annual & special meeting june 29, 2015 drill ready discovery commerciality production alue a...

TRANSCRIPT

Page 01

© 2011 Pan Orient Energy Corp.

Annual & Special Meeting June 29, 2015

Page 02

© 2011 Pan Orient Energy Corp.

Cautionary Statement

This presentation contains forward looking statements which involve subjective judgment and analysis and are

subject to significant uncertainties, risks and contingencies including those risk factors associated with the oil and

gas industry, many of which are outside the control of and may be unknown to Pan Orient. No representation,

warranty or assurance, express or implied, is given or made in relation to any forward looking statement. In particular,

no representation, warranty or assumption, express or implied, is given in relation to any underlying assumption or

that any forward looking statement will be achieved. Actual and future events may vary materially from the forward

looking statements and the assumptions on which the forward looking statements were based.

Given these uncertainties, readers are cautioned not to place undue reliance on such forward looking statements, and

should rely on their own independent enquiries, investigations and advice regarding information contained in this

presentation. Any reliance by a reader on the information contained in this presentation is wholly at the readers own

risk.

Readers are cautioned that well test results are not necessarily indicative of long-term performance or of ultimate

recovery.

Pan Orient and its related bodies corporate and affiliates and their respective directors, partners, employees, agents

and advisors disclaim any liability for any direct, indirect or consequential loss or damages suffered by a person or

persons as a result of relying on any statement in, or omission from, this presentation. Subject to any continuing

obligations under applicable law or any relevant listing rules of the TSX-V, Pan Orient disclaims any obligation or

undertaking to disseminate any updates or revisions to any forward looking statements in this presentation to reflect

any change in expectations in relation to any forward looking statements or any such change in events, conditions or

circumstances on which any such statements were based.

Page 03

© 2011 Pan Orient Energy Corp.

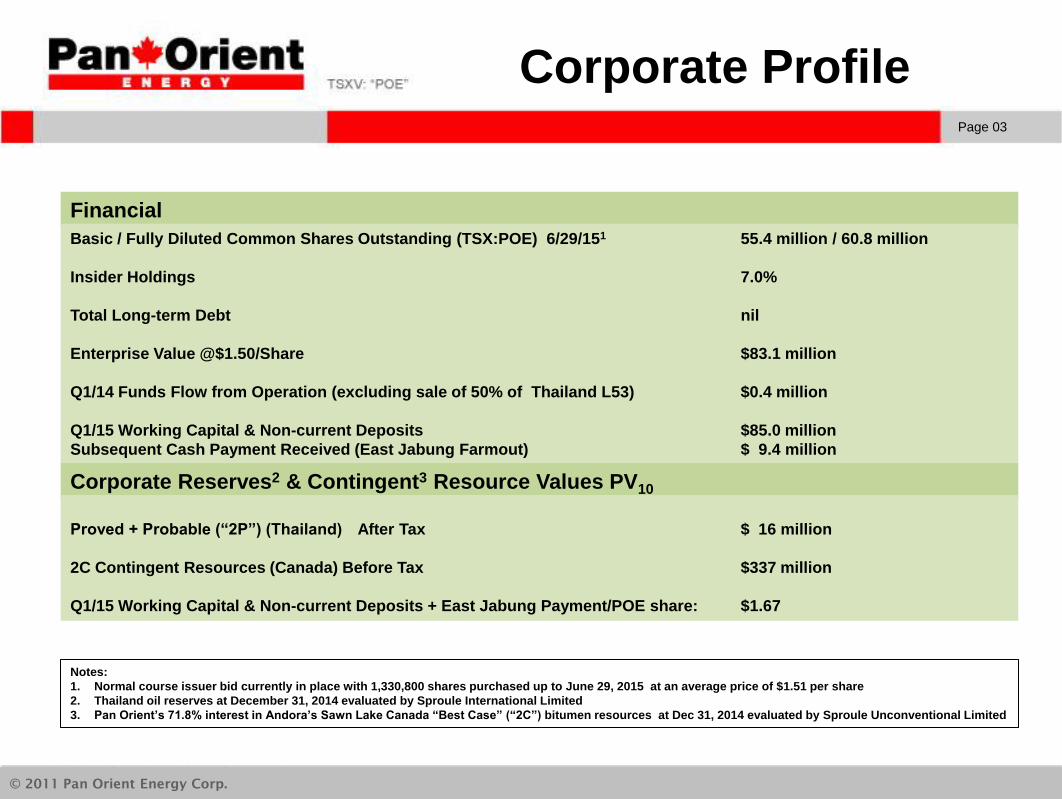

Corporate Profile

Financial

Basic / Fully Diluted Common Shares Outstanding (TSX:POE) 6/29/151 55.4 million / 60.8 million

Insider Holdings 7.0%

Total Long-term Debt nil

Enterprise Value @$1.50/Share $83.1 million

Q1/14 Funds Flow from Operation (excluding sale of 50% of Thailand L53) $0.4 million

Q1/15 Working Capital & Non-current Deposits $85.0 million

Subsequent Cash Payment Received (East Jabung Farmout) $ 9.4 million

Corporate Reserves2 & Contingent3 Resource Values PV10

Proved + Probable (“2P”) (Thailand) After Tax $ 16 million

2C Contingent Resources (Canada) Before Tax $337 million

Q1/15 Working Capital & Non-current Deposits + East Jabung Payment/POE share: $1.67

Notes:

1. Normal course issuer bid currently in place with 1,330,800 shares purchased up to June 29, 2015 at an average price of $1.51 per share

2. Thailand oil reserves at December 31, 2014 evaluated by Sproule International Limited

3. Pan Orient’s 71.8% interest in Andora’s Sawn Lake Canada “Best Case” (“2C”) bitumen resources at Dec 31, 2014 evaluated by Sproule Unconventional Limited

Page 04

© 2011 Pan Orient Energy Corp.

A Simple Story….

1. Currently trading near positive working capital & non current deposit value of approximately $94.4MM cdn

2. All Asian assets profitable in a sub $60USD Brent environment

3. Drilling Akeh-1 Indonesian exploration well (approx $5MMcdn) at Batu Gajah PSC in August 2015:

– Offsetting an existing gas, condensate and oil discovery in Batu Gajah PSC in August 2015.

