accounting principles second canadian edition prepared and edited by: carolyn doering, huron heights...

TRANSCRIPT

Accounting Accounting PrinciplesPrinciplesSecond Canadian EditionSecond Canadian Edition

Prepared and Edited by: Carolyn Doering, Huron Heights SS

Weygandt · Kieso · Kimmel · Trenholm

PRESENT VALUE PRESENT VALUE CONCEPTSCONCEPTS

AppendixAppendix

BB

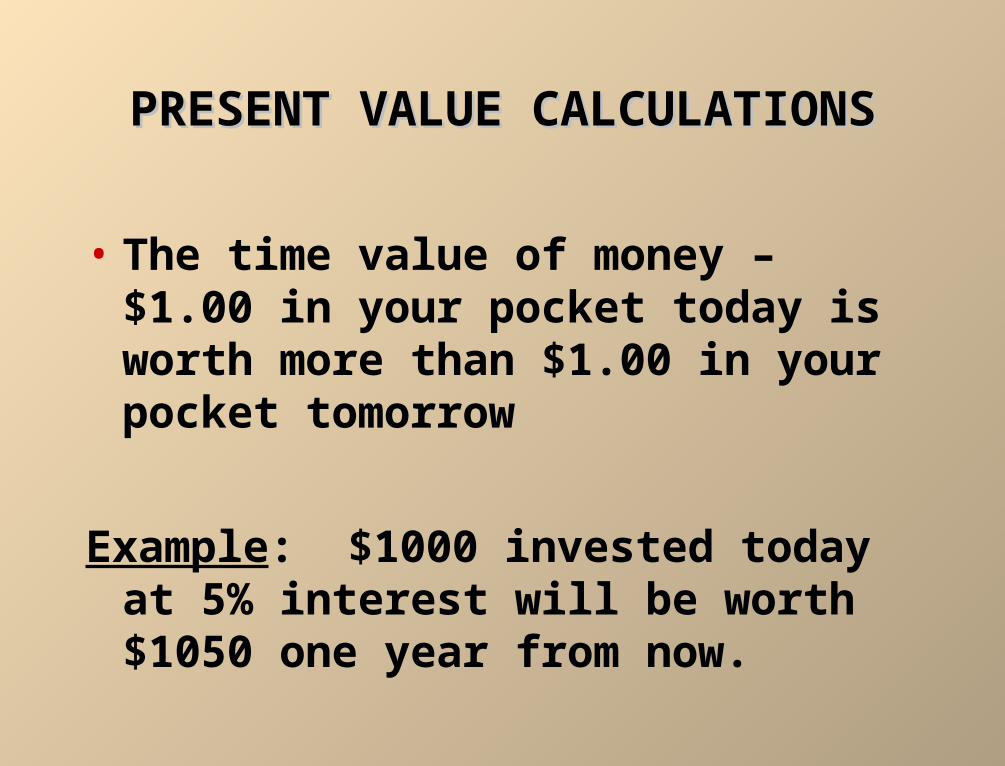

PRESENT VALUE CALCULATIONSPRESENT VALUE CALCULATIONS

• The time value of money – $1.00 in your pocket today is worth more than $1.00 in your pocket tomorrow

Example: $1000 invested today at 5% interest will be worth $1050 one year from now.

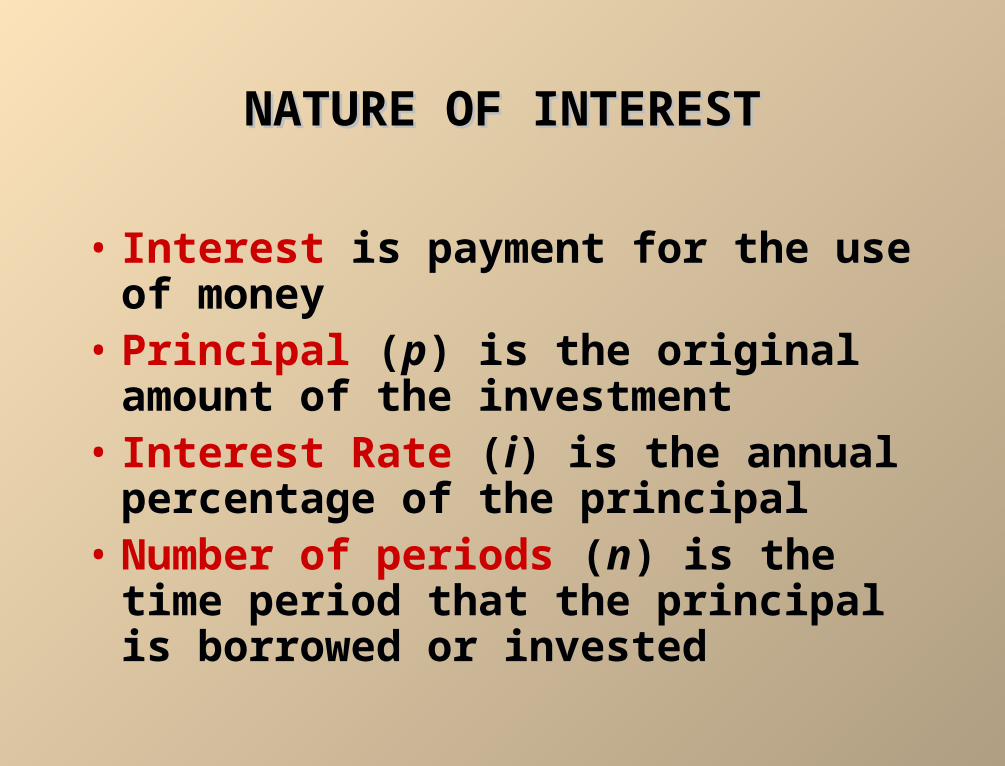

NATURE OF INTERESTNATURE OF INTEREST

• Interest is payment for the use of money• Principal (p) is the original amount of

