alpha bank fy 2012 results · alpha bank 2012 update ... of modern times ... jan-13 opap baupost...

TRANSCRIPT

27 March 2013

Alpha Bank FY 2012 Results

Alpha Bank 2012 Update

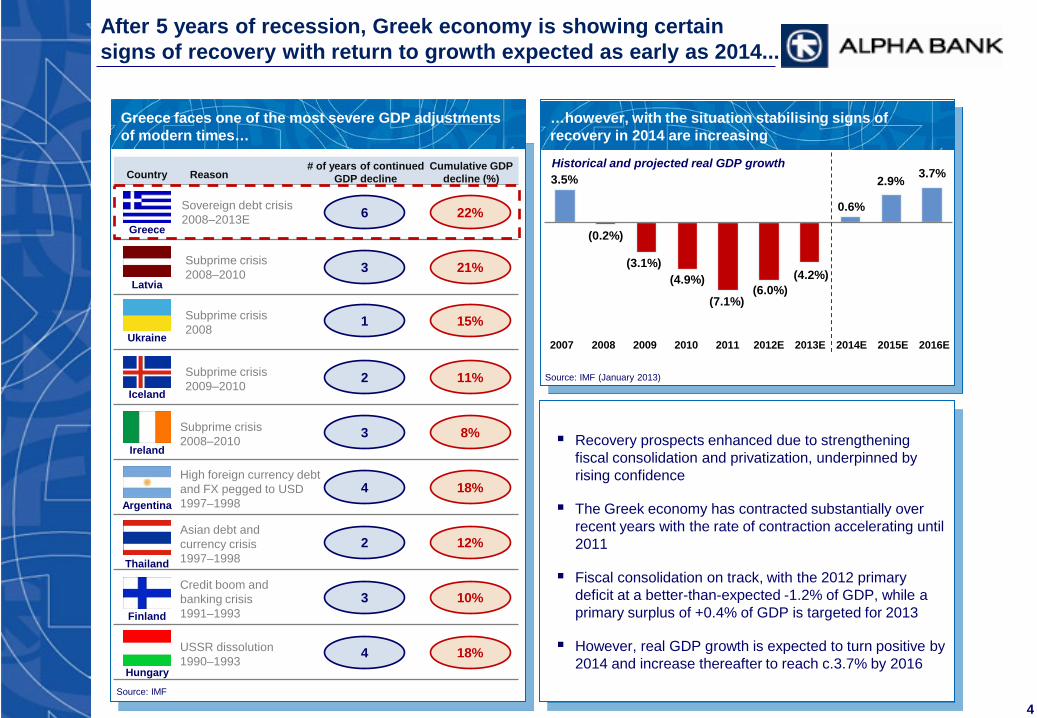

After 5 years of recession, Greek economy is showing certain signs of recovery,

delivering on targets and return to growth expected by 2014

Returning confidence to the banking sector which has rapidly consolidated in 2012

Emporiki acquisition strengthens capital base, provides positive impact on liquidity

and further upside; pro-forma Tangible Equity at €2.1bn

Full year 2012 results affected by multiple headwinds, but positive outlook mainly

related to significant NII improvement

Recent upheaval in Cyprus, where uninsured deposits of banks under resolution

were bailed-in, may increase market uncertainty but should also make depositors

more conscious in selecting the banking relationships

Agenda

1. Macroeconomic Update: First Signs of Stabilisation and FDI

2. Consolidated Banking Sector and Returning Confidence

3. Emporiki Acquisition Bringing Significant Benefits

4. Solid 2012 Performance Despite Multiple Headwinds and Technical Effects

3.5%

(0.2%)

(3.1%) (4.9%)

(7.1%) (6.0%)

(4.2%)

0.6%

2.9% 3.7%

2007 2008 2009 2010 2011 2012E 2013E 2014E 2015E 2016E

4

After 5 years of recession, Greek economy is showing certain signs of recovery with return to growth expected as early as 2014...

Greece faces one of the most severe GDP adjustments of modern times…

Recovery prospects enhanced due to strengthening fiscal consolidation and privatization, underpinned by rising confidence

The Greek economy has contracted substantially over recent years with the rate of contraction accelerating until 2011

Fiscal consolidation on track, with the 2012 primary deficit at a better-than-expected -1.2% of GDP, while a primary surplus of +0.4% of GDP is targeted for 2013

However, real GDP growth is expected to turn positive by 2014 and increase thereafter to reach c.3.7% by 2016

Source: IMF (January 2013)

…however, with the situation stabilising signs of recovery in 2014 are increasing

Historical and projected real GDP growth

Source: IMF

Greece

Country Reason # of years of continued

GDP decline Cumulative GDP

decline (%)

Sovereign debt crisis 2008–2013E 6 22%

Latvia

Subprime crisis 2008–2010 3 21%

Iceland

Subprime crisis 2009–2010

2 11%

Ireland

Argentina

3 8%

Thailand

Finland

2 12%

4 18%

3 10%

4 18%

Asian debt and currency crisis 1997–1998

Credit boom and banking crisis 1991–1993

High foreign currency debt and FX pegged to USD 1997–1998

Subprime crisis 2008–2010

Hungary

USSR dissolution 1990–1993

Ukraine

Subprime crisis 2008

1 15%

€bn 2011 2012E 2013E 2014E 2015E 2016E

Budget revenue 87.9 85.0 79.1 79.2 79.8 82.7

Budget expenditures (92.6) (87.9) (79.1) (76.4) (76.8) (77.6)

Primary balance (4.7) (2.9) 0.0 2.8 5.7 9.0

% of GDP (2.2%) (1.5%) 0.0% 1.5% 3.0% 4.5%

Interest expense (14.9) (10.1) (8.4) (9.0) (9.9) (10.2)

Budget balance (19.6) (13.0) (8.4) (6.2) (4.1) (1.2)

% of GDP (9.1%) (6.7%) (4.5%) (3.4%) (2.2%) (0.6%)

€bn 2011 2012E 2013E 2014E 2015E 2016E Import 61.5 54.2 51.2 49.7 49.7 50.5

Goods 47.5 41.9 39.7 38.5 38.4 38.9

Services 14.0 12.3 11.5 11.2 11.3 11.6

Exports 48.8 49.4 50.6 52.2 54.5 57.1

Goods 20.2 21.7 22.2 22.7 23.3 24.0

Services 28.6 27.7 28.4 29.5 31.2 33.1

Trade balance (12.6) (4.8) (0.5) 2.4 4.8 6.5 Current account bal. (20.6) (8.1) (2.3) (0.5) 0.8 1.4 % GDP (9.9%) (4.2%) (1.2%) (0.3%) 0.4% 0.7%

5

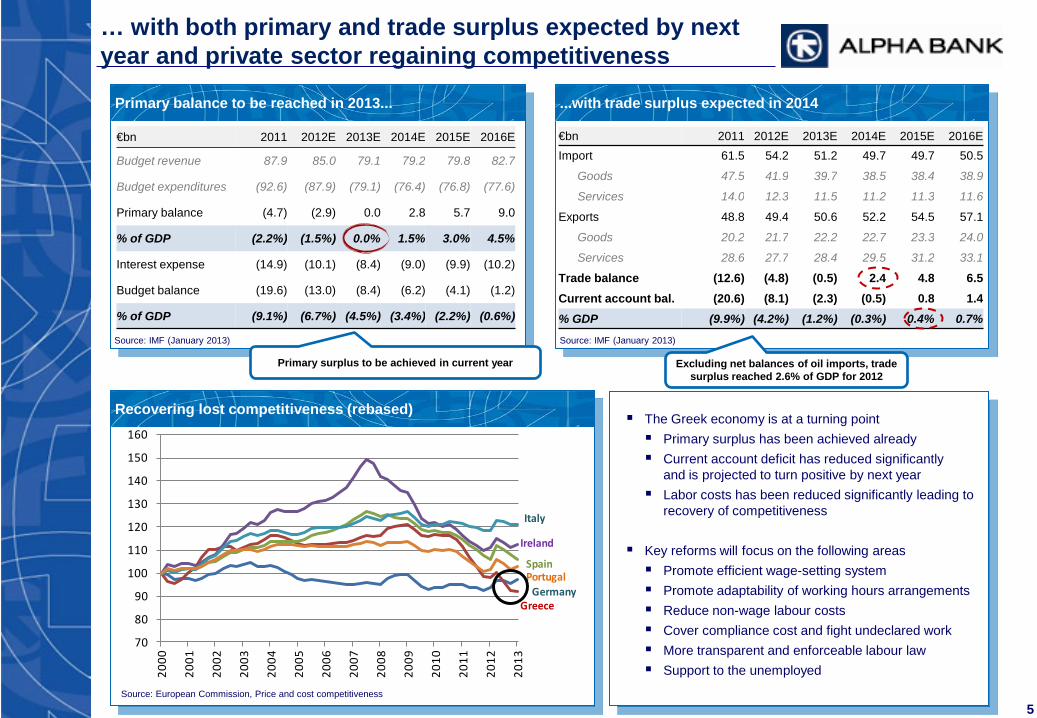

… with both primary and trade surplus expected by next year and private sector regaining competitiveness

Primary balance to be reached in 2013... ...with trade surplus expected in 2014

The Greek economy is at a turning point Primary surplus has been achieved already Current account deficit has reduced significantly

and is projected to turn positive by next year Labor costs has been reduced significantly leading to

recovery of competitiveness

Key reforms will focus on the following areas Promote efficient wage-setting system Promote adaptability of working hours arrangements Reduce non-wage labour costs Cover compliance cost and fight undeclared work More transparent and enforceable labour law Support to the unemployed

Excluding net balances of oil imports, trade surplus reached 2.6% of GDP for 2012

Primary surplus to be achieved in current year

Source: IMF (January 2013) Source: IMF (January 2013)

70

80

90

100

110

120

130

140

150

160

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Germany

Italy

Ireland

SpainPortugal

Greece

Source: European Commission, Price and cost competitiveness

Recovering lost competitiveness (rebased)

Date Target Foreign investor Deal value

(€mm) Sale considerations Sector

Pending DEPA Gazprom, Sintez n.d. Sale expected during H1’13 Energy (Gas and Pipeline networks)

Pending OPAP Fosun, German Operators ~700 Sale of 33% stake, current mkt cap. €2.2bn Football Prognostics Organization

Mar-13 Dolphin Third Point, Monarch ~74 Backstopped Convertible Bonds Real estate developer

Feb-13 Kassiopi/Corfu NCH Capital 100¹ Privatization sale by HRADF of concession rights for 99 years Real estate development plan in Corfu

Feb-13 M.J. Maillis Grace Bay Holdings c.10 Share capital increase International packaging operator

Jan-13 Opap Baupost Group 106² Stake building of 5.2% Greek lottery under privatization

Jan-13 Eurodrip Paine & Partners 70 Completed MTO Irrigation and farming management

Jan-13 S&B Rhône Capital 115 Tender offer for 39% of the capital Mining

Dec-12 Folli follie TPG Axon 43 c.6.8% stake acquired from Piraeus Semi-luxury retailer

Oct-12 Dolphin nina Third Point 45 Share capital increase Real estate developer

Oct-12 Folli follie Dufry group 500 51% stake in Hellenic Durty Free shop Greek duty free shops

6

Improving fundamentals are already attracting certain international investment into selected sectors …

Recent pick up in activity demonstrated also by Hewlett-Packard (HP) and

Chinese shipping company Cosco agreement to distribute regional

supplies through the Greek port of Piraeus which would become its

European regional hub

Piraeus Port, the next European hub?

Recent completed transactions with foreign investments inflows

Visible pick up in tourism activity

(23.0%)

9.5%

(5.2%)

7.0%

2009 2010 2011 2012

Visitor exports real growth (%)

Source: WTTC Travel & Tourism Economic Impact 2013

Source: Company information, Press Releases, Factiva

7

Greek issuers have also re-accessed the international markets, albeit at expensive re-entering levels

Benchmark bond yield compared to Portugal Recent bond issues in Greece

0

5

10

15

20

25

30

35

Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12 Jan-13

Greece

Portugal

10.8%

Greek debt swap Second bail-out

package approved

6.1%

Greece and Portugal benchmark 10 year bond yield evolution

10 42 51

99 76

19

53

102

2007 2008 2009 2010 2011¹ 2012

Eurosystem funding reliance of Greek banks

ELA (€bn)

ECB (€bn)

Company 1 Company 2 Company 3

Date Dec-12 Jan-13 Jan-13

Amount US$250mm €200mm €700mm

Term 8 years 4 years 5 years

Yield (%) 9.875% 8.75% 7.875%

130 122

Limited in crease in absolute terms of Eurosystem funding reliance since 2010, negative

impact due to mix effect Source: Dataquery

Source: Company information, Factiva

Source: Bank of Greece ¹ For 2011 ELA includes NFA

Portugal and Greece benchmark bond yields both peaked towards mid-2012 on the back of the increased sovereign concerns

Recent easing on sovereign risk has lead to a significant decrease in sovereign bond yields

However, Greek yields still at c.4.5% spread vs. Portuguese

8

Greek debt is consolidated in the official sector which acknowledges the wide ranging set of reforms that the country has implemented

Projections for Greek public debt Eurogroup statement on conditional further support

Greek debt composition (FY 2012 estimate)

Eurogroup statement on Greece “The Eurogroup in particular welcomes the updated assessment of the Troika that Greece has implemented in a satisfactory manner a wide ranging set of reforms, as well as the budget for 2013 and an ambitious medium term fiscal strategy 2013-16.(…) Euro area Member States will consider further measures and assistance, including inter alia lower co-financing in structural funds and/or further interest rate reduction of the Greek Loan Facility, if necessary, for achieving a further credible and sustainable reduction of Greek debt-to-GDP ratio (…) As was stated by the Eurogroup on 21 February 2012, we are committed to providing adequate support to Greece during the life of the programme and beyond until it has regained market access, provided that Greece fully complies with the requirements and objectives of the adjustment programme.”

