agm notice of meeting and proxy form - asx april 2012 company announcements office australian...

TRANSCRIPT

20 April 2012 Company Announcements Office Australian Securities Exchange Limited Level 4 20 Bridge Street SYDNEY NSW 2000 AGM NOTICE OF MEETING AND PROXY FORM In accordance with Listing Rule 3.17, please find attached copies of the Notice of Meeting and Proxy Form for the Company’s Annual General Meeting, to be held on Tuesday 22 May 2012, which will be dispatched to shareholders today. We also attach a copy of the Company’s December 2011 Concise Annual Report which will also be dispatched to shareholders today. The Company’s December 2011 Concise Annual Report was previously released to the ASX on 30 March 2012. These documents will be available on the Leighton Holdings website at www.leighton.com.au Yours faithfully, LEIGHTON HOLDINGS LIMITED A. J. MOIR Company Secretary

To: The Shareholders

Notice is hereby given that the 2012 Annual General Meeting of Leighton Holdings Limited (Company) will be held in The Ballroom, Four Seasons Hotel Sydney, 199 George Street Sydney, New South Wales, on Tuesday 22 May 2012 at 10am to transact the following business:

1. Annual Financial Report and Directors’ and Auditor’s Reports

To receive the Financial Report and Reports of the Directors and Auditor for the 6 month financial period from 1 July 2011 to 31 December 2011 (December 2011 Transitional Financial Year).

To consider and if thought fit pass the following resolutions as ordinary resolutions:

2. Remuneration Report

To adopt the Remuneration Report for the December 2011 Transitional Financial Year.

(Note: The vote on this resolution is non-binding.)

3. Election of Directors

3.1 That Ms Paula Dwyer, who was appointed as a Non-executive Director of the Company on 1 January 2012 and, in accordance with Clause 17.2 of the Company’s Constitution, holds office as a Director until the conclusion of this meeting and, being eligible, offers herself for election, be elected.

3.2 That Mr Wayne Osborn, who retires by rotation in accordance with Clause 18 of the Company’s Constitution and, being eligible, offers himself for re-election, be re-elected.

3.3 That Mr Peter Sassenfeld, who was appointed as a Non-executive Director of the Company on 29 November 2011 and, in accordance with Clause 17.2 of the Company’s Constitution, holds office as a Director until the conclusion of this meeting and, being eligible, offers himself for election, be elected.

3.4 That Dr Michael Llewellyn-Smith, who has nominated himself for election as a Director of the Company in accordance with Clause 19.2(c) of the Company’s Constitution, be elected.

See the accompanying Explanatory Notes for information about the election of Directors.

4. Appointment of Deloitte Touche Tohmatsu as auditor of the Company

That Deloitte Touche Tohmatsu, having consented to do so, be appointed to act as auditor of the Company.

5. Approval of the Leighton Holdings Equity Incentive Plan

That the Leighton Holdings Equity Incentive Plan, details of which are summarised in the Explanatory Notes to this Notice of Meeting, is approved for all purposes under the Corporations Act 2001 (Cth) and the ASX Listing Rules.

6. Approval of incentive grants to Executive Directors

6.1 That approval is given to grant rights to receive fully paid ordinary shares in the Company to the Company’s Chief Executive Officer, Mr Hamish Tyrwhitt, under the Leighton Holdings Equity Incentive Plan on the terms summarised in the Explanatory Notes to this Notice of Meeting.

6.2 That approval is given to grant rights to receive fully paid ordinary shares in the Company to the Company’s Chief Financial Officer, Mr Peter Gregg, under the Leighton Holdings Equity Incentive Plan on the terms summarised in the Explanatory Notes to this Notice of Meeting.

Invitation

After the meeting, all shareholders are invited to join the Directors for light refreshments.

By Order of the Board A.J. Moir, Sydney 18 April 2012

LEIGHTON HOLDINGS LIMITED ABN 57 004 482 982

NOTICE OF ANNUAL GENERAL MEETING 2012

Registered Office:472 Pacific HighwaySt Leonards NSW 2065 AustraliaFax number +61 2 9925 6005

Share Registrar:Computershare Investor ServicesPty LimitedLevel 4, 60 Carrington Street Sydney NSW 2000 Australia Fax number + 61 3 9473 2555

Share Registrar’s Postal Address:Share RegistrarComputershare Investor ServicesPty LimitedGPO Box 242Melbourne VIC 3001 Australia

1

Proxies

A proxy form accompanies this notice. Additional proxy forms will be provided by the Company’s Share Registrar, Computershare Investor Services Pty Limited, on request.

As a shareholder entitled to attend and vote at the meeting, you may appoint up to 2 proxies to attend and vote for you. You may specify the proportion or number of votes that the proxy may exercise. If you appoint 2 proxies and do not specify the proportion or number of votes each proxy may exercise, each proxy may exercise half of the votes.

A proxy need not be a shareholder of the Company.

The key management personnel (KMP) of the Company (which includes each of the Directors) and their closely related parties will not be able to vote your proxy on items 2, 5 and 6 unless you have directed them how to vote. The term “closely related party” is defined in the Corporations Act 2001 (Cth) and includes a member of the KMP’s spouse, dependant and certain other close family members, as well as any companies controlled by the KMP. If you intend to appoint a member of the KMP as your proxy, please ensure that you direct them how to vote on items 2, 5 and 6. If you intend to appoint the Chairman of the meeting as your proxy, you can direct him how to vote on items 2, 5 and 6 by marking the relevant boxes on the proxy form. However, if the Chairman of the meeting is your proxy and you do not mark any of the boxes opposite items 2, 5 and 6, you will be deemed to have directed the Chairman to vote in favour of those items.

The proxy form must be signed by you or your attorney. Proxies given by corporations must be executed either in accordance with section 127 of the Corporations Act 2001 (Cth) or under the hand of a duly authorised officer or attorney.

The proxy form and the power of attorney or other authority under which it is signed (if any), or a certified copy of the power of attorney or authority, must be received at or sent by fax to the Company’s Share Registrar not later than 10 am (AEST) on Sunday, 20 May 2012. See above for the fax number and address of the Share Registrar.

Online Lodgement: You may lodge an electronic proxy online at www.investorvote.com.au (Control Number 185488) not later than 10 am (AEST) on Sunday, 20 May 2012. You will need your Securityholder Reference Number (SRN) or Holder Identification Number (HIN)

and to confirm your postcode if you reside in Australia or country of residence if you reside outside Australia.

Eligibility to Vote

For the purposes of the meeting, shares will be taken to be held by persons who are registered as members as at 7 pm (AEST) on Sunday, 20 May 2012. Accordingly, transactions registered after that time will be disregarded in determining shareholders entitled to attend and vote at the meeting.

Voting Exclusions

Item 2

The Company will disregard any votes cast on item 2:

• byoronbehalfofamemberoftheKMP(whoseremuneration is disclosed in the Remuneration Report) and any closely related parties (such as close family members and any companies the person controls) of those persons; and

• asaproxy,byamemberoftheKMPoracloselyrelated party of a member of the KMP,

unless the vote is cast as proxy for a person entitled to vote on item 2 in accordance with a direction on the proxy form.

Item 5

The Company will disregard any votes cast on item 5:

• inanycapacitybytheExecutiveDirectors(beingtheonly Directors entitled to participate in an employee incentive scheme) and any of their associates; and

• asaproxy,byamemberoftheKMPoracloselyrelated party of a member of the KMP,

unless the vote is cast as proxy for a person entitled to vote on item 5 in accordance with a direction on the proxy form.

In addition, any shareholder who is:

• anemployeeorDirectorofacompanyintheLeighton Group; or

• anassociateofsuchanemployee,

should not cast any votes on item 5 (other than as a directed proxy) if they wish to preserve the benefit of the approvals being sought.

2

Registered Office:472 Pacific HighwaySt Leonards NSW 2065 AustraliaFax number +61 2 9925 6005

Share Registrar:Computershare Investor ServicesPty LimitedLevel 4, 60 Carrington Street Sydney NSW 2000 Australia Fax number +61 3 9473 2555

Share Registrar’s Postal Address:Share RegistrarComputershare Investor ServicesPty LimitedGPO Box 242Melbourne VIC 3001 Australia

Item 6

The Company will disregard any votes cast on items 6.1 and 6.2:

• inanycapacitybytheExecutiveDirectors(beingtheonly Directors entitled to participate in an employee incentive scheme) and any of their associates; and

• asaproxy,byamemberoftheKMPoracloselyrelated party of a member of the KMP,

unless the vote is cast as proxy for a person entitled to vote on items 6.1 and 6.2 in accordance with a direction on the proxy form.

3

Registered Office:472 Pacific HighwaySt Leonards NSW 2065 AustraliaFax number +61 2 9925 6005

Share Registrar:Computershare Investor ServicesPty LimitedLevel 4, 60 Carrington Street Sydney NSW 2000 Australia Fax number + 61 3 9473 2555

Share Registrar’s Postal Address:Share RegistrarComputershare Investor ServicesPty LimitedGPO Box 242Melbourne VIC 3001 Australia

ITEM 1

ANNUAL FINANCIAL REPORT AND DIRECTORS’ AND AUDITOR’S REPORTS

The Financial Report and the Directors’ and Auditor’s Reports for the December 2011 Transitional Financial Year will be tabled at the meeting. Shareholders will have a reasonable opportunity at the meeting to ask questions about or make comments on the Financial Report and the Directors’ and Auditor’s Reports as well as on the management of the Company. The Financial Report for consideration at the meeting will be the full Financial Report. Any shareholder wishing to receive a copy of the full Financial Report should contact the Company’s Share Registrar, Computershare Investor Services Pty Limited, and a copy will be provided free of charge.

