an overview of the us downstream project landscape

TRANSCRIPT

US Downstream Construction Overview

Mr. Toad’s wild ride

Global oil demand vs. refinery capacity builds (2014‐2020)

90 92 94 96 98 100 102 104

2015

2016

2017

2018

2019

2020

Global Refining Capacity

Global Oil Demand

• Detailed and up‐to‐date information for active construction projects in the refining, gas processing, LNG and petrochemical industries across the globe

www.constructionboxscore.com

$230 B

$343 B

$77 B$89 B

$230 B

$141 B

$478 B

Total announced downstream project investments by region, 2015‐2030

Total active projects breakdown

27%

6%

10%17%

40%Planning

Study

FEED

Engineering

Under Construction

Total new project announcements by region, February 2013‐present.

0

20

40

60

80

100

120

140

160

180

Africa Asia‐Pacific Canada Europe* Latin America Middle East US

2013

2014

2015

*Europe includes Eastern Europe, Russia and the CIS

Total new project announcements by region and sector, 2015

0

5

10

15

20

25

30

35

40

45

50

Africa Asia‐Pacific Canada Europe Latin America Middle East US

Refining

Petrochemical

Gas Processing/LNG

7%, 6%, 5%

20%, 24%, 31%, 36%

8%, 9%, 5%

6%, 4%, 8%

16%, 16%, 7%

14%, 12%, 12%

25%, 22%, 26%

Market share analysis of new projects, 2013‐2015

Gulf Coast new project market share, 2015‐present

US vs. Gulf Coast

USNon‐GulfCoastUS GulfCoast

64%36%

9

17

46

7 9

17

36

151

1520

0

20

40

60

80

100

120

140

160

PADD 1 PADD 2 PADD 3 PADD 4 PADD 5

new projects

active projects

USGC market breakdown

Gulf Coast Market Share Breakout

AlabamaFloridaLouisianaMississippiTexas

62%33%

4%

USGC Sector Breakdown

Refining

GasProcessing/LNG

Petrochemical

46%41%

13%

• 95% of active USGC projects are located in Texas and Louisiana• Nearly 90% of USGC active projects are in the gas processing/LNG or petrochemical

industries

New project announcements along the Gulf Coast, 2012

Gas Processing/LNG ProjectsPetrochemical ProjectsRefining Projects

New project announcements along the Gulf Coast, 2013

New project announcements along the Gulf Coast, 2014

New project announcements along the Gulf Coast, 2015‐present

US refining capacity by PADD

PADD 3: GULF COASTNo. of refineries: 55Total capacity: 9.258 MMbpd

PADD 5: WEST COASTNo. of refineries: 30Total capacity: 2.933 MMbpd

PADD 4: THE ROCKIESNo. of refineries: 17Total capacity: 646 Mbpd

PADD 2: MIDWESTNo. of refineries: 26Total capacity: 3.859 MMbpd

PADD 1: EAST COASTNo. of refineries: 9Total capacity: 1.268 MMbpd

• Over 330 MMtpy of LNG capacity announced

• US DOE non‐FTA approvals:• Sabine Pass LNG• Freeport LNG• Lake Charles Exports (Trunkline)• Dominion Cove Point LNG• Jordan Cove (Coos Bay)• Cameron LNG• Oregon LNG• Corpus Christi LNG• Crowley (formerly Carib Energy)• Alaska LNG (conditional)• American LNG

• The billion‐dollar question: What will be built?

US LNG export terminal projects

US LNG capacity online by 2020 = @ 58 MMtpy2016 = 9 MMtpy• Sabine Pass Trains 1 & 22017 = 14.5 MMtpy• Sabine Pass Trains 3 & 4 (late 2016 thru mid/late 2017)

• Dominion Cove LNG Train 12018 = 25.4 MMtpy • Cameron LNG Trains 1, 2, 3• Freeport LNG Train 1• Corpus Christi LNG Trains 1