the investment• Interest Rate (i) is the annual percentage

of the principal• Number of periods (n) is the time period

that the principal is borrowed or invested

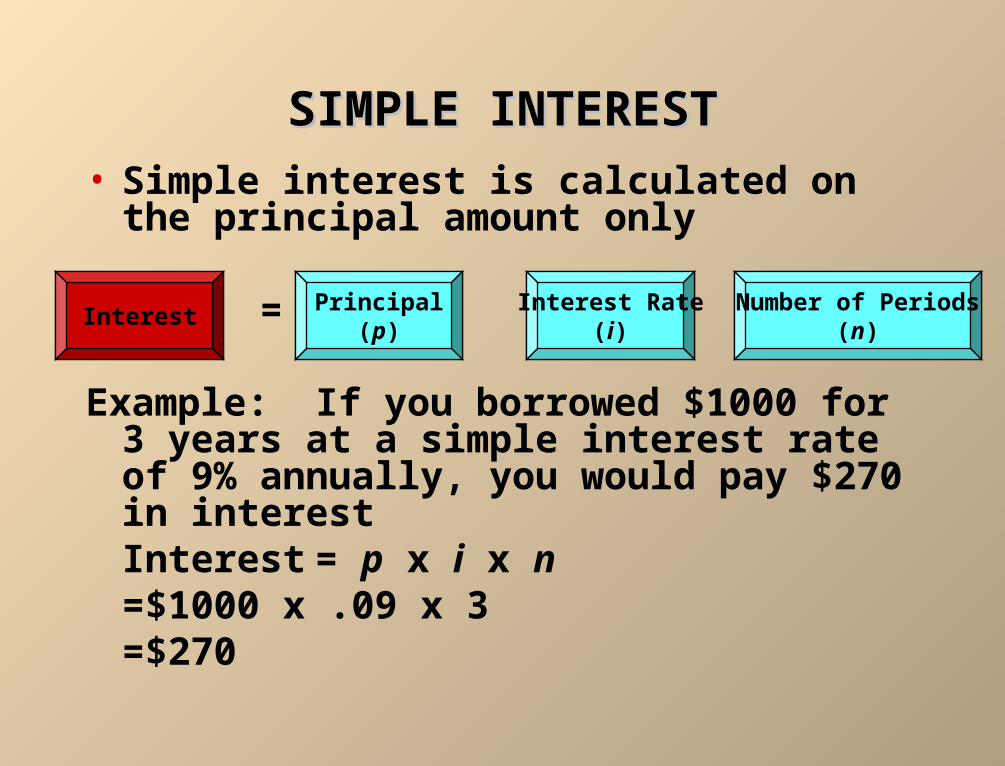

SIMPLE INTERESTSIMPLE INTEREST

• Simple interest is calculated on the principal amount only

= X X

Example: If you borrowed $1000 for 3 years at a simple interest rate of 9% annually, you would pay $270 in interestInterest = p x i x n

=$1000 x .09 x 3=$270

InterestPrincipal

(p)Interest Rate

(i)Number of Periods

(n)

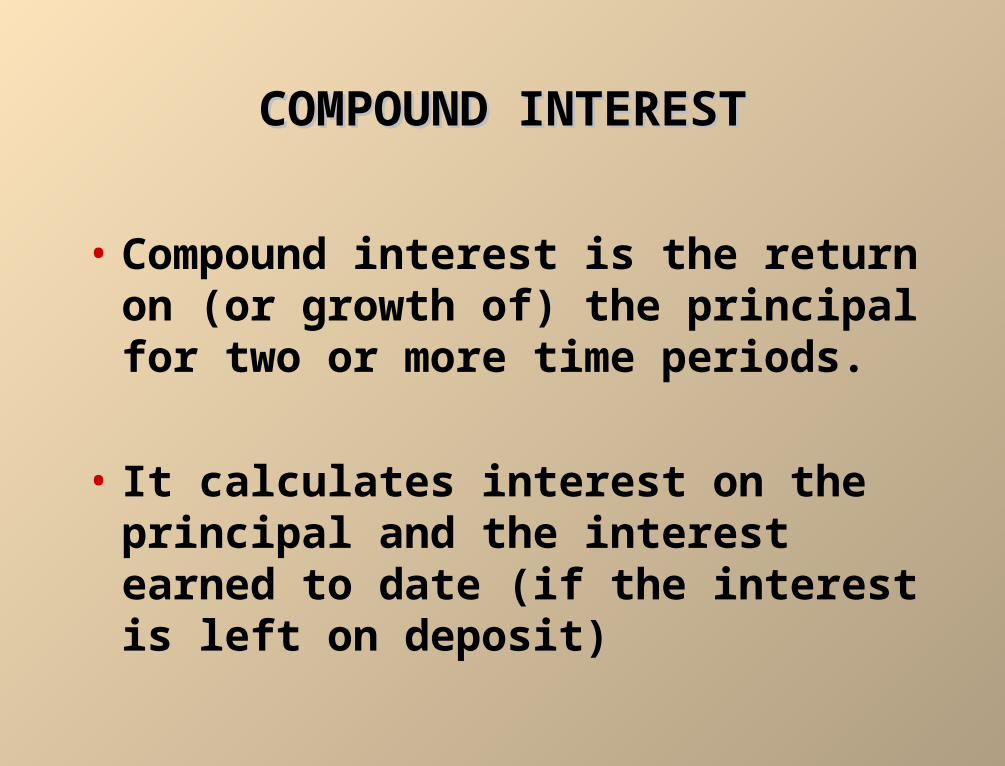

COMPOUND INTERESTCOMPOUND INTEREST

• Compound interest is the return on (or growth of) the principal for two or more time periods.

• It calculates interest on the principal and the interest earned to date (if the interest is left on deposit)

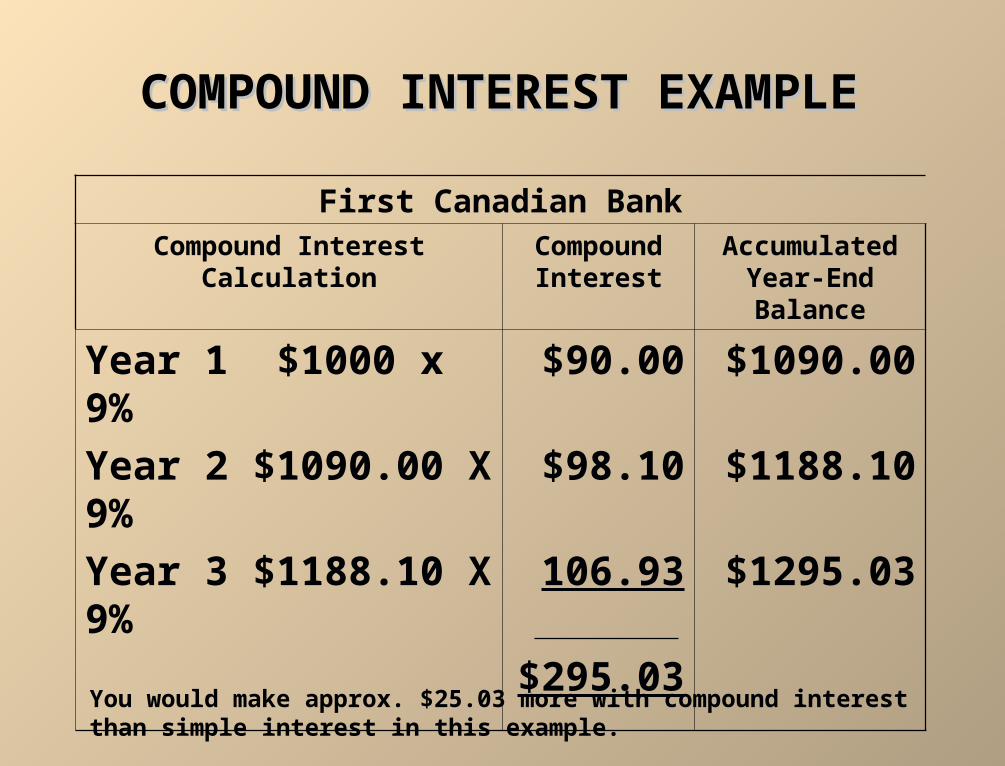

COMPOUND INTEREST EXAMPLECOMPOUND INTEREST EXAMPLE

First Canadian BankCompound Interest Calculation Compound

InterestAccumulated

Year-End Balance

Year 1 $1000 x 9% $90.00 $1090.00

Year 2 $1090.00 X 9% $98.10 $1188.10

Year 3 $1188.10 X 9% 106.93 $1295.03

$295.03

You would make approx. $25.03 more with compound interest than simple interest in this example.

