accounting & auditing update 2016 ky hfma winter...

TRANSCRIPT

Accounting & Auditing Update2016 KY HFMA Winter Institute

January 21, 2016

Bill Kohm, CPA, MBA, CGMADirector of Assurance Services

deandorton.com

Agenda

Audit Update

Highlight Accounting Standards From 2013 – 2016

Emerging Issues

Other Matters

deandorton.com

Accounting and Audit Goals

1. Awareness of

key changes in accounting and audit standards that impact your job

potential changes to accounting and audit standards that may impact your job

2. Strengthen Internal Controls

3. Aid in educating your stakeholders on A&A changes

deandorton.com

# Trending

# Acquisition Accounting

# Selective International Convergence

# Lease Accounting Standard Final ???

# Simplification

# Not For Profit Update

# Audit Committee Engagement

deandorton.com

Audit Update

deandorton.com

Audit Update

Audit Initiatives Fraud Oversight

deandorton.com

Audit Initiatives

AICPA issues audit standards for private company auditors

Public Company Accounting Oversight Board (PCAOB) governs public company auditors

PCAOB initiatives may impact AICPA

deandorton.com

PCAOB Initiatives

Work of Specialist – investigating the need to require more rigorous audit procedures surrounding reliance on third party specialists like valuation specialists and actuaries

Auditing accounting estimates including FV Measurements and related disclosures

Going Concern – align audit standard with the new accounting standard

deandorton.com

PCAOB Initiatives

Audit Team Transparency Supervision of other auditors and

multilocation Audit Report model Audit quality initiatives (28 points of

focus)

deandorton.com

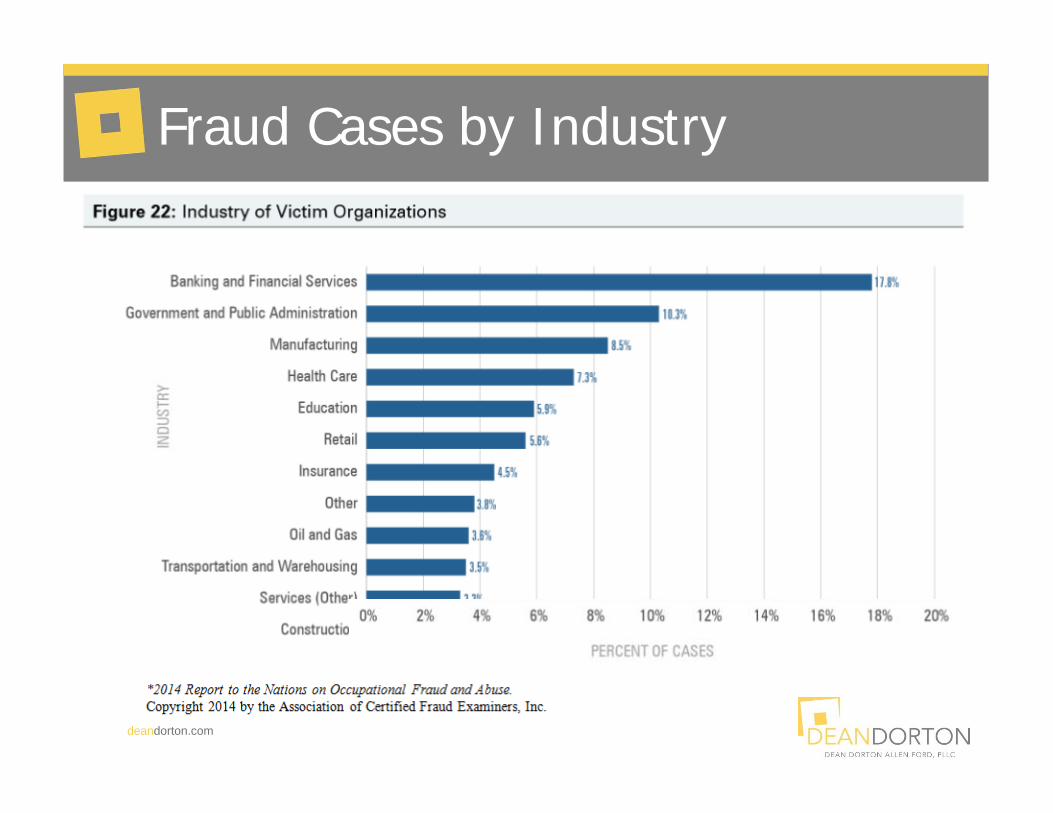

Fraud Cases by Industry

deandorton.com

Fraud Median Loss by Industry

deandorton.com

Anti-Fraud Controls

deandorton.com

Why Use Data Analytics to Prevent Fraud?

