al-babtain company · al-babtain company inside look and ... income statement 25 balance sheet 26...

TRANSCRIPT

1

ALJAZIRA CAPITAL

Al-Babtain CompanyInside Look and Vision

Please read Disclaimer on the back

© All rights reserved, AlJAZIRA CAPITAL

Research DepartmentCompany Reports January 2010

2

Asset Management Department

Brokerage and Investment Centers

DivisionResearch Division

Head of Funds Distribution

Khaled Al-Saree’+966 1 [email protected]

Head of Brokerage - AGM

Ala’a Al-Youssef+966 1 [email protected]

Division Manager

Abdullah Alawi+966 2 [email protected]

Central RegionRegional Manager

Sultan Mutawe’+966 1 [email protected]

Area Manager

Saleh Al-Zu’bi+966 2 [email protected]

West and South RegionsRegional Manager

Abdullah Misbahi+966 2 [email protected]

Assistant Manager

Saleh Alquati+966 2 [email protected]

Area Manager - Qassim

Abdullah Ruhait+966 6 [email protected]

Officer

Wael Sindi+966 2 [email protected]

Area Manager - Eastern Region

Maher Ajaji+966 3 [email protected]

International, GCC, and Institutional Division Manager

Amjad Subeih+966 2 [email protected]

Aljazira Capital is a Saudi Investment Company licensed by the Capital Market Authority (CMA), License No. 07076-37

3

Table of Contents

INVESTMENT RISKS 7VALUATION SUMMARY 8

DCF Valuation 8Sensitivity Analysis 9Valuation under Different Scenarios 10Comparative Valuation 11Blended Valuation 12

1. Diversified product portfolio, favorable gearing 13Growth across all segments 13GCC focus a key positive for long-term growth 14…Complemented by projects across the globe 14Strategic subsidiaries and JVs helped tap growing demand 14…And unused capacity to serve built-up demand 14

2. Design, supply and installation segment to continue pulling its weight 15Has provided growth impetus so far 15Recurring revenue stream to ensure steady cash flows 15…growth to be backed by greater focus on attractive markets 15

3. Power and telecom to follow suit 16Expanding power generation capacity 16Large investments to keep momentum going 16T&D lines to supplement growth 16…Sustained demand for telecom towers 16

4. Poles and lighting to get infrastructure boost 17Investments to continue… 17Growing transportation network to augment growth 17Mega economic cities 17

5. Substantial experience in project execution 18Higher number of international orders 18

6. 9MFY09 financial performance 19Economic slowdown casts shadow over profitability 19Improving working capital position 19Debt-equity ratio eases 19

7. Company Overview 21Growth Strategy 21Product Offerings 22Shareholding Pattern 23Management 23

8. Financial Forecasts: Profitability to steadily rise 24Income Statement 25Balance Sheet 26Cash Flow Statement 27

9. Appendices 28Appendix – 1 Future power generation projects coming up in KSA 28Appendix – 2 Future transmission projects coming up in KSA 28

4

Powering up to Connect

We view Al-Babtain as a strong play on the infrastructural theme �in the GCC

Al-Babtain’s strong product portfolio indicates it is well poised to benefit from the massive spending currently underway in the infrastructure, power and telecom sectors in the GCC, the larger MENA region and South East Asia. The buoyant investment and business climate in these sectors in the GCC boosted Al-Babtain’s revenues, which expanded at a CAGR of 16.8% during FY04-08. The company’s strong project execution capabilities in regional as well as international markets supported the growth. Although 2009 was a challenging year for the company, we expect its revenues to grow 22.3% in FY10E as the macroeconomic climate improves in tandem with economic recovery and revival in oil prices. IMF expects KSA’s economy to record a strong CAGR of 4.7% during 2010-14. This is likely to substantially boost the country’s investment climate, positively impacting Al-Babtain’s end-market.

Target Price: SAR52.4Current Price: SAR35.1Upside: 49.4%

Al-Babtain Power and Telecommunication Co.Initiation | KSA | Building & Constr. 23 December 2009

Key informationReuters code: 2320.SE Bloomberg code: ALBABTAI ABCountry: Saudi ArabiaSector: Building & ConstructionPrimary Listing: TASIM-Cap: SAR1,422mn52 Weeks H/L: SAR50.5/33.9

Al-Babtain Power and Telecommunication Co. (Al-Babtain)

Established in 1955, Al-Babtain is a leading enterprise in Saudi Arabia’s engineering and manufacturing space.

The company’s product portfolio includes Outdoor Lighting (Poles, High Mast & Luminaries), Transmission and Distribution (Transmission Tower, Monopoles, and Distribution Poles), Testing Station, Telecommunications (Towers & Monopoles), Steel Structures and Galvanizing Services.

Al-Babtain’s production base is concentrated in Riyadh (Saudi Arabia) and Cairo (Egypt).

We initiate coverage on Al-Babtain Power and Telecommunication Co. (Al-Babtain) with a fair price valuation of SAR52.4. This implies an upside potential of 49.4% from current levels. We used a blended valuation approach based on the DCF and comparative methods to value the company. DCF method assumes a conservative 2.5% perpetual growth rate and a WACC of 10.5%. In our opinion, the impact of subdued FY09 earnings due to the substantial compression in margins has been more than factored into the stock price. At current levels, the Al-Babtain stock is trading at a P/E multiple of 12.4x, its all time low of its two-year historical average of 13.2x-22.7x. The stock, therefore, offers an attractive investment proposition based on the expected improvement in business volumes and margins in the wake of the reviving macroeconomic climate on the long term.

Table 1: Key Financial and Valuation Data

SAR mn (unless specified) 2008 2009E 2010E 2011E 2012E 2013E 2014E

Revenues 1,013 1,173 1,435 1,650 1,810 1,943 2,083 EBITDA 210 199 252 292 322 347 373 Net Income 131 119 165 194 217 237 259 EPS (SAR) 4.9 2.9 4.1 4.8 5.4 5.9 6.4 P/E 10.9x 12.0x 8.6x 7.3x 6.5x 6.0x 5.5xROE 28% 22% 27% 27% 26% 26% 25%ROA 11% 9% 13% 14% 14% 15% 16%

TASIBabtain

5

Design, Supply and Installation segment to provide growth impetus �

Demand for design, supply and maintenance of telecom systems gained momentum in tandem with the expansion of operations by incumbent operators and liberalization of the telecom sector in the GCC region. The segment expanded at a CAGR of 56.3% during FY2004-08, with revenue contributions surging to 30% in 2008 from 9% in 2004. Several telecom companies in the GCC have cut back their planned capex marginally, but are moving ahead with most of their expansion plans. In KSA alone, Zain KSA and Mobily are expected to jointly incur annual capital expenditure of SAR3-5 bn until 2011 to expand their network coverage. The planned capex is likely to ensure solid demand for design, installation and maintenance of telecommunication systems in the region. Maintenance of these newly-installed telecommunication systems would provide Al-Babtain a sustained recurring source of revenue. Consequently, we expect the Design, Supply and Installation segment to register a high annual average growth rate of 17.8% over FY09-14E.

Tower and Steel Structures business to supplement �

The capex likely to be incurred by large regional telecom companies would also drive demand for telecom towers. Spending in the telecom sector is also expected to benefit from a revival in expatriate inflows once economic activity in the region starts gathering pace. Additionally, demand for power transmission towers continues to grow as the region increases its power generation capacity and builds the necessary support infrastructure. In KSA alone, there are 110 ongoing power projects to boost the power generation capacity in the country that accounts for 56% of the total electricity consumed in GCC. Considering the strong demand environment, we expect Al-Babtain’s Tower and Steel Structures segment to grow at an annual average rate of 7.2% during FY09-14E.

Higher investments in infrastructure to drive demand for lighting and poles �

The aggressive investments planned in the infrastructure segment, especially transport infrastructure such as roads, railways and ports are likely to drive demand for lightings and poles. Governments in the GCC region continue to allocate huge budgetary support and are promoting investments in the infrastructure segment. The KSA government allocated SAR16.5bn (USD4.4bn) in its 2009 budget to develop municipality services, including intercity roads, bridges and road lights. The transport and communication segment had been allotted SAR14.6bn (USD3.9bn) to develop existing infrastructure and construct 5,400 km of new roads. An additional SAR7.8bn (USD2bn) has been allocated for the two industrial cities of Jubail and Yanbu. These investments will likely keep demand for outdoor lighting, luminaries and poles high. Subsequently, we expect growth in the lighting and poles segment to average 10.1% over the forecasted period (FY09-14E).

