agricultural products: russian embargo and import ... · food embargoes: import substitution and...

TRANSCRIPT

Agricultural Products.

Russian Embargo and

Import Substitution:

Current Status and Trends

Dr. Sholpan Gaisina

Professor, BMS

Outline

1. A short history of Russian agricultural products embargo.

2. Russian embargo impact on European agricultural sector

3. Russian embargo impact on Russian Economy and

agricultural sector

4. Russian import substitution policy. Expectations and

Concerns

On August 7, 2014, the Russian government imposed an embargo on a

range of agricultural and food products imported from the European

Union (EU), the United States, Canada, Australia and Norway.

On August 13, 2015 the countries which joined the anti-Russian sanctions

as Albania, Montenegro, Iceland, Liechtenstein, since 1 January 2016,

Ukraine were included into this list.

Since August 2015 “sanction products” in Russia are subject to

destruction.

The EU Council extended anti-Russian sanctions until January 31 2017, and

Russia extended its counter-sanctions until December 31 2017.

M. Petrick, 2015, One year after the Russian ban on food imports from the West : effects and implications, XXIX International Conference of Agricultural Economists, Milan, Italy

A short history of Russian agricultural products embargo

A short history of Russian agricultural products embargo

The products covered include bovine meat, pig meat, processed meat, poultry,

fish and other seafood, milk and milk products, vegetables, fruits and nuts.

It was supposed that the countries fallen under the embargo will not be able to

find a replacement for the Russian market and will suffer losses.

Economists of РАНХиГС (Russian Academy of Public Economics and

Government Service) say: the Russian share in agricultural exports of these

countries in 2013 was about 4.8%.

At the same time the dependence of Russia on imported agricultural products

from these countries was high, import declined from 44% in 2013 to 24% in 2015.

M. Petrick, 2015, One year after the Russian ban on food imports from the West : effects and implications, XXIX International Conference of Agricultural Economists, Milan, Italy Bulletin. Food embargoes: import substitution and changes in the structure foreign trade, 2015, Analytical Center of the Russian Government

N. Ischenko, P. Kozlov, 2016, Economists recognized ineffectiveness of Russian embargo as a reaction to sanctions. Vedomosty, 18 April, 2016