& 22019 = 8.8 MMtpy• Freeport LNG Trains 2 & 3

Sabine Pass LNG project

Cove Point LNG project

US petrochemicals

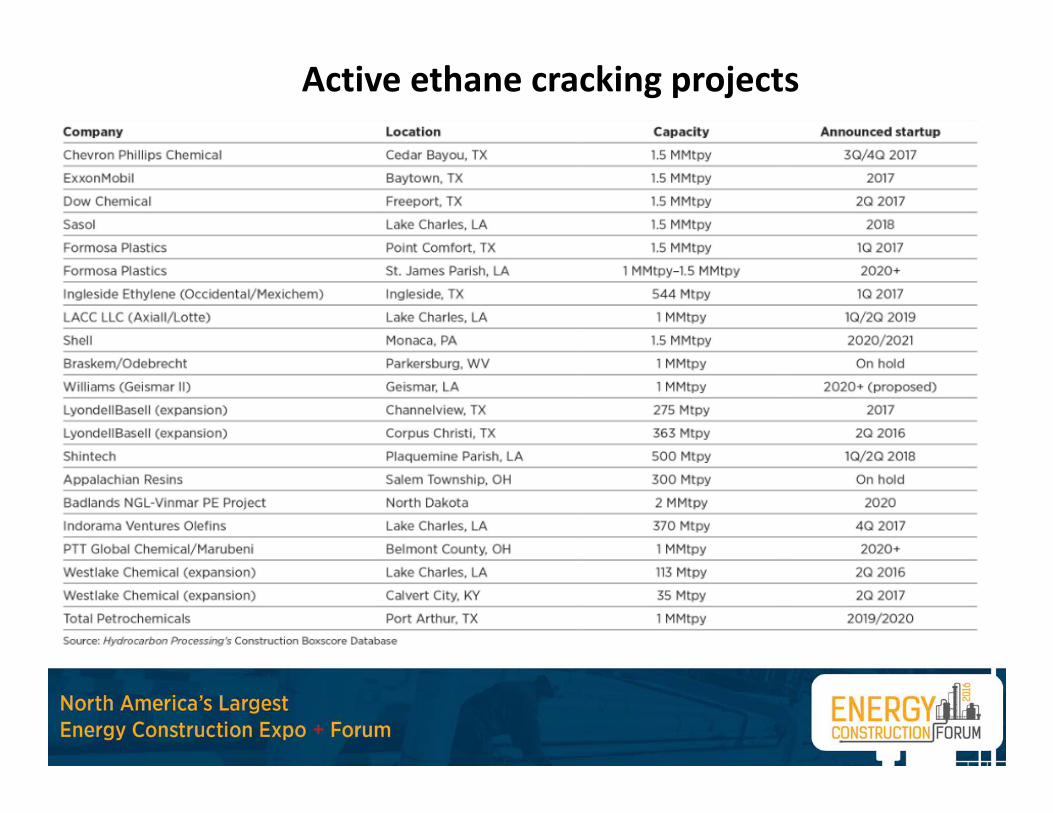

Active ethane cracking projects

Active US methanol projectsCompany Location Capacity Cost, US $ MM Announced start‐up

Methanex – Geismar I Geismar, LA 1 MMtpy 550 Completed 2015

Methanex – Geismar II Geismar, LA 1 MMtpy 550 Completed 2016

OCI (Natgasoline) Beaumont, TX 1.75 MMtpy 1,000 4Q 2016

Valero Norco, LA 1.6 MMtpy 700 2018 (delayed)

NWIW – Port of Kalama Port of Kalama, WA 3.65 MMtpy 1,800 4Q 2019

NWIW – Port of St. Helens Port of St. Helens, OR 3.65 MMtpy 1,800 2021

NWIW – Tacoma Tacoma, WA 7.3 MMtpy 3,400 2021 – Phase 1 (on hold)

South Louisiana Methanol St. James Parish, LA 1.825 MMtpy 1,300 2Q 2017 (delayed)

