africa s business revolution

TRANSCRIPT

AFRICA’S BUSINESS

REVOLUTION

HOW TO SUCCEED IN THE WORLD’S

NEXT BIG GROWTH MARKET

BY ACHA LEKE, MUTSA CHIRONGA,

AND GEORGES DESVAUX

Contents

Figure P-1 3

Figure 1-1 4

Figure 1-2 5

Figure 1-3 6

Figure 1-4 7

Figure 1-5 8

Figure 2-1 9

Figure 2-2 10

Figure 2-3 11

Figure 2-4 12

Figure 2-5 13

Figure 3-1 14

Figure 3-2 15

Figure 3-3 16

Figure 4-1 17

Figure 5-1 18

Figure 5-2 19

Figure 6-1 20

Figure 6-2 21

Figure 6-3 22

Figure 6-4 23

FM.indd Page x 29/11/18 1:59 PM

African countries with over40 million citizens in 2017,millions of people

AlgeriaEgypt SudanUgandaEthiopia KenyaTanzaniaDRC S. AfricaNigeria

189

93 92 87

5750 47 42 42 41

African countries by population in 2017,millions of people

*Data for Somalia and South Sudan from the World Bank. Other country data on mapcame from the UN.

Source: United Nations World Population Prospects; World Bank; International MonetaryFund; World Economic Outlook Database, April 2017.

Morocco

Senegal

CaboVerde

EritreaDjibouti

Tunisia

Cameroon

Congo

EquatorialGuinea

Benin

Togo Gabon

CentralAfrican Rep.

Somalia*

UgandaRwandaBurundi

Madagascar

Swaziland

Lesotho

Namibia

AngolaComoros

Mauritius

Seychelles

Mozambique

Malawi

Zambia

Zimbabwe

Botswana

Libya

Chad

South Sudan*

Niger

BurkinaFaso

Ghana

Guinea

Côted'Ivoire

LiberiaSierra Leone

Guinea-BissauThe Gambia

MauritaniaMali

Egypt

Sudan

Ethiopia

Kenya

Tanzania

DemocraticRepublic

of the Congo(DRC)

SouthAfrica

Nigeria

Algeria

<10 10–40 >40

São Toméand Príncipe

Africa’s 54 countries are home to 1.2 billion people

FIGURE P-1

3

Chapter_01.indd Page 10 27/08/18 9:39 PM

The numbers highlight Africa’s acceleration—andthe opportunity for business

trillion dollars in projectedconsumer and businessspending by 2025

FIGURE 1-1

5.6billion people—with population expectedto double by 2050

1.2

89

54potential growth in manufacturing output by 2025

2x

million square miles ofland—three times thatof Europe

11companies with annual revenues of $1 billionor more

400

million active users of mobile �nancial services

122cities of over 1 millioninhabitants by 2030

countries expected to create the world’s largest free trade area

4

Chapter_01.indd Page 13 27/08/18 9:39 PM

Among respondents to our Africa business survey, Africa-basedcompanies are especially bullish.

Most companies see Africa as a major growth market

FIGURE 1-2

Of the following scenarios in Africa over the next 20 years,which do you believe are likely to occur? % of respondents*

African All other African All other

What changes do you expect for your organization in Africain the next five years? % of respondents*

Increase in number ofcountries where theorganization operates

Increase in revenuefrom Africa

Increase in workforcesize in Africa

African All other African All other

89

76

African All other

72

49 4958

Africa’s educational performance has improvedsignificantly, due to digital technologies and otherinvestments.

Most African households have joined the consumer class.

Africa’s combined GDP is one of the fastest-growing in the world.

New investments in Africa’s mineral resources have contributed significantly to the continent’s economic growth.

85

65

African All other

62

50

African All other

65

54

6663

*Total respondents = 1,025 (respondents from Africa = 253; from all other regions = 772).

Source: Mckinsey Insights executive survey on business in Africa, 2017.

5

Chapter_01.indd Page 19 27/08/18 9:39 PM

Africa’s 700 largest companies earn a combined$1.4 trillion in revenues

Source: MGI African companies database; McKinsey Global Institute analysis.

13>$10 billion

Number of companies Total revenue*Revenue size

42$5 billion–$10 billion

341$1 billion–$5 billion

296$500 million–$1 billion

200

703

284

261

$ billion

Companieswith >$1 billionrevenue

396companies

$1.2 trillion revenue

Total 692companies

$1.4 trillionrevenue

Breakdown of companies by revenue size, April 2016

*2014 or most recent data.

