annuity market trends and...

TRANSCRIPT

5/1/2012

1

Joseph Montminy Assistant Vice President, LIMRA

Chris Raham

Senior Actuarial Advisor, Ernst & Young

This publication is a benefit of LIMRA membership. No part may be shared with other organizations

or reproduced in any form without LIMRA’s written permission.

Annuity Market – Trends and

Opportunities

© LL Global, Inc.SM

• Individual Annuity Market Trends

• Sales by product type

• Distribution Channels

• Drivers of Sales

• Who is Buying Guaranteed Lifetime Income products

• Annuity Assets

• Sales Forecast

Agenda

2

5/1/2012

2

© LL Global, Inc.SM 3

Annuity Sales

© LL Global, Inc.SM

Total Individual Annuity Sales Rebound

111 117 130 133 137 160

184 156

128 141 159

74

103 89 88 79

78

73 109

111 82

81 $185

$220 $219 $221 $216

$239

$257 $265

$239

$222

$240

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Fixed Variable

Source: LIMRA, U.S. Individual Annuities survey.

Do

lla

rs in

Bil

lio

ns

4

5/1/2012

3

© LL Global, Inc.SM

Indexed Annuity Sales Remain At Record Levels While

Traditional Fixed-rate Sales Flat

7 12 14 23 27 25 25 27 30 32 32

11

18 8

7 5 9 8

18 14 6 5 47

63

56 47 37 32

27

51 53

30 30

$65

$93

$79 $77

$68 $66 $60

$95 $98

$69 $68

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Indexed Market value adjusted Book value deferred

Source: LIMRA, U.S. Individual Annuities survey.

Do

lla

rs in

Billi

on

s

5

© LL Global, Inc.SM

Fixed immediate Annuity Sales Hit Record High

3.0 3.6 4.8 4.8 5.3 5.3 6.1 6.5

7.9 7.5 7.6 8.1

5.0

6.0

5.9 6.0 6.0 5.9

5.9 6.2

6.4 5.6 5.8 5.1

0.8

0.7

0.6

$8.8

$10.3 $11.3 $11.3 $11.6 $11.5

$12.4 $13.0

$14.4

$13.2 $13.4 $13.2

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Variable immediate Structured Settlements Fixed immediate

Source: LIMRA, U.S. Individual Annuities survey.

Do

lla

rs in

Billi

on

s

6

Amounts $0.5 billion or less not shown

5/1/2012

4

© LL Global, Inc.SM 7

Distribution Channels

© LL Global, Inc.SM

Independent B-Ds Retain Market Share Among VA

Distribution Channels

29% 31% 32% 33% 33%

21% 18% 18% 18% 19%

14% 12% 10% 11% 12%

21% 23% 24% 24% 24%

9% 10% 12% 12% 11%

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011

Independent B-D Full Service Nat'l B-D Banks

Career Independent Agents Direct

Source: LIMRA, U.S. Individual Annuities survey.

