advice for the wise - february 2013

TRANSCRIPT

1

ADVICE for the WISE

Newsletter – FEBRUARY 2013

Economic Update 4

Equity Outlook 8

Debt Outlook 13

Forex 15

Commodities 16

Index Page No.

Contents

Real Estate 17

2

From the Desk of the CIO…

“Advisory services are provided through Karvy Stock Broking Ltd. (PMS) having SEBI Registration No: INP000001512. Investments are subject to market risks. Please read the disclaimer on slide 20”

Dear Investors,

The enthusiastic mood of January in capital markets was duly followed by

some somber reflections towards the end of the month. RBI obliged the

capital markets, the government and the real economy alike by reducing

the repo rate by 25 bps. It further tried to reduce the liquidity strain in

the banking system by reducing the cash reserve ratio by 25 bps as well.

The long due monetary easing finally began! It came with the usual

caveats from the Governor though, when he reminded everyone that the

pace of further easing is contingent on inflation coming down. Hence

even now, we cannot take further rate cuts for granted. The high base

effect may suppress inflation numbers for long enough to create a climate

for a moderate pace of monetary easing but the picture is complicated by

diesel price hike, not to mention RBI’s awareness of the base effect itself.

While RBI did its part by reducing the repo rate and CRR much rests with

banks and real economy decision makers as regards revival of high

economic growth. Consumption growth has held up quite well in India

through the last few years. Most of the slowdown in growth was a result

of a sharp reduction in real investments i.e. new factories, roads, power

plants and the like. Even real estate construction had slowed down

significantly, though prices remained firm. Part of this slowdown was due

to high interest rates, but a large part was due to bearish sentiments in

the real economy. Stated simply, companies and individuals alike

postponed or cancelled their investment plans due to concerns regarding

future growth in whatever they sell (for companies) or in their income

(for individuals).

The repo rate cut to translate into pick-up in investment activity has to

have two other favorable developments as well. One is the willingness

and ability of banks to lend for funding investments and second is the

willingness and ability of borrowers to ask for loans. The first is not a

major concern for private sector banks (a leading bank recently raised

significant fresh equity, signaling aggressive lending plans) but will remain

a worry for public sector banks with balance sheets still under strain from

NPAs. The second might emerge as a concern if the banks increasingly

find the only willing borrowers to be already overleveraged; worse still if

most real economy participants are still focusing on lightening their

balance sheets.

The repo rate cut thus is a good starting point for revival of growth.

However, we will have to watch for signs of investment activity picking up

before declaring victory on the growth front. The other factor to track is

the global risk appetite. Even on this front, there are some murmurs of

caution – largely due to fresh hints of trouble in Euro-zone and less than

jubilant data in US on employment. The actual numbers are hard enough

to predict; the reaction of market participants to them even more so. We

continue to believe that an unpleasant development on either EU front or

US front may send the risk appetite in reverse gear with immediate

consequences for emerging market fund flow. Investing into equities at

this stage, while lucrative, requires the awareness of the potential short

term volatility.

Long term debt continues to be a safe heads-I-win-tails-I-don’t-lose bet.

Slower pace of monetary easing will reduce the capital appreciation in

long term debt but the coupon accrual will still deliver decent returns.

3

As on 31st Jan 2013

Change over last month

Change over last year

Equity Markets

BSE Sensex 19895 2.4% 15.7%

S&P Nifty 6035 2.2% 16.1%

S&P 500 1498 5.0% 14.1%

Nikkei 225 11139 7.2% 26.5%

Debt Markets

10-yr G-Sec Yield 7.91% (14 bps) (36 bps)

Call Markets 7.80% 53 bps 124 bps

Fixed Deposit* 8.50% 0 (75 bps)

Commodity Markets

RICI Index 3847 4% 2.6%

Gold (`/10gm) 30169 (0.9%) 7.3%

Crude Oil ($/bbl) (As on 29th Jan)

115.22 4.0% 4.5%

Forex

Markets

Rupee/Dollar 53.3 2.8% (6.8%)

Yen/Dollar 91.0 (5.7%) (15.9%)

Economic Update - Snapshot of Key Markets

Gold

• Indicates SBI one-year FD •New 10 Year benchmark paper(8.15%, 2022 Maturity) was listed in the month of June, the 1 year yield is compared to the earlier benchmark(2021 Maturity)

4

75

85

95

105

115

125

135 Sensex Nifty S&P 500 Nikkei 225

7.30

7.80

8.30

8.80

9.30 10 Year G-Sec

15000

20000

25000

30000

35000

40

42

44

46

48

50

52

54

56

58

60

`/$

US

Europe

Japan

Emerging economies

• The Conference Board Consumer Confidence Index, which had declined in December, fell further in

January 2013. It now stands at 58.6 , down from 66.7 in December.

• Gross domestic product (GDP) fell at a 0.1% annual rate in Q4 2012 after growing at a 3.1% in the Q3

2012.

• The US unemployment rate rose to 7.9% in January 2013 from 7.8 % in December 2012

• The seasonally adjusted Markit Eurozone Manufacturing PMI rose to 47.9 in January 2013, from 46.1 in

December 2012. The survey continues to signal an overall deterioration of business conditions, but rose

to an 11-month high to suggest that the industrial sector is close to stabilizing after contracting

throughout much of last year.

