 2007

0%

5%

10%

15%

20%

25%

30%

35%

0-25 25-35 35-45 45-55 55-65

Age structure in industry, in total and by skill type – the case of France in 2005

Engineers &white collarworkers

Blue-collarworkers

% of workforce

Total salaried employment

Source: based on the Labour Force Surveys, INSEE

Final report overview40© BIPE 2007

Defence industries employ personnel with comparatively high skill levels

Graduates, engineers, managers etc.; 28%

Manual workers; 38%

Others; 34%

Source: ASD

Composition of employment in aeronautics and defence, by skill level

Final report overview41© BIPE 2007

Outline

Developments during the past decade and present industry structureDefining the defence industryOverview of demand trends: budgets, procurement, R&D expenditure, trade, competitiveness and market access conditionsTrend in employmentOrganisation of supply and changes therein: activities covered, key European defence producers, production location and country specialisations, trend in M&A, ownership structure, cross-border collaboration

ChallengesOutlook

Key factors influencing the futurePossible future scenarios

Anticipating change: examples of innovative practices

Final report overview42© BIPE 2007

On the supply side, the key factors of influence are :

The large variety, high technicity and rapidly rising production cost of defence equipment and systemsThe dominance of (often national) champions, highlydependent on trends in national procurement budgetsThe high dependence of certain regions on defence activitiesThe transition phase which the industry in eastern Europe isgoing through(Past and future) M & A patternsThe growing concentration of the industryThe particular ownership structure (with governments as major shareholder in France and Italy)Mixed experiences with cooperation

Final report overview43© BIPE 2007

A large range of activities

The defence sector is very diverseThe companies are engaged in the production of:

small arms/ammunitionartilleryaircraftselectronicsenginesmissilesmilitary vehiclesshipsspaceservices (incl. support, training, …)Etc.

… plus all the inputs (products and services) and equipments (machinery, buildings, infrastructure) that are used at some stage during the productionprocess

Final report overview44© BIPE 2007

The main EU defence producers in a global perspective

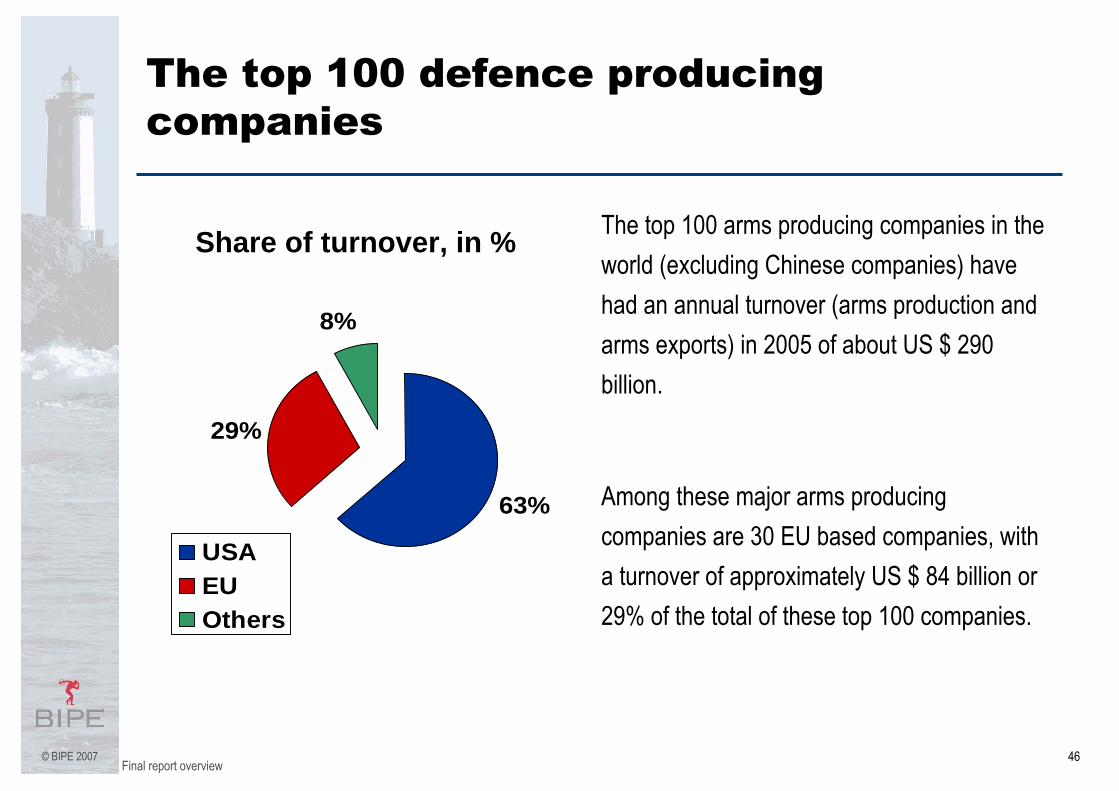

There are 30 EU based companies amongst the top 100 arms producing companies in the world (excluding Chinese companies)With a turnover of approximately US $ 84 billion in 2005, the 30 largest EU companies accounted for 29% of the total turnover of about US $ 290 billion of the top 100 companies.Among the top 10 arms producing companies there are four EU-based companies: BAE Systems (UK), Finmeccanica(Italy), EADS (headquartered in The Netherlands) and Thales (France).

Final report overview45© BIPE 2007

Ranking of EU companies among the top 100 defence producers

Ranking in top 100 Number of EU-based companies

1 – 10 411 – 25 526 – 50 651 – 100 15

Final report overview46© BIPE 2007

The top 100 defence producing companies

63%

29%

8%

USAEUOthers

Share of turnover, in % The top 100 arms producing companies in the world (excluding Chinese companies) have had an annual turnover (arms production and arms exports) in 2005 of about US $ 290 billion.

Among these major arms producing companies are 30 EU based companies, with a turnover of approximately US $ 84 billion or 29% of the total of these top 100 companies.

