andritz capital market days...

TRANSCRIPT

Capital Market Days 2007

23-25 October 2007China

Slide No. 2

Disclaimer

Certain statements contained in this presentation constitute “forward-looking statements.” These statements, which contain the words “believe”, “intend”, “expect” and words of similar meaning, reflect Management’s beliefs and expectations and are subject to risks and uncertainties that may cause actual results to differ materially. As a result, readers are cautioned not to place undue reliance on such forward-looking statements. The Company disclaims any obligation to publicly announce the result of any revisions to the forward-looking statements made herein, except where it would be required to do so under applicable law.

Slide No. 3

Agenda

Update on recent developments

- Review on targets of past Andritz Investor Days

- Important achievements and developments during the last 12 months

Growth and the supply chain

Outlook 2008 by Business Area

Summary

Slide No. 4

Agenda

Update on recent developments

- Review on targets of past Andritz Investor Days

- Important achievements and developments during the last 12 months

Growth and the supply chain

Outlook 2008 by Business Area

Summary

Slide No. 5

Review on targets of past Investor Days

Increase profitability (EBITDA) of Feed Technology Business Area (FT) from 4.4% in 2001 to 10% in 2004

Targets Achievements

Target reached

Become a 2 billion Euro companyby 2007

Event

Investor Days 2003:

Investor Days 2004: Target reached

Reach Group EBIT(A) margin of 7% by 2008

Increase dividend payout ratio to 40% over the next few years

Investor Days 2005:

Targets not yetreached!

Slide No. 6

5.2 5.3 5.1

6.3 6.15.9

0

1

2

3

4

5

6

7

2001 2002 2003 2004 2005 2006

Update on EBITA margin target of 7%

Achievements

EBIT(A) margins Andritz Group (%)

Margin development in recent years mainly influenced by acquisition of VA TECH HYDRO and fast growth of the capital business

Excluding VA TECH HYDRO, EBITA margin in 2006 would have been approx. 6.3%

Due to the strong growth of the capital business, service sales as % of total sales declined from 26.5% in 2004 to 22.5% in 2006, thus impacting margin on the down side

Slide No. 7

Target to increase profitability of VA TECH HYDRO by 1 percentage point per year: from ~3.5% in H2 2006 to 6.5% in 2009:

- Full integration of VA TECH HYDRO’s existing production facilities into Andritz Group

- Optimization of Group sourcing through integration of VA TECH HYDRO

- Regional employee adjustment

Recent acquisitions of Service companies and launch of new products should support share of Service Sales, thus enhancing margins

Maintain focus on correct pricing

Planned measures and expected developments to reach EBITA Group goal of 7%

Slide No. 8

Update on dividend payout ratio

Dividend per share and payout ratio: 2002: 0.23 EUR (44.1%)2003: 0.25 EUR (44.2%)2004: 0.35 EUR (34.3%)2005: 0.50 EUR (32.6%)2006: 0.75 EUR (32.5%)

New target is to increase the dividend payout ratio to 40%for the financial year 2007

Dividend per share (adjusted for share split of 1:4)

0.23 0.25

0.35

0.50

0.75

0,00

0,50

1,00

2002 2003 2004 2005 2006

EUR1.00

0.50

0.00

Slide No. 9

Agenda

Update on recent developments

- Review on targets of past Andritz Investor Days

- Important achievements and developments during the last 12 months

Growth and the supply chain

Outlook 2008 by Business Area

Summary

Slide No. 10

Continuation of Group growth in 2007 and 2008

Successful integration and development of VA TECH HYDRO

Complementary acquisitions further extend product range and strengthen market position

Successful start-ups and major orders in pulp and stainless steel confirm excellent market position

Important achievements and developments during the last 12 months

Slide No. 11

Continuation of Group growth in 2007 and 2008

13191110 1225

1481

2710

35003200

1744

937656666

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007E 2008E

Andritz Group Sales in MEUR

For 2007, Group Sales are expected to increase by 20% compared to 2006; most of the Sales increase comes from first-time consolidation of VA TECH HYDRO

Based on the current high Order Backlog of approximately 3.8 bn EUR, Group Sales are expected to grow organically to approximately 3.5 bn EUR in 2008

CAGR 1998-2007:+19%

Slide No. 12

Strong organic growth

666

937

1319

2710

3200

14811225

1110

1744

3500

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007E 2008E

Andritz Group Sales in MEUR

+7.4%

+18.4%

-15.8%+7.1% +13

.0%

+16.5

%

+29.