• Eurozone's unemployment rate remained at 11.7% in December 2012, the highest level since the

introduction of the euro in 1999.

Economy Update - Global

• Japan’s Manufacturing PMI posted a reading of 47.7 in January 2013, up from 45.0 in December 2012.

However, by remaining below the 50.0 no-change mark for an eighth successive month in January, the

PMI again pointed to a deterioration in manufacturing operating conditions.

• Unemployment rate rose to a seasonally adjusted 4.2% in December 2012 from 4.1% in November 2012.

• China’s HSBC PMI inched slightly higher to 52.3 in January 2013 , up from 51.5 in December 2012

signaling a modest improvement of operating conditions in the Chinese manufacturing sector for the

third successive month.

• India’s HSBC Purchasing Managers’ Index(PMI) posted 53.2 in January 2013, down from the reading of

54.7 in December 2012 signaling a slightly lower improvement in the health of the manufacturing sector. 5

Economy Outlook - Domestic

• The Indian economy grew by 5.3 per cent in the July-September

period of the current financial year (2012-13), pulled down by

poor performance of manufacturing and agriculture sectors,

showing persistent signs of slowdown. The gross domestic

product (GDP) had expanded by 6.7 per cent in the same period

of last fiscal. During the three-month period ended September

30, the manufacturing sector grew marginally by 0.8 per cent,

against 2.9 per cent growth in the same period of 2011-12

• The economic growth in the first six month of this fiscal (April-

September) is 5.4 per cent, lower than 7.3 per cent growth

clocked in the year-ago period

• The Reserve Bank of India (RBI) sharply lowered the economic

growth projection to 5.8%, from 6.5%, projected earlier. The

growth rate in 2011-12 slipped to a nine-year low of 6.5%.

GDP growth

• Dashing hopes of a rebound, the industrial output contracted to a

four-month low of 0.1% in November due to poor performance of

manufacturing and mining sectors and decline in production of

capital goods. IIP dipped from a robust 8.3% in October. Factory

output growth was 1% in April-November period this fiscal, down

from 3.8% in the same period in 2011-12.

• the manufacturing sector rose a paltry 0.3% in November compared

with 6.6% expansion in the year ago period while mining fell 5.5%

compared to a decline of 3.5%. The capital goods sector, which is a

key indicator of industrial activity, fell 7.7% compared to a fall of

4.7% in the year-earlier period.

• The growth in the industrial production during October last year

was revised upward to 8.3%, from earlier provisional estimates of

8.2% released last month.

IIP

6

8.3

7.8 7.7

6.9

6.1

5.3 5.5

5.3

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

FY11(Q3) FY11(Q4) FY12(Q1) FY12(Q2) FY12(Q3) FY12(Q4) FY13(Q1) FY13(Q2)

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Nov 11

Dec 11

Jan 12

Feb 12

Mar 12

Apr 12

May 12

Jun 12

Jul 12

Aug 12

Sep 12

Oct 12

Nov 12

Economic Outlook - Domestic

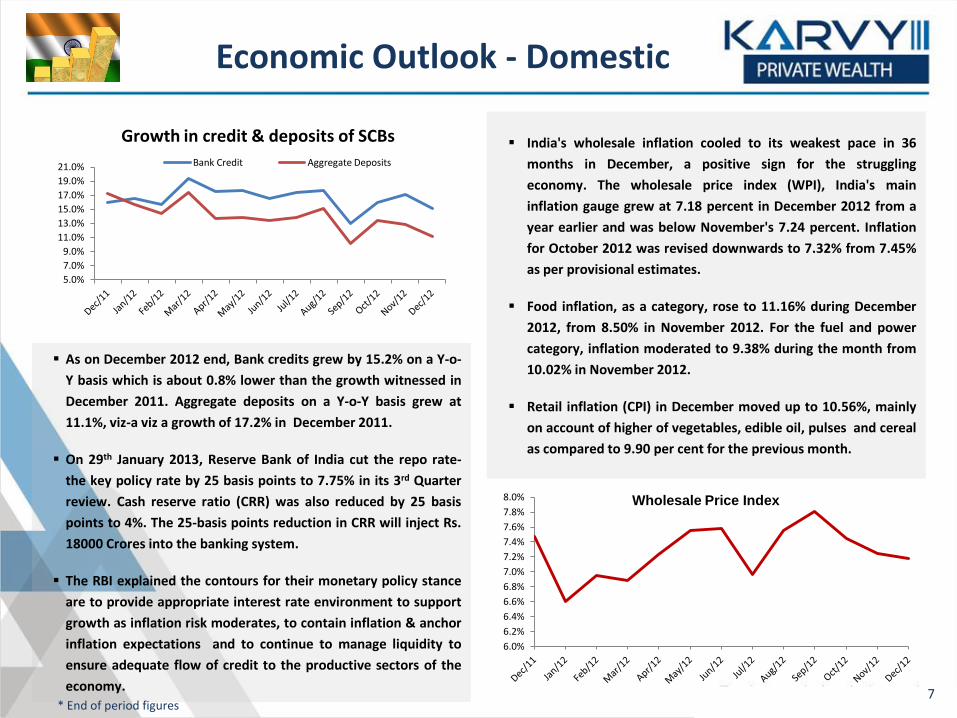

As on December 2012 end, Bank credits grew by 15.2% on a Y-o-

Y basis which is about 0.8% lower than the growth witnessed in

December 2011. Aggregate deposits on a Y-o-Y basis grew at

11.1%, viz-a viz a growth of 17.2% in December 2011.