– Batu Gajah has a $50MMusd cost recovery pool net to POE that would be recovered from 80% of the gross revenue

until payout ,upon first production

– Onshore, with low drilling & development costs & substantial additional prospects that can be drilled with cost recovery

dollars upon first production

4. Carried for at least 1 high impact exploration well in East Jabung PSC Indonesia in Q2/16:

– The best fiscal terms in Indonesia with a 65%/35% after tax & cost recovery split in favor of the GOI for oil after POE

recovers its costs

– There is a second carried well if success in the first well

– Onshore with low drilling & development costs

– Very experienced operator in the region with nearby existing infrastructure (Talisman)

5. Approx 300 BOPD of low cost oil production onshore Thailand that will be used to fund material exploration

upside at the A North East Prospect, drilling Q4/15 –Q1/16

6. A SAGD bitumen pilot currently performing above the third party engineering well performance estimate for

the “best case” contingent resources:

– Steam chamber has yet to reach the cap rock whereupon higher, near peak rates is anticipated

– Andora Energy – operator & 72% owned by POE has a monthly burn rate of approx $0.1MM while operating the pilot &

approx $6.5MMcdn cash…..we can wait….. if required

•

Page 05

© 2011 Pan Orient Energy Corp.

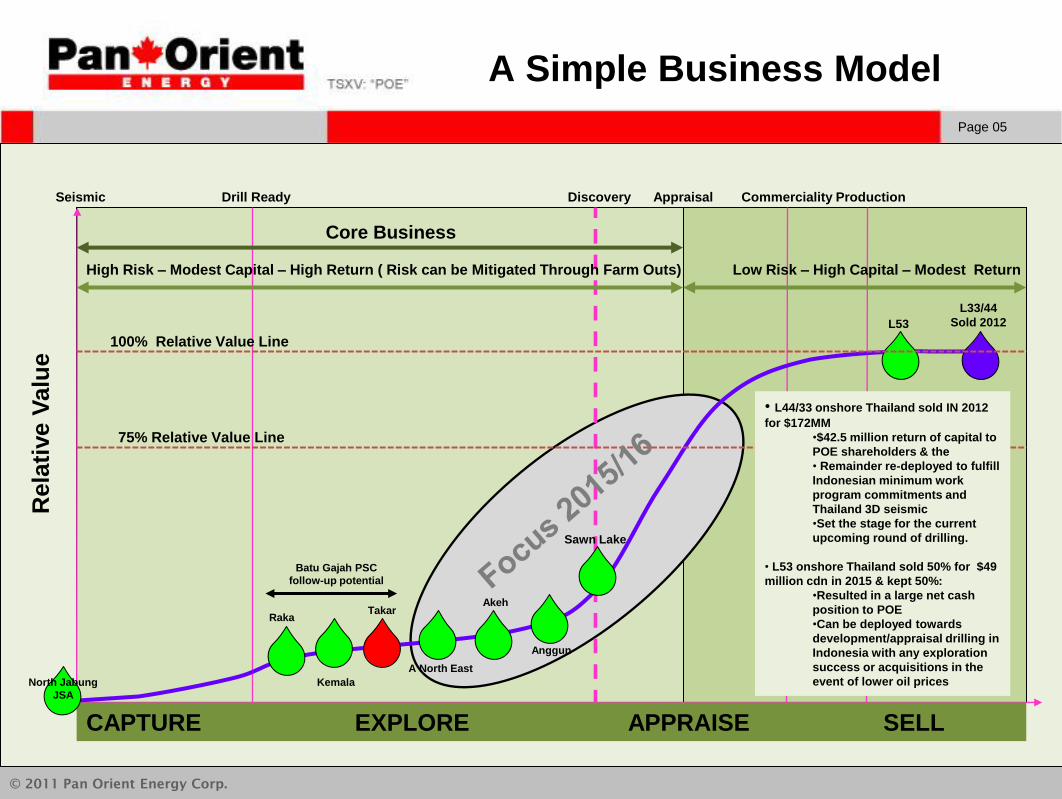

A Simple Business Model

Commerciality Drill Ready Discovery Production Seismic

Rela

tive V

alu

e

A North East

Anggun

Akeh

Sawn Lake

Raka

Kemala

L33/44

Sold 2012

Takar

100% Relative Value Line

75% Relative Value Line

Core Business

High Risk – Modest Capital – High Return ( Risk can be Mitigated Through Farm Outs) Low Risk – High Capital – Modest Return

Appraisal

• L44/33 onshore Thailand sold IN 2012

for $172MM

•$42.5 million return of capital to

POE shareholders & the

• Remainder re-deployed to fulfill

Indonesian minimum work

program commitments and

Thailand 3D seismic

•Set the stage for the current

upcoming round of drilling.

• L53 onshore Thailand sold 50% for $49

million cdn in 2015 & kept 50%:

•Resulted in a large net cash

position to POE

•Can be deployed towards

development/appraisal drilling in

Indonesia with any exploration

success or acquisitions in the

event of lower oil prices

CAPTURE EXPLORE APPRAISE SELL

L53

North Jabung

JSA

Batu Gajah PSC

follow-up potential

Page 06

© 2011 Pan Orient Energy Corp.

A Very Good L53 Thailand

Transaction

• Sale of 50% of the shares in POES which holds a 100%

interest in Concession L53, to Sea Oil Public Company

listed on the Stock Exchange of Thailand

• Gross consideration of CDN$53.5MM

• Net CDN$48.9 million for L53 interests after deducting

working capital of $3.2 million & transaction costs

• Closed Feb 2, 2015

• Modest L53 cash flow will be utilized towards further

exploration on the concession

• Proceeds to be redeployed to any possible future

Indonesian development

E-01 Rig on L53-G1 Well Location

Page 07

© 2011 Pan Orient Energy Corp.

East Jabung PSC (POE 49% Non Operator)

– 2,948 km2 (Gross)

Batu Gajah PSC (POE 77% Operator)

– 793 km2 (Gross)

North Jabung JSA (POE 20% Option/Non Operator)

– 4,106 km2 (Gross)

Core Region for POE

Gas Fields

Oil Fields

Gas Condensate Fields

• A 51% participating interest & operatorship In East

Jabung transferred to Talisman (Repsol) in

exchange for:

• $8MMusd cash payment (received Q2/15)

