amara raja batteries limited -...

TRANSCRIPT

Firstcall India Equity Advisors Pvt Ltd 1

Amara Raja Batteries Limited

BUY Target price: Rs.185.00 CMP: Rs. 161.00 Market Cap. : Rs.13750.21mn. Date: December 11th, 2009.

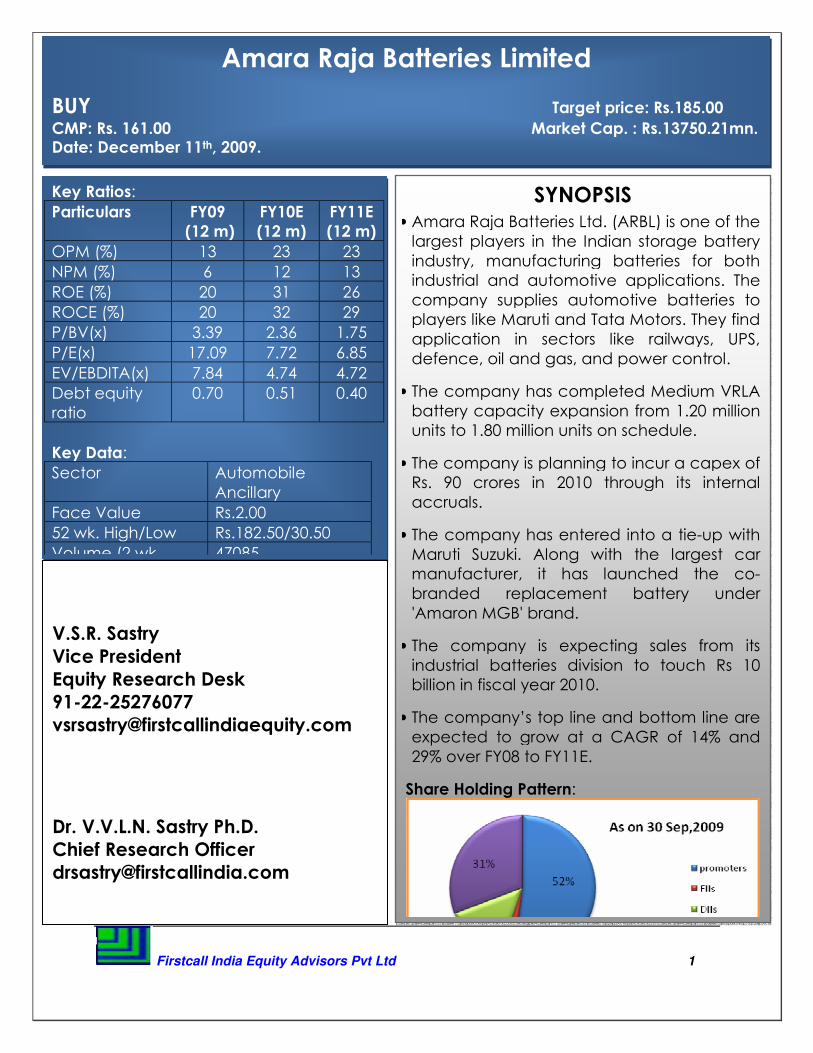

Key Ratios:

Particulars FY09

(12 m)

FY10E

(12 m)

FY11E

(12 m)

OPM (%) 13 23 23

NPM (%) 6 12 13

ROE (%) 20 31 26

ROCE (%) 20 32 29

P/BV(x) 3.39 2.36 1.75

P/E(x) 17.09 7.72 6.85

EV/EBDITA(x) 7.84 4.74 4.72

Debt equity ratio

0.70 0.51 0.40

Key Data:

Sector Automobile Ancillary

Face Value Rs.2.00

52 wk. High/Low Rs.182.50/30.50

Volume (2 wk. 47085

SYNOPSIS • Amara Raja Batteries Ltd. (ARBL) is one of the largest players in the Indian storage battery industry, manufacturing batteries for both industrial and automotive applications. The company supplies automotive batteries to players like Maruti and Tata Motors. They find application in sectors like railways, UPS, defence, oil and gas, and power control.