Proactive instead of reactive Strong preventative measure if employees

know every transaction is being monitored and analyzed

Enhances the risk assessment process

deandorton.com

Data Analytics Examples

Payroll Compare vendor and employee contact info Compare bank account numbers of employees

Expense Reimbursements Amounts over allowed thresholds for certain

expense types Reimbursements for the same expense on

multiple reports or multiple payment methods Average expenses by employee Unusual merchant classification codes on credit

card transactions

deandorton.com

Data Analytic Tools

Microsoft Excel Microsoft Access ACL, IDEA Microsoft SQL Server Text analytic tools or keyword searching SAP, Oracle SAS, Stata Hadoop, Map Reduce

deandorton.com

1. Economic and political uncertainty and volatility

2. Regulation and the impact of public policy initiatives

3. Operational risk4. Cybersecurity

Source: KPMG Global Audit Committee Survey, 2015

Audit Committee Biggest Concerns in 2015

deandorton.com

Government Accounting Standards Board

deandorton.com

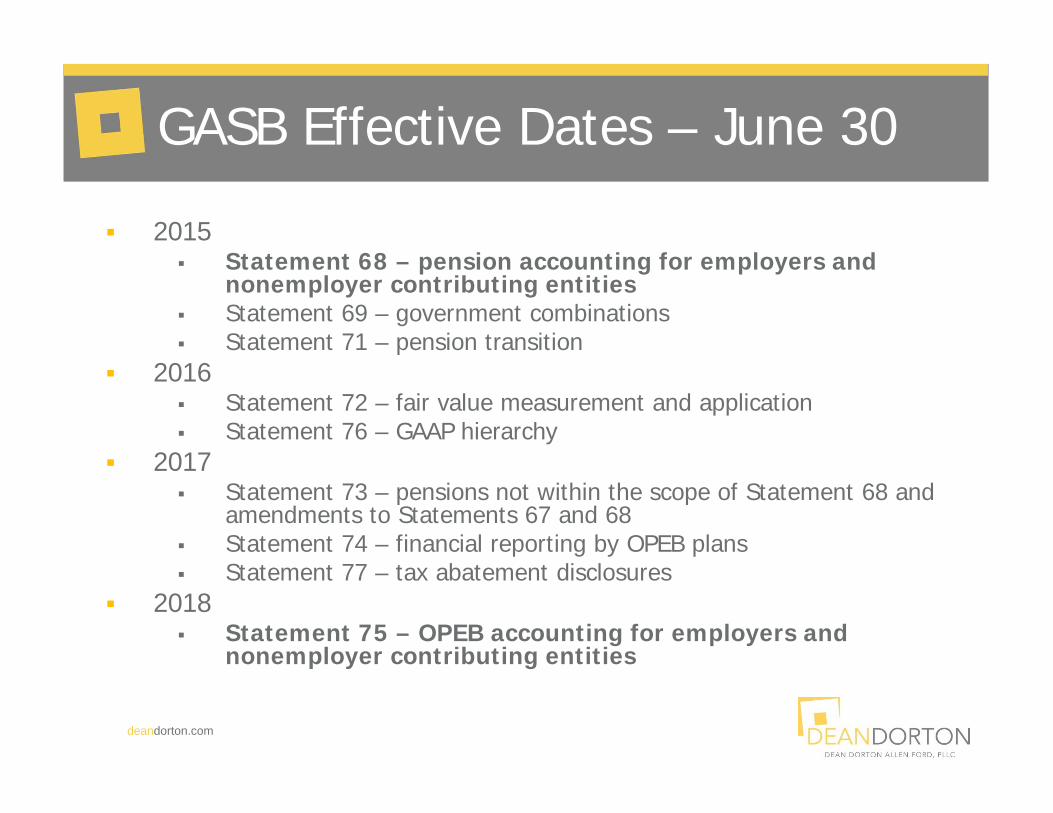

GASB Effective Dates – June 30

2015 Statement 68 – pension accounting for employers and

nonemployer contributing entities Statement 69 – government combinations Statement 71 – pension transition

