american bar association annual meeting san francisco, ca

TRANSCRIPT

{W1842975.3} 1

American Bar Association Annual Meeting

San Francisco, CA Section of Business Law

Consumer Financial Services Committee Banking Law Committee

August 7, 2010

Program: Regulatory Reset: Consumer Financial Services Regulation Under Federal Reform Legislation

Moderator:

Richard P. Hackett Pierce Atwood LLP

Speakers:

Roland E. Brandel Morrison & Foerster LLP Sandra Braunstein Director, Division of Consumer and Community Affairs Board of Governors of the Federal Reserve System James L. Brown Emeritus Professor Center for Consumer Affairs University of Wisconsin - Milwaukee Heather Koenig Associate General Counsel for Global Risk Bank of America Joel Winston Director, Division of Financial Practices Federal Trade Commission

Topic: Overview of New Consumer Financial Services Regulator

• a technical overview of the scope of the jurisdiction of the CFP Bureau

{W1842975.3} 2

• review of the organization, funding, oversight, governance, relationship to other agencies, and transition to power of the new Bureau

• review of new explicit authority to interpret and enforce the Enumerated Consumer Laws and the transferred authorities, and to exercise new substantive powers, such as preventing unfair, deceptive and abusive practices

• examination and supervision of financial service providers, bank and nonbank • new remedial and enforcement powers • “regulatory improvements”

Changes to Federal Preemption

• The scope and likely impact of new preemption rules on national consumer lending businesses

{W1842975.3} 3

Contents Consumer Financial Services Regulation Going Forward Scope and Exceptions -- Contrasting House and Senate Versions by James L. Brown Financial Regulatory Reform - organization, governance, funding, transition by Joel Winston Bureau of Consumer Financial Protection Supervision and Enforcement by Heather Koenig Preemption by Roland E. Brandel Comparison of House Bill vs. Senate “Base” Bill Sent to Conference Committee vs. Conference Report by Richard P. Hackett

{W1842975.3} 4

Richard P. Hackett Experience Rick is one of New England’s leading lawyers involved in consumer financial services law and retail financial services regulation. His practice involves all aspects of state and federal regulation of retail financial products origination and marketing, e-payments, regulation of financial service entities, and lending, deposit, and insurance transactions. Rick’s clients include regional and national banks, e-payments companies, web-based credit card companies, education loan marketers and processors, mortgage companies, licensed consumer lenders, insurers, and commercial lenders to the financial services industry. Rick has extensive experience in planning, structuring, and reviewing consumer financial products, and in negotiating complex joint venture, marketing, servicing, and financing arrangements for retail financial service providers. Rick has served as lead counsel in the negotiation and documentation of student loan origination and purchase programs that govern the creation and disposition of over $4 billion alternative student loans annually. Rick’s recent projects include: development of a fully web-based electronic application and E-Signature system for closed-end loans; structuring private-label business charge-card programs for business-to-business commercial finance companies; development of a Customer Identification Program for use in a web-based environment by more than 20 national lenders; complete redocumentation of cash management services for a top-20 national bank; comprehensive representation of a web-based business credit card company providing enhanced data services to the building trades; drafting and supporting the enactment of a complete rewrite of Maine's "Predatory Lending" statute; negotiating, documenting, and obtaining regulatory approval for bank acquisitions; and counseling lenders in consumer direct and indirect financing programs for autos, boats, condos, and timeshares. Rick is an adjunct member of the faculty of the Morin Center for Banking Law at Boston University School of Law and a frequent national lecturer on consumer financial services law. From 1978 to 1979, Rick served as Law Clerk to the Honorable Frank M. Coffin, then Chief Judge of the U.S. Court of Appeals to the First Circuit. Honors and Distinctions An attorney with Pierce Atwood since 1979, Rick has been listed in The Best Lawyers in America since 1996. Publications Rick is the co-author of Current Developments in Payment Systems, Deposit Accounts, and Electronic Delivery of Financial Services, (The Business Lawyer, Vol. 62, No. 2, 2007). Rick is the author of: “Foreign Corporations,” Published as Chapter 12 in Maine Corporation Law and Practice, Prentiss Hall (1990) and “Note: Punitive Damages in Arbitration, The Search for a Workable Rule,” 63 Cornell L. Rev. 272 (1978).

{W1842975.3} 5

Professional Activities Rick is a Regent of the American College of Consumer Financial Services Lawyers. He is Vice Chair of the Consumer Financial Services Committee of the Business Law Section of the American Bar Association. From 2003 to 2006 he served as that committee’s chair of its Subcommittee on Internet Delivery/Electronic Banking. He is active in the Maine State Bar Association Consumer and Financial Institutions Law Section (serving as chair from 1982 to 1986 and 1998 to 1999).

{W1842975.3} 6

Roland E. Brandel Roland E. Brandel is a Senior Counsel in the San Francisco office of the international law firm of Morrison & Foerster. He is a member of, and formerly chaired, the firm’s financial services practice group. He has written several books, including The Law of Electronic Fund Transfer Systems, The Community Reinvestment Act, Policies and Compliance, and Truth in Lending: A Comprehensive Guide and numerous articles on financial service topics. He has served as Chair of the ABA’s Consumer Financial Services Committee, Chair of the California State Bar’s Financial Institution Committee, Chair of the Legal Advisory Committee of the National Center on Financial Services and president of the American College of Consumer Financial Services Lawyers. Mr. Brandel, as part of a National Conference of Commissioners on Uniform State Laws (NCCUSL) major effort to rewrite UCC Articles 3 and 4, served as ABA Advisor to NCCUSL and chaired the ABA Ad Hoc Committee on Payment Systems. He was appointed by the Federal Reserve Board as a charter member of its Consumer Advisory Council and served two terms on the Council. He has been presented with lifetime achievement awards by the American College of Financial Services Lawyers, the Business Law Section of the State Bar of California and the California Bankers Association.

{W1842975.3} 7

Sandra Braunstein Director

Division of Consumer and Community Affairs Board of Governors of the Federal

Reserve System

Sandra Braunstein is the Director of the Board’s Division of Consumer and Community Affairs. As Director, Ms. Braunstein is principally responsible for the development and administration of Federal Reserve policies and functions related to consumer protection for financial services. She administers programs that write and review regulations for federal consumer protection laws. In addition to regulation development, the division is responsible for consumer compliance supervision and enforcement, and has oversight for the Federal Reserve System’s consumer compliance examinations of state member banks and consolidated supervision in bank holding companies. Other supervisory responsibilities housed in the division include analysis of bank and bank holding company applications for consumer-related issues, and consumer complaint handling and response.

Ms. Braunstein administers outreach efforts to the financial services industry,

state, local, and federal government officials, and consumer and community organizations. Some of these responsibilities are carried out through the System’s Community Affairs programs. Community Affairs staff, housed at the Board, and in the Reserve Bank and branch offices, conduct community development activities and promote increased access to capital and credit in underserved markets. Other division staff develop consumer education materials and conduct research on consumer behaviors. The division also coordinates meetings of the Board’s Consumer Advisory Council, a group that includes industry, consumer, and community group representatives who provide input for the Board’s consumer protection policy decisions.

Prior to joining the Federal Reserve Board, Ms. Braunstein served as the

executive director of the Northeast Community Development Corporation in Washington, D.C., the coordinator for commercial revitalization in Alexandria, Virginia, and as a management consultant for McManis Associates, specializing in economic diversification and development studies for city and county governments. She also worked as a federal program administrator for the city of Wilmington, Delaware.

{W1842975.3} 8

James L. Brown James L. Brown is Director of the Center for Consumer Affairs, an applied research unit within the School of Continuing Education at the University of Wisconsin-Milwaukee, a position he has held since 1977. He is an Associate Professor with UW-M. Prior to joining the University, he was a staff attorney with Milwaukee Legal Services, concentrating on consumer law matters. He teaches in the regular course offerings of the Center, and has taught for several different schools and departments at various campuses within the University of Wisconsin system. He also served as Associate Dean of the School of Continuing Education at UW-M from 2003-2004. He has written numerous articles on consumer financial services. He drafted or took part in the drafting of many Wisconsin consumer protection and financial services statutes and regulations. He has testified on numerous occasions on a variety of consumer-related matters before the Wisconsin Legislature, as well as the legislatures of California, Florida, Hawaii, Louisiana, and New Mexico, in addition to both Houses of Congress. Among the numerous organizations to which he has made presentations on various consumer and legal issues are: the American Bankers Association, Consumer Federation of America, the United States Department of the Treasury, the Office of the Comptroller of the Currency, the US League of Savings Institutions, the Money Management Council of the United Kingdom, the Congressional Office of Technology Assessment, the National Conference of Commissioners on Uniform State Laws, the Permanent Editorial Board for the Uniform Commercial Code, various White House Conferences on Financial Services, the Senior Management Committee of Ford Motor Company, the Executive Management Committee of the State Farm Insurance Group, the US Bank Administration Institute, the Electronic Funds Transfer Association, the National Automated Clearinghouse Association, the Federal Reserve Bank of New York, the Smart Card Forum, the European Economic Community, the Food Marketing Institute Payment Systems Council, the select Committee on Banking Law of the Bank of England, the American Bar Association, the Payment Card Center of the Federal Reserve Bank of Philadelphia, and the Practicing Law Institute. He has conducted training programs or research for American Express, the MAC (EFT) network, the Food Marketing Institute, Ford Motor Company, Citibank NA, TYME Corp., State Farm Insurance Company, the Task Force on the Future of the Canadian Financial Services Sector of the Federal Government of Canada, and the United Nations, among others. He is frequently interviewed by media from across the country on a variety of consumer related topics. He has lectured on consumer financial services topics in Belgium, Canada, Japan, Spain, and the United Kingdom. He serves or has served on various professional, civic, advisory and corporate boards, including: Current: - Member, Board of Directors, Consumer Federation of America (elected 1992)

{W1842975.3} 9

- Member, Board of Overseers to the Institute for Civil Justice of the RAND Corporation (appointed 2000)

- Member, Board of Directors, Electronic Funds Transfer Association (elected 1992) - Member, Board of Directors, Coalition Against Insurance Fraud (elected 1997) (Co-Chair) - Member, Advisory Board for the American Antitrust Institute (appointed 2005) - Member, Partners Council, National Consumer Law Center (appointed 2002)

Previous:

- TYME Corporation (the regional EFT network in Wisconsin), member, Board of Directors (1982-2002); Corporate Secretary (1994-2002) - Member, Board of Directors, National Consumers League (1999-2002) - Member, Experian Consumer Advisory Council (2000-2003) - Member, Consumer Advisory Council to the Board of Governors of the Federal Reserve System (1979-81) - Member, New Payments Code Committee of the Permanent Editorial Board for the Uniform Commercial Code (1979-82)

- Member, Board of Directors, Family Services of Milwaukee (1983-89); Vice Chairman (1987-89) - Member, Wisconsin Bell Consumer Advisory Council (1984-1991); Chair (1985-89) - Member, Wisconsin Electric Power Consumer Advisory Council (1983-1992) - Member, Board of Directors, Wisconsin Insurance Plan (1982-87); Chair (1985-87)

He has also served on several study committees for the Wisconsin Legislative Council, including the Special Committee on Consumer Credit Regulation (1979-1981). He is a former President of the Planning Council for Health and Human Services of Southeastern Wisconsin, and has been President of the Wisconsin Consumers League since 1983. He was a public member for many years during the 1990s of the State of Wisconsin, Department of Regulation & Licensing: (1) Real Estate Contractual Forms Advisory Council; and (2) Mortgage Banking Advisory Committee. He recruited, appointed, and trained arbitrators for Ford Motor Company's acclaimed alternative warranty dispute resolution mechanism, the Dispute Settlement Board program, from 1988 through 2005. In connection with this program, he consulted regularly with Ford on a variety of policy and legal interpretive matters regarding various state refund/replacement statutes ('Lemon Laws') and the federal Magnuson-Moss Warranty Act. He has participated in state rule-making proceedings respecting implementing regulations under various 'Lemon Laws'. He has participated as an expert or invited witness regarding a diverse variety of topical matters affecting consumers such as predatory lending, overdraft checking programs, insurance scoring, attorney advertising, misleading and deceptive trade practices, alleged ‘lemon laundering’, ‘choice’ auto insurance reform proposals, electronic funds transfers, and payment card joint venture antitrust litigation. He was an expert witness for the prevailing side in the case resulting

{W1842975.3} 10

in the largest civil antitrust action settlement in US history. [In re VisaCheck/MasterMoney Antitrust Litigation, CV-96-5238, (US Dist. Ct., E. Dist., NY) (2003)] He holds a fellowship as a representative for consumer and public interests with (and has made numerous presentations to) the Consumer Financial Services Committee, Business Law Section, American Bar Association (1994-present). He was co-chair of the Federalism and Preemption subcommittee of such Committee from 2001-2002. He was elected a Fellow of the American College of Consumer Financial Services Lawyers in 2000 and a member of the Board of Regents of the College in 2003. He currently serves as Secretary for the College’s Board of Regents. He chaired the College’s Annual Legal Writing Competition in 2006, 2007, and 2008. He received the Louis Linxwiler Award for outstanding achievement in consumer credit education from the National Foundation for Consumer Credit in 1994. He holds a BA in Physics from Princeton University and a JD from the University of Wisconsin Law School.

{W1842975.3} 11

Heather Koenig Associate General Counsel Bank of America Heather Koenig is Associate General Counsel supporting the Global Risk Organization at Bank of America. In her nearly four years at Bank of America, Heather has led the legal teams for Customer Segments and Deposits business, Online Banking, eChannels and Customer Solutions, Enterprise Privacy, Sales and Marketing. Heather also has supported Bank of America’s acquisitions of LaSalle Bank, Countrywide, and Merrill Lynch, and she is active with the public policy activities concerning the consumer side of the company. She is based in Charlotte, North Carolina. Before joining the Bank in October 2006, Heather was Counsel at Skadden, Arps, Slate, Meagher & Flom, LLP in Washington, DC in the firm’s Financial Institutions Regulatory Group. In that capacity, Heather principally focused on: financial institution mergers, acquisitions, and restructurings; consumer financial services; and general bank regulatory matters. From 1999 to 2002, Heather was resident in Skadden’s London office where she focused on international corporate finance and cross-border mergers and acquisitions. Prior to joining Skadden in 1998, Heather was clerk to the Honorable Claude M. Hilton, Chief Judge, United States District Court for the Eastern District of Virginia. Heather graduated with a B.A. from the College of William and Mary in 1993 and with a J.D. from American University in 1997. In law school, Heather served as Senior Articles Editor for the American University Law Review and was awarded the Most Outstanding Graduate award. During law school, Heather worked at the U.S. Treasury Department and at the Federal Reserve Bank of New York. Prior to law school, Heather was a consultant with Andersen Consulting (now Accenture). Heather is a member of the New York and Washington DC bars. She is active in the Banking Law Committee and the Consumer Financial Services Committee of the American Bar Association. Heather’s authorships include: The Real Estate Settlement Procedures Act, chapter in Consumer Financial Services, Law Journal Press (2001); The Eastern District of Virginia: A Working Solution for Civil Justice Reform, 32 U. Rich. L. Rev. 799 (1998); Florence County School District Four v. Carter: A Good IDEA, 45 AM.U.L. REV. 1479 (1996).

{W1842975.3} 12

Joel Winston Joel Winston is Associate Director of the Division of Financial Practices in the Federal Trade Commission’s Bureau of Consumer Protection. That Division has responsibility for enforcing federal consumer protection laws relating to mortgages and other credit products, debt collection, debt relief services, fair lending, and other financial products and services. Prior to that position, Mr. Winston was Associate Director of the FTC’s Division of Privacy and Identity Protection, with responsibilities covering the areas of consumer privacy, data security, identity theft, and credit reporting. While in that position, Mr. Winston served on a presidential Identity Theft Task Force, was a member of the Advisory Board for the BNA Privacy & Security Law Reporter, and served on the Editorial Board and as an author for a treatise published in 2009 by the American Bar Association, “Consumer Protection Law Developments.” In 2008, Mr. Winston received the Presidential Rank Award of Meritorious Executive, one of the highest honors given to members of the federal government’s Senior Executive Service. Earlier in his career at the FTC, Mr. Winston served as a staff attorney and Assistant Director in the Division of Advertising Practices. Mr. Winston is a frequent speaker and provides guidance and advice to the business and legal communities on consumer protection issues. He received his undergraduate degree (with high honors) and law degree (with honors) from the University of Michigan.