• The company has completed Medium VRLA battery capacity expansion from 1.20 million units to 1.80 million units on schedule.

• The company is planning to incur a capex of Rs. 90 crores in 2010 through its internal accruals.

• The company has entered into a tie-up with Maruti Suzuki. Along with the largest car manufacturer, it has launched the co-branded replacement battery under 'Amaron MGB' brand.

• The company is expecting sales from its industrial batteries division to touch Rs 10 billion in fiscal year 2010.

• The company’s top line and bottom line are expected to grow at a CAGR of 14% and 29% over FY08 to FY11E.

Share Holding Pattern:

V.S.R. Sastry

Vice President

Equity Research Desk

91-22-25276077

Dr. V.V.L.N. Sastry Ph.D.

Chief Research Officer

Firstcall India Equity Advisors Pvt Ltd 2

Table of Content

Content Page No.

1. Investment Highlights 03

2. Peer Group Comparison 06

3. Key Concerns 06

4. Financials 07

5. Charts & Graph 09

6. Outlook and Conclusion 11

7. Industry Overview 12

Firstcall India Equity Advisors Pvt Ltd 3

Investment Highlights

• Result Updates (Q2FY10)

For the second quarter, the top line of the company increased 6%YoY and stood at Rs.3611.67mn against Rs.3399.61mn of the same period of the last year. The bottom line of the company for the quarter stood at Rs.478.97mn from Rs.187.92mn of the corresponding period of the previous year i.e., an increase of 155%YoY.

EPS of the company for the quarter stood at Rs.5.61 for equity share of Rs.2.00 each.

Firstcall India Equity Advisors Pvt Ltd 4

Expenditure for the quarter stood at Rs.2757.79mn, which is around 9% lower than the corresponding period of the previous year. Raw material cost of the company for the quarter accounts for 59 % of the sales of the company and stood at Rs.2134.35mn from Rs.2185.99mn of the corresponding period of the previous year i.e., a decrease of 2%YoY. Employee cost stood at Rs.153.90mn from Rs.113.27mn. and accounts for 4% of the revenue of the company for the quarter i.e., an increase of 36%YoY.

OPM and NPM for the quarter stood at 24% and 13% respectively from 12% and 6% respectively of the same period of the last year.

Firstcall India Equity Advisors Pvt Ltd 5

• The Industrial Battery business has shown a steady growth in Q2. The UPS

battery markets continue to remain robust. The company has completed Medium VRLA battery capacity expansion from 1.20 million units to 1.80 million units on schedule, which will provide growth and help in garnering additional market share going forward. Telecom market potential in near future is influenced by trends in infrastructure sharing, roll out of rural network and implementation of GSM projects by new licensees.

• Growth in automotive OE business tracked the strong revival in passenger

vehicle demand. The commercial vehicle segment has also begun to look up. The aftermarket continues to grow in both the formats of AMARON® and POWERZONETM. In the space of 2-wheeler battery market, AMARON ProbikeRiderTM has gained momentum and further capacity addition is on the anvil. Based on buoyant industry growth forecast, automotive battery business is expected to be on a strong growth path.

• Capex plan

The company is planning to incur a capex of Rs. 90 crores in 2010 through its internal accruals. The company will be investing Rs. 50 crores in the UPS segment and Rs. 20 crores in the Motor cycle segment. The rest of it will be used for the industrial segment. ARBL is not looking at expanding the capacity in the automotive batteries segment in the near future.

• Amara Raja expects industrial batteries sales to touch Rs 10bn by FY10

Firstcall India Equity Advisors Pvt Ltd 6

Amara Raja Batteries is expecting sales from its industrial batteries division to touch Rs 10 billion in fiscal year 2010.

By fiscal year 2010, the company`s revenue from industrial segment will account for more than half of total sales on the back of capacity addition. The company said that it saw industrial batteries sales in the current fiscal at about Rs 7.5 billion.