2016 Statement 72 – fair value measurement and application Statement 76 – GAAP hierarchy

2017 Statement 73 – pensions not within the scope of Statement 68 and

amendments to Statements 67 and 68 Statement 74 – financial reporting by OPEB plans Statement 77 – tax abatement disclosures

2018 Statement 75 – OPEB accounting for employers and

nonemployer contributing entities

deandorton.com

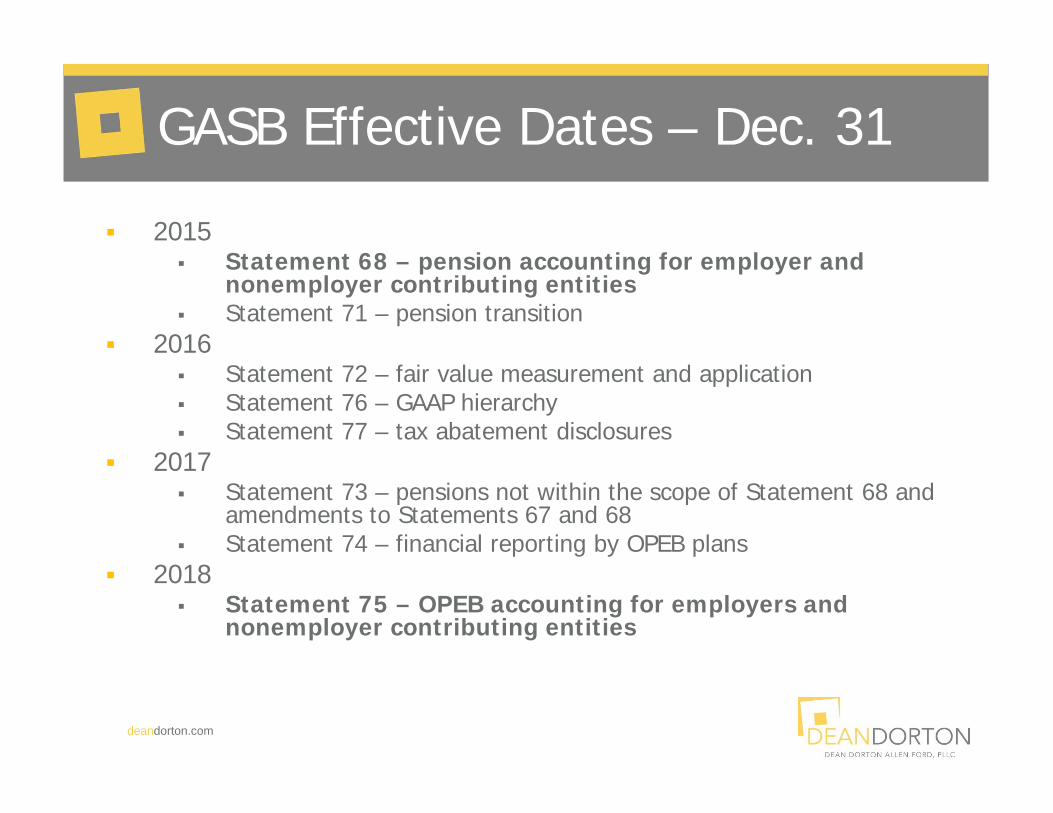

GASB Effective Dates – Dec. 31

2015 Statement 68 – pension accounting for employer and

nonemployer contributing entities Statement 71 – pension transition

2016 Statement 72 – fair value measurement and application Statement 76 – GAAP hierarchy Statement 77 – tax abatement disclosures