8

5/1/2012

5

© LL Global, Inc.SM

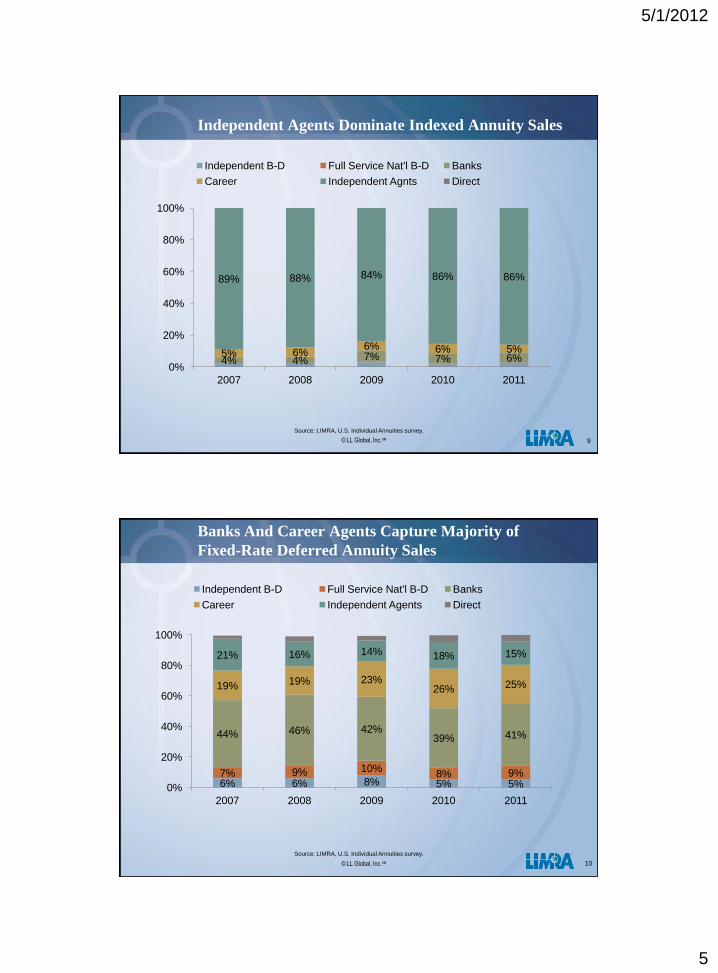

Independent Agents Dominate Indexed Annuity Sales

4% 4% 7% 7% 6% 5% 6% 6% 6% 5%

89% 88% 84% 86% 86%

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011

Independent B-D Full Service Nat'l B-D Banks

Career Independent Agnts Direct

Source: LIMRA, U.S. Individual Annuities survey.

9

© LL Global, Inc.SM

Banks And Career Agents Capture Majority of

Fixed-Rate Deferred Annuity Sales

6% 6% 8% 5% 5% 7% 9% 10%

8% 9%

44% 46% 42% 39% 41%

19% 19% 23% 26% 25%

21% 16% 14% 18% 15%

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011

Independent B-D Full Service Nat'l B-D Banks

Career Independent Agents Direct

Source: LIMRA, U.S. Individual Annuities survey.

10

5/1/2012

6

© LL Global, Inc.SM

Full Service National Broker-Dealers Gain

Immediate Annuity Market Share

6% 9% 10% 8% 8%

12% 10% 15% 19% 22% 8% 9%

14% 14% 15% 26%

30%

34% 32% 31%

35% 33%

19% 21% 19%

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011

Independent B-D Full Sevice Nat'l B-D Banks

Career Independent Agents Direct

Source: LIMRA, U.S. Individual Annuities survey.

11

© LL Global, Inc.SM 12

Drivers of Sales

5/1/2012

7

© LL Global, Inc.SM

GLBs Drive VA Sales

2011 VA New Sales

In Billions

Source: LIMRA, Variable Annuity Guaranteed Living Benefit Election Tracking Survey.

GLB Not Available

$13 B 11%

GLB Not Elected $13 B 12%

GLB Elected $96 B 88%

GLB Available $109 B

89%

VA GLB Election Rates

(When Any GLB Available)

25% 29% 25%

15% 17% 17% 17% 18% 16% 17% 22% 27% 26%

57% 55%

59%

69% 64% 64% 64% 65% 65% 65%

61% 57% 59%

89% 90% 89% 89% 87% 87% 88% 89% 87% 88% 88% 88% 90%

4Q '08

1Q '09

2Q '09

3Q '09

4Q '09

1Q '10

2Q '10

3Q '10

4Q '10

1Q '11

2Q '11

3Q '11

4Q '11

Hybrid GLB GMWB GMAB GMIB GLWB

13

© LL Global, Inc.SM

Indexed GLWB Election Rates Are Strong

Source: LIMRA, Indexed Annuity Guaranteed Lifetime Withdrawal Benefit Elections Survey.