Project execution expertise would attract international orders �

Al-Babtain is expanding operations in other developing countries in the Asia Pacific region. Its share of non-KSA revenues grew from 14% in FY07 to 22% in FY08. We believe the company is rapidly tapping fast-growing markets in the region to derive higher growth. The company had earlier executed multiple orders from government agencies in Asian countries like India and Hong Kong. It also supplied steel structures and telecom towers to neighboring countries such as Jordan. GCC would continue to be the company’s key focus area. However, Al-Babtain would also continue to bid for projects in the MENASEA region to derive higher growth, given its reputation and project execution expertise.

6

Volatile input prices root cause of erratic margins �

Al-Babtain enters fresh raw material supply contracts at the time of securing new project orders. The inherent volatility in key input materials such as steel is the root cause of Al-Babtain’s erratic margins. Steel prices zoomed to an average of USD642/MT in 2008 from USD550/MT in 2007 before correcting to USD481/MT in 9MFY09. Aluminum prices, on the other hand, ranged from USD1592-2663 per MT. As a result, Al-Babtain’s gross margins have been erratic, ranging from 22.9% in FY07 to 24.7% in FY08 (it was an impressive 26.7% in FY04). With costs of sales accounting for over three-fourth of sales, raw material prices are a key determinant of Al-Babtain’s profitability. High inventory level and the fact that Al-Babtain procured most input materials at high prices negatively impacted the company’s margins. Gross margins thus contracted significantly to 20.5% in 9MFY09. However, following the correction in commodity prices, we expect Al-Babtain to post a gradual recovery in margins going forward as it enters into fresh raw material supply contracts for projects bagged recently.

Sensitivity to Margins �

During our forecast period, we have assumed gross margins to gradually improve and average 21.6% during FY10-14E. However, this is likely to be below the company’s 23.6% average for the last four years. We have also checked how sensitive our fair price is to changes in gross margins. All else equal, a 1% change in gross margins over the forecasted period impacts our DCF-based target price by SAR5.5 per share.

Earnings to improve steadily over forecast horizon �

In line with the views discussed above, despite recording a revenue growth of 19.5% YoY in 9MFY09, Al-Babtain’s operating profit grew just 6.6% YoY. However, during the period, the company made a conscious effort to reduce its high inventory level, bringing it down from SAR683.9bn in FY08 to SAR416.2bn in 9MFY09. This helped Al-Babtain to post positive operating cash flows of SAR382bn in 9MFY09. We expect revenues to grow at an average annual rate of 12.2% during FY09-14E. This will be majorly driven by the Design, Supply & Installation segment. With a gradual expansion in margins, we expect operating income to increase at an average rate of 13.8% during FY09-14E. Supplemented by declining interest expenses, we expect the net income to reach SAR259.0mn in FY14E from SAR131.0mn in FY08.

6

7

Volatility in the steel prices �

With cost of inputs, especially steel, fluctuating continuously, any sharp increase in steel prices could significantly impact Al-Babtain’s margins. We have been conservative in our forecasts for average realized gross margins. However, a sharp increase in steel prices over the forecasted period could negatively impact Al-Babtain’s margins and (consequently) its valuations.

High competition �

The tower and pole manufacturing, lighting, masts and luminaries industry is highly competitive. Several local, regional and international players are active in these segments. Companies generally bundle these offerings with other products and services in order to bag additional projects. New entrants and additional products and services launched by existing players could intensify competition in the industry, exerting pressure on margins. However, Al-Babtain is a leading company in Saudi Arabia, and enjoys an edge over its peers due to its fully integrated portfolio of bundled products and service offerings.

Correction in oil prices �

KSA’s economy relies heavily on oil. Consequently, any decline in oil prices due to the prevailing economic slowdown could dent the government’s coffers and affect business activities and sentiment in the Kingdom. Lower oil prices could also affect infrastructure spending in the Kingdom and lead to project delays and cancellations. Such a scenario would negatively impact our valuations.

Investment Risks

7

8

We initiate our coverage on Al-Babtain with a fair value estimate of SAR52.4. This implies an upside potential of 49.4% from the current price level. Our fair value estimate is derived from a weighted average of Discounted Cash Flow (DCF) and peer comparison-based methods. We have assigned 60% weightage to DCF and 40% to the comparables-based method.

Our DCF model generated an enterprise value of SAR2.5bn. This implies an equity value of SAR2.2bn (SAR53.5 per share) after adjusting for net debt, long-term investments and minority interests. The DCF-generated fair value is based on a five-year explicit forecast period (FY09-14E) and a terminal value. The terminal value assumes an average growth rate of 2.5%.

Valuation Summary

Table 2: DCF Valuation, Key Financial Metrics

All figures in SAR Mn, unless specified

2008 2009E 2010E 2011E 2012E 2013E 2014E

Revenues 1,013 1,173 1,435 1,650 1,810 1,943 2,083 EBITDA 210 199 252 292 322 347 373

Margins (%) 20.7% 17.0% 17.6% 17.7% 17.8% 17.8% 17.9%EBIT 178 164 211 246 272 292 313

Margins (%) 17.6% 14.0% 14.7% 14.9% 15.0% 15.0% 15.0%Net income 131 119 165 194 217 237 259

Margins (%) 12.9% 10.1% 11.5% 11.8% 12.0% 12.2% 12.4%Cash from operations (86) 332 117 168 218 261 286 Total assets 1,416 1,220 1,335 1,465 1,557 1,591 1,676 Shareholders equity 498 567 662 767 874 979 1,081 Total liabilities & equity 1,416 1,220 1,335 1,465 1,557 1,591 1,676 Free Cash Flow Analysis (FCF) NOPLAT 171 158 203 237 262 281 302 Depreciation and amortization 32 35 41 46 51 55 60 Less: Change in working capital 276 (156) 121 112 94 80 86 Less: Capex 74 31 27 33 34 37 42 FCF (147) 318 96 138 184 219 234

FCF consideration 25% 100% 100% 100% 100% 100%Discount factor 1.00 0.90 0.82 0.74 0.67 0.60

PV of FCF 79 87 113 136 146 142

Sum of PV of FCF 703 Terminal value 2,993 PV of Terminal value 1,810 Enterprise value 2,513 Add: Net debt & others (346)Total equity value 2,167 Shares 40.5 Fair Value (SAR Per share) 53.5 Terminal Growth rate 2.5%WACC (%) 10.5%

Source : Company Data, AlJazira Capital

DCF Valuation

9

Core Assumptions:

Financial Estimates �

Revenues � :

Revenues are expected to increase 15.8% YoY in FY09E. Thereafter, it is forecast to grow at an annual average growth rate of 12.2% over the period FY09-14E.

Margins: �

In line with significant contraction witnessed in 9MFY09, we expect Al-Babtain’s gross margins to average 20.6% in FY09E (it was 24.7% in FY08). However, we expect gross margins to improve to an average of 21.6% during FY10-14E as the reduction in input prices and better cost management makes a favorable impact. However, gross margins will remain below the last four years’ average of 23.6%.

Weighted Average Cost of Capital (WACC) �

A WACC of 10.5% is based on the following assumptions:

Cost of Equity of 11.8% assumes a risk-free rate of 3.4% (equivalent to the 10- �year US treasury yield of 3.4% at present), risk premium of 6.7%, a beta of 0.96, and country risk premium of 2.0%.

Cost of Debt: We arrived at the cost of debt by considering the interest rate on �both short-term and long-term borrowings. We arrived at post tax cost of debt of 5.2%.

Terminal Value �

Represents the present value of perpetuity free cash flows, growing at a conservative perpetual growth rate of 2.5%.

