adverse selection in resale markets for securitized assets · adverse selection in resale markets...

TRANSCRIPT

Adverse Selection in Resale Markets for Securitized Assets

Adverse Selection in Resale Markets for SecuritizedAssets

Martin Kuncl

Bank of Canada

Banque de FranceOctober 23, 2015

Disclaimer: The views expressed in this paper are those of the author. Noresponsibility for them should be attributed to the Bank of Canada.

Adverse Selection in Resale Markets for Securitized AssetsMotivation

Motivation

Prior to the recent financial crisissecuritization became popular, and a lot of risk wasaccumulated in securitized assets (especially MBS),nevertheless markets for securitized assets worked well.

During the crisisa sudden and extreme market dry-up: increase in spreads anddrop in volumes Graphs

How to explain accumulation of low quality investment and thensudden dry-up of markets?

Underestimation of risks? Panic? Irrational expectations?(Shleifer and Vishny 2010, Gennaioli et al. 2013)

This behavior can be explained by a varying degree ofasymmetric information about quality of securitized assetsover the business cycle.

Adverse Selection in Resale Markets for Securitized AssetsMotivation

Motivation

Prior to the recent financial crisissecuritization became popular, and a lot of risk wasaccumulated in securitized assets (especially MBS),nevertheless markets for securitized assets worked well.

During the crisisa sudden and extreme market dry-up: increase in spreads anddrop in volumes Graphs

How to explain accumulation of low quality investment and thensudden dry-up of markets?

Underestimation of risks? Panic? Irrational expectations?(Shleifer and Vishny 2010, Gennaioli et al. 2013)

This behavior can be explained by a varying degree ofasymmetric information about quality of securitized assets overthe business cycle.

Adverse Selection in Resale Markets for Securitized AssetsOverview of results

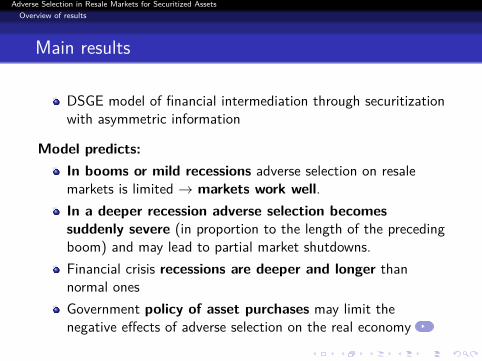

Main results

DSGE model of financial intermediation through securitizationwith asymmetric information

Model predicts:In booms or mild recessions adverse selection on resalemarkets is limited → markets work well.In a deeper recession adverse selection becomessuddenly severe (in proportion to the length of the precedingboom) and may lead to partial market shutdowns.Financial crisis recessions are deeper and longer thannormal onesGovernment policy of asset purchases may limit thenegative effects of adverse selection on the real economy

Adverse Selection in Resale Markets for Securitized AssetsModel mechanism

Outline

1. Motivation2. Overview of results3. Model mechanism4. Results of MS DSGE model

a. Methodologyb. Impulse responses

5. Conclusion

Adverse Selection in Resale Markets for Securitized AssetsModel mechanism

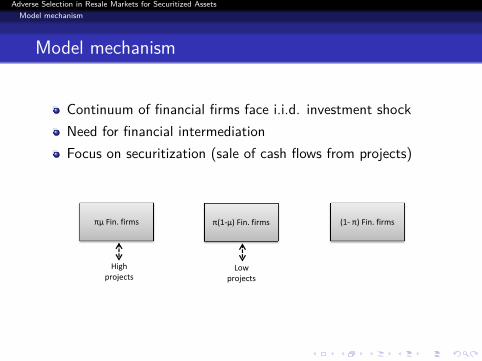

Model mechanism

Continuum of financial firms face i.i.d. investment shockNeed for financial intermediationFocus on securitization (sale of cash flows from projects)