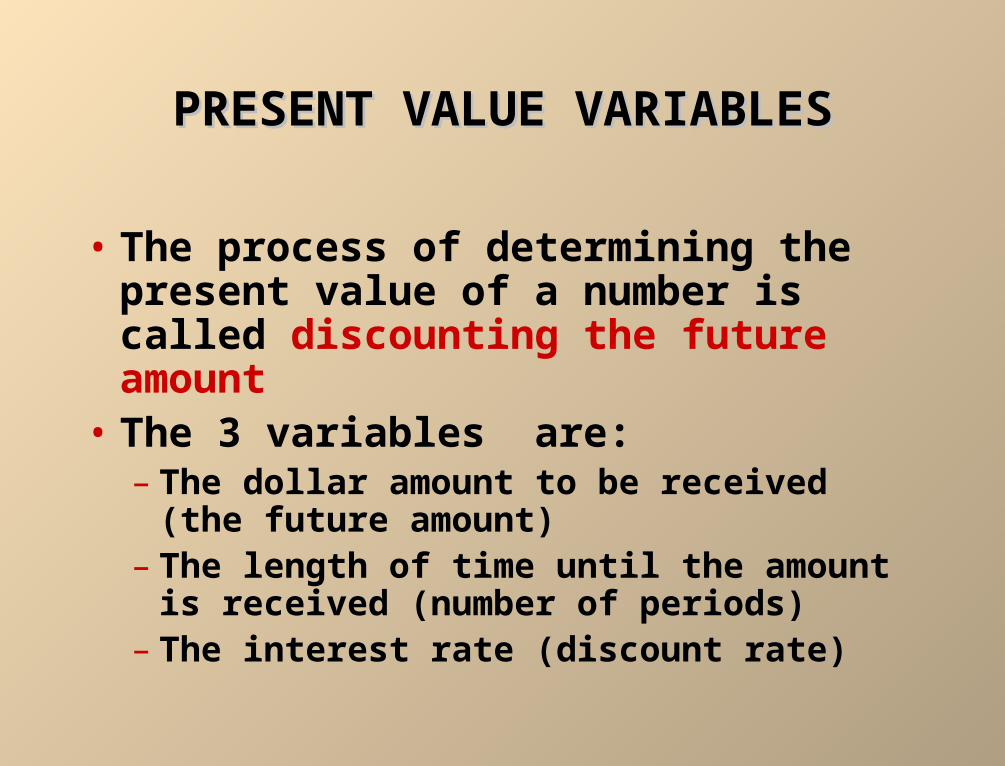

PRESENT VALUE VARIABLESPRESENT VALUE VARIABLES

• The process of determining the present value of a number is called discounting the future amount

• The 3 variables are:– The dollar amount to be received (the future

amount)– The length of time until the amount is

received (number of periods)– The interest rate (discount rate)

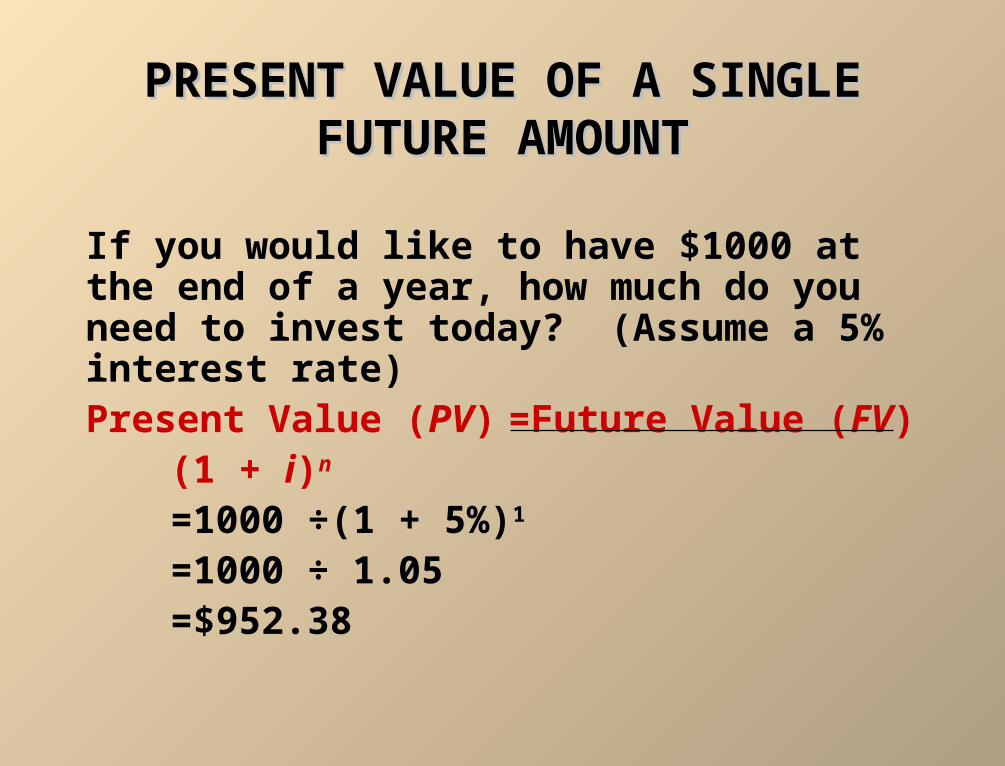

PRESENT VALUE OF A SINGLEPRESENT VALUE OF A SINGLEFUTURE AMOUNTFUTURE AMOUNT

If you would like to have $1000 at the end of a year, how much do you need to invest today? (Assume a 5% interest rate)Present Value (PV)=Future Value (FV)