November 27, 2012

Source: IMF; ¹ Includes subsector debt net of intra-government holdings

90

110

130

150

170

190

210 20

02

2003

20

04

2005

20

06

2007

20

08

2009

20

10

2011

20

12

2013

20

14

2015

20

16

2017

20

18

2019

20

20

2021

20

22

Historical evolution November 2012 agreement (latest projections)

March 2012 programme April 2010 programme

Post debt buy-back 2012

% GDP

IMF estimate €bn % total General government (State) 307.2 100% Tbills 18.4 6% Official sector 183.6 60% IMF 22.3 7% European Commission 161.3 53% Exchanged bonds 29.9 10% Non-exchanged bonds 56.3 18% Loans 18.0 6% Other¹ 1.0 0%

175% 124% <110% Eurogroup targets

Greece’s current debt maturities

5.3 3.5

1.3 3.0

10.3 7.4

2.5

Q2 Q3 Q4 Q1 Q2 Q3 Q4

Quarterly (€bn)

2013 2014

Source: European Commission

Source: European Commission

Source: IMF, Bank of Greece, European Commission

Agenda

1. Macroeconomic Update: First Signs of Stabilisation and FDI

2. Consolidated Banking Sector and Returning Confidence

3. Emporiki Acquisition Bringing Significant Benefits

4. Solid 2012 Performance Despite Multiple Headwinds and Technical Effects

36%

32%

23%

3%

2% 1% 1% 1% 1%

10

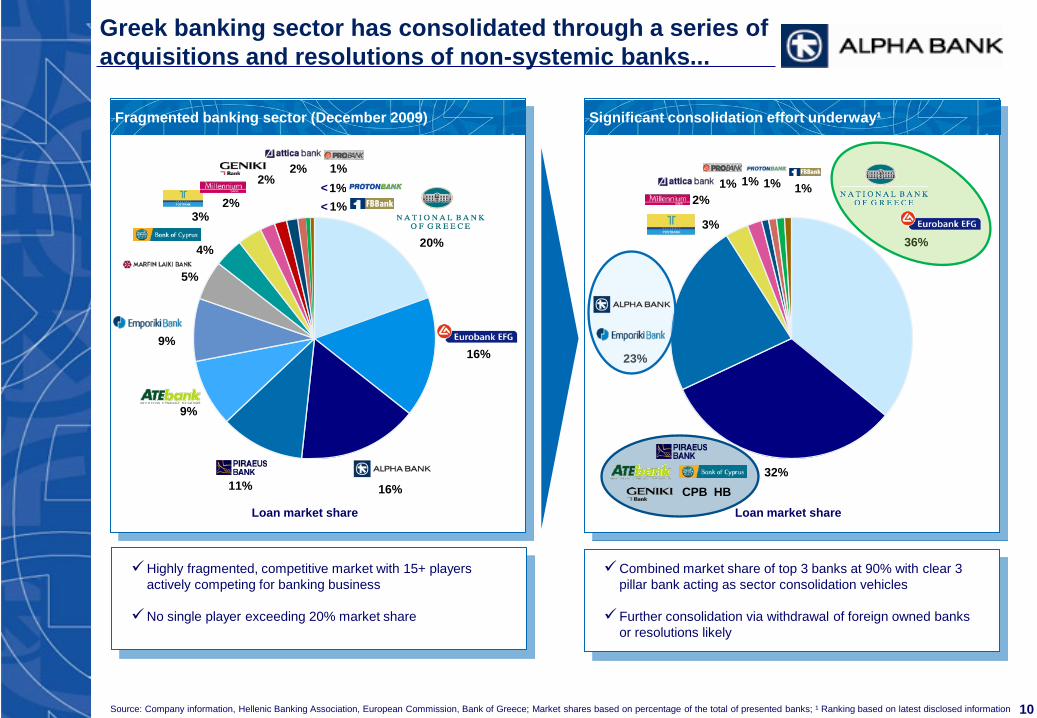

Greek banking sector has consolidated through a series of acquisitions and resolutions of non-systemic banks...

Fragmented banking sector (December 2009) Significant consolidation effort underway¹

Source: Company information, Hellenic Banking Association, European Commission, Bank of Greece; Market shares based on percentage of the total of presented banks; ¹ Ranking based on latest disclosed information

Combined market share of top 3 banks at 90% with clear 3 pillar bank acting as sector consolidation vehicles

Further consolidation via withdrawal of foreign owned banks or resolutions likely

20%

16%

16%

11%

9%

9%

5%

4%

3%

2%

2%

2%

1% 1% 1%

< <

CPB HB

Loan market share Loan market share

Highly fragmented, competitive market with 15+ players actively competing for banking business

No single player exceeding 20% market share

11

... which is expected to lead to improved deposit margins

Greek System Deposits (Bank of Greece)

160 175 198

228 238 210

174 165 151 154 161 161

Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Jan-13

(€ bn)

7%

Deposits in Greece decreased significantly between Dec-09

and mid ’12

However, reversal of deposit trends following June elections

with Alpha Bank outperforming the market by more than

10%, a testament to the returning confidence to the Greek

banking sector overall and Alpha Bank in particular

Time deposit pricing levels

Consolidation and regained access to Eurosystem

liquidity improved the situation towards the end of 2012

Market is expected to normalise further with a gradual

easing of margin pressure further 2013 and beyond

Consolidation of banking sector expected to lead to

improved deposit pricing

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Dec-09 Apr-10 Aug-10 Dec-10 Apr-11 Aug-11 Dec-11 Apr-12 Aug-12 Dec-12

Average interest rate on new euro-denominated time deposits

Source: Bank of Greece, Bloomberg

1.2%

3.4%

4.4% 4.2%

Up to 130bps deposit cost increase between mid-2010 and mid-2011 as competition for funding increased

Retail Corporate

4.7%

5.0%

3.7%

2.1%

Source: Bank of Greece

(37%)

Deposits/Nominal GDP

Eurozone: 115%

Greece: 83% Compared to +18%

for Alpha Bank

0.2% 0.7%

1.6%

Euribor 3M

360 150 118 43

240

50 76 7

600

200 194 50

12

Furthermore, consolidator banks are projected to realise significant synergies, further improving the profitability of the sector

Key measures announced by the newly formed groups:

Cost synergies

o Footprint optimisation (branch network, ATMs, etc.)

o Reduction in central functions

o Business units realignment (streamline centralised functions, IT and operations, procurement)

Funding and revenue synergies

o Lower funding costs through re-pricing of deposit base and mix

o Recovery improvement through additional client base attraction

o New cross-selling and up-selling opportunities

o Increase of fee-based business for corporate customers

Source: Company information, Investor Presentations ¹ Based on Company information (Eurobank and NBG based on Greece segement for 9M’12 annualized, Emporiki and Alpha based on Investor Presentation disclosure, Piraeus based on LTM Mar-12 figures, ATEbank based on 9M’11 annualized figures, Geniki implied cost base FY’11 based on Piraeus Investor Presentation)

Announced synergies

Announced combined synergies for recent Greek bank mergers amount to €1bn

Cost synergies represent the largest part of the announced savings, amounting to a total of c.€0.7bn or c.65% of total synergies

Funding and revenue synergies amount to c.€370mm or c.35% of total synergies

Pre-tax, fully phased synergies per annum (€mm)

Funding and revenue synergies

Cost synergies

18%

Cost synergies, % combined cost base

12% 12% 4%

€ 2.0bn € 1.2bn € 1.0bn € 1.1bn

Combined cost base¹

Key announced measures

Agenda

1. Macroeconomic Update: First Signs of Stabilisation and FDI

2. Consolidated Banking Sector and Returning Confidence

3. Emporiki Acquisition Bringing Significant Benefits

4. Solid 2012 Performance Despite Multiple Headwinds and Technical Effects

0.9

2.3

2.9

(1.5)

Dec-11 share capital

CASA capital injection

FY12 losses

Emporiki Equity

14

Emporiki transaction has significantly enhanced Alpha Bank’s capital position

Emporiki capital position (€bn) Credit Agricole capital increases of Emporiki (€mm)

850 989

2,000

2,905

2009 2010 2011 2012

5,019 Stock of provisions

Emporiki transaction brings a net benefit of €2.3bn to Alpha Bank as of December 2012

Significant capital buffer created by Credit Agricole reflected in strong provision buffer

Stock of balance sheet provisions close to €5bn, exceeding 25% of the total gross loan book

€bn

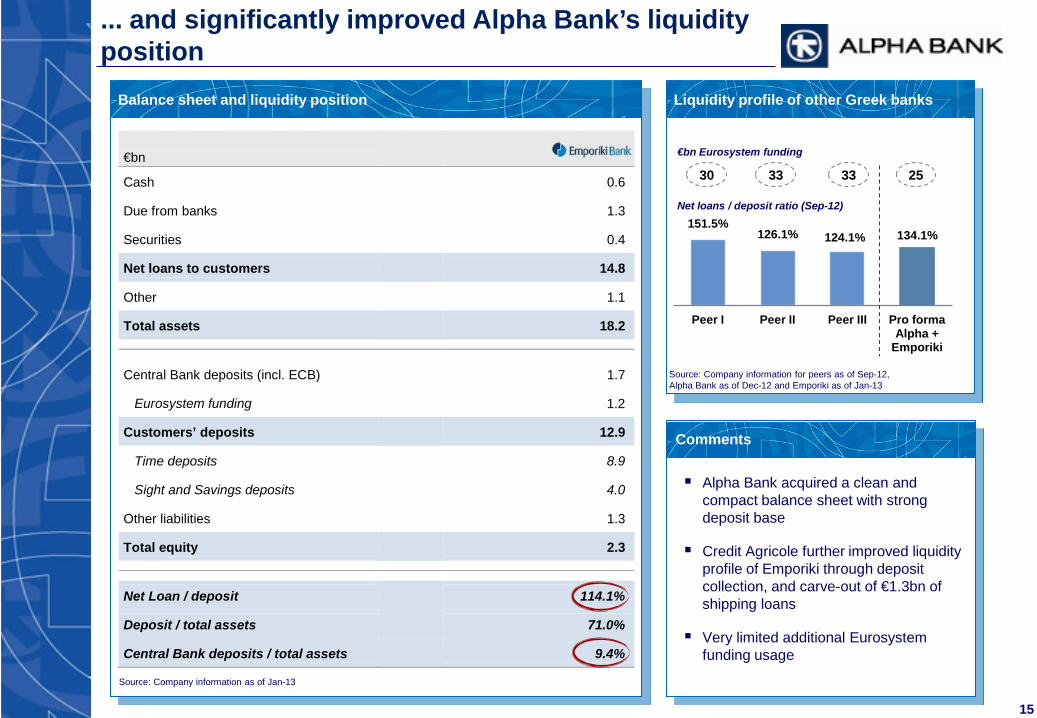

Cash

0.6

Due from banks

1.3

Securities

0.4

Net loans to customers

14.8

Other

1.1

Total assets

18.2

Central Bank deposits (incl. ECB)

1.7

Eurosystem funding

1.2

Customers’ deposits

12.9

Time deposits

8.9

Sight and Savings deposits

4.0

Other liabilities

1.3

Total equity

2.3

Net Loan / deposit

114.1%

Deposit / total assets

71.0%

Central Bank deposits / total assets

9.4%

15

... and significantly improved Alpha Bank’s liquidity position

Balance sheet and liquidity position

Source: Company information as of Jan-13

Liquidity profile of other Greek banks

151.5% 126.1% 124.1% 134.1%

Peer I Peer II Peer III Pro forma Alpha +

Emporiki

Net loans / deposit ratio (Sep-12)

30 33 33

€bn Eurosystem funding

Alpha Bank acquired a clean and compact balance sheet with strong deposit base

Credit Agricole further improved liquidity profile of Emporiki through deposit collection, and carve-out of €1.3bn of shipping loans

Very limited additional Eurosystem funding usage

25

Source: Company information for peers as of Sep-12, Alpha Bank as of Dec-12 and Emporiki as of Jan-13

Comments

16

Emporiki’s loan portfolio is well provided for with NPLs covered by 61%

Greece 96%

Cyprus 4%

Consumer 10.7%

Total gross loans: €19.8bn

Business 52.0%

Mortgage 37.3%

Emporiki loan book

By type

By country

Emporiki NPLs and provision coverage by type (Dec-12)

Coverage of non-performing loans exceeding 60%

NPL ratio as of December 2012 of 41.8% which compares to Alpha Bank NPL of 22.8% with a 45% cash coverage

Well diversified loan book

Greece accounting for 97% of total gross loan portfolio with Cyprus representing 3%

€mm Gross loans Provisions Net loans NPL ratio Coverage

ratio

Business Loans 10,279 2,995 7,284 38.4% 76.0%

Mortgages 7,384 1,088 6,295 40.4% 36.4%

Consumer 2,123 936 1,187 63.6% 69.3%

Total 19,785 5,019 14,766 41.8% 60.6%

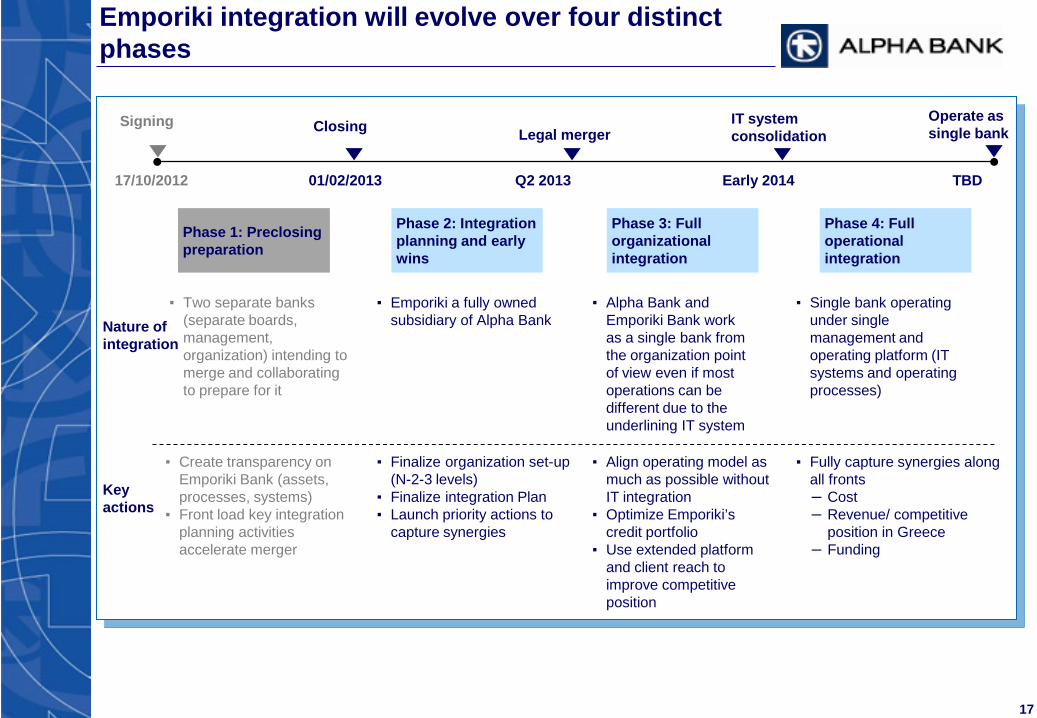

Emporiki integration will evolve over four distinct phases

▪ Two separate banks (separate boards, management, organization) intending to merge and collaborating to prepare for it

▪ Single bank operating under single management and operating platform (IT systems and operating processes)

▪ Emporiki a fully owned subsidiary of Alpha Bank Nature of

integration

Phase 1: Preclosing preparation

Phase 2: Integration planning and early wins

Phase 3: Full organizational integration

Phase 4: Full operational integration

Legal merger IT system consolidation

Operate as single bank

▪ Alpha Bank and Emporiki Bank work as a single bank from the organization point of view even if most operations can be different due to the underlining IT system

▪ Create transparency on Emporiki Bank (assets, processes, systems)

▪ Front load key integration planning activities accelerate merger

▪ Fully capture synergies along all fronts – Cost – Revenue/ competitive

position in Greece – Funding

▪ Finalize organization set-up (N-2-3 levels)

▪ Finalize integration Plan ▪ Launch priority actions to

capture synergies

Key actions

▪ Align operating model as much as possible without IT integration

▪ Optimize Emporiki’s credit portfolio

▪ Use extended platform and client reach to improve competitive position

17/10/2012 01/02/2013 Q2 2013 Early 2014 TBD

Signing Closing

17

Estimate of synergies raised to €265mn as integration progresses successfully

Total

100-140

Network re-organization/ rebranding

10-15

IT integration

30-35

Platform rightsizing

60-90

Year 3 (2015)

165-195

Year 2 (2014)

130-150

Year 1 (2013)

20-30

Total estimate Phasing

0

Year 3 (2015) Year 2 (2014)

70-95

Year 1 (2013)

30-45

Cost synergies fully phased-in in year 3

Note: Synergies and integration costs are pre tax 18

(€ million)

Year 3 (2015)

75-95

Year 2 (2014)

50-65

Year 1 (2013)

20-25

Cost synergies

Funding and revenue

synergies

Integration costs

Total

165-195

Non-branch related

130-150

Branch related

35-45

Total

75-95

Revenue synergies

45-55

Funding synergies

30-40

Agenda

1. Macroeconomic Update: First Signs of Stabilisation and FDI

2. Consolidated Banking Sector and Returning Confidence

3. Emporiki Acquisition Bringing Significant Benefits

4. Solid 2012 Performance Despite Multiple Headwinds and Technical Effects

Key Developments and Results Highlights for FY 2012

EBA CTI at 12.8%, pro-forma for €4.6bn recapitalization and the €150mn convertible bond issued by

Alpha Bank and subscribed by CASA. Including Emporiki, EBA CTI stands at pro-forma 13.7%.