2017 Statement 73 – pensions not within the scope of Statement 68 and

amendments to Statements 67 and 68 Statement 74 – financial reporting by OPEB plans

2018 Statement 75 – OPEB accounting for employers and

nonemployer contributing entities

deandorton.com

Accounting Standards Update

deandorton.com

ASU 2016-1

Purpose: Improve measurement and valuation of financial instruments

Effective Date: FY beginning after December 15, 2017 (2018 for private)

deandorton.com

ASU 2016-1 Requirements

Fair value measurement of equity investments (does not apply to equity method accounting) Can rely on cost if valuation is not readily available

Qualitative impairment assessment for investments valued at cost

No need to disclose fair value for those investments measured at amortized cost (private company)

Separate presentation of financial assets and liabilities on face or in disclosures based on form

deandorton.com

ASU 2015-17

Purpose: Simplify deferred tax balance sheet presentation. All netted and shown as either LT Asset or LT Liability.

Consistent with IFRSRetroactive or prospective application

Effective Date: FY beginning after December 15, 2016 (2017 for private)

deandorton.com

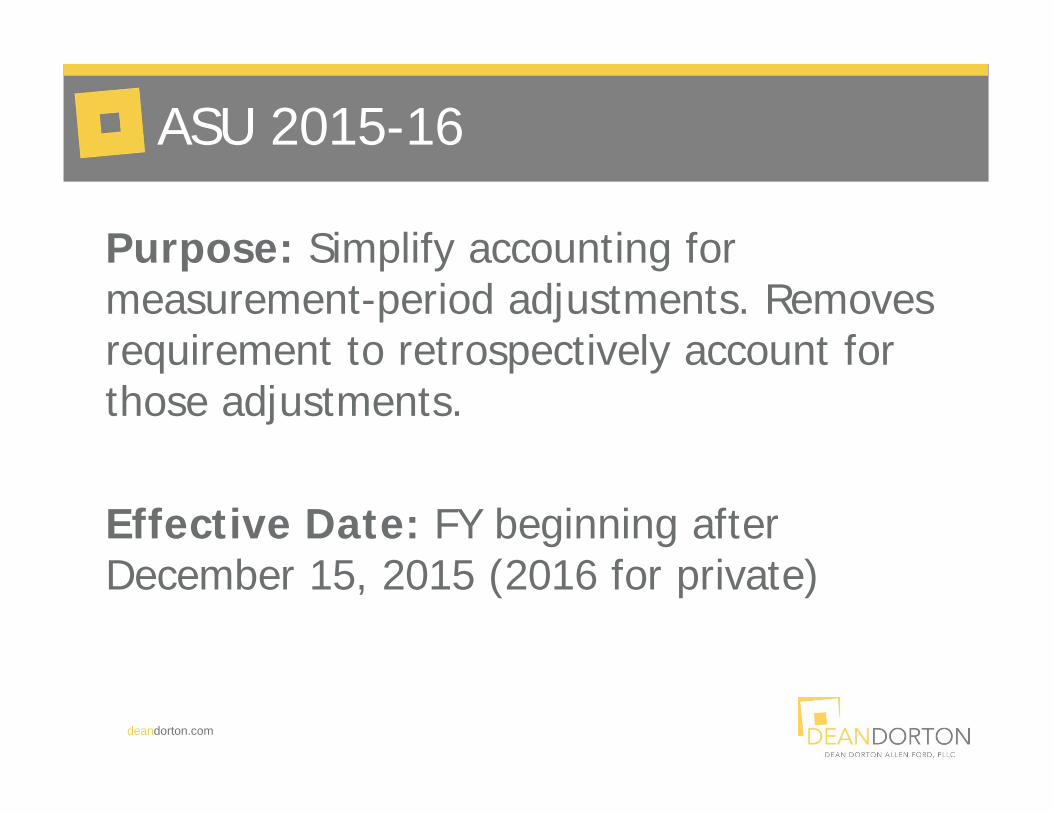

ASU 2015-16

Purpose: Simplify accounting for measurement-period adjustments. Removes requirement to retrospectively account for those adjustments.