{W1842975.3} 13

Consumer Financial Services Regulation Going Forward Scope and Exceptions -- Contrasting House and Senate Versions

Jim Brown Director, Professor Emeritus Center for Consumer Affairs

University of Wisconsin-Milwaukee

ABA Business Law Section Consumer Financial Services Committee

San Francisco, CA August, 2010

[caveat: CONSUMER DISCLOSURE: This outline reflects

legislatively-adopted approaches – in some instances contrasting – taken by the US House and Senate respectively, to selected structural issues in addressing major consumer financial services regulatory reform as of late June, 2010, when the outline was initially prepared.

Subsequent to these actions, a Committee of Conference issued

Title X, of S. 1021. Provisions in bold and italics are those contained in that Title.

Both bodies’ versions are presented then, primarily for their

legislative historical value, with Title X provisions reflecting the next step in the evolutionary process of this monumental effort.]

{W1842975.3} 14

The primary entity created under the contrasting versions to engage in the regulation of consumer financial services products and activities will

be referred to herein as ‘the Agency’. This entity would be a separate agency as envisioned in the House version and a bureau housed within the Federal Reserve per the Senate version, with differing structures,

funding mechanisms, oversight bodies, and degrees of autonomy. Provisions found within (and unique to) the House-passed version

will be referred to as ‘CFPA-H’ while those within the Senate-passed version will be ‘CFPA-S’.

Specific section references are included, and refer respectively (in

the House version) to Title IV of HR 4173, and (in the Senate version) to Title X of HR 4173 (SB 3217, as amended).

The House version can be found at http://financialservices.house.gov/Key_Issues/Financial_Regulator

y_Reform/FinancialRegulatoryReform/hr4173eh.pdf

while the Senate version is available is at http://frwebgate.access.gpo.gov/cgi-bin/getdoc.cgi?dbname=111_cong_bills&docid=f:s3217as.txt.pdf As noted before, provisions in bold and italics are those from Title X from the Committee of Conference. - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

{W1842975.3} 15

Agency Goals CFPA-H: to promote transparency, simplicity, fairness, accountability, and equal access in the market for consumer financial products or services [Sect. 4201(a)] CFPA-S: to implement and, where applicable, enforce Federal consumer financial law consistently for the purpose of ensuring that markets for consumer financial products and services are fair, transparent, and competitive [Sect. 1021 (a)] Both also envision promotion of efficiency in the operation of markets while allowing [CFRA-H] or facilitating [CFPA-S] innovation. Title X: “The Bureau shall seek to implement and, where applicable, enforce Federal consumer financial law consistently for the purpose of ensuring that all consumers have access to markets for consumer financial products and services and that markets for consumer financial products and services are fair, transparent, and competitive.” [Sect. 1021(a)] Objectives:

- provide timely and understandable information to consumers - protect consumers from unfair, deceptive, or abusive acts or

practices, and from discrimination - cull outmoded or unduly burdensome regulations - provide for regulation according to function rather than

institutional status - promote transparent and efficient operation of markets, while

facilitating access and innovation [Sect. 1021(b)]

{W1842975.3} 16

Agency Powers/Authorities To administer, enforce, and otherwise implement federal consumer protection laws. [Sects. 4202(a) and 1022 (a), respectively] The Agency may develop and implement regulations and issue orders and guidance in support of its purposes and goals. [Sects. 4202(b)(1) and 1022 (b)(1), respectively] The Agency shall consider benefits and costs for consumers and for other affected persons and shall consult with prudential regulators regarding its rulemaking. [Sects. 4202(a)(2) and 1022(b)(2), respectively.] The Agency may, in its rulemaking, exempt otherwise covered persons, service providers, or products or services as appropriate based upon, inter alia, various characteristics such as total assets, transactional volumes, the existence of other applicable laws as may provide consumers with adequate protections, and (in CFPA-H) situations where a covered person engages in 1 or more financial activities. [Sects. 4202(b)(3)(B) and Sect. (b)(3)(B), respectively] Title X: Administer, enforce, and implement the provisions of Federal consumer financial law. [Sect. 1022(a)] Unfair, deceptive or abusive acts or practices. The Agency can bring actions to “prevent a person from committing or engaging in an unfair, deceptive, or abusive act or practice under Federal law in connection with any transaction with a consumer for a consumer

{W1842975.3} 17

financial product or service, or the offering of a consumer financial product or service.” [Sect. 4301(a) and Sect. 1031(a), respectively] The Agency also can prescribe “regulations identifying as unlawful unfair, deceptive, or abusive acts or practices in connection with any transaction with a consumer for a consumer financial product or service of the offering of a consumer financial product or service.” [Sect. 4301(b)(1) and Sect. 1031(b), respectively] CFPA-H defines unfair and deceptive as following the definitions of those terms as established under the FTC Act and the FTC’s various interpretations and policy statements. CFPA-S does not specifically refer to defining ‘deceptive.’ [Sect. 4301(c)(1 and 2) and 1031(c)(1) as regards ‘unfairness’] CFPA-S also provides that in determining ‘unfairness’, the Agency may look to established public policies as evidence to be considered with all other evidence; however, such public policy considerations may not serve as a primary basis for such determination.” [Sect. 1031(c)(2)] CFPA-H allows the Agency to determine an act or practice is abusive, but only if a finding is made that

“(A) the act or practice is reasonably likely to result in a consumer’s inability to understand the terms and conditions of a financial product or service or to protect their own interests in selecting or using a financial product or service; and

(B) the widespread use of the act or practice is reasonably likely to contribute to instability and greater risk in the financial system.” [Sect. 4301(c)(3)]

CFPA-S allows the Agency to determine an act or practice is abusive but only if

“the act or practice—

{W1842975.3} 18

(1) materially interferes with the ability of a consumer to understand a term or condition of a consumer financial product or service; or (2) takes unreasonable advantage of— (A) a lack of understanding on the part of the consumer of the material risks, costs, or conditions of the product or service; (B) the inability of the consumer to protect the interests of the consumer in selecting or using a consumer financial product or service; or (C) the reasonable reliance by the consumer on a covered person to act in the interests of the consumer.” [Sect. 1031(d)]

Title X: Unfairness – limited to instances where the Bureau has a “reasonable basis” finding the act or practice causes or is likely to cause substantial injury to consumer not reasonably avoidable by them, and such injury not outweighed by benefits to consumers or to competition. [Sect. 1031(c)(1)] In so doing, Bureau “may” consider established public policies; however, such policies cannot be a primary basis for Bureau’s determination. [Sect. 1031(c)(2)] Abusive – limited to instances where “the act or practice materially interferes with the ability of a consumer to understand a term or condition of a consumer financial product or service; or, takes unreasonable advantage of…” a lack of understanding, an inability of the consumer to protect self interests in choosing or using a product or service, or the reasonable reliance by the consumer on a covered person to act in the consumer’s interests. [Sect. 1031(d)] Fair Dealing – CFPA-H allows for the promulgation of regulations imposing duties of fair dealing on “covered persons,” their agents or

{W1842975.3} 19

employees, or independent contractors. This can include considerations as to whether (1) a provider is acting in the interest of the consumer; (2) the provider is providing advice to the consumer; (3) the consumer is reasonably and justifiably relying on such advice; and, (4) the benefit to consumers of imposing the duty outweigh its costs. [Sect. 4306(a)(2)]

CFPA-H expressly empowers the Agency to prescribe regulations and issue orders and guidance regarding the manner, settings, and circumstances for the provision of any consumer financial products or services to ensure that the risks, costs, and benefits of the products of services, both initially and over the term of the products or services, are fully and accurately represented to consumers. [Sect. 4303]

Title X does not contain specific provisions regarding the creation of duties of ‘fair dealing.’ [Preemption issues?] Key Definitions [See generally, Sects. 4002 and 1002, respectively]

“consumer” – an individual or an agent, trustee, or representative acting on behalf of an individual Adopted in Title X as is. “consumer financial product or service” – any financial product [CFPA-H] [CFPA-S] “to be used” “offered or provided for use by consumers” for personal, family, or household purposes Senate version adopted in Title X. In addition, it must be a “financial product or service” as defined in Sect. 1002(15).

{W1842975.3} 20

CFPA-H defines “covered person” as any person engaging directly or indirectly in “financial activity.” CFPA-S defines a “covered person” as any person offering a “consumer financial product or service,” including affiliates if acting as a service provider. Senate version adopted in Title X. “financial activity” includes

- deposit taking, money acceptance, or money movement activities

- extending credit and servicing loans - performing appraisals - check cashing and guaranty services - credit reporting-related activities - debt collection - real estate settlement services - leasing or lease brokering activity - investment advising (unless regulated by the CFTC, the

SEC, or a State securities commission - providing educational courses on financial management

matters - credit counseling, tax planning (excluding return

preparations) - debt management or settlement, or mortgage foreclosure

services - certain financial data processing activities CFPA-S also explicitly enumerates selling, providing or issuing stored value or payments instruments where the seller exercises substantial control over the terms or conditions of the stored value. Title X adopts a definition of “financial product or service.” [Sect. 1002(15)] A person (or its affiliate acting as a service

{W1842975.3} 21

provider) is a “covered person” where it engages in offering or providing such a product or service. These include: - extending credit or servicing loans, including brokering,

acquiring, and purchasing - extending or brokering leases of property that are the

functional equivalent of purchase finance arrangements - providing real estate settlement purposes - performing appraisal services - engaging in deposit-taking, transmission of funds, acting

as a custodian or funds or financial instruments - selling, providing, or issuing stored value or payment

instruments (seller must exercise substantial control over terms or conditions)

- providing check cashing, collection or guaranty services - providing payments or financial data processing services

(exclusion where involvement limited to being paid by such means)

- providing financial advisory services (exceptions if subject to SEC or State Securities Commission regulation)

- credit counseling, debt management or settlement, credit modifications, and foreclosure avoidance services

- most consumer reporting activities - debt collection

Excluded is the business of insurance. Under CFPA-H, electronic data transmission, routing, storage, or network connection services are also excluded insofar as service provision is concerned.

Title X provides for supervision of nondepository covered persons under certain circumstances. [Sect. 1024] This includes:

{W1842975.3} 22

- persons offering or providing consumer purpose, real estate-secured loans, loan modifications, or foreclosure relief services

- “a larger participant of a market for other consumer financial products or services” as defined by rule; rule development to be in accord with Agency consultations with the FTC as to identity of such persons

- persons engaging in conduct posing risks to consumers with regard to consumer financial products or services

- offering or providing any private education loan - offering or providing a payday loan.

Exclusions – Title X excludes the business of insurance and electronic conduit services.

Statutory Enforcement – “Enumerated Consumer Laws” [Sect. 4002(16) and 1002(11), respectively] The Agency is specifically charged to exercise, among other things, the authorities transferred to it under the “enumerated consumer laws.” Under CFPA-H, these include inter alia:

- AMTPA - EFT Act - ECOA - FCRA - FDCPA - GLB (privacy provisions) - HMDA - RESPA - TILA - Truth in Savings

{W1842975.3} 23

CFPA-S also specifically lists

- Consumer Leasing - HOEPA - Fair Credit Billing

Title X adopts all of the above, plus selected sections from the FDIC Act, the SAFE Mortgage Licensing Act , and the Interstate Land Sales Full Disclosure Act. Model Forms – the Bureau may provide model forms in any final rule requiring disclosures; the use of such forms constitutes a safe harbor. [Sect. 1032(b)] A single, integrated disclosure for mortgage loan transactions shall be developed, combining TILA and RESPA requirements within 1 year of enactment, unless the FED and the HUD Secretary do so first.

{W1842975.3} 24

Exemptions and Exclusions A number of parties are specifically exempted from the coverage of the establishing legislation, either in whole by virtue of what they are, or for certain purposes by virtue of what they do. Additionally, there are specific activities or actions that are expressly excluded from the Agency’s authority. Party Exemptions

- credit by a retailer enabling the consumer to purchase from that retailer where the debt is not sold to another [Sect. 4205(a)(1) and 1027(a)(1)]

- debt collection efforts by such a retailer (NB: exclusion is not transferable)

- entities regulated by other federal agencies - real estate brokers and agents - lawyers engaged in the practice of law:

o FCPA-H: included where providing certain foreclosure prevention services

- Manufactured/mobile homes – agents acting as a broker for a buyer or seller

- Small banks, thrifts, and credit unions with less that $10 Billion in assets will be subject only to relatively limited involvement with the Agency as respects examinations or certain reporting requirements [Sect. 4203(a)(2) and Sect. 1026]; the FDIC or the NCUA would examine these FIs for purposes of compliance with Agency regulations, with limited Agency involvement

- FCPA-S: Small businesses (per SBA standards) that extend and retain credit for sale of nonfinancial goods or services [sect. 1027(a)(2)(D)(ii)]

{W1842975.3} 25

- FCPA-H: pawnbrokers [Sect. 4205(o)] - FCPA-H: credit reporting agencies to the extent they

furnish a consumer report they believe will be used for employment purposes, government licensing, or evaluating a consumer’s residential or tenancy history [Sect. 4205(p)]

- FCPA-H: auto dealers except where the dealer operates so as to extend credit or engage in leasing regarding motor vehicles and does not routinely assign the debt to a 3rd party [Sect. 4205(k)]

{W1842975.3} 26

Title X provides EXCLUSIONS for certain merchants, retailers, and sellers of nonfinancial goods or services. [Sect. 1027] These exclusions are characterized based upon the activity engaged in.

- credit by a retailer enabling the consumer to purchase from that retailer where the debt is not sold to another

- subject to Bureau where offering or providing consumer financial product or service or is otherwise subject to an enumerated consumer law.

- such retailers excluded where not engaged

“significantly” in offering consumer financial products or services

- Small businesses (per SBA standards) that extend and retain credit for sale of nonfinancial goods or services

- real estate brokers or agents

- Manufactured/mobile homes – agents acting as a broker for a buyer or seller - Accountants and Tax Preparers - Practitioners engaged in the Practice of Law - Persons Regulated by a State Insurance Regulator

- Persons Regulated by a State Securities Commission - Persons Regulated by the CFTC

{W1842975.3} 27

- Persons Regulated by the Farm Credit Administration - Insurance Title X provides an exclusion for auto dealers. [Sect. 1029] Where a contract is offered in connection with a line of business of the dealer providing for extensions of retail credit or retail leases that is not routinely assigned to an unaffiliated third party financing or leasing source, the Bureau would retain the authority to oversee such entity.

Specific activity restrictions: - the Agency cannot impose usury limits - FCPA-H: the Agency cannot require a covered person to

offer a specific financial product or service (i.e., cannot require the offering of ‘plain vanilla’ products)

- the Agency cannot create private causes of action to enforce statutory rights (although existing private causes of action are unaffected)

Title X provides that the Bureau has no authority to impose a usury limit. [Sect. 1027 (o)] Class Exemptions [Sect. 1022]: The Bureau may exempt classes of covered persons, service providers, or specific consumer financial products or services from any provision of Title X or any rule issued thereunder. In issuing conditional or unconditional exemptions, the Bureau shall consider, inter alia,

{W1842975.3} 28

- the total assets of the class of covered persons - the volume of transactions of the class - the existence of other laws that may provide consumers

with adequate protections [Sect. 1022(a)(3)(A) + (B)]

Deference – deference a Court affords to a Bureau determination to be applied as if Bureau were only agency addressing such issue [Sect. 1022(a)(4)(B)]

{W1842975.3} 29

ABA Annual Meeting San Francisco, CA Program on Regulatory Reset: Consumer Financial Services August 7, 2010

Bureau of Consumer Financial Protection - Organization, Governance, Funding, Transition

Joel Winston1

Associate Director, Division of Financial Practices Federal Trade Commission

Washington, DC

I. Organization of the Bureau of Consumer Financial Protection

• The bill establishes a Bureau of Consumer Financial Protection ("Bureau") in the Federal Reserve System to regulate the offering and provision of consumer financial products or services. Sec. 11 01 (a) (cites are to the conference report on the Consumer Financial Protection Act of 2010 ("CFPA")). • The CFPA mandates specific functional units, including research, community affairs, complaint tracking, fair lending & equal opportunity, financial literacy, service member affairs, and financial protection for older Americans. Sec. 1013(b).