Reversal of negative trend in deposits with inflows of €2.2bn in Q4 2012, and further increasing by

€1.2bn in the first two months of 2013

Central Banks funding decreased by €1.7bn for the quarter and further by €4.5bn at the end of February

2013

NPLs at 22.8%, backed by €4.6bn of on-balance sheet provisions, yielding 45% cash coverage or 123%

inclusive of collaterals

FY2012 impairments rise to €1.7bn from €1.1bn, up 47.6% yoy to address asset quality deterioration

Net losses at €1.1bn, including extraordinary costs of €125.1mn and the pre-tax trading loss of €288.3mn

from the recognition of the new GGBs at their market value at the transaction date

20

21

FY 2012 Performance Highlights

Romania

Pro forma FY 12 with Emporiki 31.01.2013 FY 12 FY 11 Change %

(€ billion)

Net Loans 55.5 40.5 44.9 (9.8%)

Deposits 41.3 28.5 29.4 (3.2%)

Accumulated Provisions 9.6 4.6 2.9 60.9%

Common Shareholders’ Tangible Equity 2.1 (0.5) 0.3 n.m.

Assets 76.5 58.4 59.1 (1.3%)

(€ million)

Operating Income 1,502.7 2,283.8 (34.2%)

Operating Expenses1 (1,053.6) (1,096.3) (3.9%)

Pre-Provision Income2 681.4 1,045.2 (34.8%)

Impairment Losses on credit risk (1,668.9) (1,130.3) 47.6%

Profit/ (Loss) after tax excluding trading losses from new GGBs and impairment on PSI eligible portfolio1,3 (747.1) 21.4 …

Impairment Losses on PSI 0.0 (3,831.4) …

Profit / (Loss) after tax attributable to Shareholders (1,086.3) (3,810.2) (71.5%)

1 Excluding extraordinary costs of €125.1mn 2 Excluding trading result and extraordinary costs 3 Adjusted for the trading loss of €288.3mn resulting from the recognition of new GGBs at their market value at the transaction date

22

Capital Adequacy of Alpha Bank – Emporiki

Alpha Emporiki

Group RWAs development Alpha – Emporiki Total CAD Built up

14.5% 14.4% 13.7% (€ billion)

EBA Core Tier I Build up

5.2 (4.1)

0.3 (0.9) 0.15

4.6 5.3

2.6

7.9

EBA Core Tier I 31/03/2011

PSI losses LME Period losses Convertible bond

HFSF EBA Core Tier I Emporiki contribution

EBA Core Tier I 31/12/2012

Alpha

10.9% 12.8%

13.7% (€ billion)

(1) Emporiki’s total contribution as of 31.01.2013

(1)

12.8% 14.5% 13.7%

0.4% 0.3% 0.5% 0.4%

Alpha Emporiki Group

Core Tier I (EBA) Tier I Total CAD

37.8

57.6

0.6 3.2

15.0 0 1.0

Credit Market Operational Credit Market Operational Total Group RWA

23

Operating performance impacted by higher funding cost and cost of deposits

Central Bank Funding Average Balances and Cost

(€mm)

(€bn)

Pre-Provision Income Build-up (excl. Trading and OPEX one-offs)

(€mm)

1,045

(386)

(22)

1 43 681

FY 11 Δ NII Δ Fees Δ Other Δ OPEX FY 12

Net Interest Income Movement

1Excluding Fees

13.7 13.5 12.2 5.2 0.6

5.8 9.6 11.1 19.1 24.2

19.5 23.2 23.3 24.3 24.8

1.90% 1.83% 1.96% 2.36%

2.70%

Q4 11 Q1 12 Q2 12 Q3 12 Q4 12

ELA

ECB

Funding Cost

1

1,784 83

(122)

(353)

6 1,397

FY 11 Loans Deposits Funding Cost

Bonds & Other

FY 12

(386mn)

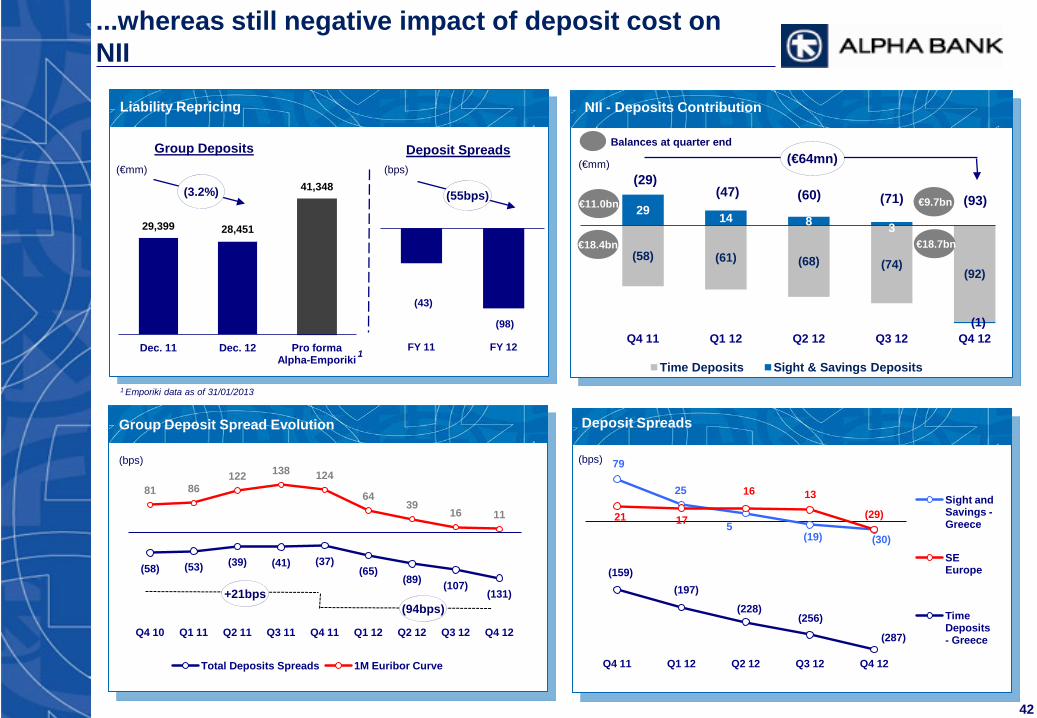

Repricing and overall portfolio focus led to increased interest income from loans, but more than outweighted by rising funding and deposit costs, particularly in the second half of the year

Net interest income decline in FY12 mainly due to higher funding costs (up €353mm from FY11) and increased cost of deposits (up €122mm from FY11)

Underlying trends specific to 2012 adverse macroeconomic situation and banking sector consolidation; some of those trends have already reversed in 2013

Comments

24

Net interest income expected to improve significantly over the medium term

Improved funding mix Capital increase supporting NII

Positive base effect in NII from substitution of wholesale funding from ELA to ECB (c.2% of ELA base)

Normalisation of time deposit pricing: min 0.5% on €20bn curve gain on loans

Yield on capital raise (on the remaining capital bridge of €1,629mn on top of two tranches which have been received over the last year)

Improving time deposit pricing

13.5 13.3

8.4

23.7 5.9

2011 2012 Feb-13

1,900

1,042

1,629

1st HFSF Recap Tranche

(28/5/12)

2nd HFSF Recap Tranche

(21/12/12)

Remaining amount for full recapitalisation

14.1

27.2

41.3

2012

(159)

(197) (228)

(256) (287) (350)

(300)

(250)

(200)

(150)

(100)

(50)

0 Q4 Q1 Q2 Q3 Q4

Time deposits spreads-Greece

Eurosystem funding evolution (€ billion)

€21.9bn €23.7bn

ELA funding (+NFA for 2011) ECB funding

Additional NII support from remaining €1.6bn capital increase following two

HFSF advances in 2012

(€ million)

Greek deposits (€billion) Pro forma for Emporiki

Time

Sight & Saving

2011 2012 2013

bps

Comments

€19.2bn

Buffer w/o Emporiki

7.7

12.7

Buffer incl. Emporiki

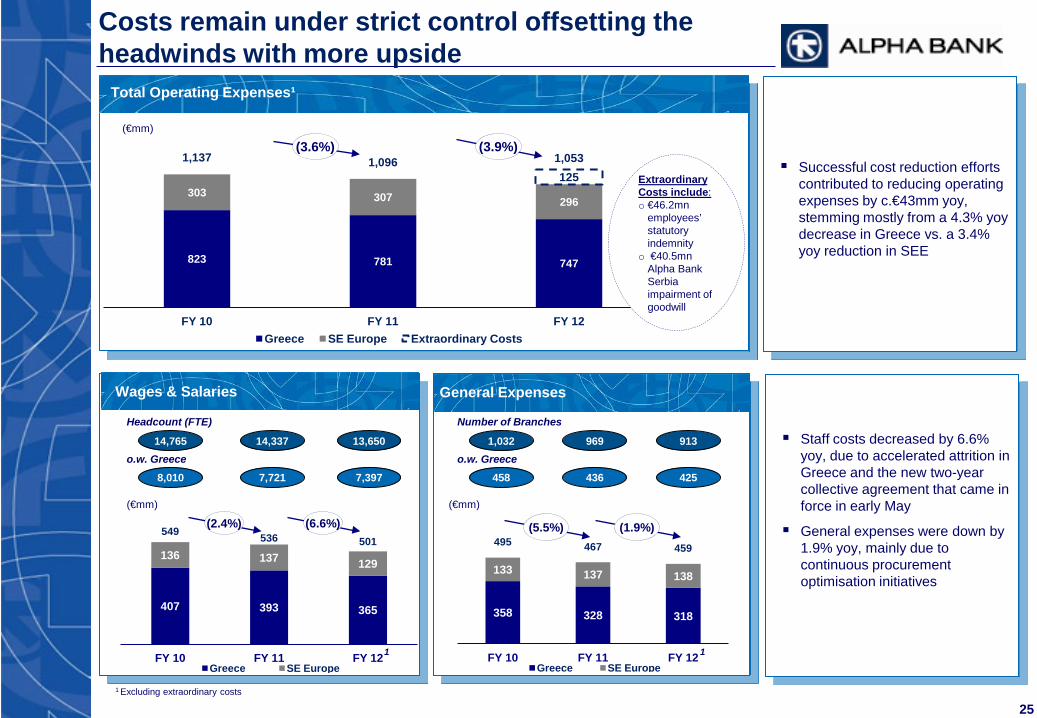

358 328 318

133 137 138

495 467 459

FY 10 FY 11 FY 12 Greece SE Europe

25

Total Operating Expenses¹

Wages & Salaries General Expenses

Costs remain under strict control offsetting the headwinds with more upside

823 781 747

303 307 296

125 1,137 1,096 1,053

FY 10 FY 11 FY 12 Greece SE Europe Extraordinary Costs

407 393 365

136 137 129

549 536 501

FY 10 FY 11 FY 12 Greece SE Europe

(1.9%)

(3.9%) (€mm)

(€mm)

(6.6%)

1

1 Excluding extraordinary costs

Successful cost reduction efforts contributed to reducing operating expenses by c.€43mm yoy, stemming mostly from a 4.3% yoy decrease in Greece vs. a 3.4% yoy reduction in SEE

Staff costs decreased by 6.6% yoy, due to accelerated attrition in Greece and the new two-year collective agreement that came in force in early May

General expenses were down by 1.9% yoy, mainly due to continuous procurement optimisation initiatives

(3.6%)

(2.4%) (5.5%)

Headcount (FTE)

14,765 14,337 13,650

Number of Branches

1,032 969 913

8,010 7,721 7,397 458 436 425 o.w. Greece o.w. Greece

(€mm)

1

Extraordinary Costs include: o €46.2mn

employees’ statutory indemnity

o €40.5mn Alpha Bank Serbia impairment of goodwill

Stabilizing economic environment led to a decreased NPL formation of 190bps in Q4

Coverage increased to 45% or 123% when including collaterals

NPL formation

Stabilizing Economic Environment led to a Decreased NPL Formation in Q4, while Increasing Coverage at 45%

26

90 100 130

200 200

250 270

190

Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12

(bps)

NPL ratio 22.8%2

1 Adjusted for the PSI+ impact on state guaranteed loans 2 NPL ratio at 28.6% pro forma with Emporiki

1 1

1

Group NPLs and Coverage (without Emporiki)

6.4

3.0

2.7

0.7

1.2

0.9

10.3

4.6

NPLs Impairment Allowances Collateral

Business Loans Mortgages Consumer Credit

78%

45%

123% (€bn)

Coverage

186 204 215 235 250 275

345 392

440

Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12

(bps)

1 1

1

Loan Loss Provisions

Pre-crisis (2004-2008) 5Y Average: 91bps

Comments

Agenda

Appendix

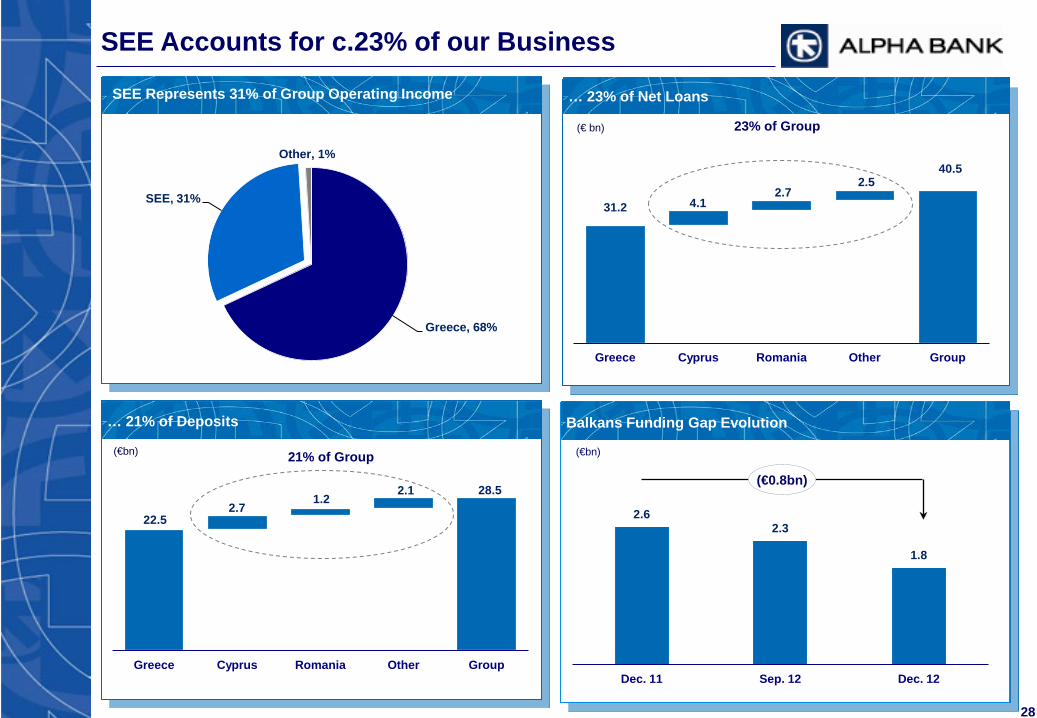

SEE Operations Overview

Greece, 68%

SEE, 31%

Other, 1%

31.2 4.1 2.7

2.5 40.5

Greece Cyprus Romania Other Group

22.5 2.7

1.2 2.1 28.5

Greece Cyprus Romania Other Group

28

SEE Accounts for c.23% of our Business

… 23% of Net Loans

… 21% of Deposits

(€ bn) 23% of Group

SEE Represents 31% of Group Operating Income

Balkans Funding Gap Evolution

2.6 2.3

1.8

Dec. 11 Sep. 12 Dec. 12

(€bn) 21% of Group (€bn)

(€0.8bn)

