amtrak fleet strategy plan update 2011 ken uznanski amtrak policy and development aashto standing...

TRANSCRIPT

Amtrak Fleet Strategy Plan Update 2011

Ken UznanskiAmtrak Policy and Development

AASHTO Standing Committee on Rail Transportation2011 Annual Meeting

Charlotte, NCSeptember 12, 2011

Amtrak Fleet Strategy Plan

• Initially Published February 2010

– Why a comprehensive fleet plan?

– Intercity Passenger Rail in United States has unprecedented opportunity that must be addressed

– Amtrak, as the nation’s passenger railroad, will play a vital role- Amtrak’s fleet is and will be at the heart of its ability to deliver competitive

service, impacting all aspects of Amtrak services- History of underinvestment has constrained Amtrak’s ability to deliver modern

and reliable services our customers deserve- Average age of equipment in the existing Amtrak Fleet is approaching 25 years- Essential need for recapitalization of the fleet to sustain and grow service- Continuing, predictable equipment replacement plan is needed to rebuild and

stabilize supplier base

• Fleet Strategy Plan Update 2011

– Further refines and updates previous plan

– Addresses new developments

– Responds to feedback received from stakeholders

Fleet Strategy Plan Objectives

• Replace our aging fleet with modern equipment

• Buy equipment in a manner that will develop and support a viable manufacturing base and fleet

– Orders of sufficient size to attract, develop and sustain a robust car building industry

– Deliveries spread out over period of years, to allow for economical use of manufacturing plant, ease of incorporation into fleet

– Allows us to ‘debug’ issues on small batches of new equipment at the beginning of a production run

• Establish guidelines for the commercial life of new equipment

• Establish a foundation for continuing fleet plan update– Determinations of demand so that we can estimate costs, capacities, and

fleet size

– Numbers aren’t chiseled in stone – will change as the plan develops in response to changing economic and technical conditions

Why is this such an urgent need?

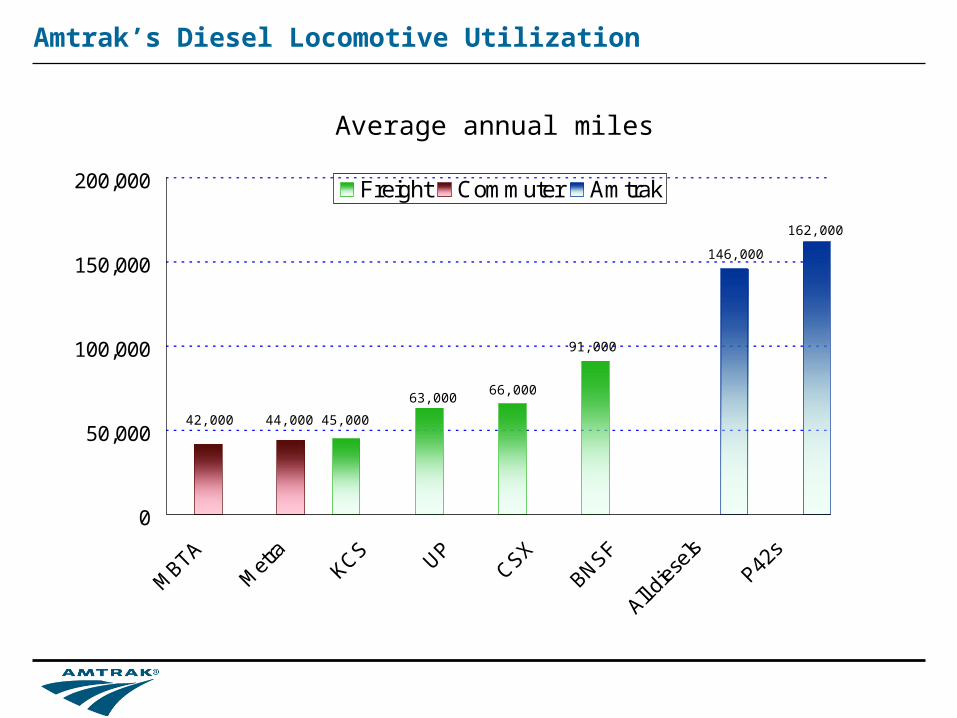

Amtrak’s Diesel Locomotive Utilization

0

50,000

100,000

150,000

200,000

MBTA

Met

raKCS UP

CSX

BNSF

All dies

elsP42

s

Freight Commuter Amtrak

Average annual miles

42,000 44,000

146,000

162,000

45,000

63,00066,000

91,000

Amtrak Electric Locomotive Utilization

Average annual miles

25,375 26,505

61,000

126,600

0

25,000

50,000

75,000

100,000

125,000

150,000

SEPTA NJT MARC Amtrak

Amtrak’s Average Annual Car Miles – Highest in US Passenger Rail

619 21 24

31 32 32 3339 44 44 46 49 51 52 53 56

69

145 143

166 166157

193 195

0

44

88

132

176

220

Se

attl

e

Va

./D.C

.

