acquisition of mach gen, llctalenenergy.investorroom.com/download/talen+energy... · 2016 ev /...

TRANSCRIPT

Acquisition of MACH Gen, LLC

July 2015 Investor Presentation

2.5 GWs of Efficient Gas-Fired Generation

We Generate Energy for a Brighter Tomorrow

© Talen Energy Corporation 2015 2

Safe Harbor

Forward Looking Statements:

Any statements made in this presentation about future operating results

or other future events are forward-looking statements under the Safe

Harbor Provisions of the Private Securities Litigation Reform Act of

1995. Actual results may differ materially from such forward-looking

statements. A discussion of factors that could cause actual results or

events to vary is contained in the Supplemental Information to this

presentation and in the Company’s SEC filings, including the factors

discussed under “Risk Factors” in the Company’s Registration

Statement on Form S-1.

© Talen Energy Corporation 2015 3

Agenda

Transaction Highlights

MACH Gen Overview

Financial Considerations

Closing Remarks and Q&A

P. Farr

P. Farr

J. McGuire

P. Farr

© Talen Energy Corporation 2015 4

Creating Value from Day 1

© Talen Energy Corporation 2015 5

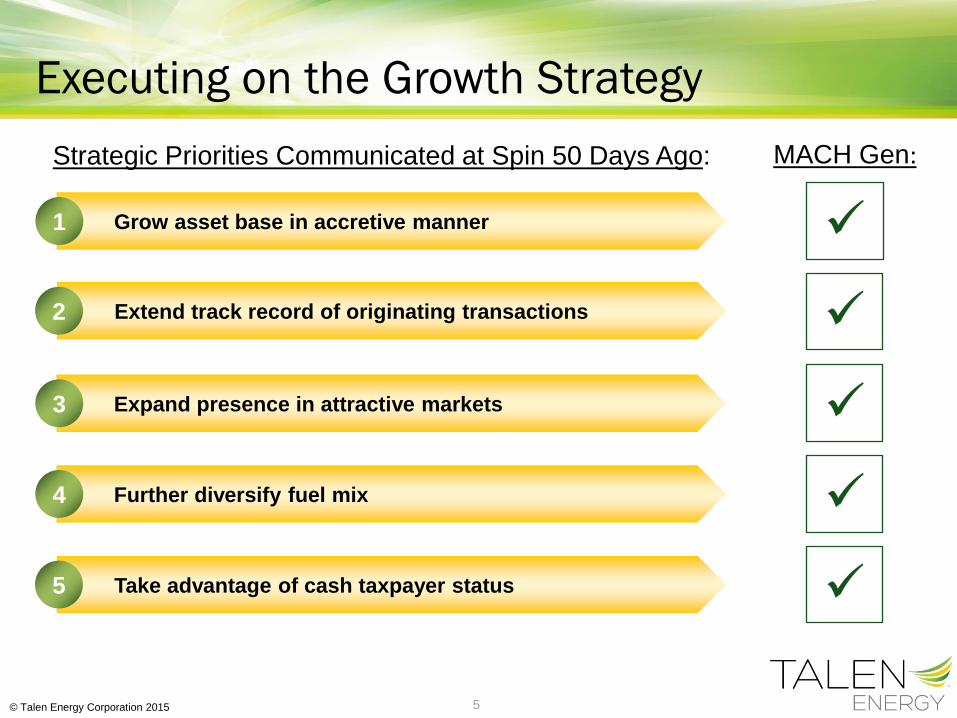

Executing on the Growth Strategy

Grow asset base in accretive manner 1

Extend track record of originating transactions 2

Expand presence in attractive markets 3

Further diversify fuel mix 4

Take advantage of cash taxpayer status 5

Strategic Priorities Communicated at Spin 50 Days Ago: MACH Gen:

© Talen Energy Corporation 2015 6

Transaction Highlights

Acquiring 2.5 GW MACH Gen portfolio for $1.175 billion, in a

negotiated deal, including significant tax attributes

Achieving goal of growth in key markets and fuel diversity with high

quality assets

Efficient Siemens 501G machines, with fleet benefits to Talen Energy’s

Ironwood and Lower Mount Bethel stations

Substantial, immediate free cash flow accretion of over 10%

Significant value from optimizing the Harquahala station

Fleet Diversification + Immediate Cash Flow Accretion

(1) Includes $13 million of inventory

(2) Based upon projected 2016E Adjusted Free Cash Flow assuming close by 12/31/2015

(2)

(1)

© Talen Energy Corporation 2015 7

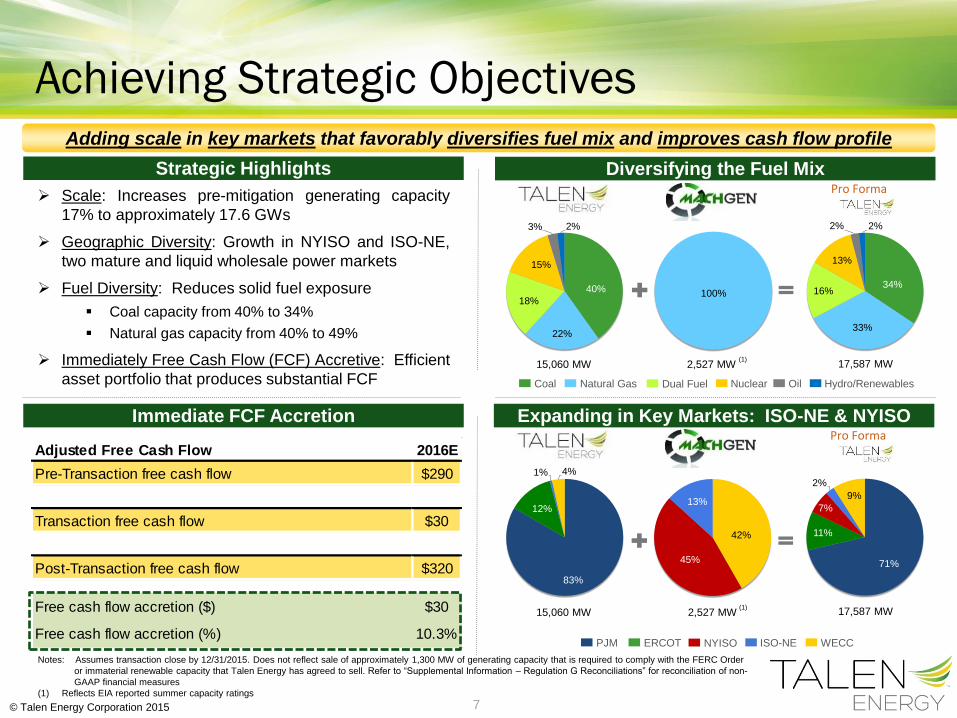

Adjusted Free Cash Flow 2016E

Pre-Transaction free cash flow $290

Transaction free cash flow $30

Post-Transaction free cash flow $320

Free cash flow accretion ($) $30

Free cash flow accretion (%) 10.3%

40%

22%

18%

15%

3% 2%

Pro Forma

34%

33%

16%

13%

2% 2%

Strategic Highlights

Immediate FCF Accretion

Adding scale in key markets that favorably diversifies fuel mix and improves cash flow profile

Scale: Increases pre-mitigation generating capacity

17% to approximately 17.6 GWs

Geographic Diversity: Growth in NYISO and ISO-NE,

two mature and liquid wholesale power markets

Fuel Diversity: Reduces solid fuel exposure

Coal capacity from 40% to 34%

Natural gas capacity from 40% to 49%

Immediately Free Cash Flow (FCF) Accretive: Efficient

asset portfolio that produces substantial FCF

Expanding in Key Markets: ISO-NE & NYISO

Achieving Strategic Objectives

Diversifying the Fuel Mix Pro Forma

15,060 MW 2,527 MW 17,587 MW

Coal Natural Gas Nuclear Oil Hydro/Renewables

15,060 MW 2,527 MW 17,587 MW

Notes: Assumes transaction close by 12/31/2015. Does not reflect sale of approximately 1,300 MW of generating capacity that is required to comply with the FERC Order

or immaterial renewable capacity that Talen Energy has agreed to sell. Refer to “Supplemental Information – Regulation G Reconciliations” for reconciliation of non-