29

Loans 4,578 0.4% 3,025 (7.9%) 742 (12.6%) 780 (11.5%) 375 (5.2%) 69 (5.3%) 9,681 (4.6%)

Mortgages 2,112 (0.1%) 903 3.3% 160 (1.2%) 199 1.6% 102 (8.1%) 16 (5.9%) 3,501 0.6%

Consumer Credit

257 (8.9%) 204 (10.3%) 68 (9.9%) 158 (18.4%) 7 (14.2%) 25 (15.9%) 781 (11.4%)

Businesses 2,208 2.1% 1,918 (12.2%) 513 (16.0%) 423 (14.0%) 266 (3.8%) 28 6.7% 5,399 (6.7%)

Deposits 2,658 (0.3%) 1,241 7.0% 341 (5.5%) 585 2.3% 468 5.4% 69 8.8% 5,421 2.1%

Cyprus Bulgaria Romania Serbia Albania FYROM TOTAL Δ% Δ% Δ% Δ% Δ% Δ% Δ% (€mm)

Dec. 2012 yoy yoy yoy yoy yoy yoy yoy

SEE: Deleveraging in Progress

30

Operating Income 174.2 (12.5%) 152.6 (14.7%) 49.4 26.8% 41.1 (9.1%) 20.8 7.8% 4.2 (26.6%) 462.6 (8.2%)

Operating Expenses (pre-O/H allocation)

63.7 3.6% 85.6 (7.4%) 33.6 (1.4%) 40.4 (8.3%) 14.3 (5.4%) 8.2 0.3% 260.0 (2.9%)

Impairment Losses

164.8 25.9% 88.9 19.5% 38.3 40.6% 15.7 44.3% 4.6 (46.2%) 0.2 (81.6%) 314.2 23.7%

Profit Before Tax (pre- O/H allocation)

(54.3) … (21.9) … (22.5) 0.9% (15.0) 54.6% 1.9 … (4.1) 22.1% (111.6) …

Loan Market Share

6.4% 6.2% 2.8% 4.5% 9.4% 1.9%

NPL Ratio 23.6% 13.8% 21.7% 17.2% 16.5% 30.4% 19.4% +695bps

Branches 31 150 88 134 42 19 487 -45

Employees 833 2,123 819 1,433 385 242 6,190 -360

(€mm) Cyprus Bulgaria Romania Serbia Albania FYROM SE Europe Δ% Δ% Δ% Δ% Δ% Δ% Δ%

Dec. 2012 yoy yoy yoy yoy yoy yoy yoy

SEE: Performance Affected by Deleveraging and Impairments

Agenda

Appendix

Greece macro economy overview

The Green k Shoots Of Recovery

70

80

90

100

110

120

130

140

150

160

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Germany

Italy

Ireland

SpainPortugal

Greece

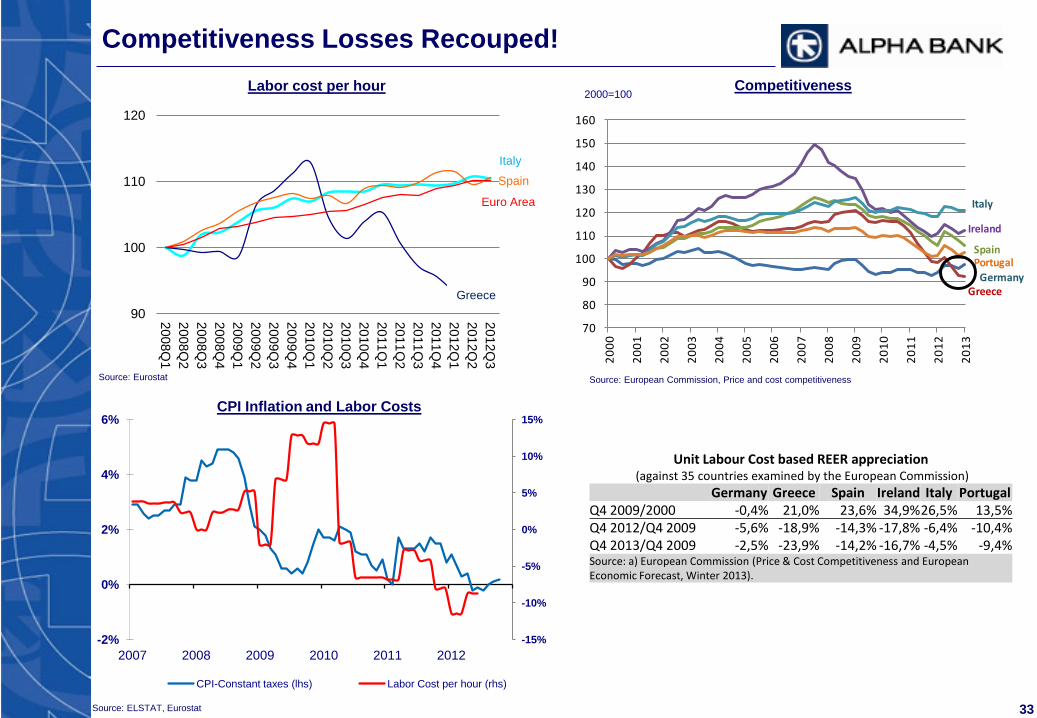

Competitiveness Losses Recouped! Labor cost per hour Competitiveness

Source: Eurostat

2000=100

Source: European Commission, Price and cost competitiveness

90

100

110

120

2008Q1

2008Q2

2008Q3

2008Q4

2009Q1

2009Q2

2009Q3

2009Q4

2010Q1

2010Q2

2010Q3

2010Q4

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

Greece

Spain

Euro Area

Italy

Unit Labour Cost based REER appreciation (against 35 countries examined by the European Commission)

Germany Greece Spain Ireland Italy Portugal Q4 2009/2000 -0,4% 21,0% 23,6% 34,9% 26,5% 13,5% Q4 2012/Q4 2009 -5,6% -18,9% -14,3% -17,8% -6,4% -10,4% Q4 2013/Q4 2009 -2,5% -23,9% -14,2% -16,7% -4,5% -9,4% Source: a) European Commission (Price & Cost Competitiveness and European Economic Forecast, Winter 2013).

-15%

-10%

-5%

0%

5%

10%

15%

-2%

0%

2%

4%

6%

2007 2008 2009 2010 2011 2012

CPI-Constant taxes (lhs) Labor Cost per hour (rhs)

CPI Inflation and Labor Costs

Source: ELSTAT, Eurostat 33

External Balance Restored!

External Balance

60

80

100

120

140

160

2007 2008 2009 2010 2011 2012

Value of Exports of Goods Greece

Value of Imports of Goods Greece

Value of Exports of Goods EuroArea

2007=100

Source: Bank of Greece

15,4 14,1 13,3

9,6 10,5 10,0

12,2 14,0 14,6

13,617,3 17,6

31,8 30,124,1

Non-OilExports

Shipping

Tourism

OilImports

2011 2012

Non-Oil Imports

2010

2010 2011 2012 Exports of goods and services as % of GDP 20.5% 23.4% 25.4% yoy % change 7.7% 7.2% 0.6% Non-oil Imports of goods and services as % of GDP 21.2% 21.2% 18.8% yoy % change -5.5% -6.1% -17.6% Imports of oil as % of GDP 6.1% 8.3% 9.0% Current Account Deficit* in € bn 20.4 18.8 3.3 as % of GDP 9.2% 8.6% 1.7% Source: Bank of Greece, ELSTAT * including capital tranfers

-4%

-2%

0%

2%

4%

6%

8%

10%

2007 2008 2009 2010 2011 2012 2013 Industrial Goods Services

Tradables vs Non-Tradables Inflation

* Net of EU transfers and Income Balance

(In € bn)

34

Structural Adjustment: A Star Is Born!

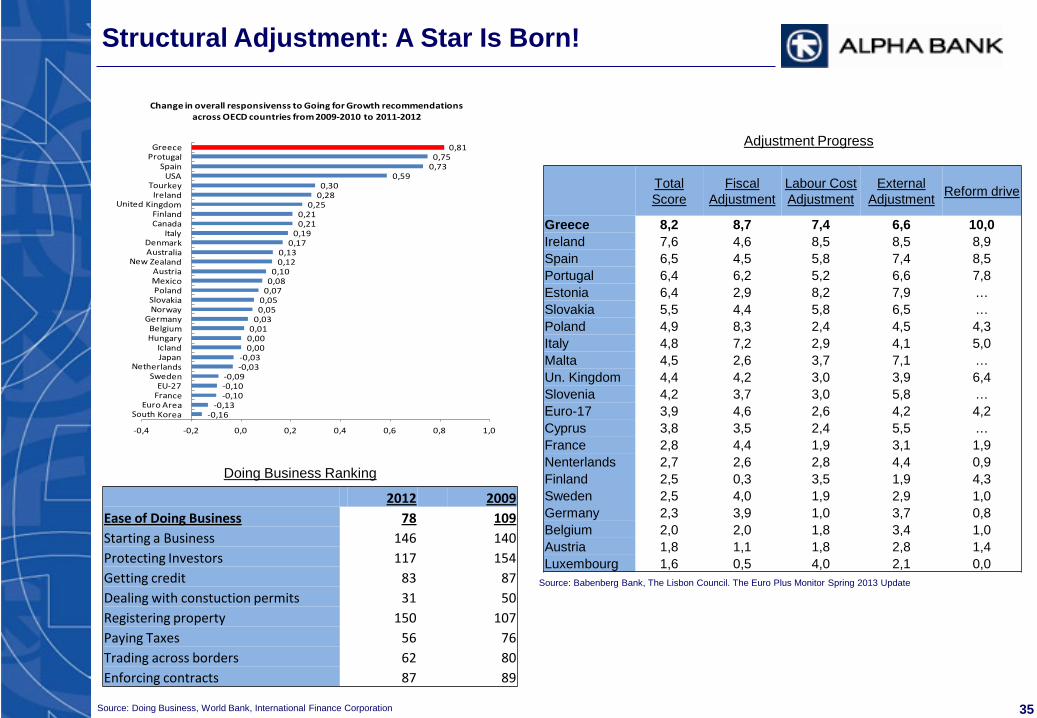

Doing Business Ranking

Source: Doing Business, World Bank, International Finance Corporation

Source: OECD, Going for Growth, 2013

Adjustment Progress

Source: Babenberg Bank, The Lisbon Council. The Euro Plus Monitor Spring 2013 Update

-0,16-0,13

-0,10-0,10-0,09

-0,03-0,03

0,000,000,010,030,050,050,070,080,10

0,120,13

0,170,19

0,210,21

0,250,280,30

0,590,730,75

0,81

-0,4 -0,2 0,0 0,2 0,4 0,6 0,8 1,0

Change in overall responsivenss to Going for Growth recommendations across OECD countries from 2009-2010 to 2011-2012

2012 2009 Ease of Doing Business 78 109 Starting a Business 146 140 Protecting Investors 117 154 Getting credit 83 87 Dealing with constuction permits 31 50 Registering property 150 107 Paying Taxes 56 76 Trading across borders 62 80 Enforcing contracts 87 89

Total Score

Fiscal Adjustment

Labour Cost Adjustment

External Adjustment Reform drive

Greece 8,2 8,7 7,4 6,6 10,0 Ireland 7,6 4,6 8,5 8,5 8,9 Spain 6,5 4,5 5,8 7,4 8,5 Portugal 6,4 6,2 5,2 6,6 7,8 Estonia 6,4 2,9 8,2 7,9 … Slovakia 5,5 4,4 5,8 6,5 … Poland 4,9 8,3 2,4 4,5 4,3 Italy 4,8 7,2 2,9 4,1 5,0 Malta 4,5 2,6 3,7 7,1 … Un. Kingdom 4,4 4,2 3,0 3,9 6,4 Slovenia 4,2 3,7 3,0 5,8 … Εuro-17 3,9 4,6 2,6 4,2 4,2 Cyprus 3,8 3,5 2,4 5,5 … France 2,8 4,4 1,9 3,1 1,9 Nenterlands 2,7 2,6 2,8 4,4 0,9 Finland 2,5 0,3 3,5 1,9 4,3 Sweden 2,5 4,0 1,9 2,9 1,0 Germany 2,3 3,9 1,0 3,7 0,8 Belgium 2,0 2,0 1,8 3,4 1,0 Austria 1,8 1,1 1,8 2,8 1,4 Luxembourg 1,6 0,5 4,0 2,1 0,0

35

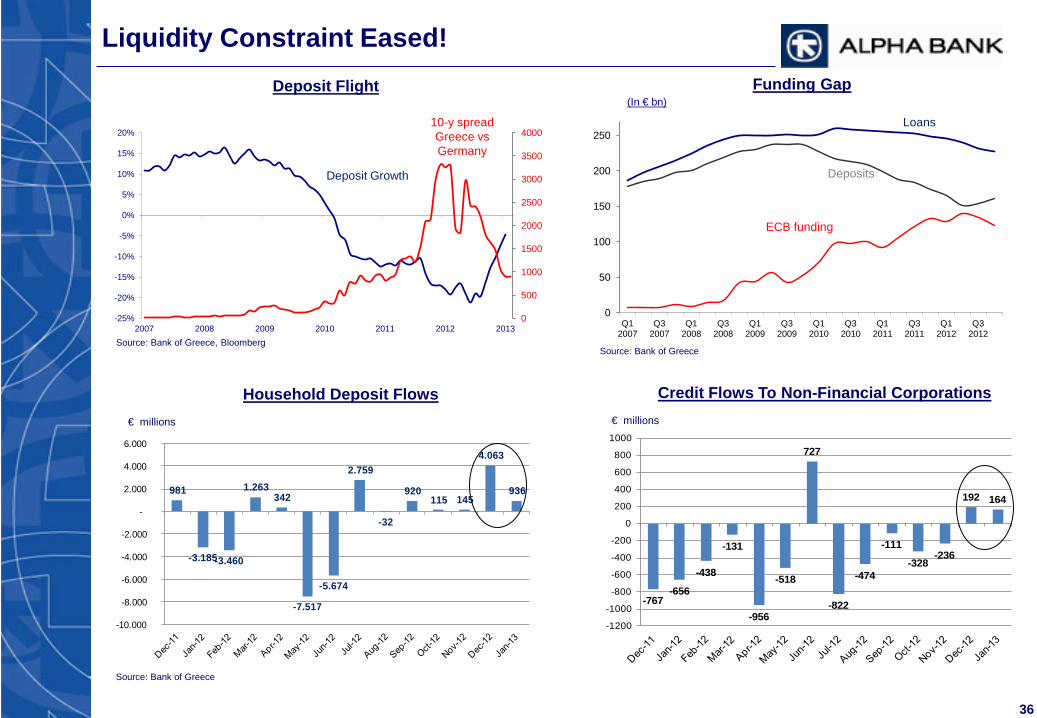

Liquidity Constraint Eased! Deposit Flight Funding Gap

0

500

1000

1500

2000

2500

3000

3500

4000

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2007 2008 2009 2010 2011 2012 2013

Deposit Growth

10-y spread Greece vs Germany

(In € bn)