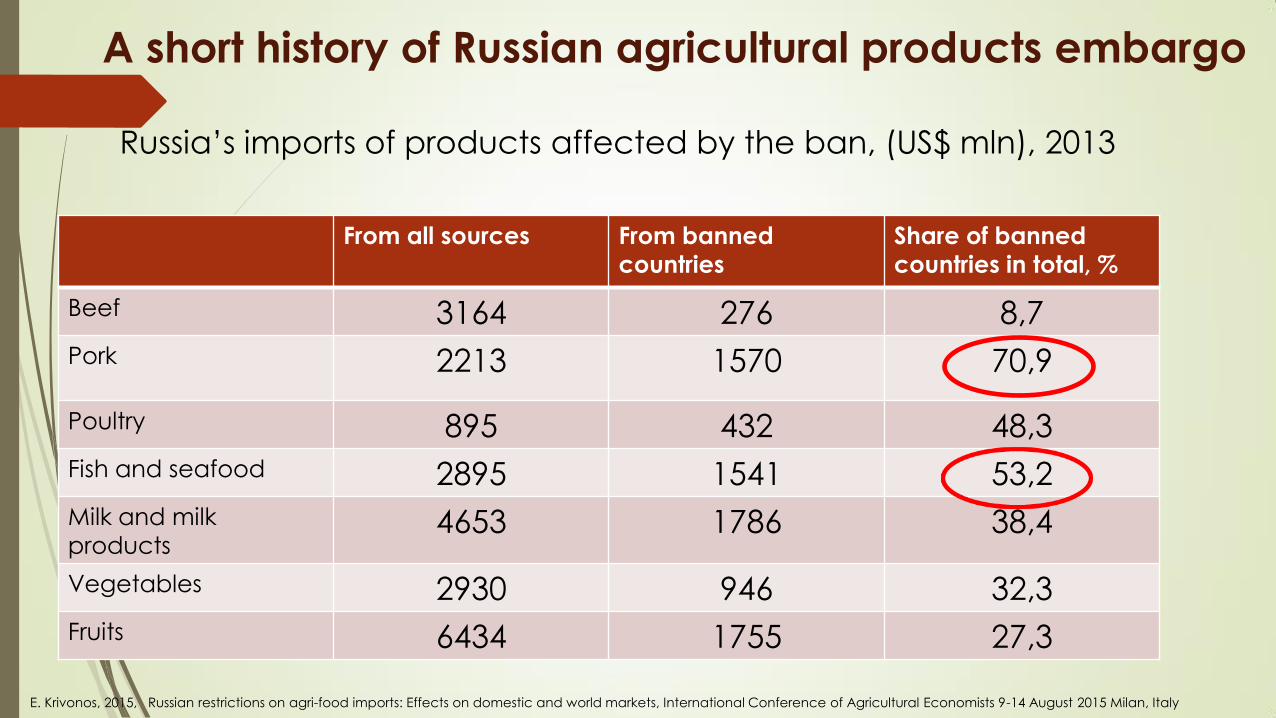

From all sources From banned

countries

Share of banned

countries in total, %

Beef 3164 276 8,7

Pork 2213 1570 70,9

Poultry 895 432 48,3

Fish and seafood 2895 1541 53,2

Milk and milk

products 4653 1786 38,4

Vegetables 2930 946 32,3

Fruits 6434 1755 27,3

E. Krivonos, 2015, Russian restrictions on agri-food imports: Effects on domestic and world markets, International Conference of Agricultural Economists 9-14 August 2015 Milan, Italy

Russia’s imports of products affected by the ban, (US$ mln), 2013

A short history of Russian agricultural products embargo

The ban was a reaction to sanctions imposed by Western countries in the

course of the political conflict over Ukraine, including the annexation of

the Crimea by the Russian Federation earlier in 2014.

It was not by accident that the Russian administration chose the

agricultural sector as an arena for import restrictions

Against the collapse of the domestic livestock herd after the dissolution of

the Soviet Union, worldwide food price increases, and recurrent droughts

in some of the main agricultural regions, self-sufficiency in food has

become a key political goal of the Russian government.

M. Petrick, 2015, One year after the Russian ban on food imports from the West : effects and implications, XXIX International Conference of Agricultural Economists, Milan, Italy

A short history of Russian agricultural products embargo

The ban raises some important question:

To what extent do the sanctions imply price increases and welfare losses

for Russian consumers?

Which previous exporters were hit most?

To what extent and how fast will they be replaced by other sources?

Will the ban be instrumental for boosting domestic productivity in

agriculture?

M. Petrick, 2015, One year after the Russian ban on food imports from the West : effects and implications, XXIX International Conference of Agricultural Economists, Milan, Italy

A short history of Russian agricultural products embargo

E. Krivonos, 2015, Russian restrictions on agri-food imports: Effects on domestic and world markets, International Conference of Agricultural Economists 9-14 August 2015 Milan, Italy

Russian embargo impact on European agricultural sector

Beef Pork Poultry Fish and

seafood

Milk and

milk

products

Vegetabl

es

Fruits

USA 0 0,4 6,2 1,6 0 0,1 1,5

EU* 20,1 25,4 4,9 4,6 6,6 25,3 32,4

Canada 0 9,6 0 2,8 0 0,2 0

Australia 2,8 0 0 0 3,3 0 0,9

Norway 0 0 0 11,0 3,6 0 0

Share of exports to Russia in the value of exports of the affected

product, by exporter, 2013

*Intra-EU trade is excluded

It is possible to identify the differential impact of the ban across countries

reflecting the significance of the Russian market for their respective export

trades.

For example, Russia had been a key destination for cheese exports from the

Baltic countries, representing more than 30% of Lithuanian, and some 83% of

Finland's cheese exports went to Russia.

Russia was a key destination for Finnish butter exports outside the EU, while for

France, Russia represented 15% of its extra - EU exports.