Co

nn

DO

T

Da

llas

MA

RC

Fo

rt W

ort

h

Sa

n F

ran

cisc

o

Ch

i.-M

etr

a

Sa

n J

ose

Sa

n D

ieg

o

SE

PT

A

Ch

i.-N

ICT

D

MB

TA

Me

tro

No

rth

Lo

s A

ng

ele

s

Ne

w J

ers

ey

Lo

ng

Isla

nd

Tri

-Ra

il

Ho

rizo

n

Su

rflin

er

Am

flee

t

Ace

la

19

50

’s D

ine

rs

Vie

wlin

ers

Su

pe

rlin

ers

Commuters:

Maintained nights, weekends, off-peak

Amtrak:

Operate 24x7, turnaround in 4 to 6 hours

Amtrak

Average annual miles (in thousands)

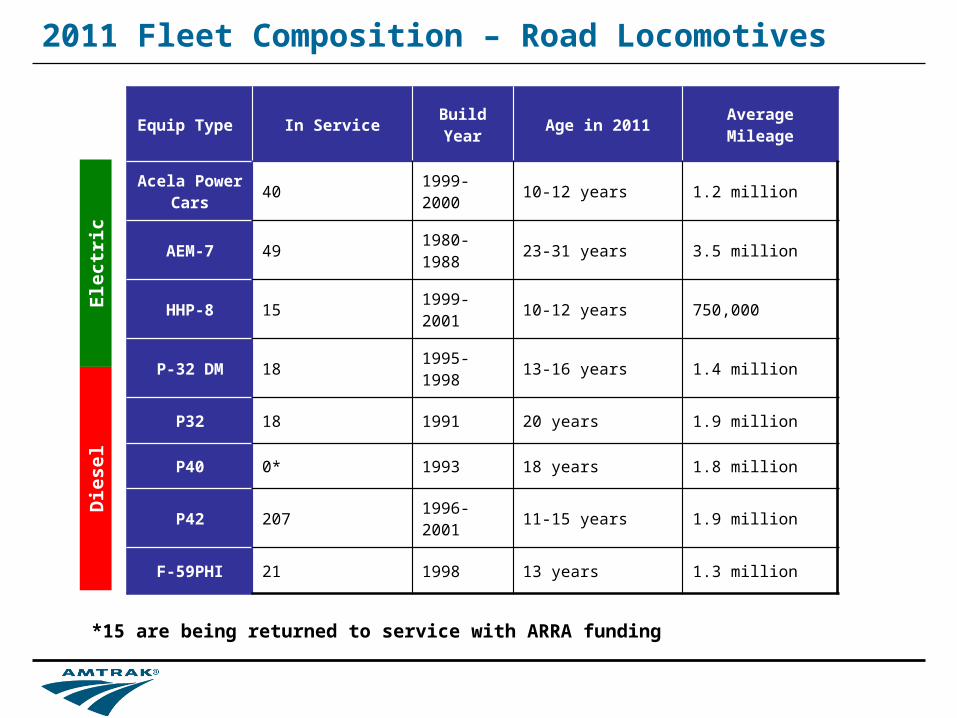

2011 Fleet Composition – Road Locomotives

Equip Type In Service Build Year Age in 2011 Average Mileage

Acela Power Cars

40 1999-2000 10-12 years 1.2 million

AEM-7 49 1980-1988 23-31 years 3.5 million

HHP-8 15 1999-2001 10-12 years 750,000

P-32 DM 18 1995-1998 13-16 years 1.4 million

P32 18 1991 20 years 1.9 million

P40 0* 1993 18 years 1.8 million

P42 207 1996-2001 11-15 years 1.9 million

F-59PHI 21 1998 13 years 1.3 million

*15 are being returned to service with ARRA funding

Ele

ctri

cD

ies

el

2011 Fleet Composition - Cars

Equip TypeIn

ServiceBuild Year Age in 2011 Service

Average Mileage

Acela 120 1999-2000 11-12 years NEC 1.2 million

Talgo 29 1999 12 years SD 1.7 million

Amfleet I 412† 1974-1977 34-37 years NEC/SD 3.8 million

Amfleet II 144‡ 1980-1981 30-32 years LD/SD 5.1 million

Superliner I 249§ 1979-1981 20-32 years LD 5.5 million

Superliner II

184+ 1994-1996 15-17 years LD 2.9 million

Viewliner 50± 1995-1996 15-16 years LD 2.5 million

Horizon 97 1989-1990 21-22 years SD 2.4 million

Metroliner 17 1967 44 years NEC Unknown*

Heritage 92 1948-1956 55-63 years LD Unknown*

*Mileage for equipment that predates Amtrak is unknown – but in some cases includes 20+ years of daily revenue service

