alejandro izquierdo andrew powell research department, iadb

TRANSCRIPT

Alejandro IzquierdoAlejandro IzquierdoAndrew PowellAndrew Powell

Research Department, IADBResearch Department, IADB

Unlocking CreditUnlocking Credit

• Stylized Facts• Crisis and Volatility• Sudden Stops and Banking Crises• Crisis Resolution• Crisis Prevention• Exit Rules• Creditor Rights• Industrial Structure• The Policy Agenda

Unlocking CreditUnlocking Credit

• Stylized Facts• Crisis and Volatility• Sudden Stops and Banking Crises• Crisis Resolution• Crisis Prevention• Exit Rules• Creditor Rights• Industrial Structure• The Policy Agenda

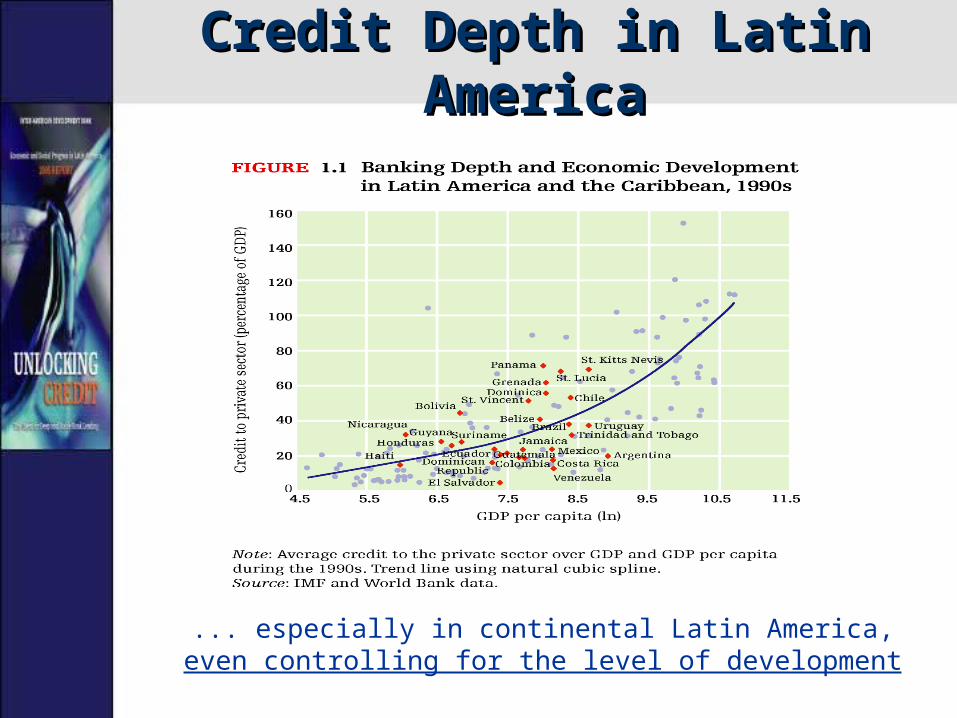

Credit Depth in Latin AmericaCredit Depth in Latin America

In Latin America, credit is scarce ...

Note: Simple average within regions. Mean Value for the 1990s.

Source: World Bank data.

Credit Depth in Latin AmericaCredit Depth in Latin America

... especially in continental Latin America, even controlling for the level of development

Interest Rate MarginInterest Rate Margin

Credit in Latin America is costly.

Note: Simple average within regions. Mean Value for the 1990s.

Source: IMF data.

Interest Rate MarginInterest Rate Margin

Low financial development is associated with high spreads.

Credit VolatilityCredit Volatility

And credit is also highly volatile

Credit VolatilityCredit Volatility

...credit volatility is related with an underdeveloped financial sector.

Recurring Banking CrisesRecurring Banking Crises

LAC is the region of the world with the highest banking crisis recurrence

Banking Credit in Latin AmericaBanking Credit in Latin America

• No wonder, lack of credit is No wonder, lack of credit is firms’ concernfirms’ concern number 1number 1

• Moreover, access to credit is restrictedrestricted for certain groups, in particular SMEs

• These characteristics of credit limitlimit economic performance and poverty alleviation.