Source: Bank of Greece Source: Bank of Greece, Bloomberg

ECB funding

0

50

100

150

200

250

Q1 2007

Q3 2007

Q1 2008

Q3 2008

Q1 2009

Q3 2009

Q1 2010

Q3 2010

Q1 2011

Q3 2011

Q1 2012

Q3 2012

Deposits

Loans

981

-3.185 -3.460

1.263 342

-7.517

-5.674

2.759

-32

920 115 145

4.063

936

-10.000

-8.000

-6.000

-4.000

-2.000

-

2.000

4.000

6.000

Household Deposit Flows € millions

Source: Bank of Greece

-767-656

-438

-131

-956

-518

727

-822

-474

-111

-328-236

192 164

-1200

-1000

-800

-600

-400

-200

0

200

400

600

800

1000

€ millions

Credit Flows To Non-Financial Corporations

36

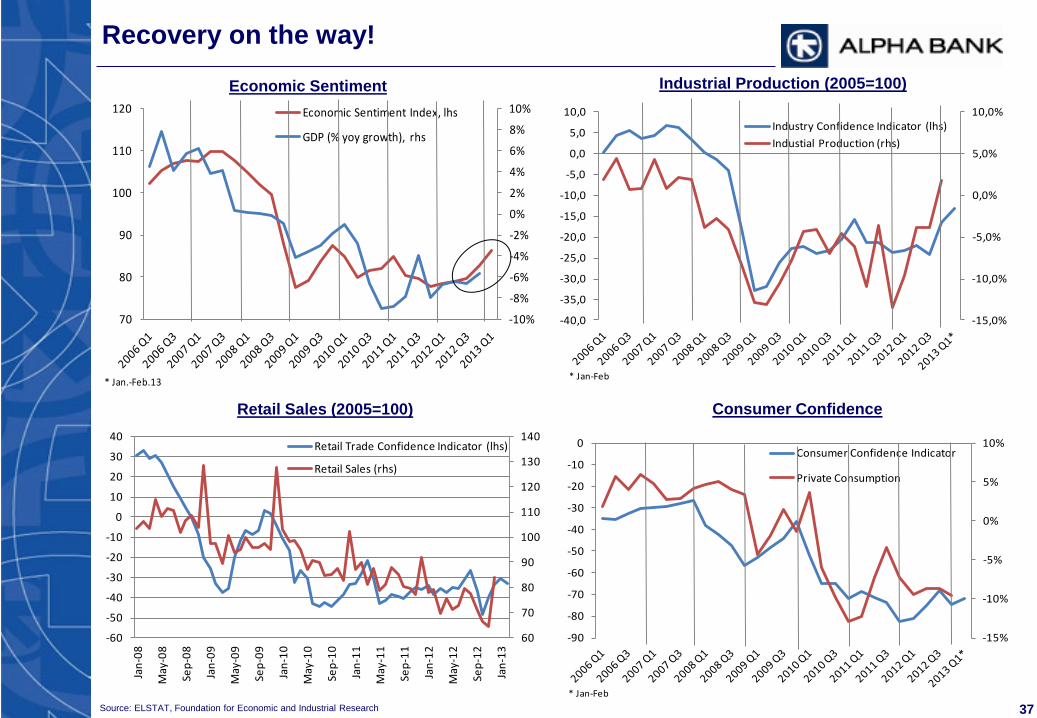

Recovery on the way!

Source: ELSTAT, Foundation for Economic and Industrial Research

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

70

80

90

100

110

120 Economic Sentiment Index, lhs

GDP (% yoy growth), rhs

* Jan.-Feb.13

Economic Sentiment

-15,0%

-10,0%

-5,0%

0,0%

5,0%

10,0%

-40,0

-35,0

-30,0

-25,0

-20,0

-15,0

-10,0

-5,0

0,0

5,0

10,0Industry Confidence Indicator (lhs)

Industial Production (rhs)

* Jan-Feb

Industrial Production (2005=100)

60

70

80

90

100

110

120

130

140

-60

-50

-40

-30

-20

-10

0

10

20

30

40

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

Retail Trade Confidence Indicator (lhs)

Retail Sales (rhs)

Retail Sales (2005=100) Consumer Confidence

-15%

-10%

-5%

0%

5%

10%

-90

-80

-70

-60

-50

-40

-30

-20

-10

0Consumer Confidence Indicator

Private Consumption

* Jan-Feb

37

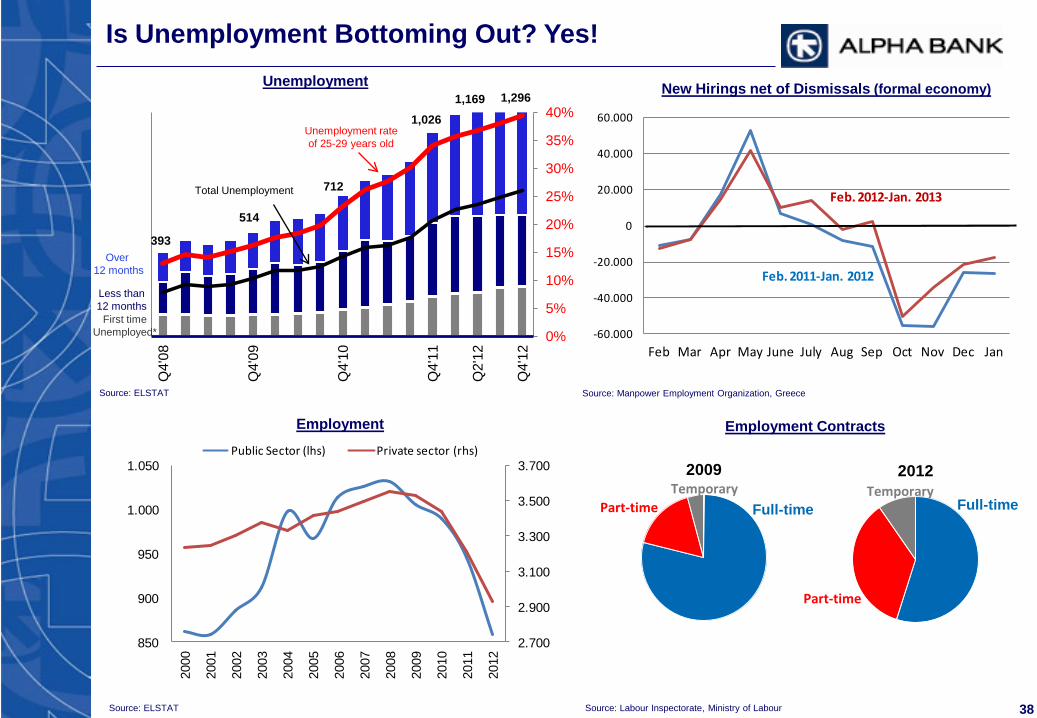

Is Unemployment Bottoming Out? Yes!

0%

5%

10%

15%

20%

25%

30%

35%

40%

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

1,000.0

1,100.0

1,200.0

1,300.0

1,400.0

Q4'

08

Q4'

09

Q4'

10

Q4'

11

Q2'

12

Q4'

12

Unemployment rate of 25-29 years old

Total Unemployment

Less than 12 months

First time Unemployed*

Over 12 months

393

514

712

1,026 1,169

Unemployment New Hirings net of Dismissals (formal economy)

Source: ELSTAT Source: Manpower Employment Organization, Greece

1,296

-60.000

-40.000

-20.000

0

20.000

40.000

60.000

Feb Mar Apr May June July Aug Sep Oct Nov Dec Jan

Feb. 2012-Jan. 2013

Feb. 2011-Jan. 2012

2.700

2.900

3.100

3.300

3.500

3.700

850

900

950

1.000

1.050

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Public Sector (lhs) Private sector (rhs)

Source: ELSTAT

2009

Full-time Temporary

Part-time

2012

Full-time Temporary

Part-time

Employment Employment Contracts

Source: Labour Inspectorate, Ministry of Labour 38

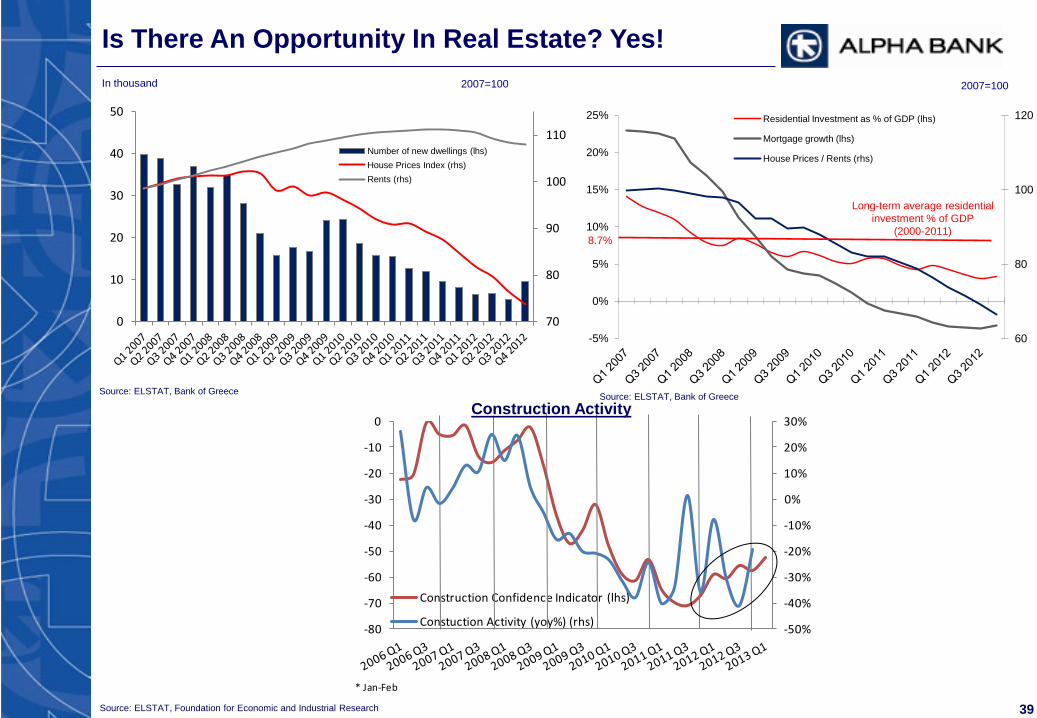

Is There An Opportunity In Real Estate? Yes!

60

80

100

120

-5%

0%

5%

10%

15%

20%

25% Residential Investment as % of GDP (lhs)

Mortgage growth (lhs)

House Prices / Rents (rhs)

Long-term average residential investment % of GDP

(2000-2011)

In thousand 2007=100

Source: ELSTAT, Bank of Greece Source: ELSTAT, Bank of Greece

2007=100

8.7%

70

80

90

100

110

0

10

20

30

40

50

Number of new dwellings (lhs) House Prices Index (rhs) Rents (rhs)

Source: ELSTAT, Foundation for Economic and Industrial Research

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

-80

-70

-60

-50

-40

-30

-20

-10

0

Construction Confidence Indicator (lhs)

Constuction Activity (yoy%) (rhs)

* Jan-Feb

Construction Activity

39

Agenda

Appendix

Financial Review

41

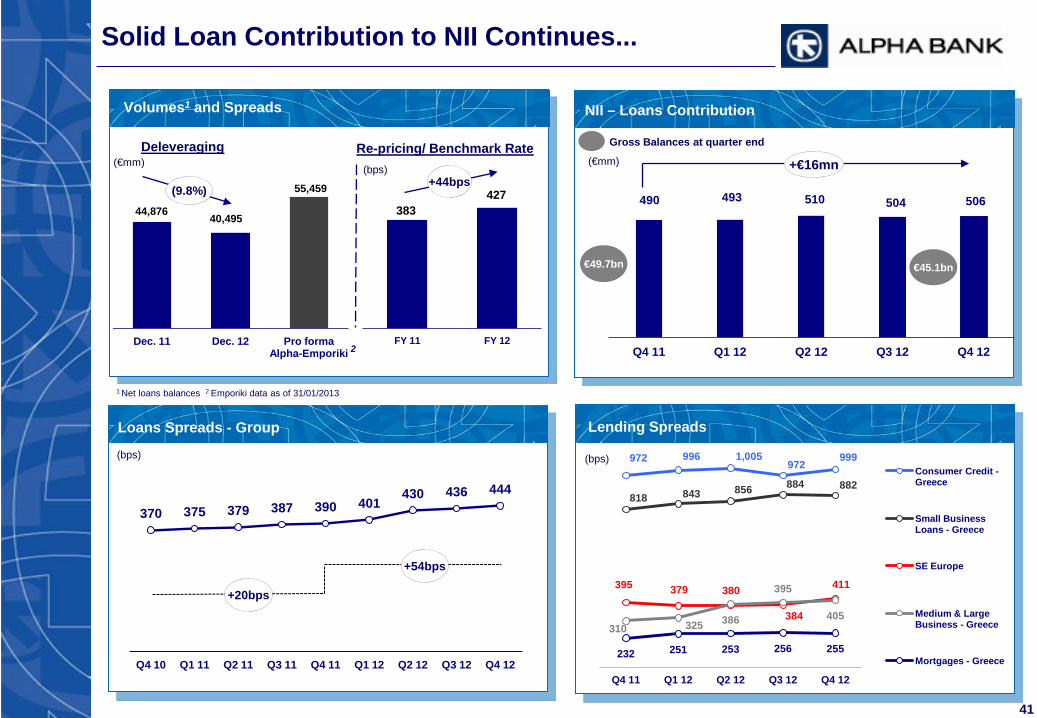

Solid Loan Contribution to NII Continues...

NII – Loans Contribution Volumes1 and Spreads

Gross Balances at quarter end

(bps)

Lending Spreads

Deleveraging Re-pricing/ Benchmark Rate

1 Net loans balances 2 Emporiki data as of 31/01/2013

Loans Spreads - Group

(bps)

44,876 40,495

55,459

Dec. 11 Dec. 12 Pro forma Alpha-Emporiki

972 996 1,005 972

999

818 843 856 884 882

395 379 380

384

411

310 325 386

395

405

232 251 253 256 255

Q4 11 Q1 12 Q2 12 Q3 12 Q4 12

Consumer Credit - Greece

Small Business Loans - Greece

SE Europe

Medium & Large Business - Greece

Mortgages - Greece

490 493 510 504 506

Q4 11 Q1 12 Q2 12 Q3 12 Q4 12

383 427

FY 11 FY 12

370 375 379 387 390 401 430 436 444

Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12

+20bps

+54bps

€49.7bn €45.1bn

(€mm) +€16mn

(9.8%)

(€mm) (bps)

+44bps

2

42

...whereas still negative impact of deposit cost on NII

NII - Deposits Contribution

Balances at quarter end

Deposit Spreads

Liability Repricing

(55bps)

Group Deposit Spread Evolution

29,399 28,451

41,348

Dec. 11 Dec. 12 Pro forma Alpha-Emporiki

(bps) (bps)

(€mm) Group Deposits Deposit Spreads

(€mm) (bps)

(3.2%)

(58) (61) (68) (74) (92)

29 14 8 3

(1) Q4 11 Q1 12 Q2 12 Q3 12 Q4 12

Time Deposits Sight & Savings Deposits

(43)

(98)

FY 11 FY 12

(58) (53) (39) (41) (37) (65)

(89) (107) (131)

81 86 122 138 124

64 39

16 11

Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12

Total Deposits Spreads 1M Euribor Curve

€11.0bn

€18.4bn

€9.7bn

€18.7bn

+21bps (94bps)

(€64mn)

(93) (29)

(71) (60) (47)

79

25

5 (19) (30)

21 17

16 13

(29)

(159) (197)

(228) (256)

(287)

Q4 11 Q1 12 Q2 12 Q3 12 Q4 12

Sight and Savings - Greece

SE Europe

Time Deposits - Greece

1

1 Emporiki data as of 31/01/2013

43

Group Wholesale Lending

(€ billion)

(€ billion)

(€ billion)