GAAP financial measures

(1) Reflects EIA reported summer capacity ratings

Dual Fuel

PJM ERCOT ISO-NE WECC NYISO

83%

12%

1% 4%

100%

71%

11%

7%

2%

9%

42%

45%

13%

(1)

(1)

© Talen Energy Corporation 2015 8

MACH Gen Overview

© Talen Energy Corporation 2015 9

Athens Millennium Harquahala

Capacity (MW) 1,080 360 1,092

COD June 2004 April 2001 September 2004

Facility Type Combined Cycle Combined Cycle Combined Cycle

Equipment Siemens 501G Siemens 501G Siemens 501G

Configuration 3-1 CT x 1 ST 1 CT x 1 ST 3-1 CT x 1 ST

Heat Rate

(Btu/kWh)7,100 6,975 7,100

Portfolio Highlights

Portfolio Metrics Facilities Overview

MACH Gen Portfolio Diverse Geographic Footprint

3

1 2

AZ

ME

NH

CT NY

MA

RI

VT

1 2 3 2014 Generation – 5,794GWh Capacity – 2,532MW

Attractive low heat rate CCGT portfolio of scale with

over 2.5 GW of generating capacity

Relatively new portfolio with well maintained units

CODs ranging from 2001 - 2004

Proven operating track record – substantial past

investment to improve operations and reliability has

resulted in a 3 year availability factor of over 93%

Well-positioned to benefit from infrastructure

developments and improving market dynamics

23%

46%

31%

Athens Millennium Harquahala

(1) Based on nominal capacity ratings

(1)

43%

43%

14%

(1)