FIGURE 1-3

6

Chapter_01.indd Page 21 27/08/18 9:39 PM

Nearly half of Africa’s big firms are based in South Africa

Source: MGI African companies database; McKinsey Global Institute analysis.

*Regional definition from the African Development Bank; 2014 or most recent data.

Note: Includes multinational corporations with local branches registered in Africa; does notinclude those based outside of Africa.

North Africa 133

East Africa 25

West Africa 40

Nigeria 56

Southern Africa 43

Central Africa 19

South Africa 300

North

South Africa West Central

EastSouthern

49 22 7 6 4 3

North Africa

West Africa East Africa

Central Africa

Nigeria

Southern Africa

SouthAfrica

Nigeria

9

Companies with more than $500 million in revenue, by region, 2014,*number of companies

Regional share of Africa’s total, %

FIGURE 1-4

7

Chapter_01.indd Page 32 27/08/18 9:39 PM

How to win in Africa

Set a clear aspiration for growth

Prioritize the markets that matter most

De�ne how you’ll achieve scale and relevance

Build the ecosystem you need to thrive

Map your Africastrategy4 navigation tools:

Innovate yourbusiness model4 innovation practices:

Build vocational skills for frontline workers

Create robust processes to grow talent from within

Harness the power of inclusion—particularly women’s advancement

Unleash Africa’stalent3 talent imperatives:

Do wellby doing good

Solve Africa’s unmet needs to drive

pro�table,sustainable

growth

Take a long-term view—and ride out short-term volatility

Diversify to build a balanced portfolio

Integrate up and down your value chain

Understand local context and engage with governments

Build resiliencefor the long term4 cornerstones:

Create products and services that ful�ll Africa’s unmet needs

Rethink your business model to truly engage with customers

Get lean to drive down cost and price points

Harness technology to unleash the next wave of innovation

FIGURE 1-5

8

Chapter_02.indd Page 39 29/08/18 12:41 AM

Megatrends create big opportunities for business

In our Africa business survey, digitization, consumer, and infrastructurestand out.

What trends and/or forces do you expect to be the biggest growthopportunities in Africa over the next 20 years?* % of respondents,n = 792

Source: McKinsey Insights executive survey on business in Africa, 2017.

Increasing adoption of mobile and/or digital technologies

Growing demand for basic services (e.g., education, health care)

Demand for new or improved infrastructure

Rise in consumer spending

Rapid urbanization

Africa’s growing workforce

Increasing use of renewable energy

Potential to increase agricultural production

Abundance of mineral resources

Rise in spending by businesses

*Respondents who answered “other” or “don’t know/not applicable” are not shown.Question was asked only of respondents who said they have been to at least one countryin Africa, for either personal or business reasons, and who said 5 percent or more of theirorganizations’ current revenue is earned in Africa.

38

37

37

35

29

19

19

18

16

12

FIGURE 2-1

9

Chapter_02.indd Page 42 29/11/18 2:03 PM

Africa’s cities are growing rapidly

African cities by population,millions of people

African cities bypopulation, number

Source: United Nations World Population Prospect, June 2014 revision, UN populationdivision; MGI Cityscope; McKinsey Global Institute analysis.

1+ million

2015

546

3

2030 2015 2030

2015 2030

5+ million

10+ million

89

17

*Greater Johannesburg includes the City of Johannesburg, Ekurhuleni, and the West Rand.