On 29th January 2013, Reserve Bank of India cut the repo rate-

the key policy rate by 25 basis points to 7.75% in its 3rd Quarter

review. Cash reserve ratio (CRR) was also reduced by 25 basis

points to 4%. The 25-basis points reduction in CRR will inject Rs.

18000 Crores into the banking system.

The RBI explained the contours for their monetary policy stance

are to provide appropriate interest rate environment to support

growth as inflation risk moderates, to contain inflation & anchor

inflation expectations and to continue to manage liquidity to

ensure adequate flow of credit to the productive sectors of the

economy.

India's wholesale inflation cooled to its weakest pace in 36

months in December, a positive sign for the struggling

economy. The wholesale price index (WPI), India's main

inflation gauge grew at 7.18 percent in December 2012 from a

year earlier and was below November's 7.24 percent. Inflation

for October 2012 was revised downwards to 7.32% from 7.45%

as per provisional estimates.

Food inflation, as a category, rose to 11.16% during December

2012, from 8.50% in November 2012. For the fuel and power

category, inflation moderated to 9.38% during the month from

10.02% in November 2012.

Retail inflation (CPI) in December moved up to 10.56%, mainly

on account of higher of vegetables, edible oil, pulses and cereal

as compared to 9.90 per cent for the previous month.

Growth in credit & deposits of SCBs

* End of period figures 7

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

19.0%

21.0% Bank Credit Aggregate Deposits

6.0%

6.2%

6.4%

6.6%

6.8%

7.0%

7.2%

7.4%

7.6%

7.8%

8.0% Wholesale Price Index

Budget FY 14

In the last several months, Government of India has demonstrated its willingness to restart the reform process by pushing several

politically difficult reform measures. The FDI in Retail, Aviation & broadcasting are all measures which will have a long term beneficial

impact on the Indian Economy. Government has displayed a lot of political courage in pushing ahead with these measures despite stiff

political opposition. We see the Government’s decision to raise railway passenger fares and allow oil companies to raise diesel & petrol

prices periodically and free bulk diesel prices as positive for sentiment and much needed from a fiscal consolidation perspective.

It is important to note that most of these measures have been pushed before the announcement of the budget as government might

want a politically non-controversial budget considering its precarious majority in the Parliament. We expect most of the reform

measures to be carried out through executive actions before the budget and after it.

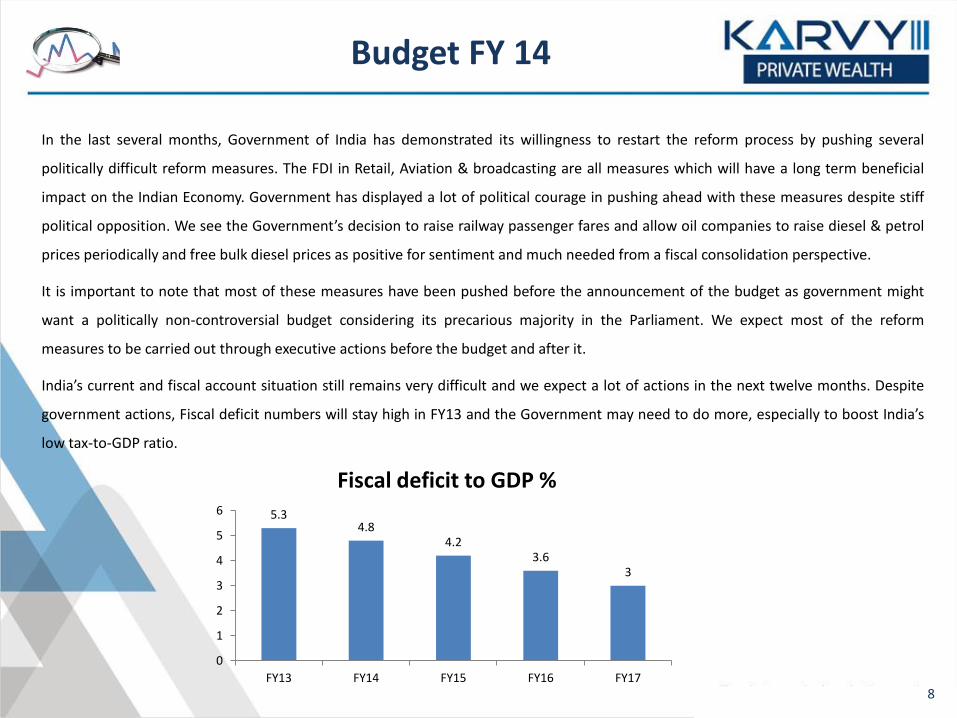

India’s current and fiscal account situation still remains very difficult and we expect a lot of actions in the next twelve months. Despite

government actions, Fiscal deficit numbers will stay high in FY13 and the Government may need to do more, especially to boost India’s

low tax-to-GDP ratio.