As cost of capital and terminal growth rate assumptions form a core part of our DCF based fair value, we have also performed a sensitivity analysis. The table below highlights the sensitivity of Al-Babtain’s fair value estimate to changes in perpetual growth and cost of capital.

Sensitivity Analysis

Table 3: Sensitivity Analysis

Term

ina

l g

row

th r

ate Cost of Capital

9.5% 10.0% 10.5% 11.0% 11.5%

3.5% 72.17 65.81 60.35 55.62 51.49

3.0% 67.07 61.51 56.70 52.48 48.77

2.5% 62.70 57.79 53.50 49.71 46.34

2.0% 58.91 54.53 50.67 47.24 44.18

1.5% 55.59 51.65 48.16 45.03 42.22Source: AlJazira Capital

10

تدفق الديونالنفدي -

حتمل القضية

تدفق الديونالنفدي -

أساس القضية

خفض الهوامشب ١٫٠٪

زيادة الهوامشب ١٫٠٪

خفض استخدامالطاقةب ٥٫٠٪

زيادة استعمالالطاقةب ٥٫٠٪

زيادة املعدلاملرجح لتكلفة

رأس املال ب ٠٫٥٪

خفض في املعدلاملرجح لتكلفة

رأس املال ب ٠٫٥٪

تدفق الديونالنقدي

قضية الثور

SA

R

3.31

2.51 53.5

65.59

2.51

5.71

4.87

5.2

42.47

DCF Bear case

DCF Base Case

WACC inrease by 0.5%

Margins decrease

by 1%

Capacity Utilization decrease

by 5%

Capacity Utilization increase

by 5%

Margins inrease by

1%

WACC decrease by 0.5%

DCF Bull case

We have further tested our core fundamental assumptions under two possible scenarios: Bull Case and Bear Case. These scenarios illustrate how sensitive our DCF-based fair value is to changes in key input variables. We chose capacity utilization, gross margins and WACC as three important variables.

Bull Case: �

In the Bull Case scenario, we have assumed:Capacity utilization to increase 5% across business segments; �Gross margins to increase 1%; and �WACC to decrease 0.5%. �

This generated a fair value of SAR66.6, representing an upside of 89.7% to the current market price.

Bear Case: �In this scenario, we have assumed: �Capacity utilization to decrease 5% across segments; �Gross margins to decrease 1%; and �WACC to increase by 0.5%. �

This generated a fair value of SAR42.5, representing an upside of 21.0% to the current market value.

Valuation under Different Scenarios

Table 4: Scenario Analysis

Source: AlJazira Capital

11

We have also used comparative valuation based on P/E and EV/EBITDA metrics to value Al-Babtain relative to its peers in the region. Because of its varied product portfolio and services, nature of operations and level of business maturities, Al-Babtain has no direct peers. However, there are a few privately-held companies or subsidiaries that compete with Al-Babtain in some or all lines of businesses. We, therefore, chose peers geared to the infrastructure, telecom and power sectors with prime business focus in the GCC region.

EV/EBITDAP/ECompany

2010 E2009 ECurrent2010 E2009 ECurrent6.0x5.0x3.8x14.8x12.5x9.8xEmcor Group Inc6.0x 6.1x 9.4x 6.6x 7.3x 19.3x Mohammad Al-Mojil Group5.4x 5.9x 8.1x 6.9x 7.3x 10.3x Galfar Engineering & Construction3.0x 3.0x 3.5x 4.1x 4.0x 3.9x Arabtec Holding PJSC3.5x 3.7x 3.2x 7.5x 6.5x 3.6x Nass Corporation4.1x 5.7x 11.6x 10.4x 11.4x 10.7x Alarko Holding6.5x 6.7x 6.8x 11.4x 10.4x 9.7x Ameren Corporation

4.9x 5.2x 6.6x 8.8x 8.5x 9.6x Peer Average6.5x 6.7x 11.6x 14.8x 12.5x 19.3x Max3.0x 3.0x 3.2x 4.1x 4.0x 3.6x Min

6.8x8.6x9.4x8.6x12.0x12.4xAl-Babtain Power & TelecomSource: Reuters, AlJazira Capital

Al-Babtain’s current TTM P/E and EV/EBITDA multiples stand at 12.4x and 9.4x, respectively. Both multiple are at the lower end of the historical range of 13.2x-22.7x and 10.6x-18.0x, respectively, for the last eight quarters. We believe most excesses related to the substantial compression in margins have already been factored in, and margins are likely to improve from here on as the reduction in key input prices, higher utilization, and cost-rationalization along with the anticipated surge in business volumes yield positive results. Margins and (consequently) multiples are expected to expand going forward.

Based on P/E metrics, we derived a fair value of SAR 50.3 per share, while EV/EBITDA metrics yielded a fair value estimate of SAR 51.5 per share.

Comparative Valuation

Table 5: Comparative Valuation: P/E and EV/EBITDA

12

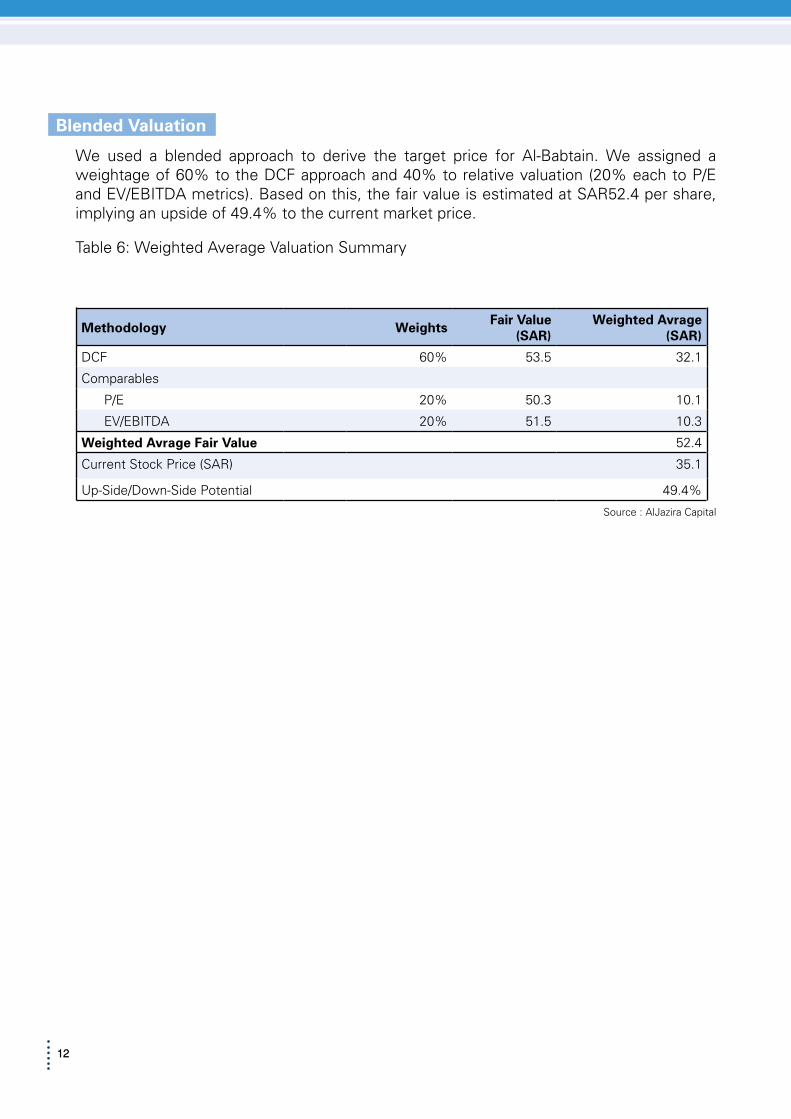

We used a blended approach to derive the target price for Al-Babtain. We assigned a weightage of 60% to the DCF approach and 40% to relative valuation (20% each to P/E and EV/EBITDA metrics). Based on this, the fair value is estimated at SAR52.4 per share, implying an upside of 49.4% to the current market price.