6%

656

+8%Since 1998, the Andritz Group has shown a strong organic growth of 12% p.a.

Organic growth+12% p.a.

Slide No. 13

0

500

1000

1500

2000

2500

3000

1998 2006

+18%

+40%

+16%

+23%

+7%

Growth by Business AreaSales 1998-2006

666 MEUR

2,710 MEUR

+264%

+1,343

%+2

34%

+417

%+7

5%

Pulp and Paper

Hydro Power

Rolling Mills and Strip Processing

Lines

Environmentand Process

Feed and Biofuel

CAGR by Business Area:MEUR

Slide No. 14

0

500

1000

1500

2000

2500

3000

1998 2006

+260%

+120%

+3,900%

+370

%+280

%

666 MEUR

2,710 MEUR

Growth by regionSales 1998-2006

+21%

+18%

+11%

+59%

+44%

Europe

North America

South America

Asia

ROW

CAGR by region:MEUR

Slide No. 15

Further continuation of Group growth in 2007 and 2008

Successful integration and development of VA TECH HYDRO

Complementary acquisitions further extend product range and strengthen market position

Successful start-ups and major orders in pulp and stainless steel confirm excellent market position

Important achievements during the last 12 months

Slide No. 16

R&DAndritz HM will be fully integrated into VA TECH HYDRO’s R&D program

EngineeringHarmonization of all computation and design (CAD) tools and software

Organizational integrationIntegration has been progressing as planned since June 1, 2006; completion expected by end of 2006

Controlling and AccountingWill be fully harmonized by end of Q3 2006 and will remain under well-established VA TECH HYDRO management

Integration: Markets

Review on CMD 2006 regarding integration measuresof VA TECH HYDRO

The entire product range of VA TECH HYDRO and Andritz HM will be integrated into the Hydro Power Business Area

All activities for “small turbines” so far handled by Andritz Graz will be integrated into the Compact Hydro Division of VA TECH HYDRO(CoC Grenoble and Ravensburg)

Graz will remain the Center of Competence for all types of pumps (except pump turbines)

Integration: Products

Integration: Cross Functions

Existing overlaps:

Service business for Austria and Germany

Large Hydro core component business in ChinaStatus of integration:

Service business for Austria directed from Graz location (former HM Business Area)

German market is served by Ravensburg (VA TECH HYDRO)

Chinese market will be served by both VA TECH HYDRO Beijing as well as ATC (Andritz Technologies China) in Foshan. Key account approach will be followed.

in progress

Slide No. 17

VATH16%

Alstom22%

Voith16%

GE5%

Others41%

World market shares for hydropower equipment

Hydro Power: Strong development of VA TECH HYDRO

Order Intake of VA TECH HYDRO developedsubstantially above expectations

Given the high Order Backog of over 1.7 bn. EUR of VA TECH HYDRO, Sales of the Hydro Power Business Area could approach 1 bn. EUR in 2008 already Simon Bolivar hydropower station

0

100

200

300

400

500

600

H1 2005 H2 2005 H1 2006 H2 2006 H1 2007

Order Intake VA TECH HYDRO

260.8310.6

389.2

474.4512.6

Source: Estimate VA TECH HYDRO

MEUR

Acquisition by Andritz

Slide No. 18

Planned measures and targets for 2008

Further enhancement of supply chain and business processmanagement

Combine organizations in China; VA TECH HYDRO to benefit fromstrong local presence of the Andritz Group in China

Further exploitation of cross-functional synergies with the Andritz Group

Expansion of sourcing, engineering, and production capacities forturbines and generators in China, India, and Brazil

Further increase competitiveness of Hydro Generator Business byfocussing on technical and standardization issues as well as on optimization of the supply chain

Slide No. 19

Further continuation of Group growth in 2007 and 2008

Successful integration and development of VA TECH HYDRO

Complementary acquisitions further extend product range and strengthen market position