High projects

Low projects

(1‐ π) Fin. firms πµ Fin. firms π(1‐µ) Fin. firms

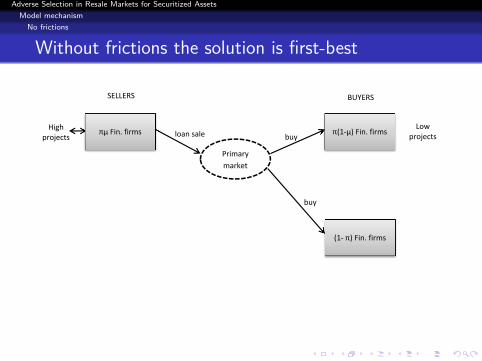

Adverse Selection in Resale Markets for Securitized AssetsModel mechanism

No frictions

Without frictions the solution is first-best

Primary market

High projects

Low projects loan sale

buy

buy

SELLERS BUYERS

(1‐ π) Fin. firms

πµ Fin. firms π(1‐µ) Fin. firms

Adverse Selection in Resale Markets for Securitized AssetsModel mechanism

Introducing frictions

Introducing frictions

Primary market

High projects

Low projects loan sale

buy

buy

SELLERS BUYERS

(1‐ π) Fin. firms

πµ Fin. firms π(1‐µ) Fin. firms

Introduce frictions:“skin in the game”asymmetric information in primary and resale markets

Adverse Selection in Resale Markets for Securitized AssetsModel mechanism

Introducing frictions

Introducing frictions

Primary market

Resale market

High projects

Low projects loan sale

buy

buy

buy

buy

loan sale

SELLERS BUYERS

(1‐ π) Fin. firms

πµ Fin. firms π(1‐µ) Fin. firms

Introduce frictions:“skin in the game”asymmetric information in primary and resale markets

Adverse Selection in Resale Markets for Securitized AssetsModel mechanism

Introducing frictions

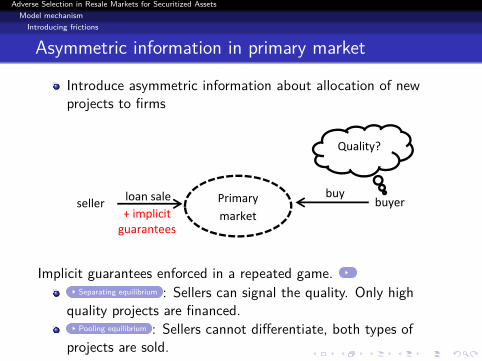

Asymmetric information on primary market

Introduce asymmetric information about allocation of newprojects to firms

Primary

marketbuyer seller

Quality?

loan sale buy

Adverse Selection in Resale Markets for Securitized AssetsModel mechanism

Introducing frictions

Asymmetric information in primary market

Introduce asymmetric information about allocation of newprojects to firms

Primary

marketbuyer seller

Quality?

loan sale buy

+ implicit guarantees

Implicit guarantees enforced in a repeated game.Separating equilibrium : Sellers can signal the quality. Only high

quality projects are financed.Pooling equilibrium : Sellers cannot differentiate, both types of

projects are sold.

Adverse Selection in Resale Markets for Securitized AssetsModel mechanism

Introducing frictions

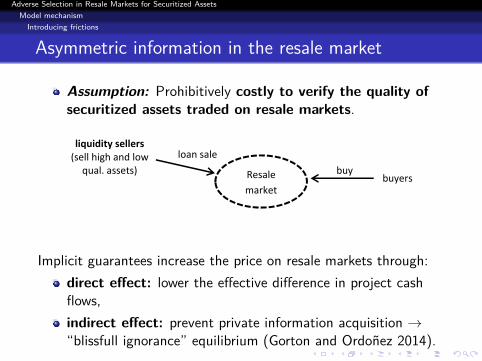

Asymmetric information in the resale market

Assumption: Prohibitively costly to verify the quality ofsecuritized assets traded on resale markets.

Resale

marketbuyers

liquidity sellers (sell high and low

qual. assets)

loan sale

buy

Implicit guarantees increase the price on resale markets through:direct effect: lower the effective difference in project cashflows,indirect effect: prevent private information acquisition →“blissfull ignorance” equilibrium (Gorton and Ordonez 2014).