J. McEldowney, 2016, The Russian ban on agricultural products, EPRS, European Parliamentary Research Service

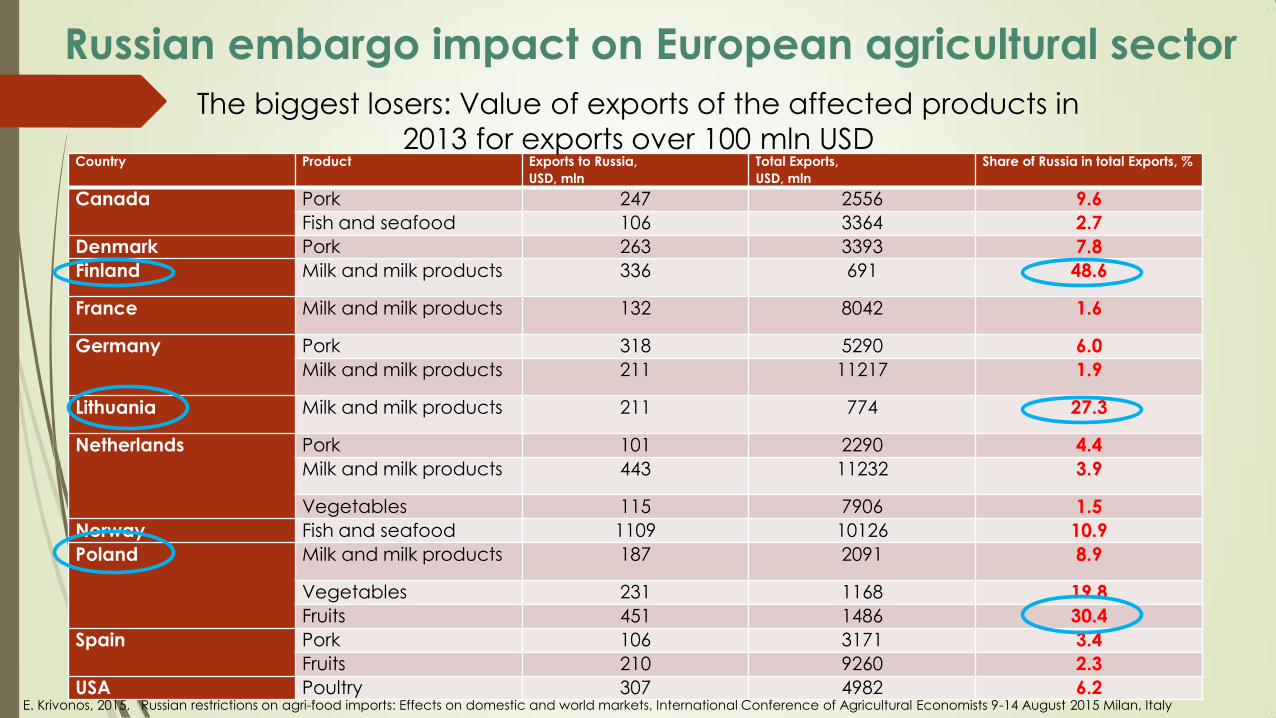

Russian embargo impact on European agricultural sector

Country Product Exports to Russia,

USD, mln

Total Exports,

USD, mln

Share of Russia in total Exports, %

Canada Pork 247 2556 9.6

Fish and seafood 106 3364 2.7

Denmark Pork 263 3393 7.8

Finland Milk and milk products 336 691 48.6

France Milk and milk products 132 8042 1.6

Germany Pork 318 5290 6.0

Milk and milk products 211 11217 1.9

Lithuania Milk and milk products 211 774 27.3

Netherlands Pork 101 2290 4.4

Milk and milk products 443 11232 3.9

Vegetables 115 7906 1.5

Norway Fish and seafood 1109 10126 10.9

Poland Milk and milk products 187 2091 8.9

Vegetables 231 1168 19.8

Fruits 451 1486 30.4

Spain Pork 106 3171 3.4

Fruits 210 9260 2.3

USA Poultry 307 4982 6.2 E. Krivonos, 2015, Russian restrictions on agri-food imports: Effects on domestic and world markets, International Conference of Agricultural Economists 9-14 August 2015 Milan, Italy