8

5.3 4.8

4.2 3.6

3

0

1

2

3

4

5

6

FY13 FY14 FY15 FY16 FY17

Fiscal deficit to GDP %

9

Budget FY 14

The implementation of GST looks unlikely in FY2014 but unaccounted income can be taxed through other innovative methods which

might find a place in this year’s budget. The finance minister has promised to curb the fiscal deficit without raising taxes. There could be

realignment of government expenditure to reduce the impact of new subsidies on the fiscal deficit numbers.

An area where budget might play a role is expenditure control. Government is trying hard to curtail expenditure and the biggest cut that

we expect will come in Plan expenditure. Already, Defense Ministry’s capex plan has been cut by 10,000 crores. There is an expectation

that there could be drastic cut in plan expenditure of various ministries with an objective of reducing deficit by 0.5%-1% of GDP in this

fiscal. This could well go into next year’s budget. Disinvestment is another area where government may be looking to raise some more

revenue. While budget targets are rarely met, we expect a mobilization of 25000 crores in FY13 from this route which could increase to

40000 crores next year. Further deregulation of fertilizer and fuel prices might also happen post the budget but it is a politically

inconvenient decision to push in an election year. We expect a fiscal deficit of around 5.5% for FY13 and 5% for FY14.

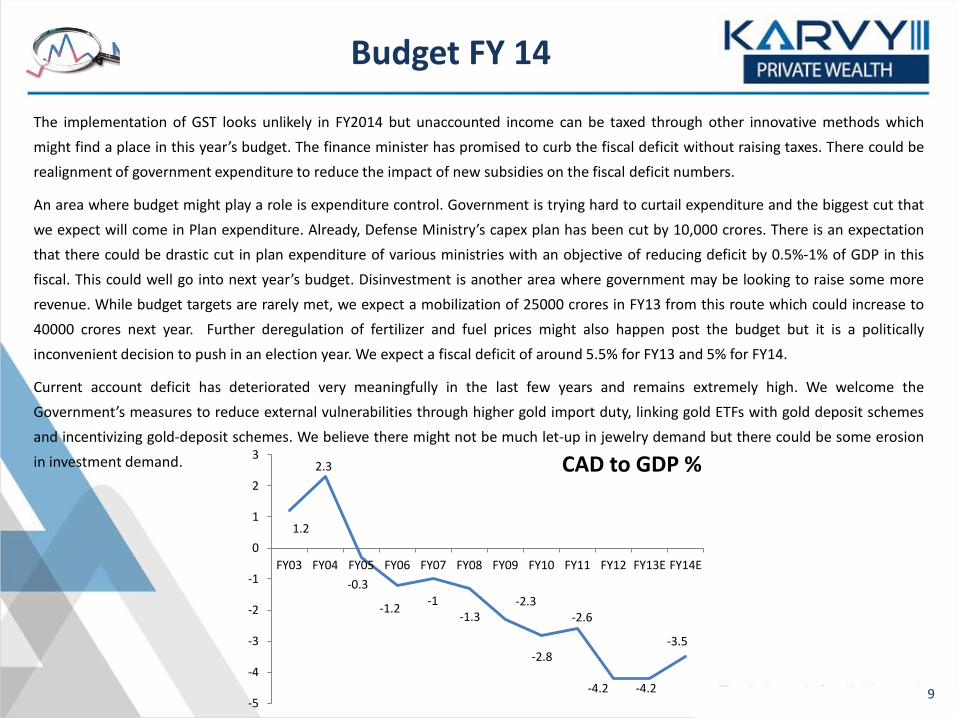

Current account deficit has deteriorated very meaningfully in the last few years and remains extremely high. We welcome the

Government’s measures to reduce external vulnerabilities through higher gold import duty, linking gold ETFs with gold deposit schemes

and incentivizing gold-deposit schemes. We believe there might not be much let-up in jewelry demand but there could be some erosion

in investment demand.

1.2

2.3

-0.3

-1.2 -1

-1.3 -2.3

-2.8

-2.6

-4.2 -4.2

-3.5

-5

-4

-3

-2

-1

0

1

2

3

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13E FY14E

CAD to GDP %

10

More such actions might be taken in the next few months. To ensure that FII continue to invest in India, GAAR has been postponed till

April 2016 and will not be applicable to FIIs whose intention is clear, i.e., not to avoid taxes using tax treaties. Government will keep

taking these kind of measures in an attempt to bridge the deficit on the current account with capital inflows. Investment limits in

Government and corporate bond markets have already been enhanced several times in the last year and could be increased further. If

Foreign investment limits in insurance sector is raised, that can bring fresh foreign capital into India. We expect swift approvals to

investment plans of foreign retailers.

Domestic Investment demand continues to be very weak and will likely remain so till the time underlying issues are addressed. It will

take time to fix the structural issues that plague investment. The IIP numbers indicate the low level of industrial activity in the country.

5.8 7

11.7

8.6

12.9

15.5

2.5

5.3

8.2

2.9 1.4

4.5

0

2

4

6

8

10

12

14

16

18

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13E FY14E

IIP Growth % The new land acquisition bill might be placed in the

budget session of Parliament which will streamline the

land acquisition process for large industrial projects.

Cabinet Committee for Infrastructure announced last

month will look at solving inter-ministerial issues on

various infra project and their first meeting is expected at

the end of January. The biggest road block to large

projects in the last three years has been the delays in

getting approvals from the environment ministry. Again,

something where budget can have very little impact.