Adverse Selection in Resale Markets for Securitized AssetsModel mechanism

Introducing frictions

Asymmetric information in the resale market

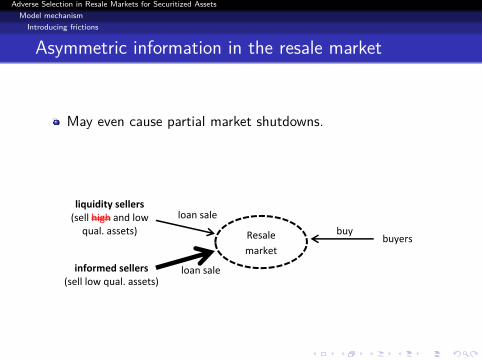

In a “deep recession” there is economy-wide default onimplicit guarantees → surge in adverse selection.

Resale

marketbuyers

liquidity sellers (sell high and low

qual. assets)

loan sale

buy

informed sellers (sell low qual. assets)

loan sale

Drop in the price & lower investment and output in theeconomy.

Adverse Selection in Resale Markets for Securitized AssetsModel mechanism

Introducing frictions

Asymmetric information in the resale market

May even cause partial market shutdowns.

Resale

marketbuyers

liquidity sellers (sell high and low

qual. assets)

loan sale

buy

informed sellers (sell low qual. assets)

loan sale

Adverse Selection in Resale Markets for Securitized AssetsResults of MS DSGE model

Outline

1. Motivation2. Overview of results3. Model mechanism4. Results of MS DSGE model

a. Methodologyb. Impulse responses

5. Conclusion

Adverse Selection in Resale Markets for Securitized AssetsResults of MS DSGE model

Methodology

Perturbation method for Markov-Switching DSGEAssumption: Counter-cyclical dispersion in TFP of projects(following Bloom (2009) and Bloom et al. (2012) )Three Markov states:

Regime 1 - Expansion: (high TFP, low dispersion →pooling equilibrium on primary market)

Regime 2 - Mild Recession: (low TFP, higher dispersion →separating equilibrium on primary market)

Regime 3 - Deep Recession: (low TFP, largest dispersion →separating equilibrium, default on outstanding implicitrecourse)

I use perturbation method for Markov-switching DSGE modelsusing methodology by Foerster et al. (2013)

Can capture differences in equilibrium across regimes.Can be used for more complex space of state variables.

Adverse Selection in Resale Markets for Securitized AssetsResults of MS DSGE model

Methodology

Perturbation method for Markov-Switching DSGEAssumption: Counter-cyclical dispersion in TFP of projects(following Bloom (2009) and Bloom et al. (2012) )Three Markov states:

Regime 1 - Expansion: (high TFP, low dispersion →pooling equilibrium on primary market)

Regime 2 - Mild Recession: (low TFP, higher dispersion →separating equilibrium on primary market)

Regime 3 - Deep Recession: (low TFP, largest dispersion →separating equilibrium, default on outstanding implicitrecourse)

I use perturbation method for Markov-switching DSGE modelsusing methodology by Foerster et al. (2013)

Can capture differences in equilibrium across regimes.Can be used for more complex space of state variables.

Adverse Selection in Resale Markets for Securitized AssetsResults of MS DSGE model

Methodology

Perturbation method for Markov-Switching DSGEAssumption: Counter-cyclical dispersion in TFP of projects(following Bloom (2009) and Bloom et al. (2012) )Three Markov states:

Regime 1 - Expansion: (high TFP, low dispersion →pooling equilibrium on primary market)

Regime 2 - Mild Recession: (low TFP, higher dispersion →separating equilibrium on primary market)

Regime 3 - Deep Recession: (low TFP, largest dispersion →separating equilibrium, default on outstanding implicitrecourse)

I use perturbation method for Markov-switching DSGE modelsusing methodology by Foerster et al. (2013)

Can capture differences in equilibrium across regimes.Can be used for more complex space of state variables.