†55 will be returned to service with ARRA funding

‡5 will be returned to service with ARRA funding

§14 will be returned to service with ARRA funding

+6 will be returned to service with ARRA funding

±1 will be returned to service with ARRA funding

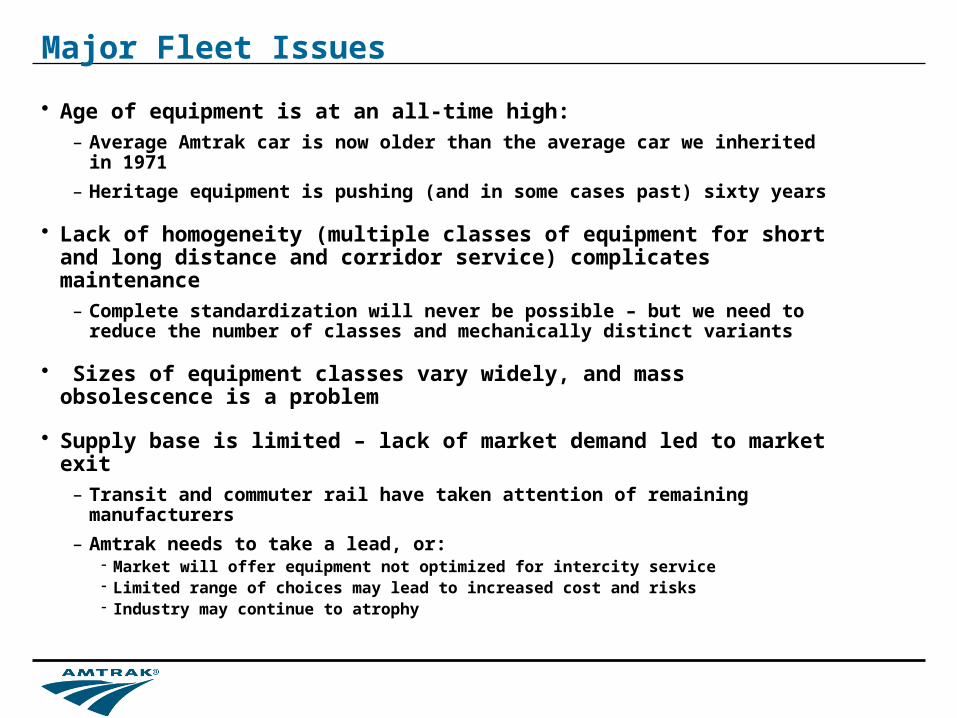

Major Fleet Issues

• Age of equipment is at an all-time high:– Average Amtrak car is now older than the average car we inherited in 1971

– Heritage equipment is pushing (and in some cases past) sixty years

• Lack of homogeneity (multiple classes of equipment for short and long distance and corridor service) complicates maintenance

– Complete standardization will never be possible – but we need to reduce the number of classes and mechanically distinct variants

• Sizes of equipment classes vary widely, and mass obsolescence is a problem

• Supply base is limited – lack of market demand led to market exit– Transit and commuter rail have taken attention of remaining manufacturers

– Amtrak needs to take a lead, or:- Market will offer equipment not optimized for intercity service- Limited range of choices may lead to increased cost and risks- Industry may continue to atrophy

Major components of the 2010 Fleet Plan

• Set limits on maximum equipment age (“lifing”)

– Need to retire 60 year old equipment

– Need to determine useful life and commercial life- Useful life is the maximum period we want to have equipment in service – 30 years for engines, 40 years for passenger cars- Commercial life is the period when the equipment is maintainable, technically viable and commercially attractive for its designed service

• Estimate ridership demand in future years

• Develop assumptions for costs and

production/purchase rates

• Include associated costs (acquisition, maintenance, etc.)