Shareholders will also have a reasonable opportunity at the meeting to ask questions of the Company’s current external auditor, KPMG, relevant to:

(a) the conduct of the audit;

(b) the preparation and content of the Auditor’s Report;

(c) the accounting policies adopted by the Company in relation to the preparation of the financial statements; and

(d) the independence of the auditor in relation to the conduct of the audit.

ITEM 2

REMUNERATION REPORT

Shareholders will have a reasonable opportunity at the meeting to ask questions about or make comments on the Remuneration Report. The Remuneration Report on pages 75 to 112 of the Concise Annual Report sets out the remuneration policies of the Company and reports on the remuneration arrangements in place for Non-executive Directors, Executive Directors and the senior executives of the Group during the December 2011 Transitional Financial Year. As foreshadowed at the Annual General Meeting in November 2011, the Board has conducted a comprehensive review of executive remuneration and incentives. The revised remuneration and incentive scheme is currently being implemented and is described on pages 84 to 88 of the Concise Annual Report.

As prescribed by the Corporations Act 2001 (Cth) (the Act), the vote on the adoption of the Remuneration Report is advisory only and does not bind the Directors or the Company. However, the Board does take the outcome of the vote and discussion at the meeting into account in setting remuneration policy for future years.

The Board recommends that shareholders vote in favour of the adoption of the Remuneration Report.

ITEM 3

ELECTION OF DIRECTORS

The Board’s policy is to maintain a Board with a mix of skills, experience and diversity of backgrounds suitable for the Company’s current and anticipated future circumstances. The Remuneration & Nominations Committee undertakes an assessment of each candidate standing for election or re-election as a Director, based on their background, skills and experience and having regard to the size, market position, complexity and strategic focus of the Leighton Group. On the basis of this assessment, the Remuneration & Nominations Committee makes a recommendation to the Board on whether to support the election or re-election of each candidate.

The experience, qualifications and other details about the candidates for election to the office of Director are set out below.

Item 3.1 Election of Ms Paula Dwyer

Ms Paula Dwyer (51) Non-executive Director B.Com. FCA, FAICD, F.Fin

An independent Non-executive Director and Chairman of the Audit Committee since 1 January 2012. Ms Dwyer holds a Bachelor of Commerce from the University of Melbourne. Ms Dwyer is a Fellow of the Institute of Chartered Accountants in Australia, the Australian Institute of Company Directors and the Financial Services Institute of Australasia.

Ms Dwyer had an executive career in finance holding senior positions in investment management, investment banking and chartered accounting with Ord Minnett (now JP Morgan) and PricewaterhouseCoopers. Ms Dwyer is a Member of the Takeovers Panel, a Board Member of the Faculty of Business and Economics at the University of Melbourne, a Member of the Geelong

4

LEIGHTON HOLDINGS LIMITED ABN 57 004 482 982

EXPLANATORY NOTES

Grammar School Council and Deputy Chairman of the Baker IDI Heart and Diabetes Institute.

Ms Dwyer is the Chairman of Tabcorp Holdings Limited (a role she has held since June 2011) and has been a Director of that company since August 2005. Ms Dwyer was appointed a Non-executive Director of Australia and New Zealand Banking Group Limited and of Lion Group on 1 April 2012.

Ms Dwyer was formerly a Director of Suncorp Group Limited from 2007 to February 2012 (where she was also Chairman of the Audit Committee), Foster’s Group Limited from May to December 2011, Healthscope Limited from March to October 2010, Astro Japan Property Group Limited from February 2005 to December 2011, Promina Group Limited from 2002 to 2007, David Jones Limited from 2003 to 2006 and RACV Limited from 2001 to 2002.

Recommendation The Directors (excluding Ms Dwyer) unanimously recommend that shareholders vote in favour of Resolution 3.1.

Item 3.2 Election of Mr Wayne Osborn

Mr Wayne Osborn (60) Non-executive Director Dip EE, MBA, FSTE, MIE Aust, FAICD

An independent Non-executive Director since November 2008. Chair of Thiess Pty Ltd since October 2008 (Director since October 2005). Chair of the Council of the Australian Institute of Marine Science, Trustee of Western Australian Museum, Fellow of Australian Academy of Technological Sciences & Engineering, Fellow of the Explorers Club – New York, Member of the Institution of Engineers Australia and former Chair of Australian Aluminium Council. A Director of Alinta Holdings (formerly Amber Holdings) since March 2011. Mr Osborn has 35 years of experience in the Australian mining, resources and manufacturing sectors and was a former Chairman and Managing Director of Alcoa Australia Ltd.

Mr Osborn is a Director of the following other ASX listed entities: Wesfarmers Limited since March 2010 and Iluka Resources Limited since March 2010.

Recommendation The Directors (excluding Mr Osborn) unanimously recommend that shareholders vote in favour of Resolution 3.2.

Item 3.3 Election of Mr Peter Sassenfeld

Mr Peter Sassenfeld (45) Non-executive Director MBA

A Non-executive Director since 29 November 2011. Mr Sassenfeld joined HOCHTIEF in November 2011 as the Chief Financial Officer and prior to this role he was Chief Financial Officer of Ferrostaal AG. Mr Sassenfeld has also worked as Chief Financial Officer at Krauss Maffei AG and in senior finance roles at Bayer AG and the Mannesmann Group. Mr Sassenfeld graduated in 1991 from the University of Saarland, Germany with an MBA (Diplom-Kaufmann).

Recommendation The Directors (excluding Mr Sassenfeld) unanimously recommend that shareholders vote in favour of Resolution 3.3.

Item 3.4 Election of Dr Michael Llewellyn-Smith

Dr Michael Llewellyn-Smith has nominated himself for election as a Non-executive Director in accordance with Clause 19.2(c) of the Company’s Constitution. Dr Llewellyn-Smith’s biographical details are set out below. These details were provided by Dr Llewellyn-Smith and have not been verified by the Company. By including the statement below on Dr Llewellyn-Smith, the Company does not in any way endorse its accuracy or reliability.

Dr Michael Llewellyn-Smith (69) MA (Cantab), MTCP (Sydney), MA (Adelaide). PhD (Adelaide), LFAIA, LFPIA, LMLGMA. KStJ, JP.

Dr Llewellyn-Smith is the Managing Director of Llewellyns International Urban Management Consultants. He has qualifications and over thirty years’ experience in the fields of Architecture, Town Planning and City Management. He holds three Masters’ Degrees (from Cambridge, Sydney and Adelaide Universities) and a PhD in city planning from The University of Adelaide. Dr Llewellyn-Smith has served as the Deputy City Planner of Sydney, the City Planner and then the Chief Executive Officer of the City of Adelaide, and as the Presiding Member of the South Australian Development Assessment Commission. He is a Life Fellow of the Australian Institute of Architects and the Planning Institute Australia and a Life Member of Local Government Managers Australia. Dr Llewellyn-Smith has worked as a consultant throughout Australia for all spheres of government and has worked overseas

5

in Poland, Sri Lanka and South Africa.

On the basis of the assessment and recommendation from the Remuneration & Nominations Committee, the Board has formed the view that the external candidate, Dr Llewellyn-Smith, does not have the necessary experience for a Director of a publicly listed company of Leighton’s size and complexity.

Recommendation The Board unanimously recommends that shareholders vote against Resolution 3.4.

ITEM 4

APPOINTMENT OF AUDITOR

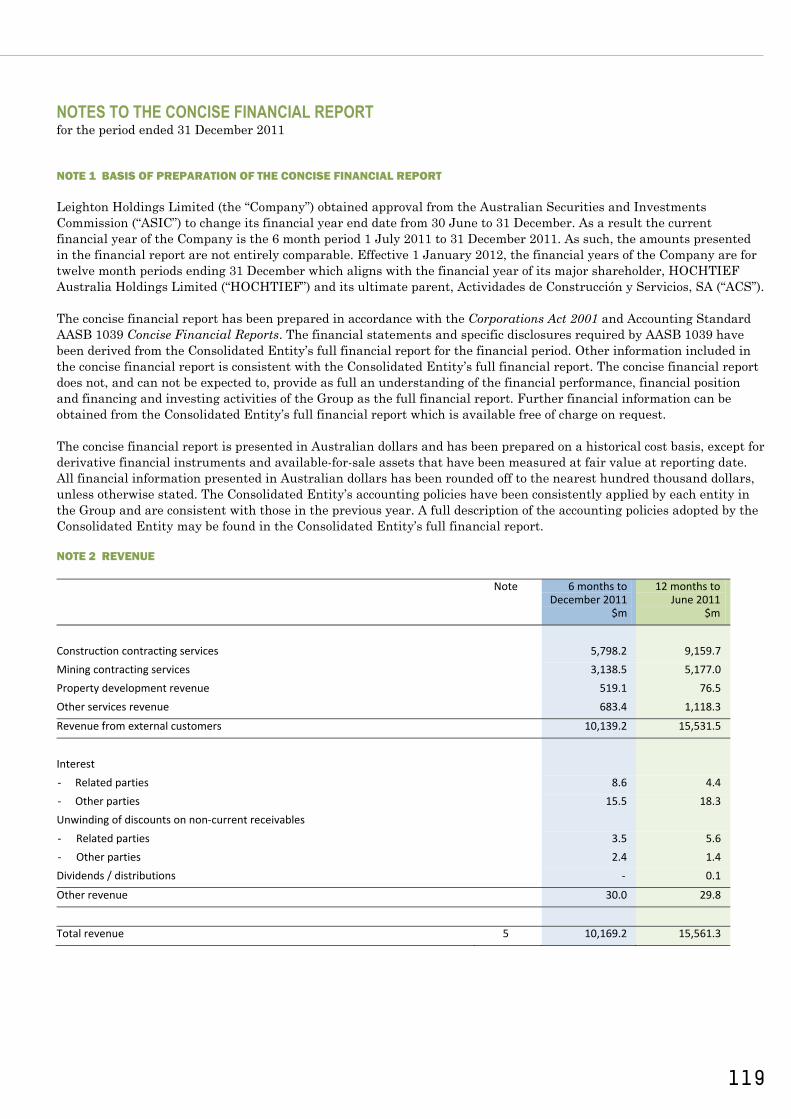

In order to align the Company’s auditor with that of its parent entity HOCHTIEF, the Board has selected Deloitte Touche Tohmatsu as the Company’s auditor. The Board believes that the appointment of Deloitte Touche Tohmatsu is in the best interests of the Company and its shareholders as it will facilitate the streamlining of the audit process between the Company and its parent entity, HOCHTIEF, as well as resulting in a reduction in costs over time.