• Amara Raja ties up with Maruti Suzuki

The company has entered into a tie-up with Maruti Suzuki. Along with the largest car manufacturer, it has launched the co-branded replacement battery under 'Amaron MGB' brand. This is aimed at capitalizing on the Amaron brand, which has been an OE fitment in the automotive battery segment for most models of passenger cars from the Maruti stable. The tie-up has made 'Amaron' as the brand endorsed by Maruti Suzuki as a replacement battery. Amaron MGB will now be an addition to Maruti Suzuki's existing array of genuine spares offerings. Amaron MGB now presents customers with the dual advantage of Amara Raja's finest battery technology and a wide availability through Maruti Suzuki's largest network of 3,000 plus authorized outlets across the length and breadth of the country.

Peer Group Comparison

Name of the

company

CMP(Rs.)

(As on

Dec

11th,2009

)

Market

Cap.

(Rs. Mn.)

EPS

(Rs.)

P/E

(x)

P/BV

(x)

Dividend

(%)

(FY08)

Amara raja batteries ltd 161.00 13750.21 16.07 10.02 3.39 40.00

Exide industries 112.95 90360.00 4.96 22.77 7.42 60.00

Bosch 4620.00 145062.90 164.82 28.03 4.69 250.00

Firstcall India Equity Advisors Pvt Ltd 7

Motherson Sumi Systems 128.50 45688.70 2.48 51.81 11.04 135.00

Amtek Auto 186.00 26224.70 9.62 19.33 1.06 25.00

Key Concerns

� Adverse Govt. policies

� Economic slow down.

� Highly competition

Financials

Results Update

12 months ended Profit and Loss A/C (Standalone):

Value(Rs in million) FY08A FY09A FY10E FY11E

Description 12m 12m 12m 12m

Net Sales 10833.26 13241.27 14300.57 16016.64

Other Income 256.10 16.52 31.39 37.67

Total Income 11089.36 13257.79 14331.96 16054.31

Expenditure -9256.21 -11503.28 -11082.94 -12412.90

Operating Profit 1833.15 1754.51 3249.02 3641.41

Interest -129.31 -182.37 -120.07 -126.07

Firstcall India Equity Advisors Pvt Ltd 8

Gross Profit 1703.84 1572.14 3128.95 3515.34

Depreciation -244.45 -345.56 -414.67 -456.14

Profit before Tax 1459.38 1226.59 2714.28 3059.20

Tax -515.75 -421.80 -933.39 -1052.00

Net Profit 943.63 804.79 1780.89 2007.20

Equity Capital 113.88 170.81 170.81 170.81

Reserves 3217.14 3885.05 5665.94 7673.15

Face Value 2.00 2.00 2.00 2.00

Total No. of Shares 56.94 85.41 85.41 85.41

EPS 16.57 9.42 20.85 23.50

Quarterly ended Profit and Loss A/C (Standalone):

Value(Rs. in million) 31-Mar-09 30-Jun-09 30-Sep-09 31-Dec-09E

Description 3m 3m 3m 3m

Net Sales 3330.29 3065.34 3611.67 3792.25

Other Income 5.58 6.12 9.59 10.36

Total Income 3335.87 3071.46 3621.26 3802.61

Expenditure -2765.75 -2298.82 -2757.79 -2895.68

Operating Profit 570.12 772.64 863.47 906.93

Interest -48.66 -29.84 -25.73 -26.76

Firstcall India Equity Advisors Pvt Ltd 9

Gross Profit 521.46 742.80 837.74 880.17

Depreciation -99.72 -102.01 -106.57 -110.83

Profit before Tax 421.75 640.79 731.17 769.34

Tax -141.26 -215.05 -252.20 -265.37

Net Profit 280.49 425.74 478.97 503.97

Equity Capital 170.81 170.81 170.81 170.81

Face Value 2.00 2.00 2.00 2.00

Total No. of Shares 85.41 85.41 85.41 85.41

EPS 3.28 4.98 5.61 5.90

Charts

• Net sales & PAT

Firstcall India Equity Advisors Pvt Ltd 10

• P/E Ratio (x)