Table 6: Weighted Average Valuation Summary

Weighted Avrage (SAR)

Fair Value (SAR) Weights Methodology

32.153.560% DCF

Comparables

10.150.320%P/E

10.351.520%EV/EBITDA

52.4Weighted Avrage Fair Value

35.1Current Stock Price (SAR)

49.4%Up-Side/Down-Side Potential

Source : AlJazira Capital

Blended Valuation

13

Growth across all segments

With its strong product portfolio of telecom towers, monopoles, power transmission and distribution poles, lighting poles, high mast and luminaires, Al-Babtain is favorably geared to high growth sectors such as infrastructure, power and telecom. The company also offers testing stations and galvanizing services that supplement its principal products. This coupled with Al-Babtain’s technical expertise and ability to execute large projects enable the company to bag new orders in regional as well as international markets. Consequently, Al-Babtain posted impressive growth across business segments. The company’s revenues increased at a CAGR of 16.8% during FY04-08. Most of this growth was propelled by the design, supply and installation segment, which expanded at a CAGR of 56.3% during the same period. The segment benefited from the surge in volume of design, installation and maintenance services as telecom companies expand operations in the GCC region. Revenues from the poles and light segment grew at a CAGR of 9.3% over FY04-08, benefiting from a surge in project orders due to rising investment for the development of infrastructure and transportation networks in the country. Revenues from Al-Babtain’s tower and steel structure business increased at a CAGR of 11.2% during FY04-08. This can be ascribed primarily to high demand for telecommunication and power transmission and distribution towers. Government initiatives to liberalize the telecom sector and the region’s strong base of young people, coupled with rising spending power, led to fast paced growth of the GCC telecom sector. Further, with high population growth resulting in per capita energy consumption being among the highest in the world, GCC governments initiated various measures to improve the power infrastructure. These factors, in turn, ensured high demand for Al-Babtain’s products and services.

However, the robust revenue growth witnessed during FY04-08 failed to reflect in the bottom-line mainly due to the significant rise in cost of key input materials such as steel and aluminum. With costs of sales accounting for over three-fourth of sales, raw material prices are a key determinant of Al-Babtain’s profitability. Consequently, the company’s net margins contracted from 15.9% in FY04 to 12.9% in FY08. Normalized earnings increased at a CAGR of 11% during FY04-08.

Source : Company Documents

1. Diversified product portfolio

Graph 1: Al-Babtain: Revenue and Profitability (FY04-08)

-300

0

300

600

900

1,200

2004 2005 2006 2007 2008

-7%

0%

7%

14%

21%

28%

Revenues Net profit Net profit margin (RHS)

14

GCC focus a key positive for long-term growth

Al-Babtain primarily operates in the GCC region—Saudi Arabia accounts for 78% of its revenues from the region. We expect the company’s focus on KSA to translate into significant gains, given the massive scale of investments committed in the infrastructure, power generation and telecom sectors in the Kingdom. As of June 2009, there are 234 ongoing power projects in the GCC region valued at a collective USD162bn. These projects are expected to add 24,734 MW, besides facilitating the setting-up of related transmission and distribution network by 2014. In addition, network upgrades and government spending on expanding transmission and distribution lines are expected to create long-term demand for Al-Babtain’s power transmission towers and testing stations. Economic growth drove regional telecom companies to expand operations and increase spending to increase network coverage in these countries. These efforts are expected to ensure sustained demand for Al-Babtain’s telecom towers.

…Complemented by projects across the globe

Along with GCC, the company also targets other international markets. Al-Babtain’s pole and lighting division has executed various orders from municipalities and road and port authorities in Asia, specifically in India, Hong Kong and Sri Lanka. Al-Babtain Egypt has been supplying towers and poles to African countries since its inception in 1999. The Company has also supplied steel structures and telecom towers for various projects in neighboring Jordan and Iraq, besides undertaking projects involving testing stations for transmission and distribution in India and Iran. Thus, despite its GCC focus, we are encouraged by Al-Babtain continuing to bid for international projects in the MENASA region.

Strategic subsidiaries and JVs helped tap growing demand

Al-Babtain entered into a strategic JV with LeBlanc in 1994, forming Al-Babtain LeBlanc Telecommunications Co. to tap the surge in demand for supply, installation and maintenance of telecom towers in the GCC region. Al-Babtain holds 51% stake in the JV. The strategy proved a success as the JV completed a number of supply orders in the KSA and the maintenance division grew exponentially, driven by the telecom boom in the region. Additionally, with these revenues being recurring in nature, Al-Babtain is expected to experience sustained top line growth. Identifying high growth potential in the African power sector as early as 1999, Al-Babtain formed its subsidiary Al-Babtain Egypt with a fully operational plant producing poles to power transmission towers. Additionally, both the JV and the subsidiary have been enjoying healthy margins by leveraging on economies of scale through bulk steel orders to reduce cost. Furthermore, Al-Babtain, through its subsidiary Al-Babtain LeBlanc Co., is actively scouting for strategic partnerships to boost services earnings. In line with this strategy, on November 18, 2009, Al-Babtain LeBlanc Co. entered into an exclusive agreement with Eveready (South Africa) for alternative energy products. Under the agreement, Eveready will supply wind power generation equipment, Kestrel, in the Middle East and North Africa region exclusively through Al-Babtain. The subsidiary also signed a 50:50 JV agreement with CME of Portugal on December 13, 2009, which includes design and installation of wired networks and information systems. According to Zawya, the SAR2mn venture is likely to add sales of SAR19.8mn and profits of SAR1.6mn in 2010.

…And unused capacity to serve built-up demand

The Company was operating at 80% of installed capacity for both its poles and lighting division in 2008. As the market improves, 2010 onwards, we expect demand to increase and the company to record improvement in its capacity utilization. The strengthening of the transport network and planned economic cities in the KSA are also expected to boost demand in the poles and lighting segment. The Towers division has been historically operating at over 90% installed capacity. The current unutilized capacity of 10% will enable the company to accommodate more orders, given the large number of planned infrastructure projects in the region. However, maximum improvement in utilization rates is expected in the steel structures division, which was operating at just 70% of its total installed capacity in 2008.

15

Has provided growth impetus so far

Liberalization of the telecom sector in the GCC enabled the government to issue licenses to new players. Investments by these new players to establish their infrastructure network is increasing demand for design, supply and maintenance of telecommunication systems. To tap this attractive opportunity, Al-Babtain formed a JV with LeBLANC Telecommunications, Canada. The company enjoys a strong relationship with contractors serving STC and Etihad Etisalat in Saudi Arabia, and has actively expanded into the larger and lucrative MENA market. Consequently, due to the growing demand and expanded services offering, the company’s design, supply and installation segment revenues grew at a CAGR of 56.3% during FY04-08; the segment’s revenue contribution increased from 9% in FY04 to 30% by FY08. We believe this segment will continue to provide growth impetus to Al-Babtain’s top line even as telecom operators in the region continue investing aggressively to expand their infrastructure network.

Source : Company Documents

Recurring revenue stream to ensure steady cash flows

While new licenses and expansion of operations by incumbent operators to increase network coverage provided higher supply and installation revenues, servicing of existing telecom operations in the region, along with catering to earlier installed equipment, provided a recurring stream of maintenance income for Al-Babtain. In the long term, we expect Al-Babtain to benefit from its strong presence in this segment through its strategic JV with LeBlanc. Many operators fall back on continual maintenance contracts with their equipment suppliers—Al-Babtain in this case.

…growth to be backed by greater focus on attractive markets

Al-Babtain has been servicing key geographical areas like UAE and Qatar. The company is expected to benefit from the expansion plans of existing networks by incumbent operators such as Zain, Mobily and Etisalat. In particular, Zain KSA that launched its operations last year is expected to incur capital expenditure of SAR1.5-2bn each year until 2011 to expand its network coverage and provide the latest technology. Mobily also is expected to invest SAR2-3bn each year on infrastructure during the same period. These investments are likely to translate into higher revenues for Al-Babtain.

2. Design, Supply and Installation Segment to continue pulling its weight

Graph 2: Design, supply & installation segment growth: FY04-08

0

50

100

150

200

250

300

350

2004 2005 2006 2007 2008

Revenues (SAR mn)

16

Expanding power generation capacity

KSA and Kuwait are the largest consumers of electricity in GCC, with KSA alone accounting for 56% of the total consumption in the region. To meet the surging demand for power in the wake of buoyant economic activity and surging industrial expansion, GCC governments invested heavily to increase total power generation capacity from 46,579 MW in 2002 to 73,339 MW in 2007, registering a CAGR of 10%.

