andrew rashbass and colin jones 22 november 2017 · andrew rashbass and colin jones 22 november...

TRANSCRIPT

Andrew Rashbass and Colin Jones

22 November 2017

FY17 results presentation

Page 2

2016 – no outward change

2017 – year of transition

2018 – year of growth

Message from our Investor Day in March 2016 Message from today

We’re on track

Strategic journey

Page 3

Strategy recap

Page 4

Euromoney’s capital allocation decisions can be understood along two dimensions

Structure

We characterise the business models of B2B information companies into three generations, which we call B2B Information 1.0, 2.0 and 3.0.

We service fundamentally cyclical markets. Understanding which point in the cycle they are in is fundamental to our capital allocation decisions.

Cycle

Plotting the businesses along the axes supports our investment decisions, capital allocation and defines strategic priorities.

Quadrants

Page 5

Successful B2B information companies will be 3.0 businessesStructure

- +

B2B Information 1.0

Monologue

Advertising-centric

Product-centric

B2B Information 2.0 B2B Information 3.0

Digital

Dialogue

Subscriptions

Customer-centric

Embedded in workflow

Part of the industry structure

Licensing revenues based on customer outcomes

Solution-centric

We aim to anticipate our markets’ development to become 3.0

Page 6

Market cycles impact the sectors that we serveCycle

Equities Commodities Banking and financial institutions

Commodity indexEquity index Bank shares index

0

50

100

150

200

250

300

350

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

60

80

100

120

140

160

180

200

220

240

1990 1994 1998 2002 2006 2010 2014 2018 1991 1995 1999 2003 2007 2011 2015 2018 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Source: S&P 500 index Source: Bloomberg Commodity index Source: S&P Bank index

Page 7

Based on the cycle and structure we categorise the businesses in the portfolio Quadrants

The quadrants guide investment decisions, capital allocation and also define strategic priorities

B2B Information 3.0

-

3 Prepare for the upturn• Protect and enhance competitive position• Selective investments for when cycle turns• Opportunistic revenue initiatives• Tight cost control• Fix any operational deficit

B2B Information 1.0

Challenged market Strong tailwinds

-

1

4

2

Cycle Stru

ctu

re

Invest

Use the time wiselyDisinvest• Modest investment to move to top-right quadrant• Maximise short-term profit and cash• Fix any operational deficit• Consider divestment

• Maximise short-term profit and cash• Divest• Prevent future build-up

• New product development• Sales and marketing• Acquisition• Fix any operational deficit• Accelerate transition to 3.0

+

+

Page 8

The actions dictated in the quadrant can be collected into our three key pillars of strategic activity

Prepare for the upturn

Invest3 4

1 2Disinvest

Use the time wisely

Prepare for the upturn

Invest3 4

1 2Disinvest

Use the time wisely

Prepare for the upturn

Invest3 4

1 2Disinvest

Use the time wisely

Invest around big themes

Actions depend on market characteristics

Disruption

Semi-opaque market

Inefficiency

Barriers to entry

Challenged business models

Transform the operating model Actively manage the portfolio

Product development and creating our future operating model

3.0 Business model

Must have, not nice to have

Create once, sell many

Best of both worlds

Recycling capital

Acquisition

Disposal

Page 9

Our portfolio of businesses are split into four segments composed of seven divisions with support from central functions

Price ReportingSpecialist

Information

Euromoney Institutional Investor PLC

Banking & FinanceGlobal Market

Intelligence

Asset Management Banking & Finance

Investment Research

Institutional Investor

Pricing, Data & Market IntelligenceCommodity

Events

Events

Central functions

Corporate Development

Finance

HR

IT

Marketing

Legal, Risk and Programmes

Fin

ance

Legal

Project and Asset Financing

Insurance

Derivatives

Commodity

TelC

ap

Segment Division

Page 10

Boeing Fleet Database (January 2016)

Reinsurance Security (August 2016)

FastMarkets (September 2016)

Broadgroup (March 2017)

RISI (April 2017)

Layer123 (April 2017)

Acquisitions Disposals Gulf & PE (April 2016)

HedgeFund Intelligence (December 2016)

II Intelligence (December 2016)

Euromoney Indices (March 2017)

LatinFinance (March 2017)

Adhesion & WBWE (October 2017)

CEIC & EMIS held for sale– Rationale: Recycling of capital towards big

investment themes

– Status: process on track. Any announcement unlikely before January 2018

– Impact on FY17 numbers (slide 55)