The biggest losers: Value of exports of the affected products in

2013 for exports over 100 mln USD

Russian embargo impact on European agricultural sector

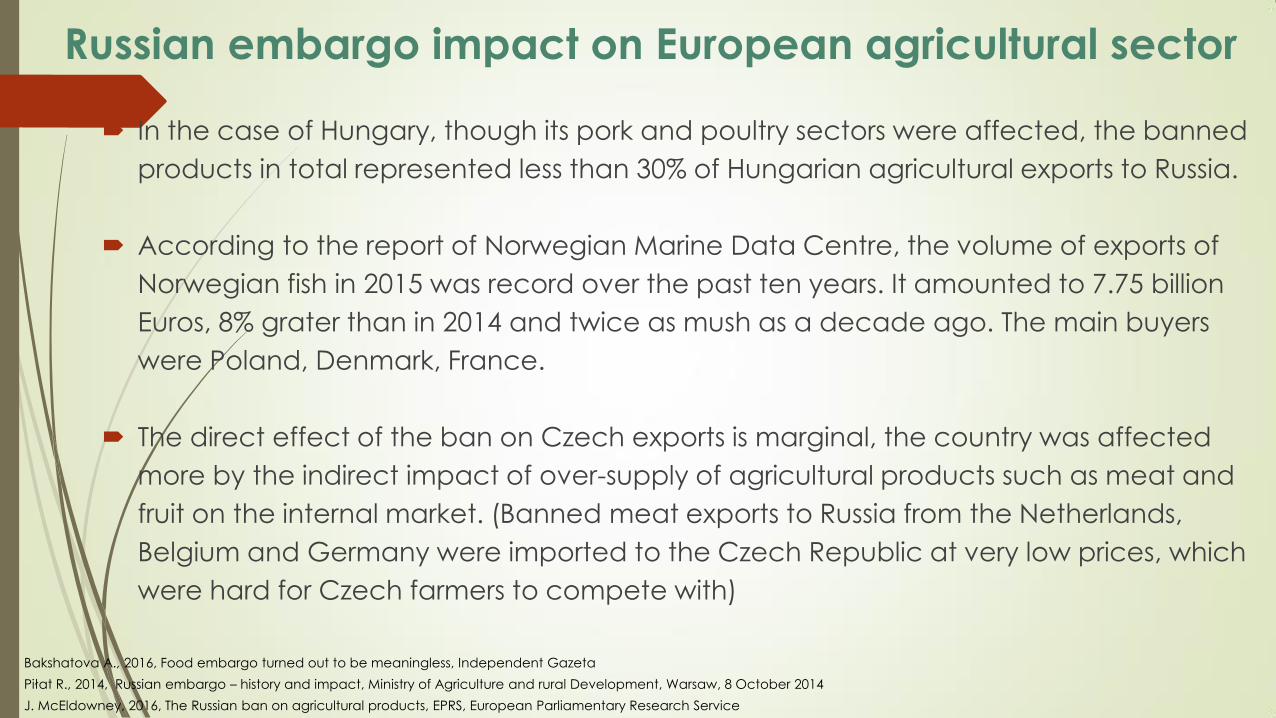

In the case of Hungary, though its pork and poultry sectors were affected, the banned

products in total represented less than 30% of Hungarian agricultural exports to Russia.

According to the report of Norwegian Marine Data Centre, the volume of exports of

Norwegian fish in 2015 was record over the past ten years. It amounted to 7.75 billion

Euros, 8% grater than in 2014 and twice as mush as a decade ago. The main buyers

were Poland, Denmark, France.

The direct effect of the ban on Czech exports is marginal, the country was affected

more by the indirect impact of over-supply of agricultural products such as meat and

fruit on the internal market. (Banned meat exports to Russia from the Netherlands,

Belgium and Germany were imported to the Czech Republic at very low prices, which

were hard for Czech farmers to compete with)

J. McEldowney, 2016, The Russian ban on agricultural products, EPRS, European Parliamentary Research Service

Piłat R., 2014, Russian embargo – history and impact, Ministry of Agriculture and rural Development, Warsaw, 8 October 2014

Bakshatova A., 2016, Food embargo turned out to be meaningless, Independent Gazeta