We believe that a lot of actions will be taken by the government in the next twelve months to revive the ailing economy. However, there

will be a mix of executive decisions and few economic bills outside of budget. Those looking for a new economic vision for India in the

budget might end of getting disappointed again.

Budget FY 14

Sector Stance Remarks

BFSI Overweight

.The reversal of the interest rate cycle will assist in managing asset quality better and would lead

to increase in credit growth. However, we like the private sector more than public sector due to

better management quality and higher balance sheet discipline

FMCG Overweight

We like the secular consumption theme. We prefer “discretionary consumption” beneficiaries such

as Cigarettes, IT hardware, durables and branded garments, as the growth in this segment will be

disproportionately higher vis-à-vis the increase in disposable incomes.

Automobiles Overweight

Raw material prices have started coming down which would boost margins. Auto loans are also

getting cheaper. We are more bullish on SUV’s and agricultural vehicles segment due to lesser

competition and higher pricing power.

Healthcare Neutral

We believe in the large sized opportunity presented by Pharma sector in India. India’s strength in

generics is difficult to replicate due to quality and quantity of available skilled manpower. With the

developed world keen to cut healthcare costs, and a vast pipeline of drugs going off-patent, Indian

Pharma players are at the cusp of rapid growth. However, the government policy of putting price

control on selected drugs might cause some short term pressure on stock prices.

E&C Neutral

The significant slowdown in order inflow activity combined with high interest rates has hurt the

sector. Now since the interest rate cycle has started to reverse, we have turned more constructive

on this space.

Sector View

11

Sector Stance Remarks

Telecom Neutral The regulatory hurdles and competitive pressures seem to be reducing. Incumbents have started

to increase tariffs slowly and we believe that consolidation will happen sooner than expected

Cement Neutral Cement industry is facing over capacity issues and lackluster demand. With regulator taking a

strong view against pricing discipline, the profits of the sector are expected to stay muted.

Power Utilities Neutral We like the regulated return characteristics of this space. This space provides steady growth in

earnings and decent return on capital.

IT/ITES Neutral Demand seems to be coming back in Europe. US volume growth has also remained resilient. With

pricing already bottomed out, we have turned positive on the space selectively.

Energy Underweight We would stay away from oil PSUs, due to issues of cross subsidization distorting the underlying

economics of oil exploration and refinery businesses.

Metals Underweight Commodity prices have corrected significantly over the last few months due to concerns about

growth in China and developed parts of the world.

Sector View

12

Debt Outlook

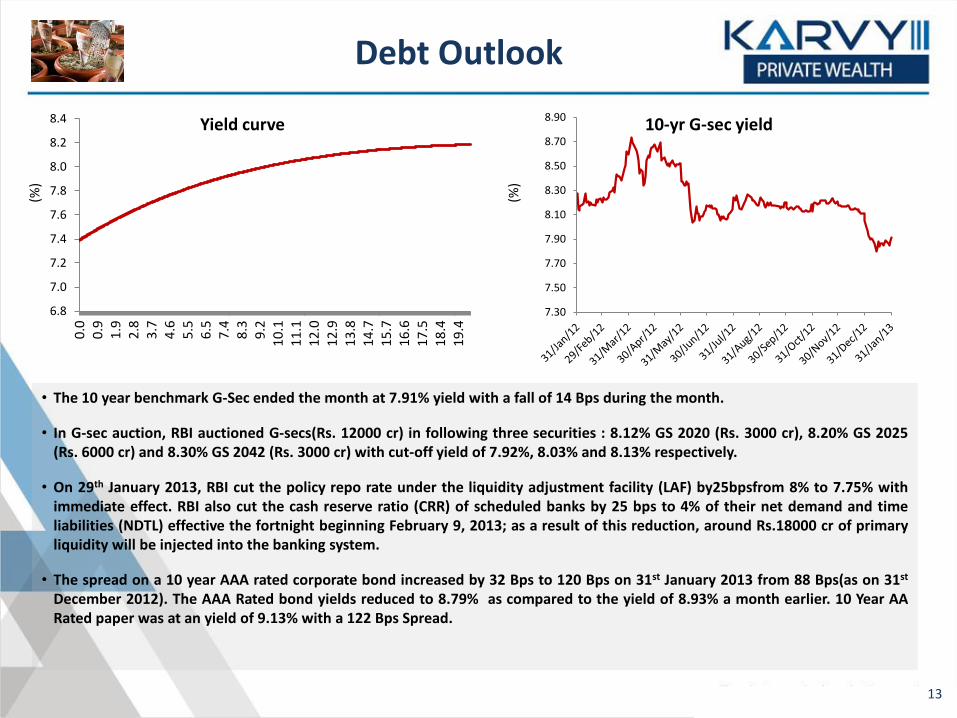

• The 10 year benchmark G-Sec ended the month at 7.91% yield with a fall of 14 Bps during the month.

• In G-sec auction, RBI auctioned G-secs(Rs. 12000 cr) in following three securities : 8.12% GS 2020 (Rs. 3000 cr), 8.20% GS 2025 (Rs. 6000 cr) and 8.30% GS 2042 (Rs. 3000 cr) with cut-off yield of 7.92%, 8.03% and 8.13% respectively.