Active portfolio management

Page 11

Appointment of three independent Non-executive Directors in November:– Imogen Joss

– Jan Babiak (from Dec 1)

– Lorna Tilbian (from Jan 1)

Other Board changes:– Chairman/SID

– DMGT representatives

Governance

From March 2016 Investor Day

FY14/FY15growth

(underlying)

Disinvest Batten downthe hatches

Use thetime wisely

Invest,Organic

Achievableorganicgrowth

Invest,Acquisitions

Achievablegrowth

New

2015Existing

Margin: Lower margin Margin-enhancing Higher margin

Quality: Lower quality Improving quality High quality

1

1. Underlying revenue growth from FY14 to FY15, excluding the impact of acquisitions, disposals, currency movements and significant event timing differences.

2. Note: Chart for illustrative purposes only. Not drawn to scale

Strategy: achievable revenue growth (not guidance)

Page 13

Full-year results

Page 14

FY16 FY17 Change

Total revenue1 (£m) 403.1 428.4 6%

Adjusted PBT1 (£m) 102.5 106.5 4%

Statutory PBT (£m) 33.4 40.7 22%

Adjusted EPS1 (p) 66.5p 76.4p 15%

Dividend per share (p) 23.4p 30.6p 31%

Net cash/(debt) (£m) 83.8 (154.6)

1. Includes the results of continuing and discontinued operations and reconciled in the appendix to the Preliminary Statement.

Full-year snapshot

Page 15

Statutory profit (£m)

40.7

106.5 (20.8)

(33.7)

(9.2)

(5.2) 3.1

Adjusted PBT Acquired intangible amortisation

Exceptional items (slide 42)

Discontinuedoperations PBT

Associates/JVs

Acquisition commitmentmovements

Statutory PBT

Page 161. Includes the results of continuing and discontinued operations and reconciled in the appendix to the Preliminary Statement.

Adjusted1 results

£m FY16 FY17 Change

Total revenue 403.1 428.4 6%

Adjusted operating profit 101.4 107.1 6%

Adjusted operating margin 25.2% 25.0% (0.2%)

Adjusted PBT 102.5 106.5 4%

Page 17

FY16 to FY17 total revenue1 bridge (£m)

433.4428.4

403.1

34.5 (3.0) (1.2) (5.0)

FY16 FX Timing Net M&A FY16 underlying revenue(restated on FY17 basis

for continuing businesses)

Business revenue FY17

£41.5m Global Markets Intelligence Division

£37.1m Global Markets Intelligence Division

1. Includes the results of continuing and discontinued operations.

Page 18

FY16 to FY17 total revenue1 bridge (by segment) (£m)

428.4

433.4 (3.0)

5.1 (4.7)

(2.4)

FY16 underlying revenue(restated on FY17 basis

for continuing businesses)