• 100% of the first $10MMusd + overhead

towards the drilling of the first well

• 100% of the first $5MMusd + overhead

towards the drilling of the second well if the

first well is successful

• POE granted a 20% option on the North

Jabung Joint Study Area “JSA” in South

Sumatra

East Jabung

PSC

Conoco/Talisman

Production Pertamina/Talisman

Production

With Another at East Jabung

North Jabung

JSA

Batu Gajah

PSC

Page 08

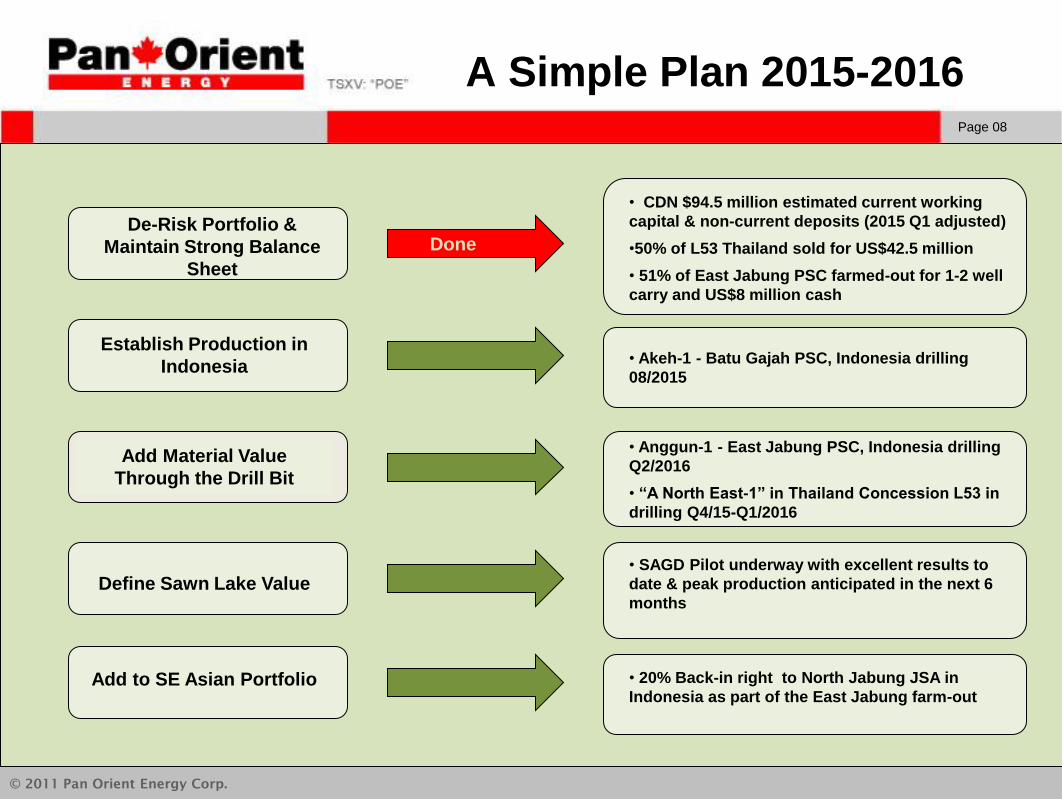

© 2011 Pan Orient Energy Corp.

A Simple Plan 2015-2016

De-Risk Portfolio &

Maintain Strong Balance

Sheet

Establish Production in

Indonesia

Add Material Value

Through the Drill Bit

Define Sawn Lake Value

Add to SE Asian Portfolio

• CDN $94.5 million estimated current working

capital & non-current deposits (2015 Q1 adjusted)

•50% of L53 Thailand sold for US$42.5 million

• 51% of East Jabung PSC farmed-out for 1-2 well

carry and US$8 million cash

• Akeh-1 - Batu Gajah PSC, Indonesia drilling

08/2015

• Anggun-1 - East Jabung PSC, Indonesia drilling

Q2/2016

• “A North East-1” in Thailand Concession L53 in

drilling Q4/15-Q1/2016

• SAGD Pilot underway with excellent results to

date & peak production anticipated in the next 6

months

• 20% Back-in right to North Jabung JSA in

Indonesia as part of the East Jabung farm-out

Done

Page 09

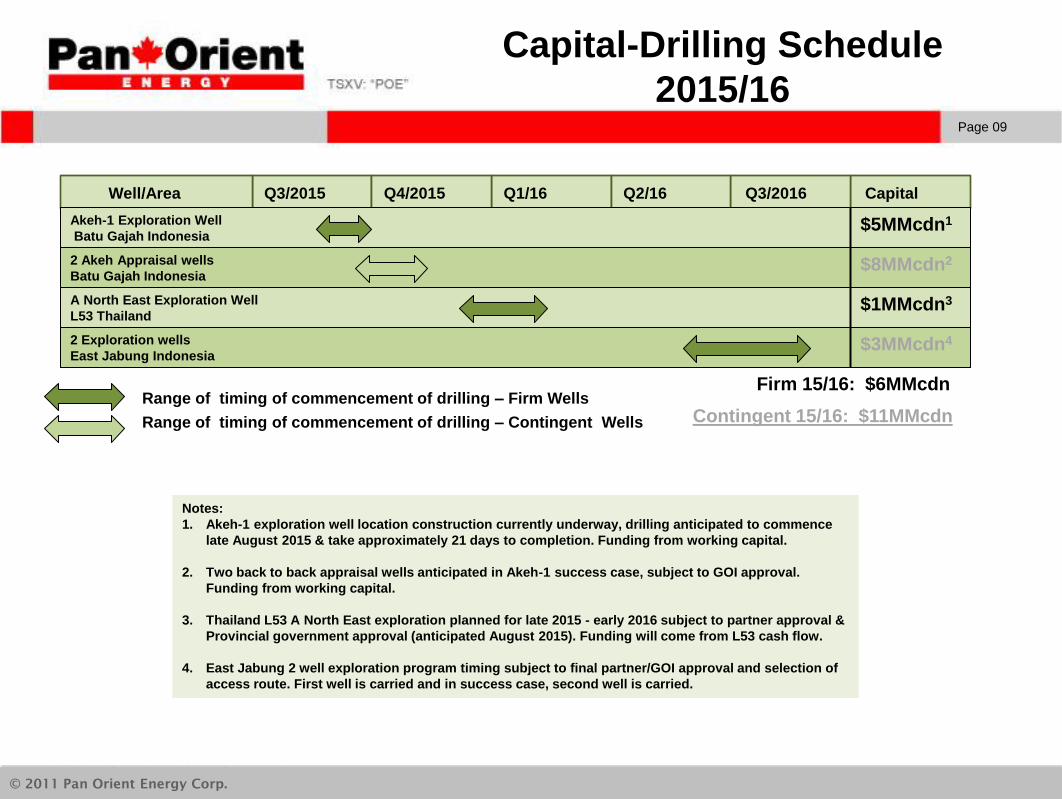

© 2011 Pan Orient Energy Corp.

Capital-Drilling Schedule

2015/16

Notes:

1. Akeh-1 exploration well location construction currently underway, drilling anticipated to commence

late August 2015 & take approximately 21 days to completion. Funding from working capital.

2. Two back to back appraisal wells anticipated in Akeh-1 success case, subject to GOI approval.

Funding from working capital.

3. Thailand L53 A North East exploration planned for late 2015 - early 2016 subject to partner approval &

Provincial government approval (anticipated August 2015). Funding will come from L53 cash flow.

4. East Jabung 2 well exploration program timing subject to final partner/GOI approval and selection of

access route. First well is carried and in success case, second well is carried.