Effective Date: FY beginning after December 15, 2015 (2016 for private)

deandorton.com

ASU 2015-16 Requirements

Applies to situations where acquisition is incomplete at end of reporting period

Impacts provisional assets/liabilities Go back to acquisition date Quantify impact to previously reported

items Current period earnings by line item

Face of income statement or Disclosure

deandorton.com

ASU 2015-16 Example

Appraisal incomplete at reporting date At 12/31/15 value fixed asset at $30,000

(preliminary) During 2016 receive appraisal after

issuance Value appraised at $40,000 Go back and restate 2015 or correct in

2016?

deandorton.com

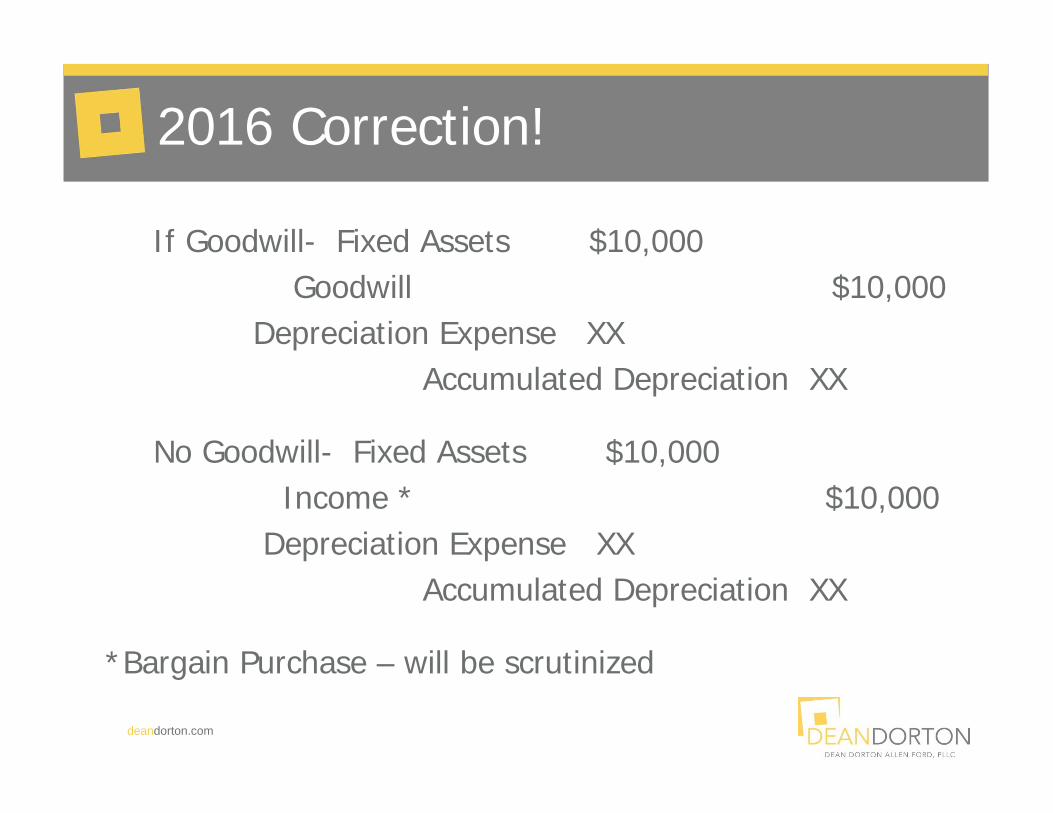

2016 Correction!

If Goodwill- Fixed Assets $10,000Goodwill $10,000

Depreciation Expense XXAccumulated Depreciation XX

No Goodwill- Fixed Assets $10,000Income * $10,000

Depreciation Expense XXAccumulated Depreciation XX

*Bargain Purchase – will be scrutinized

deandorton.com

Disclosure Reminders

If acquisition accounting incomplete reasons why*

Specific identification of assets and liabilities subject to change

Nature and amount of Measurement Period Adjustments

Amounts recorded in current period (retrospective)

* Practice Reminder –BIG difference error vs. incomplete

deandorton.com

ASU 2015-15

Purpose: Address debt issuance cost presentation associated with line of credit arrangements. ASU 2015-03 does not address.