(1 + i)n

=1000 ÷(1 + 5%)1

=1000 ÷ 1.05=$952.38

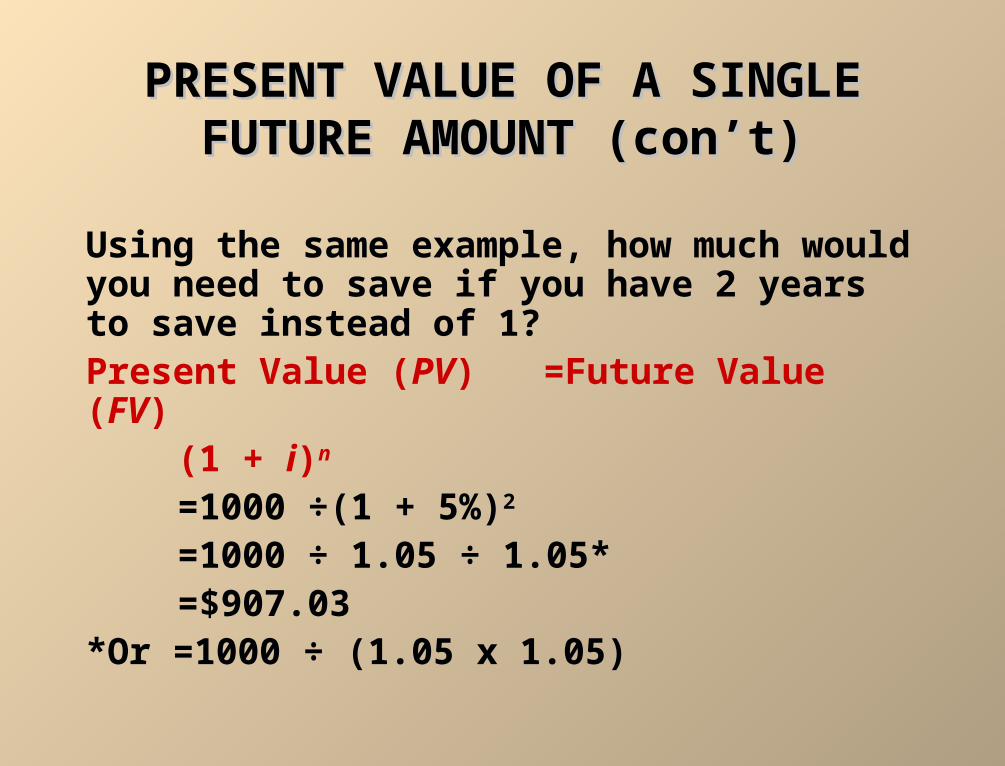

PRESENT VALUE OF A SINGLE PRESENT VALUE OF A SINGLE FUTURE AMOUNT (con’t)FUTURE AMOUNT (con’t)

Using the same example, how much would you need to save if you have 2 years to save instead of 1? Present Value (PV) =Future Value (FV)

(1 + i)n

=1000 ÷(1 + 5%)2

=1000 ÷ 1.05 ÷ 1.05*=$907.03

*Or =1000 ÷ (1.05 x 1.05)

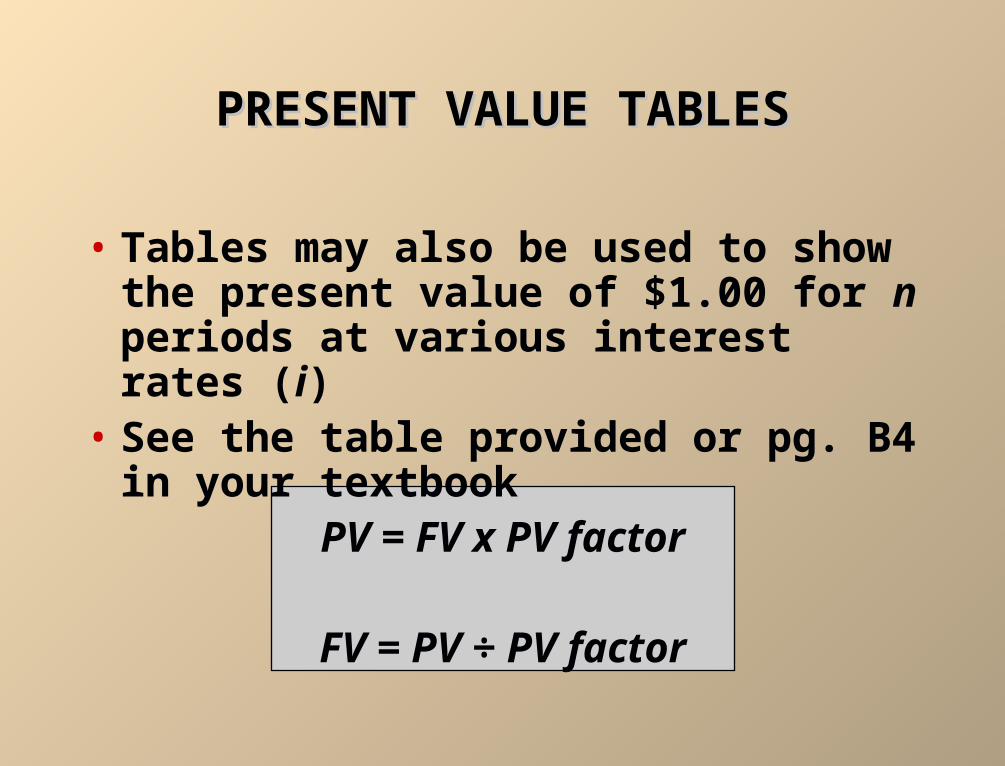

PRESENT VALUE TABLESPRESENT VALUE TABLES

• Tables may also be used to show the present value of $1.00 for n periods at various interest rates (i)

• See the table provided or pg. B4 in your textbook

PV = FV x PV factor

FV = PV ÷ PV factor

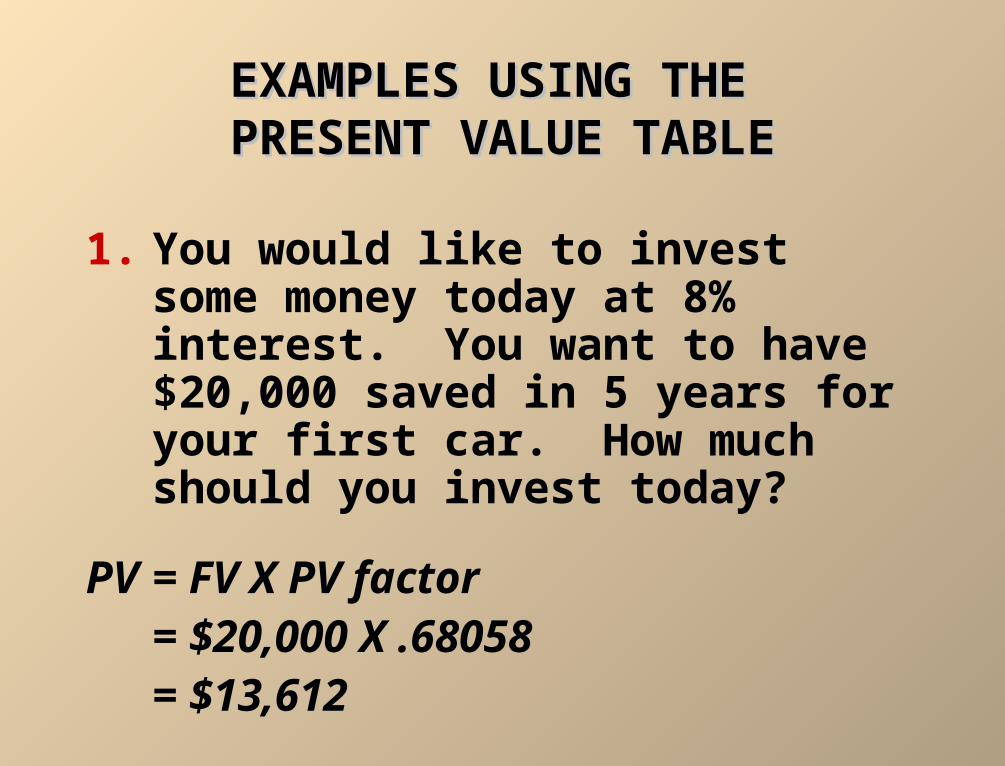

EXAMPLES USING THE EXAMPLES USING THE PRESENT VALUE TABLEPRESENT VALUE TABLE

1. You would like to invest some money today at 8% interest. You want to have $20,000 saved in 5 years for your first car. How much should you invest today?