• Create demand for every type of equipment, and provide potential economies of scale and consistency for suppliers and state partners

Major components of the 2010 Fleet Plan (cont’d)• Commercial life of equipment is set in plan; from 20-30 years (depending on

equipment type)

• Plan designed for 2% ridership growth on existing services – but procurement model allows us to easily expand order sizes based on

– Requirements of new corridors (Sec 305 committee)

– Large-scale growth beyond conservative levels

• Average cost is about $743 million per year

• Total anticipated cost in 2009 dollars will be– $11 billion through 2023

– $23 billion through 2040

– These costs include associated improvements to maintenance facilities, provision of spare parts, and provision of fleet overhaul services for the period

• Total fleet procurement over a 30 year period will include more than 2,500 cars and 700 locomotives, independent of needs for projected state-supported corridors and new services

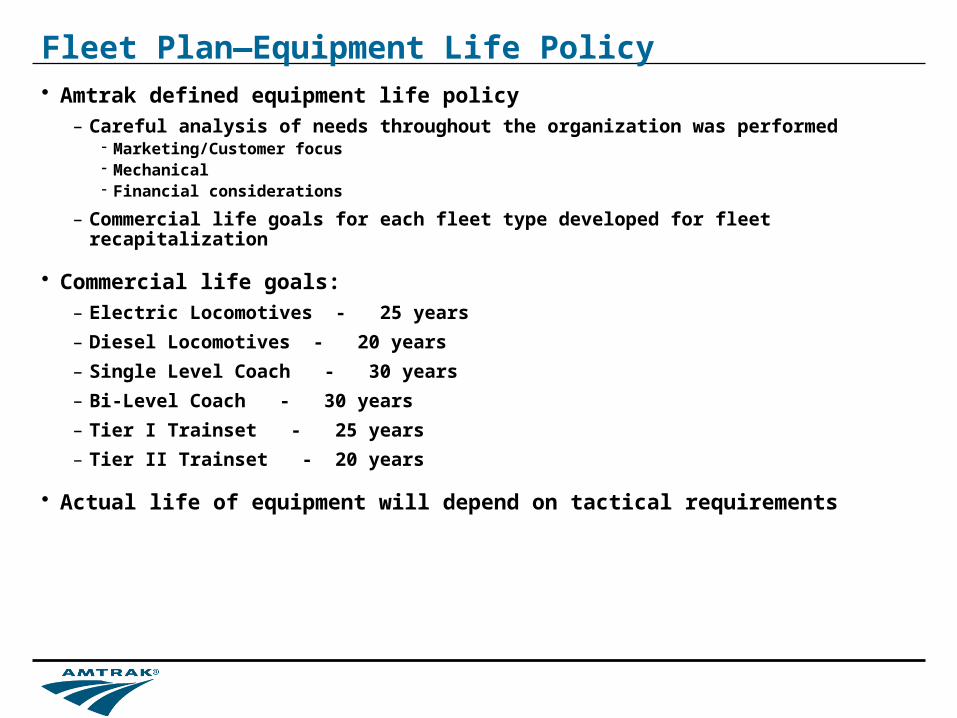

Fleet Plan—Equipment Life Policy• Amtrak defined equipment life policy

– Careful analysis of needs throughout the organization was performed- Marketing/Customer focus- Mechanical- Financial considerations

– Commercial life goals for each fleet type developed for fleet recapitalization

• Commercial life goals:– Electric Locomotives - 25 years

– Diesel Locomotives - 20 years

– Single Level Coach - 30 years

– Bi-Level Coach - 30 years

– Tier I Trainset - 25 years

– Tier II Trainset - 20 years

• Actual life of equipment will depend on tactical requirements

Amtrak Fleet Acquisition Plan• Provides for a smoothed acquisition of high volume vehicle types

• Grouped acquisition of lower volume vehicle types

• Steady state procurement– Approximately 65 single level cars per year

– Approximately 35 bi-level cars per year

– 70 electric locomotives under present procurement

– Begin acquisition of 265 diesel locomotives at rate of 25 per year

– Replace switcher fleet at rate of 10 per year

• Actual batch sizes and composition will be determined as necessary

• Coordination with PRIIA Section 305– Baseline that is scalable to accommodate state needs

Florida-bound Silver Star at Seabrook, Maryland

Heritage diner(1948-1958)

Heritage baggage car(1946-1976)

AEM-7 DC electric locomotive (1980)

Viewliner sleeping cars(1995-1996)

Amfleet II coachesand lounge car(1981-1983)