This Report ...This Report ...

• Explores these characteristics of banking credit from three perspectives– The effects of crises, their resolution and

prevention– The impact of changes in the structure of the

banking sector– The role played by the institutions supporting

credit markets

Unlocking CreditUnlocking Credit

• Stylized Facts• Crisis and Volatility• Sudden Stops and Banking Crises• Crisis Resolution• Crisis Prevention• Exit Rules• Creditor Rights• Industrial Structure• The Policy Agenda

Crisis and VolatilityCrisis and Volatility• The volatility of the banking sector reflects a history of

macroeconomic imbalances

In many countries dollarization is high ...

Crisis and VolatilityCrisis and Volatility

... as well as public sector debt holdings.

Unlocking CreditUnlocking Credit

• Stylized Facts• Crisis and Volatility• Sudden Stops and Banking Crises• Crisis Resolution• Crisis Prevention• Exit Rules• Creditor Rights• Industrial Structure• The Policy Agenda

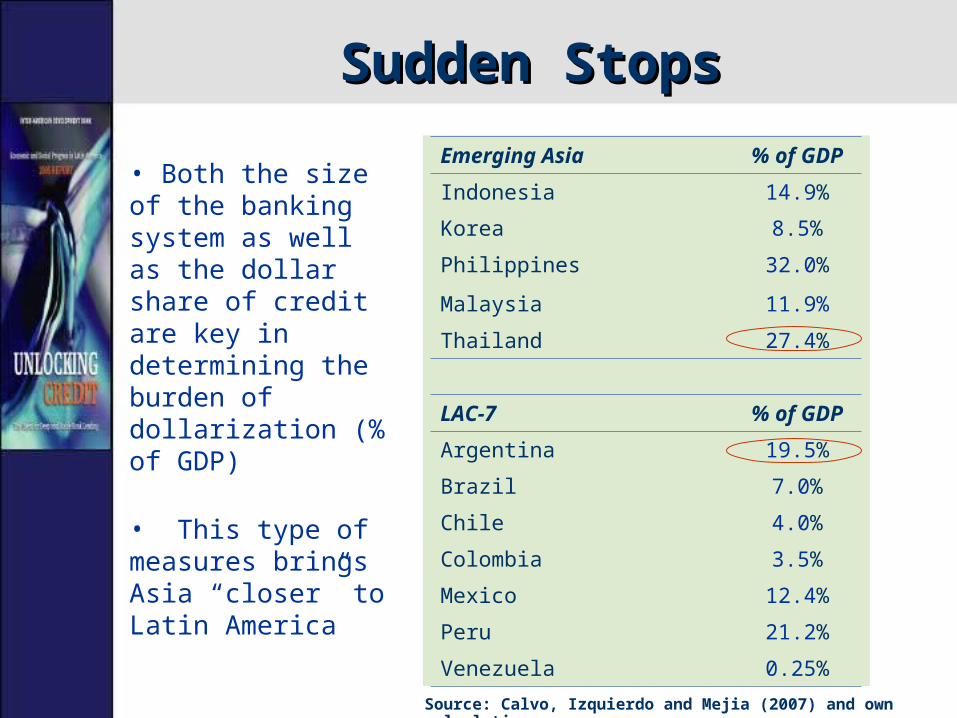

Sudden StopsSudden Stops

Despite contagion in capital markets, the probability of a sudden stop depends on the interaction between the supply of tradable goods (a proxy for potential changes in relative prices) and the degree of dollarization

Sudden StopsSudden Stops

Emerging Asia % of GDP

Indonesia 14.9%

Korea 8.5%

Philippines 32.0%

Malaysia 11.9%

Thailand 27.4%

LAC-7 % of GDP

Argentina 19.5%

Brazil 7.0%

Chile 4.0%

Colombia 3.5%

Mexico 12.4%

Peru 21.2%

Venezuela 0.25%

Source: Calvo, Izquierdo and Mejia (2007) and own calculations.

• Both the size of the banking system as well as the dollar share of credit are key in determining the burden of dollarization (% of GDP)

• This type of measures brings Asia “closer” to Latin America

Twin CrisesTwin CrisesThis is highly relevant considering that sudden stops and

banking crises are another set of twins (75% in dollarized countries)

Balance SheetsBalance Sheets

Abrupt changes in relative prices lead to government’s and non tradable firm’s bankruptcies.