© Talen Energy Corporation 2015 10

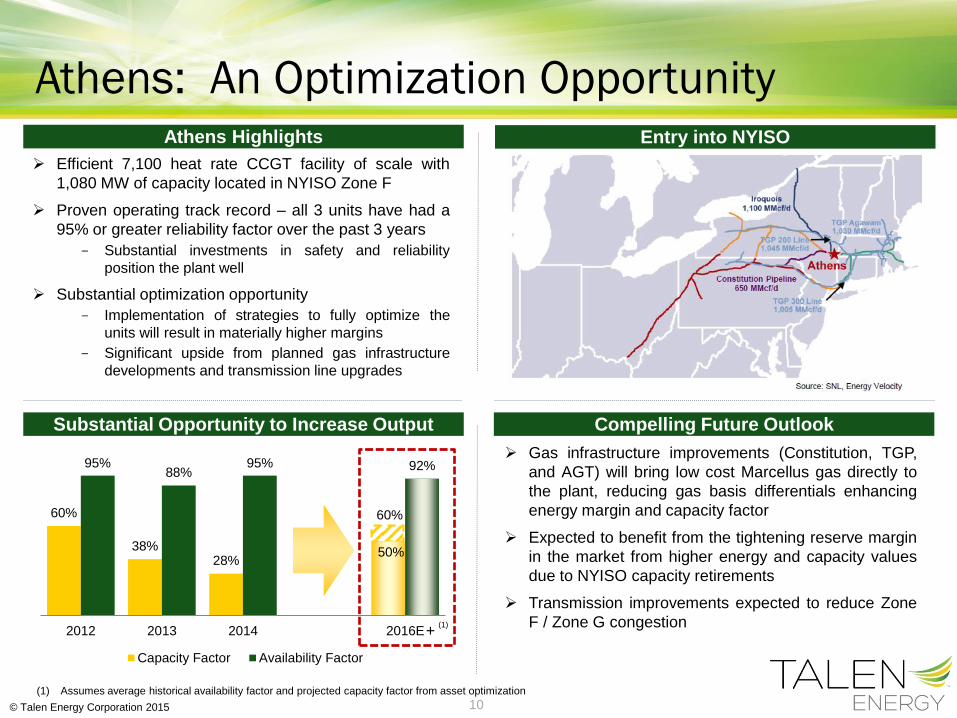

Athens Highlights

Substantial Opportunity to Increase Output Compelling Future Outlook

Athens: An Optimization Opportunity Entry into NYISO

Efficient 7,100 heat rate CCGT facility of scale with

1,080 MW of capacity located in NYISO Zone F

Proven operating track record – all 3 units have had a

95% or greater reliability factor over the past 3 years

- Substantial investments in safety and reliability

position the plant well

Substantial optimization opportunity

- Implementation of strategies to fully optimize the

units will result in materially higher margins

- Significant upside from planned gas infrastructure

developments and transmission line upgrades

Gas infrastructure improvements (Constitution, TGP,

and AGT) will bring low cost Marcellus gas directly to

the plant, reducing gas basis differentials enhancing

energy margin and capacity factor

Expected to benefit from the tightening reserve margin

in the market from higher energy and capacity values

due to NYISO capacity retirements

Transmission improvements expected to reduce Zone

F / Zone G congestion

60%

+ (1)

(1) Assumes average historical availability factor and projected capacity factor from asset optimization

60%

38%28%

50%

95%88%

95% 92%

2012 2013 2014 2016E

Capacity Factor Availability Factor

© Talen Energy Corporation 2015 11

Millennium Highlights

Historically Solid Availability and Output Strong Market Fundamentals & Outlook

Millennium: Highly Attractive CCGT in ISO-NE Adding a well-positioned Asset in ISO-NE

