accounting is the art of recording, classifying and summarizing in a significant manner and in terms...

TRANSCRIPT

Accounting is the art of recording, classifying and

summarizing in a significant manner and in terms of

money, transactions and events which are, in part at

least, of a financial character, and interpreting the results thereof

1

Who are the users of Accounting information?

1. Management.

2. Users with direct financial interest (investors and creditors).

3. Users with an indirect financial interests (tax

authorities, Regulatory Agencies and others)

2

• Matching Principal.• Continuity.• Historical Cost.• Revenue recognition.• Full Disclosures.

3

• Going Concern.• Periodicity.• Accrual

Accounting• Economic Entity.• Monetary Unit.

Is to provide (report) the required financial information timely to the users (Internal users/ external users).

The financial information1. Assets. All asset accounts have a debit nature2. Liabilities. All liability accounts have a credit nature3. Owners Equity. All equity accounts have a credit nature4. Revenue. All revenue accounts have a credit nature 5. Expenses. All expense accounts have a debit nature

4

• An asset is a resource controlled by the enterprise as a result of past events and from which future economic benefits are expected to flow to the enterprise

• Items of value owned and controlled by the Business– Buildings

– Cash

– Vehicles – equipment

5

1. Assets are resources owned by a business.

2. They are used in carrying out such activities as production, consumption and exchange.

6

Amounts owed by the Business to people or

Organizations : Loans- Creditors/Accounts Payable

Liabilities are claims against assets. They are existing

debts and obligations.

7

Creditors (Accounts Payable) •people or organizations other than the owner to whom the Business owes money.•Usually because of goods or services received which remain unpaid

Creditors are a liability to the business

8

Capital or Investments by Owners - Amounts owed

by the Business to the owner (money and other

items contributed to the business by the owner from

his or her resources ie. CAPITAL)

9

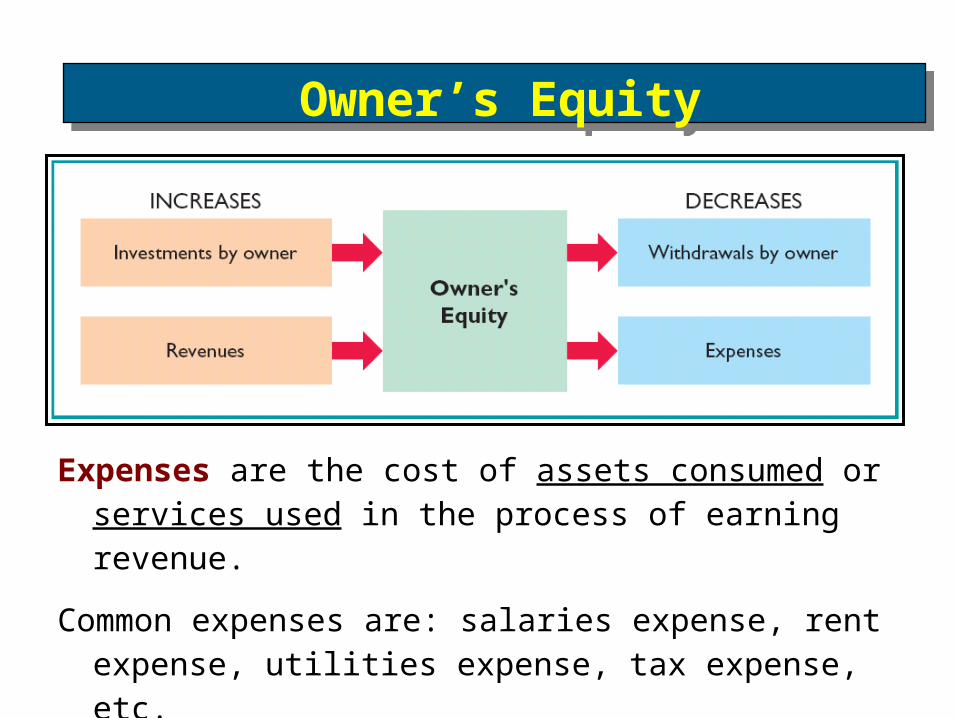

• Investments (assets) increase owner’s equity• Drawings decrease the owner’s equity• Revenues increase the owner’s equity• Expenses decrease owner’s equity

10

• Owner’s Equity is equal to total assets minus total liabilities.

• Owner’s Equity represents the ownership claim on total assets.

11

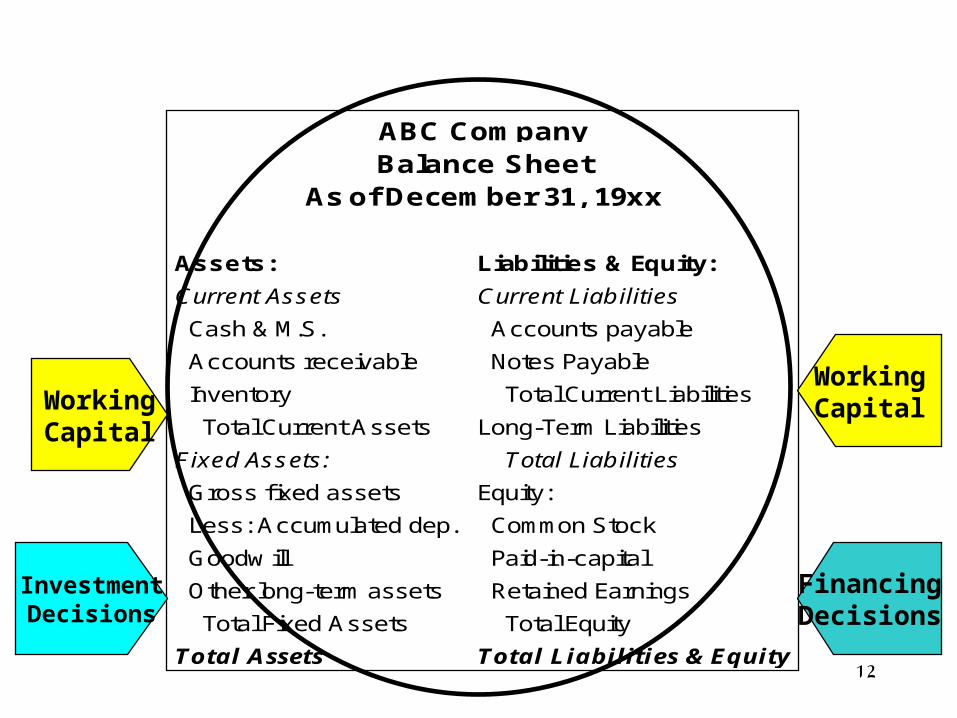

Assets: Liabilities & Equity:

Current Assets Current Liabilities

Cash & M.S. Accounts payable

Accounts receivable Notes Payable

Inventory Total Current Liabilities

Total Current Assets Long-Term Liabilities

Fixed Assets: Total Liabilities

Gross f ixed assets Equity:

Less: Accumulated dep. Common Stock

Goodw ill Paid-in-capital

Other long-term assets Retained Earnings

Total Fixed Assets Total Equity

Total Assets Total Liabilities & Equity

ABC CompanyBalance Sheet

As of December 31, 19xx

WorkingCapital

WorkingCapital

InvestmentDecisions

FinancingDecisions

12

Revenue: Gross inflow of economic benefits resulting from an

enterprise's ordinary activities is considered "revenue" provided

those inflows result in increases in equity.