Conclusion: Can present costs separate as an asset from debt and amortize over life of arrangement

Effective Date: Immediate

deandorton.com

ASU 2015-14

Purpose: Defer effective date of ASU 2014-09 – Revenue from Contracts

Effective Date: FYs beginning after December 15, 2017 (2018 for private); All can early adopt FYs beginning after December 15, 2016

deandorton.com

ASU 2015-12

Purpose: Remove contract value to fair value reconciliation for

fully benefit responsive investment contracts. Remove disclosure requirement that individual

investments that >5% of net assets available for benefits and remove net appreciation/depreciation by investment type.

Measure investments as of month end date that is closest to FY end when fiscal period does not match month end.

Effective Date: FYs beginning after December 15, 2015

deandorton.com

ASU 2015-11

Purpose: Clarify “market” definition in inventory valuation. Does not apply to inventory valued by: Retail method LIFO

Consistent with IFRSEffective Date: FYs beginning after December 15, 2016

deandorton.com

Inventory

LCM – Lower of Cost or Market Market = Net Realizable Value Net Realizable Value = Estimated sales

price less cost of completion, disposal and transportation

Removes use of replacement cost or net realizable value less profit margin

deandorton.com

Inventory Example

Cost = $4.50/unit Sales price based on agreements in place

$7.00/unit Costs to get product to customer ($1.50)

Transportation/Loading $1.00/unit Commissions $0.50/unit

NRV = $7.00-$1.50 = $5.50 LCM = $4.50 < $5.50

deandorton.com

ASU 2015-08

Purpose: Amends various SEC paragraphs of FASB Codification pursuant to SAB No. 115 (conform to ASU 2014-17)

Effective Date: Immediate

deandorton.com

ASU 2015-07

Purpose: Removes need to categorize investments measured using net asset value per share practical expedient into the FV hierarchy disclosure

Effective Date: FYs beginning after December 15, 2015 (2016 for private)

deandorton.com

Practical Expedient

Applicable to investments No readily determinable fair value AND Located in an investment company or Real estate fund

Group investments into similar nature with detailed descriptions. Common types: Equity long/short hedge funds Event driven hedge funds Real estate funds

deandorton.com

ASU 2015-05

Purpose: Accounting for fees paid in a cloud computing arrangement

Effective Date: FYs beginning after December 15, 2015 (2016 for private)

Prospective or retrospective application

deandorton.com

Examples

Software as a service Platform as a service Infrastructure as a service Other similar hosting arrangements

End user of the software does not take possession

deandorton.com

Criteria

Customer has contractual right to take possession of software

AND

Feasible for customer to run the software or contract with another party to host

deandorton.com

Conclusion

If Yes = software license (capitalize fees –350 Intangibles – 40 Internal Use Software)

If No = service contract (expense fees)

deandorton.com

ASU 2015-04

Purpose: Practical expedient for the measurement date of any employer’s defined benefit obligation and plan assets. Use of month end closest to FY end when FY end does not fall at end of a month.

Effective Date: FYs beginning after December 15, 2015 (2016 for private)

deandorton.com

ASU 2015-03

Purpose: Change presentation of debt costs from assets to contra liability (offset associated debt). Consistent with IFRS.

Effective Date: FYs beginning after December 15, 2015 (2016 for private)

Retrospective

deandorton.com

ASU 2015-02

Purpose: Focus on consolidation evaluation

Effective Date: FYs beginning after December 15, 2015 (2016 for private)

deandorton.com

Consolidation Items

More emphasis on risk of loss and less on fee arrangements

Reduce frequency of application of related party guidance

deandorton.com

ASU 2015-01

Purpose: Remove extraordinary items presentation from the income statement.Consistent with IFRS.

Effective Date: FYs beginning after December 15, 2015

deandorton.com

ASU 2014-18

Purpose: Simplify acquisition accounting and identification of intangible assets for Private Companies (DOES NOT APPLY NFP)

Effective Date: FYs beginning after December 15, 2015

deandorton.com

Intangibles

Election If Elected must adopt PC goodwill policy No need to recognize separately

Customer related intangibles that can’t be sold or licensed separately

Noncompetition agreements

deandorton.com

ASU 2014-17

Purpose: Guidance for pushdown of acquisition accounting adjustments to subsidiary level.

