anaerobic digestion deployment in the uk

TRANSCRIPT

Anaerobic Digestion Deployment

in the United Kingdom

Lucy Hopwood

Lead Consultant – Bioenergy & Anaerobic Digestion

REA Biogas Group Meeting, London

01 December 2014

Copyright © NNFCC 2014.

AD Deployment in the UK

Copyright © NNFCC 2014.

AD Deployment in the UK

Definitions

Plant scale

• Small scale refers to installations with an installed capacity of 250kWe and below.

• Medium scale refers to installations with an installed capacity of above 250kWe to 500kWe.

• Large scale refers to installations with an installed capacity of above 500kWe.

Plant type

• Waste-fed refers to installations where the contribution of municipal (e.g. food waste; green waste), commercial (e.g. food waste) and industrial wastes (e.g. brewery waste; animal processing wastes) towards the total feedstock requirement is greater than 50%.

• Farm-fed refers to installations where the contribution of farm-based feedstocks (e.g.

manure; slurry; energy crops; crop wastes) towards the total feedstock requirement is greater than 50%.

Copyright © NNFCC 2014.

AD Deployment in the UK

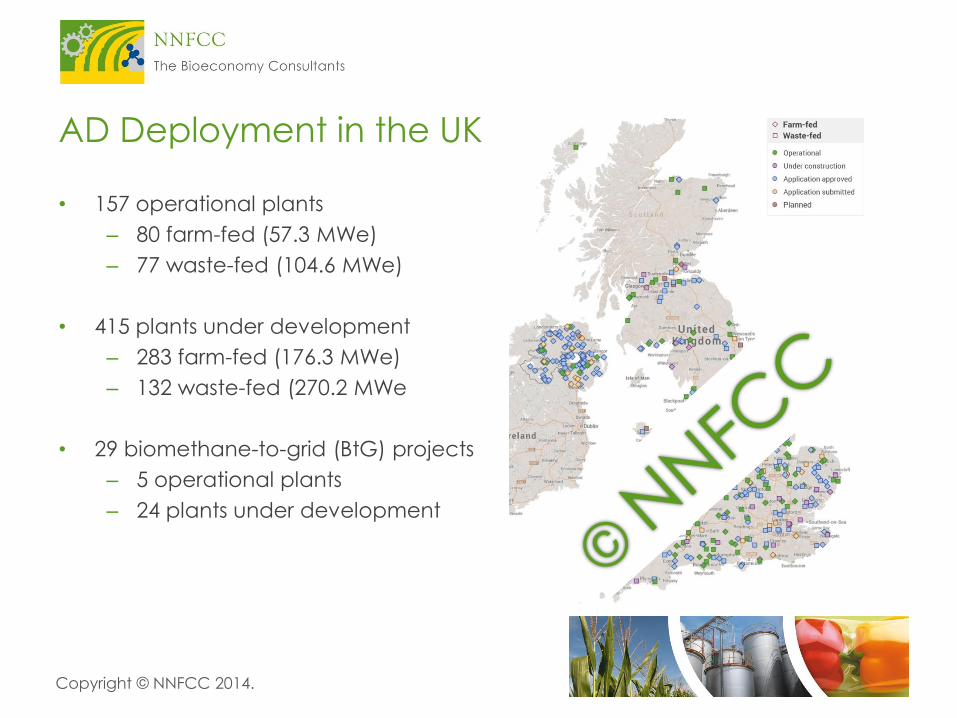

• 157 operational plants

– 80 farm-fed (57.3 MWe)

– 77 waste-fed (104.6 MWe)

• 415 plants under development

– 283 farm-fed (176.3 MWe)

– 132 waste-fed (270.2 MWe

• 29 biomethane-to-grid (BtG) projects

– 5 operational plants

– 24 plants under development

Copyright © NNFCC 2014.

AD Deployment in the UK

• 19 plants online since last report (15

farm-fed; 4 waste-fed)

• 74 more plants undergoing

development (70 farm-fed; 4 waste-

fed)

• Clear movement towards the

development of agricultural plant

Copyright © NNFCC 2014.

AD Deployment in the UK

National Deployment

• Deployment currently

strongest in England

• Attractive support under

NIRO could see NI

deployment increase over

the next few years

0

50

100

150

200

250

300

350

400

450

500

0

50

100

150

200

250

300

350

400

450

500

United

Kingdom

England Northern

Ireland

Scotland Wales

Nu

mb

er o

f pla

nts

Inst

alle

d C

ap

ac

ity (

MW

e)

Operational (MWe) In Development (MWe) Operational In Development

© NNFCC

Copyright © NNFCC 2014.

AD Deployment in the UK

Regional Deployment

• Deployment strongest across

the Midlands and Southern

regions

• Deployment weakest in

North East

• Broadly consistent

distribution in other regions

0

10

20

30

40

50

60

70

80

0

10

20

30

40

50

60

70

80

NW NE YH WM EM EE SW SE LDN IoW

Nu

mb

er o

f pla

nts

Inst

alle

d C

ap

ac

ity (

MW

e)

Operational (MWe) In Development (MWe) Operational In Development

© NNFCC

Copyright © NNFCC 2014.