• On 29th January 2013, RBI cut the policy repo rate under the liquidity adjustment facility (LAF) by25bpsfrom 8% to 7.75% with immediate effect. RBI also cut the cash reserve ratio (CRR) of scheduled banks by 25 bps to 4% of their net demand and time liabilities (NDTL) effective the fortnight beginning February 9, 2013; as a result of this reduction, around Rs.18000 cr of primary liquidity will be injected into the banking system.

• The spread on a 10 year AAA rated corporate bond increased by 32 Bps to 120 Bps on 31st January 2013 from 88 Bps(as on 31st December 2012). The AAA Rated bond yields reduced to 8.79% as compared to the yield of 8.93% a month earlier. 10 Year AA Rated paper was at an yield of 9.13% with a 122 Bps Spread.

10-yr G-sec yield Yield curve

(%)

(%)

13

7.30

7.50

7.70

7.90

8.10

8.30

8.50

8.70

8.90

6.8

7.0

7.2

7.4

7.6

7.8

8.0

8.2

8.4

0.0

0

.9

1.9

2

.8

3.7

4

.6

5.5

6

.5

7.4

8

.3

9.2

1

0.1

1

1.1

1

2.0

1

2.9

1

3.8

1

4.7

1

5.7

1

6.6

1

7.5

1

8.4

1

9.4

Debt Strategy

Outlook Category Details

Long Tenure Debt

Indian long term debt is likely to see capital appreciation owing to the expected monetary easing. With the second policy rate cut happening in Jan2013, with a 25 Bps cut in Repo and CRR along with signals of future cuts in the policy rates in the coming quarter, we would recommend to start investing in the Longer term papers and hold on to the current investments as well. These, while being available at attractive yields, also provide an opportunity for Capital appreciation due to a decrease in interest rates. Hence, these would be suitable for both - investors who may want to stay invested for the medium term (exiting when prices appreciate) and those who would want to lock in high yields for the longer term.

Some AA and select A rated securities are very attractive at the current yields. A similar trend can be seen in the Fixed Deposits also. Tight liquidity in the system has also contributed to widening of the spreads making entry at current levels attractive.

With the second policy rate cut that happened in Jan2013, with a 25 Bps cut in Repo rate and CRR along with signals of future cuts in the policy rates in the coming quarter, we would recommend to hold on to current investments in short term debt and direct fresh investments towards long term Debt. Due to liquidity pressures increasing in the market as RBI has a huge borrowing plan, short term yields would remain higher. Short Term funds still have high YTMs (9%–9.5%) providing interesting investment opportunities.

Short Tenure Debt

Credit

14

Forex

• INR has appreciated against the major four currencies. INR saw an appreciation of 2.79% against dollar, where as the appreciation against Euro was minute. It saw a high appreciation against Japanese Yen of 8.5%.

• Recovery in US economy increased risk appetite among global investors, sending funds flowing into riskier assets, including those in emerging markets. One more Factor for INR to strengthen is that it did not react adversely to fiscal deficit for April-December 2012 being reported at Rs 407,000 crore, or 78.8% of the budgeted fiscal deficit of Rs 991,000 crore for fiscal 2010-13.

• Volatility as last year is expected to continue as the rupee would track cues from the domestic markets as well as global shores.

Rupee movement vis-à-vis other currencies (M-o-M) Trade balance and export-import data

• The preliminary capital account balance for Q2 FY 13 came in at Rs. 1,31,800 Cr. Thus, taking H1 FY 13 figure to Rs. 2,19,000 Cr.

• Capital account surplus improved further in Q2 FY13, widening Rs. 1,31,800 as against Rs. 87,200 in Q1 FY 13.

68531 73903 75512

99033

66748

37298

95500 78800

0

20000

40000

60000

80000

100000

120000

140000

FY 10 (Q3) FY 10 (Q4) FY 11 (Q1) FY 11 (Q2) FY 11 (Q3) FY 11 (Q4) FY 12 (Q1) FY 12 (Q2)

Capital Account Balance

Exports during December, 2012 were valued at US$ 24.88 bn which was 1.92% lower than the level of US $ 25.36 bn during December, 2011. Imports during December, 2012 were valued at US $ 42.60 Bn representing a negative growth of 6.26% over the level of imports valued at US $ 40.04 Bn in December 2011, translating into a trade deficit of $17.7 Bn.