A snapshot of the present

Bob Pickering photo

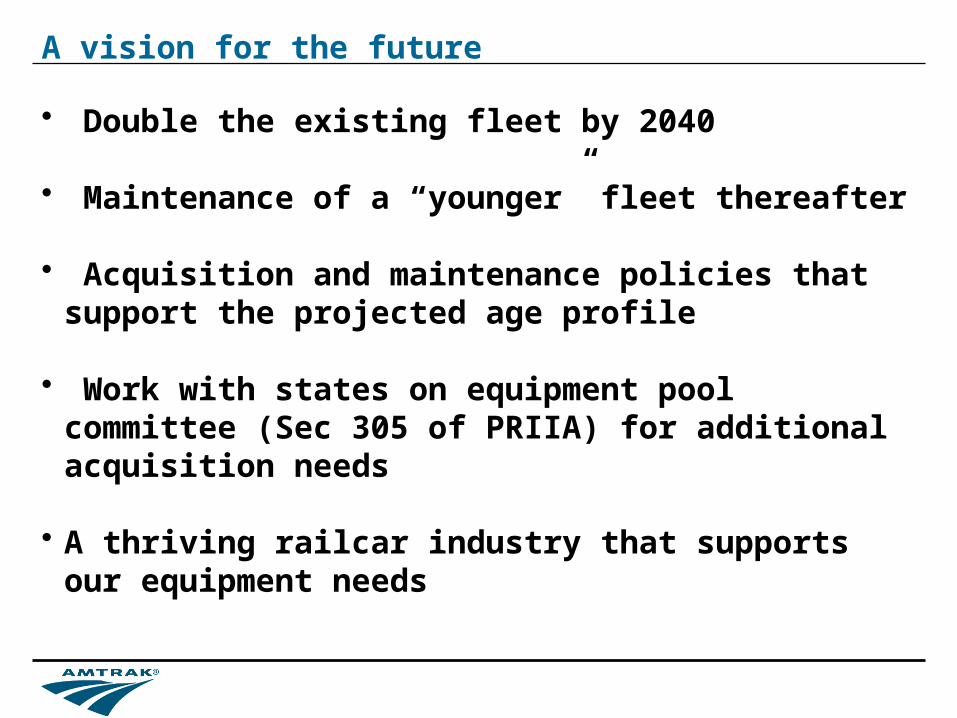

A vision for the future

• Double the existing fleet by 2040

• Maintenance of a “younger” fleet thereafter

• Acquisition and maintenance policies that support the projected age profile

• Work with states on equipment pool committee (Sec 305 of PRIIA) for additional acquisition needs

• A thriving railcar industry that supports our equipment needs

Current Amtrak Equipment Aquisitions

• Long Distance Single Level Program

–130 car procurement awarded to CAF, USA in June 2010

–Will replace Heritage cars and bolster capacity of fleet

–Deliveries begin October 2012

• Electric Locomotives

–Contract awarded to Siemens Transportation for 70 new electric locomotives in September 2010