Efficient sub-7,000 heat rate CCGT plant with 360 MW

of capacity located in ISO-NE

Proven operating track record – 97% or greater

reliability factor over the past 3 years

Plant node pricing substantially correlated to Mass

Hub, reducing basis risk

ISO-NE has adopted a number of constructive market

reforms, including capacity performance incentives,

improved day-ahead market modeling and the

adoption of a sloped demand curve, which should drive

long-term pricing to reflect new build costs

Favorable supply and demand dynamics, including the

retirement of aging plants, phase out of nuclear

generation and no significant construction in progress

have resulted in tight capacity markets and a marked

shift in pricing

Tennessee and Algonquin gas transmission pipelines

expected to bring low-cost Marcellus gas to

Massachusetts beginning in 2016, with incremental

improvements scheduled through 2018

65%

47%

58%

89% 88% 90%

2012 2013 2014

Capacity Factor Availability Factor

© Talen Energy Corporation 2015 12

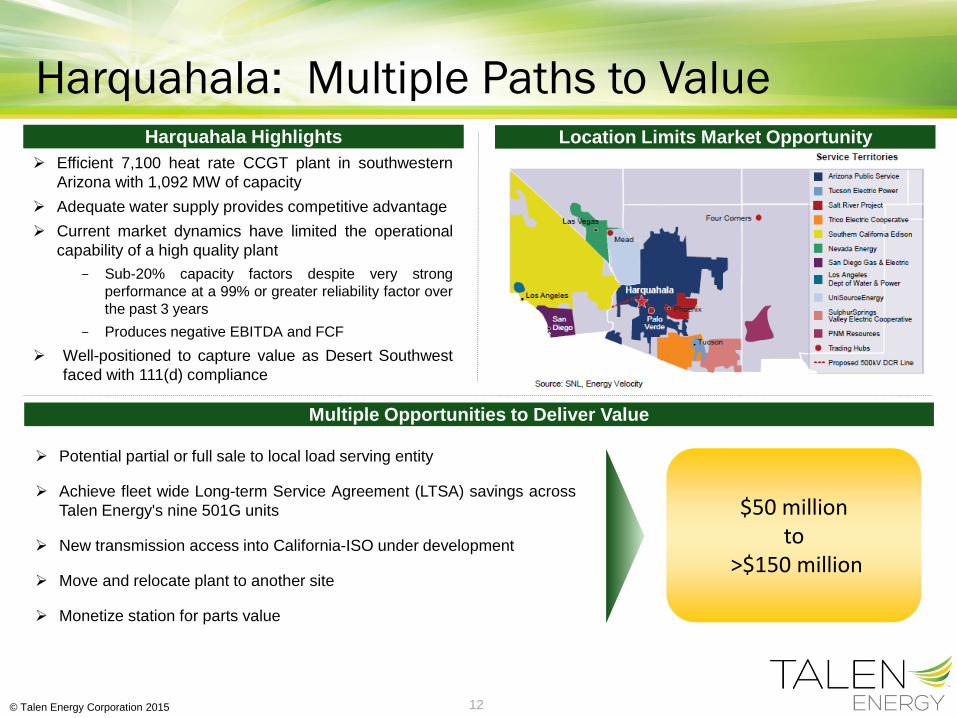

Harquahala Highlights

Multiple Opportunities to Deliver Value

Harquahala: Multiple Paths to Value Location Limits Market Opportunity

Efficient 7,100 heat rate CCGT plant in southwestern

Arizona with 1,092 MW of capacity

Adequate water supply provides competitive advantage

Current market dynamics have limited the operational

capability of a high quality plant

- Sub-20% capacity factors despite very strong

performance at a 99% or greater reliability factor over

the past 3 years

- Produces negative EBITDA and FCF

Well-positioned to capture value as Desert Southwest

faced with 111(d) compliance

$50 million to

>$150 million

Potential partial or full sale to local load serving entity

Achieve fleet wide Long-term Service Agreement (LTSA) savings across

Talen Energy's nine 501G units

New transmission access into California-ISO under development

Move and relocate plant to another site

Monetize station for parts value

© Talen Energy Corporation 2015 13

Financial Considerations

© Talen Energy Corporation 2015 14

Purchase Price $1,175

Less Inventory Value (13)

Net Purchase Price 1,162

2016 EV / EBITDA ($120) 9.7x

Implied $ / kW 459

Implied $ / kW, excluding Harquahala 807

Tax Attribute Value

Net Purchase Price $1,162

Less NPV of Tax Attributes (245)

Adjusted Purchase Price 917

2016 EV / EBITDA ($120) 7.6x

Implied $ / kW 362

Implied $ / kW, excluding Harquahala 637

Harquahala Monetized

Adjusted Purchase Price $917

Less Monetization of Harquahala (50) (150)

Net Price for Athens and Millennium 867 767

2016 EV / EBITDA, excluding Harquahala ($130) 6.7x 5.9x

Implied $ / kW, excluding Harquahala 602 533

Compelling Value

Nominal purchase price of $1,162

million net of inventory implies an

EV / 2016 EBITDA multiple of 9.7x A

Deducting the PV of tax attributes

reduces the asset purchase price

to $917 million which is 7.6x 2016E

EBITDA

B

C

Monetizing Harquahala and

removing its negative EBITDA

contribution results in multiples in

the low-to-mid 6.0x EV / 2016

EBITDA range

Tax attributes and Harquahala offer significant value,

driving the purchase price to a considerable discount

to market multiples

Notes: Market data as of July 17, 2015. Peer multiples based upon EBITDA per FactSet consensus estimates.

Implied $ / kW based on nominal capacity ratings

($ millions)

Peer Trading Multiples 2016 2017

Calpine 8.8x 8.6x

Dynegy 7.5x 7.6x

NRG 8.7x 9.2x

© Talen Energy Corporation 2015 15

($ in millions) Pre-Transaction Post-Transaction

EBITDA:

2016E Adjusted EBITDA $885 $1,005

2016E Adjusted EBITDA, including special items $840 $960

Free Cash Flow:

2016E Adjusted Free Cash Flow $290 $320

2016E Adjusted Free Cash Flow, including special items $263 $293

Projected Net Debt Outstanding at 12/31/2015 $3,700 $4,875

Projected Net Debt / 2016E Adjusted EBITDA 4.2x 4.9x

2016 EBITDA & FCF Projections

Notes: Assumes transaction close by 12/31/2015. Does not reflect sale of approximately 1.3 GW of generating capacity that is required to comply with FERC

order approving Talen Energy transaction. Refer to “Supplemental Information – Regulation G Reconciliations” for reconciliation of non-GAAP

financial measures

(1) Special items include Transition Service Agreements from Talen Energy transaction and restructuring costs

(2) Does not include growth capex of $85 million

(3) Includes projection of $170 million in short-term debt outstanding

(1) (2)

(2)

(3)

(1)

© Talen Energy Corporation 2015 16

Transaction Financing

Purchase price backed by committed acquisition facility

- Sized to accommodate full purchase price should MACH Gen debt not

remain in place

Committed

Acquisition

Facility

Permanent

Financing

Plan

Total $1.175 billion purchase price to be financed with debt

MACH Gen debt may be retained provided waiver on

change of control achieved - Expected balance of approximately $565 million at time of closing

- Cash required at closing dependent upon MACH Gen debt balance

Will consider secured and/or unsecured debt - Final financing plan will take into consideration market conditions,

amount of the existing MACH Gen debt to be retained as well as

expected proceeds from FERC mitigation sales and other pending

divestitures

- May approach market ahead of closing

Strategic and Prudent Use of Balance Sheet

© Talen Energy Corporation 2015 17

Regulatory Approvals and Expected Timeline

Principal Required Approvals

Required Approval Expected Timing

Federal Energy Regulatory Commission (FERC) 3-4 months

NY Public Service Commission 3-4 months

Hart-Scott-Rodino – Federal Trade Commission (FTC) / Department of Justice (DOJ) 1-2 months

(1)

(1) An additional 3-4 months could be added for certain supplementary filings if change of control waiver is not obtained from MACH Gen’s lender

and facility is pledged in support of acquisition financing

© Talen Energy Corporation 2015 18

Closing Remarks

© Talen Energy Corporation 2015 19

Executing Talen Energy’s Strategy

Grow asset base in accretive manner 1

Extend track record of originating transactions 2

Expand presence in attractive markets 3

Further diversify fuel mix 4

Take advantage of cash taxpayer status 5

Strategic Priorities Communicated at Spin 50 Days Ago: MACH Gen:

© Talen Energy Corporation 2015 20

Supplemental Information

© Talen Energy Corporation 2015 21

Transaction Terms and Timing

On July 18, 2015, Talen Energy Supply, LLC entered into an agreement to acquire MACH

Gen, LLC for $1.175 billion including value of existing debt assumed

Transaction &

Purchase Price

Financing

Plan

Regulatory

Approvals

Timing

Federal: FERC and antitrust clearance under Hart-Scott-Rodino

State: New York Public Service Commission

Expected to close by end of 2015

Citi has provided committed debt financing sufficient to fund the purchase price

Considering retaining Mach Gen's existing term loan in combination with new secured or

unsecured debt issued at Talen Energy Supply, LLC

The final financing plan will take into consideration market conditions and the amount of

existing MACH Gen debt to be retained, as well as expected proceeds from FERC

mitigation sales and other pending divestitures

(1) Includes $13 million of inventory

(1)

