all joy foods limited - sharedata online · all joy foods limited (registration number...

TRANSCRIPT

ALL JOY FOODS LIMITED

ANNUAL REPORT

FOR THE 16 MONTHS ENDED 30 JUNE 2006

CONTENTS

Report of the chief executive officer – 1 - 2

Corporate governance – 3 - 8

Report of the independent auditors to the shareholders – 9

Directors' Responsibilities and Approval - 10

Directors' Report – 11 - 13

Balance Sheet - 14

Income Statement - 15

Statement of Changes in Equity - 16

Cash flow Statement - 17

Accounting Policies – 18 - 28

Notes to the Annual Report – 29 - 37

Information page - 38

ALL JOY FOODS LIMITED (Registration number 1989/000100/06) Annual Financial Statements for the 16 months ended 30 June 2006

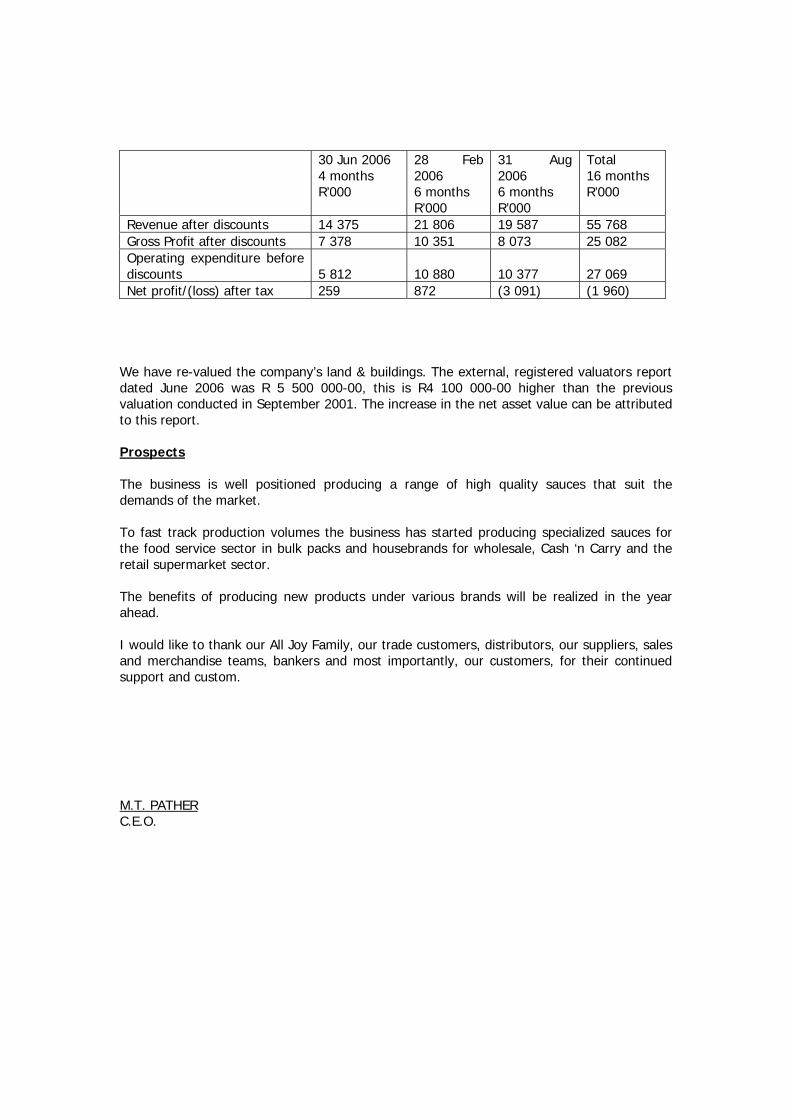

Report of the chief executive officer__________________ Introduction The turnaround strategy implemented by the company during the six months ended 28 February 2006 to increase sales revenue and net trading profit, has gained further momentum. The group has managed to contain its trading loss from the reported figures as at 28 February 2006, and has improved its financial performance for the four months ended 30 June 2006. All Joy Food’s strategy remains focused to increase market share and to reduce manufacturing and infrastructure overhead costs, in order to enhance competitiveness in the market. Financial review The Group has incurred a net loss after taxation of R1,960,152 for the sixteen months under review. This net trading figure is a further improvement on the reported loss after taxation of R2,219,000 for the twelve months ended 28 February 2006 and the loss after taxation of R3,091,000 reported for the six months ended 31 August 2005. We believe that this positive trend in profitability will continue as proven in the last ten months of the current financial period. In line with International Financial Reporting Standards (IFRS), the revenue reported is net of trade discounts allowed. The revenue, before trade discounts, has remained constant compared to the twelve months ended 28 February 2005. We are, however, confident that our market position and revenue, will continue to grow in the coming year. The gross profit percentage has shown a slight decrease from 46.7% to 44.9% in the current financial period. We will, however, continue our endeavours to reduce manufacturing costs and believe that these efforts will come to fruition in the months ahead. The increased operating expenditure is largely attributed to investments in human resources, I.T. systems and in maintaining our production plant and distribution facilities. We believe that this expenditure is critical in our strategy to grow our position in the market and to ensure that our plant and equipment can deliver on increased demand for our product. The depreciation charge on plant and equipment is lower than in the previous financial year, in line with our estimates on the remaining productive useful life and residual values of plant and equipment, in compliance with current financial reporting standards. The increased operating expenditure reported has also been influenced to a lesser extent by the failed merger with Retailer Brands during the first six months of the financial period. The marked increase in financial performance of the group from the first six months to the last ten months can be seen from the summary below: increases in revenue, gross profit and decrease in operating expenditure in the last four months are clear indicators of our commitment to the group’s financial success

30 Jun 2006 28 Feb 2006

31 Aug 2006 6 months

Total 4 months R’000

16 months 6 months R’000 R’000

R’000

Revenue after discounts 14 375 21 806 19 587 55 768 Gross Profit after discounts 7 378 10 351 8 073 25 082 Operating expenditure before discounts

5 812

10 880

10 377

27 069

Net profit/(loss) after tax 259 872 (3 091)

(1 960)

We have re-valued the company’s land & buildings. The external, registered valuators report dated June 2006 was R 5 500 000-00, this is R4 100 000-00 higher than the previous valuation conducted in September 2001. The increase in the net asset value can be attributed to this report. Prospects The business is well positioned producing a range of high quality sauces that suit the demands of the market. To fast track production volumes the business has started producing specialized sauces for the food service sector in bulk packs and housebrands for wholesale, Cash ‘n Carry and the retail supermarket sector. The benefits of producing new products under various brands will be realized in the year ahead. I would like to thank our All Joy Family, our trade customers, distributors, our suppliers, sales and merchandise teams, bankers and most importantly, our customers, for their continued support and custom. M.T. PATHER C.E.O.

ALL JOY FOODS LIMITED (Registration number 1989/000100/06) Annual Financial Statements for the 16 months ended 30 June 2006

Corporate Governance____________________________ Corporate social responsibility All Joy Foods Corporate Social Investment program is our flagship food program for all new owners of RDP houses. This is a program that provides all new RDP house owners with food hampers for the first few days so that they can get settled in their new house. We therefore provide financial support via food after the owners had to pay the deposit on their house. This reflects the vision of RDP – “A better life for all”. All Joy Foods offers support to thousands of South Africans and South African families in need of assistance each month by sponsoring products to a numerous of charity organizations and soup kitchens. Environmental report An appreciation of the high importance of environmental awareness is integral to the company’s operations. All Joy Foods is committed to ensuring that in all its spheres of activity it will conduct itself in a way that is safe, healthy and environment friendly. Corporate Governance All Joy Foods is committed to the principles of openness, integrity and accountability in its dealings with all stakeholders. The company supports the code of corporate practices and conduct as recommended by the King II report on corporate governance. The primary objective of any system of corporate governance is to ensure that directors and managers, to whom the management of corporations has been entrusted to by the shareholders, carry out their responsibilities faithfully and effectively, placing the interests of the corporation and society ahead of their own. This process is facilitated through the establishment of appropriate reporting and control structures within the organization. Ethics Directors and employees are required to observe the principles of the All Joy Foods Code of Ethics to ensure that business practices are conducted in a manner which is beyond reproach. Copies of the Code of Ethics are available on request from the company secretary. Financial statements The directors of All Joy Foods are responsible for preparing financial statements and other information presented in the annual report in a manner that fairly presents the state of affairs and results of the operations of the company and the Group. The external auditors are responsible to carry out an independent examination of the financial statements in accordance with Statements of International Auditing Standards and to report their findings thereof. Refer to page 9 for the layout of the auditor’s report. The annual financial statements (refer to page 11 - 37) have been prepared in accordance with International Financial Reporting Standards. They are based on appropriate accounting policies and are supported by reasonable and prudent judgments and estimates.