Russian embargo impact on European agricultural sector

In the case of Poland, the Russian ban is considered as contributing to the collapse of

apple prices in the country (about 40% of Polish exports went to Russia) and it also

affected other sectors such as mushrooms and tomatoes. Its exports of cheese to

Russia represented 43% of total cheese exports, equivalent to 4% of Poland's entire

cheese production. Based on data from 2013 , the ban covered 67% of Polish agri-

food export to Russian Federation

However, according to the Ministry of Agriculture and Rural Development, Poland

almost immediately adapted to the changed conditions. Agri-food product exports

income in 2015, is reached a value of ca. 22.5 billion Euro, and is 3% greater than in

2014. Exports of pork and beef was reoriented to the EU countries.

The crash of cheese export to Russia resulted in the dairy industry increasing sales to

Algeria and countries of Asia, which report demand mainly for milk and powdered

whey.

Agriculture and Food Economy in Poland, Institute of Agricultural and Food Economics, Warsaw 2015

Russian embargo impact on European agricultural sector

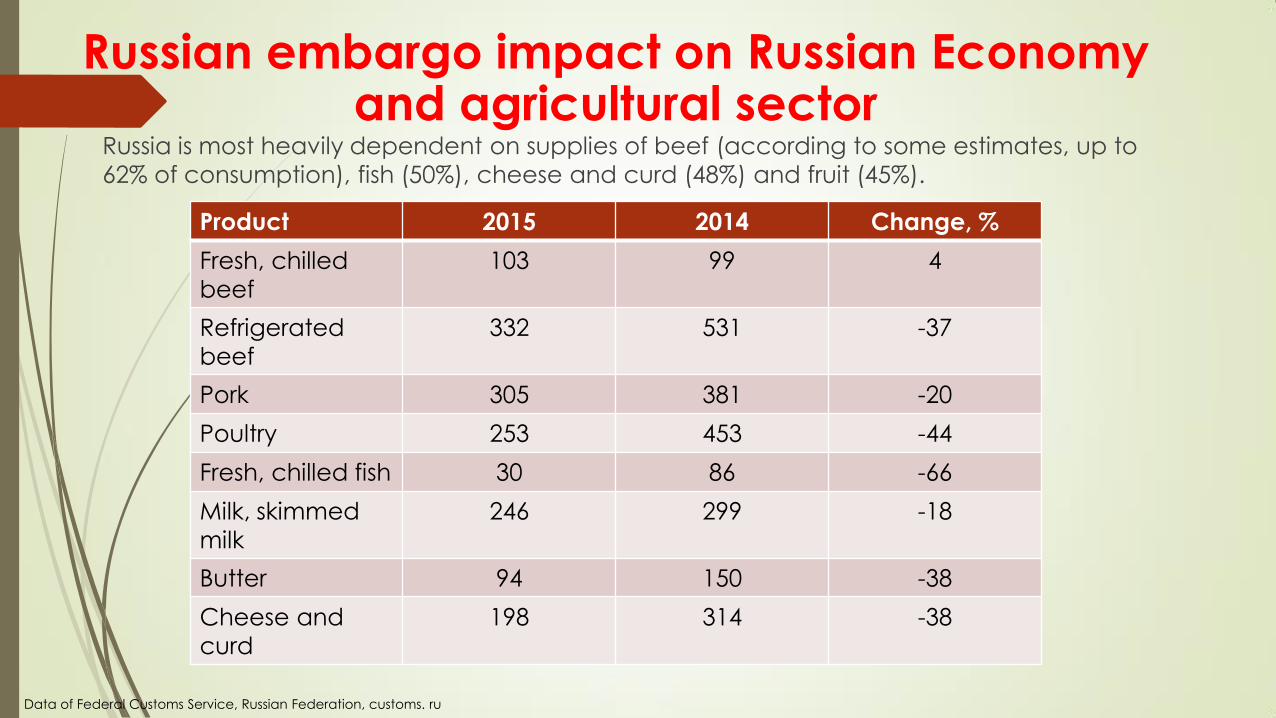

Russia is most heavily dependent on supplies of beef (according to some estimates, up to

62% of consumption), fish (50%), cheese and curd (48%) and fruit (45%).