Adverse Selection in Resale Markets for Securitized AssetsResults of MS DSGE model

Impulse responses

Effects of defaults on implicit recourse on adverseselection

2 4 6 8 10 12 14time

200

400

600

fNIR

2 4 6 8 10 12 14time

-4

-3

-2

-1

1

qs

2 4 6 8 10 12 14time

-5

-4

-3

-2

-1

K

2 4 6 8 10 12 14time

10203040506070

Z

2 4 6 8 10 12 14time

-7-6-5-4-3-2-1

output

2 4 6 8 10 12 14time

1

2

3

4

Ω

Implicit guar. defaulted Implicit guar. honored

Adverse Selection in Resale Markets for Securitized AssetsResults of MS DSGE model

Impulse responses

Introducing government policy of asset purchases

Motivated by the quantitative easing of the FED, I consider apolicy of asset purchases Graph

exchange of secur. assets in resale markets for governmentbonds at advantageous conditionscosts covered by lump sum taxes

Two effects:Cleans the market from low quality assets → eliminatesadverse selectionMoral hazard problem

Details

Adverse Selection in Resale Markets for Securitized AssetsResults of MS DSGE model

Impulse responses

Government policy eliminates the effects of assetrepurchases

2 4 6 8 10 12 14time

200

400

600

fNIR

2 4 6 8 10 12 14time

-4-3-2-1

123

qs

2 4 6 8 10 12 14time

-5

-4

-3

-2

-1

K

2 4 6 8 10 12 14time

10203040506070

Z

2 4 6 8 10 12 14time

-7-6-5-4-3-2-1

output

2 4 6 8 10 12 14time

1

2

3

4

Ω

Without Policy With Policy

Adverse Selection in Resale Markets for Securitized AssetsConclusion

Conclusion

The model proposes an explanation for:Accumulation of low quality securitized assets on financialsystem balance sheets prior to the crisisSmooth working of the market for securitized assets prior tothe crisisResale market collapse during the crisisFinancial turmoil on securitization markets cause deeper andlonger recessionBenefits and costs of the government policy of assetpurchases (similar to FED quantitative easing)

Adverse Selection in Resale Markets for Securitized AssetsReferences

Selected references

Brunnermeier, M. 2009. Deciphering the liquidity and credit crunch 2007-2008. Journal of Economic Perspectives23 (1): 77-100.Calomiris, C. and Mason, J. (2004). Credit card securitization and regulatory arbitrage. Journal of FinancialServices Research, Vol. 26, pp. 5-27.Cho, I.-K., and D. M. Kreps. (1987). Signaling Games and Stable Equilibria. The Quarterly Journal of Economics102 (2): 179-222.Foerster, A., Rubio-Ramırez, J., Waggoner, D. F. and Zha, T., 2013. Perturbation methods for Markov-switchingDSGE models. Federal Reserve Bank of Atlanta Working Paper Series (2013-1).Gertler, M. and Karadi, P., (2011). A model of unconventional monetary policy. Journal of Monetary Economics58 (1), 17-34.Gorton, G. and Pennacchi, G. (1995). Banks and loan sales: Marketing nonmarketable assets. Journal of MonetaryEconomics 35, pp. 389–411.Gorton, G. and Ordonez, P. (2012). Collateral crises. American Economic Review 104 (2), 343-378.Gennaioli, N., Shleifer, A. and Vishny, R. W., (2013). A model of shadow banking. The Journal of Finance 68 (4),1331-1363.Higgins, E. and Mason, J. (2004). What is the value of recourse to asset-backed securities? A clinical study ofcredit card banks. Journal of Banking and Finance, Vol. 28, pp. 875–899.Kiyotaki, N. and Moore, J. (2012). Liquidity, Business Cycles and Monetary Policy. NBER Working Papers, no.17934.Kuncl, M., (2014). Securitization under asymmetric information over the business cycle. CERGE-EI Working PaperSeries (506).Ordonez, G., (2014). Confidence banking and strategic default. Mimeo. University of Pennsylvania and NBER.Shleifer, A. and Vishny, R. (2010). Unstable banking. Journal of Financial Economics, Vol. 97, pp. 306–318.