Large investments to keep momentum going

There are nearly 234 projects (worth USD162bn) underway in the power sector, which is likely to provide substantial boost to the region’s total power generation capacity. Saudi Electricity Company (SEC), a primary electricity supplier in Saudi Arabia, plans to independently spend nearly USD 80 bn to expand its generation capacity by 20,000 MW by 2018. It intends to spend an additional USD 20 bn on independent power producer projects in KSA. The independent power producer projects are likely to add 10,000 MW of capacity in the country. These projects will also require substantial investments for the establishment and upgradation of the transmission and distribution network. This is likely to offer significant business opportunities to companies active in transmission and distribution networks. (For the list of ongoing power and transmission projects in KSA, please refer appendices). The expected commissioning of the GCC-wide power grid project by 2010 is also likely to further drive up demand for transmission/distribution towers and testing stations.

T&D lines to supplement growth

The total distribution network in the Kingdom grew from 226,664 CKM in 2000 to 345,420 CKM in 2008 to support the increase in power generation capacity and network expansion. The T&D network is expected to grow further considering the capacity expansion projects lined up in the region. Electrification of all regions of the Kingdom is also expected to result in the launch of several new transmission and distribution projects in Saudi Arabia. Of the total investment commitment of USD 100 bn, discussed above, SEC plans to spend around USD30bn on transmission and USD 20 bn on distribution by 2018. Al-Babtain, with its comprehensive product offerings ranging from transmission towers, monopoles and distribution poles, and testing stations capabilities, is favorably geared to this segment. The setting up of the transmission and distribution network will boost demand for towers, both transmission and distribution, and testing stations.

…Sustained demand for telecom towers

The GCC telecom sector has witnessed high growth historically, supplemented by growing population (CAGR of 2% during 2003-2008) and expanding GDP per capita. The region’s GDP per capita grew at a CAGR of 19% to USD 22800 during 2003-2008. Young demographic profile also contributes to the sector’s growth prospects. Despite penetration rates reaching near saturation levels in most GCC countries, we believe recent government efforts towards liberalizing the sector and initiatives by incumbent players to increase network coverage and expand to neighboring regions will likely result in massive capital investments in the sector. With oil trading in the range of USD 65-75 for most part of 2009, and expectations of the region returning to economic growth soon, we believe regional telecom companies would increase spending on infrastructure. Zain KSA and incumbent Mobily, which entered the domestic market recently, are expected to spend SAR 3-4 bn annually over the next three years. This would propel demand. These factors could boost Al-Babtain’s order book for telecommunication towers and galvanizing services.

3. Power and Telecom to follow suit

17

We expect infrastructure development, especially related to transport infrastructure (roads, highways, ports), to continue to drive demand for poles and luminaries in the region. Infrastructure has historically been the largest revenue contributor for Al-Babtain.

Investments to continue…

Poles and luminaries segment has been witnessing strong demand in the GCC region in line with substantial capital investment on infrastructure development. In KSA’s 2009 budget, the infrastructure segment received an allocation of SAR7.8bn (USD2bn). The total pre-planned investments in infrastructure to be implemented under public-private partnerships are expected to be in excess of SAR1,100bn (USD300bn) during 2007-2012. With government’s aggressive investments in new projects in oil & gas, construction, real estate and infrastructure, demand for steel and poles and luminaries is likely to record robust growth.

Growing transportation network to augment growth

The construction of a robust transportation network has emerged as a major target for KSA authorities. Multiple ongoing projects across transportation modes with a total investment of USD100bn are expected to be completed over the next 10 years. The government has planned projects to develop ports, airports, railroads, roads and logistics centers. The KSA government has also allocated SAR16.5bn (USD4.4bn) in its 2009 budget to develop municipality services, including intercity roads, bridges and road lights in the new cities being developed. These investments aimed at transforming KSA into a global transport and logistics hub are, in turn, expected to boost demand for installation of luminaires and lighting poles.

Mega economic cities

The KSA government plans to develop several mega economic cities as part of its diversification goals. These new economic cities would also create substantial demand for outdoor lightings such as street lightings, area masts, flood lights in various dimensions and models.

Economic City Area (mn sq.mt)

Investment (USDbn)

Expected year of completion

Knowledge Economic City (Madina) 4.8 7 2014

Prince Abdul Aziz bin Mousaed Economic City (Hail) 156 8 2018

Jazan Economic City (Jazan province) 100 27 2011

King Abdullah Economic City (Makkah province) 168 27 2016Source : SAGIA, MEED

4. Poles and Lighting to get infrastructure boost

Table 7: Key Information – Economic Cities in KSA

18

Higher number of international orders

Al-Babtain, ranked amongst the top 100 companies in the GCC, has executed projects in 33 countries and this experience has helped its bag more number of international orders over the last two years. The company has exported products to Jordan in the GCC region, India and Hong Kong in Asia, and Russia, Cyprus and France in Europe. We believe Al-Babtain’s production capabilities, ranging from the concept stage to designing, delivery, installation and maintenance, have enabled it to strengthen its relationship with contracting companies in the region. It is also one of the key factors helping the company to win additional projects in regional and international markets. In line with this trend, non-KSA revenue contribution increased from 14% in FY07 to 22% in FY08.

In order to expand its presence in domestic and international markets, Al-Babtain contends with a number of local, regional and international players. In the GCC region, it faces competition from Saudi Lighting Co., Zamil Steel, Arabian Pipes Co., Saudi Steel Pipes Co. Ltd. In the international market, Al-Babtain competes against Larsen & Toubro, Shreider and Philips among many others. Companies generally bundle their offerings with other products and services in order to bag additional projects. However, because of its varied product portfolio and services, nature of operations and level of business maturities, Al-Babtain enjoys an edge over its peers. In Saudi Arabia, for instance, Al-Babtain is a leading company and enjoys a competitive advantage over its peers due to its fully integrated portfolio of bundled products and service offerings, reputation and project execution expertise.

Going forward, we believe Al-Babtain would continue to bid for projects across MENA and South East Asia to increase its share of international revenues and boost top-line growth.

Source : Bloomberg

22%

78%

5. Substantial Experience in Project Execution

Graph 4: Countries where Al-Babtain has executed projects

Graph 3: Geographical distribution of revenues

Source : Company Documents

19

Economic slowdown casts shadow over profitability

Al-Babtain’s revenues grew at a slower pace (19.5% YoY to SAR 865.1mn in 9MFY09 after recording a CAGR of 23.1% during FY05-08). This can be ascribed to the slowdown in expansion activities by telecom companies and project delays in the power and infrastructure sector due to economic slowdown. However, due to the high inventory level and the fact that Al-Babtain procured most input material at high prices, cost of goods sold outpaced revenue growth. Consequently, Al-Babtain’s gross margin contracted 232 bps to 20.5%, while its operating profit grew just 6.6% YoY in 9MFY09. The company’s woes were aggravated by higher interest expenses coupled with decline in other income, including revenues from repairs and maintenance services and rent revenue. Consequently, the bottom-line plunged 16.8% YoY to SAR 84.1mn in spite of the 19.5% YoY growth in revenues. Net profit margin contracted 423 bps to 9.7% in 9MFY09.

Improving working capital position

Despite procuring raw materials at the time of signing contracts, Al-Babtain experienced a huge pile up of inventories worth SAR 690.7mn by Q3FY08. This can be attributed to contract delays due to economic slowdown in the region. Inventory days rose to a five-year high from 248 in FY07 to 328 in FY08. Cash cycle surged from 301 days to 391 days during the same period due to the increase in inventory and receivables outstanding, which was marginally offset by higher payables outstanding. This increased the company’s working capital requirement by SAR 276.5mn, leading to a negative cash flow of SAR 86.1mn from operating activities in FY08. However, the management has strived to bring down inventory levels in order to reduce working capital requirements. As a result, inventories have reduced to SAR 416mn, equivalent to 166 days in 9MFY09.