• P/BV (X)

Firstcall India Equity Advisors Pvt Ltd 11

• EV/EBITDA(X)

1 Year Comparative Graph

Firstcall India Equity Advisors Pvt Ltd 12

Outlook and Conclusion

• At the market price of Rs.161.00, the stock is trading at 7.72 x and 6.85 x for FY10E and FY11E respectively.

• EPS of the company is expected to be at Rs.20.85 and Rs.23.50 for the

earnings of FY10E and FY11E respectively. • On the basis of EV/EBDITA, the stock trades at 4.74 x and 4.72 x for FY10E and

FY11E respectively. • The price to book value of the company is expected to be at 2.36 x and 1.75

x for FY10E and FY11E respectively.

• The company has completed Medium VRLA battery capacity expansion from 1.20 million units to 1.80 million units on schedule, which will provide growth and help in garnering additional market share going forward.

• The flow in profits was aided by operational efficiencies and cost-savings. The

uncertainties in telecom infrastructure rollout and volatility in lead price might pose challenges in the second half of the current financial year. However, the expected double-digit growth in automotive industry and projected GDP growth of more than 6% for the current fiscal are positive signals for the industry.

Amara Raja BSE SENSEX

Firstcall India Equity Advisors Pvt Ltd 13

• The company is planning to incur a capex of Rs. 90 crores in 2010 through its internal accruals. The company will be investing Rs. 50 crores in the UPS segment and Rs. 20 crores in the Motor cycle segment. The rest of it will be used for the industrial segment. ARBL is not looking at expanding the capacity in the automotive batteries segment in the near future.

• The company has entered into a tie-up with Maruti Suzuki. Along with the

largest car manufacturer, it has launched the co-branded replacement battery under 'Amaron MGB' brand.

• The company is expecting sales from its industrial batteries division to touch

Rs 10 billion in fiscal year 2010.

• ARBL batteries support the transmission & distribution networks of Power stations. Increased spending by the government in the power sector will boost demand as government plans a 48% growth in transmission grid growth in the eleventh plan.

• We recommend ‘BUY’ for this stock with a target price of Rs.185.00 for long

term.

Industry Overview

The Indian auto ancillary industry has come a long way since it had its small

beginnings in the 1940s. If the evolution of the industry is traced in India, it can

be classified into three distinct phases namely: Period prior to the entry of Maruti

Udhyog Ltd, Period after the entry of Maruti Udhyog Ltd and Period post

Liberalization. The period prior to the entry of Maruti Udhyog Ltd was

characterized by small number of auto majors like Hindustan Motors, Premier

Automobiles, Telco, Bajaj, Mahindra and Mahindra, low technology and assured

business for most of the auto-component manufacturers.

The entry of Maruti in the 1980s marked the beginning of the second phase of

the industry. The auto ancillary industry in the country really showed a spurt in

growth during this period. This period witnessed the emergence of a new

generation of auto ancillary manufacturers who were required to meet the

stringent quality standards of Maruti’s Korean collaborator Suzuki of Japan. The

good performance of Maruti resulted in an upswing for the domestic auto

Firstcall India Equity Advisors Pvt Ltd 14

ancillary industry. It was during this period that auto components from India

began to be exported.

The entry of foreign automobile manufacturers ranging from Mercedes Benz,

Ford, and General Motors to Daewoo following the government liberalizing the

foreign investment limits saw the beginning of the third phase of the evolution of

the industry. The auto ancillary industry witnessed huge capacity expansions

and modernization initiatives in the post liberalization period. Technological

collaborations and equity partnerships with world leaders in auto components

became a common affair. However, the tough competitive scenario saw a lot

of consolidation in the industry and it still continues unabated.