Adverse Selection in Resale Markets for Securitized AssetsAppendix

Appendix

Adverse Selection in Resale Markets for Securitized AssetsAppendix

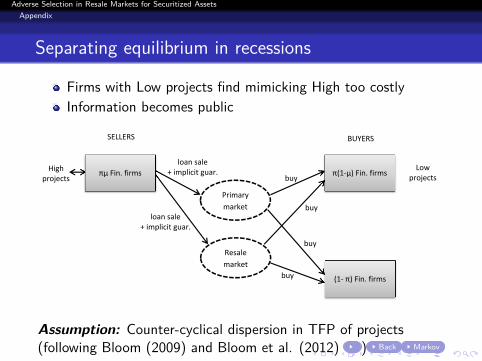

Separating equilibrium in recessions

Firms with Low projects find mimicking High too costlyInformation becomes public

Primary market

Resale market

High projects

Low projects

loan sale + implicit guar.

buy

buy

buy

buy

loan sale + implicit guar.

SELLERS BUYERS

(1‐ π) Fin. firms

πµ Fin. firms π(1‐µ) Fin. firms

Assumption: Counter-cyclical dispersion in TFP of projects(following Bloom (2009) and Bloom et al. (2012) ) Back Markov

Adverse Selection in Resale Markets for Securitized AssetsAppendix

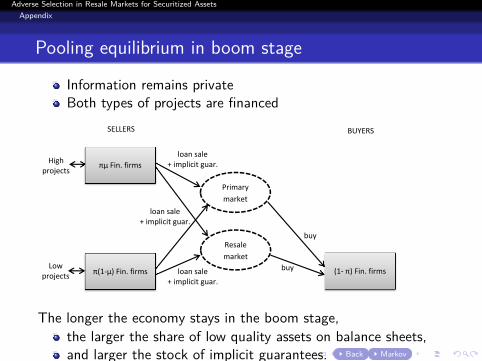

Pooling equilibrium in boom stage

Information remains privateBoth types of projects are financed

Primary market

Resale market

High projects

Low projects

loan sale + implicit guar.

buy

buy

loan sale + implicit guar.

SELLERS BUYERS

(1‐ π) Fin. firms

πµ Fin. firms

π(1‐µ) Fin. firms loan sale + implicit guar.

The longer the economy stays in the boom stage,the larger the share of low quality assets on balance sheets,and larger the stock of implicit guarantees. Back Markov

Adverse Selection in Resale Markets for Securitized AssetsAppendix

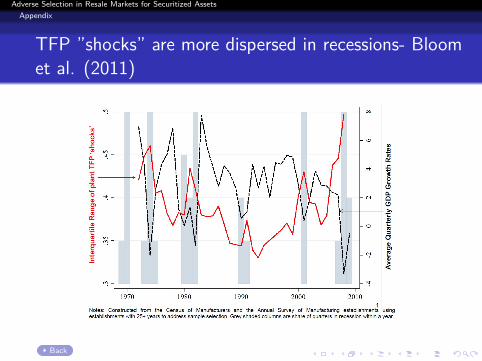

TFP ”shocks” are more dispersed in recessions- Bloomet al. (2011)