Product 2015 2014 Change, %

Fresh, chilled

beef

103 99 4

Refrigerated

beef

332 531 -37

Pork 305 381 -20

Poultry 253 453 -44

Fresh, chilled fish 30 86 -66

Milk, skimmed

milk

246 299 -18

Butter 94 150 -38

Cheese and

curd

198 314 -38

Data of Federal Customs Service, Russian Federation, customs. ru

Russian embargo impact on Russian Economy and agricultural sector

Consumer prices for all key socially important goods rose by double digits.

In May 2015 the average consumer price of beef increased by 23% compared to

May 2014, for pork - by 22%, cheese - by 20%, for frozen fish - by 38%, carrot - by

39%, for apples - 37%, cereals and beans - by 49.2%.

The prices of goods that do not fall under the embargo did grow too: the price of

sugar rose by 52.2%, sunflower oil - by 23.7%, pasta - by 21.6%.

The embargo only strengthened previously established price trends in the markets

of meat and fish.

The rise in prices for dairy products and apples became a direct result of

decreased supply and reduced competition in the Russian market.

Russian embargo impact on Russian Economy and agricultural sector

Gontmacher E., Visischkevich E., 2015, The reverse output of food embargo, Vedomosty

In 2015, there was a sharp drop in household income: real disposable

income and the average wage in real terms decreased by 4% and

9.5%, respectively, which led not only to a significant reduction in

consumption, but also to a change in its structure.

In 2014, the share of food in the consumer basket resumed growth and

reached 38%.

This share is much higher than in developed countries (10-20%) and even

higher than in some developing countries (e.g., in Brazil food accounts

for 17.8% of the consumer basket).

Fedotova I., 2016, How “sanctions war” impact commodity markets, Politeconomica

Russian embargo impact on Russian Economy and agricultural sector

Export of dairy products from Belarus significantly increased. In 2015, more than 80% of imported cheese in Russia was delivered by Belarus. Thus, in 2015 the dependence of

Russia on imported cheeses, cottage cheese, butter and other fats from one country –

Belarus is significantly increased.

At the same time a positive impact of food embargo experience some Russian and

foreign cheesemakers.

During two years of embargo, foreign manufacturers of cheese, with production facilities in Russia, greatly expanded the production of famous brands. Finnish Valio made

significant investments in production and expanded co-operation with Russian

cheesemakers under their own brands.

According to the Analytical Center of Government of RF, the market share of the most

famous brands of cheese that are produced in Russia, increased in 2013-2015 from 23.5%

to 25%. In particular, the company Hochland has fixed its leading position in the Russian

market. dairynews.ru

Russian embargo impact on Russian Economy and agricultural sector

Russia’s partners in the Customs Union of Eurasian Economic community,

Belarus and Kazakhstan, will face serious temptation to benefit from the

situation.

Although President of Belarus Alexander Lukashenko ensured Vladimir Putin

that his country will obey the Russian embargo, he specifically said that

Belarus will not allow transit of banned foods to Russia, but will continue

buying European products for its internal purposes.

Such wording gives a wide range of opportunities for Belarusian businesses to

engage in profitable relabeling and light processing of banned food

products.

Kobylyanskiy A., 2014, Implications of Russia’s food embargo, Exclusively for Globalriskinsights.com

Russian embargo impact on Russian Economy and agricultural sector

The Russian government has taken action to downplay the negative

impact of Embargo on internal market supplies and to convince the

public that Russia is ready to replace selected missing goods with imports

from countries on which sanctions have not been imposed (Latin

America, Turkey, Egypt, Morocco, China, Uzbekistan, Turkmenistan and

Azerbaijan).

In addition to this political aspect, the Russian counter-sanctions were

intended to stimulate Russia's agricultural production, which constitutes

around four percent of Russia's GDP.

Fischer E., 2014, The Russian embargo is affecting Russia, The Centre for Eastern Studies

Russian import substitution policy. Expectations and Concerns

In 2015 Russia's agricultural industry recorded annual growth of 3

percent, and grew by another 2.6 percent (annualized) in the first

half of 2016.