II. Governance

• The President appoints a Director, who must be confirmed by the Senate and serves a 5-year term. Sec. 1101(b-c). • The Director appoints a Deputy Director, who serves as acting Director in the absence or unavailability of the Director. Sec. 1101(b)(5). • The Board of Governors of the Federal Reserve may not intervene in Bureau matters, including recommendations and testimony to Congress. Sec. 1012(c). • On the petition of a member agency of the Financial Stability Oversight Council, the Council may set aside a final regulation prescribed by the Bureau, if it determines that the regulation would put the safety and soundness of the banking system or the stability of the financial system at risk. Sec. 1023. • The Director must establish a Consumer Advisory Board to advise and consult with the Bureau in the exercise of its functions under the consumer financial laws and to provide

1 This outline was prepared July 1, 2010, immediately after the House and Senate conference report. It does not reflect later changes, if any. The statements contained in this outline and my remarks are mine only, and do not represent the views of the Federal Trade Commission or any individual Commissioner.

{W1842975.3} 30

information on emerging practices in the consumer financial products or services industry, including regional trends and concerns. Sec. 1014(a).

III. Funding

• All funding comes from the combined earnings of the Federal Reserve System. Sec. 1017(a). • The funding amount is the amount that the Director determines to be reasonably necessary to carry out the Bureau's authorities under Federal consumer financial law, not to exceed 12% of the Federal Reserve System's total operating expenses (after a phase-in period in 2011-12 in which the amount cannot exceed 10-11 % of expenses). Sec. 1017.

IV. Transition

• Within 60 days after enactment, the Treasury Secretary, in consultation with other agencies, must designate a date for the transfer of functions to the Bureau. The date must be between six and twelve months from date of enactment; the bill also provides for extensions of time. Sec. 1062. • After the date of enactment and until the designated transfer date, the Board of Governors is required to transfer to the Bureau the amount of funds, estimated by the Secretary, needed to carry out the Bureau's authorities. Sec. 1017(a)(3).

V. FTC Role

• The Bureau and the FTC have concurrent enforcement authority over many nondepository institutions. The agencies are required to negotiate an agreement for coordinating enforcement actions with respect to mortgage-related companies and so-called larger entities, as defined by the Bureau, that are nondepositories. Sec. 1024(c)(3). • The FTC will have the authority to enforce Bureau rules prescribed under Title X. Sec. 1061 (b)(5)(C). • The Bureau has exclusive authority to issue regulations or guidance, to the extent that the Bureau and the FTC are authorized to do so under specific statutes. The FTC retains its FTC Act rulemaking authority under the "Magnuson-Moss" procedures. Sec. 1024(d); Sec. 1061(b)(5)(B). The Bureau and the FTC also must negotiate an agreement related to rulemaking to avoid duplication of, or conflict between, rules. Sec. 1061(b)(5)(D). • Congress had considered, but declined to include in the conference report, additional powers for the FTC (notice and comment rulemaking authority for FTC Act rulemaking, civil penalties for FTC Act violations, and aiding & abetting authority for FTC Act violations). The bill provides the FTC notice and comment rulemaking authority with respect to auto dealers. Sec. 1029(d).

{W1842975.3} 31

ABA Annual Meeting San Francisco, California

Program on Regulatory Reset: Consumer Financial Services August 7, 2010

Bureau of Consumer Financial Protection Supervision and Enforcement

Heather Koenig

Associate General Counsel Bank of America, Charlotte, North Carolina

I. Bureau of Consumer Financial Protection

A. CFPB will have primary rulemaking, supervisory and enforcement authority over consumer financial products and services.

B. Director will be appointed by President to serve a five year term. C. Dedicated budget paid by the Federal Reserve System D. Bureau will be autonomous and have very broad jurisdiction over almost all

entities that offer consumer financial products or services. Board of Governors may not intervene in any matter or proceeding before the Director. Rules or orders of the CFPB will not be subject to review or approval by the Board.

II. Supervision A. There will be three categories of supervision by the CFPB:

1. Large insured depository institutions 2. Smaller depository institutions 3. Nondepository institutions

B. Large insured depository institutions 1. Defined as an insured depository institution or insured credit union with

total assets of more than $10 billion and any affiliate of such institution (except exempted entities, such as insurance companies)

2. CFPB will have exclusive rulemaking and examination authority over these large depository institutions

3. CFPB will conduct periodic exams in coordination with federal and state agencies

4. Draft exam reports will be shared between the federal agencies and the CFPB

5. Large depository institutions will be permitted to appeal in the event of a conflict between supervisors

C. Smaller depository institutions

{W1842975.3} 32

1. Defined as an insured depository institution or insured credit union with total assets of $10 billion or less and any affiliate of such institution (except exempted entities, such as insurance companies)

2. Prudential regulator will retain examination authority 3. CFPB could require reports in addition to using existing reports 4. CFPB could participate in exams on a “sampling basis” where the prudential

regulator will be required to a. Provide exam related materials to the CFPB b. Involve the CFPB examiner in the entire exam process; and c. Consider the CFPB’s input regarding the scope and conduct of the

exam as well as the contents of the Report of Examination and the exam ratings

D. Nondepository Institutions 1. Definition includes:

a. originators, brokers, or servicers of real estate secured loans b. “larger participants” of a market for other consumer financial products

or services as defined by the CFPB within one year and after consultation with the FTC

c. entities that the CFPB has reasonable cause to determine are engaging, or have engaged, in conduct that poses risks to consumers with regard to the offering or provision of consumer financial products or services

d. entities that offer or provide private education loans e. payday lenders

2. CFPB will have the ability to examine institutions in (a) through (e) above 3. CFPB will conduct periodic exams in coordination with federal and state

agencies 4. CFPB will establish a supervision program based on the risk posed to

consumers of financial products and services 5. CFPB will establish registration requirements, reporting requirements and

examination standards for nonbanks III. Enforcement

A. CFPB will have broad administrative enforcement authority that is broader than normal banking agency administrative authorities and will include: 1. Authority to grant orders to pay damages (excluding exemplary and punitive

damages) 2. Recovery of costs from covered institutions by CFPB, State AGs or state

regulators to enforce any Federal consumer financial law

{W1842975.3} 33

B. When commencing a civil action under Federal consumer financial law, the CFPB will provide notice to DOJ and also to the appropriate prudential regulator for insured depository institutions or insured credit unions

C. CFPB will refer potential Federal criminal violations to DOJ D. Like Supervision, there will be three categories of enforcement by the CFPB:

1. Large insured depository institutions 2. Smaller depository institutions 3. Nondepository institutions

E. Large insured depository institutions 1. CFPB will have primary enforcement authority 2. Any Federal agency, other than the FTC, authorized to enforce a Federal

consumer financial law may recommend that the CFPB initiate enforcement action against a covered institution

a. CFPB has 120 days to initiate an enforcement action based on a referral from another Federal agency

b. If CFPB does not take action within 120 day, the referring agency may initiate an enforcement proceeding

F. Smaller depository institutions 1. Prudential regulator will retain exclusive enforcement authority 2. CFPB will have ability to refer potential violations to prudential regulator

G. Nondepository institutions 1. CFPB will have exclusive enforcement authority 2. Any Federal agency authorized to enforce a Federal consumer financial law may

recommend that the CFPB initiate enforcement action against a covered institution

3. CFPB and FTC will within six months negotiate an agreement for coordinating with respect to enforcement actions

{W1842975.3} 34

ABA Annual Meeting San Francisco, CA

Program on Regulatory Reset: Consumer Financial Services

August 7, 20102

Preemption

Roland E. Brandel Morrison & Foerster, LLP

San Francisco, CA

I. THE BIG PICTURE

A. The Legal Foundation for Uniform National Rules – the Supremacy Clause of the

U.S. Constitution:

“This Constitution, and the Laws of the United States . . . shall be the

supreme Law of the Land; and the Judges in every State shall be bound

thereby, any Thing in the Constitution or Laws of any State to the Contrary

notwithstanding. (Const., art. VI, cl. 2).”

B. The doctrines under which the Supremacy Clause is implemented

1. Express or implied preemption;

2. Field preemption;

3. Conflict preemption;

II. PREEMPTION IN EXISTING STATUTES OF GENERAL APPLICATION

A. Consumer Financial Protection Act of 2010 (“CFPA”), Section 1041(b) locks in

the preemption principles contained in existing statutes:

2 This outline was prepared July 1, 2010 immediately after the House and Senate conference reported on the CFPA to the Congress. It was accurate as of July 1, 2010, but does not reflect later changes, if any.

{W1842975.3} 35

“RELATION TO OTHER PROVISIONS OF ENUMERATED CONSUMER LAWS THAT

RELATE TO STATE LAW. – No provision of this title, except as provided in section

1083, shall be construed as modifying, limiting, or superseding the operation of

any provision of an enumerated consumer law that relates to the application of a

law in effect in any State with respect to such Federal law.”

B. “Enumerated consumer laws” are defined in Section 1002(12) in a list of all or

part of federal statutes that cover consumer financial services.

C. The existing principles are quite inconsistent, sometimes within a single statute.

D. Examples of explicit “relation to state laws” provisions in financial services related

federal statutes.

1. No impact on state law unless inconsistent (general TILA rule, Reg Z

§ 226.28(a)(1));

2. State law not deemed inconsistent if it is more protective of consumers

(Reg E, § 205.12(b)); GLB Privacy Act (Reg P, § 216.17(b)): concept of

federal minimum floor of consumer protection;

3. State law is preempted if “rights, responsibilities or procedures . . . are

different from those required by federal law” (TILA re billing error

correction, Reg Z, § 226.28(a)(2)(i)) and “state law requirements relating

to [disclosures on credit card applications or solicitations] . . . are

preempted.” (15 USC 1610(e) (1988); Reg Z, § 226.28(d)) (1989);

4. The Fair and Accurate Credit Transactions Act of 2003 (“FACT Act”)

amendments to the FCRA reauthorized seven 1996 preemption

provisions to the FCRA and added sixteen additional national uniformity

or preemption provisions; and

E. Absent an explicit Congressional directive to the contrary, the preemption

standards for post-CFPA laws are:

{W1842975.3} 36

1. State law is preempted only if it is inconsistent and then only to the extent

of the inconsistency (Section 1041(a)(1));

2. State law is not inconsistent if it affords to consumers greater protection

(Section 1041(a)(2);

F. Who decides preemption issues?

1. Usually, Congress and the courts; but

2. Sometimes federal agencies have been delegated by Congress with the

power to make preemption determinations as a result of explicit statutory

authority (e.g., see FTC re Privacy Act questions concerning whether a

state law is more protective of consumers (Reg P, § 216.17(b)) and

Federal Reserve Board re TILA (Reg Z § 226.28(a), (b), (c)).

3. Those existing limited powers contained in specific consumer protection

legislation will be transferred to the Bureau;

4. Additionally, the Bureau is given the general power to determine whether

a State law is “inconsistent.” Section 1041(a)(2);

III. CHARTER (NATIONAL BANKS, FEDERAL SAVINGS ASSOCIATIONS) BASED PREEMPTION-

SUBSTANTIVE PROTECTIONS

A. State consumer financial laws are preempted only if (Section 1044 (b); Section

1046):

1. there is a discriminatory effect on federally chartered FIs or;

2. applying the test of Barnett Bank v. Nelson, 517 U.S. 25 (1996) would

result in preemption or;

3. application of some other Federal law results in preemption

B. Note, Congress inserted last minute language giving its interpretation of the

Barnett standard: preemption occurs if “the State consumer financial law

{W1842975.3} 37

prevents or significantly interferes with the exercise by the national bank of its

powers; . . . “

C. Note the absence of an explicit “safe harbor” provision to protect banks that have

relied on an OCC preemption determination.

D. Subsidiaries or affiliates of nationally chartered FIs will not receive charter-based

preemption protections (overturning the result in Watters v. Wachovia Bank, 550

U.S. 1 (2007)) (Sections 1044(b)(2); 1044(e)).

C. A preemption determination may be made by a court or the OCC “on a case-by-

case basis.” Section 1044(b)(1)(B).

D. OCC must consult the Bureau in some “case-by-case” determinations (Section

1044(b)(3)(B)).

E. There are requirements of substantial evidence on the record to support an OCC

preemption finding (Section 1044(c)).

F. OCC must conduct periodic “public” reviews of preemption determinations

(Section 1044(d)(1)) and report to Congress (Section 1044(d)(2)).

IV. CHARTER (NATIONAL BANKS) BASED PREEMPTION – ENFORCEMENT AUTHORITY

A. State attorney generals may sue federally chartered FIs to enforce the CFPA in

some circumstances. (Section 1042(a)(2).

B. State regulators may sue State – chartered, or authorized to do business,

persons.

C. Limitations on the visitorial power of states regarding federally chartered FIs do

not restrict the power of state attorney generals to sue such FIs (Section 1047(a),

citing the 2009 decision of the U.S. Supreme Court in Cuomo v. Clearing House

Assn.)

{W1842975.3} 38

V. GRANDFATHER/TRANSITIONAL RULE REGARDING CONTRACTS ENTERED INTO BY

FEDERALLY CHARTERED FIS (SECTION 1043)

A. If a contract is entered into prior to enactment of the CFPA,

B. Parties can rely on the preemption interpretations of the OCC or OTS in spite of

Bureau promulgations.

VI. RATE LIMITS

A. The Bureau is prohibited from establishing usury limits generally. (Section

1027(o)).

B. The CFPA does not affect the authority conferred by 12 U.S.C. 85 “for the

charging of interest by a national bank . . . , including with respect to the

meaning of ‘interest’ under such provisions” (Section 1044(f)).

C. Preemption regarding interest limits through parity:

1. Congress determined in 1864 as part of the National Bank Act that it

would not preempt the ability of states to impose interest rate limits on

national banks (12 U.S.C. 85). Rather, the NBA demanded parity for

national banks with rate caps applied to other lenders. Tiffany v National

Bank of Missouri, 85 U.S. 409 (1873).

2. More than a century later, the U.S. Supreme Court determined that a

national bank could “export” a favorable interest rate from the state in

which it was located to any other state. Marquette National Bank v First

of Omaha Service Corp., 439 U.S. 29 (1978).

3. Over the next decades the concept of what constitutes “interest”

expanded to include most charges levied in a credit extension via “home

state” state legislative actions and OCC interpretations.

{W1842975.3} 39

4. The result – a uniform standard nationally for any given national bank.

Each bank need only look to the state law where it is “located.” Other

states cannot regulate such charges by imposing their laws.

VII. A NEW POWER OF STATES TO MANDATE COMMENCEMENT OF BUREAU RULEMAKING

A. If “a majority of the Sates has enacted a resolution“ that supports rulemaking

(Section 1041(c)(1).