The Chairman of the Audit Committee, Ms Dwyer, as a member of the Company, nominated Deloitte Touche Tohmatsu as auditor of the Company and Deloitte Touche Tohmatsu consented to the appointment. A copy of the nomination of Deloitte Touche Tohmatsu as auditor of the Company is on page 12 of the Explanatory Notes.

KPMG, the Company’s auditor since 1976, has agreed to resign as auditor with effect from the close of this Annual General Meeting and the Australian Securities & Investments Commission has consented to the resignation in accordance with section 329(5) of the Act.

Under the Act, shareholder approval is required for the appointment of a new auditor. Subject to this approval being obtained, the appointment of Deloitte Touche Tohmatsu will become effective from the close of this Annual General Meeting.

Recommendation The Board recommends that shareholders vote in favour of the appointment of Deloitte Touche Tohmatsu as auditor of the Company.

ITEM 5

APPROVAL OF THE LEIGHTON HOLDINGS EQUITY INCENTIVE PLAN

The Company is seeking shareholder approval for a new employee share plan. The Leighton Holdings Equity Incentive Plan (Plan) will replace the existing Leighton Senior Executive Option Plan and the Leighton Management Share Plan. The Plan establishes the legal framework under which equity grants will be made for the purposes of the Leighton Group’s short-term incentive and long-term incentive arrangements and any other equity grants.

The Plan is being introduced in light of various legislative changes and follows a review by management and the Remuneration & Nominations Committee (the Committee) of the existing remuneration arrangements. The Plan facilitates the new remuneration arrangements which aim to:

• assistwiththeattraction,motivationandretentionof employees and more closely align the interest of employees with shareholders by matching rewards with the long-term performance of the Company, and accordingly drive the Company’s improved performance;

• aligntheincentivesprovidedtoparticipatingemployees with current market practice and recent legislative changes; and

• providetheCompanywithflexibilitytoaccommodate changes in the Company’s circumstances and shifts in regulatory and market practice from time to time.

A summary of the rules for the Plan (Administration Rules) is set out below. The Administration Rules set out the general terms under which equity grants will be made. The grant of securities to an employee is subject to both the Administration Rules and the terms of the specific grant as set out in an individual employee’s offer documents.

Reasons for seeking approval

Shareholder approval of the Plan is sought for all purposes under the Act and the ASX Listing Rules, including but not limited to:

• ASXListingRule7.2(exception9),sothatanyshares issued under the Plan will be excluded from the calculation of the maximum number of new

6

EXPLANATORY NOTES (continued)

shares that can be issued by the Company in any 12 month period (currently 15% of shares previously on issue) for a period of 3 years from the date of approval.

• Sections200Band200EoftheAct,toenabletheCompany to provide termination benefits arising under the Plan to any current or future participant in the Plan who holds:

- a managerial or executive office in the Group at the time of their leaving or at any time in the 3 years prior to their leaving; and

- securities under the Plan at the time of their leaving,

but only if those securities are granted, or if the Committee exercises certain discretions under the Administration Rules, during the period from the date that this resolution is passed through to close of the 2015 Annual General Meeting.

Summary of the Administration Rules

The key terms are as follows:

• Securities offered: The types of securities that the Committee may offer are options over fully paid ordinary shares (Options), rights to receive fully paid ordinary shares (Rights) and fully paid ordinary shares (Restricted Shares). This provides theCompanywithbroadflexibilitysothatitcaneffectively incentivise employees using the most appropriate instrument (which may vary depending on the seniority of the executive, the jurisdiction in which they are issued, or prevailing market and regulatory conditions). Options, Rights and Restricted Shares are collectively referred to as Incentive Securities under the Administration Rules.

• Eligible to participate: The Committee has the discretion to determine which employees are eligible to participate in the Plan. The definition of employees under the Administration Rules captures any employee of the Company and its wholly-owned subsidiaries, including the Company’s Executive Directors.

• Flexibility to source Shares: Upon vesting of Incentive Securities, participants will become entitled to fully paid ordinary shares in the Company (Shares). The Committee can decide whether to purchase Shares on-market or issue new Shares for the purposes of the Plan.

• Performance conditions: The vesting and/or exercise of Incentive Securities will be conditional on the satisfaction of performance and/or service conditions (depending on the nature of the award) as determined by the Committee and advised to the participant at the time of the grant. This allows the Company to tailor the conditions according to the nature of the award and the relevant participant(s) andtoreflectmarketpracticeasitevolves.

• Price: Unless the Committee determines otherwise, no payment is required by the participant for the grant of an Incentive Security, as the grant will constitute part of the participant’s remuneration.

• Lapse / forfeiture: Unvested or restricted Incentive Securities will lapse or be forfeited (as the case may be) on the earlier of:

- any expiry date applicable to that Incentive Security;

- the participant dealing in respect of an Incentive Security in contravention of the Administration Rules;

- the Committee determining that the participant has acted fraudulently or dishonestly or acted in a way that brings the Group or any company within the Group into disrepute or breached his or her employment obligations;

- at the Committee’s discretion, on cessation of employment in certain circumstances, or in exceptional circumstances including a change of control of the Company; or

- failure to meet a performance condition applicable to the Incentive Security within the prescribed period.

Under the Administration Rules, the Committee also has a discretion to specify additional circumstances in which participant’s entitlement to Incentive Securities may be reduced or extinguished in order to prevent the participant from obtaining an inappropriate benefit.

• Cessation of employment: Unless the Committee determines otherwise, where a participant ceases employment before their Incentive Securities have vested or become exercisable due to:

- resignation or termination for cause – all Incentive Securities held by the participant will lapse or be forfeited (as the case may be); or

7

8

EXPLANATORY NOTES (continued)

- for any other reason – all Incentive Securities held by the participant will remain on foot, subject to the original performance conditions and will be tested in the ordinary course.

The Committee has discretion under the Administration Rules to determine an alternative treatment for a particular grant and/or participant. This discretion may be exercised by the Committee in appropriate circumstances to accelerate vesting of some or all of a participant’s Incentive Securities so that they vest on termination.

Further details regarding the proposed cessation of employment treatment for short-term and long-term incentive awards are set out in the Explanatory Notes for items 6.1 and 6.2.

The value of any acceleration of vesting cannot be determined in advance and will depend on a range of factors including:

- the Company’s share price at the time of vesting;

- the participant’s length of service and the portion of any relevant performance periods that have expired at the time they cease employment;

- the circumstances in which the participant ceases employment; and

- the number of unvested Incentive Securities that the participant holds at the time they cease employment.

• Exceptional circumstances: The Committee has the discretion to determine that some or all of a participant’s Incentive Securities will vest or cease to be subject to restrictions (as applicable) in exceptional circumstances. The types of exceptional circumstances that could result in the Committee exercising its discretion include:

- an actual or probable change in the control of the Company;

- a participant’s earning capacity being diminished due to injury, incapacitation or other health issues; and

- severe financial hardship affecting the participant or the participant’s family.

• Corporate action / capital reorganisation: In the event of any corporate action or capital reconstruction by the Company (including bonus issues and rights issues), the Committee may

adjust the terms of Rights or Options granted to a participant so as to ensure no material advantage or disadvantage to the participant.

• No dealing / hedging: Any dealing in respect of an Incentive Security is prohibited, unless the Committee determines otherwise or the dealing is required by law. The term “dealing” includes a sale, transfer, assignment, encumbrance, option, swap, any alienation of all or any part of the rights attaching to the Incentive Security or to the underlying share, or an attempt to do so, and any hedging.

Recommendation

The Board (with the Executive Directors abstaining) considers the Plan to be an effective way of incentivising participating employees and more closely aligning their interests with those of shareholders and recommends that shareholders vote in favour of Resolution 5.

ITEMS 6.1 and 6.2

APPROVAL OF INCENTIVE GRANTS TO EXECUTIVE DIRECTORS

Items 6.1 and 6.2 relate to the equity grants to the Executive Directors, Mr Hamish Tyrwhitt and Mr Peter Gregg. These grants are contemplated by the Executive Directors’ employment agreements and will be made under the Leighton Holdings Equity Incentive Plan, as described in item 5. If shareholder approval is obtained, it is intended that these grants will be made in the form of rights to receive fully paid ordinary shares in the Company (rights) on the terms set out below. The purpose of the grants is to more closely align the Executive Directors’ interests with the interest of shareholders, and to encourage the achievement of performance goals and the growth of the Company’s business.

Where the applicable vesting conditions attaching to the rights are satisfied, Mr Tyrwhitt and Mr Gregg will be allocated fully paid ordinary shares in the Company without further action required on their part. Leighton’s current intention is that any shares allocated to the Executive Directors upon vesting of the rights will be acquired on-market, however, it wishes to preserve maximumflexibilityastothesourcingofshares.