PV = FV X PV factor= $20,000 X .68058= $13,612

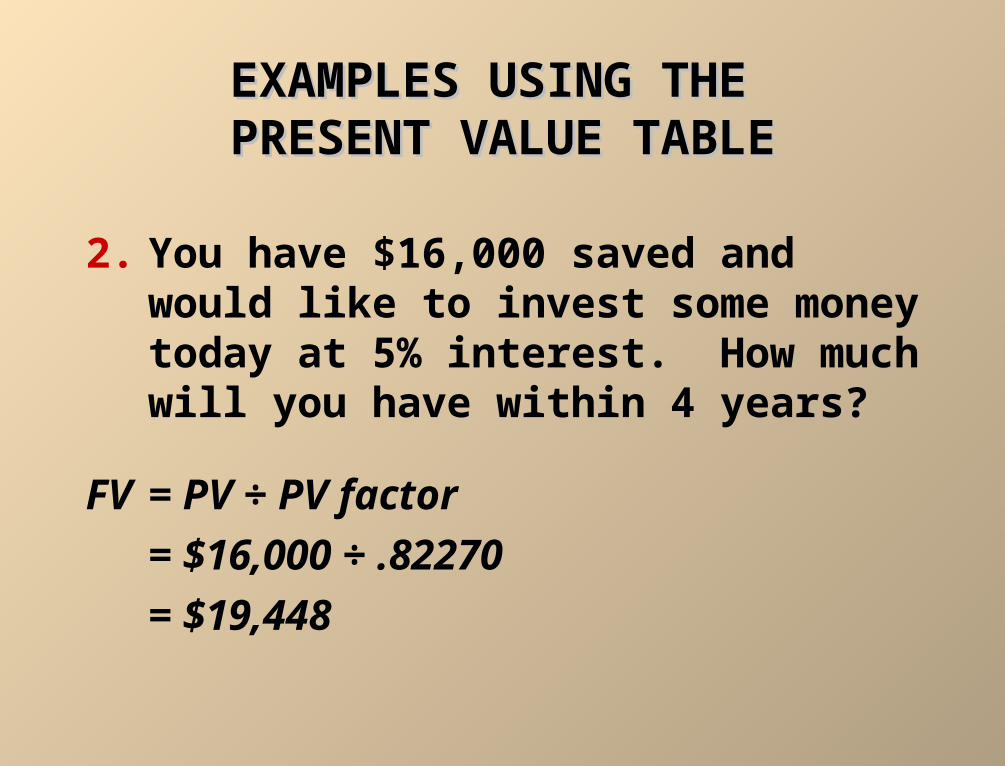

EXAMPLES USING THE EXAMPLES USING THE PRESENT VALUE TABLEPRESENT VALUE TABLE

2. You have $16,000 saved and would like to invest some money today at 5% interest. How much will you have within 4 years?

FV = PV ÷ PV factor

= $16,000 ÷ .82270

= $19,448

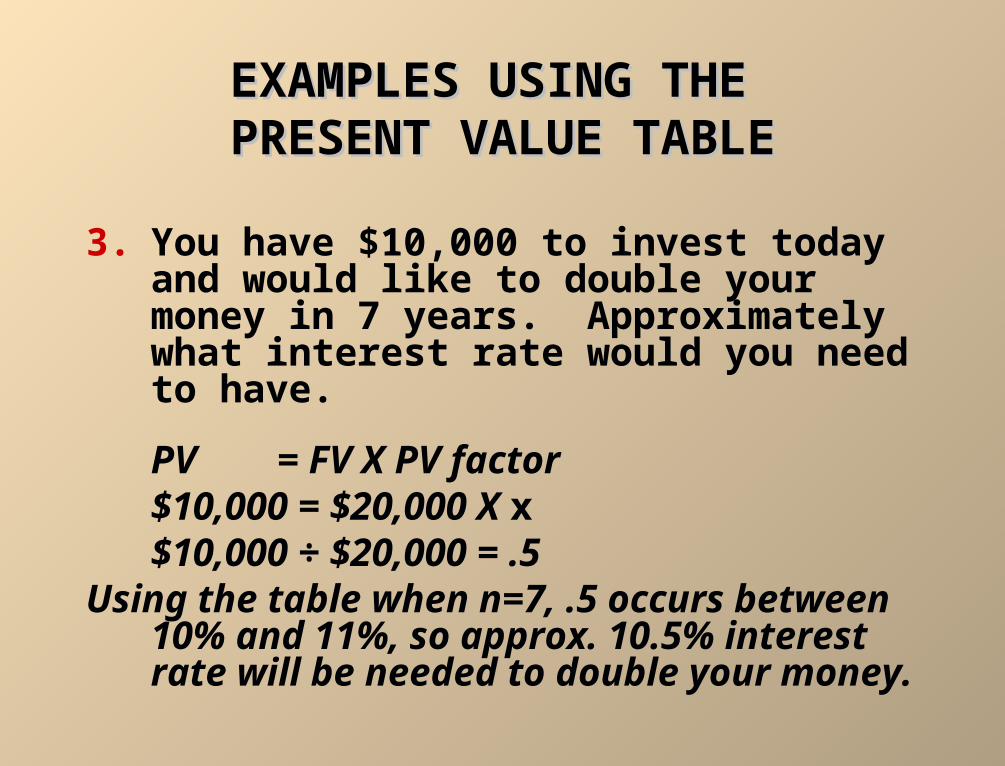

EXAMPLES USING THE EXAMPLES USING THE PRESENT VALUE TABLEPRESENT VALUE TABLE

3. You have $10,000 to invest today and would like to double your money in 7 years. Approximately what interest rate would you need to have.

PV = FV X PV factor$10,000 = $20,000 X x$10,000 ÷ $20,000 = .5

Using the table when n=7, .5 occurs between 10% and 11%, so approx. 10.5% interest rate will be needed to double your money.

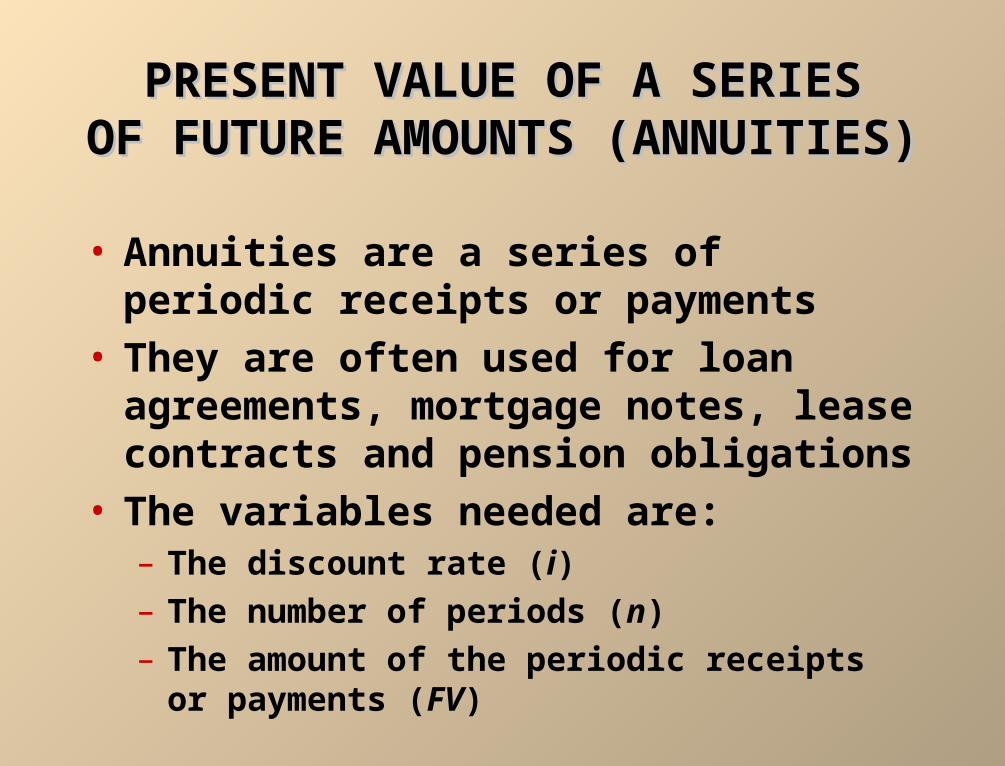

PRESENT VALUE OF A SERIESPRESENT VALUE OF A SERIESOF FUTURE AMOUNTS (ANNUITIES)OF FUTURE AMOUNTS (ANNUITIES)