AssetManagement

Pricing, Data & Market Intelligence

Banking &Finance

Commodity Events

FY17

HeadwindsStrategy & tailwinds

Self help

1. Includes the results of continuing and discontinued operations.

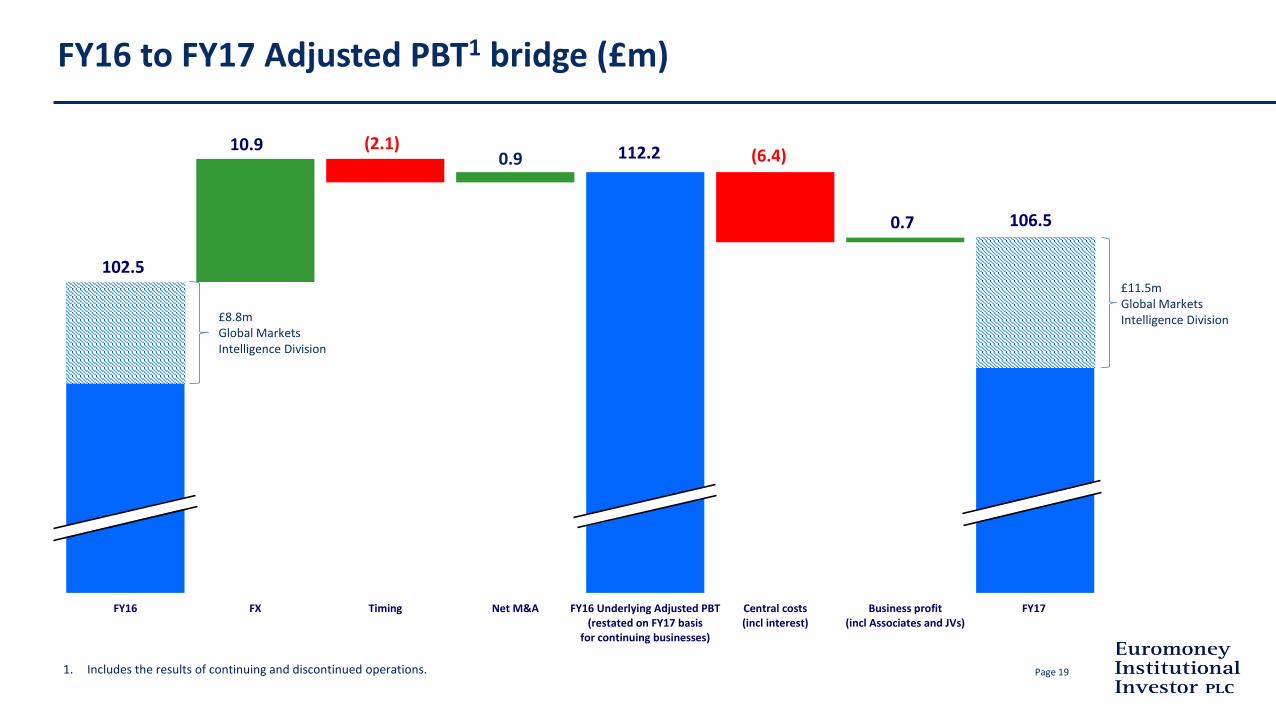

Page 19

FY16 to FY17 Adjusted PBT1 bridge (£m)

112.2

106.5

102.5

10.9 (2.1)0.9 (6.4)

FY16 FX Timing Net M&A FY16 Underlying Adjusted PBT(restated on FY17 basis

for continuing businesses)

Central costs(incl interest)

Business profit(incl Associates and JVs)

FY17

0.7

£8.8m Global Markets Intelligence Division

£11.5m Global Markets Intelligence Division

1. Includes the results of continuing and discontinued operations.

Page 20

FY16 to FY17 underlying1 segmental performance (£m)

Revenue

Profit

Pricing, Data & Market Intelligence

Banking & Finance Commodity Events

Battening down the hatches

Top-rightinvestment

Shifting quadrants

Self-help, plus H1 headwinds

Total

(5.0)

0.7

Asset Management

1. At constant exchange rates, including pro forma prior year comparatives for acquisitions and excluding disposals and significant event timing differences.

Associates/JVs

Page 211. At constant exchange rates, including pro forma prior year comparatives for acquisitions and excluding disposals and significant event timing differences.2. Includes other revenues but excludes revenues from sold/closed businesses. FX hedging losses restated in prior year at current year level.3. Q4 adjusted for ‘self-help’ actions and decision not to repeat events in certain markets due to increased geopolitical instability.