B. The Bureau will:

1. commence a rulemaking procedure (Section 1041(c)(1);

2. apply Congressionally mandated criteria that the Bureau must “take into

account” (Section 1041(c)(2)

a. does it afford greater protection?

b. do a cost-benefit analysis

c. inquire whether it would “discriminate unfairly” against some

consumers

d. if a Federal banking agency advises that it is likely to present an

“unacceptable safety and soundness risk to insured depository

institutions”

VIII. GOVERNMENT INTERVENTION REGARDING INTERCHANGE FEES (DURBIN AMENDMENT

SECTION 1076)

A. Authorizes the Federal Reserve Board (not the Bureau) to establish rules

regarding interchange fees for electronic debit transactions.

B. Interchange fees must be “reasonable and proportional to the actual cost

incurred”.

C. Small issuers (assets less than $10 billion) are exempt.

{W1842975.3} 40

D. Prepaid government benefit cards and most other prepaid cards are exempt.

E. Merchants may offer discounts for payment types (e.g. credit card, debit card, check or cash).

{W1842975.3} 41

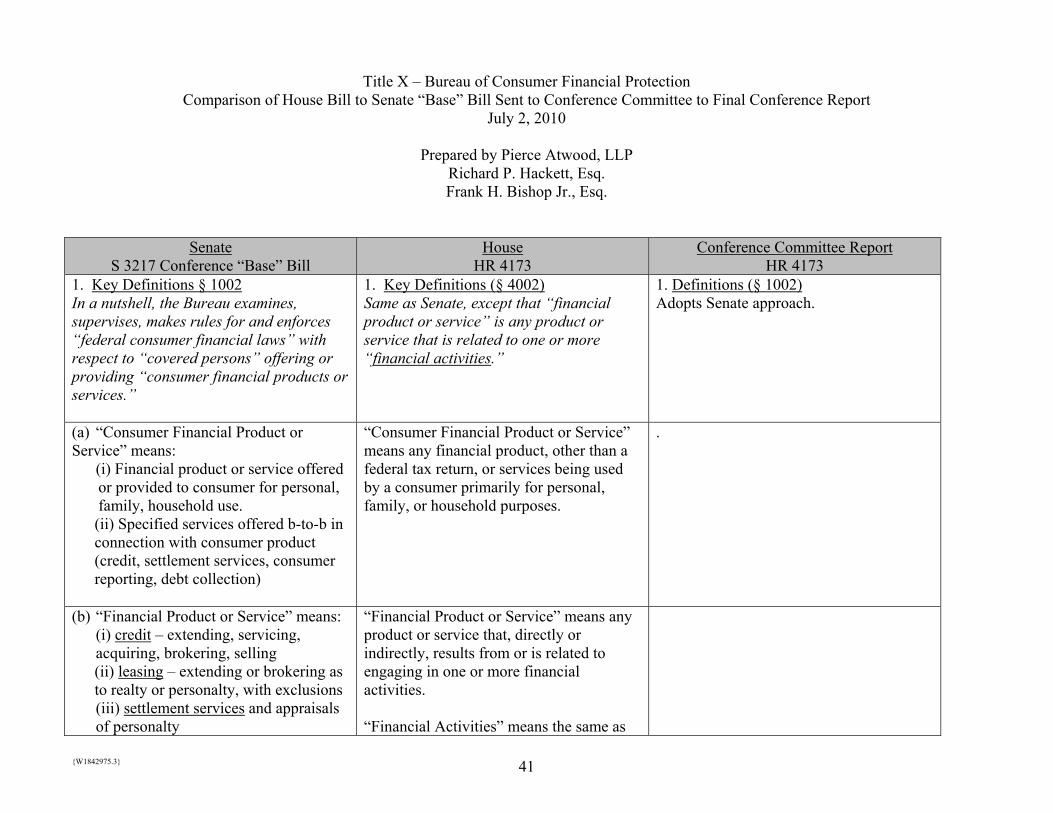

Title X – Bureau of Consumer Financial Protection Comparison of House Bill to Senate “Base” Bill Sent to Conference Committee to Final Conference Report

July 2, 2010

Prepared by Pierce Atwood, LLP Richard P. Hackett, Esq. Frank H. Bishop Jr., Esq.

Senate S 3217 Conference “Base” Bill

House HR 4173

Conference Committee Report HR 4173

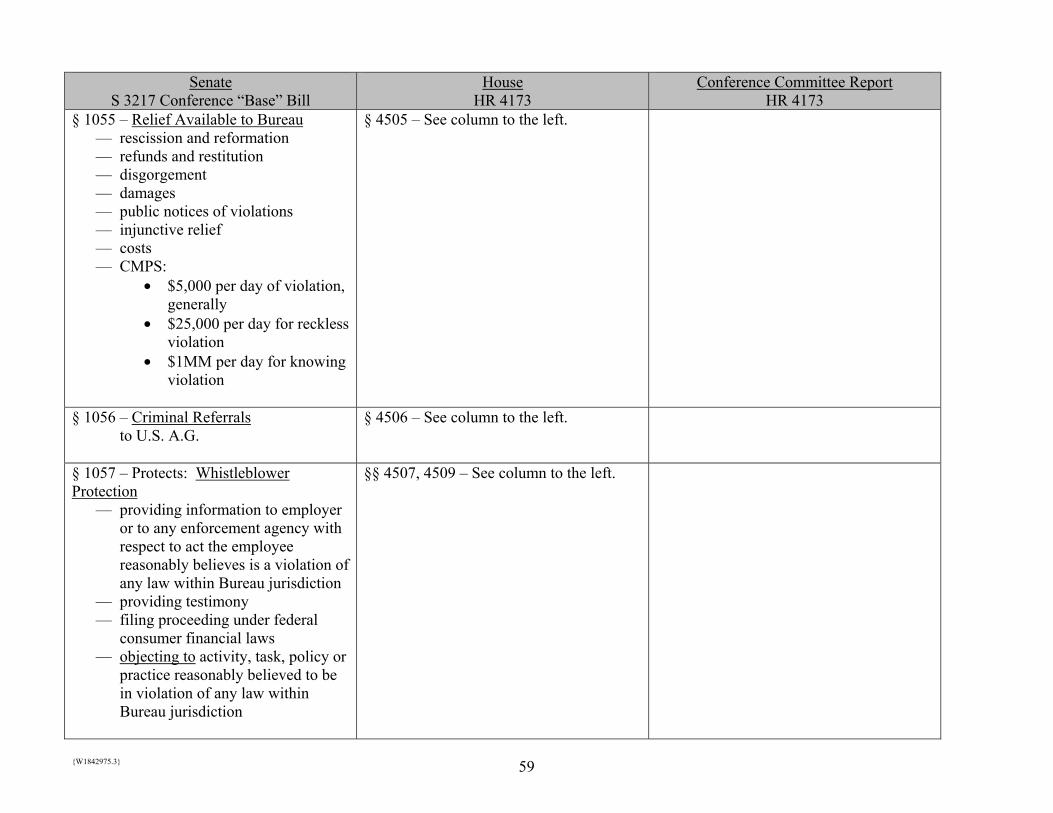

1. Key Definitions § 1002 In a nutshell, the Bureau examines, supervises, makes rules for and enforces “federal consumer financial laws” with respect to “covered persons” offering or providing “consumer financial products or services.”

1. Key Definitions (§ 4002) Same as Senate, except that “financial product or service” is any product or service that is related to one or more “financial activities.”

1. Definitions (§ 1002) Adopts Senate approach.

(a) “Consumer Financial Product or Service” means: (i) Financial product or service offered

or provided to consumer for personal, family, household use.

(ii) Specified services offered b-to-b in connection with consumer product (credit, settlement services, consumer reporting, debt collection)

“Consumer Financial Product or Service” means any financial product, other than a federal tax return, or services being used by a consumer primarily for personal, family, or household purposes.

.

(b) “Financial Product or Service” means: (i) credit – extending, servicing, acquiring, brokering, selling (ii) leasing – extending or brokering as

to realty or personalty, with exclusions (iii) settlement services and appraisals of personalty

“Financial Product or Service” means any product or service that, directly or indirectly, results from or is related to engaging in one or more financial activities. “Financial Activities” means the same as

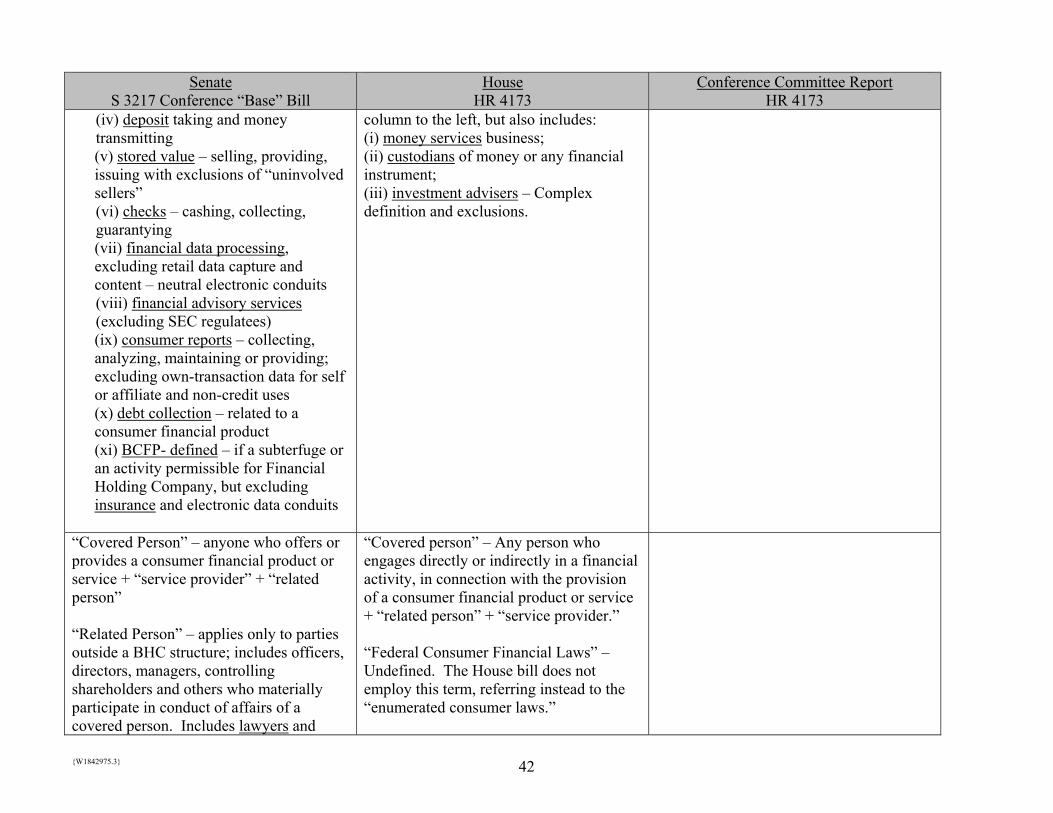

{W1842975.3} 42

Senate S 3217 Conference “Base” Bill

House HR 4173

Conference Committee Report HR 4173

(iv) deposit taking and money transmitting (v) stored value – selling, providing,

issuing with exclusions of “uninvolved sellers”

(vi) checks – cashing, collecting, guarantying (vii) financial data processing,

excluding retail data capture and content – neutral electronic conduits

(viii) financial advisory services (excluding SEC regulatees)

(ix) consumer reports – collecting, analyzing, maintaining or providing; excluding own-transaction data for self or affiliate and non-credit uses (x) debt collection – related to a consumer financial product (xi) BCFP- defined – if a subterfuge or an activity permissible for Financial Holding Company, but excluding insurance and electronic data conduits

column to the left, but also includes: (i) money services business; (ii) custodians of money or any financial instrument; (iii) investment advisers – Complex definition and exclusions.

“Covered Person” – anyone who offers or provides a consumer financial product or service + “service provider” + “related person” “Related Person” – applies only to parties outside a BHC structure; includes officers, directors, managers, controlling shareholders and others who materially participate in conduct of affairs of a covered person. Includes lawyers and

“Covered person” – Any person who engages directly or indirectly in a financial activity, in connection with the provision of a consumer financial product or service + “related person” + “service provider.” “Federal Consumer Financial Laws” – Undefined. The House bill does not employ this term, referring instead to the “enumerated consumer laws.”