Debt-equity ratio eases

Al-Babtain’s gross debt outstanding rose significantly from SAR 424.9mn in FY07 to SAR 697.0mn in FY08. During the same period, net debt grew from SAR 404.6mn to SAR 628.7mn. However, short-term loans constitute a major chunk of outstanding debt (92.1% in FY08) which, we believe, the company took to fund its working capital requirements. Consequently, Al-Babtain’s debt-equity ratio rose from 1.0x in FY07 to 1.4x in FY08. Since then, the company’s total debt outstanding has declined to SAR 332.9mn (net debt: SAR 291.9mn), while its debt-equity ratio eased to 0.60x at the end of 9MFY09 benefiting from the improving working capital position. With interest coverage of 4.6x in 9MFY09, we believe the company is in a comfortable position to regularly repay its outstanding debt.

6. 9MFY09 Financial Performance

20

All figures in SAR Mn, unless specified 9MFY08 9MFY09 YOY Change

Gross Revenues 724.3 865.1 19.5%Poles & light segment 339.2 307.2 -9.4%

Towers & steel structure 175.5 282.7 61.1%

Design, supply & installation 209.5 275.2 31.4%

Cost of Revenues (559.3) (688.1) 23.0%

Gross Profit 165.0 177.0 7.3%

Selling, General & Administrative expenses (53.0) (57.6) 8.7%

Operating Income 112.0 119.5 6.6%Interest Expense (20.7) (26.0) 25.7%

Income from associates - -

Other income, net 25.2 11.2 -55.5%

Profit before zakat, tax, minority int. 116.5 104.7 -10.2%Zakat/Tax provision (2.4) (1.9) -19.0%

Profit before minority interest 114.2 102.8 -10.0%Minority Interest (13.1) (18.6) 42.3%

Net profit after Zakat/Tax 101.1 84.1 -16.8%Earnings per share (SAR) 2.5 2.1

Source : Company Documents

Financial Ratios 9MFY08 9MFY09Profitability Ratios (%)

Gross Profit Margin 22.8 20.5

Operating Margin 15.5 13.8

Net Profit Margin 14.0 9.7

Return on Average Assets 11.7 8.8

Return on Average Equity 30.2 21.2

Liquidity Ratios (x)

Current Ratio 1.3 1.8

Quick Ratio 0.4 0.9

Turnover Ratios (Days)

Inventory 338 166

Receivables Outstanding 92 96

Payables Outstanding 27 24

Operating Cycle 430 262

Cash Cycle 403 237

Capital Structure

Debt/Equity (%) 1.3 0.6

Interest coverage (x) 5.4 4.6Source : Company Documents, AlJazira Capital

Table 8: Income Statement: 9MFY09

Table 9: Financial Ratios: 9MFY09

21

Al-Babtain Power & Telecommunications is a KSA-based company operating in the engineering and manufacturing sector across multiple business segments, including power transmission and distribution, telecom towers, lighting poles, structural steel and galvanizing services. Established in 1955, the company has implemented projects in around 30 countries and has offices/agents in 10 countries. KSA accounts for around 78% of its revenues.

Source : Company Documents

Growth Strategy

The company’s growth strategy entails catering to the increasing demand for telecom and power transmission and distribution towers, outdoor lighting and structural sectors in GCC and international markets. In order to tap increasing project orders in the buzzing telecom sector, Al-Babtain entered into a joint venture with LeBLANC Telecommunications, Canada, to form Al-Babtain LeBLANC Telecommunication Systems Ltd. (ABL) in 1993. This JV provided a solid platform for the company to offer engineering, manufacturing and installation of communication towers (Fixed Line, GSM, Microwave, Roof Top Structures, Antenna Mounts etc.) in KSA, neighboring countries in the of Arab world and countries in North Africa.

To expand its footprint in the African continent, Al-Babtain formed a wholly owned subsidiary (Al- Babtain) Egypt in 1999. The subsidiary became fully operational in 2000 and currently provides power & telecommunication products to the whole of Africa.

7. Company Overview

Graph 5: Al-Babtain Operations

Al-Babtain Power & Telecommunication

InfrastructurePower SectorTelecom Sector

Tower Manufacturer Towers T&D Lighting Poles

Installation & Maintenance

Testing Stations Steel Structure

22

Al-Babtain offers a wide range of products and services across three core sectors – power, telecom and infrastructure. It also offers services such as testing stations and galvanizing to supplement its principal product offerings.

Business Segments Product OfferingsTransmission and Distribution Designing & manufacturing of Transmission Towers, Monopoles, Distribution Poles

Outdoor Lighting Poles, High Mast, Luminaires

Testing Station Testing of overhead transmission structures

Telecommunication Towers & Monopoles

Steel Structures Engineering & manufacturing applications

Galvanizing Services Steel galvanizing services across industriesSource : Company Documents

Outdoor Lighting – Poles, High Mast, Luminaires

Al-Babtain provides a wide range of outdoor lighting products – Poles, High Mast and Luminaires. The company has executed projects and installed lighting poles in the Middle East region and in many other countries such as India, Sri Lanka, Hong Kong, Russia, France, and Ireland. Al-Babtain has a 123,000 square meter manufacturing facility to design and cast outdoor lighting poles with a capacity to produce 120,000 poles per annum. Al-Babtain’s current manufacturing facility has a galvanizing capacity of 100,000 tons per year.

Transmission & Distribution

Al-Babtain provides a range of transmission and distribution products, including transmission towers, transmission monopoles and distribution poles. Al-Babtain has the capacity to manufacture transmission towers up to 500KV and above, transmission monopoles up to 230KV and distribution poles up to 33KV. In tonnage, the company has a capacity to manufacture 60,000 tons per annum and galvanize 80,000 tons per annum.

Testing Stations

Al-Babtain has constructed a facility to test the overhead transmission structures in line with international standards. Al-Babtain Testing Station has a capacity to test towers up to 500KV (Double Circuit) and 800KV (Single Circuit) and monopoles up to 230KV (Double Circuit).

Telecommunications Towers and Monopoles

Al-Babtain operates in the telecom industry through its telecom subsidiary, Al-Babtain LeBLANC Telecommunications System Ltd. (ABL). The company’s manufacturing facility has an annual licensed capacity of 30,000 tons and annual production capacity of 25,000 tons.

Steel Structures

The company provides steel structures to the oil & gas, cement, and industrial segments. The company has a manufacturing facility spread over 37,000 sq. mts with the capacity to manufacture 15,000 tons per annum.