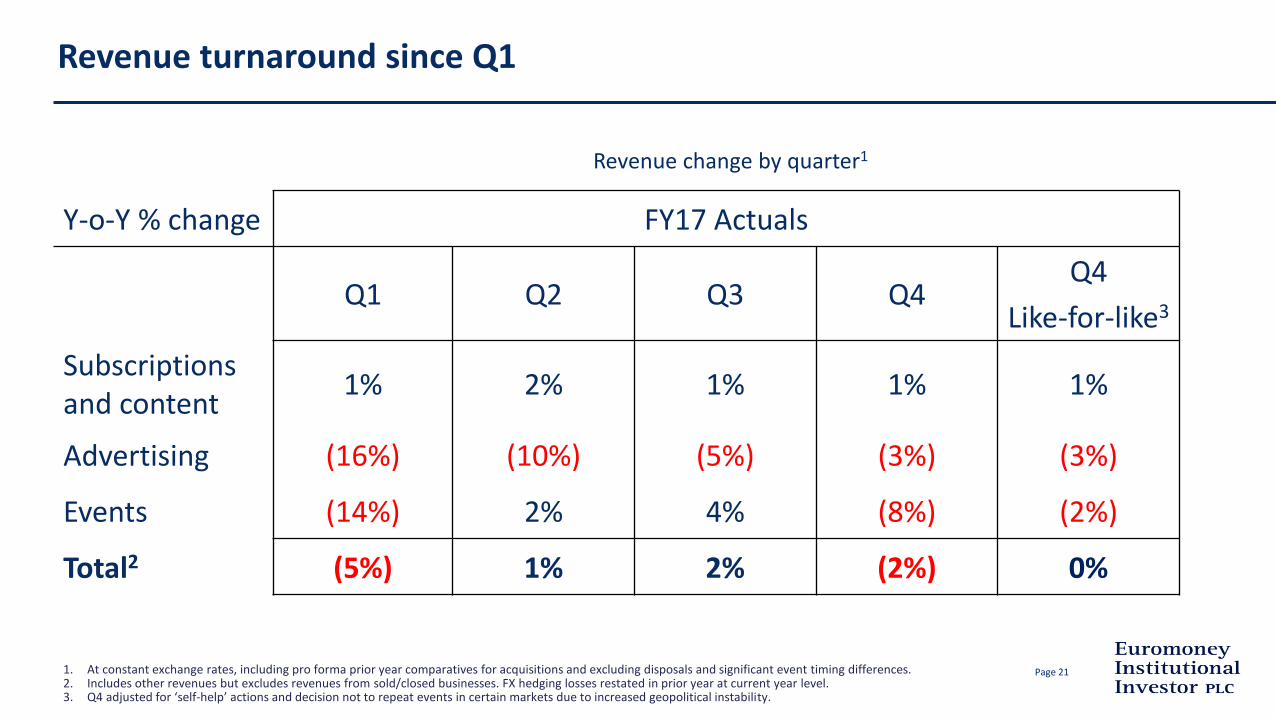

Revenue turnaround since Q1

Y-o-Y % change FY17 Actuals

Q1 Q2 Q3 Q4Q4

Like-for-like3

Subscriptions and content

1% 2% 1% 1% 1%

Advertising (16%) (10%) (5%) (3%) (3%)

Events (14%) 2% 4% (8%) (2%)

Total2 (5%) 1% 2% (2%) 0%

Revenue change by quarter1

Page 22

Adjusted operating margin: year-on-year movement

FY16 adjusted operating margin 25.2%

FX 0.5%

Timing (0.3%)

Net M&A 0.3%

Standalone company (0.8%)

Underlying business:

- Asset Management 0.7%

- Pricing, Data & Market Intelligence (1.0%)

- Banking & Finance 0.5%

- Commodity Events (0.1%)

0.1%

FY17 adjusted operating margin 25.0%

Page 23

FY17 revenue and profit matrix by segment/type1 (£m)

Divergence in subscriptions performance between Asset Management and Pricing, Data & Market Intelligence

Decline in overall sponsorship and delegate revenues reflects ‘self-help’ strategic actions taken in FY16 to remove low-margin activities

Repeat events achieved underlying growth of 4%, reflecting strategic focus on large ‘must-attend’ annual events

1. See slide 48 and 49 for notes, colour key and reconciliation to Adjusted PBT

Asset management 138.2 (2%) 14.2 (9%) 16.1 4% 3.2 4% 0.1 108% 171.8 (2%) 64.3 3%

Pricing, data & market intelligence 113.9 5% 16.7 (13%) 14.4 8% 19.0 4% 1.5 (9%) 165.5 3% 51.3 (6%)

Banking & finance 8.9 (5%) 9.8 8% 28.1 (7%) 21.7 (10%) 1.4 (11%) 69.8 (6%) 13.8 7%

Commodity events 6.0 (4%) 20.8 (7%) 0.6 (2%) 27.4 (8%) 6.9 (10%)

Total segment revenue/profit 261.0 1% 40.7 (8%) 64.6 (1%) 64.7 (5%) 3.5 (8%) 434.5 (1%) 136.3 (1%)

Total

Profit (£m)Revenue (£m)

Delegates Other Total

N/A N/A

Subscriptions/

Content Advertising Sponsorship

Page 24

£10.9m year-on-year FX benefit to adjusted PBT:

– GBP/USD rate fell 14 cents

– £9.4m FX benefit on translation of overseas profits

– UK embedded FX benefit £9.4m partly offset by movement in hedging losses of £5.6m

– £0.4m FX loss on balance sheet revaluation (FY16: £1.9m gain)

FX hedging losses do not repeat in FY18 at current exchange rates

Impact of favourable FX

GBP/USD rate

Page 251. As reconciled in appendix to Preliminary Statement.