As the rights form part of the Executive Directors’ remuneration packages, they will be granted at no cost to the Executive Directors. Further details of the Executive Directors’ remuneration packages are set out in the Remuneration Report contained in the Company’s December 2011 Concise Annual Report.

Reasons for seeking approval

The Company is seeking the approval for the proposed grants of rights to the Executive Directors pursuant to ASX Listing Rule 10.14, which requires the Company to obtain shareholder approval for the issue of new securities to a director under an employee incentive scheme.

Item 6.1 - Equity incentive grant to Mr Hamish Tyrwhitt

In accordance with his employment agreement, item 6.1 seeks approval for the Company to grant Mr Tyrwhitt:

• 104,499rightsashisLTIentitlementforthe2012calendar year (LTI Rights); and

• rightsashisdeferredSTIentitlementforthe2012calendar year (STI Rights) with a maximum value of $1.8 million.

The number of LTI Rights to be granted to Mr Tyrwhitt was calculated by dividing $2.4 million (the maximum value of Mr Tyrwhitt’s LTI opportunity for the 2012 calendar year under his employment agreement) by the volume weighted average price (VWAP) of ordinary shares in the Company over the five trading days following the announcement of the financial results for the December 2011 Transitional Financial Year (excluding the date of the announcement), being $22.9667.

The maximum value of the STI Rights granted as Mr Tyrwhitt’s deferred STI component for the 2012 calendar year is $1.8 million. This value is conditional upon the achievement of exceptional performance levels. Mr Tyrwhitt’s maximum STI is 150% of total fixed remuneration, and 50% of any STI award will be deferred into STI Rights. The maximum deferred STI component therefore equates to 75% of Mr Tyrwhitt’s total fixed remuneration. Further details of Mr Tyrwhitt’s remuneration package (including the value of his STI opportunity at target and threshold performance levels) are set out in the Remuneration Report contained in the Company’s December 2011 Concise Annual Report.

The terms on which Mr Tyrwhitt’s LTI Rights and STI Rights will be granted are summarised below.

Item 6.2 - Equity incentive grant to Mr Peter Gregg

In accordance with his employment agreement, item 6.2 seeks approval for the Company to grant Mr Gregg:

• 76,197LTIRights;and

• STIRightswithamaximumvalueof$1,312,500.

The number of LTI Rights to be granted to Mr Gregg was calculated by dividing 100% of Mr Gregg’s current total fixed remuneration ($1,750,000), by the VWAP of ordinary shares in the Company over the five trading days following the announcement of the financial results for the December 2011 Transitional Financial Year (excluding the date of the announcement), being $22.9667.

The maximum value of the STI Rights granted as Mr Gregg’s deferred STI component for the 2012 calendar year is $1,312,500. This value is conditional upon the achievement of exceptional performance levels. Mr Gregg’s maximum STI is 150% of total fixed remuneration and 50% of any STI award made to Mr Gregg will be deferred into STI Rights. The maximum deferred STI component therefore equates to 75% of Mr Gregg’s total fixed remuneration.

The terms on which Mr Gregg’s LTI Rights and STI Rights will be granted are summarised below.

LTI opportunities for the Executive Directors

Timing of grant If approved, the LTI Rights will be granted shortly following this Annual General Meeting (and, in any event, prior to 22 May 2013). If not approved, the remuneration intended to be provided by way of rights will instead be delivered in cash. The cash award will be equal to the aggregate face value of rights that would otherwise have been granted and be subject to equivalent terms.

Performance period The performance period for the grants will be from 1 January 2012 to 31 December 2014.

9

10

EXPLANATORY NOTES (continued)

Performance Hurdles

The grants of LTI Rights will be divided into two equal parcels (Parcel A and Parcel B). Parcel A is to be tested against a total shareholder return (TSR) hurdle and Parcel B is to be tested against an earnings per share (EPS) hurdle. Performance against these hurdles is tested at the end of the performance period.

An explanation of how the TSR and EPS hurdles apply and when performance will be tested against those hurdles is set out below.

Parcel A - TSR hurdle

TSR measures the growth in the Company’s share price together with the value of dividends during the period, assuming that all those dividends are re-invested into new shares.

The comparator group comprises those entities within the S&P/ASX 100 Index as at 1 January 2012. The comparator group may be adjusted to take into account events including but not limited to takeovers, mergers, de-mergers or de-listings.

The share prices used to calculate the TSR of a company for the performance period will be measured as follows:

• theopeningsharepricewillbetheVWAPofthatcompany for the 20 trading days preceding (but not including) the first day of the performance period; and

• theclosingsharepricewillbetheVWAPofthatcompany for the 20 trading days ending on the last day of the performance period.

The percentage of Parcel A rights that vest (if any) at the end of the performance period will be determined by reference to the percentile ranking achieved by the Company over the performance period compared to the entities in the comparator group as follows:

TSR Percentile Ranking % of Parcel A that will vest

Below 51st percentile Nil

Equal to the 51st percentile 50%

Between the 51st and 75th percentile

Progressive pro-rata vesting from 50% to 100% (straight-line basis)

75th percentile or above 100%

All Parcel A rights that do not vest following testing of the TSR hurdle will lapse immediately.

Parcel B - EPS Hurdle

EPS measures the percentage earnings generated by the Company attributable to each share on issue. EPS will be calculated based on Net Profit After Tax (NPAT) for the relevant financial year, divided by the weighted average number of shares on issue during the year.

The growth in the Company’s EPS over the performance period will be measured in relation to a notional earnings base of $600 million NPAT (being $1.7830 NPAT per share as at 24 August 2011, based on there being 336,515,596 shares on issue).

The percentage of Parcel B rights that vest (if any) at the end of the performance period will be determined based on the performance achieved against the following hurdle, subject to any adjustments for abnormal or unusual profit items:

Compound annual growth in EPS over the performance period

% of Parcel B that will vest

Below 8% Nil

Equal to 8% 50%

Between 8% and 13% Progressive pro-rata vesting between 50% and 100% (straight-line basis)

13% or above 100%

All Parcel B rights that do not vest following testing of the EPS hurdle will lapse immediately.

11

Treatment of rights on cessation of employment

Subject to the Committee’s discretion to determine otherwise:

• wheretheExecutiveDirectorresignsortheiremployment is terminated by the Company for cause, all unvested LTI Rights will immediately lapse; or

• wheretheExecutiveDirector’semploymentisterminated for any other reason, a pro-rata portion of the unvested LTI Rights (based on how much of the performance period has elapsed) will remain on foot, subject to the original performance conditions and will be tested in the ordinary course. A cash payment will be made in respect of any LTI Rights that vest based on the performance achieved.

STI opportunities for the Executive Directors

Mr Tyrwhitt and Mr Gregg’s STI for 2012 will be determined by reference to the following categories of objectives:

• financialkeyperformanceindicators,whichwillgenerally relate to the financial performance of the Group as a whole; and

• personalobjectives,beinganumberofspecifickey performance indicators relating to matters which are generally within the Executive Directors’ influence.

Following the end of the financial year, performance against the objectives will be tested and an STI will be awarded to the extent that the objectives are satisfied.

Of the STI amount awarded:

• 50%willbedeliveredincash;and

• 50%willbedeferredintoSTIRightsfortwoyearsfrom 1 January 2013.

The number of STI Rights granted will be determined by dividing the relevant dollar amount (ie 50% of the STI award value) by the VWAP of ordinary shares of the Company traded on the ASX over the five trading days following the announcement of the final full-year financial results (excluding the date of announcement).

Timing of grant

If: • shareholderapprovalisobtained;and

• MrTyrwhittandMrGreggsatisfytheminimum

performance levers required to qualify for an STI award,

the STI Rights will be granted in early 2013 and, in any event, prior to 22 May 2013. If not approved, the remuneration intended to be provided by way of rights will instead be delivered in cash on terms equivalent to those set out below.

Treatment of rights on cessation of employment

Subject to the Committee’s discretion to determine otherwise:

• wheretheExecutiveDirectorresignsortheiremployment is terminated by the Company for cause, all unvested STI Rights will immediately lapse; or

• wheretheExecutiveDirector’semploymentisterminated for any other reason (including by way of a genuine retirement), it is intended that any unvested STI Rights will remain on foot until the end of the vesting period and a cash payment will be made in respect of any STI Rights that vest in accordance with the award terms.

Preventing inappropriate benefits

The Committee has a broad discretion to reduce or extinguish the Executive Directors’ entitlement to STI Rights in order to prevent the Executive Director from obtaining an inappropriate benefit. Circumstances in which the Committee could exercise this discretion include an adverse change in the Executive Director’s performance or the Group’s financial position, material misrepresentations or accounting errors, major negligence or reputational damage to the Group.

Shareholder approval

If shareholders do not approve the grant of STI Rights to Mr Tyrwhitt and/or Mr Gregg, the Company will defer payment of 50% of the relevant STI so that it is paid as a cash payment (instead of as an award of STI Rights) on terms consistent with those applicable to STI Rights.

Terms applying to all rights for the Executive Directors

Rights attaching to the rights

The rights do not carry any voting rights or entitlements to receive dividend payments during the vesting period. However, for any STI Rights that vest, the Executive Directors are entitled to receive a cash amount in lieu of any dividends that they would have received if they had enjoyed full rights of ownership in

respect of the underlying shares from the grant date to the vesting date. No dividend equivalent payment will be made for LTI Rights that vest.

In the event the Company makes a bonus issue or pro-rata rights issue to shareholders or undertakes a capital reorganisation, the Committee may make any adjustments it considers appropriate to the terms of the rights in order to minimise or eliminate any material advantage or disadvantage that arises as a result of such action.