Back

Adverse Selection in Resale Markets for Securitized AssetsAppendix

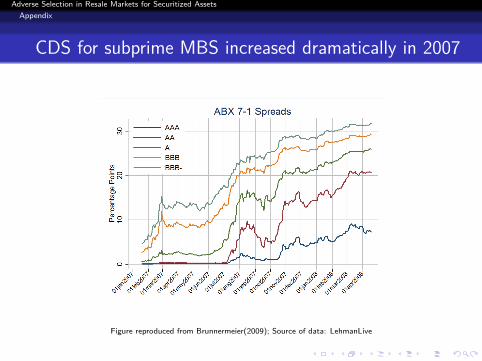

CDS for subprime MBS increased dramatically in 2007

Figure reproduced from Brunnermeier(2009); Source of data: LehmanLive

Adverse Selection in Resale Markets for Securitized AssetsAppendix

Drying-up of ABCP markets in 2007

200

400

600

800

1000

1200

2001‐01

2001‐07

2002‐01

2002‐07

2003‐01

2003‐07

2004‐01

2004‐07

2005‐01

2005‐07

2006‐01

2006‐07

2007‐01

2007‐07

2008‐01

2008‐07

2009‐01

2009‐07

2010‐01

2010‐07

2011‐01

2011‐07

2012‐01

2012‐07

2013‐01

2013‐07

2014‐01

2014‐07

Amount Outstanding (Billions USD

)

Commercial Paper

ABCP Other CP

Source: Board of Governors of the Federal Reserve System (US)

Back

Adverse Selection in Resale Markets for Securitized AssetsAppendix

Quantitative easing by the FED

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

Billions USD

Selected Federal Reserve Assets

Treasuries MBS

Source: Board of Governors of the Federal Reserve System (US)/FRED

Back to Motivation Back to Policy

Adverse Selection in Resale Markets for Securitized AssetsAppendix

Introducing government policy of asset purchases

Motivated by the quantitative easing of the FED, I consider apolicy of asset purchases Graph

exchange of secur. assets in resale markets for governmentbonds at advantageous conditionscosts covered by lump sum taxes

Two effects:Cleans the market from low quality assets → eliminatesadverse selectionMoral hazard problem

Simplifying assumptions:Triggered in “Deep Recession”: r B

t+1 = Er ht+1 and following

periods target returns s.t. qBt+s+1 = qs

t+s+1Back to Policy

Adverse Selection in Resale Markets for Securitized AssetsAppendix

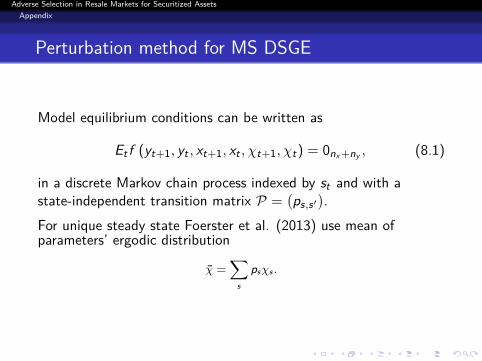

Perturbation method for MS DSGE

Model equilibrium conditions can be written as

Et f (yt+1, yt , xt+1, xt , χt+1, χt) = 0nx+ny , (8.1)

in a discrete Markov chain process indexed by st and with astate-independent transition matrix P =

(ps,s′

).

For unique steady state Foerster et al. (2013) use mean ofparameters’ ergodic distribution

χ =∑

s

psχs .

Adverse Selection in Resale Markets for Securitized AssetsAppendix

Perturbation method for MS DSGE

The solution of the recursive model (8.1) is

xt+1 = h (xt , ψ, st) ,

yt = g (xt , ψ, st) ,

yt+1 = g (xt+1, ψ, st+1) ,

The first order approximations hfirst and gfirst are

hfirst (xt , ψ, st)− xss = Dhss (st)St ,

gfirst (xt , ψ, st)− yss = Dgss (st)St ,

where St =[(xt − xss)

T ψ]T

. Back

Adverse Selection in Resale Markets for Securitized AssetsAppendix

Literature review

Securitization under asymmetric information (Gorton andPennachi 1995, Paligorova 2009 etc.)Implicit recourse - can be sustained in a reputationequilibrium (Gorton and Souleles 2006); may signal quality(Higgins and Mason 2004, Calomiris and Mason 2004)

”As the saying goes, the only securitization without recourse isthe last.” (Rosner and Mason 2007, p.38)

Confidence banking (Ordonez 2014), “Blissful ignorance”equilibrium (Gorton and Ordonez 2014)Kiyotaki and Moore (2012), Gertler and Karadi (2011),Gertler and Kiyotaki (2010), Kuncl (2014)

Back