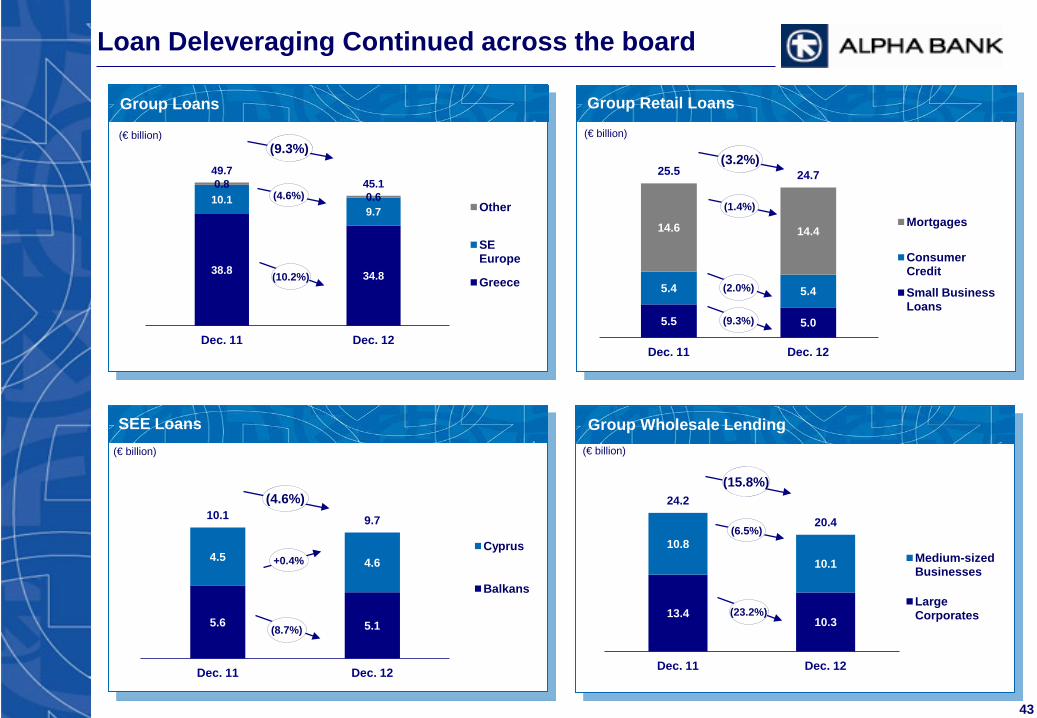

Loan Deleveraging Continued across the board

Group Loans Group Retail Loans

SEE Loans (€ billion)

38.8 34.8

10.1 9.7

0.8 0.6

49.7 45.1

Dec. 11 Dec. 12

Other

SE Europe

Greece

5.5 5.0

5.4 5.4

14.6 14.4

25.5 24.7

Dec. 11 Dec. 12

Mortgages

Consumer Credit

Small Business Loans

5.6 5.1

4.5 4.6

10.1 9.7

Dec. 11 Dec. 12

Cyprus

Balkans

13.4 10.3

10.8 10.1

24.2

20.4

Dec. 11 Dec. 12

Medium-sized Businesses

Large Corporates

(9.3%)

(10.2%)

(4.6%)

(3.2%)

(2.0%)

(1.4%)

(4.6%)

(8.7%)

+0.4%

(9.3%)

(15.8%)

(23.2%)

(6.5%)

44

Deposit inflows continued in the first months of 2013

Reversal of deposit trends in Greece following June elections with Alpha Bank outperforming the market

Stability of deposits abroad, despite negative developments in Greece

Alpha Bank deposit trends broadly in line with Greek system’s deposit evolution

Evolution of Alpha Bank Deposits

22.1

(2.3)

19.8

0.7

20.5

2.0

22.5

1.2

5.8 5.8 5.8

0.2

6.0

27.9 25.6 26.3

28.5

Mar. 12 Δ Q2 2012 Jun. 12 Δ Q3 2012 Sep. 12 Δ Q4 2012 Dec. 12 Δ Jan. & Feb. 13

Abroad

Greece

(€bn) (8.1%) qoq +2.6% qoq +8.3% qoq

Comments

45

Customer Assets

Deposit Evolution Breakdown

(€ billion) (€ million)

Core Deposits

Time Deposits:

Deposits Evolution – Group

10,996

(1,002) (421) (48)

194 9,719

Dec. 11 Q1 12 Q2 12 Q3 12 Q4 12 Dec. 12

18,403

(545) (1,832)

725 1,981 18,732

Dec. 11 Q1 12 Q2 12 Q3 12 Q4 12 Dec. 12

On Balance Sheet

Sight & Savings Deposits

Time Deposits Money Morket Mutual Funds

Other Mutual Funds

Private Banking

11.0 9.7

18.4 18.7

0.1 0.1

0.7 0.8

1.5 1.6

Dec.11 Dec. 12

Investment Balances

30.9 31.7

Liquidity

Transaction Balances

(2.5%)

(11.6%)

+1.8%

46

NII Impacted by Higher Funding Cost and Cost of Deposits

(€ million)

(€ million)

Group Net Interest Income

Net Fee & Commission Income Trading Income

Group NII decomposition (€ million)

429 450 451 453 414 365 334 284

Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12

(50) (34) (35) (29) (47) (60) (71) (93)

474 478 490 490 493 510 504 506

2.6% 2.8% 2.9% 3.0% 2.8% 2.6% 2.3% 2.0%

Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12

Loans

Deposits

NIM

1 Adjusted for the trading loss of €288.3mn resulting from the recognition of new GGBs at their market value at the transaction date

1

261.3 248.5

23.5 17.4

9.4 6.9

294.2 272.8

FY 11 FY 12 Investment Banking & Brokerage Asset Management Commercial & Corporate Banking

31.0 32.5

111.3

23.4

142.3

55.9

FY 11 FY 12

Foreign Exchange Bonds & Other

(21.7%)

1,784 1,397

(€ million) (7.3%)

47

(€ million) (€ million)

Mortgage Balances - Greece

Retail Lending

Consumer Credit Balances - Greece

Small Business Lending Balances - Greece

(€ million)

(€ million)

(€ million)

Stricter underwriting caused housing loans rejection rate to increase to 56% from 48% a year ago

New production mortgages LTV at 40%, total book average LTV at 54%

Consumer loan rejection rate at 71% from 69% a year ago

Comments

11,106 10,878

Dec. 11 Dec. 12

3,248 3,285

1,324 1,281

4,572 4,566

Dec. 11 Dec. 12

Credit cards

Consumer loans

1,970 1,695

2,659 2,520

4,629 4,215

Dec. 11 Dec. 12

Credit limits from € 150.000 to € 1 mn

Credit limits up to € 150.000

(0.1%)

(3.3%)

(8.9%)

(13.9%)

(5.2%)

(2.1%)

+1.1%

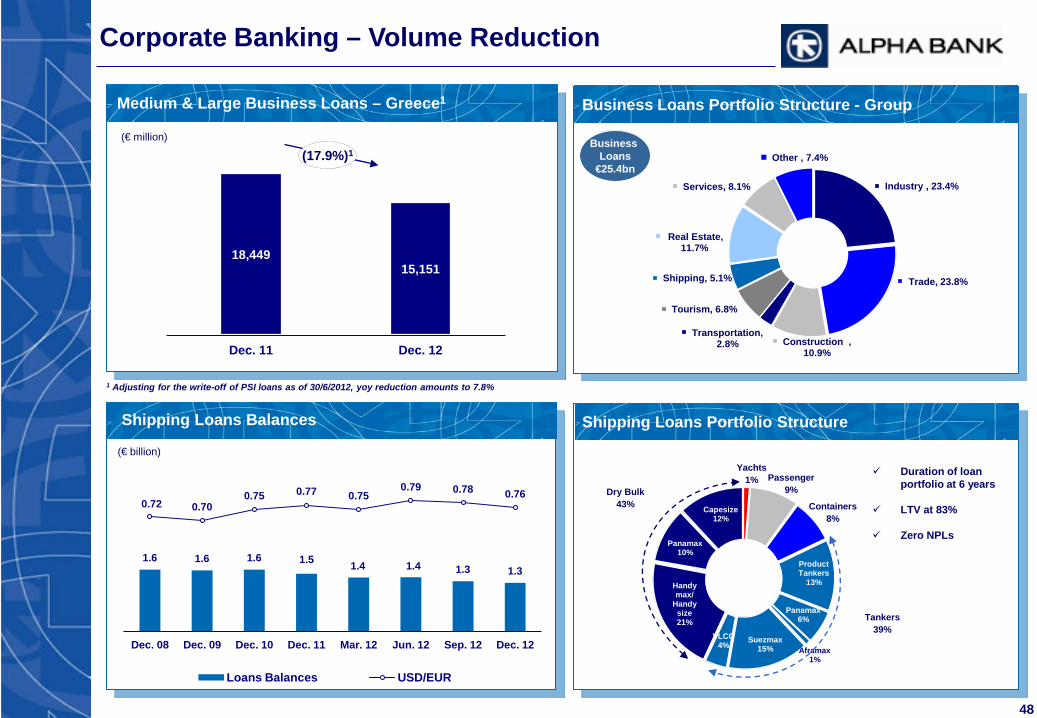

Product Tankers

13%

Panamax 6%

Aframax 1%

Suezmax 15%

VLCC 4%

Handy max/

Handy size 21%

Panamax 10%

Capesize 12%

Industry , 23.4%

Trade, 23.8%

Construction , 10.9%

Transportation, 2.8%

Tourism, 6.8%

Shipping, 5.1%

Real Estate, 11.7%

Services, 8.1%

Other , 7.4%

18,449 15,151

Dec. 11 Dec. 12

48

(€ million)

Medium & Large Business Loans – Greece1

Corporate Banking – Volume Reduction

(€ billion)

Business Loans Portfolio Structure - Group

Business Loans

€25.4bn

Duration of loan portfolio at 6 years

LTV at 83%

Zero NPLs

Shipping Loans Balances

Tankers 39%

Dry Bulk 43%

Shipping Loans Portfolio Structure

Yachts 1% Passenger

9%

Containers 8%

1.6 1.6 1.6 1.5 1.4 1.4 1.3 1.3

0.72 0.70 0.75 0.77 0.75

0.79 0.78 0.76

Dec. 08 Dec. 09 Dec. 10 Dec. 11 Mar. 12 Jun. 12 Sep. 12 Dec. 12

Loans Balances USD/EUR

1 Adjusting for the write-off of PSI loans as of 30/6/2012, yoy reduction amounts to 7.8%

(17.9%)1

49

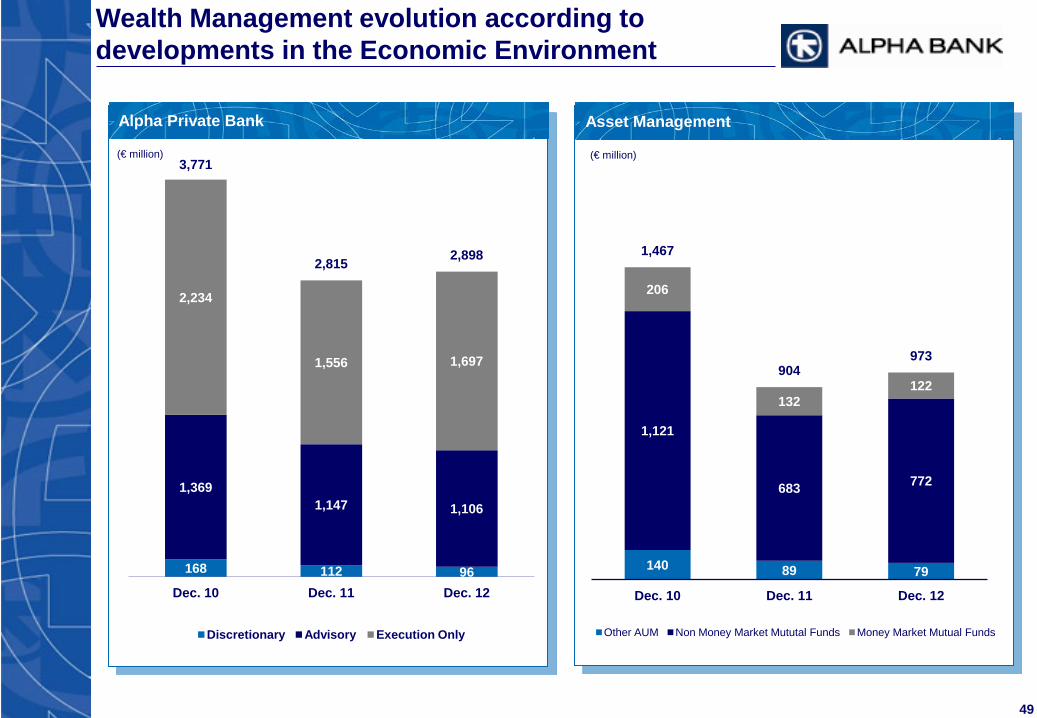

Wealth Management evolution according to developments in the Economic Environment

Asset Management Alpha Private Bank

(€ million) (€ million)

168 112 96

1,369 1,147 1,106

2,234

1,556 1,697

3,771

2,815 2,898

Dec. 10 Dec. 11 Dec. 12

Discretionary Advisory Execution Only

140 89 79

1,121

683 772

206

132 122

1,467

904 973

Dec. 10 Dec. 11 Dec. 12

Other AUM Non Money Market Mututal Funds Money Market Mutual Funds

Agenda

Appendix

Group Profit & Loss & Business Unit Financials

51

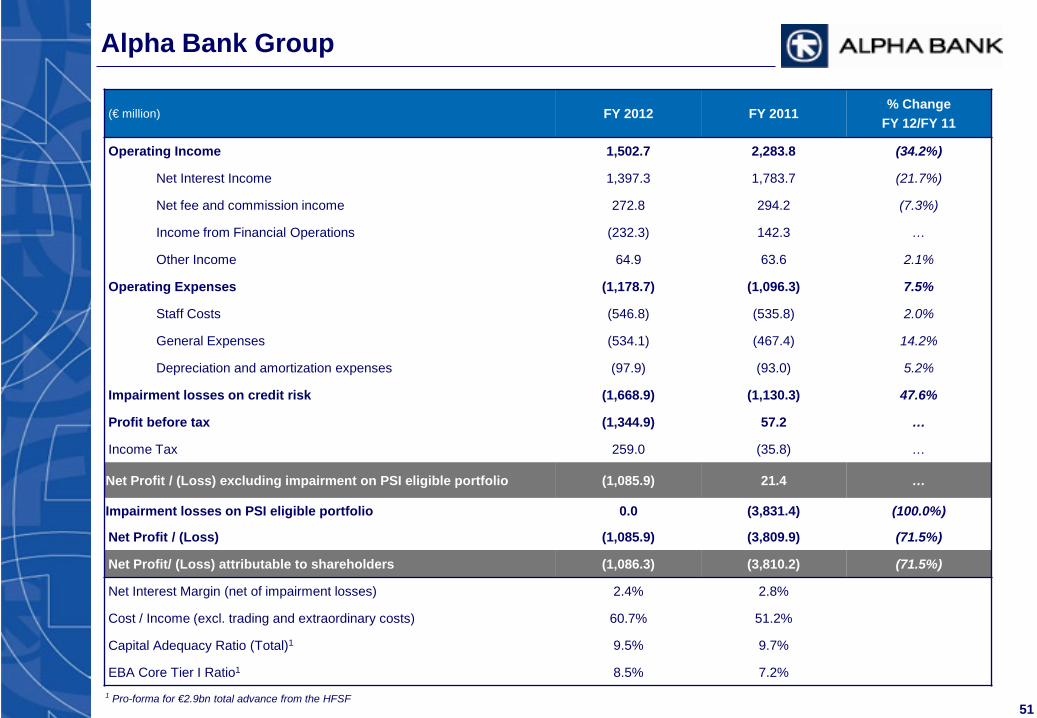

(€ million) FY 2012 FY 2011 % Change

FY 12/FY 11

Operating Income 1,502.7 2,283.8 (34.2%)

Net Interest Income 1,397.3 1,783.7 (21.7%)

Net fee and commission income 272.8 294.2 (7.3%)