Graph 6: Products and Services Portfolio

Product Offerings

23

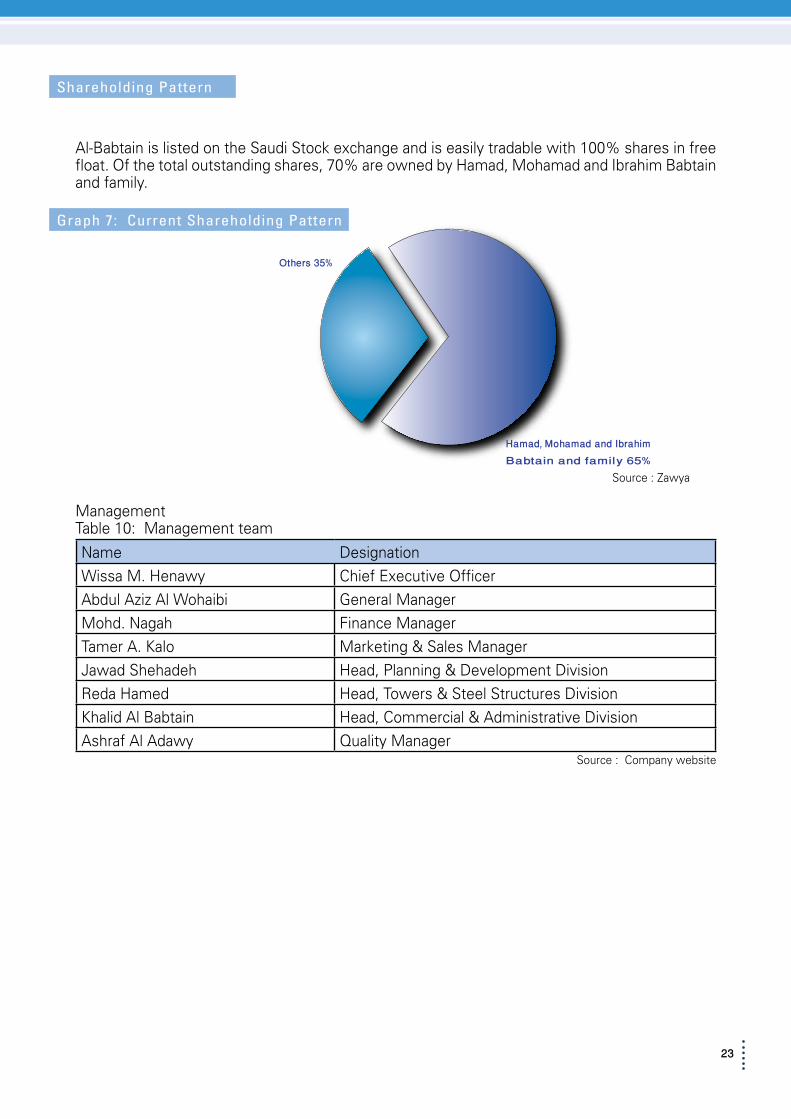

Al-Babtain is listed on the Saudi Stock exchange and is easily tradable with 100% shares in free float. Of the total outstanding shares, 70% are owned by Hamad, Mohamad and Ibrahim Babtain and family.

Source : Zawya

ManagementTable 10: Management team

Name Designation

Wissa M. Henawy Chief Executive Officer

Abdul Aziz Al Wohaibi General Manager

Mohd. Nagah Finance Manager

Tamer A. Kalo Marketing & Sales Manager

Jawad Shehadeh Head, Planning & Development Division

Reda Hamed Head, Towers & Steel Structures Division

Khalid Al Babtain Head, Commercial & Administrative Division

Ashraf Al Adawy Quality ManagerSource : Company website

Shareholding Pattern

Graph 7: Current Shareholding Pattern

Hamad, Mohamad and IbrahimBabtain and family 65%

Others 35%

24

Income StatementRevenues – We expect Al-Babtain’s revenues to reach SAR2.1bn by FY14E, registering a CAGR of 12.2% (FY09E-14E), with significant contribution from the design, supply and installation segment. We expect revenues from this segment to record 17.8% CAGR during FY09E-14E. Hence, the segment’s contribution to total revenues is expected to increase from 30% in FY08 to 43% in FY14E. We also expect the other segments (Poles & Light, Tower & Steel Structure) to contribute to growth in a sustained way. Revenues from both these segments are expected to expand at a CAGR of 8.8% during FY09E-FY14E, backed by the favorable investment climate in GCC and the company’s ability to capitalize on the increasing demand.

-

200.0

400.0

600.0

800.0

1,000.0

1,200.0

2004 2005 2006 2007 2008

Revenues (SAR mn)

Poles & light segment Towers & steel structure Design, supply & installationSource:AlJazira Capital

Costs/Margins

On the margins front, we expect operating margins to decline in FY09E due to higher input costs arising from the huge pile up of inventories procured at high prices. Beyond FY09E, we expect margins to improve steadily due to higher capacity utilization and reduced cost pressures. Operating margins are expected to reach 15.0% by FY14E, while net margins are likely to improve from 10.1% in FY09E to 12.4% by FY14E, as reduced debt levels drive down interest expenses.

Earnings per share

Due to subdued revenue growth and higher cost pressures, Al-Babtain’s EPS is expected to reduce to SAR2.9 in FY09E from SAR3.2 in FY08. However, better utilization rates and higher revenues are expected to boost EPS to SAR6.4 in FY14E.

8. Financial Forecasts: Profitability to steadily rise

Graph 8: Segmental Revenue Growth (FY09E-14)

25

All figures in SAR Mn, unless specified 2008 2009E 2010E 2011E 2012EGross Revenues 1,012.7 1,172.7 1,434.6 1,650.0 1,810.5 Cost of Revenues (762.1) (931.4) (1,129.3) (1,293.7) (1,417.4)

Gross Profit 250.6 241.3 305.3 356.3 393.1

Selling & Distribution expenses (21.9) (15.1) (17.5) (21.1) (23.2)

General & Administrative expenses (50.8) (62.3) (77.1) (89.2) (98.2)

Operating Income 177.9 164.0 210.7 245.9 271.7 Interest Expense (30.3) (31.5) (22.0) (21.1) (19.3)

Income from associates 5.5 5.9 6.2 6.5 6.8

Other income, net 1.4 8.4 8.6 8.8 9.0

Profit before zakat, tax, minority int. 154.5 146.7 203.4 240.1 268.2 Zakat/Tax provision (5.6) (5.3) (7.3) (8.6) (9.6)

Profit before minority interest 148.9 141.5 196.1 231.5 258.6 Minority Interest (17.9) (22.6) (31.4) (37.0) (41.4)

Net profit after Zakat/Tax 131.0 118.8 164.7 194.4 217.2 Earnings per share (SAR) 4.9 2.9 4.1 4.8 5.4

Normalized earnings per share (SAR) 3.2 2.9 4.1 4.8 5.4 Source : Company Data, AlJazira Capital

Balance Sheet

Capital expenditure plans - We do not expect the company to incur any substantial capital expenditure towards the fixed asset base as it is currently operating below its full rated capacity.

Debt balance

As of Q3FY09, Al-Babtain had debt outstanding of SAR333mn and a corresponding debt-equity ratio of 0.60x. We expect this ratio to improve, with minimal capex plans and healthy revenue inflows resulting in timely repayments.

Table 11: Al-Babtain Income Statement (FY08-12E)

26

All figures in SAR Mn, unless specified 2008 2009E 2010E 2011E 2012ECurrent Assets

Cash & cash equivalents 68.3 41.8 29.3 49.4 52.3

Other current assets 993.1 825.4 964.6 1,085.9 1,188.4

Total Current Assets 1,061.4 867.2 993.9 1,135.3 1,240.6 Non-current assets

Fixed Assets, net 327.4 325.6 313.6 302.7 288.9

Other non-current assets 27.6 27.3 27.2 27.2 27.2

Total non-current assets 355.0 352.9 340.8 329.9 316.1

Total Assets 1,416.4 1,220.1 1,334.6 1,465.2 1,556.7 Current Liabilities

Short-term loans 612.3 360.4 349.5 346.5 309.8

Current portion of long-term debt 29.5 11.6 9.3 18.6 9.3

Total Current Liabilities 792.4 516.1 527.9 552.1 524.0 Non-current liabilities

Long-term debt 55.2 46.6 37.2 18.6 9.3

Total non-current liabilities 55.2 46.6 37.2 18.6 9.3 Shareholder’s equity

Paid-up Capital 270.0 405.0 405.0 405.0 405.0

Legal/Statutory Reserve 45.1 57.0 73.4 92.9 114.6

Retained Earnings/ Accumulated losses 185.1 106.5 185.3 271.0 356.1

Total shareholder equity 498.5 566.7 662.0 767.2 874.0 Total liabilities, provisions & equity 1,416.4 1,220.1 1,334.6 1,465.2 1,556.7