© Talen Energy Corporation 2015 22

MACH Gen Asset Overview Athens Millennium Harquahala

Location Athens, NY

Nominal

Capacity

1,080 MW

COD June 2004

Heat Rate 7,100 Btu/kWh

Market NYISO

Trading Hub NYISO Zone F

Capacity NYISO Rest-of-State

Primary Fuel Natural Gas

Gas

Interconnection

Iroquois Gas

Facility Type Combined-Cycle

Configuration 3–1 CT x 1 ST

Key Equipment 3 Siemens 501G CTs

3 Nooter Eriksen HRSGs

3 Siemens STs

Site 42-acre parcel

Location Charlton, MA

Nominal

Capacity

360 MW

COD April 2001

Heat Rate 6,975 Btu/kWh

Market ISO-NE

Trading Hub Mass Hub

Capacity ISO-NE Rest-of-Pool

Primary Fuel Natural Gas

Gas

Interconnection

Tennessee Gas

Facility Type Combined-Cycle

Configuration 1 CT x 1 ST

Key Equipment 1 Siemens 501G CTs

1 Nooter Eriksen HRSGs

1 Siemens STs

Site 13-acre parcel

Location Tonopah, AZ

Nominal

Capacity

1,092 MW

COD September 2004

Heat Rate 7,100 Btu/kWh

Market AZ-NM-SNV

Trading Hub Palo Verde

Fuel Natural Gas

Gas

Interconnection

El Paso

Facility Type Combined-Cycle

Configuration 3–1 CT x 1 ST

Key Equipment 3 Siemens 501G CTs

3 NEM HRSGs

3 Siemens STs

Site 640 acres

Water Supply Five on-site wells

Existing delivery agreements with

CAWCD / HVID

Reliability and Availability Factors Reliability and Availability Factors Reliability and Availability Factors

99.5% 98.9% 98.0%

94.6%

87.8%

94.6%

2012 2013 2014

Reliability Factor Availability Factor

99.6% 99.0% 98.4%

88.9% 88.2%90.3%

2012 2013 2014

Reliability Factor Availability Factor

99.7% 99.1% 99.9%

96.8%

93.5%95.5%

2012 2013 2014

Reliability Factor Availability Factor

(1) (1)

(1) Fuel oil capable

© Talen Energy Corporation 2015 23

Regulation G Reconciliations

Adjusted EBITDA

($ in Millions) Pre-Transaction

Midpoint – 2016E

Transaction

Adjustments

Post-Transaction

Midpoint – 2016E

Net Income/(Loss) $105 $2 $107

Income Taxes 56 1 57

Interest Expense 209 81 290

Depreciation & Amortization 422 36 458

EBITDA 792 120 912

Non-Cash Compensation 21 21

ARO 37 37

MTM losses (gains)

NDT losses (gains) (10) (10)

Adjusted EBITDA, including special items 840 120 960

Special items:

TSA costs and allocations 45 45

Adjusted EBITDA $885 $120 $1,005

© Talen Energy Corporation 2015 24

Regulation G Reconciliations

Adjusted Free Cash Flow

($ in Millions) Pre-Transaction

Midpoint – 2016E

Transaction

Adjustments

Post-Transaction

Midpoint – 2016E

Cash from Operations $727 $55 $782

Sustenance Capital Expenditures (464) (25) (489)

Adjusted Free Cash Flow, including special

items 263 30 293

Special items:

TSA costs & allocations (after tax) 27 27

Adjusted Free Cash Flow $290 $30 $320

© Talen Energy Corporation 2015 25

Forward-Looking Information Statement

Statements contained in this presentation, including statements with respect to future earnings, EBITDA results, cash flows, tax

attributes, financing, regulation and corporate strategy are "forward-looking statements" within the meaning of the federal securities

laws. Although Talen Energy Corporation believes that the expectations and assumptions reflected in these forward-looking

statements are reasonable, these statements are subject to a number of risks and uncertainties, and actual results may differ

materially from the results discussed in the statements. Among the important factors that could cause actual results to differ

materially from the forward-looking statements are: market demand and prices for energy, capacity and fuel; weather conditions

affecting customer energy usage and operating costs; competition in power markets; the effect of any business or industry

restructuring; the profitability and liquidity of Talen Energy Corporation and its subsidiaries; new accounting requirements or new

interpretations or applications of existing requirements; operating performance of generating plants and other facilities; unforeseen

difficulties in successfully integrating the MACH Gen power facilities into Talen Energy's portfolio and/or in successfully executing

efforts to optimize the value of the Harquahala plant; unexpected costs or liabilities associated with the MACH Gen power facilities;

the length of scheduled and unscheduled outages at our generating plants; environmental conditions and requirements and the

related costs of compliance, including environmental capital expenditures and emission allowance and other expenses; system