AD Deployment in the UK

Future Deployment

• If all plants under

development completed

capacity would quadruple

by 2017

• However, only around 30-

50% of plants in pipeline

expected to complete

• Consistent with existing linear

deployment

0

50

100

150

200

250

300

350

400

0

50

100

150

200

250

300

350

400

pre

2005

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Cu

mu

lativ

e N

um

be

r of P

lan

ts

Cu

mu

lative

In

sta

lled

Ca

pa

city (

MW

e)

Farm-fed (MWe) Waste-fed (MWe) Farm-fed Waste-fed

© NNFCC

Copyright © NNFCC 2014.

AD Deployment in the UK

Deployment by scale

• Large scale plants currently

dominate in terms of

number and capacity

• Consistent growth across all

scales, despite FiT degression

for small and medium scale

earlier in the year

• Deployment of small scale

and BtG still at low level

• BtG sector anticipated for

growth, although RHI tariff

undergoing review

0

50

100

150

200

250

300

350

400

0

50

100

150

200

250

300

350

400

Small scale Medium scale Large scale BtG

Nu

mb

er o

f pla

nts

Inst

alle

d c

ap

ac

ity (

MW

e)

Operational (MWe) In Development (MWe) Operational In Development

© NNFCC

Copyright © NNFCC 2014.

AD Deployment in the UK

Current feedstock requirements

• 1,780,000 tpa food waste

• 880,000 tpa energy crops

• 830,000 tpa ‘other’ waste

• 520,000 tpa manure/slurry

• 220,000 tpa crop waste

0

1,000

2,000

3,000

4,000

5,000

6,000

pre

2005

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Fe

ed

sto

ck V

olu

me

s (k

tpa

)

Manure/Slurry Crop Food Waste

Crop waste Other Manure/Slurry (Cum.)

Crop (Cum.) Food Waste (Cum.) Crop waste (Cum.)

Other (Cum.)

© NNFCC

Copyright © NNFCC 2014.

AD Deployment in the UK

Projected (theoretical) feedstock requirements – March 2014

0

1,000

2,000

3,000

4,000

5,000

6,000

pre

2005

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Fe

ed

sto

ck V

olu

me

s (k

tpa

)

Manure/Slurry Crop Food Waste

Crop waste Other Manure/Slurry (Cum.)

Crop (Cum.) Food Waste (Cum.) Crop waste (Cum.)

Other (Cum.)

© NNFCC

Copyright © NNFCC 2014.

AD Deployment in the UK

Projected (theoretical) feedstock requirements – September 2014

0

1,000

2,000

3,000

4,000

5,000

6,000

pre

2005

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Fe

ed

sto

ck V

olu

me

s (k

tpa

)

Manure/Slurry Crop Food Waste

Crop waste Other Manure/Slurry (Cum.)

Crop (Cum.) Food Waste (Cum.) Crop waste (Cum.)

Other (Cum.)

© NNFCC

Copyright © NNFCC 2014.

AD Deployment in the UK

Projected feedstock requirements

• Balance of feedstock in projections changed noticeably over the last 6

months

– Food waste projections increased by under 200,000 tpa

– ‘Other’ waste projections increased by 400,000 tpa

– Manure projections increased by just over 400,000 tpa

– Crop projections increased by almost 1.2 million tpa

Copyright © NNFCC 2014.

AD Deployment in the UK

Food waste

• New report from Eunomia

suggests the UK is near

capacity with regards to

volumes of available food

waste entering AD

• NNFCC data provides

further evidence for this

notion

© Eunomia Research & Consulting; 2014

Copyright © NNFCC 2014.

AD Deployment in the UK

Energy crops

• Large growth in anticipated demand for energy crops in AD

• Largely on account of the initiation of a number of very large scale crop-

only projects in the East Midland and East of England

• Possible reasons:

– Large scale AD developers attracted towards crop feedstock as food

waste approaches capacity

– FiT degression for small and medium scale AD has encouraged farm-

based AD developers to consider larger scales than initially envisaged

– Biomethane-to-grid now becoming very attractive at scale

Copyright © NNFCC 2014.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

pre

2005

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Cro

p a

rea

(H

a)

Crop area Crop area (Cum.)

AD Deployment in the UK

Required cropland

• Assuming an energy crop

yield of 45 fresh tonnes/Ha

the UK AD industry requires

19,500 Ha of land

• If all plants under

development were to

complete the UK AD industry

would require 86,000 Ha of

land (1.5% of UK crop land)

• Break crops often used for AD

© NNFCC

Copyright © NNFCC 2014.

AD Deployment in the UK

Summary and future development

• Development pipeline remains strong despite FiT degression earlier in the year

• However, considerable challenges ahead for both the agriculture and food

waste AD sectors

• Improved utilisation of slurries/manures, especially from poultry sector, could

support increased deployment

• RHI could become a more stable form of support in the future and result in

further BtG deployment

Celebrating 10 years of Bioeconomy

development

NNFCC is a UK based consultancy with

expertise on the conversion of biomass

to bioenergy, biofuels and biobased

products.

We help industry solve complex

business challenges and provide vital

evidence for policy makers.

| | www.nnfcc.com | [email protected]

Lucy Hopwood,

Lead Consultant – Bioenergy & Anaerobic Digestion