Source : Company Data, AlJazira Capital

Cash Flow Statement

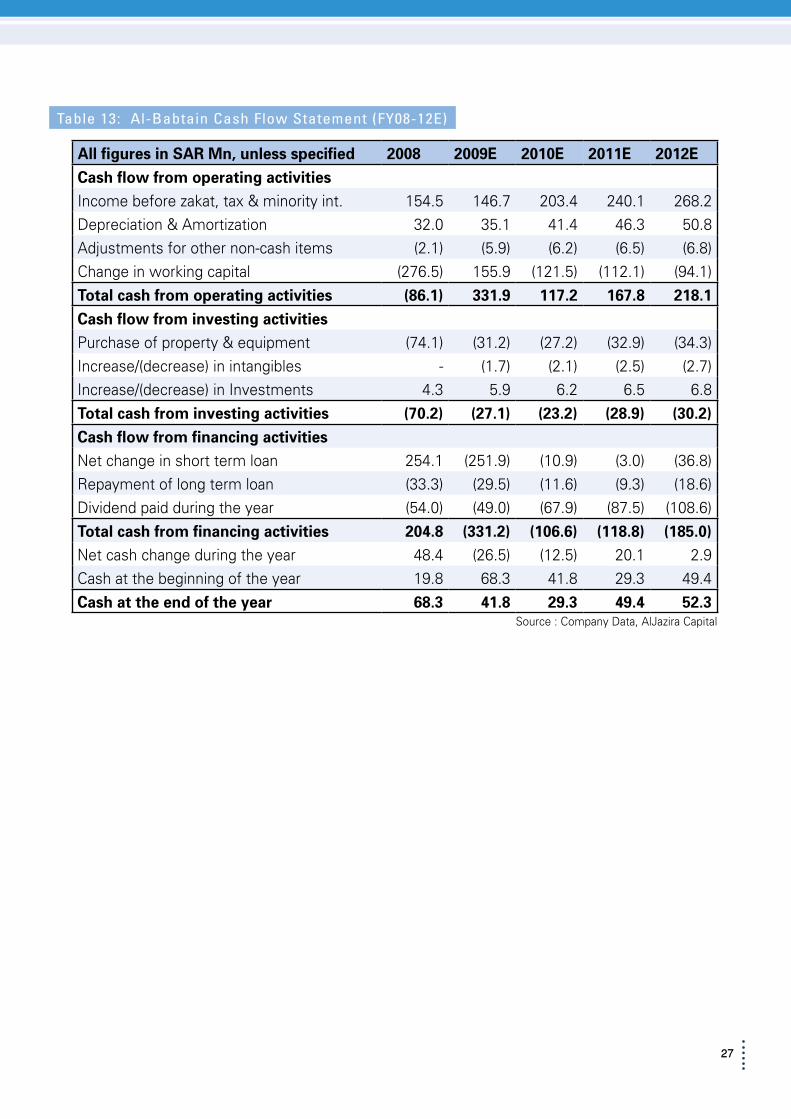

Cash flow from operations – The company’s cash from operating activities is expected to grow robustly and reach SAR218.1mn by FY12E, led by improving earnings and better working capital management backed by declining inventory levels. Al-Babtain’s current cash balance and the anticipated operational profit are expected to be sufficient for funding working capital requirements.

Cash flow from investments

We expect the minimal investments in the fixed asset base and intangible asset base.

Cash flow from financing activities

We expect the company to make regular periodic repayments of outstanding debt and maintain a dividend payout ratio of 41% during the forecast period.

Table 12: Al-Babtain Balance Sheet (FY08-12E)

27

All figures in SAR Mn, unless specified 2008 2009E 2010E 2011E 2012ECash flow from operating activitiesIncome before zakat, tax & minority int. 154.5 146.7 203.4 240.1 268.2

Depreciation & Amortization 32.0 35.1 41.4 46.3 50.8

Adjustments for other non-cash items (2.1) (5.9) (6.2) (6.5) (6.8)

Change in working capital (276.5) 155.9 (121.5) (112.1) (94.1)

Total cash from operating activities (86.1) 331.9 117.2 167.8 218.1 Cash flow from investing activitiesPurchase of property & equipment (74.1) (31.2) (27.2) (32.9) (34.3)

Increase/(decrease) in intangibles - (1.7) (2.1) (2.5) (2.7)

Increase/(decrease) in Investments 4.3 5.9 6.2 6.5 6.8

Total cash from investing activities (70.2) (27.1) (23.2) (28.9) (30.2)Cash flow from financing activitiesNet change in short term loan 254.1 (251.9) (10.9) (3.0) (36.8)

Repayment of long term loan (33.3) (29.5) (11.6) (9.3) (18.6)

Dividend paid during the year (54.0) (49.0) (67.9) (87.5) (108.6)

Total cash from financing activities 204.8 (331.2) (106.6) (118.8) (185.0)Net cash change during the year 48.4 (26.5) (12.5) 20.1 2.9

Cash at the beginning of the year 19.8 68.3 41.8 29.3 49.4

Cash at the end of the year 68.3 41.8 29.3 49.4 52.3Source : Company Data, AlJazira Capital

Table 13: Al-Babtain Cash Flow Statement (FY08-12E)

28

Project Capacity (MW) Year entering into serviceRas Al-Zor Power Plant 1,000 2012

Power Plant 11 2,000 2012

Rabigh Power Plant 1,200 2012

Qurayyah Power Plant 2,000 2014

Jubail (Marafeq) 2,600 2009

Al-Shoaiba 900 2009

Al-Shuqaiq 850 2010

Qurayyah Power Plant (Expansion) 1,255 2012

Rabigh Steam Power Plant (Expansion) 2,400 2012

Power Plant 10 (Expansion) 990 2014

Shuqaiq Power Plant 3,200 2014

Dhabaa Steam Power Plant 1,000 2014

Ras Al-Zor Power Plant 3,600 2015

South Jeddah Power Plant 3,600 2015

Al-Uqair Power Plant 3,600 2016Source: Saudi Electricity Company (SEC)

Budget Year Project Year entering into service

2009 Connecting Ha’il -Al-Jouf 380 KV 2012

2009 Connecting Al-Qassim - Madina 380 KV 2011

2010 Connecting Jizan - Najran 380 KV 2012

2010 Fifth connection line between both the Eastern and Central Regions 380 KV 2013

2011 Connecting Bisha - Wadi Aldowaser 380 KV 2014

2011 Connecting Al-Qaysumah to the 380 KV 2014

2012 Madina - Hail connection line 380 KV 2015

2012 Central - Western Regions connection line (HVDC) Stage 1 2017

2013 Boosting Connection of the Western-Southern Regions 2016

2013 Tabuk - Tabarjal connection line 380 KV 2016

2014 Connecting Amlaj - Wajh/Al-Ula 380 KV 2016

2014 Central - Western Regions connection line (HVDC) - Stage 2 2017

2015 Second connection line between both the Southern and Western Regions 2017

2015 Al-Jouf - Tabarjal connection line 380 KV 2018

2016 Boosting connection of Madina - Ha’il 2019

2017 Connecting Tabarjal - Qurayyah 380 KV 2020Source: Saudi Electricity Company (SEC)

9. Appendices

Appendix – 1 Future power generation projects coming up in KSA

Appendix – 2 Future transmission projects coming up in KSA

29

COMPANY PROFILE

AlJazira Capital, the investment arm of Bank AlJazira, is a Shariaa Compliant Saudi Closed Joint Stock company and operating under the regulatory supervision of the Capital Market Authority. AlJazira Capital is licensed to conduct securities business in all securities business as authorized by CMA, inlcuding dealing, managing, arranging, advisory, and custody. AlJazira Capital is the continuation of a long success story in the Saudi Tadawul market, having occupied the market leadership position for several years. With an objective to maintain its market leadership position, AlJazira Capital is expanding its brokerage capabilities to offer further value-added services, brokerage across MENA and International markets, as well as offering a full suite of securities business.

For further queries about our special services, contact us at the toll free number 800 116 9999.

30

Disclaimer

The information and opinions contained on this report is believed to be compiled from various reliable sources; however neither Aljazira Capital nor its mother, sister and affiliate companies can guarantee or assure the accuracy of the information provided. The purpose of this report is to offer a clear picture of the company, the sector or the national economy for our clients and the public, and not to offer recommendation to a certain stock or other Investment Assets. Based on that, we strongly advise clients to take other measurements and factors into account to make such decisions. To the maximum extent permitted by applicable law and regulation, Aljazira Capital, its mother, sister and affiliate companies shall not be liable for any loss that may arise from the use of this report or its contents. All opinions, numbers and statements on this report are subject to change without prior notice. No part of this report may be reproduced without the written permission of Aljazira Capital.

Asset Management Brokerage Corporate Finance Advising Custody

Head Office: Madinah Road, Mosadia، P.O. Box: 6277, Jeddah 21442, Saudi Arabia، Tel: 02 6692669 - Fax: 02 669 7761