Indexed Annuity GLWB Election Rates

(when available)

GLWB Not Available

$3.1 B 13%

GLWB Available - Not Elected

$7.3 B 34%

GLWB Available -

GLB Elected $14.0 B

66%

GLWB Available $21.3 B

87%

2011 Indexed New Sales

In Billions

14

69%

67%

62%

64%

70%

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Data is based on survey results from 21 companies representing 71 percent of industry sales.

5/1/2012

8

© LL Global, Inc.SM

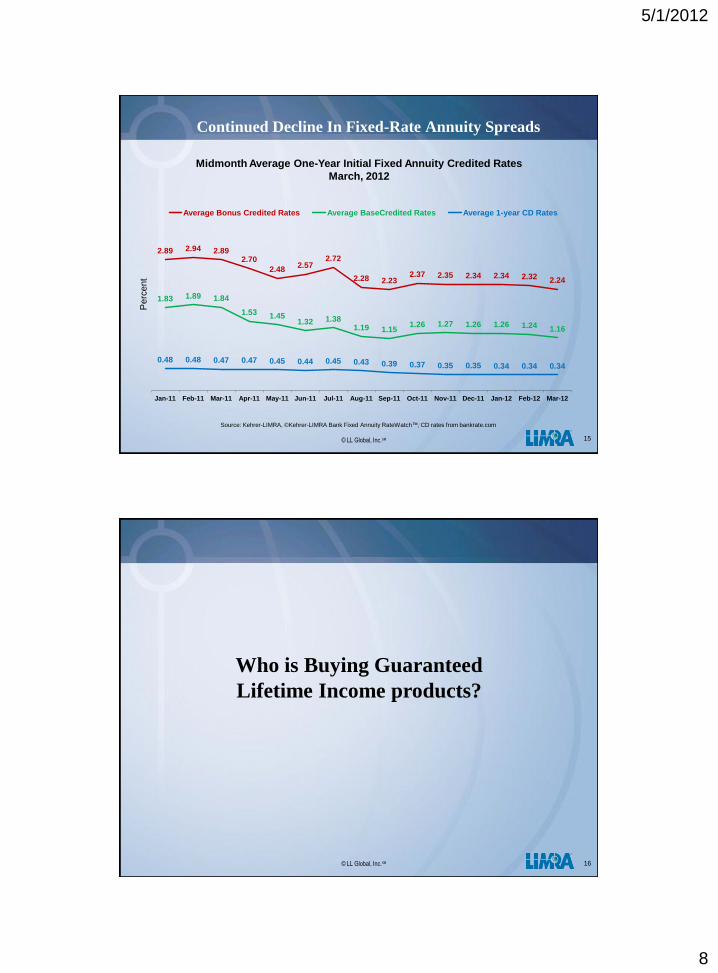

Continued Decline In Fixed-Rate Annuity Spreads

2.89 2.94 2.89 2.70

2.48 2.57

2.72

2.28 2.23 2.37 2.35 2.34 2.34 2.32 2.24

1.83 1.89 1.84

1.53 1.45 1.32 1.38

1.19 1.15 1.26 1.27 1.26 1.26 1.24 1.16

0.48 0.48 0.47 0.47 0.45 0.44 0.45 0.43 0.39 0.37 0.35 0.35 0.34 0.34 0.34

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12

Average Bonus Credited Rates Average BaseCredited Rates Average 1-year CD Rates

Perc

ent

Source: Kehrer-LIMRA, ©Kehrer-LIMRA Bank Fixed Annuity RateWatch™; CD rates from bankrate.com

Midmonth Average One-Year Initial Fixed Annuity Credited Rates

March, 2012

15

© LL Global, Inc.SM 16

Who is Buying Guaranteed

Lifetime Income products?