conditions and operating costs; development of new projects, markets and technologies; performance of new ventures; asset or

business acquisitions and dispositions; receipt of necessary governmental permits or approvals; capital market conditions and

decisions regarding capital structure; the impact of state, federal or foreign investigations applicable to Talen Energy Corporation

and its subsidiaries; the outcome of litigation against Talen Energy Corporation and its subsidiaries; stock price performance; the

market prices of equity securities and the impact on pension income and resultant cash funding requirements for defined benefit

pension plans; the securities and credit ratings of Talen Energy Corporation and its subsidiaries; political, regulatory or economic

conditions in states, regions or countries where Talen Energy Corporation or its subsidiaries conduct business, including any

potential effects of threatened or actual terrorism or war or other hostilities; foreign exchange rates; new state, federal or foreign

legislation, including new tax legislation; changes in earnings estimates or buy/sell recommendations by analysts; volatility in market

demand and prices for energy, capacity, transmission services, emission allowances and RECs; competition in retail and wholesale

power and natural gas markets; and the commitments and liabilities of Talen Energy Corporation and its subsidiaries. Any such

forward-looking statements should be considered in light of such important factors and in conjunction with Talen Energy

Corporation's Registration Statement on Form S-1 and its other reports on file with the Securities and Exchange Commission.

© Talen Energy Corporation 2015 26

In this presentation the company presents EBITDA, Adjusted EBITDA and Adjusted EBITDA, including special items,

each of which are non-GAAP financial measures. EBITDA represents net income (loss) before interest expense, income

taxes, depreciation and amortization. Adjusted EBITDA represents EBITDA adjusted for certain items as detailed in the

reconciliation. Adjusted EBITDA, including special items, is Adjusted EBITDA prior to adjustment for items management

considers special including TSA costs, pre-spin PPL charges and restructuring costs. EBITDA, Adjusted EBITDA and

Adjusted EBITDA, including special items, are not intended to represent cash flows from operations or net income (loss)

as defined by U.S. GAAP as indicators of operating performance and are not necessarily comparable to similarly-titled

measures reported by other companies. We believe EBITDA, Adjusted EBITDA and Adjusted EBITDA, including special

items, are useful to investors and other users of our financial statements in evaluating our operating performance

because they provide additional tools to compare business performance across companies and across periods. We

believe that EBITDA is widely used by investors to measure a company’s operating performance without regard to such

items as interest expense, income taxes, depreciation and amortization, which can vary substantially from company to

company depending upon accounting methods and book value of assets, capital structure and the method by which

assets were acquired. Additionally, we believe that investors commonly adjust EBITDA information to eliminate the effect

of restructuring and other expenses, which vary widely from company to company and impair comparability. We adjust for

these and other items as our management believes that these items would distort their ability to efficiently view and

assess our core operating trends.

In summary, our management uses EBITDA, Adjusted EBITDA and Adjusted EBITDA, including special items, as

measures of operating performance to assist in comparing performance from period to period on a consistent basis and

to readily view operating trends, as measures for planning and forecasting overall expectations and for evaluating actual

results against such expectations, and in communications with our Board of Directors, shareholders, creditors, analysts

and investors concerning our financial performance.

Definitions of Non-GAAP Financial Measures

© Talen Energy Corporation 2015 27

Adjusted free cash flow is derived by deducting sustenance capital expenditures and after-tax special items from cash

flow from operations, while adjusted free cash flow, including special items, is derived from adjusted free cash flow prior

to adjustment for after-tax special items. These two non-GAAP measures should not be considered alternatives to cash

flow from operations, which is determined in accordance with GAAP. We believe that adjusted free cash flow and

adjusted free cash flow, including special items, although both non-GAAP measures, are important measures to both

management and investors as indicators of the company’s ability to sustain operations without additional outside

financing beyond the requirement to fund maturing debt obligations. These measures are not necessarily comparable to

similarly-titled measures reported by other companies as they may be calculated differently.

Definitions of Non-GAAP Financial Measures