The directors have no reason to believe that the Group’s operations will not continue as going concerns in the year ahead, other than where closures or discontinuations are anticipated, in which case provision is made to reduce the carrying cost of the relevant assets to net realisable value. Audit committee The company has an audit committee which operates under an approved charter and is chaired by an independent non-executive director. The remaining members of the committee are two independent non-executive directors and one executive director. The respective audit committee reviews the effectiveness of internal control in the Group with reference to the findings of both the internal and external auditors. Other areas covered include the review of important accounting issues, including specific disclosures in the financial statements and a review of the major audit recommendations. In addition, the audit committee also fulfills the role of risk committee. The external auditors have unrestricted access to the audit committee. Risk committee The board acknowledges its responsibility for the total process of risk management as well as forming its own opinion on the effectiveness of the process. Management is accountable for designing, implementing and monitoring the process of risk management and integrating it into the day to day activities of the company. The members of the risk committee are representatives of the marketing, legal/secretarial, financial and manufacturing functions of the company. As and when requested, independent specialists or other specialists are invited to attend meetings of the committee and to provide their views on matters of risk addressed by the committee. The risk committee has met two times during the 2006 financial year. In terms of the risk committee charter, the committee assesses the effectiveness of the company’s risk management process. The risk management process includes the establishment of formalised systems to assist in the identification, control and monitoring of risks. The company’s key strategic risks have been identified and documented by the committee. The responsibility for each of the key identified risks has been assigned to an appropriate member of the company’s senior management team. In conducting the risk assessments, all relevant risk categories are considered, including reputation risk, brand risk, product risk, legislative issues, human recourses risks, strategic risk, competitive forces, information technology issues, insurable perils and financial risks. Material risks, both strategic and operational in nature, are reviewed annually and also updated during the course of the year should the risk environment change. Disaster recovery plans are reviewed regularly as disruptions in critical management information systems could have a material impact on the group’s continuing operations. At operational level, the group runs a number of risk control initiatives addressing safety management, security, fire defense, food safety, environmental management and quality management. These initiatives include processes for the identification of risk, the implementation of risk mitigation and compliance with relevant legislation. The group performs regular risk control audits using external consultants. The focus of these audits is to ensure that the group’s assets are adequately safeguarded. The results are reported on at operational management level as well as to the risk committee.

The company adopts systems of incident reporting at operational level that allow for reporting to management by exception. Other specific features of the group’s system of risk management include a formal policy covering the company’s code of ethics and a control risk assessment process at operational level. Attendance register of the Risk committee

Meeting dateMT

PatherC

CarrollS.

FanaroffWA

ParsonsR

BagusA

RuitersJW

WaltersAdvisor Auditors

20 September 2005 x x25 April 2006 x x x x

x : Attendin

x xx

g aa : Absence with apologies a : Absence without apologies r : Resigned Internal control The group maintains internal controls and systems designed to provide reasonable assurance as to the integrity and reliability of the financial statements and to adequately safeguard, verify and maintain accountability for its assets. Such controls are based on established policies and procedures.These are implemented by trained personnel and the financial manager with an appropriate segregation of duties. Risk control The group has comprehensive risk and loss insurance in place. The layered structure of the programme allows the group to obtain very competitive rates. Directorate and executive management The board of directors of All Joy Foods includes independent non-executive directors who are chosen for their business acumen and skills. New appointees to the board are appropriately familiarized with the company’s businesses through an induction programe. The board of the company meets regularly and monitors the performance of executive management. It addresses a range of key issues and ensures that debate on matters of policy, strategy and performance is critical, informed and constructive. All directors of All Joy Foods Limited have access to the advice and services of the company secretary and, in appropriate circumstances, may, at the company’s expense, seek independent professional advice concerning its affairs.

Attendances register of the Board meeting

Meeting dateMT

PatherC

CarrollS.

FanaroffWA

ParsonsR

BagusA

RuitersJW

WaltersAdvisor Auditors

25 January 2005 x x x x aa aa x x30 March 2005 x x x x x aa x x23 May 2005 x r x a aa aa x x28 July 2005 x x x aa aa x xAGM19 August 2005 x x x x x x x11 October 2005 x x x r aa x x26 October 2005 x x x x x x24 November 2005 x x a r x x25 April 2006 x x x x xAGM12 June 2006 x a a x x

x : Attending aa : Absence with apologies a : Absence without apologies r : Resigned Remuneration Committee The Remuneration Committee (“the Committee”) has been delegated by the Board with the responsibility for determining the remuneration of the executive directors and other senior management members. The Committee comprises three independent non-executive directors. The chairman of the Committee reports to the board on the Committee’s deliberations and decisions. Attendances register of the remuneration committee

Meeting dateMT

PatherC

CarrollS.

FanaroffWA

ParsonsR

BagusA

RuitersJW

WaltersAdvisor Auditors

14 July 2005 x x20 September 2005 x x

x : Attendin

xx x

g aa : Absence with apologies a : Absence without apologies r : Resigned Remuneration policy Remuneration policy is formulated to attract, retain and motivate top-quality people in the best interests of shareholders, and is based upon the following principles:

• Remuneration arrangements will be designed to support All Joy Foods business strategy, vision and to conform to best practices.

• Total rewards will be set at levels that are competitive within the context of the relevant areas of responsibility and the industries in which the company operates.

• Total incentive-based rewards are earned through the attainment of demanding targets consistent with shareholders’ growth expectations.

Composition of executive remuneration The remuneration of executive directors is determined on a total cost-to-company basis. The total remuneration packages comprise an annual cash salary, incentive bonus plan, other benefits including group life, health and disability insurance, and a car allowance scheme. These are dealt with in more detail below:

• Annual salaries The salaries of the executive directors are subject to annual review and benchmarked against external market data taking into account the size of the company, its market sector and business complexity. Individual performance and overall responsibility are also taken into consideration.

• Incentive bonus plan The executive directors participate in an annual incentive bonus plan, which is based on the achievement of short-term performance targets. These targets are based on the overall group financial performance as well as the attainment of agreed strategic and personal objectives. No incentive bonus was paid in the 2005 and 2006 financial year because of the financial difficulties that the company is experiencing.

• Other benefits The executive directors enjoy various other benefits including medical aid cover, permanent health insurance, death in service and funeral benefits, and a car allowance.

Directors’ employment agreements Mr. M.T. Pather and Mr. J.W. Walters have employment agreements with the company. The employment agreements are subject to a notice period of not less than one month to be given by either party. Succession planning Revision of a formal succession plan for senior and executive management is undertaken in June each year and thereafter discussed by the Remuneration Committee. The objective is to ensure that immediate succession is in place but also to develop a pool of persons with potential for development and future placement. This includes managers at lower levels. Non-executive directors’ fees The remuneration of the non-executive directors is approved by the shareholders in terms of the company’s Articles of Association. In terms of the company’s Articles of Association, non-executive directors who perform services outside the scope of the ordinary duties of a director may be paid additional remuneration, the reasonable maximum of which is fixed by a disinterested quorum of directors.

2006 - R'000 Salary as a director

Salary for management

Fringe benefits Provident Total

Executive directorsMT Pather - 687 303 249 1,239 JW Walters - - - - - Non-executive directorsS Fanaroff 30 - - - - WA Parsons 2 76 - - 78

32 763 303 249 1,317 2005 - R'000

Executive directorsMT Pather 88 518 113 112 831 AJ Gonsalves 18 140 36 70 264 C Carrol 35 338 4 - 377 Non-executive directorsS Fanaroff 14 - - - 14 WA Parsons 11 54 - - 65

166 1,050 153 182 1,551

Management reporting There are comprehensive management reporting disciplines in place, which include the preparation of annual budgets by all operating units and categories. Individual operational, functional and category budgets are approved by the relevant company executives, while the group budget is reviewed by the directors of the company. Monthly results and the financial status of operating units are reported against approved budgets and compared to the prior year. Profit projections and cash flow forecasts are updated monthly, while working capital and cash/borrowing levels are monitored on an ongoing basis. Planning process In line with its mission to build a world-class business, the overall strategy for All Joy Foods is clearly focused. Annual business, category growth and brand plans are compiled at the appropriate level, with detailed action plans and allocated responsibilities. Progress is reviewed regularly. Statement of compliance by the company secretary Declaration by the company secretary in respect of section 268g(d) of the Companies Act. I declare that that to the best of my knowledge, the company has lodged with the Registrars all such returns as are required by a public company in terms of the Companies Act and that all such returns are true, correct and up to date. JW Walters Company secretary

ALL JOY FOODS LIMITED(Registration number 1989/000100/06)Annual Financial Statements for the 16 months ended 30 June 2006

A.R.CIncorporatedIngelyf

,'"'

RegisteredCharteredAccountants&Auditors(SA)

GeregistreerdeGeoktrooieerdeRekenmeesters&Ouditeure(SA)

Report of the Independent Auditors

To the shareholders of All Joy Foods Limited

We have audited the annual financial statements of All Joy Foods Limited set out on pages 11 to 37 for the 16months ended 30 June 2006. These annual financial statements are the responsibility of the company'sdirectors. Our responsibility is to express an opinion on these annual financial statements based on our audit.