Unlocking CreditUnlocking Credit

• Stylized Facts• Crisis and Volatility• Sudden Stops and Banking Crises• Crisis Resolution• Crisis Prevention• Exit Rules• Creditor Rights• Industrial Structure• The Policy Agenda

Crisis Resolution: Basic PrinciplesCrisis Resolution: Basic Principles

Principles

• Allocation of non-inflationary public funds

• Ensure risk takers bear a large fraction of restructuring costs

• Avoid gambling for resurrection

Actions

• Reserve accumulation or foreign packages

• Discrimination among banks and depositors

• Resolution of insolvent banks (private & public)

Unlocking CreditUnlocking Credit

• Stylized Facts• Crisis and Volatility• Sudden Stops and Banking Crises• Crisis Resolution• Crisis Prevention• Exit Rules• Creditor Rights• Industrial Structure• The Policy Agenda

Regulation and SupervisionRegulation and Supervision

• Regulation and supervision have been weak in Latin America.

• However, the situation is improving….

Low Compliance withLow Compliance withBasel Core PrinciplesBasel Core Principles

Average

0

5

10

15

20

25

Compliant and Largely CompliantPrinciples

Materially Non-Compliant and Non-Compliant Principles

Initial Assessment

Update

Guatemala

-

5

10

15

20

25

30

Compliant and Largely Compliant Principles Materially Non-Compliant and Non-CompliantPrinciples

Initial Assessment

Update

Mexico

0

5

10

15

20

25

30

Compliant and Largely CompliantPrinciples

Materially Non-Compliant and Non-Compliant Principles

Initial Assessment

Update

Peru

-

5

10

15

20

25

30

35

Compliant and Largely Compliant Principles Materially Non-Compliant and Non-CompliantPrinciples

Initial Assessment

Update

Source: IMF-World Bank Financial Sector Assessment Program, Presentation A. de la Torre, WB

Selected Countries:Selected Countries:Improvements in BCP ComplianceImprovements in BCP Compliance

Basel II Implementation (cont)Basel II Implementation (cont)

• Some countries fall between two stools– Standardized approach does little to link capital to risk

– More advanced Internal Rating Based Approach (IRB) approach give too much autonomy to banks and are difficult to supervise

• I have suggested an intermediate Centralized Rating Based (CRB) Approach– See Powell (2004) “Sailing Through the Sea of Standards” World

Bank Policy Research Working Paper Series 3387– Majnoni and Powell (2005) Bank Capital and Loan-Loss

Reserves under Basel II: Implications for Latin America Economia p105-149

Basel II Implementation (cont)Basel II Implementation (cont)

• Is Basel II a standard for 100 banks across G10 or for all banks in each G100?

• The US is keeping most banks on Basel I and may allow a handful to adopt the most advanced approaches but still uncertain…

• Some countries in LAC are staying with Basel I for now, but even here there are adaptations…

• China has said Basel I + = Basel I plus Operational Risk

• Some may allow some banks aspects of Basel II but there is a danger that the essence of a standard will be lost as countries adapt different elements