Revenue. The IASC's framework defines "Income" to include both

revenue and gains.

13

14

Revenues

• Revenue for a given period equals:

Cash + Receivables from goods and services provided.

• Liabilities are generally not affected by revenues.

• A bank loan increases liabilities but is not revenue.

• A collection of accounts receivable increases cash but is not revenue.

• Owner investments increase Owner’s Equity but are not revenues.

If revenues are increases in owner’s equity resulting from selling goods, or rendering services.

Expenses:are decreases in owner’s equity resulting from the costs of selling goods, rendering services or performing other business activities.

15

16

Expenses

• Expenses are the costs of doing business.

• Not all cash payments are expenses.

• Prepaid expenses are recorded as assets. As they expire, they become expenses.

• Purchase of plant assets (e.g. equipment) is not an expense.

• Owner withdrawals are not expenses.

• Payment on a liability is not an expense.

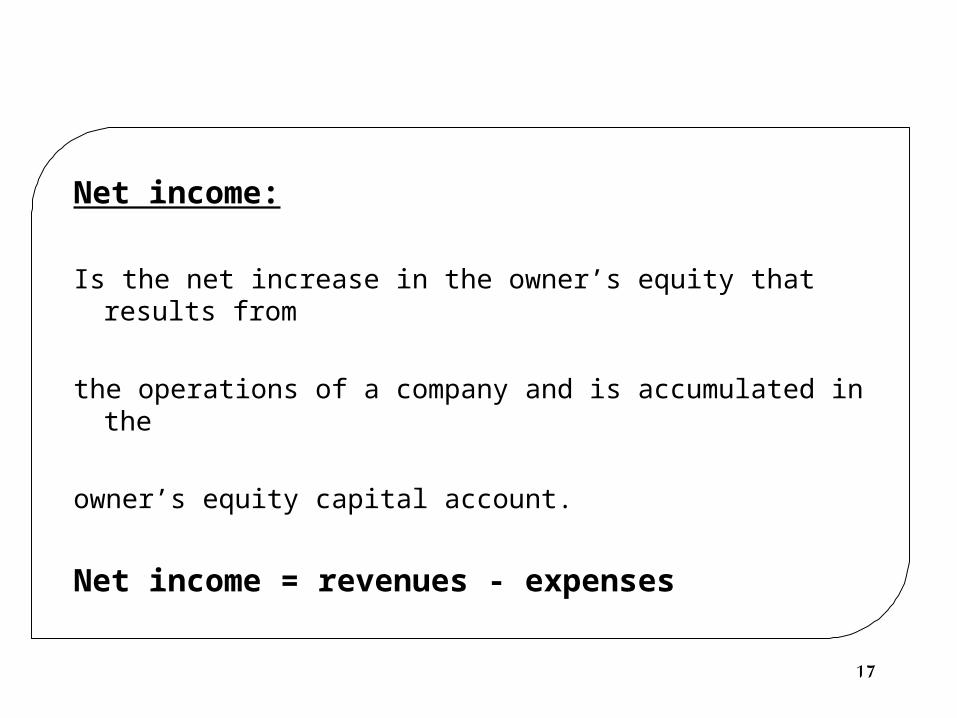

Net income:

Is the net increase in the owner’s equity that results from

the operations of a company and is accumulated in the

owner’s equity capital account.

Net income = revenues - expenses

17

18

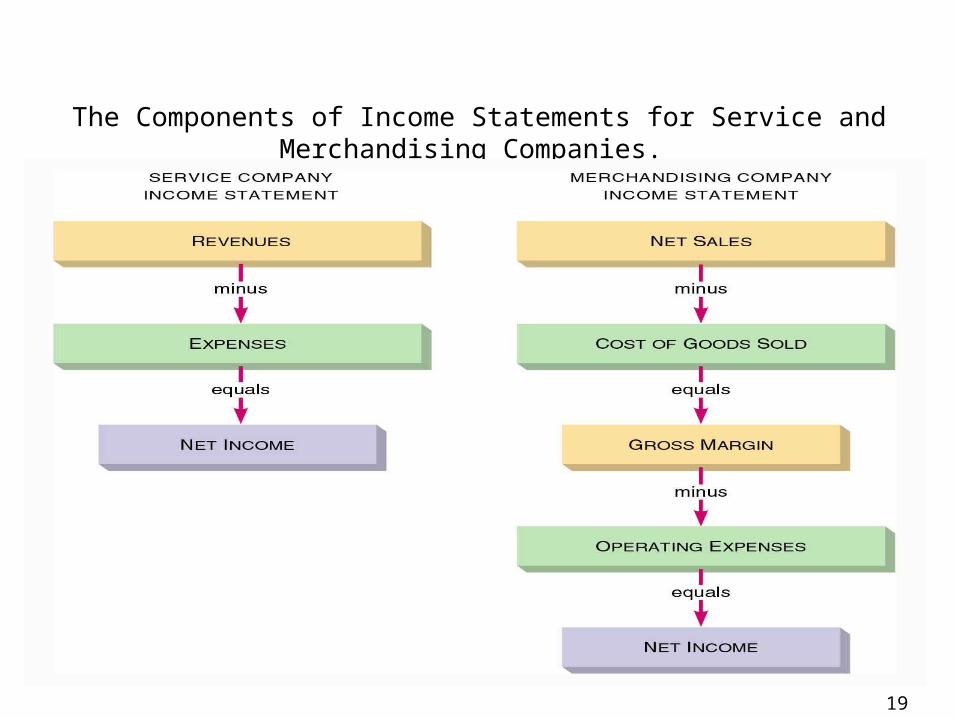

Merchandising Income Statement as an example

• Income statement consists of three major parts.

1. Net sales.

2. Cost of goods sold.

3. Operating expenses.

• Gross margin represents net sales minus cost of goods sold.

19

The Components of Income Statements for Service and Merchandising Companies.

20

Net Sales

• Net Sales consists of gross sales less sales returns and allowances.

• Gross sales is the total cash and credit sales occurring during the period.

• Sales Returns and Allowances is a contra-revenue account used to accumulate cash refunds, credits on account, and allowances to customers for defective merchandise.