Final report overview47© BIPE 2007

Defence activities typically account for a high share of the total turnover of the largest EU producers

0 20 40 60 80 100

RheinmetallSaab

DassaultSAFRAN

Rolls RoyceDCNS

ThalesEADS

FinmeccanicaBAE Systems

Defence sales 2005 - Source SIPRI

Among the top ten EU defence producers, only DCNS has no civil production; the other companies (BAE Systems, Finmeccanica, Thales, Dassault and Saab) have a share of

defence production of over 50%.

Final report overview48© BIPE 2007

Role of EU companies

Two principal conclusions can be drawn from company statistics:

(1) EU based defence production is of global importance(2) The high percentage of arms sales of the 40 US companies (63% of the total) highlights the US dominance in the defence sector.

In addition to the major defence producers, there are literally hundreds of companies engaged in defence production, with location throughout the EU

Final report overview49© BIPE 2007

(UK) 34,980 m.$

(France) 25,870 m.$

(Spain) 1,640 m.$

(Sweden) 2,110 m.$

(Netherland) 14,620 m.$(Germany) 6,520 m.$

(Italy) 18,240 m.$

Source: SIPRI Data base

Arms Sales of Major EU Companies(in million US $, at 2005 prices and exchange rates)

weiter

Final report overview50© BIPE 2007

460Meggitt

490Ultra Electronics

610Babcock International Group

740GKN

800Devonport Management (KBR)

1010Cobham

1170VT Group

1450Smiths

1550QinetiQ

3470Rolls Royce

23230BAE SYSTEMS

34,980

back

Major Arms Producing Companies in the UKarms sales of top companies, m. US$

Military expenditure in the UK(in million US $ at constant 2005 prices and exchange rates)

2.7 %592135094948276

Share of GDP in 2006200620021997

Defence Industry Employment in the UK(1993 – 2003)* workforce in thousands

200280380

200319981993

Final report overview51© BIPE 2007

380Areva (CEA)

410SMA (SAFRAN)

910Nexter Industries (formerly GIAT)

1710CEA

2120Eurocopter Group (EADS)

2210Dassault Aviation Groupe

2707SAFRAN (consolidated, March 2006)

3520DCN

8940Thales

25,870

back

Major Arms Producing Companies in Francearms sales of top companies, m. US$

Military expenditure in France(in million US $ at constant 2005 prices and exchange rates)

2.5 %530915125751926

Share of GDP in 2006200620021997

Defence Industry Employment in France(1993 – 2003)* workforce in thousands

240266345

200319981993

Final report overview52© BIPE 2007 back

18,240390Oto Melara (Finmeccanica)

410MBDA Italia (MBDA Europe)

470Selex Sistemi Integrati (Finmeccanica)

530Avio

610Fincantieri

680Selex Communications (Finmeccanica)

1120Alenia Aeronautica (Finmeccanica)

1380Selex Sensors & Airborne Systems (Finmeccanica)

2850Agusta Westland (Finmeccanica)

9800Finmeccanica

Major Arms Producing Companies in Italyarms sales of top companies, m. US$

Military expenditure in Italy(in million US $ at constant 2005 prices and exchange rates)

1.9 %298913445929781

Share of GDP in 2006200620021997

Defence Industry Employment in Italy(1993 – 2003)* workforce in thousands

263550

200319981993

Final report overview53© BIPE 2007 back

14,620

960EADS Space (EADS, Netherlands)

4080MBDA (BAE Systems, UK/EADS, W. Eur.,/Finmeccanica, Italy)

9580EADS

Major Arms Producing Companies in the Netherlandsarms sales of top companies, m. US$

Military expenditure in the Netherlands (in million US $ at constant 2005 prices and exchange rates)

1.5 %975193449147

Share of GDP in 2006200620021997

Defence Industry Employment in the Netherlands(1993 – 2003)* workforce in thousands

101018

200319981993

Final report overview54© BIPE 2007 back

6,520

460MAN

500MTU Friedrichshafen (DC)

500DaimlerChrysler, DC

610MTU Aero Engines

720Diehl

750Krauss-Maffei Wegmann

1240ThyssenKrupp

1740Rheinmetall

Major Arms Producing Companies in Germanyarms sales of top companies, m. US$

Military expenditure in Germany(in million US $ at constant 2005 prices and exchange rates)

1.4 %369844060440854

Share of GDP in 2006200620021997

Defence Industry Employment in Germany(1993 – 2003)* workforce in thousands

8095160

200319981993

Final report overview55© BIPE 2007 back

1,640

670Indra

970Navantia

Major Arms Producing Companies in Spainarms sales of top companies, m. US$

Military expenditure in Spain(in million US $ at constant 2005 prices and exchange rates)

1.1 %123281148310599

Share of GDP in 2006200620021997

Defence Industry Employment in Spain(1993 – 2003)* workforce in thousands

202550

200319981993

Final report overview56© BIPE 2007 back

2,110

2110Saab

Major Arms Producing Companies in Swedenarms sales of top companies, m. US$

Military expenditure in Sweden(in million US $ at constant 2005 prices and exchange rates)

1.5 %527158335780

Share of GDP in 2006200620021997

Defence Industry Employment in Sweden(1993 – 2003)* workforce in thousands

252634

200319981993

Final report overview57© BIPE 2007

Industry organisation in the easternEuropean member states (1)

Defence industries in the eastern European countries have distinct features

Before 1990, defence industries in EE countries were direct elements of military strategy of the Warsaw Treaty,The location of production and tasks of the individual producers, factories and industries were defined in the frame of the Warsaw Treaty’s military strategyThis resulted in a high level of country specialisation in the production of elements of final products and systems, divided and distributed across factories and countriesEconomic factors and market aspects did not play a primarily role

Final report overview58© BIPE 2007

Industry organisation in the easternEuropean member states (2)

Since the, the main problems of defence industries in the eastern European member states have been:

difficulties in adapting to the new political and economic context after the break-up of the Warsaw Treatylack of internal EE countries experience in conducting restructuring and privatisation changes on such large scalethe consequences of actions by international competitors perceived at attempting to eliminate potential internal and international competition

The restructuring process is not yet completed. The eastern European countries’ defence industries are still in “transformation shock”

Final report overview59© BIPE 2007

The situation in Poland

The Polish defence industry was the most important producer amongst the EE countriesAll the factors previously mentioned influenced the present situation of the Polish defence industry

Employment in the sector decreased by approximately 60% during the 1990sThe first years of restructuring and the privatisation process led to important decreases in production, increased unemployment and social problems

As elsewhere, the restructuring and privatisation process is not completed:Over the past years, several future industry concepts and organisation structures were evaluated by various industrial and professionalorganisations, and by administrative bodiesDiscussions led to the recent publication of the Strategy of consolidation and support of development of Polish defence industry in 2007-2012, approved by the Polish government on 31.08.2007.