Successful start-ups and major orders in pulp and stainless steel confirm excellent market position

Important achievements during the last 12 months

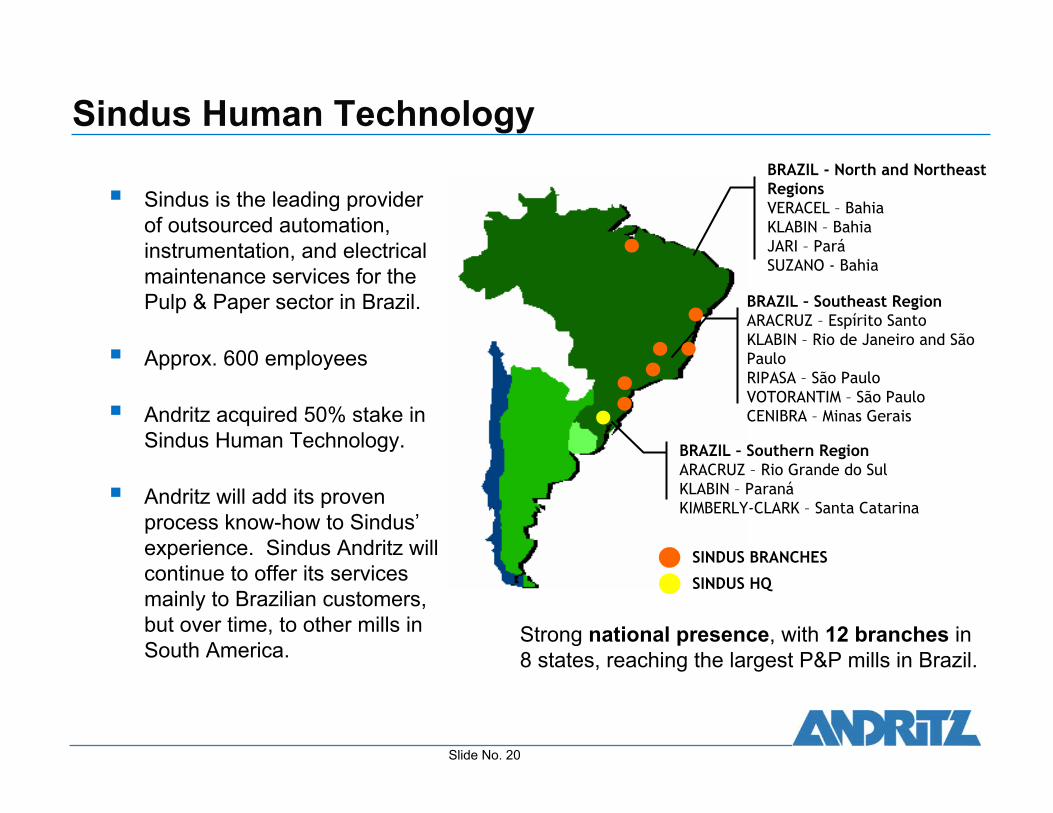

Slide No. 20

Sindus Human TechnologyBRAZIL - North and Northeast RegionsVERACEL – BahiaKLABIN – BahiaJARI – ParáSUZANO - Bahia

BRAZIL – Southeast RegionARACRUZ – Espírito SantoKLABIN – Rio de Janeiro and São PauloRIPASA – São PauloVOTORANTIM – São PauloCENIBRA – Minas Gerais

BRAZIL – Southern RegionARACRUZ – Rio Grande do SulKLABIN – ParanáKIMBERLY-CLARK – Santa Catarina

SINDUS BRANCHES

SINDUS HQ

Sindus is the leading provider of outsourced automation, instrumentation, and electrical maintenance services for the Pulp & Paper sector in Brazil.

Approx. 600 employees

Andritz acquired 50% stake in Sindus Human Technology.

Andritz will add its proven process know-how to Sindus’experience. Sindus Andritz will continue to offer its services mainly to Brazilian customers, but over time, to other mills in South America.

Strong national presence, with 12 branches in 8 states, reaching the largest P&P mills in Brazil.