A North East Exploration Well

L53 Thailand

Capital Q3/2015 Q1/16 Q3/2016 Q4/2015 Well/Area

2 Akeh Appraisal wells

Batu Gajah Indonesia

2 Exploration wells

East Jabung Indonesia

Q2/16

Akeh-1 Exploration Well

Batu Gajah Indonesia

Range of timing of commencement of drilling – Firm Wells

Range of timing of commencement of drilling – Contingent Wells

$5MMcdn1

$8MMcdn2

$1MMcdn3

$3MMcdn4

Firm 15/16: $6MMcdn

Contingent 15/16: $11MMcdn

Page 010

© 2011 Pan Orient Energy Corp.

INDONESIA

Page 011

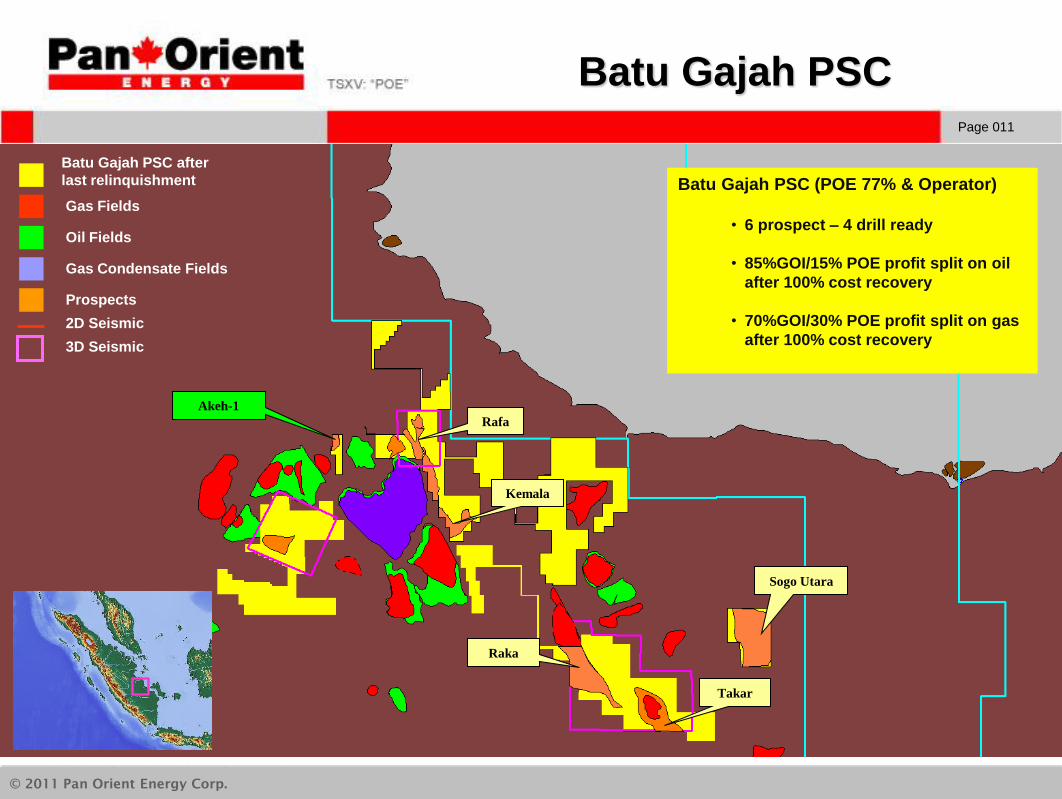

© 2011 Pan Orient Energy Corp.

Batu Gajah PSC

Gas Fields

Oil Fields

Gas Condensate Fields

Prospects

Pan Orient 3D Seismic 2013

Wells Drilled (POE)

East Jabung PSC

POE 100%

Akeh-1

Rafa

Kemala

Raka

Takar

Sogo Utara

Batu Gajah PSC

Batu Gajah PSC after

last relinquishment

Gas Fields

Oil Fields

Gas Condensate Fields

Prospects

2D Seismic

3D Seismic

Batu Gajah PSC (POE 77% & Operator)

• 6 prospect – 4 drill ready

• 85%GOI/15% POE profit split on oil

after 100% cost recovery

• 70%GOI/30% POE profit split on gas

after 100% cost recovery

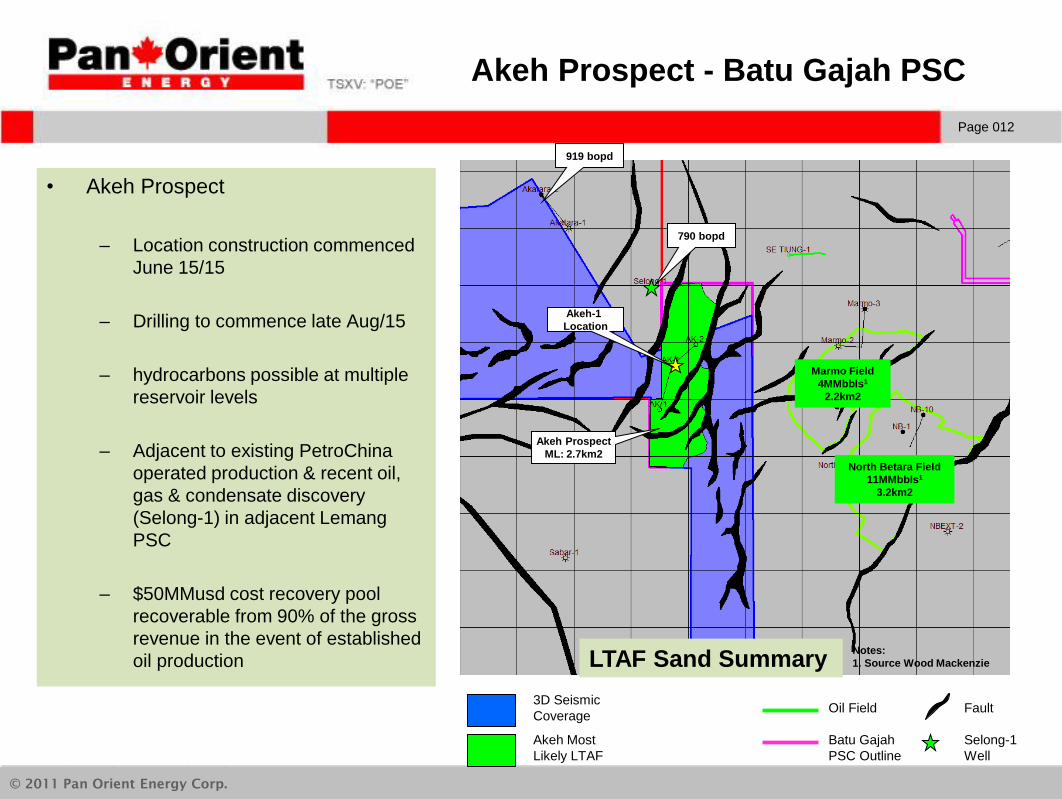

Page 012

© 2011 Pan Orient Energy Corp.