5

Alexandria

20302015

Cairo

KhartoumKano

DakarOuagadougou

Abidjan

Bamako

Lagos

Kinshasa

Yaoundé

Ibadan

Luanda

Nairobi

Addis Ababa

Antananarivo

GreaterJohannesburg*

5 million–10 million

>10 million

FIGURE 2-2

10

Chapter_02.indd Page 51 29/08/18 12:41 AM

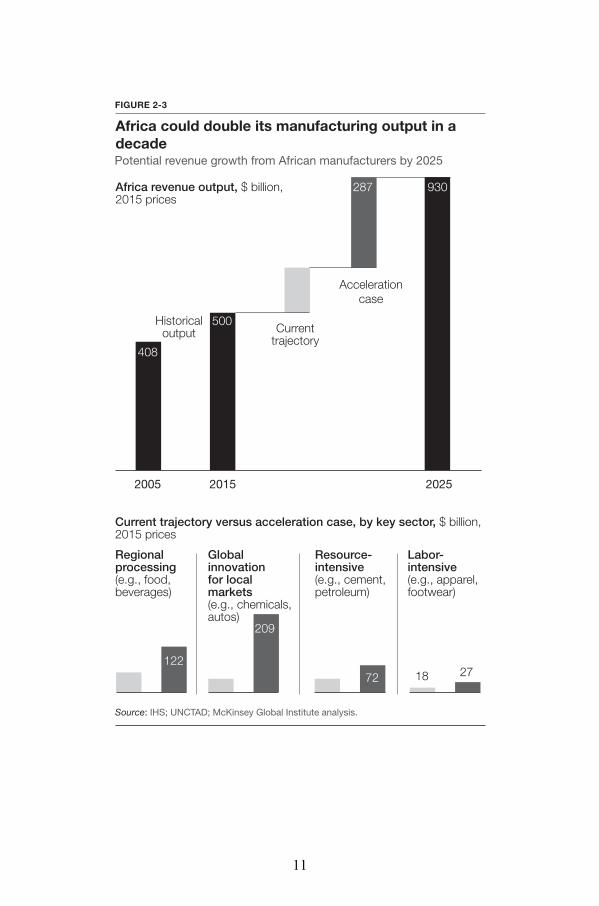

Africa could double its manufacturing output in adecadePotential revenue growth from African manufacturers by 2025

Africa revenue output, $ billion,2015 prices

Current trajectory versus acceleration case, by key sector, $ billion,2015 prices

Source: IHS; UNCTAD; McKinsey Global Institute analysis.

2005

143

53 36 3618 27

2015 2025

Current trajectory

Historicaloutput

Accelerationcase

287

122

209

72

930

Regionalprocessing(e.g., food, beverages)

Globalinnovationfor local markets(e.g., chemicals, autos)

Resource-intensive(e.g., cement, petroleum)

Labor-intensive(e.g., apparel, footwear)

408

500

FIGURE 2-3

11

Chapter_02.indd Page 59 29/08/18 12:41 AM

4.1x

Most African countries lag other emerging marketsin infrastructure

Africa SouthAfrica

Egypt Algeria Ghana Kenya Nigeria Ethiopia BRIC*

Electric power consumption, kilowatt hours per person

Source: World Bank, World Development Indicators Database; CIA, World Factbook.

*Brazil, Russia, India, and China. Comparisons exclude Russia for roads and rail.

632

2,622

4,198

1,6581,356

355 167 144 70

1.5x

Africa SouthAfrica

Kenya Egypt Nigeria Ghana Algeria Ethiopia BRIC

Rail density, kilometers of track per square km

7.1

10.4

17.2

6.65.1

4.1 4.01.7

0.6

Africa SouthAfrica

Ghana Kenya Nigeria Egypt Ethiopia Algeria BRIC

Road density, kilometers of road per square km

97

485

613

459

277209

137100

48

5.0x

FIGURE 2-4

12

Chapter_02.indd Page 78 29/08/18 12:41 AM

FIGURE 2-5

East Asiaand Pacific

Latin Americaand Caribbean

1Active for 90 days.2Age 15 or over.

Source: GSMA Mobile Money Deployment Tracker; GSMA State of Industry Report 2016;World Bank Global Findex.

Sub-Saharan Africa

SouthAsia

Europe andCentral Asia

Adults2 with mobile money account, 2017, %

Sub-Saharan Africa

SouthAsia

Middle Eastand N. Africa

East Asiaand Pacific

Latin Americaand Caribbean

Middle Eastand N. Africa

Europe andCentral Asia

Africa is the world leader in mobile money

Active1 mobile money accounts, 2017, million

20.9

121.9 86.3 18.3 11.5 7.2

4.2 5.8 1.3 3.2

1.7

5.3

13

Chapter_03.indd Page 84 27/08/18 10:33 PM

Africa is bigger than you think: it dwarfs China, India,Europe, and the United States

FIGURE 3-1

EuropeChina India ContinentalUnited States

Source: Kai Krause, “The True Size of Africa,” http://kai.sub.blue/images/True-Size-of-Africa-kk-v3.pdf.