Exceptional circumstances

In exceptional circumstances, the Committee may determine that some or all of an Executive Director’s unvested rights will vest before the end of the relevant performance period. The balance (if any) will remain on foot, subject to the existing performance conditions. The types of exceptional circumstances in which the Committee may exercise its discretion to accelerate vesting of the rights include:

• aprobableoractualchangeinthecontrolof the Company;

• theExecutiveDirectors’earningcapacitybeingdiminished due to injury, incapacitation or other health issue; and

• severefinancialhardshipaffectingtheExecutiveDirectors or their families.

No dealing of rights

Any dealing in respect of a right is prohibited unless the Committee determines otherwise or the dealing is required by law. ‘Dealing’ is defined broadly to include sales, transfers, assignments, options, swaps and hedges relating to a security.

Other information relating to the incentive grants to the Executive Directors

• MrTyrwhittandMrGreggaretheonlyDirectorsofthe Company entitled to participate in the Plan.

• ThereisnoloanschemeinrelationtothePlan.

• TherightswillbegrantedatnocosttoMrTyrwhitt and Mr Gregg, as they form part of their remuneration package.

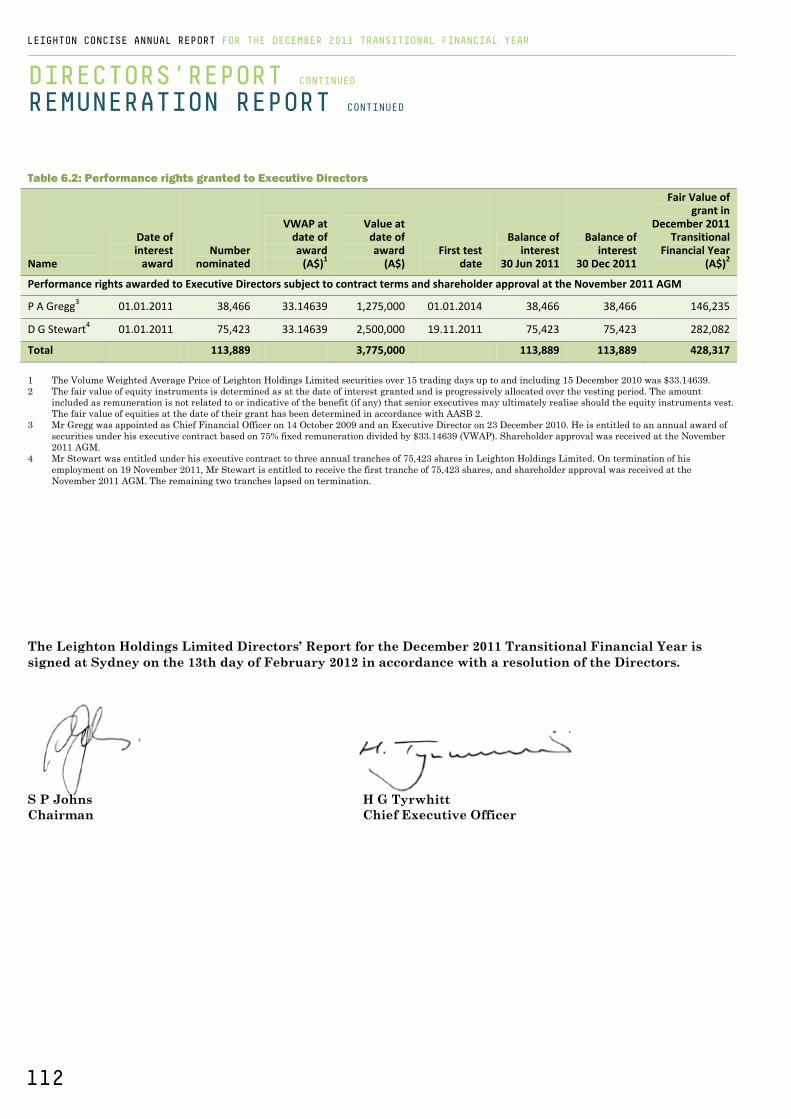

• Nosecuritieshaveasyetbeenreceivedbyparticipants under the Plan. Mr Gregg was granted 38,466 rights as his 2011 LTI award under and in accordance with his employment agreement upon shareholder approval being obtained at the 2011 Annual General Meeting. Further details regarding the rights previously awarded to Mr Gregg are provided in the Remuneration Report contained in the Company’s December 2011 Concise Annual Report.

Recommendation

The Board (with Mr Tyrwhitt and Mr Gregg abstaining) considers the grant of rights to the Executive Directors to be appropriate in all the circumstances and recommends that shareholders vote in favour of Resolution 6.1 and Resolution 6.2.

12

EXPLANATORY NOTES (continued)

LEIGHTON HOLDINGS LIMITED ABN 57 004 482 982

NOTICE OF ANNUAL GENERAL MEETING 2012

000001 000 LEI

MR SAM SAMPLEFLAT 123123 SAMPLE STREETTHE SAMPLE HILLSAMPLE ESTATESAMPLEVILLE VIC 3030

Lodge your vote:

Online:www.investorvote.com.au

By Mail:Computershare Investor Services Pty LimitedGPO Box 242 MelbourneVictoria 3001 Australia

Alternatively you can fax your form to(within Australia) 1800 783 447(outside Australia) +61 3 9473 2555

For Intermediary Online subscribers only(custodians) www.intermediaryonline.com

For all enquiries call:(within Australia) 1300 850 505(outside Australia) +61 3 9415 4000

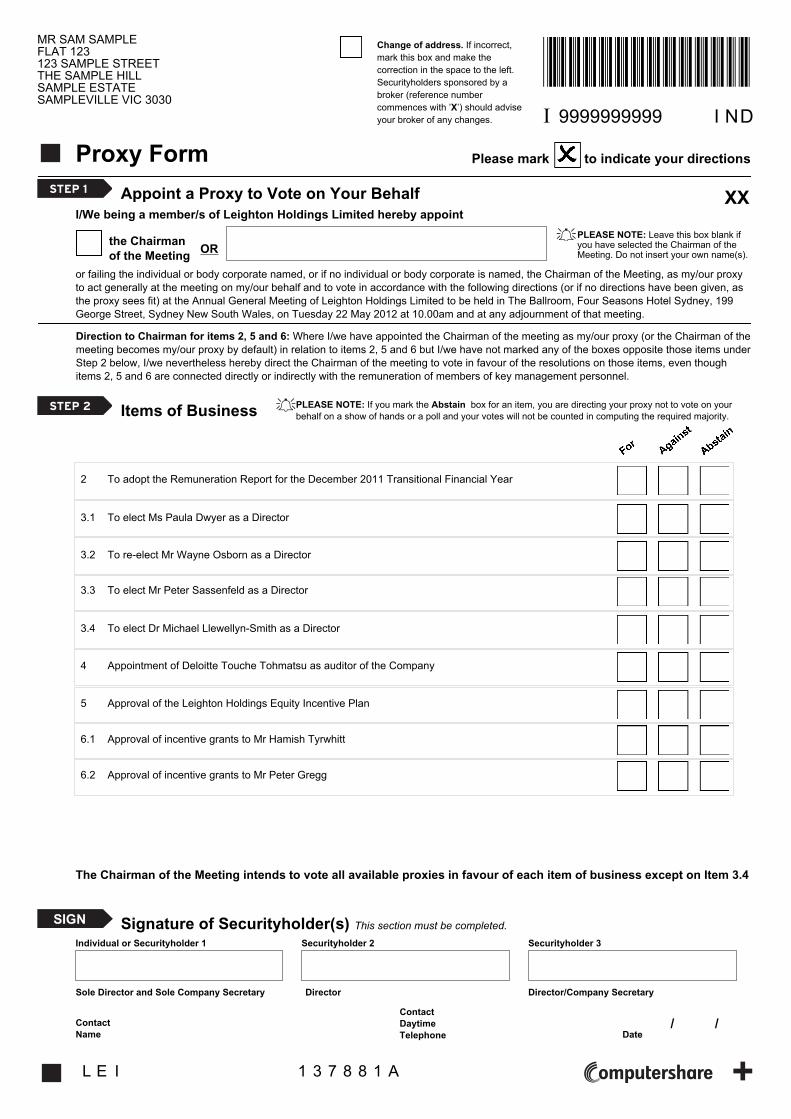

Proxy Form

For your vote to be effective it must be received by 10.00am (AEST) Sunday 20 May 2012

How to Vote on Items of BusinessAll your securities will be voted in accordance with your directions.

Appointment of Proxy Voting 100% of your holding: Direct your proxy how to vote by markingone of the boxes opposite each item of business. If you do not mark a boxyour proxy may vote as they choose (except in relation to items 2, 5 and 6where you have appointed a member of the key management personnel ofthe company or one of their closely related parties as your proxy, in whichcase there are additional restrictions explained below). If you mark more thanone box on an item your vote will be invalid on that item.Voting a portion of your holding: Indicate a portion of your voting rights byinserting the percentage or number of securities you wish to vote in the For,Against or Abstain box or boxes. The sum of the votes cast must not exceedyour voting entitlement or 100%.Appointing a second proxy: You are entitled to appoint up to two proxies toattend the meeting and vote on a poll. If you appoint two proxies you mustspecify the percentage of votes or number of securities for each proxy,otherwise each proxy may exercise half of the votes. When appointing asecond proxy write both names and the percentage of votes or number ofsecurities for each in Step 1 overleaf.A proxy need not be a securityholder of the Company.Default to the Chairman of the Meeting: Any directed proxies that are notvoted on a poll at the meeting will automatically default to the Chairman of theMeeting, who is required to vote proxies as directed.Proxy voting by key management personnel: The key managementpersonnel of Leighton Holdings Limited (which includes each of the directors)and their closely related parties will not be able to vote your proxy on items 2,5 and 6 unless you tell them how to vote. If you intend to appoint a member ofthe key management personnel or one of their closely related parties as yourproxy, please ensure that you direct them how to vote on items 2, 5 and 6. Ifyou intend to appoint the Chairman of the Meeting as your proxy, you candirect him how to vote by marking the boxes for items 2, 5 and 6. However, ifthe Chairman of the Meeting is your proxy and you do not mark any of theboxes opposite items 2, 5 and 6, you will be deemed to have directed theChairman to vote in favour of those items.