21

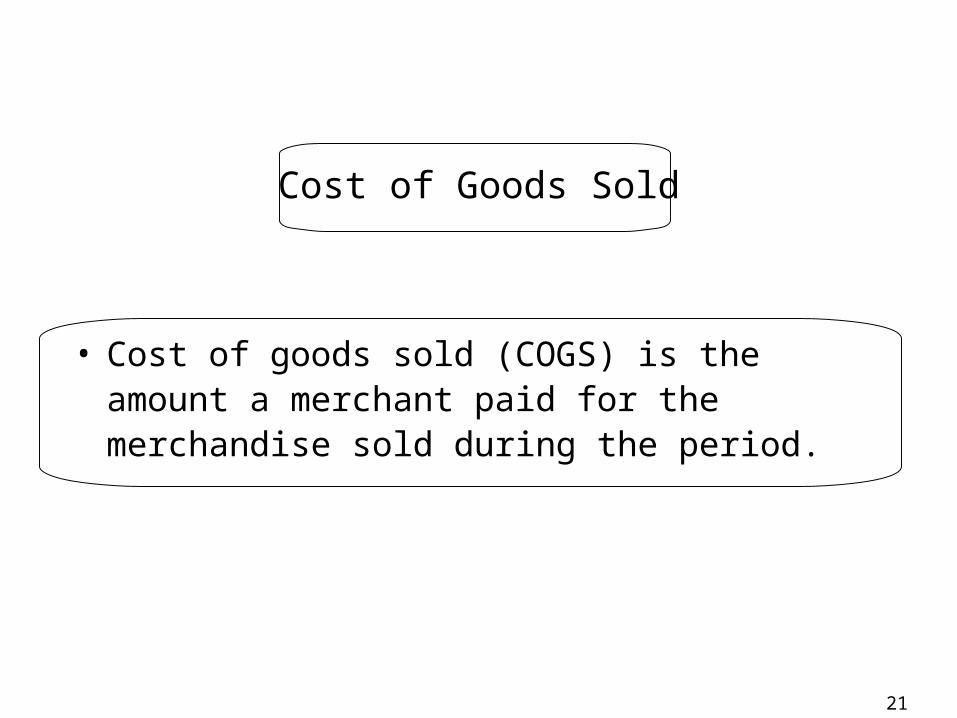

Cost of Goods Sold

• Cost of goods sold (COGS) is the amount a merchant paid for the merchandise sold during the period.

22

Gross Margin

• Gross margin, or gross profit, is the difference between net sales and cost of goods sold.

• To be successful a firm must have gross margin sufficient enough to pay operating expenses and provide an adequate income.

23

Operating Expenses

• Operating expenses represent the expenses other than cost of goods sold that are incurred in running a business.

• Operating expenses are classified as either:

1. Selling expenses.

2. General and administrative expenses.

24

Operating Expenses

• Selling expenses include the costs of storing goods

and preparing them for sale, displaying,

advertising, and otherwise promoting sales and

delivering goods to the buyer (freight out expense).

• General and Administrative expenses include

expenses for accounting, personnel, credit and

collections, and any other expenses that apply to

overall operation.

25

Net Income

• Net income is the final figure or “bottom line” of the income statement.

• Net income is what remains after operating expenses are deducted from gross margin.

• Net income represents the amount of business earnings that accrue to the owners during a period of time.

26

Overview of theAccounting Cycle

27

Overview of the Accounting Cycle

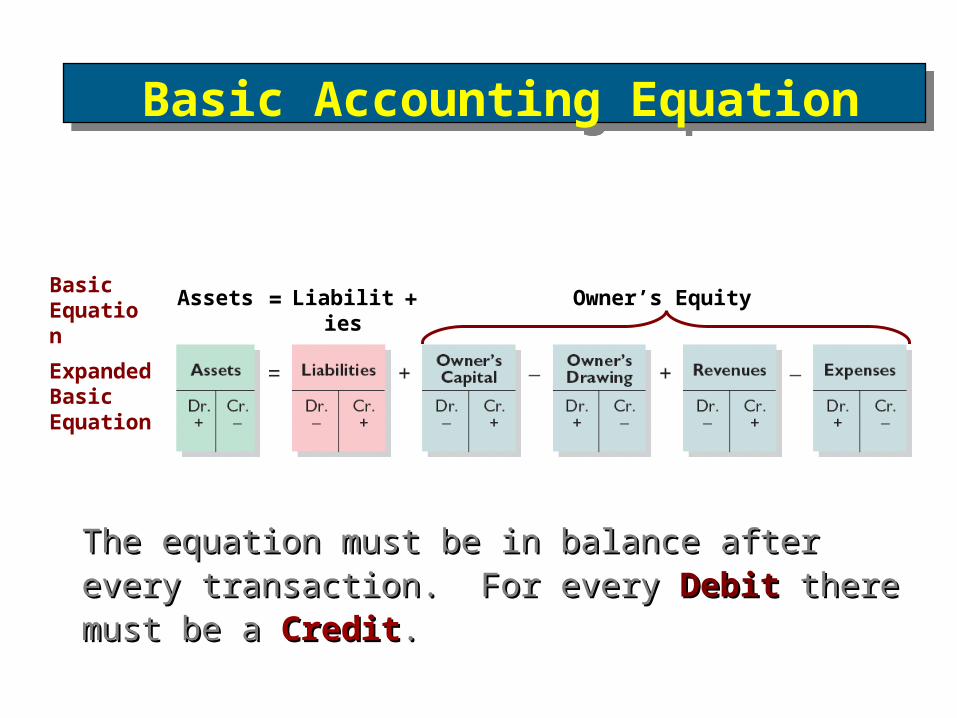

The equation must be in balance after every The equation must be in balance after every transaction. For every transaction. For every DebitDebit there must be a there must be a CreditCredit..

Assets Liabilities= Owner’s EquityBasic Equation

Expanded Basic Equation

+

Basic Accounting EquationBasic Accounting Equation

AssetsAssetsAssetsAssets LiabilitiesLiabilitiesLiabilitiesLiabilitiesOwner’s Owner’s EquityEquity

Owner’s Owner’s EquityEquity

= +

Provides the underlying framework for recording and summarizing economic events.

Resources a business owns.

Provide future services or benefits.

Cash, Supplies, Equipment, etc.