Akeh Prospect - Batu Gajah PSC

• Akeh Prospect

– Location construction commenced

June 15/15

– Drilling to commence late Aug/15

– hydrocarbons possible at multiple

reservoir levels

– Adjacent to existing PetroChina

operated production & recent oil,

gas & condensate discovery

(Selong-1) in adjacent Lemang

PSC

– $50MMusd cost recovery pool

recoverable from 90% of the gross

revenue in the event of established

oil production

Marmo Field

4MMbbls1

2.2km2

North Betara Field

11MMbbls1

3.2km2

3D Seismic

Coverage

Akeh Most

Likely LTAF

Oil Field

Batu Gajah

PSC Outline

Fault

Notes:

1. Source Wood Mackenzie

790 bopd

919 bopd

Selong-1

Well

Akeh Prospect

ML: 2.7km2

LTAF Sand Summary

Akeh-1

Location

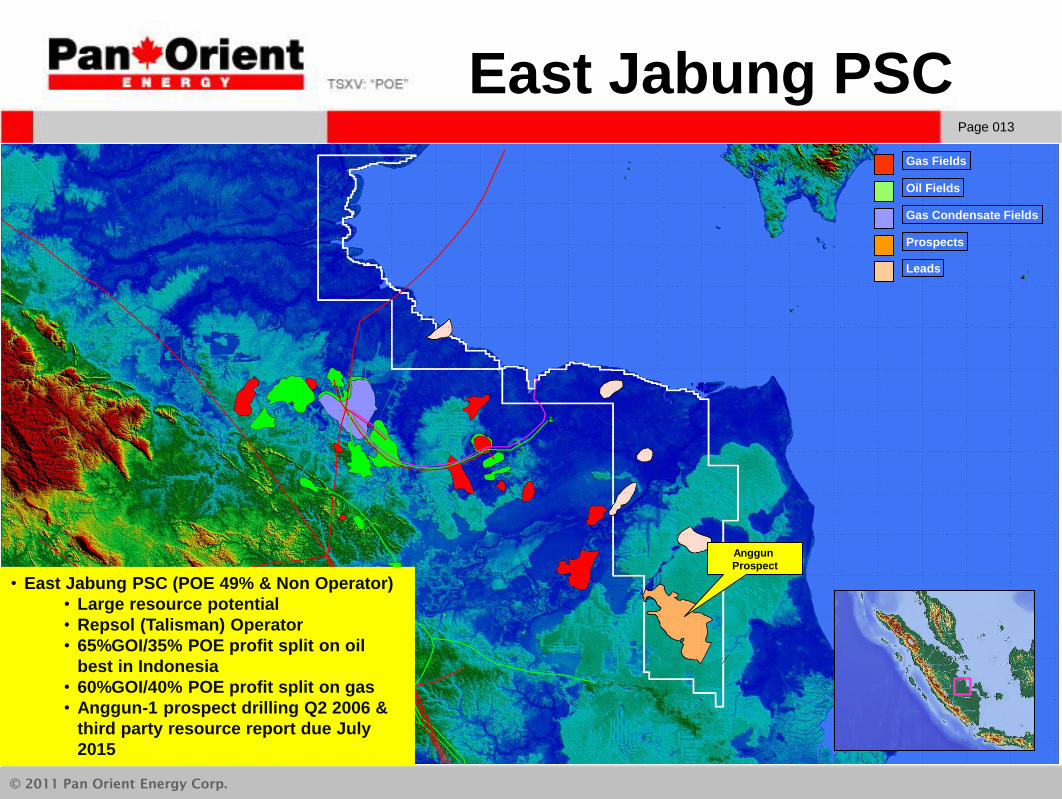

Page 013

© 2011 Pan Orient Energy Corp.

East Jabung PSC

Gas Fields

Oil Fields

Gas Condensate Fields

Prospects

Leads

• East Jabung PSC (POE 49% & Non Operator)

• Large resource potential

• Repsol (Talisman) Operator

• 65%GOI/35% POE profit split on oil

best in Indonesia

• 60%GOI/40% POE profit split on gas

• Anggun-1 prospect drilling Q2 2006 &

third party resource report due July

2015

Anggun

Prospect

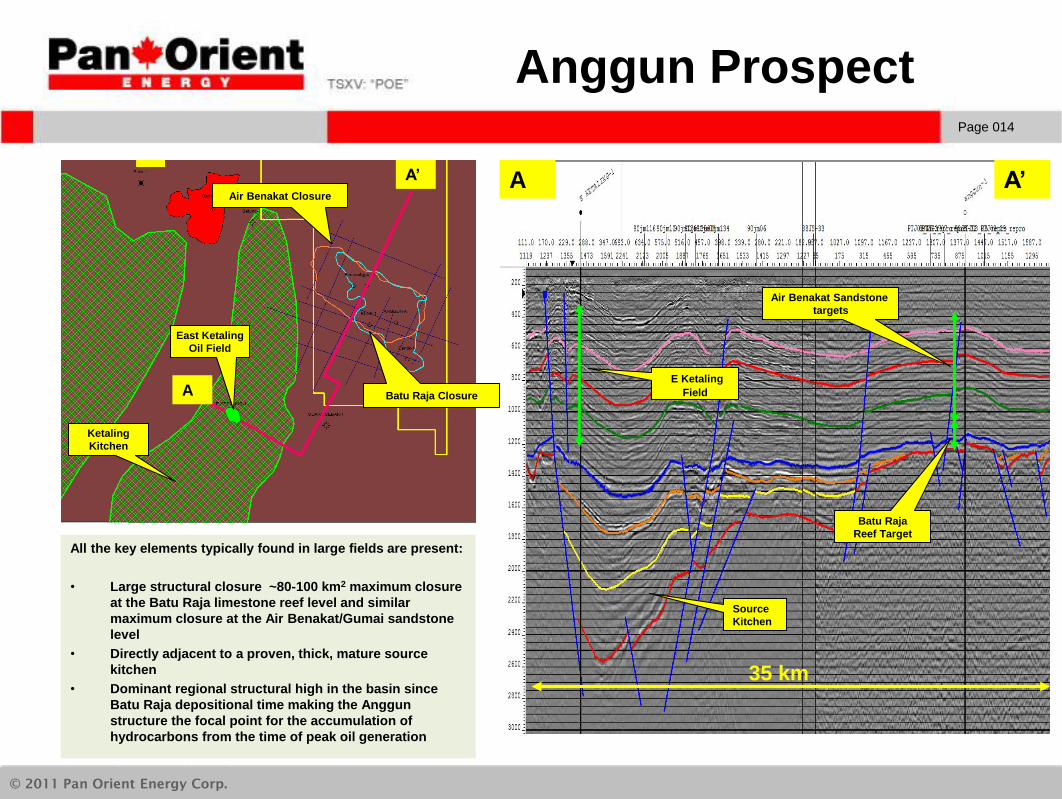

Page 014

© 2011 Pan Orient Energy Corp.