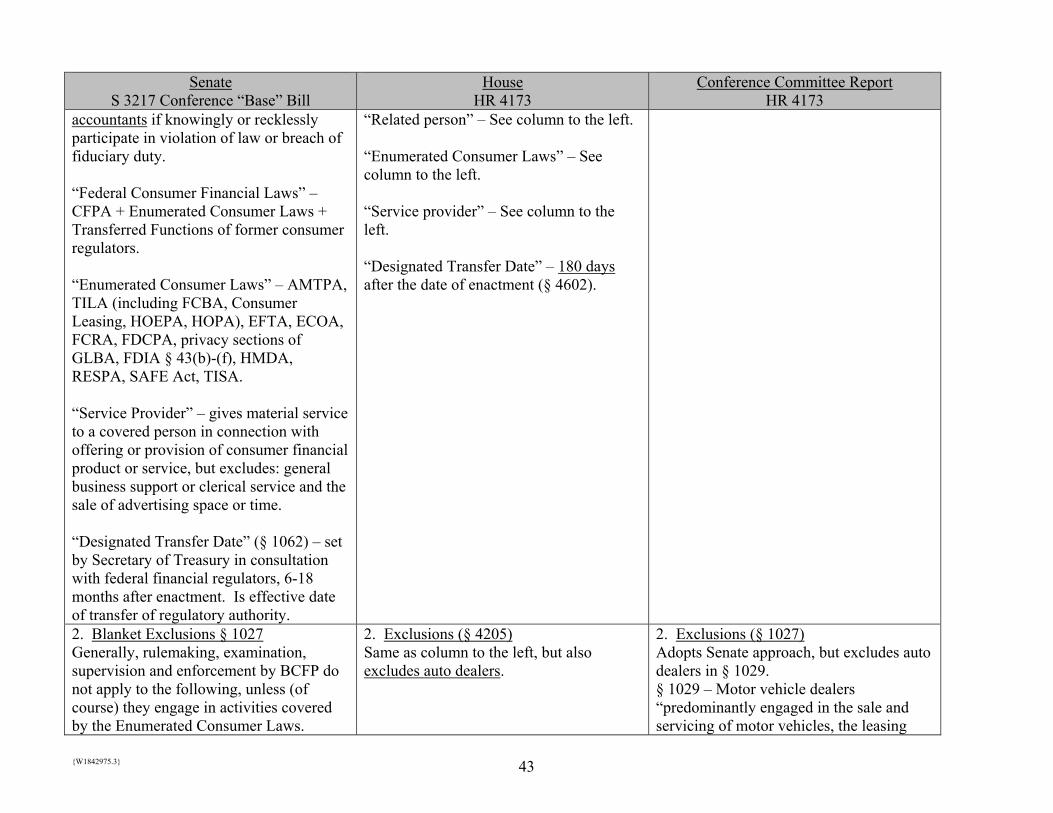

{W1842975.3} 43

Senate S 3217 Conference “Base” Bill

House HR 4173

Conference Committee Report HR 4173

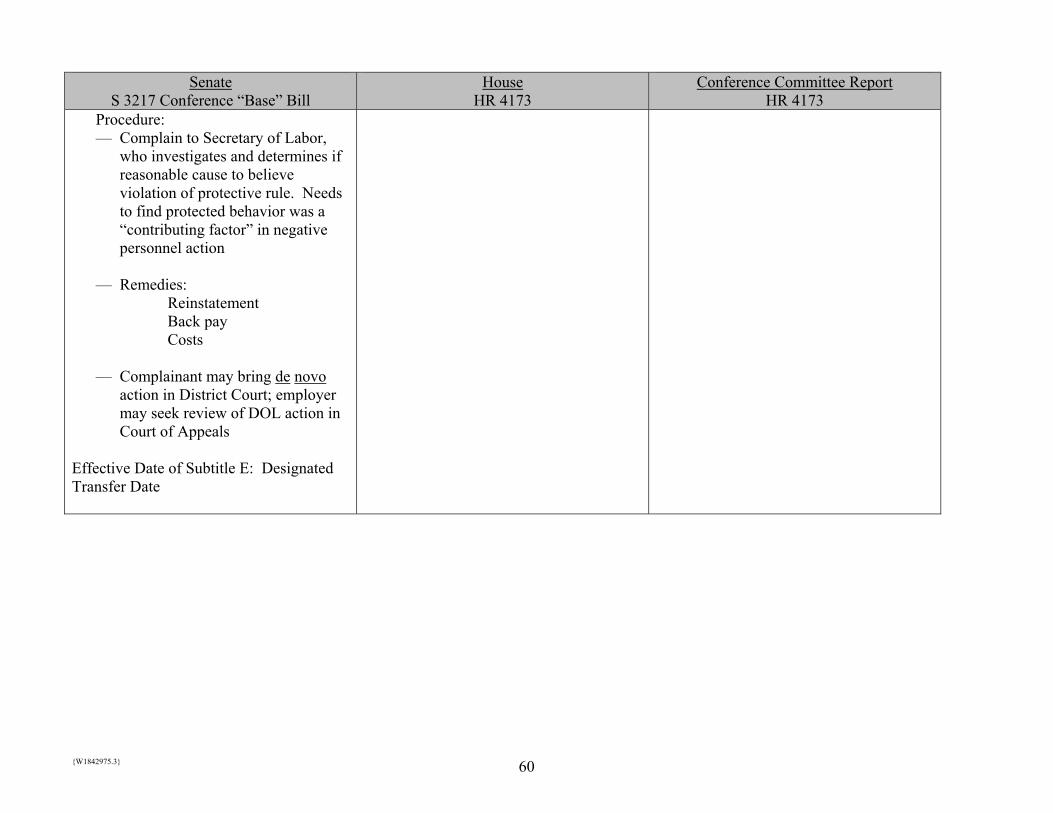

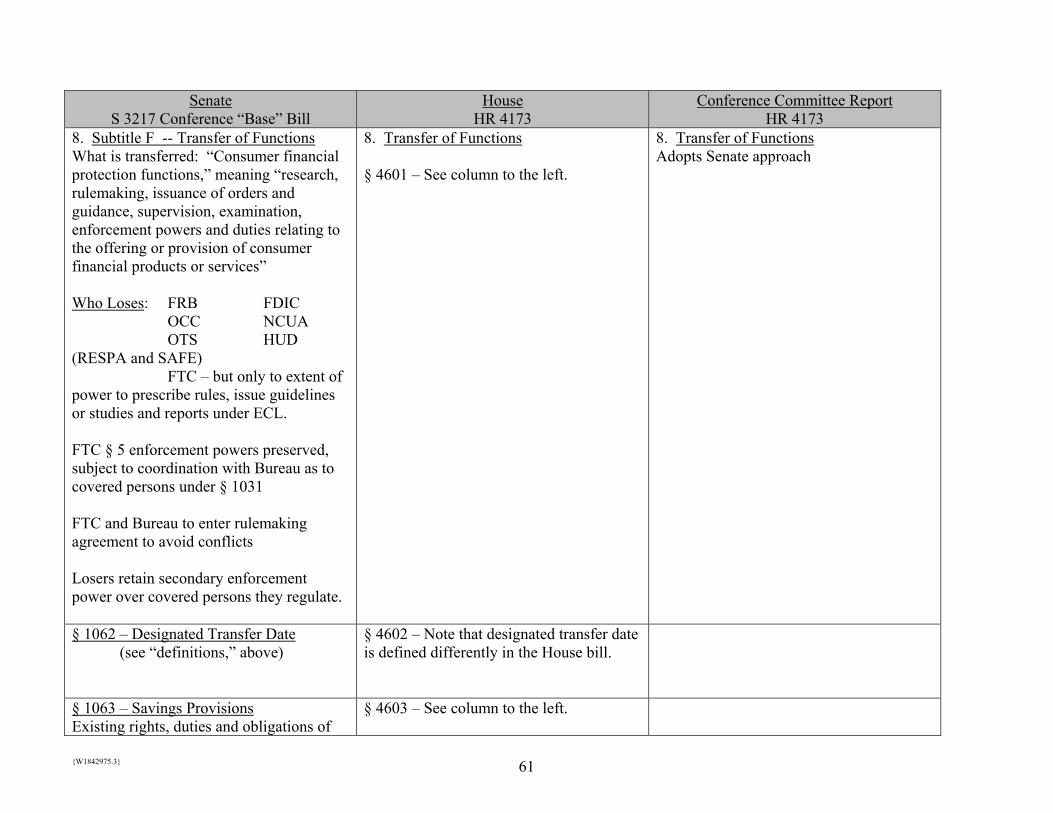

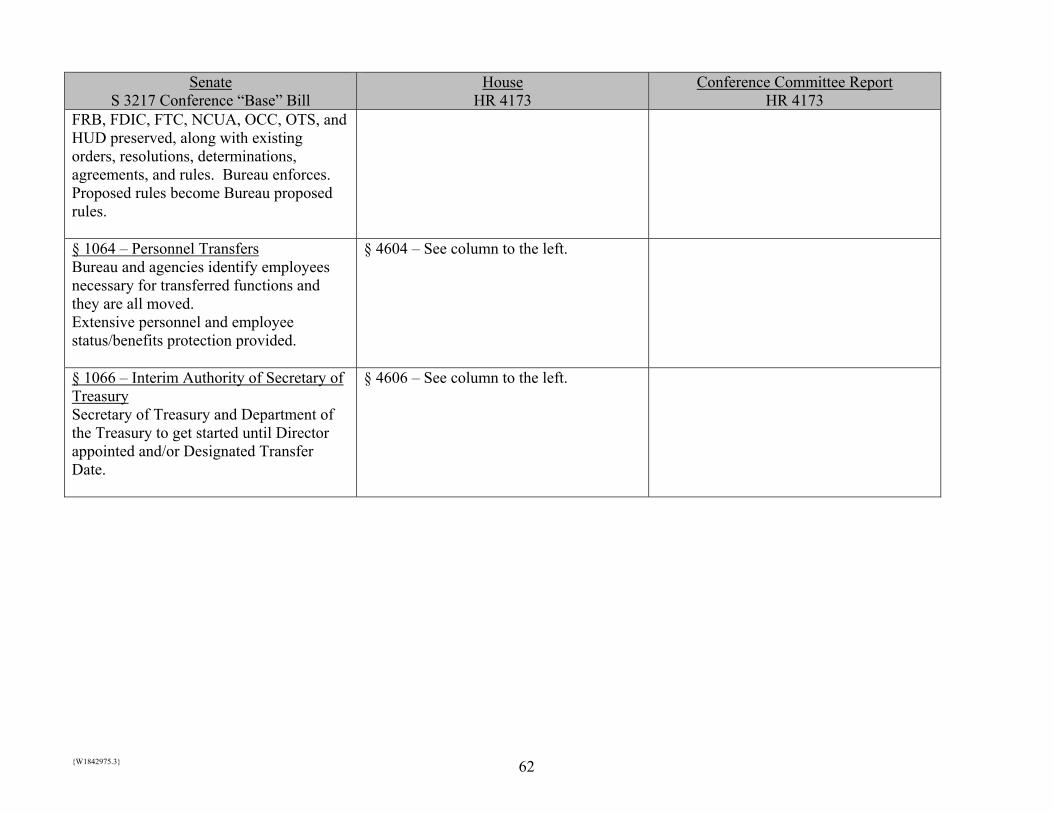

accountants if knowingly or recklessly participate in violation of law or breach of fiduciary duty. “Federal Consumer Financial Laws” – CFPA + Enumerated Consumer Laws + Transferred Functions of former consumer regulators. “Enumerated Consumer Laws” – AMTPA, TILA (including FCBA, Consumer Leasing, HOEPA, HOPA), EFTA, ECOA, FCRA, FDCPA, privacy sections of GLBA, FDIA § 43(b)-(f), HMDA, RESPA, SAFE Act, TISA. “Service Provider” – gives material service to a covered person in connection with offering or provision of consumer financial product or service, but excludes: general business support or clerical service and the sale of advertising space or time. “Designated Transfer Date” (§ 1062) – set by Secretary of Treasury in consultation with federal financial regulators, 6-18 months after enactment. Is effective date of transfer of regulatory authority.

“Related person” – See column to the left. “Enumerated Consumer Laws” – See column to the left. “Service provider” – See column to the left. “Designated Transfer Date” – 180 days after the date of enactment (§ 4602).

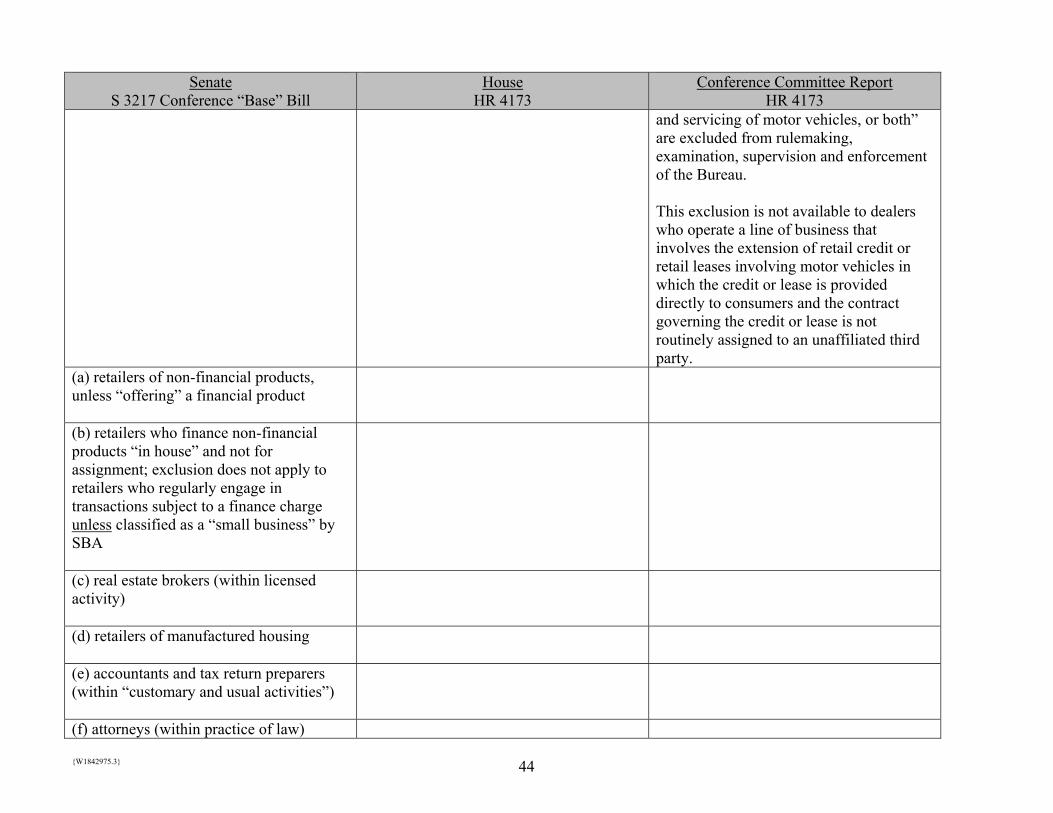

2. Blanket Exclusions § 1027 Generally, rulemaking, examination, supervision and enforcement by BCFP do not apply to the following, unless (of course) they engage in activities covered by the Enumerated Consumer Laws.

2. Exclusions (§ 4205) Same as column to the left, but also excludes auto dealers.

2. Exclusions (§ 1027) Adopts Senate approach, but excludes auto dealers in § 1029. § 1029 – Motor vehicle dealers “predominantly engaged in the sale and servicing of motor vehicles, the leasing

{W1842975.3} 44

Senate S 3217 Conference “Base” Bill

House HR 4173

Conference Committee Report HR 4173

and servicing of motor vehicles, or both” are excluded from rulemaking, examination, supervision and enforcement of the Bureau. This exclusion is not available to dealers who operate a line of business that involves the extension of retail credit or retail leases involving motor vehicles in which the credit or lease is provided directly to consumers and the contract governing the credit or lease is not routinely assigned to an unaffiliated third party.

(a) retailers of non-financial products, unless “offering” a financial product

(b) retailers who finance non-financial products “in house” and not for assignment; exclusion does not apply to retailers who regularly engage in transactions subject to a finance charge unless classified as a “small business” by SBA

(c) real estate brokers (within licensed activity)

(d) retailers of manufactured housing

(e) accountants and tax return preparers (within “customary and usual activities”)

(f) attorneys (within practice of law)

{W1842975.3} 45

Senate S 3217 Conference “Base” Bill

House HR 4173

Conference Committee Report HR 4173

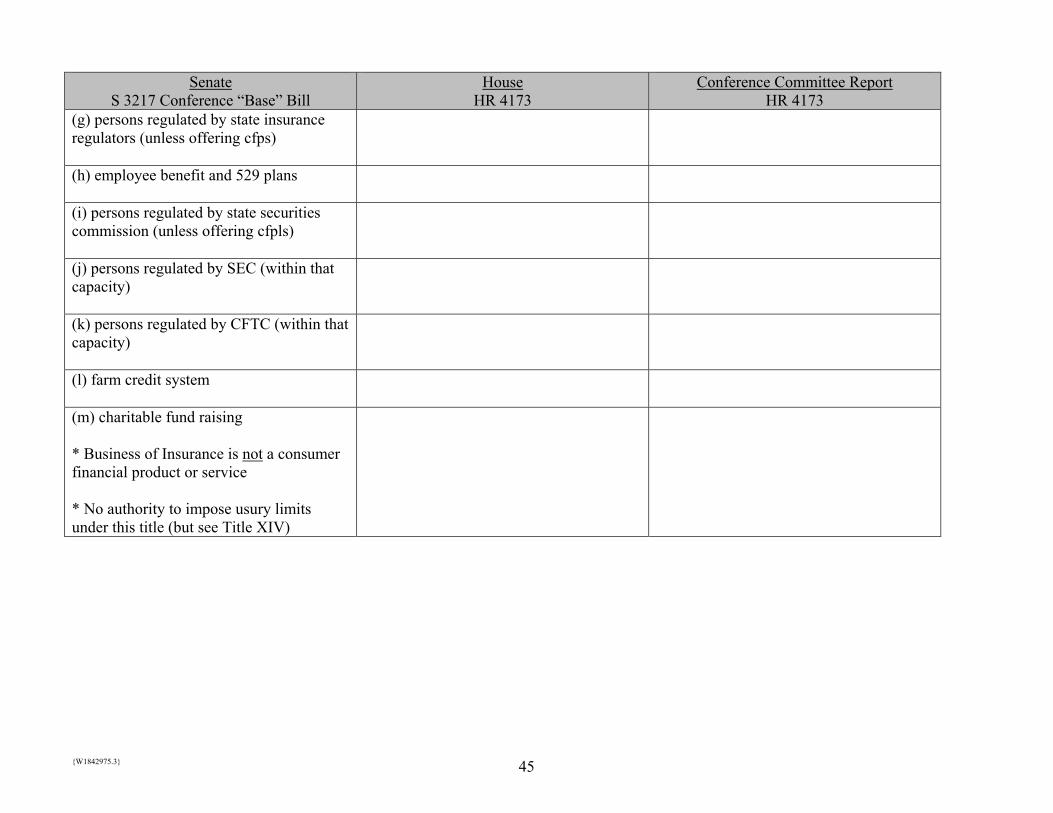

(g) persons regulated by state insurance regulators (unless offering cfps)

(h) employee benefit and 529 plans

(i) persons regulated by state securities commission (unless offering cfpls)

(j) persons regulated by SEC (within that capacity)

(k) persons regulated by CFTC (within that capacity)

(l) farm credit system

(m) charitable fund raising * Business of Insurance is not a consumer financial product or service * No authority to impose usury limits under this title (but see Title XIV)