AssetAssetssAssetAssetss

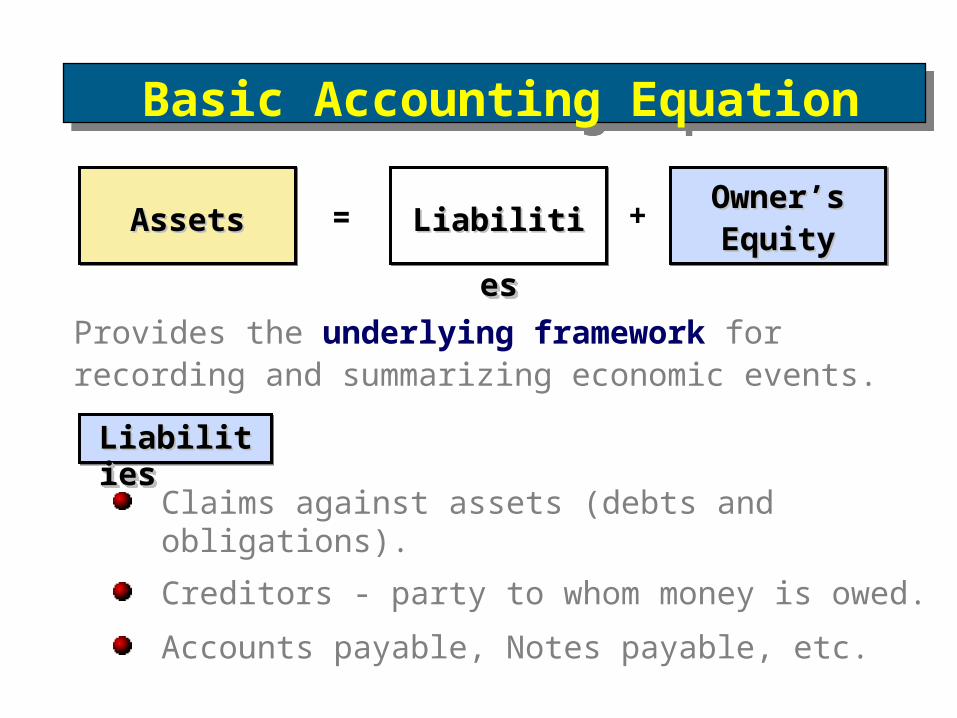

Basic Accounting EquationBasic Accounting Equation

AssetsAssetsAssetsAssets LiabilitiesLiabilitiesLiabilitiesLiabilitiesOwner’s Owner’s EquityEquity

Owner’s Owner’s EquityEquity

= +

Provides the underlying framework for recording and summarizing economic events.

Claims against assets (debts and obligations).

Creditors - party to whom money is owed.

Accounts payable, Notes payable, etc.

LiabilitiLiabilitiesesLiabilitiLiabilitieses

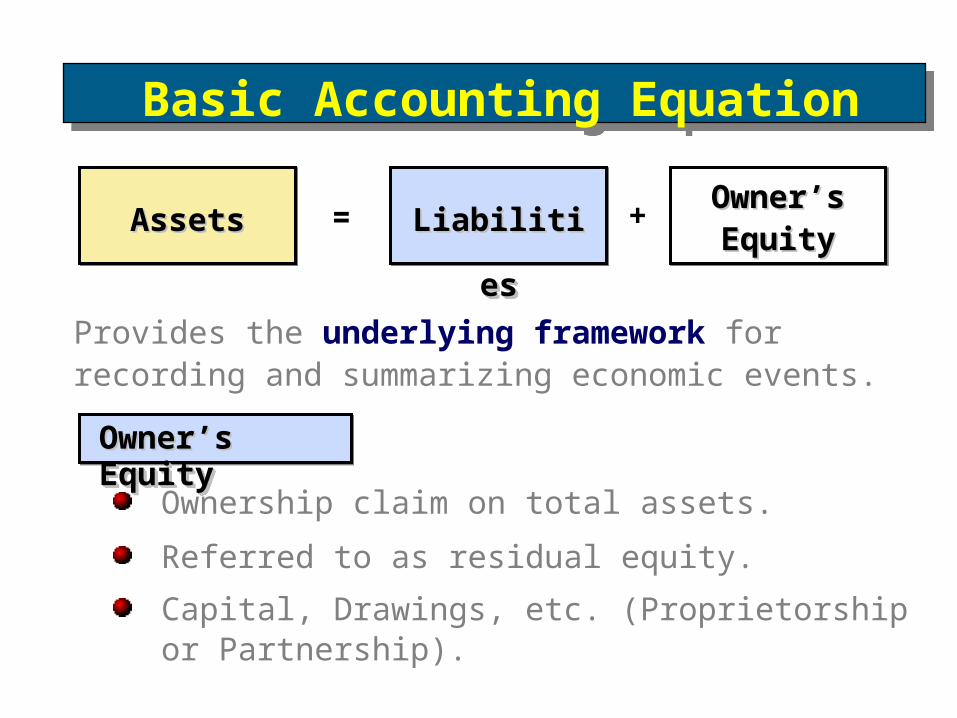

Basic Accounting EquationBasic Accounting Equation

AssetsAssetsAssetsAssets LiabilitiesLiabilitiesLiabilitiesLiabilitiesOwner’s Owner’s EquityEquity

Owner’s Owner’s EquityEquity

= +

Provides the underlying framework for recording and summarizing economic events.

Ownership claim on total assets.

Referred to as residual equity.

Capital, Drawings, etc. (Proprietorship or Partnership).

Owner’s Owner’s EquityEquityOwner’s Owner’s EquityEquity

Basic Accounting EquationBasic Accounting Equation

Revenues result from business activities entered into for the purpose of earning income.

Common sources of revenue are: sales, fees, services, commissions, interest, dividends, royalties, and rent.

Owner’s EquityOwner’s Equity

Expenses are the cost of assets consumed or services used in the process of earning revenue.

Common expenses are: salaries expense, rent expense, utilities expense, tax expense, etc.

Owner’s EquityOwner’s Equity

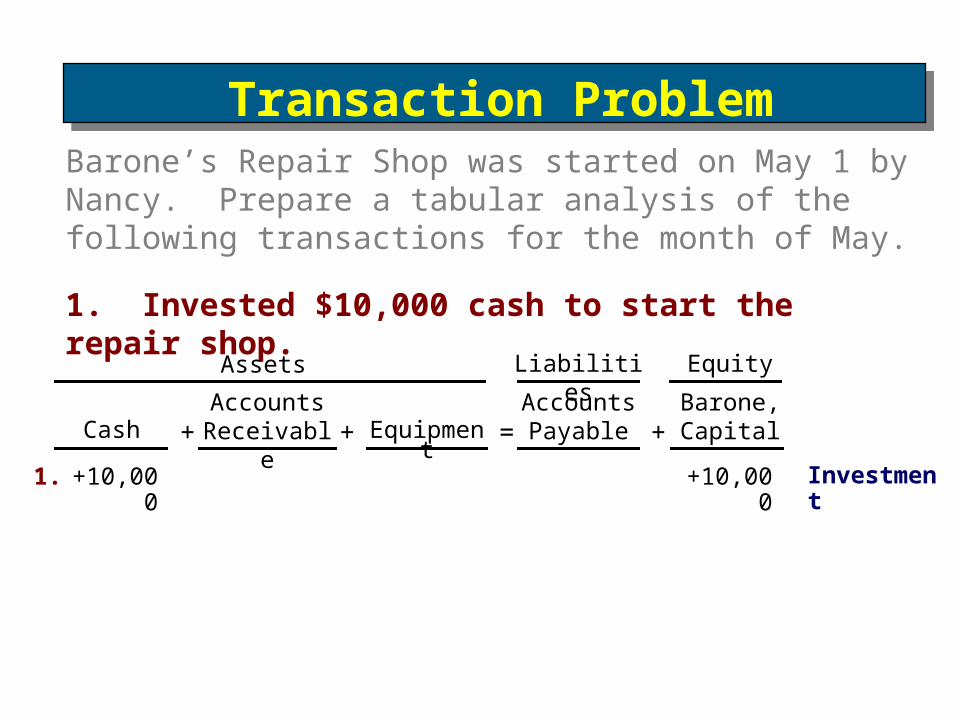

Barone’s Repair Shop was started on May 1 by Nancy. Prepare a tabular analysis of the following transactions for the month of May.