Final report overview60© BIPE 2007

The Polish government strategyobjectives (1)

The objectives are to:Ensure that the state security requirements in the sphere of armament, army equipment and weapons defined within the framework of the national security strategy and taking into account EU membership obligations, can be metSecure the participation of the national defence industry in R&DprogramsIncrease exports to the world markets, and achieve a significantposition in the future European defence industry

Final report overview61© BIPE 2007

The Polish government strategyobjectives (2)

In the short term, this implies the following objectives:adjusting defence production capacity and R&D work to national and export potentialIncreasing the diversity of supply of modern army equipment and weaponsFinancial and technological reinforcement of the defence industryStrengthening the position of Polish producers on internal and international markets as well as in relation with financial institutionsModernizing the technology and the defence productsCo-ordinated policies with respect to defence R&D workMoving up the value added chain (increasing the value of defence industry exports)Co-ordination of commercial and marketing activities,Rationalisation of production costs Stabilising employment

Final report overview62© BIPE 2007

Quantified objectives have been set

Target export value between 360 to 520 million €Value of R&D work : between 125-130 million €Target share of deliveries of army equipment and weapons produced in Poland in total purchases by the Polish Ministry of Defence : 59% in 2006, coming down to 34% in 2012. The decrease is due to the execution of international agreements on deliveries already signed by the MinistryIncrease in the number of factories consolidated within the frame of BUMAR GROUP (the national champion) : from 15 entities at present to 36 by 2012. This denotes a strong consolidation trend.

Final report overview63© BIPE 2007

The national champion’s dependence on national procurement budgets

The size and diversification of the defence industry in the EU is clearly a reflection of the size of the military budgets:

The United Kingdom has the largest defence budget among the EU countries, closely followed by FranceIn Germany, the third largest spender on defence in the EU, the budget is considerably smallerThe fourth largest spender is Italy

These four countries account for two thirds of the EU’sdefence budgets

Final report overview64© BIPE 2007

Diversification and regional distributionof production across the EU

Many small and mediums sized companies are engaged in defence production, both in the main producing countries and in other EU countries such as Austria, Belgium, Czech Republic, Denmark, Finland, Greece, Poland and PortugalThese companies produce small arms and ammunition, low calibre artillery, military vehicles, small ships, military electronics, and subsystems for weapons and components. Often they are not classified as defence producers since they are usually diversified companies with non-defence (dual-) production.A similar pattern of concentration as with the largest defence producers appears in the regional distribution of the different defence sectors in Europe. The four top producing countries, UK, France, Italy and Germany, are the home base for companies from all sectors of defence: small arms/ammunition; artillery; aircraft; engines; electronics; military vehicles; missiles and ships. However, a large number of SME are engaged in all sectors of defence production; they operate from countries across the EU.

Final report overview65© BIPE 2007

An example of the regional distribution of production

The example of the helicopter production sites of Eurocopter and Agusta Westland illustrates the diversity and distribution of production sites and employment.

Source: Fondation pour la Recherche Stratégique

Final report overview66© BIPE 2007

Trend in mergers and acquisitions

A general process of consolidation is under way:In contrast to other industrial branches, M&As took place primarily at national level during the early 1990s. National champions were formed in several EU countries.Typical of this process of consolidation largely along national lines in the EU, is the land defence sector, as well as naval industry.

Acquisition activity has recently accelerated in the EU, at a time when it has slowed down in the United States. The primary reason for theacquisition of defence companies during the early phase in the 1990s was their uncertain future as a result of the end of the Cold War and the reduced budgets.In the US, the consolidation process started earlier. Wall Street played an instrumental role in the restructuring process. Big companies (Northrop Grumman and Lockheed Martin) were formed.

Final report overview67© BIPE 2007

Consequences on industry structure

As a result of mergers and acquisitions along national lines, the leading producers offer equipment that is not necessarily standardised, since each pursues its own technology lines.

There are too many and too small companies to survive. For example, after the commercial failure of the Leclerc tank and drastic reduction in orders by the French government, GIAT (France) cut its staff by 85% over 15 years (from 18,000 employees in 1990 to 2500 in 2006). The situation, which had become a financial disaster for the state, was sorted out in 2006.

Some European states are turning to foreign countries to satisfy their munitions needs. Financial difficulties of firms has allowed U.S. industry and financial investors to acquire several outstanding companies of the ground weapons industry at low prices (Bofors, Mowag, Santa Barbara).

Final report overview68© BIPE 2007

Major pan-European companies have nevertheless emerged, through differentapproaches

The first European corporations were formed during the second half of the 1990s. Typical examples are:

EADS = Aérospatiale-Matra, DASA, CASA and a number of smaller companies. The merger was made possible by an agreement between the French and German governments, which encouraged the mergerThales = Thomson CSF, Racal, Signaal in addition to a number of companies from the US, UK, Canada, South Korea, South Africa, Australia, Brazil and West European countries: this is a model of growth through acquisitionBAE followed a different approach, centered on the US market

It is of interest that not only companies based in the EU were acquired, but from a wide range of countries.