15

2.79%

5.09%

0.04%

8.52%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

USD GBP EURO YEN

-25000

-20000

-15000

-10000

-5000

0

-20

-10

0

10

20

30 Export Import Trade Balance (mn $)

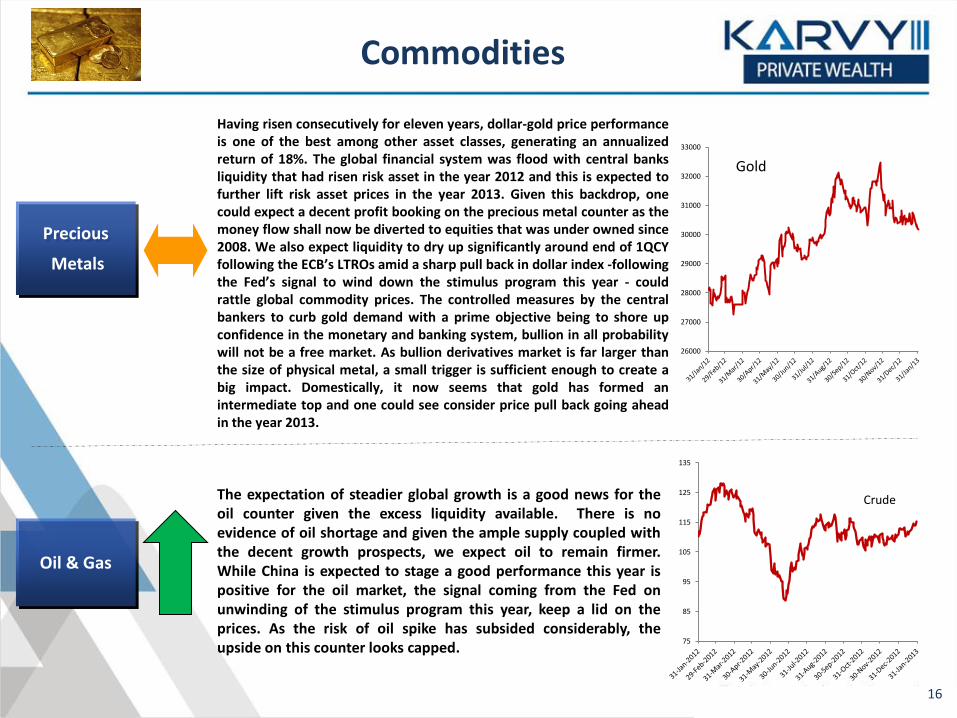

Commodities

Precious

Metals

Oil & Gas

The expectation of steadier global growth is a good news for the oil counter given the excess liquidity available. There is no evidence of oil shortage and given the ample supply coupled with the decent growth prospects, we expect oil to remain firmer. While China is expected to stage a good performance this year is positive for the oil market, the signal coming from the Fed on unwinding of the stimulus program this year, keep a lid on the prices. As the risk of oil spike has subsided considerably, the upside on this counter looks capped.

Crude

Gold

Having risen consecutively for eleven years, dollar-gold price performance is one of the best among other asset classes, generating an annualized return of 18%. The global financial system was flood with central banks liquidity that had risen risk asset in the year 2012 and this is expected to further lift risk asset prices in the year 2013. Given this backdrop, one could expect a decent profit booking on the precious metal counter as the money flow shall now be diverted to equities that was under owned since 2008. We also expect liquidity to dry up significantly around end of 1QCY following the ECB’s LTROs amid a sharp pull back in dollar index -following the Fed’s signal to wind down the stimulus program this year - could rattle global commodity prices. The controlled measures by the central bankers to curb gold demand with a prime objective being to shore up confidence in the monetary and banking system, bullion in all probability will not be a free market. As bullion derivatives market is far larger than the size of physical metal, a small trigger is sufficient enough to create a big impact. Domestically, it now seems that gold has formed an intermediate top and one could see consider price pull back going ahead in the year 2013.

16

26000

27000

28000

29000

30000

31000

32000

33000

75

85

95

105

115

125

135

Real Estate Outlook

17

Asset Classes Tier I Tier II

Residential

Prices continued to be at peak levels in most markets with sales being slow,

more so in the premium segment. Going forward, the expectation of a general

recovery of the economy is likely to improve the sentiment in the real estate

sector. Residential asset class shall continue to be the prime focus. If the RBI

does implement key policy rates cuts, cheaper home loans will significantly

improve the liquidity in the market.

A lot of new supply is expected to hit the market specially in NCR and Mumbai

regions in the near future as developers have been waiting for some time for

the liquidity situation to improve. In December, DLF launched a 13 acre

project, SkyCourt in Gurgaon which was completely sold off.

On an average, projects with Rs. 4,000 – 5,000 per sq. ft. entry pricing with

good developers in Pune, Bangalore, NCR and Mumbai suburbs are expected

to see good percentage returns.

The recent increase of 5-30% in the Ready Reckoner values, used to calculate

the stamp duty cost, from January 1 by the Maharashtra Government may act

as the slight dampener for the Mumbai market.

Demand in Tier II cities is largely driven by the trend towards

nuclear families, increasing disposable income, rising

aspiration to own quality products and the growth in

infrastructure facilities in these cities. Price appreciation is

more concentrated to specific micro-markets in these cities.

Cities like Chandigarh, Jaipur, Lucknow, Ahmedabad, Bhopal,

Nagpur, Patna and Cochin are expected to perform well.

Commercial/IT

Commercial asset class continues to be under pressure as most markets

continue to have an over-supply . Lease transactions are still slow as demand

has not yet revived. On an average, lease rentals have also not seen much

increase.

However, specific pre-leased properties with good tenant profile and larger

lock-in periods may present good investment opportunities over a long-term

horizon.

Lower unsold inventory and smaller unit sizes have led to

stable lease rentals in Tier II cities.

Real Estate Outlook

Please Note: Tier I* markets include Mumbai, Delhi & NCR, Bangalore, Pune, Chennai, Hyderabad and Kolkatta Tier II* markets includes all state capitals other than the Tier I markets The IC note is proposed to be presented every quarter

18

Asset Classes Tier I Tier II

Retail

Government has recently approved 51% foreign

ownership in multi-brand retail and 100% in single-brand

retail. Entry of foreign retailers in the Indian markets may

infuse new enthusiasm in the sector and improve the

demand for retail space.