+10,000

1. +10,000

CashAccounts

Receivable Equipment

Accounts Payable

Barone, Capital+ + = +

1. Invested $10,000 cash to start the repair shop.

Investment

Assets Liabilities Equity

Transaction ProblemTransaction Problem

+10,000

1. +10,000

CashAccounts

Receivable Equipment

Accounts Payable

Barone, Capital

2. Purchased equipment for $5,000 cash.

-5,0002. +5,000

+ + = +

Investment

Assets Liabilities Equity

Transaction ProblemTransaction Problem

+10,000

1. +10,000

CashAccounts

Receivable Equipment

Accounts Payable

3. Paid $400 cash for May office rent.

-5,0002. +5,000

+ + = +

-4003. -400 Expense

Barone, Capital

Investment

Assets Liabilities Equity

Transaction ProblemTransaction Problem

+10,000

1. +10,000

CashAccounts

Receivable Equipment

Accounts Payable

4. Received $5,100 from customers for repair service.

-5,0002. +5,000

+ + = +

-4003. -400 Expense+5,1004. +5,100 Revenu

e

Barone, Capital

Investment

Assets Liabilities Equity

Transaction ProblemTransaction Problem

+10,000

1. +10,000

CashAccounts

Receivable Equipment

Accounts Payable

5. Withdrew $1,000 cash for personal use.

-5,0002. +5,000

+ + = +

-4003. -400 Expense+5,1004. +5,100 Revenu

e-1,0005. -1,000 Drawings

Barone, Capital

Investment

Assets Liabilities Equity

Transaction ProblemTransaction Problem

+10,000

1. +10,000

CashAccounts

Receivable Equipment

Accounts Payable

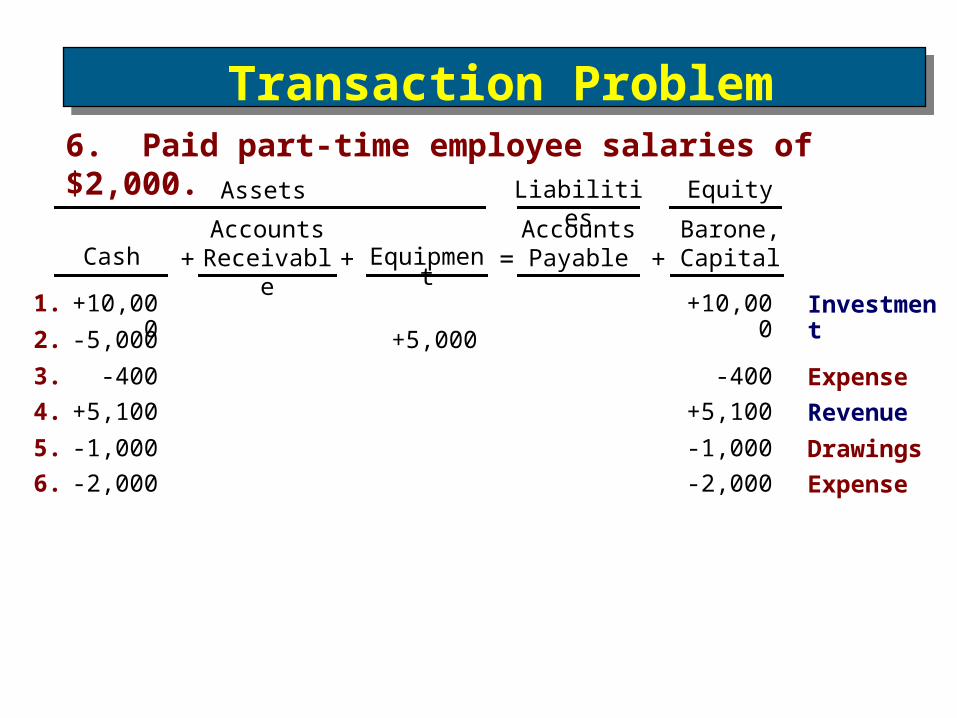

6. Paid part-time employee salaries of $2,000.

-5,0002. +5,000

+ + = +

-4003. -400 Expense+5,1004. +5,100 Revenu