{W1842975.3} 46

Senate

S 3217 Conference “Base” Bill House

HR 4173 Conference Committee Report

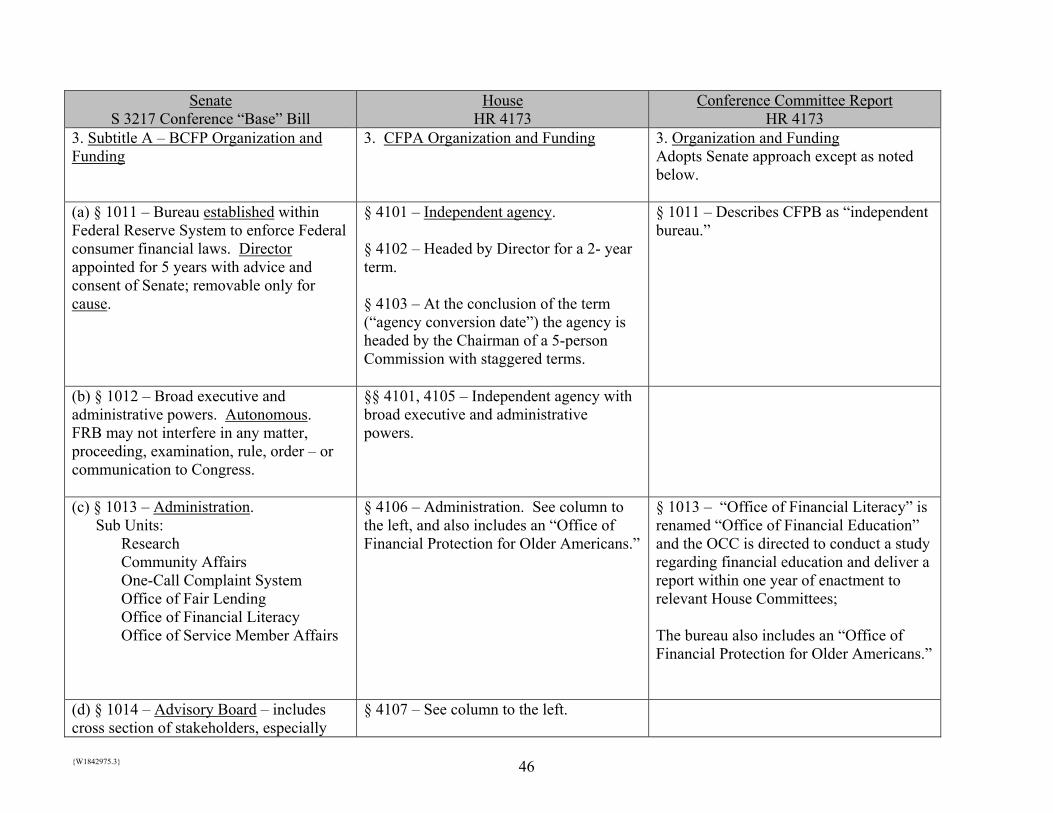

HR 4173 3. Subtitle A – BCFP Organization and Funding

3. CFPA Organization and Funding 3. Organization and Funding Adopts Senate approach except as noted below.

(a) § 1011 – Bureau established within Federal Reserve System to enforce Federal consumer financial laws. Director appointed for 5 years with advice and consent of Senate; removable only for cause.

§ 4101 – Independent agency. § 4102 – Headed by Director for a 2- year term. § 4103 – At the conclusion of the term (“agency conversion date”) the agency is headed by the Chairman of a 5-person Commission with staggered terms.

§ 1011 – Describes CFPB as “independent bureau.”

(b) § 1012 – Broad executive and administrative powers. Autonomous. FRB may not interfere in any matter, proceeding, examination, rule, order – or communication to Congress.

§§ 4101, 4105 – Independent agency with broad executive and administrative powers.

(c) § 1013 – Administration. Sub Units:

Research Community Affairs One-Call Complaint System Office of Fair Lending Office of Financial Literacy Office of Service Member Affairs

§ 4106 – Administration. See column to the left, and also includes an “Office of Financial Protection for Older Americans.”

§ 1013 – “Office of Financial Literacy” is renamed “Office of Financial Education” and the OCC is directed to conduct a study regarding financial education and deliver a report within one year of enactment to relevant House Committees; The bureau also includes an “Office of Financial Protection for Older Americans.”

(d) § 1014 – Advisory Board – includes cross section of stakeholders, especially

§ 4107 – See column to the left.

{W1842975.3} 47

Senate S 3217 Conference “Base” Bill

House HR 4173

Conference Committee Report HR 4173

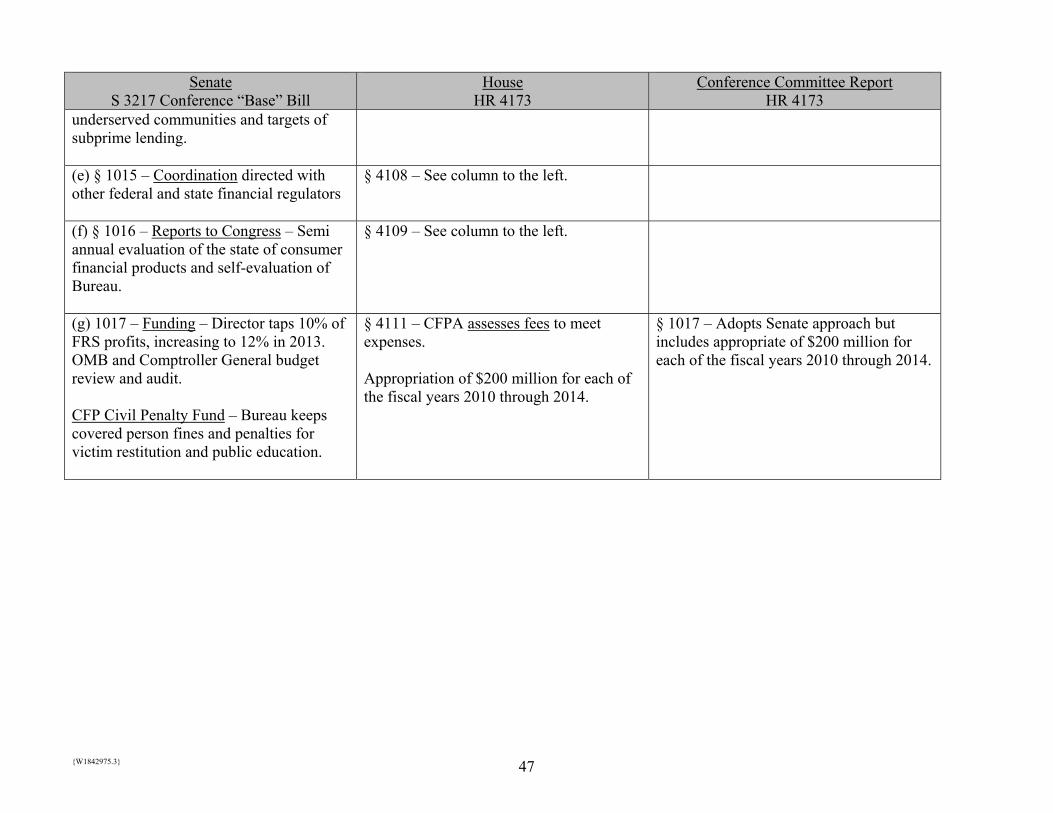

underserved communities and targets of subprime lending. (e) § 1015 – Coordination directed with other federal and state financial regulators

§ 4108 – See column to the left.

(f) § 1016 – Reports to Congress – Semi annual evaluation of the state of consumer financial products and self-evaluation of Bureau.

§ 4109 – See column to the left.

(g) 1017 – Funding – Director taps 10% of FRS profits, increasing to 12% in 2013. OMB and Comptroller General budget review and audit. CFP Civil Penalty Fund – Bureau keeps covered person fines and penalties for victim restitution and public education.

§ 4111 – CFPA assesses fees to meet expenses. Appropriation of $200 million for each of the fiscal years 2010 through 2014.

§ 1017 – Adopts Senate approach but includes appropriate of $200 million for each of the fiscal years 2010 through 2014.

{W1842975.3} 48

Senate

S 3217 Conference “Base” Bill House

HR 4173 Conference Committee Report

HR 4173 4. Subtitle B General Powers

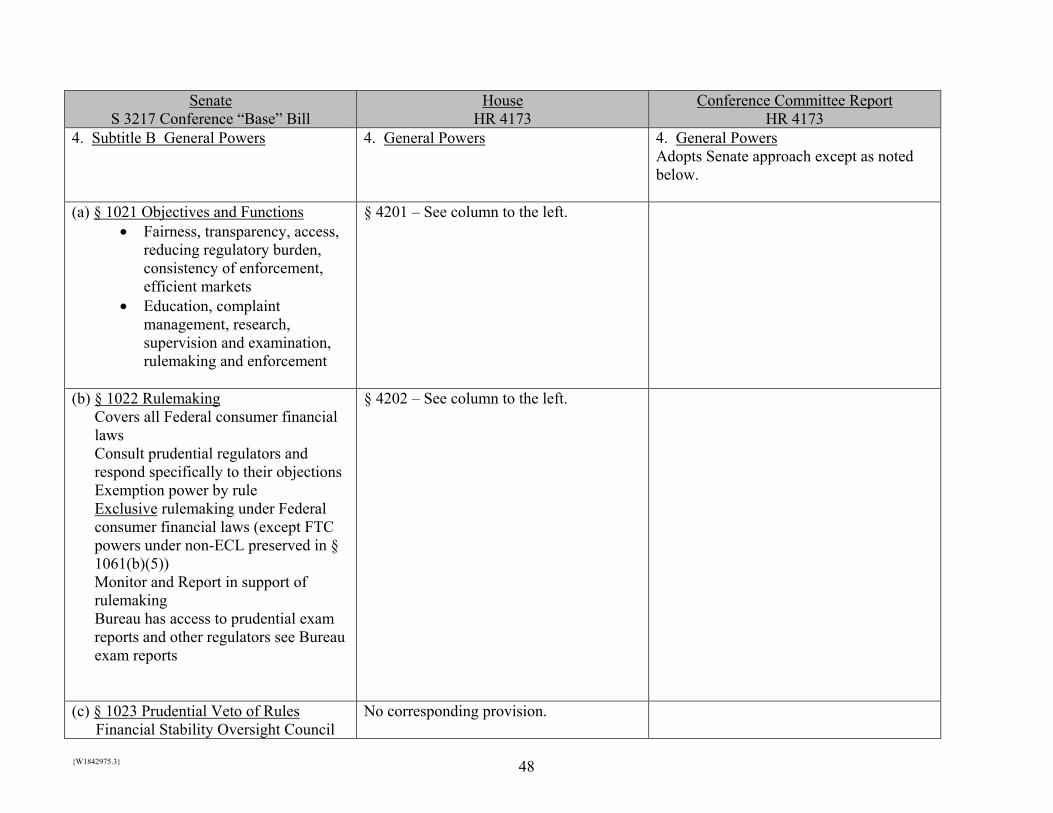

4. General Powers 4. General Powers Adopts Senate approach except as noted below.

(a) § 1021 Objectives and Functions • Fairness, transparency, access,

reducing regulatory burden, consistency of enforcement, efficient markets

• Education, complaint management, research, supervision and examination, rulemaking and enforcement

§ 4201 – See column to the left.

(b) § 1022 Rulemaking Covers all Federal consumer financial laws Consult prudential regulators and respond specifically to their objections Exemption power by rule Exclusive rulemaking under Federal consumer financial laws (except FTC powers under non-ECL preserved in § 1061(b)(5)) Monitor and Report in support of rulemaking Bureau has access to prudential exam reports and other regulators see Bureau exam reports

§ 4202 – See column to the left.

(c) § 1023 Prudential Veto of Rules Financial Stability Oversight Council

No corresponding provision.

{W1842975.3} 49

Senate S 3217 Conference “Base” Bill

House HR 4173

Conference Committee Report HR 4173

member agency may stay (by act of Chairman) or set-aside (by 2/3 vote) a BCFP rule that threatens safety and soundness of US banking system or stability of financial system

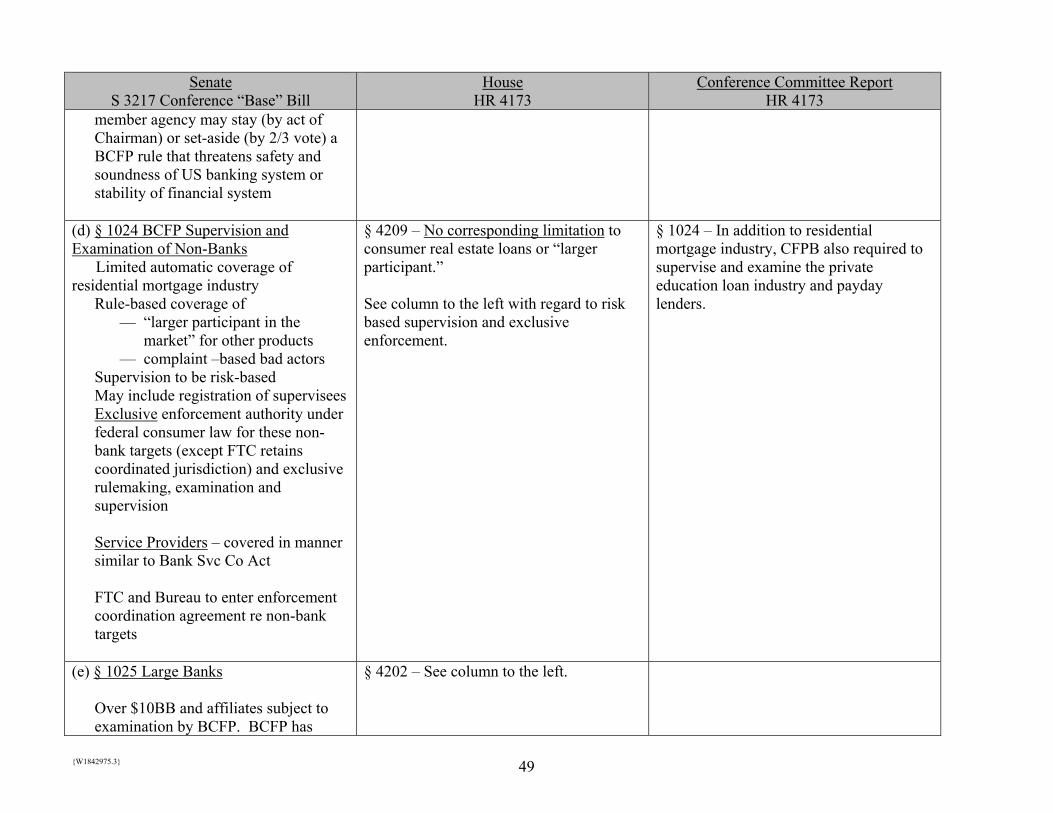

(d) § 1024 BCFP Supervision and Examination of Non-Banks Limited automatic coverage of residential mortgage industry

Rule-based coverage of — “larger participant in the

market” for other products — complaint –based bad actors

Supervision to be risk-based May include registration of supervisees Exclusive enforcement authority under federal consumer law for these non-bank targets (except FTC retains coordinated jurisdiction) and exclusive rulemaking, examination and supervision Service Providers – covered in manner similar to Bank Svc Co Act FTC and Bureau to enter enforcement coordination agreement re non-bank targets

§ 4209 – No corresponding limitation to consumer real estate loans or “larger participant.” See column to the left with regard to risk based supervision and exclusive enforcement.

§ 1024 – In addition to residential mortgage industry, CFPB also required to supervise and examine the private education loan industry and payday lenders.

(e) § 1025 Large Banks

Over $10BB and affiliates subject to examination by BCFP. BCFP has

§ 4202 – See column to the left.