Signing Instructions for Postal FormsIndividual: Where the holding is in one name, the securityholder mustsign.Joint Holding: Where the holding is in more than one name, all of thesecurityholders should sign.Power of Attorney: To sign under Power of Attorney you must lodgethe Power of Attorney with the registrar by 10.00am (AEDT) Sunday 20May 2012. If you have not already lodged the Power of Attorney withthe registrar, please attach a certified photocopy of the Power ofAttorney to this form when you return it.Companies: Where the company has a Sole Director who is also theSole Company Secretary, this form must be signed by that person. Ifthe company (pursuant to section 204A of the Corporations Act 2001(Cth)) does not have a Company Secretary, a Sole Director can alsosign alone. Otherwise this form must be signed by a Director jointly witheither another Director or a Company Secretary. Please sign in theappropriate place to indicate the office held.

Attending the MeetingBring this form to assist registration. If a representative of a corporatesecurityholder or proxy is to attend the meeting you will need toprovide the appropriate “Certificate of Appointment of CorporateRepresentative” prior to admission. A form of the certificate may beobtained from Computershare or online at www.investorcentre.comunder the information tab, "Downloadable Forms".

Comments & Questions: If you have any comments or questions forthe company, please write them on a separate sheet of paper andreturn with this form.

GO ONLINE TO VOTE, or turn over to complete the form

Control Number: 999999

SRN/HIN: I9999999999 PIN: 99999

Leighton Holdings LimitedA.B.N 57 004 482 982

www.investorvote.com.auVote online or view the annual report, 24 hours a day, 7 days a week:

Cast your proxy vote

Access the annual report

Review and update your securityholding

Your secure access information is:

PLEASE NOTE: For security reasons it is important that you keep yourSRN/HIN confidential.

916CR_0_Sample_Proxy/000001/000001

*L000001*

Change of address. If incorrect,mark this box and make thecorrection in the space to the left.Securityholders sponsored by abroker (reference numbercommences with ’X’) should adviseyour broker of any changes.

Proxy Form Please mark to indicate your directions

Appoint a Proxy to Vote on Your BehalfI/We being a member/s of Leighton Holdings Limited hereby appoint

STEP 1

the ChairmanOR

PLEASE NOTE: Leave this box blank ifyou have selected the Chairman of theMeeting. Do not insert your own name(s).

or failing the individual or body corporate named, or if no individual or body corporate is named, the Chairman of the Meeting, as my/our proxyto act generally at the meeting on my/our behalf and to vote in accordance with the following directions (or if no directions have been given, asthe proxy sees fit) at the Annual General Meeting of Leighton Holdings Limited to be held in The Ballroom, Four Seasons Hotel Sydney, 199George Street, Sydney New South Wales, on Tuesday 22 May 2012 at 10.00am and at any adjournment of that meeting.

STEP 2 Items of Business PLEASE NOTE: If you mark the Abstain box for an item, you are directing your proxy not to vote on yourbehalf on a show of hands or a poll and your votes will not be counted in computing the required majority.

SIGN Signature of Securityholder(s) This section must be completed.

Individual or Securityholder 1 Securityholder 2 Securityholder 3

Sole Director and Sole Company Secretary Director Director/Company Secretary

ContactName

ContactDaytimeTelephone Date

The Chairman of the Meeting intends to vote all available proxies in favour of each item of business except on Item 3.4

of the Meeting

*I9999999999*I 9999999999 I ND

L E I 1 3 7 8 8 1 A

MR SAM SAMPLEFLAT 123123 SAMPLE STREETTHE SAMPLE HILLSAMPLE ESTATESAMPLEVILLE VIC 3030

/ /

XX

To adopt the Remuneration Report for the December 2011 Transitional Financial Year

To elect Ms Paula Dwyer as a Director

To re-elect Mr Wayne Osborn as a Director

To elect Mr Peter Sassenfeld as a Director

2

3.1

3.2

3.3

Direction to Chairman for items 2, 5 and 6: Where I/we have appointed the Chairman of the meeting as my/our proxy (or the Chairman of themeeting becomes my/our proxy by default) in relation to items 2, 5 and 6 but I/we have not marked any of the boxes opposite those items underStep 2 below, I/we nevertheless hereby direct the Chairman of the meeting to vote in favour of the resolutions on those items, even thoughitems 2, 5 and 6 are connected directly or indirectly with the remuneration of members of key management personnel.

To elect Dr Michael Llewellyn-Smith as a Director

Appointment of Deloitte Touche Tohmatsu as auditor of the Company

3.4

4

Approval of incentive grants to Mr Hamish Tyrwhitt6.1

Approval of the Leighton Holdings Equity Incentive Plan5

Approval of incentive grants to Mr Peter Gregg6.2

2

LEIGHTON HOLDINGS LIMITEDABN 57 004 482 982

CONCISE ANNUAL REPORTfOR THE DECEMBER 2011 TRANSITIONAL fINANCIAL YEAR

2011DECEMBER

LEIGHTON CONCISE ANNUAL REPORT fOR THE DECEMBER 2011 TRANSITIONAL fINANCIAL YEAR

Leighton is a strong company with an exciting future. Our businesses are in growth markets in many of the fastest developing regions in the world. We are the 11th largest global contractor* and the world’s largest contract miner. Our solid track record over more than 60 years has been built on a foundation of core values of discipline, integrity, safety and success, and a policy of empowerment of our people. In 2011, we faced serious challenges. The Leighton Group has since rebounded strongly, demonstrating that we are back on track to deliver attractive returns to our shareholders. We are well positioned to meet the challenges and volatility of the global environment.

* Engineering News Record 29 August 2011

1

NOTICE OF ANNUAL GENERAL MEETING 2012LEIGHTON HOLDINGS LIMITED ABN 57 004 482 982To: The ShareholdersNotice is hereby given that the 51st Annual General Meeting of the members of Leighton Holdings Limited will be held in the: Grand Ballroom, The Four Seasons Hotel 199 George Street, Sydney, New South Wales on Tuesday 22 May 2012 at 10.00 am.

A separate Notice of Meeting and Proxy Form are enclosed. During the course of the meeting, a short presentation on the Group’s operations will be given by Mr Hamish Tyrwhitt, Chief Executive Officer. All present are invited to join the Directors for light refreshments after the meeting.

This document is available in PDF format online at Leighton Holdings’ website www.leighton.com.au

Shareholder Updates can also be downloaded from the company’s website. Printed copies of corporate brochures can also be obtained on request: Phone +612 9925 6636Email [email protected]

Geo

rge

St

Bridge StGrosvenor St

Jamison St

Dalley St

Bent St

Har

ringt

on S

t

Glo

uces

ter S

t

Cum

berla

nd S

tB

radfi

eld

Hw

y Argyle St

Cahill Expressway

Alfred St

Reiby Pl

Loftu

s St

Pitt

St

Youn

g St

The Four Seasons Hotel

The Rocks

Sydney CBD

Circular Quay

LEIGHTON CONCISE ANNUAL REPORT fOR THE DECEMBER 2011 TRANSITIONAL fINANCIAL YEAR

2

NOTICE OfMEETING

3

CONTENTS

1 Overview 2 Notice of Meeting 4 A leading international contractor 6 Highlights 8 Chairman’s review 12 Vision & values – refreshed & energised 16 Chief Executive’s review 28 How we operate 30 Operational analysis & investments

32 Board & Senior Management 34 Directors’ resumes 41 Group Executives

42 Corporate Governance Report 44 Governance at Leighton 44 Principle 1: Lay solid foundation for management and oversight 47 Principle 2: Structure the Board to add value 51 Principle 3: Promote ethical and responsible decision-making 53 Principle 4: Safeguard integrity in financial reporting 54 Principle 5: Make timely and balanced disclosure 54 Principle 6: Respect the rights of shareholders 55 Principle 7: Recognise and manage risk 57 Principle 8: Remunerate fairly and responsibly

58 Directors’ Report 75 Remuneration Report

113 Concise Financial Report 114 Consolidated Income Statement 115 Consolidated Statement of Comprehensive Income 116 Consolidated Balance Sheet 117 Consolidated Statement of Changes in Equity 118 Consolidated Statement of Cash Flows 119 Notes to the Concise Financial Report

128 Statutory Statements and Shareholder Information 130 Directors’ Declaration and Auditor’s Report 132 Shareholdings 133 Shareholder information

134 5 Year statistical summary

136 Directory and offices

China

Indonesia

India

Sri Lanka

Hong Kong

Macau Taiwan

Thailand

Philippines

Cambodia

Laos

Malaysia Brunei

Mongolia

Vietnam

Singapore

Botswana

Saudi Arabia

Iraq

BahrainKuwait

Oman

United ArabEmiratesQatar

Papua New Guinea

NewZealand

Australia

A LEADING INTERNATIONAL CONTRACTOR

WHO WE ARELeighton was founded in 1949, listed on the Australian Securities Exchange in 1962 and is based in Sydney, Australia. The Group comprises nine brands, our Operating Companies: Thiess, Leighton Contractors, John Holland, Leighton Properties, Leighton Asia, Leighton Offshore, Leighton Welspun, Habtoor Leighton Group and Leighton Africa. Some of these Operating Companies have been in existence since the 1930s. Our people are our business. We employ more than 53,000 people whose activities are underpinned by our values of discipline, integrity, safety and success. To attract, retain and motivate the best people they must be empowered. People perform their best when they are provided with realistic goals and a clear framework in which to operate. When empowered and accountable, people step up, accepting responsibilities and delivering results. This is the Leighton way. This empowerment occurs within a corporate governance framework defined by Leighton Holdings, which sets standards for ethical and financial performance, health, safety and rehabilitation, and diversity, community and environmental matters.