China

Spain

BelgiumNetherlandsPortugal

United States EasternEurope

China Ireland

Italy

Switzerland

France

India

UK

Japan

Germany

India

14

Chapter_03.indd Page 87 27/08/18 10:33 PM

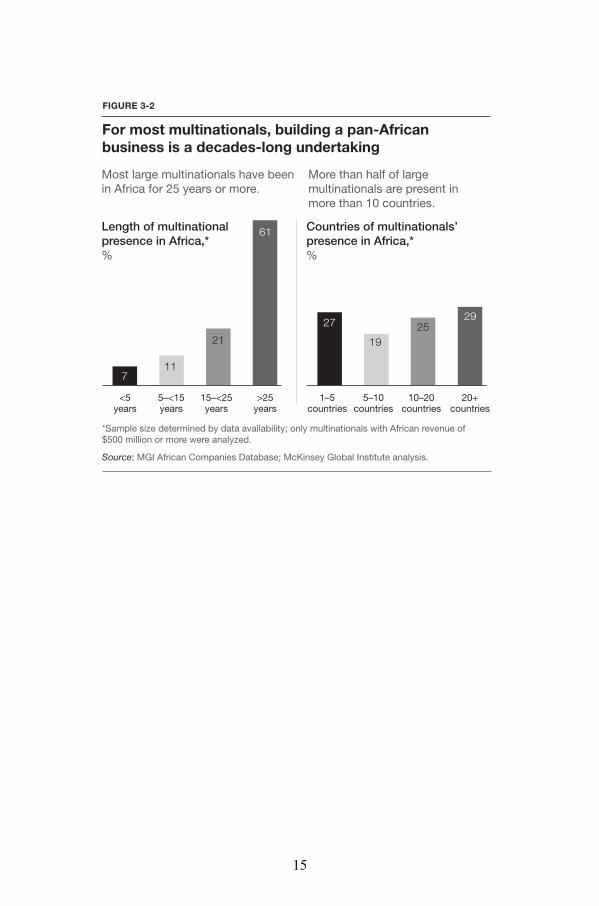

For most multinationals, building a pan-Africanbusiness is a decades-long undertaking

Most large multinationals have beenin Africa for 25 years or more.

More than half of largemultinationals are present inmore than 10 countries.

Length of multinationalpresence in Africa,*%

Countries of multinationals’presence in Africa,*%

<5years

5–<15years

15–<25years

>25years

Source: MGI African Companies Database; McKinsey Global Institute analysis.

*Sample size determined by data availability; only multinationals with African revenue of$500 million or more were analyzed.

711

21

61

1–5countries

5–10countries

10–20countries

20+countries

27

1925

29

FIGURE 3-2

15

Chapter_03.indd Page 97 27/08/18 10:33 PM

*Includes 15 countries in Central and West Africa; excludes North Africa and East Africa.

Consumption is growing much faster in some parts ofAfrica than others

Source: Oxford Economics: IHS; African Development Bank; McKinsey Global Institute analysis.