e-1,0005. -1,000 Drawings-2,0006. -2,000 Expense

Barone, Capital

Investment

Assets Liabilities Equity

Transaction ProblemTransaction Problem

+10,000

1. +10,000

CashAccounts

Receivable Equipment

Accounts Payable

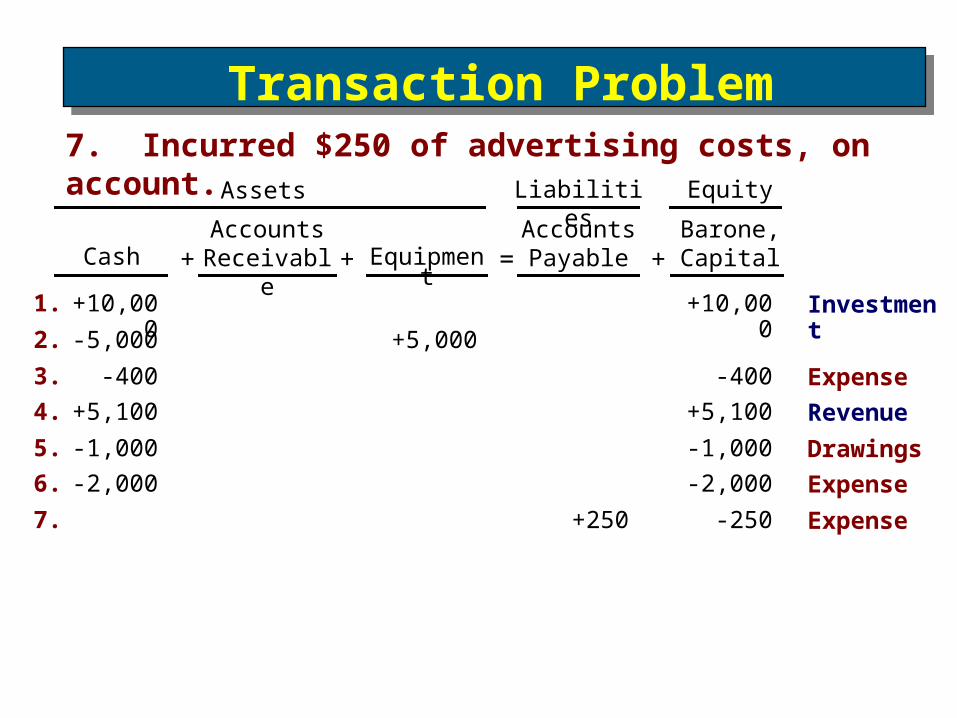

7. Incurred $250 of advertising costs, on account.

-5,0002. +5,000

+ + = +

-4003. -400 Expense+5,1004. +5,100 Revenu

e-1,0005. -1,000 Drawings-2,0006. -2,000 Expense

+2507. -250 Expense

Barone, Capital

Investment

Assets Liabilities Equity

Transaction ProblemTransaction Problem

+10,000

1. +10,000

CashAccounts

Receivable Equipment

Accounts Payable

8. Provided $750 of repair services on account.

-5,0002. +5,000

+ + = +

-4003. -400 Expense+5,1004. +5,100 Revenu

e-1,0005. -1,000 Drawings-2,0006. -2,000 Expense

+2507. -250 Expense+7508. +750 Revenu

e

Barone, Capital

Investment

Assets Liabilities Equity

Transaction ProblemTransaction Problem

+10,000

1. +10,000

CashAccounts

Receivable Equipment

Accounts Payable

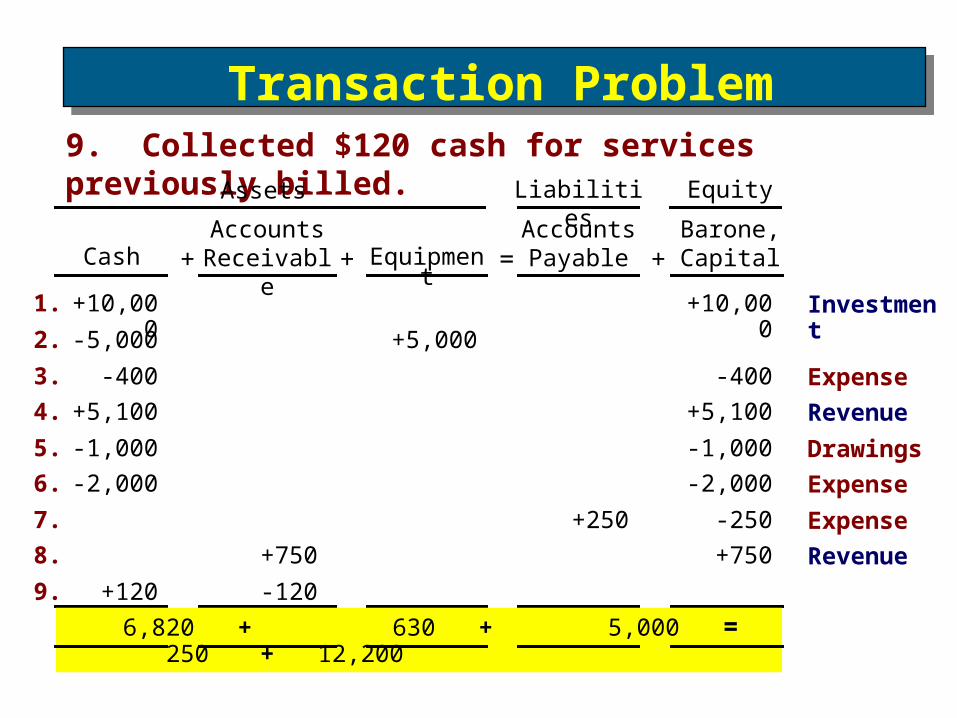

9. Collected $120 cash for services previously billed.

-5,0002. +5,000

+ + = +

-4003. -400 Expense+5,1004. +5,100 Revenu

e-1,0005. -1,000 Drawings-2,0006. -2,000 Expense

+2507. -250 Expense+7508. +750 Revenu

e+1209. -120

Barone, Capital

Investment

Assets Liabilities Equity

6,820 + 630 + 5,000 = 250 + 12,200

Transaction ProblemTransaction Problem

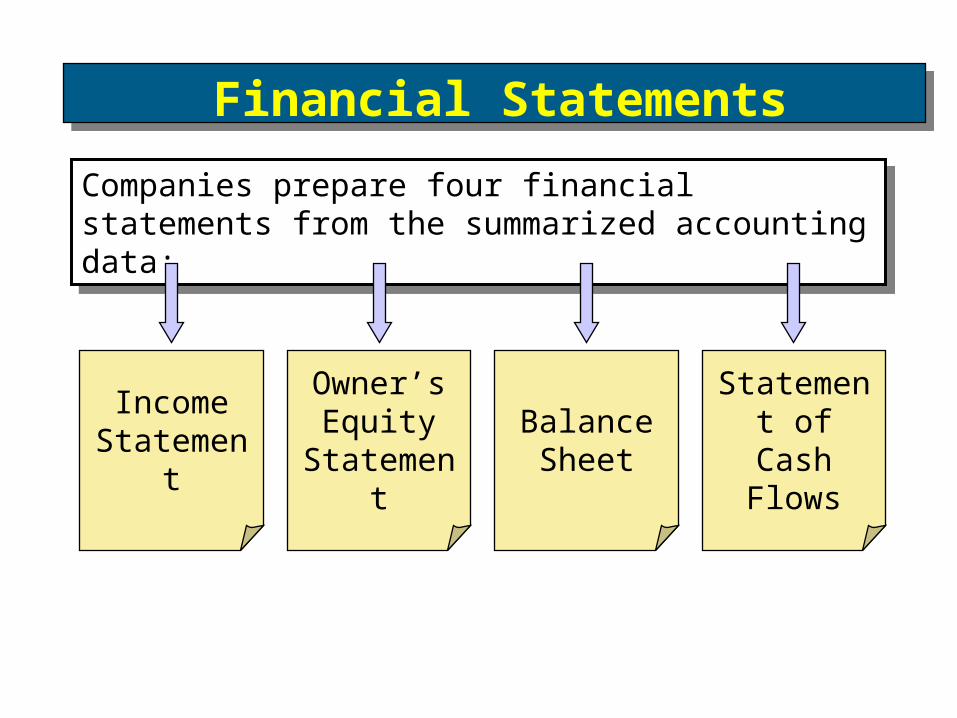

Companies prepare four financial statements from the summarized accounting data:Companies prepare four financial statements from the summarized accounting data:

Balance Sheet

Income Statemen

t

Statement of Cash

Flows

Owner’s Equity

Statement

Financial StatementsFinancial Statements

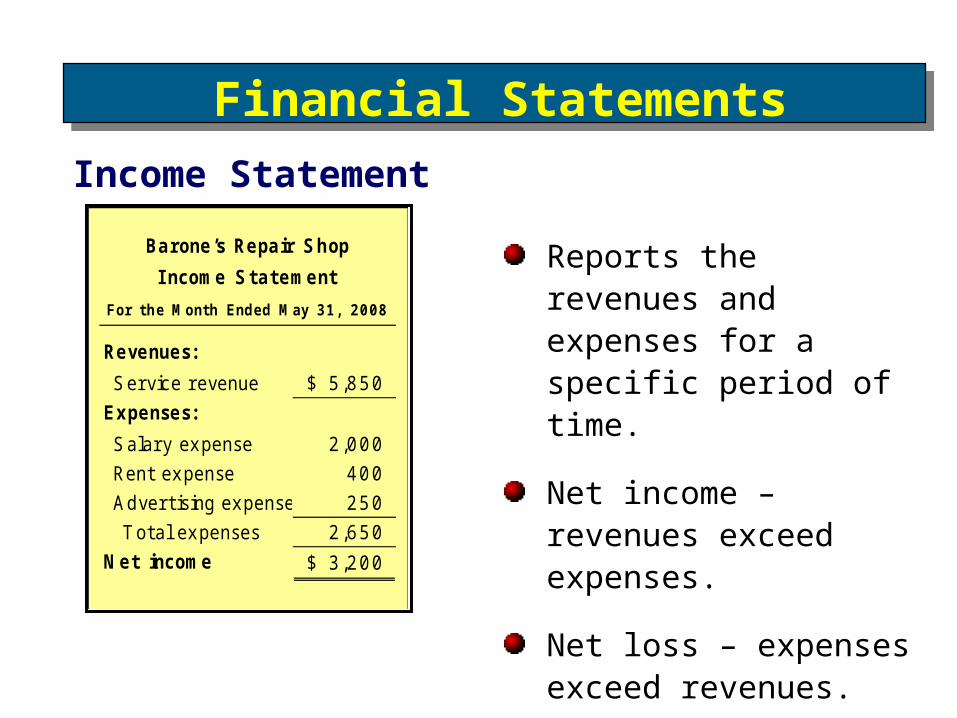

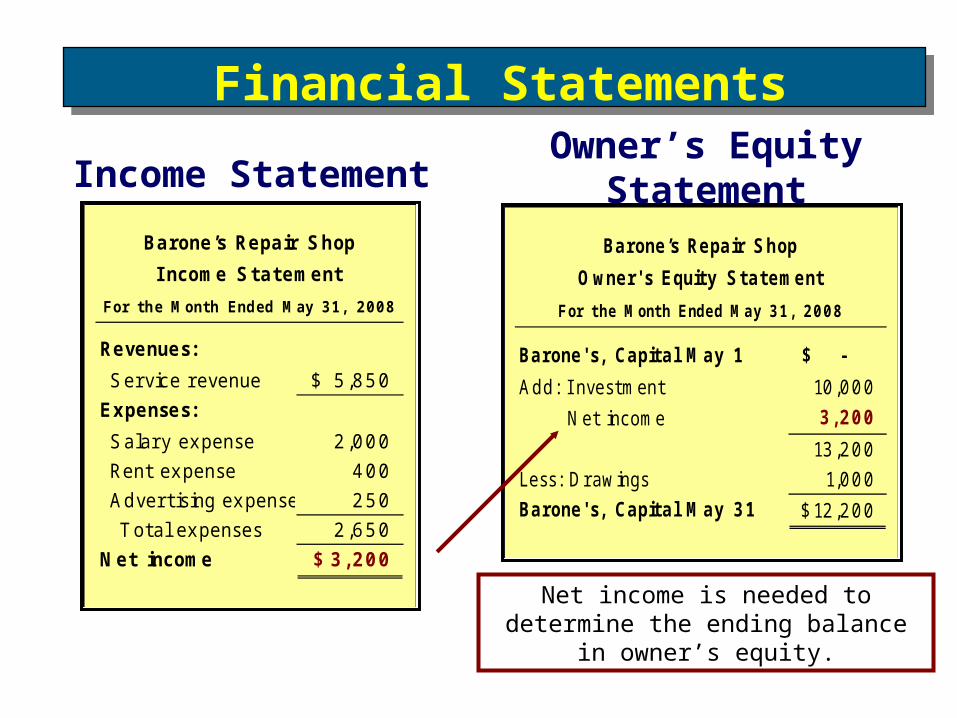

Income Statement

Reports the revenues and expenses for a specific period of time.

Net income – revenues exceed expenses.

Net loss – expenses exceed revenues.

Revenues:

S ervice revenue 5,850$

Expenses:

S alary expense 2,000

Rent expense 400

Adver tising expense 250

T otal expenses 2,650

Net income 3,200$

Barone’s Repair Shop

I ncome Statement

For the Month Ended May 31, 2008

Financial StatementsFinancial Statements

Net income will result during a time period when:

a. assets exceed liabilities.

b. assets exceed revenues.

c. expenses exceed revenues.

d. revenues exceed expenses.

Review QuestionReview QuestionFinancial StatementsFinancial Statements

Revenues:

S ervice revenue 5,850$

Expenses:

S alary expense 2,000

Rent expense 400

Adver tising expense 250

T otal expenses 2,650

Net income 3,200$

Barone’s Repair Shop

I ncome Statement

For the Month Ended May 31, 2008

Income Statement

Barone' s, Capital May 1 -$

Add: I nvestment 10,000

N et income 3,200

13,200

Less: Drawings 1,000

Barone' s, Capital May 31 12,200$

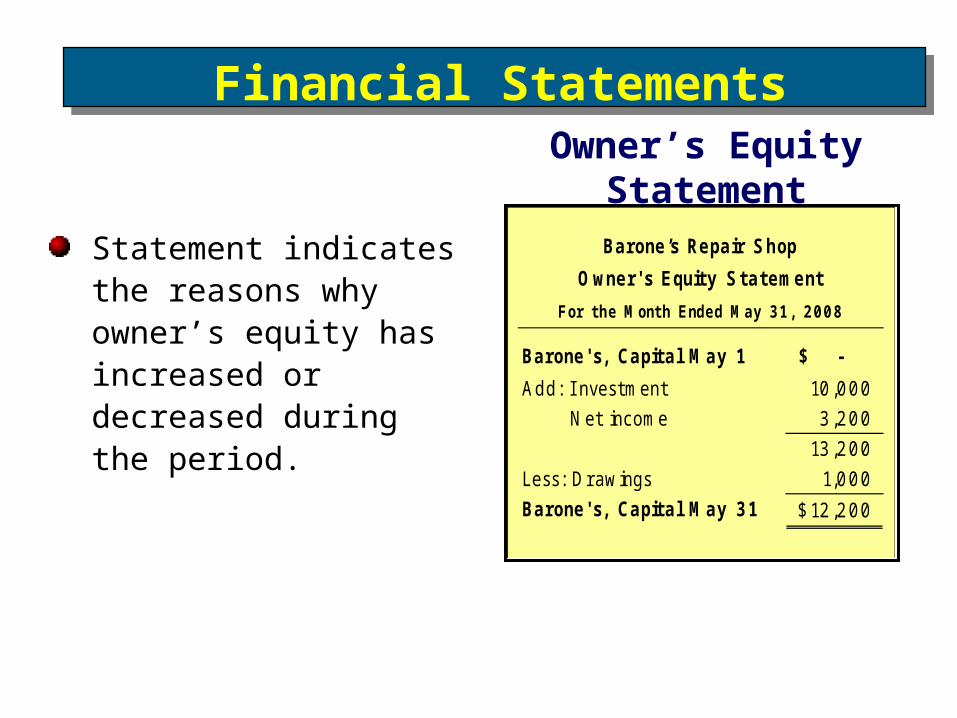

Barone’s Repair Shop

Owner' s Equity Statement

For the Month Ended May 31, 2008

Owner’s Equity Statement

Net income is needed to determine the ending balance in owner’s

equity.