Final report overview69© BIPE 2007

Example: the formation of EADS1985-2005

1985 1986 1987 1988 1989 1990 1991

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005Matra Haute Technologie (France)Aerospatiale (France)

Aerospatiale Matra (France)

Siemens Defence Electronics (Germany)MBB/GermanyAEG/GermanyDornier/GermanyMTU/Germany

DASA (Germany)

CASA (Spain)

EADS

Patria Industries, 27 % (Finland)Astrium (UK)Siemens Unit (Germany)Racal Instruments (USA)Nokias professional mobile radio buisness (Finnland)

Source: SIPRI Yearbook 2006

Final report overview70© BIPE 2007

The formation of Thales1987 - 2005

Source: SIPRI Yearbook 2006

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005TDA Amemenis (Western Europe)Arieem (France)Racal (UK)

Samsung Electronics detence unit, 50 % (South Korea)Pillington Optronics, 10 % (UK)Shorts Missiles Systems (Canada)ADI, 50 % (Australia)African Defense Systems (South Africa)Sextant in-Flight Systems (USA)Avimo, 25 % (UK)Embraer, 6% (Brazil)Pilkington Opironica, 40 % (UK)Dassault Electronique (France)Aerosperlic´s military electronics units (France)Sectant Avionique, 50 % (France)Signaal HSA (Netherlands)Pilkington Opironics, 50 % (UK)Link-Miles (UK)Radilon MEL (UK)Wiloc Electric (USA)GE/RCA (USA)

Thomson SA Thales

Final report overview71© BIPE 2007

BAE´s Alternative Approach

BAE Systems (UK) chose a different approach: The company pursued a strategy of a forceful entry into the US defence market by acquiring US defence producing companies. BAE Systems now employs 35,000 people in the United Sates. By far the largest acquisition in the defence sector in 2005 was that of United Defence (USA) by BAE Systems, a deal worth US $ 4192 million. This was the largest acquisition of a US defence company by a non-US buyer.

As a result, this British company is now the sixth-largest contractor of the US Department of Defence

One should, however, note that BAE is a defence specialist ,whereasEADS and Boeing have a mix of military and civil business

Final report overview72© BIPE 2007

The formation of BAE Systems1977 - 2005

Source: SIPRI Yearbook 2006

1977 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Siemens Plessey Systems (Germany)

Saab, 35 % (Sweden)

BAeSEMA (UK)

STN Atlas Elekt., 49 % (Germany)

LFK, 15 % (Germany)

AWADI (Australia)

British Aircraft Corp. (UK) Heckler & Koch (Germany, divested in 2002)

Hawker Siddeley Av. (UK) Roval Ordnance (UK)

Hawker Siddeley Dy. (UK) Reflectone (UK)

Scottisch Avierlion (UK) SD-Scicon (UK)

British Aerospace BAE Systems

Marconi Electronic Systems (UK)

Lockheed Martin Control Systems (USA)

Lockheed Martin AES (USA)

Watkins Johnson (USA)

Ferntornierics (USA)

Condor Pacifics (USA)

Piper Group (UK)

Advanced Power Tech. (USA)

MEVATEC (USA)

Alphatech (USA)

Commercials electronics unit of Boeing (USA)

Digital Nierl Holdings (USA)

Practical Imagineering (USA)

STI Government Systems (USA)

Alvis (UK)

Aerosystems International (UK)

United Defense (USA)

Y

Final report overview73© BIPE 2007

Four factors explain the acceleration in M&A activity in the 1990s

1. Governments in the EU have encouraged mergers in certain cases (EADS and its family of companies); in other cases governments try to prevent foreign (non-EU) investment.

2. There is a trend to invest in expanding sectors. This is particularly the case in areas which are affected by the outsourcing and privatisation strategies of traditional military functions, such as services, logistics, information technology and the so called network-centric programmes: to increase market shares, companies seek to acquired smaller specialized companies.

3. There is a desire of non-US companies to access the lucrative US market by acquiring US-producing companies. This has proved more successful than the direct export of military goods to the United States. The reverse process also takes place. US-based companies have been actively acquiring EU-based companies.

4. Private equity groups (financial investors) have begun to purchase defence producing companies. There are several outstanding examples. In 2005 the private equity group EQT (Sweden) bought MTU Friedrichshafen (Germany) from DaimlerChrysler (Germany). This transaction has been a source of political tension in Germany. It included also the Off-Highway Division of Detroit Diesel (USA) and was valued at approximately US $ 1.9 billion.

Final report overview74© BIPE 2007

List of recent mergers within Western Europe (1)

…Nokia (Finland)Professional Mobile Radio businessEADS (W. Europe)

…Royal Philips (Netherlands)Philips Aerospace Electronics(Netherlands)

Avio Group (Italy)

2…Graphics Research (UK)QinetiQ (UK)

156RAC (UK)Lex Vehicle Solutions (UK)VT Group (UK)

18ECI Partners (UK)Hotel and Catering Training Company(UK)

VT Group (UK)

825Alcatel (France)Alcatel´s satellite unit (France)Thales (France)

550Ericsson (Sweden)Ericsson Microwave Systems (Sweden)

Saab (Sweden)

…Saab (Sweden)Nammo (Norway)Norwegian Governmenand Patria (Finland)

……Navtek (Norway)Kongsberg (Norway)

3 400Carlyle Group (USA)Avio (Italy)Cinven (W. Europe)

Deal value($ m.)

Seller company(country)

Acquired company(country)

Buyer Company(country/region)

Source: SIPRI Yearbooks 2006 and 2007

Final report overview75© BIPE 2007

List of recent mergers within Western Europe (2)

172BAE SystemsAtlas Elektronik (Germany)ThyssenKrupp Technologies (Germany) and EADS (W. Europe)

…EADS (W. Europe)TDA Armements (W. Europe)Thales (France)

……Sagem (France)Snecma (France)

31…Farran Technology (Ireland)Smiths Group (UK)

……Arges (Austria)Rheinmetall (Germany)

…EADS (W. Europe)LFK (Germany)MBDA (W. Europe)

…MAN-Technologies (Germany)MAN-Mobile Bridges (Germany)Krauss-Maffei Wegmann (Germany)

171…Datamat SpA (Italy)Finmeccanica (Italy)

1 900DaimlerCrysler (Germany)MTU Friedrichshafen (Germany) and the off-highway division of Detroit Diesel Corporation (USA)

EQT (Sweden)

Deal value($ m.)