Total household consumption by region, %, $ billion, 2015 prices

826

9

1215

14

16

2005100% =910

13

14

9

16

26

9

13

2015

100% = 1,420

11

12 15

17

13

1022

2025

100% = 2,065

South Africa East Africa

Egypt

Nigeria

Franco-phoneAfrica*

Rest ofNorthAfrica

Rest of sub-SaharanAfrica

FIGURE 3-3

16

Chapter_04.indd Page 124 27/08/18 4:06 PM

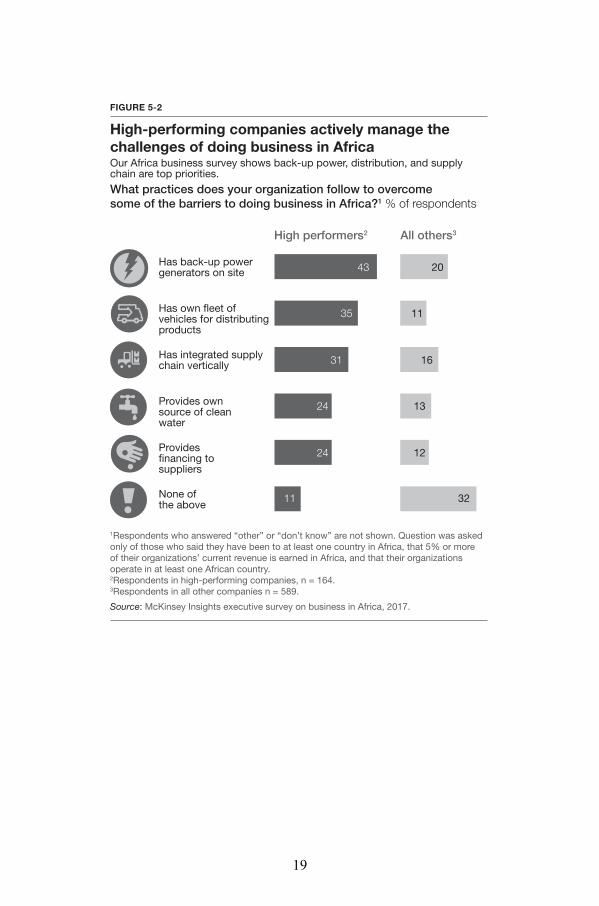

High performers2 All others3

High-performing firms put technology at the heart oftheir Africa growth strategyQuestion: Which technologies will most support your organization’sgrowth in Africa in the next five years?1 % of respondents

1Respondents who answered “other” or “don’t know” are not shown.2Respondents in high-performing companies, n = 166.3Respondents in all other companies n = 603.

Applications on mobile computing devices

Social mediatools

Big dataand analytics

The internetof things

Self-service websites and/or portals

Cloudcomputing

Artificial intelligenceand machine learning

Blockchain

2439

1534

2331

1729

1619

1618

415

512

38Autonomousvehicles

Source: McKinsey Insights executive survey on business in Africa, 2017.

FIGURE 4-1

17

Chapter_05.indd Page 142 25/08/18 3:27 PM

McKinsey’s African Stability Index pinpointscountries’ growth and risk profiles1

Comparison of historical GDP growth rates to country stabilityrankings2

Real GDPgrowth,2012–17% CAGR3

Relative stability ranking 2017

Source: McKinsey Global Institute analysis.

1The index covers 30 economies accounting for 97% of Africa’s GDP.2Bubble size represents country GDP estimate, 2016.3Compound annual growth rate.4Equatorial Guinea and Libya are plotted manually because of negative growthrates over this period.

10

8

6

2

00 8 16 24 32

Vulnerable growers make up 33% of Africa’s GDP

Stable growersmake up 31%

Slow growers make up 36%

Vulnerable

Low

High

Stable

Low

High

4

South Africa

Egypt

AlgeriaAngola

Morocco

GLOBAL

Sudan

Kenya

Tanzania

Tunisia

Democratic Republic ofCongo

GhanaCameroon

Côte d’Ivoire

Uganda

Zambia

Ethiopia

Botswana

Mozambique

Gabon

Senegal

Namibia

Burkina Faso

Mauritius

Mali

Madagascar

Rwanda

Libya4 EquatorialGuinea4

Togo

Nigeria

FIGURE 5-1

18

Chapter_05.indd Page 145 25/08/18 3:27 PM

High performers2 All others3

High-performing companies actively manage thechallenges of doing business in Africa

Source: McKinsey Insights executive survey on business in Africa, 2017.

What practices does your organization follow to overcomesome of the barriers to doing business in Africa?1 % of respondents

1Respondents who answered “other” or “don’t know” are not shown. Question was askedonly of those who said they have been to at least one country in Africa, that 5% or moreof their organizations’ current revenue is earned in Africa, and that their organizationsoperate in at least one African country.2Respondents in high-performing companies, n = 164.3Respondents in all other companies n = 589.

Has back-up power generators on site

Our Africa business survey shows back-up power, distribution, and supply chain are top priorities.