• Annuities are a series of periodic receipts or payments

• They are often used for loan agreements, mortgage notes, lease contracts and pension obligations

• The variables needed are:– The discount rate (i)– The number of periods (n)– The amount of the periodic receipts or payments

(FV)

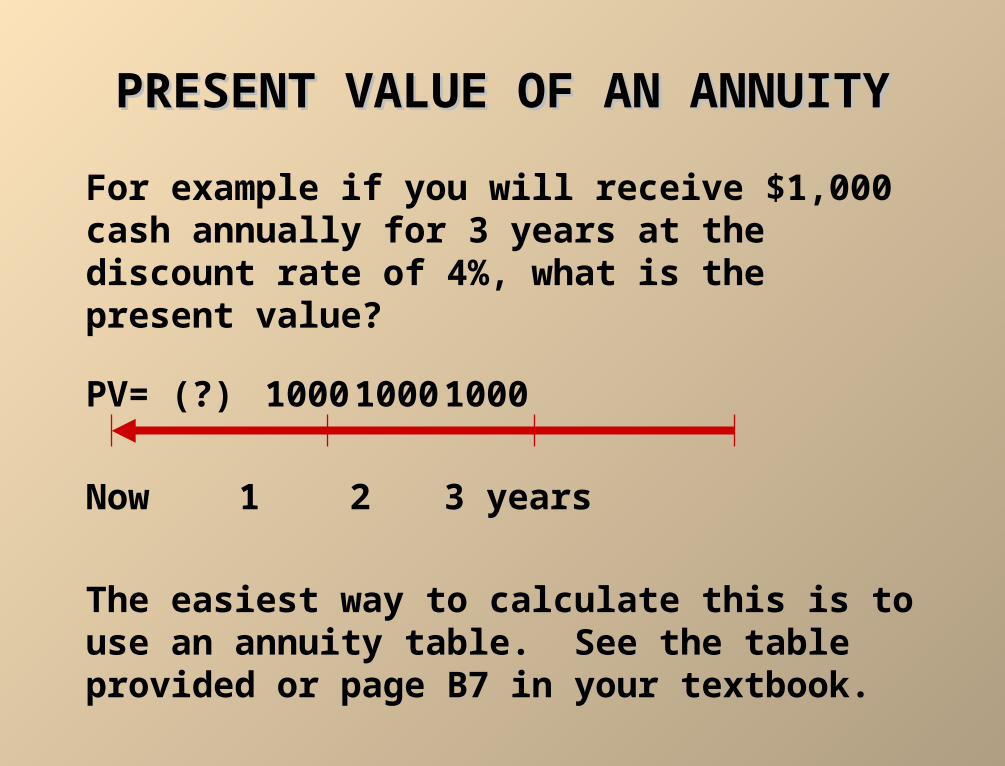

PRESENT VALUE OF AN ANNUITYPRESENT VALUE OF AN ANNUITY

For example if you will receive $1,000 cash annually for 3 years at the discount rate of 4%, what is the present value?

PV= (?) 1000 1000 1000

Now 1 2 3 years

The easiest way to calculate this is to use an annuity table. See the table provided or page B7 in your textbook.

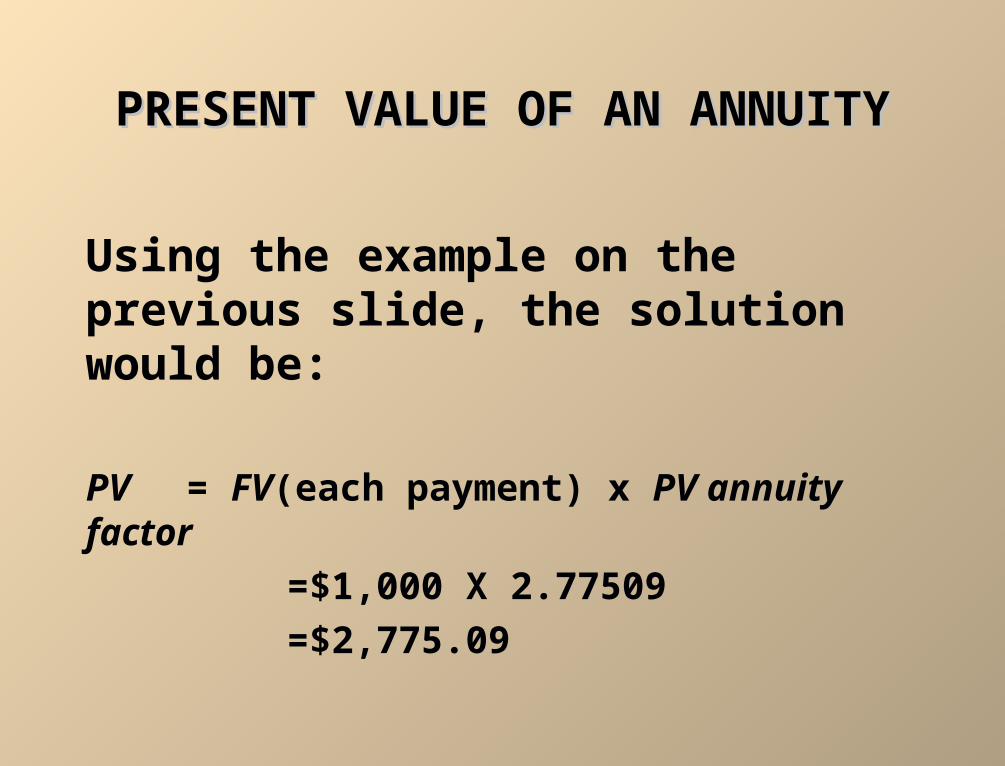

PRESENT VALUE OF AN ANNUITYPRESENT VALUE OF AN ANNUITY

Using the example on the previous slide, the solution would be:

PV = FV(each payment) x PV annuity factor

=$1,000 X 2.77509

=$2,775.09

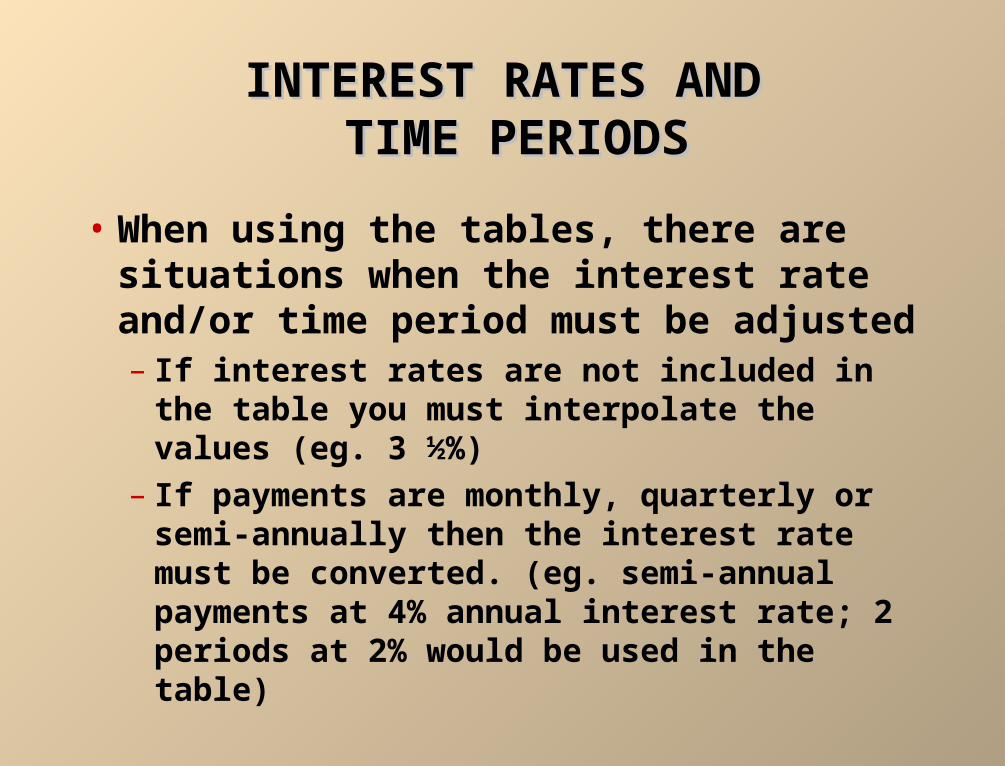

INTEREST RATES ANDINTEREST RATES AND TIME PERIODS TIME PERIODS

• When using the tables, there are situations when the interest rate and/or time period must be adjusted– If interest rates are not included in the table

you must interpolate the values (eg. 3 ½%)

– If payments are monthly, quarterly or semi-annually then the interest rate must be converted. (eg. semi-annual payments at 4% annual interest rate; 2 periods at 2% would be used in the table)

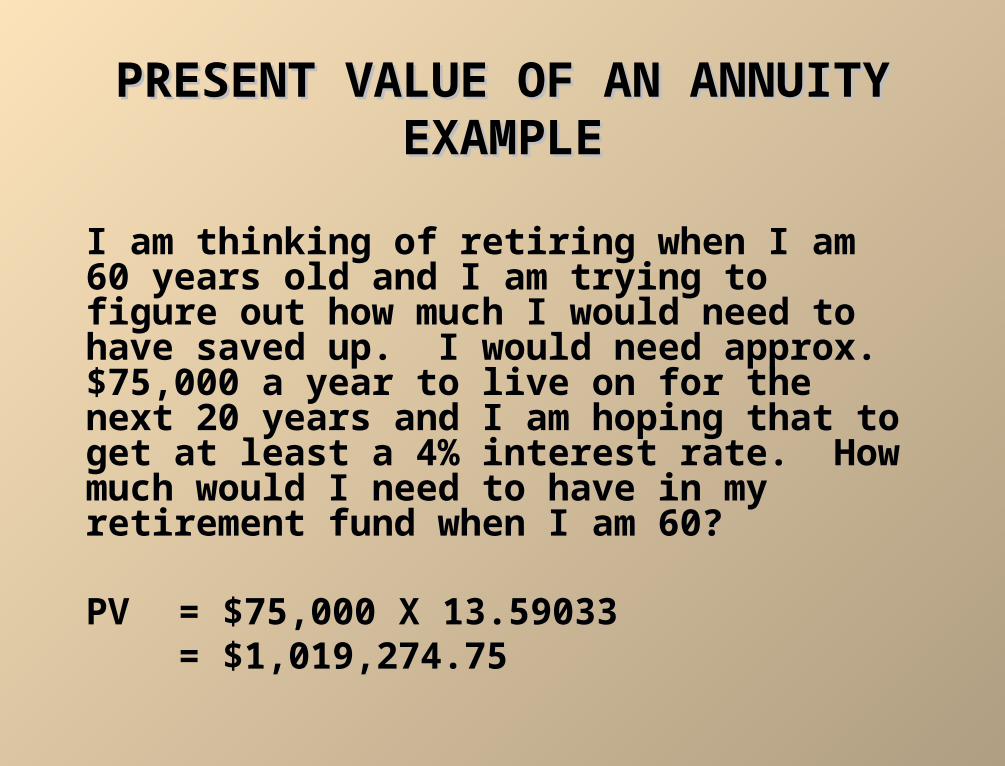

PRESENT VALUE OF AN ANNUITY PRESENT VALUE OF AN ANNUITY EXAMPLEEXAMPLE

I am thinking of retiring when I am 60 years old and I am trying to figure out how much I would need to have saved up. I would need approx. $75,000 a year to live on for the next 20 years and I am hoping that to get at least a 4% interest rate. How much would I need to have in my retirement fund when I am 60?