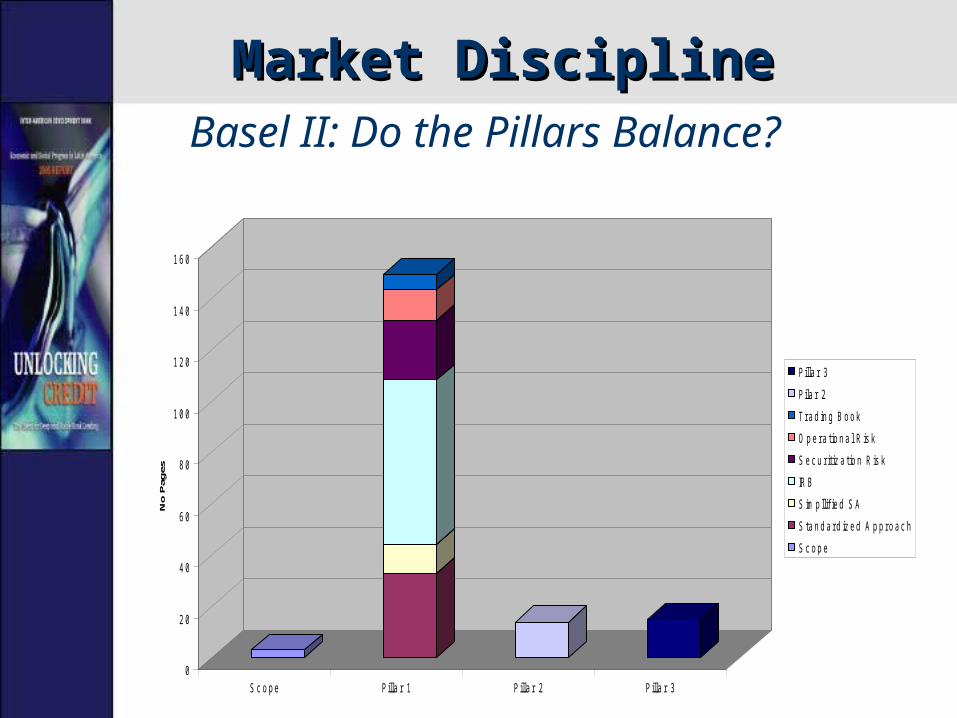

Market DisciplineMarket Discipline

• Market discipline is alive in Latin America– Martinez Peria and Schmukler (2001): depositors run

weak banks and demand higher interest rates.

– Galindo, Loboguerrero and Powell (2005): ….and banks react, shrinking assets and/or increasing capital

• Is the best/only form of discipline for banks?– Berth, Caprio and Levine (2006) “Rethinking Banking

Regulation: When Angels Govern…”

• Need to ensure those that take risks bear costs…• Basel II does not go far enough….

Market DisciplineMarket DisciplineBasel II: Do the Pillars Balance?

0

2 0

4 0

6 0

8 0

1 0 0

1 2 0

1 4 0

1 6 0

No

Page

s

S c o p e P illa r 1 P illa r 2 P illa r 3

P illa r 3

P ila r 2

T r a d in g B o o k

O p e r a t io n a l R is k

S e c u r it iz a t io n R is k

IR B

S im p llif ie d S A

S t a n d a r d iz e d A p p r o a c h

S c o p e

Unlocking CreditUnlocking Credit

• Stylized Facts• Crisis and Volatility• Sudden Stops and Banking Crises• Crisis Resolution• Crisis Prevention• Exit Rules• Creditor Rights• Industrial Structure• The Policy Agenda

Bank Exit Rules

• Latin America has been introducing new exit rules for banks

• In the wake of the 1995 “Tequila crisis”, Argentina adopted a “least cost” resolution process for the deposit insurance fund.

• And the possibility of creating a “good bank” to be sold and a “bad bank” to be liquidated

• This idea has been catching on in several countries, to resolve problem banks quickly and avoid costly judicial procedures.

Unlocking CreditUnlocking Credit

• Stylized Facts• Crisis and Volatility• Sudden Stops and Banking Crises• Crisis Resolution• Crisis Prevention• Exit Rules• Creditor Rights• Industrial Structure• The Policy Agenda