Financial StatementsFinancial Statements

Barone' s, Capital May 1 -$

Add: I nvestment 10,000

N et income 3,200

13,200

Less: Drawings 1,000

Barone' s, Capital May 31 12,200$

Barone’s Repair Shop

Owner' s Equity Statement

For the Month Ended May 31, 2008

Owner’s Equity Statement

Statement indicates the reasons why owner’s equity has increased or decreased during the period.

Financial StatementsFinancial Statements

Barone' s, Capital May 1 -$

Add: I nvestment 10,000

N et income 3,200

13,200

Less: Drawings 1,000

Barone' s, Capital May 31 12,200$

Barone’s Repair Shop

Owner' s Equity Statement

For the Month Ended May 31, 2008

Owners’ Equity Statement

Assets

Cash 6,820$

Accounts receivable 630

Equipment 5,000

T otal assets 12,450$

Liabilities

Accounts payable 250$

Owner' s Equity

Barone' s, capital 12,200

T otal liab. & equity 12,450$

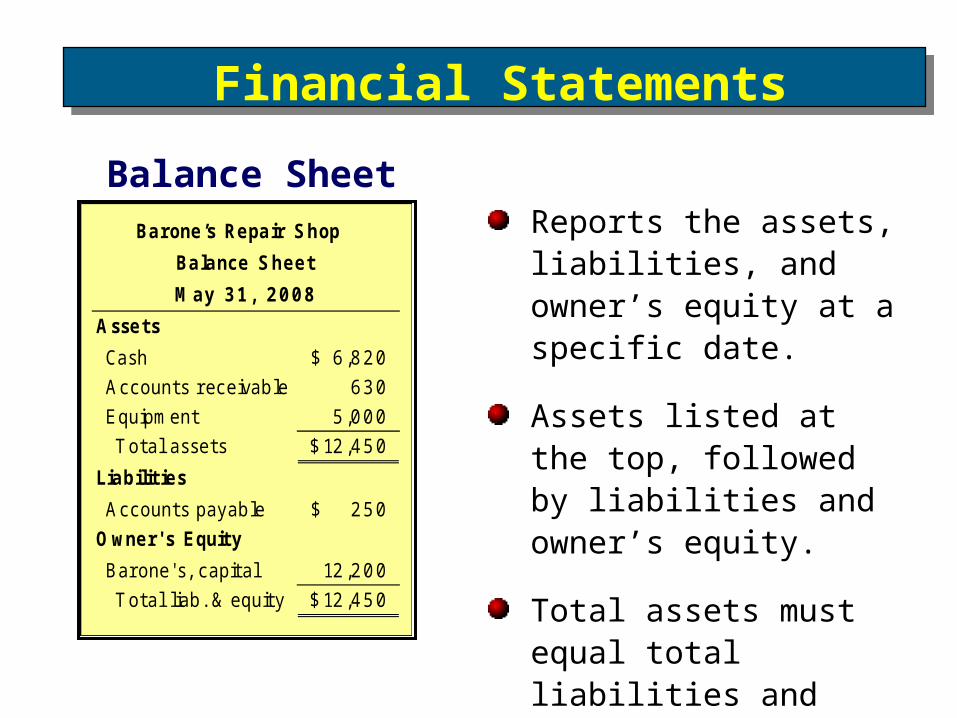

Balance Sheet

Barone’s Repair Shop

May 31, 2008

The ending balance in owner’s equity is needed in preparing the

balance sheet

Balance Sheet

Financial StatementsFinancial Statements

Balance SheetReports the assets, liabilities, and owner’s equity at a specific date.

Assets listed at the top, followed by liabilities and owner’s equity.

Total assets must equal total liabilities and owner’s equity.

Assets

Cash 6,820$

Accounts receivable 630

Equipment 5,000

T otal assets 12,450$

Liabilities

Accounts payable 250$

Owner' s Equity

Barone' s, capital 12,200

T otal liab. & equity 12,450$

Balance Sheet

Barone’s Repair Shop

May 31, 2008

Financial StatementsFinancial Statements

Balance Sheet

Assets

Cash 6,820$

Accounts receivable 630

Equipment 5,000

T otal assets 12,450$

Liabilities

Accounts payable 250$

Owner' s Equity

Barone' s, capital 12,200

T otal liab. & equity 12,450$

Balance Sheet

Barone’s Repair Shop

May 31, 2008Cash fl ow f rom operating activities

Cash receipts f rom revenues 5,220$

Cash paid f or expenses (2,400)

Cash provided by operations 2,820

Cash fl ow f rom investing activitites

Purchase of equipment (5,000)

Cash fl ow f rom fi nancing activities

I nvestment by owners 10,000

Drawings by owners (1,000)

Cash provided by fi nancing 9,000

Net increase in cash 6,820

Cash balance, May 1 -

Cash balance, May 31 6,820$

Statement of Cash Flows

Barone’s Repair Shop

For the Month Ended May 31, 2008

Statement of Cash Flows

Financial StatementsFinancial Statements

Cash fl ow f rom operating activities

Cash receipts f rom customers 5,220$

Cash paid f or expenses (2,400)

Cash provided by operations 2,820

Cash fl ow f rom investing activities

Purchase of equipment (5,000)

Cash fl ow f rom fi nancing activities

I nvestment by owners 10,000

Drawings by owners (1,000)

Cash provided by fi nancing 9,000

Net increase in cash 6,820

Cash balance, May 1 -

Cash balance, May 31 6,820$

Statement of Cash Flows

Barone’s Repair Shop

For the Month Ended May 31, 2008

Statement of Cash FlowsInformation for a

specific period of time.

Answers the following:1. Where did cash

come from?

2. What was cash used for?

3. What was the change in the cash balance?

Financial StatementsFinancial Statements

Which of the following financial statements is prepared as of a specific date?

a. Balance sheet.

b. Income statement.

c. Owner's equity statement.

d. Statement of cash flows.

Review QuestionReview Question

Financial StatementsFinancial Statements