WHAT WE DOAs a strategic management company, Leighton Holdings provides a robust corporate governance structure, strategic leadership and the financial strength to enable our Operating Companies to compete effectively in the global market place. This role includes:

• setting the vision, values and strategic direction;• setting Group policies and operating guidelines; • maintaining the highest standards of discipline, integrity,

safety and success; • ensuring strict adherence to our Code of Ethics; • reviewing risk management and performance; and • approving acquisitions, investments and development

initiatives. The leadership of an experienced management team and a strong balance sheet support the growth of our Operating Companies. The Operating Companies offer a broad range of contracting and project development services and skills to public and private sector clients across a wide range of industries and geographic locations. These skills include construction, contract mining, operations and maintenance and development services to the infrastructure, resources and property markets. Leighton Holdings is focused on sustainability and the pursuit of excellence in creating solutions for our clients, safe, rewarding and fulfilling careers for our people, and superior and sustainable returns for our shareholders.

The Leighton Group is one of the world’s leading international contractors. We operate in more than 25 countries in Asia, the Middle East, Southern Africa and throughout Australia. We aim to be renowned for excellence through our operating brands and the empowerment of our people.

LEIGHTON CONCISE ANNUAL REPORT fOR THE DECEMBER 2011 TRANSITIONAL fINANCIAL YEAR

4

China

Indonesia

India

Sri Lanka

Hong Kong

Macau Taiwan

Thailand

Philippines

Cambodia

Laos

Malaysia Brunei

Mongolia

Vietnam

Singapore

Botswana

Saudi Arabia

Iraq

BahrainKuwait

Oman

United ArabEmiratesQatar

Papua New Guinea

NewZealand

Australia

Leighton Group Operations

WHERE WE AREThe Leighton Group’s Operating Companies conduct business in more than 25 countries. While the listed entity is based in Australia, our Operating Companies have been operating internationally for many years. A strategic move into Asia culminated in the formation of Leighton Asia in 1975. Through the 1980s, 1990s and 2000s, Leighton Asia continued to diversify throughout East and South-East Asia. In 2004, we opened offices in India and the Middle East. The Group took a major step in 2007 with the acquisition of a 45% stake in the UAE and Qatar-based Al Habtoor Engineering, one of the largest contractors in the Middle East. This was renamed the Habtoor Leighton Group in 2007 and has since expanded to Saudi Arabia, Oman, Kuwait and Bahrain. In 2007, Leighton Asia opened its first office in Mongolia, and by 2011 the Group had ventured into Southern Africa. Leighton’s strategy has positioned the Group in prime locations – Australia, Asia, the Middle East and Southern Africa – through operating brands that are highly regarded. Today, the Leighton Group has the broadest footprint of any international contractor in the regions that are poised to provide the greatest share of the world’s economic growth over the next 20 years.

5

6

LEIGHTON CONCISE ANNUAL REPORT fOR THE DECEMBER 2011 TRANSITIONAL fINANCIAL YEAR

HIGHLIGHTS

Total revenue#

6 months to 31 Dec 2011

$12.2 billion

Work in hand#

as at 31 Dec 2011

$44.6 billion

Profit / (loss) before tax6 months to 31 Dec 2011

$475.4 million

Profit / (loss) after tax6 months to 31 Dec 2011

$340.0 million

6 months to 6 months to 12 months to 31 Dec 2011 31 Dec 2010 30 Jun 2011PROFIT & LOSS ITEMS $million $million Change $millionRevenue – Group 10,169.2 7,370.6 +38% 15,561.3 – Joint ventures and associates 2,007.7 2,338.5 -14% 3,815.4Total revenue# 12,176.9 9,709.1 +25% 19,376.7

EBITDA (post sales and impairments) 1,111.6 865.1 +28% 534.9Depreciation of property, plant and equipment (512.7) (448.4) +14% (865.6)Amortisation of intangibles (33.0) – n/a (0.6)EBIT 565.9 416.7 +36% (331.3)Finance costs (90.5) (92.2) -2% (159.6)Profit/(loss) before tax 475.4 324.5 +47% (490.9)Income tax (expense)/benefit (130.5) (106.2) +23% 85.2Profit/(loss) after tax 344.9 218.3 +58% (405.7)Profit/(loss) attributable to minority interests (4.9) (1.5) +226% 3.1Profit/(loss) attributable to members 340.0 216.8 +57% (408.8)

EPS AND DPSEarnings per ordinary share 101.0¢ 72.0¢ +40% (133.1¢)Dividends per ordinary share 60.0¢ 60.0¢ nil 60.0¢

NEW CONTRACTS & WORk IN HAND (BACkLOG)New contracts, extensions & variations 10,054.0 16,053.8 -37% 26,065.0Value of work in hand at end of period# 44,559.7 45,641.5 -2% 46,225.8

As at 31 Dec 2011 As at 30 Jun 2011 BALANCE SHEET ITEMS $million $million ChangeTotal capital and reserves 2,766.9 2,319.9 +19%Total assets 9,900.4 9,800.2 +1%Cash and cash equivalents 1,503.2 1,414.7 +6%Interest bearing liabilities 2,143.7 1,826.5 +17%Undrawn loan and guarantee facilities (excl. Devine) 1,163.9 1,191.7 -2%Gearing (including operating leases)^ 32% 35% n/a# Includes the Group’s share of joint ventures and associates. ^ Gearing expressed as: net debt including operating leases to net debt including operating leases plus total equity.

475.

4

340.

0

12.2

44.6

Dec

07

Jun

08

Dec

08

Jun

09

Dec

09

Jun

10

Dec

10

Jun

11

Dec

11

Dec

07

Jun

08

Dec

08

Jun

09

Dec

09

Jun

10

Dec

10

Jun

11

Dec

11

Dec

07

Jun

08

Dec

08

Jun

09

Dec

09

Jun

10

Dec

10

Jun

11

Dec

11

Dec

07

Jun

08

Dec

08

Jun

09

Dec

09

Jun

10

Dec

10

Jun

11

Dec

11

7

6 months to 6 months to 12 months to SAFETy* 31 Dec 2011 31 Dec 2010 Change 30 Jun 2011Fatalities (Australia) 2 1 +100% 1Fatalities (international) 1 1 nil 3TRIFR (Australia)1 14.4 16.1 -11% 15.6TRIFR (international)1 3.2 3.5 -9% 3LTIFR (Australia)2 1.6 1.8 -11% 1.8LTIFR (international)2 0.4 0.8 -50% 0.6Potential class 1 (Australia)3 200 229 -13% 454Potential class 1 (international)3 49 63 -22% 100Actual class 1 (Australia) 2 1 +100% 2Actual class 1 (international) 3 5 -40% 7

ENvIRONMENT# Actual environmental level 1 (Australia)4 0 2 -100% 2Actual environmental level 1 (international)4 0 0 nil 0EIFR (Australia)5 0.28 0.22 +27% 0.43EIFR (international)5 0.02 0.08 -75% 0.05

COMMUNITy Corporate Community Investment $2.64m No data n/a $7.89m

WORkFORCE* As at 31 Dec 2011 As at 31 Dec 2010 Change As at 30 Jun 2011Number of direct employees (total) 53,113 49,802 +7% 51,281Female participation (Australia) 16.7% 15.0% +11% 16.1%Female participation (international) 7.0% 7.8% -10% 8.0%Indigenous participation (Australia) 1.3% 1.5% -13% 1.5%Local participation (international)6 56.6% No data n/a No data* Excludes Leighton Middle East & Africa (comprising Habtoor Leighton Group, Leighton Africa and Thiess Services).# Excludes Habtoor Leighton Group. 1 Total recordable injury frequency rate (per million hours worked).2 Lost time injury frequency rate (per million hours worked).3 Class 1 risks are those which could cause a fatality or permanent disabling injury.4 Level 1 environmental incidents are those with highly detrimental impacts on the environment, community and/or company including irreversible and long-term environmental, cultural,

heritage or reputational damage, breaches of statutory or approval conditions with serious legal or contractual consequences, or those with total cleanup costs in excess of $100,000.5 Environmental incident frequency rate (Level 1 and 2) per million hours worked.6 Local participation refers to percentage of locally employed staff in our international operations. Local participation rate not measured prior to 1 July 2011.

Corporate Community Investment

6 months to 31 Dec 2011

$2.64 million

2.64

07/0

8

08/0

9

09/1

0

10/1

1

Dec

11

Number of fatalities 6 months to 31 Dec 2011

3

3

Dec

07

Jun

08

Dec

08

Jun

09

Dec

09

Jun

10

Dec

10

Jun

11

Dec

11

Number of direct employeesas at 31 Dec 2011

53,113

53,1

13

Dec

07

Jun

08

Dec

08

Jun

09

Dec

09

Jun

10

Dec

10

Jun

11

Dec

11

Total level 1 environmental incidents

6 months to 31 Dec 2011

nil

nil

Dec

07

Jun

08

Dec

08

Jun

09

Dec

09

Jun

10

Dec

10

Jun

11

Dec

11

In my report to you last year, I said that we had tackled the serious challenges we faced head on, and that the business was now well positioned for the next phase of strong growth and development. In this report, you will see that we have delivered on that promise. The Leighton Group has demonstrated its underlying strength by generating strong performances across our core construction and mining operations in Australia and Asia. We have reported a solid operating profit supplemented by a capital gain from the sale of the HWE Mining iron ore business.