FY17 cash flow (£m)

83.8 (193.5)

126.0 (30.8)

(12.9)(102.2)

(21.8)

(4.8) 9.4 (7.8)(154.6)

Net cash atSept 30 2016

Share buyback(incl fees)

Underlying cashgenerated from

operations

Dividends Capex Net M&A Net tax Interest Other(incl FX)

Non tradingitems

Net debt atSept 30 2017

Underlying 12-month cash conversion 118%

Page 26

Outlook & summary

Page 27Source: Financial Times ‘Countdown to MiFID II’ (November 2017)

Asset Management and MiFID II impact

MiFID II: How asset managers will pay for research?

Absorb costs, 85%

Pass costs on to clients, 5%

Undecided, 7%

Page 28Source: BCG 2017

Asset Management: Asset class, AUM and fees

9/ $3 11/ $417/ $11 18/ $12 20/ $19

3/ $3 3/ $6 6/ $14 6/ $14 7/ $20

57/ $1747/ $18 36/ $23 35/ $24 29/ $26

39/ $43

28/ $48 23/ $58 23/ $58 19/ $57

6/ $2

9/ $313/ $9 13/ $9

15/ $14

4/ $4

5/ $8 8/ $21 8/ $2110/ $31

20/ $6

19/ $7 20/ $13 19/ $13 20/ $18

26/ $28

24/ $41 22/ $55 21/ $54 21/ $63

9/ $314/ $6 14/ $9 15/ $10 16/ $14

28/ $31

39/ $66 40/ $100 42/ $104 43/ $130

2003 2008 2015 2016 2021 2003 2008 2015 2016 2021

Total ($trillions) Total ($billions)

Passive Active core

Solutions/LDI/balanced Active Specialties

Alternatives

GLOBAL AuM SPLIT BY PRODUCT (% / $TRILLIONS) GLOBAL REVENUES SPLIT BY PRODUCT (% / $BILLIONS)

31 38 65 69 92 110 168 248 250 300

16

4

13

1

9

8

8

14

4 4

1414

9

9

9

6 6

7

2

7

17

8

14

3

3

14

2

12 13

4

4

6

-3

1

0

0

0

8

8

5

CAGR (%)

Page 29Source: LME Price Index

Metals prices turned in late 2015

Jan 07 Jan 08 Jan 09 Jan 10 Jan 11 Jan 12 Jan 13 Jan 14 Jan 15 Jan 16 Jan 17

Page 30Source: Coalition IB Index – 1H17 - September 2017

Banking & Finance: Global investment bank revenues have stabilised

57.749.5 45.3 42.7

38.2 38.5

19.8

24.723.8 28.5

23.4 22.6

16.5 19.822.6 21.9

17.6 21.0

1H12 1H13 1H14 1H15 1H16 1H17

(USD

Bill

ion

)

Figure 1. Revenues by Business

FICC Equities IBD

94.0 94.191.6

0% (3%) 2% (15%)

19%

(3%)

1%

YoY Change1H17 vs. 1H1693.1

79.282.0

4%

Page 31

Book of business – reported (c60% of total revenue)

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

Total book of business at reported GBP/US$ rate

2015 2016 2017 2018

X

18.1% 19.2%

Page 32

Book of business – underlying

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

Total book of business at constant GBP/US$ rate adjusted for net M&A

2015 2016 2017 2018

X0.8%

0.4%

Page 33

Effect of Acquisitions on BOB

19.2%

9.4%

4.2%4.7%

15.8%

11.2%

Page 34

Book of business – Asset Management vs Pricing, Data & Market Intelligence

(8.0%)

(6.0%)

(4.0%)

(2.0%)

-

2.0%

4.0%

6.0%

8.0%

10.0%

Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct

Book of business growth at constant GBP/US$ rate adjusted for net M&A (%)

Group Pricing, Data & Market Intelligence Asset Management

0.8%

8.5%

(5.9%)

Page 35

Advertising – underlying (c10% of total revenue)

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

Advertising 52 week rolling sales at constant GBP/US$ rate

2015 2016 2017 2018

(6.1%)(5.3%)

Page 36

Events – underlying (c30% of total revenue)

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

Events 52 week rolling sales at constant GBP/US$ rate

2015 2016 2017 2018

5.9%

6.4%

Page 37

Strategy on track. FY18 “year of growth”

Capital being rigorously allocated and quadrants managed. Continuing strong cash flow

DMGT sell down accelerates strategy. But there are standalone company costs

Invested FX benefit to accelerate strategy. FX no longer favourable

Asset management markets more challenged with MiFID II headwinds

Banking & finance and commodities markets improving

Summary: we’re where we expected to be – perhaps a bit ahead.