Income from Financial Operations (232.3) 142.3 …

Other Income 64.9 63.6 2.1%

Operating Expenses (1,178.7) (1,096.3) 7.5%

Staff Costs (546.8) (535.8) 2.0%

General Expenses (534.1) (467.4) 14.2%

Depreciation and amortization expenses (97.9) (93.0) 5.2%

Impairment losses on credit risk (1,668.9) (1,130.3) 47.6%

Profit before tax (1,344.9) 57.2 …

Income Tax 259.0 (35.8) …

Net Profit / (Loss) excluding impairment on PSI eligible portfolio (1,085.9) 21.4 …

Impairment losses on PSI eligible portfolio 0.0 (3,831.4) (100.0%)

Net Profit / (Loss) (1,085.9) (3,809.9) (71.5%)

Net Profit/ (Loss) attributable to shareholders (1,086.3) (3,810.2) (71.5%)

Net Interest Margin (net of impairment losses) 2.4% 2.8%

Cost / Income (excl. trading and extraordinary costs) 60.7% 51.2%

Capital Adequacy Ratio (Total)1 9.5% 9.7%

EBA Core Tier I Ratio1 8.5% 7.2%

Alpha Bank Group

1 Pro-forma for €2.9bn total advance from the HFSF

52

(€ million) Q4 2012 Q3 2012 Q2 2012 Q1 2012 Q4 2011 Q3 2011 Q2 2011 Q1 2011

Operating Income 433.1 407.4 453.8 208.3 553.3 614.4 564.0 552.0

Net Interest Income 284.5 333.7 364.7 414.5 453.1 451.3 450.0 429.4

Net fee and commission income 74.6 64.8 68.8 64.5 77.7 72.2 74.4 69.9

Income from Financial Operations 56.5 (12.7) 6.0 (282.2) 10.2 76.0 20.1 35.9

Other Income 17.6 21.6 14.3 11.5 12.3 14.9 19.5 16.9

Operating Expenses (392.9) (259.2) (261.7) (264.8) (264.4) (275.6) (282.4) (273.9)

Staff Costs (167.0) (121.0) (127.8) (130.9) (132.0) (133.2) (137.0) (133.5)

General Expenses (197.1) (114.9) (111.0) (111.0) (109.0) (118.9) (122.7) (116.9)

Depreciation and amortization expenses (28.8) (23.3) (22.9) (22.9) (23.3) (23.5) (22.7) (23.5)

Impairment losses on credit risk (498.4) (450.0) (399.7) (320.7) (302.9) (295.2) (271.9) (260.3)

Profit before tax (458.2) (301.8) (207.6) (377.2) (13.9) 43.5 9.7 17.9

Income Tax 84.0 52.5 59.4 63.0 (6.3) (15.9) (6.3) (7.3)

Net Profit / (Loss) excluding impairment on PSI eligible portfolio (374.2) (249.3) (148.2) (314.2) (20.2) 27.6 3.4 10.5

Impairment losses on PSI eligible portfolio 0.0 0.0 0.0 0.0 (3,223.3) (69.4) (538.6) 0.0

Net Profit / (Loss) (374.2) (249.3) (148.2) (314.2) (3,243.5) (41.8) (535.2) 10.5

Net Profit / (Loss) attributable to shareholders (374.5) (249.3) (148.2) (314.2) (3,243.5) (41.9) (535.3) 10.5

Net Interest Margin (net of impairment losses) 2.0% 2.3% 2.6% 2.8% 3.0% 2.9% 2.8% 2.6%

Cost / Income (excluding trading and extraordinary costs) 71.1% 61.7% 58.4% 54.0% 48.7% 51.2% 51.9% 53.1%

Alpha Bank Group

53

(€ million) Retail Commercial &

Corporate SE Europe Investment Banking & Treasury

Asset Management Other Group

Jan-Dec Jan-Dec Jan-Dec Jan-Dec Jan-Dec Jan-Dec Jan-Dec 2012 2011 2012 2011 2012 2011 2012 2011 2012 2011 2012 2011 2012 2011

Operating Income 946.8 1,006.4 631.4 566.1 462.6 503.7 (246.3) 129.9 37.9 47.5 (329.7) 30.2 1,502.7 2,283.8

Net Interest Income 829.2 881.1 521.1 475.4 377.1 408.4 (343.4) 1.3 11.7 15.5 1.6 2.0 1,397.3 1,783.7

Net fee and Commission Income 106.3 117.7 97.0 84.1 49.0 62.0 (1.3) 1.9 22.1 28.8 (0.2) (0.4) 272.7 294.2

Income from Financial Operations 6.3 6.4 10.4 5.5 15.9 19.3 91.5 120.1 3.9 2.4 (360.3) (11.5) (232.3) 142.3

Other Income 5.0 1.1 3.0 1.1 20.6 13.9 6.9 6.7 0.3 0.7 29.1 40.1 64.9 63.6

Operating Expenses (524.1) (544.1) (129.2) (130.8) (296.6) (307.0) (20.8) (26.9) (27.2) (30.6) (180.7) (56.8) (1,178.7) (1,096.3)

Staff Costs (245.1) (261.4) (81.9) (88.8) (129.3) (137.4) (11.6) (13.6) (14.8) (15.5) (64.1) (19.1) (546.8) (535.8)

General Expenses (241.2) (245.3) (31.9) (31.3) (137.8) (137.1) (2.1) (3.2) (10.6) (13.0) (104.7) (28.7) (534.1) (467.4)

Depreciation (37.9) (37.4) (15.4) (10.7) (29.6) (32.5) (1.3) (1.4) (1.9) (2.1) (11.9) (9.0) (97.9) (93.0)

Impairment Losses (773.1) (466.3) (581.5) (410.0) (314.2) (254.1) 0.0 0.0 0.0 0.0 0.0 (4,788.9) (1,668.8) (5,919.2)

Profit / (Loss) before tax (350.5) (4.1) (79.3) 25.4 (148.3) (57.4) (267.1) 103.0 10.7 16.9 (510.4) (4,815.5) (1,344.9) (4,731.7)

Risk Adjusted Return on 8% Regulatory Capital (33%) 0% (6%) 2% (22%) (8%) (77%) 26% 16% 24% … … (43%) (92%)

Cost / Income Ratio (excl. trading and extraordinary costs) 56% 54% 20% 23% 66% 63% (6%) 273% 80% 68% 193% 136% 68% 51%

Group Results by Business Unit

54

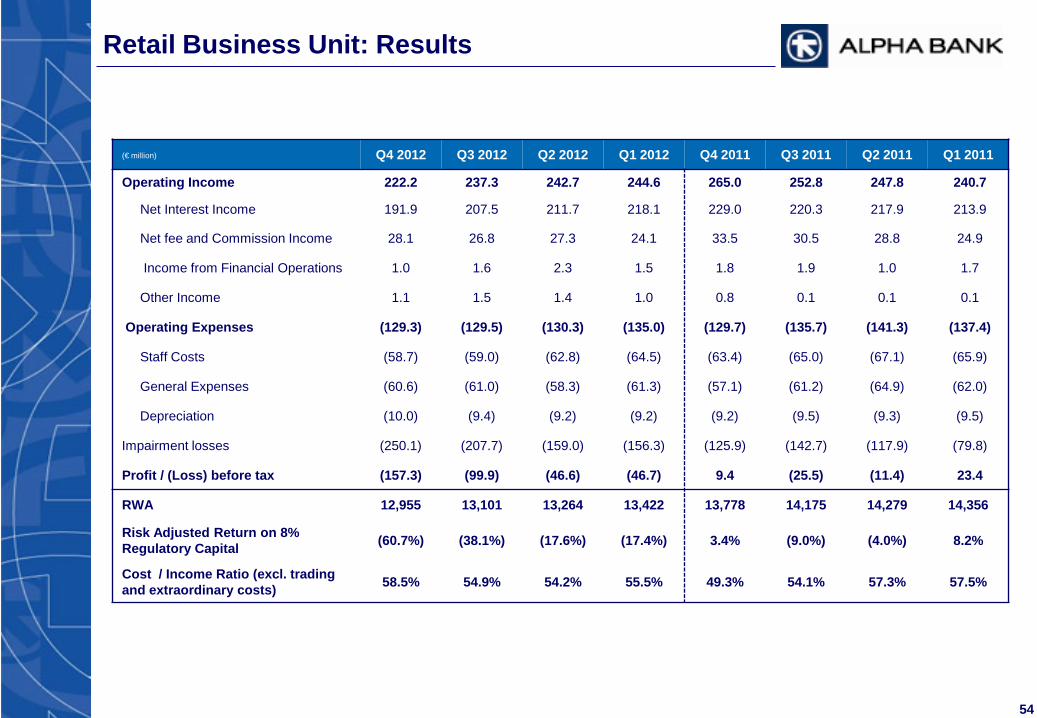

Retail Business Unit: Results

(€ million) Q4 2012 Q3 2012 Q2 2012 Q1 2012 Q4 2011 Q3 2011 Q2 2011 Q1 2011

Operating Income 222.2 237.3 242.7 244.6 265.0 252.8 247.8 240.7

Net Interest Income 191.9 207.5 211.7 218.1 229.0 220.3 217.9 213.9

Net fee and Commission Income 28.1 26.8 27.3 24.1 33.5 30.5 28.8 24.9

Income from Financial Operations 1.0 1.6 2.3 1.5 1.8 1.9 1.0 1.7

Other Income 1.1 1.5 1.4 1.0 0.8 0.1 0.1 0.1

Operating Expenses (129.3) (129.5) (130.3) (135.0) (129.7) (135.7) (141.3) (137.4)

Staff Costs (58.7) (59.0) (62.8) (64.5) (63.4) (65.0) (67.1) (65.9)

General Expenses (60.6) (61.0) (58.3) (61.3) (57.1) (61.2) (64.9) (62.0)

Depreciation (10.0) (9.4) (9.2) (9.2) (9.2) (9.5) (9.3) (9.5)

Impairment losses (250.1) (207.7) (159.0) (156.3) (125.9) (142.7) (117.9) (79.8)

Profit / (Loss) before tax (157.3) (99.9) (46.6) (46.7) 9.4 (25.5) (11.4) 23.4

RWA 12,955 13,101 13,264 13,422 13,778 14,175 14,279 14,356

Risk Adjusted Return on 8% Regulatory Capital (60.7%) (38.1%) (17.6%) (17.4%) 3.4% (9.0%) (4.0%) 8.2%

Cost / Income Ratio (excl. trading and extraordinary costs) 58.5% 54.9% 54.2% 55.5% 49.3% 54.1% 57.3% 57.5%

55

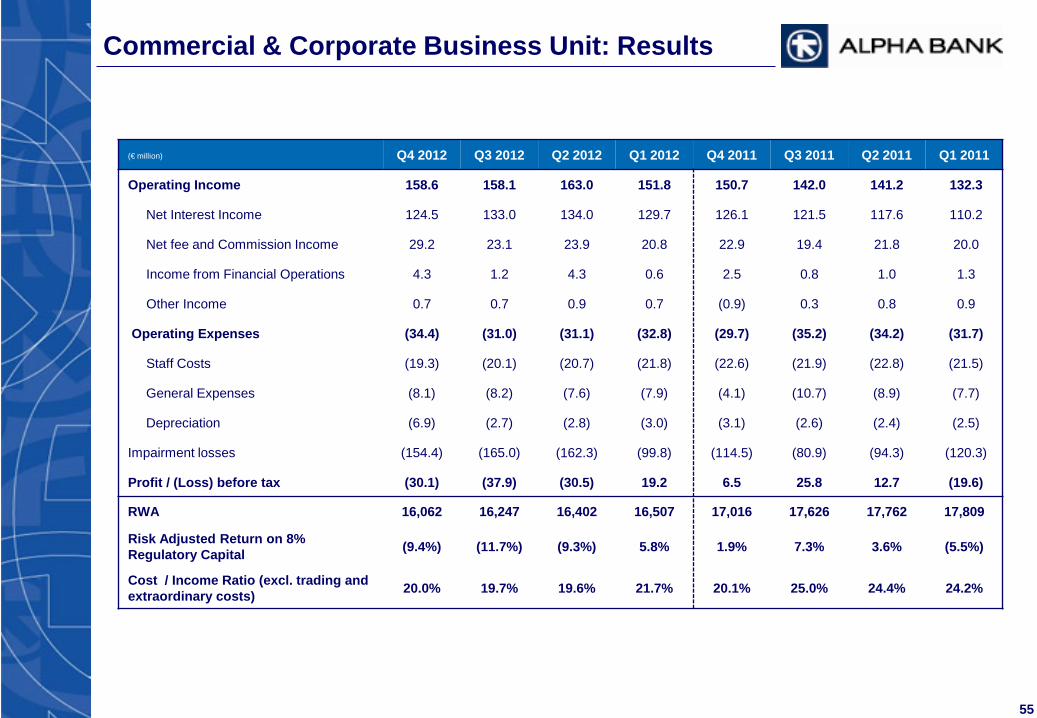

Commercial & Corporate Business Unit: Results

(€ million) Q4 2012 Q3 2012 Q2 2012 Q1 2012 Q4 2011 Q3 2011 Q2 2011 Q1 2011

Operating Income 158.6 158.1 163.0 151.8 150.7 142.0 141.2 132.3

Net Interest Income 124.5 133.0 134.0 129.7 126.1 121.5 117.6 110.2

Net fee and Commission Income 29.2 23.1 23.9 20.8 22.9 19.4 21.8 20.0

Income from Financial Operations 4.3 1.2 4.3 0.6 2.5 0.8 1.0 1.3

Other Income 0.7 0.7 0.9 0.7 (0.9) 0.3 0.8 0.9

Operating Expenses (34.4) (31.0) (31.1) (32.8) (29.7) (35.2) (34.2) (31.7)

Staff Costs (19.3) (20.1) (20.7) (21.8) (22.6) (21.9) (22.8) (21.5)

General Expenses (8.1) (8.2) (7.6) (7.9) (4.1) (10.7) (8.9) (7.7)

Depreciation (6.9) (2.7) (2.8) (3.0) (3.1) (2.6) (2.4) (2.5)

Impairment losses (154.4) (165.0) (162.3) (99.8) (114.5) (80.9) (94.3) (120.3)

Profit / (Loss) before tax (30.1) (37.9) (30.5) 19.2 6.5 25.8 12.7 (19.6)

RWA 16,062 16,247 16,402 16,507 17,016 17,626 17,762 17,809

Risk Adjusted Return on 8% Regulatory Capital (9.4%) (11.7%) (9.3%) 5.8% 1.9% 7.3% 3.6% (5.5%)

Cost / Income Ratio (excl. trading and extraordinary costs) 20.0% 19.7% 19.6% 21.7% 20.1% 25.0% 24.4% 24.2%