Effective Date: Immediate

deandorton.com

Push-Down Accounting

Entity OPTION for each change in control event

Example- Entity A acquires 51% of Entity B and acquisition leads to $2 million of Goodwill Push Goodwill and other acquisition

adjustments down to sub or leave at parent level?

Need to select a policy in preparing sub’s stand- alone financials

deandorton.com

Push-Down Accounting

If choose to push down Disclose impact of the acquisition accounting

adjustments to the financial statements (similar to business combination disclosure)

Bargain purchase income not able to be reflected in sub’s income statement (shown as increase in paid in capital)

If choose not to push down Disclose policy to use historical accounting

despite change in control If in future years change application deemed

change in accounting principle

deandorton.com

ASU 2014-15

Purpose: Guidance for Management to address going concern of entity

Effective Date: FYs ending after December 15, 2016

deandorton.com

Going Concern

Requires management’s assessment

Footnote disclosure required under following:

(Substantial Doubt Exists) Probably not able to meet obligations within 1 year of financial statements’ ISSUANCE date w/out taking actions outside ordinary course

(Substantial Doubt Alleviated) Still disclose circumstances and how management’s plan alleviated the concerns

deandorton.com

ASU 2014-02

Purpose: Goodwill relief for private companies (DOES NOT APPLY NFP)

Effective Date: Prospective FYs December 15, 2014 (private)

Early adoption

deandorton.com

ASU 2014-02

Policy option Amortize Goodwill over 10 years or less Simplified impairment model

Triggering event Company level or Reporting unit level

deandorton.com

ASU 2013-06

Purpose: Recognize uncompensated services provided by NFP affiliate at the cost of the affiliate and increase to net assets.

Effective Date: Prospective FYs begin post June 15, 2014

Early Adoption: permitted

Modified retrospective approach: allowed

deandorton.com

ASU 2013-06 Journal Entry

FACTS: NFP A provides IT services to NFP B at no cost. Cost to NFP A is $1,000

NFP B J/EIT consulting expense $1,000Net Assets $1,000To record uncompensated IT services from NFP A

deandorton.com

ASU 2013-04

Purpose: Clarifies accounting and reporting requirements for Joint and Several Arrangements with fixed amounts.

Effective Date: Prospective FYs begin post Dec. 15, 2013 (public) post Dec. 15, 2014 (private)

Early Adoption: Allowed and retrospective treatment required for obligations that exist at year of adoption

deandorton.com

ASU 2013-04 Example

RP A and RP B enter into a $3 million loan agreement with a bank. Both related parties have joint and several responsibility to service the loan. All proceeds go to RP A. Note amortizes over 5 years.

What does RP B record (if anything)?

deandorton.com

ASU 2013-04 Example

Initial Year – records nothing based on review of RP A’s financial condition and ability to service loan.

Year 3 ($1.4 million remains unpaid) RP A is not in compliance with loan

covenants and has missed payments. RP B records remaining balance due

to uncertainties surrounding RP A.

deandorton.com

ASU 2013-04 Example

What is the Entry on RP B books?Equity $1,400,000

Debt $1,400,000Due to common control treated as equity transaction.

If RP A is able to service loan then debt and equity are reversed by applicable amounts.

deandorton.com

ASU 2013-04 Disclosures

Nature of the arrangement Total outstanding obligation Amount (if any) recorded on the books Recourse provisions Entry to record the obligation and where

amounts reside in the f/s

deandorton.com

Emerging Issues in Accounting

deandorton.com

The Issues

Not For Profit Update Simplification Initiative Disclosure Framework Revenue recognition Leases

deandorton.com

NFP Project Goals

Over 20 year Refresh Improve the current net asset

classification requirements Improve the information presented in

financial statements and notes about a NFPs liquidity, financial performance, and cash flows

deandorton.com

Proposed Amendments Intended to Address

Complexities with the current three classes of net assets

Inconsistencies in reporting of the intermediate measure of operations

Inconsistencies between operations reported in the statement of activities and operating cash flows in the statement of cash flows