Outlook & summary

Page 38

Q&A

Andrew Rashbass and Colin Jones

22 November 2017

FY17 results presentation

Appendix:Supplementary information

Page 41

Adjusted Statutory

Revenue (£m) 428.4 386.9

Operating profit (£m) 107.1 43.4

Operating margin (%) 25.0% 11.2%

Profit before tax (£m) 106.5 40.7

EPS (p) 76.4p 37.9p

FY17 adjusted and statutory results

Page 421. See note 3 of the Preliminary Statement for fuller description.

Exceptional items1

£m FY17

Impairment (29.7)

Profit on disposal of businesses 2.9

Tax settlement 3.9

Restructuring and other (8.4)

Continuing operations (31.3)

Discontinued operations (2.4)

Total (33.7)

Page 431. See note 4 of the Preliminary Statement.

Net finance costs1

£m FY16 FY17

Interest on DMGT debt facility (1.3) (0.2)

Interest on cash deposit with DMGT 0.4 0.1

Interest on external borrowings - (3.7)

Interest on tax (0.4) (0.1)

Other 0.2 (0.1)

Adjusted net finance costs (1.1) (4.0)

Acquisition deferred consideration - 0.2

Acquisition commitments (0.6) 3.0

Total net finance costs (1.7) (0.8)

Page 441. See note 5 of the Preliminary Statement.

Tax1

£m FY16 FY17

Adjusted PBT 102.5 106.5

Total tax charge (12.9) (6.7)

Other tax adjustments (5.2) (13.1)

Adjusted tax charge (18.1) (19.8)

Adjusted effective tax rate 18% 19%

Page 45

Cash conversion

£m FY16 FY17

Adjusted operating profit 101.4 107.1

Cash generated from operations 103.8 118.2

Exceptional items 3.7 12.4

Timing differences (1.4) (4.6)

Underlying cash generated from operations 106.1 126.0

Cash conversion % 102% 110%

Underlying 12-month cash conversion % 105% 118%

Page 46

Deferred revenue

Sep-16 to Sep-17

£m Subscriptions Events Advertising

Opening balance1 93.5 22.5 2.8

Net M&A 11.2 1.1 (0.1)

FX (2.7) (0.4) -

Adjusted opening balance 102.0 23.2 2.7

Underlying movement 4.5 1.8 -

Closing balance2 106.5 25.0 2.7

Underlying growth % 4% 8% 0%

1. Excludes FY16 deferred revenue classified within total liabilities of businesses held for sale.2. Includes FY17 deferred revenue classified within total liabilities of business held for sale.

Page 47

Banking facilities

£m Purpose

Term-loan 120 Share buyback

Revolving credit facility 130 Acquisitions & working capital

250

Accordion 130 Additional acquisitions

380

Funding costs

Net Debt: EBITDA Margin above LIBOR

< 1.0 1.25%

<1.5 1.50%

<2.0 1.75%

<2.5 2.00%

>2.5 2.50%

Rate hedging

£32m of term-loan swapped to fixed rate of 0.76% p.a

$80m of term-loan swapped to fixed rate of 1.97% p.a

Page 48

FY17 revenue and profit matrix by segment/type (£m)

Notes

The absolute £ figures represent total segment revenue/profit, central

costs and Adjusted PBT.

The percentages represent underlying growth rates, including pro forma

prior year comparatives for acquisitions and excluding disposals and

significant event timing differences at constant exchange rates.

Total segment revenue of £434.5m excludes FX on forward contracts

(-£10.8m) and sold/closed businesses (+£4.7m).

For a reconciliation of segment profit to Adjusted PBT, refer to slide 49.