However, domestic production in the case of many product

groups is uncompetitive in terms of price and quality when

compared to imported goods.

Many of the products on which the sanctions have been imposed

are not produced or processed in Russia at all.

https://sputniknews.com/russia/20160807/1044026162/russia-counter-sanctions-two-years.html

Fischer E., 2014, The Russian embargo is affecting Russia, The Centre for Eastern Studies

Russian import substitution policy. Expectations and Concerns

According to the Russian Minister of Agricutlrue Mr. Tkachev, Russian agriculture and production

sector has become much more competitive. He says that the average operating profitability of

farming producers reaches 20% with governmental support and about 10% without donations.

Deprecation of the ruble is another reason why home-made goods are in a more advantageous

position if compared to the foreign products. The stronger is the US dollar the higher are the

prices of foreign goods. And what is even more important Russians started to choose domestic

products over foreign goods.

http://agroinfo.com/en/news/mr-tkachev-even-abolish-embargo-nothing-bad-will-happen-domestic-market/

Russian import substitution policy. Expectations and Concerns

That is why the market creep is very unlikely to happen even if the

embargo will be abolished says Mr. Tkachev.

For example the country has no more need for foreign pork or

poultry – this niche is fully covered by the domestic producers. The

same is relevant for sugar, buckwheat, potato and oil.

The Minister highlighted that when it comes to beef market Russian

farmers should be able to cover this niches for 80-85 % within five

years from now.

Russian import substitution policy. Expectations and Concerns

Tatyana Radchenko, deputy head of the Russian government's Analytical

Center told RIA Novosti that during 2014 and 2015, Russia's production of

meat and poultry rose by an average of ten percent, the production of

cheese products rose by 10.6 percent and butter by 3.2 percent.

Radchenko said that the proportion of imported meat and poultry

products on the Russian market decreased from 27 percent in 2013 to 13

percent in 2015. The proportion of imported butter decreased from 36

percent to 26 percent, and imported cheese from 48 percent to 23 percent.

https://sputniknews.com/russia/20160807/1044026162/russia-counter-sanctions-two-years.html

Russian import substitution policy. Expectations and Concerns

Beef and dairy herd numbers have fallen while almost all the rest of

the sector has seen increased levels of activity.

Natalya Zubarevich argues persuasively that the difference is due to

uncertainty about the duration of the counter-sanctions, since crops,

pigs and poultry have relatively short payback periods whereas

investing in cattle requires a five-to seven-year horizon, and nobody

can be confident that the counter-sanctions will last that long.

The increase in the agricultural yields and reallocation of resources

would require additional time.

Connolly R. and Hanson P., 2016, Import Substitution and Economic Sovereignty in Russia, Research Paper, Russia and Eurasia Programme

Kobylyanskiy A., 2014, Implications of Russia’s food embargo, Exclusively for Globalriskinsights.com

Russian import substitution policy. Expectations and Concerns

The development of land cultivation, animal husbandry and gardening

have been neglected for years in Russia and so this along with the

reconstruction of food and agricultural production processing plants

(slaughterhouses, warehouses, cold stores, sorting plants, etc.) will require a

few years, vast financial outlays and the preparation of qualified staff at the

very least.

The development of agricultural production must also be accompanied by

the development of agricultural machinery production and services, the

reconstruction of research and development centres dedicated to

agriculture, the development of veterinary and epidemiological services

and many other measures.

Fischer E., 2014, The Russian embargo is affecting Russia, The Centre for Eastern Studies

Russian import substitution policy. Expectations and Concerns

Electricity and farming tycoon Dmitry Arzhanov told that he plans to invest heavily in

apples and potatoes to fill gaps caused by the food embargo.

But Arzhanov said cheap Polish apples would probably flood back to Russia if the

embargo were lifted soon.

In general Russia needed to keep import restrictions in place long enough for domestic producers to invest and turn a profit, which often required several years, he

said.

"I'm not for counter-sanctions or against them. I'm for consistency. If they have been introduced then they will need to remain for a certain time."