Slide No. 21

Bachofen + Meier (Andritz BMB)

PrimeCoat™ Super Roll Off Machine Coating Station

Board Coating Line

Supplier of coating equipment, size and film presses, air turns, and related equipment since the 1960’s.

Complements existing product range for paper and board production.

Slide No. 22

Cooperation with UPM for biomass gasification

Utilizing technology of Andritz Carbona, a specialist in advanced biomass gasification processesJoint development of technology and processesTesting to be conducted at the Gas Technology Institute’s (GTI) pilot lab near ChicagoTests expected to be finalized in 2008Targeting biomass gasification plants for:

Fuel gas production for pulp mill energy needsSynthetic gas production for Biomass-to-Liquid (BTL) motor fuels

Joint development project of Andritz Carbona and UPM for biomass gasification and synthetic gas production

Slide No. 23

Supplier of renewable energy products

Approximately 35-40% of Andritz‘sSales are derived from

renewable energy products

Pulp and Paper

Hydro Power

Rolling Mills and Strip

ProcessingLines

Environmentand Process

Feed and Biofuel

Andritz Group Order Intake H1 2007: 2,037 MEUR

Pulp and PaperRecovery boilers in pulp mills

generate net surplus of electricity from biomass;

Wood gasification

Hydro PowerWater turbines and

generators

Feed and BiofuelSystems for production

of biofuel pelletsComponents for bio-ethanol

Environmentand Process

Conversion of liquid sewagesludge into dry granulate, which can beused as a substitute for fossil fuels in

heat and power generation;Centrifuges for bio-ethanol

40% Renewableenergyproducts

Slide No. 24

Further continuation of Group growth in 2007 and 2008

Successful integration and development of VA TECH HYDRO

Complementary acquisitions further extend product range and strengthen market position

Successful start-ups and major orders in pulp and stainless steel confirm excellent market position

Important achievements during the last 12 months

Slide No. 25

Single-line successes

World record of 3,796 t/d

Record start-u

p –within 6 months

already exceeding nominal

capacity

Slide No. 26

Andritz: Preferred technology for eucalyptus

Aug 20053,740 t/dDigester Retrofit, EvapsJacarei,Brazil

VCP

Dec 20062,405 t/dFiberline, Pulp Drying, Recovery Boiler, White Liquor Plant

Santa Fe,Chile

CMPC

Sept 2007

3,000 t/dComplete MillFray Bentos,Uruguay

Botnia

Oct 20073,160 t/dWoodyard, Washing, and Bleaching

Mucuri,Brazil

Bahia Sul

April 2009

3,924 t/dFiberline, Pulp Drying, White Liquor Plant

Três Lagoas,Brazil

VCP

Sept 2004

700 t/dComplete FiberlineLençois Paulista,Brazil

Lwarcel

May 20052,830 t/dFiberline, Pulp Drying, White Liquor Plant

Eunapolis, Brazil

Veracel

Start-upSizeAndritz ScopeLocationCustomer

Slide No. 27

Rolling Mills and Strip Processing Lines:Successful start-ups of stainless steel plants

Annealing and pickling linesupplied by Andritz to LianzhongLianzhong Stainless Steel Corp:

Complete stainless steel annealing and pickling line; with 550 meters length, this line has an annual production capacity of 800,000 metric tons and is capable of handling strip with thicknesses of up to 10 mm.

ThyssenKrupp: Stainless steel annealing and pickling line for hot-rolled and cold-rolled strip. The line went into operation only six months after a severe fire damage and reached its full performance of 400,000 tons/year two months later.

Slide No. 28

Agenda

Update on recent developments

- Review on targets of past Andritz Investor Days

- Important achievements and developments during the last 12 months

Growth and the supply chain

Outlook 2008 by Business Area

Summary

Slide No. 29

Andritz purchasing

600750

9501100

1250

1750

1200

400400350

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Purchasing volume of local Andritz Group subsidiaries in MEUR: Europe as most important

region (~75% of total purchasing volume), followed by North America, China, and India

Main components purchased:Special components Raw materials (sheet metal, castings, forgings, etc.)Electrical drive engineering, including control systems, process control and instrumentationVessels, steel structures, pipeworks