Has own fleet of vehicles for distributing products

Has integrated supply chain vertically

Provides own source of clean water

Provides financing to suppliers

None of the above

43 20

35 11

31 16

24 13

24 12

11 32

FIGURE 5-2

19

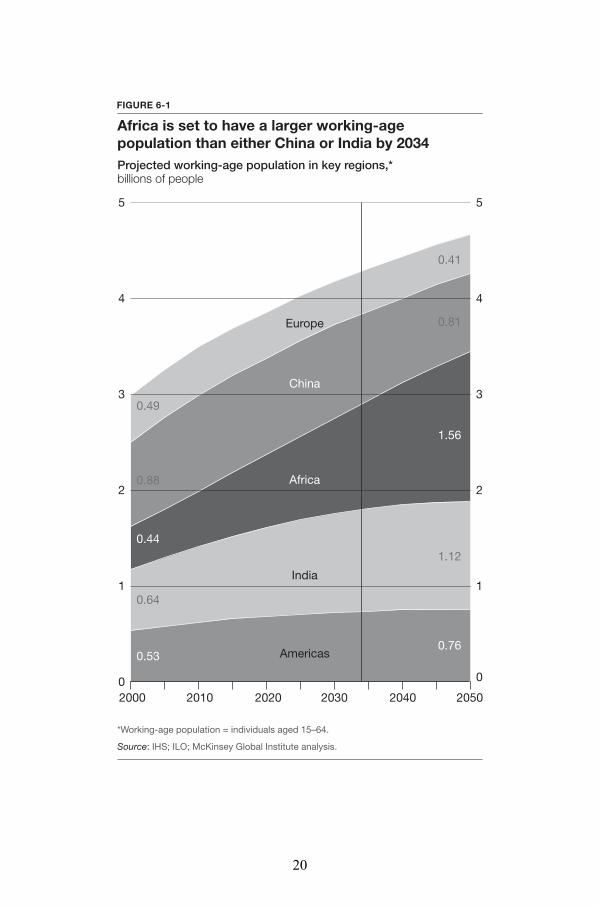

Chapter_06.indd Page 159 27/08/18 3:48 PM

Africa is set to have a larger working-agepopulation than either China or India by 2034

Source: IHS; ILO; McKinsey Global Institute analysis.

Projected working-age population in key regions,*billions of people

*Working-age population = individuals aged 15–64.

0

1

2

3

4

5

0

2000 2010 2020 2030 2040 2050

1

2

3

4

5

Europe

India

Americas

China

Africa

0.53

0.64

0.44

0.88

0.49

0.76

1.12

1.56

0.81

0.41

FIGURE 6-1

20

Chapter_06.indd Page 163 27/08/18 3:48 PM

Africans’ enrollment in tertiary and vocationaleducation is low compared with other regions

Students in secondary education enrolled in vocational programsin African countries, %

Students in secondary education enrolled in vocational programsby region, %

Source: World Bank education indicators; McKinsey Global Institute analysis.

Egypt 22 Rwanda 14 Algeria 8 S. Africa 7

East Asiaand Pacific 18

OECD17

Latin America andthe Caribbean 10

SouthernAsia 1

Africa 8

Students enrolled in tertiary education by region, %

United States 89 Turkey 79 China 30 Africa 12India 25

Morocco 6

FIGURE 6-2

21

Chapter_06.indd Page 168 27/08/18 3:48 PM

High performers2 All others3

High-performing companies are investing heavily indeveloping local talent

Source: McKinsey Insights executive survey on business in Africa, 2017.

What practices does your organization use to source and developtalent in Africa?1 % of respondents

1Respondents who answered “other” or “don’t know” are not shown. Question was askedonly of those who said they have been to at least one country in Africa, that 5% or more oftheir organizations’ current revenue is earned in Africa, and that their organizations operatein at least one African country.2Respondents in high-performing companies, n = 166.3Respondents in all other companies n = 603.

Runs training programs within workforce

Offers internship or apprenticeship programs

Partners with local universities

Brings in employees from offices in other countries

Seeks out talent working for local competitors

Runs programs to support women’s careers

None of the above

Partners with others to run vocational training

4061

3046

1942

3335

1630

1529

1722

283

FIGURE 6-3

Our Africa business survey underlines the importance of training andapprenticeship.

22

Chapter_06.indd Page 173 27/08/18 3:48 PM

A link between gender diversity and profitmargins creates a sound business case for women’s advancement

Women’s representation on the ExCos of African companiesversus EBIT margin deviation from industry average.3

Diversity and EBIT by business quartile,2 %

Representation and EBIT by business quartile, %

Women EBIT

QUARTILE 1

1Earnings before interest and taxes.2A quartile is defined as each of four equal groups into which a population can bedivided according to the distribution of values of a particular variable.Total number of companies in sample = 210. 32010 to 2014; GSMA Mobile Money Deployment Tracker.

Source: Orbis database, 2014; company annual reports and websites.

31

20

Women EBIT

QUARTILE 2

18

2

Women Women

EBIT

QUARTILE 3

9

–6

EBIT

QUARTILE 4

0

–17

Women EBIT

QUARTILE 1

33

14

Women EBIT

QUARTILE 2

17

6

Women Women

EBIT

QUARTILE 3

9

–1

EBIT

QUARTILE 4

1

–18

FIGURE 6-4

Women’s representation on the boards of African companiesversus EBIT1 margin deviation from industry average.

23