Celanese/Mitsui Clear Lake, TX 1.3 MMtpy 800 Completed 4Q 2015

Celanese Bishop, TX 1.3 MMtpy 700‐800 2018

CCI Braithwaite, LA 1.825 MMtpy 1,200 2019

Yuhuang Chemical (Plant 1) St. James Parish, LA 1.7 MMtpy 1,000 2018

Yuhuang Chemical (Plant 2) St. James Parish, LA 1.3 MMtpy 1,000 2020

Conell Group‐Chemical Inv. Corp. JV

Shoal Point, TX 7.2 MMtpy 4,500 2020+

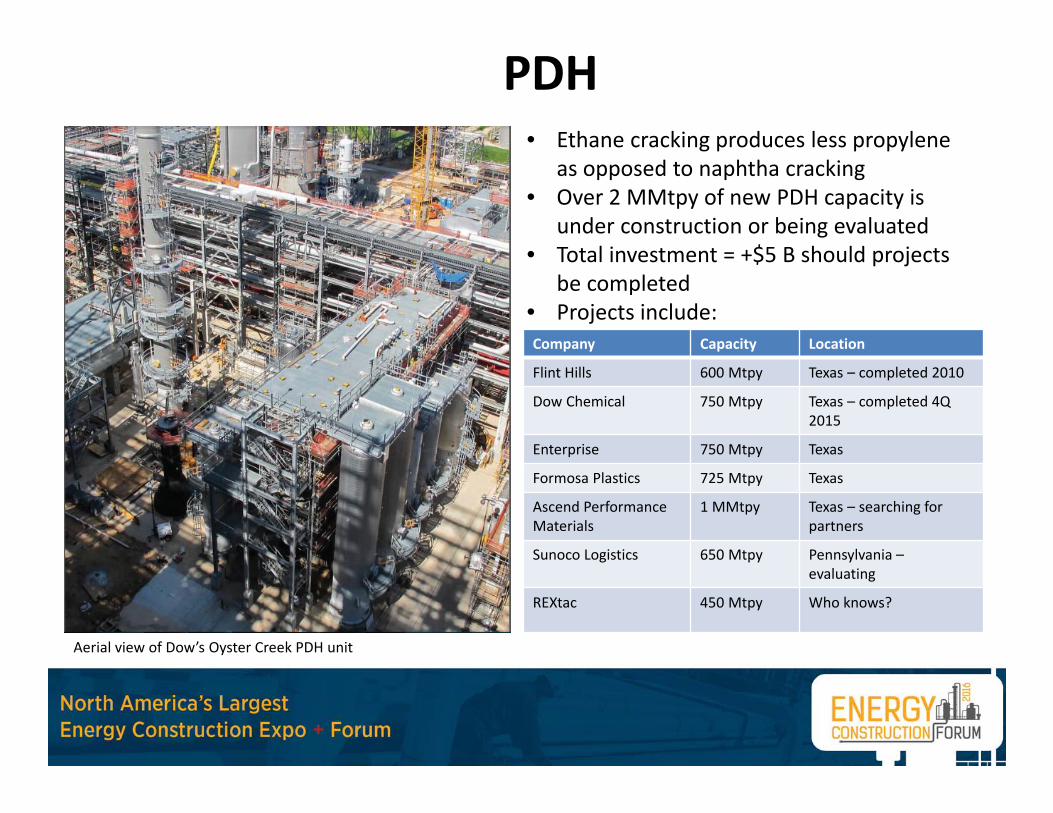

PDH • Ethane cracking produces less propylene

as opposed to naphtha cracking• Over 2 MMtpy of new PDH capacity is

under construction or being evaluated • Total investment = +$5 B should projects

be completed• Projects include:Company Capacity Location

Flint Hills 600 Mtpy Texas – completed 2010

Dow Chemical 750 Mtpy Texas – completed 4Q 2015

Enterprise 750 Mtpy Texas

Formosa Plastics 725 Mtpy Texas

Ascend PerformanceMaterials

1 MMtpy Texas – searching for partners

Sunoco Logistics 650 Mtpy Pennsylvania –evaluating

REXtac 450 Mtpy Who knows?

Aerial view of Dow’s Oyster Creek PDH unit

Ammonia‐Urea plant capacity build‐out

• Over $16 B in new ammonia‐urea plant capacity

• Down from $20 B (CHS & EuroChem)

• 2016 – year of the fertilizer build‐out

• Total capacity could top 12 MMtpy by 2020 should all projects be built

The Gift Shop

Updated 2016 version available Summer 2016

• FULL DATA ACCESS PLAN NOW AVAILABLE!

Contact:

Lee NicholsEditor/Associate PublisherHydrocarbon Processing

Gas Processing Data Division713‐520‐4484

Thank you for attending the 2nd annual ENERGY CONSTRUCTION FORUM