5/1/2012

9

© LL Global, Inc.SM

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Age 30 35 40 45 50 55 60 65 70 75 80 85

Age of Buyer

GLWB GMIB GMWB GMAB

Note: Based on 392,827 GLWB contracts,128,683 GMIB contracts, 12,642 GMWB contracts and 36,217 GMAB contracts issued in 2010 and still in force at the end of the year.

17

Percent of buyers by age

% of buyers under age 65

GLWB 70%

GMIB 75%

GMWB 58%

GMAB 85%

VA GLWBs And GMIBs Have Similar Buyer Profiles

Source: Guaranteed Living Benefit Utilization Study – 2010 Data, LIMRA 2012.

© LL Global, Inc.SM

GLWBs And Income Annuities – Two Separate Markets

0.0%

2.0%

4.0%

6.0%

30 35 40 45 50 55 60 65 70 75 80 85 90 95

Age of Buyer

VA w/ GLWB

Income Annuity

Source: Guaranteed Living Benefit Utilization Study – 2010 Data, LIMRA 2012

Based on GLWB contracts issued in 2010

Average Age:

VA w/ GLWB 61

Income Annuity 73

Percentage of GLWB and Immediate Income Buyers by Age

Pe

rce

nt

of

bu

ye

rs

18

5/1/2012

10

© LL Global, Inc.SM

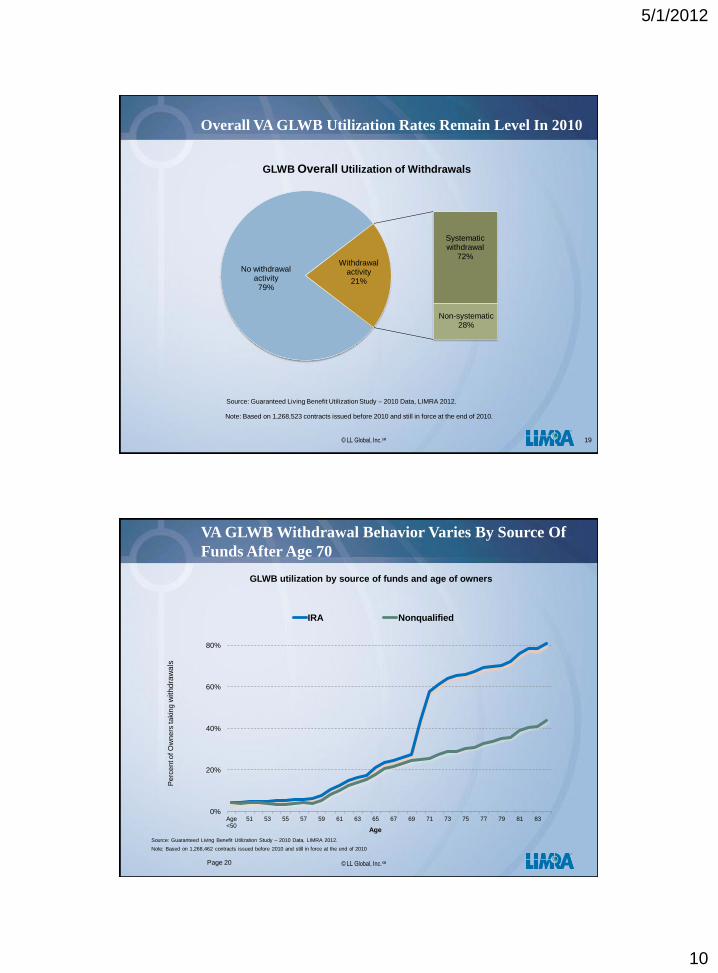

Overall VA GLWB Utilization Rates Remain Level In 2010

19

No withdrawal activity 79%

Systematic withdrawal

72%

Non-systematic 28%

Withdrawal activity 21%

Note: Based on 1,268,523 contracts issued before 2010 and still in force at the end of 2010.

GLWB Overall Utilization of Withdrawals

Source: Guaranteed Living Benefit Utilization Study – 2010 Data, LIMRA 2012.