Inconsistencies in reporting of expenses Opportunities to enhance the understandability

and utility of the statement of cash flows

deandorton.com

Proposed Amendments

Balance Sheet: Two net asset classes Changes to underwater endowment accounting

and reporting Statement of Activities:

Prescribed operating measure Restriction releases to operations with long-lived

assets transferred from operating to non-operating Statement of Cash Flows:

Direct method cash flows for operating activities Reclassification of certain items

An analysis of natural and functional expenses Disclosure modifications

deandorton.com

Simplification Initiative

Equity method of accounting No need to account for fair value net

asset basis difference at inception Remove retroactive application upon

increase in ownership

Definition of “Business” Reduce number of acquisition

accounting applications

deandorton.com

Simplification Initiative

Debt classification Will be principle based Focus on contractual maturity and borrowers’

right (vs management judgment) Debt covenant violation waived (break out

debt on face and note) Goodwill

Allow private company option for all Other intangibles

Allow private company option to minimize acquisition accounting application

deandorton.com

Disclosure Framework Project

Proposed amendment to Statement of Financial Accounting Concepts No. 8 –Conceptual Framework for Financial Reporting – Chapter 3: Qualitative Characteristics of Useful Financial Information

ASU 2015-310 – Notes to Financial Statements (Topic 235) – Assessing whether disclosures are material

deandorton.com

Revenue Recognition

ASU 2015-320 – Revenue from Contractswith Customers (Topic 606) Focal points:

Collectability Noncash considerations Completed contracts Contract modifications Accounting policy elections

deandorton.com

Revenue (AICPA) What To Do Now?

Develop an implementation plan Training Evaluate accounting changes

May not have big changes but won’t know until implement

Everyone will have additional disclosures Determine retrospective adoption

Interim disclosures before effective Potential IT system changes Tax implications Educate key stakeholders

deandorton.com

AICPA Revenue Recognition Task Forces

1. Aerospace & Defense2. Airlines3. Broker Dealer4. Construction Contractors5. Depository Institutions6. Gaming7. Healthcare8. Hospitality

9. Insurance10.Asset Management11.Not for Profit12.Oil & Gas13.Power & Utilities14.Software15.Telecommunications16.Time Share

deandorton.com

Revenue Recognition Issues

Methods to measure transfer of control Treatment of contract costs Identifying performance obligations Gross vs. net Contract modifications Disclosures Determine transaction price as relates to

third party estimates Individual contract vs. portfolio

deandorton.com

Leases (Topic 842)

FINAL STANDARD stage Estimated completion: Q1 2016 Goal is to increase transparency of leasing

activities across all types of leases Focus on leases > 1 year Balance sheet presentation for BOTH

(Right of Use Asset) A-Finance lease (depreciate/ interest) B-Operating lease (rent expense)

deandorton.com

Other Matters

deandorton.com

Overtime Rules Change

On June 30, 2015, the Department of Labor (DOL) announced a significant proposed change to the overtime rules under the Fair Labor Standards Act (FSLA)

Final version expected by end of 2016 with a first half 2017 effective date

Will the 2016 political season impact final version?

deandorton.com

Overtime Rules Change

DOL has proposed changing the salary level test by increasing the threshold from $23,660 to $50,440 (with provision for future annual adjustments).

Estimated to impact over 20 million workers nationwide1975 – about 62% salaried employees OT eligibleToday – about 8% salaried employees OT eligible

deandorton.com

Overtime Rules Change-What to do?

Identify current employees who this will impact Determine the actual hours they work each week

Consider increasing salary of some positions Financial planning and budgetary

considerations Determine how hours will be captured and

OT controlled Prepare conversation and message to

employees

deandorton.com

2016 Focal Points

1. Overtime Regs Evaluation2. Final Lease Standard3. Continued refinement of revenue standard4. Simplification of disclosures5. Private company differences and possible

trickle down to NFPs6. Not-for-profit financial statement refinement

deandorton.com

Want More?

FASB.org – signup for newsletter and periodical free CPEs