In 2008-09, automobile sales are expected to grow by around 12 per cent in

value-terms, driven mainly by favourable demographic trends, anticipated

growth recovery in commercial vehicles and robust export growth. Consistent

growth and dedication have made the Indian automobile industry the second-

largest tractor and two-wheeler manufacturer in the world. It is also the fifth-

largest commercial vehicle manufacturer in the world. It is also the fifth-largest

commercial vehicle manufacturer in the world. The Indian automobile market is

among the largest in Asia.

The key players like Hindustan Motors, Maruti Udyog, Fiat India Private Ltd, Tata

Motors, Bajaj Motors, Hero Motors, Ashok Leyland, and Mahindra & Mahindra

have been dominating the vehicle industry. A few of the foreign players like

Toyota Kirloskar Motor Ltd., Skoda India Private Ltd., Honda Siel Cars India Ltd.

have also entered the market and have catered to the customers’ needs to a

large extent.

Not only the Indian companies but also the international car manufacturing

companies are focusing on compact cars to be delivered in the Indian market

at a much smaller price. Moreover, the automobile companies are coming up

with financial schemes such as easy EMI repayment systems to boost sales. There

have been exhibitions like Auto-expo at Pragati Maidan, New Delhi to share the

technological advancements. Besides, there are many new projects coming up

in the automobile industry leading to the growth of the sector.

The Government of India has liberalized the foreign exchange and equity

regulations and has also reduced the tariff on imports, contributing significantly

to the growth of the sector. Having firmly established its presence in the

Firstcall India Equity Advisors Pvt Ltd 15

domestic markets, the Indian automobile sector is now penetrating the

international arena. Vehicle exports from India are at their highest levels. The

leaders of the Indian automobile sector, such as Tate Motors, Maruti and

Mahindra and Mahindra are leading the exports to Europe, Middle East and

African and Asian markets.

The Ministry of Heavy Industries has released the Automotive Plan 2006-2016, with

the motive of making India the most popular manufacturing hub for

automobiles and its components in Asia. The plan focuses on the removal of all

the bottlenecks that are inhibiting its growth in the domestic as well as

international arena.

Key points:

Supply : The Indian automobile market has some amount of excess

capacity.

Demand : Largely cyclical in nature and dependent up on economic

growth and per capita income. Seasonality is also a vital

factor.

Barriers to entry : High capital costs, technology, distribution network, and

availability of auto components.

Competition : High Expected to increase even further.

Some of the major characteristics of Indian automobile sector are:

• Second largest two-wheeler market in the world. • Fourth largest commercial vehicle market in the world. • 11th largest passenger car market in the world. • Expected to become the world's third largest automobile market by 2030,

behind only China and the US.

The Future Growth Drivers: • India's huge geographic spread- Mass Transport System. • Increasing Road Development. • Increasing disposable Income with the service sector. • Replacement of aging four wheelers. • Graduating from two wheelers to four wheelers. • Increasing dispensable income of rural agri sector. • Growing Concept of Second Vehicle in Urban Areas.

Firstcall India Equity Advisors Pvt Ltd 16

___________________________________________________________

Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation

for the purchase or sale of any financial instrument or as an official confirmation of any

transaction. The information contained herein is from publicly available data or other

sources believed to be reliable but we do not represent that it is accurate or complete and it

should not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s

affiliates shall not be in any way responsible for any loss or damage that may arise to any

person from any inadvertent error in the information contained in this report. This document

is provide for assistance only and is not intended to be and must not alone be taken as the

basis for an investment decision.

Firstcall India Equity Research: Email – [email protected]

B. Harikrishna Banking

B. Prathap IT

A. Rajesh Babu FMCG

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

E. Swethalatha Oil & Gas

D. Ashakirankumar Automobile

Rachna Twari Diversified

Kavita Singh Diversified

Nimesh Gada Diversified

Priya Shetty Diversified

Tarang Pawar Diversified

Neelam Dubey Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s, Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions (domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

Other international stock exchanges.