Scope

We conducted our audit in accordance with International Standards on Auditing. Those standards require thatwe plan and perform the audit to obtain reasonable assurance about whether the annual financial statementsare free of material misstatement. An audit includes examining on a test basis, evidence supporting the amountsand disclosures in the annual financial statements. An audit also includes assessing the accounting policiesused and significant estimates made by management, as well as evaluating the overall financial statementpresentation. We believe that our audit provides a reasonable basis for our opinion.

Audit opinion

In our opinion, the annual financial statements present fairly, in all material respects, the financial position of thecompany at 30 June 2006 and the results of its operations and cash flows for the 16 months then ended inaccordance with International Financial Reporting Standards, and in the manner required by the Companies Actof South Africa.

0J1.(, 1t1c.°1oMlJvARC Chartered Accountants and Auditors IncorporatedRegistered Chartered Accountants and Auditors (S.A.)

Johannesburg28 September 2006

ARC Chartered Accountants & Auditors Incorporated

Reg. No.: 1996/003163/21

Directors:

MS Appelgryn B.Com (Hons) (RAU) CA(SA)TJ Rautenbach B.Com (Hons) (RAU) CA(SA)JC Cronje B.Com (Hons) (RAU) CA(SA)JL van Schalkwyk B.Compt (Hons) (Unisa) CA(SA)

~Tel +27 11 476-3210Fax +2711 476-3221

CA(SA)

PO Box252Cresta2118

1st Floor, Unit 5299 Pendoring Road.Blackheath Ext. 62195

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Directors' Responsibilities and Approval

The directors are required by the South African Companies Act, 1973, to maintain adequate accounting recordsand are responsible for the content and integrity of the annual financial statements and related financialinformation included in this report. It is their responsibility to ensure that the annual financial statements fairlypresent the state of affairs of the group as at the end of the financial 16 months and the results of its operationsand cash flows for the year then ended, in conformity with International Financial Reporting Standards. Theexternal auditors are engaged to express an independent opinion on the annual financial statements.

The annual financial statements are prepared in accordance with International Financial Reporting Standardsand are based upon appropriate accounting policies consistently applied and supported by reasonable andprudent judgments and estimates.

The directors acknowledge that they are ultimately responsible for the system of internal financial controlestablished by the group and place considerable importance on maintaining a strong control environment. Toenable the directors to meet these responsibilities, the board sets standards for internal control aimed atreducing the risk of error or loss in a cost effective manner. The standards include the proper delegation ofresponsibilities within a clearly defined framework, effective accounting procedures and adequate segregation ofduties to ensure an acceptable level of risk. These controls are monitored throughout the group and allemployees are required to maintain the highest ethical standards in ensuring the group’s business is conductedin a manner that in all reasonable circumstances is above reproach. The focus of risk management in the groupis on identifying, assessing, managing and monitoring all known forms of risk across the group. While operatingrisk cannot be fully eliminated, the group endeavours to minimise it by ensuring that appropriate infrastructure,controls, systems and ethical behaviour are applied and managed within predetermined procedures andconstraints.

The directors are of the opinion, based on the information and explanations given by management, that thesystem of internal control provides reasonable assurance that the financial records may be relied on for thepreparation of the annual financial statements. However, any system of internal financial control can provide onlyreasonable, and not absolute, assurance against material misstatement or loss.

The directors have reviewed the group’s cash flow forecast for the 16 months to 30 June 2007 and, in the light ofthis review and the current financial position, they are satisfied that the group has or has access to adequateresources to continue in operational existence for the foreseeable future.

Although the board is primarily responsible for the financial affairs of the group, they are supported by thegroup's external auditors.

The external auditors are responsible for independently reviewing and reporting on the group's annual financialstatements. The annual financial statements have been examined by the group's external auditors and theirreport is presented on page 10.

The annual financial statements set out on pages 11 to 37, which have been prepared on the going concernbasis, were approved by the board on 28 September 2006 and were signed on its behalf by:

M.T. Pather

S. Fanaroff

10

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Directors' Report

The directors submit their report for the 16 months ended 30 June 2006.

1.

Review of activities

Main business and operations

All Joy Foods Limited is a food company which develops, procures, manufactures and markets a range oftomato sauces, mayonnaise, salad creams, specialty sauces and drinking chocolates as well as othercondiments and preserves.

The operating results and state of affairs of the company are fully set out in the attached annual financialstatements and do not in our opinion require any further comment.

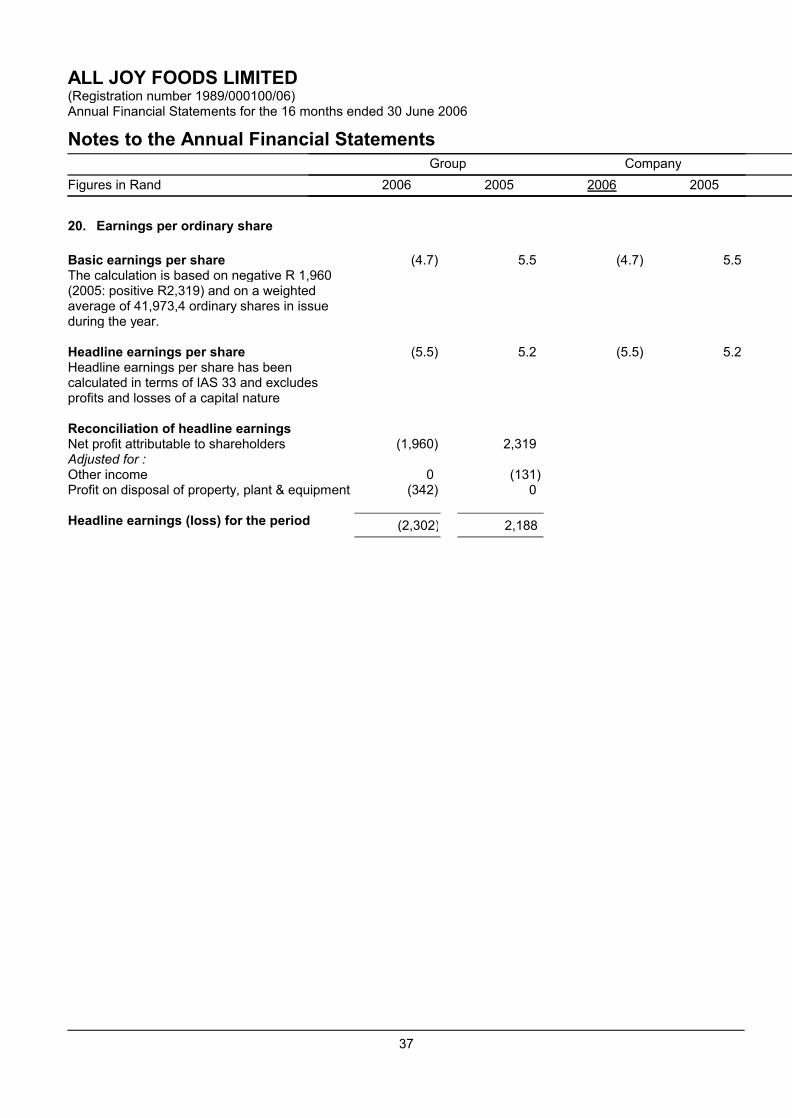

Net loss of the group was R (1,960,152) (2005:Profit of R 2,319,348), after taxation of R (468,264) (2005: R782,984)

2.

Post balance sheet events

The directors are not aware of any matter or circumstance which may have an impact on these financialstatements, to the date of signing the annual financial statements arising since the end of the financial 16months.

3.

Directors' interest in shares

At the financial year-end the directors held the following direct and indirect interest in the company's shares:

Direct

Beneficial

Direct

Beneficial

IndirectNon-

Beneficial

Indirect

Non-Beneficial

2006

2005

2006

2005

Ordinary Shares

MT Pather

3,000,000

3,000,000

7,429,775

7,429,775WA Parsons

20,000

20,000

-

-

S Faranoff

20,000

20,000

-

- 3,042,006

3,042,005

7,431,781

7,431,780

4.

Accounting policies

The annual financial statements have been prepared based on International Financial Reporting Standards.

5.

Authorised and issued share capital

There were no changes in the authorised or issued share capital of the group during the 16 months underreview.

6.

Property, plant and equipment

There have been additions to property, plant and equipment during the period under review but no changes inthe policy relating to their use.

Property,plant and equipment to the amount of R1,119,081 was acquired, as well as disposals of R193,155.

11

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Directors' Report

7.

Dividends

No dividends were declared or paid to shareholders during the 16 months.

8.

Directors

The directors of the company during the 16 months and to the date of this report are as follows:

Name

Change in appointment

M.T. Pather

S. Fanaroff

DR W.A. Parson

M.R. Bagus

Resigned 26 October

2005

C. Carrol

Resigned 23 May 2005

A. Ruiters

Resigned 25 October

2005

J.W. Walters

9.

Secretary

The secretary of the company is JW Walters of:

Business address

103 Booysens Reserve Road

Crown Mines

Johannesburg

2135

Postal address

PO Box 2152

Southdale

2135

10.