{W1842975.3} 50

Senate S 3217 Conference “Base” Bill

House HR 4173

Conference Committee Report HR 4173

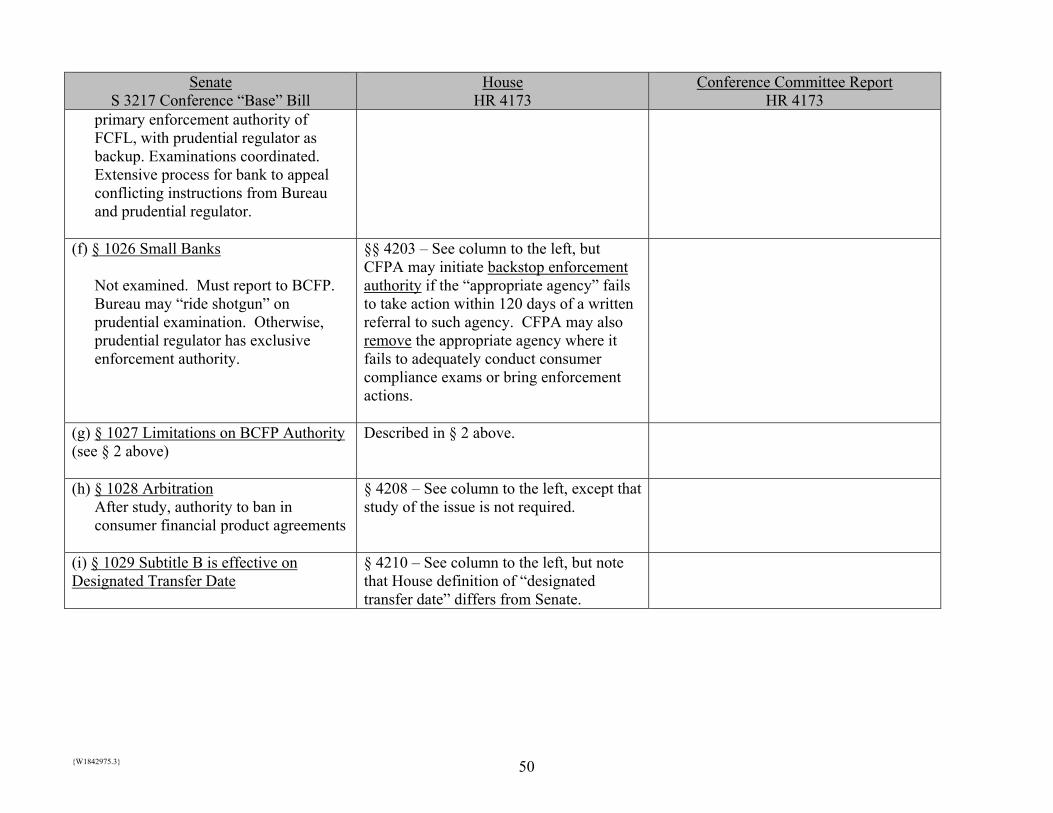

primary enforcement authority of FCFL, with prudential regulator as backup. Examinations coordinated. Extensive process for bank to appeal conflicting instructions from Bureau and prudential regulator.

(f) § 1026 Small Banks

Not examined. Must report to BCFP. Bureau may “ride shotgun” on prudential examination. Otherwise, prudential regulator has exclusive enforcement authority.

§§ 4203 – See column to the left, but CFPA may initiate backstop enforcement authority if the “appropriate agency” fails to take action within 120 days of a written referral to such agency. CFPA may also remove the appropriate agency where it fails to adequately conduct consumer compliance exams or bring enforcement actions.

(g) § 1027 Limitations on BCFP Authority (see § 2 above)

Described in § 2 above.

(h) § 1028 Arbitration After study, authority to ban in consumer financial product agreements

§ 4208 – See column to the left, except that study of the issue is not required.

(i) § 1029 Subtitle B is effective on Designated Transfer Date

§ 4210 – See column to the left, but note that House definition of “designated transfer date” differs from Senate.

{W1842975.3} 51

Senate

S 3217 Conference “Base” Bill House

HR 4173 Conference Committee Report

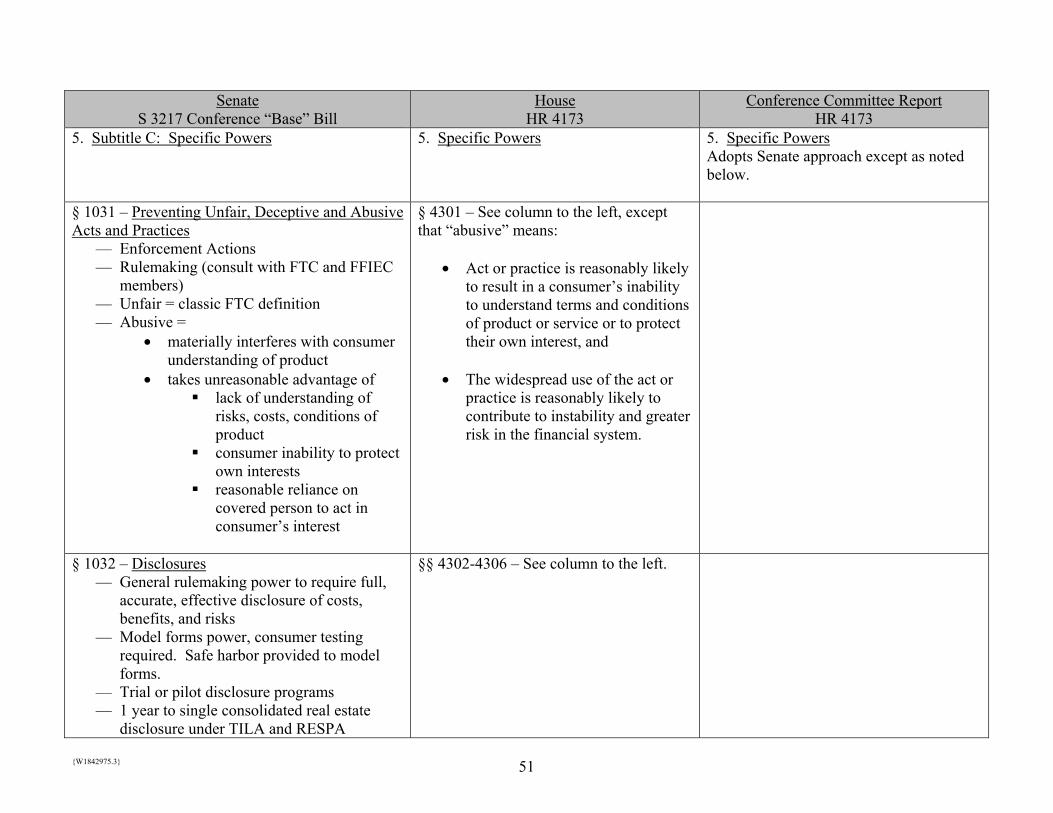

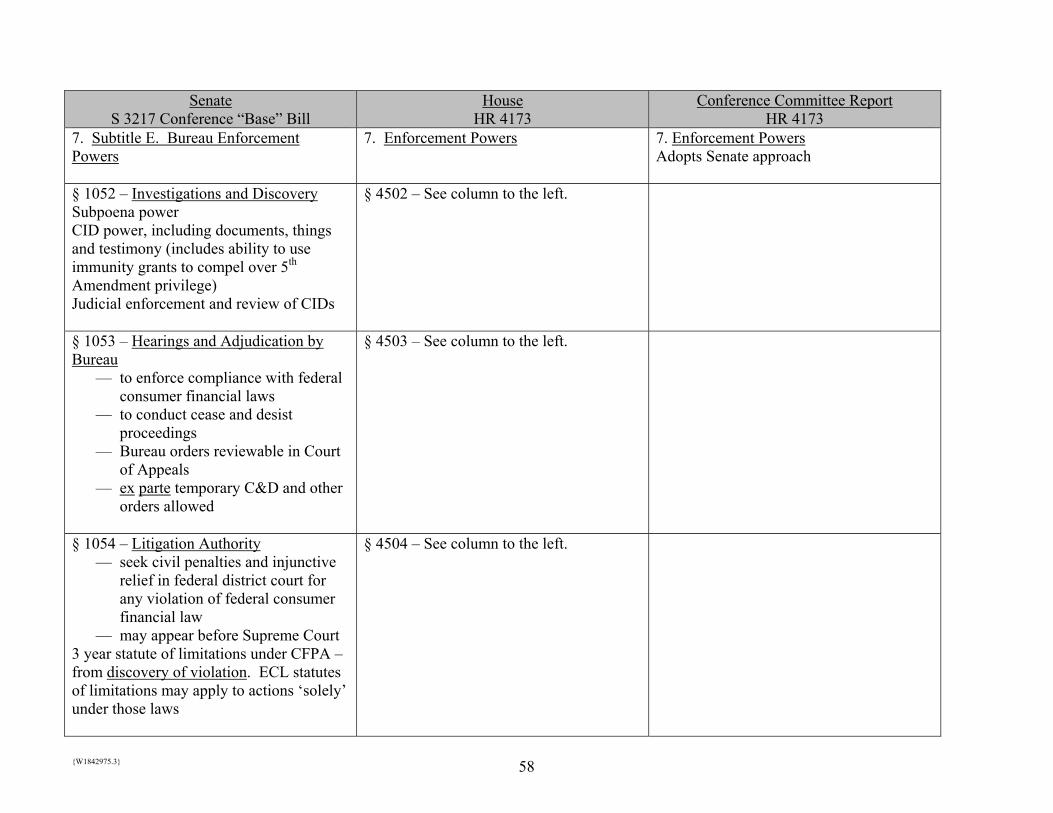

HR 4173 5. Subtitle C: Specific Powers

5. Specific Powers 5. Specific Powers Adopts Senate approach except as noted below.

§ 1031 – Preventing Unfair, Deceptive and Abusive Acts and Practices

— Enforcement Actions — Rulemaking (consult with FTC and FFIEC

members) — Unfair = classic FTC definition — Abusive =

• materially interferes with consumer understanding of product

• takes unreasonable advantage of lack of understanding of

risks, costs, conditions of product

consumer inability to protect own interests

reasonable reliance on covered person to act in consumer’s interest

§ 4301 – See column to the left, except that “abusive” means:

• Act or practice is reasonably likely to result in a consumer’s inability to understand terms and conditions of product or service or to protect their own interest, and

• The widespread use of the act or

practice is reasonably likely to contribute to instability and greater risk in the financial system.

§ 1032 – Disclosures — General rulemaking power to require full,

accurate, effective disclosure of costs, benefits, and risks

— Model forms power, consumer testing required. Safe harbor provided to model forms.

— Trial or pilot disclosure programs — 1 year to single consolidated real estate

disclosure under TILA and RESPA

§§ 4302-4306 – See column to the left.

{W1842975.3} 52

Senate S 3217 Conference “Base” Bill

House HR 4173

Conference Committee Report HR 4173

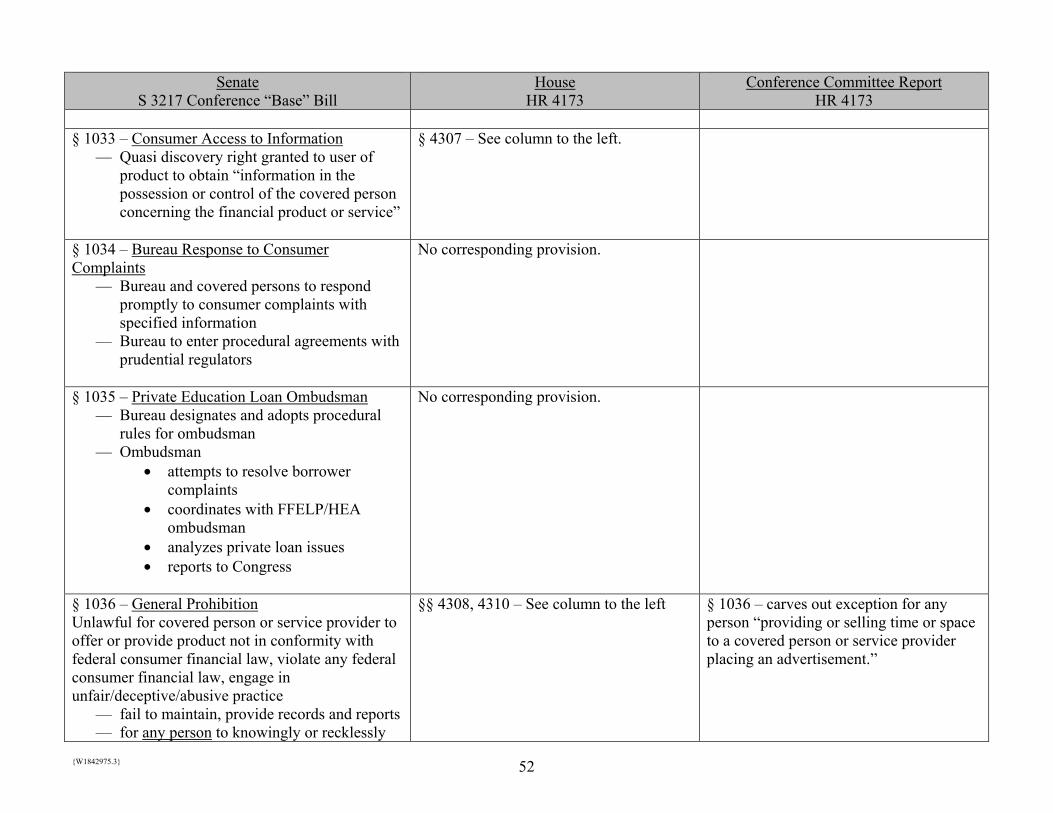

§ 1033 – Consumer Access to Information

— Quasi discovery right granted to user of product to obtain “information in the possession or control of the covered person concerning the financial product or service”

§ 4307 – See column to the left.

§ 1034 – Bureau Response to Consumer Complaints

— Bureau and covered persons to respond promptly to consumer complaints with specified information

— Bureau to enter procedural agreements with prudential regulators

No corresponding provision.

§ 1035 – Private Education Loan Ombudsman — Bureau designates and adopts procedural

rules for ombudsman — Ombudsman

• attempts to resolve borrower complaints

• coordinates with FFELP/HEA ombudsman

• analyzes private loan issues • reports to Congress

No corresponding provision.

§ 1036 – General Prohibition Unlawful for covered person or service provider to offer or provide product not in conformity with federal consumer financial law, violate any federal consumer financial law, engage in unfair/deceptive/abusive practice

— fail to maintain, provide records and reports — for any person to knowingly or recklessly

§§ 4308, 4310 – See column to the left

§ 1036 – carves out exception for any person “providing or selling time or space to a covered person or service provider placing an advertisement.”