Key

Dark green – growth more than 2%

Light green – growth of 0% to 2%

Amber – decline of 0% to -1%

Pink – decline of -1% to -5%

Dark red – decline more than -5%

The white cells have not been colour-coded due to their size

Asset management 138.2 (2%) 14.2 (9%) 16.1 4% 3.2 4% 0.1 108% 171.8 (2%) 64.3 3%

Pricing, data & market intelligence 113.9 5% 16.7 (13%) 14.4 8% 19.0 4% 1.5 (9%) 165.5 3% 51.3 (6%)

Banking & finance 8.9 (5%) 9.8 8% 28.1 (7%) 21.7 (10%) 1.4 (11%) 69.8 (6%) 13.8 7%

Commodity events 6.0 (4%) 20.8 (7%) 0.6 (2%) 27.4 (8%) 6.9 (10%)

Total segment revenue/profit 261.0 1% 40.7 (8%) 64.6 (1%) 64.7 (5%) 3.5 (8%) 434.5 (1%) 136.3 (1%)

Central costs (incl FX/interest/associates & JVs) (29.8) -Adjusted PBT 106.5 (5%)

Total

Profit (£m)Revenue (£m)

Delegates Other Total

N/A N/A

Subscriptions/

Content Advertising Sponsorship

Page 49

FY17 segment profit to adjusted PBT reconciliation (£m)

Segment profit1 136.3

Non-segment items:

- Central costs (18.0)

- FX on hedging/balance sheet items (11.2)

- Associates/JVs 3.4

- Interest (4.0)

(29.8)

Adjusted PBT1 106.5

1. Includes the results of continuing and discontinued operations.

Page 501. After sold/closed businesses, FX and other revenues.2. Percentage of total FY17 revenue excluding closed businesses, FX and other revenues.

Total revenue change

Y-o-Y % change FY16 FY17 FY17

H1 H2 H1 H2 Full Year % revenue2

Subscriptions and content

5% 11% 19% 17% 18% 61%

Advertising (3%) (6%) 3% 6% 5% 9%

Sponsorship (3%) 10% 13% 10% 11% 15%

Delegates (5%) (5%) (2%) 4% 1% 15%

Total1 (2%) 2% 5% 8% 6%

Page 511. At constant exchange rates, including pro forma prior year comparatives for acquisitions and excluding disposals and significant event timing differences.2. Includes other revenues but excludes revenues from sold/closed businesses. FX hedging losses restated in prior year at current year level.

Underlying1 revenue change by quarter

Y-o-Y % change FY16 FY17

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Subscriptions and content

2% 0% 1% 2% 1% 2% 1% 1%

Advertising (2%) (16%) (14%) (12%) (16%) (10%) (5%) (3%)

Sponsorship (7%) (8%) 9% (7%) (14%) 5% 5% (6%)

Delegates (18%) (17%) (9%) (12%) (14%) 1% 2% (11%)

Total2 (6%) (6%) (1%) (4%) (5%) 1% 2% (2%)