Holding company

The company's holding company is Farm Food Holdings (Pty) Ltd incorporated in South Africa.

11.

Auditors

ARC Chartered Accountants and Auditors Incorporated will continue in office in accordance with section 270(2)of the Companies Act.

12

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Directors' Report

12.

Analysis of shareholders

Shareholder spread analysis as at 30 June 2006:

Shareholder spread

No. ofshareholders

%

No. ofshares

%

1 - 1 000 shares

79

35.3

29,599

0.11 001 - 10 000 shares

90

40.2

463,979

1.1

10 001 - 100 000 shares

46

20.5

1,442,522

3.4100 001 - 1 000 000 shares

5

2.2

1,153,500

2.8

1 000 001 shares and over

4

1.8

38,883,733

92.6 224

100.0

41,973,333

100.0

Distribution of shareholders

Banks and close corporations

7

3.2

86,260

0.2Empowerment

1

0.4

8,221,833

19.5

Individuals

199

88.8

5,709,701

13.6Nominee and Trusts

8

3.6

191,339

0.5

Other corporations

4

1.8

37,100

0.1Private and public companies

5

2.2

27,727,100

66.1

224

100.0

41,973,333

100.0

Public/non-public shareholders

Non-public shareholders

8

3.6

35,135,233

83.7Directors and associated of the holding

company

6

2.7

3,110,900

7.4

Holding Company

1

0.4

23,802,500

56.7Holdings of more than 10%

1

0.4

8,221,833

19.6

Public shareholders

216

96.4

6,838,100

16.3 232

100.0

41,973,333

100.0

Shareholders with an interest of 3%

or more in shares

Farm Food Holdings (Pty) Ltd

23,802,500

56.7Purple Rain Properties (Pty) Ltd

3,859,400

9.2

Pather MT

3,000,000

7.1National Empowerment Fund

8,221,833

19.6

13

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

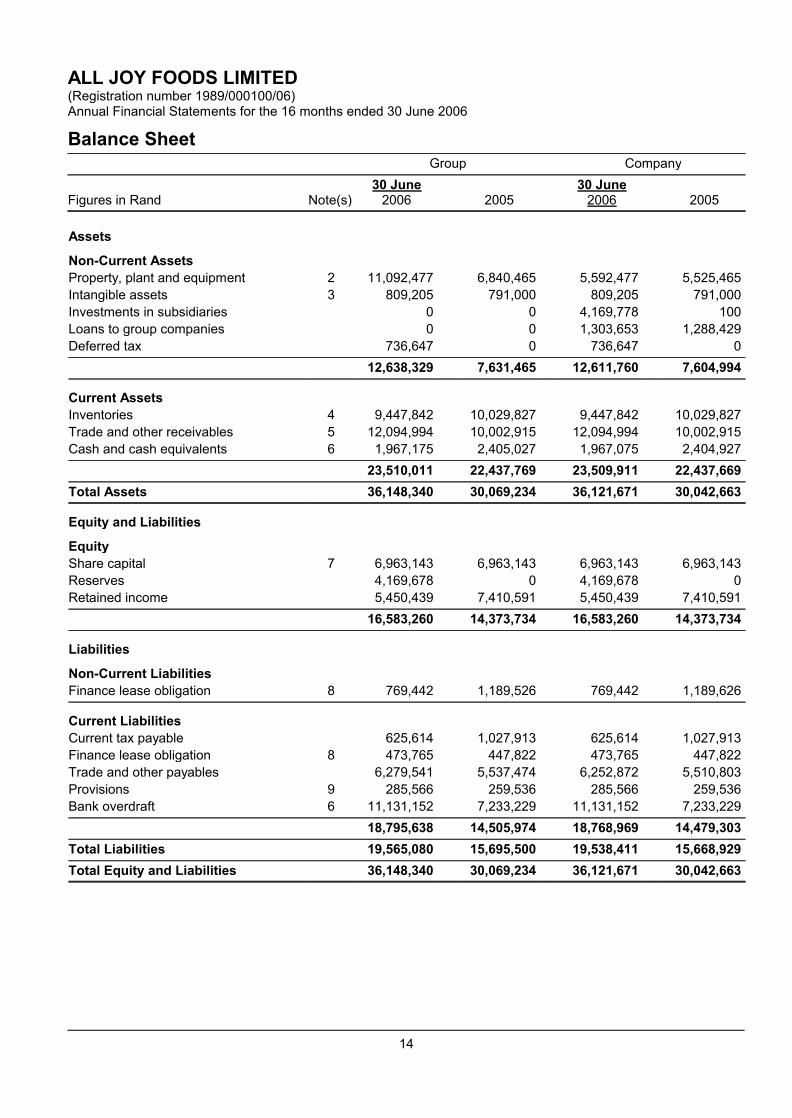

Balance Sheet

Group

Company

30 June

30 June

Figures in Rand Note(s) 2006

2005

2006

2005

Assets

Non-Current Assets

Property, plant and equipment

2

11,092,477

6,840,465

5,592,477

5,525,465Intangible assets

3

809,205

791,000

809,205

791,000

Investments in subsidiaries

0

0

4,169,778

100Loans to group companies

0

0

1,303,653

1,288,429

Deferred tax

736,647

0

736,647

0 12,638,329

7,631,465

12,611,760

7,604,994

Current Assets

Inventories

4

9,447,842

10,029,827

9,447,842

10,029,827Trade and other receivables

5

12,094,994

10,002,915

12,094,994

10,002,915

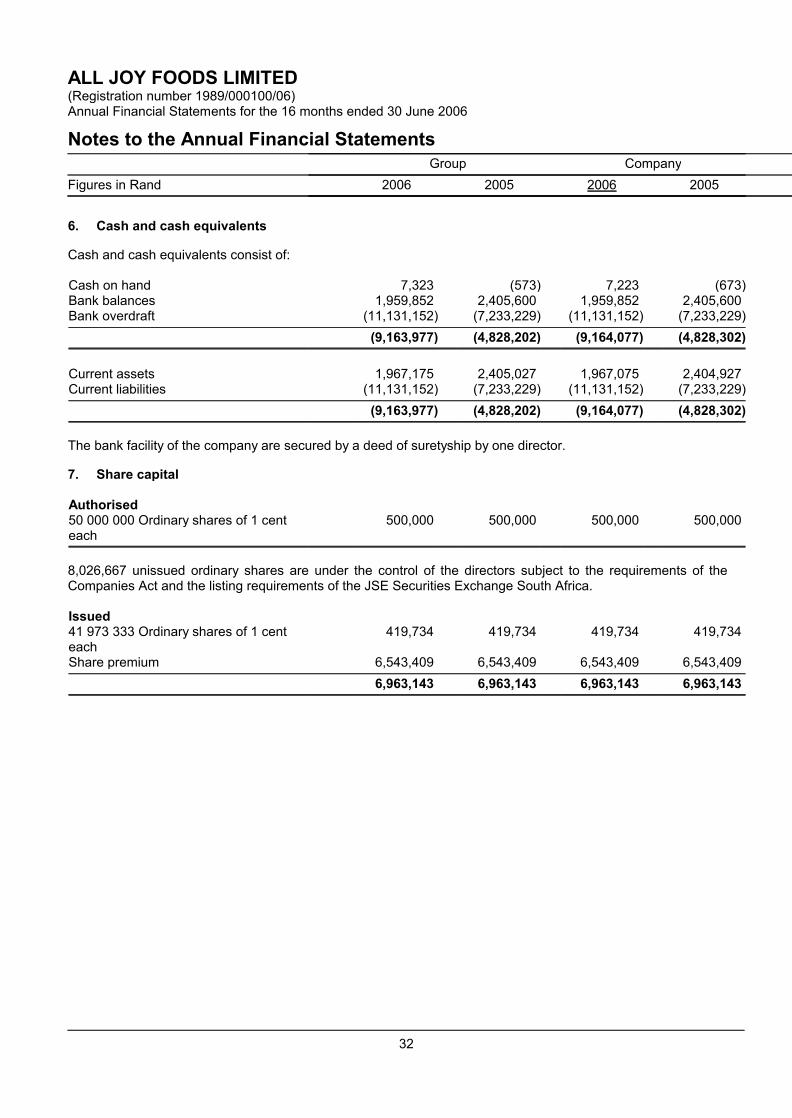

Cash and cash equivalents

6

1,967,175

2,405,027

1,967,075

2,404,927 23,510,011

22,437,769

23,509,911

22,437,669

Total Assets

36,148,340

30,069,234

36,121,671

30,042,663

Equity and Liabilities

Equity

Share capital

7

6,963,143

6,963,143

6,963,143

6,963,143Reserves

4,169,678

0

4,169,678

0

Retained income

5,450,439

7,410,591

5,450,439

7,410,591 16,583,260

14,373,734

16,583,260

14,373,734

Liabilities

Non-Current Liabilities

Finance lease obligation

8

769,442

1,189,526

769,442

1,189,626

Current Liabilities

Current tax payable

625,614

1,027,913

625,614

1,027,913Finance lease obligation

8

473,765

447,822

473,765

447,822

Trade and other payables

6,279,541

5,537,474

6,252,872

5,510,803Provisions

9

285,566

259,536

285,566

259,536

Bank overdraft

6

11,131,152

7,233,229

11,131,152

7,233,229 18,795,638

14,505,974

18,768,969

14,479,303

Total Liabilities

19,565,080

15,695,500

19,538,411

15,668,929

Total Equity and Liabilities

36,148,340

30,069,234

36,121,671

30,042,663

14

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Income Statement

Group

Company

16 months

16 months

ended

ended

30 June

30 June

Figures in Rand Note(s) 2006

2005

2006

2005

Revenue

10

55,767,840

42,734,350

55,767,840

42,734,350Cost of sales

(30,686,506)