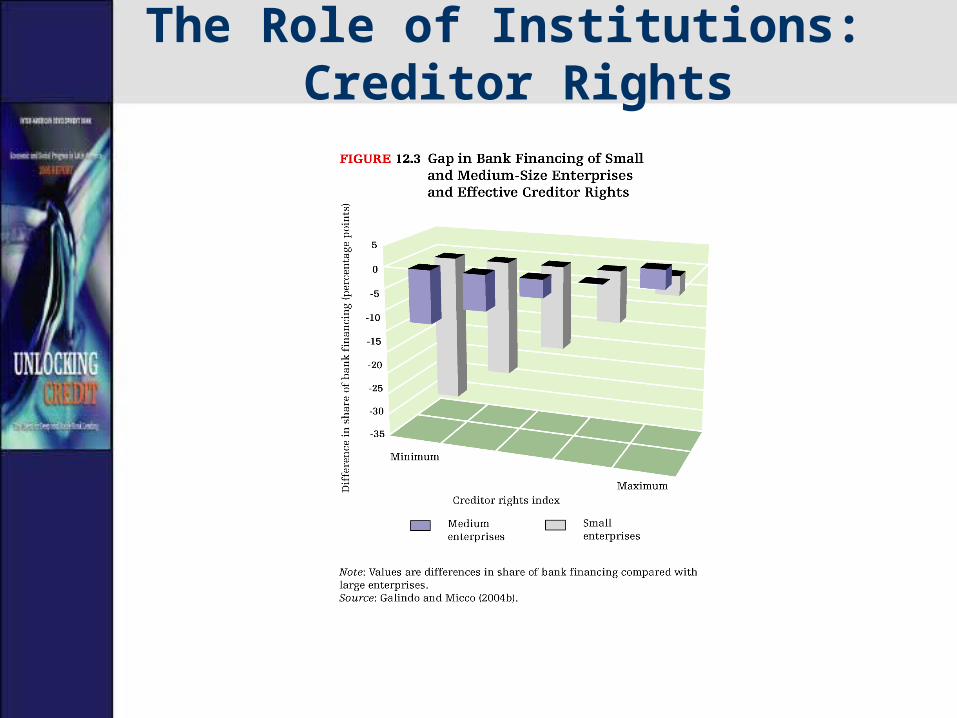

The Role of Institutions: Weak Creditor Rights in LAC

The Role of Institutions: Creditor Rights

• Creditor rights in LAC are weak. – Regulations in favor of debtors during bankruptcy. – Courts are inefficient (bankruptcy procedure, 4 years)– Obstacles to recover collateral

• Improving creditor rights can:– increase financial depth (by 15% of GDP)– reduce credit volatility by nearly half...– and increase access to credit by SMEs by at least 15%.

• However, reform is difficult to implement.• Banks are seen as bad, but weak creditor rights

implies no credit market hurting good borrowers.

The Role of Institutions: Creditor Rights

The Role of Institutions: Creditor Rights

The Role of Institutions: Creditor Rights

Unlocking CreditUnlocking Credit

• Stylized Facts• Crisis and Volatility• Sudden Stops and Banking Crises• Crisis Resolution• Crisis Prevention• Exit Rules• Creditor Rights• Industrial Structure• The Policy Agenda

Banking System Structure: Consolidation Banking System Structure: Consolidation

• Following the banking crises of the 1980’s and 1990’s, and financial liberalization, there has been massive consolidation in the banking industry

• But concentration has not reduced competition.

•Higher concentration reduces NIM and overhead costs.

•Concentration has reduced credit volatility, increased access to credit, and eased supervision.

Banking System Structure:Banking System Structure:The Role of Information The Role of Information

• Normally would talk about improving credit information in terms of improving credit access or reducing non performing loans.

• But information plays a critical part in determining the industrial structure of banks too.

• Latin American financial systems are characterized by poor information flows, high swtiching costs and local monopoly power, this implies a structure of many, smaller banks with high overheads.

• As information improves, competition is enhanced and overheads must decline, concentration and lower spreads follow.