Seller company(country)

Acquired company(country)

Buyer Company(country/region)

Source: SIPRI Yearbooks 2006 and 2007

Final report overview76© BIPE 2007

List of transatlantic mergers (1)

Source: SIPRI Yearbooks 2006 and 2007

……Alcoa´s Aerospace ServiceBusiness (USA)

ThyssenKrupp Service(Germany)

59SAIC (USA)Data Systems & Solutions(USA)

Rolls Royce (UK)

……Firearms Training Systems(USA)

Meggit (UK)

…Carlyle Group (USA)Stellex Aerostructures (USA)GKN (UK)

9…National Sensor Systems (USA)BAE Systems (UK)

26…Cube Corporation (USA)VT Group (UK)

60Privately heldAudiopack (USA)Ultra Electronics (UK)

42…Planning Systems Inc. (USA)QinetiQ (UK)

288…Apogen Technoligies (USA)QinetiQ (UK)

26…Gallium Software (Canada)Kongsberg (Norway)

……Talon InstrumentsEADS (W. Europe)

260Remec. Inc. Defense & Space unitChelton Microwave Corporation(UK)

4 192…United Defense (USA)BAE Systems (UK)

Deal value($ m.)

Seller company(country)

Acquired company(country)

Buyer Company(country/region)

West European acquisitions of companies based in North America

Final report overview77© BIPE 2007

List of transatlantic mergers (2)

Source: SIPRI Yearbooks 2006 and 2007

169…TRL Electronics (UK)L-3 Communications (USA)

65Nautronix Holdings (UK)Nautronix Defence Group (UK)L-3 Communications (USA)

……Magnet-Motor (Germany)L-3 Communications (USA)

……Advanced Systems Architectures(UK)

L-3 Communications (USA)

…Privately heldHMT Vehicles (UK)Lockheed Martin (USA)

59Cobham (UK)Wallop Defence Systems (UK)Esterline Technologics (USA)

47…Automotive Technik (UK)Stewart & StevensonServices (USA)

22Northrop Grumman (USA)Teldix (Germany)Rockwell Collins (USA)

……INSYS Group Limited (UK)Lockheed Martin (USA)

150…SAM Electronics (Germany)L-3 Communikations (USA)

270Cobham (UK)Aerospace fluid and air divisionEaton Corporation (USA)

54Reinhold Industries (UK)NP Aerospace (UK)Carlyle Group (USA)

Deal value($ m.)

Seller company(country)

Acquired company(country)

Buyer Company(country/region)

North American acquisitions of West European-based companies

Final report overview78© BIPE 2007

As a result of the consolidation process, the degree of concentration has significantly increased

0102030405060708090

1990 1995 2000 2005

top 20top 15top 10top 5

Share of arms’ sales of the top 100 defence producers

The result of this concentration process can also be seen in the turnover of companies. In 1990 the top 5 defence producing companies of the world accounted for 22% of the total arms sales of the top 100 companies. This figure has doubled now to exactly 44

Final report overview79© BIPE 2007

In several countries, public ownershipstill dominates

This is the case in particular in France, Italy and SpainElsewhere, governments are progressively reducing theirstake in the defence companiesPrivate funds have entered the sectorUS companies have also increased their presence in Europe through acquisitions

Final report overview80© BIPE 2007

What will be the fate of public ownership in France?

(*) Etat: 75% à partir de début 2007

% CA Défense 2006 Effectif 2006

100%100%

12 4592 491

50% 68 000

20% 61 357

25,4% 116 848

38% 12 086

(*)

46,5% 4 2964 719

Final report overview81© BIPE 2007

What will be the Fate of Public Ownership in Italy and Spain?

Source: Fondation pour la Recherche Stratégique

Final report overview82© BIPE 2007

The European collaboration record ismixed

A few projects have been highly successful. However they have often been used to pursue national procurement or industrial aims. A few positive and negative examples are listed below.The juste retour principle, often applied in collaborative projects, leads to inefficiencies and higher cost, since the placement of a procurement orders is largely based on the percentage of finances in the project of the participating countries rather than selection of the most economic or technically most competent supplier.

Positive collaboration seems to happen:in helicopters with the NH 90 and Tiger, and with the Anglo-French helicopter packagein missiles with the Meteor and, to a lesser extent, PAAMSin transport aircraft with the A400Min satellites with the Galileo

Final report overview83© BIPE 2007

The NH-90 helicopter : an example of European cooperation

EADS/Eurocopter, EADS/Eurocopter Deutschland, Augusta (Italy) Fokker (Netherlands) and OGMA Portugal) cooperate in development and production.

Source: Fondation pour la Recherche Stratégique

Final report overview84© BIPE 2007

Poor collaboration examples also exist

Often, the stage of collaboration is not reached and national programs prevail

The number of duplications (with higher cost and inefficiencies) of weapon systems is high:

Four main battle tanks are being built,

There are 16 national programmes for armoured fighting vehicles (AFV),

Three combat aircraft programs are being pursued, despite heavy competition from the USA

Duplications in development are particularly frequent in IT-and Command and Control Systems

Final report overview85© BIPE 2007

Example: number of systems produced in the EU and the USA

Final report overview86© BIPE 2007

There are three competing combat aircraft programs in Europe

The combat aircraft sector illustrates the failure in European cooperation. The lack of joint political will and the dominance of national ambitions lead to multiple programs (Gripen,

Eurofighter, Rafale) and diffused R&D spending. The results are increased program costs, slipping deadlines, export sales difficulties.

Source: Fondation pour la Recherche Stratégique

Final report overview87© BIPE 2007

Can the A400M transport aircraft be a model?

Final report overview88© BIPE 2007

Outline of the situation by segment

The following slides present a summary of the situation across the key segments of defence industries:

AerospaceNaval industryLand / ground forces

Of which: armoured vehiclesOf which : munitions

Missiles and electronics

Final report overview89© BIPE 2007

The aerospace industry covers both civil and military production

The aircraft/space industry is the most Europeanized industry segment.The consolidation process has taken place over many years and was accelerated by financial needs.However, looking at the non-military (Airbus, space) and the military sector (fighter aircraft, missiles, military electronics) it becomes clear that the civil part is more European than the defence part. Despite present problems in the structure of Airbus Industries and its production process, Airbus has established itself on the basis of reimbursable aid from the member states as a competitive producer of a family of civilian aircraft. The question is: can Airbus serve as a model?