Page 52

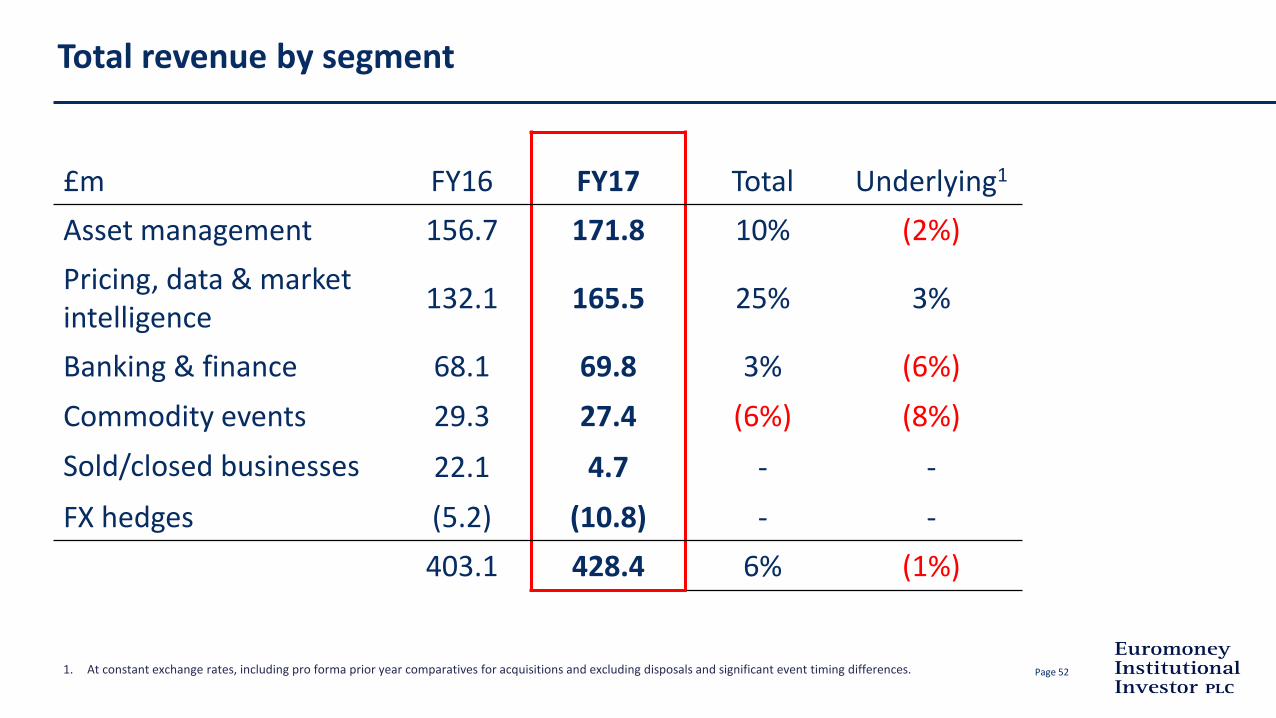

Total revenue by segment

£m FY16 FY17 Total Underlying1

Asset management 156.7 171.8 10% (2%)

Pricing, data & market intelligence

132.1 165.5 25% 3%

Banking & finance 68.1 69.8 3% (6%)

Commodity events 29.3 27.4 (6%) (8%)

Sold/closed businesses 22.1 4.7 - -

FX hedges (5.2) (10.8) - -

403.1 428.4 6% (1%)

1. At constant exchange rates, including pro forma prior year comparatives for acquisitions and excluding disposals and significant event timing differences.

Page 531. At constant exchange rates, including pro forma prior year comparatives for acquisitions and excluding disposals and significant event timing differences.

Total revenue by type

£m FY16 FY17 Total Underlying1

Subscriptions and content 221.2 261.0 18% 1%

Advertising 38.9 40.7 5% (8%)

Sponsorship 58.2 64.6 11% (1%)

Delegates 64.3 64.7 1% (5%)

Other 3.6 3.5 (3%) (8%)

Sold/closed businesses 22.1 4.7 - -

FX hedges (5.2) (10.8) - -

Total 403.1 428.4 6% (1%)

Page 54

Adjusted operating profit by segment

£m FY16 FY17 Adjusted Underlying1

Asset management 55.2 64.3 16% 3%

Pricing, data & market Intelligence

43.8 51.3 17% (6%)

Banking & finance 10.5 13.8 31% 7%

Commodity events 8.0 6.9 (14%) (10%)

Sold/closed businesses 1.7 - - -

Central costs (14.5) (18.0) - -

FX hedges/balance sheet (3.3) (11.2) - -

Total 101.4 107.1 6% (4%)

1. At constant exchange rates, including pro forma prior year comparatives for acquisitions and excluding disposals and significant event timing differences.

Page 55

Discontinued operations1 (£m)

£m FY16 FY17 Change

Revenue 37.1 41.5 12%

Adjusted operating profit 10.1 11.9 18%

Adjusted operating margin 27.2% 28.6% 1.4%

Adjusted PBT 10.4 11.9 15%

Statutory PBT 10.5 9.2 (12%)

1. Discontinued operations represents the Global Markets Intelligence Division (CEIC and EMIS). All figures disclosed above are reconciled in the appendix to the Preliminary Statement.

Page 56

Sale of Adhesion and WBWE in October for €13.6m (£12.0m)

1. Adhesion’s FY16 results include its biennial wine exhibition, Vinisud. Its FY17 results include the first edition of an annualised Vinisud.

Disposal of Adhesion and WBWE

£m FY16 FY17

Revenue

- Adhesion1 7.9 6.5

- WBWE (held as a subsidiary) - 1.4

Operating profit

- Adhesion1 1.8 (0.1)

- WBWE (held as an associate) 0.1 -

- WBWE (held as a subsidiary) - 0.4

Page 57

Impact of FX

GBP/USD FY17 FY16

Average rate 1.27 1.41

Closing rate 1.34 1.30

GBP/USD 1¢ movement

Revenue +/- £1.9m

Operating profit +/- £0.8m

US$, 70%

£, 12%

€, 8%Other, 9%

REVENUE

US$, 81%

£, 11%

€, 3%Other, 5%

OPERATING PROFIT