–Replaces all electric locomotives on NEC with single type

–First locomotive for testing to be delivered December 2012

17

Fleet Strategy Plan Update

• Fleet Strategy Plan is to be updated on an annual basis

• Previous plan was issued in February 2010

• The update is an evolutionary rather than revolutionary one

• Much of the plan is unchanged

• Updates are provided where circumstances have moved on

• External feedback has been added to internal updates

• The new plan brings all of this together

18

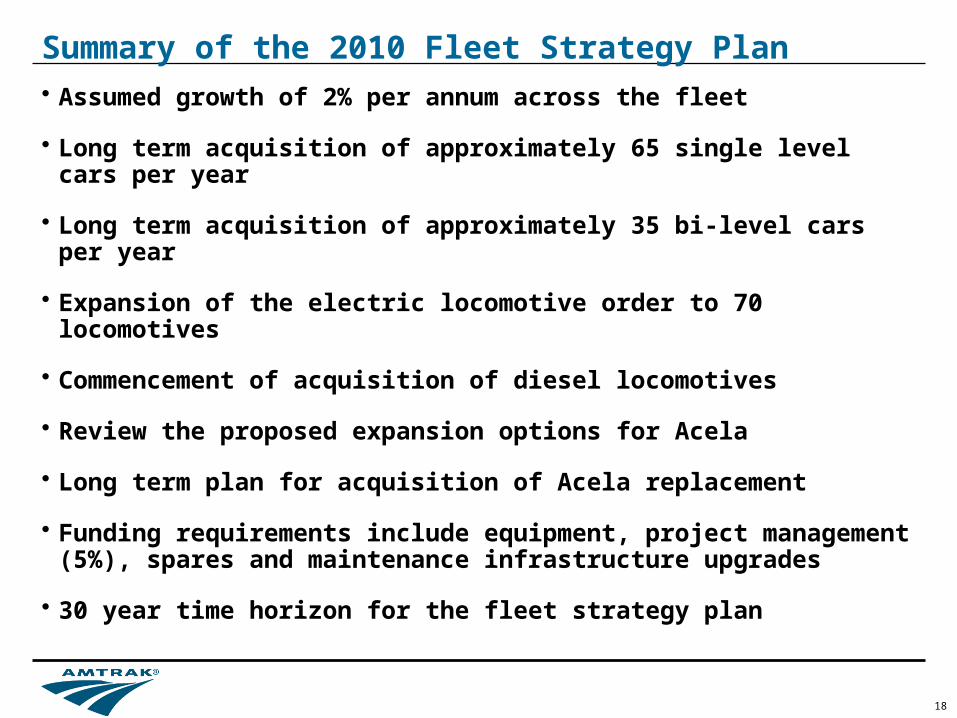

Summary of the 2010 Fleet Strategy Plan

• Assumed growth of 2% per annum across the fleet

• Long term acquisition of approximately 65 single level cars per year

• Long term acquisition of approximately 35 bi-level cars per year

• Expansion of the electric locomotive order to 70 locomotives

• Commencement of acquisition of diesel locomotives

• Review the proposed expansion options for Acela

• Long term plan for acquisition of Acela replacement

• Funding requirements include equipment, project management (5%), spares and maintenance infrastructure upgrades

• 30 year time horizon for the fleet strategy plan

19

Feedback from the 2010 Fleet Strategy Plan

• Briefings were provided to industry groups and political staffers

• External interests provided comments directly

• OIG Review

Comments received included:

– The 2% growth assumptions are not sufficient

– Bi-level vehicle introduction would be cost beneficial

– Life assumptions are too short

– Demand level is too small for industry to be competitive

– Where will the funding come from?

20

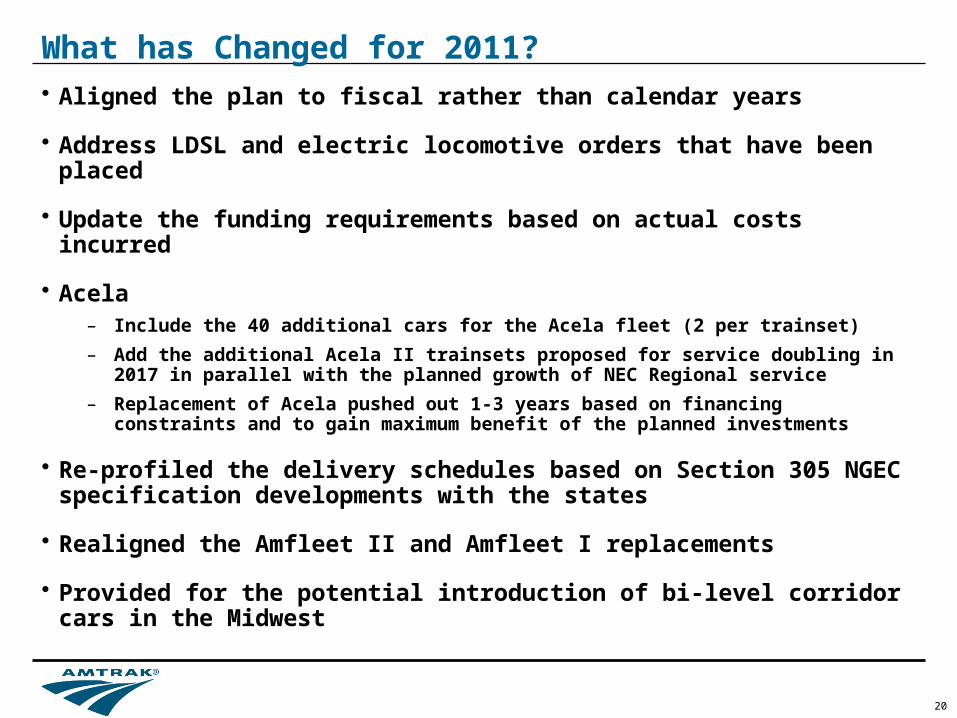

What has Changed for 2011?• Aligned the plan to fiscal rather than calendar years

• Address LDSL and electric locomotive orders that have been placed

• Update the funding requirements based on actual costs incurred

• Acela– Include the 40 additional cars for the Acela fleet (2 per trainset)

– Add the additional Acela II trainsets proposed for service doubling in 2017 in parallel with the planned growth of NEC Regional service

– Replacement of Acela pushed out 1-3 years based on financing constraints and to gain maximum benefit of the planned investments

• Re-profiled the delivery schedules based on Section 305 NGEC specification developments with the states

• Realigned the Amfleet II and Amfleet I replacements

• Provided for the potential introduction of bi-level corridor cars in the Midwest