Final report overview90© BIPE 2007

The military segment of aerospace is veryspecific, but consolidation at EU-level is already well advanced

There are some distinct differences in the arms ‘market’: defence is not really a market, products are essentially sold domestically by one supplier to one customerGovernments are customers and shareholders in the enterpriseseconomic considerations are often overruled by political interests (although this is to some extent the case in Airbus Industry as well) state protectionism has often favoured national programsthe civilian aircraft market has constantly grown; defence has experienced fluctuations in demand

Final report overview91© BIPE 2007

The different activity segments in military aerospace

Source: Fondation pour la Recherche Stratégique

Final report overview92© BIPE 2007

The naval industry remains organised along national lines

Although the naval sector is undergoing significant technological changes, the concentration process has largely proceeded along national lines : about two dozen shipyards are engaged in the design, development and production of military vessels.Four major groups of national champions have emerged in UK, France, Germany and Spain.In contrast to the United States, where vertical groups (integration of platform and systems producers) have been formed, the shipyards in Europe operate horizontally at the national level. Cooperative programs in the EU exist on bi- or tripartite levels (Fremm, CVF/PA2 and others). A typical example of a most recent national decision is the procurement of four frigates Type 125 in 2007 for a value of 2.6 billion € in Germany. A European solution, possibly along the lines of Airbus or EADS in the aerospace sector, is not on the agenda, neither is there a development of transnational programs which involve more than two or three countries.

Final report overview93© BIPE 2007

There is a need for consolidation at EU level in the naval industry

Financial constraints might accelerate the need for consolidation

This seems within the realm of possibility: not long ago, a joint British-French aircraft carrier – a symbol of the states’sovereignty – would have been inconceivable

Similarly, rationalisation is required to reduce overcapacities:The capabilities to develop and produce naval vessels are larger than actual demand. It is both difficult and costly to retain such facilities during gaps in development and production

Final report overview94© BIPE 2007

Overview of the naval sector in the EU

BAE Systems

E A D S

Atlas Electronics

Thales UnderwaterSystems THALES

100%

100%

ThyssenKrupp HDW

ETMarinesystème

50%

50%

TNF

MOPA2

DCN

100%25%

FlagshipTraining

37%

Fleet Support

50%

Rolls-Royce

Vosper Thornycroft

50%37%

Babcock Borsig

Preussag

Saab

RDM

FRANCE

SWEDENGERMANY

UK

Daimler-Chrysler

Abeking&Rasmussen

Kochums

35%

75%

CMN

Armaris

Babcok Rosyth

Devonport

Lürssen

Celsius

MTU

MAN

Siemens

Technicatome

WärtsiläAker Yards JeumontSchneider

SEMT Pielstick

100%

FincantieriFinmeccanica

AMSWASS100%

ITALY

TNN (Signaal)Royal Schelde

eld

100%NL

SPAINNAVANTIASEPI

100%

TKMS100%

OEP25%

B&V

100%

National Champions

INDRA systemas

Source: Alpha

Final report overview95© BIPE 2007

Further consolidation is also expected in the land defence industry

The structure of the producers of equipment for the ground forces is similar to the naval industry. Governments often opted for national solutions to retain advanced technologies in this sector, and secure jobs. The development and production on the national level of major battle tanks, armoured vehicles, artillery and small arms and ammunitions was affordable in large EU countries.There is a clear lack of Europeanization of industry and lack ofcooperative projects. Procurement of armoured vehicles has slowed down in recent years and the industry is in economic difficulties. There are too many and too small companies to survive. Major companies exist in France, Germany (2), Italy and the UK.

Final report overview96© BIPE 2007

Mergers and acquisitions in the armoured vehicles segment

Breda Meccania

Oto MelaraItaly

Panhard

GIATFrance

ArgesAustria

KUKA

IWKA

Krupp MAK

Thyssen Henschel

Rheinmetall

Wegmann

Krauss MaffeiGermany

VSEL

Royal Ordnance

Vickers

GKN

AlvisUnited Kingdom

Hägglunds

BoforsSweden

United DefenseUSA

Oto Melara (Finmeccania)

GIAT

BAE Systems

Krauss-Maffei Wegmann

RheinmetallLandsysteme GmbH

Final report overview97© BIPE 2007

Several joint programs and cooperation at the industry level take place in the munitions industry

Source: Fondation pour la Recherche Stratégique

Final report overview98© BIPE 2007

The missile and electronic industry

Similar to the area of aerospace, the defence electronics and the missile/propulsion industry is more EuropeanizedCross-border mergers and bi- and multilateral joint ventureshave facilitated the Europeanization process

Final report overview99© BIPE 2007

The EU missile and propulsion industry

ALLEMAGNE

Finmeccanica

BAE Systems

LFK

Rheinmetall

Saab

37.5%

100%

25%

35%

37.5%

EMEO 40%

Bodenseewerk

20%

TDA

Taurus Systems

67%

100%

SME

50%

NEXTER CTA 50%

RGR 33%

Nitrochemie Wimmis 51%

Dynamit Nobel

Diehl Stiftung&Co

80%

10%

100%Oerliken Contraves

100%

Otobreda division

WASS

100%

Nammo Sweden AB

Empressa Portu. Defesa Spel SA 50.9%

Kongsberg Gruppen ASA

Raufoss Technology

15%

Patria Industrie

26.8%

45% 27.5%

27.5%

SIG Arms International AG RUAG

49%

50%

Indra 75%

40%

50%

33%

10%

R.O.