Arzhanov's concerns illustrate the likelihood that import restrictions may ultimately

prove hard to remove because of the domestic lobbies that benefit from them.

http://www.reuters.com/article/us-russia-economy-import-substitution-idUSKCN0RV4W920151001

Russian import substitution policy. Expectations and Concerns

According to the report of analytical Center of RF Government:

“The introduction of the embargo has created an opportunity for

import substitution by domestic manufacturers, but the potential of

import substitution in the short term proved to be far from fully realized."

The reasons lie in a number of objective economic factors:

The production of some products, such as beef and fish, is associated

with long payback periods of investment projects;

Bulletin. Food embargoes: import substitution and changes in the structure foreign trade, 2015, Analytical Center of the Russian Government

Russian import substitution policy. Expectations and Concerns

The production cycle can significantly exceed the annual period of the

embargo, which has a negative impact on incentives to invest in

production capacity. The announcement of the extension of the

embargo for a year increases the incentives to invest, however, the

planning horizon is again limited to an annual period;

An increase in interest rates to a large extent limited the ability of

producers to obtain loans not only for investment but also for working

capital;

Increased expenses for imported raw materials;

Food production has grown only in several food categories, and could

only partially substitute imported products under ban.

Russian import substitution policy. Expectations and Concerns (cont.)

Bulletin. Food embargoes: import substitution and changes in the structure foreign trade, 2015, Analytical Center of the Russian Government

Russia remains one of the world’s largest manufacturers.

The problem is that much of this manufacturing is not competitive on global

markets, is consumed domestically and is correlated with performance in the

hydrocarbons industry.

Research suggests that successful economic diversification occurs when there is a

substantial and sustained investment in activities that are close to a country’s

existing areas of comparative advantage.

This might see resources allocated to the development of oil refining,

petrochemicals, and even the oil and gas extraction equipment industry.

In Russia’s case, this might mean that at tempts to stimulate industries such as

nanotechnology or beef herds are likely to fail.

Connolly R. and Hanson P., 2016, Import Substitution and Economic Sovereignty in Russia, Research Paper, Russia and Eurasia Programme

Russian import substitution policy. Expectations and Concerns

An October 2015 article under the name of Prime Minister Dmitry Medvedev, who also chairs

the Government Commission on Import Substitution, suggests that part of the political elite still

wishes to see Russia pursuing integration with the global economy.

It starts with the proposition that the main aim of economic policys to enable the country “to

enter the group of countries with the highest level of well-being’.

But, it continues, Russia lags behind these countries in labor productivity and needs to become

more competitive.

Most countries that make a breakthrough into the leading group use the advantages of free

trade: “It is hard to name countries that have made continuing, steady progress by prolonged

self-limitation in trade.”

The article concludes that sanctions will sooner or later come to an end, that a return to

cooperation with the Wests inevitable, and that import substitution must not become the

“slogan of the day”.

Connolly R. and Hanson P., 2016, Import Substitution and Economic Sovereignty in Russia, Research Paper, Russia and Eurasia Programme

Russian import substitution policy. Expectations and Concerns

The import-substitution plans may reduce competition in the economy is made even more worrying by the fact that the intensity of competition a cross the Russian economy is already low by global standards

This is important because of the role that competition plays in stimulating productivity and innovation

Real diversification will occur only if new industries are export-oriented.

Connolly R. and Hanson P., 2016, Import Substitution and Economic Sovereignty in Russia, Research Paper, Russia and Eurasia Programme

Russian import substitution policy. Expectations and Concerns

Pascal Lamy, a former head of the World Trade Organization:

import-substitution policies rarely bring long-term economic benefits, because they

contradict the principles of free trade.

It's a tiny and shrinking part of the market of ideas. But blaming the foreigner has always

been a fundamental trick of domestic politics: it has worked for centuries.

Import-substitution policies may well work in terms of boosting domestic production. But

they do so at the expense of consumers, who end up paying more, and erode overall

economic performance by distorting the allocation of resources.

In most of the cases import substitution policies have failed. They degrade the efficiency

of their economy.

http://www.reuters.com/article/us-russia-economy-import-substitution-idUSKCN0RV4W920151001

Russian import substitution policy. Expectations and Concerns

Thank you very much for your attention!