21

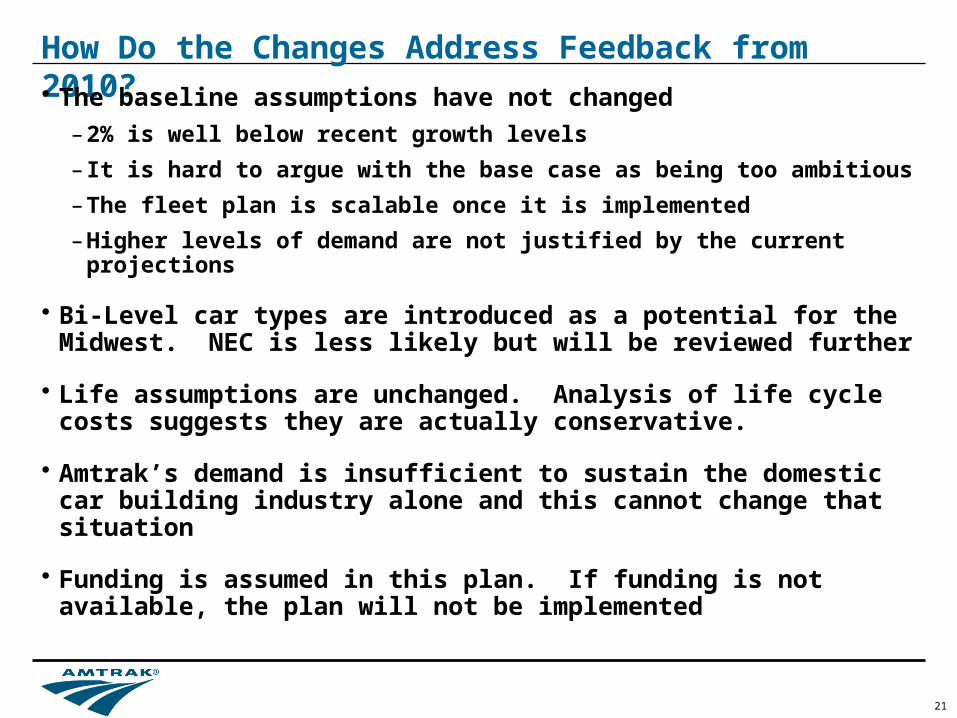

How Do the Changes Address Feedback from 2010?

• The baseline assumptions have not changed

– 2% is well below recent growth levels

– It is hard to argue with the base case as being too ambitious

– The fleet plan is scalable once it is implemented

– Higher levels of demand are not justified by the current projections

• Bi-Level car types are introduced as a potential for the Midwest. NEC is less likely but will be reviewed further

• Life assumptions are unchanged. Analysis of life cycle costs suggests they are actually conservative.

• Amtrak’s demand is insufficient to sustain the domestic car building industry alone and this cannot change that situation

• Funding is assumed in this plan. If funding is not available, the plan will not be implemented