Anggun Prospect

Batu Raja

Reef Target

Ketaling

Kitchen

A

A’ A A’

Source

Kitchen

E Ketaling

Field

Air Benakat Sandstone

targets

All the key elements typically found in large fields are present:

• Large structural closure ~80-100 km2 maximum closure

at the Batu Raja limestone reef level and similar

maximum closure at the Air Benakat/Gumai sandstone

level

• Directly adjacent to a proven, thick, mature source

kitchen

• Dominant regional structural high in the basin since

Batu Raja depositional time making the Anggun

structure the focal point for the accumulation of

hydrocarbons from the time of peak oil generation

35 km

Air Benakat Closure

Batu Raja Closure

East Ketaling

Oil Field

Page 015

© 2011 Pan Orient Energy Corp.

THAILAND

Page 016

© 2011 Pan Orient Energy Corp.

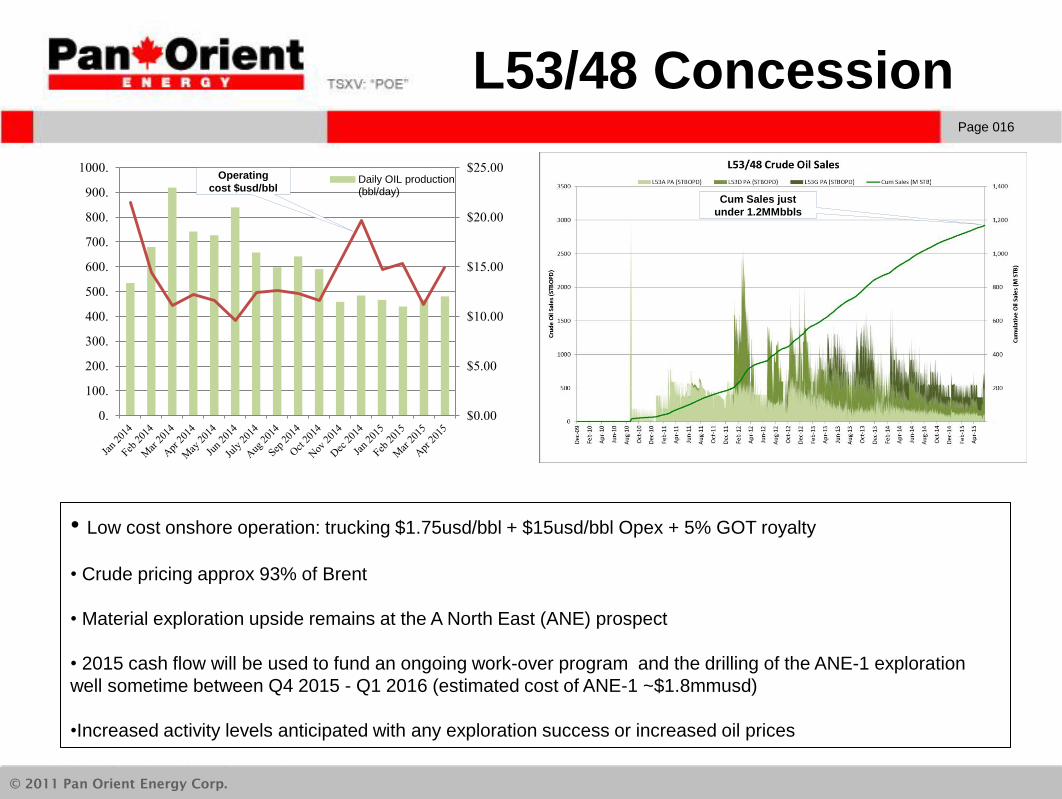

L53/48 Concession

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

0.

100.

200.

300.

400.

500.

600.

700.

800.

900.

1000.Daily OIL production(bbl/day)

• Low cost onshore operation: trucking $1.75usd/bbl + $15usd/bbl Opex + 5% GOT royalty

• Crude pricing approx 93% of Brent

• Material exploration upside remains at the A North East (ANE) prospect

• 2015 cash flow will be used to fund an ongoing work-over program and the drilling of the ANE-1 exploration

well sometime between Q4 2015 - Q1 2016 (estimated cost of ANE-1 ~$1.8mmusd)

•Increased activity levels anticipated with any exploration success or increased oil prices

Operating

cost $usd/bbl Cum Sales just

under 1.2MMbbls

Page 017

© 2011 Pan Orient Energy Corp.

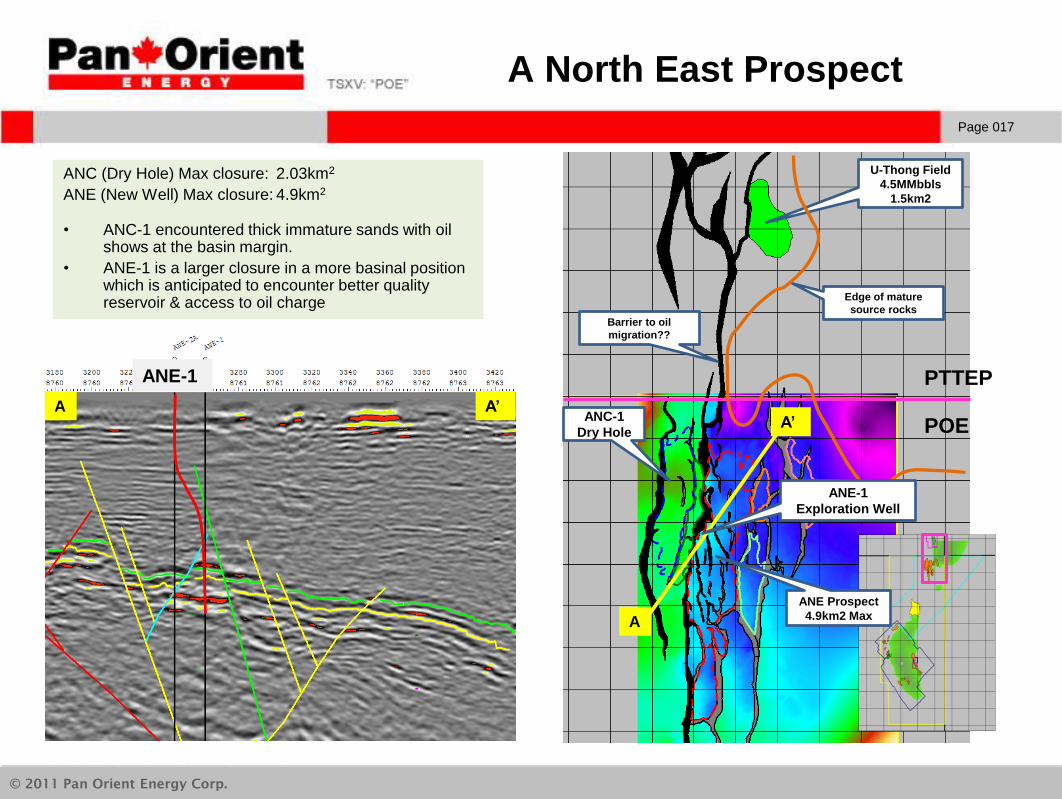

A North East Prospect

ANC (Dry Hole) Max closure: 2.03km2

ANE (New Well) Max closure: 4.9km2

• ANC-1 encountered thick immature sands with oil shows at the basin margin.