(22,747,420)

(30,686,506)

(22,747,420)

Gross profit

25,081,334

19,986,930

25,081,334

19,986,930Other income

883,893

783,049

883,893

783,049

Operating expenses

(27,068,713)

(16,180,669)

(27,198,317)

(16,180,669)

Operating (loss) profit

11

(1,103,486)

4,589,310

(1,233,090)

4,589,310Investment revenue

108,608

0

238,212

0

Finance costs

12

(1,433,538)

(1,486,978)

(1,433,538)

(1,486,978)

(Loss) profit before taxation

(2,428,416)

3,102,332

(2,428,416)

3,102,332Taxation

13

468,264

(782,984)

468,264

(782,984)

(Loss) profit after taxation

(1,960,152)

2,319,348

(1,960,152)

2,319,348

15

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Statement of Changes in Equity

Figures in Rand

Share capital

Share

premium

Total share

capital

Revaluation

of property,

plant and

equipment

Retained

income

Total equity

Group

Balance at 01 March 2004

330,000

1,960,000

2,290,000

0

6,098,000

8,388,000Changes

Profit for the year

0

0

0

0

2,194,000

2,194,000Issue of shares

89,734

5,166,409

5,256,143

0

0

5,256,143

Share allotment costs

0

(583,000)

(583,000)

0

0

(583,000)

Total changes

89,734

4,583,409

4,673,143

0

2,194,000

6,867,143

Balance at 28 February 2005

as previously reported 419,734

6,543,409

6,963,143

0

8,292,000

15,255,143

Correction of Debtors error of

2004 0

0

0

0

(712,000)

(712,000)

Correction of Debtors error of

2005 0

0

0

0

(295,000)

(295,000)

Revaluation of intangible

assets (IAS 37) 0

0

0

0

125,591

125,591

Balance at 01 March 2005

as restated 419,734

6,543,409

6,963,143

0

7,410,591

14,373,734

Changes

Revaluation of property

0

0

0

4,169,678

0

4,169,678

Net income (expenses)

recognised directly in equity 0

0

0

4,169,678

0

4,169,678

Loss for the year

0

0

0

0

(1,960,152)

(1,960,152)

Total recognised income and

expenses for the period 0

0

0

4,169,678

(1,960,152)

2,209,526

Total changes

0

0

0

4,169,678

(1,960,152)

2,209,526

Balance at 30 June 2006

419,734

6,543,409

6,963,143

4,169,678

5,450,439

16,583,260

Note(s)

7

7

7

16

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Cash flow Statement

Group

Company

16 months

16 months

ended

ended

30 June

30 June

Figures in Rand Note(s) 2006

2005

2006

2005

Cash flows from operating activities

Cash receipts from customers

63,438,522

45,795,240

63,438,522

45,795,240Cash paid to suppliers and employees

(64,489,326)

(43,557,314)

(64,619,028)

(43,557,314)

Cash (used in) generated from

operations 15

(1,050,804)

2,237,926

(1,180,506)

2,237,926

Interest income

108,608

0

238,212

0Finance costs

(1,433,538)

(1,486,978)

(1,433,538)

(1,486,978)

Tax paid

16

(670,682)

(1,252,087)

(670,682)

(1,252,087)

Net cash from operating activities

(3,046,416)

(501,139)

(3,046,514)

(501,139)

Cash flows from investing activities

Purchase of property, plant and

equipment 2

(1,119,081)

(1,956,000)

(1,103,759)

(1,551,000)

Sale of property, plant and equipment

2

242,168

111,694

242,168

111,694Purchase of other intangible assets

3

(18,205)

(161,000)

(18,205)

(161,000)

(Increase)/Decrease in group company's

loan

0

0

(15,224)

0

Net cash from investing activities

(895,118)

(2,005,306)

(895,020)

(1,600,306)

Cash flows from financing activities

Proceeds on share issue

7

0

4,673,243

0

4,673,143Finance lease payments

(394,241)

(188,000)

(394,241)

(593,000)

Net cash from financing activities

(394,241)

4,485,243

(394,241)

4,080,143

Total cash movement for the year

(4,335,775)

1,978,798

(4,335,775)

1,978,698Cash at the beginning of the year

(4,828,202)

(6,807,000)

(4,828,302)

(6,807,000)

Total cash at end of the year

6

(9,163,977)

(4,828,202)

(9,164,077)

(4,828,302)

17

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Accounting Policies

1.

Presentation of Annual Financial Statements

The annual financial statements have been prepared in accordance with International Financial ReportingStandards and the Companies Act of South Africa. The annual financial statements have been prepared on thehistorical cost basis, except for the measurement of investment properties and certain financial instruments atfair value (and biological assets at fair value less point of sale costs), and incorporate the principal accountingpolicies set out below.

These accounting policies are consistent with the previous 16 months.

1.1

Significant judgements

In preparing the annual financial statements, management is required to make estimates and assumptions thataffect the amounts represented in the annual financial statements and related disclosures. Use of availableinformation and the application of judgement is inherent in the formation of estimates. Actual results in the futurecould differ from these estimates which may be material to the annual financial statements. Significantjudgements include:

Impairment testing

Management used the value in use to determine the recoverable amount of goodwill, intangible assets with anindefinite useful life and identifying assets that may have been impaired.

Provisions

Provisions were raised and management determined an estimate based on the information available. Additionaldisclosure of these estimates of provisions are included in note 9 - Provisions.

1.2

Property, plant and equipment

The cost of an item of property, plant and equipment is recognised as an asset when:

� it is probable that future economic benefits associated with the item will flow to the company; and

� the cost of the item can be measured reliably.

Costs include costs incurred initially to acquire or construct an item of property, plant and equipment and costsincurred subsequently to add to, replace part of, or service it. If a replacement cost is recognised in the carryingamount of an item of property, plant and equipment, the carrying amount of the replaced part is derecognised.

The initial estimate of the costs of dismantling and removing the item and restoring the site on which it is locatedis also included in the cost of property, plant and equipment.

Property, plant and equipment is carried at cost less accumulated depreciation and any impairment losses.

Depreciation is provided on all property, plant and equipment other than freehold land, to write down the cost,less residual value, on a straight line basis over their useful lives as follows:

Item

Average useful life

Plant and machinery

10 years

Furniture and fixtures

12 years

Motor vehicles

5 years

Office equipment

5 years

IT equipment

8 years

Computer software

3 years

Leasehold improvements

10 years

Laboratory equipment

10 years

Pallets

5 years

18

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Accounting Policies

1.2

Property, plant and equipment (continued)

The residual value and the useful life of each asset are reviewed at each financial year-end.

Each part of an item of property, plant and equipment with a cost that is significant in relation to the total cost ofthe item shall be depreciated separately.

The depreciation charge for each period is recognised in profit or loss unless it is included in the carrying amountof another asset.

The gain or loss arising from the derecognition of an item of property, plant and equipment is included in profit orloss when the item is derecognised. The gain or loss arising from the derecognition of an item of property, plantand equipment is determined as the difference between the net disposal proceeds, if any, and the carryingamount of the item.

1.3

Goodwill

Goodwill is initially measured at cost, being the excess of the business combination over the company's interestof the net fair value of the identifiable assets, liabilities and contingent liabilities.

Subsequently goodwill is carried at cost less any accumulated impairment.

The excess of the company’s interest in the net fair value of the identifiable assets, liabilities and contingentliabilities over the cost of the business combination is immediately recognised in profit or loss.

Internally generated goodwill is not recognised as an asset.

1.4

Intangible assets

An intangible asset is recognised when:

� it is probable that the expected future economic benefits that are attributable to the asset will flow tothe entity; and

� the cost of the asset can be measured reliably.

Intangible assets are initially recognised at cost.

Intangible assets are carried at revalued amount, being fair value at the date of revaluation less any subsequentaccumulated amortisation and any subsequent accumulated impairment losses. Revaluations are made withsufficient regularity such that the carrying amount does not differ materially from that which would be determinedusing fair value at the balance sheet date.

Any increase in the carrying amount of an intangible asset, as a result of a revaluation, is credited directly toequity in the revaluation reserve. The increase is recognised in profit or loss to the extent that it reverses arevaluation decrease of the same asset previously recognised in profit or loss.