Stephen Johns Chairman

CHAIRMAN’S REvIEw

LEIGHTON CONCISE ANNUAL REPORT fOR THE DECEMBER 2011 TRANSITIONAL fINANCIAL YEAR

8

9

The Leighton Group has rebounded strongly to record a net profit after tax of $340 million for the 6 month period to 31 December 2011. This result includes a capital gain from the sale of the HWE Mining iron ore business, and impairments to the carrying values of BrisConnections – the listed toll road owner in Brisbane – and the Habtoor Leighton Group.

This result demonstrates the underlying strength of the business, the capability and commitment of our people and the effectiveness of our strategies.

During this 6 month period we have:• renewed our vision and values to ensure they are aligned with

our shareholders, clients and employees as we look to the next exciting phase of our development;

• made significant improvements to the Group’s approach to risk management; and

• revised the Group’s remuneration and incentive arrangements following engagement with many of our stakeholders.

DIvIDENDS AND RETURNS TO SHAREHOLDERSInvestment returns for shareholders are a combination of share price performance and dividends. I am pleased to report that following our return to profitability we have restored the payment of dividends to shareholders.

Your directors announced an unfranked final dividend of 60 cents per share for the period. This represents a payout ratio of almost 60% of the Group’s reported net profit after tax. While the dividend rate is the same as that paid to shareholders for the 6 months ended 31 December 2010, the total payout is greater as a consequence of the Group’s larger capital base following the capital raising in April 2011.

THE OPERATING ENvIRONMENTWhile growth in the developed economies of Europe and the United States is likely to be less than 2% this year, in Asia (where the Leighton Group has substantial operations) growth is expected to exceed 7%. This growth continues to be fuelled by urbanisation and industrialisation, creating demand for energy, infrastructure, commercial and domestic buildings, and commodities.

Australia, our home market, remains one of the best performing economies in the developed world, with growing global demand for energy, iron ore and other commodities significantly increasing investment in resource projects and accompanying infrastructure.

We are well positioned to meet the challenges and volatility of the global environment.

FINANCIAL STRENGTHDespite the ongoing uncertainty in the global financial markets, at year end the Group had a solid capital base with $2.8 billion of shareholders’ equity and $9.9 billion of total assets. At balance date we retained $1.5 billion in cash on hand and had undrawn bank facilities of $856 million.

Gross debt, including recourse and non-recourse loans, stood at $2.1 billion at 31 December 2011. The maturity profile of this debt has remained relatively long-term in nature. $670 million of loans and other facilities fall due within the next 12 months. Negotiations are well advanced for refinancing the majority of these facilities, with the remainder budgeted to be repaid at maturity.

Gearing, including operating leases, decreased from 35% at 30 June 2011 to 32% at 31 December 2011, below the Group’s targeted range of 35% to 45%. This additional debt capacity, together with the aforementioned cash on hand, highlights the financial strength of the Leighton Group.

During the period Standard & Poor’s downgraded our credit rating from ‘BBB/A-2’ to ‘BBB-/A-3’, and Moody’s lowered our corporate credit rating to ‘Baa2 stable’ outlook from ‘Baa1 negative’ outlook. It is important to note that these changes do not impact existing credit facilities and we strongly believe that these new ratings are not a true reflection of the Group’s credit quality.

In September 2011, Leighton successfully closed a US$600 million syndicated Master Lease Facility. The new 6-year facility streamlines our existing Indonesian leasing arrangements and provides the Group’s two operating subsidiaries in Indonesia with additional capacity to fund their expanding Indonesian mining activities. →

10

SAFETy AND SUSTAINABILITySafety is a core value that is demonstrated through the Group’s commitment to the elimination of fatalities and permanent disabling injuries, and the significant reduction of all other injuries across our operations. We are also committed to zero environmental incidents.

I am therefore deeply saddened to report that there were three fatalities in the 6 months to 31 December 2011. I would like to acknowledge those of our colleagues who lost their lives. On behalf of the Board, I extend our deepest sympathies to their families and friends.

We have stepped up our application of “hard” engineering controls to seek to ensure that there are no further fatalities and no serious injuries. Further details of the Group’s performance and approach to safety are set out in the Directors’ Report starting on page 58 of this Concise Annual Report.

This year we also focused on the following key sustainability areas:

• workplace diversity, with a specific emphasis on gender diversity among senior management;

• the environment; and • community investment.

In line with the ASX Corporate Governance Council’s Principles and Recommendations on diversity, the Board has committed to measurable diversity targets. Further information in relation to the Group’s commitment to workforce diversity is contained in the Corporate Governance Report starting on page 42 of this Concise Annual Report.

REMUNERATIONAs I foreshadowed at the Annual General Meeting in November 2011, the Board has conducted a comprehensive review of executive remuneration and incentives over recent months. The review has included consultation with shareholders, external stakeholders and independent advisers.

The revised remuneration and incentive scheme is underpinned by a number of principles which include:

• an increase in variable rather than fixed remuneration based on performance, including the forfeiture of unvested incentives in appropriate circumstances;

• an increased focus on long-term rather than short-term incentives;

• a greater proportion of total remuneration to be paid in shares rather than cash; and

• alignment of total remuneration with the market so that we can continue to attract and retain the highest quality executives.

WORk IN HANDWork in hand stands at close to record levels. This reflects continuing strong market conditions which are providing the Group with numerous tendering opportunities. We have adopted a highly considered approach when taking on new work. We are selectively pursuing volume that delivers superior profit through a highly disciplined and structured approach to tendering. Our primary focus is to ensure we bid on projects that are expected to deliver an appropriate risk-adjusted return to shareholders.

Work in hand at 31 December 2011 was $44.6 billion, with 64% from the Australia/Pacific region and 36% from international markets. Work in hand is 3% lower than the $46.2 billion recorded at 30 June 2011 and 2% lower than the $45.6 billion reported at 31 December 2010.

The Group’s margin in hand at the project level – which reflects the inherent profit in work in hand – remains at around 11%, supporting a very positive outlook.

During the period, we won around $6.2 billion worth of new contracts and $3.9 billion in extensions and variations.

The Group has an additional $12.4 billion worth of work in mining and services contracts extending beyond five years that is not reflected in the aforementioned work in hand.

We are currently tendering for around $30 billion worth of work. This demonstrates the strength of our operating environment.

SALE OF HWE MINING IRON ORE BUSINESSIn September 2011, the Group sold its HWE Mining iron ore entities and assets to BHP Billiton for $452 million, resulting in a pre tax gain of $229 million and an after tax gain of $167 million. The sale reflected BHP Billiton’s publicly stated intention to transition to an owner operator model, and the sale of the Pilbara-based iron ore assets represented a positive result for both parties. We have been able to recycle capital with the transaction generating net cash flow of approximately $400 million.

CHAIRMAN’S REvIEw CONTINUED

LEIGHTON CONCISE ANNUAL REPORT fOR THE DECEMBER 2011 TRANSITIONAL fINANCIAL YEAR

11

The details of the revised remuneration and incentive scheme, including certain transitional arrangements, are set out in the Remuneration Report starting on page 75 of this Concise Annual Report. Any necessary shareholder approvals for these plans will be sought at the next Annual General Meeting which will be held on 22 May 2012.

The Board believes that the revised remuneration and incentive scheme reflects a best practice approach. It achieves our objective of ensuring that we have in place a remuneration and incentive framework to drive performance and behaviours aligned to the long term interests of our shareholders, while providing appropriate rewards for our executives in a competitive environment.

THE BOARD AND SENIOR MANAGEMENTIn the last Concise Annual Report, I reported on important management and Board changes, including my appointment as Chairman and the appointment of our CEO, Hamish Tyrwhitt. The Board is encouraged by the strategic vision and leadership that Hamish is providing.

The Board has moved to fill two vacancies. Mr Peter Sassenfeld, recently appointed as CFO of HOCHTIEF AG, has joined the Board as a Non-executive Director. In addition, Ms Paula Dwyer has been appointed as a Non-executive Director and Chairman of the Audit Committee. Further details of each of their experience and backgrounds are set out on pages 35 and 37 of this Concise Annual Report.

The Board has recently established a Tender Review and Risk Committee comprised solely of Non-executive Directors. The Committee is responsible for monitoring and reviewing the integrity, adequacy and utility of the Group’s risk management systems, controls and metrics. The Committee has oversight of tenders for all key projects or those projects which are considered `high risk’. This is an important initiative for monitoring and reporting on the tendering and risk management practices throughout the Group’s operations.

CODE OF ETHICSThe Board is firmly of the view that the reputation and integrity of the Group will only be maintained if all of its officers and employees observe the highest standards of conduct, and these are set out in our Code of Ethics.

It is therefore extremely disappointing that, as set out in our announcement on 13 February 2012, we have reported to the Australian Federal Police a possible breach of our Code of Ethics in relation to payments that may have been made in connection with work to expand the offshore loading facilities for Iraq’s crude oil exports. We are fully cooperating with the Australian Federal Police as they conduct their investigation, which is still at an early stage.

Observance of our Code of Ethics by all of our people is essential and the Board does not tolerate anything other than the strictest adherence to our Code.

OUTLOOkThe Group’s outlook is positive based on a near record level of work in hand, a solid balance sheet and favourable market conditions. We have rebounded strongly from a disappointing financial year to 30 June 2011 to report a solid level of profitability during the 6 month period to 31 December 2011. This establishes an excellent platform for the future profitability and growth for the Leighton Group.