• ANE-1 is a larger closure in a more basinal position which is anticipated to encounter better quality reservoir & access to oil charge

ANC-1

Dry Hole A’

A A’

A

U-Thong Field

4.5MMbbls

1.5km2

ANE Prospect

4.9km2 Max

POE

PTTEP ANE-1

Barrier to oil

migration??

Edge of mature

source rocks

ANE-1

Exploration Well

Page 018

© 2011 Pan Orient Energy Corp.

CANADA

Page 019

© 2011 Pan Orient Energy Corp.

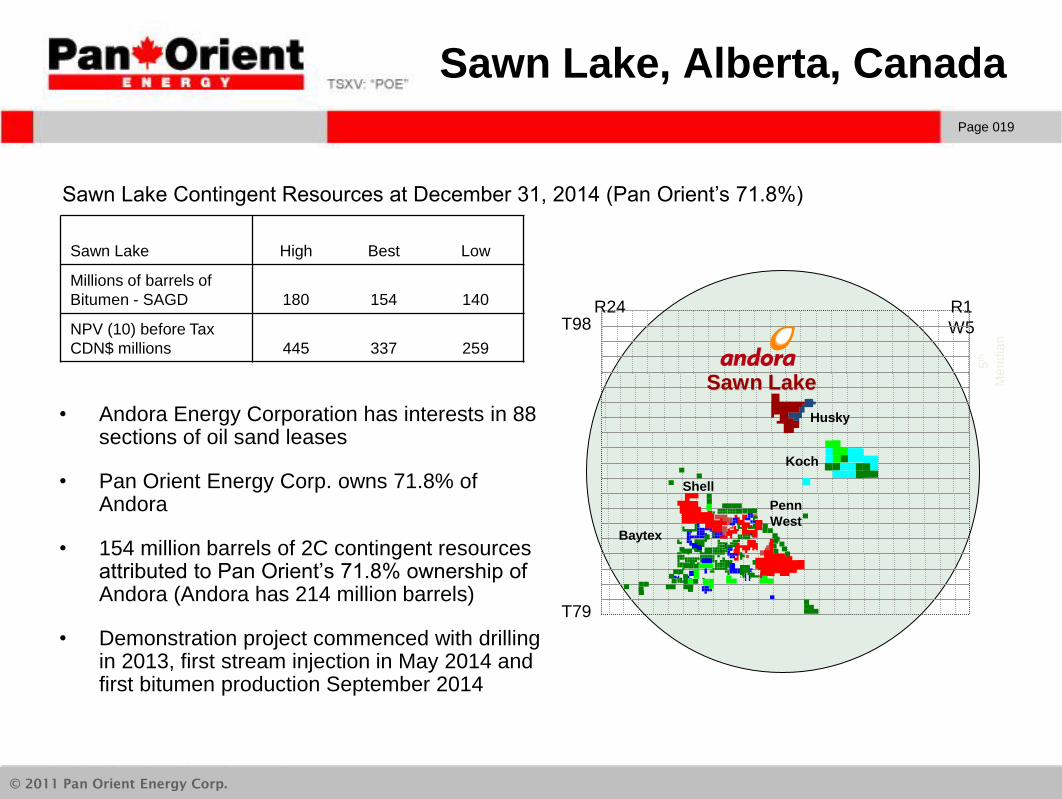

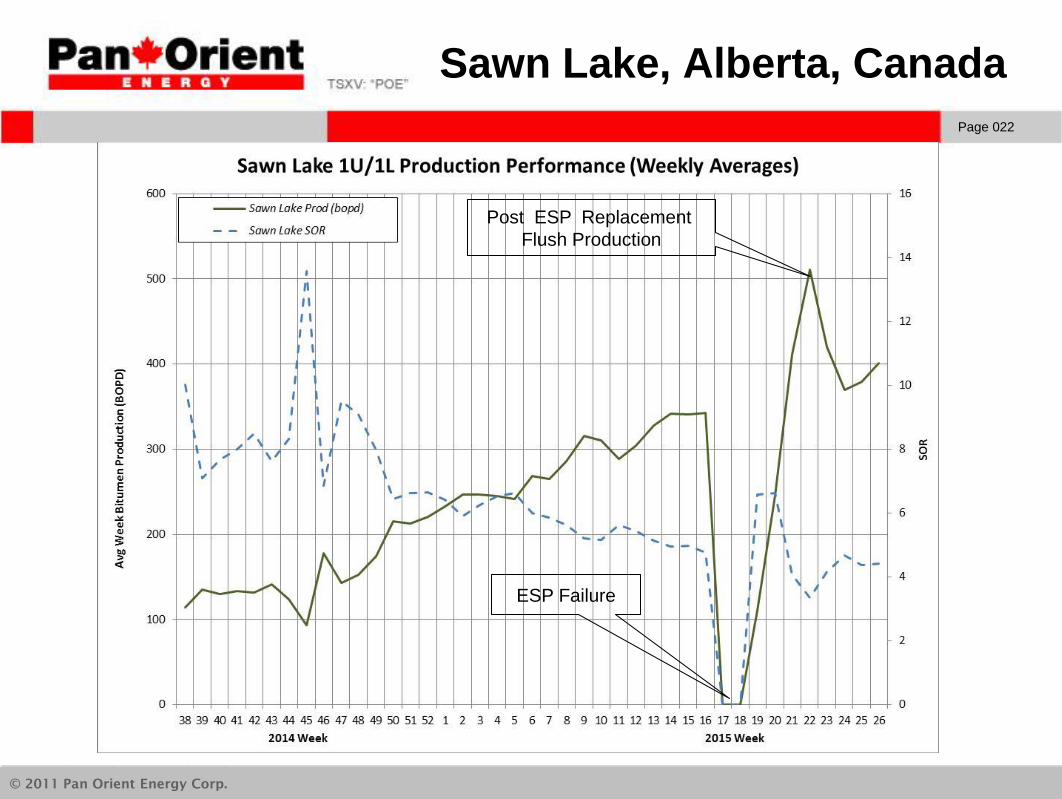

Sawn Lake, Alberta, Canada

• Andora Energy Corporation has interests in 88 sections of oil sand leases

• Pan Orient Energy Corp. owns 71.8% of Andora

• 154 million barrels of 2C contingent resources attributed to Pan Orient’s 71.8% ownership of Andora (Andora has 214 million barrels)