Any decrease in the carrying amount of an intangible asset, as a result of a revaluation, is recognised in profit orloss in the current period. The decrease is debited directly to equity in the revaluation reserve to the extent ofany credit balance existing in the revaluation surplus in respect of that asset.

An intangible asset is regarded as having an indefinite useful life when, based on all relevant factors, there is noforeseeable limit to the period over which the asset is expected to generate net cash inflows. Amortisation is notprovided for these intangible assets. For all other intangible assets amortisation is provided on a straight linebasis over their useful life.

Reassessing the useful life of an intangible asset with a definite useful life after it was classified as indefinite isan indicator that the asset may be impaired. As a result the asset is tested for impairment and the remainingcarrying amount is amortised over its useful life.

19

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Accounting Policies

1.4

Intangible assets (continued)

Internally generated brands, mastheads, publishing titles, customer lists and items similar in substance are notrecognised as intangible assets.

Amortisation is provided to write down the intangible assets, on a straight line basis, to their residual values asfollows:

Item

Useful life

Brand names

indefinite

1.5

Financial instruments

Initial recognition

The group classifies financial instruments, or their component parts, on initial recognition as a financial asset, afinancial liability or an equity instrument in accordance with the substance of the contractual arrangement.

Financial assets and financial liabilities are recognised on the group's balance sheet when the group becomesparty to the contractual provisions of the instrument.

Loans to (from) group companies

These included loans to holding companies, fellow subsidiaries, subsidiaries, joint ventures and associates andare recognised initially at fair value plus direct transaction costs.

Subsequently these loans are measured at amortised cost using the effective interest rate method, less anyimpairment loss recognised to reflect irrecoverable amounts.

On loans receivable an impairment loss is recognised in profit or loss when there is objective evidence that it isimpaired. The impairment is measured as the difference between the investment’s carrying amount and thepresent value of estimated future cash flows discounted at the effective interest rate computed at initialrecognition.

Impairment losses are reversed in subsequent periods when an increase in the investment’s recoverableamount can be related objectively to an event occurring after the impairment was recognised, subject to therestriction that the carrying amount of the investment at the date the impairment is reversed shall not exceedwhat the amortised cost would have been had the impairment not been recognised.

Loans to shareholders, directors, managers and employees

These financial assets are initially recognised at fair value plus direct transaction costs.

Subsequently these loans are measured at amortised cost using the effective interest rate method, less anyimpairment loss recognised to reflect irrecoverable amounts.

On loans receivable an impairment loss is recognised in profit or loss when there is objective evidence that it isimpaired. The impairment is measured as the difference between the investment’s carrying amount and thepresent value of estimated future cash flows discounted at the effective interest rate computed at initialrecognition.

Impairment losses are reversed in subsequent periods when an increase in the investment’s recoverableamount can be related objectively to an event occurring after the impairment was recognised, subject to therestriction that the carrying amount of the investment at the date the impairment is reversed shall not exceedwhat the amortised cost would have been had the impairment not been recognised.

20

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Accounting Policies

1.5

Financial instruments (continued)

Trade and other receivables

Trade receivables are measured at initial recognition at fair value, and are subsequently measured at amortisedcost using the effective interest rate method. Appropriate allowances for estimated irrecoverable amounts arerecognised in profit or loss when there is objective evidence that the asset is impaired. The allowancerecognised is measured as the difference between the asset’s carrying amount and the present value ofestimated future cash flows discounted at the effective interest rate computed at initial recognition.

Trade and other payables

Trade payables are initially measured at fair value, and are subsequently measured at amortised cost, using theeffective interest rate method.

Cash and cash equivalents

Cash and cash equivalents comprise cash on hand and demand deposits, and other short-term highly liquidinvestments that are readily convertible to a known amount of cash and are subject to an insignificant risk ofchanges in value. These are initially and subsequently recorded at fair value.

Bank overdraft and borrowings

Bank overdrafts and borrowings are initially measured at fair value, and are subsequently measured atamortised cost, using the effective interest rate method. Any difference between the proceeds (net of transactioncosts) and the settlement or redemption of borrowings is recognised over the term of the borrowings inaccordance with the group’s accounting policy for borrowing costs.

Held for trading financial assets

Investments are recognised and derecognised on a trade date basis where the purchase or sale of aninvestment is under a contract of which the terms require delivery of the investment within the timeframeestablished by the market concerned.

Investments are measured initially and subsequently at fair value, gains and losses arising from changes in fairvalue are included in profit or loss for the period.

Derivatives

Derivative financial instruments, consisting of foreign exchange contracts and interest rate swaps, are initiallymeasured at fair value on the contract date, and are re-measured to fair value at subsequent reporting dates.

Derivatives embedded in other financial instruments or other non-financial host contracts are treated as separatederivatives when their risks and characteristics are not closely related to those of the host contract and the hostcontract is not carried at fair value with unrealised gains or losses reported in profit or loss.

Changes in the fair value of derivative financial instruments are recognised in profit or loss as they arise.

Available for sale financial assets

Investments are recognised and derecognised on a trade date basis where the purchase or sale of aninvestment is under a contract whose terms require delivery of the investment within the timeframe establishedby the market concerned.

These investments are measured initially and subsequently at fair value. Gains and losses arising from changesin fair value are recognised directly in equity until the security is disposed of or is determined to be impaired, atwhich time the cumulative gain or loss previously recognised in equity is included in the profit or loss for the

21

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Accounting Policies

1.5

Financial instruments (continued)

period.

Impairment losses recognised in profit or loss for equity investments classified as available-for-sale are notsubsequently reversed through profit or loss. Impairment losses recognised in profit or loss for debt instrumentsclassified as available-for-sale are subsequently reversed if an increase in the fair value of the instrument can beobjectively related to an event occurring after the recognition of the impairment loss.

Held to maturity and loans and receivables

These financial assets are initially recognised at fair value plus direct transaction costs.

At subsequent reporting dates these are measured at amortised cost using the effective interest rate method,less any impairment loss recognised to reflect irrecoverable amounts. An impairment loss is recognised in profitor loss when there is objective evidence that the asset is impaired, and is measured as the difference betweenthe investment’s carrying amount and the present value of estimated future cash flows discounted at theeffective interest rate computed at initial recognition. Impairment losses are reversed in subsequent periodswhen an increase in the investment’s recoverable amount can be related objectively to an event occurring afterthe impairment was recognised, subject to the restriction that the carrying amount of the investment at the datethe impairment is reversed shall not exceed what the amortised cost would have been had the impairment notbeen recognised.

Financial assets that the group has the positive intention and ability to hold to maturity are classified as maturity.

1.6

Tax

Current tax assets and liabilities

Current tax for current and prior periods is, to the extent unpaid, recognised as a liability. If the amount alreadypaid in respect of current and prior periods exceeds the amount due for those periods, the excess is recognisedas an asset.

Current tax liabilities (assets) for the current and prior periods are measured at the amount expected to be paidto (recovered from) the tax authorities, using the tax rates (and tax laws) that have been enacted or substantivelyenacted by the balance sheet date.

Deferred tax assets and liabilities

A deferred tax liability is recognised for all taxable temporary differences, except to the extent that the deferredtax liability arises from:

� the initial recognition of goodwill; or

� goodwill for which amortisation is not deductible for tax purposes; or

� the initial recognition of an asset or liability in a transaction which:

- is not a business combination; and

- at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss).

A deferred tax liability is recognised for all taxable temporary differences associated with investments insubsidiaries, branches and associates, and interests in joint ventures, except to the extent that both of thefollowing conditions are satisfied:

� the parent, investor or venturer is able to control the timing of the reversal of the temporary difference;and

� it is probable that the temporary difference will not reverse in the foreseeable future.

22

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Accounting Policies

1.6

Tax (continued)

A deferred tax asset is recognised for all deductible temporary differences to the extent that it is probable thattaxable profit will be available against which the deductible temporary difference can be utilised, unless thedeferred tax asset arises from the initial recognition of an asset or liability in a transaction that:

� is not a business combination; and

� at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss).

A deferred tax asset is recognised for all deductible temporary differences arising from investments insubsidiaries, branches and associates, and interests in joint ventures, to the extent that it is probable that:

� the temporary difference will reverse in the foreseeable future; and

� taxable profit will be available against which the temporary difference can be utilised.

A deferred tax asset is recognised for the carry forward of unused tax losses and unused STC credits to theextent that it is probable that future taxable profit will be available against which the unused tax losses andunused STC credits can be utilised.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply to the period whenthe asset is realised or the liability is settled, based on tax rates (and tax laws) that have been enacted orsubstantively enacted by the balance sheet date.

Tax expenses

Current and deferred taxes are recognised as income or an expense and included in profit or loss for the period,except to the extent that the tax arises from:

� a transaction or event which is recognised, in the same or a different period, directly in equity, or

� a business combination.

Current tax and deferred taxes are charged or credited directly to equity if the tax relates to items that arecredited or charged, in the same or a different period, directly to equity.

1.7

Leases

A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental toownership. A lease is classified as an operating lease if it does not transfer substantially all the risks and rewardsincidental to ownership.