Slide No. 30

Andritz purchasing strategy and trends

Increase volume of purchased components in East Asia (particularly China), in South America, and in India

Tendency towards more complex purchased components/systems

Increase inter- and intra-continental cooperation by Andritz subsidiaries in South America, North America, and China

Slide No. 31

Buy-ratio continues to increaseSales of the Andritz Group

1997-2006; in MEUR

0

500

1000

1500

2000

2500

3000

1997 2006

2,710

646

+320

%

Outsourcing > 50%

0

1

2

3

4

5

6

+227

%

1997 2006

1.5

4.9

Direct labour hours of the Andritz Group 1997-2006; in million

Slide No. 32

Pittsburg (TX)/USA

Pomerode/BR

Senden/D

Chennai/IND

Graz/A

Sibiu/RO

Spisska/SKCologne/D

Foshan ATC/RC

Kuala Lumpur/MAL

Singapore/SGP

Geldrop/NL

Châteauroux/F

Bretten/D

Regensburg/D

Savonlinna/FIN

Brantford/CAN

Muncy/USA

Foshan J.V. /RC

Växjö/SVallentuna/S

Esbjerg/DK

Humenne/SK

Hemer/D

Varkaus/FIN

Morelia/MEX

Madrid/E

Kriens/CH

Ravensburg/D

Jevnaker/N

Weiz/A

Krefeld/D

Bhopal/INDFaridabad/IND

São Paulo/BR

Päiverinne/FIN

Foshan AnWo/RC

Bülach/CH

Manufacturing sites worldwide

Direct labour hours :

> 500 kh100-500 kh< 100 kh

Slide No. 33

Sales/Direct labour hours 2006 by Business Area

Breakdown of Sales 2006 by Business Area

* Share of Sales based on pro-forma 2006 figuresincluding VA TECH HYDRO

45%*

4%*

15%*

24%*

12%*

Breakdown of direct labour hours 2006 by Business Area

6%

6%

37%

20%

31%

Pulp and Paper

Hydro Power

Rolling Mills and Strip Processing Lines

Environment andProcess

Feed and Biofuel

Slide No. 34

Andritz manufacturing strategy

Manufacturing strategy:

Focus manufacturing on key components (A parts)

Maintain outsourcing (C parts permanently, B parts partly)

Increase production capacities in emerging markets to serve both local and global markets

Further enhance lead times

Focus on productivity and quality

Consistent use of temporary staff

Slide No. 35

Development of employees by region

Europe65.6%

N-America12.4%

Asia 1.7%

S-America7.0%

RoW1.3%

China7.2%India

4.7%H1 2007:~ 22% of employees

in Emerging Markets

H1 20072000

2000: ~ 3% of employeesin EmergingMarkets

Employees Europe:

Europe70.1%

N-Am erica26.9%

As ia 0.8%

S-Am erica0.4%

RoW0.3%

China1.1%

India0.3%

Employees North America: Employees Brazil, India, China:

0

500

1000

1500

2000

2000 H1 20070

2000

4000

6000

8000

2000 H1 2007

2,950

7,200

+140%

1,950

50

+3,1

00

>50%in

manu-facturing

0

500

1000

1500

2000

2000 H1 2007

1,1501,350

+20%

~40%in

Manu-facturing

~40%in

Manu-facturing

Slide No. 36

Agenda

Update on recent developments

- Review on targets of past Andritz Investor Days

- Important achievements and developments during the last 12 months

Growth and the supply chain

Outlook 2008 by Business Area

Summary

Slide No. 37

Many pulp mill projects …

Major new pulp mill/expansionprojects planned or announceduntil 2012:

Gunns, Australia Ence, Uruguay Visy Paper, Australia

Aracruz, BrazilVCP, BrazilStora Enso, Brazil/UruguayCenibra, BrazilVeracel, BrazilStora Enso, RussiaMondi, RussiaInternational Paper, RussiaRuukki, Russia

High project activity for new pulp mills/expansion of existing lines to continue during the next few years In total, approximately 15 million tons of new pulp mill capacity are expected to be decided until 2012