{W1842975.3} 53

Senate S 3217 Conference “Base” Bill

House HR 4173

Conference Committee Report HR 4173

provide substantial assistance to a covered person or service provider in violation of § 1031 UDAP rules adopted by Bureau

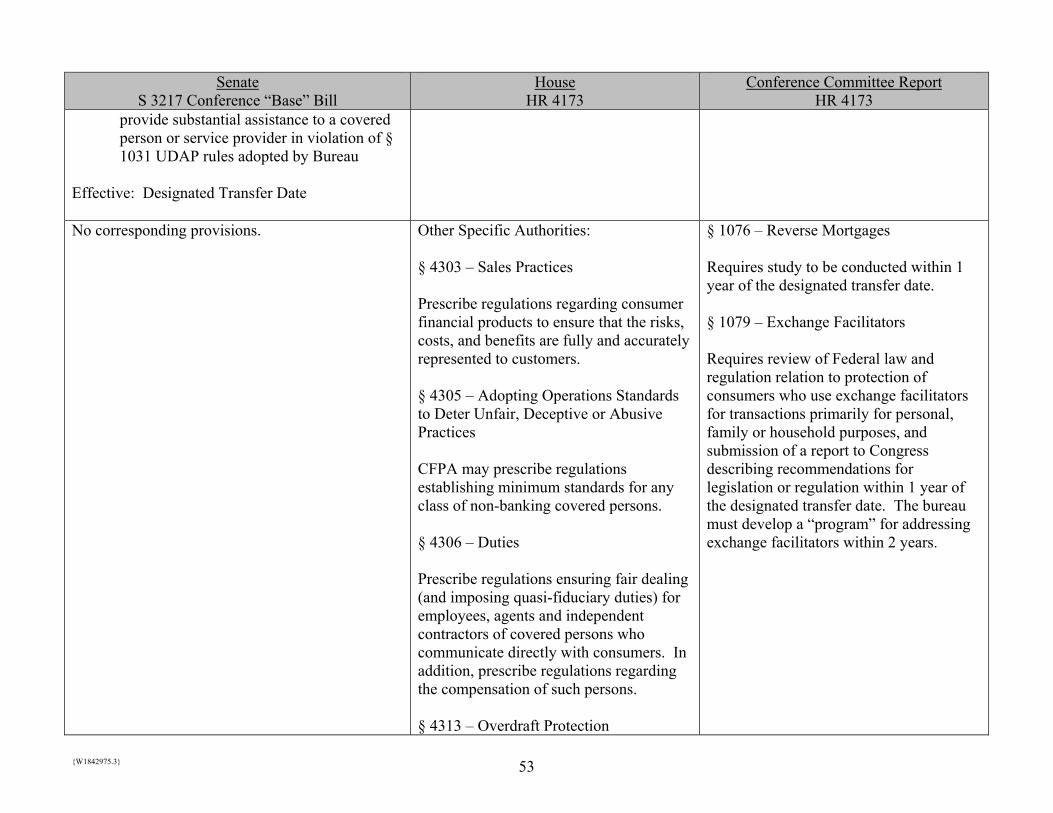

Effective: Designated Transfer Date No corresponding provisions. Other Specific Authorities:

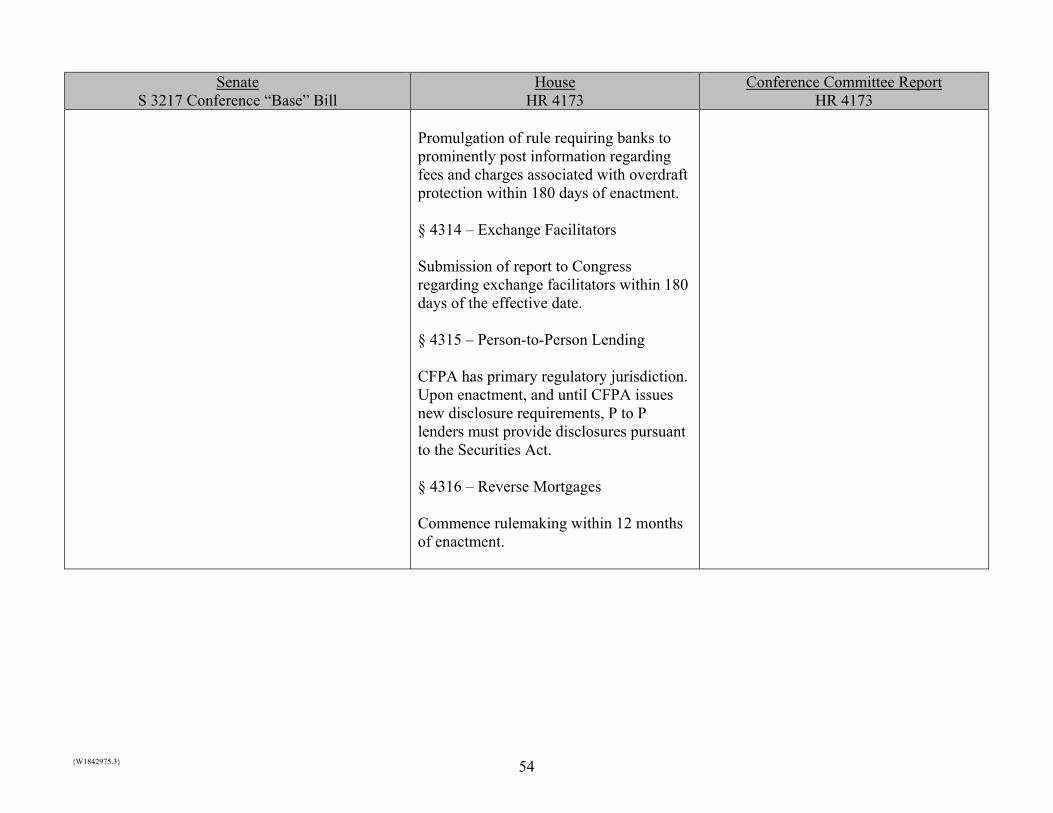

§ 4303 – Sales Practices Prescribe regulations regarding consumer financial products to ensure that the risks, costs, and benefits are fully and accurately represented to customers. § 4305 – Adopting Operations Standards to Deter Unfair, Deceptive or Abusive Practices CFPA may prescribe regulations establishing minimum standards for any class of non-banking covered persons. § 4306 – Duties Prescribe regulations ensuring fair dealing (and imposing quasi-fiduciary duties) for employees, agents and independent contractors of covered persons who communicate directly with consumers. In addition, prescribe regulations regarding the compensation of such persons. § 4313 – Overdraft Protection

§ 1076 – Reverse Mortgages Requires study to be conducted within 1 year of the designated transfer date. § 1079 – Exchange Facilitators Requires review of Federal law and regulation relation to protection of consumers who use exchange facilitators for transactions primarily for personal, family or household purposes, and submission of a report to Congress describing recommendations for legislation or regulation within 1 year of the designated transfer date. The bureau must develop a “program” for addressing exchange facilitators within 2 years.

{W1842975.3} 54

Senate S 3217 Conference “Base” Bill

House HR 4173

Conference Committee Report HR 4173

Promulgation of rule requiring banks to prominently post information regarding fees and charges associated with overdraft protection within 180 days of enactment. § 4314 – Exchange Facilitators Submission of report to Congress regarding exchange facilitators within 180 days of the effective date. § 4315 – Person-to-Person Lending CFPA has primary regulatory jurisdiction. Upon enactment, and until CFPA issues new disclosure requirements, P to P lenders must provide disclosures pursuant to the Securities Act. § 4316 – Reverse Mortgages Commence rulemaking within 12 months of enactment.

{W1842975.3} 55

Senate

S 3217 Conference “Base” Bill House

HR 4173 Conference Committee Report

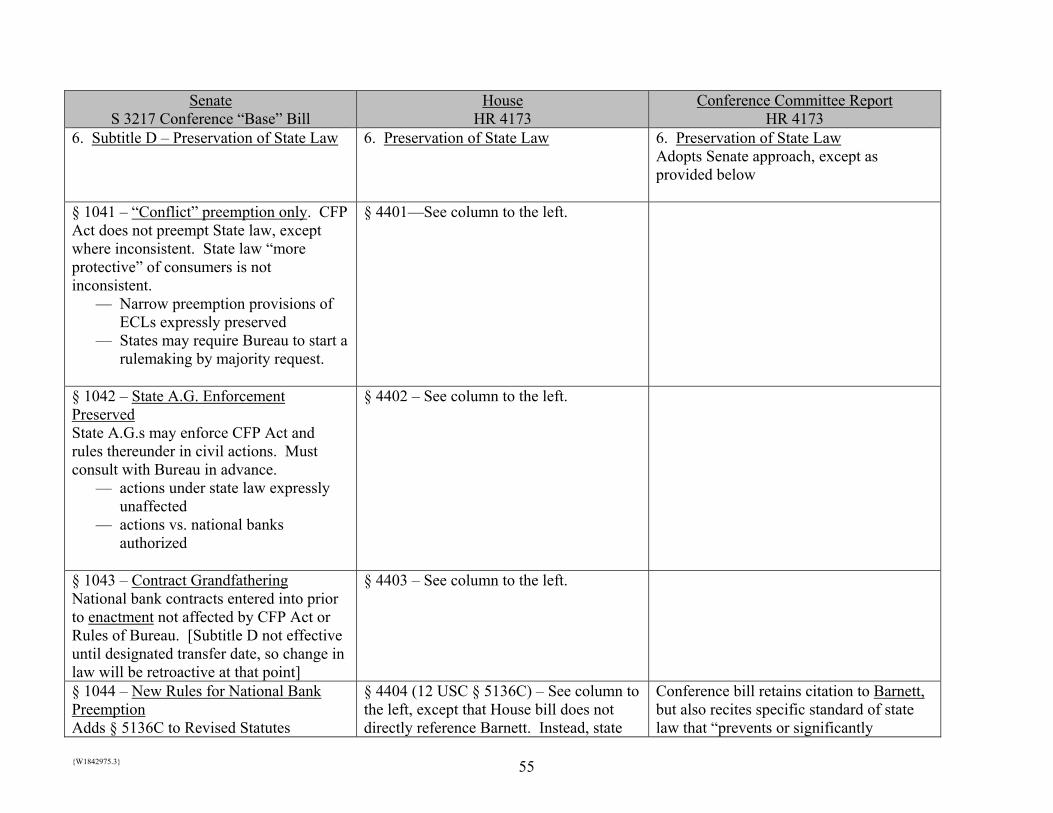

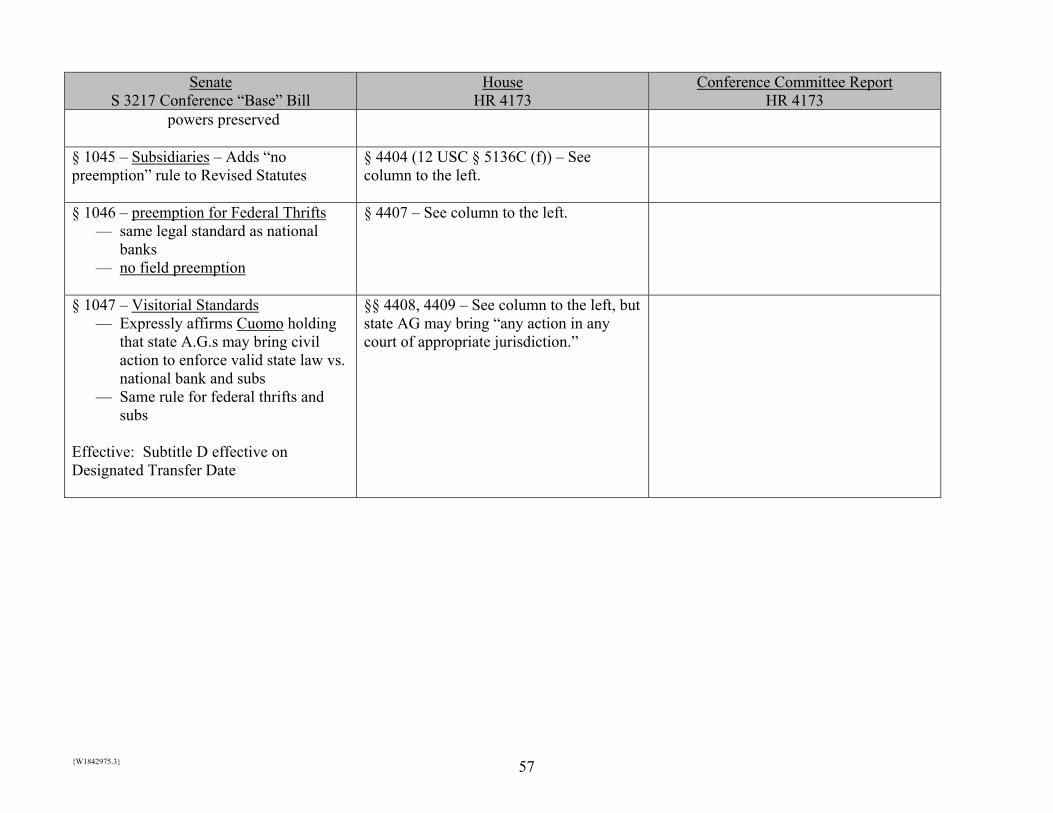

HR 4173 6. Subtitle D – Preservation of State Law

6. Preservation of State Law 6. Preservation of State Law Adopts Senate approach, except as provided below

§ 1041 – “Conflict” preemption only. CFP Act does not preempt State law, except where inconsistent. State law “more protective” of consumers is not inconsistent.

— Narrow preemption provisions of ECLs expressly preserved

— States may require Bureau to start a rulemaking by majority request.

§ 4401—See column to the left.

§ 1042 – State A.G. Enforcement Preserved State A.G.s may enforce CFP Act and rules thereunder in civil actions. Must consult with Bureau in advance.

— actions under state law expressly unaffected

— actions vs. national banks authorized

§ 4402 – See column to the left.

§ 1043 – Contract Grandfathering National bank contracts entered into prior to enactment not affected by CFP Act or Rules of Bureau. [Subtitle D not effective until designated transfer date, so change in law will be retroactive at that point]

§ 4403 – See column to the left.

§ 1044 – New Rules for National Bank Preemption Adds § 5136C to Revised Statutes

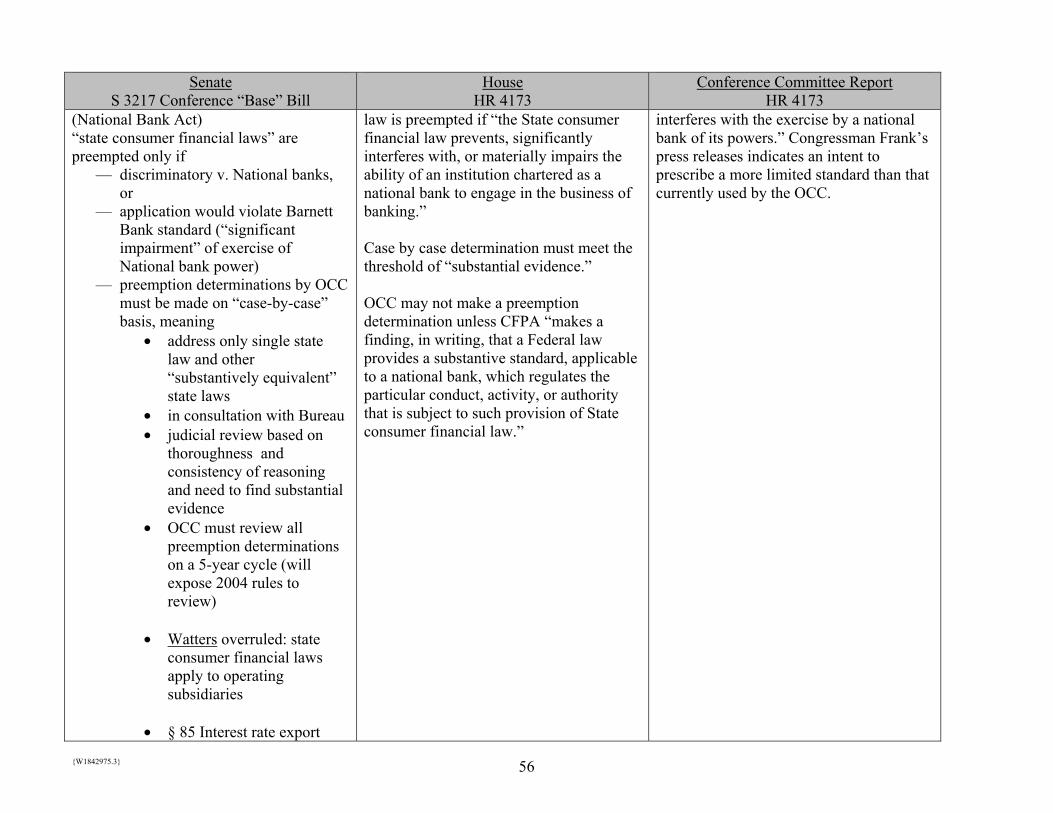

§ 4404 (12 USC § 5136C) – See column to the left, except that House bill does not directly reference Barnett. Instead, state

Conference bill retains citation to Barnett, but also recites specific standard of state law that “prevents or significantly

{W1842975.3} 56