© LL Global, Inc.SM Page 20

0%

20%

40%

60%

80%

Age <50

51 53 55 57 59 61 63 65 67 69 71 73 75 77 79 81 83

Age

IRA Nonqualified

VA GLWB Withdrawal Behavior Varies By Source Of

Funds After Age 70

GLWB utilization by source of funds and age of owners

Note: Based on 1,268,462 contracts issued before 2010 and still in force at the end of 2010

Pe

rce

nt o

f O

wn

ers

ta

kin

g w

ith

dra

wa

ls

Source: Guaranteed Living Benefit Utilization Study – 2010 Data, LIMRA 2012.

5/1/2012

11

© LL Global, Inc.SM 21

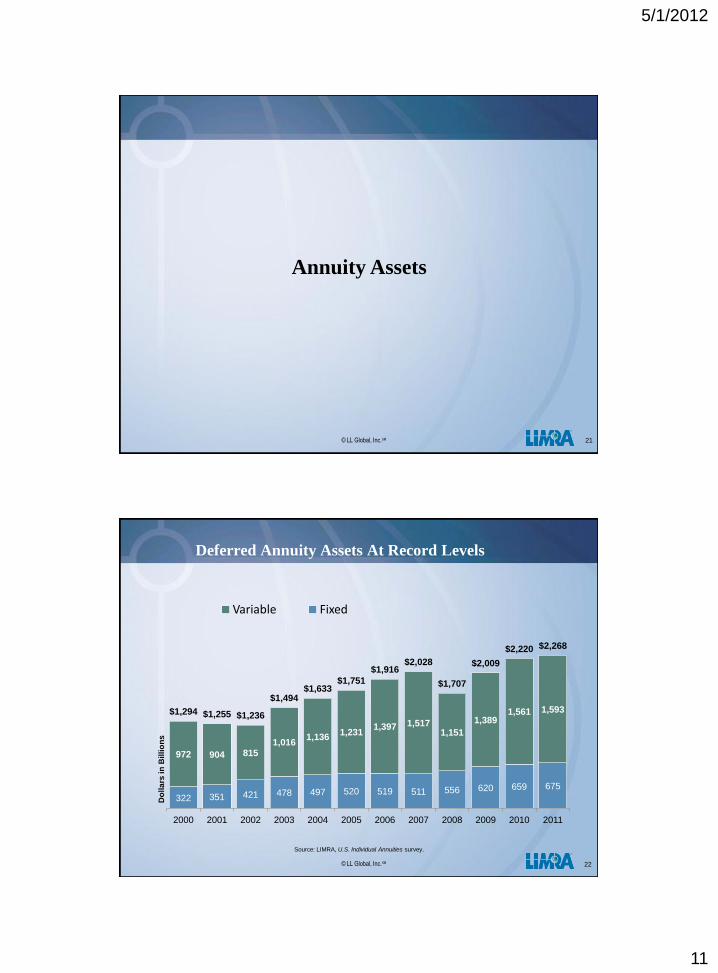

Annuity Assets

© LL Global, Inc.SM

322 351 421 478 497 520 519 511 556 620 659 675

972 904 815 1,016

1,136 1,231

1,397 1,517 1,151

1,389 1,561 1,593 $1,294 $1,255 $1,236

$1,494 $1,633

$1,751

$1,916 $2,028

$1,707

$2,009

$2,220 $2,268

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Variable Fixed

Do

lla

rs in

Bil

lio

ns

Source: LIMRA, U.S. Individual Annuities survey.

Deferred Annuity Assets At Record Levels

22

5/1/2012

12

© LL Global, Inc.SM

Annuity Surrenders Decreasing Or Flat

7.5%

7.2%

5.9%

7.6%

8.2%

5.1%

7.1%

7.8%

5.6%

4%

5%

6%

7%

8%

9%

Q1 '09 Q2 '09 Q3 '09 Q4 '09 Q1 '10 Q2 '10 Q3 '10 Q4 '10 Q1 '11 Q2 '11 Q3 '11 Q4 '11

Variable Indexed Book-value/MVA

Source: LIMRA, U.S. Annuity Persistency.