100%SAGEM

Nexplo Indus. 60%

40%

6%

United Defense Bofors Defense AB Akers Krutbruk

Selex

100%

0%

Eurosam 33%

33%

33%

Euromissile

100%

Bayern Chemie / Protac

0% 100%

FRANCE

ITALY

UK

SPAN - PORTUGAL

SCANDINAVIA

E A D S

Italie UKams

THALES

Europaams

33% 66%

Euro-Art

SAFRAN R.O. rocket motor

MBDA

Roxel

SEPI

SNPE

Eurenco

60,2%

19,9%19,9%

GERMANY

ASTRIUM

THALES UK

100%

Source: Alpha

Final report overview100© BIPE 2007

The EU’s leading missile producer

Source: Fondation pour la Recherche Stratégique

Final report overview101© BIPE 2007

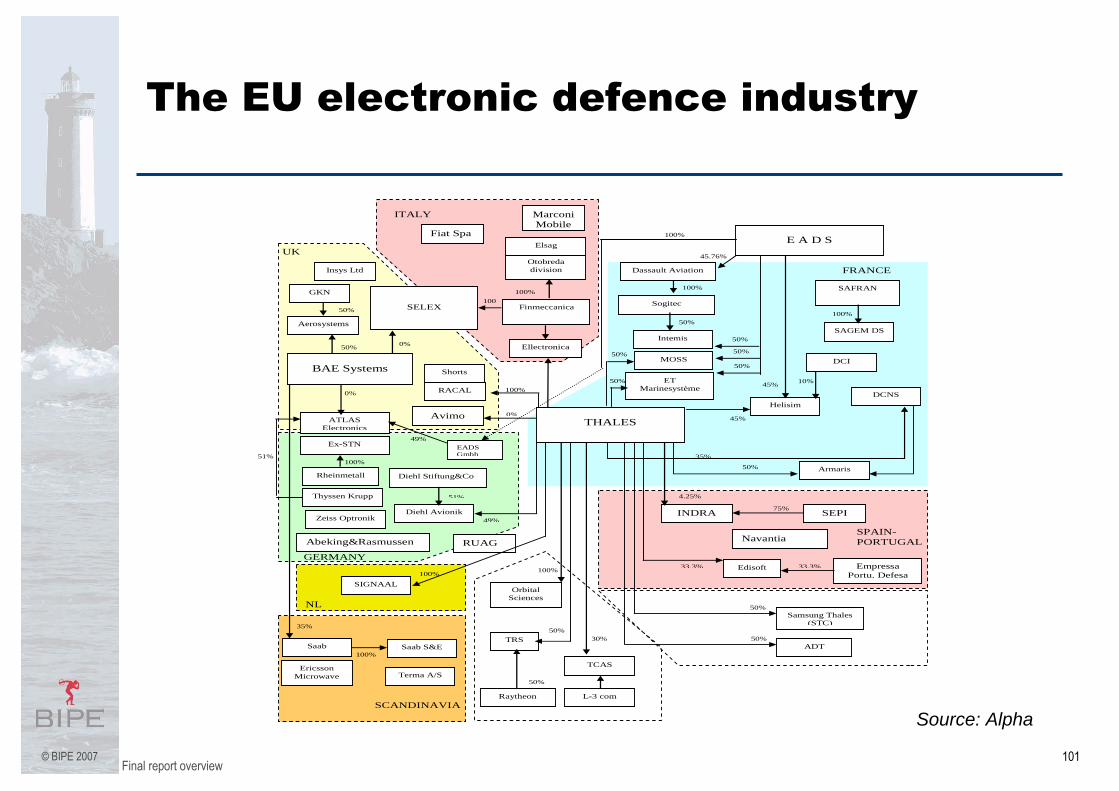

The EU electronic defence industry

Finmeccanica

Dassault Aviation

SELEX

E A D S

ATLAS Electronics

Diehl Avionik

Rheinmetall

Saab

Ellectronica

Samsung Thales (STC)

Edisoft

ADT

100

45.76%

0%

100%

49%

35%

50%

33.3%

SAFRAN

0%

TCAS

30%

L-3 com

TRS

Raytheon

Helisim

50%

Sogitec

100%

45%

DCI

10%

Insys Ltd

Zeiss Optronik

Diehl Stiftung&Co

51%

SEPI INDRA 75%

4.25%

Navantia

Otobreda division

Elsag

100%

Fiat Spa

Ericsson Microwave

Saab S&E 100%

Empressa Portu. Defesa

33.3%

RUAG

50%

50%

DCNS

Intemis

50%

50%

Abeking&Rasmussen

Avimo 0%

Orbital Sciences

RACAL

Shorts

100%

100%

THALES

45%

GKN

BAE Systems

Aerosystems

50%

50%

Terma A/S

ITALY

UK

SPAIN- PORTUGAL

SCANDINAVIA

GERMANY

Marconi Mobile

MOSS 50%

ET Marinesystème

50%

50%

50%

SIGNAAL

NL

100%

Ex-STN

Armaris

FRANCE

35%

50%

SAGEM DS

100%

EADS Gmbh

100%

Thyssen Krupp

51%

49%

Source: Alpha

Final report overview102© BIPE 2007

Outline

Developments during the past decade and present industry structureDefining the defence industryOverview of demand trends: budgets, procurement, R&D expenditure, trade, competitiveness and market access conditionsTrend in employmentOrganisation of supply and changes therein: activities covered, key European defence producers, production location and country specialisations, trend in M&A, ownership structure, cross-border collaboration

ChallengesOutlook

Key factors influencing the futurePossible future scenarios

Anticipating change: examples of innovative practices

Final report overview103© BIPE 2007

Summary of the analysis of the presentsituation

Persistent primarily national procurement strategies : although in principle in favour of joint procurement – national procurement authorities often favour national entrepreneursStrict national rules hindered or prohibited foreign ownership of defence companiesThe juste retour principle in collaborative projects results in suboptimal procurementDifferences in arms exports complicates marketingSecuring jobs at home is used to legitimize cost-inefficient procurementThe management of cross-border collaboration projects is cumbersome, which leads to cost and time overrunsThe frequent recourse to Art. 296 has de facto prevented the implementation of the Single Market in the defence sector

Final report overview104© BIPE 2007

Yet …

The creation of the Regime on Defence Procurement and adoption of the EDTIB Strategy are important steps towards the creation of the European Defence Equipment Market and the strengthening of the European defence industry

Final report overview105© BIPE 2007

Summary of the key challenges for the future (1)

• Continued downward pressure on defence budgets (due to perceived trade-offswith social welfare expenditures)Rising input cost of equipment, and rising cost of R&D for new weapon systemsRising input costs for military personnel for an AVFThere has been a major change in the security situation, leading to a new required equipment mixAt the political level, despite intensive efforts, there is still no integrated or unified European defence marketThe EU member states do not have the financial means to sustain the full spectrum of a defence technology industrial base. This means continueddownward pressure on defence budgets (due to a preference for social welfarespending)At the industrial level, the defence industry is – with a few outstanding exceptions, most notably EADS and BAE Systems – still geared towards national procurementAt the technical level, the defence technology and research base is inadequate in most defence sectors to allow for national solutions. The new security risks have accelerated the race for innovations, resulting in increased demand for R&D resources.