Finance leases - lessor

The group recognises finance lease receivables on the balance sheet at the amount of the net investment in theleases.

Finance income is recognised based on a pattern reflecting a constant periodic rate of return on the group’s netinvestment in the finance lease.

Finance leases – lessee

Finance leases are recognised as assets and liabilities in the balance sheet at amounts equal to the fair value ofthe leased property or, if lower, the present value on the minimum lease payments. The corresponding liability tothe lessor is included in the balance sheet as a finance lease obligation.

The discount rate used in calculating the present value of the minimum lease payments is the interest rateimplicit in the lease.

The lease payments are apportioned between the finance charge and reduction of the outstanding liability.Thefinance charge is allocated to each period during the lease term so as to produce a constant periodic rate on theremaining balance of the liability.

23

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Accounting Policies

1.7

Leases (continued)

Operating leases – lessee

Operating lease payments are recognised as an expense on a straight-line basis over the lease term. Thedifference between the amounts recognised as an expense and the contractual payments are recognised as anoperating lease asset. This liability is not discounted.

Any contingent rents are expensed in the period they are incurred.

1.8

Inventories

Inventories are measured at the lower of cost and net realisable value.

The cost of inventories comprises of all costs of purchase, costs of conversion and other costs incurred inbringing the inventories to their present location and condition. The latter is allocated on the basis of normaloperating capacity.

The cost of inventories of items that are not ordinarily interchangeable and goods or services produced andsegregated for specific projects is assigned using specific identification of the individual costs.

The cost of inventories is assigned using the first-in, first-out (FIFO) formula. The same cost formula is used forall inventories having a similar nature and use to the entity.

When inventories are sold, the carrying amount of those inventories are recognised as an expense in the periodin which the related revenue is recognised. The amount of any write-down of inventories to net realisable valueand all losses of inventories are recognised as an expense in the period the write-down or loss occurs. Theamount of any reversal of any write-down of inventories, arising from an increase in net realisable value, arerecognised as a reduction in the amount of inventories recognised as an expense in the period in which thereversal occurs.

1.9

Non-current assets held for sale (and) (disposal groups)

Non-current assets and disposal groups are classified as held for sale if their carrying amount will be recoveredthrough a sale transaction rather than through continuing use. This condition is regarded as met only when thesale is highly probable and the asset (or disposal group) is available for immediate sale in its present condition.Management must be committed to the sale, which should be expected to qualify for recognition as a completedsale within one year from the date of classification.

Non-current assets held for sale (or disposal group) are measured at the lower of its carrying amount and fairvalue less costs to sell.

A non-current asset is not depreciated (or amortised) while it is classified as held for sale, or while it is part of adisposal group classified as held for sale.

Interest and other expenses attributable to the liabilities of a disposal group classified as held for sale arerecognised in profit or loss.

24

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Accounting Policies

1.10

Impairment of assets

The group assesses at each balance sheet date whether there is any indication that an asset may be impaired.If any such indication exists, the group estimates the recoverable amount of the asset.

Irrespective of whether there is any indication of impairment, the group also:

� tests intangible assets with an indefinite useful life or intangible assets not yet available for use forimpairment annually by comparing its carrying amount with its recoverable amount. This impairmenttest is performed during the annual year and at the same time every year.

� tests goodwill acquired in a business combination for impairment annually.

If there is any indication that an asset may be impaired, the recoverable amount is estimated for the individualasset. If it is not possible to estimate the recoverable amount of the individual asset, the recoverable amount ofthe cash-generating unit to which the asset belongs is determined.

The recoverable amount of an asset or a cash-generating unit is the higher of its fair value less costs to sell andits value in use.

If the recoverable amount of an asset is less than its carrying amount, the carrying amount of the asset isreduced to its recoverable amount. That reduction is an impairment loss.

An impairment loss of assets carried at cost less any accumulated depreciation or amortisation is recognisedimmediately in profit or loss. Any impairment loss of a revalued asset is treated as a revaluation decrease.

Goodwill acquired in a business combination is, from the acquisition date, allocated to each of the cash-generating units, or groups of cash-generating units, that are expected to benefit from the synergies of thecombination.

An impairment loss is recognised for cash-generating units if the recoverable amount of the unit is less than thecarrying amount of the units. The impairment loss is allocated to reduce the carrying amount of the assets of theunit in the following order:

� first, to reduce the carrying amount of any goodwill allocated to the cash-generating unit and

� then, to the other assets of the unit, pro rata on the basis of the carrying amount of each asset in theunit.

An entity assesses at each reporting date whether there is any indication that an impairment loss recognised inprior periods for assets other than goodwill may no longer exist or may have decreased. If any such indicationexists, the recoverable amounts of those assets are estimated.

The increased carrying amount of an asset other than goodwill attributable to a reversal of an impairment lossdoes not exceed the carrying amount that would have been determined had no impairment loss been recognisedfor the asset in prior years.

A reversal of an impairment loss of assets carried at cost less accumulated depreciation or amortisation otherthan goodwill is recognised immediately in profit or loss. Any reversal of an impairment loss of a revalued assetis treated as a revaluation increase.

1.11

Share capital and equity

An equity instrument is any contract that evidences a residual interest in the assets of an entity after deductingall of its liabilities.

25

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Accounting Policies

1.12

Employee benefits

Short-term employee benefits

The cost of short-term employee benefits, (those payable within 12 months after the service is rendered, such aspaid vacation leave and sick leave, bonuses, and non-monetary benefits such as medical care), are recognisedin the period in which the service is rendered and are not discounted.

The expected cost of compensated absences is recognised as an expense as the employees render servicesthat increase their entitlement or, in the case of non-accumulating absences, when the absence occurs.

The expected cost of profit sharing and bonus payments is recognised as an expense when there is a legal orconstructive obligation to make such payments as a result of past performance.

1.13

Provisions and contingencies

Provisions are recognised when:

� the group has a present obligation as a result of a past event;

� it is probable that an outflow of resources embodying economic benefits will be required to settle theobligation; and

� a reliable estimate can be made of the obligation.

The amount of a provision is the present value of the expenditure expected to be required to settle the obligation.

Where some or all of the expenditure required to settle a provision is expected to be reimbursed by anotherparty, the reimbursement shall be recognised when, and only when, it is virtually certain that reimbursement willbe received if the entity settles the obligation. The reimbursement shall be treated as a separate asset. Theamount recognised for the reimbursement shall not exceed the amount of the provision.

If an entity has a contract that is onerous, the present obligation under the contract shall be recognised andmeasured as a provision.

A constructive obligation to restructure arises only when an entity:

� has a detailed formal plan for the restructuring, identifying at least:

- the business or part of a business concerned;

- the principal locations affected;

- the location, function, and approximate number of employees who will be compensated forterminating their services;

- the expenditures that will be undertaken; and

- when the plan will be implemented; and

� has raised a valid expectation in those affected that it will carry out the restructuring by starting toimplement that plan or announcing its main features to those affected by it.

After their initial recognition contingent liabilities recognised in business combinations that are recognisedseparately are subsequently measured at the higher of:

� the amount that would be recognised as a provision; and

� the amount initially recognised less cumulative amortisation.

1.14

Revenue

Revenue from the sale of goods is recognised when all the following conditions have been satisfied:

� the group has transferred to the buyer the significant risks and rewards of ownership of the goods;

� the group retains neither continuing managerial involvement to the degree usually associated withownership nor effective control over the goods sold;

� the amount of revenue can be measured reliably;

� it is probable that the economic benefits associated with the transaction will flow to the group; and

� the costs incurred or to be incurred in respect of the transaction can be measured reliably.

26

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Accounting Policies

1.14

Revenue (continued)

When the outcome of a transaction involving the rendering of services can be estimated reliably, revenueassociated with the transaction is recognised by reference to the stage of completion of the transaction at thebalance sheet date. The outcome of a transaction can be estimated reliably when all the following conditions aresatisfied:

� the amount of revenue can be measured reliably;

� it is probable that the economic benefits associated with the transaction will flow to the group;

� the stage of completion of the transaction at the balance sheet date can be measured reliably; and

� the costs incurred for the transaction and the costs to complete the transaction can be measuredreliably.

When the outcome of the transaction involving the rendering of services cannot be estimated reliably, revenueshall be recognised only to the extent of the expenses recognised that are recoverable.

Service revenue is recognised by reference to the stage of completion of the transaction at balance sheet date.Stage of completion is determined by the proportion of costs incurred to date bear to the total estimated costs ofthe transaction.

Contract revenue comprises:

� the initial amount of revenue agreed in the contract; and

� variations in contract work, claims and incentive payments:

- to the extent that it is probable that they will result in revenue; and

- they are capable of being reliably measured.

Revenue is measured at the fair value of the consideration received or receivable and represents the amountsreceivable for goods and services provided in the normal course of business, net of trade discounts and volumerebates, and value added tax.

Interest is recognised, in profit or loss, using the effective interest rate method.

Royalties are recognised on the accrual basis in accordance with the substance of the relevant agreements.

Dividends are recognised, in profit or loss, when the company’s right to receive payment has been established.