56

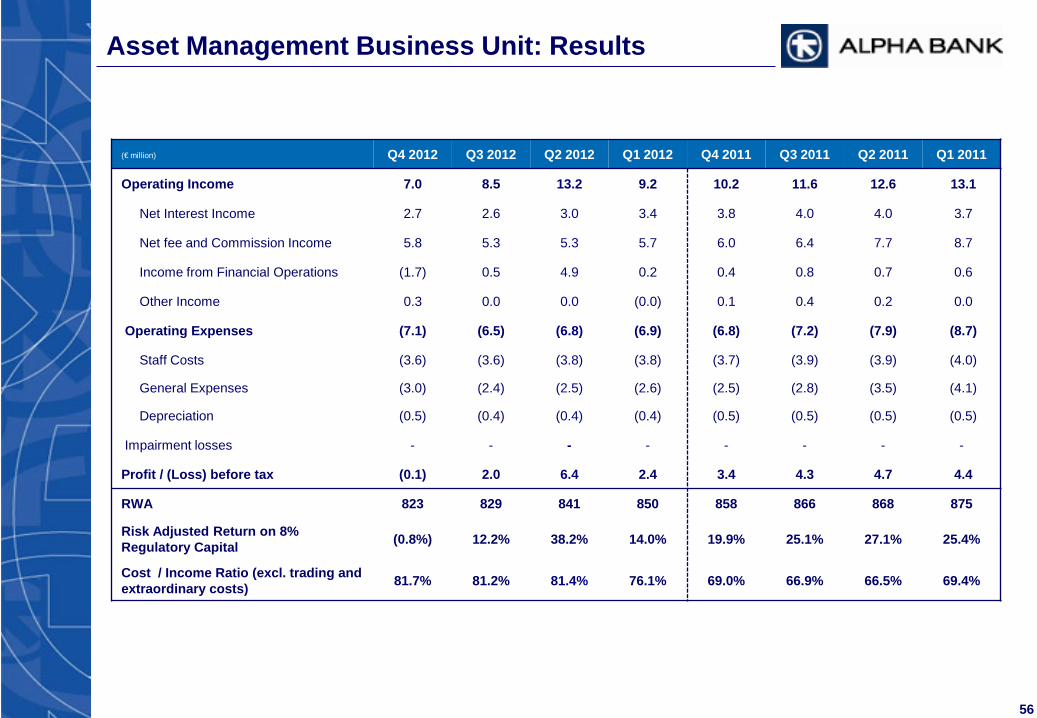

Asset Management Business Unit: Results

(€ million) Q4 2012 Q3 2012 Q2 2012 Q1 2012 Q4 2011 Q3 2011 Q2 2011 Q1 2011

Operating Income 7.0 8.5 13.2 9.2 10.2 11.6 12.6 13.1

Net Interest Income 2.7 2.6 3.0 3.4 3.8 4.0 4.0 3.7

Net fee and Commission Income 5.8 5.3 5.3 5.7 6.0 6.4 7.7 8.7

Income from Financial Operations (1.7) 0.5 4.9 0.2 0.4 0.8 0.7 0.6

Other Income 0.3 0.0 0.0 (0.0) 0.1 0.4 0.2 0.0

Operating Expenses (7.1) (6.5) (6.8) (6.9) (6.8) (7.2) (7.9) (8.7)

Staff Costs (3.6) (3.6) (3.8) (3.8) (3.7) (3.9) (3.9) (4.0)

General Expenses (3.0) (2.4) (2.5) (2.6) (2.5) (2.8) (3.5) (4.1)

Depreciation (0.5) (0.4) (0.4) (0.4) (0.5) (0.5) (0.5) (0.5)

Impairment losses - - - - - - - -

Profit / (Loss) before tax (0.1) 2.0 6.4 2.4 3.4 4.3 4.7 4.4

RWA 823 829 841 850 858 866 868 875

Risk Adjusted Return on 8% Regulatory Capital (0.8%) 12.2% 38.2% 14.0% 19.9% 25.1% 27.1% 25.4%

Cost / Income Ratio (excl. trading and extraordinary costs) 81.7% 81.2% 81.4% 76.1% 69.0% 66.9% 66.5% 69.4%

57

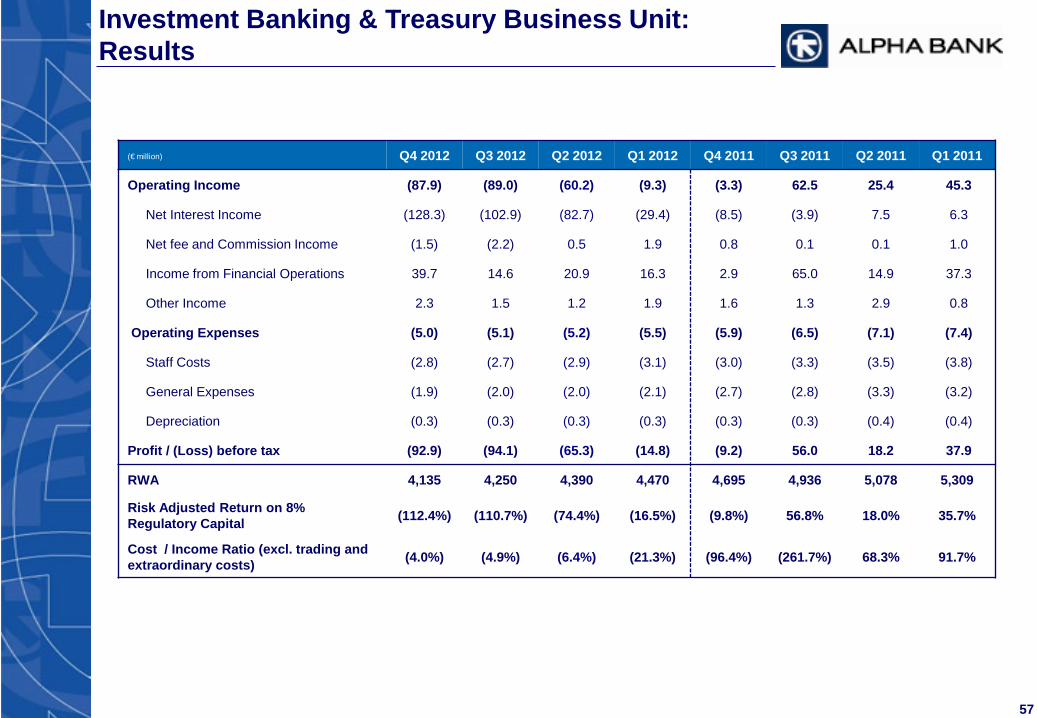

Investment Banking & Treasury Business Unit: Results

(€ million) Q4 2012 Q3 2012 Q2 2012 Q1 2012 Q4 2011 Q3 2011 Q2 2011 Q1 2011

Operating Income (87.9) (89.0) (60.2) (9.3) (3.3) 62.5 25.4 45.3

Net Interest Income (128.3) (102.9) (82.7) (29.4) (8.5) (3.9) 7.5 6.3

Net fee and Commission Income (1.5) (2.2) 0.5 1.9 0.8 0.1 0.1 1.0

Income from Financial Operations 39.7 14.6 20.9 16.3 2.9 65.0 14.9 37.3

Other Income 2.3 1.5 1.2 1.9 1.6 1.3 2.9 0.8

Operating Expenses (5.0) (5.1) (5.2) (5.5) (5.9) (6.5) (7.1) (7.4)

Staff Costs (2.8) (2.7) (2.9) (3.1) (3.0) (3.3) (3.5) (3.8)

General Expenses (1.9) (2.0) (2.0) (2.1) (2.7) (2.8) (3.3) (3.2)

Depreciation (0.3) (0.3) (0.3) (0.3) (0.3) (0.3) (0.4) (0.4)

Profit / (Loss) before tax (92.9) (94.1) (65.3) (14.8) (9.2) 56.0 18.2 37.9

RWA 4,135 4,250 4,390 4,470 4,695 4,936 5,078 5,309

Risk Adjusted Return on 8% Regulatory Capital (112.4%) (110.7%) (74.4%) (16.5%) (9.8%) 56.8% 18.0% 35.7%

Cost / Income Ratio (excl. trading and extraordinary costs) (4.0%) (4.9%) (6.4%) (21.3%) (96.4%) (261.7%) 68.3% 91.7%

58

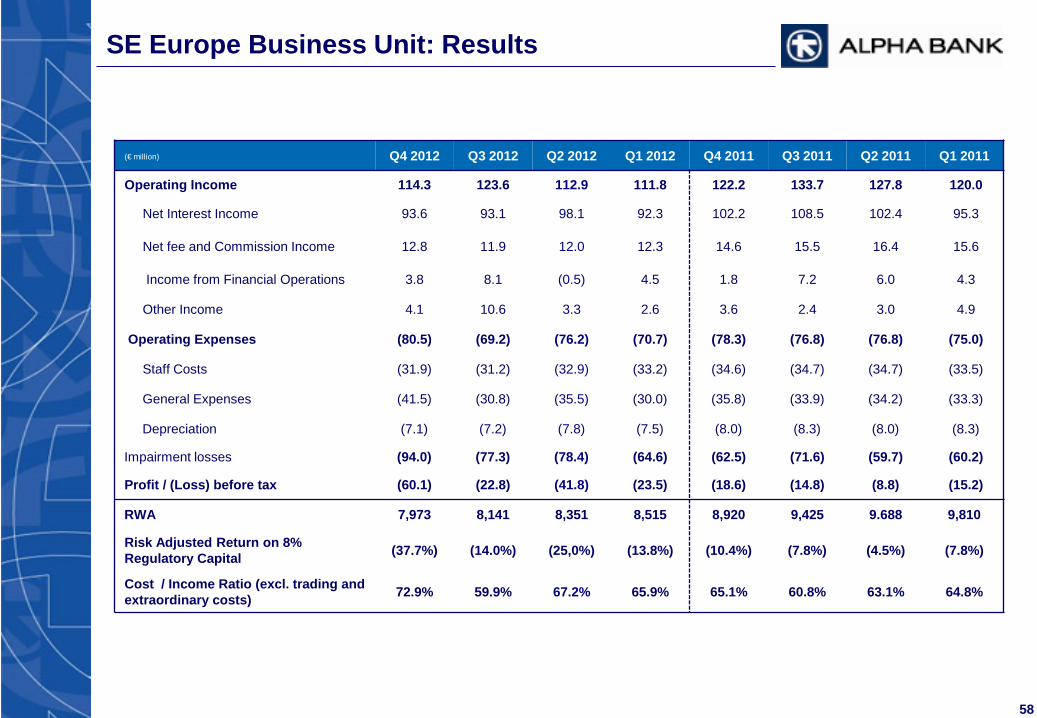

SE Europe Business Unit: Results

(€ million) Q4 2012 Q3 2012 Q2 2012 Q1 2012 Q4 2011 Q3 2011 Q2 2011 Q1 2011

Operating Income 114.3 123.6 112.9 111.8 122.2 133.7 127.8 120.0

Net Interest Income 93.6 93.1 98.1 92.3 102.2 108.5 102.4 95.3

Net fee and Commission Income 12.8 11.9 12.0 12.3 14.6 15.5 16.4 15.6

Income from Financial Operations 3.8 8.1 (0.5) 4.5 1.8 7.2 6.0 4.3

Other Income 4.1 10.6 3.3 2.6 3.6 2.4 3.0 4.9

Operating Expenses (80.5) (69.2) (76.2) (70.7) (78.3) (76.8) (76.8) (75.0)

Staff Costs (31.9) (31.2) (32.9) (33.2) (34.6) (34.7) (34.7) (33.5)

General Expenses (41.5) (30.8) (35.5) (30.0) (35.8) (33.9) (34.2) (33.3)

Depreciation (7.1) (7.2) (7.8) (7.5) (8.0) (8.3) (8.0) (8.3)

Impairment losses (94.0) (77.3) (78.4) (64.6) (62.5) (71.6) (59.7) (60.2)

Profit / (Loss) before tax (60.1) (22.8) (41.8) (23.5) (18.6) (14.8) (8.8) (15.2)

RWA 7,973 8,141 8,351 8,515 8,920 9,425 9.688 9,810

Risk Adjusted Return on 8% Regulatory Capital (37.7%) (14.0%) (25,0%) (13.8%) (10.4%) (7.8%) (4.5%) (7.8%)

Cost / Income Ratio (excl. trading and extraordinary costs) 72.9% 59.9% 67.2% 65.9% 65.1% 60.8% 63.1% 64.8%

59

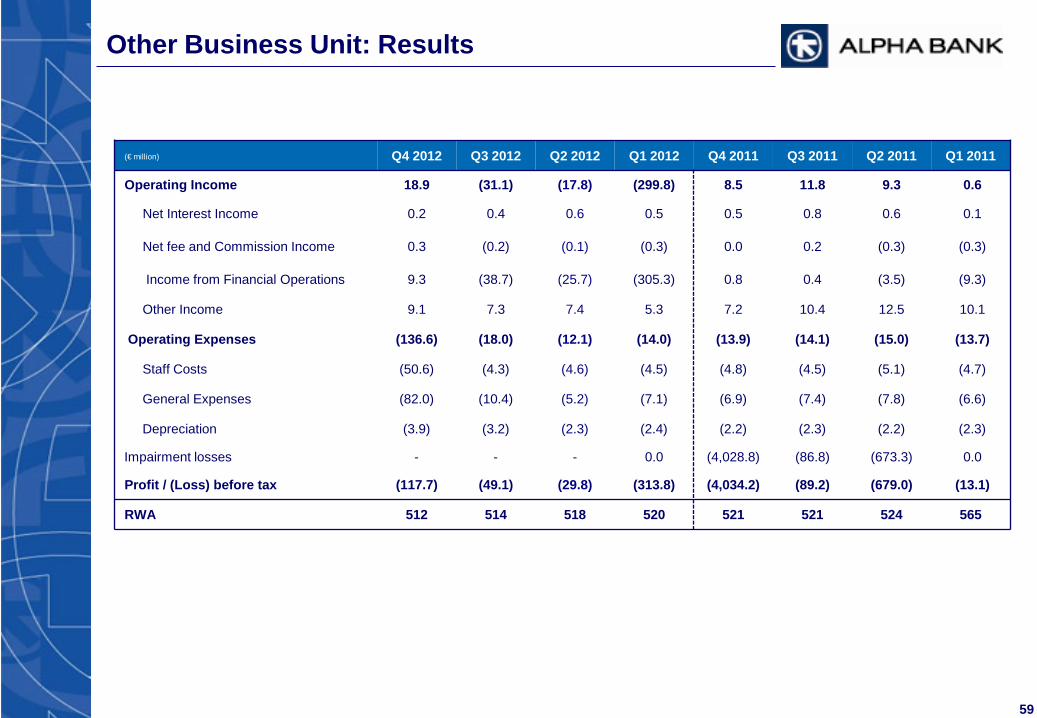

Other Business Unit: Results

(€ million) Q4 2012 Q3 2012 Q2 2012 Q1 2012 Q4 2011 Q3 2011 Q2 2011 Q1 2011

Operating Income 18.9 (31.1) (17.8) (299.8) 8.5 11.8 9.3 0.6

Net Interest Income 0.2 0.4 0.6 0.5 0.5 0.8 0.6 0.1

Net fee and Commission Income 0.3 (0.2) (0.1) (0.3) 0.0 0.2 (0.3) (0.3)

Income from Financial Operations 9.3 (38.7) (25.7) (305.3) 0.8 0.4 (3.5) (9.3)

Other Income 9.1 7.3 7.4 5.3 7.2 10.4 12.5 10.1

Operating Expenses (136.6) (18.0) (12.1) (14.0) (13.9) (14.1) (15.0) (13.7)

Staff Costs (50.6) (4.3) (4.6) (4.5) (4.8) (4.5) (5.1) (4.7)

General Expenses (82.0) (10.4) (5.2) (7.1) (6.9) (7.4) (7.8) (6.6)

Depreciation (3.9) (3.2) (2.3) (2.4) (2.2) (2.3) (2.2) (2.3)

Impairment losses - - - 0.0 (4,028.8) (86.8) (673.3) 0.0

Profit / (Loss) before tax (117.7) (49.1) (29.8) (313.8) (4,034.2) (89.2) (679.0) (13.1)

RWA 512 514 518 520 521 521 524 565

60

ALPHA BANK 40, Stadiou Street, 102 52 Athens, Greece Internet : www.alpha.gr Reuters : ACBr.AT Bloomberg : ALPHA GA

Mr. Michael Massourakis Senior Manager Economic Research Division +30210 326 2828 [email protected] Mr. Dimitrios Maroulis Manager Economic Research Division +30210 326 2832 [email protected]

Investor Relations Contacts Mr. Vassilios Psaltis General Manager and CFO +30210 326 4009 [email protected] Mr. Dimitrios Kostopoulos Manager Investor Relations Division +30210 326 4195 [email protected] Ms. Elena Katopodi Assistant Manager Investor Relations Division +30210 326 4184 [email protected] Ms. Stella Traka Investor Relations Officer +30210 326 4182 [email protected]