22

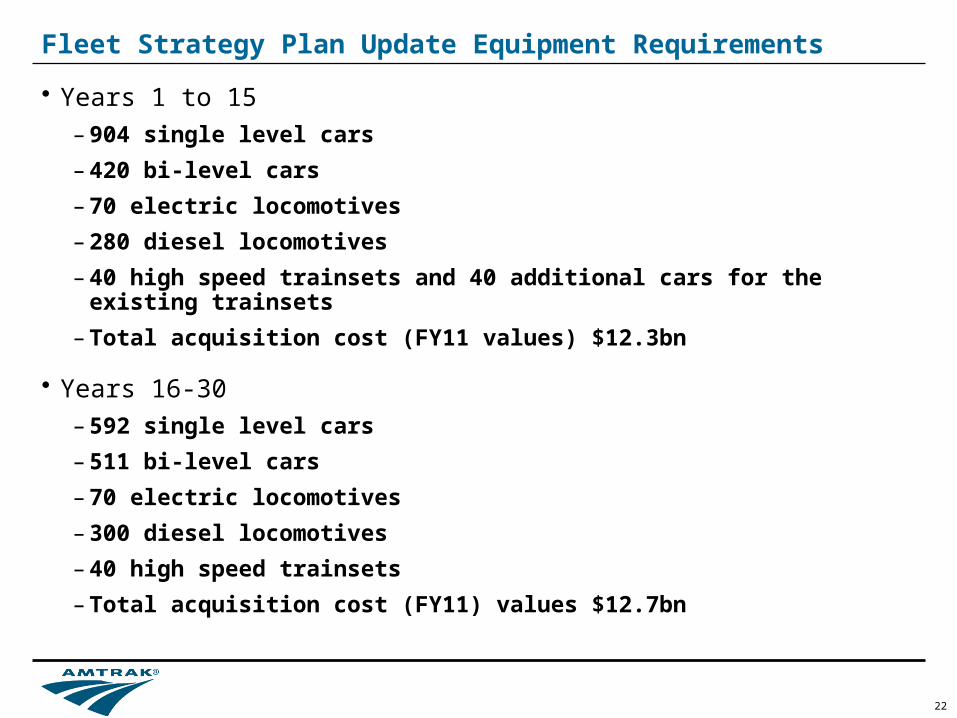

Fleet Strategy Plan Update Equipment Requirements

• Years 1 to 15

– 904 single level cars

– 420 bi-level cars

– 70 electric locomotives

– 280 diesel locomotives

– 40 high speed trainsets and 40 additional cars for the existing trainsets

– Total acquisition cost (FY11 values) $12.3bn

• Years 16-30

– 592 single level cars

– 511 bi-level cars

– 70 electric locomotives

– 300 diesel locomotives

– 40 high speed trainsets

– Total acquisition cost (FY11) values $12.7bn

23

What is not in the 2011 Plan Update?• Very high speed equipment for the minimum operating segment between NYC

and PHL is discussed but not quantified

• State equipment needs funded through HSIPR grants

• Any infrastructure issues outside maintenance facilities, e.g. stations, track condition, power supplies, catenary.

– Upgrades necessary to improve performance of the existing equipment

– Enhancements necessary to accommodate a growth in the service from additional equipment

• New maintenance facilities or significant expansion of facilities for additional capacity are not included

– Upgrade to the current facilities for new equipment is included

– Infrastructure upgrades are not optional when acquiring equipment

• Capacity growth above the 2% projection. – Actual growth is above 2% and has average that for a number of years

– Additional equipment to meet that growth can be accommodated through scaling of the core plan but will require additional capital funding

24

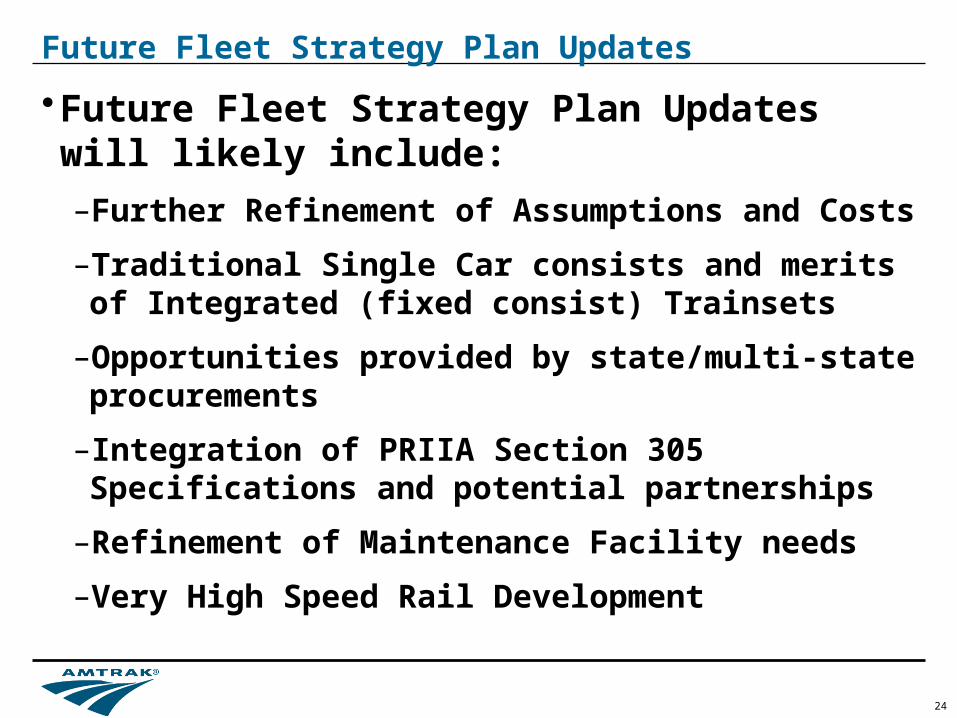

Future Fleet Strategy Plan Updates

•Future Fleet Strategy Plan Updates will likely include:

–Further Refinement of Assumptions and Costs

–Traditional Single Car consists and merits of Integrated (fixed consist) Trainsets

–Opportunities provided by state/multi-state procurements

–Integration of PRIIA Section 305 Specifications and potential partnerships

–Refinement of Maintenance Facility needs

–Very High Speed Rail Development