However, it will take a gestation period of at least an year

for this to translate into actaul offtake of space. In the

immediate near term, unsold invesntory levels continue

to be high levels and lease rentals stagnant.

Long term investments in retail space along pre-

eastblished hubs may be attractive.

Tier II cities see a preference of hi-street retail as compared

to mall space in Tier I cities. While not much data on these

rentals gets reported, these are expected to have been

stagnant.

The mall culture has repeatedly failed in the past n the

Tier-2 cities. Whether the FDI in retail can change this

phenomenon can be known with more certainty once the

effect of FDI is more visible in Tier I cities.

Land

As Tier I cities continue to grow, new proposed /

implemented infrastructure developments at the

outskirts of these cities are making adjoining lands

expensive and attracting a lot of investor attention.

Caution should however be exercised due to the

complexities typically involved in land investments.

Land in Tier II and III cities along upcoming / established

growth corridors have seen good percentage appreciation

due to low investment base in such areas.

Why Karvy Private Wealth?

We are an open-architecture firm at two levels – asset class level and product level : • Offering COMPREHENSIVE choice of investing across all asset classes • Offering EXTENSIVE choice of multiple products from different product providers under each asset class

Open Architecture – Widest array of products

Intensive Research

We closely track the historical performance across asset classes, sub-asset classes and product providers to identify, evaluate and recommend investment products (KPW’s or third-party). We have our own proprietary methodology for evaluating products; for product providers, we also note the investment style and risk management philosophy. Our comprehensive analysis determines truly exceptional performers to be added to your portfolio

When you become a Client of KPW, besides getting intelligent & practicable Investment Advice, you get the benefit of “The KPW 3-S Service Promise” :

• Smooth and Hassle Free – Attention, Service & Convenience • Sharp and proactive – Portfolio monitoring and tracking • Smart –Incisive insights on markets and Investment products

The KPW 3-S Service promise:

Group-wide, we have no Mutual Fund or Insurance products of our own unlike most of the financial services groups (banks or broking houses), who are doing wealth management. Neither do we have exclusive tie-up with any single insurance company like all banks do.

Honest, unbiased advise

A talented team of leaders with global and Indian experience, having a unique blend of backgrounds of wealth management, private equity, strategy consulting and building businesses powers Karvy Private Wealth and its operations.

Pedigreed Senior Management Team

19

Disclaimer

The information and views presented here are prepared by Karvy Private Wealth(a division of Karvy Stock Broking Limited) or other Karvy Group

companies. The information contained herein is based on our analysis and upon sources that we consider reliable. We, however, do not vouch for the

accuracy or the completeness thereof. This material is for personal information and we are not responsible for any loss incurred based upon it.

The investments discussed or recommended here may not be suitable for all investors. Investors must make their own investment decisions based on

their specific investment objectives and financial position and using such independent advice, as they believe necessary. While acting upon any

information or analysis mentioned here, investors may please note that neither Karvy nor any person connected with any associated companies of

Karvy accepts any liability arising from the use of this information and views mentioned here.

The author, directors and other employees of Karvy and its affiliates may hold long or short positions in the above-mentioned companies from time to

time. Every employee of Karvy and its associated companies are required to disclose their individual stock holdings and details of trades, if any, that

they undertake. The team rendering corporate analysis and investment recommendations are restricted in purchasing/selling of shares or other

securities till such a time this recommendation has either been displayed or has been forwarded to clients of Karvy. All employees are further

restricted to place orders only through Karvy Stock Broking Ltd.

The information given in this document on tax are for guidance only, and should not be construed as tax advice. Investors are advised to consult their

respective tax advisers to understand the specific tax incidence applicable to them. We also expect significant changes in the tax laws once the new

Direct Tax Code is in force – this could change the applicability and incidence of tax on investments

Karvy Private Wealth (A division of Karvy Stock Broking Limited) operates from within India and is subject to Indian regulations.

Karvy Stock Broking Ltd. is a SEBI registered stock broker, depository participant having its offices at:

702, Hallmark Business plaza, Sant Dnyaneshwar Marg, Bandra (East), off Bandra Kurla Complex, Mumbai 400 051 .

(Registered office Address: Karvy Stock Broking Limited, “KARVY HOUSE”, 46, Avenue 4, Street No.1, Banjara Hills, Hyderabad 500 034)

SEBI registration No’s:”NSE(CM):INB230770138, NSE(F&O): INF230770138, BSE: INB010770130, BSE(F&O): INF010770131,NCDEX(00236,

NSE(CDS):INE230770138, NSDL – SEBI Registration No: IN-DP-NSDL-247-2005, CSDL-SEBI Registration No:IN-DP-CSDL-305-2005, PMS Registration No.:

INP000001512”

20

Contact Us

Bangalore 080-26606126

Chennai 044-45925923

Coimbatore 0422-4291018

Hyderabad 040-44507282

Kolkata 033-40515100

Mumbai 022-33055000

Gurgaon 0124-4780228

Email: [email protected] SMS: ‘HNI’ to 56767 Website: www.karvywealth.com

Corporate Office : 702, Hallmark Business Plaza, Off Bandra Kurla Complex, Bandra (East), Mumbai – 400 051

Pune 020-30116238

Kochi 0484-2321831

Delhi 011-43533941

21