23

Annualized Contract Surrender Rates

Note: Results based on a constant group of 55 companies.

© LL Global, Inc.SM

GLWB Surrender Rates Are The Lowest Among All GLBs

Source: LIMRA, Variable Annuity Guaranteed Living Benefit Election

Tracking Survey.

$272

$425 $454

$386

$476

$527 $521

$470

$570 $579

$439

$575

GLB assets Non-GLB assets Employer plan assets

2008 2009 2010 2011

CAGR= 29% CAGR= 1% CAGR= 8%

VA Assets by Types In Billions

VA Surrender Rates In 2010

24

Note: Surrender rates are based on contracts issued before 2010.

9.4%

4.1%

2.6%

3.9%

5.6%

8.8%

Non-GLB

With GLB

GLWB GMIB GMWB GMAB

Source: Guaranteed Living Benefit Utilization Study – 2010 Data,

LIMRA 2012.

5/1/2012

13

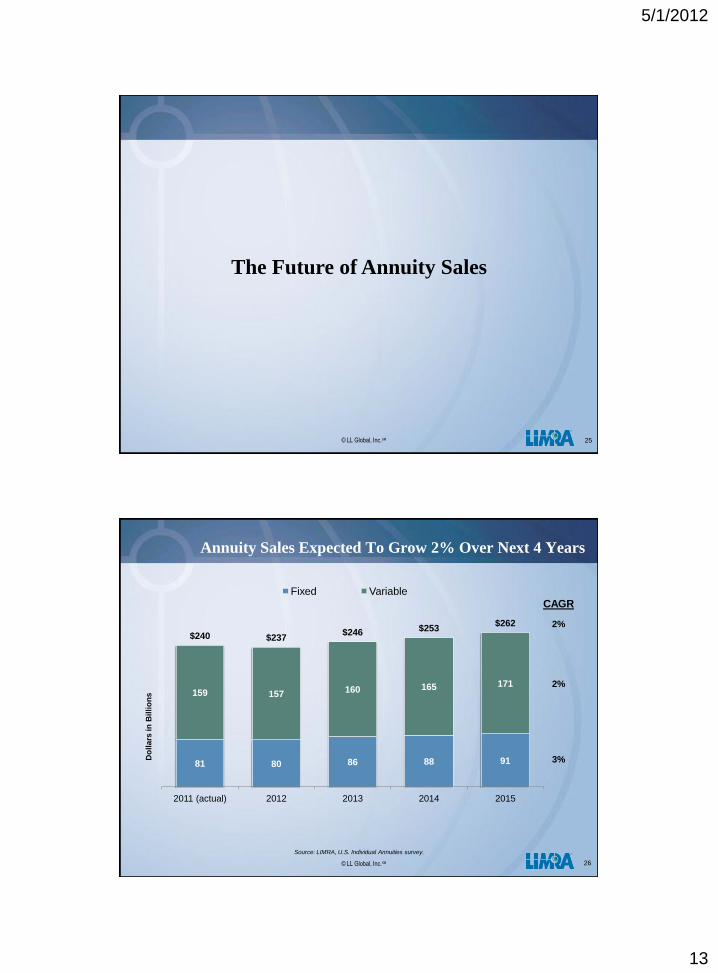

© LL Global, Inc.SM 25

The Future of Annuity Sales

© LL Global, Inc.SM

81 80 86 88 91

159 157 160 165 171

$240 $237 $246 $253

$262

2011 (actual) 2012 2013 2014 2015

Fixed Variable

Do

lla

rs in

Bil

lio

ns

26

Annuity Sales Expected To Grow 2% Over Next 4 Years

CAGR

2%

2%

3%

Source: LIMRA, U.S. Individual Annuities survey.