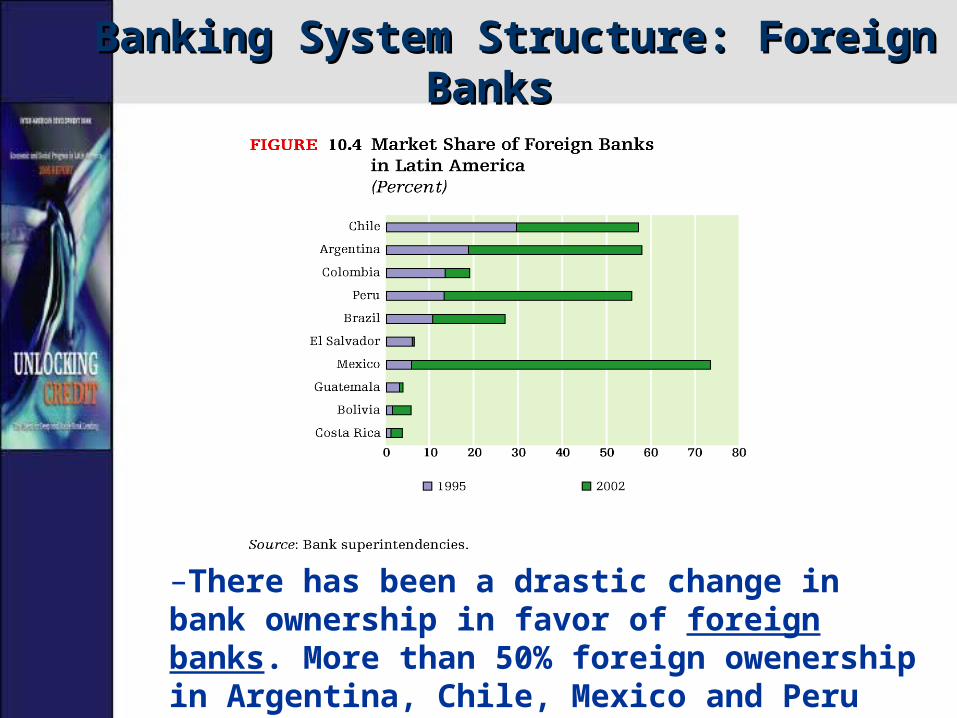

Banking System Structure: Foreign Banks Banking System Structure: Foreign Banks

–There has been a drastic change in bank ownership in favor of foreign banks. More than 50% foreign owenership in Argentina, Chile, Mexico and Peru

Banking System Structure: Foreign Banks Banking System Structure: Foreign Banks

• Foreign banking has:

– Increased efficiency (lower interest rate margins)

– Had mixed results in other areas:• There is controversy as to whether credit access has increased,

particularly to SME’s.

• Has made credit less vulnerable to liquidity shocks, but potentially more vulnerable to productivity shocks

• Raises difficult questions regarding supervision

Banking System Structure: Public Banking Banking System Structure: Public Banking

Public banks have reduced their participation in LAC through both sale and competition as private banks have grown faster

Banking System Structure: Public Banking Banking System Structure: Public Banking

• But public banking has remains an important share of total banking:– Public banks enjoy strong political support ...– They appear to be inefficient (high operating costs)– And have low portfolio quality and– Have low deposit rates due to implicit government

guarantee and implying a hidden fiscal liability.• Performance should be measured against their

mandate, but few countries are explicit about what that is and fewer have targets and evaluations.

• Tellingly they do not appear to lend more to SMEs nor to sectors that would accord with the “social mandate”.

Unlocking CreditUnlocking Credit

• Stylized Facts• Crisis and Volatility• Sudden Stops and Banking Crises• Crisis Resolution• Crisis Prevention• Exit Rules• Creditor Rights• Industrial Structure• The Policy Agenda

Policy AgendaPolicy Agenda

• Plan ahead to avoid crises– Enhanced regulation and supervision, especially in the

upswing, lean against the wind.

– Control credit booms and asset price bubbles.

– Self insurance or programs with multilaterals to reduce the probability of a Sudden Stop or reduce impact.

– Reduce risks with incentives to dedollarize and the creation of hedging markets.

– Dedollarization is not easy requires a concerted approach with monetary policy and prudential regulation

Policy AgendaPolicy Agenda

• Pay for your sins:– Crisis resolution processes must ensure that the parties

that took higher risks bear the costs. – Explicit, limited deposit insurance and appropriate exit

rules for banks.

• Play safe:– Financial regulation needs to appropriately measure

credit risks (including the treatment of dollar loans and government debt) to determine safe levels of capital- adequacy ratios and provisions.

– Supervision has improved but Basel II adoption poses many challenges for region.

– Foreign Banks can play an important role, must consider their supervision very carefully.

Policy AgendaPolicy Agenda

• Define the government’s business:– The role of government in commercial banking needs

to be defined by specifying the objectives of public banks and evaluating whether they are met in a cost effective manner.

• Design the right financial environment:– Increasing creditor protection requires a serious reform

of secured transaction laws and enhancing judicial efficiency. The creation of specialized courts to deal with collateral claims may play a role.

Alejandro IzquierdoAndrew Powell

Research Department, IADB