PV = $75,000 X 13.59033= $1,019,274.75

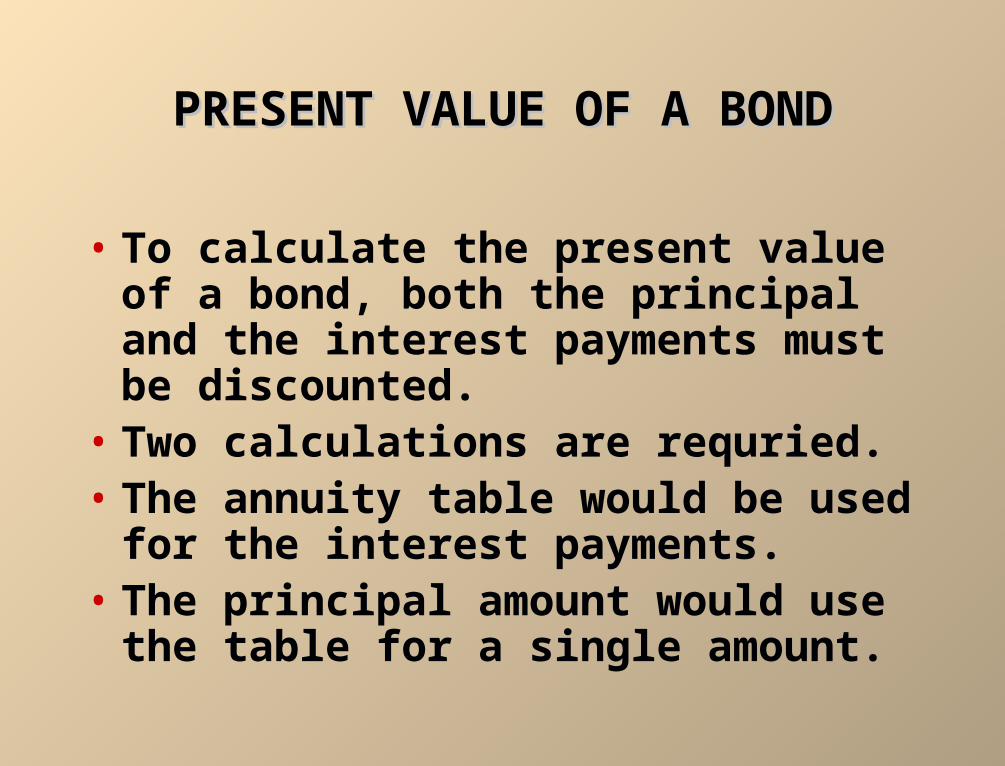

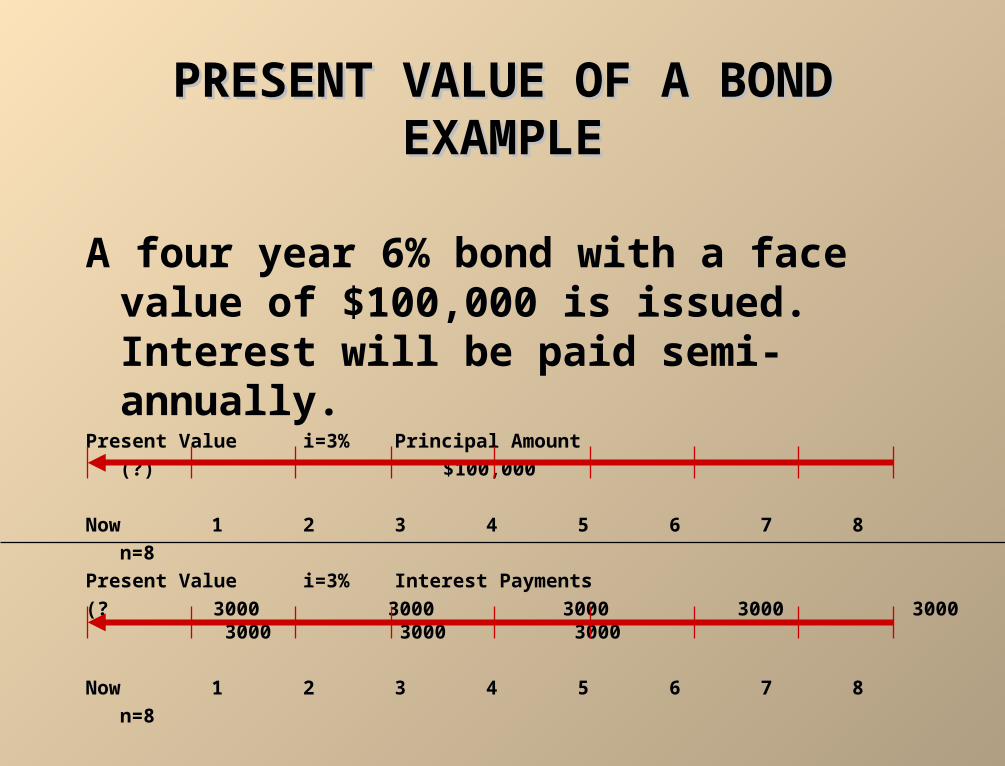

PRESENT VALUE OF A BONDPRESENT VALUE OF A BOND

• To calculate the present value of a bond, both the principal and the interest payments must be discounted.

• Two calculations are requried.• The annuity table would be used for the

interest payments.• The principal amount would use the

table for a single amount.

PRESENT VALUE OF A BONDPRESENT VALUE OF A BONDEXAMPLEEXAMPLE

A four year 6% bond with a face value of $100,000 is issued. Interest will be paid semi-annually.

Present Value i=3% Principal Amount

(?) $100,000

Now 1 2 3 4 5 6 7 8

n=8

Present Value i=3% Interest Payments

(? 3000 3000 3000 3000 3000 3000 3000 3000

Now 1 2 3 4 5 6 7 8

n=8

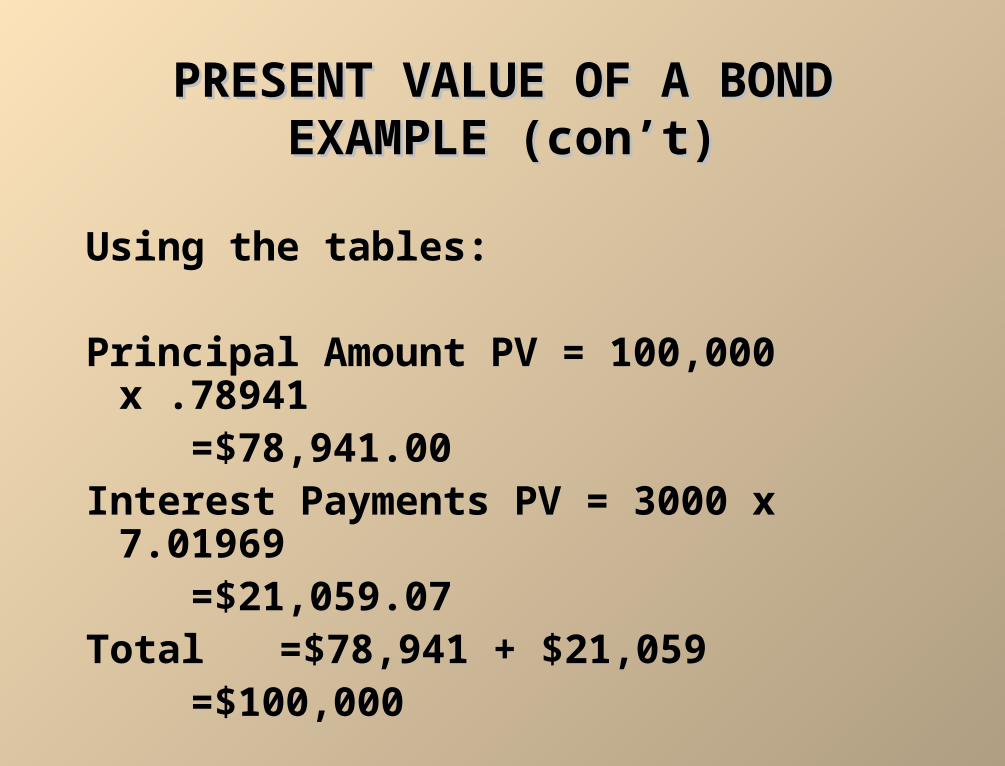

PRESENT VALUE OF A BONDPRESENT VALUE OF A BONDEXAMPLE (con’t)EXAMPLE (con’t)

Using the tables:

Principal Amount PV = 100,000 x .78941 =$78,941.00

Interest Payments PV = 3000 x 7.01969 =$21,059.07

Total =$78,941 + $21,059 =$100,000

COPYRIGHTCOPYRIGHT

Copyright © 2002 John Wiley & Sons Canada, Ltd. All rights reserved. Reproduction or translation of this work beyond that permitted by CANCOPY (Canadian Reprography Collective) is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons Canada, Ltd. The purchaser may make back-up copies for his / her own use only and not for distribution or resale. The author and the publisher assume no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.