• Demonstration project commenced with drilling in 2013, first stream injection in May 2014 and first bitumen production September 2014

Sawn Lake High Best Low

Millions of barrels of

Bitumen - SAGD 180 154 140

NPV (10) before Tax

CDN$ millions 445 337 259

Sawn Lake Contingent Resources at December 31, 2014 (Pan Orient’s 71.8%)

Red

Earth

T79

R1

W5

R24 T98

Husky

Baytex

5th

Meridia

n

Shell

Penn

West

Sawn Lake

Koch

Page 020

© 2011 Pan Orient Energy Corp.

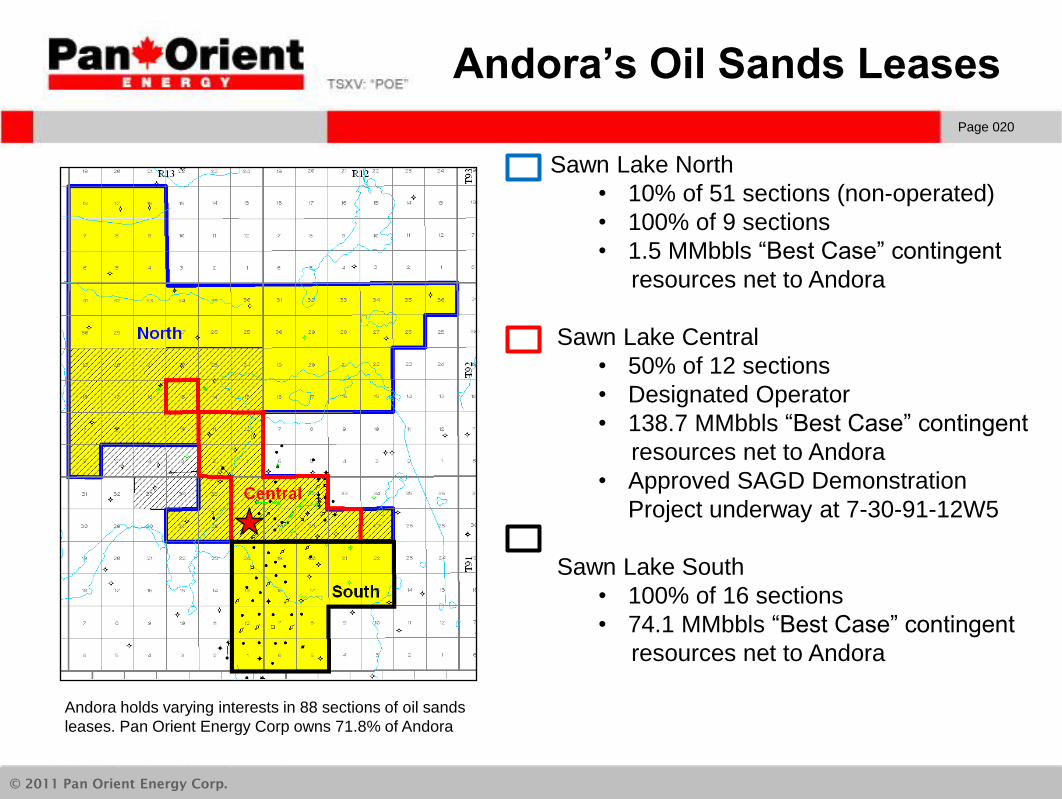

Andora’s Oil Sands Leases

Sawn Lake North

• 10% of 51 sections (non-operated)

• 100% of 9 sections

• 1.5 MMbbls “Best Case” contingent

resources net to Andora

Sawn Lake Central

• 50% of 12 sections

• Designated Operator

• 138.7 MMbbls “Best Case” contingent

resources net to Andora

• Approved SAGD Demonstration

Project underway at 7-30-91-12W5

Sawn Lake South

• 100% of 16 sections

• 74.1 MMbbls “Best Case” contingent

resources net to Andora

Andora holds varying interests in 88 sections of oil sands

leases. Pan Orient Energy Corp owns 71.8% of Andora

Page 021

© 2011 Pan Orient Energy Corp.

Sawn Lake Pilot Project

• Results to date of the first SAGD well pair indicate that the SAGD process works in the Bluesky

formation reservoir.

• The well is still in its ramp-up phase and the steam chamber has not reached the top of the Bluesky

reservoir. For the period June 1st to 22nd bitumen production averaged 391 BOPD with a Steam-

Oil Ratio (“SOR”) of 4.4. May 2015 bitumen production averaged 388 BOPD with an SOR of 4.3.

All production numbers are on a 100% basis.

• Production exceeding “Best” case estimate used by Sproule in the December 31, 2014 contingent

resource evaluation of 345 BOPD with an SOR of 4.0. Sproule “High” case is 449 BOPD with an

SOR of 3.1.

• Canadian patent approved for produced water boiler (PWB) technology capable of meeting

regulatory water recycle requirements on a per well pair basis allowing for modular, scaled

development

• Starting the process for next set of regulatory approvals for expansion.

Page 022

© 2011 Pan Orient Energy Corp.

Sawn Lake, Alberta, Canada

ESP Failure

Post ESP Replacement

Flush Production

Page 023

© 2011 Pan Orient Energy Corp.

PWB Technology

Patent

Canadian patent issued (2015-06-16) for Produced Water Boiler (PWB) technology enabling steam

generation from SAGD produced water meeting regulatory water recycle requirements on a per well pair

scale enabling lower capital SAGD project expansions with mitigated capital requirements and risk.

Background

• Economics of scale surrounding traditional SAGD water recycle technologies have generally required

large capital investments to achieve adequate capital intensities. These large scale projects are

inflexible once initiated and are susceptible to severe cost overruns

Application

• Produced Water Boiler (PWB) technology allows for low capital intensities at a smaller scale

(1000bopd+, $70MM+)

• Well pair scaled expansions allow for conversion of pilot facilities to commercial pods that meet

regulatory requirements, enable modularization of facilities to reduce costs and optimise well pair

placement

Page 024

© 2011 Pan Orient Energy Corp.

Contacts

Pan Orient Energy Corp

Suite 1505, 505 3rd St SW

Calgary, Canada

Telephone: +1 403 294-1770

Fax: +1 403 294-1780

www.panorient.ca