Record start-up within 171 daysof CMPC‘s fiberline supplied by Andritz

Slide No. 38

… based on fast growing plantations and …

Approx. 150,000 - 200,000 hectars ofplantations needed for a

pulp mill with 1 million tons capacity

Source: J. Pöyry

Slide No. 39

… natural wood resourcesRussia holds the largest resource of unutilized softwood and hardwood

Source: J. Pöyry

Slide No. 40

Hydro Power: High project activity worldwide

Andritz VA TECH HYDRO is a global leading supplier of turnkey electromechanical equipment and services for hydropower plants with a leading position in the growing market of plant refurbishment

Integration of VA TECH HYDRO(acquired in June 2006) has been progressing as planned

Goal to increase profitability to Group level over the next few years

Continued high project activity worldwide, with focus on Asia and South America (especially for new plants) as well as North America and Europe (especially modernizations/replacements)

Simon Bolivar rehabilitation project, Venezuela

Lang Ya Shan hydropower station, China

Rehabilitation of Dolna Arda Cascade, Bulgaria

Slide No. 41

Big replacement cycle underway

Source: VA TECH International GmbH; Reinhard Laurich; Hydropower Generation – Industry Analysis

Share of installed turbines older than 30 years

The predominant markets for rehabilitation and upgrades areEurope and North America.

Inst

alle

dC

apac

ity

Asia

192,000 MW

North America

159,000 MW

25%

65%

Western Europe

154,000 MW70%

Central/South America125,000 MW

15%

Eastern Europe 87,000 MW 55%

30%Middle East 30,000 MWAfrica 13,000 MW 35%

World Average50%

Slide No. 42

Overall continued good projectactivity with focus on:

China:- Long-term modernization of domestic

steel industry targeted- Continued expansion of stainless steel

capacities due to fast growing demand: market share of Andritz over 60%

- Temporary production and price cuts in August/September 2007

- Anti-dumping process initiated in the European Union

North America: Slightly increasing project activity (project of ThyssenKrupp for steel mill in the US; recent order from NAS)

India: Increased project activity in carbon and stainless steel

Europe: Modernizations and capacity enlargements

Good project activity for Rolling Mills and Strip Processing Lines

Annealing and pickling line for SKS, China

Slide No. 43

Environment and Process – excellent growth prospects

Andritz offers complete systems for solid/liquid separation (centrifuges, thermal driers) for various types of sludges from municipalities and industries

Directives and stringent environmental regulations as long-term major growth drivers, especially in Europe and the U.S.

Increased demand from mining and steel industries due to global shortage of raw materials (iron ore, coal, etc.)

Increasing Sales from Emerging Markets (from 10% in 2000 to 30% in 2007); for mining equipment, Emerging Markets account for over 65% of Sales

Drum drying plant Bran Sands, UK

Slide No. 44

Feed & Biofuel – continued strong organic growth

Andritz wood pelleting plant

Wood pellets

Andritz is a world market leader forplants to produce animal feed and biofuel pellets out of materials, such as wood, peat, and agriculturalby-products.

Continued strong organic growthof Order Intake (+25.6% in 2006; +17.1% in H1 2007); maincontributor is wood pelletingequipment, currently approx. 25% of the Business Area‘s Sales

Since 2002, more than 200 woodand biomass pelleting linessupplied to customers, mainly in North America, and Northern and Eastern Europe

Slide No. 45

Agenda

Update on recent developments

- Review on targets of past Andritz Investor Days

- Important achievements and developments during the last 12 months

Growth and the supply chain

Outlook 2008 by Business Area

Summary

Slide No. 46

Summary and goals

Assuming an overall solid development of the global economy, Andritz expects good project activity in all Business Areas to continue

Continuation of strategy to acquire complementary businesses/companies in all Business Areas

Focus on improving the Group EBITA towards 7%

Based on the high Order Backlog and the overall good development of Order Intake, Group Sales in 2008 are expected to grow organically to approximately 3.5 billion Euros (~+9% vs. 2007)

Increase of dividend payout ratio to 40% for financial year 2007

Increase of share buy-backs if no large acquisition opportunities materialize

A Global Market Leaderin High-Tech Production Systems

for Pulp & Paper, Steel and other Specialized Industries