Service fees included in the price of the product are recognised as revenue over the period during which theservice is performed.

1.15

Turnover

Turnover comprises of sales to customers and service rendered to customers. Turnover is stated at the invoiceamount and is exclusive of interest and value added taxation.

1.16

Cost of sales

When inventories are sold, the carrying amount of those inventories is recognised as an expense in the period inwhich the related revenue is recognised. The amount of any write-down of inventories to net realisable value andall losses of inventories are recognised as an expense in the period the write-down or loss occurs. The amountof any reversal of any write-down of inventories, arising from an increase in net realisable value, is recognised asa reduction in the amount of inventories recognised as an expense in the period in which the reversal occurs.

The related cost of providing services recognised as revenue in the current period is included in cost of sales.

Contract costs comprise:

� costs that relate directly to the specific contract;

� costs that are attributable to contract activity in general and can be allocated to the contract; and

� such other costs as are specifically chargeable to the customer under the terms of the contract.

27

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Accounting Policies

1.17

Borrowing costs

Borrowing costs are recognised as an expense in the period in which they are incurred.

1.18

Translation of foreign currencies

Foreign currency transactions

A foreign currency transaction is recorded, on initial recognition in Rands, by applying to the foreign currencyamount the spot exchange rate between the functional currency and the foreign currency at the date of thetransaction.

At each balance sheet date:

� foreign currency monetary items are translated using the closing rate;

� non-monetary items that are measured in terms of historical cost in a foreign currency are translatedusing the exchange rate at the date of the transaction; and

� non-monetary items that are measured at fair value in a foreign currency are translated using theexchange rates at the date when the fair value was determined.

Exchange differences arising on the settlement of monetary items or on translating monetary items at ratesdifferent from those at which they were translated on initial recognition during the period or in previous annualfinancial statements are recognised in profit or loss in the period in which they arise.

When a gain or loss on a non-monetary item is recognised directly in equity, any exchange component of thatgain or loss is recognised directly in equity. When a gain or loss on a non-monetary item is recognised in profit orloss, any exchange component of that gain or loss is recognised in profit or loss.

Cash flows arising from transactions in a foreign currency are recorded in Rands by applying to the foreigncurrency amount the exchange rate between the Rand and the foreign currency at the date of the cash flow.

28

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Notes to the Annual Financial Statements

Group

Company

Figures in Rand

2006

2005

2006

2005

2.

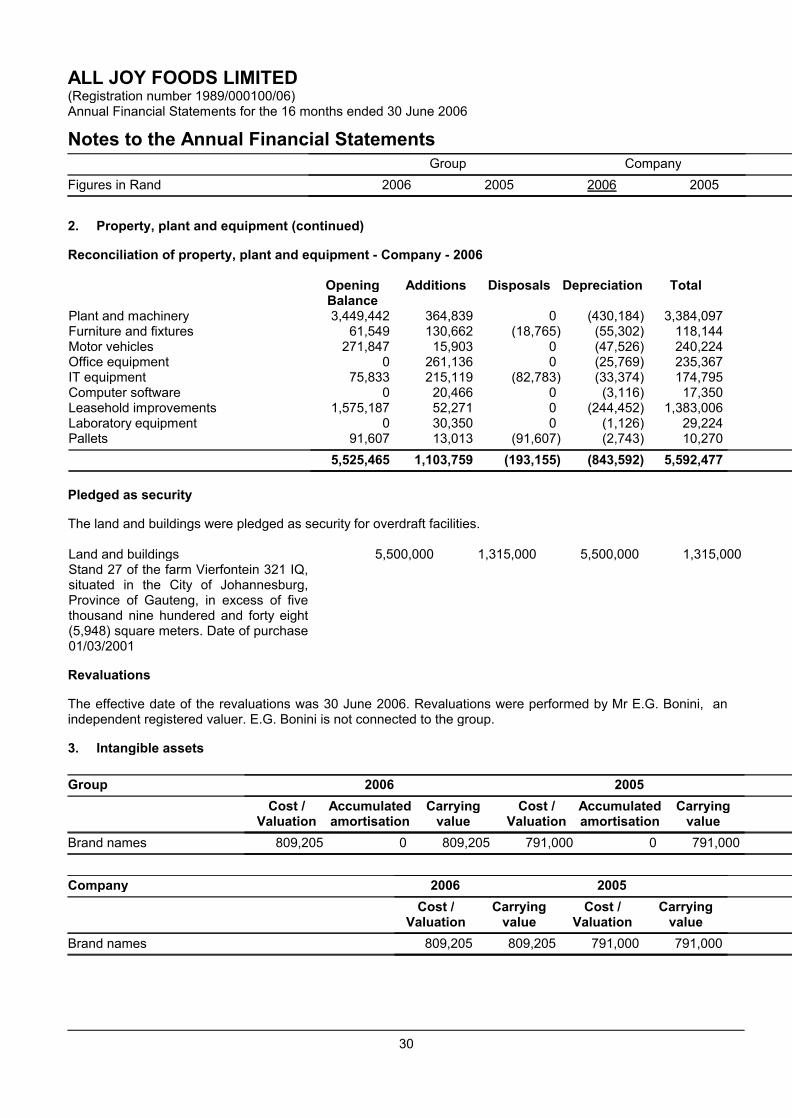

Property, plant and equipment

Group

2006

2005

Cost /

Valuation Accumulated

depreciation Carrying

value Cost /

Valuation Accumulated

depreciation Carrying

value

Land and Buildings 5,500,000

0

5,500,000

1,350,839

(35,839)

1,315,000

Plant and machinery 6,339,985

(2,955,888)

3,384,097

5,975,147

(2,525,705)

3,449,442

Furniture and fixtures 546,103

(427,959)

118,144

905,497

(843,948)

61,549

Motor vehicles 647,186

(406,962)

240,224

631,283

(359,436)

271,847

Office equipment 261,136

(25,769)

235,367

0

0

0

IT equipment 206,892

(32,097)

174,795

75,833

0

75,833

Computer software 20,466

(3,116)

17,350

0

0

0

Leasehold improvements 1,863,321

(480,315)

1,383,006

1,811,050

(235,863)

1,575,187

Laboratory equipment 124,452

(95,228)

29,224

0

0

0

Pallets 13,013

(2,743)

10,270

91,607

0

91,607

Total 15,522,554 (4,430,077) 11,092,477 10,841,256 (4,000,791) 6,840,465

Company

2006

2005

Cost /

Valuation Accumulated

depreciation Carrying

value Cost /

Valuation Accumulated

depreciation Carrying

value

Plant and machinery 6,339,985

(2,955,888)

3,384,097

5,975,147

(2,525,705)

3,449,442

Furniture and fixtures 546,103

(427,959)

118,144

905,497

(843,948)

61,549

Motor vehicles 647,186

(406,962)

240,224

631,283

(359,436)

271,847

Office equipment 261,136

(25,769)

235,367

0

0

0

IT equipment 206,892

(32,097)

174,795

75,833

0

75,833

Computer software 20,466

(3,116)

17,350

0

0

0

Leasehold improvements 1,863,321

(480,315)

1,383,006

1,811,050

(235,863)

1,575,187

Laboratory equipment 124,452

(95,228)

29,224

0

0

0

Pallets 13,013

(2,743)

10,270

91,607

0

91,607

Total 10,022,554 (4,430,077) 5,592,477 9,490,417 (3,964,952) 5,525,465

Reconciliation of property, plant and equipment - Group - 2006

Opening

Balance Additions

Disposals

Revaluations

Depreciation

Total

Land and Buildings

1,315,000 15,322 0 4,169,678 0 5,500,000Plant and machinery

3,449,442 364,839 0 0 (430,184) 3,384,097

Furniture and fixtures

61,549 130,662 (18,765) 0 (55,302) 118,144Motor vehicles

271,847 15,903 0 0 (47,526) 240,224

Office equipment

0 261,136 0 0 (25,769) 235,367IT equipment

75,833 215,119 (82,783) 0 (33,374) 174,795

Computer software

0 20,466 0 0 (3,116) 17,350Leasehold improvements

1,575,187 52,271 0 0 (244,452) 1,383,006

Laboratory equipment

0 30,350 0 0 (1,126) 29,224Pallets

91,607 13,013 (91,607) 0 (2,743) 10,270

6,840,465 1,119,081 (193,155) 4,169,678 (843,592) 11,092,477

29

ALL JOY FOODS LIMITED

(Registration number 1989/000100/06)

Annual Financial Statements for the 16 months ended 30 June 2006

Notes to the Annual Financial Statements

Group

Company

Figures in Rand

2006

2005

2006

2005

2.

Property, plant and equipment (continued)

Reconciliation of property, plant and equipment - Company - 2006

Opening

Balance Additions

Disposals

Depreciation

Total

Plant and machinery

3,449,442 364,839 0 (430,184) 3,384,097Furniture and fixtures

61,549 130,662 (18,765) (55,302) 118,144

Motor vehicles

271,847 15,903 0 (47,526) 240,224Office equipment

0 261,136 0 (25,769) 235,367

IT equipment