Final report overview106© BIPE 2007

Summary of the key challenges for the future (2)

At the social level, the defence sector has experienced drastic reductions in employment. This process has slowed down in recent years. Additional job losses are, however, expected given the changing overall context.At the legal level, a range of political and legal guidelines have been designed and institutions were founded to improve coordination, to internationalise procurement and encourage competition. Art. 296 allows Member to derogate from general EU rules on a case-by-case basis when their essential security interests are at stake. The frequent recourse to Art. 296 has de facto prevented the implementation of the Single Market in the defence sector.In Eastern Europe, specific challenges are linked to the breakdown of supply chains afterthe fall of the Berlin Wall, and the new national defence strategies which put priority on national autonomy and restoring supply chainsNew technology will be coming on stream over the coming 25 yearsSupply-side changes are underway: mergers, privatisation, outsourcing, growth of servicesmarkets, etc.Competitive threat from US and emerging competition from China, Japan, Russia, Korea, India (both primes and suppliers), and IsraëlEC/EDA Policy on development of a EDEM and on EDTIB calls for major changesEDA debate on ways to mitigate adverse impact of offsets on fair competition in the EDEM, and EDTIBRisk of new threats

Final report overview107© BIPE 2007

Consequences of the fragmented European market

Duplication of research and development effortsUnnecessary duplication of capacities in the defence industry, hence inadequate utilization of the potential for rationalizationLack of standardization of military equipment, resulting in avoidable costsInefficiency and increased cost resulting from limited competitionA weak Europe in global markets

Final report overview108© BIPE 2007

Risks for the future (1)

Despite recent restructuring, the concentration and consolidation process in the EU is incomplete. Continued duplication of capacities and duplication of weapon programs leads to inefficienciesIf concentration continues on the national (or the bi-lateral) level, protected industries will become uncompetitiveThe collaboration experience is mixedFurther restructuring will imply social costs (notably job losses)

Result: difficult choices must be made

Final report overview109© BIPE 2007

Risks for the future (2)

Further consolidation increases the risk of domestic (national or EU) monopolies, oligopolies or duopolies with the consequences on the rate of dependence, inefficiencies and higher costsGovernment control will be reduced through outsourcing of traditional military functions The financial logic and shareholder value concept raise questions regarding the reliability of the delivery of defence products Governments remain torn between national and EU preferences on one side (with possibly higher cost but job security) and competition (with dependence on outside suppliers and job losses at home)

Final report overview110© BIPE 2007

Consequences for employment

The consequences for employment – and in particular for employment at local level – vary depending on the future development of the industryEmployment in the defence industries is often located in areas that are highly dependent upon it. The location of plants has usually been determined historically by security concerns and kept away from urban centres. Thus, local communities can heavily depend on developments in the activity in defence facilities and factoriesEmployment is also often highly skilled, very specialised. In particular one finds a higher proportion of engineers and scientists and higher levels of qualification than on average for industry. Although past experience indicates that most persons find a new job relatively easily after having been made redundant, this is not the case for all. For those who do find another job, this may not be an equivalent job (lower pay for example), entailing costs in terms of purchasing power and/or quality of life.To assess the social costs, it is essential to take into account the possible inter-changeability of workforce between the defence, security and civilian sectors and to compare blue and white collar workforce ratios in the various sectors (land, aerospace, naval)Increased geographical mobility of the workforce may also be required as a result of the restructuring and consolidation process.

Final report overview111© BIPE 2007

Outline

Developments during the past decade and present industry structure

Defining the defence industryOverview of demand trends: budgets, procurement, R&D expenditure, trade, competitiveness and market access conditionsTrend in employmentOrganisation of supply and changes therein: activities covered, key European defence producers, production location and country specialisations, trend in M&A, ownership structure, cross-border collaboration

ChallengesOutlook

Key factors influencing the futurePossible future scenarios

Final report overview112© BIPE 2007

The nine steps of the scenario building exercise

1. Definition of “underlying structural trends”2. Identification of key stakeholders3. Identification of structuring variables for the future4. Identification of the possible objectives of the stakeholders5. Rank the objectives for each stakeholder6. List shared objective and identify areas of conflict7. Map the influences / dependencies between players8. Analyse results9. Identify key questions for the future, and discuss their consequences

Final report overview113© BIPE 2007

The key stakeholders in European defenceindustries

Governments of major producing (exporting) countriesGovernments of client (=importing) countriesLocal governmentsUS GovernmentGovernments of competing producing countries (Russia, Japan, China, India)NATOEuropean organisations and regulators:

EC, EDA, OCCAR, LoI, etc.Private financial investorsForeign investors, with regulatory controlSystem integratorsPlatform producers and assemblersSpecialised subcontractorsCommodity contractorsWorkers’ representatives, trade unions

Final report overview114© BIPE 2007

The key factors that will influence the future

Common foreign and security policy (CFSP)European Industrial policy for defence industriesNational industrial policies for defence industriesValue and trend in (intra- and extra-EU) defence procurementAccess conditions to non-EU marketsCompetitor strategies (risks related to new entrants)Ownership, control and conditions of access to key technologiesAccess to key competencies (HR)Structure of the industry portfolio (civil vs defence)Degree of aversion to risk of (private) financial investors (venture capital, restructuring funds, pension funds,...)Financial investors' time horizon and expected rate of return on investmentOvercapacity problems / restructuringEfficiency (and amount) of R&D expenditureLabour market trends, risk of skill depletion/shortage, attractivenessproblems, etc.

Final report overview115© BIPE 2007

The assumptions common to all scenarios (1)